Cash Out Refinance for ADU: The 2026 Rate Trap, Real LTV Math, and When It Backfires

By The Dwelling Index Editorial Team · · Last verified May 19, 2026 · 22-min read

Independent ADU resource · Not a lender or broker · Editorial standards →

The bottom line

A cash out refinance for an ADU works when three conditions line up: your current first-mortgage rate is at or above today's market, your home's current appraised value gives you enough room to fit the project inside an 80% LTV cap (100% on VA, with most lenders overlaying to 90%), and you don't depend on projected ADU rental income to qualify. When any of those three break — most commonly because the homeowner locked a sub-5% rate between 2020 and 2022 — cash out can cost $200,000–$320,000 more than keeping the existing mortgage and adding a second-lien product. This guide works through the math, the agency rules, and the cases where cash out genuinely wins.

Confirm your lot is buildable before you borrow

Setbacks, lot coverage, height limits, fire-zone rules, and owner-occupancy requirements decide what your ADU can be — and what it will appraise for.

See What You Can Build → Get Your Free ADU Report

Should you use a cash out refinance for your ADU? The verdict table

Find your row. The table below gives a fast verdict and points you to the first alternative to test.

| Your situation | Cash out refi verdict | Why | First alternative to test |

|---|---|---|---|

| Current first-mortgage rate is meaningfully below today's market (sub-5%, locked 2020–2022) | Usually a poor fit | You'd reprice your entire balance just to borrow the ADU portion | HELOC or home equity loan |

| Current rate is near or above today's market (6.5%+) | Possible fit | Limited or no penalty for replacing the mortgage | Cash out refi vs. home equity loan side-by-side |

| Home is paid off or nearly paid off | Strong fit | No favorable first mortgage to protect | Cash out refi vs. HELOC for flexibility |

| ADU budget fits inside (home value × 80%) − payoff − closing costs | Eligible to consider | Borrowing room exists | Run the rate-reset math |

| ADU budget exceeds current-value borrowing room | Poor fit | Cash out uses today's value, not future value | Construction loan, HomeStyle, CHOICERenovation, or FHA 203(k) |

| You need projected (not-yet-built) ADU rent to qualify | Disqualifying | Agency rules exclude standard cash out refis from the ADU-rent carve-out | HomeStyle on a purchase or limited cash-out, or build first and refi later |

| VA-eligible homeowner needing more than 80% LTV | Best-in-class agency option | VA cash out is the only mainstream agency-backed cash out path that allows up to 100% LTV | VA cash out refinance (covered in detail below) |

| ADU already built, legal, and rented for 12+ months | Possible recoup tool | As-is value supports the loan if you qualify without relying on the cash-out ADU-rent carve-out | Standard cash out refi if you can qualify on income alone |

| Texas homestead property | Not available with VA or FHA | Texas Constitution Section 50(a)(6) prohibits FHA cash out; Texas AG Opinion KP-0183 precludes VA cash out | Texas Section 50(a)(6) conventional cash out, capped at 80% |

| Unpermitted or non-conforming ADU on the property | Conditional | Lenders and appraisers care whether the ADU is legal, legal-nonconforming, or fully outside zoning | Legalize or document status first; then refinance |

This table is editorial guidance based on the verified agency rules cited below. It is not a loan offer or a guarantee of approval. Eligibility depends on lender underwriting, credit, DTI, appraisal, occupancy, property type, and state law.

What we verified for this guide

- Fannie Mae cash out refinance rules in Selling Guide B2-1.3-03, B2-3-04, and the 2026 Eligibility Matrix.

- Fannie Mae ADU expansion in SEL-2025-10 (Dec 10, 2025; effective March 31, 2026 only for lenders using UAD 3.6 policy).

- Fannie Mae ADU rental income rules in Selling Guide B3-3.8-01 and DU 12.1 release — scoped to purchase and limited cash-out only, not standard cash-out.

- FHA cash out 80% LTV in HUD Mortgagee Letter 2019-11 (effective Sept 1, 2019; still current); FHA ADU rules in HUD Mortgagee Letter 2023-17, including explicit prohibition on ADU rental income for cash out qualifying.

- VA cash out refinance rules in the VA Cash-Out Refinance User Guide and 2026 VA funding fee schedule.

- Texas Constitution Section 50(a)(6) and Texas AG Opinion KP-0183 — VA cash out precluded on Texas homesteads; FHA cash out also unavailable.

- FHFA 2026 conforming loan limits — $832,750 baseline, $1,249,125 high-cost.

- Live benchmark rates as of May 17–18, 2026: Bankrate 30-yr fixed refinance APR 6.76% (May 18); Bankrate 30-yr cash out reference range 6.5–7.0%; Curinos HELOC national average 7.21%, HELOAN 7.36% (May 17); WSJ prime rate 6.75% (May 17). Re-verify before relying.

- IRS Publication 936 — home mortgage interest deductibility, including the buy/build/substantially-improve rule.

Last verified: May 19, 2026. Next scheduled review: June 19, 2026 for benchmark rates; August 19, 2026 for agency-rule review.

What is a cash out refinance for an ADU?

A cash out refinance for an ADU replaces your existing first mortgage with a new, larger first mortgage and pays you the difference as a lump sum, which you use to fund accessory dwelling unit construction. ADU construction is a fully compliant home-improvement use of cash out proceeds under conventional, FHA, and VA guidelines, and unlike a renovation loan or construction loan, it doesn't require lender-managed construction draws or progress inspections.

The mechanics are simple. On a $700,000 home with a $400,000 existing mortgage and an 80% conventional cash out cap, the new loan can reach $560,000. After paying off the $400,000 first mortgage and roughly $15,000 in closing costs, the homeowner walks away with about $145,000 in cash for the ADU. The new mortgage payment is calculated on the full $560,000 balance — including the $400,000 of old debt now repriced at today's rate.

That repricing is the entire question. A cash out refinance is not a way to "borrow extra against your home." It is a complete reset of your first mortgage. Every other decision flows from it.

