ADU Grants in 2026: How to Get an ADU Grant (and What's Actually Still Open)

There is no easy, nationwide ADU grant waiting for you. California's famous $40,000 CalHFA grant — the one you probably searched for — has been fully allocated since December 2023 with no confirmed relaunch date. But ADU grants, forgivable loans, rebates, and fee waivers do still exist in scattered pockets across the country. New York City's Plus One program reopened in March 2026 with up to $395,000 in financial and technical support. Vermont offers up to $50,000 through its VHIP 2.0 forgivable loan. Boston gives qualifying homeowners a $7,500 soft-cost grant plus up to $50,000 in deferred 0% financing. Juneau, Alaska has rolling grants up to $13,500. Portland, Oregon waives system development charges worth thousands. And a dozen California cities have local programs still running even though the statewide program is closed.

We built this page to be the most complete ADU grant resource available — a verified, source-linked database of programs we've confirmed against official administering agencies, with honest status badges so you know what's open, what's closed, and what's just a waitlist. And because most homeowners won't qualify for or receive a grant, we also break down the financing paths that are actually funding ADUs across the U.S. every day.

Use the table below to check your state. If your program is closed, don't panic — skip to the financing section. Your ADU project isn't dead. You just need a different path.

Most ADUs in America are funded through home equity products and construction loans — not grants.

Editorial disclosure: The Dwelling Index is an independent educational publisher — not a lender, broker, or builder. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Read our full affiliate disclosure and editorial methodology

Most homeowners won't get a true cash ADU grant — and that's okay

Here's the honest admission we owe you before anything else: the phrase “ADU grant” is one of the most misleading search terms in residential construction.

Thousands of homeowners search for it every month expecting to find a pot of money that will meaningfully fund their backyard cottage or garage conversion. What they actually find is a patchwork of local programs — most of which are paused, limited to a few dozen recipients per year, restricted to specific income levels, or not really grants at all. They're forgivable loans with 10-year deed covenants. Or fee waivers worth a few thousand dollars on a six-figure project. Or reimbursements you collect after you've already paid.

That doesn't mean these programs are worthless. If you're in the right geography with the right income and the right timeline, some of them are genuinely helpful — especially for covering the pre-development soft costs (permits, architectural plans, engineering, soil tests) that surprise most first-time ADU builders.

But the honest picture is this: the vast majority of ADUs in America are funded through home equity products, construction loans, or savings — not grants. And understanding that upfront is the fastest way to move from “hoping for free money” to “actually building your ADU.”

So we're going to give you both paths. First, the verified grant and incentive programs we've confirmed. Then, the financing lanes that homeowners are actually using right now. Your job is to check the table, see if anything fits, and if not, find the financing path that matches your equity situation.

Verified ADU grants, loans, rebates, and incentives we've confirmed

This is the section that should end your search. We verified every program below against the official administering agency's website — not builder blogs, not marketing pages, not two-year-old articles. Each row includes a status badge, the type of help, the biggest restriction you need to know about, and a direct link to the source.

This is not an exhaustive list of every program in the country. New programs launch regularly, and some smaller city initiatives may not be listed here. If you know of a program we've missed, email our research team. We verify and add confirmed programs within 48 hours.

Status badge legend:

Statewide programs

| State | Program | Type | Max Amount | Status | Biggest Catch | Source | Verified |

|---|---|---|---|---|---|---|---|

| California | CalHFA ADU Grant | Grant (pre-development costs) | $40,000 | ⛔ Closed | Fully allocated Dec 2023. No relaunch confirmed. CalHFA warns of scammers claiming to help access funds. | CalHFA.ca.gov/adu | Apr 2026 |

| New York | Plus One ADU Program | Grants via local program administrators | Up to $125,000 | ⚠️ Limited | Funds flow through local program administrators (LPAs), not directly from state to homeowners. Select municipalities only. 10-year regulatory period. No short-term rentals. | hcr.ny.gov/adu | Apr 2026 |

| Vermont | VHIP 2.0 | 0% interest forgivable loan | Up to $50,000 | ✅ Open | Forgivable loan, not a pure grant. Reimbursement/draw basis. Must rent at or below fair market rate for 5–10 years. 20% match required (can be in-kind). | Vermont ACCD VHIP 2.0 | Apr 2026 |

| Colorado | ADUG via HB24-1152 | State grants to municipalities | Varies by municipality | ⚠️ Limited | Grants go to certified ADU Supportive Jurisdictions, not directly to homeowners. Homeowner benefit depends on local implementation. | dlg.colorado.gov | Apr 2026 |

| Colorado | CHFA ADU Finance Programs | Subsidized financing (not a grant) | Varies | ✅ Open | Lender-facing finance programs for residents of ADU Supportive Jurisdictions. Not a direct cash grant. | chfainfo.com | Apr 2026 |

| Massachusetts | MassHousing ADULP | State loan program (not a grant) | Up to $250,000 detached / $150,000 attached | ✅ Open | This is a loan program, not a grant. State-level ADU lending support for qualifying homeowners. | masshousing.com/adu | Apr 2026 |

