Bridge Loan for ADU: When It Works, When It's Risky, and What to Use Instead

By The Dwelling Index Editorial Team · ·

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder.

Quick answer: a bridge loan is the right tool in exactly three situations

A bridge loan for an ADU is short-term (typically 6–24 months), interest-only, secured against the property, and repaid through a refinance or sale at maturity. It wins on exactly three dimensions: (1) speed — closing in 7–21 days vs. 30–90 for conventional products, (2) ARV underwriting — some lenders will lend against after-completion value instead of current equity, and (3) non-owner-occupied investor property — where most home-equity products will not lend.

On every other dimension — cost, payment predictability, qualification ease, consumer protection — at least one of the other seven ADU financing paths beats it. Published institutional bridge rates run 9%–13.5% interest-only plus 1.5–3 origination points and 1–3% closing costs. The most common reason bridge loans default is not the interest rate — it is borrowers who could not refinance because the exit plan failed. The exit is the underwriting.

Quick verdict — find your situation

| If you're… | Bridge loan verdict | Jump to |

|---|---|---|

| An investor adding an ADU to a non-owner-occupied rental | Often the right tool | Fit matrix |

| Closing on a deal in days, not weeks | Strong fit on speed | Fit matrix |

| An owner-occupant with enough equity and 30+ days to wait | HELOC or reno loan first | Alternatives |

| Unsure if your exit plan will work at refinance | Stop — read the exit section | Exit strategy |

| In a state with an active low-cost program (Massachusetts) | Program first, bridge last | State notes |

| Credit below 660 and no strong collateral | Will not qualify at most lenders | Who qualifies |

60 seconds, no obligation — confirm what's buildable before you compare loan options.

What we verified for this guide

Primary sources reviewed May 20, 2026:

- • Published bridge loan pricing from Kiavi, RCN Capital, Stormfield Capital, AHL, Capital Direct Funding, Vaster, Clearhouse Lending, Arbitrust (Jan–Apr 2026)

- • ADU-specific bridge products: HCS Equity, Mortgage Vintage, SnapADU, Valor Lending, TaliMar Financial

- • Fannie Mae Selling Guide B3-3.8-01 (ADU rental income, DU 12.1 effective March 21, 2026)

- • Freddie Mac CHOICERenovation fact sheet and single-family ADU page (ADU takeout rules, rental income cap)

- • HUD Mortgagee Letter 2023-17 (FHA 203(k) ADU eligibility, rental income cap, reserves)

- • FHFA 2026 conforming loan limits (announced November 25, 2025)

- • MassHousing ADULP program page (active as of May 20, 2026)

- • California 2025 HCD ADU Handbook update (Gov. Code §§ 66310–66342); CalHFA ADU Grant status

- • CFPB Regulation X §1024.5 (RESPA coverage and exemptions for business-purpose loans)

Update cadence: quarterly review of all rate ranges, federal underwriting rules, and state program status.

What is a bridge loan for an ADU?

A bridge loan is short-term debt — typically 6 to 24 months — that funds a real estate project until a permanent financing solution takes over. For ADUs, the loan is usually interest-only during the build, secured by the property in either a first or second lien position, and repaid via refinance, sale, or takeout loan at maturity. The balloon payment at the end is not a minor detail. It is the event the entire financing structure is built around.

Consumer-purpose vs. business-purpose: the distinction that matters

The most important structural fact about ADU bridge loans is that many — particularly on non-owner-occupied investment properties — are made as business-purpose loans. Business-purpose loans are generally outside the consumer-protection framework that applies to residential mortgages. That means the Loan Estimate, Closing Disclosure, and three-day right of rescission may not apply. The lender determines the loan's primary purpose case by case, so owner-occupied ADU financing can be treated differently than non-owner-occupied investor financing.

| Feature | Consumer-purpose bridge | Business-purpose bridge |

|---|---|---|

| Typical borrower | Owner-occupant | Investor / non-owner-occupied property |

| RESPA / TILA disclosures | Generally required | Often exempt (§1024.5) |

| Right of rescission | 3-day, may apply | May not apply |

| Entity requirement | Individual usually acceptable | LLC/entity often required |

Why ADUs make bridge loans more complicated

Bridge loans are well-established for fix-and-flip and ground-up residential investment. ADU-specific bridge financing has unique complications: (1) permit timing — ADU permit review can add weeks to the project timeline in ways that standard fix-and-flip timelines don't account for; (2) thin appraisal comparables — in many markets, ADU sales comparables are still sparse, and the ARV haircut lenders apply often understates how much value the ADU actually adds; (3) owner-occupied complexity — if you live on the property, the lender's product choice and consumer-protection requirements change; and (4) DSCR exit timing — most DSCR lenders want 3–6 months of documented rent before refinancing, which has to fit within the bridge term.

