ADU Construction Loan 2026: 4 Products Compared [Fit Matrix]

By The Dwelling Index Editorial Team · · Last verified May 19, 2026 · 28-min read

Independent ADU resource · Not a lender or broker · Editorial standards →

The bottom line, up front

An ADU construction loan is the right financing lane when your current home equity will not cover your full ADU budget, your project is a detached or larger attached build, and you need a lender to release funds in stages as construction progresses. Here is the catch most pages skip: “ADU construction loan” is not one product. It is four — a true construction-to-permanent (C2P) loan from a bank or credit union, an FHA 203(k) Standard rehabilitation mortgage, a Fannie Mae HomeStyle Renovation loan, and a Freddie Mac CHOICERenovation mortgage. Each has different LTV caps, different rental-income rules, and different draw mechanics.

Who this applies to: U.S. homeowners and prospective buyers planning a permitted ADU between roughly $80,000 and $400,000 in total project cost who do not have enough current equity for a HELOC.

The key constraint to know first: For conventional renovation loans (HomeStyle and CHOICERenovation), on purchase transactions, renovation costs are capped at 75% of the lesser of (purchase price plus renovation costs) or the as-completed appraised value. On refinance transactions, the cap is 75% of the as-completed appraised value. This single rule eliminates more applicants than any other.

Your next step: Run our free 60-second buildability and financing check, then read the four-product matrix below before you call a single lender.

Check your property before you borrow

Check zoning, ADU type eligibility, and your likely financing lane before spending money on plans, permits, or lender applications.

See What You Can Build → Get Your Free ADU Report

Is an ADU construction loan even your first lane?

Before the long version, read this. If your situation lands you outside construction financing entirely, we would rather route you to the right page than convert a click that will not serve you.

| Your situation | First lane to check | Why |

|---|---|---|

| You have 20%+ existing equity and a current mortgage rate under 5% | HELOC or home equity loan | Faster, simpler, fewer fees. You keep your low first mortgage. A construction loan is overkill here. |

| You bought your home in the last 1–5 years and lack the equity to cover a $150K+ project | Renovation loan (HomeStyle or CHOICERenovation) or true C2P | These underwrite against your home's as-completed value — the projected value after the ADU is built. |

| You are purchasing a home and plan to add an ADU at the same time | FHA 203(k), HomeStyle, or CHOICERenovation | Combines purchase + construction into one closing. Freddie's CHOICERenovation paired with Home Possible can go down to 3% down for eligible first-time buyers. |

| You are doing a garage or basement conversion (attached) and want to use future rent to qualify | FHA Standard 203(k) | FHA allows 50% of estimated rent for a new attached ADU under 203(k) — but only attached or interior conversion, not new detached new construction. |

| You have a low first-mortgage rate and refuse to lose it | HELOC, second-lien construction loan, or local ADU program | Most renovation and cash-out refinances replace your first mortgage. A second-lien path preserves it. |

| You live in Massachusetts and have plans + permits in hand | MassHousing ADU Loan Program (ADULP) | Now active statewide through participating lenders. Fixed 5.25% rate; up to $250K detached or $150K attached. |

| You have no plans, no permits, no contractor bid | You are not lender-ready yet | Most ADU construction lenders and public programs require these before final approval or closing. |

What we verified for this guide

This page was built by reviewing primary-source documents, not aggregator summaries. Specifically:

- Fannie Mae Single-Family Selling Guide sections B2-3-04 and B5-3.2-01; Announcement SEL-2025-10 issued December 10, 2025; DU 12.1 release notes

- Fannie Mae HomeStyle Renovation FAQ and Accessory Dwelling Units page (singlefamily.fanniemae.com)

- Freddie Mac CHOICERenovation FAQ and Accessory Dwelling Unit FAQ (sf.freddiemac.com)

- HUD Mortgagee Letter 2023-17, Revisions to Rental Income Policies, Property Eligibility, and Appraisal Protocols for Accessory Dwelling Units (Oct. 16, 2023)

- HUD Mortgagee Letter 2024-13, Revisions to the 203(k) Rehabilitation Mortgage Insurance Program (effective for FHA case numbers assigned on or after Nov. 4, 2024)

- HUD Handbook 4000.1 sections covering FHA 203(k) and ADU policy

- MassHousing ADU Loan Program (ADULP) page (masshousing.com/adu)

- San Diego Housing Commission (SDHC) ADU Finance Program page; City of Long Beach Backyard Builders Loan Program page and press releases; City of Boston ADU Financial Assistance Program page (boston.gov); Community Development Long Island (CDLI) Plus One ADU Loan Product page

- Orange County Housing Finance Trust status notice (program discontinued May 21, 2025)

- California Government Code § 66317 for state ADU permitting timelines; Federal Reserve federal funds rate target range as of May 2026; CFPB HELOC consumer guidance

- Forum threads on BiggerPockets and Reddit used only for voice-of-customer language and common objections — not as proof of any lending, code, or regulatory claim

Date of last verification: May 19, 2026.

Rates, agency rules, and program statuses change. We refresh agency rules quarterly and public-program availability monthly. If a number on this page looks materially different from a current lender quote or program page, the lender or program page is the controlling source.

What an “ADU construction loan” actually is — and the four products people call by the same name

Two terms appear in every conversation with a lender and trip up first-time applicants:

- As-completed value (also called after-completed value or after-renovation value): the appraiser’s estimate of what your property will be worth once the ADU is finished. Construction and renovation loans underwrite against this projected number — which is how homeowners with little current equity can still borrow enough to build.

- Draw schedule: the sequence of partial loan payouts released during construction, each tied to a verified milestone (foundation poured, framing complete, mechanical rough-in, drywall, completion). You pay interest only on the amount drawn so far, not the full approved loan.

These two concepts are what make construction financing different from a HELOC or a cash-out refinance. A HELOC pays you a lump sum or revolving line against your home’s current equity. A construction loan pays your contractor in stages against the home’s future equity once the ADU exists. That distinction is the entire reason this product category exists.

