ADU Financing New York: Grants, Loans, and the First Path to Test in 2026

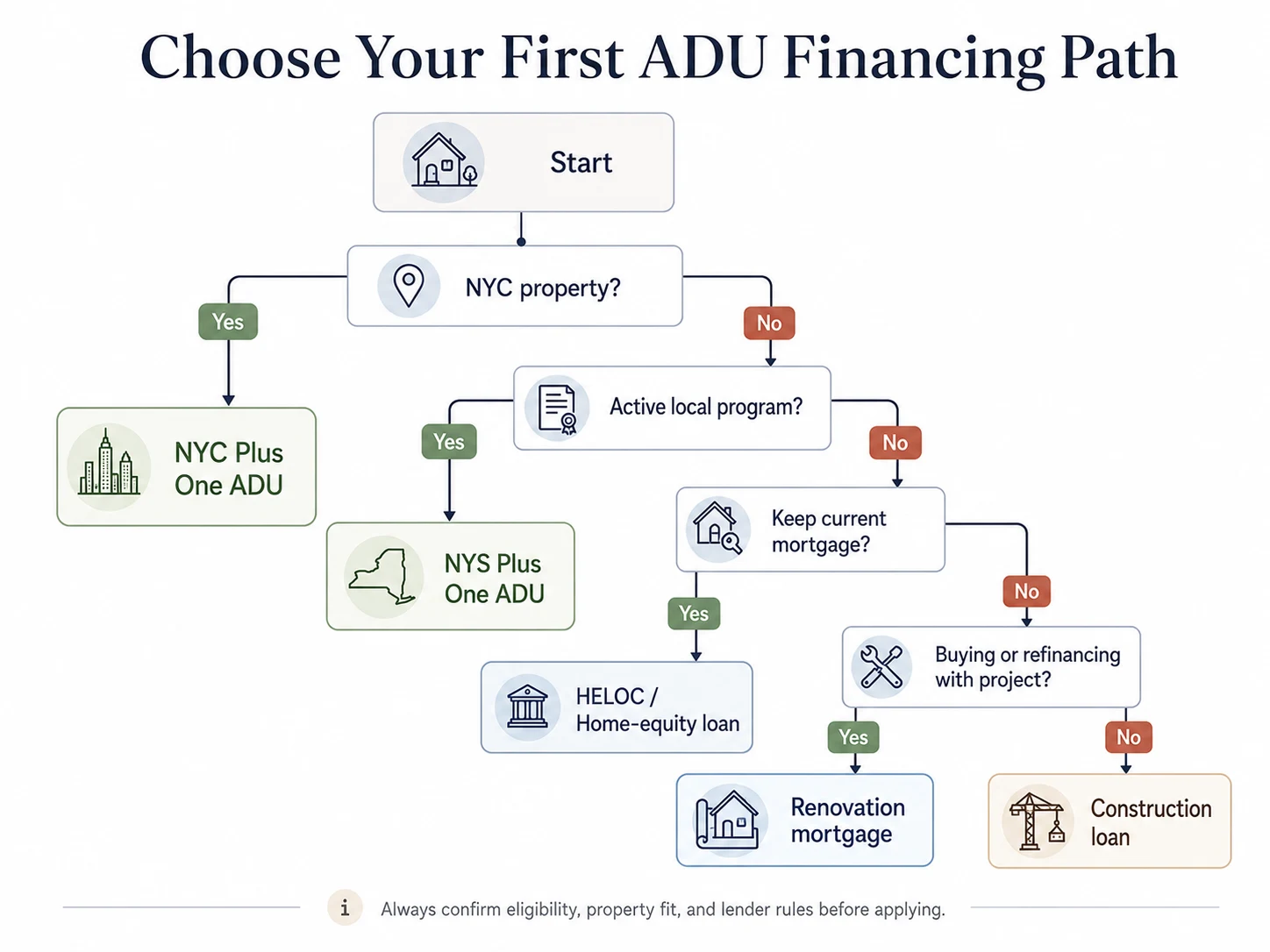

Bottom line: Most New York homeowners should check Plus One ADU eligibility first, then choose a loan path based on four things — whether the property is in New York City or the rest of the state, whether your local municipality has an active program administrator, whether you can live with long-term rent and owner-occupancy restrictions, and whether you need to keep a low first mortgage. Outside NYC, Plus One support is generally up to $125,000 total per project (and that total often includes design, permitting, and program delivery, so the money for actual construction can be lower). In NYC, eligible owner-occupants can combine up to $175,000 in state grant funds with up to a $220,000 city loan — about $395,000 total — and the current NYC interest window runs through Friday, June 12, 2026. If you don’t qualify for either, the realistic paths are a HELOC, home-equity loan, cash-out refinance, renovation mortgage (FHA 203(k), Fannie HomeStyle, Freddie CHOICERenovation), or a construction loan. This page shows which lane to test first.

Free property check

See what you can build → get your free ADU report

Check your address before you chase financing. We’ll show what type of ADU may be feasible on your lot, which financing lane to test first, and what to confirm with your local program administrator or lender.

Check my property for free →ADU financing New York: what is the fastest path to test first?

New York homeowners have three financing lanes: public Plus One ADU support, mortgage-backed renovation financing, and private home-equity financing. Start with Plus One only if your location, income, property type, and tolerance for use-restrictions all fit. If any one of those fails, the fastest route is usually a loan that preserves your current mortgage rather than one that replaces it.

That’s the entire decision in two sentences. The rest of this page is how to act on it without wasting months or money.

The table below is the fastest way to find your lane. Find the row that sounds like you, then follow it across. Every figure is sourced and dated in the sections that follow.

| Your New York situation | First path to test | Why | The main catch | Next action |

|---|---|---|---|---|

| NYC owner-occupant, income up to 165% AMI, eligible 1–2 unit home | NYC Plus One ADU | The largest public support package in the state — up to ~$395,000 combined. | Income, property, rent, owner-occupancy and repayment restrictions; the interest window closes June 12, 2026. | Run the feasibility check, then HPD / Restored Homes intake. |

| Outside NYC, your municipality is on the HCR list and active | NYS Plus One via your local administrator | Direct ADU support through a vetted nonprofit/municipal partner. | Generally up to $125,000 total (construction portion can be lower); 10-year covenant; no short-term rentals. | Find your administrator in the lookup table below. |

| Municipality not listed, or income too high | Home-equity / renovation / construction loan | No waiting on public funding; you keep control. | Loan qualification, equity, rate, appraisal, contractor draws. | Compare the loan lanes. |

| You have an existing legal ADU and need the rent to qualify | Conventional or FHA path using ADU-rent rules | Rent from an existing legal unit may count — within limits. | Agency caps (often 30% of qualifying income) and documentation rules; rent from a unit you're building usually won't count. | Confirm the exact rule with a lender. |

| Existing unpermitted basement/garage unit | Legalization first, then Plus One or renovation financing | May bring the unit into code and unlock financing. | Work already done may not be reimbursable; some NYC legalization paths aren't open yet. | Verify with your local buildings department first. |

Always confirm eligibility, property fit, and lender rules before applying.

