Home Equity Investment for ADU Construction: Will You Share the Value Your ADU Creates?

The Short Answer

A home equity investment (HEI) — also called a home equity agreement (HEA) or home equity sharing agreement (HESA) — can provide a lump sum that may fund part or all of your ADU build with no required monthly payment. Unlock advertises a $15,000 minimum and up to $500,000; Hometap and Point advertise up to $600,000. In exchange, you owe a future settlement tied to your home’s value when the agreement ends (typically 10 to 30 years from signing). For ADU builders specifically, the question that decides whether an HEI is brilliant or punishing is one most pages skip: does the provider share in the value your ADU creates, or does the agreement carve that improvement value out? Hometap, Unlock, and Point each answer that question differently. For most ADU builders who can qualify for a HELOC, a HELOC costs less over ten years.

Two minutes, no signup. Know your lot's ADU potential before you pick a financing path.

The financing path you choose today shapes how much of your ADU’s future value you actually keep.

Last updated: May 19, 2026 · Last verified: May 19, 2026

Editorial disclosure. The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. We are not affiliated with Hometap, Unlock, Point, Splitero, or Unison — they appear on this page for editorial comparison only, and we earn nothing if you choose them. Full disclosure · Editorial methodology

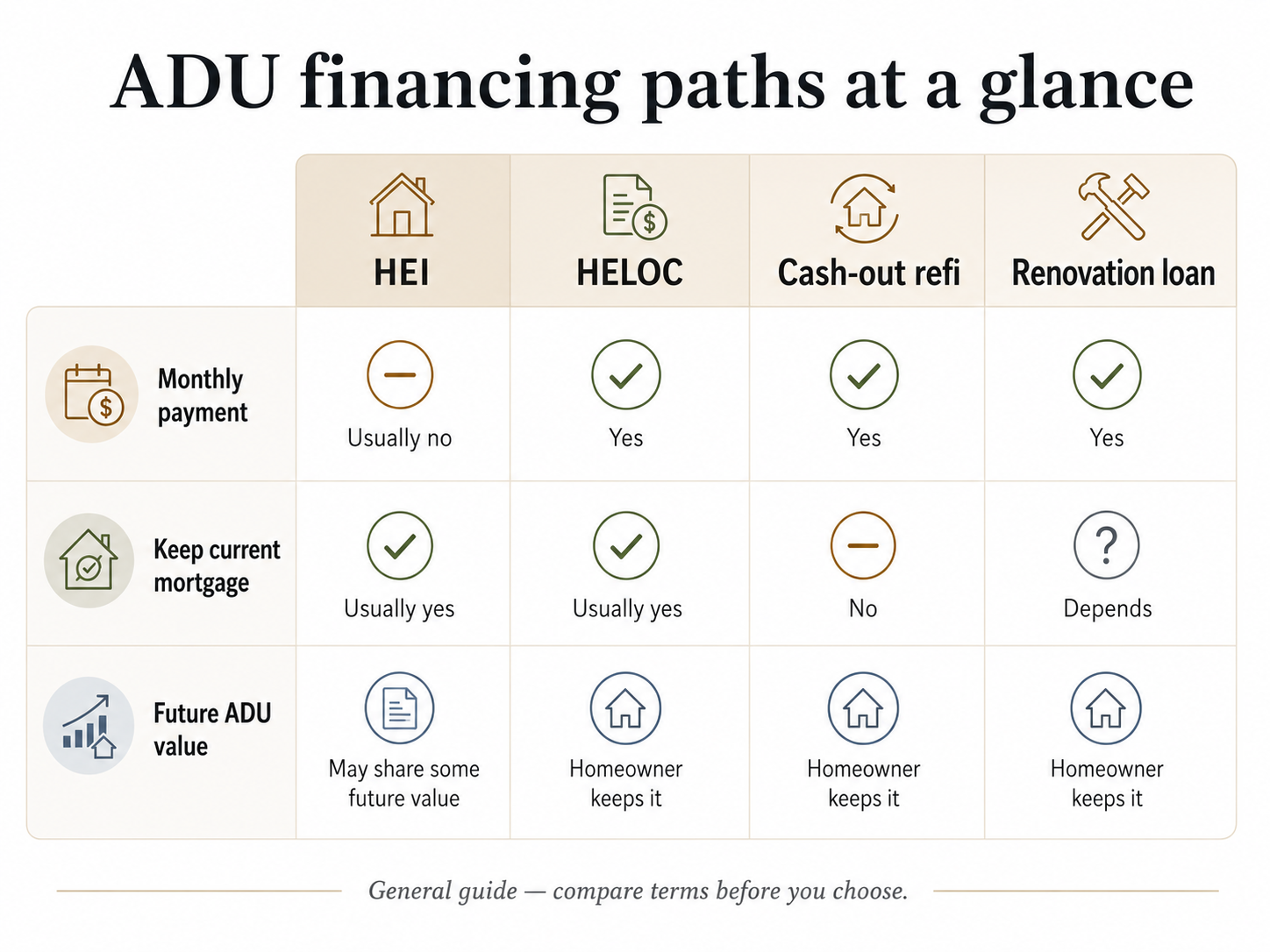

How the four ADU financing paths compare in 60 seconds

The single first-screen table on this page. Save it, screenshot it, send it to your spouse. The rest of the article explains why each row reads the way it does.

| Path | Monthly payment? | Keeps first mortgage? | Who keeps ADU value? | Best fit for | Main risk |

|---|---|---|---|---|---|

| Home equity investment (HEI) | Usually none required | Yes (HEI sits in second-lien or junior position) | Depends entirely on the agreement | Cash-flow-constrained owner who can't carry a payment | Future settlement size; appreciation sharing; refinance friction |

| HELOC (Home Equity Line of Credit) | Yes (interest-only during draw, then principal+interest) | Yes | You | Owner who can carry a payment and wants flexibility during construction | Variable rate; underwriting; equity cap (typically 80–85% combined LTV) |

| Cash-out refinance | Yes (replaces existing mortgage) | No — replaces it | You | Owner whose current mortgage rate isn't worth preserving | Losing a low first-mortgage rate; closing costs |

| Renovation loan (RenoFi-style, Fannie Mae HomeStyle, FHA 203(k)) | Yes | Sometimes, depending on product | You | Owner with limited current equity but strong post-ADU appraisal | More paperwork; appraisal of post-ADU value; contractor requirements |

Sources: HELOC and cash-out refi structures per Bankrate HELOC rates page (May 2026); renovation loan ARV underwriting per Fannie Mae HomeStyle product guidance and FHA 203(k) guidelines. HEI structure per the CFPB Issue Spotlight on home equity contracts (January 15, 2025). Last verified May 19, 2026.

General guide — compare terms before you choose.

What is a home equity investment for an ADU?

A home equity investment is a financial arrangement in which a company gives you a lump-sum cash payment today in exchange for a share of your home’s value at a future settlement date. There are no required monthly payments and no stated interest rate. The agreement is secured by a lien on your property. Settlement is typically due at the end of a 10- to 30-year term, or upon a triggering event such as sale or refinance. For ADU construction, that lump sum funds your build directly.

The product goes by several names — home equity investment (HEI), home equity agreement (HEA), home equity sharing agreement (HESA), shared appreciation agreement, or what the CFPB officially calls a “home equity contract.” The terminology varies; the structure does not. You receive cash. You eventually owe a settlement amount. The settlement amount depends on your home’s value when you exit. (Source: CFPB Issue Spotlight on Home Equity Contracts, January 15, 2025.)

The five-step mechanic

Here’s how money actually moves through an HEI for an ADU build, end to end:

- 1You apply. The provider reviews your home value, mortgage balance, credit (FICO floors range from 500 at Unlock and Point to 575 at Hometap as of May 2026, per each provider's published materials), property type, and state availability.

- 2The provider appraises your home and applies a risk adjustment. This is industry-standard — the provider values your home below its appraised value to offset their own risk. Money.com reported in 2025 that risk adjustments range from roughly 2.75% to 20% of appraised value depending on the provider.