City and county programs

| Location | Program | Type | Max Amount | Status | Biggest Catch | Source |

|---|---|---|---|---|---|---|

| New York City, NY | NYC Plus One ADU | Low/no-interest loans or construction grants + technical support | Up to $395,000 combined | ⚠️ Limited | Reopened March 18, 2026 with limited funding. Income-qualified. Must be owner-occupant of 1-3 family home. Confirm current intake window before applying. | nyc.gov/hpd |

| San Diego, CA | Housing Commission ADU Finance | Subsidized financing + technical help | Up to $250,000 | ⚠️ Limited | Owner-occupancy and affordability restrictions required. Check current funding availability — FY 2025 funds were limited. | adu.sdhc.org |

| Salt Lake City, UT | Backyard Keys ADU Loan | Low-interest loan | Varies | ✅ Open | Loan program administered by SLC Community Reinvestment Agency. Not a grant. Income and eligibility requirements apply. | cra.slc.gov |

| Lafayette, CA | SD7 ADU Accelerator Rebate | Rebate | Up to $7,500 / $15,000 (deed-restricted) | ✅ Open | Rebate, not upfront cash. Higher tier requires deed restriction for affordable rental. | lovelafayette.org |

| Walnut Creek, CA | ADU Acceleration Program | Rebate | Up to $7,500 / $15,000 (deed-restricted) | 📋 Waitlist | All rebates claimed as of July 2025. Backup list only. | walnutcreekca.gov |

| Dublin, CA | ADU Fee Waivers | Fee waiver | Varies (impact fee + permit fee savings) | ✅ Open | Available through December 2026. Deed restriction required for income-tier waivers. No short-term rental use. | dublin.ca.gov |

| Boston, MA | ADU Financial Assistance Program | Grant + deferred 0% loan | $7,500 grant + up to $50,000 loan | ✅ Open | Must attend both ADU Design and Budget Workshops. Must work with a licensed architect. Income-eligible. Requires advanced stage of readiness. | boston.gov/adu |

| Portland, OR | ADU SDC Waiver | Fee waiver | Varies (saves thousands in system development charges) | ✅ Open | Must agree to 10-year recorded covenant: no short-term rental use. | portland.gov |

| Portland, OR | Energy Trust of Oregon ADU Incentives | Performance incentive | Varies | ✅ Open | Energy-efficient new construction only. Must work with an approved EPS verifier during design and construction. | energytrust.org |

| Juneau, AK | ADU Grant Program | Grant | Up to $13,500 | ✅ Open | Rolling basis until all grants are awarded. Limited number available. Unit cannot be used as a short-term rental for 5 years. | juneau.org |

| Mad River Valley, VT | Mad River Valley Housing Coalition | Construction grant | Up to $10,000 | ✅ Open | Must rent at affordable rate for 5 years. | MRV Housing Coalition |

A note on California fee waivers

Many California cities offer ADU fee waivers or reductions, but specific terms, amounts, and deed-restriction requirements vary by jurisdiction. Check your local planning department website directly — Dublin, Vista, and several East Bay cities have current programs.

Don't see your city? New programs launch regularly. Check your local planning department website or contact your city's housing authority directly. Found a program we missed? Email our research team.

Before you chase grants

Find out what your property actually allows

Zoning rules determine what you can build — and some homeowners discover they can build more than they expected. Our free Feasibility Engine checks your address and gives you a personalized ADU report in 60 seconds. No phone call, no commitment, just clarity.

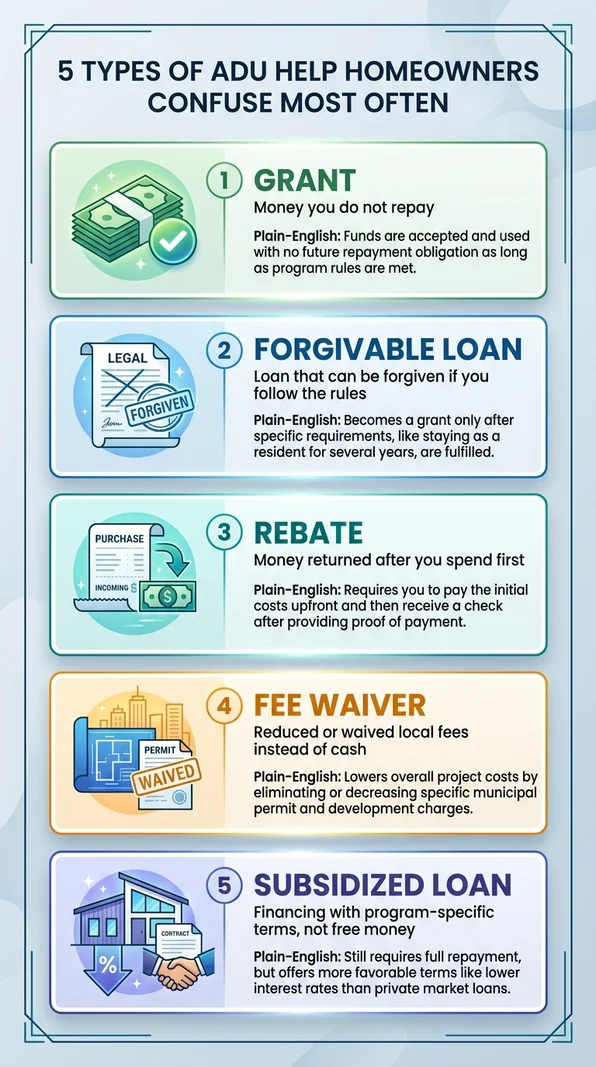

See What You Can Build → Get Your Free ADU Report“Grant” doesn't always mean what you think it means