A quick vocabulary note

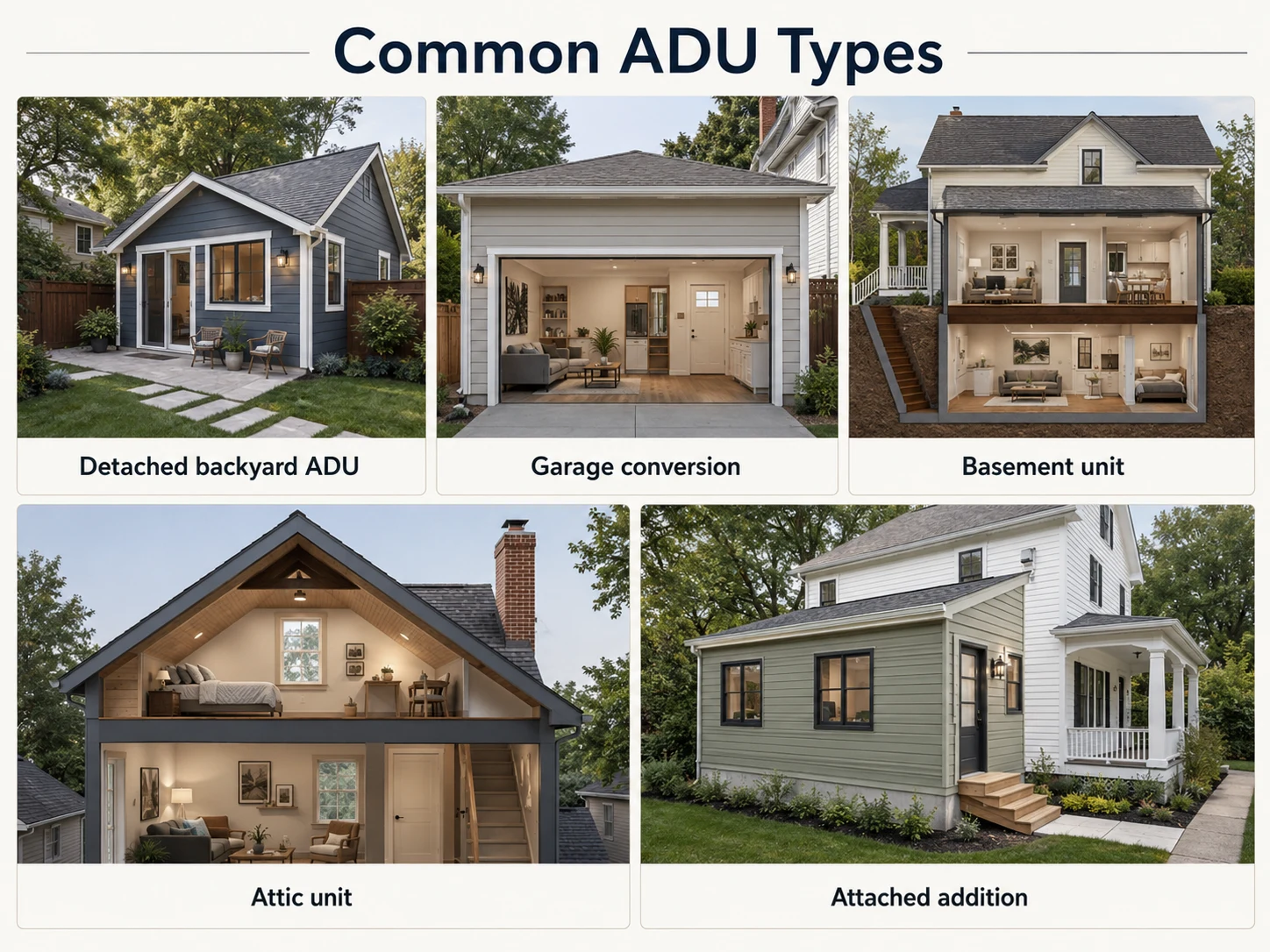

- ADU (accessory dwelling unit):

- called an ancillary dwelling unit in NYC — a secondary home on the same lot as a primary residence: a detached backyard cottage, garage conversion, basement or cellar unit, attic unit, or attached addition.

- HELOC:

- a revolving credit line secured by your home, usually at a variable rate.

- Cash-out refinance:

- replaces your existing mortgage with a larger one and hands you the difference in cash.

- Renovation mortgage:

- lets you borrow against your home's after-improvement value — what it'll be worth once the ADU exists.

- AMI (Area Median Income):

- the income benchmark HUD publishes annually; New York's grant programs cap eligibility at a percentage of it.

- Covenant:

- a recorded legal restriction that runs with the property for a set number of years.

- LPA (local program administrator):

- the nonprofit or municipal entity HCR designates to administer Plus One funds for a specific municipality or region.

Why we lead with Plus One: for the homeowner who qualifies and stays compliant, it is usually the cheapest money available — part of it is a grant that can be forgiven over the program’s regulatory period. But qualifying is narrow, and most New Yorkers won’t. We’re honest about that throughout, and the loan lanes below exist precisely for everyone the grant leaves out.

Do New York ADU grants actually pay for the whole project?

Short answer: Sometimes a grant closes a major gap, but outside NYC you should not treat Plus One as full project funding. HCR’s program provides up to $125,000 in total support per homeowner — and that total can include program delivery, design, permitting, oversight, and compliance, so the slice available for actual construction is often lower. HCR’s own program manual is blunt that additional funds will be needed in most or all cases. In NYC, the combined package is larger (up to ~$395,000) but the strings are tighter.

Here’s what the money can and can’t do.

What Plus One can pay for:

Design and architectural/engineering fees, permitting, environmental review and testing, construction and rehabilitation costs, and certain professional and developer fees. NYC’s term sheet lists renovation and construction costs, architectural and engineering fees, environmental testing, and a developer’s fee as potentially eligible. (Source: NYC HPD Plus One ADU Term Sheet, verified May 25, 2026.)