- 3You receive cash, minus an origination fee. Origination fees range from roughly 3% to 4.9% (Bankrate: Hometap ~3%, Unlock up to 4.9% as of March 2026). Closing costs apply on top.

- 4You build the ADU. Funds aren't restricted to construction — but for the purposes of this article, that's what they're doing.

- 5At settlement, you owe the provider's share of your home's value. Sometimes plus the original advance, sometimes calculated as a percentage of total value, sometimes capped, sometimes credited for renovations. The specific formula is in your agreement, and it is the single most important paragraph in the document.

Why “no monthly payment” doesn’t mean “no cost”

No monthly payment is not the same as low cost. A 10-year HEI on a home that appreciates at historical norms typically costs the equivalent of a 9% to 13% APR loan over the term. The CFPB modeled scenarios in its January 2025 Issue Spotlight showing repayment amounts ranging from roughly $94,000 to $216,000 on a $50,000 advance over ten years, depending on appreciation. The cost isn’t visible monthly — it shows up as one large payment at exit.

The advantage of an HEI is genuine: you preserve cash flow. The cost of that preservation is real: you may pay substantially more in absolute dollars than a HELOC would have cost over the same period. Neither is inherently better. The right one depends on whether you can carry a payment.

How an HEI for ADU differs from a HEI for a kitchen remodel

This is where ADU borrowers diverge from typical HEI customers — and where most generic HEI guides fail you.

An ADU is not a cosmetic improvement. The Federal Housing Finance Agency’s 2024 analysis of California Enterprise-backed purchase appraisals found median appraised values of $1,064,000 for properties with ADUs versus $715,000 for properties without ADUs in 2023, and 9.34% annualized median appraised-value growth from 2013 to 2023 for California ADU-equipped properties versus 7.65% for properties without ADUs. (Source: FHFA, “Trends in Median Appraised Value for Properties with Accessory Dwelling Units in California”.) The pattern is California-specific, but the directional point applies broadly: a kitchen remodel does not move the appraisal the way a permitted ADU does.

That means the dollar amount you owe at HEI settlement may be substantially larger after an ADU build than after a kitchen remodel of the same cost. Whether that’s a problem depends on the provider’s improvement-value treatment — and that’s the next section.

Check your property's ADU potential before you choose a financing path.

Can you actually use a home equity investment to build an ADU?

Yes. Hometap, Unlock, and Point each publish flexible-use or home-improvement language in their consumer materials, and ADU construction qualifies under that language. But three ADU-specific catches matter: the property must qualify under the provider’s eligibility rules, the lien position must work with any construction loan you plan to layer on, and the agreement’s improvement-value language must align with what you’re about to build.

What HEI cash typically covers in an ADU project

- Architectural design and feasibility work

- Permit and plan-review fees (these vary substantially by city and project; verify with your local building department)

- Site work (grading, utility trenching, soil testing)

- Utility connection upgrades or new laterals (a utility lateral is the pipe or conduit running from the public main to your property; site-specific work may require new water, sewer, or upgraded electrical service)

- Garage conversion construction

- Detached ADU construction

- Prefab or modular ADU installation

- Construction contingency (typically 15–20% of construction cost)

Property eligibility — what stops an HEI deal

HEI providers don’t lend on every property. Common ineligibility flags as of May 2026, drawn directly from each provider’s published eligibility pages:

- Manufactured homes — Hometap, Unlock, and Point all exclude manufactured homes per their published disclosures.

- Existing unpermitted ADUs or rental units on the lot — Some providers ask, some don't, but disclosure matters and unpermitted units often disqualify.

- Large parcels — Point states it does not currently offer HEIs on properties with 7 or more acres. Splitero and other providers have their own acreage limits; verify directly.

- Home value minimums — Point requires a minimum home value per its help center; Unlock requires $175,000+ per Unlock's how-it-works page; Splitero publishes its own minimum on its eligibility page.

- Insufficient equity — Unlock publishes a 30% equity requirement; Hometap looks for 25%+ post-investment; Point requires homeowners to retain a significant percentage of equity after Point's investment, with the exact percentage confirmed by prequalifying.

- Credit score below the floor — Unlock and Point accept 500 FICO per their published terms; Hometap publishes a 575 minimum FICO per its resource page on accessing home equity without perfect credit; Unison historically requires 620.

- Active flood zone without insurance — Hometap will fund flood-zone properties only if flood insurance is maintained for the duration.

Will an HEI lien interfere with a construction draw or future refinance?

Possibly — and this is the question most homeowners don’t ask in time.

An HEI lien sits in second-lien position behind your first mortgage. If you want to add a construction loan or a HELOC during the build, that lender will need to be comfortable with the HEI’s position, and many will require the HEI to subordinate or won’t lend at all. If you want to refinance your first mortgage later — say, to pull cash out of the ADU’s added value to settle the HEI itself — your refinance lender will see the HEI lien on title and price accordingly, or may decline.

The CFPB specifically noted in its January 2025 Issue Spotlight that consumers reported difficulties refinancing their first-lien mortgage after entering home equity contracts. This isn’t a hypothetical. Ask your HEI provider for its written subordination policy and refinance rules before signing.

What an HEI does not solve

An HEI gives you cash. It does not give you a permit. It does not give you a buildable lot. It does not give you a contractor. The work that determines whether your ADU project succeeds — confirming zoning eligibility, navigating local setback and Floor Area Ratio (FAR — the ratio of total building floor area to the lot size, used as a zoning cap) rules, securing ministerial approval (a ministerial permit is one where the city must approve if you meet objective standards, no discretionary review allowed), passing plan check (the city’s engineering and code review of your construction documents), and getting through inspections — all happens independently of the financing path. Don’t take HEI cash before confirming the ADU itself is feasible.

Two minutes. No signup. Know your lot's ADU potential before financing.

Will the HEI company share in the value your ADU creates?

This is the central question for any ADU homeowner considering an HEI, and the answer varies dramatically by provider. Hometap allows a renovation adjustment for qualifying renovations of $25,000 or more with proper documentation. Unlock states it does not share in the value created by improvements made at the homeowner’s expense. Point’s help center states that improvement appreciation is part of the appreciation Point shares. The same ADU built with the same cash from three different providers can produce three very different settlement amounts ten years later.

This is the answer that no other ADU financing page on the internet assembles in one place. We built the table below by reading each provider’s official help center and public agreement summaries. Verification date: May 19, 2026.

The improvement-value matrix

| Provider | Improvement-value position | What that means for an ADU | Documentation typically required | Source |

|---|---|---|---|---|

| Hometap | Renovation adjustment available for qualifying renovations of $25,000 or more, subject to appraisal review and provider approval. Not guaranteed. | Your ADU build may qualify for an adjustment that excludes the ADU-created value from Hometap's share at settlement, if you document the project per Hometap's requirements and the appraisal reflects the adjustment. | Before/after photos, contractor receipts and invoices, permit records, final inspection documentation, appraisal review. | Hometap renovation adjustment policy, verified May 2026 |

| Unlock | Improvement-value protection language stating that Unlock does not share in value created by improvements made at the homeowner's expense; improvement value is determined by a third-party appraiser. | Strongest documented improvement-value protection of the three major providers, on paper. The ADU value you create should be carved out of Unlock's share — but the exact carve-out depends on appraiser methodology. Ask for the appraiser-selection and dispute process in writing. | Receipts, before/after appraisal, third-party appraiser review at settlement. | Unlock home equity agreement materials, verified May 2026 |

| Point | Point's help center states that when it is time to repay, value includes appreciation from improvements made during the agreement, and that increase is part of the appreciation Point shares. | Highest ADU-created-value-sharing risk of the three major providers. The improvement appreciation from your ADU is, by Point's own published policy, included in what Point shares at settlement. | Less negotiable based on published policy; verify directly with Point before signing. | Point help center: "Can I remodel the home at any time?", verified May 2026 |

| Splitero | Improvement consideration in some agreements; verify per offer. | Variable; not a published default. Confirm directly with Splitero before applying. | Per-offer; ask before signing. | Splitero.com; verify per offer |

| Unison | Historically limited improvement credit; subject to ongoing litigation. | Confirm current policy and litigation status before signing. | Per-offer. | Unison.com; verify directly |

This is the table to print and bring to any HEI conversation. Three identical homeowners with three identical $200,000 ADU builds and three identical home appreciation rates will owe meaningfully different amounts at settlement depending on which provider’s agreement they signed. The improvement-value clause is, for an ADU builder, the single most consequential paragraph in the document.

