ADU Financing Without Monthly Payments: Real 2026 Options

Last updated: · Last verified: · By the Dwelling Index Editorial Team

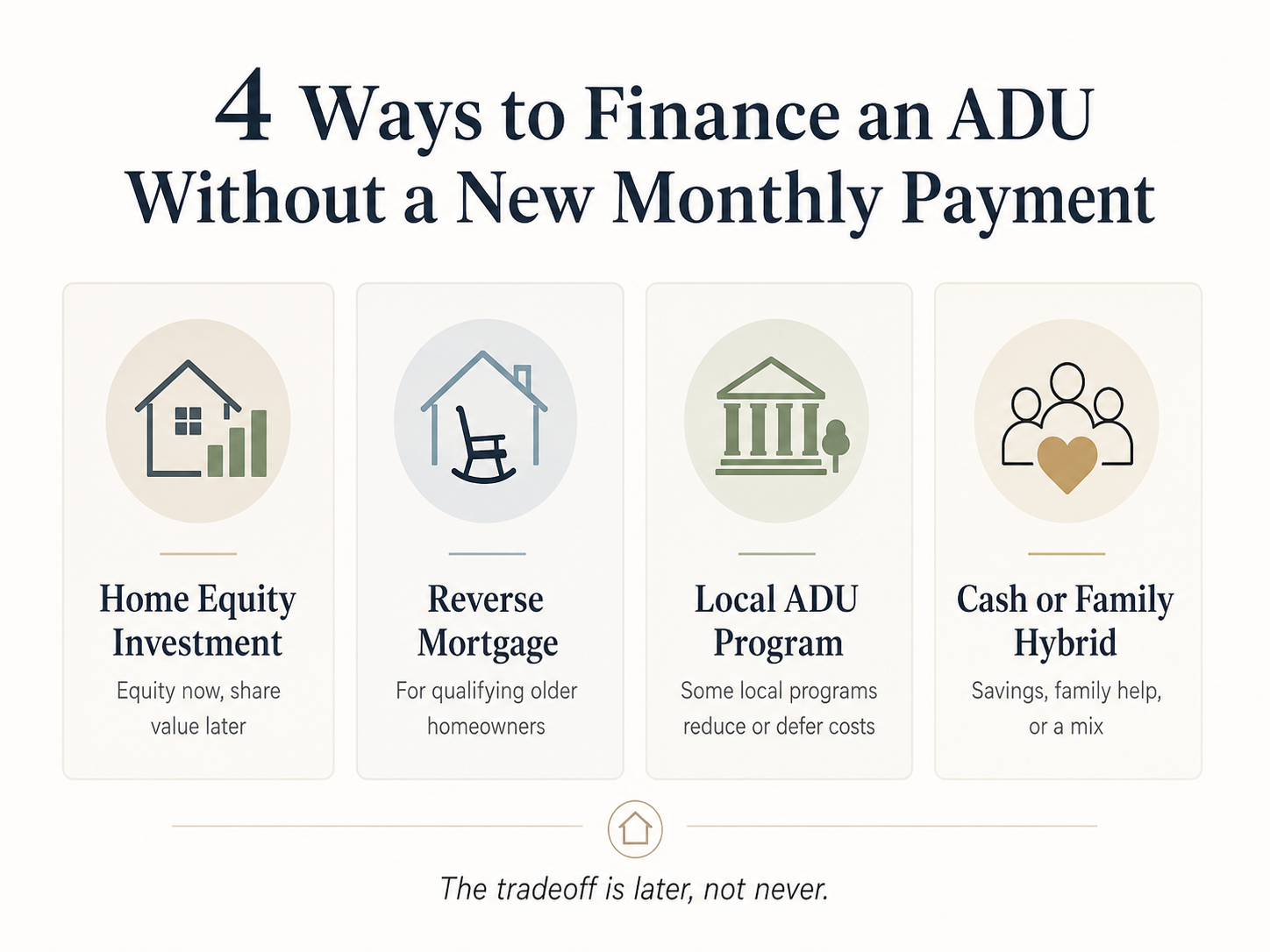

The short answer

ADU financing without monthly payments is possible, but the paths are narrower than most builder blogs admit. In 2026, the four realistic ways to fund an accessory dwelling unit (ADU) build without taking on a new required monthly payment are: a home equity investment or home equity agreement from companies like Hometap, Unlock, or Point; a HUD-insured Home Equity Conversion Mortgage (HECM) for homeowners 62 and older; a local deferred-payment ADU program where one exists; or cash and family contributions. The critical ADU-specific question isn’t just “no monthly payment?” — it’s “who gets the value the new ADU creates?”

