ADU Financing Guide · Updated May 2026

HELOC for ADU 2026: Real Rates, Eligible Lenders, and the Math That Actually Decides It

By The Dwelling Index Editorial Team · Independent ADU research · Not a lender or broker · · · 30 sources cited

Bottom Line

A HELOC for an ADU is a second-lien revolving credit line you draw against as construction costs arrive. National HELOC rates in mid-May 2026 sit roughly in the 7.20%–7.50% range across major surveys — Bankrate's national average is 7.26% as of May 6, 2026 and Curinos / Yahoo Finance's snapshot is 7.21% as of May 17, 2026. California-only ADU-specific HELOC programs run higher: Patelco Credit Union's ADU HELOC starts at 8.25% APR for the most-qualified applicants at up to 125% CLTV (verified May 18, 2026). A standard HELOC works for you when (1) your current home value × an 80–85% CLTV cap, minus your mortgage balance, covers your ADU budget plus a 15% contingency, (2) you want to keep your first mortgage, and (3) your state actually allows the structure — which Texas restricts significantly under Article XVI § 50(a)(6) of its state constitution. If any one of those three conditions fails, the right tool is usually an after-renovation-value (ARV) HELOC, a renovation loan, or a construction-to-permanent loan instead.

Should You Test a HELOC First? The 30-Second Decision Table

Answer capsule: A standard HELOC is the strongest first path when you have substantial current-value equity, a favorable first mortgage you want to preserve, and an ADU type whose budget fits inside your borrowing room. If your equity is thin, your project is a high-cost detached build, or you live in Texas, a different financing path usually fits better.

| Your situation | First path to test | Why it wins | Biggest watch-out |

|---|---|---|---|

| Substantial current equity + low first mortgage + staged contractor payments | Standard HELOC | Preserves your existing mortgage; you draw and pay interest only as invoices arrive | Variable rate — stress-test your payment at +2% |

| Substantial current equity but you want a fixed monthly payment | Home equity loan (HEL) | Lump sum, fixed rate, predictable payment | No draw flexibility — you pay interest on the full amount from day one |

| Your current first-mortgage rate is no longer competitive | Cash-out refinance | Consolidates into one payment; may improve overall position | You lose your existing mortgage terms |

| Your project only pencils because of post-ADU value (you're equity-short) | ARV HELOC, renovation loan, or construction-to-perm | Underwrites based on completed value, not today's value | Replaces your first mortgage (in renovation/construction-to-perm cases) and requires more documentation |

| Detached new build from scratch | Construction-to-permanent loan or HomeStyle / CHOICERenovation | Designed for ground-up builds with phased draws | Plans, licensed builder, and full underwriting required before approval |

| You can't carry another monthly payment (fixed income, retired) | Home equity investment (HEI) | No monthly payment; settle when you sell or refinance | Equity-share trade-off; state availability is limited — verify your state before relying on it |

| You live in Texas and the ADU sits on your homestead | Standard HELOC capped at 80% CLTV (constitutional max) | Same product, hard ceiling | Section 50(a)(6) constraints — see state rules section below |

Sources: CFPB consumer guidance on HELOCs and home equity loans, verified May 19, 2026; Urban Institute "To Increase the Housing Supply, Focus on ADU Financing," April 2024; Texas Constitution Article XVI § 50(a)(6); Fannie Mae Selling Guide B3-3.8-01; Freddie Mac CHOICERenovation; HUD Mortgagee Letter 2023-17.

Free Tool — Run Your ADU HELOC Fit Calculator

The fastest way to know which row above you're in is to plug your own numbers into our calculator. It returns your usable HELOC room, your project funding gap, your HELOC fit score, and the alternative path most likely to close any gap — without an email gate for the basics.

Open the ADU HELOC Fit Calculator (interactive widget on this page)Can You Use a HELOC to Build an ADU?

Answer capsule: Yes — in most states. A HELOC can fund any phase of an ADU project from design and permits through final finishes, as long as your lender allows new-construction use, your equity covers the budget, and your property and credit qualify. The CFPB defines a HELOC as an open-end credit line secured by home equity, and that structure aligns naturally with phased ADU construction. The Urban Institute reports that 56% of mortgage-financed ADUs use a HELOC or home equity loan as the funding tool — the most common path by a wide margin.

You can use a HELOC to build:

- An interior conversion (basement, attic, or unused first-floor space)

- A garage conversion (existing structure retained, MEP and finishes built out)

- An attached ADU addition to your primary home

- A detached new-build ADU in your backyard (with conditions — see the lender matrix below)

- A prefab or modular ADU delivered and installed on permanent foundation

- A junior ADU (JADU) carved out of the existing main home (typically under 500 sq ft, with a kitchenette)

1. Equity room

Your usable HELOC line has to cover the budget plus contingency.

2. Lender willingness

Most national HELOC lenders allow home improvement. A meaningful minority restrict new-construction draws unless disclosed.

3. State rules

Texas's constitutional 50(a)(6) framework limits HELOCs on homestead property; most other states leave HELOC mechanics to lender policy.

Sources: CFPB "What is a home equity line of credit (HELOC)?", verified May 19, 2026; Urban Institute, "To Increase the Housing Supply, Focus on ADU Financing," April 2024.

How a HELOC for an ADU Actually Works

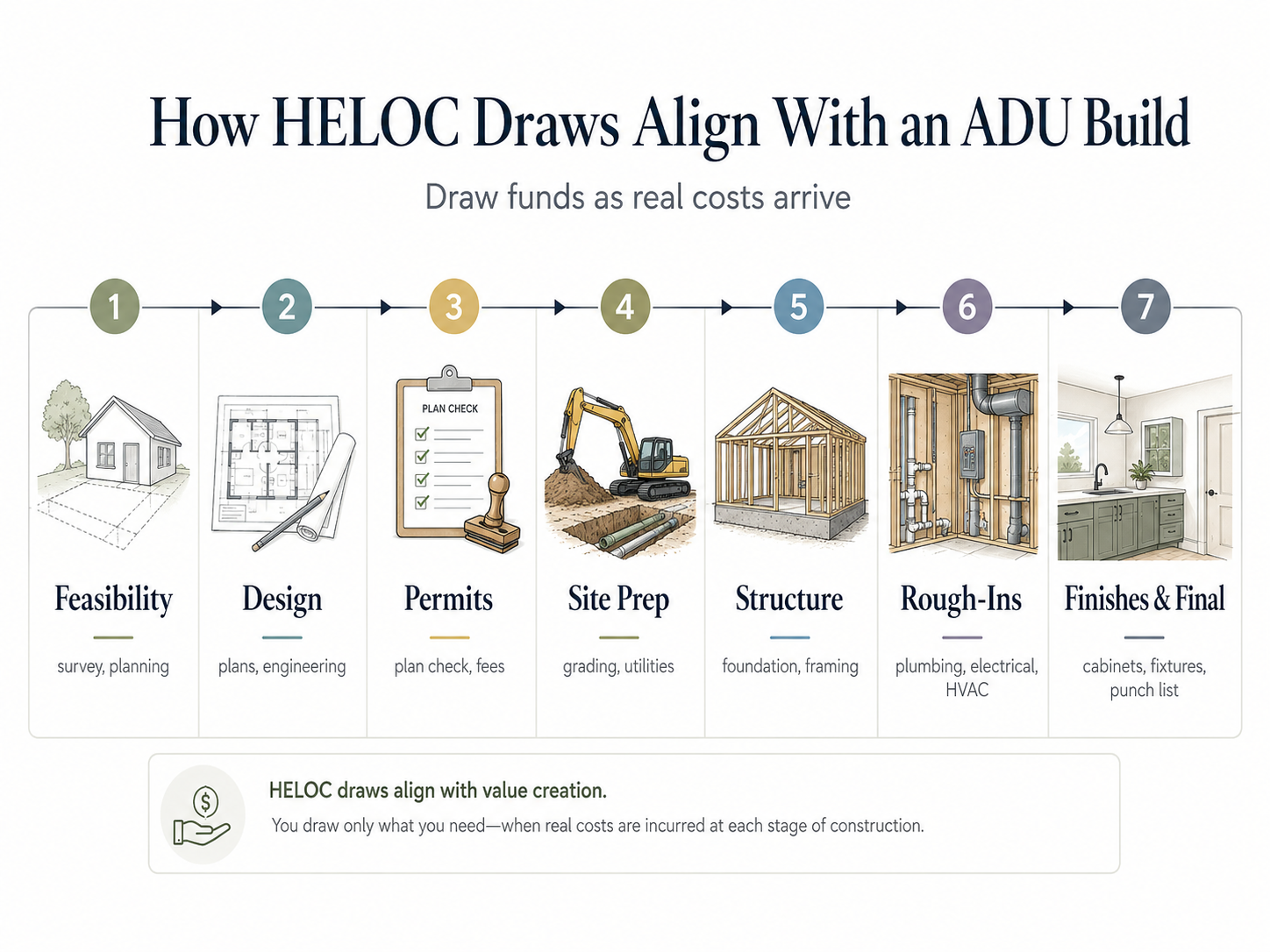

Answer capsule: A HELOC is a revolving second-lien credit line secured by your home's equity. You're approved for a maximum line amount but draw funds as construction costs arrive and pay interest only on the outstanding balance. Most HELOCs have a 5–10 year draw period followed by a 10–20 year repayment period. The rate is typically variable, tied to the Wall Street Journal Prime Rate plus a margin. Your first mortgage stays intact as a separate, untouched loan.