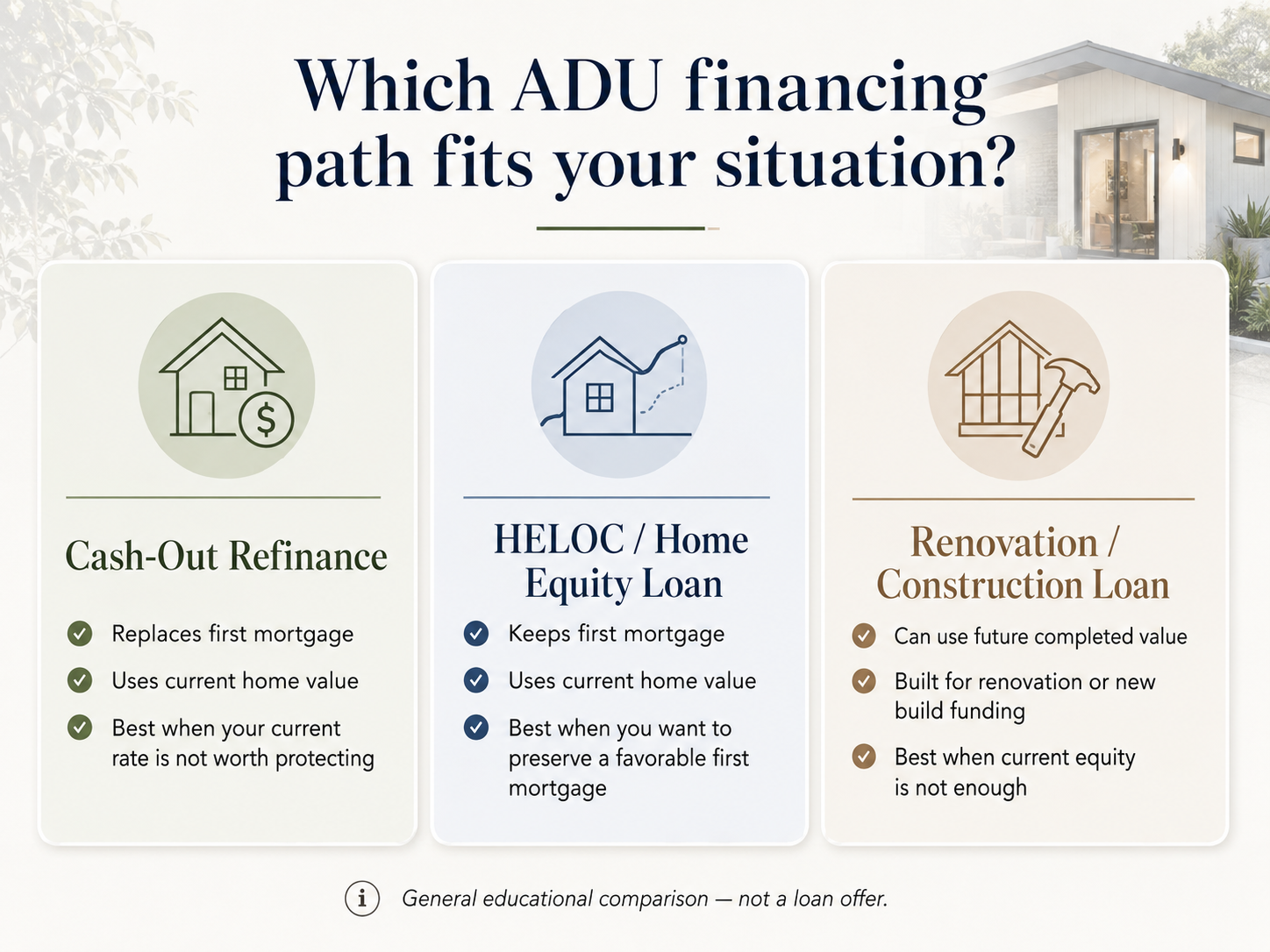

How a cash out refinance differs from other ADU financing paths

Three of the seven mainstream ADU financing paths use your home's current value. Four use the future value after the ADU is built. The distinction matters more than the loan name.

| Path | Replaces 1st mortgage? | Underwrites against | LTV cap (1-unit primary) | Reference rate, May 2026 | Best ADU use case |

|---|---|---|---|---|---|

| Cash out refinance | ✅ Yes | Current value | 80% conventional/FHA; 100% VA (lenders typically overlay to 90%) | 30-yr fixed refi 6.76% (Bankrate, May 18, 2026); cash out adds ~0.25–0.50% typical | Existing high-rate or paid-off home; recoup after ADU completion |

| HELOC | ❌ No | Current value | 80–85% CLTV | 7.21% national avg (Curinos, May 17, 2026) | Phased builds; preserves favorable first mortgage |

| Home equity loan | ❌ No | Current value | 80–85% CLTV | 7.36% national avg (Curinos, May 17, 2026) | Fixed lump sum; preserves favorable first mortgage |

| Construction-to-permanent loan | Often yes | Future value | Varies by lender | ~7%–9% range | Ground-up detached new build with insufficient current equity |

| Fannie Mae HomeStyle / Freddie Mac CHOICERenovation | ✅ Yes | Future value | Up to 95% on purchase | ~6.8%–7.5% range | Buying-plus-building, or refi-plus-build with low equity |

| FHA 203(k) | ✅ Yes | Future value | Up to 96.5% on purchase | ~6.5%–7.5% range | Lower credit, conversion-heavy scope |

| Home equity investment (HEI) | ❌ No | Current value | Provider-specific | No required monthly payment | Cannot carry another monthly payment; accept appreciation sharing |

Rates shown are reference benchmarks from publicly visible sources on the dates noted, not loan offers. Rates move daily; always verify with a licensed lender.

For the full seven-path comparison, our How to Finance an ADU in 2026 guide compares all paths side by side. For a deep dive on HELOC specifically, see our Best HELOC for ADU guide.

When does a cash out refinance make sense for ADU construction — and when doesn't it?

A cash out refinance makes sense when replacing your current first mortgage costs you little or nothing in rate, your current-value equity covers the ADU budget, and you can qualify without depending on projected ADU rental income. It doesn't make sense when you'd give up a meaningfully below-market mortgage rate, when your current equity is insufficient, or when the project only works because future ADU rent counts toward qualifying.

This is the most important section on the page. Most ADU-curious homeowners arrived at this search after a builder quoted a number that exceeded their savings, and a lender's first instinct is to pitch a cash out refinance because it's the simplest product to sell. The math frequently disagrees.

The 30-year dollar cost of replacing a low-rate first mortgage

We modeled the same scenario across four existing-rate situations: a homeowner with a $700,000 home, a $400,000 existing mortgage, and a $200,000 ADU budget. Option A is a cash out refinance to $600,000 at an illustrative 6.85% APR (reflecting May 2026 reference cash-out levels). Option B keeps the existing first mortgage and adds a HELOC for the $200,000 ADU portion, modeled at a fixed 7.21% for apples-to-apples comparison.

| Your existing first-mortgage rate | Option A — Cash out refi: total interest over 30 yrs on $600K @ 6.85% | Option B — Keep $400K existing + $200K HELOC @ 7.21%: total interest over 30 yrs | Cost of choosing cash out refi |

|---|---|---|---|

| 3.00% (typical 2020–2021 lock) | ~$815,360 | ~$496,325 | +$319,035 |

| 4.00% (typical 2019 or early-2022 refi) | ~$815,360 | ~$576,693 | +$238,667 |

| 5.50% (typical 2018–2019 purchase) | ~$815,360 | ~$706,831 | +$108,529 |

| 7.00% (post-2022 buyer) | ~$815,360 | ~$847,251 | −$31,891 (cash out wins) |

Illustrative only. Calculations assume 30-yr fixed amortization, 6.85% cash-out APR as an illustrative input within May 2026 reference levels, and a HELOC modeled at fixed 7.21% for comparability — real HELOC payments vary with prime rate. Closing costs excluded to isolate the rate effect. Not a loan offer.

