ADU Financing Calculator 2026: Compare Your Monthly Payment Across 7 Loan Paths

The bottom line

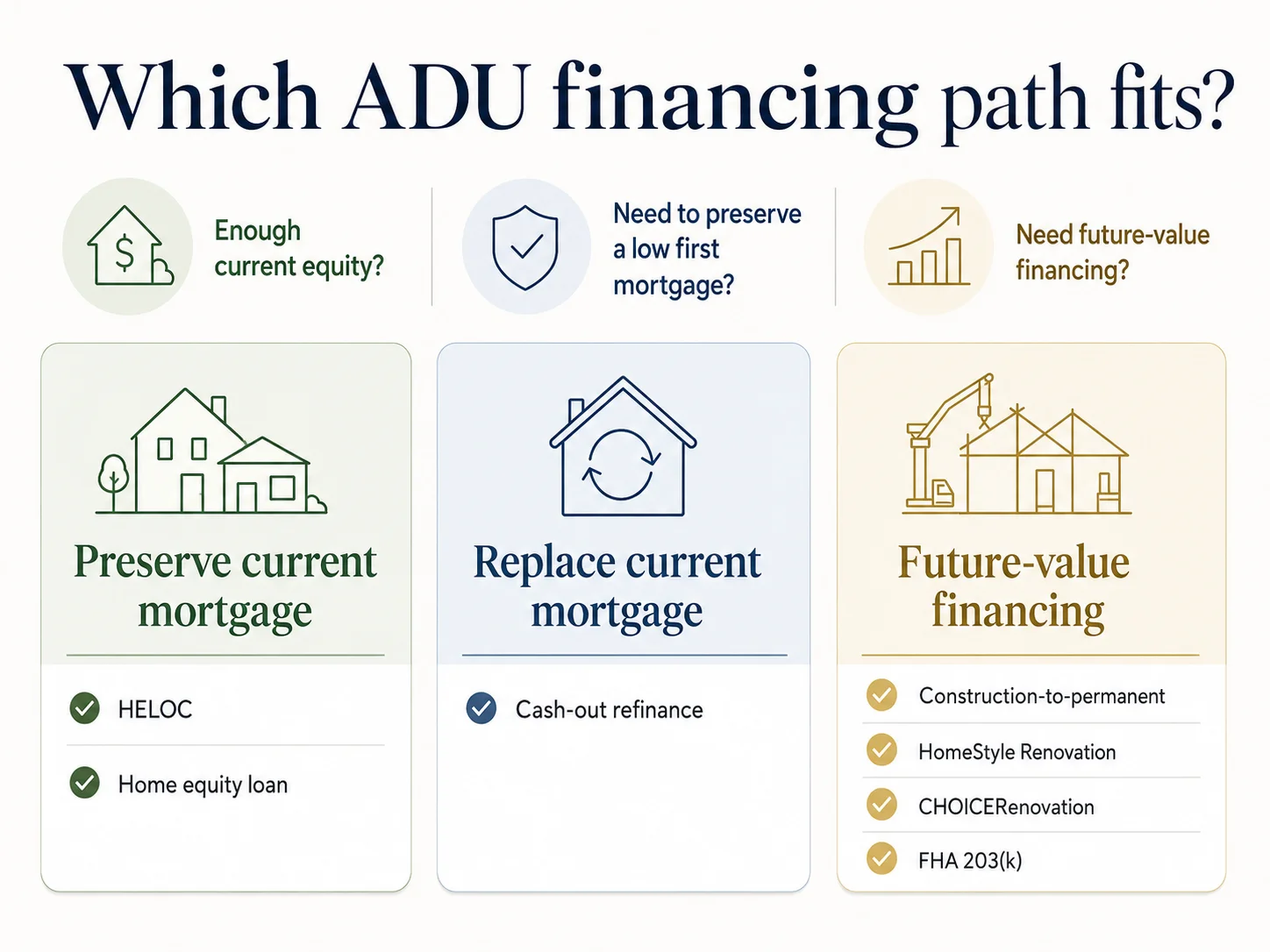

There are seven realistic financing paths for an ADU in 2026. The one that fits you depends on three numbers you already know: your current home value, your first-mortgage balance, and your total ADU budget. If (home value × 80%) − mortgage balance − other liens ≥ ADU budget, you likely qualify for a HELOC or home equity loan. If not, a construction-to-permanent or renovation loan can underwrite against what your home will be worth after the ADU is built. The calculator on this page runs all seven paths side by side at May 2026 benchmark rates so you can see the monthly payment and total interest for each one.

Which path should you test first?

| Your situation | Path to test first |

|---|---|

| Strong equity, want flexibility | HELOC (Path 1) |

| Strong equity, want fixed payment | Home equity loan (Path 2) |

| Existing rate at or above ~6.75% | Cash-out refinance (Path 3) |

| Low current equity, strong income, plans ready | Construction-to-perm (Path 4) |

| Buying or refinancing, adding ADU in one loan | HomeStyle or CHOICERenovation (Paths 5–6) |

| FHA borrower, conversion or addition scope | FHA Standard 203(k) (Path 7) |

Benchmark rates as of May 21, 2026: HELOC 7.21%, home equity loan 7.36%, 30-yr cash-out refi 6.78% APR (Curinos, Bankrate). Rates are illustrative averages; your actual rate will vary.

The ADU Financing Calculator

ADU Financing Calculator — 7 Paths, Side by Side

Enter your numbers. Benchmark rates as of May 2026 (Curinos, Bankrate). Illustrative estimates — not a loan offer.

Current appraised value

All-in: design, permits, construction

Used for cash-out refi risk flag

Existing HELOC, second mortgage, etc.