Draw period (typically 5–10 years)

You can borrow, repay, and re-borrow within your approved credit limit. Many lenders allow interest-only payments during this phase, which keeps cash flow light while your ADU is mid-build. Patelco's California ADU HELOC structures a shorter two-year, interest-only draw specifically because most ADU construction wraps inside 24 months.

Repayment period (typically 10–20 years)

The line closes for new draws. Your balance fully amortizes through principal-plus-interest payments — usually a meaningful jump from your interest-only draw payments. We show this in dollars in the cost section below.

HELOC draw phases aligned with ADU construction milestones.

What "variable rate" actually means for an ADU build

Most HELOC rates are quoted as WSJ Prime + a margin. When the Federal Reserve adjusts rates, Prime moves with it, and your HELOC rate moves with Prime. The next FOMC meeting is scheduled for June 16–17, 2026 (federalreserve.gov). Bankrate's senior industry analyst Ted Rossman forecasts the 2026 average HELOC rate around 7.3% on the assumption of three quarter-point Fed cuts this year (Bankrate forecast, January 2026). Don't try to time the Fed — model your build at today's rate plus a buffer.

Most HELOC agreements also include a lifetime cap that prevents the rate from running away. Bay Federal Credit Union's HELOC disclosure caps the rate at 18.00% for the term of the plan, and Foothill Credit Union's published terms set the same 18% ceiling. Stress-test your monthly payment at +2% over today's quoted rate before signing.

Three definitions worth nailing before you read further

- CLTV

- Combined loan-to-value: the sum of your first mortgage balance plus your new HELOC line, divided by your home's appraised value. Most standard HELOCs cap CLTV at 80–85%. ADU-specific products from a small number of California credit unions push it higher.

- Draw

- A specific withdrawal from your approved HELOC line, usually paid by check or bank transfer to your contractor or escrow.

- Subordination

- The agreement that places your HELOC behind your first mortgage in lien priority. If you ever refinance the first mortgage, the HELOC lender has to agree to re-subordinate, or you have to pay the HELOC off as part of the refi.

The CFPB is direct about it: a HELOC uses your home as collateral, and missed payments can lead to foreclosure (consumerfinance.gov, verified May 19, 2026). That's not a reason to avoid the product. It's a reason to make sure the equity math, the payment math, and the timeline math all work before you sign.

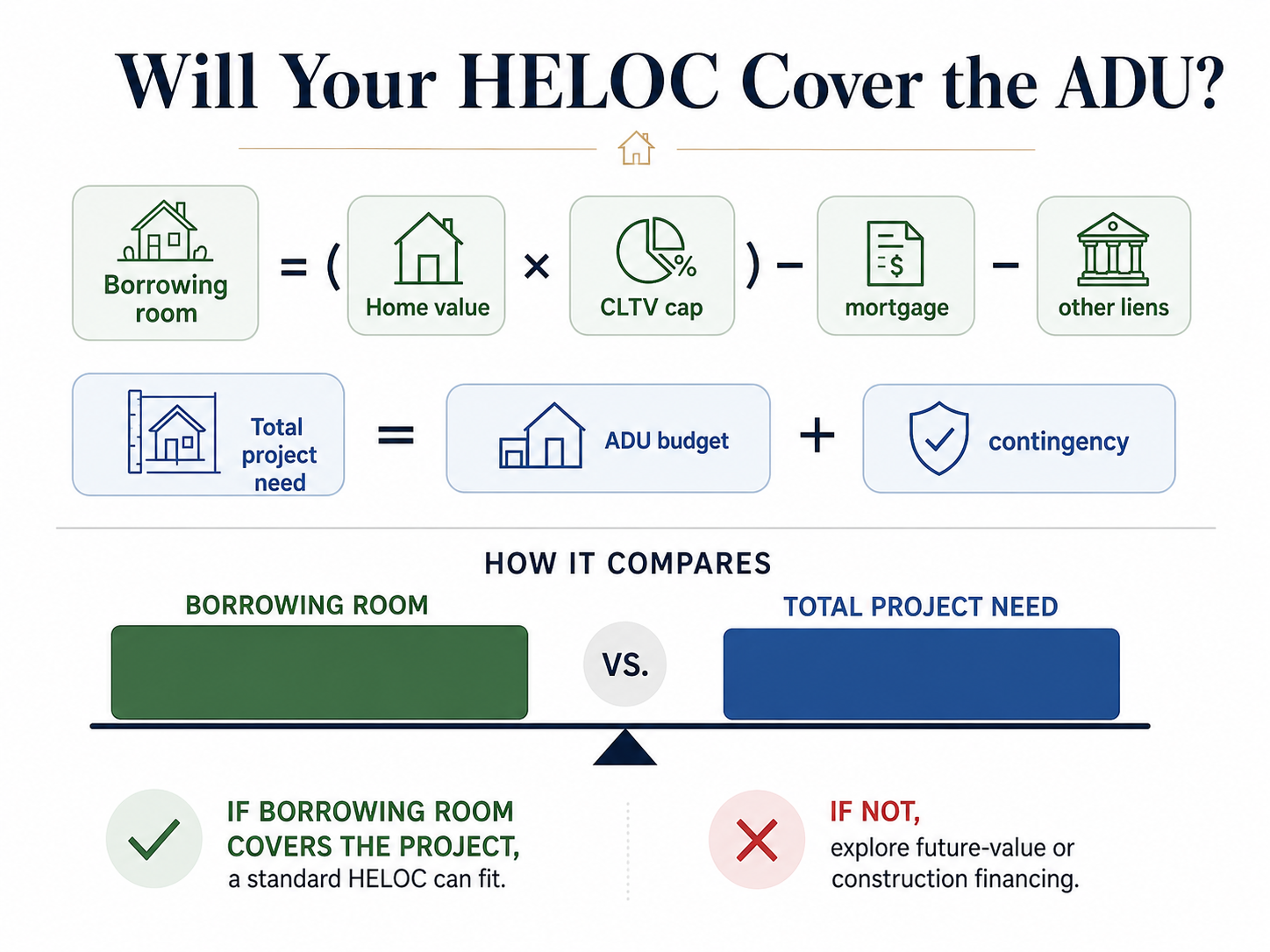

How Much Equity Do You Actually Need?

Answer capsule: You need enough usable equity — measured after the lender's CLTV cap — to cover your full ADU budget plus a contingency reserve, typically 10–15% of construction cost. The basic formula: (Home value × CLTV cap) − current mortgage balance − any other liens = your estimated HELOC room. Compare that result to your contractor's total written estimate, plus contingency. If your HELOC room covers it, you've passed the first test. If not, you need either an ARV product, a renovation loan, or a smaller project.

The 3-Number Formula

Estimated HELOC room = (Home value × Lender CLTV cap) − Current first mortgage balance − Any other secured liens on the home

A worked example

| Input | Amount |

|---|---|

| Estimated current home value | $850,000 |

| Lender CLTV cap (representative) | 80% |

| Maximum combined debt allowed | $680,000 |

| Current first mortgage balance | $500,000 |

| Other liens | $0 |

| Estimated HELOC room | $180,000 |

That $180,000 is the number to compare to your contractor's total estimate plus contingency. Not your contractor's "construction-only" quote. The total that includes design, engineering, plan check, permits, impact fees, utility hookups, site work, and your buffer.

Why "equity" is not the same as "usable HELOC room"

Many homeowners calculate equity as (home value − mortgage balance) and stop there. That's your market equity, not your borrowing room. Market equity ignores three things lenders care about: the CLTV ceiling, your debt-to-income ratio, and your credit profile. Lenders ration usable equity through all three filters. NerdWallet's HELOC lender survey (May 2026) notes that most lenders set their borrower CLTV ceiling at 80–85%; getting above that requires either a niche ADU-specific product or a different loan type entirely.