Half the frustration homeowners feel about ADU grants comes from not understanding what kind of help they're actually looking at. The word “grant” gets thrown around loosely — by builder blogs, by marketing pages, sometimes even by the programs themselves. But the financial mechanics behind each type of assistance are very different.

| Type | What It Actually Means | Do You Repay? | Common Strings | Real Example |

|---|---|---|---|---|

| True grant | Cash or reimbursement you never pay back | No | Income limits, owner-occupancy, approved lender, typically covers only pre-development costs | CalHFA ADU Grant (CA) |

| Forgivable loan | Loan that gets forgiven IF you meet conditions over time | Forgiven if conditions met; repaid if broken | Must rent at affordable rates for 5–15 years, deed covenants, no short-term rentals | NY Plus One, Vermont VHIP |

| Rebate | Money returned to you after you've already paid | No (but you front the cost) | Must complete the project and submit proof of costs | Lafayette SD7 ADU Accelerator |

| Fee waiver | Government reduces or eliminates permit/impact fees | N/A (reduced cost, not cash) | May require deed restriction, no STR covenant, income qualification | Portland SDC Waiver, Dublin CA |

| Subsidized loan | Below-market-rate financing, sometimes with deferred payments | Yes | Income limits, affordability periods, occupancy requirements | San Diego, Boston ADU loan, MassHousing |

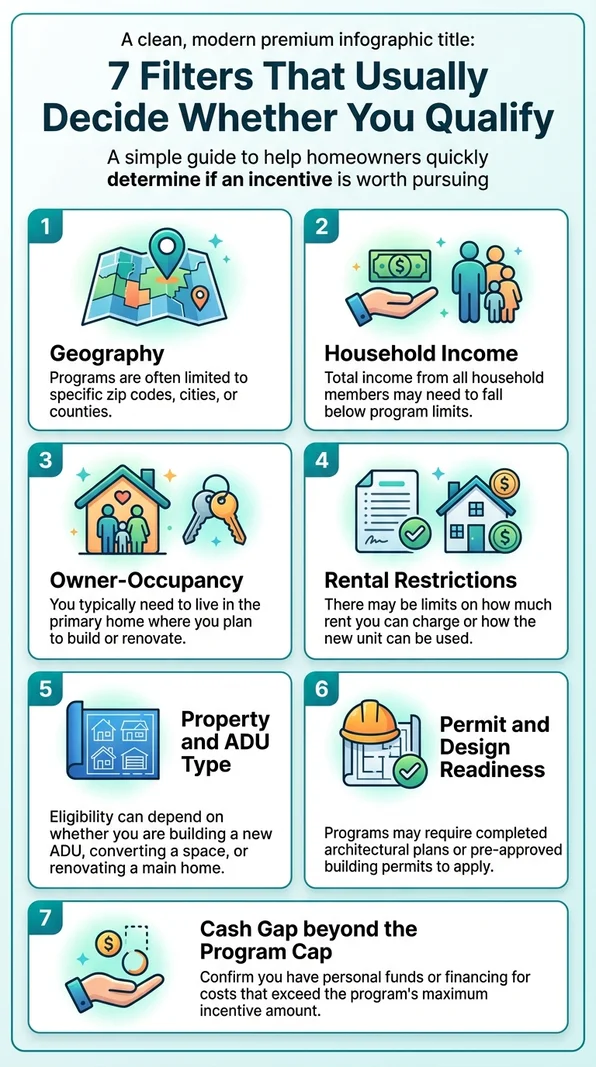

Do you actually qualify? The 7 filters that matter

Most grant rejections aren't mysterious. They come down to a handful of the same filters. Before you gather a single document or call a single lender, run yourself through these seven checks. If you can't clear all of them for a specific program, save yourself the time and look at the next option.

Geography

This is the biggest one. Most programs serve a single city, county, or state. Even statewide programs like New York's Plus One only operate through specific local program administrators in participating municipalities. If you're not in the right zip code, the program doesn't exist for you.

Household Income

Most grant programs target low-to-moderate-income homeowners, defined as a percentage of Area Median Income (AMI). The thresholds vary widely — what counts as "moderate income" in San Francisco is very different from rural Vermont. Always check the specific income limit for your county on the program's official page.

Owner-Occupancy

Nearly every ADU grant program requires you to live in the primary residence as your main home. Investment properties, LLC-owned properties, and vacation homes are almost universally excluded. Some programs require you to continue living there during and after construction.

Rental Restrictions

Many programs come with restrictions on how you can use the ADU — typically prohibiting short-term rental use, sometimes requiring the unit to be rented at or below fair market rates, and sometimes requiring a deed covenant that stays with the property through any future sale.

Property and ADU Type

Eligibility can depend on whether you are building a new ADU, converting an existing space (garage, basement), or renovating a main home. Some programs exclude JADUs or limit to specific ADU types. Confirm that your planned project type falls within the program's scope.

Permit and Design Readiness

Programs may require completed architectural plans or pre-approved building permits to apply. Boston requires applicants to be working with a licensed architect with draft or permitted plans before submission. CalHFA required plans before an appraisal could be ordered.