What Plus One generally won’t pay for:

Costs you incurred before the program agreement and environmental clearance, luxury upgrades beyond what’s needed to create a legal unit, unrelated landscaping, routine maintenance, taxes, debt payments, and insurance. The NYC term sheet states plainly: “luxury upgrades, or scope items beyond the work that is required to create a legal unit and address critical home repairs, will not be considered.” (Source: NYC HPD Term Sheet, verified May 25, 2026.)

Total award vs. money for construction

One thing nobody puts up front: across the state, the “$125,000” you see quoted is the total award, not the construction budget. We pulled the real split from individual administrators, because it changes what you actually have to build with.

| Administrator / area | Total support | What the total includes | Money toward construction |

|---|---|---|---|

| HCR baseline (statewide rule) | Up to $125,000 | Delivery, design, permitting, oversight, compliance | Manual says additional funds needed in most/all cases |

| CDLI (parts of Suffolk) | Up to $125,000 | Includes project-management costs | Construction capped around $115,000 |

| Hudson River Housing (Dutchess) | Up to $125,000 | Includes program delivery/administration | Up to ~$112,500 in direct assistance |

| RUPCO (Ulster/Columbia/Orange/Sullivan) | Current materials cite up to $112,500 | Program-dependent | Confirm per current round |

Sources: hcr.ny.gov/adu-program-manual; CDLI; Hudson River Housing / Town of Poughkeepsie; RUPCO/Ulster County. Verified May 25, 2026. Confirm the current split with your administrator before budgeting.

The damaging admission, stated plainly: the grant is real, but it is not “free ADU, no strings” money. It’s a public-benefit housing program — with income limits, compliance monitoring, biennial site visits, and a multi-year covenant that can trigger repayment if you break the rules or sell early. For the right homeowner — someone planning to stay long-term and rent to a family member or a long-term tenant — that tradeoff is often well worth it. For someone who wants to Airbnb the unit or sell in three years, it usually isn’t.

The reality check we wish more pages ran

| What homeowners hear | The more accurate version | Why it matters |

|---|---|---|

| "New York gives $125,000 for ADUs." | That's the total award in participating municipalities; the construction slice is often lower, and not every town or homeowner qualifies. | Saves you months chasing a program your town isn't in. |

| "NYC gives almost $400,000." | Eligible NYC owners may combine a state grant and a city loan, subject to underwriting — it isn't automatic, and part is a repayable loan. | Sets realistic expectations before you spend on plans. |

| "It's a grant, so there are no strings." | HCR requires long-term housing use, owner-occupancy, monitoring, and a declining-balance repayment covenant for at least 10 years. | Protects you from a covenant surprise at resale. |

| "I'll start now and get reimbursed." | Work done before selection, award, and environmental clearance may be ineligible. | This is the single most expensive mistake homeowners make. |

Free feasibility check

Check your ADU funding fit → get your free report

See whether your property even looks like a public-funding candidate before you spend a dollar on plans or pre-development.

Get my free ADU report →Is NYC Plus One ADU open right now?

Yes. NYC reopened the Plus One ADU program on March 18, 2026 — the first reopening since the initial 2024 intake — and the current opportunity to submit interest runs through Friday, June 12, 2026, on HPD’s program webpage. Funding is limited, so the window matters. Always confirm the current status with HPD/Restored Homes before you apply.

NYC’s first round in 2023 drew over 1,300 submissions within two weeks before closing in February 2024, so demand outstrips funding fast. Alongside the reopening, the city launched its “ADU for You” toolkit and a Pre-Approved Plan Library — currently nine DOB-reviewed detached backyard-cottage designs — that can shorten the permitting path because the city has already done an initial code review. (Source: NYC HPD press release, March 18, 2026, verified May 25, 2026.)

If you’re an income-eligible NYC owner-occupant and the program looks like a fit, the next two weeks-to-a-month are the window to submit interest. The eligibility detail is in the NYC section below.

Am I in a New York Plus One ADU municipality?

Maybe — and this is the question that decides everything. New York’s Plus One ADU funds flow through local program administrators (LPAs), not a single statewide homeowner portal. HCR’s public homeowner page lists the participating municipalities and their administrators; HCR’s 2026 Gap Loan materials describe 14 local program administrators working with over 80 communities statewide. You apply through the administrator that serves your town. If your town isn’t covered, the state program simply isn’t available to you yet, and you move to the loan lanes.

We pulled the participating-municipality list directly from HCR and mapped each town to its administrator, the typical funding, and the live status where an administrator publishes it. Status changes round to round; always confirm intake is open before applying.

New York Plus One ADU local administrator lookup

Sources: hcr.ny.gov/adu participating-municipality list and the individual administrator pages linked below. Verified May 25, 2026. Funding figures reflect currently published amounts; confirm your project’s split and current status with the administrator.

| Municipality | County / region | Administrator (LPA) | Current status | Support | Source |

|---|---|---|---|---|---|

| New York City (5 boroughs) | NYC | NYC HPD + Restored Homes HDFC | Open — interest window through June 12, 2026 | Up to ~$395,000 (grant + loan) | nyc.gov HPD |

| Huntington | Suffolk | LIHP | Active | Up to $125,000 | lihp.org/adu |

| Riverhead | Suffolk | LIHP | Active on LIHP listing — verify vs. HCR | Up to $125,000 | lihp.org/adu |

| Brookhaven | Suffolk | LIHP | Closed (per LIHP listing) | Up to $125,000 | lihp.org/adu |

| Islip | Suffolk | LIHP | Closed (per LIHP listing) | Up to $125,000 | lihp.org/adu |

| Southold | Suffolk | LIHP | Closed (per LIHP listing) | Up to $125,000 | lihp.org/adu |

| Babylon | Suffolk | CDLI | Closed/waitlist (per CDLI) | Up to $125,000 (constr. ~$115,000) | cdli.org |

| Southampton, Shelter Island, East Hampton | Suffolk | CDLI | Open/limited (per CDLI); HCR lists East Hampton "pending contract execution" | Up to $125,000 | cdli.org |

| Dobbs Ferry, Irvington, Hastings-on-Hudson, Cortlandt, Croton-on-Hudson, Yorktown | Westchester | Habitat NYC & Westchester | Active program page | Up to $125,000; homeowner funds likely needed | habitatnycwc.org |

