ADU Rental Income: How Much Can You Actually Make?

By The Dwelling Index Editorial Team · Last verified: April 2026 · Sources: HUD, Fannie Mae, Freddie Mac, FHA, IRS

Here's the bottom line on ADU rental income: a well-located, permitted accessory dwelling unit earns most homeowners between $1,000 and $3,000 per month in gross long-term rent — and roughly $800 to $2,200 per month after real operating expenses. A typical 600 sq ft detached unit pulls roughly $1,500–$2,000/mo nationally, with higher-cost metros pushing well above that. Those are real numbers, not marketing brochures.

But gross rent is not your income. After property taxes, insurance, maintenance, vacancy, and the occasional broken water heater, the gap between what you collect and what you keep is meaningful. The math still works for most homeowners — if you understand the full picture before you commit.

What makes this moment different: Fannie Mae announced a policy in October 2025 allowing eligible borrowers to count ADU rental income toward mortgage qualification — capped at 30% of total qualifying income, with specific documentation requirements. Freddie Mac and FHA have their own versions of this rule. That changes the financing math for a lot of homeowners.

Below, we break down exactly what an ADU can realistically earn, what eats into that income, how lenders treat it, how the IRS treats it, and what local rules can change the entire picture.

Jump to a section: Rent by market · Mortgage qualifying · Tax rules · Real scenarios · FAQ

A well-designed detached ADU with private outdoor space and modern finishes consistently rents above comparable apartments in the same ZIP code.

How much can an ADU rent for in your market?

National averages mislead. Your ADU's income depends on where it sits, what it looks like, and how you rent it. HUD publishes Fair Market Rent estimates for every county and metro area in the country — those represent the 40th percentile of gross rents (including utilities) paid by recent movers, and they give us a conservative floor to work from. (Source: HUD FY2026 FMR Documentation, effective Oct. 1, 2025.)

Here's what the real-world rent ranges look like by ADU type and size. These are illustrative ranges based on our internal research model, which combines HUD FMR baselines with rental platform data and builder-reported figures across multiple markets:

ADU Rental Income by Type and Size

| ADU Type | Typical Size | Monthly Gross Rent | After Expenses (Est. Net) |

|---|---|---|---|

| Studio / JADU | 300–500 sq ft | $800–$1,500 | $600–$1,100 |

| 1-Bedroom Detached | 500–750 sq ft | $1,200–$2,500 | $900–$1,900 |

| 2-Bedroom Detached | 750–1,000 sq ft | $1,800–$3,500 | $1,400–$2,700 |

| Garage Conversion | 400–600 sq ft | $1,000–$1,800 | $800–$1,400 |

| Basement Conversion | 500–800 sq ft | $1,000–$2,000 | $800–$1,600 |

| Above-Garage Unit | 500–700 sq ft | $1,200–$2,200 | $900–$1,700 |

Net estimates assume operating expenses of roughly 20–30% of gross rent, consistent with typical residential rental operations. These are illustrative ranges from our internal model — not established market facts. Your actual rent depends on your specific location, finishes, and local market conditions. Sources: HUD FY2026 FMR/SAFMR data, Zillow rental listings, builder-reported data, Rentometer comps. Model last updated April 2026.

Those ranges are wide for a reason. A 1-bedroom detached ADU in San Diego commands substantially more than the same unit in a mid-size Midwest city. Location is the single biggest variable.