Cash Gap Beyond the Program Cap

Even a generous program covers only part of total project costs. Confirm you have personal funds or financing (HELOC, construction loan) to cover costs that exceed the program's maximum incentive amount. Going in without a gap plan is a common reason projects stall after award.

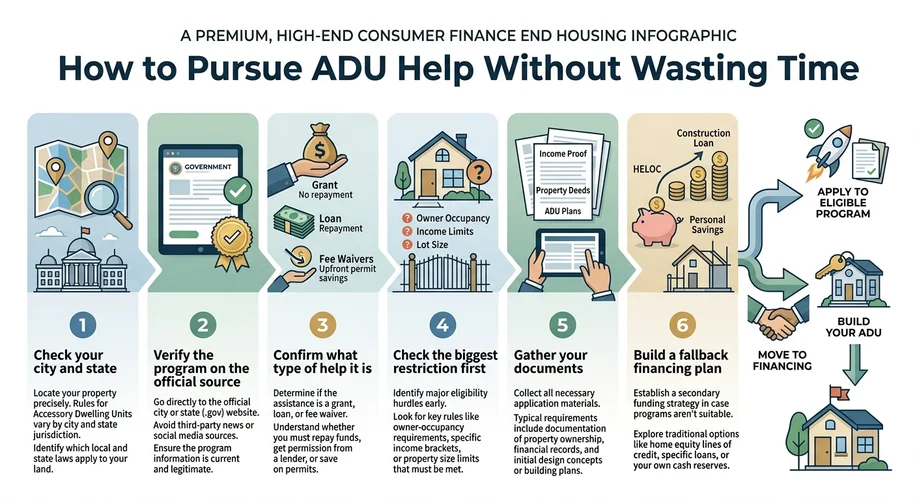

How to apply without wasting weeks on a dead program

The application process varies by program, but the fastest path always follows the same logic: verify first, gather documents second, apply fast.

Step 1 — Verify the program is accepting applications right now

Check the official administering agency website — not a builder blog, not a marketing page, not a two-year-old article. Programs pause, exhaust funding, and change rules without much fanfare. CalHFA's grant page still exists and still describes the program in detail, but the funding has been fully allocated since December 2023.

Step 2 — Confirm the program type before you celebrate

Is it a true grant, a forgivable loan, a rebate, or a fee waiver? The answer changes everything about your budgeting timeline. If it's reimbursement-based, you need to front the money. If it's a forgivable loan, you need to be comfortable with the deed covenant and rental restrictions for the full regulatory period. See the comparison table above.

Step 3 — Check the biggest restriction first

Don't gather 15 documents and then discover you need to rent the ADU at below-market rates for a decade, or that the program doesn't cover your ADU type, or that your LLC ownership structure disqualifies you. Identify the single biggest restriction and confirm you're okay with it before investing time.

Step 4 — Gather your documents

Most programs ask for: proof of ownership (recorded deed), income verification (W-2s, tax returns, pay stubs), a utility bill proving occupancy, preliminary ADU plans or scope of work with a budget, any existing permits or zoning approvals, and a contractor estimate. For programs requiring an approved lender (like CalHFA's structure), you'll apply for construction financing and the grant simultaneously through that lender.

Step 5 — Apply early and move fast

CalHFA's $100 million was fully allocated within roughly 18 months. When programs reopen or new rounds launch, funding depletes quickly. Juneau's program is rolling — once the grants are awarded, they're gone. NYC's Plus One reopened in March 2026 with a limited funding window. If you find an active program you qualify for, don't wait.

Step 6 — Build a fallback budget

Even if your application goes smoothly, most programs cover only part of the project. You need a plan for the gap between what the program provides and what the project actually costs. That's where the financing section below becomes critical.

What grants actually pay for — and what's still on you

When a program advertises “up to $40,000” or “up to $125,000,” it's natural to mentally subtract that from your total project cost. But the coverage is almost always narrower than the headline suggests.

What most programs cover

- Architectural plans and design drawings

- Permit fees and plan review fees

- Impact and development fees (often the largest soft cost in high-cost cities)

- Site survey and soil testing

- Energy reports and compliance documentation

- Environmental assessments, when required

- Construction loan interest rate buydowns (CalHFA model)

What's typically NOT covered

- Full construction labor and materials — the bulk of any ADU project

- Utility hookups and meter separation — can be a major budget surprise

- Electrical panel upgrades — required if existing panel can't support ADU load

- Sewer/septic connection — highly variable depending on site conditions

- Landscaping restoration — after heavy equipment works the backyard

- Contingency budget — most experienced builders recommend 10-15% above estimates

- Furnishing and finishing — if you're planning to rent, the unit needs to be move-in ready

Actual costs for these items vary widely by location, project scope, and contractor. Check our ADU cost guides for detailed breakdowns by project type.