| Bedford | Westchester | (HCR-listed under Habitat) | Verify — not on current Habitat eligibility list | Up to $125,000 | hcr.ny.gov/adu |

| Amenia, Beacon, Clinton, Northeast, Pine Plains, Pleasant Valley, Poughkeepsie (Town), Rhinebeck, Stanford, Unionvale | Dutchess | Hudson River Housing | Rolling; priority for shovel-ready | Up to $125,000 (incl. delivery); ~$112,500 direct | townofpoughkeepsie.com |

| Ancram, Austerlitz, Canaan, Chatham, Claverack, Clermont, Copake, Cornwall, Ellenville, Gallatin, Germantown, Ghent, Greenport, Hillsdale, Kinderhook, Kingston, Livingston, Lloyd, New Lebanon, Olive, Philmont, Plattekill, Rosendale, Saugerties, Stockport, Stuyvesant, Ulster, Wawayanda, Woodstock | Columbia / Ulster / Orange / Sullivan | RUPCO | Open per RUPCO | Current materials cite up to $112,500 | rupco.org/plusone |

| Albany, Troy | Capital Region | TAP Inc. | Verify current intake | Up to $125,000 (up to 10% admin) | tapinc.org |

| City of Buffalo | Western NY | BURA | Funding available per BURA | Up to 100% construction/rehab for ≤120% AMI owner-occupants; confirm cap | buffalourbanrenewal.com |

| Ithaca | Tompkins | Ithaca Neighborhood Housing Services | Verify | Varies | ithacanhs.org |

| Utica | Oneida | Utica Center for Development | Verify | Varies | ucdevelopment.org/adu |

| Amherst | Erie | Town of Amherst | Verify | Varies | amherst.ny.us |

Three things this table makes obvious that single-source pages hide. First, most of upstate and the Hudson Valley runs through one administrator, RUPCO. Second, “listed” is not “open” — several Suffolk towns currently show closed. Third, two official sources can disagree — HCR lists East Hampton as “pending contract execution” while CDLI shows it in its program, so confirm directly before you rely on either.

If your municipality is listed but status is unclear, call the administrator and ask: Is intake open right now? Is my ADU type eligible? Are funds still available this round? Can I use my own architect and contractor? How much actually reaches the homeowner after delivery and administration fees? What income documentation do you need? Do not pay for full construction drawings until feasibility and funding are clearer.

If your municipality is not listed, you still have moves. Check your local zoning anyway — you may be able to build with private financing today. Submit HCR’s program-expansion interest form so your town is on record for future rounds. Then read the loan lanes below; they don’t depend on your town being funded.

What we verified (Plus One status)

We read HCR’s official Plus One ADU page and participating-municipality list, the NYC HPD Plus One materials, the HPD Term Sheet, the March 18, 2026 HPD/DOB press release, the NYC DOB Ancillary Dwelling Units page, and the individual administrator pages (LIHP, CDLI, Habitat NYC & Westchester, Hudson River Housing, RUPCO, TAP, BURA). We confirmed the $85 million program size, the local-administrator model, the ~$125,000 total outside-NYC support, the NYC ~$395,000 combined structure, the June 12, 2026 NYC interest window, and the 10-year minimum regulatory period. We did not call every administrator to confirm live slot counts; confirm those before you apply. Verified May 25, 2026.

Check your address

Check my address against this list → get my free ADU report

This is the highest-stakes “am I eligible?” moment on the page. Before you call an administrator, see what your specific lot looks like.

Check my property for free →How is NYC ADU financing different from the rest of New York?

NYC runs its own Plus One structure through the Department of Housing Preservation and Development (HPD), administered with Restored Homes HDFC. Eligible owner-occupants can combine up to $175,000 in HCR grant funds with up to a $220,000 HPD loan — about $395,000 combined — roughly three times what’s available elsewhere in New York. But NYC layers on income, property, rental, occupancy, and affordability controls the rest of the state’s program doesn’t, and the NYC version is where the strings are tightest.

The NYC Plus One funding stack, decoded

| Component | Amount | What it actually means |

|---|---|---|

| HCR grant | Up to $175,000 | The state grant portion. On the deferred path it functions as forgivable money. |

| HPD loan | Up to $220,000 | A city loan at 5% interest, which can be lowered in quarter-point steps to as low as 0% for affordability, and stretched from 15 up to 30 years. |

| Combined | Up to $395,000 | Not automatic — it depends on your income, your project scope, and underwriting. |

| (Separate HCR gap loan) | $10,000–$85,000 at 0% | A separate state program for applicants already approved for Plus One who need to close a shortfall — and only after all other funding is secured. Lent through selected CDFI or nonprofit program lenders, not handed out directly. |

The HPD loan’s design centers on one rule: HPD sets your monthly payment so your household keeps at least $200 of monthly cash flow after debts. If a repayable loan isn’t affordable even at 0% over 30 years, HPD converts it to a deferred, forgivable loan — but that triggers a rent restriction. The two paths are genuinely different deals:

Repayable vs. deferred-forgivable: the NYC fork

| Repayable loan | Deferred-forgivable loan | |

|---|---|---|

| Interest | 5%, reducible toward 0% for affordability | Effectively 0% / forgiven over the term |

| Monthly payment | Yes (set to leave ≥$200 cash flow) | Deferred |

| Rent restriction on the ADU | No mandated rent cap | Yes — rent at/below 100% AMI at lease-up, increases capped at 2%/yr |

| Regulatory term | Owner-occupancy for the loan term | 15-year regulatory agreement |

| Best for | Owners who can carry a payment and want flexibility | Owners who need the cheapest money and accept the rent cap |

Source: NYC HPD Plus One ADU Term Sheet, verified May 25, 2026.

Who’s eligible in NYC

- •Owner-occupant of an eligible home. Note a real source nuance: HPD's public page describes detached, semi-detached, or semi-attached homes with one to two existing units, while the HPD term sheet describes one-unit single-family detached buildings. Confirm your specific property type through HPD/Restored Homes screening rather than assuming every one- or two-family home qualifies.

- •Household income up to 165% of AMI, with preference for lower-income households. The dollar figure varies by household size and updates annually — check the current HPD/HCR AMI chart for your household.

- •Current on existing mortgages, with valid homeowner's insurance, and current (or on a payment plan) with the Department of Finance and Department of Environmental Protection.

- •Home must be outside the Special Coastal Risk District and free of disqualifying violations (unless they relate to the ADU work or you agree to fix them).