Will your HELOC cover your ADU? The equity math infographic.

Four modeled scenarios

The scenarios below are illustrative — they show how the formula behaves at four different equity positions across representative markets and budgets.

Scenario A — Deep equity (HELOC fully covers)

| Home value | $1,400,000 |

| Mortgage balance | $480,000 |

| CLTV cap (standard) | 85% |

| Max combined debt | $1,190,000 |

| Estimated HELOC room | $710,000 |

| ADU budget (detached, 800 sq ft, high-cost) | $400,000 |

| Plus 15% contingency | $60,000 |

| Total needed | $460,000 |

| Result | Standard HELOC covers, with $250K of headroom. |

Scenario B — Recent buyer (HELOC partially covers)

| Home value | $625,000 |

| Mortgage balance | $475,000 |

| CLTV cap | 85% |

| Max combined debt | $531,250 |

| Estimated HELOC room | $56,250 |

| ADU budget (garage conversion) | $140,000 |

| Plus 15% contingency | $21,000 |

| Total needed | $161,000 |

| Result | HELOC covers ~35%. Either combine with savings, scale the project, or pivot to an ARV product / renovation loan. |

Scenario C — High mortgage balance (standard HELOC isn't viable)

| Home value | $560,000 |

| Mortgage balance | $470,000 |

| CLTV cap | 85% |

| Max combined debt | $476,000 |

| Estimated HELOC room | ~$6,000 |

| ADU budget | Any |

| Result | A standard HELOC won't fund this. The right path is a construction-to-permanent loan or HomeStyle / CHOICERenovation — products that underwrite based on the home's post-ADU value. |

Scenario D — Texas homeowner constrained by Section 50(a)(6)

| Home value | $500,000 |

| Mortgage balance | $260,000 |

| CLTV cap (Texas constitutional maximum) | 80% |

| Max combined debt | $400,000 |

| Estimated HELOC room | $140,000 |

| ADU budget (detached) | $180,000 |

| Plus 15% contingency | $27,000 |

| Total needed | $207,000 |

| Result | ~$67,000 gap. In Texas, the 80% ceiling is constitutional, not lender choice — see state rules section for what alternatives may work on a Texas homestead. |

A useful sanity check before you call any lender

If your HELOC room covers less than 80% of your total project budget including contingency, the project is structurally fragile on a standard HELOC. You're one change order away from running out of room mid-build. That's the moment to look at ARV HELOCs (where available) or renovation loans rather than push a standard HELOC to its ceiling.

Run Your Numbers — Free ADU HELOC Fit Calculator

Plug in your home value, mortgage balance, and ADU budget. Get your usable HELOC room, funding gap, fit score, and the alternative path most likely to close any gap. (60 seconds, no email required for the basics)

Free Tool

HELOC Fit Calculator

See if a standard HELOC covers your ADU — or if you need a different path.

Already know your numbers don't quite work?

See What You Can Build → Get Your Free ADU ReportCheck zoning, feasibility, and the financing paths that match your specific lot — before you call a single lender.

What Does a HELOC for an ADU Cost in 2026?

Answer capsule: As of mid-May 2026, the national average HELOC rate sits in the 7.21%–7.50% range across major surveys — Bankrate at 7.26% as of May 6, 2026 and Curinos / Yahoo Finance at 7.21% as of May 17, 2026. HELOC rates are variable and reset weekly; survey averages move with the Fed. ADU-specific HELOC programs, which trade higher CLTV ceilings for higher pricing, start at 8.25% APR — Patelco's California ADU HELOC quotes 8.25% APR for the most-qualified applicants at up to 125% CLTV (verified May 18, 2026). At a representative 7.50% rate, a $150,000 HELOC carries approximately $938 per month during the interest-only draw period and approximately $1,391 per month once it amortizes over a 15-year repayment period. These are illustrative payments, not personalized loan offers.

Current rate context, with verification dates

| Rate source | Reported rate | Date verified | Notes |

|---|---|---|---|

| Bankrate national survey | 7.26% | $30K line, 700 FICO, 80% CLTV — Bankrate methodology | |

| Curinos / Yahoo Finance | 7.21% | 780+ FICO, sub-70% CLTV | |

| Experian / Curinos | 7.50% | Broader credit range | |

| Bankrate 2026 forecast (avg.) | 7.30% | Assumes three Fed quarter-point cuts | |

| Patelco ADU HELOC (CA only) | Starting at 8.25% APR | Up to 125% as-is value / 90% post-construction value; primary CA residences; not all applicants qualify for the lowest rate | |

| Patelco standard HELOC (CA only) | Starting at 7.25% APR | Up to 80% CLTV | |

| Bay Federal Credit Union (CA only) | 7.00–8.50% range | Up to $400K, 18.00% maximum APR | |

| Foothill Credit Union (6 SoCal counties) | WSJ Prime + lender margin | 10-yr draw, 15-yr repay, 18.00% maximum APR |

Sources: bankrate.com/home-equity/heloc-rates (verified May 6, 2026); finance.yahoo.com Curinos snapshots (May 17, 2026); experian.com/blogs/ask-experian/heloc-rates (May 2026); patelco.org/credit-cards-and-loans/home-equity (verified May 18, 2026); bayfed.com (March 1, 2026); foothillcu.org (2026). All HELOC rates are variable, reset weekly, and depend on your credit profile, line size, CLTV, state, and lender. We make no rate guarantees.

Monthly payment math at four loan amounts

Below is illustrative payment math at a representative 7.50% rate. Your actual payment depends on your lender, product, credit, CLTV, and state. The "stress-test" column shows what your payment looks like if your variable rate rises by 2 percentage points — a scenario worth modeling before you commit, especially for an ADU build that spans 12–24 months.

| Line drawn | Interest-only (draw at 7.50%) | Fully amortizing (15-yr repayment at 7.50%) | Stress-test amortizing (rate rises to 9.50%) |

|---|---|---|---|

| $75,000 | ~$469 / month | ~$695 / month | ~$783 / month |

| $150,000 | ~$938 / month | ~$1,391 / month | ~$1,567 / month |

| $200,000 | ~$1,250 / month | ~$1,854 / month | ~$2,089 / month |

| $250,000 | ~$1,563 / month | ~$2,317 / month | ~$2,611 / month |

Illustrative only. Payment math assumes simple amortization at the stated rate; actual HELOC rates are variable and recalculate periodically. These are not loan offers, qualification quotes, or guarantees. Confirm exact payment structure with your lender.

What drives your specific rate

- 1.Credit score. Borrowers above 740 typically see the lowest published rates; sub-680 often see meaningfully higher pricing.

- 2.CLTV. The lower your combined LTV, the lower your rate. Curinos publishes its 7.21% average specifically for borrowers at sub-70% CLTV.

- 3.Line size. Larger lines often qualify for tighter pricing at some lenders, smaller lines at others.

- 4.Autopay / relationship pricing. Patelco's disclosure offers a 0.50% rate discount after the loan funds when you set up automatic payments and recurring deposits (patelco.org, verified May 18, 2026).

- 5.State. State-specific overlays — most notably Texas — set hard ceilings on what a lender can legally do.

- 6.Product type. ADU-specific HELOCs that push CLTV higher carry higher pricing than standard HELOCs.

A worked Patelco ADU HELOC example

Patelco's ADU HELOC is the most-cited example of a California credit union pushing CLTV above standard limits. The math, taken directly from their published example: a home valued at $800,000 with a $600,000 first mortgage. A standard HELOC at 90% CLTV gives you $720,000 secured ceiling − $600,000 = $120,000 available. The ADU HELOC at 125% CLTV gives you $1,000,000 secured ceiling − $600,000 = $400,000 available — roughly 3.3× the standard borrowing room on the same property. (Source: patelco.org/credit-cards-and-loans/home-equity/adu-line-of-credit, verified May 18, 2026.)

The tradeoffs are real. The ADU HELOC's draw period is two years instead of the standard ten. The starting APR is roughly a full percentage point higher than the standard product. The program is California primary residences only. Patelco's program disclosure also includes a fixed-rate conversion option that lets you lock all or part of the outstanding balance to a fixed rate during the draw period — useful insurance against a rising variable rate.

A note on closing costs

HELOCs typically cost less to set up than a refinance, but they're not free. Expect appraisal fees, title search, recording, and (for some lenders) a small lender fee. Bay Federal advertises a "no closing cost" structure that requires you to keep the line open for 36 months or reimburse those costs (bayfed.com disclosure, verified March 1, 2026). Patelco charges a $250 lender fee on the ADU HELOC plus a monthly construction-management fee of $50 (lines up to $100,000) or $100 (above $100,000) while the build is active. Read each lender's fee schedule before you sign — fees are part of the all-in cost, not a footnote.