The 3.00% homeowner pays roughly $319,000 more in interest over the life of the loan by choosing the cash out refinance. That is not closing costs — it is the pure cost of repricing $400,000 of old, low-rate debt to today's rate just to access $200,000 of new ADU money. The break-even sits between 5.50% and 7.00%.

The reframe that most pages miss: what percentage of your new loan is just old debt?

When a lender quotes you a cash out refinance, ask one question: of every dollar in the new loan, how many are new money for the ADU, and how many are old mortgage debt being repriced?

| Existing mortgage balance | ADU cash needed | New cash out loan | Old mortgage as % of new loan | What it means |

|---|---|---|---|---|

| $400,000 | $150,000 | $550,000 | 73% | $0.73 of every new-loan dollar reprices old debt to today's rate. Bad math unless your existing rate is already at market. |

| $600,000 | $200,000 | $800,000 | 75% | Same problem, larger scale. A second-lien product almost always wins. |

| $200,000 | $200,000 | $400,000 | 50% | Half the new loan is old debt. Worth running the full comparison. |

| $100,000 | $250,000 | $350,000 | 29% | The new loan is mostly ADU money — cash out becomes more plausible. |

| $0 (home paid off) | $300,000 | $300,000 | 0% | Pure ADU borrowing. Cash out competes well with a home equity loan. |

The cleanest cases where cash out refi for an ADU wins

- Your existing first-mortgage rate is at or above today's cash out APR. If you're locked at 7.25%+, replacing the mortgage costs you nothing in rate and may improve it.

- You own the home free and clear. No mortgage to preserve, so the only cost is the new loan's rate and closing costs.

- You're VA-eligible. The VA cash out refinance is the only mainstream agency-backed cash out path that allows up to 100% LTV. No HELOC or home equity loan reaches that ceiling.

- You were already planning a rate-and-term refinance. Adding cash out to a refinance you were doing anyway changes only the LLPAs, not the full rate decision.

- Your existing mortgage is an ARM nearing its first reset to a rate likely to exceed today's cash out APR.

- You're consolidating significant high-interest debt at the same time as the ADU spend, and the blended cost of the consolidated cash out beats keeping the high-interest debts separate.

The cases where cash out refi almost always loses

- Sub-5% first mortgage locked in 2020–2022. Per Redfin data reported by Fortune, 82.8% of mortgaged U.S. homeowners had rates below 6% as of Q3 2024. For nearly all of them, replacing the mortgage costs more than the ADU.

- Insufficient current equity. Cash out underwrites against today's value. If your project budget needs the post-construction value to work, you are in renovation- or construction-loan territory.

- You need projected ADU rent to qualify. Fannie Mae's expanded ADU rental-income rule (DU 12.1, March 21, 2026) applies only to purchase and limited cash out refinance — not standard cash out. FHA prohibits ADU rental income on cash out under HUD ML 2023-17.

- Short expected hold period. Closing costs of 2–5% don't recoup if you sell within 36 months.

- Appraisal risk. Markets with limited comparable ADU sales can produce conservative valuations that shrink your borrowing room below the project budget.

Confirm your lot is buildable before you commit to any financing path.

See What You Can Build → Get Your Free ADU ReportHow much equity do you need for a cash out refinance to fund an ADU?

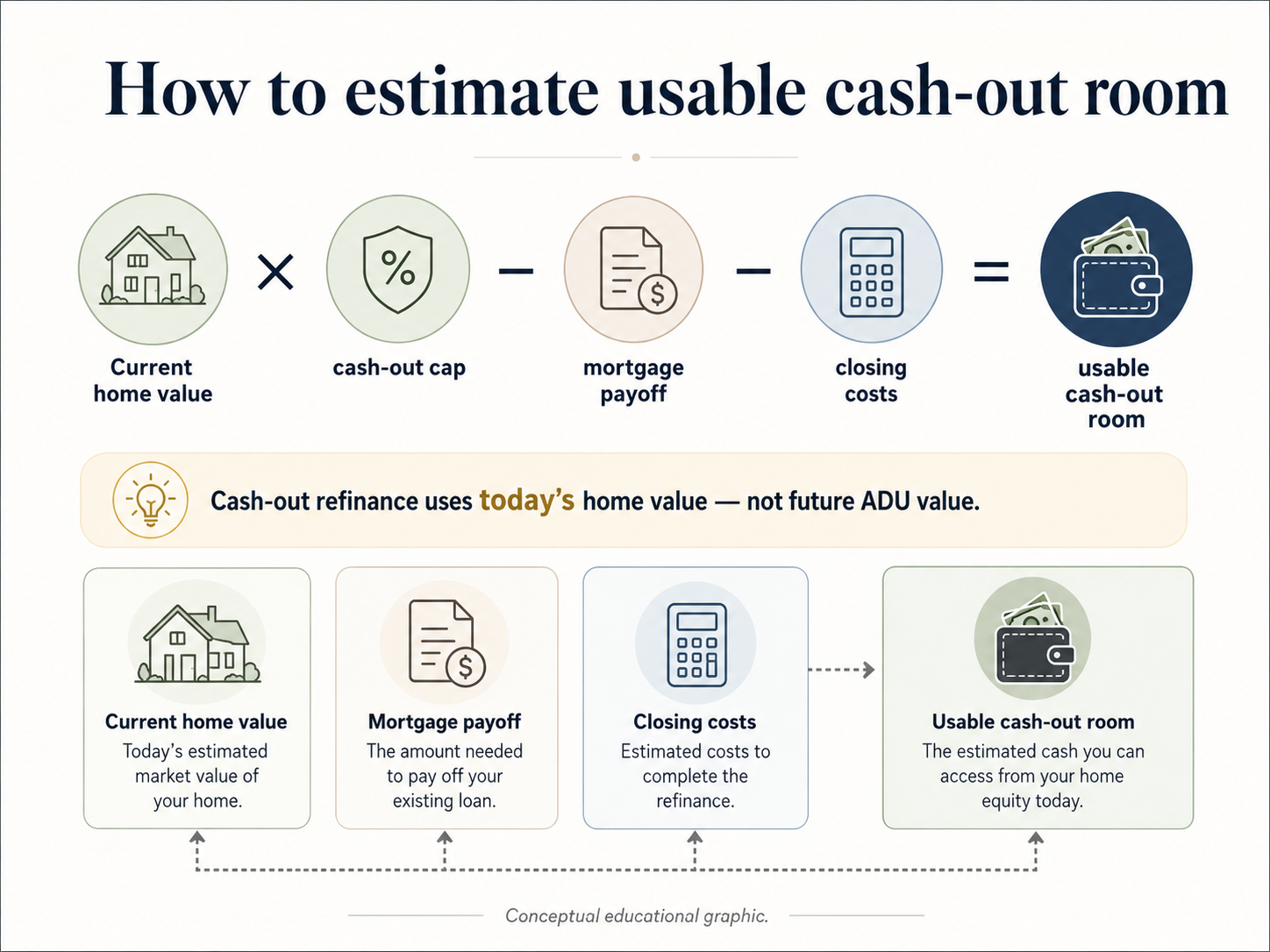

For a single-unit primary residence, you need to retain at least 20% equity after the refinance closes — meaning the new total loan cannot exceed 80% of the home's current appraised value under both conventional (Fannie Mae and Freddie Mac) and FHA rules. The practical formula is: (current appraised value × 0.80) − existing mortgage payoff − closing costs = cash available for your ADU. VA cash out can reach 100% LTV (most lenders cap at 90% via overlay). Two-to-four-unit primary residences cap at 75% conventional. Investment properties drop further.