Path 1 — HELOC

Revolving line · variable rate · second lien

- Loan amount

- $200,000

- Draw period (interest-only / mo)

- $1,202

- Repayment period P&I / mo

- $1,576

- Est. total interest (30 yr)

- $322K

Path 2 — Home Equity Loan

Fixed lump sum · fixed rate · second lien

- Loan amount

- $200,000

- Monthly P&I

- $1,594

- Est. total interest (20 yr)

- $183K

Path 3 — Cash-Out Refinance

Replaces first mortgage · fixed rate

- New loan amount

- $600,000

- Monthly P&I

- $3,904

- Est. total interest (30 yr)

- $805K

Path 4 — Construction-to-Perm

Future-value underwriting · two-phase

- Construction interest / mo (est.)

- $3,750

- Permanent phase P&I / mo

- $3,904

- Est. total interest (30 yr perm)

- $850K

Path 5 — Fannie Mae HomeStyle

Renovation loan · as-completed value · up to 97% LTV

- Combined loan amount

- $600,000

- Monthly P&I

- $3,904

- Est. total interest (30 yr)

- $805K

Path 6 — Freddie Mac CHOICERenovation

Renovation loan · as-completed value

- Combined loan amount

- $600,000

- Monthly P&I

- $3,904

- Est. total interest (30 yr)

- $805K

Path 7 — FHA Standard 203(k)

Gov't-backed renovation · HUD ML 2023-17

- Combined loan amount

- $600,000

- Monthly P&I (excl. MIP)

- $4,073

- Est. total interest (30 yr, excl. MIP)

- $866K

Rates: Curinos national averages (HELOC 7.21%, home equity loan 7.36%), Bankrate (cash-out refi 6.78%, 30-yr conventional 6.71%), May 2026. Illustrative estimates only — not a loan offer, pre-qualification, or guarantee of approval. Does not include closing costs, insurance, taxes, or APR. Your actual rate will vary based on credit, CLTV, lien position, and lender.

How the calculator works (static summary)

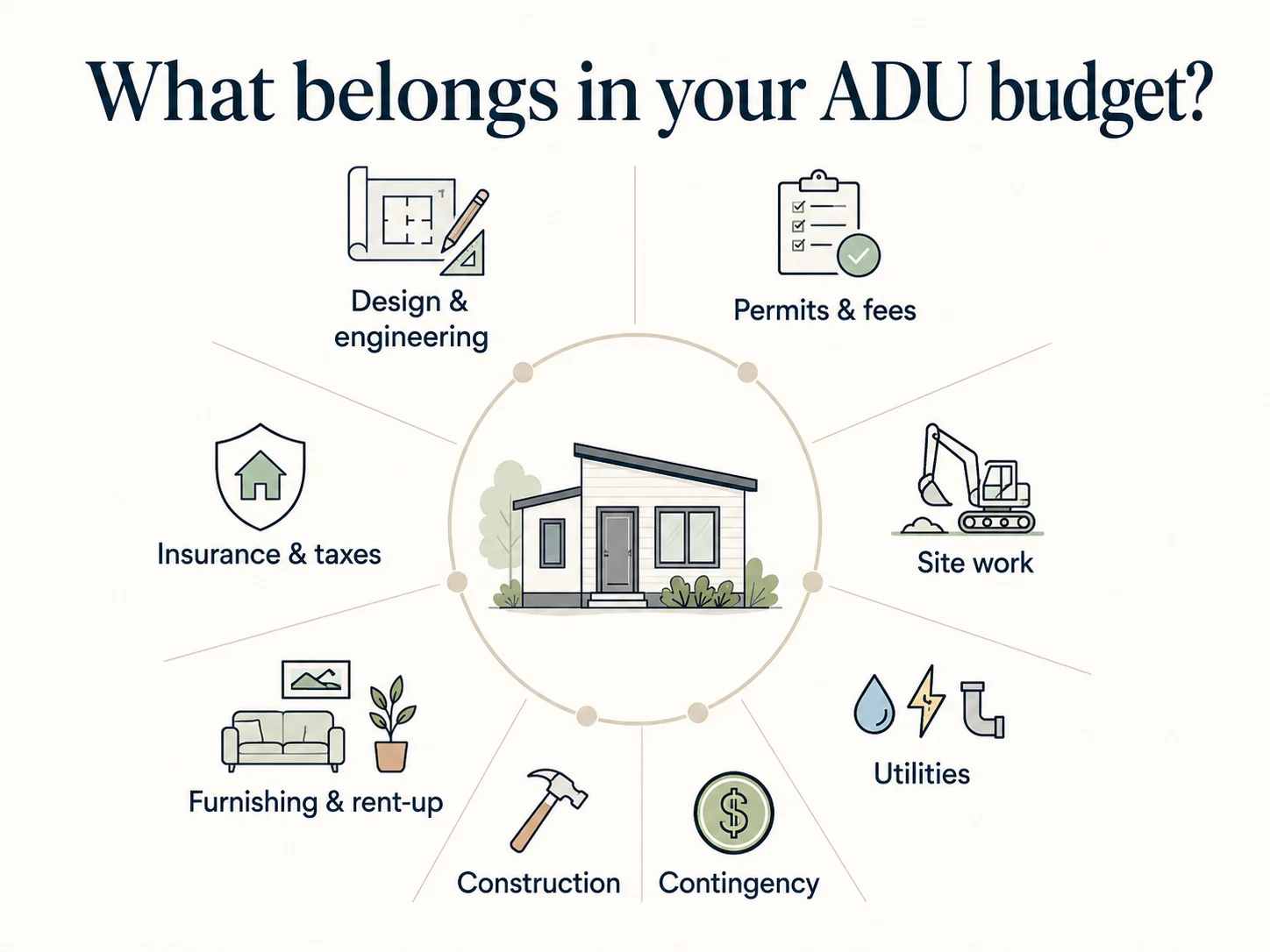

Inputs: Home value, first-mortgage balance, existing mortgage rate, total ADU project cost (all-in: design, permits, construction, contingency), other liens, and optional estimated as-completed home value (for construction and renovation loan paths).