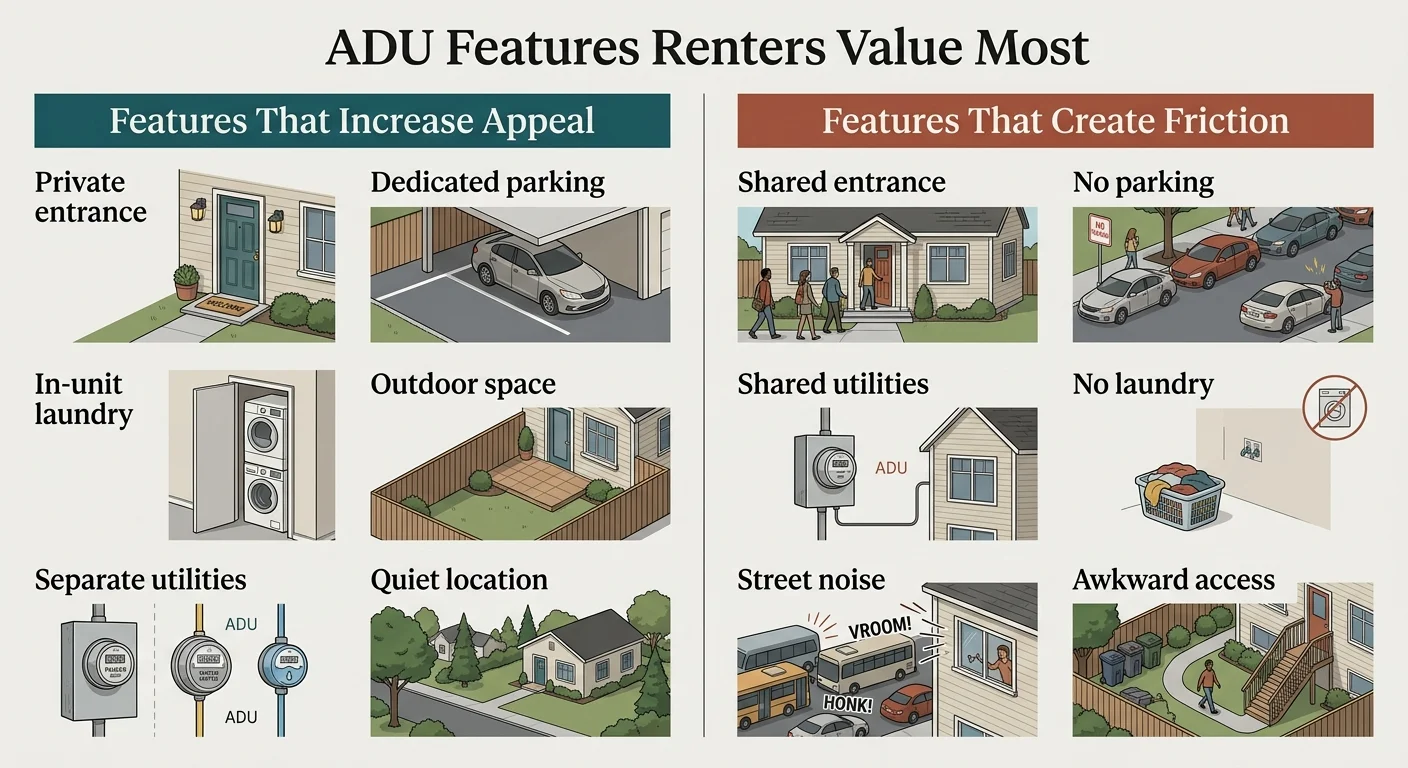

What Pushes Rent Up — and Down

It's not just square footage. ADU tenants pay premiums for specific features because they're choosing an ADU over a traditional apartment. The features that justify higher rent:

Private entrance, dedicated parking, and in-unit laundry are the top rent-boosting features — and each is achievable in a well-planned ADU.

Rent Boosters

- Private entrance

- Dedicated parking

- In-unit washer/dryer

- Outdoor space (patio or yard)

- New or modern finishes

- Separate utility meters

- Quiet/private location on lot

- Proximity to transit or job centers

Rent Killers

- Shared entrance with main house

- No parking

- Shared utilities, unclear billing

- Street noise

- Awkward lot access

- Visible construction shortcuts

A well-designed ADU with a private entrance, modern kitchen, and its own outdoor space consistently rents above comparable studio apartments in the same ZIP code. The privacy premium is real — renters will pay more for a backyard cottage than a unit where they share a hallway with their landlord.

Illustrative Rent by Metro Area

| Market | 1-BR ADU (Monthly) | 2-BR ADU (Monthly) |

|---|---|---|

| Los Angeles, CA | $2,000–$3,500 | $2,500–$5,000 |

| San Diego, CA | $1,900–$2,900 | $2,600–$3,700 |

| Bay Area, CA | $2,200–$3,500 | $2,800–$4,500 |

| Seattle, WA | $1,500–$2,300 | $1,900–$2,800 |

| Portland, OR | $1,200–$1,800 | $1,600–$2,400 |

| Denver, CO | $1,400–$1,900 | $1,800–$2,500 |

| Austin, TX | $1,100–$1,700 | $1,500–$2,200 |

| Salt Lake City, UT | $1,000–$1,500 | $1,400–$2,000 |

| Jacksonville, FL | $1,000–$1,500 | $1,300–$1,900 |

Illustrative ranges for long-term rental of permitted ADUs with standard finishes. Derived from our internal model using HUD FY2026 FMR/SAFMR data, Zillow, Rentometer, and builder-reported figures. Your results will vary. Model last updated April 2026.

One important note: HUD's Fair Market Rent represents the 40th percentile gross rent — meaning it includes utilities — paid by recent movers. It's designed to be conservative. Most well-built ADUs with modern finishes rent above FMR because they offer something apartments don't: privacy, outdoor space, and a neighborhood feel.

Want to see what your address can support? Get a free ADU report in 60 seconds.

Check your address in 60 seconds — free, no commitment.

Check My Property →Detailed reports available in CA, UT, TX, CO, and NY.

Why most ADU income projections are wrong (and what the real math looks like)

Here's the honest admission most ADU content won't make: the ROI numbers floating around the internet are often inflated. We see blogs claiming 15%, 25%, even 50% ROI on ADUs. Those numbers typically blend property appreciation with rental cash flow into a single figure, which makes the investment look dramatically better on paper than it performs in your bank account month-to-month.

That doesn't mean ADUs are bad investments — far from it. It means you need honest math to make a confident decision.

Cash-on-Cash Return — The Number That Actually Matters for Income

This tells you what your rental income produces relative to what you invested. It's the metric that answers "is this worth it as a rental?"

Formula: Annual Net Rental Income ÷ Total Cash Invested × 100

Illustrative Example

- Build cost: $200,000 (paid cash)

- Monthly gross rent: $1,800

- Monthly operating expenses: $450 (insurance, taxes, maintenance, vacancy reserve)

- Monthly net income: $1,350

- Annual net income: $16,200

- Cash-on-cash return: 8.1%

That's an honest, solid return — better than most bond yields and competitive with many stock market years. But it's not 25%. And knowing the real number lets you make a real decision.

Simple Payback Period — How Long Until Rental Income Covers the Build

Formula: Total Build Cost ÷ Annual Net Rental Income

Using the same numbers: $200,000 ÷ $16,200 = 12.3 years

That looks long on its own. But it doesn't account for what the ADU does to your property's value — and FHFA's California appraisal data shows meaningfully higher median appraised values for enterprise-backed single-family purchase appraisals with ADUs than for those without. That property value effect is real, even though the exact amount varies by market and project.

Why “Blended ROI” Claims Are Misleading

Many competitors use formulas that combine rental income with projected property appreciation into a single ROI figure. The result looks great — but property appreciation isn't realized until you sell or refinance. We keep these separate so you can evaluate each on its own terms and make a more grounded decision.

The right way to think about it: an ADU is a wealth-building tool with two engines — rental income and equity creation. Both matter. But you should understand each one separately before you combine them in your head.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, and regulatory approvals.