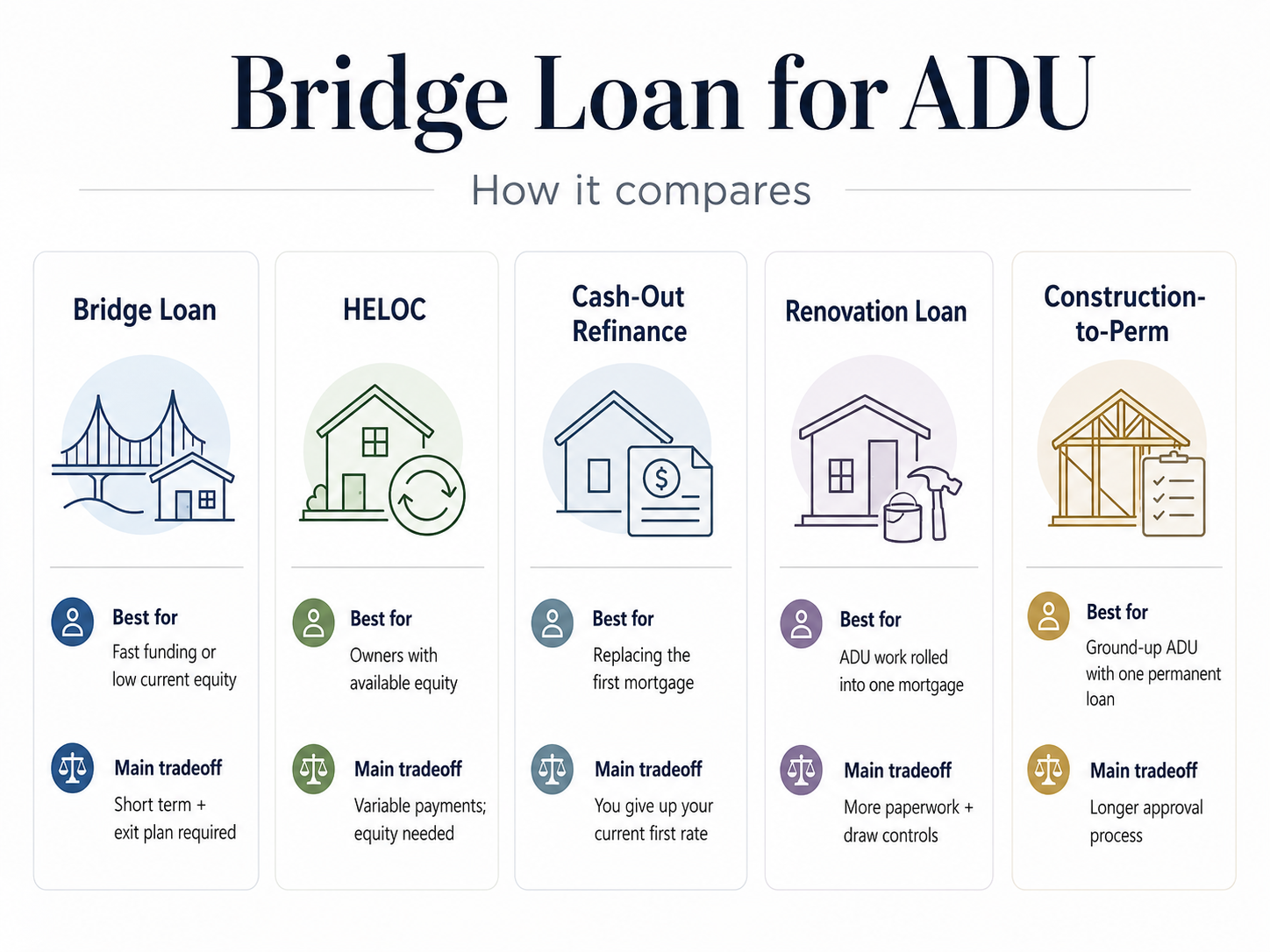

Bridge loan vs. other ADU financing products

| Feature | Bridge / hard money | Construction loan | HELOC | Renovation loan |

|---|---|---|---|---|

| Rate (2026) | 9%–13.5% | 7%–10% | 7%–9.5% | 6.5%–8.5% |

| Time to fund | 7–21 days | 45–90 days | 3–6 weeks | 45–60 days |

| Equity required | Low / none (ARV) | Low–medium | High | Low (as-completed) |

| Owner-occupancy | Not required (investor) | Sometimes | Usually yes | Usually yes |

| Refinance risk | High (balloon at maturity) | Low (single-close) | None | None (single-close) |

| Points / fees | 1.5–3% + closing costs | 1–2% + closing costs | Low (often none) | 1–2% + closing costs |