Outputs: For each of the seven paths — loan amount, estimated monthly payment, and estimated total interest over the loan term. HELOC outputs both draw-period (interest-only) and repayment-period (P&I) payments. Construction-to-perm outputs both construction-phase and permanent-phase payments separately. FHA 203(k) payment excludes MIP (add separately).

Formulas: Standard PMT amortization for all fixed-payment paths. HELOC modeled as interest-only on the outstanding balance during a 10-year draw period (rate = WSJ prime + lender margin, benchmark 7.21%), then fully amortized over a 20-year repayment period. Construction-to-perm modeled as 12 months of interest-only at 7.50% on the full loan amount, then amortized at 6.78% over 30 years. Renovation loans and cash-out refis modeled as fully amortized 30-year products. All rates are May 2026 national benchmarks from Curinos and Bankrate.

Before you borrow against your home, confirm the build is actually legal on your lot. Zoning, setbacks, lot coverage, and owner-occupancy rules all affect whether an ADU is even permitted — and lenders won't fund a project that can't get a permit.

See What You Can Build → Get Your Free ADU ReportHow does the ADU financing calculator work?

The calculator takes three required inputs — your current home value, your first-mortgage balance, and your total ADU project cost — and runs them through the standard math for all seven financing paths simultaneously. It returns an estimated monthly payment and total interest for each path, flags which paths your equity covers today, and identifies which paths require as-completed (future-value) underwriting.

The three inputs that drive everything

| Input | Why it matters | Where to get it |

|---|---|---|

| Home value | Sets borrowing capacity for all current-equity paths (HELOC, HEQL, cash-out refi) | Recent appraisal or Zillow/Redfin estimate (use conservatively) |

| First-mortgage balance | Reduces available equity; increases new loan size for first-lien paths | Mortgage statement (most recent) |

| Total ADU project cost | Sets the loan amount needed; determines whether current equity is sufficient | Contractor bids + 10% contingency + design + permits |

The HELOC draw vs. repayment payment — a common surprise

A HELOC has two phases. During the 10-year draw period, you pay interest only on what you've drawn. At the end of year 10, the draw period closes and the remaining balance fully amortizes over 20 years — creating a higher monthly payment that surprises many homeowners.

Illustrative example. A $200,000 HELOC at 7.25% variable during the draw period costs roughly $1,208/month in interest-only payments while you build. After the draw period closes, the same balance amortized over 20 years runs approximately $1,580/month. Illustrative only — not a loan offer.

How construction-to-perm underwriting works

The construction-to-perm path lets you borrow against your home's projected as-completed value — the value after the ADU is built — rather than its current value. This is the only way to borrow against equity that doesn't exist yet. A homeowner with $500,000 current value and a $475,000 mortgage has effectively zero usable current equity. But if the same home with a completed ADU appraises at $625,000, a construction-to-perm lender can model borrowing against that $625,000 figure.

Which ADU financing path fits your numbers?

The fit matrix below distills the key eligibility and trade-off logic for all seven paths. Use it alongside the calculator above to identify your lane before you talk to a lender.

| Path | Best fit | Bad fit | Benchmark rate (May 2026) | Preserves first mortgage? | Underwrites on future value? |

|---|---|---|---|---|---|

| HELOC | Strong equity, want flexibility to draw as invoices come in | <20% equity, variable-rate risk averse | 7.21% variable | Yes ✓ | No |

| Home equity loan | Defined budget, want fixed payment, rate certainty | Phased build, expect to pay off and re-borrow | 7.36% fixed | Yes ✓ | No |

| Cash-out refi | Existing rate at or above ~6.75%; want one payment | Locked low rate (below 5.5%); replaces entire mortgage | 6.78% fixed (30 yr) | No ✗ | No |

| Construction-to-perm | Low current equity; strong income; plans and permits ready | Want simplicity; owner-builder; no GC | ~7.50% construction / 6.78% perm | No ✗ | Yes ✓ |

| HomeStyle Renovation | Purchase or refi + ADU in one loan; detached or modular ADU | Have a low first-mortgage rate you'd lose | 6.78% (30 yr benchmark) | No ✗ | Yes ✓ |

| CHOICERenovation | Purchase or refi + ADU; Freddie Mac product preferred | Depending on ADU rent to qualify (see May 2026 restriction) | 6.78% (30 yr benchmark) | No ✗ | Yes ✓ |

| FHA Standard 203(k) | FHA borrower; conversion or addition scope; FICO 580+ with 3.5% down | New standalone detached ADU from the ground up | ~7.20% fixed (excl. MIP) | No ✗ | Yes ✓ |

The five-question fork

If the matrix isn't resolving your situation, run through these five questions in order:

- Does (home value × 80%) − mortgage balance − other liens ≥ ADU budget? If yes, start with HELOC or home equity loan. If no, skip to question 2.

- Is your existing first-mortgage rate below 5.5%? If yes, avoid cash-out refi. If your rate is at or above current market, cash-out refi becomes viable.

- Do you have approved plans and a licensed GC? If yes, construction-to-perm becomes viable. If no, renovation loans (HomeStyle, 203(k)) may work for conversion or addition scope.

- Is your credit score 580+? If yes, FHA 203(k) is on the table (with 3.5% down at 580+, or 10% down at 500+). If no, conventional renovation loans require 620+ in most cases.

- Is the ADU scope primarily a conversion or addition? FHA 203(k) and HomeStyle both work well here. For brand-new standalone detached ADUs, construction-to-perm is typically the right first-lien path.

If the calculator points you toward a construction loan, renovation loan, or cash-out refi, Mortgage Research Center connects homeowners with lenders that handle these products. We don't rank lenders by compensation and we don't promise approval — but the right product comparison is a 15-minute conversation, not a leap of faith.