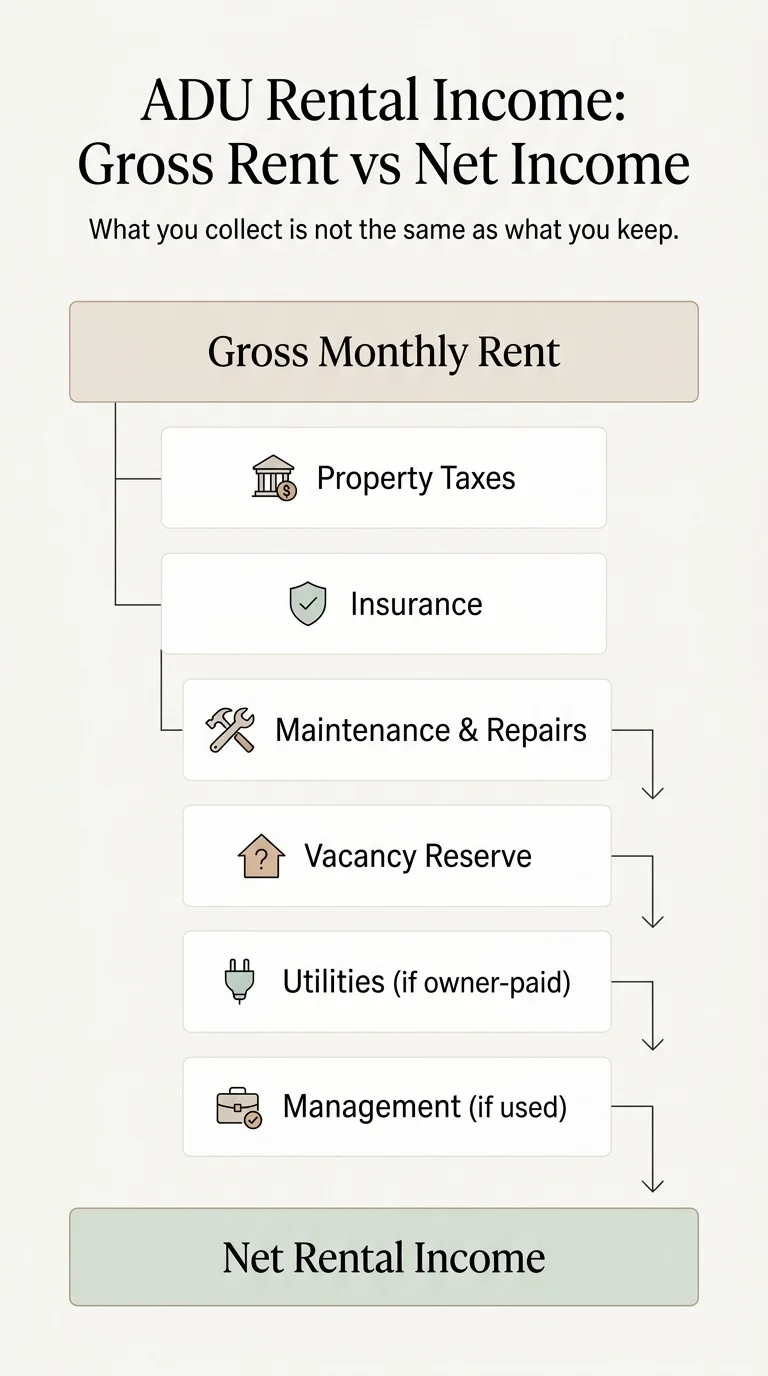

What are the real operating expenses for an ADU rental?

Gross rent is what you collect. Net income is what you keep. Understanding every expense category prevents ugly surprises.

Gross rent is vanity. Net income is sanity. Plan for roughly $300–$600 per month in total operating expenses for a typical ADU. Here's where the money goes:

ADU Operating Expense Breakdown

| Expense Category | Illustrative Monthly Cost | Notes |

|---|---|---|

| Property tax increase | $40–$150 | Assessed on ADU construction cost — not a full reassessment of your entire property. Varies by jurisdiction. |

| Landlord / rental insurance | $25–$75 | Separate rental dwelling policy or rider on homeowner's policy |

| Maintenance & repairs | $100–$250 | Budget 1–2% of ADU value annually; covers appliances, plumbing, HVAC, general upkeep |

| Vacancy reserve | $75–$150 | Set aside roughly 5% of gross rent. ADUs on owner-occupied properties tend to have low vacancy rates |

| Property management | $0–$200 | 8–12% of rent if using a manager. Many ADU owners self-manage — the unit is in your backyard |

| Utilities (if owner-paid) | $50–$150 | Depends on metering. Separate meters save long-term headaches |

| Total | $290–$975 | Most ADUs land in the $350–$550 range |

Illustrative ranges based on typical residential rental operations. Actual costs vary by jurisdiction, property, and management approach.

A word on vacancy: ADUs have a structural advantage here. Unlike a standalone rental property across town, an ADU on your property is easy to show, easy to manage, and appealing to tenants who want privacy without apartment living. When a unit combines a separate entrance, dedicated parking, and a neighborhood feel, quality tenants find it and stay.

Pro Tip

Separate your utility meters during construction. The upfront cost varies by location, but it eliminates the single most common landlord-tenant dispute — utility billing — and makes your rental income easier to document for mortgage qualifying.

Gross Rent vs. Net Income — Illustrative Scenarios

| Scenario | Monthly Gross Rent | Operating Expenses | Monthly Net Cash Flow | Annual Net Income |

|---|---|---|---|---|

| Garage conversion, mid-market | $1,300 | $320 | $980 | $11,760 |

| 1-BR detached, strong market | $2,200 | $480 | $1,720 | $20,640 |

| 2-BR detached, high-cost metro | $3,200 | $650 | $2,550 | $30,600 |

| Studio JADU, modest market | $900 | $250 | $650 | $7,800 |

Illustrative scenarios from our internal model. Your results will differ based on your location and specific costs.

Even the modest garage conversion scenario produces nearly $12,000 in annual net income. That's a mortgage offset, a retirement supplement, or a college fund — from a unit that sits in your own backyard.

Long-term vs. short-term vs. mid-term: which rental strategy makes more money?

Long-term rentals produce the most stable, qualification-friendly, and manageable income for the vast majority of ADU owners. Short-term rentals can earn more per night, but they come with significantly more work, higher expenses, and growing regulatory restrictions.

ADU Rental Strategy Comparison

| Factor | Long-Term (12+ mo) | Mid-Term (1–6 mo) | Short-Term (<30 days) |

|---|---|---|---|

| Monthly income potential | $1,000–$3,000 | $1,500–$4,000 | $2,500–$5,000+ |

| Income stability | Very high | High | Variable |

| Management effort | Low | Medium | High |

| Vacancy risk | Low | Moderate | Higher (seasonal) |

| Regulatory risk | Low | Low–Moderate | HIGH — many cities restrict or ban |

| Furnishing required? | No | Yes | Yes |

| Mortgage qualifying friendly? | Yes | Sometimes | Rarely |

| Best for | Stable passive income, hands-off owners | Hospital/university towns, corporate relocators | Tourist areas, hosts who enjoy hospitality |

Income ranges are illustrative and vary significantly by market.