Why an ADU is uniquely affected by this clause

Most HEI customers use the cash for debt consolidation, education, retirement supplementation, or general renovations — uses that don’t dramatically change the home’s appraised value. An ADU is different. The FHFA’s California data shows ADU-equipped properties appraising at a median value 49% higher than properties without ADUs, with measurably faster annualized appraisal growth. The ADU isn’t a marginal addition — it’s often a category change in the property’s valuation.

If your provider includes that uplift in its share, the cash advance can become a very expensive trade. If the provider carves it out, the trade becomes much more reasonable. Same ADU, same cash, same homeowner — radically different outcomes.

The damaging admission, said plainly

If you fund your ADU with an HEI from a provider that includes improvement appreciation in its share, you may be using the cash to create the exact property value you’ll later have to share back. It’s the inverse of how a HELOC works — with a HELOC, you keep all the appreciation you create. With certain HEI agreements, you don’t.

This doesn’t make HEIs disqualifying. It makes the improvement-value clause the negotiable item. The path forward is to confirm the treatment in writing for your specific ADU build before you sign, and to walk away from any provider that won’t put it on paper.

Documentation checklist before you sign

- Written confirmation from the provider that the ADU qualifies as a covered improvement

- Approved permits (not just submitted — approved)

- Signed construction contract with itemized scope

- Before photos taken before any work begins, geo-tagged and dated

- Itemized contractor invoices showing what was spent where

- Receipts for materials purchased directly

- Final inspection card or certificate of occupancy

- Appraisal dispute process described in writing in your agreement

- The exact settlement formula with worked example for your home value

Save every document in cloud storage with backups. The settlement will happen a decade from now. The contractor you used may not be in business then. The receipts you toss today are the receipts you’ll wish you had.

See what's possible at your address before you commit to any financing path.

Is a home equity investment for ADU construction better than a HELOC?

For most homeowners who can qualify for a HELOC, no. A HELOC will typically cost less in absolute dollars over a 10-year horizon than a home equity investment for ADU construction, and you keep 100% of the appreciation your ADU creates. The home equity investment for ADU funding wins in a narrow set of cases: when you can’t qualify for or can’t carry a HELOC payment, when your local market is unlikely to appreciate over the term, or when the provider’s improvement-value clause explicitly carves out the ADU’s contribution.

This is the comparison most ADU-financing pages skip because it requires actually running the math. We ran it.

Across realistic appreciation scenarios (3% to 7% annual), the HELOC costs less in absolute dollars than a 35%-share HEI — and you keep all the appreciation your ADU creates. The HEI cost rises because your ADU works.

Compare both before you decide.

If you can qualify for a HELOC, you almost certainly should.

For a full HELOC deep-dive see our guide: HELOC for ADU: Real 2026 Rates, Draw Schedules & How to Qualify. For a head-to-head Hometap comparison see: Hometap vs HELOC for ADU: Real Costs, Risks & the Right Fit.

Which home equity investment companies are available in my state?

HEI availability is state- and address-specific. As of May 2026, Hometap publishes availability in 16 states; Point publishes availability in select regions of 27 states plus Washington, D.C.; Unlock requires the property to be in Unlock’s service area, verified by address. Connecticut, Maryland, Illinois, and Maine have enacted laws that bring shared-appreciation or HEI-style products into mortgage or consumer-credit regulatory frameworks. Washington has open Department of Financial Institutions rulemaking and pending legislation. State availability is the first filter; if no provider operates where you live, the rest of the decision is moot.

Provider state availability (verified May 19, 2026)

| Provider | Published states / regions as of May 2026 | Source |

|---|---|---|

| Hometap | AZ, CA, FL, IN, MI, MN, MO, NV, NJ, NY, OH, OR, PA, SC, UT, VA (16 states). | Hometap.com state coverage, verified May 2026 |

| Unlock | Property must be in Unlock's service area; eligibility includes 30% equity, $175,000+ property value, and 500 minimum credit score. Verify by address on Unlock's current service-area page. | Unlock how-it-works page, verified May 2026 |

| Point | Select regions in AZ, CA, CO, CT, FL, GA, HI, IL, IN, KY, MD, MI, MN, MO, NV, NJ, NY, NC, OH, OR, PA, SC, TN, UT, VA, WA, WI, plus Washington, D.C. (27 states + D.C.). Coverage is region-specific within served states; address-level eligibility must still be verified. | Point help center: "Where does Point offer HEIs?", verified May 2026 |

| Splitero | Verify directly at splitero.com. Eligibility includes a minimum home value and credit floor; current minimum and acreage limits should be verified directly before applying. | Splitero.com; verify per offer |

| Unison | Historically broad state coverage; active litigation may have changed current availability. Verify at unison.com before applying. | Unison.com; verify directly |

Why we don’t publish a single Unlock state count: Unlock’s official availability page directs prospective customers to verify by address rather than presenting a clean state list, and provider service-area maps can change between our verification dates. We treat each provider’s own current “where we operate” page as the source of truth — and re-verify monthly.

Why “state available” doesn’t mean “you qualify”

State availability is the floor, not the ceiling. Within a served state, providers may still decline based on:

- Property type (manufactured homes, mixed-use, raw land, certain co-ops are commonly excluded)

- County or region (Point in particular notes "select regions" within served states)

- Lot size (Point excludes 7+ acre properties; other providers have their own limits)

- Existing liens or encumbrances

- Title issues (trusts, life estates, co-ownership complications)

- HOA restrictions on improvements

- Property condition flagged in the appraisal

- Recent bankruptcy or foreclosure (typical waiting periods of 3–5 years)

A “yes, we’re in your state” is not an offer. It’s permission to apply.

State regulatory map for HEIs (as of May 19, 2026)

A growing number of states have moved to regulate HEIs as mortgage loans or under consumer-credit frameworks. The status varies — enacted, in rulemaking, or in committee — and matters because the consumer-protection environment around HEIs is genuinely different in regulated states than in unregulated ones.

| State | Status | What changed / is changing | Source |

|---|---|---|---|

| Connecticut | Enacted | Brought shared-appreciation / HEI-style products into mortgage or consumer-credit regulatory frameworks. | JD Supra licensing update, 2025 |

| Maryland | Enacted | Same direction as Connecticut. | JD Supra licensing update, 2025 |

| Illinois | Enacted, effective January 1, 2025 | Brought HEI-style products under state mortgage / consumer-credit regulation. | JD Supra licensing update, 2025 |

| Maine | Enacted via LD 1901, April 13, 2026 | Brought HEI-style products under state regulatory framework. | Maine Legislature LD 1901 |

| Washington | Not enacted; HB 1464 in committee; DFI rulemaking open | Department of Financial Institutions rulemaking is open; legislative bill remains pending. | Washington State Legislature; Washington DFI |

The pattern across state action is the same: lawmakers and regulators are concluding that HEIs function as home-secured credit and need disclosure, licensing, or consumer-protection coverage. If you are entering a 10- to 30-year agreement, plan for the possibility that the rules around it will be different at exit than they were at signing.

The real 10-year cost: HEI vs HELOC vs cash-out refinance for a $150,000 ADU

On a $150,000 ADU funded by HEI in our illustrative model (10% risk adjustment, 35% share at settlement, 4% origination fee), expect to settle between $245,000 (if your home stays flat) and $482,000 (if your home appreciates at 7% annually) at the end of a 10-year term. A HELOC at an 8% interest rate, interest-only for 10 years, costs roughly $120,000 in interest plus the original $150,000 principal at exit — total $270,000. The HEI is cheaper only in scenarios where your home substantially depreciates. In every realistic appreciation scenario, the HELOC costs less.

This is the math no HEI provider will run for you in writing. Here it is.