Independent educational resource · Not a lender or broker · Terms verified against official provider documentation · Sources: HUD, CFPB, provider sites, court filings

At a glance: the four no-monthly-payment paths

| Path | Monthly payment? | Who it fits | Biggest gate | Biggest ADU-specific risk |

|---|---|---|---|---|

| Home Equity Investment (HEI / HEA) | None during the term | Equity-rich, cash-flow-sensitive owners under 62 | State availability + 20–40% equity | Provider may share in the value your new ADU creates |

| HECM Reverse Mortgage | No required mortgage payment (taxes, insurance, occupancy obligations remain) | Owners 62+ staying in the home long term | Age, primary residence, HUD counseling | Loan balance grows; reduces estate equity |

| Local Deferred-Payment ADU Loan | Deferred until sale, refinance, or transfer | Homeowners in qualifying cities (Boston is the strongest 2026 example) | Geography + program rules | Recorded lien + program-specific repayment triggers |

| Cash, Family Contribution, or Hybrid | None | Liquid or family-supported owners | Liquidity or family willingness | Estate, tax, and family-dynamic risk |

See what’s possible at your address → Before comparing financing, confirm your lot, ADU type, and likely scope are realistic. (60 seconds, no commitment)

Get Your Free ADU ReportOr jump straight to the decision tool → Answer five questions about your state, age, equity, ADU type, and exit horizon.

Use the ADU Financing Path Finder

Is ADU financing without monthly payments actually possible?

Answer capsule: Yes. Four products allow homeowners to fund ADU construction without a new required monthly payment: home equity investments (HEI/HEA), HUD-insured Home Equity Conversion Mortgages (HECM), specific local deferred-payment ADU programs, and cash or family contributions. “No monthly payment” does not mean free — each path carries a future cost in the form of appreciation share, accrued interest, program covenants, or opportunity cost. None of these are short-term solutions.

We need to draw a clean line, because the phrase “no monthly payments” gets used loosely. A builder offering “no payments for six months” while construction is underway is still selling you a loan that will have monthly payments — it’s a promotional deferral, not the structural answer you’re looking for. The four paths above are structurally different. They are products designed so the homeowner never makes a required monthly payment to the financing provider — for the life of the agreement, not just a teaser period.

The homeowners who typically need this answer are usually solving for one of three constraints:

- A low first-mortgage rate they refuse to touch. A 2.875% or 3.25% mortgage locked in during 2020–2021 is worth a lot. Refinancing to fund an ADU at today’s rates would trade a 30-year-low coupon for a current-cycle rate. A no-monthly-payment product preserves that first lien untouched.

- A debt-to-income (DTI) ratio that won’t approve another payment. Self-employed homeowners, retirees, and homeowners already carrying student loans or a car note often can’t add another fixed monthly obligation. HEIs typically have no DTI requirement at all; HECM underwriting tests residual income rather than DTI.

- A fixed income with no room for another bill. Retirees on Social Security and a pension can absorb one-time costs through accumulated equity but cannot absorb a recurring payment without compressing their lifestyle.

If you fit one of those three profiles, the right question isn’t “can I get a loan” — it’s “which path costs me the least over the time I plan to hold this property, and who ends up with the value the ADU itself creates?”

Important terminology

- ADU (accessory dwelling unit)

- A secondary, smaller, fully independent living unit on a single-family lot. Subtypes include detached ADUs (DADU), attached ADUs, garage conversions, basement ADUs, and junior ADUs (JADU — typically under 500 square feet within the existing home footprint).