Long-term rental is the default for good reason. Stable income, minimal turnover, lower expenses, and — critically — it's the cleanest path for mortgage qualification. Lenders want documented lease income, not fluctuating platform receipts.

Mid-term rental (30 days to 6 months) is the sleeper strategy. Traveling nurses, corporate relocators, visiting professors, and construction crews need furnished housing for weeks or months. You can typically charge above long-term rates, and turnover is manageable. If you're near a hospital, university, or corporate campus, this is worth serious consideration.

Short-term rental (Airbnb/VRBO) looks attractive on paper. Nightly rates are higher. But the reality: cleaning between guests, furnishing costs, platform fees, higher insurance, seasonal vacancies, and — most importantly — an accelerating wave of local regulations restricting or banning short-term ADU rentals. Short-term-rental rules vary sharply by city, and you should verify your local ordinance before underwriting Airbnb-style income.

Additionally, FHA underwriting guidance specifically excludes hotel-style or transient rental income (under 30 days) from ADU rent comparables used for qualification purposes. (Source: HUD Mortgagee Letter 2023-17.) Lenders want stable, documentable income.

Which strategy is right for you?

- →If you want simple, stable income with minimal involvement: long-term rental.

- →If you're near a hospital, university, or corporate center: mid-term furnished rental.

- →If you're in a tourist area AND your city explicitly allows it AND you enjoy hosting: short-term rental.

- →If your mortgage qualification depends on ADU income: long-term rental, documented with a lease.

Most homeowners land on long-term or mid-term — and that's usually the right call.

A detached ADU with separate entrance and professional landscaping attracts long-term tenants who value privacy — and commands top-of-market rents.

Can you use ADU rental income to qualify for a mortgage?

Yes — with conditions that matter. This is the section where most content online gets vague or outdated. We're going to get specific, because the rules are specific — and getting them wrong can derail a purchase or refinance.

As of 2025–2026, all three major mortgage agencies — Fannie Mae, Freddie Mac, and FHA — have pathways to count ADU rental income toward mortgage qualification. But none of them count 100% of projected rent, and each has its own documentation and eligibility requirements.

Fannie Mae ADU Rental Income Rules

Policy reference: Selling Guide SEL-2025-08, announced October 8, 2025. Lenders could implement immediately for eligible manually underwritten loans. Desktop Underwriter Version 12.1 added support in Q1 2026.

Eligible scenarios: Purchase or limited cash-out refinance of a one-unit, owner-occupied principal residence with an existing ADU.

Key requirements:

- Rental income from only one ADU, even if multiple ADUs exist on the property

- ADU income capped at 30% of the borrower's total qualifying income

- Lender calculates monthly market rent using Form 1007 (Single-Family Comparable Rent Schedule) or a current lease agreement

- When using market rent from Form 1007, only 75% of the estimated rent is used as qualifying income — this accounts for vacancy and maintenance

- All standard Selling Guide documentation requirements for rental income still apply

What This Means in Practice

Suppose you earn $7,000/month from your job. Your ADU rents for $2,000/month. After the 75% treatment, that's $1,500/month in qualifying income. The 30% cap on your total ($8,500 × 0.30 = $2,550) isn't binding here. So the full $1,500 counts. Your qualifying income rises from $7,000 to $8,500/month — potentially a meaningful boost to what you can borrow.

Not eligible for: Full cash-out refinances, second homes, or investment properties (for this specific ADU-income provision).

Source: Fannie Mae Selling Guide B3-3.1-08, B3-3.8-01. Verified April 2026.

Freddie Mac ADU Rental Income Rules

Policy reference: Freddie Mac Guide Chapter 5306, ADU Fact Sheet.

Eligible scenarios: Purchase or no-cash-out refinance of a one-unit, owner-occupied principal residence with a legal ADU.

Key requirements:

- ADU must be legally permissible by local jurisdiction (or legal nonconforming)

- 75% of lease amount used as qualifying income

- ADU income capped at 30% of the borrower's total qualifying income

- Appraisal must include comparable sales and comparable rentals

- Borrower may need to complete landlord education unless they have documented landlord experience

- Available across all Freddie Mac mortgage products, including CHOICERenovation® for adding or renovating an ADU

Important: Freddie Mac's published guidance states that rental income from an illegal ADU may not be used to qualify in the subject 1-unit primary-residence scenario.

Source: Freddie Mac Guide Chapter 5306, ADU Fact Sheet. Verified April 2026.

FHA ADU Rental Income Rules

Policy reference: HUD Mortgagee Letter 2023-17, effective October 2023.

Eligible scenarios: Purchase or rate/term refinance of an owner-occupied property with an existing or planned ADU.

Key requirements:

- For an existing ADU with rental history: up to 75% of the lesser of the appraiser's estimated fair market rent or the current lease amount

- For a new ADU via FHA Standard 203(k) rehab loan: up to 50% of estimated rental income. Note: under HUD's 203(k) guidelines, the ADU must be attached to the existing structure

- ADU income capped at 30% of the borrower's total qualifying income

- ADU market rent comparables must not include hotel-style, transient, or under-30-day rental income

- Cannot use ADU income to qualify for cash-out refinances

Source: HUD Mortgagee Letter 2023-17. Verified April 2026.