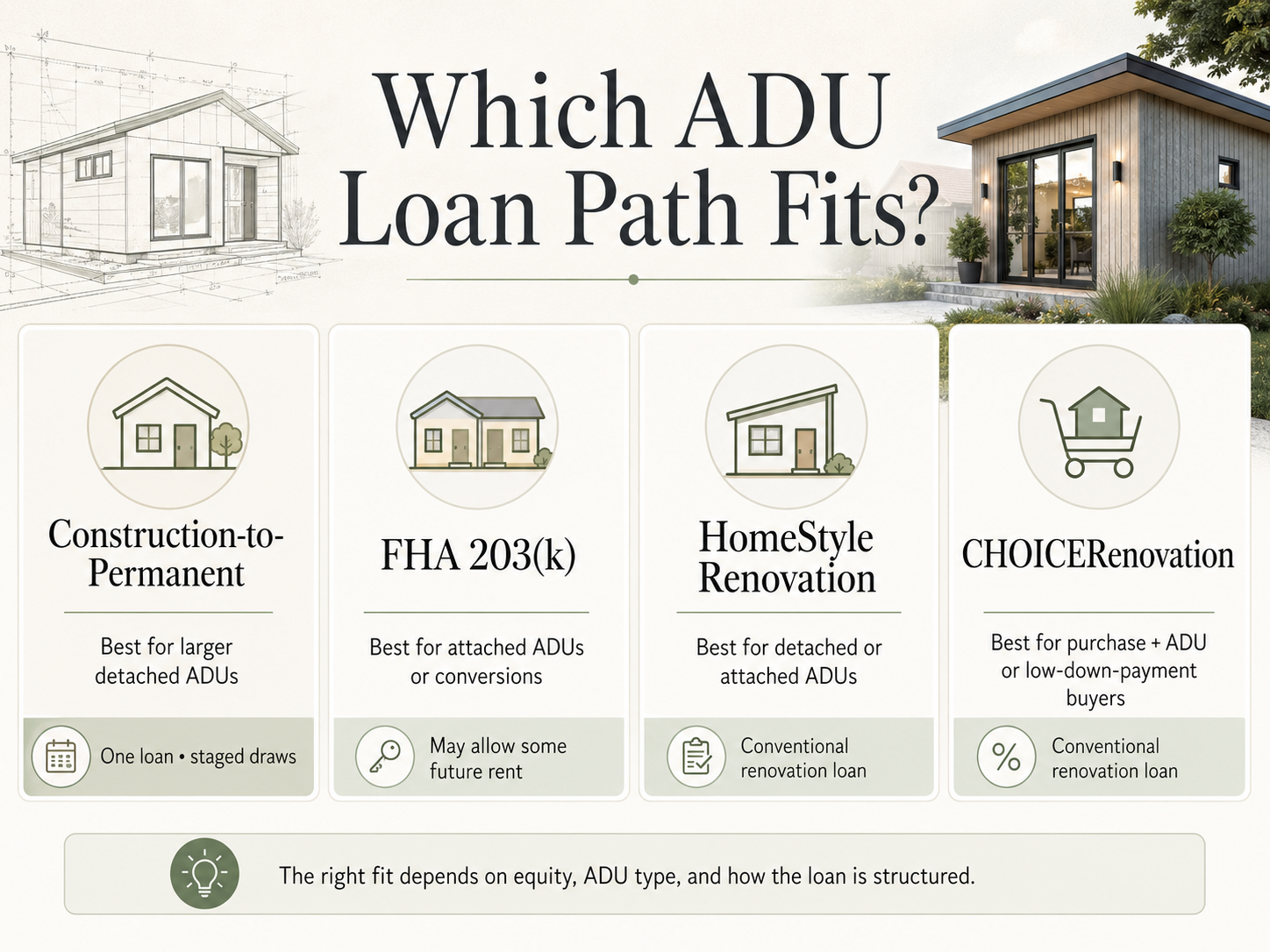

The four products at a glance

| Product | What it actually is | Best fit |

|---|---|---|

| True construction-to-permanent (C2P) | A bank or credit union loan with a construction phase (interest-only draws) that converts to a permanent mortgage at completion | Larger detached ADUs, borrowers willing to refinance their first mortgage |

| FHA Standard 203(k) | Government-insured rehab mortgage allowing one loan to cover purchase or refinance plus construction | Lower-credit borrowers, garage/basement/attached conversions, anyone wanting to use future rent to qualify |

| Fannie Mae HomeStyle Renovation | Conventional renovation mortgage allowing detached ADU construction | Conventional borrowers wanting flexibility on ADU type, including detached |

| Freddie Mac CHOICERenovation | Conventional renovation mortgage with low-down-payment option for first-time buyers | First-time buyers or borrowers combining purchase + ADU construction |

Which ADU construction loan product fits your project?

We assembled the matrix by reading the Fannie Mae HomeStyle Renovation FAQ, Freddie Mac’s CHOICERenovation FAQ and ADU FAQ, HUD Mortgagee Letters 2023-17 and 2024-13, HUD Handbook 4000.1 (referenced via current AFR Wholesale and Plaza Home Mortgage product profiles), and current rate disclosures and product guides from several national lenders.

| Attribute | True C2P (bank/credit union) | FHA 203(k) Standard | Fannie Mae HomeStyle Renovation | Freddie Mac CHOICERenovation |

|---|---|---|---|---|

| Detached new-construction ADU eligible? | Yes | No — HUD 4000.1 allows new attached or interior-conversion ADU under 203(k); new detached construction is not eligible. Renovation of an existing detached ADU is eligible. | Yes — Fannie HomeStyle FAQ: "an accessory unit may be detached from the primary dwelling" | Yes — CHOICERenovation FAQ: "addition or renovation of ADUs" eligible |

| Attached ADU / addition? | Yes | Yes | Yes | Yes |

| Garage or basement conversion? | Yes | Yes (the 203(k)'s main ADU use case) | Yes | Yes |

| Prefab / modular / manufactured ADU? | Lender-specific | Lender-specific; modular generally OK if installed as real property | Yes — including manufactured-home ADUs under updates from Announcement SEL-2025-10 (Dec. 2025) | Yes |

| Borrowing base | After-completed appraised value | Lesser of (as-is + cost) or after-improved value | Purchase: lesser of (purchase + renovation) or as-completed value · Refi: as-completed value | Purchase: lesser of (purchase + renovation) or as-completed value · Refi: as-completed value |

| Max renovation cost cap | Lender-set, typically 80–95% of after-completed value | Bound only by FHA county loan limit; no specific dollar cap on rehab costs | 75% of the applicable borrowing base above | 75% of the applicable borrowing base above |

| Minimum down (purchase) or equity (refi) | 5–20%+ depending on lender, occupancy, credit | 3.5% (FICO 580+); 10% (FICO 500–579) | 3% with HomeReady; standard 5% | Up to 95% LTV standard; up to 97% LTV with eligible Home Possible (income-limited) or HomeOne (first-time-buyer rules) |

| Minimum credit score (typical) | 680+ at most banks | 580 (3.5% down) per HUD 4000.1 | DU no longer requires a published minimum third-party credit score after the November 2025 update, but eligibility matrices, manual underwriting, and lender overlays still apply | LPA Accept loans may not require a minimum Indicator Score; manually underwritten loans and lender overlays still apply |

| Future ADU rental income for qualifying? | Lender-specific; generally no during construction | Per HUD ML 2023-17: 50% of estimated rent for a new attached ADU; 75% for existing ADU. ADU income capped at 30% of total qualifying income. 2 months PITI reserves required. Cash-out refinance excluded. | Per Fannie DU 12.1: ADU income may be considered on a one-unit principal residence purchase or limited cash-out refinance when requirements are met, including manufactured homes. Income from only one ADU may be used. Capped at 30% of total qualifying income. | Per Freddie ADU FAQ: income must be received at time first mortgage payment is due — projected rent during construction generally cannot be used |

| Upfront disbursement at closing | Lender-specific, typically permits and deposits only | Limited initial advance per HUD requirements | Up to 50% of total renovation costs at closing — per Fannie SEL-2025-10 effective Dec. 10, 2025 | Lender-specific |