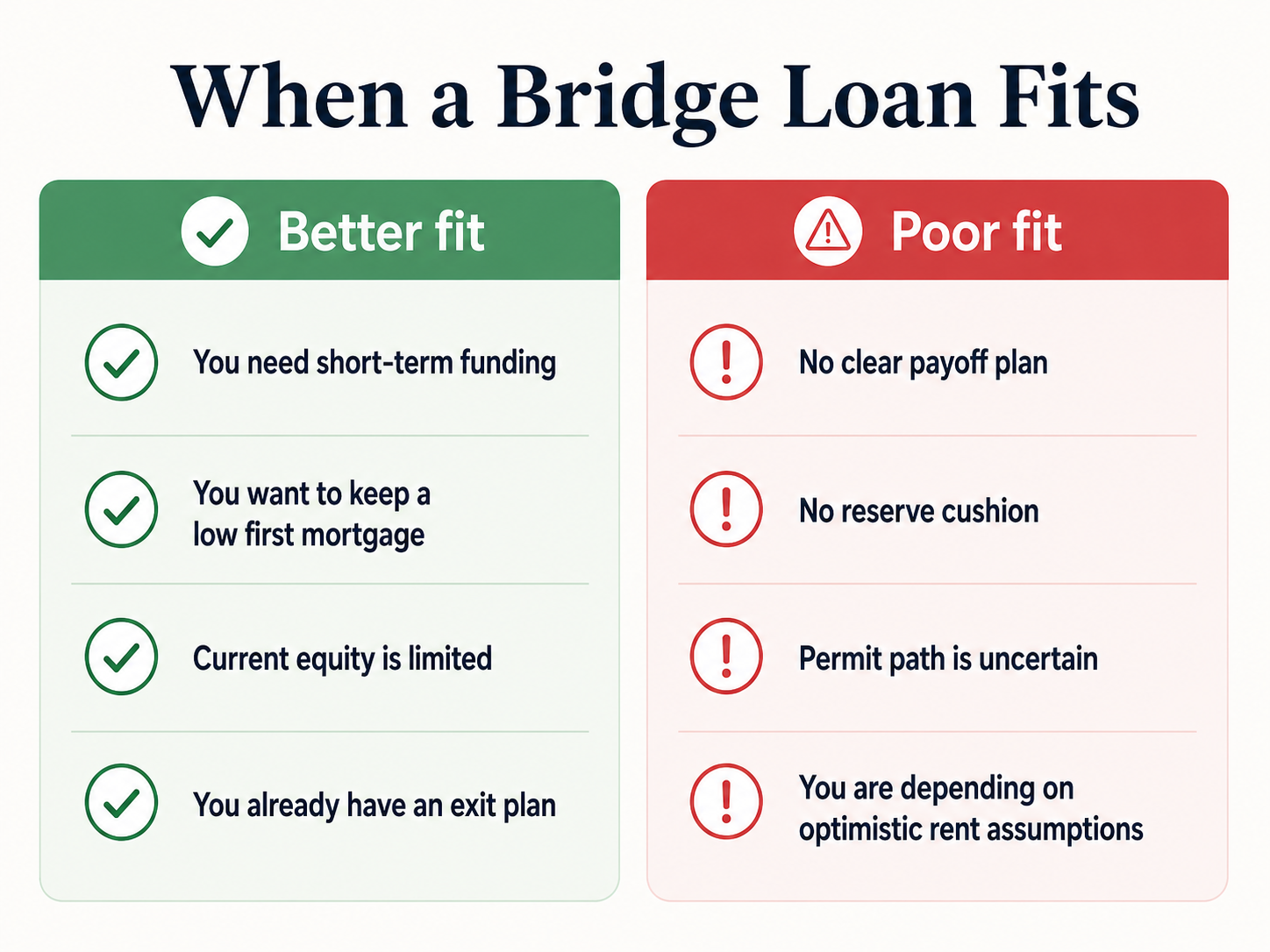

Fit matrix: when a bridge loan actually fits an ADU project

A bridge loan fits an ADU project when at least one of the following is true: you are an investor on a non-owner-occupied property, you need to fund in days and not weeks, or you lack current equity but can support underwriting based on ARV. In all other cases, price the cheaper paths first.

| Scenario | Bridge loan fit | Why | Better alternative if one exists |

|---|---|---|---|

| Investor, non-owner-occupied, no meaningful equity, need to build fast | Strong fit | Bridge is one of the few products that lends on investor rental property against ARV | DSCR construction or local program |

| Owner-occupant, time-sensitive deal, HELOC too slow | Conditional fit | Speed justifies cost only if the timeline truly cannot wait | HELOC or HomeStyle if timeline allows |

| Owner-occupant with solid equity, 30+ days available | Wrong tool | HELOC or renovation loan will cost 3–5x less over the same period | HELOC, HomeStyle, CHOICERenovation, or FHA 203(k) |

| Massachusetts owner-occupant, income-eligible | Wrong tool | MassHousing ADULP (active, up to $250k, lower cost) is almost always cheaper | MassHousing ADULP |

| No exit plan identified yet | Stop | The exit plan is the underwriting — signing without one is the most common bridge loan failure | Any permanent product |

Confirm what you can legally build before you price any loan.

What does an ADU bridge loan cost in 2026?

Bridge loan carry is the highest of any ADU financing path. The all-in cost includes the interest rate, origination points, closing costs, monthly inspection fees (if draws are inspection-tied), and potential extension fees if construction runs long. On a $300,000 12-month bridge at 11% with 2 points and 2.5% closing costs, the total carry before refinance costs is approximately $48,500.

Published 2026 pricing ranges from verified lender sources

- •Interest rate: 9%–13.5% interest-only (Kiavi: 9.75%–13.5%; Capital Direct Funding California: 9.5%–10.95% as of March 2026)

- •Origination points: 1.5–3% of loan amount (SnapADU investor program: 2%, minimum $10,000)

- •Closing costs: 1–3% of loan amount (title, escrow, appraisal, inspections, doc prep)

- •Extension fees: 1–2 points per extension; most products allow up to two extensions

- •Draw inspection fees: $150–$300 per inspection; some lenders tie every construction draw to a site visit

- •Minimum interest / prepayment: Some lenders require minimum-interest guarantees of 3–6 months even if you repay early

Three worked examples at 2026 rates

| Scenario | Loan amount | Rate / term | Total carry (12 mo) |

|---|---|---|---|

| Investor, detached ADU, non-owner-occupied SFR | $200,000 | 11%, 12-month, 2 pts | ~$30,000 |

| California investor, full ground-up ADU, 80% LTC | $350,000 | 10.5%, 12-month, 2 pts | ~$49,750 |

| Owner-occupant, 2nd-lien bridge, behind low-rate 1st mortgage | $500,000 | 12%, 18-month, 2.5 pts + 1 extension | ~$108,500 |

Illustrative examples based on published 2026 lender pricing. Actual costs depend on borrower, property, lender, and state. Not a loan quote.

Who qualifies for an ADU bridge loan?

Bridge loan qualification is primarily asset-based, not income-based — which is both the attraction and the trap. The lender underwrites the collateral first and the borrower second. But liquidity matters more than income: lenders want to see enough reserves to carry the loan through construction and into the refinance window.

Tier 1 — institutional bridge lenders (national)

Kiavi (formerly LendingHome): Up to 100% LTC on construction, 80% ARV, max $3M; SFR and 2–4 unit non-owner occupied; minimum FICO typically 660+; rates 9.75%–13.5%; 12–24 month terms. RCN Capital: up to 100% purchase plus 100% rehab not to exceed 75% ARV; SFR, 2–4 unit, 5–20 unit residential; minimum FICO 660; 12–18 month terms. Stormfield Capital: 70–80% ARV; SFR, multifamily, commercial; minimum FICO 640; 6–24 month terms. AHL (American Heritage Lending): SFR and multifamily; 65–75% ARV; fix-and-flip and new construction products; FICO as low as 620 on strong collateral.

Tier 2 — regional and private lenders

Capital Direct Funding (California): Published rates 9.5%–10.95% as of March 2026; 1–2 points; 6–24 month terms; first and second position available. Regional and private lenders in California, Texas, Florida, Arizona, and the Northeast corridor make up the bulk of the non-institutional market and are often willing to underwrite unusual ADU configurations that institutional lenders decline.

Tier 3 — builder-affiliated programs (geo-restricted)

SnapADU investor program (Greater San Diego / San Diego County): 80% LTC; 12-month term plus 3-month extension; interest-only; 2% origination ($10,000 minimum); permits required in hand before funding; personal guaranty required; minimum FICO 720. SnapADU notes it is not a licensed financial advisor or lender and connects customers with lending partners.

The disqualifier most borrowers underestimate: liquidity

Most bridge lenders want to see 6–12 months of debt service in liquid reserves after closing, plus a construction contingency of 15–20% of the project budget. If you are funding the project from proceeds of the bridge loan with no separate cash reserve, most serious lenders will pass.