The 80% cap is the most important number on this page. It is hard, program-wide, and has been the rule since FHA Mortgagee Letter 2019-11 brought FHA into alignment with Fannie Mae and Freddie Mac in September 2019. As of May 2026, it has not changed.

Worked equity-room examples on a 1-unit primary residence

| Home value | Existing mortgage | 80% LTV cap | Cash before closing costs |

|---|---|---|---|

| $500,000 | $250,000 | $400,000 | $150,000 |

| $600,000 | $300,000 | $480,000 | $180,000 |

| $700,000 | $400,000 | $560,000 | $160,000 |

| $800,000 | $400,000 | $640,000 | $240,000 |

| $900,000 | $500,000 | $720,000 | $220,000 |

| $1,000,000 | $550,000 | $800,000 | $250,000 |

| $1,200,000 | $600,000 | $960,000 | $360,000 |

Subtract approximately 2–5% of the new loan amount for closing costs. CFPB data places average refinance closing costs near $4,979 in recent years. Real costs vary by state, lender, and loan size.

Compare those cash-out room numbers against real ADU costs. Our ADU Cost Per Square Foot guide and How Much Does an ADU Cost? show garage conversions running $80,000–$175,000 nationally, attached ADUs $150,000–$300,000, and detached new builds $200,000–$400,000+. A $700,000 home with a $400,000 existing mortgage and $160,000 of cash-out room can cover most conversions but will fall short of a typical detached new build in a higher-cost market.

The full 2026 LTV matrix by loan program and property type

| Program | 1-unit primary | 2-unit primary | 3–4 unit primary | Second home | 1-unit investment | 2–4 unit investment | Ownership / seasoning | Primary source |

|---|---|---|---|---|---|---|---|---|

| Conventional (Fannie Mae) | 80% | 75% | 75% | 75% | 75% | 70% | At least 6 months on title; 12 months between note dates when paying off existing first lien (subject to exceptions) | Fannie Mae 2026 Eligibility Matrix |

| Conventional (Freddie Mac) | 80% | 75% | 75% | 75% | 75% | 70% | At least 6 months on title; 12 months between note dates when paying off first lien | Freddie Mac Guide 4301.5 |

| FHA | 80% | 80% | 80% | Not eligible | Not eligible | Not eligible | 12 months occupancy + 12 months on-time payments | HUD ML 2019-11 |

| VA | 100% (lenders typically overlay to 90%) | 100% (with overlays) | 100% (with overlays) | Not eligible | Not eligible | Not eligible | 210 days + 6 payments if refinancing existing VA loan | VA Cash-Out Refinance User Guide |

| Fannie Mae manufactured housing | 65% (multi-width only; single-width not eligible for cash out) | N/A | N/A | Not eligible for cash out | Not eligible | Not eligible | 12 months ownership of home and land | Fannie Mae B5-2-03 |

| Jumbo (non-conforming) | 70–80% | 65–75% | 65–70% | 60–70% | 60–70% | 60–65% | Lender-specific | Individual lender overlays |

| USDA | Not available | — | — | — | — | — | — | USDA HB-1-3555 |

Verified May 17–19, 2026. Individual lender overlays may impose stricter caps. Always confirm with a licensed lender. Texas homestead properties are not eligible for FHA or VA cash out refinance.

The appraisal trap most ADU borrowers don't see coming

A cash out refinance appraisal uses your home's current value — not the higher value the home will have after the ADU is built. Plans, contractor bids, and projected post-construction values do not change a cash out refi appraisal. If your borrowing room comes up short, the lender cannot "factor in what the home will be worth." You are capped at today's value. The two ways around it: bring more cash to closing, or switch to a future-value product — a construction-to-permanent loan, Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, or FHA 203(k).

Cash out refinance vs. HELOC, home equity loan, and renovation loan for an ADU

For most ADU homeowners with a sub-5% first mortgage, a HELOC or home equity loan beats a cash out refinance because second-lien products preserve the favorable first-mortgage rate. Cash out wins when the existing rate is at or above today's market or when consolidating to a single payment matters more than the rate differential. Renovation loans beat both when current equity is insufficient — because they underwrite against the home's projected as-completed value.

| Your situation | Cash out refi | HELOC | Home equity loan | Construction loan | Renovation loan |

|---|---|---|---|---|---|

| Existing rate < 5%, sufficient equity | ❌ Loses on math | ✅ Best fit | ✅ Strong fit | ❌ Refi required | ❌ Refi required |

| Existing rate ≥ 6.5%, sufficient equity | ✅ Strong fit | ⚠️ Workable | ⚠️ Workable | ❌ Complex | ⚠️ Workable |

| Home paid off or nearly paid off | ✅ Strong fit | ⚠️ Available | ✅ Strong fit | ❌ N/A | ⚠️ Available |

| Insufficient current equity, strong income | ❌ Room too small | ❌ Same problem | ❌ Same problem | ✅ Strong fit | ✅ Best fit |

| VA-eligible, need 80%+ LTV | ✅ Up to 100% | ❌ Not VA | ❌ Not VA | Limited | Limited |

| Buying property + building ADU | ❌ Doesn't apply | ❌ Doesn't apply | ❌ Doesn't apply | ⚠️ Possible | ✅ Best fit |

| Phased build over many months | ⚠️ Lump sum upfront | ✅ Draw as needed | ⚠️ Lump sum | ✅ Built around draws | ✅ Built around draws |

| Need projected ADU rent to qualify | ❌ Not eligible | ❌ Not eligible | ❌ Not eligible | Lender-specific | ⚠️ HomeStyle purchase/limited cash-out only |

| Lower credit (580–620) | ⚠️ FHA 80% LTV | ⚠️ Tighter overlays | ⚠️ Tighter overlays | Limited options | ✅ FHA 203(k) accepts 580 |

For the full path-by-path mechanics, see HELOC for ADU and How to Finance an ADU in 2026.

Affiliate disclosure applies to the following link.

Compare current cash out refinance and renovation-loan options

Explore mortgage-backed ADU financing options →Via Mortgage Research Center. We may earn a commission; you pay nothing extra. Full disclosure.

Can ADU rental income help you qualify for a cash out refinance?