- •A $200 non-refundable fee applies after pre-screening.

Source: NYC HPD Term Sheet and HPD Plus One page, verified May 25, 2026.

The NYC strings nobody puts above the fold

On the deferred-forgivable path — the one that gives you the most non-repayable money — a 15-year regulatory agreement applies. Under it: the new ADU must be rented at or below 100% AMI at lease-up, with annual increases capped at 2%, and the tenant must be offered a renewal (family members occupying the unit may be exempt). You must keep the home as your primary residence — at least 270 days per year — for the loan term, and sign a primary-residence affidavit. If you sell to a non-eligible buyer or do a cash-out refinance during the term, the loan must be repaid. And you generally cannot rent out both the main home and the ADU. (Source: NYC HPD Term Sheet, verified May 25, 2026.)

None of that should scare off the core reader — a homeowner who wants to house family or hold a long-term tenant and stay put. It should scare off the homeowner who wanted a short-term rental cash machine, and it’s better to know now than after a $30,000 design bill.

NYC feasibility check

See if your NYC property looks ADU-feasible → get your free report

City of Yes legalized ADUs citywide in 2024, but flood zones, historic districts, and contextual zoning districts still rule out many lots. Get your report before you submit interest by June 12.

Check my NYC property →What are the strings attached to New York’s Plus One ADU money?

Plus One funding — statewide and in NYC — comes with housing-use obligations: income eligibility, owner-occupancy, local zoning compliance, long-term tenant or family use (no short-term rentals), a recorded covenant of at least 10 years, compliance monitoring with site visits every two years, and possible repayment if you break the rules. These aren’t fine print; they’re the core deal.

- ✅

The 10-year covenant and recapture (verified)

HCR requires a Regulatory Agreement with a regulatory period of not less than 10 years, secured by a declining-balance enforcement document. The obligation shrinks over the covenant period and reaches zero after it ends — but if you violate the terms before then, a portion can be recaptured.

Source: hcr.ny.gov/adu, verified May 25, 2026

- ✅

No short-term rentals (verified)

HCR's compliance monitoring confirms the ADU is "being used as permanent housing rather than as a short-term rental." Airbnb, seasonal, and vacation use are treated as noncompliance that can trigger repayment.

Source: hcr.ny.gov/adu, verified May 25, 2026

- ✅

Owner-occupancy and tenant use (verified)

The home must remain the owner's primary residence, and the ADU is for long-term tenants or family members. In NYC, primary residence means at least 270 days per year.

Source: hcr.ny.gov/adu; NYC HPD Term Sheet; verified May 25, 2026

- ✅

The work-before-approval trap (verified)

Costs incurred before environmental clearance and a signed program agreement may be ineligible. If you've already started — or already built an unpermitted unit — don't assume you'll be reimbursed.

Source: NYC HPD Term Sheet and HCR program structure, verified May 25, 2026

When the strings are worth it (our editorial conclusion)

Plus One makes sense when the grant is the difference between impossible and feasible, you plan to stay in the home long-term, and you intend the ADU for family or a long-term tenant. It’s a poor fit if you want short-term rental income, expect to sell or cash-out refinance soon, or value maximum flexibility. If you’re in that second group, the loan lanes below give you that flexibility — at the cost of a monthly payment, which is the trade you’d be making anyway.

What loan should you test if you don’t qualify for a New York ADU grant?

If Plus One doesn’t fit — wrong town, income too high, can’t accept the covenant, or you need to move faster than the program allows — your first loan to test depends on three questions: Do you want to keep your current mortgage? Do you have equity? Is the ADU part of a purchase or refinance? For homeowners with equity, second-lien or home-equity paths are often the first non-grant lane to test, because they can preserve a low existing first mortgage.

We sort the table by best fit, not by rate. We don’t quote APRs or monthly payments — those depend entirely on your borrower profile, the property, and current market conditions. We’ve added a column for the New York-specific issue each path raises.

New York ADU loan path matrix

| Financing path | Best fit | Watch out for | NY-specific issue to verify |

|---|---|---|---|

| HELOC (home equity line of credit) | You have equity and want to keep a low first mortgage; useful for staged draws during permitting | Usually a variable rate; payment can rise; may not produce enough alone | Confirm the lender lends on NY ADUs and whether the ADU must already be legal |

| Home-equity loan (second mortgage) | You want a fixed payment and to keep your first mortgage | Equity and debt-to-income limits; closing costs | NY mortgage recording costs may apply on a new lien |

| Cash-out refinance | Your current mortgage rate is at or above today's market, or you want one consolidated loan | Replaces your first mortgage — a poor trade if your existing rate is low; closing costs apply | NY mortgage recording tax can be significant on a larger loan |

| Fannie Mae HomeStyle Renovation | Buying or refinancing with ADU work rolled in, borrowing against after-completed value | Contractor, appraisal, documentation rules | Confirm NY lender offers it and how ADU rent is treated |

| Freddie Mac CHOICERenovation | Buying or refinancing, including constructing a new ADU or renovating an existing one | Lender execution and documentation | Confirm NY availability |

| FHA 203(k) | Owner-occupant who fits FHA and has eligible ADU work | FHA mortgage insurance; contractor/consultant process | Confirm eligible ADU scope with an FHA lender |

| Construction-to-permanent loan | Larger detached or ground-up builds; appraisal based on as-completed value | Draw schedule tied to inspections; reserves; builder requirements | Confirm draw process and NY licensing for your builder |

| After-completed-value renovation loan (e.g., RenoFi-style) | Low current equity — borrows against the home's projected post-ADU value | Product availability varies by lender and state | Confirm the product is offered in New York |

| Personal loan / gap financing | A small remaining gap only | Higher cost, shorter term, unsecured | — |

| HEI (Home Equity Investment — a lump sum for a share of future home value, no monthly payment) | Cash-flow-sensitive owners who can't add a payment | Limited state availability; you give up equity at sale/refi | Confirm New York availability before relying on it |

How to actually choose. If you have strong equity and a low existing mortgage rate, a HELOC for an ADU or fixed home-equity loan lets you keep that rate while you build; some owners use a HELOC during the build, then refinance into a fixed product once the ADU is finished, rented, and the home reappraises higher. If your existing rate is high, a cash-out refinance for an ADU can consolidate everything at one fixed rate. If you have little equity, the after-completed-value renovation loans and ADU construction loans exist precisely because they appraise on what the home will be worth with the ADU, not today. And if the ADU is part of a home purchase, the renovation mortgages (HomeStyle, CHOICERenovation, 203(k)) let you finance the buy and the build in one loan.