When a bridge lender will say no

- •ADU is not legally permissible at this address or is already built without permits

- •Property is in a jurisdiction where ADUs were recently legalized and comparables are absent

- •FICO below 640 with no compensating collateral strength

- •No liquidity reserve post-close

- •ARV does not support the loan amount requested

- •No identified exit strategy or a strategy that the lender cannot verify

- •Lender is not licensed in your state for this loan type

Not sure the bridge loan is right for your situation?

Explore Mortgage-Backed ADU Financing Options →Partner link — we may earn a commission at no cost to you.

The exit strategy — refinancing your bridge loan into permanent financing

The exit strategy is the most important part of the bridge loan, full stop. The three viable exits are (1) refinance into a DSCR loan once the ADU has 3–6 months of seasoned rent, (2) refinance into a conventional, FHA, or cash-out loan once the property re-appraises and you re-qualify on personal income, or (3) sell the property. The most common reason bridge loans default or extend is not interest rates rising — it is borrowers who could not refinance because their ARV came in low, their rent did not season fast enough, or their DSCR ratio did not clear 1.0–1.25x. The exit is not a future task. It is the underwriting.

The six exit paths, ranked by feasibility

| Exit path | Best fit | Verified rule or evidence | Practical risk |

|---|---|---|---|

| Refinance into a DSCR loan | Investor with stabilized rental ADU | DSCR loans qualify on property cash flow, not personal income. Industry standard is 1.0–1.25x minimum coverage. Most DSCR lenders require 3–6 months of seasoned rent before approval. | If projected rent overshoots actual market rent, the DSCR ratio fails. ADU must be legally permitted and rentable. |

| Refinance into Freddie Mac CHOICERenovation (no-cash-out) | Owner needing a formal takeout for short-term ADU renovation financing | Freddie Mac's published ADU fact sheet states CHOICERenovation provides an option to use a no-cash-out refinance to pay off short-term financing that financed ADU renovations. Applies to 1-, 2-, and 3-unit properties. | Requires Freddie/lender eligibility, zoning status, completion timing, and appraisal support. When ADU rental income is used to qualify, Sales Comparison Approach must include at least one comparable sale with an ADU; ACE not acceptable. |

| Refinance into Fannie Mae HomeStyle Renovation | Owner willing to use a renovation mortgage with as-completed value | Fannie Mae HomeStyle Renovation finances renovation costs based on as-completed value. 2026 conforming loan limit baseline: $832,750 (one unit); high-cost ceiling: $1,249,125. | Lender overlays, draw control, contractor approval, and as-completed appraisal all matter. Not casual gap money. |

| Cash-out refinance into a conventional loan | Owner with strong income, willing to replace the first mortgage | Standard 80% LTV cap on the new loan. Works best when current first-mortgage rate is at or above today's market. | Sacrifices a low pandemic-era first mortgage rate. FHA cash-out specifically cannot use ADU rental income to qualify per HUD Mortgagee Letter 2023-17. |

| Refinance into an FHA 203(k) | Specific ADU work that fits HUD's published eligible categories | HUD Mortgagee Letter 2023-17 lists eligible improvements including converting a one-family structure to include an ADU, adding an attached ADU, and renovating an existing ADU. 2026 FHA one-unit floor $541,287, ceiling $1,249,125. | Not universal for ground-up detached ADUs. Verify with an FHA lender before treating 203(k) as the takeout. When ADU rental income is used to qualify, mortgagee must verify two months' PITI in reserves after closing. |

| Sell the property | Investor exit, downsizer with completed ADU adding value | Direct payoff from sale proceeds. Often cleaner than refinance when the market is active. | Time on market, capital-gains exposure, transaction costs typically 5–7% of sale price. |

Verified May 20, 2026. Sources: Freddie Mac single-family ADU page and ADU fact sheet; Fannie Mae HomeStyle Renovation product page; HUD Mortgagee Letter 2023-17; FHFA 2026 loan limits.

Why most exits fail — the three patterns we keep seeing

1. Overestimated stabilized rent

A borrower projects $3,000/month rent based on Zillow's median. The actual lease comes in at $2,400. At a 1.25x DSCR threshold, that $600/month gap drops the maximum supportable mortgage by roughly $90,000–$110,000. The refinance amount you need is the refinance amount you cannot get. The fix: pull actual lease comparables for ADUs within 1–2 miles before signing the bridge note, and underwrite at the 25th percentile of that data — not the median.

2. Late rental seasoning

Most DSCR lenders want to see 3–6 months of bank deposits showing rent received. A borrower whose ADU receives its Certificate of Occupancy in month 9 of a 12-month bridge loan does not have time to season rent before the balloon. The fix: pre-lease before CO if local rules allow, or start the DSCR refinance application at month 4–6, not month 10.

3. ARV miss on the appraisal

ADU comparables are still thin in many markets. An appraiser who cannot find recent ADU sales nearby will lean on per-square-foot averages, which often come in 10–15% below builder marketing. The fix: order a pre-construction appraisal with the same lender's appraiser before locking the bridge loan, and design the project to the appraisal's number — not to the contractor's “what's possible” number.

Stress-testing your exit before you sign

Before signing any bridge loan, run the exit math under three scenarios:

- Base:Construction completes on time, ARV hits projection, rent leases at the median you assumed.

- Stress:Construction takes 3 months longer than the bid, ARV comes in 10% below projection, rent leases at the 25th percentile.

- Disaster:Construction runs 6 months long, ARV comes in 15% below projection, you cannot find a tenant for 60 days.

If the stress case still results in a successful refinance — even at a higher rate or with a 6-month bridge extension — the deal is signable. If the stress case results in a foreclosure, the deal is not signable at the size you are considering. Reduce the scope, increase the down payment, or wait.

Before you sign a bridge note, test the exit plan on your actual numbers — not the seller's pitch.

Download the Exit Worksheet + ADU Starter Kit →Free — includes DSCR exit math worksheet and full ADU financing checklist.

Can ADU rental income help you qualify for the takeout loan?