The Dwelling Index is reader-supported. When you use this link to explore financing, we may earn a commission at no extra cost to you. We are not a lender or broker, do not rank lenders by compensation, and never guarantee rates, approval, or specific outcomes. Read our full disclosure.

Explore Mortgage, Refinance, Cash-Out, and Construction-Loan Options Nationwide → See Your Optionsvia Mortgage Research Center

The ADU HELOC Coverage Gap Table — Will a HELOC Actually Cover Your Build?

Answer capsule: A standard HELOC is most likely to cover interior conversions, basement ADUs, and simple garage conversions, and least likely to cover detached new construction in high-cost coastal markets. We assembled current 2026 cost benchmarks from Boston.gov, Angi, CALI ADU, and SnapADU to show where the typical HELOC borrower will hit the "current-value gap." We added a 15% contingency line to each cost band because that's the reserve most experienced ADU builders recommend.

| ADU project type | Verified 2026 cost benchmark | + 15% contingency | HELOC fit likelihood | Plain-English takeaway |

|---|---|---|---|---|

| Internal / basement conversion (Boston benchmark) | $75,000–$100,000 | $86,250–$115,000 | Strong | Most likely to fit inside standard HELOC room. The lowest-friction ADU type for HELOC financing. |

| Garage conversion ADU (Angi national) | $25,000–$225,000 (avg. ~$110,000) | $28,750–$258,750 | Strong to partial | Simple garage conversions usually fit; older garages needing major utility, foundation, or roof work can push toward the high end. |

| Garage conversion ADU (Los Angeles, CALI ADU) | $140,000–$245,000+ | $161,000–$281,750+ | Partial | High-cost coastal labor pushes garage conversions into territory where modest HELOCs run short. |

| Attached new construction (Angi ADU data) | $100,000–$216,000 | $115,000–$248,400 | Partial | Workable with strong equity. Tight for recent buyers. |

| Above-garage attached (Angi) | $128,000–$225,000 | $147,200–$258,750 | Partial | Site complexity (utilities to second story, structural retrofit) can swing budget materially. |

| Detached new construction — national (Angi) | $110,000–$285,000 | $126,500–$327,750 | Partial to weak | This is where most homeowners hit the current-value gap. |

| Detached ADU — Boston benchmark (Boston.gov) | $250,000–$350,000 | $287,500–$402,500 | Weak unless equity is deep | Many Boston-area homeowners need future-value financing. |

| Detached ADU — Los Angeles (CALI ADU) | $219,000–$459,000 | $251,850–$527,850 | Weak for most | High-cost coastal builds often require renovation / construction-to-perm financing. |

| Detached ADU — San Diego (SnapADU) | ~$430,000 in 2026 (CA Cost Index rose 44% from Jan 2021–Dec 2025) | ~$494,500 | Weak for standard HELOC | A standard HELOC is more likely to be a partial funding source than the whole plan. |

Sources: Boston.gov "Frequently Asked ADU Questions"; Angi 2026 cost data; CALI ADU "ADU Cost Los Angeles 2026"; SnapADU "Cost to Build an ADU in San Diego (2026)." All cost ranges verified May 19, 2026. Contingency calculations our own; assume 15% added to each band. Actual project costs vary by site, design, finishes, season, and contractor.

Three rules for using this table

See exactly what your lot can support

See What You Can Build → Get Your Free ADU ReportThe Feasibility Engine checks zoning, lot fit, and the financing paths that match your specific address — takes 60 seconds.

Which Lenders Publish HELOCs That Fit ADU Construction

Answer capsule: Most national HELOC lenders allow "home improvement" as a permitted use, but a meaningful minority quietly restrict new-construction draws — especially for detached ADUs. A small number of California credit unions market ADU-specific HELOC products with higher CLTV ceilings. RenoFi-powered renovation HELOCs underwrite the post-ADU value but are not available in Texas. Below is a verified matrix of lenders that publish ADU-relevant HELOC terms publicly. We pulled every cell directly from each lender's current public disclosure on or before May 19, 2026.

Verified lender matrix

| Lender | Markets to ADU borrowers? | Construction draws? | Max CLTV | Draw period | Interest-only? | Fixed-rate option? | States | ADU program? |

|---|---|---|---|---|---|---|---|---|

| Patelco Credit Union | Yes — dedicated ADU HELOC | Yes (phased) | Up to 125% as-is / 90% post-construction (ADU); 80% (standard) | 2 yrs (ADU) / 10 yrs (standard) | Yes | Yes — fixed-rate option on all or part of balance | CA primary residences only | Yes — ADU HELOC |

| Bay Federal Credit Union | Yes — explicitly cites ADU | Yes (general HELOC) | Up to 80% | Standard | Yes | Yes — partial-balance fixed-rate lock during draw | CA only | No (uses standard HELOC) |

| Foothill Credit Union | Yes — ADU content marketing | Yes (general HELOC) | Standard | 10-yr draw, 15-yr repay | Yes | Verify with lender | 6 SoCal counties (LA, Orange, Riverside, San Bernardino, Ventura, San Diego) | No (uses standard HELOC) |

| Figure | Yes — markets to renovation | Funded fully at close — full line disbursed upfront, not phased | Up to ~85% | 5 years | No — fully amortizing from day one | Yes — fixed-rate HELOC structure | Most U.S. states (check availability) | No |

| RenoFi (via partner credit unions) | Yes — built for renovation | Yes | Up to 90% of after-renovation value | Lender-dependent | Yes | Yes (fixed-rate option) | Not available in Texas | Yes — renovation HELOC |

Sources: patelco.org and Patelco ADU HELOC program disclosure (verified May 18, 2026); bayfed.com (verified March 1, 2026); foothillcu.org (verified 2026); figure.com FAQ page on HELOC funding (verified May 19, 2026); renofi.com (verified May 19, 2026). All terms subject to change — verify directly before applying.

How to read this matrix

"Yes — phased construction draws" means the lender's public guidance and product structure allow ADU-construction use. Always confirm in writing for your specific application.

"Funded fully at close" (Figure's structure per its public FAQ) means you receive the entire approved line on closing day and begin paying principal and interest from day one. That eliminates the main draw-flexibility benefit of a HELOC for a phased ADU build.

"Not available in Texas" — Texas's constitutional restrictions under Article XVI § 50(a)(6) prevent some renovation-HELOC structures from operating in the state. RenoFi is explicit about this.

Other national HELOC lenders to consider

Spring EQ, FourLeaf Federal Credit Union, Bank of America, Chase, Truist, U.S. Bank, Citizens Bank, PNC Bank, KeyBank, Third Federal, and TD Bank all publish HELOC programs nationally or in major markets. We did not include them in the matrix above because their public disclosures don't always specify ADU-construction-draw policy, fixed-rate conversion terms, or current draw structure to the level a homeowner needs before applying. Verify each lender's terms directly using the 7-question script below. Spring EQ is not authorized in New York, for example — a detail not visible on their main marketing pages but stated on their mortgage disclosure (mortgage.springeq.com, verified May 19, 2026).

A lender mentioning "ADU" in their content marketing is not a written commitment to fund phased construction draws on a new detached unit. Regulation Z (12 CFR § 1026.40(f)) permits a lender to freeze or reduce a HELOC under specific conditions — including evidence of material misrepresentation at origination. If you don't disclose new-construction use at application and the lender later discovers it, that can become the basis for a restriction. The right move is to disclose construction use upfront and get the lender's commitment in writing.

The 7-Question Lender Pre-Application Script

Email this to your loan officer before you submit a formal application. Require written responses. If the lender won't put any of these in writing, you've learned what you need to learn.

"Will your HELOC product allow phased construction draws for a new detached ADU on my property, including drawing funds against my licensed contractor's invoices?"

"Will you commit in writing that this line will not be frozen, reduced, or restricted solely because the disclosed draws are being used for new ADU construction?"

"What are the specific conditions under which your bank can freeze or reduce my HELOC under Regulation Z (12 CFR § 1026.40(f))?"

"What is the draw period, what is the repayment period, and are interest-only payments allowed during the draw period?"

"Do you offer a fixed-rate conversion option on all or part of the outstanding balance during the draw period? If so, what is the conversion margin and any conversion fee?"

"What is the maximum combined LTV at the lender level on this product, and will you consider any future or existing ADU rental income for qualification?"

"What documentation will you require at each draw — contractor invoices, lien waivers, inspector sign-off, or none?"