| Draw schedule | 4–6 draws tied to milestones with inspections | Max 5 draws after closing; 203(k) Consultant required for Standard | Lender-managed via custodial account; inspections per program rules | Lender-managed draws via custodial account; final inspection at completion |

| Number of closings | One (true C2P); two (construction-only) | One | One | One |

| Rehabilitation timeline cap | Lender-specific, typically 12 months | 12 months per HUD ML 2024-13 (effective Nov. 4, 2024) | 15 months (18 max with Fannie approval) | 450 days from note date per Freddie's CHOICERenovation fact sheet |

| Contingency reserve required? | Most lenders require 10–15% | Standard 203(k) requires 10% | Not required for 1-unit; 10% required for 2–4-unit | Generally 10%; 15% when utilities are not operable; 20% maximum with limited exceptions |

| Replaces existing first mortgage? | Yes if true C2P; not always if construction-only | Yes — refinance into new FHA loan | Yes for refi; or used for purchase | Yes for refi; or used for purchase |

| Single most common denial trigger | Insufficient reserves or contractor not pre-approved | Detached new-construction ADU (ineligible) | Renovation costs exceed the 75% cap | Renovation costs exceed the 75% cap |

Verification date: May 19, 2026. Lender-specific items vary; the rule of thumb is that the agency selling guide or HUD handbook sets the floor and individual lenders may impose stricter “overlays” on top.

How to read this table — the three diagnostic questions

The matrix is large because the products are different. To use it, ask yourself three questions in order:

- Is your ADU detached new construction? If yes, eliminate FHA 203(k) for ground-up construction. HUD 4000.1 allows the Standard 203(k) program to construct a new attached ADU, convert interior space, or renovate an existing ADU — including an existing detached ADU — but not new detached construction. This is the single most common surprise on competing pages.

- Do you want to use the ADU’s future rental income to qualify? If yes, FHA 203(k) becomes powerful for attached ADUs (50% of estimated rent counted, capped at 30% of total qualifying income, two months PITI reserves required). Under Fannie Mae’s DU 12.1, ADU rental income may also be considered for qualifying on a one-unit principal residence purchase or limited cash-out refinance when requirements are met. Under Freddie Mac CHOICERenovation, projected rent during construction generally cannot be used.

- What is your current first-mortgage rate? If it is at or below 5%, you almost certainly want to avoid any product that replaces your first mortgage — which is most of these. A second-lien construction loan, HELOC, or local-program option becomes more attractive.

What changed at Fannie Mae in December 2025

Fannie Mae’s Announcement SEL-2025-10, issued December 10, 2025, materially expanded HomeStyle Renovation in three ways relevant to ADU builders. Lenders may now disburse up to 50% of total renovation costs at closing for material purchases, permit fees, architectural and design services, and borrower deposits — effective immediately. The previous restrictive caps on initial disbursements were the single biggest contractor-cash-flow headache under the program. SEL-2025-10 also removed the $50,000 renovation cost cap for manufactured homes (now 50% of as-completed value) and expanded property eligibility criteria for ADUs and manufactured homes. The property-eligibility expansions take effect March 31, 2026, and apply to lenders using UAD 3.6 policy.

Source: Fannie Mae Announcement SEL-2025-10, singlefamily.fanniemae.com

Resolve the equity and product question for your address

If the matrix has resolved your product question, the next decision is whether your specific lot can host the ADU you want to build. The free report runs your address against zoning, lot size, setbacks, and ADU eligibility.

See What You Can Build → Get Your Free ADU ReportCan you use future ADU rental income to qualify? The rule that trips up first-time buyers

This is the most-misreported rule on competing pages. Lender marketing pages cherry-pick whichever interpretation flatters their product. We are going to walk through each agency’s rule with the exact citation, because if you get this wrong, you can be approved on paper and denied at underwriting.

FHA Standard 203(k) — the most generous future-rent rule (with conditions)

HUD Mortgagee Letter 2023-17 (October 16, 2023) made FHA the most flexible program on future ADU rent. Two distinct scenarios:

Existing ADU on a property you’re buying: When there is no prior rental history, the mortgagee may use 75% of the lesser of the fair market rent reported by the appraiser (on Fannie Mae Form 1007 / Freddie Mac Form 1000) or the rent stated in the lease. ADU rental income used as effective income cannot exceed 30% of the borrower’s total qualifying income. Reserves of two months’ PITI are required for one-unit properties with an ADU.

New ADU being added via Standard 203(k): When no prior rental history exists and the project will add a new ADU (attached or interior conversion only — remember, detached new construction is ineligible under 203(k)), the mortgagee may use 50% of the lesser of the appraiser’s estimated fair market rent or the lease rent. Same 30% income cap. Same two-month PITI reserves rule.

Important: A one-unit property with an ADU cannot use rental income as effective income for FHA cash-out refinance loans. The rental-income flexibility applies to purchase and rate-and-term refinances, not cash-out.

Source: HUD Mortgagee Letter 2023-17, hud.gov/sites/dfiles/OCHCO/documents/2023-17hsgml.pdf

Fannie Mae — DU 12.1 update

Fannie Mae’s DU 12.1 release notes confirm that ADU rental income may be considered on a one-unit principal residence purchase or limited cash-out refinance, including manufactured homes, when program requirements are met. Rental income from only one ADU may be used, and qualifying ADU rental income is capped at 30% of the borrower’s total qualifying income. For loans where ADU income would otherwise exceed that cap, DU will issue a message and the lender must reduce the amount used.

For homeowners adding a new ADU via HomeStyle Renovation, qualifying ADU rental income generally requires the income to be receivable at the time the first mortgage payment is due, which during construction is not yet the case. After construction is complete and the ADU is rented to a documented tenant, both Fannie and Freddie allow the rental income to be counted on a future refinance, typically at 75% of gross rent (a standard vacancy/expense factor).

Source: Fannie Mae Accessory Dwelling Units page and DU release notes, singlefamily.fanniemae.com

Freddie Mac CHOICERenovation — the timing trap

Freddie Mac’s Accessory Dwelling Unit FAQ states the rule plainly: for rental income to be used in qualifying, the income must be received at the time mortgage payments are due. If the lease does not require monthly rental income payments to begin before or on the date the first mortgage payment is due — for example because the ADU is undergoing construction — the projected rental income cannot be used for qualifying purposes.

In plain English: you generally cannot use the ADU’s future rent during the construction phase to qualify for a CHOICERenovation loan. A common borrower assumption (“I’ll have the ADU rented within six months, so the lender will count that income”) fails here. Freddie will count the rent only once it is actually being received.

Source: Freddie Mac Accessory Dwelling Unit FAQ, sf.freddiemac.com/faqs/accessory-dwelling-unit-faq

Why this rule matters more than the rate

A reader anchored on a 0.5% rate difference between two products is optimizing the wrong variable. The rental-income rule changes whether you qualify at all. If your DTI is borderline and your ADU is a garage conversion, FHA 203(k) may be the only program that approves you — even at a slightly higher rate — because it is the only one that lets you count 50% of the future rent toward effective income at the time of construction.