Setup assumptions for the illustrative model

- Home appraised today at $700,000

- Existing mortgage balance: $300,000 (43% LTV — Loan-to-Value, the ratio of debt to property value)

- ADU project cost: $150,000 (a mid-range garage-conversion-plus-detached scenario in many U.S. markets)

- HEI advance: $150,000 — Risk adjustment: 10% — Provider’s share at settlement: 35% (illustrative; actual provider formulas vary)

- Origination fee: 4% deducted from disbursement, so the homeowner receives $144,000 in cash

- Term: 10 years

This is illustrative modeling using the assumptions stated above — not a quote from any provider, and not a guarantee of any outcome. Actual settlement amounts depend on the specific agreement, the actual appraisal at settlement, and the provider’s improvement-value treatment.

Worked HEI scenarios on a $150,000 ADU

| Appreciation scenario | Home value at Year 10 | HEI provider’s 35% share | What you pay to settle | Equivalent annualized cost on $144K received |

|---|---|---|---|---|

| Home value flat (0%/yr) | $700,000 | $245,000 | $245,000 | ~5.5% per year |

| Modest appreciation (3%/yr) | $941,000 | $329,350 | $329,350 | ~8.6% per year |

| Average appreciation (5%/yr) | $1,140,000 | $399,000 | $399,000 | ~10.7% per year |

| Strong appreciation (7%/yr) | $1,377,000 | $481,950 | $481,950 | ~12.8% per year |

The HELOC comparison

Same $150,000 ADU, 10-year horizon. Bankrate’s HELOC rates page reported a national average HELOC rate of approximately 7.26% as of May 6, 2026; U.S. Bank’s HELOC calculator (December 11, 2025) listed 7.20%–10.85% APR. We use 8% as a middle assumption.

| HELOC structure | Monthly cost | Total interest over 10 years | Principal owed at Year 10 | Total cost at exit |

|---|---|---|---|---|

| Interest-only first 10 years, balloon $150,000 at end | ~$1,000/month | ~$120,000 | $150,000 | $270,000 |

| Standard amortization over 10 years | ~$1,820/month | ~$68,000 | $0 | $218,000 |

The verdict

Across every realistic appreciation scenario (3% to 7% annual), the HELOC costs less in absolute dollars than the HEI — and you keep 100% of the appreciation your ADU creates. The HEI wins only if your home stays flat or depreciates. That isn’t a bet most homeowners want to make.

Why does the HEI get more expensive precisely because your ADU works?

Because in most HEI agreements, the provider’s share is calculated on your home’s value at settlement — and your ADU is what drives that value up. The very success of the project that justified the HEI is what enlarges the settlement. This is why the improvement-value clause matters so much.

When does HEI math actually beat HELOC math?

- The homeowner truly cannot qualify for or carry a HELOC payment (self-employed with inconsistent income, retired on a fixed income, recent bankruptcy aged off but credit not yet recovered) — in which case the HEI isn't being compared to a HELOC; it's being compared to no financing at all.

- The home is unlikely to appreciate much over the term (flat or declining local market, plans to sell at a known price) — in which case the HEI share stays small.

- The ADU's improvement value is contractually excluded from the provider's share — which puts you back in territory where the math is reasonable.

See real 2026 rate ranges and qualification requirements for HELOC, cash-out refinance, and construction-to-permanent loans. Independent research, no payment to apply.

Affiliate disclosure: Mortgage Research Center is a paid partner. We earn a commission if you proceed; you pay nothing extra. Full disclosure

The 2025–2026 regulatory reality: what the CFPB and the courts have said about HEIs

On January 15, 2025, the Consumer Financial Protection Bureau issued three coordinated actions on home equity contracts: a Consumer Advisory warning homeowners to “beware” of these products, an Issue Spotlight characterizing them as costly, risky, and complex, and an amicus brief in Roberts v. Unlock arguing that the specific product at issue meets the federal definition of a “residential mortgage loan” under the Truth in Lending Act. The CFPB later moved to withdraw that amicus brief. State-level action has continued: Connecticut, Maryland, Illinois, and Maine have enacted laws; Washington has open rulemaking and pending legislation. None of this makes HEIs illegal. It does mean the agreement you sign today may be reinterpreted by a regulator or a court during its 10- to 30-year life.

The 2024–2026 regulatory timeline

| Date | Event | What it means |

|---|---|---|

| Jan 1, 2025 | Illinois HEI / shared-appreciation legislation takes effect | HEIs in Illinois now operate under state mortgage / consumer-credit regulatory framework |

| Jan 15, 2025 | CFPB Issue Spotlight + Consumer Advisory + amicus brief in Roberts v. Unlock | CFPB officially characterizes home equity contracts as "costly, risky, complex." Bureau argues the Unlock product is a residential mortgage loan subject to TILA |

| Feb 2025 | Massachusetts AG sues Hometap | Complaint alleges Hometap's HEI structure places consumers at heightened risk of losing their homes |

| Aug 7, 2025 | Olson v. Unison Agreement Corp., 9th Circuit | Unpublished memorandum on whether the agreement is a loan under Washington consumer-protection statutes. Appeal dismissed October 17, 2025 after settlement |

| Aug 2025 | Massachusetts court denies Hometap's motion to dismiss in MA AG case | The Massachusetts case will move forward; Hometap contests the allegations |

| 2025 | CFPB moves to withdraw amicus brief in Roberts v. Unlock | CFPB filed a motion to withdraw, indicating it was reconsidering the arguments previously asserted |

| Jul 30, 2025 | Stone v. Real Estate Equity Exchange, U.S. Bankruptcy Court, D. Colorado | Court allowed claims that the agreement is unconscionable and may be rejected as an executory contract under Colorado bankruptcy law |

| 2025 | Weingot v. Unison Agreement Corp., D.N.J. | Federal magistrate recommended denying Unison's summary-judgment motion. Deceptive-marketing claims allowed to proceed |

| Apr 13, 2026 | Maine enacts LD 1901 | HEIs in Maine now operate under state regulatory framework |

| Jan 29, 2026 | Hometap 2026 Outlook Report | Industry leader publicly acknowledges "active state-level regulatory engagement" and predicts continued state-by-state regulatory development |

Sources: CFPB Issue Spotlight + Consumer Advisory, January 15, 2025; CFPB motion to withdraw amicus in Roberts v. Unlock; National Consumer Law Center issue brief, May 27, 2025; CommonWealth Beacon; JD Supra licensing update; Justia case records; Maine Legislature; Washington State Legislature.

What the CFPB actually said (and didn’t say)

The CFPB’s Consumer Advisory used unusually direct language: it told homeowners to “beware” of home equity contracts and warned that even if the home loses value, the homeowner will probably still have to pay the company more than they received and might have to sell the home.

In the Issue Spotlight, the CFPB modeled scenarios showing the equivalent of 20% annual interest in the early years, with final repayment amounts ranging from $94,074 to $215,892 on a $50,000 advance. Consumers also complained of:

- Surprise at the size of repayment amounts

- Feeling misled about how rate caps work

- Difficulty refinancing their first-lien mortgage with an HEI lien on title

- Disputes about home valuations (too low at origination, too high at repayment)

- Feeling that their only option was to sell the property to repay the HEI

- Six of 21 published complaint narratives used the word “predatory”

The CFPB did not ban HEIs. What it did was put providers on notice and provide a roadmap for state regulators and plaintiffs’ attorneys.

What all of this means for an HEI you sign in 2026

- 1Read the agreement with a lawyer. A licensed attorney in your state, ideally one with consumer-protection or mortgage experience. The agreement is 30–60 pages of provisions written by sophisticated counsel for the provider. You deserve sophisticated counsel reading it for you.

- 2Assume the regulatory environment will continue to develop. Four states have enacted HEI-relevant laws; a fifth has open rulemaking. If you're entering a 10-year agreement, plan for the possibility that the rules around it will be different at exit than they were at signing.

- 3Flag any mandatory arbitration clause for attorney review before signing. The CFPB specifically identified arbitration provisions as a consumer-protection concern; their inclusion limits your remedies if disputes arise. Some providers have removed them. Ask.