- HEI / HEA / HESA

- Home Equity Investment, Home Equity Agreement, and Home Equity Sharing Agreement are all names for the same product category — a non-loan contract giving you cash now in exchange for a share of your home's future value.

- HECM

- Home Equity Conversion Mortgage. The FHA-insured reverse mortgage available to homeowners age 62 and older.

- HELOC

- Home Equity Line of Credit. A revolving second mortgage that does require monthly payments — included here for comparison because it's the most common payment-bearing alternative.

- Covenant

- A recorded restriction on the property requiring the owner to do something (or not do something) for a defined period. Some local ADU programs attach affordability covenants.

- Lien position

- The order in which secured creditors get paid from sale proceeds. Your first mortgage is typically first-lien; a HELOC is usually second-lien. HEI providers record a lien too — confirm position in your specific contract.

The four no-monthly-payment paths in 2026 — full matrix

Answer capsule: In 2026, HEI providers publish maximum investments of $500,000 to $600,000 with terms of 10 to 30 years; the HECM maximum claim amount is $1,249,125 per HUD’s December 2025 announcement effective January 1, 2026; Boston’s ADU Financial Assistance Program offers up to $50,000 at 0%. Every row in this matrix carries verification dates — we re-verify quarterly.

Below is our 2026 No-Monthly-Payment ADU Financing Matrix, assembled from primary provider sources, HUD Mortgagee Letter 2023-17 and the Single Family Housing Policy Handbook 4000.1, the CFPB’s January 2025 Issue Spotlight on home equity contracts, and the official program pages of the municipal lenders cited.

| Path / Provider | Monthly payment? | Max cash | Term | Geography | Min FICO | ADU-created-value treatment | Verified |

|---|---|---|---|---|---|---|---|

| Hometap (HEI) | None | Up to $600,000 | Up to 10 years | 16 states: AZ, CA, FL, IN, MI, MN, MO, NV, NJ, NY, OH, OR, PA, SC, UT, VA. Not currently originating in Massachusetts. | 575 | “Renovation adjustment” framework — case-by-case, must be confirmed in writing before signing | |

| Point (HEI) | None | Up to $600,000 | Up to 30 years | ~25–28 states + DC | 500 | Per Point’s published help center, “remodel-created appreciation is included in overall appreciation” used for repayment — a material ADU tradeoff | |

| Unlock (HEA) | None | Up to $500,000 | Up to 10 years | ~25 states | 500 | Publishes “improvement adjustments” that may credit the homeowner for qualifying improvements — confirm documentation requirements | |

| Unison (HEA) | None | Up to $500,000 (capped at 15% of home value) | 30 years | ~29 states + DC | ~650 | See regulatory risk section below for Olson v. Unison context | |

| HECM Reverse Mortgage (HUD-insured) | No required mortgage payment; taxes, insurance, occupancy obligations remain | Principal limit capped by $1,249,125 maximum claim amount (2026); actual draw is age- and rate-dependent | Until borrower sells, moves, or passes away | All 50 states (HUD-approved lenders) | No minimum | No investor share of ADU value; loan balance grows over time | |

| Boston ADU Financial Assistance | Deferred (0%) | Up to $50,000 | Deferred until sale, ownership transfer, or cash-out refinance | City of Boston only | Program-set | No investor share; program-specific repayment triggers apply | |

| Cash / family contribution | None | Whatever family or savings supports | N/A | Anywhere | N/A | Homeowner retains 100% of ADU-created value | Editorial |

Hometap’s Massachusetts exit is real and recent. Massachusetts Attorney General Andrea Joy Campbell filed a complaint against Hometap on February 19, 2025; a Suffolk County Superior Court judge denied Hometap’s motion to dismiss in August 2025. Hometap stopped originating new agreements in Massachusetts while the case proceeds.

Point’s published treatment of “remodel-created appreciation” is the single most important ADU-specific contract fact most homeowners miss. If you build a $300,000 ADU that raises your appraised home value by $250,000 at sale, Point’s published help docs include that improvement-driven appreciation in the value used to calculate repayment. That single contract clause can swing the cost of your no-payment agreement by tens of thousands of dollars at settlement.