Disclaimer: These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

ADU construction loan requirements: credit, down payment, DTI, and the documents lenders actually ask for

Credit score requirements by program

| Program | Typical minimum FICO | Down payment at that FICO |

|---|---|---|

| FHA 203(k) | 580 | 3.5% |

| FHA 203(k) with 10% down | 500–579 | 10% |

| Fannie Mae HomeStyle / HomeReady combo | No DU minimum after Nov. 2025 update; lender overlays apply | 3% (HomeReady); 5% standard |

| Freddie Mac CHOICERenovation / Home Possible combo | No LPA Accept minimum; lender overlays apply | Up to 97% LTV via Home Possible (income-limited) or HomeOne (first-time-buyer rules) |

| Conventional construction-to-permanent (bank/CU) | 680+ typical | 5–20%+ |

A “no published GSE minimum” does not mean “no minimum.” Individual lenders impose their own credit floors as overlays — a lender selling loans to Fannie Mae or Freddie Mac may still require 620 or 640 minimum FICO even though the GSE selling guide does not. Always ask the lender for their specific overlay.

Down payment math (worked example)

You are buying a $475,000 home and plan to add a $150,000 ADU. The appraiser’s as-completed valuation comes in at $700,000.

- Total project cost basis: $475,000 + $150,000 = $625,000

- Lesser of (cost) or (as-completed value): $625,000 (cost is lower)

- Required down payment under CHOICERenovation paired with Home Possible (3%) for an eligible first-time buyer: $625,000 × 3% = $18,750

- Required down payment at 5%: $625,000 × 5% = $31,250

This is real borrowing power for newer homeowners. A buyer with $20K saved who could not qualify for a conventional mortgage on a $475K home plus a $150K addition can, in this scenario, do both with a single low-down-payment renovation loan.

DTI and the reserves rule

Most ADU construction loans require a debt-to-income ratio under 43–45% for automated underwriting approval, with compensating factors potentially allowing 50%. Reserves vary by program:

- FHA 203(k) with ADU rental income: 2 months of full PITI (principal, interest, taxes, insurance, MIP) after closing

- Conventional C2P (bank): typically 2–6 months reserves required

- HomeStyle on a 2–4-unit property: 10% contingency reserve required (not on 1-unit)

- HomeStyle DIY (homeowner-completed) work: limited to 10% of as-completed value, lender approval required, lender must inspect work over $5,000

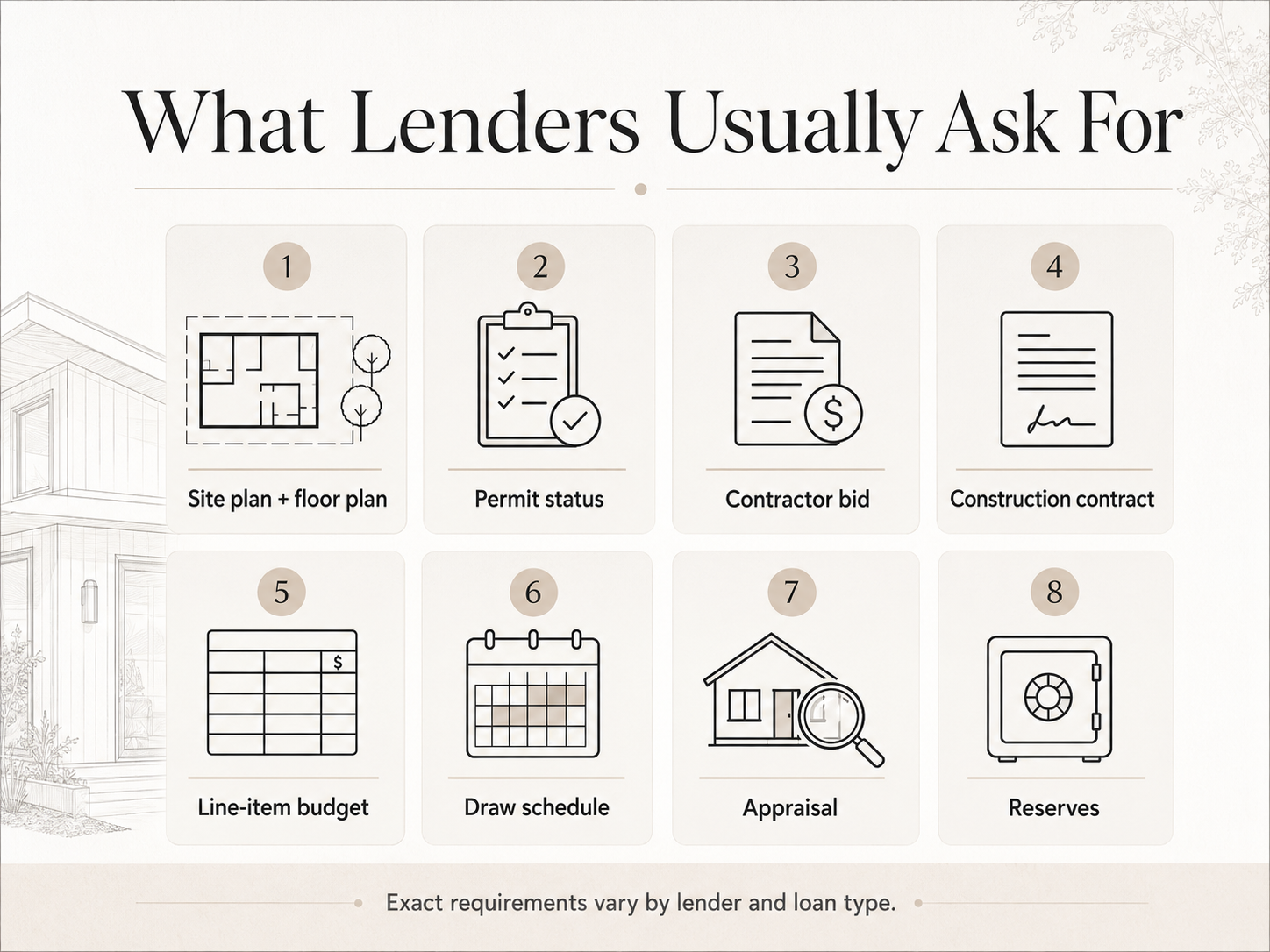

The 24-document lender package

Pull all of these before you call lenders. Applicants with the complete package close materially faster than those who submit incrementally — because every missing document adds an underwriting cycle.