Side-by-Side: Fannie vs. Freddie vs. FHA

| Rule | Fannie Mae | Freddie Mac | FHA |

|---|---|---|---|

| Eligible transactions | Purchase, limited cash-out refi | Purchase, no-cash-out refi | Purchase, rate/term refi |

| Property type | 1-unit owner-occupied primary | 1-unit owner-occupied primary | Owner-occupied primary |

| Rent treatment | 75% of market rent (Form 1007) or lease | 75% of lease amount | 75% of lesser of appraised FMR or lease |

| Income cap | 30% of total qualifying income | 30% of total qualifying income | 30% of total qualifying income |

| New ADU (not yet built) | No — existing ADU only | No — existing ADU only | Yes, via Standard 203(k) at 50% (attached to existing structure) |

| Illegal/unpermitted ADU | Limited exceptions may apply | Not eligible in 1-unit primary scenario | Case-by-case |

| Key documentation | Form 1007 or lease | Comparable rentals, lease, appraisal | Appraiser FMR estimate, lease |

Sources: Fannie Mae Selling Guide B3-3.1-08, B3-3.8-01; Freddie Mac Guide Chapter 5306, ADU Fact Sheet; HUD Mortgagee Letter 2023-17. All verified April 2026.

What This Means for Your Decision

If you're buying a home with an existing legal ADU, the rental income may meaningfully expand what you can qualify for. Ask your lender whether they've adopted the updated guidelines — lender adoption timelines have varied since the Q1 2026 DU 12.1 rollout.

If you're refinancing to fund an ADU build, the income from the new unit generally can't help you qualify for the refi itself (with the exception of FHA Standard 203(k) for attached ADUs). You'll need to qualify based on your existing income and equity.

If you're planning to rely on ADU income to afford your mortgage, be thoughtful. The qualification rules exist to help you qualify — they don't guarantee perfect occupancy or on-time rent. Smart homeowners plan to afford the property without the ADU income, then treat the rental as supplemental income that accelerates their financial goals.

That said — supplemental income of $12,000–$25,000+ per year is nothing to dismiss. That's a retirement contribution, a college fund, or years shaved off your mortgage payoff date.

Curious how ADU income could change your financing picture? See how homeowners are financing their ADUs →

Ready to see what ADU income could mean for your financing? Start with what's buildable at your address.

Our free report checks your specific property against local zoning, size limits, and setbacks — takes about 60 seconds.

Get Your Free ADU Feasibility Report →Detailed reports currently available in CA, UT, TX, CO, and NY.

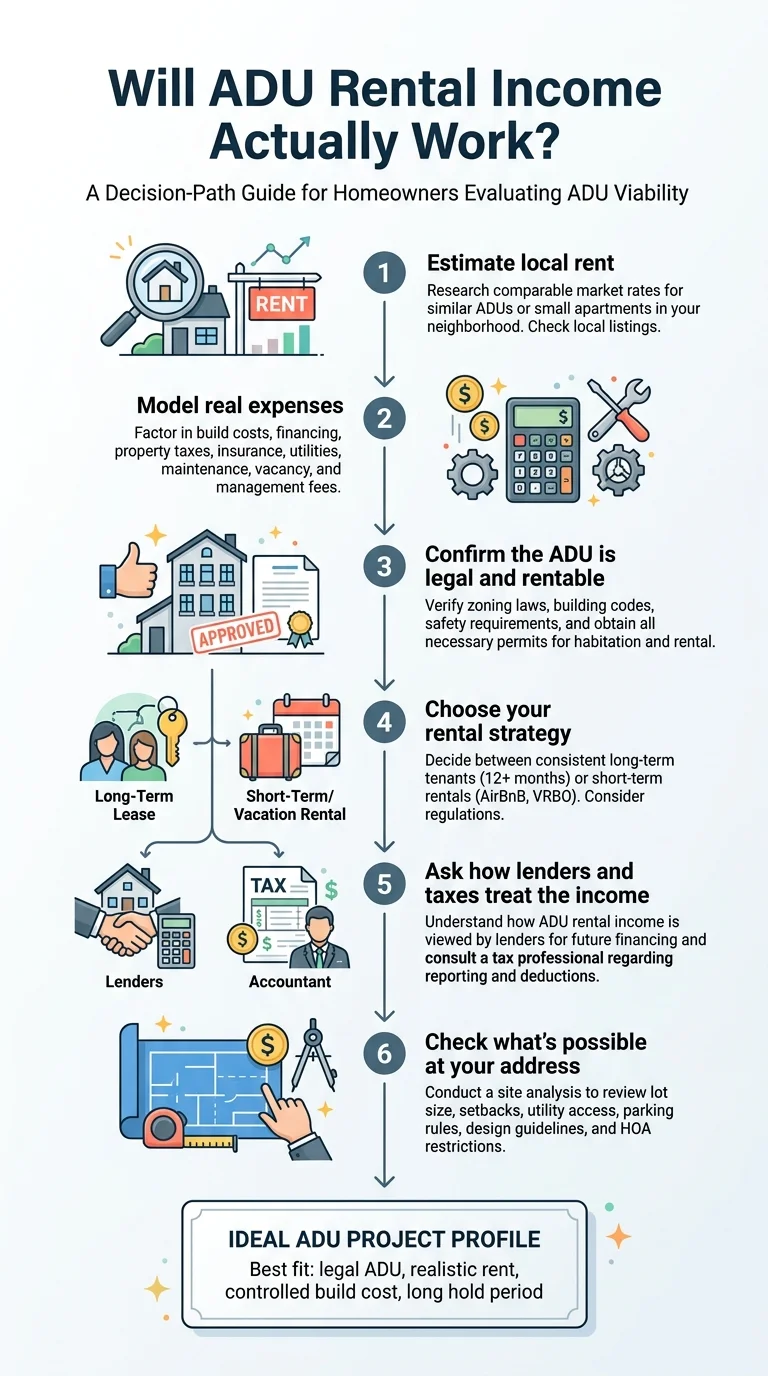

The six-step decision framework for evaluating ADU rental income viability before committing to a build.

Is ADU rental income taxable? (And what can you deduct?)

Yes, ADU rental income is taxable as ordinary income. You report it on IRS Schedule E (Supplemental Income and Loss), which flows into your Form 1040. But — and this is important — the deductions available to ADU landlords can dramatically reduce your tax liability. In some cases, you can show a paper loss on your taxes even while generating positive cash flow.

Reporting the Income

All gross rental income — monthly rent collected, any forfeited security deposits, and even non-cash income (like a tenant providing services in lieu of rent) — goes on Schedule E. (Source: IRS Topic 414, Publication 527.)