Compare options →via Mortgage Research Center — affiliate disclosure applies.

The whole financing question only matters if you can actually build the ADU. Zoning, setbacks, lot coverage, and state law all affect whether your property is eligible.

See What You Can Build → Get Your Free ADU ReportHow much ADU financing can you actually access?

Current-equity formula

| Your situation (home value · mortgage) | Usable equity at 80% CLTV | Covers $200K ADU? |

|---|---|---|

| $900K value · $400K mortgage | $320,000 | Yes ✓ |

| $750K value · $550K mortgage | $50,000 | No ✗ |

| $600K value · $450K mortgage | $30,000 | No ✗ |

| $1.2M value · $500K mortgage | $460,000 | Yes ✓ |

Formula: (home value × 0.80) − first-mortgage balance − other liens. Illustrative examples only.

Future-value underwriting — what it unlocks

Construction-to-permanent loans and renovation loans (HomeStyle, CHOICERenovation, FHA 203(k)) can underwrite against your home's as-completed value — what it will appraise for after the ADU is built. The FHFA has documented that properties with ADUs in California command a meaningful premium over comparable non-ADU properties. That premium becomes your borrowing room.

The trade-off: these paths are more complex. They require approved plans, a licensed insured GC (on most products), a detailed draw or renovation schedule, and lender-ordered inspections at each milestone. The loan origination timeline is typically 60–90 days from application to closing, versus 30–45 days for a HELOC or home equity loan.

The loss-of-low-rate problem: when cash-out refi destroys value

A cash-out refinance replaces your entire first mortgage at today's rate. For homeowners who locked a 3.0–4.5% rate in 2020–2022, this is almost always the wrong move. Here's the illustrative dollar cost over 30 years for a homeowner with a $400,000 mortgage and a $200,000 ADU project:

| Existing first-mortgage rate | HELOC total interest ($200K) | Cash-out refi total interest ($600K at 6.78%) | Extra cost of refi path |

|---|---|---|---|

| 3.25% | ~$171,000 (HELOC) + ~$117,000 (existing) | ~$811,000 | ~$523,000 more |

| 5.00% | ~$171,000 (HELOC) + ~$186,000 (existing) | ~$811,000 | ~$454,000 more |

| 7.00% | ~$171,000 (HELOC) + ~$268,000 (existing) | ~$811,000 | ~$372,000 more |

| 6.75%+ (near market) | ~$171,000 + ~$255,000 | ~$811,000 | ~$385,000 more |

Illustrative estimates using standard amortization at benchmark rates. Does not include closing costs. HELOC existing-mortgage interest uses the original rate on a declining balance. The CFPB has flagged that cash-out refinancing converts home equity into mortgage debt and can increase foreclosure risk.

When is the calculator wrong?

The calculator is a planning tool, not a lender decision. It will over-estimate your borrowing power if:

- Your credit score triggers a lender overlay that tightens the CLTV limit (some lenders cap at 75% CLTV for scores below 700)

- Your DTI is above the qualifying threshold — typically 43–50% depending on the product and loan level

- Your as-completed appraisal comes in below your projected budget

- Local zoning doesn't allow the ADU type you're planning, making the project un-permittable

- The lender applies a property-type overlay (some lenders add restrictions for manufactured ADUs)

If you don't know yet whether your lot is buildable, that's the question to answer before you talk to a lender.

If you don't know yet whether your lot is buildable, that's the question to answer before you talk to a lender. Zoning rejections waste time and application fees on both sides.

See What You Can Build → Get Your Free ADU ReportWhat should you do after your ADU financing calculator result?

Use the calculator result to choose your next verification step, not to declare the project approved. The result should send you to one of three next moves: confirm feasibility if the lot is in question, run the specific-product comparison if you have a clear lane, or rework the project scope if no path covers the budget.

Result-to-next-step routing

| Calculator result | Your next action | Relevant guide |

|---|---|---|

| Strong HELOC fit | Compare HELOC terms, draw-period risk, lender-margin range | HELOC for ADU |

| Strong home equity loan fit | Compare fixed-rate home equity loan terms | Home Equity Loan for ADU |

| Cash-out refi looks right | Test the whole-mortgage payment impact in detail | Cash-Out Refinance for ADU |

| Low current equity, strong income | Review no-equity paths and future-value structures | How to Finance an ADU With No Equity |

| Construction draws needed | Review construction-loan structure and contractor requirements | ADU Construction Loan |

| One-close construction-to-perm preferred | Review C-to-perm structure and lender process | Construction-to-Permanent Loan for ADU |

| Renovation loan path | Compare HomeStyle, CHOICERenovation, FHA 203(k) | ADU Financing Options 2026 |

| FHA borrower | Review FHA 203(k) ADU rules | FHA 203(k) Loan for ADU |

| Unsure if ADU is legal | Run feasibility check before anything else | Feasibility Engine |

Twelve questions to ask every ADU lender

Once the calculator has narrowed your lane, the next conversation is with a loan officer. Ask these:

- What's your ADU loan volume in the last 12 months?

- Is this loan based on current value or as-completed value?

- Can ADU rental income count toward my qualifying income — and if so, what's the cap, what documentation is required, and does it apply to my specific transaction type?

- What's the draw schedule for construction (if applicable)?

- Who orders the appraisal, and how long does it typically take?

- What happens if the appraisal comes in below the budget?

- Are there prepayment penalties?

- What are all the closing costs, itemized?

- Will the rate change between application and closing? If so, what's the lock policy?

- Do you finance modular and manufactured ADUs the same way?

- What contractor qualifications do you require, and will you finance owner-builder projects?

- What's the earliest date you can close?

If a loan officer can't answer most of these without checking with someone else, find a different lender. ADU financing is specialized enough that experience matters — the wrong loan officer can cost you weeks and tens of thousands of dollars.