There’s also a fifth product class many homeowners ask about: Splitero. We’ve reviewed Splitero’s public materials but were unable to verify current state availability, maximum investment, term, and improvement-treatment language to the standard we require for this matrix. If you’re considering Splitero, request the current term sheet and improvement-treatment language directly before applying.

See what’s possible at your address → Confirming the ADU itself is feasible — lot, zoning, scope, likely budget — is the step that should happen before you compare financing terms. (60 seconds, no commitment)

Get Your Free ADU ReportWhat happens to the value your ADU creates?

Answer capsule: Before signing any no-monthly-payment financing agreement, the most important ADU-specific question is whether the provider shares in the value the new unit creates. Some HEI providers, like Point, publish that remodel-created appreciation is included in the appreciation used for repayment. Others, like Unlock and Hometap, publish improvement-adjustment language that may credit the homeowner — but documentation requirements and final treatment depend on the contract you sign. A permitted ADU can add hundreds of thousands of dollars in market value, which means this single clause can swing the cost of an equity-sharing agreement materially at settlement.

This is the question almost no national ADU financing guide answers clearly, and it’s the reason this page exists.

Worked example — the math that makes the question matter

Suppose you sign an HEI today for $200,000 against a home appraised at $1,000,000. You then build a permitted, detached 800-square-foot ADU for $300,000 that adds approximately $250,000 to your appraised home value. At sale ten years later, the home appraises higher than it would have without the ADU. The provider’s contract gives them a percentage share of your home’s value at settlement. Whether that share is calculated on a value that includes or excludes the ADU’s contribution is the difference between two materially different settlement numbers.

| Assumption | Value |

|---|---|

| Home value at signing | $1,000,000 |

| HEI investment received | $200,000 (20% of value, 25% of appreciation share) |

| Risk-adjusted starting value | $850,000 (15% discount, typical) |

| Planned ADU build cost | $300,000 |

| ADU contribution to appraised value | $250,000 |

| Broader market appreciation | 3% annually |

| Exit year | Year 10 (sale) |

| Exit value, broader market only | ~$1,343,000 |

| Exit value, broader market + ADU | ~$1,593,000 |

| Provider share base if ADU excluded | (~$1,343,000 − $850,000) × 25% ≈ $123,000 plus principal repayment |

| Provider share base if ADU included | (~$1,593,000 − $850,000) × 25% ≈ $186,000 plus principal repayment |

| Approximate difference in settlement | ~$63,000 (illustrative) |

These figures are illustrative. They depend on your home’s actual appraisal, specific contract terms, fees, and market conditions. Not a quote or offer.

What we found by reading the providers’ own published materials (May 2026)

| Provider | Published improvement-treatment language | What we read it to mean for ADU builders | What you need to do before signing |

|---|---|---|---|

| Hometap | Hometap publishes a “renovation adjustment” framework, but the accepted adjustment is not guaranteed. Documentation requirements apply. | Permitted ADU construction may qualify, but the adjustment is case-by-case and not a contractual entitlement. | Ask, in writing, whether a permitted ADU completed during the term qualifies, what documentation is required, and what the cap on adjustment is. |

| Unlock | Unlock publishes that qualifying improvements may be credited so the value added by the improvement is not subject to the share. | This is the most favorable published language we found for ADU builders. | Ask exactly what documents Unlock needs and confirm before construction starts. |

| Point | Per Point’s published help center: when it is time to repay, the home value includes appreciation from improvements made during the agreement, and that increase is part of the overall appreciation shared. | This is the least favorable language for ADU builders. The new ADU’s value gets pulled into Point’s share. | If you choose Point anyway, model your settlement under multiple appreciation scenarios that include the ADU’s contribution. |

| Unison | Treatment varies by contract. See regulatory risk section below for Olson v. Unison context. | Treatment must be confirmed in writing before signing. | Request the specific contract language about home improvements and have a real estate attorney review. |