These are illustrative examples, not guarantees of returns or terms. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Compare mortgage options

Explore ADU mortgage and refinance options

If Plus One doesn’t fit your municipality, income, timeline, or use case, compare mortgage-backed paths — before you replace a low-rate first mortgage. This is educational — approval, rates, terms, and eligibility vary by borrower, property, lender, and location.

Compare ADU loan paths →Via Mortgage Research Center — affiliate disclosure applies.

Can projected ADU rent help you qualify for financing in New York?

Sometimes — but less broadly than homeowners expect, and usually only for a unit that already exists. Fannie Mae, Freddie Mac, and FHA each allow ADU rental income in specific circumstances, generally capped at 30% of qualifying income, with documentation rules tied to occupancy and loan purpose. The single most important question to ask a lender up front: will this program count income from the ADU I’m building, or only from an existing legal ADU?

The rules differ by agency. Here’s the shape of each — treat it as orientation and confirm the current version with your lender, since guidelines change. For more detail, see our guide on financing an ADU rental.

| Agency | Whose rent counts | Loan purpose | Cap | Key limit |

|---|---|---|---|---|

| Fannie Mae | Existing ADU only, one-unit principal residence | Purchase or limited cash-out refinance | 30% of total qualifying income | Won't count rent from a unit you're building |

| Freddie Mac (CHOICERenovation) | Subject one-unit primary; can fund a new or existing ADU | Purchase / no-cash-out | 30% of qualifying income | Income from an illegal unit isn't counted |

| FHA (incl. 203(k)) | ADU on the subject property | Purchase/refinance; 203(k) for ADU work | 30% of effective income | No ADU rent allowed on FHA cash-out refinance |

Source categories: Fannie Mae Selling Guide §B3-3.8-01; Freddie Mac ADU fact sheet, Feb 2026; HUD Mortgagee Letter 2023-17. Verified against published guidance May 25, 2026; confirm current figures with a licensed lender.

The plain-English decision rule: if your financing only works because the lender counts future ADU rent, get that confirmed in writing before you spend on design. Lenders treat “income from a unit that doesn’t exist yet” very differently from “income from a legal, leased unit,” and the gap between those two assumptions has sunk more than a few ADU budgets.

Which financing path fits a detached ADU, garage conversion, basement, attic, or legalization?

The ADU type changes the best financing path because it changes cost, permit risk, appraisal complexity, and whether the project counts as new construction, renovation, or legalization. A backyard cottage and a basement conversion are not the same financing problem — and in NYC, they’re not even the same legal problem.

| ADU type | Usually most relevant paths | Special risks |

|---|---|---|

| Basement / cellar ADU | NYC Plus One, NYS Plus One, FHA 203(k), renovation loan, HELOC | Ceiling height, egress, flood-zone limits; in NYC, legalization and new cellar ADU applications aren't being accepted yet |

| Garage conversion | Plus One, HELOC, renovation loan, FHA 203(k) | Structural/code upgrades, loss of parking/storage — but not restricted as a backyard ADU in NYC |

| Detached backyard ADU (DADU) | Plus One, construction-to-permanent, renovation loan, HELOC | Site work, utility laterals, setbacks, appraisal comps |

| Attached addition | Renovation loan, Plus One, construction loan | Structural integration; zoning and building permits |

| Attic ADU | NYC Plus One (if eligible), renovation financing | Egress, ceiling height, fire safety |

| Existing unpermitted unit | Plus One if legalizable, renovation loan after feasibility | Can't be financed as income-producing until compliant; prior work may be ineligible for reimbursement |

NYC City of Yes ADU rules that affect financing

In NYC, the City of Yes for Housing Opportunity zoning reform (adopted December 2024 via Local Laws 126 and 127) legalized ADUs up to 800 square feet in one- and two-family homes, with one ADU per home, an owner-occupancy requirement at initial occupancy, and no additional parking required. But the details matter, and they’re where homeowners get tripped up:

- ⚠New backyard (rear-yard) ADUs are prohibited in Historic Districts, in R1-2A/R2A/R3A districts outside the Greater Transit Zone, and in part of the Special Bay Ridge District. However, converting an existing garage is not treated as a backyard ADU under Zoning 12-10, so garage conversions are not restricted in those areas.

- ⚠Subgrade (basement/cellar) ADUs are not permitted in high-risk flood areas — FEMA's Special Flood Hazard Area, the Coastal Flood Risk Area, and DEP's 10-Year Rainfall Flood Risk Area.

- ⚠Legalizing an existing basement/cellar unit (Local Law 126) is limited to units that existed before April 20, 2024, in specific program-area community districts (parts of the Bronx, Brooklyn, Manhattan, and Queens), and — critically — legalization and new cellar ADU applications are not currently being accepted until DOB finalizes the Housing Maintenance Code amendment and rules. If your plan hinges on a basement unit, confirm the application path is open before you budget around it.

Source: nyc.gov DOB Ancillary Dwelling Units, verified May 25, 2026.

Outside NYC

There is no statewide ADU law yet — the Accessory Homes Act (S4547 / A4854) remains pending in Albany as of this writing — so your local zoning governs entirely. Check your town’s code before you assume any ADU type is allowed.

What can make ADU financing fail in New York even when the money looks available?

Financing falls apart for predictable reasons: the property isn’t eligible, the ADU can’t be permitted, the owner misses income or occupancy rules, the project already started, the budget gap is too large, or the owner can’t accept the program’s long-term restrictions. Almost all of these are knowable before you spend money — which is exactly why a feasibility check comes first.

| Risk | Why it matters | What to do |

|---|---|---|

| Municipality not active | State money runs through selected administrators only | Use the lookup table above; contact the LPA |

| Income too high | Public funding targets low/middle-income owners | Test loan paths instead |

| Not owner-occupied | Plus One targets owner-occupants | Confirm local rules; consider private financing |

| Short-term rental plan | Plus One ADUs can't be Airbnb | Use private financing or change the use case |

| Work already started | Prior costs may be ineligible | Pause and verify before spending more |

| Flood / coastal restriction | Critical for NYC basement units and coastal lots | Check HPD/DOB and local code |

| No plan for the budget gap | HCR says extra funds are usually needed | Pair the grant with savings or a loan, or redesign |

| Future rent assumed incorrectly | Lenders may not count rent on a unit that doesn't exist yet | Ask the agency-specific rent question early |

Flag your disqualifiers early

Find your first safe step → get your free ADU report

It flags the disqualifiers above against your actual address, before you apply, borrow, or pay for plans.