Document checklist by financing path

| Document | HELOC / HEQL | Cash-out refi | Construction loan | HomeStyle / 203(k) |

|---|---|---|---|---|

| Pay stubs / W-2s / tax returns | ✓ | ✓ | ✓ | ✓ |

| Bank statements | ✓ | ✓ | ✓ | ✓ |

| Current mortgage statement | ✓ | ✓ | ✓ | ✓ |

| Property insurance declaration | ✓ | ✓ | ✓ | ✓ |

| Approved ADU plans | Often optional | Often optional | ✓ | ✓ |

| Permit status or eligibility | Often optional | Often optional | ✓ | ✓ |

| Two contractor bids | Recommended | Recommended | ✓ | ✓ |

| Signed lease or Form 1007/1025 (rental income) | If applicable | If applicable | If applicable | If applicable |

Get our full cost-category worksheet, the loan-officer interview script, the document checklist by financing path, and the state-level program directory — packaged as one PDF you can take to your contractor and your lender.

Download the Free 2026 ADU Starter Kit →The seven realistic ADU financing paths, in detail

The fit matrix above gave you the at-a-glance comparison. Here's the editorial on each path — when it wins, when it loses, and the 2026 rule changes that matter.

Path 1 — HELOC for an ADU

A home equity line of credit is a revolving credit line secured by your home's available equity. Lenders typically allow combined loan-to-value up to 80–85% of current appraised value, minus your existing first-mortgage balance. As of May 17, 2026, the Curinos national average HELOC rate is 7.21%, near the 2026 low of 7.19% first observed in mid-March. The FTC describes HELOCs as revolving credit secured by your home — meaning if you fail to repay, the lender can foreclose (consumer.ftc.gov).

- Best fit

- Meaningful equity; draw funds as invoices arrive; preserve favorable rate on existing mortgage.

- Bad fit

- Bought recently with <20% equity; uncomfortable with variable-rate risk; can't tolerate payment rising if prime moves.

How it works: Two phases — a 10-year draw period (interest-only on what you've drawn) followed by a 20-year repayment period (fully amortized P&I). Variable-rate HELOCs are indexed to WSJ prime rate (6.75% as of May 20, 2026) plus a lender margin, typically 0.50–2.00%.

Biggest upside: Flexibility. You only pay interest on what you've drawn. Your first mortgage stays untouched.

Biggest downside: Rate risk. If prime rises during your draw period, your payment rises. And the payment step-up at month 121 — when the draw closes and amortization begins — surprises homeowners who didn't model both phases.

The detail most guides miss: Credit unions and regional banks often beat the big banks on HELOC pricing. As of mid-May 2026, some credit unions were advertising introductory APRs around 5.99% for the first 12 months on lines up to $500,000. Always run the math past the intro period.

Path 2 — Home equity loan for an ADU

A home equity loan gives you a fixed lump sum at a fixed rate, repaid over a set term. It sits as a second lien on top of your first mortgage. As of May 17, 2026, the Curinos national average home equity loan rate is 7.36%.

- Best fit

- Defined ADU budget; want rate certainty; want one predictable monthly payment.

- Bad fit

- Phased build where costs hit over months; anticipate paying off chunks and re-borrowing.

The detail most guides miss: Home equity loans and HELOCs can be stacked. Some homeowners use a small HELOC for early soft costs (design, plans, permits — where flexibility helps) and a larger home equity loan for the locked-in construction draw. Interest accrues on the entire lump sum from day one — even if you don't need all the funds until month 8.

Path 3 — Cash-out refinance for an ADU

A cash-out refinance replaces your entire existing first mortgage with a larger one, and you take the difference as cash. Freddie Mac's max-LTV table caps cash-out refis at 80% LTV for one-unit primary residences. This path can work when your existing rate is at or above current market — but it rarely wins for anyone who locked a sub-5% rate in the 2020–2022 window.

- Best fit

- Existing rate similar to or higher than today's rates; owe relatively little; want to consolidate into one payment.

- Bad fit

- Low first-mortgage rate. The CFPB has flagged that cash-out refinancing converts home equity into mortgage debt and can increase foreclosure risk.

Path 4 — Construction loan / construction-to-permanent loan for an ADU

A construction loan funds the ADU in staged draws as your contractor hits milestones, with lender-ordered inspections verifying progress before each draw. A construction-to-permanent loan converts automatically into a permanent mortgage at completion; a construction-only loan requires a separate refi at completion. Both can underwrite against your home's projected as-completed value — the only way to borrow against equity that doesn't exist yet.

- Best fit

- Low current equity; strong income; approved plans; contractor bids; permitted or permit-eligible project.

- Bad fit

- Want simplicity; owner-builder; no licensed GC. More complex than any other path — higher closing costs, longer timeline (60–90 days).

How ADU construction draws actually work

Construction loans release funds in stages as your contractor hits documented milestones. A typical detached ADU build has four to six draws: foundation, framing, rough-in (plumbing, electrical, HVAC), drywall and finishes, and final inspection. A lender-appointed inspector verifies progress before each draw is released.

- Pre-funded draws. The lender releases funds at the start of each phase; the contractor uses those funds during the phase.

- Reimbursement draws. The contractor pays vendors and labor out of pocket, then submits invoices for reimbursement after the inspector signs off.

- Hybrid. Pre-funding for materials (with proof of order); reimbursement for labor. Ask your lender exactly which model applies.

The detail most guides miss: In California, AB 1332 requires qualifying detached ADU applications using a preapproved plan to be approved or denied within 30 days. Start the lender conversation before you submit for permit — the lender's approved plan set may differ from the city's, and you'll need both.

Construction and renovation loans are specialized — not every lender does them well. Mortgage Research Center connects homeowners with lenders who actively underwrite construction and renovation loans.