Who HEI for ADU actually fits — and the better path for everyone else

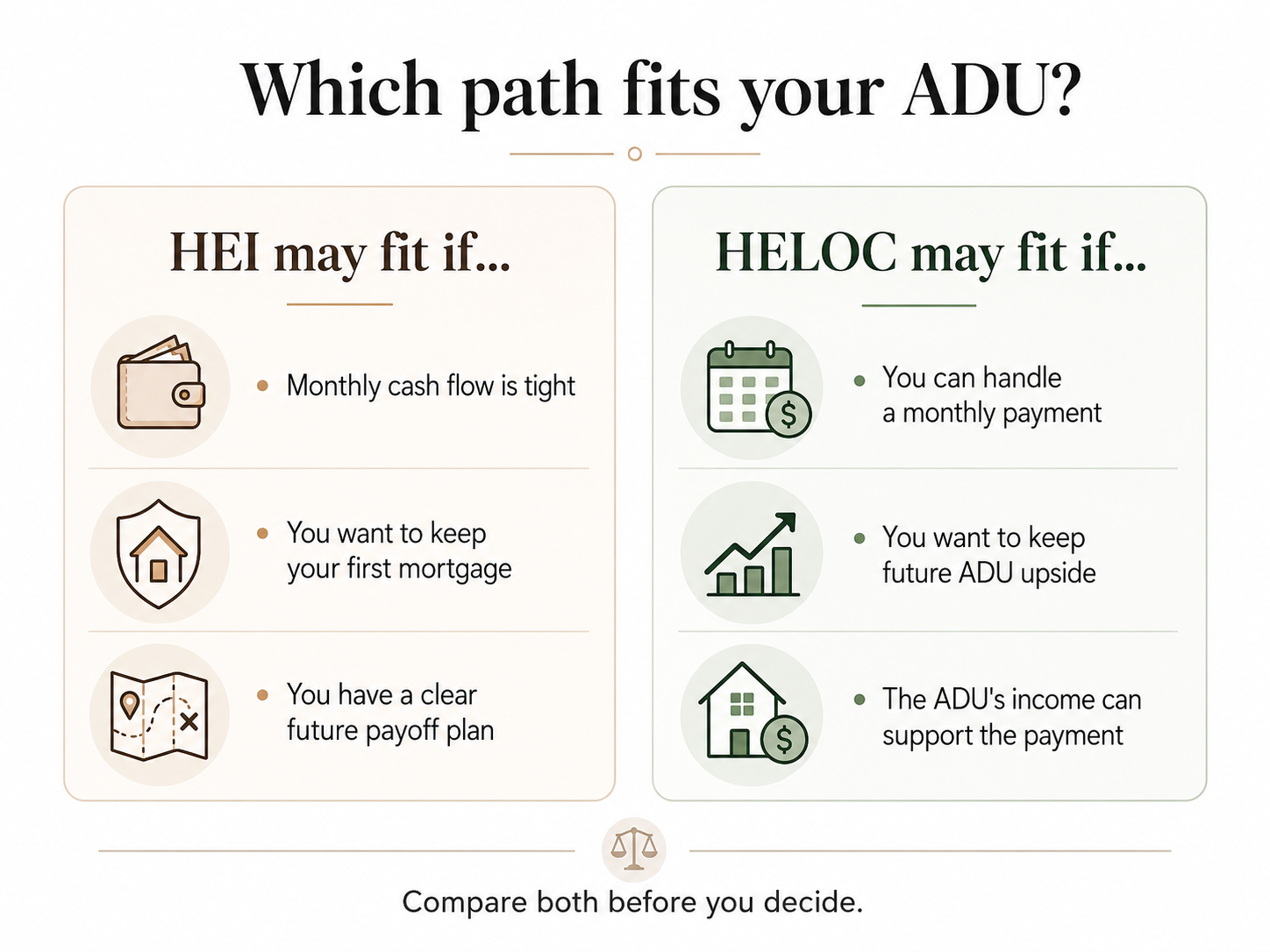

An HEI for ADU funding is a reasonable choice when all five conditions are true: (1) an HEI provider serves your state, (2) you have substantial equity but limited W-2 income, below-prime credit, or another barrier that prevents HELOC qualification, (3) you plan to stay in the home for the full HEI term, (4) you have a written and credible plan to settle the lump sum at term-end, and (5) the agreement’s improvement-value clause explicitly excludes the ADU’s value-add from the provider’s share. For everyone else, one of four alternative financing paths typically costs less over ten years.

The five-condition HEI fit check

You fit the HEI-for-ADU profile if all five are true:

A reputable HEI provider operates in your state.

You cannot qualify for or cannot carry a HELOC, cash-out refi, or renovation loan payment.

You plan to stay in the home long enough to make the HEI term economic (typically 8+ years of the 10-year term).

You can describe — out loud, in two sentences — exactly how you intend to settle the lump sum at term end.

The improvement-value treatment for your specific ADU is confirmed in writing before signing.

If any one is false, look elsewhere.

The 6-path ADU financing decision matrix

| If you are… | And you have… | The path most likely to fit | Why |

|---|---|---|---|

| W-2 employed, strong credit (720+) | 30%+ equity, low first-mortgage rate (sub-5%) | HELOC | Cheapest capital; doesn't touch your first mortgage; interest-only during construction; you keep all appreciation |

| W-2 employed, strong income | 30%+ equity, high first-mortgage rate (7%+) | Cash-out refinance or construction-to-permanent loan | One consolidated loan; may lower overall rate; works when your existing mortgage isn't worth preserving |

| W-2 with limited current equity | 10–20% equity now, but ADU will materially increase home value | Renovation loan (RenoFi-style, Fannie Mae HomeStyle, FHA 203(k)) | Underwrites against your after-renovation value (ARV) rather than current equity; gives you the borrowing power that current equity alone wouldn't |

| Self-employed or 1099 income | Solid equity, irregular income | Bank-statement HELOC, DSCR loan, or HEI | DSCR — Debt Service Coverage Ratio loan, qualifies on the property's rental income rather than your personal income; works when traditional underwriting can't see your real cash flow |

| Retired, on fixed income, can't take monthly payment | Significant equity, plan to stay 10+ years | HEI (if state allows) or HECM (if 62+) | HECM — Home Equity Conversion Mortgage, the FHA-insured reverse mortgage available to homeowners 62+, with mandatory housing counseling and consumer protections that HEIs lack |

| Building ADU for aging parent on a 2-year timeline | Equity, ability to carry payment short-term | HELOC during build, then refinance when ADU is complete and appraised | Speed; HEI underwriting can take 30–60 days; HELOC moves faster, and the post-ADU refi cleans up the structure |

Assembled from the underwriting realities of each path, cross-referenced against Urban Institute ADU financing research (2024) and Terner Center for Housing Innovation data on California ADU financing usage, which found that 56% of California homeowners who built an ADU used a Home Equity Loan or HELOC.

If you can qualify for a HELOC, you almost certainly should.

A HELOC will almost always cost less than an HEI over a 10-year horizon for someone who can qualify for one. You also keep 100% of the appreciation your ADU creates, avoid the lien complications, avoid the regulatory uncertainty, and avoid the settlement-day balloon shock.

If your equity is thin, look at after-renovation-value lending

ARV — after-renovation value — lenders underwrite against what your home will be worth after the ADU is built, not what it’s worth today. RenoFi is the best-known consumer-facing brand in this category; Fannie Mae HomeStyle and FHA 203(k) loans operate on similar principles through traditional bank channels. For a homeowner with 10–20% current equity but a strong projected post-ADU appraisal, ARV-based lending often beats HEI in both cost and structure. See our guide: How to Finance an ADU With No Equity: 7 Paths.

If you’re 62+, a HECM may be safer than an HEI

A Home Equity Conversion Mortgage (HECM) — the FHA-insured reverse mortgage — gives you cash without a monthly payment, just like an HEI. But unlike an HEI, a HECM is insured by the federal government, is regulated by HUD, requires mandatory housing counseling from a HUD-approved counselor before signing, and lets you remain in the home indefinitely as long as it remains your primary residence and you keep up taxes, insurance, and maintenance. HECMs are available to homeowners 62 and older. The consumer protections are dramatically stronger than those around HEIs.