Borrower documents (10)

- Two years of W-2s or 1099s

- Two months of pay stubs (most recent)

- Two months of bank statements (all accounts)

- Two years of federal tax returns (signed)

- Two years of business tax returns + P&L (if self-employed)

- Photo ID and Social Security verification

- Credit authorization

- Asset documentation (retirement, brokerage, gift letters if applicable)

- Current mortgage statement (for refinance)

- Homeowners insurance policy and proof of payment

Project documents (8)

- Architectural plans / floor plan / elevations

- Site plan showing setbacks and lot boundaries

- Building permit application receipt or approved permit

- Detailed line-item construction budget (signed)

- Proposed draw schedule (signed)

- Construction timeline / Gantt chart

- Soils report (if structural)

- Survey or plot plan (if required)

Contractor documents (6)

- Signed construction contract

- Contractor license verification

- Contractor general liability and workers’ comp insurance

- Contractor references (typically 3+ prior ADU projects)

- Contractor’s W-9

- Contractor’s bond information (if required by lender)

Download the Free ADU Starter Kit + Construction Loan Document Checklist

Get the printable checklist with explanations of why each document matters, plus blank copies of Fannie Mae Form 1007 (Comparable Rent Schedule), a sample line-item budget template, and a sample draw schedule.

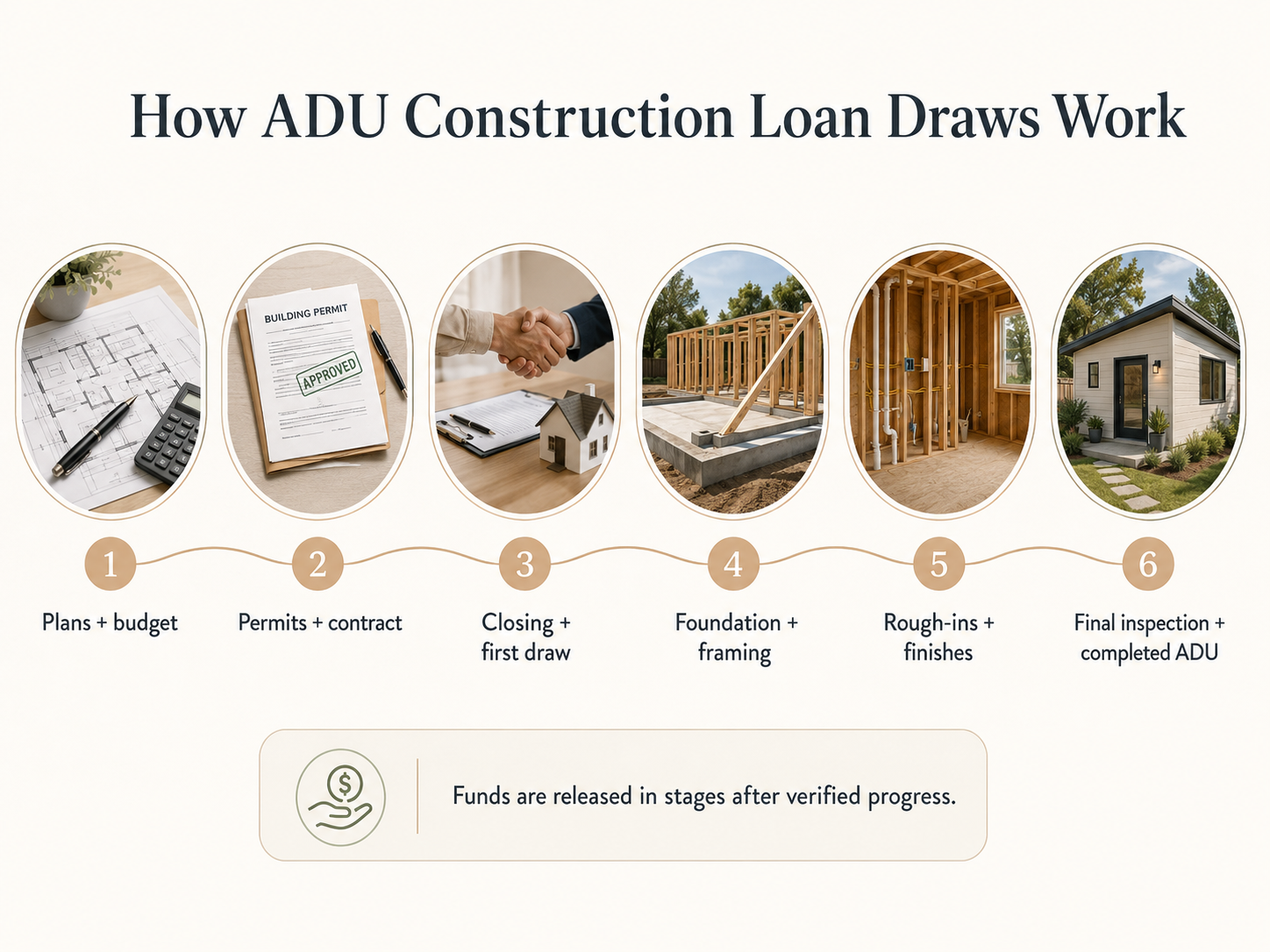

Get the Free ADU Starter Kit →The draw schedule, inspections, and what actually happens between closing and your keys

A sample 6-draw schedule for a $200,000 detached ADU

Illustrative only — actual draws are set by each lender and contractor in writing. Not a quote or commitment.

| Draw # | Trigger milestone | % of loan released (typical) | What can stall this draw |

|---|---|---|---|

| 1 | Closing — permits, design, deposits, mobilization | 10–20% | Missing permit, missing contractor license verification |

| 2 | Foundation poured and inspected | 15–20% | Failed soils or foundation inspection; setback issue |

| 3 | Framing complete, roof on, building shell weathertight | 15–20% | Failed framing inspection; design revision |

| 4 | Mechanical, electrical, plumbing rough-in complete and inspected | 15–20% | Utility upgrade needed (sewer lateral, service panel) |

| 5 | Drywall, interior finishes, mechanical trim | 15–20% | Change-order disputes; finish material delays |

| 6 | Final inspection, certificate of occupancy, final lien waivers | 10–15% | Punch list, missing CO, missing waiver from a sub |

Each draw requires the contractor to submit signed lien waivers from every subcontractor who has worked since the last draw. Missing or incomplete lien waivers are a common cause of mid-build draw delays — if a single sub’s waiver is not received, the lender will hold the next disbursement until it is.

How interest accrues during construction

You pay interest only on the amount drawn, not the full approved loan. On a $200,000 construction loan where Draw 1 of $30,000 has been released and Draw 2 has not yet occurred, your monthly interest is calculated on $30,000 — not on $200,000. This is a major cash-flow advantage compared to taking out a lump-sum home equity loan and watching interest accrue on the full balance from day one.

After completion, the construction-phase rate ends. On a construction-to-permanent loan, the loan automatically converts to a permanent mortgage at the rate locked at origination (or at the prevailing rate, depending on lock structure). On a construction-only loan, you must obtain separate permanent financing at completion — a second closing, a second set of fees, and a separate rate exposure.

What an inspector actually checks

The lender-approved inspector is not the city building inspector. They are a separate party verifying that the percentage of work claimed by the contractor matches the percentage actually completed on-site. They check for substantial completion of each draw’s deliverables, not building code compliance (that is the city inspector’s job). A draw is held until the lender’s inspector signs off — typically a 2–5 day turnaround from request to inspection.