Compare options →via Mortgage Research Center — affiliate disclosure applies.

Path 5 — Fannie Mae HomeStyle Renovation

HomeStyle is a conventional renovation loan that combines purchase or refinance with renovation funding in a single mortgage, underwriting against the property's projected after-completion value. Per Fannie Mae's Selling Guide, eligible ADU types include detached, attached, modular, and HUD-code manufactured ADUs (with permanent foundation and real-property classification).

Fannie Mae Selling Guide Announcement SEL-2025-10 (December 10, 2025) expanded UAD 3.6-policy eligibility for one-unit properties with up to three ADUs. Effective March 31, 2026, only available to lenders using UAD 3.6 policy. Rental-income qualification is still capped at one ADU's rent per property.

- Best fit

- Buying or refinancing and adding an ADU in one transaction; detached, modular, or HUD-code manufactured ADU.

- Bad fit

- You have a low first-mortgage rate you'd lose by refinancing. Key rule: renovation must be completed within 15 months of closing per Fannie Mae Selling Guide B5-3.2-01.

Path 6 — Freddie Mac CHOICERenovation

CHOICERenovation is Freddie Mac's renovation product, similar in structure to HomeStyle. It can finance ADU renovation or addition through an as-completed appraisal framework on eligible properties.

- Best fit

- Purchase or refinance plus ADU renovation when the lender or borrower prefers a Freddie product.

- Critical 2026 limitation

- Effective May 4, 2026 (Freddie Mac Bulletin 2026-1 / Guide §4607.5): rental income from any unit included in the renovation project cannot be used to qualify the borrower. Confirm this restriction with your lender before choosing this lane if ADU rent is part of your qualification strategy.

Path 7 — FHA Standard 203(k)

The Standard 203(k) is a government-backed renovation loan that allows ADU work — including conversions, additions, and renovations of existing ADUs — under HUD Mortgagee Letter 2023-17. Eligible improvements include converting a one-family structure to one-family-with-ADU, adding an ADU attached to an existing structure, and renovating an existing attached or unattached ADU.

- Best fit

- FHA borrower (FICO 580+ with 3.5% down, or 500+ with 10% down); buying a property and adding or renovating an ADU; conversion-heavy scope.

- Bad fit

- Building a brand-new standalone detached ADU from the ground up — program scope is oriented toward conversions and additions.

- Upfront MIP: 1.75% of loan amount

- Monthly MIP for the life of the loan in most cases

- ADU rental income capped at 30% of total monthly effective income

- 75% of the lesser of fair market rent or lease amount on existing ADUs

- 50% of the lesser on prospective ADUs (no rental history) under Standard 203(k)

- ADU rental income is not allowed on FHA cash-out refinance transactions

- Two months of PITI in reserves after closing required when using ADU rental income

Bonus: home equity investments (HEIs) and HECMs

Both HEIs and HECMs can avoid required monthly payments — but neither is free money. The CFPB has flagged home equity contracts (HEIs) as a complex, evolving category that consumers should evaluate carefully against traditional debt products. HECM reverse-mortgage borrowers must continue paying property taxes, homeowners insurance, and HOA fees; failure to meet those obligations can lead to default and foreclosure even though no monthly mortgage payment is required. We cover both more fully in our ADU Financing Options 2026 guide.

Local programs and grants

The California CalHFA ADU Grant is fully allocated and has been since December 28, 2023 (calhfa.ca.gov/adu/) — and CalHFA's own program page warns that any website or person offering to "help you access" the grant is operating a scam. Beyond CalHFA, real programs still exist in select cities and states:

- MassHousing's ADU Loan (Massachusetts)

- Boston Home Center's ADU Assistance

- SDHC's ADU Finance Program (San Diego)

- New York City's Plus One ADU

- Colorado CHFA's ADU programs

- Portland's SDC Waiver

- Salt Lake City's Backyard Keys

- Orlando's ADU Incentive Program and Charlotte's Queen City ADU Program

Each carries eligibility constraints, income limits, or rent restrictions. Our ADU Financing Options 2026 guide has the verified, per-program directory with current status and official source links, refreshed monthly.

ADU rental income: program-by-program comparison

| Product | Existing ADU rent allowed? | Prospective ADU rent allowed? | Cap | Key restriction |

|---|---|---|---|---|

| Fannie Mae (DU 12.1) | Yes — 75% of gross rent | Limited (purchase/LCOR only) | 30% of qualifying income | PITIA cap if no 12-month landlord experience |

| Freddie Mac | Yes (parallel to Fannie) | Not on CHOICERenovation (5/4/26) | Per Freddie guidelines | CHOICERenovation: rental income from renovated unit excluded |

| FHA 203(k) | Yes — 75% of FMR or lease | Yes — 50% of FMR or lease | 30% of effective monthly income | Not on FHA cash-out refi; 2 months PITI reserves required |

| HELOC / HEQL | Lender-specific | Rarely | No standard rule | Income must be established; most require 12–24 months documentation |

If you're underwriting on projected rent, you'll need an organized system for leases, rent ledgers, tenant communications, expense tracking, and maintenance records — the kinds of documents lenders ask for over time. Buildium handles tenant screening, online rent collection, maintenance ticketing, lease storage, and financial reporting that maps to standard ADU rental documentation.

See how Buildium handles ADU rentals →via Buildium — affiliate disclosure applies.

A note on tax treatment

We are not a tax advisor, and the IRS rules on home-equity interest deductibility are narrower than most homeowners realize. IRS Publication 936 (current edition) explains that interest on home-equity debt is generally deductible only when the loan proceeds are used to buy, build, or substantially improve the home that secures the loan, subject to the overall acquisition-debt cap (irs.gov/publications/p936).