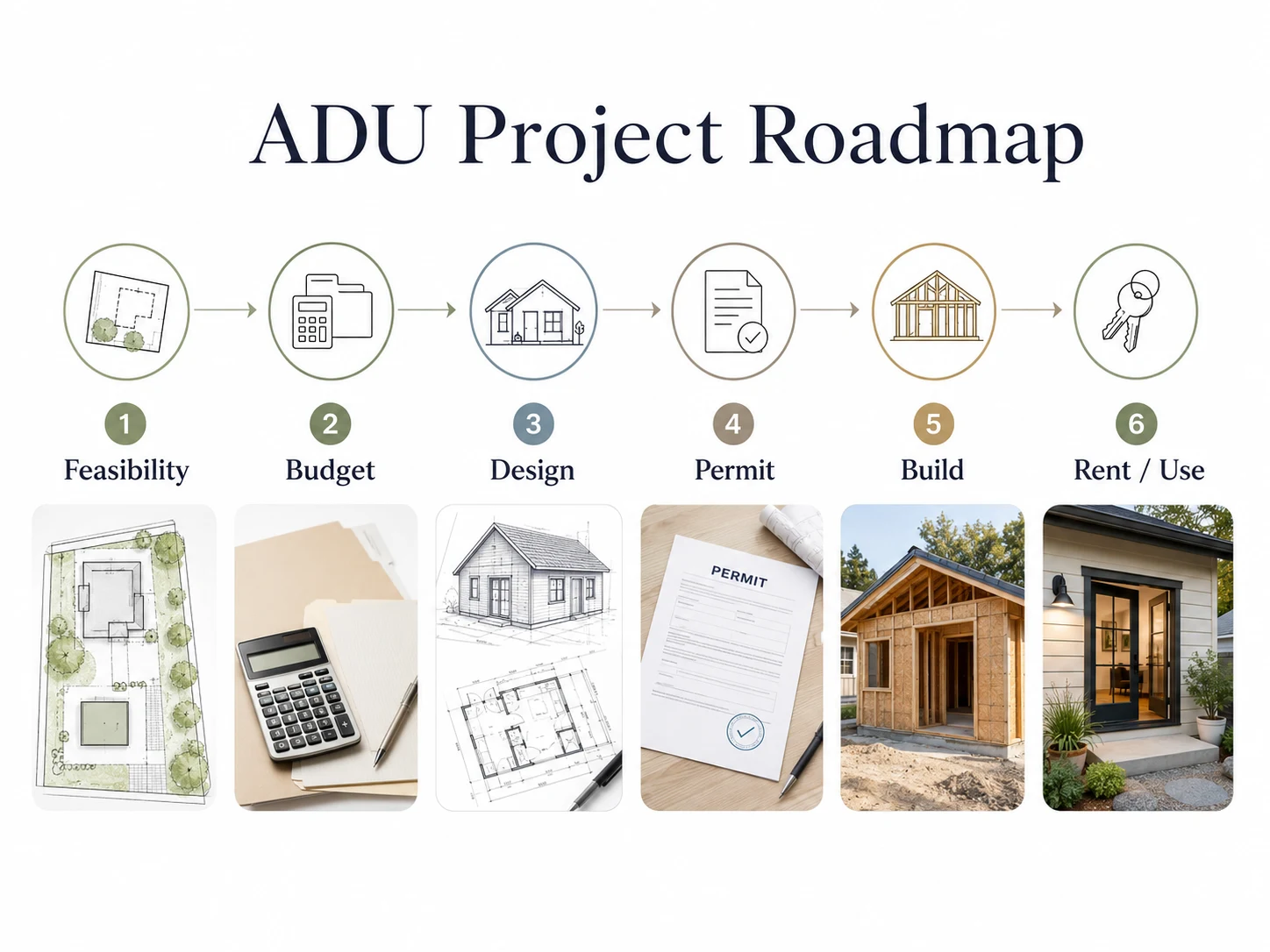

Get my free ADU report →How do you apply without wasting months?

Start with eligibility and feasibility, not a full design package. Confirm location, owner-occupancy, income band, ADU type, and zoning/building feasibility — and decide whether you can live with the program restrictions. Then contact the correct administrator or lender. Doing it in this order is the difference between a built ADU and a folder of expensive, unusable drawings. In NYC specifically, expect roughly 18–24 months from intake to a finished, leased unit (a planning estimate based on program and local-administrator guidance, not a guarantee).

A realistic 7-step action plan

- 1

Run a feasibility / path check.

Identify your likely ADU type and financing lane.

- 2

Check the local administrator table above.

Decide whether public funding is worth pursuing for your town.

- 3

Gather property basics:

deed, latest tax bill, mortgage statement, homeowner's insurance, and a rough idea of the ADU type.

- 4

Estimate income eligibility

against the current AMI chart. Never submit inaccurate figures.

- 5

Ask the program or lender the right questions

(see below) before you formally apply.

- 6

Verify zoning and building blockers

with your local department — flood zone, historic district, setbacks, egress.

- 7

Choose your next step:

apply to the program, pursue a loan, or redesign to fit what's fundable.

Document checklist by route

| Route | Have ready |

|---|---|

| NYC Plus One | Deed, mortgage statement (current), homeowner's insurance, proof current with DOF/DEP, income docs, property type confirmation, $200 fee after pre-screen |

| NYS Plus One (local admin) | Deed, income documentation, proof of owner-occupancy, rough ADU scope, any existing survey/plans |

| HELOC / home-equity loan | Income docs, mortgage statement, equity estimate, credit profile |

| Renovation mortgage / FHA 203(k) | Stamped plans, contractor bid/contract, appraisal access, income docs |

| Construction loan | Detailed budget, plans, signed contractor agreement, contingency reserve |

Ask the local Plus One administrator:

- →Is intake open now?

- →Is my municipality included this round?

- →How many slots remain?

- →What ADU types are eligible?

- →Are already-started projects eligible?

- →How much reaches the homeowner after delivery/admin fees?

- →What income documentation is required?

- →What covenant, rent, and owner-occupancy restrictions apply?

- →Will I need additional funds?

- →Can I use my own architect or contractor?

Ask a lender:

- →Do you finance ADUs in New York?

- →Do you count future ADU rent, existing ADU rent, or neither?