Total timeline reality check

For a detached ADU under conventional C2P or HomeStyle Renovation financing:

- Application to closing: 30–45 days; faster if your document package is complete at application

- Permit pull (often runs in parallel): varies widely by jurisdiction

- Construction (detached site-built): 6–10 months

- Construction (prefab/modular): 3–5 months in factory + 2–4 weeks on-site set + utility hookup

- Permanent loan conversion or refinance: 30–45 days post-completion if a second closing is needed

For California projects: under California Government Code § 66317, a permitting agency must determine an ADU application complete within 15 business days of receipt, then approve or deny a completed ADU application within 60 days when there is an existing single-family or multifamily dwelling on the lot; if not approved or denied within 60 days, the application is deemed approved.

Sources: HUD Mortgagee Letter 2024-13; Fannie Mae HomeStyle Renovation Process page; California Government Code § 66317

Affiliate disclosure: When you use the link below to explore financing options with Mortgage Research Center, we may earn a commission at no extra cost to you. This does not influence our editorial recommendations. Read our full disclosure.

Explore current construction and renovation loan options

Review construction-to-permanent and renovation loan options across major national lenders. Compare programs and product features before committing to a single lender.

Explore Options → Mortgage Research CenterADU construction loan vs HELOC vs cash-out refinance vs renovation loan

The full five-way comparison

| Path | Best fit | Speed to fund | Replaces first mortgage? | Borrows against | Draw schedule? | Typical use |

|---|---|---|---|---|---|---|

| HELOC | 20%+ existing equity, low first-mortgage rate, flexible draw needs | Fast (2–4 weeks) | No | Current value | Yes, revolving | Smaller projects; phased ADU work |

| Home equity loan | 20%+ equity, lump-sum need, fixed-rate preference | Fast (2–4 weeks) | No | Current value | No (lump sum) | Defined-scope ADU |

| Cash-out refinance | Existing first-mortgage rate is at or above current rates; lots of equity | Moderate (4–6 weeks) | Yes | Current value | No (lump sum) | Larger ADU with rate-improvement opportunity |

| Renovation loan (HomeStyle / CHOICERenovation) | Low current equity, want as-completed-value loan with single closing | Slower (45–60 days) | Yes for refi; or used for purchase | As-completed value | Yes | Detached or attached ADU, conventional borrower |

| True C2P | Larger detached build, willing to refinance first mortgage | Slower (45–60 days) | Yes (true C2P) | As-completed value | Yes | Larger detached ADUs |

Why HELOCs win when you actually have the equity

If you have a $700,000 home with a $300,000 mortgage balance, your usable equity at an 80% combined loan-to-value (CLTV) limit is $260,000 — more than enough to fund most ADU projects. A HELOC against that equity will typically close in two to four weeks, costs a fraction of a renovation loan in origination fees, and preserves your existing first mortgage entirely. The trade-off: HELOCs are typically variable-rate, indexed to prime. The CFPB notes that HELOC rates can rise during the draw period, and when the interest-only period ends, monthly payments can jump significantly when principal repayment begins. If you have the equity and a low first-mortgage rate, a HELOC for ADU is the simpler answer.

Why cash-out refinance rarely makes sense at low existing rates

If your current first mortgage is at 3.5% and prevailing 30-year rates are several points higher, a cash-out refinance forces you to give up the 3.5% rate on your entire mortgage balance — not just the new money — to access the equity. The math almost never works at meaningfully higher current rates. The lock-in effect of low pandemic-era mortgages is one of the largest financing barriers to ADU construction in the current environment.

Why renovation loans are the most under-used option

HomeStyle Renovation and CHOICERenovation are conventional renovation mortgages that combine purchase-or-refinance with construction funding in a single loan, single closing — and they underwrite against as-completed value just like a true construction loan. They allow detached ADU construction. They allow up to 75% of the applicable base in renovation costs. With Fannie Mae’s December 2025 update, HomeStyle now permits up to 50% of total renovation costs to be disbursed at closing, addressing the largest contractor-cash-flow issue with renovation lending. These products are under-marketed by many lenders relative to standard purchase and refinance mortgages.

When a true C2P is the right call

If you are building a larger detached ADU (say, $250K+) and your lender’s HomeStyle or CHOICERenovation overlays will not stretch to your project size (remember the 75% cap), a true construction-to-permanent loan from a bank or credit union may be the only path. These typically require 680+ FICO, 20%+ equity or down payment, and full documentation. Product fit for ADU construction specifically must be confirmed with each lender, because not every bank’s general C2P product accommodates the addition of an ADU to an existing primary residence. See our comprehensive comparison of all ADU financing options for the broader landscape.

Avoidable triggers that stop ADU construction loans (or stall draws mid-build)

- Detached new-construction ADU + FHA 203(k) — Ineligible combination. HUD 4000.1 allows attached or interior-conversion ADUs only under 203(k) for new construction (an existing detached ADU can be renovated). Switch to HomeStyle or CHOICERenovation for new detached construction.

- Insufficient post-closing reserves — FHA with ADU rental income requires 2 months PITI; most C2P lenders want 4–6 months. Verify the reserves requirement before committing your down payment funds.

- Renovation costs exceed the 75% cap — The hard cap on HomeStyle and CHOICERenovation. If your renovation budget is large relative to home value, a true C2P may be the only path.

- Contractor not pre-approved or not licensed in the state — Major banks and most renovation programs require the GC to be licensed, insured, and pre-approved by the lender. Confirm contractor eligibility before you sign a build contract.

- Incomplete or missing permit application — Lenders will not fund a project that may not be legal. Submit your permit application before applying for the loan; “in plan check” is usually acceptable.

- ADU not allowed under local zoning — The lender pulls a zoning verification and denies. Check setbacks, lot size minimums, owner-occupancy requirements, and ADU-specific zoning rules in your jurisdiction before you spend money on plans.

- Owner-builder without verified construction experience — Most C2P lenders require a licensed GC. HomeStyle permits DIY work limited to 10% of as-completed value with lender approval and required inspections on items over $5,000.

- DTI above 45% after the new loan payment — Strong compensating factors (substantial reserves, large down payment, high credit) can push this to 50% under FHA manual underwriting, but the standard is 43–45%.

- Inadequate appraisal comps — The appraiser cannot support the as-completed value because there are too few recent ADU sales nearby. Fannie’s HomeStyle Renovation Maximum Mortgage Worksheet (Form 1035) requires comparable-sales support; without them, the loan amount may be capped well below your budget.

- Plans missing lender-required elements — Lenders require a line-item budget, a draw schedule with milestone-based payment requests, contractor insurance documentation, and architectural drawings. Generic estimates do not pass underwriting.

- Failed lien-waiver delivery mid-build — Not a denial of the original loan, but it halts draws. Establish a lien-waiver collection process with your contractor before construction starts.