Using a HELOC or home equity loan to fund an ADU build on the home that secures the loan typically qualifies as "buy, build, or substantially improve" — but the determination depends on your specific facts. Confirm with a tax professional before relying on the deduction in your cash-flow modeling. The Tax Cuts and Jobs Act capped total qualifying acquisition debt; check current limits each year.

How we built and verified this calculator

We are an independent research resource covering ADU financing, costs, and regulations. We do not originate loans, act as a broker, or sort financing paths by compensation.

- Source hierarchy. Primary agency documents (Fannie Mae Selling Guide, Freddie Mac Single-Family Seller/Servicer Guide and Bulletins, HUD Mortgagee Letters) for regulatory facts. Consumer-protection authorities (CFPB, FTC, IRS) for risk and tax disclosure. Verified program pages from administering agencies for grant and program status. Rate benchmarks from Curinos, Bankrate, and Mortgage News Daily with publication dates.

- Calculator math. Standard amortization formulas. HELOC modeled as interest-only on draws during a 10-year draw period, then fully amortized over a 20-year repayment period at the lender margin plus prime. Construction-to-perm modeled as interest-only during a 12-month construction phase plus amortized permanent phase. Renovation loans and cash-out refis modeled as fully amortized 30-year products. FHA 203(k) base payment shown excluding MIP.

- Evaluation criteria for each path. Property fit, geographic availability, current-value versus future-value treatment, ability to preserve an existing first mortgage, rental-income treatment under each agency, draw structure, contractor and owner-builder constraints, and program eligibility.

- What we never do. Rank lenders by compensation. Quote specific rates or APRs as guarantees. Promote any single lender as "best." Publish schema for content that isn't visible on the page. Use fake reviews, fake testimonials, or fabricated author credentials.

- Verification cadence. Agency rules: quarterly, plus on every Fannie Mae / Freddie Mac / HUD bulletin. Rate benchmarks: monthly, plus after any Federal Reserve action. Local program status: monthly. Affiliate partner status: monthly.

See our methodology, editorial standards, and affiliate disclosure.

ADU financing calculator FAQ

How do you calculate financing for an ADU?

Add up your total all-in ADU cost (design, permits, construction, utility upgrades, site work, 10% contingency). Compare that to your usable current equity, which is (home value × 0.80) − existing first-mortgage balance − other liens. If your equity covers the project, model a HELOC and a home equity loan first. If it doesn't, model a construction-to-permanent or renovation loan that underwrites against the home's as-completed value. The calculator above runs all seven paths in parallel.

How much does it cost monthly to finance an ADU?

For a $180,000 ADU at May 2026 benchmark rates, estimated monthly payments range from roughly $1,082 (HELOC interest-only during construction) to $3,931 (cash-out refinance that replaces a low existing first mortgage). Your actual payment depends on which path fits and on your specific credit, equity, and rate. Use the calculator above for your numbers.

Can I use a HELOC to build an ADU?

Yes — it's one of the most common ADU financing paths for homeowners with sufficient equity. A HELOC's flexibility (draw funds as construction invoices come due, pay interest only on what's drawn) matches the cash-flow pattern of a construction project well. The trade-offs are variable-rate risk during the draw period and the fact that your home secures the loan; failure to repay can lead to foreclosure (FTC).

Is a home equity loan better than a HELOC for an ADU?

A home equity loan fits better when the ADU budget is locked and you want a fixed monthly payment. A HELOC fits better when your spending will hit in stages and you want to pay interest only on what you've drawn. Both are secured by the home.

Should I use a HELOC or a cash-out refinance for an ADU?

Almost always a HELOC if your current first-mortgage rate is below ~5.5%. A cash-out refi replaces your entire first mortgage at today's higher rate — and the total-interest cost over 30 years usually exceeds the ADU project cost itself. The Loss-of-Low-Rate matrix above and the calculator's total-interest output show the dollar difference for your specific situation.

Is a cash-out refinance a good idea for an ADU?

It depends entirely on your existing first-mortgage rate. If your existing rate is at or above current market (roughly 6.75–7.00% or higher), a cash-out refi can consolidate everything into one payment at a similar rate. If your existing rate is below 5.5%, a cash-out refi is almost always the wrong move.

How much equity do I need to build an ADU?

For current-value products (HELOC, home equity loan, cash-out refi), the rough formula is (home value × 0.80) − existing first-mortgage balance − other liens. If that covers your ADU budget plus a 10% contingency, you have enough current equity. If not, future-value products (construction loans, renovation loans like Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, or FHA 203(k)) can underwrite against your home's as-completed value, often unlocking significantly more borrowing power.

Can future ADU rental income help me qualify?

Sometimes. Fannie Mae's Desktop Underwriter 12.1 (effective the weekend of March 21, 2026) automates the rule for an existing ADU on a one-unit principal residence — 75% of gross monthly rent, capped at 30% of total qualifying income, on purchase or limited cash-out refi transactions only. Freddie Mac has parallel rules with the May-4-2026 CHOICERenovation restriction (Bulletin 2026-1). FHA permits 75% of the lesser of fair market rent or lease amount on existing ADUs and 50% on prospective ADUs under Standard 203(k); FHA does not allow ADU rental income on cash-out refinances (HUD ML 2023-17).

What's the interest rate on an ADU loan?

There's no single 'ADU loan rate' because there's no single ADU loan. As of May 21, 2026: HELOC ~7.21%, home equity loan ~7.36%, 30-year cash-out refi ~6.78% APR, 30-year conventional refi ~6.71% (sources: Curinos, Bankrate). Construction-to-perm and renovation loans typically run 0.25–1.00% higher than rate-and-term refi. Your specific rate will move based on credit, CLTV, lien position, property type, and state.

Can I use FHA 203(k) for an ADU?