Compare HELOC, cash-out refinance, renovation loans, and construction-to-permanent financing at current 2026 rates.

Affiliate disclosure: Mortgage Research Center is a paid partner. We earn a commission if you proceed; you pay nothing extra. Full disclosure

Your exit plan: the section that decides whether the HEI will work

Do not sign an HEI for an ADU unless you can describe — in two sentences — exactly how you will settle the obligation when the term ends. “The ADU will pay for itself someday” is not an exit plan. A real exit plan names the likely settlement method, the timing, the backup if Plan A doesn’t work, and what happens if the appraisal or refinance at settlement comes in different from what you expect.

The CFPB Issue Spotlight noted that some HEI customers reported feeling their only option was to sell their homes to settle the contract. The exit plan is what prevents you from becoming that homeowner.

The five viable exit paths

| Exit path | How it works | Best fit | Risk |

|---|---|---|---|

| Sell the property | The HEI is settled from sale proceeds; you walk with the difference | Owner planning to sell within the HEI term anyway | You give up the home and any future appreciation; if the market is soft at sale, the proceeds may be tight |

| Refinance the first mortgage | Use the ADU-boosted appraisal to pull out cash and settle the HEI | Owner whose ADU materially increased home value and who can qualify for a refi | HEI lien on title may complicate refi; the appraisal at refi may not produce enough cash |

| Pay with savings or other liquid assets | Cash buyout at term end | Owner with high liquidity and clear long-term cash position | Liquidity drain; opportunity cost of pulling capital from investments |

| Settle gradually from rental income (where partial buyback is allowed) | Make partial principal payments over the term; settle the balance at end | Long-term ADU landlord; Unlock specifically advertises partial-payment flexibility | Requires rental performance; tenant turnover and vacancy risk |

| Family or estate transfer | Settle the HEI during a property transfer event (gift, inheritance, sale to family) | Multigenerational ADU plans | Tax complexity; legal complexity around estate; provider may have triggering-event rules |

The exit-plan stress test

Before you sign, walk through these scenarios out loud and write your answer:

- → If my home appreciates at 5% per year, my settlement is approximately $X. How would I cover that?

- → If my home appreciates at 7%, settlement is approximately $Y. Same question.

- → If I want to refinance in Year 7 to settle, does my projected post-ADU appraisal support enough cash-out to cover the HEI plus closing costs?

- → If the refi doesn’t appraise, what is Plan B? Do I have it written?

- → If I need to sell, am I willing to give up this home?

If you can’t answer one of these clearly, you don’t have an exit plan yet.

The refinance warning, said plainly

The HEI lien sits on your title. A refinance lender will see it. The refinance lender’s terms may require the HEI to subordinate or be paid off entirely from the refi proceeds — and if the cash-out isn’t enough to cover the HEI buyout, the refi can’t close.

Ask your HEI provider, in writing, before signing:

- What is your subordination policy when I want to refinance my first mortgage?

- How long does subordination take to process?

- What documentation do you require?

- Will you subordinate to any first-lien lender, or only to specific ones?

- Are there fees for subordination?

A provider that won’t put this in writing isn’t a provider you want.

ADU cost reality check: what you’re actually funding

An ADU in the United States in 2026 ranges from approximately $80,000 for a basic garage conversion at the low end to $400,000 or more for a detached new build in coastal California at the high end. Most permitted ADU projects fall between $150,000 and $300,000 all-in. California projects cluster in the $200–$450 per square foot range, with Bay Area detached units in 2026 often running $250,000–$350,000 for 500–800 square feet, per industry cost guides published within 90 days. Use these as anchor points for sizing your HEI request — and remember that HEI funding caps of $500,000–$600,000 mean it’s possible to over-borrow.

For a full city-by-city cost breakdown see: ADU Financing Options: 8 Paths Compared.

ADU rental income vs HEI buyout: the math most providers won’t run for you

If you’re funding an ADU as a rental property, you’re running two cash flows simultaneously: the HEI obligation building on one side, and rental income accumulating on the other. Here’s a worked illustrative example using a $150,000 HEI advance, a $1,500/month ADU rental rate (moderate-market assumption for a one-bedroom ADU), and 5% annual appreciation.

Illustrative rental-vs-buyout scenario

- Year 10 home value at 5% appreciation: ~$1,140,000

- HEI 35% share at settlement (illustrative model): ~$399,000

- Gross rental income over 10 years (assuming 5% annual rent growth and 5% vacancy): ~$227,000

- Net rental income at 60% operating efficiency: ~$136,000

- Gap at settlement: ~$263,000

In this scenario, the rental income alone does not close the HEI buyout. The homeowner needs either (a) refinance the ADU-boosted appraisal to extract enough equity at settlement, (b) sell the property, or (c) bring substantial savings. If the provider’s improvement-adjustment language carves out the ADU’s contribution to value, the buyout drops materially.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

This is exactly the math that the improvement-value clause changes. It’s also the math no provider’s online calculator runs for you.

If you’re building for rental — the operational side

Once your ADU is built and producing, the operational side matters as much as the financing. Tenant screening, lease templates, rent collection, maintenance scheduling, and tax reporting all become real work. We recommend Buildium (affiliate) for property-management software built for landlords with one to a few rental units — useful for ADU owners stepping into the rental landlord role for the first time. Buildium handles tenant screening, lease documents, rent collection, maintenance tickets, and the accounting your CPA will ask about at tax time.

What to look for in the HEI contract before you sign (ADU-specific)

Before signing any HEI for an ADU build, get five things in writing: (1) the improvement-adjustment clause naming the ADU specifically and how the added value will be excluded from the provider’s share, (2) the rate cap on the annualized cost, (3) the partial-buyback option and prepayment penalties, (4) any restrictions on renting the ADU or the main home, and (5) the appraisal methodology and dispute process for the settlement-date valuation. These are the five clauses where HEI providers most often diverge and where ADU homeowners most often get surprised.

1. The improvement-adjustment clause — get the ADU explicitly named

Don't accept "improvements will be considered." Get the language that says your ADU build qualifies under the provider's specific framework, what documentation is required, what triggers the adjustment, and how it interacts with the settlement-date appraisal. Hometap's renovation-adjustment framework specifies renovations of $25,000 or more with documented receipts and photos. Unlock states improvement value is determined by a third-party appraiser. Point's published policy is that improvement appreciation is included in the share — meaning the adjustment may not exist for Point customers.

2. The rate cap (annualized-cost ceiling)

Most reputable HEI agreements include an annualized-cost cap — typically near 19.9% to 20% per consumer-protection research and provider disclosures. The cap means your settlement amount cannot grow faster than the cap percentage compounded annually. Without a cap, a fast-appreciating market can produce an effective annualized cost in the high 20s or beyond. Confirm the cap exists, confirm the percentage, and confirm whether the cap is on total cost or on appreciation share.

3. Partial buyback rights and prepayment penalties

Some providers (Unlock notably) allow partial buybacks — making partial principal payments during the term to reduce the final settlement amount. Others (Point) require a full buyback at exit. Hometap allows full early settlement without prepayment penalty but doesn't structure partial paybacks the way Unlock does. If you anticipate paying down portions over time from ADU rental income, Unlock's structure may fit better. Confirm prepayment penalty terms — most providers have none, but read your specific agreement.

4. Restrictions on renting your home or the ADU

HEI providers care about the property's condition and value. Most allow rental of an ADU built with HEI funds. Some require notification. Some have caps on the percentage of the main home that can be rented separately. Some have specific clauses around short-term rental (Airbnb-style use). Get these in writing if you intend to rent.

5. Settlement-date appraisal methodology and dispute process

The single biggest source of HEI complaints to the CFPB was appraisal disputes — values that came in too high at settlement (inflating the provider's share). Your agreement should specify: who orders the appraisal at settlement (usually the provider, but you can sometimes negotiate dual-appraisal rights), what appraiser qualifications are required, what the dispute process looks like, whether you have a right to an independent appraisal, and what happens if appraisals disagree.