What You Can Deduct

As a rental property, your ADU unlocks the same deduction categories as any landlord:

Depreciation (your biggest deduction): The IRS lets you depreciate residential rental property over 27.5 years using the Modified Accelerated Cost Recovery System (MACRS). You depreciate the ADU's construction cost minus the land value. This is a non-cash deduction — meaning you get the tax benefit without actually spending money each year.

Depreciation Illustrative Example

You build a $200,000 ADU. Land allocation is $30,000 (determined by appraisal or tax assessment ratio). Depreciable basis = $170,000. Annual depreciation deduction = $170,000 ÷ 27.5 = $6,182/year. That's over $500/month in non-cash tax deductions.

Other deductible expenses:

- Mortgage interest (only the portion allocated to the ADU)

- Property taxes (allocated portion)

- Insurance premiums (landlord/rental dwelling policy)

- Repairs and maintenance (deductible in the year incurred)

- Property management fees

- Utilities you pay on behalf of the tenant

- Advertising and listing fees

- Legal and professional fees (tax prep, legal advice)

The Net Effect on Your Taxes

Let's put it together with an illustrative scenario:

| Tax Item | Amount |

|---|---|

| Gross rental income | $21,600 ($1,800/mo × 12) |

| Less: operating expenses | −$5,400 |

| Less: mortgage interest (ADU portion) | −$4,200 |

| Less: depreciation | −$6,182 |

| Net taxable rental income | $5,818 |

You collected $21,600 in rent. You'll pay tax on $5,818. The depreciation alone knocked nearly $6,200 off your taxable income without you writing a check.

In some scenarios — especially in early years when mortgage interest is highest — the combination of depreciation and deductible expenses can create a net rental loss on paper even while you're cash-flow positive. Subject to IRS passive activity rules, you may be able to deduct up to $25,000 of this loss against your other income if your modified adjusted gross income is below $100,000 (this allowance phases out between $100,000 and $150,000 MAGI). (Source: IRS Form 8582 Instructions.)

Property Tax Impact

Building an ADU increases your property's assessed value — but in most jurisdictions, only by the ADU's construction cost, not a complete reassessment of your entire property. In California, new construction is assessable, but the added value is assigned to the newly constructed portion while the remainder of the property retains its existing base-year value under Proposition 13. Most homeowners see a modest increase in property taxes after adding an ADU — and that increase is tax-deductible as a rental operating expense.

What Happens When You Sell

One long-term consideration: depreciation recapture. When you sell your property, gain attributable to depreciation you claimed (or were eligible to claim) may be subject to the 25% unrecaptured Section 1250 gain rate. The IRS assumes you took the depreciation even if you didn't — the "allowed or allowable" rule. (Source: IRS Publication 544, IRS capital gains FAQ.)

This isn't a reason to skip depreciation (you'd face the recapture tax either way), but it's something to plan for with your tax professional when the time comes.

Disclaimer: This section provides general tax education, not personalized tax advice. ADU tax situations can be complex, especially when you're renting part of your own property. Consult a qualified tax professional before making decisions based on this information.

Free Resource

Free 2026 ADU Starter Kit

Income projections by state, a financing comparison guide, a permit checklist, and a step-by-step project timeline — before you talk to a single company or contractor. Over 14,000 homeowners have downloaded it this year.

Download Free Starter Kit →Which ADU type produces the best rental return?

Garage conversions and JADUs have the fastest payback periods because of lower build costs. Detached ADUs command the highest rents and contribute the most to property value. The right choice depends on whether you're optimizing for speed-to-income or long-term wealth building.

ADU Type Comparison for Rental Income

| Factor | Detached ADU | Attached ADU | Garage Conversion | Basement / Interior |

|---|---|---|---|---|

| Typical build cost | $150,000–$350,000+ | $90,000–$250,000 | $50,000–$150,000 | $60,000–$150,000 |

| Illustrative monthly rent | $1,500–$3,500 | $1,200–$2,500 | $1,000–$1,800 | $1,000–$2,000 |

| Tenant privacy | Highest | Medium | Medium–Low | Low |

| Speed to market | 8–14 months | 6–10 months | 3–6 months | 4–8 months |

| Best for | Maximum long-term value and rent premium | Adding income without a separate structure | Fastest payback on underused space | Budget-friendly entry point |

All figures are illustrative ranges from our internal model. Costs and rents vary significantly by location, finishes, and site conditions.

If you want the highest total return over 10+ years: detached ADU. Higher cost, higher rent, strongest property value contribution. This is the long game.

If you want the fastest payback: garage conversion. You're repurposing an existing structure, slashing build costs, and can often be collecting rent in under 6 months. An $80,000 garage conversion bringing in $1,300/month in net income pays back the build cost in under 7 years.

If you're buying a home and want ADU income to help qualify: look for properties with existing legal ADUs. The Fannie Mae and Freddie Mac rules apply to existing units, and you skip the construction timeline entirely. This is one of the smartest moves in the current market.

Already thinking about what type of ADU fits your property? Most homeowners start with a simple question: what can I actually build here? Zoning, setbacks, lot coverage, and utility access all shape the answer — and it varies block by block.

Find out which ADU type fits your lot — and what it could rent for at your address.

Check your address in 60 seconds — free, no commitment.

Check My Property →Detailed reports available in CA, UT, TX, CO, and NY.

What local rules can change your ADU rental income plan?

This section prevents an expensive mistake. Every ADU project lives or dies by local rules — and the gap between "state law allows it" and "my city actually permits it" can be enormous.