The script doesn't always change the outcome, but it gives you the documented basis for an informed one.

Want the lender script as a downloadable PDF?

Download the Free 2026 ADU Starter KitIncludes the lender pre-application script, a budget worksheet, the permit-readiness checklist, and the state-by-state reference table.

State Rules That Change the HELOC Math

Answer capsule: HELOC mechanics are governed federally through Regulation Z (12 CFR § 1026.40) and CFPB consumer protections, but state law sets the actual CLTV cap, the closing procedure, and the refinancing constraints. Texas is the most restrictive state in the country for HELOCs under Article XVI § 50(a)(6) of its state constitution. California has the strongest pro-ADU statutory framework (60-day approval clock under Government Code § 65852.2) but no state-level HELOC cap stricter than federal. Massachusetts adopted statewide ADU rules under 760 CMR 71.00 effective January 31, 2025. New York imposes mortgage recording tax that varies by locality.

Texas — Section 50(a)(6) Decoded

The Texas Constitution Article XVI § 50(a)(6), passed in 1997 and materially amended in 2018, sets the rules under which a Texas homeowner can borrow against their homestead. These rules are constitutional, not regulatory — a lender cannot waive them.

Sources: Texas Constitution Article XVI § 50(a)(6), statutes.capitol.texas.gov; Texas Finance Commission (fc.texas.gov/home-equity); Texas Real Estate Research Center (TAMU); Texas Bankers Association home equity loan requirements. Verified May 19, 2026.

California

California has the strongest pro-ADU statutory framework in the nation. Government Code § 65852.2 mandates ministerial (no discretionary) approval for compliant ADUs with a 60-day approval clock and a deemed-approval rule if the agency misses the deadline. No state-level HELOC cap stricter than federal standards. Multiple California credit unions — Patelco, Bay Federal, Foothill — offer HELOC products that explicitly accommodate ADU construction. Patelco's ADU HELOC pushes CLTV to 125% of as-is value (primary CA residences only, verified May 18, 2026).

Source: California Government Code § 65852.2 (2023); Patelco, Bay Federal, Foothill Credit Union product pages.

Massachusetts

Massachusetts adopted statewide ADU rules under 760 CMR 71.00, effective January 31, 2025. These regulations create "Protected Use" ADU rights across most single-family residential zones, requiring communities to allow by-right ADUs in single-family districts. No state-level HELOC restriction. Standard HELOC paths apply. High-cost detached ADU budgets in metro Boston ($250,000–$350,000+) frequently exceed moderate equity positions — see the coverage gap table above.

Source: Massachusetts 760 CMR 71.00, effective January 31, 2025 (Cornell Legal Information Institute); Boston.gov ADU FAQ.

New York

New York imposes a mortgage recording tax that varies by locality. In New York City, the combined mortgage recording tax can add 1.05–2.175% of the loan amount to your closing costs. Spring EQ is not authorized in New York (mortgage.springeq.com, verified May 19, 2026) — a detail not visible on their main marketing pages. Verify that your lender is licensed and actively originating in New York before applying.

Oregon

Oregon requires cities and counties planning under the state's land-use framework to allow ADUs in most residential zones. Oregon is a non-judicial-foreclosure state. No state-level HELOC restriction. Standard HELOC paths apply. Verify lender availability — not all national HELOC lenders originate in Oregon.

Washington

Washington's HB 1337, codified in RCW 36.70A.681, creates substantive ADU allowances for cities planning under the Growth Management Act. Washington is a non-judicial-foreclosure state, which modestly affects lender risk modeling. No state-level HELOC restriction. Standard HELOC paths apply.

Every other state

For most states, federal rules (CFPB, Regulation Z 12 CFR § 1026.40, Truth in Lending Act) govern. Always verify with the specific lender that:

Is HELOC Interest for an ADU Tax-Deductible?

Answer capsule: Potentially, yes. Under IRS Publication 936 and the Tax Cuts and Jobs Act of 2017, interest on a HELOC is deductible only when the borrowed funds are used to "buy, build, or substantially improve" the home that secures the loan. Building an ADU on the home that secures the HELOC generally meets the "substantially improve" test. The deduction is subject to a combined acquisition-debt cap of $750,000 ($375,000 if married filing separately) for loans originated after December 15, 2017. You must itemize on Schedule A to claim it. This is general tax information; consult a CPA before acting on it.

The four-part test

To qualify for the deduction, IRS Publication 936 requires all of the following:

- 1The HELOC is secured by a qualified residence (your main home or one second home).

- 2The proceeds are used to buy, build, or substantially improve that same residence.

- 3You substantiate the use with documentation tying the funds to the qualified improvement.

- 4Your combined qualified mortgage debt (first mortgage + qualifying HELOC) is within the $750,000 cap ($1,000,000 cap for loans originated before December 16, 2017).

Source: IRS Publication 936 (2025); IRS FAQ on real-estate taxes, mortgage interest, points, and other property expenses; both verified May 19, 2026.

A worked example

Sarah, single filer, draws $180,000 on a HELOC at a 7.5% representative rate over a 24-month ADU build. Her average outstanding balance over Year 1 is roughly $90,000. Year 1 interest paid is approximately $6,750.

If Sarah itemizes (her total itemized deductions exceed the $16,100 standard deduction for a single filer in 2026), and the HELOC funds were used entirely for ADU construction qualifying as a substantial improvement, the $6,750 in HELOC interest is added to her Schedule A mortgage-interest deduction. At a 24% federal marginal tax bracket, that deduction reduces her federal tax by approximately $1,620. Her after-tax effective interest rate on the borrowed money is approximately 5.7% instead of 7.5%.

Illustrative example. Numbers approximate. Whether the deduction is actually beneficial for any individual taxpayer depends on whether their total itemized deductions exceed the standard deduction, their marginal tax bracket, the cap, and other factors. This is not tax advice; consult a qualified CPA or tax professional.

The documentation framework

To protect the deduction, keep all of the following from the day you close the HELOC through at least three years after the tax filing in question:

- Signed contractor invoices showing ADU-specific work (foundation, framing, MEP, finishes).

- Lien waivers from contractors and subcontractors.

- The building permit showing the ADU as the permitted work.

- The executed HELOC agreement showing the loan secured by the same home.

- Bank statements showing each HELOC draw flowing to the contractor or escrow.

- Form 1098 from your HELOC lender each year, showing interest paid.

A clean discipline:

Don't commingle HELOC funds with personal spending. If you draw $50,000 for framing, send $50,000 to your contractor. If you commingle, the IRS will allocate the interest between qualified and personal use, and you may lose part of the deduction.

Common mistakes that kill the deduction

- Using part of the draw for personal expenses (a car, a vacation, debt consolidation). The IRS allocates the interest by use, and personal-use portions are not deductible.

- Failing to itemize when the standard deduction is higher anyway. For 2026, the standard deduction is $16,100 for single filers and $32,200 for joint filers.

- Refinancing during construction in a way that breaks the acquisition-debt trace. Talk to your CPA before a mid-build refinance.