6. The arbitration clause — flag for attorney review

The CFPB's January 2025 Issue Spotlight specifically called out arbitration clauses in HEI agreements as a consumer-protection concern. Mandatory arbitration limits your remedies if disputes arise — you can't sue, you can't join a class action, you go to arbitration on the provider's preferred terms. If the agreement contains a mandatory arbitration clause, flag it for your attorney to review before signing. Some providers have removed them.

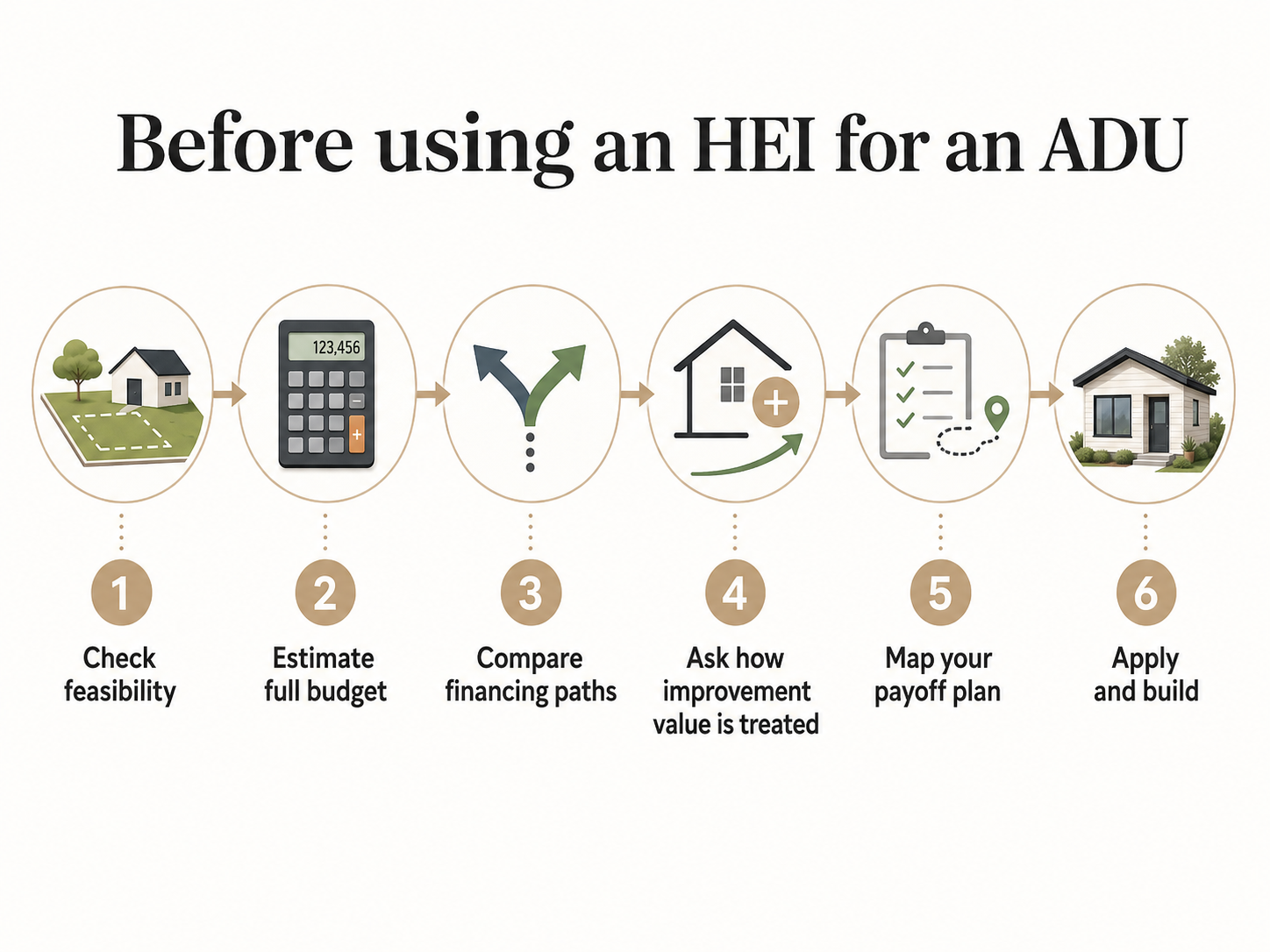

Pre-application checklist: the order to do things in

Confirm ADU feasibility first, then estimate project cost, then compare financing paths, then verify HEI provider state availability, then ask each finalist in writing about improvement-value treatment, then run the exit-plan check, then consult with a financial or legal professional, and only then apply. This order matters — applying for an HEI before confirming ADU feasibility creates a future settlement obligation against a project that may not be buildable.

The 8-step pre-application sequence

- 1Confirm your property can host the ADU you want. Setbacks, FAR, lot coverage, height limits, parking, utility capacity, HOA rules. Run the Dwelling Index feasibility check or consult a local architect or builder.

- 2Get a rough total project cost including design, permits, sitework, utilities, construction, contingency (15–20% of construction), and financing costs.

- 3Compare all financing paths for your specific situation — HELOC, cash-out refi, renovation loan (RenoFi-style, HomeStyle, 203(k)), construction-to-permanent, HEI, and cash.

- 4Check HEI provider state availability at the provider's own current "where we operate" page.

- 5Ask each HEI finalist three written questions: "How will an ADU I build with these funds be treated under your improvement-value adjustment?" / "What is your subordination policy if I refinance my first mortgage during the term?" / "What is your appraisal dispute process at settlement?"

- 6Run the exit-plan stress test (covered in this article).

- 7Consult a qualified financial, legal, or tax professional before signing. Specifically: a licensed attorney in your state with consumer-protection or mortgage experience.

- 8Apply only if the cash-flow advantage of avoiding a monthly payment outweighs the future-value tradeoff and the regulatory uncertainty.

Documentation you’ll need to gather

- Recent mortgage statement

- Most recent home appraisal (or comparable market analysis)

- Government-issued ID

- Social Security number

- Proof of homeowner's insurance

- HOA documents if applicable

- Property tax bills

- Two months of bank statements (some providers)

- Recent credit report (free at annualcreditreport.com)

- Title information / deed

- For ADU applications: preliminary design, cost estimate, permit application or approval

Know your property's ADU potential before you negotiate any HEI agreement.

Want a printable version of the questions to ask any HEI provider?

The Free ADU Starter Kit includes the ADU HEI Exit-Plan Worksheet — the five-condition fit check, the three provider-question scripts, the documentation checklist, and the worked buyout math from this article, packaged as a one-page worksheet you can take into any HEI conversation. The kit also covers ADU costs, permits, contractor-bid checklists, and the financing-comparison reference table.

Costs, permits, financing comparison, and the printable HEI provider question script. Sent once. No follow-up sales sequence.

Frequently asked questions

Can I use a home equity investment to build an ADU?

Yes. Hometap, Unlock, and Point each publish home-improvement or flexible-use language in their consumer materials, and ADU construction qualifies under that language. State availability, property eligibility, and improvement-value treatment vary by provider.

Is a home equity investment a loan?

The legal answer is unsettled. HEI providers describe their product as an investment, not a loan, and structure agreements that way. The CFPB argued in its January 2025 amicus brief in Roberts v. Unlock that at least the Unlock product is a residential mortgage loan under the Truth in Lending Act, then later moved to withdraw that amicus brief. Connecticut, Maryland, Illinois, and Maine have enacted state laws that bring HEI-style products under mortgage or consumer-credit regulation. For practical purposes, an HEI is a home-secured financial obligation with a future settlement, regardless of legal characterization.

What's the catch with home equity investments?

The settlement amount can be substantially larger than the cash received, especially if your home appreciates. The CFPB modeled a $50,000 advance settling at $94,000–$216,000 over ten years depending on appreciation. The "catch" is that "no monthly payment" is not the same as "low cost" — you pay through equity sharing, not interest, and the equity share can be larger than equivalent interest would have been.

How much do you actually pay back on an HEI?

You pay back the provider's share of your home's value at settlement, calculated per the agreement's specific formula. In our illustrative model on a $150,000 advance over 10 years, settlement amounts ranged from $245,000 (flat home value) to $482,000 (7% annual appreciation) — but the actual formula depends on the specific provider agreement, the settlement-date appraisal, and the improvement-value treatment.