Real numbers: what a grant actually means for your project budget

Let's make this concrete. Here's what a $40,000 grant (like CalHFA's, when active) actually looked like against typical project costs for a 500 sq ft detached ADU in a major metro area.

| Cost Category | Covered by a Pre-Development Grant? |

|---|---|

| Architectural plans & engineering | Yes |

| Permits & plan review fees | Yes |

| Impact/development fees | Yes |

| Soil test & site survey | Yes |

| Energy reports | Yes |

| Construction labor & materials | Not covered — this is the bulk of the project |

| Utility hookups & meter separation | Not covered — this is the bulk of the project |

| Electrical panel upgrade | Not covered — this is the bulk of the project |

| Landscaping restoration | Not covered — this is the bulk of the project |

| Contingency budget (10-15%) | Not covered — this is the bulk of the project |

In high-fee cities where impact fees alone can run well into five figures, a $40,000 grant could cover nearly all pre-development costs. But it doesn't fund the actual construction. That's why the financing paths below matter just as much as the grant table above.

The restrictions that surprise people after approval

Qualifying for a program is one thing. Living with the restrictions for 5, 10, or 15 years is another. These are the conditions we see homeowners underestimate most often.

“No short-term rentals” means exactly that

Portland's SDC waiver saves you real money on system development charges. But it comes with a 10-year recorded covenant prohibiting short-term rental use. If your plan was to Airbnb the ADU — or even to keep the option open — this waiver costs you that flexibility for a decade. Juneau's grant carries a similar 5-year restriction. And most Plus One communities and many California local programs require the same. (Source: portland.gov/ppd/residential-permitting/adu-sdc-waiver, verified April 2026)

Deed covenants and affordability periods are legally binding

Forgivable loans through programs like Vermont's VHIP and New York's Plus One come with regulatory agreements. For Plus One, the period is at least 10 years. During that time, compliance monitoring includes annual certifications and site visits every two years to confirm the ADU is used as permanent housing. Break the rules, and you may owe the full loan amount back. (Source: hcr.ny.gov/adu, verified April 2026)

Reimbursement timing can create a cash flow gap

Many programs don't hand you a check upfront. They reimburse you after you've incurred and documented costs — including VHIP 2.0, which operates on a reimbursement/draw basis. That means you need the cash (or a credit line) to cover expenses first, then submit invoices and wait for reimbursement. For homeowners already stretched thin, this timing gap is something to plan around.

Selling, refinancing, or changing your mind has consequences

If you sell the property during the regulatory period, most forgivable loans become immediately due. Some programs have clawback provisions that scale down over time (owe less in year 8 than in year 2), but others require full repayment regardless of timing. Refinancing can also trigger complications if the program placed a lien on the property. Always understand the exit conditions before you sign.

Can you stack multiple programs?

In theory, yes — some homeowners in certain geographies can combine multiple forms of assistance. A California homeowner in a participating county could potentially combine a local fee waiver with a city-level forgivable loan and standard construction financing. A Vermont homeowner could layer a VHIP forgivable loan with separate local grants. But each program has its own rules about stacking, and some explicitly prohibit it. Confirm with each program administrator individually.

The programs worth a closer look

If you've narrowed down a program from the table above, here's deeper detail on the ones that get the most searches and the most questions.

California — CalHFA ADU Grant ($40,000) — Currently closed

California's CalHFA ADU Grant was the most well-known ADU grant in the country, and the reason most people search for “ADU grant” in the first place. It offered up to $40,000 for pre-development costs — architectural plans, permits, site prep, soil tests, impact fees, energy reports, and interest rate buydowns on construction loans. The money was a true grant: no repayment required.

The program launched with $100 million in 2021 and was oversubscribed almost immediately. A second phase in 2023 added $25 million. By December 28, 2023, all funding was fully allocated. CalHFA's website currently says the program is not accepting applications, and there is no confirmed relaunch date.

If you're in California right now: The statewide grant is closed, but several local programs are active. San Diego's Housing Commission offers subsidized financing. Lafayette and parts of Contra Costa County offer rebates. Dublin and other cities have fee waiver programs. Don't write off California just because the headline program is paused.

Sources: CalHFA.ca.gov/adu, adu.sdhc.org, verified April 2026

New York — Plus One ADU Program (up to $125,000 statewide / $395,000 NYC)

New York runs the most ambitious ADU grant infrastructure in the country right now. The state's Plus One program, funded with $85 million over five years, provides support through local program administrators (LPAs) — nonprofit organizations and local governments that handle everything from design oversight to contractor selection to post-construction compliance monitoring.

At the state level, qualifying homeowners can receive up to $125,000 to build a new ADU or bring an existing one up to code. NYC launched its own Plus One program that reopened March 18, 2026, offering up to $395,000 in combined financial support and technical assistance for qualifying homeowners of 1-3 family homes.

The catch that trips people up: This is not a “fill out a form and get a check” program. Local program administrators manage the entire process. You must apply through your local LPA — not directly to the state. The regulatory period is at least 10 years, during which the ADU must be used as permanent housing (no short-term rentals). NYC's current intake has a limited funding window — confirm the timeline before applying.

Sources: hcr.ny.gov/adu, nyc.gov/hpd, verified April 2026

Vermont — VHIP 2.0 (up to $50,000 forgivable loan)

Vermont's Housing Improvement Program (VHIP 2.0) is one of the most frequently cited “ADU grants” on the internet — but it's important to understand what it actually is. According to Vermont's own official FAQ, VHIP 2.0 provides 0% interest forgivable loans, not pure grants. You can receive up to $50,000 per unit to cover the cost of building a new ADU or bringing a vacant/blighted rental unit back online.