Sometimes, with caps and conditions. Fannie Mae allows rental income from an existing ADU only — on a one-unit principal residence, from only one ADU, on purchase or limited cash-out refinance transactions, capped at 30% of total qualifying income (Selling Guide B3-3.8-01; DU 12.1 automates the calculation, effective March 21, 2026). Freddie Mac caps documented ADU rental income at 75% of lease amount, requires qualifying rental income to stay within 30% of total qualifying income, and prohibits use of rental income from an illegal ADU. FHA caps ADU rental income used as effective income at 30% of total monthly effective income, requires two months' PITI in reserves after closing when ADU rental income is used to qualify a one-unit with ADU, and prohibits use of ADU rental income to qualify for an FHA cash-out refinance.

| Program | Can ADU rent count? | Cap and conditions | Bridge-loan relevance |

|---|---|---|---|

| Fannie Mae (conventional) | Yes — existing ADU on one-unit principal residence only; purchase or limited cash-out refinance only | Capped at 30% of total qualifying income (B3-3.8-01) | Strong takeout option when ADU rental income matters to qualification — only after ADU exists and is occupied |

| Freddie Mac (CHOICERenovation) | Yes — 1-, 2-, and 3-unit properties with ADUs; documented rental income ≤75% of lease; rental from illegal ADU excluded | Qualifying rental income capped at 30% of total qualifying income; appraisal required (ACE not acceptable) | CHOICERenovation no-cash-out refinance is the only conforming product specifically designed to pay off short-term ADU financing |

| FHA 203(k) and standard | Yes — for ADUs meeting HUD's ADU definition under Mortgagee Letter 2023-17 | ADU rental income capped at 30% of total monthly effective income; two months' PITI in reserves required; cannot use ADU rent for FHA cash-out | Useful for specific eligible-improvement categories — attaching an ADU, renovating existing ADU |

| DSCR (non-agency, investor) | The property's rental income is the entire qualification — personal income not required | Industry standard 1.0–1.25x DSCR; some lenders accept down to 0.75x at higher cost | Most common exit for investor bridge loans |

Sources: Fannie Mae Selling Guide B3-3.8-01; Freddie Mac ADU fact sheet and single-family ADU page; HUD Mortgagee Letter 2023-17. Last verified May 20, 2026.

What can go wrong — the five risks nobody quotes you

The five risks every ADU bridge loan borrower should price in: balloon-at-maturity risk if the takeout does not close, extension fees if construction runs late (typical 1–2 points per extension), draw-inspection delays that stall the build, cost of capital that materially exceeds any other ADU financing path, and limited consumer protections compared to a CFPB-regulated mortgage on business-purpose loans. The most common failure is not the rate. It is the calendar.

1. Construction takes longer than the loan term

A “12-month” bridge product is built on the assumption that construction finishes in 8–9 months. For owner-occupied detached ADUs, the realistic timeline from groundbreak to Certificate of Occupancy is closer to 9–14 months when nothing goes wrong, and California ADU permit review timing varies by jurisdiction and submittal completeness. Permit re-checks, inspection re-checks, weather, and supply-chain issues compound. Build your bridge term and reserves around a realistic timeline, not the contractor's optimistic one.

2. The appraisal does not support the payoff

ADU appraisal comparables are still thin in many markets. An appraiser without enough recent ADU sales will rely on per-square-foot averages that often come in 10–15% below builder marketing. The fix: underwrite your own deal at a lower ARV than the contractor's pro forma — and lock the bridge loan based on the conservative number.

3. The ADU is not legal or rentable when you need to refinance

Freddie Mac's published rule is explicit: rental income from an illegal ADU may not be used to qualify. If the ADU was built without permits, built over-size, built outside required setbacks, or fails final inspection, you cannot count the rent for the takeout. Only build to permits, do not “build first, permit later,” and treat every inspection as non-negotiable. For the regulations in your specific jurisdiction, see our California ADU laws guide.

4. You are building on someone else's property

If you finance and build a structure on property you do not own, the structure becomes the property owner's — not yours. Loan documents, ownership agreements, and intra-family lease arrangements need to be reviewed by an attorney and a tax advisor before any bridge loan is signed. This is one of the few situations where we tell readers to stop the loan process entirely until the legal structure is clean.

5. The consumer-protection gap on business-purpose loans

A bridge loan made primarily for business purposes is generally outside the consumer-purpose disclosure framework that applies to many residential mortgages. The standard Loan Estimate, Closing Disclosure, and three-day right of rescission may not apply. The lender determines the loan's primary purpose case by case, and owner-occupied ADU financing can be treated differently than non-owner-occupied investor financing. Read the loan documents in full and have an attorney review them if you are unsure which framework applies to your specific loan.

These are illustrative risk scenarios, not guarantees of outcomes. Actual loan terms, eligibility, and risks vary by lender, property, and state. The Dwelling Index is not a lender, broker, or attorney. Consult a licensed professional before signing any loan document.

The risk profile sounds heavier than it is — provided your property and project are solid.

Run the Free Property Check (2 Minutes) →Before pricing any loan, confirm what you can legally build at your address.

What should I use instead of a bridge loan for an ADU?

The umbrella ADU financing decision has eight paths. A bridge loan wins on only three dimensions: speed, willingness to underwrite against future value instead of current equity, and willingness to lend on non-owner-occupied investment property. On every other dimension — cost of capital, payment predictability, ease of qualification, prepayment flexibility, consumer protection — at least one of the other seven paths beats it. Test the cheaper paths first.

We have a separate How to Finance an ADU in 2026: 7 Paths Compared guide that covers the other seven paths in depth.

Bridge loan vs HELOC

A HELOC wins for most owner-occupied homeowners with meaningful equity. National HELOC pricing typically runs well below private-bridge rates because it is secured by current-value equity rather than future-value underwriting. The HELOC preserves your existing first mortgage. The draw structure aligns naturally with phased construction draws. You only pay interest on what you have drawn. A HELOC loses when you do not have enough equity, when the lender will not lend on a non-owner-occupied rental, or when you need same-week funding. See our HELOC for ADU guide for full qualification thresholds.

Bridge loan vs cash-out refinance

A cash-out refinance wins when your current first-mortgage rate is already at or above today's market rate and you have enough current-value equity. It loses when your current rate is below today's market — refinancing means giving up that rate forever. It also loses on speed: a cash-out refinance closes in 30–60 days, not 7–21.