- →Is this a HELOC, home-equity loan, renovation mortgage, construction loan, or refinance?

- →Will it replace my first mortgage?

- →How are draws handled?

- →What appraisal assumptions are used — current value or as-completed?

- →What contractor documentation is required?

- →Are there NY mortgage-recording-tax or licensing issues to budget for?

Compare ADU loan paths

Compare ADU loan paths

Use this once you know a grant is unlikely or won’t cover the project — explore mortgage-backed options before committing to any single lane.

Compare ADU mortgage options →Via Mortgage Research Center — affiliate disclosure applies.

Free resource

Download the free New York ADU Financing Starter Kit

Get the document checklist, the local-program questions, the lender questions, and a one-page worksheet for weighing grant restrictions against loan flexibility — everything in this guide, condensed to act on.

Get the free Starter Kit →Frequently asked questions

Does New York give grants for ADUs?

Yes, but not through a simple statewide application. New York's Plus One ADU Program funds selected local governments and nonprofits that administer ADU support for eligible homeowners in participating municipalities. You apply through your local program administrator. (Source: hcr.ny.gov/adu, verified May 25, 2026.)

How much is the New York ADU grant?

Outside NYC, Plus One provides up to $125,000 total per homeowner (the construction portion is often lower, and additional funds are usually needed). In NYC, eligible owner-occupants may access up to $175,000 in HCR grant funds plus up to a $220,000 HPD loan — about $395,000 combined. (Sources: hcr.ny.gov/adu; NYC HPD Term Sheet; verified May 25, 2026.)

Is NYC Plus One ADU open right now?

Yes — NYC reopened the program March 18, 2026, and the current interest window runs through Friday, June 12, 2026. Funding is limited; confirm status with HPD/Restored Homes before applying.

Who qualifies for NYC Plus One ADU?

Owner-occupants of eligible homes, with household income up to 165% of AMI, current on mortgage, insurance, and municipal payments, on a property outside the Special Coastal Risk District and free of disqualifying violations. Exact eligible property type must be confirmed through HPD/Restored Homes screening. A $200 fee applies after pre-screening.

Can I use Plus One ADU money for an Airbnb?

No. HCR-funded Plus One ADUs are for long-term housing. Short-term, seasonal, or vacation rental use is treated as noncompliance that can trigger repayment.

Can I get reimbursed for an ADU I already started or built?

Don't assume so. Costs incurred before program clearance and a signed agreement may be ineligible, and an existing unpermitted unit generally can't be financed as income-producing until it's brought into compliance. Confirm with your administrator before spending more.

Can I use my own contractor for NYC Plus One?

NYC's program uses a registered design professional and contractor from a pre-qualified list, overseen by the program administrator. Confirm specifics with Restored Homes / HPD before applying.

Can ADU rental income help me qualify for a mortgage?

Sometimes — usually only for an existing legal ADU. Fannie Mae, Freddie Mac, and FHA each allow it in specific cases, commonly capped at 30% of qualifying income, with documentation rules. Confirm the exact rule with your lender.

Can FHA 203(k) finance an ADU in New York?

Yes — FHA's 203(k) allows certain ADU work, including converting a one-family home to add an ADU, adding an attached ADU, and renovating existing ADUs, subject to FHA requirements.

Do NYC ADUs need parking?

No. Under City of Yes, NYC does not require additional parking for a new ADU.

How big can a NYC ADU be?

Up to 800 square feet of zoning floor area, one ADU per one- or two-family home, with additional rear-yard limits for detached units.

Can I legalize my basement apartment in NYC right now?

Not yet through the pilot path. Legalization and new cellar ADU applications are not currently being accepted while DOB finalizes the Housing Maintenance Code amendment and rules under Local Law 126. The unit must also have existed before April 20, 2024 and sit within the designated program-area community districts.

What if my town isn't on the Plus One list?

Use the loan-path matrix above, check your local zoning (you may still be able to build privately), submit HCR's program-expansion interest form, and re-check the list periodically — HCR has added municipalities across multiple funding rounds.

Is a grant always better than a HELOC?

Not always. A grant reduces borrowing, but it brings income limits, occupancy rules, rent restrictions, program timelines (often 18–24 months in NYC), and repayment risk. A HELOC is faster and more flexible but adds debt and payment risk. The right answer depends on your timeline, your tolerance for restrictions, and whether you qualify.

Can I sell or refinance after receiving Plus One funds?

Possibly, but it may trigger repayment or compliance obligations depending on the program, timing, and transaction type. Both HCR and NYC include restrictions tied to sale, cash-out refinance, and noncompliance during the regulatory period.

How we researched this guide

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. For this guide we prioritized primary sources: New York State Homes and Community Renewal (HCR) and its Plus One ADU program materials, NYC Housing Preservation and Development (HPD) and the Plus One ADU Term Sheet, the NYC Department of Buildings and City Planning, the participating local program administrators, and federal agency mortgage guidance from Fannie Mae, Freddie Mac, and FHA/HUD. We used public homeowner forums only to understand the questions and decision friction homeowners face — never to prove financing, legal, zoning, or cost claims. Program status, income limits, funding availability, and agency lending rules change frequently; we re-verify these on the cadence noted in our source list. We present financing paths, not lender rankings, and we never sort recommendations by compensation.

Primary sources verified May 25, 2026

- •NYC HPD Plus One ADU Term Sheet

- •NYS HCR Plus One ADU (program page, municipality list, program manual, AMI chart)

- •NYC HPD/DOB press release, March 18, 2026 (June 12, 2026 window; 9 PAPL designs)

- •NYC DOB Ancillary Dwelling Units (LL126/127, 800 sf, flood/historic/Bay Ridge, cellar status)

- •Fannie Mae Selling Guide §B3-3.8-01 (ADU rental income, 30% cap)

- •Freddie Mac ADU fact sheet, February 2026

- •HUD Mortgagee Letter 2023-17 (FHA ADU rules)

A note on what we are and aren’t

The Dwelling Index is not a lender, broker, financial advisor, attorney, tax advisor, or building-code official. This page is educational and does not guarantee loan approval, grant approval, permit approval, rental income, property-value increases, or investment returns. Financing availability, underwriting, rates, fees, and eligibility vary by lender, borrower, property, and location. Verify ADU rules with your local planning and building department and confirm financing terms with a licensed lender.

Not sure where to start?

See what’s possible at your address — get your free ADU report in 60 seconds.

Check my property for free →Related guides