Yes, with important scope considerations. HUD Mortgagee Letter 2023-17 (effective October 16, 2023) made ADU work eligible under Standard 203(k): converting a one-family structure to one-family-with-ADU, adding an ADU attached to an existing structure, and renovating an existing attached or unattached ADU. The program is best for conversion-heavy work, not standalone detached new-build.

Does the calculator quote real lender rates?

No. We use national benchmark rates from Curinos, Bankrate, and Mortgage News Daily — dated and cited. Your actual lender quote will vary based on credit, CLTV, lien position, property type, and state. The calculator is a planning model, not a loan offer.

Does the calculator include closing costs?

No — closing costs vary too widely by lender, state, and product to model in a planning tool. Budget 2–6% of loan amount for closing costs on cash-out refis and renovation loans. HELOCs and home equity loans typically have lower closing costs (often $500–$2,000 or waived by some lenders).

Does the calculator include taxes?

No. Property taxes increase when the ADU is assessed; your actual increase depends on your county assessor's methodology, applicable assessment caps (like California's Proposition 13), and the assessed value the assessor assigns. Plan for an increase, but get a specific number from your county assessor before finalizing your cash-flow model.

Does the calculator guarantee approval?

No. It's an educational screening tool, not a loan offer, pre-qualification, appraisal, or tax opinion. Lender overlays, underwriter judgment, appraisal results, and documentation all affect the actual outcome.

How current is the rate data?

The benchmark rates we display are verified monthly and after any Federal Reserve action. Last verified May 21, 2026.

What does the December 2025 Fannie Mae ADU expansion mean for me?

Fannie Mae Selling Guide Announcement SEL-2025-10 (December 10, 2025) expanded UAD 3.6-policy ADU eligibility to one-unit properties with up to three ADUs, and to two-to-three-unit properties with ADUs provided the total primary dwelling units plus ADUs does not exceed four. Changes are effective March 31, 2026 and only available to lenders using UAD 3.6 policy. Practically: if your project envisions multiple ADUs on a single-family lot (where local zoning allows it under California SB 1211 or similar state law), the conventional Fannie Mae path is now viable. Rental-income qualification is still limited to one ADU's rent per property.

Will building an ADU affect my property taxes, homeowners insurance, or escrow?

In most cases, yes. Property taxes typically increase as the ADU's value is added to your assessed value (subject to state-specific assessment caps). Homeowners insurance premiums usually rise; you may need a landlord rider or umbrella if you rent the ADU. Escrow accounts will recalibrate upward. Confirm with your county assessor, your insurer, and your lender before finalizing financial projections.

What if the appraisal comes in below my ADU budget?

Your borrowing power drops. Options: bring more cash to close, reduce project scope, provide additional comparable data to support a revised appraisal, or apply with a different lender. Building a 5–10% contingency into your project budget up front protects against this risk.

Does an owner-builder approach make ADU financing harder?

Yes, significantly. Most construction loans and renovation loans require a licensed, insured general contractor. If you plan to act as your own GC, start the lender conversation early — options are more limited and terms are stricter.

Sources cited in this guide

- Fannie Mae Selling Guide B3-3.8-01: Rental Income — selling-guide.fanniemae.com/sel/b3-3.8-01/rental-income

- Fannie Mae Selling Guide B2-3-04: Special Property Eligibility Considerations

- Fannie Mae Selling Guide B5-3.2-01: HomeStyle Renovation Mortgages

- Fannie Mae Announcement SEL-2025-08 (October 2025)

- Fannie Mae Announcement SEL-2025-10 (December 10, 2025) — singlefamily.fanniemae.com/media/44506/display

- Pennymac Correspondent Announcement 26-29 (DU 12.1 effective March 21, 2026)

- Fannie Mae Accessory Dwelling Units product page

- Fannie Mae HomeStyle Renovation product page

- Fannie Mae UAD 3.6 implementation timeline

- Freddie Mac Single-Family ADU page — sf.freddiemac.com/working-with-us/accessory-dwelling-units

- Freddie Mac Bulletin 2026-1 (CHOICERenovation rental-income restriction effective May 4, 2026)

- Freddie Mac Single-Family Seller/Servicer Guide §4607.5

- Freddie Mac maximum LTV/TLTV/HTLTV requirements — sf.freddiemac.com

- HUD Mortgagee Letter 2023-17 (October 16, 2023) — hud.gov

- FTC Consumer Advice — Home Equity Loans and HELOCs — consumer.ftc.gov

- CFPB — Home Equity Contracts Market Overview — consumerfinance.gov

- IRS Publication 936 (current edition) — irs.gov/publications/p936

- California HCD ADU Handbook (March 2026 edition) — hcd.ca.gov

- CalHFA ADU Grant program page — calhfa.ca.gov/adu/

- California AB 1332 (CalMatters Digital Democracy)

- Curinos HELOC/HEL rates via Yahoo Finance (May 17, 2026)

- Bankrate Cash-Out Refinance Rates (May 19, 2026)

- Bankrate 30-Year Refinance Rates (May 19, 2026)

- Mortgage News Daily — current FHA refi rates

- Wall Street Journal Prime Rate (May 20, 2026)

- FHFA — Trends in Median Appraised Value for Properties with ADUs in California

Disclaimer. The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder. This page is educational and does not constitute legal, tax, mortgage, or financial advice. Financing availability, underwriting, rates, fees, and eligibility vary by lender, borrower, property, and location. Always confirm terms with a licensed lender and verify ADU rules with your local planning and building department. Calculator outputs are illustrative estimates only, are not loan offers, do not include all fees or APR, and are not guarantees of qualification or rate.

Rental-income estimates and rent-vs-payment comparisons are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, regulatory approvals, lender overlays, and specific transaction facts.

Get the loan-officer interview script, the document checklist by financing path, and the state-level program directory — all in one PDF.

Download the Free 2026 ADU Starter Kit →Not sure where to start? See what's possible at your address — get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU Report