Bridge loan vs construction-to-permanent loan

A construction-to-perm wins for ground-up new construction with strong income but limited current equity. It uses as-completed value, releases funds on milestone draws, and converts to a permanent mortgage at completion — eliminating the refinance risk that is the biggest weakness of a bridge loan. It loses on speed (45–90 day closings typical) and on flexibility.

Bridge loan vs Fannie HomeStyle, Freddie CHOICERenovation, and FHA 203(k)

These three renovation mortgage programs underwrite against as-completed value, like a bridge loan, but they are single-close permanent products — no refinance risk. HomeStyle's renovation cost is capped relative to as-completed value. CHOICERenovation's no-cash-out refinance is specifically designed to pay off short-term ADU financing. FHA 203(k) covers attached ADUs, conversions, and existing ADU renovations per HUD Mortgagee Letter 2023-17. They lose on speed and lender availability.

Bridge loan vs local programs and grants

Local and state ADU programs can be the cheapest path of all when they exist and you qualify:

- •CalHFA ADU Grant: The latest funding round was fully allocated on December 28, 2023, and the reservation portal is closed. (Verified May 20, 2026.)

- •MassHousing ADULP: Active — up to $250,000 for detached ADUs, up to $150,000 for attached ADUs; income-qualified owner-occupants; participating lenders only. Verified at masshousing.com May 20, 2026.

If you qualify for a state-backed program, the bridge loan is almost always the wrong path. Massachusetts owner-occupants in particular should price MassHousing ADULP before pricing any bridge loan.

The 8-path quick-compare

| Path | Cost of capital | Speed to fund | Equity required | Refinance risk |

|---|---|---|---|---|

| HELOC | Low | 3–6 weeks | High | Low |

| Home equity loan | Low | 3–6 weeks | High | None |

| Cash-out refinance | Low–Medium | 30–60 days | High | None (single-close) |

| Construction-to-perm | Medium | 45–90 days | Low–Medium | None (single-close) |

| Renovation loan (HomeStyle / CHOICE / 203k) | Low–Medium | 45–60 days | Low | None (single-close) |

| Local program / grant | Lowest when available | Varies | Varies | Varies |

| Home Equity Investment (HEI) | None monthly; appreciation share at exit | Medium | Some | None |

| Bridge loan | Highest of the eight | Fastest (7–21 days) | Low / none (ARV) | High — balloon at maturity |

How to vet a bridge loan lender — the 9-point checklist

The bridge loan market includes lenders who tell you exactly what they will and will not do, and lenders who promise speed and ghost you at week three. Before signing, verify nine things: rate structure, full fee load, prepayment policy, extension policy, draw control, LTV basis, take-out partnership availability, ADU-specific loan volume, and lien position.

- 1Is the rate fixed or floating? Floating rates tied to SOFR plus a spread typically have a SOFR floor. Know the floor.

- 2What is the full point-and-fee load? Itemize origination, underwriting, processing, document prep, title, escrow, appraisal, inspections, and funds control.

- 3What is the prepayment penalty or minimum-interest guarantee? A 6-month minimum-interest guarantee adds significant cost if you refinance fast.

- 4What is the extension policy? Maximum number of extensions, points per extension, rate during extension.

- 5Does the lender control draws and require inspections? Inspection-tied draws are slower but safer.

- 6Is LTV based on current value, ARV, or LTC? Each gives a different maximum loan amount. Compare apples to apples across lenders.

- 7Does the lender have a take-out partner or are you on your own at refinance? Lenders who originate both the bridge and the DSCR refinance reduce execution risk.

- 8How many ADU-specific bridge loans has the lender closed in the last 12 months? Generic bridge experience is not ADU experience. ADU appraisal, permit, and CO timing are specific.

- 9Is the loan first-lien or second-lien on the property? Second-lien bridge loans behind a low-rate first mortgage are common for owner-occupied ADU builds. The CLTV cap and intercreditor terms matter.

Red flags to watch for in bridge loan offer materials

- ⚠“Same-day approval” without any underwriting on file

- ⚠Vague fee disclosure or “all-in” rate quoted without itemization

- ⚠No written extension policy

- ⚠No clear chain of communication after the offer is accepted

- ⚠Loan officer who cannot answer ADU-specific underwriting questions

- ⚠Personal guaranty required on an investor entity loan without explanation

- ⚠A take-out commitment that depends on rate assumptions the lender will not disclose

State-specific notes for ADU bridge loans

Bridge loan availability and pricing vary by state. California has the deepest ADU bridge market driven by Government Code §§ 66310–66342 and high ADU volume. Massachusetts homeowners now have a state-backed alternative through MassHousing's active ADULP. Texas ADU permissibility still depends on local jurisdiction. Verify the specific state and city rules for your build before signing any loan.

California

California has the densest bridge loan market in the country, with both institutional and private lenders actively writing ADU bridge product. Capital Direct Funding's published California bridge rates ran 9.5–10.95% in March 2026. California's ADU framework is codified in Government Code §§ 66310–66342, per the 2025 HCD ADU Handbook update. A compliant local ordinance must allow ADUs of at least 850 sq ft, or 1,000 sq ft for ADUs with more than one bedroom. CalHFA says the latest ADU Grant funding round was fully allocated on December 28, 2023; CalHFA warns consumers to contact the agency directly if anyone claims they can help obtain ADU Grant funds. Verify all California-specific claims against our California ADU laws guide.

Massachusetts

MassHousing's Accessory Dwelling Unit Loan Program (ADULP) is active as of May 2026. The product offers income-eligible owner-occupants up to $250,000 for detached ADUs and up to $150,000 for attached ADUs through participating lenders, combining an amortizing interest-bearing loan with zero-interest deferred-repayment financing. Eligibility requires owning and occupying a single-family home as primary residence, meeting income guidelines, and having all plans, permits, and pre-development materials in hand before applying. For income-eligible Massachusetts homeowners, ADULP is likely cheaper than any private bridge loan. Verify lender participation and current income limits at masshousing.com.