The loan is forgivable if you meet affordability requirements for 5 to 10 years. You're required to provide a 20% match, which can be in-kind. Funds are disbursed on a reimbursement/draw basis. If you were already planning to rent the ADU at fair market rates, the rental requirement isn't really a restriction — it's what you were going to do anyway.

Source: Vermont ACCD VHIP 2.0 FAQ (PDF), verified April 2026

Colorado — HB24-1152 Municipal Grants + CHFA Finance Programs

Colorado took a different approach. When the state passed HB24-1152 legalizing ADUs statewide, it also appropriated grant funding — but the money goes to municipalities, not directly to homeowners. Cities and counties that become certified as “ADU Supportive Jurisdictions” can apply for grants to fund activities like developing pre-approved ADU plans, offsetting impact fees, and providing technical assistance.

The practical takeaway: If you're in Colorado, check whether your city has been certified as an ADU Supportive Jurisdiction and what specific incentives they've implemented. The state created the infrastructure — your city decides how it helps you. Separately, CHFA administers ADU Finance Programs through local lenders for residents of ADU Supportive Jurisdictions.

Sources: dlg.colorado.gov, HB24-1152, chfainfo.com, verified April 2026

Boston — ADU Financial Assistance Program ($7,500 grant + up to $50,000 loan)

Boston's program is one of the most structured — and most demanding — in the country. The Boston Home Center offers income-eligible homeowners a $7,500 soft-cost reimbursement grant to cover design and permitting expenses, plus access to a deferred 0% interest loan of up to $50,000 for construction costs.

Why it's harder to access than it sounds: You must attend both an ADU Design Workshop and an ADU Budget Workshop within 3 months of applying. You must be working with a licensed architect with draft or permitted plans ready. You need to be current on all city payments (property taxes, water, mortgage, insurance). And you can't have received City home repair financial assistance within the past 10 years.

Source: boston.gov/departments/housing/adu-financial-assistance-program, verified April 2026

Juneau, Alaska — ADU Grant Program (up to $13,500)

Juneau's grant program is one of the simplest in the country: a rolling, direct cash grant of up to $13,500 to qualifying homeowners building ADUs. Limited number available, awarded on a rolling basis until funds are exhausted. The primary restriction: the unit cannot be used as a short-term rental for 5 years.

Source: juneau.org, verified April 2026

What if the grant you wanted is paused, closed, or waitlisted?

This is where most ADU grant pages fail you. They tell you a program exists (or existed), maybe link to the application, and leave you hanging when you discover it's closed. We're not going to do that.

The honest reality: most homeowners who build ADUs do not receive grant funding. And thanks to a financing ecosystem that has expanded dramatically in the last few years, the options are better and more accessible than they've ever been. Here's how homeowners are actually paying for ADUs in 2026, organized by financial situation — not by who pays us more.

Disclosure: The Dwelling Index is an independent educational publisher — not a lender or broker. When you use our links to explore financing options, we may earn a commission at no extra cost to you. We organize financing by path (loan type and fit), not by compensation. Read our full affiliate disclosure

If you have strong home equity → HELOC

A Home Equity Line of Credit is a common path for homeowners funding ADUs. You borrow against the equity you've already built in your home, draw funds as needed during construction, and repay over time. If you have substantial equity and want flexible, draw-based access to funds, this is worth exploring.

Best for: Homeowners with strong existing equity who want flexible, draw-based funding.

Explore HELOC Options with FigureIf you have low current equity → Renovation HELOC

Standard HELOCs are based on your home's current value. But if your ADU will significantly increase your home's value, a renovation HELOC lends against the after-renovation value — meaning you can access equity that doesn't exist yet. This is a meaningful option for homeowners who know an ADU makes financial sense but don't have enough equity today to fund it through a standard product.

Best for: Homeowners with limited equity now but a clear path to higher home value after the ADU is built.

Explore RenoFi for Low-Equity ADU FinancingIf you can't take on monthly payments → Home equity investment

Not a loan. A home equity investment gives you cash now in exchange for a share of your home's future appreciation — with no monthly payments. You settle when you sell, refinance, or at the end of the term. Best for retirees, fixed-income homeowners, and aging-parent use cases where another monthly payment isn't feasible. Note: HEI companies have limited state availability — confirm your state is served.

Best for: Equity-rich homeowners who need cash without monthly payments.

If you need a construction loan or broader mortgage

For larger ground-up builds, construction-to-permanent loans release funds in draws as work is completed and inspected, then convert to a standard mortgage after the ADU is done. This is the traditional route for bigger detached ADU projects.

Best for: Larger detached ADU builds, complex projects, or homeowners who want everything in one loan structure.

Compare Construction Loan Lenders on LendingTreeFinancing Alternatives

While most grant programs are paused or limited, homeowners are building ADUs every day.

Your project doesn't depend on a government program. It depends on finding the financing path that matches your equity, income, and timeline — and most homeowners have more options than they realize.

Explore Your ADU Financing Options → See Which Path Fits Your SituationTax considerations worth discussing with your accountant

Even without a grant, ADUs can come with tax implications — some beneficial, some you need to plan for. We're not tax advisors, so treat this as a starting point for a conversation with your CPA or tax professional, not as tax guidance.