How to pre-empt each trigger — a 90-minute pre-application checklist

- Verify your ADU is permitted by right under local zoning

- Get a written contractor bid with line-item budget and proposed draw schedule

- Confirm contractor license, insurance, and that they have completed at least 2–3 prior ADU projects

- Pull your credit report from all three bureaus

- Calculate your DTI assuming the full new loan payment

- Confirm 2–6 months of reserves are sitting in liquid accounts

- Identify whether the appraiser can find 2–3 ADU-comparable sales in your market

Public and local ADU construction loan programs worth knowing about

| Program | Geography | What it offers | Key restriction |

|---|---|---|---|

| MassHousing ADU Loan Program (ADULP) | Massachusetts statewide via participating lenders | Fixed-rate 5.25% second mortgage; up to $250,000 for detached ADUs, up to $150,000 for attached; amortized over 20 years; paired with additional 0%-interest deferred funding | Owner-occupied; income up to 135% of AMI; plans, permits, and pre-development materials required before applying |

| San Diego Housing Commission (SDHC) ADU Finance Program | City of San Diego | Construction-to-permanent loan up to $250,000; 1% interest during construction; 4% fixed permanent rate; up to 75% LTV; free technical assistance | Owner-occupied; income up to 150% of AMI; minimum credit score 680; $2,500 application fee due at construction-loan closing; 7-year affordability covenant requiring rent below market to tenants earning ≤80% AMI; cannot rent to family during covenant period |

| City of Long Beach Backyard Builders Loan Program (Round 2) | City of Long Beach (designated program areas) | Up to $250,000 at 2% interest; 30-year loan; payments deferred for life of loan (no payments until 30-year term ends or property is sold/transferred); free project management | Applications open Summer 2026; lower-income homeowners as defined by California 2026 limits; owner-occupied single-family in program area; short-term rentals not allowed; cash-out refinance against the loan prohibited; at least 16 loans available |

| City of Boston ADU Financial Assistance Program | City of Boston | Up to $50,000 in 0% deferred gap funding; due on sale, transfer, or cash-out refinance | Income-eligible homeowners; no owner match required below 120% AMI; 1:1 match for 120–135% AMI |

| CDLI Plus One ADU Loan Product | Plus One ADU Grant municipalities on Long Island, NY (Babylon, East Hampton, Shelter Island, and Southampton) | Low-interest second mortgage up to $125,000; 4% or 6% interest (APR 4.84% or 6.909%) depending on household income | Must be approved for Plus One ADU Grant first; minimum credit score 625; income not greater than 100% AMI; second-lien structure |

| CalHFA ADU Grant (California) | California (statewide) | Previously $40,000 pre-development grant | Fully exhausted as of December 2023. CalHFA has posted a scam warning about parties claiming they can secure these grants for a fee. |

| Orange County Housing Finance Trust Affordable ADU Loan | Orange County, CA | — | Discontinued May 21, 2025. Per OCHFT's website, the board voted unanimously to discontinue the program; OCHFT is not aware of an alternative government-funded ADU financing program to recommend. |

How public-program economics actually work

A 1% construction loan from SDHC looks like an obvious win compared to a market construction loan. The math gets more complex when you factor in the 7-year affordability covenant: the rent you can collect is capped well below market for the covenant period. Whether the interest savings exceed the rent restrictions depends on three inputs you must model with your own numbers — your specific loan amount, your local market rent on the completed ADU, and the SDHC-published affordable-rent ceiling for your household-size and AMI bracket on the date you apply.

This is not a reason to reject SDHC’s program. It is a reason to model both scenarios honestly. The program is excellent for homeowners whose primary motivation is housing family, providing affordable housing in their community, or generating steady modest income, rather than maximizing rental yield.

Disclaimer: These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

For the comprehensive list of state and local ADU grants and incentives nationwide, see our ADU Grants 2026 guide.

How to apply: the 8-step path from research to keys

- 1

Confirm your ADU is legal on your lot

Pull local zoning records. Verify setbacks, lot size minimums, maximum ADU size, owner-occupancy requirements, parking rules. State laws may preempt city rules — California is the most aggressive example (Gov. Code § 66317). Free option: run our ADU feasibility report to get a starting-point summary.

- 2

Choose your ADU type

Detached, attached, garage conversion, basement conversion, or prefab/modular. This decision drives which loan products are available to you. National cost ranges by type: detached $150K–$350K+; attached $100K–$250K; garage conversion $50K–$150K; internal/basement $50K–$120K. See our guide to ADU types for a full breakdown. Add roughly 25–40% to any contractor base quote to capture soft costs and contingency.

- 3

Get preliminary plans and a contractor bid

You need at minimum a site plan, a floor plan, an exterior elevation, a line-item construction budget, and a proposed draw schedule. Two to three contractor bids gives you negotiating room and helps verify the budget is realistic.

- 4

Run the four-product matrix against your situation

Determine whether your fit is FHA 203(k), HomeStyle, CHOICERenovation, true C2P, or actually a HELOC. Do not apply for the wrong product — denial paperwork takes 30 days you cannot get back.

- 5

Pull the 24-document checklist

Get all borrower documents, project documents, and contractor documents in one folder before you call lenders.

- 6

Apply with 2–3 lenders for the same product

Comparison is the homeowner's leverage. Get loan estimates within the same 14-day window so credit pulls count as a single inquiry on your report.

- 7

Order the as-completed appraisal

Your lender orders this. If the appraisal comes in lower than your budget needs, you have three options: reduce the project scope, increase your down payment, or shop the appraisal with a different lender (lenders are not required to honor another lender's appraisal).

- 8

Close, pull permits within 30 days, and begin construction

Most renovation loans require construction to start within 30 days of closing. The draw process begins with the closing draw for permits, design, and deposits.

Lender-call script

When you call lenders, ask these questions in order before you give them your full financial picture:

- Do you offer construction-to-permanent, FHA 203(k) Standard, HomeStyle Renovation, and CHOICERenovation? Which is your specialty?

- Do you underwrite based on current value or as-completed value for ADU loans?

- Can ADU rental income be considered for qualifying? Under which program and what percentage?

- Do you require permits before application, before closing, or before construction starts?

- How many draws are typical on a $200K detached ADU? Who performs the draw inspections?

- Can deposits, permits, design, and materials be funded at closing?

- What happens if the appraisal comes in low?

- Can I preserve my existing first mortgage with a second-lien construction loan?

- Do you finance prefab, modular, or manufactured ADUs?

- Do you require the contractor to be pre-approved? What is your approval process?

- What reserves and contingency do you require?

- What is your current rate for the construction phase, and how does it convert?

A lender who cannot answer these clearly in 15 minutes is not the right lender for an ADU project.

Start with your lot, not a lender

Before you spend money on plans, permits, or lender applications, get a property-specific starting point: zoning eligibility, likely ADU types for your lot, and your closest financing lane.

See What You Can Build → Get Your Free ADU ReportHonest tradeoffs: when an ADU construction loan is the wrong call

Construction loans and renovation loans are more paperwork, more time, and more complexity than equity-based products. You will deal with appraisals on as-completed value (which can come back lower than your budget needs), inspections that delay draws, mandatory lien waivers, contingency reserves you must fund up front, and origination fees often higher than a HELOC. If you have 20%+ existing equity and a current mortgage rate you do not want to lose, a HELOC for ADU is almost always the simpler choice.