Texas

Active investor-bridge market — many of the national Tier 1 lenders (Kiavi, RCN Capital, Stormfield) lend in Texas on non-owner-occupied investment property. Texas is a non-judicial foreclosure state, which affects lender remedies. RenoFi explicitly does not lend in Texas, so the renovation-loan alternative is restricted to Fannie HomeStyle, Freddie CHOICERenovation, and FHA 203(k) routes via Texas-licensed lenders. Texas does not have a verified statewide ADU permissibility framework comparable to California's; ADU permissibility depends on local jurisdiction.

Other states

Bridge loans are offered by national and regional lenders in many states, but availability depends on lender licensing, property type, occupancy, lien position, loan purpose, and state law. Lender density is highest in California, Texas, Florida, Arizona, Colorado, and the Northeast corridor. Rural and lower-population states have fewer options and often require working with national institutional lenders licensed in your state.

After the ADU is built — managing the rental and the refinance

Once construction is complete and tenants are in, two clocks start running: the seasoning clock (most DSCR lenders want 3–6 months of documented rent before refinancing) and the bridge loan maturity clock. The gap between them is where defaults happen. Start your DSCR refinance application at month 4–6, not month 10.

The 12-month timeline from bridge close to DSCR refinance close

| Month | Action |

|---|---|

| 0 | Bridge loan funds. Construction begins. |

| 1–6 | Construction proceeds with milestone draws. Lender inspections at framing, mechanical, drywall, and finish. |

| 7 | Final inspection scheduled. Certificate of Occupancy submitted. |

| 8 | CO issued. Tenant marketing begins. Lease signed. |

| 8–9 | Tenant moves in. First month's rent collected. |

| 10 | DSCR refinance application submitted. New appraisal ordered. |

| 11 | Appraisal complete. Underwriting in progress. |

| 12 | DSCR refinance closes. Bridge loan repaid in full. |

This is the timeline when nothing goes wrong. Build a 60–90 day buffer between the projected DSCR refi close and the bridge maturity date to absorb appraisal delays, lender pipeline delays, or extra documentation requests.

Documentation to have ready at month 10

- •Permit set and approved drawings

- •Contractor agreement with line-item budget

- •Inspection records as construction proceeds

- •Final Certificate of Occupancy

- •Lease executed before refinance application

- •Rent deposit records (bank statements showing rent received)

- •Property insurance binder

- •Title commitment from the bridge close

- •Property tax records (the new assessment may take 12–24 months to update)

What should I verify before applying for an ADU bridge loan?

Verify three things in order: the property first, the project second, and the takeout loan third. If any one of those is uncertain, the bridge loan is not ready.

Checklist 1: Property verification

- ☐ADU is allowed by current zoning at this address

- ☐ADU type you want (detached, attached, garage conversion, JADU) is permitted

- ☐Setback requirements decoded for your specific lot

- ☐Parking requirements understood

- ☐Utility connection paths and costs estimated

- ☐Fire access and emergency egress requirements clear

- ☐HOA restrictions reviewed if applicable

- ☐Owner-occupancy requirements (if any) understood

- ☐Short-term rental restrictions checked (for rental scenarios)

- ☐Permit path (ministerial vs. discretionary) confirmed with your jurisdiction

- ☐Impact fees, school fees, and utility connection fees quoted

Checklist 2: Project verification

- ☐Architectural plans complete

- ☐Contractor bid received with line-item costs

- ☐Draw schedule defined

- ☐Construction contingency reserved (we recommend 15–20% of total budget)

- ☐Permit status confirmed (in-process or approved)

- ☐Expected inspection milestones mapped

- ☐Realistic completion timeline (pad the contractor's number by 30–60 days)

- ☐Certificate of Occupancy requirement understood

- ☐Prefab deposit and refund terms reviewed (if applicable)

Checklist 3: Financing verification

- ☐Current first-mortgage balance and rate documented

- ☐Current property value supported by recent comparables

- ☐Willingness or unwillingness to refinance the first mortgage decided

- ☐Intended bridge loan payoff path identified (DSCR, conventional, HomeStyle, CHOICERenovation, 203(k), or sale)

- ☐Written feedback from a take-out lender (pre-approval letter or term sheet)

- ☐Appraisal assumptions tested

- ☐Rental income assumptions tested (what does Form 1007 or Form 1000 show for comparables?)

- ☐Liquidity reserve confirmed (6–12 months of debt service plus 15–20% project contingency)

- ☐Legal review completed if family property is involved

- ☐Tax advisor consulted on deductibility of interest and depreciation strategy

Frequently asked questions about bridge loans for ADUs

What is a bridge loan for an ADU?

A bridge loan for an ADU is short-term financing — typically 6 to 24 months, interest-only, secured by the property — used to fund accessory dwelling unit construction until the borrower repays through sale, refinance, or another permanent takeout. It is most often used when a HELOC, cash-out refinance, or construction-to-permanent loan will not work for the specific borrower or property.

Can you get a bridge loan to build an ADU with no equity?

Yes, but only on investor-style products underwritten against the after-completion value (ARV) rather than existing equity. Kiavi advertises up to 100% loan-to-cost and 80% ARV; RCN Capital advertises up to 100% purchase plus 100% rehab not to exceed 75% ARV. Owner-occupied no-equity bridge loans are rarer and typically come from builder-affiliated programs or specialty private lenders.

What is the minimum credit score for an ADU bridge loan?

Most institutional bridge lenders set 660–680 as a minimum. Some private/hard-money lenders go lower with strong collateral; some advertise no FICO floor. Builder-affiliated programs can be stricter — SnapADU's published investor bridge example requires a minimum FICO score of 720.

How long does it take to close a bridge loan for an ADU?

Typical funding is 7–21 days. The fastest closings — under 7 days — come from private/hard-money lenders or institutional lenders with pre-approved borrowers. Builder-affiliated bridge products coordinate with the construction schedule rather than competing on speed.

Can I get a bridge loan on a rental property to add an ADU?

Yes — non-owner-occupied investment property is the most common bridge loan scenario. Most institutional bridge lenders (Kiavi, RCN Capital, Stormfield, AHL) lend almost exclusively on non-owner-occupied 1–4 unit residential. Owner-occupied bridge products are a smaller niche.

What is the difference between a bridge loan and a construction loan for an ADU?