On a standard cash out refinance, the answer is almost always no — and this rule kills more ADU cash out plans than any other. Fannie Mae's expanded ADU rental-income carve-out, automated in DU 12.1 on March 21, 2026, applies only to purchase and limited cash out refinance transactions on a one-unit principal residence with an existing ADU, capped at 75% of gross rent and 30% of total qualifying income. Standard cash out refinances are explicitly excluded. FHA prohibits ADU rental income on all cash out refinance transactions under HUD Mortgagee Letter 2023-17.

The agency-by-agency rental-income matrix for cash out refi

| Agency / program | Existing ADU rent for qualifying? | Projected (not-yet-built) ADU rent? | Standard cash out refi specifically? | Primary source |

|---|---|---|---|---|

| Fannie Mae | Yes: 75% of gross rent, capped at 30% of total qualifying income, from one ADU on a 1-unit primary residence | ❌ No | Not on standard cash out — purchase and limited cash out only | Selling Guide B3-3.8-01 |

| Freddie Mac | Yes: 75% of lease, capped at 30% of total income, on a 1-unit primary; illegal ADU rent excluded | ❌ No (must be existing, legal) | Not on cash out — purchase and no-cash-out only | Freddie Mac ADU Fact Sheet |

| FHA standard | 75% of lesser of fair-market rent or lease (with prior rental history) | 50% on Standard 203(k) prospective only — not cash out | ❌ Explicitly prohibited on cash out refi | HUD ML 2023-17 |

| VA | Lender-discretion; documented rental history may count | ❌ Generally not allowed | Lender-specific; commonly not allowed on cash out | VA Cash-Out Refinance User Guide |

Verified May 17, 2026 against the cited primary sources.

What this means for your project

If your DTI math relies on counting the future ADU rent, cash out refi is not your path. You have three workable alternatives:

- Build the ADU first using a HELOC, home equity loan, or HEI, rent it for 12 months, then cash out refinance later — at that point the unit is "existing" rather than "projected."

- Use Fannie Mae HomeStyle Renovation on a purchase or limited cash out — a different transaction type where the ADU rental-income carve-out applies.

- Use a construction-to-permanent loan with a lender that accepts projected rent at underwriter discretion. Rare. Lender-specific. Usually requires strong credit and reserves.

Once the ADU is built and rented, property management platforms handle rent collection, tenant screening, and tax-ready documentation. Explore property management options for your future ADU → (via Buildium — affiliate disclosure applies.)

Rental income examples are illustrative, not guarantees. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

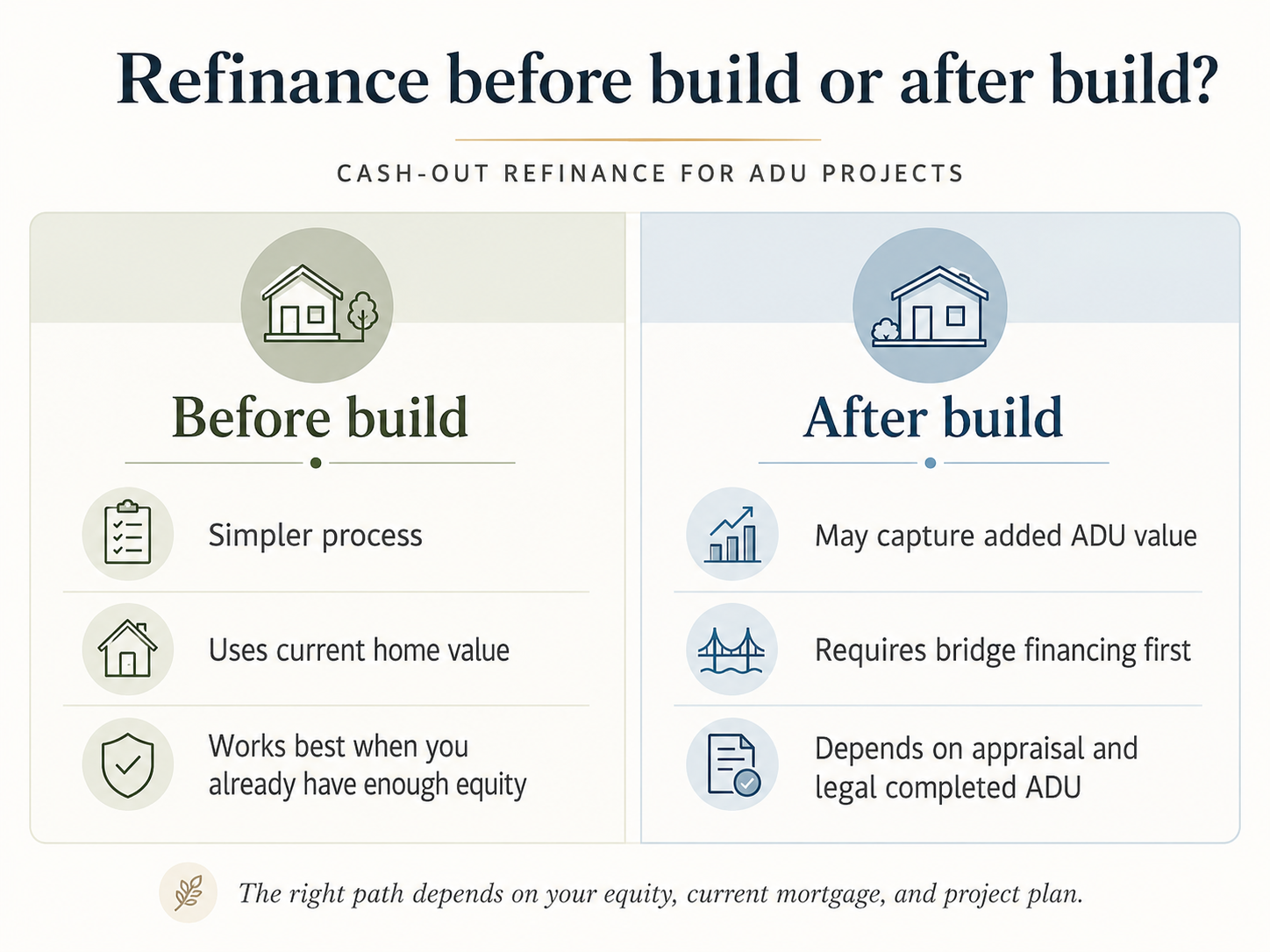

Should you refinance before or after the ADU is built?

Before-build cash out refinancing is simpler and faster but limited by today's appraised value. Post-build cash out lets you recoup equity from the value the completed ADU added, and the now-existing ADU helps you qualify on income because you may not need to count rent at all once your DTI is stronger. Post-build requires temporary financing during construction and depends on the appraisal supporting the new value.

Before-build cash out refinance: when it's the right sequence

- You have enough current-value equity to cover the ADU budget plus a 10–15% contingency.

- Your existing first mortgage is not worth protecting (paid off, near-market rate, or above-market ARM resetting).

- You don't need projected ADU rent to qualify.