Depreciation. If you rent the ADU, you may be able to depreciate the structure on your federal taxes under the standard residential rental property framework. This can meaningfully reduce taxable rental income over time. (Consult IRS Publication 527 and your tax professional for current rules.)

Property tax reassessment. Adding an ADU may trigger a reassessment — but in many jurisdictions, only the ADU's added value is reassessed, not your entire property. California's Proposition 13 framework is one well-known example. Rules vary by state — check with your county assessor.

Grant tax treatment. If you receive a grant, it may be taxable income. CalHFA indicated it would issue Form 1099-G to grant recipients. Other programs may have different tax treatment. Confirm with a tax professional before budgeting around net grant proceeds.

Why so many ADU grant pages are wrong, stale, or misleading

If you've been searching for ADU grants for more than 10 minutes, you've probably noticed that half the pages you find contradict each other. One says California's grant is “still going strong in 2026.” The next says it's been closed since 2023. This isn't accidental.

Even official pages can lag

California's HCD (Housing and Community Development) still references CalHFA's homeowner grant on its ADU funding page. CalHFA's own website says the latest round was fully allocated in December 2023. Both are government sources. Both are technically “accurate” in their own context — one just hasn't been updated to reflect that the money is gone.

Builder blogs can be flatly wrong

At least one active page on the web right now claims California's ADU grant is “still going strong into 2026” — posted by a local construction company. CalHFA's own site directly contradicts this. If you're making financial plans based on a builder blog instead of the administering agency's official page, you could be budgeting around money that doesn't exist.

“Grant” often means something different than you think

One major ADU financing site lists Vermont's VHIP as a “grant” offering “up to $50,000.” Vermont's own official VHIP 2.0 FAQ describes it as a 0% interest forgivable loan with affordability requirements and a 20% match. Labels matter. The difference between a grant and a forgivable loan is the difference between free money and a multi-year commitment.

Is there a federal ADU grant?

Short answer: No. There is no broad federal program that gives individual homeowners grant money to build an ADU.

What does exist at the federal level is indirect support:

HUD HOME Investment Partnerships Program provides block grants to states and local governments. Some localities have used HOME funds to support ADU initiatives — but you can't apply to HUD directly as a homeowner. Your local housing authority decides how to allocate those funds.

FHA policy updates now allow projected ADU rental income to count toward mortgage qualification, which makes it easier to finance an ADU through standard FHA lending. This isn't a grant — it's a more ADU-friendly lending standard.

USDA proposed rule (March 2026) would allow guaranteed-loan financing on homes with income-producing ADUs, expanding rural ADU financing options. This is still in the proposed rule stage, not finalized.

The bottom line: federal ADU activity is mostly about removing financing barriers, not providing direct cash grants. State and local programs are where the direct financial assistance lives.

7 mistakes that get ADU grant applications rejected

If you've found an active program you qualify for, don't waste your shot. These are the most common reasons applications fail — and every one of them is avoidable.

Applying for a program that's paused

This sounds obvious, but it happens constantly. People find a blog post from 2023, follow the links, and submit paperwork to a program that's been closed for a year. Always start by checking the administering agency's official page for current status.

Not using an approved lender

Programs like CalHFA require you to work with a lender from their approved list. Applying through a non-approved lender disqualifies you automatically. Check the approved lender list before you start.

Submitting without ADU plans ready

Many programs require at least preliminary plans — architectural drawings, scope of work, and sometimes permits — before your application can move forward. CalHFA's process required plans before the lender could even order an appraisal.

Exceeding income limits

Important nuance: for some programs, the income limit is based on the individual borrower, not the entire household. For others, it's household income. Confirm which standard your target program uses, and check the specific AMI limit for your county.

Property owned by an LLC or trust

Most programs require individual homeowner ownership. Properties held by LLCs, corporations, or certain trust structures are typically excluded. If your property is in an entity, check with the program before applying.

ADU already has a certificate of occupancy

Most programs fund new construction, conversions, or additions that are not yet complete. If your ADU already has a CO, you usually can't apply retroactively.

Planning to use the ADU as a short-term rental

Programs that come with affordable-housing mandates or no-STR covenants will reject or claw back funding if you Airbnb the unit. If short-term rental income is core to your plan, most grant programs aren't compatible.

Most programs require preliminary architectural plans before you can even apply.

How we verify programs and keep this page accurate

This page is only useful if it's trustworthy. Here's how we maintain it.

Verification hierarchy: We check the official administering agency's website first — the .gov page, the housing authority portal, the program's actual application page. Local program administrator pages come second. PDF program documents, RFAs, and ordinance text come third. Third-party blogs and builder sites are used for context only, never as a source of truth.

Conflict resolution: When sources disagree — and they do, regularly — we defer to the current administering agency. If California HCD's page says a program exists and CalHFA's page says funding is exhausted, we report the program as closed and note the discrepancy.

Update frequency: We re-verify every program in our table quarterly and after any major legislative or funding announcement. The “Last Verified” column tells you exactly when we last checked each program.

Corrections: If you know of a program we've missed, a status that's changed, or an error in our data, email our research team. We'll verify and update within 48 hours.

These are illustrative program summaries, not legal or financial advice. Grant program terms, eligibility criteria, and availability are subject to change without notice. Always confirm details directly with the administering agency before making financial decisions.