A construction loan funds new construction in draws based on as-completed value, typically over 12–24 months, and often converts automatically to a permanent mortgage at completion (a one-time-close construction-to-perm). A bridge loan is purely short-term and requires a separate refinance to pay off the balloon at maturity. Construction loans typically have lower rates and stricter underwriting; bridge loans have higher rates and faster funding.

What is the difference between a bridge loan and a hard money loan for an ADU?

The products overlap. Hard money and private money describe asset-based short-term loans from private lenders, usually at higher rates. Bridge loan describes the same structure but can come from institutional or private lenders. In practice, hard money loans tend to lend on more distressed property at higher cost, while bridge loans tend to lend on cleaner properties at slightly lower cost. The line between them is fuzzy.

Can I refinance an ADU bridge loan into a DSCR loan?

Yes — this is the standard investor exit. Most DSCR lenders require 3–6 months of seasoned rent and a 1.0–1.25x debt service coverage ratio.

How much does an ADU bridge loan cost compared to a HELOC?

Materially more. A bridge loan at 11% with 2 points and 3% closing costs on a $300,000 12-month loan totals roughly $40,000 in carry plus refinance costs. A HELOC on the same amount typically costs a fraction of that across the same period. The cost difference funds the speed and the no-equity-required underwriting.

What happens if I cannot refinance out of my ADU bridge loan?

Three options: extend the bridge (1–2 points per extension, usually maximum two extensions), find a different take-out lender (DSCR if the property is rented, or a small private lender), or sell the property. Foreclosure is the worst-case outcome and happens most often when the borrower has no liquidity reserves, no rental income, and no buyer.

Are bridge loans for ADUs available in all 50 states?

Bridge loans are offered by national and regional lenders in many states, but availability depends on lender licensing, property type, occupancy, lien position, loan purpose, and state law. Lender density is highest in California, Texas, Florida, Arizona, Colorado, and the Northeast corridor.

Can I use a bridge loan to convert my garage into an ADU?

Yes — garage conversions are eligible bridge loan projects on most lender products. Some ADU conversion projects can also fit FHA 203(k). HUD's ADU update under Mortgagee Letter 2023-17 includes converting a one-family structure to include an ADU, adding an attached ADU, and renovating an existing attached or unattached ADU. Verify a detached garage conversion or ground-up detached ADU with an FHA lender before treating 203(k) as the takeout.

Will building an ADU with a bridge loan increase my property taxes?

Building an ADU can trigger a new property-tax assessment or a reassessment of the improvement, depending on state and county rules. In California, new construction is generally assessed separately from the existing property basis under Proposition 13 rules; outside California, verify with the county assessor. Budget for it.

Is bridge loan interest tax-deductible on an ADU build?

Tax treatment depends on whether the ADU is personal-use, rental, mixed-use, owner-occupied, or investment property. Keep records and consult a CPA before assuming bridge-loan interest is deductible — we are not a tax advisor.

Do I need an LLC to get an ADU bridge loan?

Not always. Most institutional bridge lenders require investor loans to be made to a business entity (LLC, corporation, or partnership). Some accept individual borrowers; private/hard money lenders are often more flexible. Owner-occupied bridge loans usually do not require an entity.

Can the bridge loan cover both the ADU construction and a property purchase?

Yes on some products. Kiavi and RCN Capital both offer combined acquisition-plus-rehab bridge structures. Document the strategy clearly in the loan application.

Should I trust builder-arranged bridge financing?

Review it independently before signing. A builder may understand construction, but the financing still has to make sense for your repayment timeline, exit strategy, and legal position. Read the loan documents, run the exit math yourself, and have an attorney review if anything is unclear.

How we researched this guide

This guide was built by comparing official agency guidance from CFPB, Fannie Mae, Freddie Mac, HUD/FHA, and FHFA against published lender pricing, public ADU bridge loan examples, and the experience patterns documented across the dwellingindex.com financing library. Editorial conclusions are based on verified rules and documented risks, not on compensation.

Our source review covered ten institutional and private bridge-loan publications (Kiavi, RCN Capital, Stormfield Capital, AHL, Capital Direct Funding, Vaster, Clearhouse Lending, Arbitrust, Bankrate, Quicken/Rocket) and five ADU-specific bridge sources (HCS Equity, Mortgage Vintage, SnapADU, Valor Lending, TaliMar Financial), published between January and April 2026.

Primary sources verified:

- • Fannie Mae Selling Guide B3-3.8-01 and HomeStyle Renovation product page

- • Freddie Mac CHOICERenovation fact sheet and single-family ADU page

- • HUD Mortgagee Letter 2023-17 (ADU rental income, property eligibility)

- • FHFA conforming loan limit announcement of November 25, 2025

- • HUD 2026 FHA loan limits announcement

- • CFPB Regulation X §1024.5 (RESPA coverage and exemptions)

- • MassHousing Accessory Dwelling Unit Loan Program page

- • CalHFA ADU Grant page (program status)

- • California 2025 HCD ADU Handbook update (Gov. Code §§ 66310–66342)

Update cadence: Quarterly review of all rate ranges, federal underwriting rules, and state program status. Annual review at FHFA and FHA loan-limit announcements (November/December).

Financial disclaimer: This article is for educational purposes only and is not financial, legal, tax, or lending advice. Loan availability, eligibility, costs, and approval depend on the borrower, property, lender, state, and program rules. Do not take short-term financing for an ADU without reviewing the payoff plan, loan documents, and property-specific risks with qualified professionals.

Illustrative-returns disclaimer: Any rental-income or ROI examples on this page are illustrative only and not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Where to go next on The Dwelling Index

- → Property Eligibility Check — confirm what you can legally build before you finance

- → How to Finance an ADU in 2026: 7 Paths Compared — the umbrella view across all financing paths

- → HELOC for ADU — the path most owner-occupants actually qualify for

- → ADU Rental Income Calculator — model the rent side before signing the bridge

- → How Much Does an ADU Cost? — set the project budget the bridge loan will fund

- → ADU Construction Loan Guide — the lower-cost alternative for ground-up new builds

Not sure where to start? See what's possible at your address — get your free ADU report in 60 seconds.

Check My Property →