The construction-loan path is the right call when the equity is not there and you need to borrow against the as-completed value — not as a default option. If your situation is the HELOC scenario, this is not your page. We would rather you build the right way than convert a click.

What construction financing gives you that nothing else can: borrowing power on a home you have not yet improved. That is the entire reason this category of loan exists. If you bought your home in the last 1–5 years, lack the equity for a HELOC to cover the project, and want to build an ADU that will materially increase your property’s value and your monthly cash flow once rented, a construction or renovation loan is the only path that makes the math work.

Current ADU construction loan rate context

The Federal Reserve’s federal funds target range stands at 3.50%–3.75% following the April 30, 2026 FOMC meeting, after rate cuts at the January 29, March 19, and April 30 meetings. Mortgage rates are not set by the federal funds rate directly — they track the 10-year Treasury yield and lender-specific spreads — but Fed direction influences the broader curve over time.

Several major lenders offer extended rate locks specifically for new construction. Wells Fargo’s Builder Best Extended Rate Lock applies to newly constructed homes; Bank of America’s Builder Rate Lock Advantage and its Private Bank Construction-to-Permanent program offer extended locks under specific structures; and Alliant Credit Union offers tiered rate locks on construction loans. Product fit for adding an ADU to an existing primary residence specifically must be confirmed directly with each lender.

Frequently asked questions

Can you get a construction loan to build an ADU?

Yes. Multiple construction-style loan products are available for ADU construction, including conventional construction-to-permanent loans, FHA Standard 203(k) Rehabilitation Mortgages, Fannie Mae HomeStyle Renovation, and Freddie Mac CHOICERenovation. Each has different eligibility, ADU-type restrictions, and rental-income rules.

What is the difference between an ADU construction loan and a renovation loan?

A construction loan typically refers to a true short-term financing product that funds construction in draws and either pays off at completion or converts to a permanent mortgage. A renovation loan is a mortgage product (such as HomeStyle or CHOICERenovation) that bundles purchase or refinance plus renovation costs into one loan. In practice, both can fund ADU construction with draws and inspections.

What credit score do you need for an ADU construction loan?

FHA 203(k) Standard accepts FICO scores as low as 580 (with 3.5% down) or 500–579 (with 10% down). After Fannie Mae's November 2025 DU update, DU no longer requires a published minimum third-party credit score for HomeStyle, and Freddie's LPA Accept loans may not require a minimum Indicator Score — but individual lenders typically apply overlays of 620–680 and manual-underwriting matrices still apply. Conventional bank construction-to-permanent loans typically require 680+ FICO.

Can you use future rental income from an ADU to qualify?

Sometimes, depending on the program. FHA Standard 203(k) allows 50% of the appraiser's estimated rent for a new attached ADU to count as effective income, capped at 30% of total qualifying income, with 2 months of PITI reserves required. Fannie Mae's DU 12.1 release confirms ADU rental income may be considered on a one-unit principal residence purchase or limited cash-out refinance when requirements are met, also capped at 30% of total qualifying income. Freddie Mac CHOICERenovation generally does not allow projected ADU rent during construction because the lease cannot require payments to begin on a unit that does not yet exist.

How long does it take to close an ADU construction loan?

From a complete application to closing typically runs 30–45 days for conventional and FHA renovation products, or 45–60 days for a true bank construction-to-permanent loan. Permits often run in parallel. Total time from initial decision to keys runs roughly 9–18 months including the construction phase.

Can I finance a prefab or modular ADU with a construction loan?

Yes, with caveats. Most prefab and modular ADUs can be financed with conventional renovation loans or true C2P loans, provided the unit is installed as real property (permanently affixed to a foundation, classified as real property under state law, and properly insured). Fannie Mae's HomeStyle Renovation program specifically permits manufactured-home ADUs subject to the standard manufactured-home eligibility requirements. Some prefab models marketed as 'personal property' rather than real property may not qualify for traditional mortgage financing.

Will I have one closing or two?

A true construction-to-permanent (C2P) loan is a single closing — you close once at origination and the loan automatically converts to a permanent mortgage at completion. A construction-only loan is two closings — once at origination and again at completion when you obtain permanent financing. FHA 203(k), HomeStyle, and CHOICERenovation are all one-closing products.

What happens if the appraisal comes in lower than expected?

A low appraisal reduces the maximum loan amount. Your options: (1) increase your down payment to make up the gap, (2) reduce the project scope to fit the appraised value, (3) appeal the appraisal with comparable-sales support, or (4) order a second appraisal with a different lender (lenders are not required to honor another lender's appraisal). On Fannie Mae HomeStyle, the renovation cost cap is 75% of the applicable base, so a low appraisal can be a hard ceiling on your borrowing.

Can I be my own builder on an ADU construction loan?

Limited. Most conventional bank construction-to-permanent loans require a licensed general contractor and will not approve an owner-builder without verified construction experience and a backup contractor on standby. Fannie Mae HomeStyle permits DIY work on 1-unit properties limited to 10% of as-completed value, with lender approval required in advance and lender inspection of any item over $5,000.

Are construction loan rates higher than mortgage rates?

The construction-phase rate is typically higher than the corresponding permanent mortgage rate, reflecting the higher risk of an in-progress build. At conversion to permanent, the rate typically drops to the prevailing 30-year mortgage rate range.

Methodology

Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. For this guide, we reviewed primary-source documents from Fannie Mae (Single-Family Selling Guide sections B2-3-04 and B5-3.2-01, Announcement SEL-2025-10, DU 12.1 release notes), Freddie Mac (CHOICERenovation FAQ, Accessory Dwelling Unit FAQ), HUD (Mortgagee Letters 2023-17 and 2024-13, Handbook 4000.1 referenced via current AFR Wholesale and Plaza Home Mortgage product profiles), the Federal Reserve’s federal funds target range as of May 2026, and California Government Code § 66317.

Public-program information was verified directly against MassHousing’s ADULP page, the San Diego Housing Commission ADU Finance Program page, the City of Boston ADU Financial Assistance page (boston.gov), the City of Long Beach Backyard Builders Loan Program page, Community Development Long Island’s Plus One ADU Loan Product page, and Orange County Housing Finance Trust’s published status notice.

Forum threads on BiggerPockets and Reddit were reviewed for voice-of-customer language and common objections, not as proof for any lending, code, or regulatory claim. CFPB and FTC consumer guidance was reviewed for compliance framing.

This page contains no AI-generated rate quotes, no fictional borrowers, no fabricated testimonials, and no schema for content not visible on the page. We do not display fake review or rating schema.

Date of last research and verification: May 19, 2026.

Next scheduled re-verification: August 2026 (rates, Fed actions, program status); January 2027 (annual agency-rule and loan-limit update).

Disclosures

Financial disclaimer: This page is for educational purposes only and is not a loan offer, credit decision, financial advice, tax advice, or legal advice. We do not guarantee approval, loan terms, rates, monthly payments, rental income, property value increases, or ADU permit approval. Always confirm financing terms with a licensed lender and local requirements with your city or county planning department.

Projection disclaimer: These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

See what’s possible at your address

Get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU Report