ADU Rental Dealbreaker Checklist

| Issue | What to Check | Why It Matters |

|---|---|---|

| Is the ADU legal and permitted? | Verify permits with your local building department | Lenders, appraisers, and insurers all treat legal and unpermitted ADUs very differently. Freddie Mac's published guidance says rental income from an illegal ADU may not be used to qualify in the 1-unit primary-residence scenario. |

| Owner-occupancy requirement | Check your city's ordinance | Many cities require you to live in either the main house or the ADU. If you plan to rent both units, verify it's allowed. |

| Short-term rental restrictions | Check city STR ordinance | Many cities restrict or ban ADU short-term rentals. Some require registration, limit rental nights, or require owner-occupancy. Rules vary sharply by city. |

| HOA / CC&Rs | Review your HOA governing documents | Some HOAs restrict rentals, ADU construction, or both. State laws vary on whether HOAs can override state ADU provisions. |

| Parking requirements | Check local code | Some cities require additional off-street parking for ADU tenants, especially if you're converting a garage. |

| Separate utility metering | Plan during construction | Separate meters simplify billing, reduce disputes, and strengthen your rental income documentation for lenders. |

| Rent control | Check if your jurisdiction has rent stabilization | In some jurisdictions, your ADU may be subject to annual rent increase caps. |

The bottom line: a legal, permitted ADU on an owner-occupied property is the cleanest, most financeable, most defensible scenario. Anything else adds complexity, risk, and potential cost. If your ADU situation is ambiguous, resolve it before committing real dollars.

Not sure about your local rules? That's exactly what a feasibility check answers — zoning, setbacks, size limits, and local requirements, specific to your address.

Want to understand California's specific ADU rules? California ADU Laws 2026: Complete Guide →

Three realistic ADU rental income scenarios

Theory is useful. Specific examples are better. Here are three illustrative scenarios with honest assumptions so you can find the one closest to your situation.

Scenario 1: Detached ADU in a High-Cost Metro

| Assumption | Amount |

|---|---|

| ADU type | 1-BR detached, 650 sq ft |

| Build cost (all-in) | $280,000 |

| Monthly gross rent | $2,600 |

| Monthly operating expenses | $550 (taxes, insurance, maintenance, vacancy reserve) |

| Monthly net cash flow | $2,050 |

| Annual net income | $24,600 |

| Cash-on-cash return (if paid cash) | 8.8% |

| Simple payback (rental income only) | 11.4 years |

The verdict: Strong cash flow and meaningful equity creation from day one. This is the long-term wealth play for homeowners in expensive markets who have the capital or home equity to fund the build. Over a decade, you've collected $246,000 in net rental income and added significant value to your property.

Scenario 2: Garage Conversion in a Mid-Market

| Assumption | Amount |

|---|---|

| ADU type | Studio garage conversion, 450 sq ft |

| Build cost (all-in) | $85,000 |

| Monthly gross rent | $1,400 |

| Monthly operating expenses | $340 |

| Monthly net cash flow | $1,060 |

| Annual net income | $12,720 |

| Cash-on-cash return (if paid cash) | 15.0% |

| Simple payback (rental income only) | 6.7 years |

The verdict: The fastest path to positive cash flow. Garage conversions are the sharpest pencil in the ADU toolbox — lower cost, quicker construction, and strong returns relative to investment. If you have an underused two-car garage, the numbers here tend to be compelling.

Scenario 3: Buying a Home with an Existing Legal ADU

| Assumption | Amount |

|---|---|

| ADU type | Existing 1-BR detached, 550 sq ft |

| Additional cost over comparable home | ~$80,000–$120,000 (ADU premium in purchase price) |

| Monthly gross rent | $1,600 |

| Monthly operating expenses | $380 |

| Monthly net cash flow | $1,220 |

| Annual net income | $14,640 |

| Mortgage qualification impact (Fannie Mae 75% rule) | Up to $1,200/mo in qualifying income (at 75% of $1,600) |

The verdict: You skip construction entirely and start earning immediately. With the Fannie Mae and Freddie Mac qualifying rules, the ADU income can help you afford a home you might not otherwise qualify for — without building anything. For many homebuyers, this is the smartest play on the board right now.

All scenarios are illustrative examples from our internal model, not guarantees of returns. Actual results depend on local market conditions, construction costs, and regulatory approvals.

Your next step is simple:

Now that you've seen the scenarios — see what the numbers look like at your actual address.

Free report · 60 seconds · No sales call · No commitment

Get Your Free ADU Report →Detailed reports currently available in CA, UT, TX, CO, and NY.

When ADU rental income might not be the right move

We'd be doing you a disservice if we weren't straight about this: ADU rental income works in most situations, but not all of them.

Proceed with confidence when:

- Legal or easily permitted lot in a genuine rental market

- Build costs are controlled

- You can afford the property without ADU income

- Planning to hold 5+ years

- Local rules clearly support your rental strategy

Investigate further when:

- Rents are modest relative to high construction costs

- Cash-on-cash return is slim

- The math might still work for property value and flexibility, but run it carefully

Pause when:

- Mortgage only works with perfect rent and zero vacancy

- The unit isn't clearly legal

- Planning to sell within 1–2 years

- Haven't accounted for construction timeline

If one of those applies, it doesn't mean an ADU is wrong for you. It means the rental income angle specifically may need a different approach or timeline. Many homeowners build ADUs for family housing, aging-in-place, or home office space first — with rental income as a future option that adds flexibility down the road.

How we calculate ADU rent, ROI, and qualification rules

Transparency builds trust. Here's exactly how we develop the numbers on this page and in our calculator:

Rent estimates: Our conservative baseline uses HUD FY2026 Fair Market Rents (effective October 1, 2025), which represent the 40th percentile of gross rents paid by recent movers in each area. We then apply ADU-specific adjustments (type, size, features, privacy) based on rental platform data and builder-reported figures.

Cost data: Build cost ranges come from builder surveys, public permit records, and prefab manufacturer pricing, segmented by ADU type, region, and year. We update these quarterly.

Qualification rules: We cite directly from official agency publications: Fannie Mae Selling Guide, Freddie Mac Guide, and HUD Mortgagee Letters. We do not interpret these rules beyond their published text, and we recommend confirming specifics with your lender.

Tax information: We reference IRS Topic 414, Publication 527, Schedule E instructions, and Section 280A. We do not provide tax advice. Consult a qualified tax professional.

All numeric tables on this page are illustrative ranges from our internal research model — not established market facts. They combine multiple data sources to give you useful planning ranges, but your specific results will depend on your location, property, and local market conditions.

Update schedule: All data on this page is reviewed quarterly. Last verified: April 2026.