- You want one mortgage payment and one closing event.

- You're comfortable receiving the cash before construction begins and managing draws to the contractor yourself.

Post-build cash out refinance: when it's the right sequence

- Your current equity is insufficient — you'll fund the build through a construction loan, HELOC, or savings.

- The ADU is fully permitted, legal, and inspectable on completion.

- The home's post-construction appraisal will materially exceed pre-construction value. FHFA research on California ADU properties showed stronger median appraised-value growth for ADU-containing properties versus comparable non-ADU properties over 2013–2023; results vary by market and aren't guaranteed nationally.

- You want to consolidate temporary financing into a permanent first mortgage.

The bridge strategy: HELOC or construction loan now, cash out refi later

For homeowners with low existing rates who want long-term consolidation, a common play is to fund the ADU with a HELOC or construction-to-permanent loan during the build, then cash out refinance once the appraisal supports a meaningfully larger first mortgage. The cost is two closings instead of one, but the math frequently wins because you avoid repricing the entire first mortgage during months when rates are above your locked rate. The bridge strategy is most powerful when you expect rates to fall meaningfully within 24–36 months of build completion.

What does a cash out refinance for an ADU cost?

Closing costs on a cash out refinance typically run 2–5% of the new loan amount, per CFPB data. On a $600,000 cash out refinance that's roughly $12,000–$30,000, most of which can be financed into the new loan rather than paid out of pocket.

Itemized 2026 cost ranges for cash out refi

| Cost item | Typical range | Notes |

|---|---|---|

| Lender origination | 0.5%–1.0% of loan | Sometimes waivable for ~0.25% rate increase |

| Appraisal | $500–$900 | Higher for jumbo, rural, or complex properties |

| Title insurance + title search | $500–$2,500+ | Heavily state-dependent |

| Recording fees | $50–$500 | Set by county recorder |

| Prepaid interest | Varies | Closing-date-dependent |

| Escrow setup | Varies | 2–6 months of taxes + insurance |

| Discount points (optional) | 0%–2% of loan | Lower the rate; calculate the breakeven |

| VA funding fee (VA only) | 2.15% or 3.30% of loan | Financeable; exempt for 10%+ service-connected disability rating and Purple Heart recipients |

| FHA upfront MIP | 1.75% of loan | Financeable; not refundable |

| FHA annual MIP | 0.55% currently (most loans) | Duration of 11 years at ≤90% LTV on >15-year terms (cash out is capped at 80% LTV) |

| State / local transfer taxes | Varies | Some states exempt refis |

| Loan-level price adjustments (LLPAs) | Built into rate | Cash out carries higher LLPAs than rate-and-term refis at the same credit/LTV |

Get a Loan Estimate (LE) from any lender within three business days of application — it is the binding itemization required by the TILA-RESPA Integrated Disclosure (TRID) rule.

The recoupment-period question every lender should answer for you

Calculate the recoupment period: how many months of monthly savings to pay back the closing costs? A reasonable rule of thumb: under 36 months is strong, 36–60 months is borderline, over 60 months means costs likely outweigh benefits.

How does a cash out refinance for ADU construction work, step by step?

A cash out refinance for ADU construction follows the same workflow as any cash out refi: apply, appraisal, underwriting, conditions, closing — typically 30–60 days from application to closing. You receive the full lump sum at closing (after a 3-business-day right of rescission on a primary residence) and pay your contractor directly. There is no construction escrow, no draw schedule, and no lender-managed inspections tied to disbursement.

| Week | Step | What happens |

|---|---|---|

| Week 0 | Pre-decision | Confirm lot feasibility, get rough contractor pricing, run the cash-out-vs-keep-rate math |

| Week 1 | Application | Apply with 2–3 lenders simultaneously; compare Loan Estimates within 24 hours |

| Week 1–2 | Underwriting setup | Submit documents, lock rate (30–60 day lock typical) |

| Week 2–4 | Appraisal | Lender orders, appraiser visits, report typically delivered in 5–10 business days |

| Week 3–5 | Underwriting conditions | Respond to clarification requests within 24–48 hours |

| Week 5–7 | Clear to close | Closing Disclosure issued; 3-business-day mandatory review window |

| Week 6–8 | Closing | Sign documents; 3-day right of rescission on primary residence |

| Week 8+ | Construction begins | Pay contractor directly; no lender-managed draws |

Cash out timing vs. permit timing — the sequencing question

Cash out refinance and ADU permitting run on independent tracks. The lender does not require your ADU permit to close, because the underwriting is against current property value, not against the planned ADU. This independence is a feature: you can close the cash out, hold the funds, and continue your permit process in parallel. It's also a risk: you can close the cash out, lose your permit application, and find yourself with the larger mortgage payment and no project. A reasonable sequencing rule: do not close on cash out funds until your permit application has cleared its first major hurdle.

What the lender does not inspect — but your building department will

A cash out refi has no construction inspections. A building department has many. This list catches first-time ADU builders flat-footed: foundation inspection, plumbing rough-in, electrical rough-in, framing, mechanical rough-in, insulation, drywall, final plumbing, final electrical, final mechanical, building final, and certificate of occupancy. Build a 10–15% construction contingency into your budget specifically to absorb inspection-driven rework.

Twelve questions to ask every cash out refi lender for an ADU project

- Is this loan underwritten against current value or as-completed value?

- What's the maximum LTV for my property type, occupancy, and credit profile?

- Will my current first mortgage be replaced, and what's the LLPA cost of cash out at my LTV?

- Can ADU rental income count toward my qualifying income on this specific transaction type?

- What credit score tier do I fall into, and how would a 20-point increase affect my rate?

- What are all closing costs, itemized — and which are financeable?

- Are there prepayment penalties or early-payoff penalties?

- Will the rate change between application and closing if I lock?

- How long does appraisal typically take in my market?

- What happens if the appraisal comes in below my target loan amount?

- Does the ADU need to be permitted, completed, or have any specific legal status for funding?

- What is the earliest possible closing date if everything goes perfectly?

If a loan officer can't answer most of these without checking, find a different lender.

Special situations: VA, FHA, Texas, investment property, manufactured home

VA cash out refinance for an ADU: the 100% LTV exception

The VA cash out refinance is the only mainstream agency-backed cash out path in this guide that allows up to 100% LTV on the appraised home value, subject to lender overlays and state restrictions. That makes it the single most powerful financing tool for VA-eligible homeowners who want to fund an ADU but lack 20% post-refi equity under the conventional or FHA 80% caps. On a $700,000 home with a $400,000 existing VA mortgage, the program allows up to $700,000 in new loan — about $300,000 cash before the funding fee and closing costs. Most VA lenders overlay to 90% LTV ($630,000 in the same example).

The VA funding fee is 2.15% (first-time use) or 3.30% (subsequent use), financeable into the loan. Veterans with a 10%+ service-connected disability rating are exempt. Purple Heart recipients are exempt. Surviving spouses receiving DIC are exempt. VA cash out can refinance any prior loan type — conventional, FHA, USDA, or existing VA — into a new VA loan. The property must be the borrower's primary residence.