ADU grant FAQ

Are ADU grants actually available in 2026?

Yes — but only in specific cities and states, and with significant limitations. NYC's Plus One reopened in March 2026. Vermont's VHIP is active. Juneau, Boston, Portland, and several California cities have programs. California's statewide CalHFA grant remains fully allocated with no confirmed relaunch. See our verified table above for the current picture.

Is the California ADU grant still available?

No. The CalHFA ADU Grant Program has been fully allocated since December 28, 2023. There is no confirmed date for new funding. CalHFA has posted warnings about scammers claiming to help homeowners access grant funds. Monitor CalHFA.ca.gov/adu for updates. (Verified April 2026)

Which states offer ADU grants or grant-like help?

Statewide programs exist in New York (Plus One, up to $125,000), Vermont (VHIP, up to $50,000 forgivable loan), Colorado (municipal grants via HB24-1152), and Massachusetts (MassHousing ADULP lending, up to $250,000). California's statewide program is paused, but multiple California cities have local programs. See the full tracker table above.

What is the $40,000 ADU grant everyone talks about?

That's California's CalHFA ADU Grant, which provided up to $40,000 for pre-development costs — architectural plans, permits, site prep, engineering, soil tests, impact fees, and energy reports. It was a true grant (no repayment required). It covered only soft costs, not construction labor or materials. The program is currently paused with all funding allocated.

Is there a federal ADU grant?

No. There is no dedicated federal ADU grant for individual homeowners. Federal support is indirect: HUD HOME block grants to localities, FHA policy allowing ADU rental income for mortgage qualification, and a proposed USDA rule for guaranteed-loan financing on homes with income-producing ADUs.

What's the difference between a grant and a forgivable loan?

A grant is money you never repay, period. A forgivable loan is money you don't repay if you meet specific conditions (like renting at below-market rates for 5-15 years). If you break the conditions, the loan becomes due. Vermont's VHIP and New York's Plus One are forgivable loan structures, not pure grants.

Can I use an ADU grant for a garage conversion or basement apartment?

It depends on the program. Most programs that fund ADUs will cover garage conversions and basement apartments as long as they meet local building codes and the program's definition of an ADU. Junior ADUs (JADUs) — smaller units typically under 500 sq ft within the existing home footprint — are eligible under some programs but not all. Check the specific program rules.

Can I combine a grant with a HELOC or construction loan?

In many cases, yes. CalHFA's program required you to have a construction loan from an approved lender — the grant literally piggybacked on the loan. Other programs may allow you to layer a rebate or fee waiver with private financing. Confirm with each program whether outside financing affects eligibility.

How do I find ADU grants near me?

Start with our verified table above. Then check your city or county's planning and housing department website directly. If you're in California, even though the statewide grant is paused, your city or county may have a local program — check with your local housing authority.

What documents do I need to apply for an ADU grant?

Most programs require some combination of: proof of ownership (recorded deed), income verification (W-2s, tax returns, pay stubs), a utility bill proving occupancy, preliminary ADU plans or scope of work with a budget, any existing permits or zoning approvals, and a contractor estimate. Some programs require an approved lender — check before gathering documents.

Can an ADU grant be used for rental income properties?

Almost never. Every ADU grant program we've reviewed requires owner-occupancy — you must live in the primary residence. Investment properties, LLC-owned properties, and vacation homes are universally excluded. Additionally, most grant programs prohibit short-term rentals of the ADU.

What if no ADU grant program exists in my area?

Most homeowners build ADUs without grants — through HELOCs, renovation HELOCs, home equity investments, construction loans, or savings. The financing ecosystem has expanded significantly and most homeowners have more options than they realize. See the financing section below for paths organized by your equity situation.

Free Resource

Want this grant tracker in a printable format — plus our ADU financing decision tree?

Our free 2026 ADU Starter Kit includes everything in this guide as a downloadable PDF, plus checklists and tools we didn't have room for here. Over 5,000 homeowners have downloaded it.

Download the Free 2026 ADU Starter Kit →What to do right now

If a program is open in your area and you qualify

Apply fast. Funding is always limited and competition is real. Use our table to find the official link, confirm the program type and restrictions, gather your documents, and submit. CalHFA's $100 million was gone in 18 months. NYC's intake window won't last forever.

If your program is closed, waitlisted, or doesn't exist for your area

That's the situation most homeowners are in, and it's completely workable. ADUs were being built long before grant programs existed. The financing ecosystem is more accessible than it's ever been. Find the lane that fits your equity situation in our ADU Financing Options Guide, and your project moves forward regardless of what any government program does.

If you're trying to reduce costs on the build itself

Grants aren't the only path to a more affordable ADU. Garage conversions cost less than ground-up detached builds. Pre-approved ADU plans eliminate thousands in architectural fees. And prefab/modular construction can significantly reduce both cost and timeline. Compare prefab ADU companies.

If you're not sure what your property even allows

Start there. Zoning, setbacks, lot coverage, height limits, and local regulations determine what's possible before financing even enters the picture.

Not sure where to start? See what's possible at your address.

Get your free personalized ADU report in 60 seconds. No phone call, no commitment, just clarity.

Get Your Free ADU Report →Continue your ADU research