Author: The Dwelling Index Editorial Team. Editorial methodology and standards →

Frequently asked questions about ADU rental income

Can you use ADU rental income to qualify for a mortgage?

Yes. Fannie Mae (announced October 2025), Freddie Mac, and FHA all have pathways to count ADU rental income toward mortgage qualification on eligible owner-occupied properties. All three cap ADU income at 30% of total qualifying income and typically apply a 75% treatment to market rent to account for vacancy and expenses. Documentation requirements include lease agreements, Form 1007 (Comparable Rent Schedule), or appraiser estimates. Confirm specifics with your lender — adoption timelines vary.

How much can an ADU rent for?

A typical 1-bedroom ADU rents for roughly $1,200–$2,500/month nationally, with higher-cost metros reaching well above that. Rent depends primarily on location, ADU type, size, and features like private entrance, parking, and in-unit laundry. Check HUD's Fair Market Rent data for your area as a conservative starting point.

Is ADU rental income taxable?

Yes. ADU rental income is taxed as ordinary income and reported on IRS Schedule E. However, deductions for depreciation (27.5-year MACRS), mortgage interest, property taxes, insurance, and maintenance can significantly reduce taxable income. In some cases, depreciation alone can create a net paper loss for tax purposes. Consult a tax professional for guidance specific to your situation.

Does an ADU increase property taxes?

Building an ADU typically increases your property tax assessment, but only by the ADU's construction cost — not a full reassessment of your entire property. In California, the added value is assigned to the newly constructed portion while the rest of the property retains its base-year value under Prop 13. The increase is deductible as a rental expense.

What ADU type has the best ROI?

Garage conversions typically produce the fastest payback because of lower build costs. Detached ADUs command the highest rents and contribute the most to property value but cost more to build. The right choice depends on your goals, timeline, and budget.

How long does it take for an ADU to pay for itself?

Simple payback periods — build cost divided by annual net rental income — typically range from 3–15 years depending on ADU type and market. Garage conversions in strong rental markets can pay back in under 7 years. The property value contribution accelerates the overall financial picture further.

Can I rent my ADU on Airbnb?

It depends entirely on your local regulations. Many cities restrict or ban short-term rentals (under 30 days) for ADUs. FHA underwriting excludes hotel-style or transient rental income from ADU market-rent comparables. Always verify your city's short-term rental ordinance before building a financial plan around Airbnb income.

What about renting an unpermitted ADU?

Do not assume an unpermitted or zoning-noncompliant ADU will be treated like a legal one. Freddie Mac says rental income from an illegal ADU may not be used to qualify in the 1-unit primary-residence scenario. Fannie Mae and Freddie Mac both describe limited exception cases for certain zoning-noncompliant properties, but this must be reviewed lender-by-lender and jurisdiction-by-jurisdiction. The safest path: get the unit permitted.

Does an ADU increase my home's value?

Yes. FHFA's California appraisal dataset shows meaningfully higher median appraised values for enterprise-backed single-family purchase appraisals with ADUs compared to those without. The exact amount varies by market, ADU type, and project quality — but a well-designed, permitted ADU is consistently an equity-building asset.

Can an HOA stop me from renting my ADU?

In some states, yes. HOA authority over ADUs varies by state. California has limited HOA authority to block ADU construction on single-family lots, but other states give HOAs more power. Review your CC&Rs and check whether your state has passed legislation preempting HOA ADU restrictions.

Should I build an ADU or buy a separate rental property?

An ADU is often the more capital-efficient choice. You already own the land, you avoid a second mortgage, property management is simpler (the unit is in your backyard), and the equity gain flows to your primary residence. For homeowners looking to generate their first rental income stream, an ADU is usually the lowest-barrier, highest-convenience entry point.

What is Form 1007 for ADU rental income?

Form 1007 is Fannie Mae's Single-Family Comparable Rent Schedule. It's completed by an appraiser as part of the property appraisal and estimates the market rent for a unit based on comparable rentals in the area. Lenders use it to determine how much ADU rental income can count toward mortgage qualification.

What should you do next?

If you've made it this far, you're not casually browsing. You're evaluating whether ADU rental income can change your financial picture — and now you have the real numbers, the real rules, and the real tradeoffs to make that decision with confidence.

Here's the honest summary: for the right property, in the right market, with realistic expectations, an ADU rental is one of the strongest wealth-building moves a homeowner can make. You're creating a revenue-generating asset on land you already own, building equity from day one, and — with the new Fannie Mae, Freddie Mac, and FHA qualifying rules — potentially expanding your borrowing power in ways that weren't possible two years ago.

The next step isn't talking to a salesperson. It's spending 60 seconds to verify what's actually possible at your specific address — zoning, lot requirements, size limits, setback rules, and estimated income potential. Everything after that gets easier.

Not sure where to start? See what's possible at your address — get your free ADU report in 60 seconds.

Your next step is simple:

See What You Can Build — and What You Can Earn — at Your Address

Free report · 60 seconds · No sales call · No commitment

Get Your Free ADU Report →Detailed reports currently available in CA, UT, TX, CO, and NY.

Free Resource

Free 2026 ADU Starter Kit

Income projections by state, a financing comparison guide, a permit checklist, and a step-by-step project timeline — before you talk to a single company or contractor. Over 14,000 homeowners have downloaded it this year.

Download Free Starter Kit →Related Guides

- →ADU Financing Options 2026: HELOC vs Refi vs Loan

- →HELOC for ADU: Real Costs, Risks & Alternatives (2026)

- →How Much Does an ADU Cost? Real 2026 Prices by Type

- →California ADU Laws 2026: Rules, Setbacks, Fees & Permits

- →What Is an ADU? Definition, Types, Costs & Rules (2026)

- →Modular ADU: Costs, Rules & When Modular Wins (2026)

The Dwelling Index is an independent educational resource for homeowners exploring accessory dwelling units. We are not a lender, broker, builder, or tax advisor. The information on this page is for educational purposes only and does not constitute financial, legal, or tax advice. All financial projections and rental income estimates are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, regulatory approvals, and individual financial circumstances. Consult qualified professionals before making financial decisions.

Affiliate Disclosure · Editorial Methodology · Privacy Policy