Texas: the special case for VA and FHA cash out

Texas Constitution Section 50(a)(6) governs all home equity lending on Texas homestead properties. The Texas Attorney General issued Opinion KP-0183 in 2018 concluding that a VA cash out refinance loan is precluded by Section 50(a)(6)(H) because the federal VA guaranty serves as "additional collateral" beyond the homestead. FHA cash out is also unavailable for Texas homesteads. For Texas homeowners building an ADU, the realistic agency paths are: a Section 50(a)(6) conventional cash out (80% LTV with constitutional restrictions), a VA rate-and-term refinance combined with separate funding for the ADU, or non-cash-out paths like a home equity loan or HELOC on the same homestead. Texas borrowers should confirm specific scenarios with a Texas-licensed lender.

FHA cash out refinance for an ADU

FHA cash out refinances cap at 80% LTV (reduced from 85% in 2019), require 12 months of continuous owner-occupancy, and require 12 months of on-time payments on the existing mortgage. FHA cash out is owner-occupied only. The credit floor is 580 FHA-set, though most lenders overlay to 620+. Two FHA costs that matter: upfront MIP of 1.75% (financeable) and annual MIP at 0.55% for most loans. At FHA cash out's 80% LTV cap with a term longer than 15 years, annual MIP duration is 11 years — not life of loan. FHA cash out refis cannot use ADU rental income to qualify under HUD ML 2023-17.

Cash out refi on an investment property to build an ADU

Conventional cash out refis on investment properties cap at 75% LTV for a 1-unit investment and 70% for a 2–4 unit investment per the Fannie Mae 2026 Eligibility Matrix. FHA cash out is not available for investment properties. VA cash out requires primary-residence status. Rates run 0.5%–1.5% higher than primary-residence cash out. Investors planning to add ADUs to rental properties often find DSCR (debt-service coverage ratio) loans more flexible — they bypass personal income verification and qualify on the property's rental cash flow.

Cash out refi on a 2–4 unit primary residence

Fannie Mae SEL-2025-10 (Dec 10, 2025) introduces expanded ADU eligibility for lenders using Uniform Appraisal Dataset (UAD) 3.6 policy: up to three ADUs on a one-unit property, ADUs permitted on two-to-three-unit properties when the primary structure's units plus the ADUs do not exceed four total units, and expanded manufactured-home ADU configurations. These expanded allowances are effective March 31, 2026 and only available to lenders using UAD 3.6 policy. Ask your lender directly whether they originate under UAD 3.6 policy before assuming the expanded rules apply. Conventional cash out LTV on a 2-unit primary stays at 75%.

Cash out refi on a manufactured home with an ADU

Fannie Mae manufactured housing cash out refinance is capped at 65% LTV, with multi-width manufactured homes only — single-width manufactured homes are not eligible for cash out refinance per Fannie Mae B5-2-03. The borrower must have owned both the manufactured home and the land for at least 12 months. Permanent foundation, real-property classification, and HUD certification documentation are required at closing. The cash-out LTV math is materially harder than for site-built homes.

What can go wrong with an ADU cash out refinance?

Here are the 10 risks worth naming clearly, in plain language, so they don't surprise you mid-process.

- 1.You give up your existing rate forever. A 30-year mortgage at 3% is one of the most valuable assets most American households will ever hold. Once refinanced, it's gone.

- 2.The appraisal uses current value, not as-completed value. Plans, bids, and projected post-construction estimates do not change a cash out refi appraisal. If your project needs the future value to work, you need a different product.

- 3.No lender oversight on construction. Unlike a construction loan, there are no inspections tied to draws, no lender approval of your contractor, and no fraud-prevention check. That is freedom for sophisticated borrowers and risk for first-timers.

- 4.Closing costs are paid even if the project doesn't happen. If permits fall through, you've still paid the 2–5%.

- 5.80% LTV cuts your equity buffer sharply. A 20% nominal equity cushion is not the same as a 20% safety margin. A 10% market correction would cut your equity from 20% to roughly 11% of the new value. A correction larger than 20% — combined with selling costs or additional liens — can erase equity entirely.

- 6.Property taxes rise after the ADU is built. Most jurisdictions reassess on new construction. California's State Board of Equalization confirms new construction is generally assessable; Proposition 13 limits assessment increases on the existing primary dwelling, but the new ADU itself is assessed at current value.

- 7.Insurance costs rise too. ADU coverage, plus a landlord rider if you rent, plus potentially umbrella liability.

- 8.Cash out refis carry higher LLPAs than rate-and-term refis at the same credit and LTV — meaning the rate quoted is structurally a notch worse than a no-cash-out refi at the same credit/LTV profile.

- 9.CFPB has flagged elevated foreclosure risk. Cash out refis convert home equity into mortgage debt, and the CFPB has explicitly noted that this can elevate foreclosure exposure if repayment fails.

- 10.Cash out refi amortizes from day one. Many HELOCs require interest-only payments during the draw period. During the months when your ADU isn't yet generating rent, your cash flow on a cash out refi is meaningfully tighter than on most HELOCs at the same dollar amount.

The damaging admission worth stating directly: the entire industry has a structural incentive to recommend cash out refinances. Loan officers earn more on a $600,000 cash out refi than on a $200,000 second-lien product preserving a 3% first mortgage. That does not mean every recommendation is bad — but it does mean you should run the math yourself, ask the 12 questions above, and treat "cash out is the standard answer for ADUs" with skepticism unless your specific situation supports it. For most homeowners who locked rates between 2020 and 2022, the standard answer is wrong.

Is the interest on a cash out refinance for an ADU tax-deductible?

Cash out refinance interest may be deductible when the proceeds are used to buy, build, or substantially improve the home that secures the loan, per IRS Publication 936. ADU construction on the same parcel as your primary residence may qualify if it meets that rule. The deduction is subject to dollar limits — $750,000 of qualified residence debt for loans originated after December 15, 2017 on married-filing-jointly returns, $375,000 for married-filing-separately — and requires itemizing on Schedule A rather than taking the standard deduction. Interest used for non-home-improvement purposes from the same cash out refi is not deductible. Keep contractor invoices, permits, and closing documents to substantiate the home-improvement use if audited.

This is general tax information based on current IRS guidance, not tax advice for your specific situation. Talk to a tax professional before relying on deductibility in your financial planning. Tax law can change.

Want the full pre-build checklist before you talk to a lender?

Download the Free ADU Starter Kit →Budget, permit, and financing checklist

What if cash out refi isn't right for your ADU? Your alternatives, by situation

Sub-5% first mortgage + sufficient equity

HELOC for ADU is almost always the right first test. Second-lien products preserve the favorable first mortgage and apply the higher 2026 rate only to the ADU money. A home equity loan delivers the same rate preservation with a fixed payment structure.