What credit score do I need for an HEI?

Published FICO floors as of May 2026: Unlock and Point accept 500; Hometap publishes a 575 minimum FICO on its own resource page. Lower floors do not mean automatic approval — providers evaluate the full application, and eligibility criteria are subject to change.

How much equity do I need?

Provider equity requirements as of May 2026: Unlock publishes 30%; Hometap looks for 25%+ post-investment; Point requires homeowners to retain a significant percentage of equity after Point's investment, confirmed by prequalifying. Equity is measured as the home's appraised value minus your existing mortgage balance.

Are HEIs available in my state?

Coverage varies. As of May 2026, Hometap publishes availability in 16 states; Point operates in select regions of 27 states plus D.C.; Unlock requires the property to be in Unlock's service area, verified by address. Connecticut, Maryland, Illinois, and Maine have enacted statutes regulating HEI-style products; Washington has open rulemaking. Verify on each provider's site immediately before applying.

Can I use an HEI on a property that already has an ADU?

Provider-dependent. Some HEI agreements have specific clauses about existing rental or accessory units. Unpermitted existing ADUs are commonly disqualifying. Permitted ADUs may be acceptable. Ask the provider directly.

Does an HEI affect my first mortgage?

Yes, the HEI records a lien on title. The CFPB specifically identified refinance friction as a top consumer complaint — refinance lenders see the HEI lien and may require subordination, payoff, or decline.

Can I rent out my ADU if I funded it with an HEI?

Generally yes, but agreements vary. Some providers require notification. Some have caps. Some have restrictions on short-term (Airbnb-style) rental. Get the rental rights confirmed in writing.

What happens if I can't repay the HEI at the end of the term?

The agreement triggers settlement. You may need to sell, refinance, or otherwise produce the cash. The CFPB documented complaints from consumers who felt they were forced to sell their homes to settle. Build the exit plan before you sign — not at month 116 of a 120-month term.

Can I prepay an HEI early?

Most major providers (Hometap, Unlock, Point) allow early settlement without prepayment penalty. Unlock additionally allows partial buybacks during the term. Confirm specifics in your agreement.

Will an HEI affect a future cash-out refinance or construction loan?

Yes. The HEI lien sits on title and any future lender will see it. Construction loans during the build may require subordination from the HEI; refinance lenders later will too. Ask the HEI provider for its subordination policy before signing.

Does the CFPB still allow HEIs?

Yes. The CFPB issued a Consumer Advisory warning homeowners about home equity contracts in January 2025 and filed an amicus brief in Roberts v. Unlock arguing that some HEIs are mortgage loans under TILA; the bureau later moved to withdraw that amicus brief. The CFPB did not ban HEIs. Several states have moved to regulate HEIs as mortgage loans through state-level statute.

What we verified

Last verified: May 19, 2026

| Verified | Source |

|---|---|

| Hometap state availability (16 states), product term, no-monthly-payment structure, $600,000 advertised maximum | Hometap.com state coverage and homepage |

| Hometap minimum FICO (575), eligibility-subject-to-change disclosure | Hometap.com resource page on accessing home equity without perfect credit |

| Hometap renovation adjustment policy (renovations $25K+) | Hometap.com renovation loan content |

| Unlock service-area requirement, 30% equity, $175,000+ property value, 500 minimum credit score, $15,000 minimum advance, up to $500,000 | Unlock.com how-it-works page and FAQs |

| Unlock improvement adjustment language and partial-payment flexibility | Unlock.com blog on home equity agreement buyouts |

| Point state list (27 states + D.C.), select-regions language, up to $600,000, 30-year term, 500 minimum FICO | Point help center "Where does Point offer HEIs?" |

| Point qualification details — significant equity required, 7+ acre exclusion | Point help center qualification article |

| Point improvement-value treatment (improvement appreciation included in share) | Point help center "Can I remodel the home at any time?" |

| CFPB position on home equity contracts | CFPB Issue Spotlight and Consumer Advisory, January 15, 2025 |

| CFPB amicus brief in Roberts v. Unlock and subsequent motion to withdraw | Court docket and Orrick InfoBytes hosted motion-to-withdraw filing |

| State regulatory updates (CT, MD, IL, ME enacted; WA in process) | JD Supra licensing update 2025; Maine Legislature LD 1901; Washington State Legislature HB 1464 |

| Olson v. Unison — August 7, 2025 Ninth Circuit memorandum; appeal dismissed October 17, 2025 after settlement | Justia case records |

| Massachusetts AG v. Hometap — filed February 2025; motion to dismiss denied August 2025 | CommonWealth Beacon reporting; NCLC litigation summary |

| Stone v. Real Estate Equity Exchange — Bankr. D. Colorado, July 30, 2025 | Court records; NCLC issue brief |

| Weingot v. Unison — D.N.J., 2025 | Court records |

| Bankrate national average HELOC rate ~7.26% as of May 6, 2026 | Bankrate.com HELOC rates page |

| U.S. Bank HELOC rate range 7.20%–10.85% APR (December 11, 2025 calculator disclosure) | U.S. Bank home equity rate and payment calculator |

| FHFA California ADU appraisal data (2013–2023, single-family Enterprise-backed purchases) | FHFA, "Trends in Median Appraised Value for Properties with Accessory Dwelling Units in California" |

| HECM federal insurance, HUD oversight, mandatory counseling, age 62+ | HUD HECM home page; CFPB consumer-facing reverse mortgage information |

What we did not verify for any individual reader

- Whether your specific property qualifies with any HEI provider (requires their underwriting)

- Whether your ADU is legal in your specific city or county (requires local review)

- Whether you will be approved (provider-specific)

- Your actual settlement amount at HEI exit (depends on the agreement, the appraisal, the timing, and the home’s value at settlement)

- The tax treatment of HEI proceeds, ADU rental income, or settlement payments (consult a tax professional)

- The current affiliate / tracking status of HEI providers (none are currently active affiliates of The Dwelling Index)

Methodology

This guide was created by The Dwelling Index, an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, builder, or affiliate of any home equity investment company.

For the provider matrix, we cross-referenced six independent 2026 provider reviews (Bankrate, CNBC Select, U.S. News, FinanceBuzz, LendEDU, SuperMoney) against each provider’s official site and help center. Where 2026 sources disagreed — most notably on provider state counts — we deferred to each provider’s own current “where we operate” page and timestamp our verification date.

Cost scenarios were modeled using illustrative assumptions stated alongside each model. We cross-checked our modeling methodology against the CFPB’s January 2025 Issue Spotlight worked examples. The 35% provider share at settlement is an illustrative model assumption, not a provider-typical figure; actual provider formulas vary.

Court rulings are cited to docket numbers and to the National Consumer Law Center’s May 27, 2025 issue brief on home equity investments. Regulatory updates are cited to the JD Supra licensing update, Maine LD 1901, and Washington State Legislature records.

We sort the provider comparison table by neutral criteria (improvement-value treatment category, then alphabetical), not by compensation. We earn no commission from any HEI provider on this page. The page’s affiliate revenue comes from Mortgage Research Center (for alternative financing routing) and Buildium (for property management software for new ADU landlords) — both disclosed at the top of this page and at every CTA.

Reddit and homeowner-forum sources were consulted only for voice-of-customer language and objection identification, not as proof for legal, financial, or regulatory claims.

This page does not provide legal, financial, tax, or investment advice. Before signing any home equity contract, review the agreement with a licensed attorney in your state and a financial advisor independent of the HEI provider. The Consumer Financial Protection Bureau publishes a free consumer advisory on home equity contracts at consumerfinance.gov.

Financial disclaimer

This page is for educational purposes only and does not constitute financial, legal, or tax advice. Home equity investments are complex financial products and the long-term cost can be difficult to predict. Examples of rental income, appreciation, and buyout amounts are illustrative — not guarantees of returns. Actual outcomes depend on local market conditions, construction costs, regulatory approvals, contract terms, and your individual financial situation. Eligibility, terms, and availability change without notice.

Not sure where to start? See what’s possible at your address.

Get Your Free ADU Report in 60 Seconds