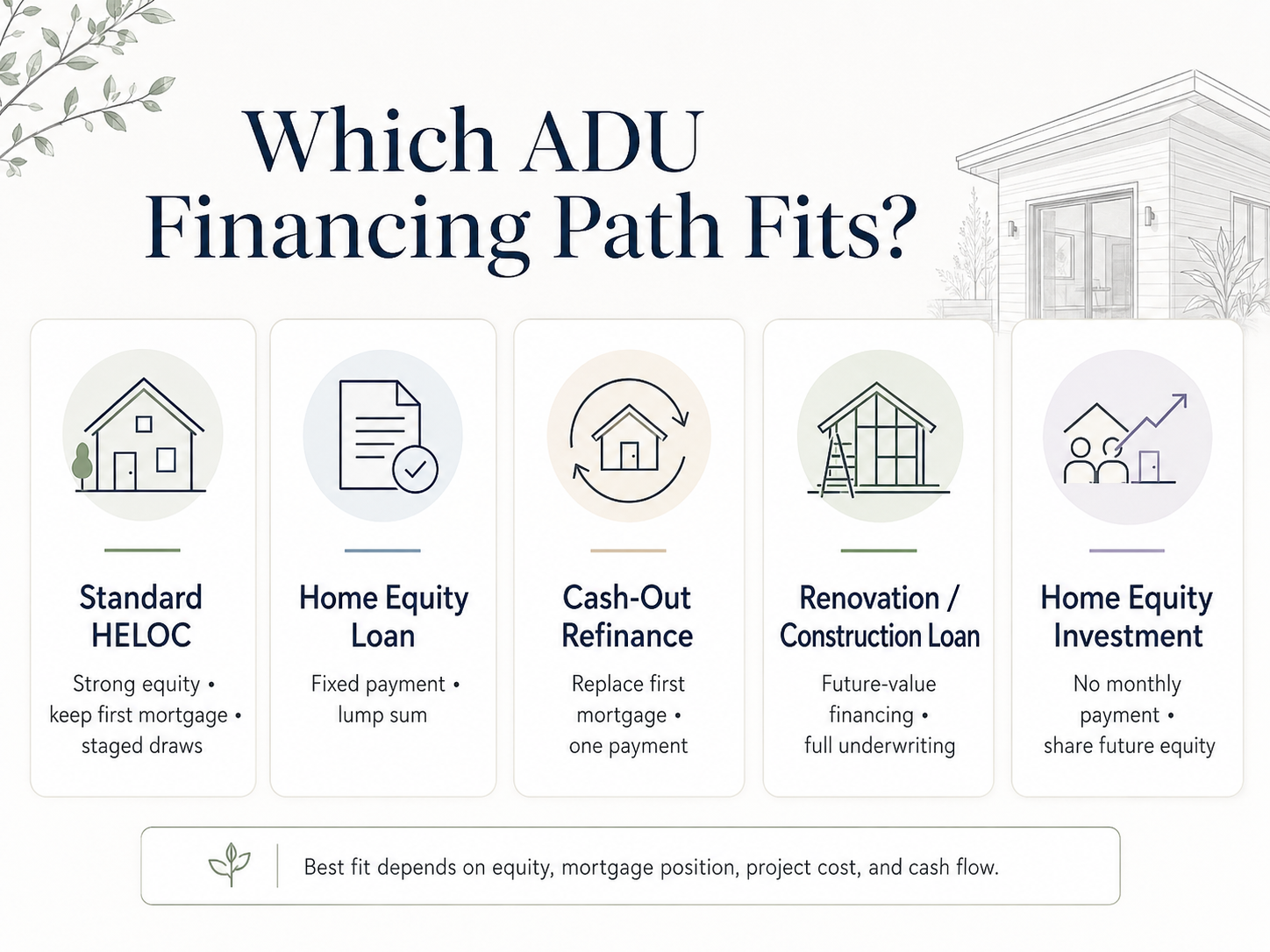

HELOC vs. Every Other ADU Financing Path

Answer capsule: A HELOC is typically the right tool when you have substantial current-value equity, want to keep your first mortgage, and need staged draws. A home equity loan fits when you want fixed payments. A cash-out refi fits only when replacing your first mortgage makes overall financial sense. A construction-to-permanent or renovation loan fits when the project requires future-value underwriting. A home equity investment fits when you can't carry another monthly payment. Match the tool to your equity position and your tolerance for monthly carrying cost.

Which ADU financing path fits your equity position and project type?

| Path | How it works | Keeps first mortgage? | Current or future value? | Draws or lump sum? | Rate type | Payment during build | Main tradeoff |

|---|---|---|---|---|---|---|---|

| Standard HELOC | Revolving second lien; draw as needed | ✅ Yes | Current | Draws | Variable | Interest-only on outstanding balance | Variable rate; capped by current equity |

| Home equity loan | Lump-sum second lien at fixed rate | ✅ Yes | Current | Lump sum | Fixed | Principal + interest from day one | No draw flexibility; interest on full amount immediately |

| ARV HELOC (where available) | Revolving second lien based on post-ADU value | ✅ Yes | Post-construction | Draws | Variable | Interest-only on outstanding balance | Limited availability; mostly CA credit unions and RenoFi partner CUs (not TX) |

| Cash-out refinance | Replaces first mortgage with a larger one; you take the difference in cash | ❌ No | Current | Lump sum | Fixed | New full mortgage payment from day one | Lose your existing first-mortgage terms |

| Construction-to-permanent | Construction loan converts to a permanent mortgage on completion | ❌ Replaces existing or stands alone | Post-construction | Construction draws | Variable during build → fixed after | Interest-only during build | Heavy paperwork; need approved plans and licensed builder |

| HomeStyle / CHOICERenovation / FHA 203(k) | Single loan covering purchase or refinance plus renovation | ❌ Replaces first mortgage | Post-construction | Construction draws | Fixed | Combined mortgage + reno payment | Strict program rules; refinances your first mortgage |

| Home equity investment (HEI) | Lump sum in exchange for a share of future appreciation; no monthly payment | ✅ Usually | Current | Lump sum | N/A (equity share) | $0 | Equity-share trade-off; settles when you sell or refinance; check availability in your state |

Sources: CFPB consumer guidance, verified May 19, 2026; Fannie Mae Selling Guide B2-3-04 and B3-3.8-01; Freddie Mac CHOICERenovation; HUD ML 2023-17; Urban Institute April 2024; Patelco, RenoFi product pages; Hometap, Unlock, Point product disclosures.

HELOC vs. cash-out refinance for ADU — which is better?

HELOC wins when:

Your first mortgage is a sub-5% rate from 2020–2022, or any rate you'd fight to keep. A HELOC adds a second lien at today's variable rate without disturbing the favorable first mortgage. You keep the low monthly payment on the bulk of your home debt and only pay today's rate on the new ADU borrowing.

Cash-out refi wins when:

Your first mortgage is already at or near today's mortgage rates (high-6%, low-7%), or your mortgage balance is small relative to home value. Refinancing into a single, fixed-rate, fully amortizing loan can simplify your monthly carrying cost.

A note on FHA 203(k) specifically

HUD's Mortgagee Letter 2023-17 makes the FHA 203(k) ADU treatment explicit. Standard 203(k) covers (a) converting a one-family dwelling into a one-family-plus-ADU, (b) adding an attached ADU, and (c) renovating an existing attached or detached ADU. A brand-new, ground-up, free-standing detached ADU is not an eligible Standard 203(k) project under HUD ML 2023-17. For a new detached ADU, the cleaner agency paths are HomeStyle Renovation (Fannie Mae), CHOICERenovation (Freddie Mac), or a construction-to-permanent loan.

A nuance on HomeStyle Renovation for ADUs

Fannie Mae's HomeStyle Renovation product can finance constructing or installing a new ADU on a one-unit primary residence — detached, attached, or manufactured — based on the home's after-completion value. Two important constraints from the Selling Guide: only one ADU per parcel is eligible, and ADUs are not allowed with two-to-four-unit dwellings under that section.

For the full breakdown of every path including the cases where they overlap, see our pillar guide: How to Finance an ADU in 2026: 7 Paths Compared →

What If a Standard HELOC Won't Cover Your ADU?

Answer capsule: If standard HELOC math falls short, the next move is not to push for a bigger HELOC. It's to switch from current-value financing to a path that can consider the completed ADU value. The most common alternatives: an ARV HELOC, Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, FHA Standard 203(k) for eligible project types, a construction-to-permanent loan, or — for cash-flow-constrained homeowners — a home equity investment (HEI).

How "future-value" lending actually works

Standard HELOC asks:

"What is the home worth today?"

Lends a percentage against current value. Capped by today's equity.

Renovation / construction loan asks:

"What will the home be worth after this ADU is complete?"

Lends a percentage against future value. Unlocks projects a standard HELOC can't fund.

When to stop shopping HELOCs and switch lanes

You should pivot to a future-value path when:

- Your HELOC room covers less than 80% of total project cost including contingency.

- You're building ground-up detached in a high-cost market.

- The lender will not consider ADU rental income at all on the loan structure you need.

- You bought your home in the last 1–3 years and have limited equity buildup.

- You need formal construction draws, inspector sign-off, and milestone funding.

- You're in Texas and the 80% (a)(6) cap leaves you short — talk to a Texas-licensed lender about a construction-loan structure outside (a)(6).

Programs to actually look at

Fannie Mae HomeStyle Renovation

Finances purchase or refinance plus ADU construction in a single loan, underwritten on after-completion value. Detached, attached, and manufactured ADUs are eligible if they meet Fannie Mae property requirements. Renovation must be complete within 15 months. Only one ADU per parcel; two-to-four-unit dwellings not eligible under this product. (Source: Fannie Mae Selling Guide B2-3-04 and B5-3.2-01, verified May 19, 2026.)

Freddie Mac CHOICERenovation

Similar structure to HomeStyle. Can be used to add or renovate an ADU on a one-unit property. (Source: Freddie Mac ADU page, verified May 19, 2026.)

FHA Standard 203(k)

Best for converting an existing structure into an ADU or adding an attached ADU. Not eligible for a brand-new, ground-up, free-standing detached ADU per HUD ML 2023-17. Down payment as low as 3.5%. Requires a HUD-approved consultant.