Insufficient current equity

Future-value financing — Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, FHA 203(k), or a construction-to-permanent loan. These underwrite against the home's projected as-completed value, often unlocking $100,000+ of additional borrowing room.

Cannot carry another monthly payment

Home equity investments (HEIs) provide a lump sum in exchange for a share of future appreciation, with no required monthly payments. HEIs are state-limited and complex — check availability in your state and run the appreciation math carefully against traditional debt for long holds. See our Home Equity Investment for ADU guide.

Want to keep first mortgage and go higher than 85% CLTV

After-renovation-value (ARV) HELOCs — limited availability, mostly California credit unions currently — borrow against post-ADU value while keeping the first mortgage intact.

Income-qualified grant and loan programs (verified May 17, 2026)

| Program | Geography | Amount / type | Status | Source |

|---|---|---|---|---|

| CalHFA ADU Grant | California statewide | Up to $40,000 for pre-development costs | Fully allocated since December 28, 2023; no relaunch date | calhfa.ca.gov/adu/ |

| MassHousing ADU Loan | Massachusetts statewide | Fixed-rate 2nd mortgage up to $250K (detached) / $150K (attached) | Active, income-qualified owner-occupants | masshousing.com/adu |

| NYC Plus One ADU | New York City (1–2 family) | Up to $395,000 combined NYC HPD + NYS HCR financing | Active; income-qualified | nyc.gov HPD |

| Colorado CHFA ADU Finance | Colorado | Loans, credit enhancements, and interest-rate buydowns | Active; ADU-Supportive Jurisdiction required | chfainfo.com |

Verify current status directly with the administering agency before relying on any program in your financing plan.

Warning: If a website tells you it can "help you access" the CalHFA ADU Grant, walk away. CalHFA's own page warns that anyone offering to help homeowners get this grant is operating a financial scam. The program is closed.

Not sure cash out is right for you?

Explore non-cash-out ADU financing options →Via Mortgage Research Center — affiliate disclosure applies. We may earn a commission; you pay nothing extra. Full disclosure.

Cash out refinance for ADU: frequently asked questions

Can you use a cash out refinance to build an ADU?

Is a cash out refinance better than a HELOC for an ADU?

How much equity do I need for a cash out refinance for an ADU?

What is the maximum LTV for a cash out refinance to build an ADU?

Can I count future ADU rental income to qualify for the cash out refinance?

Does the cash out refinance appraisal include the new ADU?

Should I refinance before or after the ADU is built?

How long does a cash out refinance to build an ADU take?

Do I need approved ADU plans or a permit to do a cash out refi for ADU construction?

What credit score do I need for a cash out refinance for an ADU?

What are the closing costs on a cash out refinance for an ADU?

Will my property taxes go up after I build an ADU with cash out refi proceeds?

Can I do a cash out refinance to build an ADU on my rental property?

Is the interest on a cash out refinance for an ADU tax-deductible?

Can I get a VA cash out refinance to build an ADU in Texas?

How The Dwelling Index researched this guide

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We do not originate loans, act as a mortgage broker, or rank financing options by compensation.

For this guide, we separated three claim types: agency and regulatory claims (Fannie Mae, Freddie Mac, HUD/FHA, VA, FHFA, CFPB, IRS), cost and benchmark claims (Bankrate, Curinos, NerdWallet, Zillow rate data with publication dates), and editorial conclusions (clearly framed as fit guidance based on the verified facts, not guaranteed outcomes). Real homeowner threads from Reddit and BiggerPockets shaped our understanding of which questions readers actually ask — they were not used as authority for any agency rule or financing fact.

We do not quote specific rates or APRs as guarantees. We do not rank lenders. We do not use fake testimonials, fabricated reviewers, or schema for content not visible on the page. Our verification cadence: agency rules quarterly, benchmark rates monthly, conforming loan limits annually each November, partner availability monthly.

See our methodology, editorial standards, and affiliate disclosure.

Sources cited

- Fannie Mae Selling Guide B2-1.3-03: Cash-Out Refinance Transactions

- Fannie Mae Selling Guide B2-1.3-02: Limited Cash-Out Refinance Transactions

- Fannie Mae Selling Guide B2-3-04: Special Property Eligibility (ADU)

- Fannie Mae Selling Guide B3-3.8-01: Rental Income

- Fannie Mae Selling Guide B5-2-03: Manufactured Housing Underwriting Requirements

- Fannie Mae 2026 Eligibility Matrix

- Fannie Mae Announcement SEL-2025-10 (ADU expansion, Dec 10, 2025; UAD 3.6 only)

- Fannie Mae DU 12.1 Release Notes (effective March 21, 2026)

- Freddie Mac ADU Fact Sheet

- HUD Mortgagee Letter 2019-11 (FHA cash out 80% LTV)

- HUD Mortgagee Letter 2023-05 (FHA annual MIP reduction to 0.55%)

- HUD Mortgagee Letter 2023-17 (FHA ADU rules; cash out rental-income prohibition)

- HUD Mortgagee Letter 2013-04 (FHA MIP duration framework)

- VA Cash-Out Refinance User Guide; VA Funding Fee Schedule 2026

- 38 U.S.C. § 3709 — VA refinance net tangible benefit test

- Texas Constitution Section 50(a)(6); Texas AG Opinion KP-0183

- FHFA 2026 Conforming Loan Limits ($832,750 baseline / $1,249,125 high-cost)

- CFPB — Using Home Equity Consumer Guide

- IRS Publication 936 — Home Mortgage Interest Deduction

- California State Board of Equalization — New Construction and Property Assessment

- California AB 2533 — Unpermitted ADU legalization pathway

- Bankrate — Current Refinance Rates (May 18, 2026); Cash-Out Refinance Rates

- Curinos — HELOC and HELOAN National Average Rates (May 17, 2026)

- Wall Street Journal — Prime Rate (May 17, 2026)

- FHFA — Trends in Median Appraised Value for Properties with ADUs in California

Ready to move forward?

Start with feasibility — then compare financing options. Don't borrow against your home before you know what you can legally build at your address.

Check what you can build

Setbacks, lot coverage, fire zones, owner-occupancy rules — confirm first.

See What You Can Build → Get Your Free ADU ReportCompare financing options

Cash out, renovation, and construction loan options side by side.

Compare at Mortgage Research Center →Get the checklist

Budget, permit, and financing checklist — free download.

Download the Free ADU Starter Kit →Not sure where to start? See what's possible at your address — get your free ADU report in 60 seconds.

Affiliate disclosure: The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial conclusions, and we do not rank lenders by compensation. The Dwelling Index is an independent research resource — not a lender, broker, or builder. Full disclosure →

Financial disclaimer: Nothing on this page is financial, tax, legal, construction, or lending advice. Cash out refinance terms, approval, rates, fees, and qualification requirements vary by lender and borrower. Rates quoted are reference benchmarks from publicly visible sources on the dates noted — not loan offers. Verify all terms directly with licensed professionals before making any financing decision. A cash out refinance is secured by your home; failure to repay can result in foreclosure.