Construction-to-permanent loan

Disburses funds in construction draws verified by an inspector, then converts to a permanent mortgage on completion. Designed for ground-up detached ADUs.

ARV HELOC

Where available (primarily California credit unions like Patelco, and RenoFi-partner credit unions in most non-Texas states), this is a second-lien option that preserves the first mortgage while underwriting on post-ADU value.

Home equity investment (HEI)

Companies like Hometap, Unlock, and Point provide a lump sum in exchange for a share of your home's future appreciation, with no monthly payment. State availability is limited and varies by company — verify the company actively serves your state before relying on this path. Best for retirees or fixed-income homeowners who genuinely cannot carry another monthly payment.

Best used after you've run the HELOC fit test and know whether current-value equity is enough. The Dwelling Index is reader-supported. When you use this link to explore financing, we may earn a commission at no extra cost to you. We are not a lender or broker, do not rank lenders by compensation, and never guarantee rates, approval, or specific outcomes. Read our full disclosure.

Explore Mortgage, Refinance, Cash-Out, and Construction-Loan Options Nationwide → See Your Optionsvia Mortgage Research Center

Can ADU Rental Income Help You Qualify?

Answer capsule: Yes — but with conditions, and not on every loan type. Under Fannie Mae Selling Guide Announcement SEL-2025-08, effective October 8, 2025, and codified in Selling Guide section B3-3.8-01, lenders can count rental income from one ADU on a one-unit primary residence toward qualifying income, capped at 30% of the borrower's total qualifying income, for purchase money mortgages and limited cash-out refinances only. Freddie Mac has a comparable framework. FHA has a more limited treatment under HUD ML 2023-17. Standard HELOC lenders generally do not count projected ADU rent for the initial line approval — so don't build your HELOC plan around income that doesn't yet exist.

What Fannie Mae's 2025 update actually says

Fannie Mae's Selling Guide section B3-3.8-01 (Rental Income, updated 10/08/2025) and the SEL-2025-08 announcement state that rental income from an ADU may be considered for qualifying purposes when all of the following conditions are met:

- The subject property is a one-unit principal residence.

- The transaction is a purchase or limited cash-out refinance (this rule does not extend to standard cash-out refinances).

- Rental income may be derived from only one ADU, even if multiple ADUs exist on the property.

- The amount of ADU rental income used for qualifying purposes may not exceed 30% of the borrower's total qualifying income.

- All other Fannie Mae documentation requirements (Form 1007 Single-Family Comparable Rent Schedule; lease agreements where applicable) apply.

Desktop Underwriter (DU) version 12.1, updated in Q1 2026, automatically applies these rules. (Source: Fannie Mae SEL-2025-08; Selling Guide B3-3.8-01; PennyMac correspondent announcement 26-29, March 2026. All verified May 19, 2026.)

The practical takeaway:

Build your HELOC plan so the math works without counting projected rent. Once the ADU is built and generating documented income, you may be able to use that income in a later refinance that consolidates your HELOC and first mortgage — at which point your position is far stronger.

Rental income projections and property value changes are illustrative, not guarantees. Actual results depend on local market conditions, construction costs, financing terms, occupancy rates, and regulatory approvals.

Six Risks Every ADU HELOC User Must Plan For

Answer capsule: A HELOC is a powerful tool with real, manageable risks. The biggest ones: variable-rate payment increases, line freezes or reductions during construction, refinance subordination friction, construction cost overruns that exceed your line, payment shock at the transition from draw to repayment period, and short-term resale math that doesn't pencil. None of these are dealbreakers if you plan for them.

Risk 1 — Variable-rate payment increases

Most HELOC rates float with WSJ Prime + margin. A 2-percentage-point move during your 18-month build adds material monthly cost. Manage it by stress-testing payments at +2%, asking the lender about annual and lifetime rate caps (commonly 18%), and asking specifically whether they offer a fixed-rate conversion option on all or part of the outstanding balance during the draw period. Bay Federal allows partial-balance fixed-rate locks during the draw period; Patelco's program disclosure offers a fixed-rate option as well.

Risk 2 — Lender freezes or reduces your line during the build

Regulation Z 12 CFR § 1026.40(f) explicitly allows lenders to freeze or reduce a HELOC under specific conditions. Triggers include: a significant decline in the value of the dwelling; the lender reasonably believes the consumer will be unable to fulfill repayment obligations because of a material change in financial circumstances; the consumer is in default; or fraud or material misrepresentation by the consumer. New-construction use is not itself a Regulation Z freeze trigger, but failing to disclose construction use at application and having the lender discover it later can become the basis for a misrepresentation-related restriction. Protect yourself by disclosing ADU construction use at application, getting written confirmation that the line won't be frozen solely because of disclosed construction use, maintaining a conservative CLTV with headroom, and keeping your credit clean during construction.

Risk 3 — Refinance subordination friction

A HELOC is a second lien. If you ever want to refinance your first mortgage — for example, to consolidate after the ADU is built — the HELOC lender has to formally agree to subordinate (stay in second position behind the new first mortgage). CFPB warns that some HELOC lenders charge subordination fees, take weeks to process the request, or in some cases refuse, requiring you to pay off the HELOC as part of the refinance. Ask your HELOC lender upfront about their subordination policy, fee, and typical timeline. (Source: consumerfinance.gov, verified May 19, 2026.)

Risk 4 — Construction cost overruns

ADU construction routinely runs over initial estimates, especially detached new builds where site work, soil conditions, or utility surprises surface mid-project. If your HELOC line exactly matches your contractor's quote, you have zero buffer. Manage it by building a 15% minimum contingency into your total project budget, drawing against the contingency only when needed, and keeping a small parallel cash reserve.

Risk 5 — Payment shock at draw-to-repayment transition

During the draw period, many HELOCs allow interest-only payments. When the draw period ends, the line stops accepting new draws and your payment shifts to fully amortizing principal-plus-interest over 10–20 years. The CFPB notes this transition often produces a sharp increase. A $150,000 balance paying ~$938 interest-only at 7.5% jumps to ~$1,391 fully amortizing over 15 years. Model the post-draw payment from day one — not just the introductory interest-only payment.

Risk 6 — Short-term resale math

If your plan is to build the ADU and sell within 12–24 months, the combination of construction cost, HELOC carrying cost during the build, real estate commissions, and any rate-lock costs on the buyer's mortgage can compress the return. ADUs add real value — but the case is far stronger over a 5–10 year hold than over a quick flip. Model conservatively if your horizon is short.

The damaging admission

A HELOC is the cleanest ADU financing tool we know of for the borrower it fits. It is also the wrong tool for a meaningful share of homeowners. If your only path to "yes" is to assume rental income arrives perfectly on schedule, your rate doesn't rise during the build, your contractor never asks for a change order, and your appraisal comes in at the top of the range — you're not financing an ADU on a HELOC. You're gambling on one. The right answer in that situation is to scale the project, build more savings, or use a future-value product that doesn't require everything to go right.

How to Structure Your HELOC Draws Across the Build

Answer capsule: Match your HELOC draws to your contractor's milestone billing — not to a calendar. Draw funds immediately before each phase begins, never weeks ahead. This minimizes interest paid on idle cash and keeps your CLTV headroom clean if anything goes sideways.

A representative draw plan for a $200,000 detached ADU build

| Phase | Typical work | Share of budget | Cumulative draw |

|---|---|---|---|

| 1. Design, engineering, plan check | Architect, structural, soils report, plan submittal | 8% (~$16,000) | $16,000 |

| 2. Permits and impact fees | City building permit, school fees, utility connection fees | 5% (~$10,000) | $26,000 |

| 3. Site prep and foundation | Demo, grading, trenching, slab or pier foundation | 18% (~$36,000) | $62,000 |

| 4. Framing and exterior shell | Framing, roof, sheathing, windows, exterior doors | 22% (~$44,000) | $106,000 |

| 5. Mechanical, electrical, plumbing rough-in | MEP rough-in, insulation, drywall | 18% (~$36,000) | $142,000 |

| 6. Interior finishes | Flooring, cabinets, fixtures, paint, tile | 18% (~$36,000) | $178,000 |

| 7. Final inspections and contingency | Punch list, final inspection, contingency reserve | 11% (~$22,000) | $200,000 |

Representative draw schedule; actual phase distribution varies by builder, market, and project. Use as a starting point for the conversation with your contractor — not a contractual schedule.

Three rules that protect your interest carry

- 1Draw immediately before the contractor invoices, not weeks in advance. Cash sitting in your checking account earns nothing while your HELOC charges interest on it.

- 2Keep your contingency undrawn until you actually need it. That's a HELOC's structural advantage over a home equity loan — use it.

- 3Document each draw to its corresponding invoice. This serves the IRS deduction trace and your records if the lender ever asks how funds were used.

Edge Cases That Change the Answer

Answer capsule: A HELOC decision can change based on HOA restrictions, local zoning quirks, utility constraints, prefab vs. site-built classification, recent home purchase, existing liens, forbearance history, owner-occupancy rules, or post-build tax reassessment. The list below isn't a verdict on any specific lender — it's a checklist of conditions to verify with your specific lender and local authorities before applying.

HOA restrictions▶

Local zoning and permit timing▶

Owner-occupancy and short-term rental restrictions▶

Recently purchased home▶

Existing HELOC or second lien▶

Prefab and modular ADUs▶

Forbearance or loan modification history▶

Investment property vs. primary residence▶

Property tax reassessment after the build▶

How to Shop for a HELOC for ADU Construction

Answer capsule: Shop the structure before the logo. For ADU construction, the things that matter are draw flexibility, CLTV cap, appraisal timing, lien and subordination policy, fixed-rate conversion options, minimum draw size, freeze terms, fees, and use-of-funds restrictions. Compare on those criteria — not on the lender's marketing.

The neutral comparison checklist

| Criterion | Why it matters for an ADU |

|---|---|

| State availability | Not every product is offered in every state. |

| Property type and occupancy | Most HELOCs require primary residence; investment property is rare. |

| CLTV cap | Determines usable HELOC room. |

| Current or post-construction value | Standard HELOCs ignore future ADU value. |

| Phased draw structure | ADU contractors bill in milestones. |

| Minimum draw size | A $4,000 minimum (Texas constitutional rule) or other lender minimums cut off micro-draws for early-phase fees. |

| Draw period length | 5 vs. 10 years matters if your build runs long. |

| Interest-only payment option during draw | Manages cash flow during the build. |

| Fixed-rate conversion option | Hedge against variable-rate increases. |

| Lender's construction-use policy | Some restrict; some don't publish a position. |

| Subordination policy | Matters if you'll refinance the first mortgage later. |

| Appraisal method | AVM vs. desktop vs. full appraisal affects approved line size. |

| Closing costs and ongoing fees | Patelco charges a $50–$100/month construction management fee during the build, for example. |

| Early closure fees | Affects whether you can refinance the HELOC after completion without penalty. |

Why we don't publish a "best ADU HELOC lender" ranking

Because there is no single best lender for every ADU homeowner. The best lender for a California homeowner with deep equity building a 600 sq ft prefab is not the best lender for a Texas homeowner doing a basement conversion. Our methodology is to sort by the structural criteria above — verified directly from each lender's current public disclosures — and let you pick the row that fits your equity, your state, and your project type. That keeps the page free of paid-ranking bias and free of stale "best of" claims that don't survive the next rate cycle.

What We Verified for This Guide

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We verified every factual claim in this guide against a primary or highly authoritative source on or before .

Frequently Asked Questions

Can I use a HELOC to build an ADU?

▶

Is a HELOC the best way to finance an ADU?

▶

How much equity do I need to build an ADU with a HELOC?

▶

What happens if a standard HELOC isn't enough?

▶

Is a HELOC better than a home equity loan for ADU construction?

▶

HELOC vs. cash-out refinance for ADU — which is better?

▶

Can ADU rental income help me qualify for a HELOC?

▶

Is HELOC interest tax-deductible for ADU construction?

▶

Are there special HELOC rules in Texas for an ADU?

▶

Will my lender let me draw a HELOC for a new detached ADU?

▶

Can a lender freeze my HELOC during construction?

▶

Will a HELOC affect my ability to refinance my first mortgage later?

▶

Should I get a HELOC before or after ADU permits?

▶

What if I just bought the home and don't have much equity?

▶

Can I use a HELOC for a prefab or modular ADU?

▶

Can I use a HELOC for a garage conversion ADU?

▶

What should I ask a lender before using a HELOC for ADU construction?

▶

Our Editorial Methodology

We built this guide to answer one specific question honestly: is a HELOC the right way to finance your ADU, and if so, how should you compare options and structure the draw?

What "best" means on this page. Best fit for your equity position, your state, your ADU type, and your tolerance for variable rates — never best by who pays us the most.

How we research. We work from federal consumer-finance guidance (CFPB, Regulation Z), agency mortgage program rules (Fannie Mae, Freddie Mac, HUD), IRS tax publications, state constitutional and statutory text where relevant, and current lender product pages. We separate verified commercial facts from regulatory facts from editorial conclusions, and we label which is which.

What we don't do. We don't rank financing products by affiliate payout. We don't fabricate author credentials. We don't guarantee approval, rates, tax deductions, construction costs, rental income, or permit outcomes. We don't quote rates or payments as offers — only as illustrative examples with verification dates.

Last verified: . Full editorial standards →

Sources and Citations

- Bankrate. "Current HELOC Rates In May 2026." bankrate.com/home-equity/heloc-rates. Verified May 19, 2026.

- Curinos / Yahoo Finance. "HELOC and home equity loan rates Sunday, May 17, 2026." Verified May 17, 2026.

- Experian. "Compare Current HELOC Rates." May 2026. Verified May 19, 2026.

- Patelco Credit Union. "ADU HELOC" product page and ADU HELOC program disclosure. patelco.org. Verified May 18, 2026.

- Bay Federal Credit Union. "HELOC." bayfed.com. Verified March 1, 2026.

- Foothill Credit Union. "Home Equity Loans & Lines." foothillcu.org. Verified 2026.

- Figure. HELOC FAQ. figure.com/faqs/home-equity-line. Verified May 19, 2026.

- RenoFi. ADU financing and renovation HELOC product pages. renofi.com. Verified May 19, 2026.

- Spring EQ. Mortgage disclosure (New York unavailability). mortgage.springeq.com. Verified May 19, 2026.

- Urban Institute. "To Increase the Housing Supply, Focus on ADU Financing." April 2024. urban.org.

- IRS Publication 936. "Home Mortgage Interest Deduction." 2025. irs.gov/publications/p936. Verified May 19, 2026.

- IRS FAQ. "Real estate (taxes, mortgage interest, points, other property expenses)." irs.gov. Verified May 19, 2026.

- Texas Constitution Article XVI § 50. statutes.capitol.texas.gov; FindLaw; Justia. Verified May 19, 2026.

- Texas Finance Commission. fc.texas.gov/home-equity. Verified 2026.

- Texas Bankers Association. Home equity loan requirements guidance. Verified May 19, 2026.

- Texas Real Estate Research Center (Texas A&M). "What to Know About Home Equity Loans in Texas." July 2025.

- Fannie Mae. Selling Guide B3-3.8-01 (Rental Income, effective 10/08/2025); SEL-2025-08 (October 8, 2025); B2-3-04. selling-guide.fanniemae.com.

- Fannie Mae. Accessory Dwelling Units product page. singlefamily.fanniemae.com. Verified May 19, 2026.

- Freddie Mac. Accessory Dwelling Units and CHOICERenovation. sf.freddiemac.com.

- HUD. Mortgagee Letter 2023-17. "Revisions to Rental Income Policies, Property Eligibility, and Appraisal Protocols for Accessory Dwelling Units." hud.gov.

- CFPB. "What is a home equity line of credit (HELOC)?", "Does a HELOC affect my ability to refinance my first mortgage loan?", and Official Interpretations of Regulation Z 12 CFR § 1026.40. consumerfinance.gov. Verified May 19, 2026.

- Regulation Z, 12 CFR § 1026.40 and Official Commentary. Truth in Lending Act open-end home-secured credit rules.

- California Government Code § 65852.2 (2023). State ADU ministerial-approval framework with 60-day clock.

- Massachusetts 760 CMR 71.00 (effective Jan 31, 2025). Protected Use Accessory Dwelling Units regulation via Cornell Legal Information Institute.

- Washington State HB 1337 / RCW 36.70A.681. State ADU requirements.

- Boston.gov. "Frequently Asked ADU Questions." content.boston.gov/departments/housing.

- Angi. ADU and garage conversion cost data, 2026. angi.com.

- CALI ADU. "ADU Cost Los Angeles 2026: Prices by Size & Type." cali-adu.com.

- SnapADU. "Cost to Build an ADU in San Diego (2026)." snapadu.com.

- PennyMac Correspondent. Announcement 26-29: Fannie Mae ADU rental income updates. March 23, 2026.

Not sure where to start?

See what's possible at your address — get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU ReportNo email required for the basics. Check zoning, feasibility, and the financing paths that match your specific lot.