The improvement-documentation file every ADU builder should keep

- The recorded building permit and any subsequent permit amendments

- Approved plans and engineered drawings

- All contractor and subcontractor invoices with dates

- Material and finish receipts

- Photographs of progress at each major construction milestone

- Pre-construction appraisal of the property (order one before you start if you don’t already have a recent one)

- Final certificate of occupancy or final inspection sign-off

- Post-construction appraisal showing the home’s value with the ADU complete

Ask this before signing — exact wording for your conversation with the provider:

“If I build a permitted accessory dwelling unit after receiving funds, does your company share in the value created by that ADU? If yes, how is that value calculated, what is the cap, and what documentation do you require? If no, what documents do I need to keep to prove the improvement-created value at settlement?”

If the answer comes back vague, you don’t have a deal — you have a future dispute. Don’t sign vague.

Or run your situation through the path finder → It flags whether your ADU plan makes improvement-treatment language especially important.

Use the ADU Financing Path FinderHome equity investments (HEI/HEA) for ADU construction — the deep dive

Answer capsule: A home equity investment gives you cash today — typically up to 20–25% of your home’s appraised value or $500,000 to $600,000, whichever is less — in exchange for a share of your home’s future value at settlement. HEIs require no monthly payments and typically no income or DTI documentation. Effective annualized cost depends on how much your home appreciates and when you settle; HEI providers commonly publish that costs can range from a single-digit IRR to over 20% annualized depending on outcome. The category is under active state regulatory scrutiny in 2026.

The mechanics

- Pre-qualification. You enter your address, mortgage balance, estimated home value, and basic eligibility data. Most providers can give a preliminary estimate in a few minutes with no hard credit pull.

- The risk-adjusted starting value. Before calculating the provider’s share, providers typically apply a discount to your home’s appraised value to protect their downside. That discount works in your favor only if home values fall — otherwise it enlarges the provider’s effective share at settlement.

- The appraisal. A third-party appraiser establishes the starting value. The provider applies the risk adjustment. The cash advance is calculated as a percentage of that adjusted value, typically capped at 20–25%.

- Closing and funding. Most providers wire funds within several weeks of application start. Hometap publishes that its application takes about 20 minutes and funding lands within a few business days of signing. Unlock publishes a 30–60 day funding timeline.

- The term. Hometap and Unlock use up-to-10-year terms. Point uses up to 30 years. Unison uses up to 30 years.

- Settlement. You settle by selling the home, refinancing, or buying out the provider — all of which trigger an exit appraisal that determines the home’s then-current value. You pay back the original cash advance plus the provider’s share of the new value.

The fees, in plain dollars

For a $200,000 investment, a typical fee load across the major providers in 2026:

| Fee type | Range | Notes |

|---|---|---|

| Origination / processing | 3.0% – 4.9% of investment | $6,000 – $9,800 on $200K |

| Appraisal | $450 – $750 | Third-party |

| Title / escrow / recording | $1,500 – $3,500 | Varies by state |

| Government fees | $0 – $2,500 | Varies by state and county |

| Total typically deducted at closing | ~$8,000 – $14,000 | Most providers deduct from the advance, so no out-of-pocket at signing |

Who qualifies — and who doesn’t

HEIs flip traditional underwriting on its head. There is typically no income verification, no DTI calculation, and no employment requirement. The product is underwritten primarily on the property: equity position, location, condition, and value.

- Credit score: Unlock and Point go as low as 500 minimum. Hometap publishes a minimum FICO of 575.

- Equity: 20–40% post-investment is the typical bar.

- Property type: all major HEI providers fund single-family homes; most fund condos and 1–4 unit multifamily. Manufactured homes are typically excluded.

- State availability: the constraint that disqualifies most homeowners before any other — see the state matrix below.

HEI is genuinely best for

- Equity-rich homeowners under 62 with low first-mortgage rates they refuse to disturb

- Self-employed or retired homeowners with income too irregular to satisfy DTI rules

- Homeowners who plan to hold the property seven or more years

- Homeowners who understand that “no payment” means cost moves to the back end

HEI is a bad fit for

- Anyone planning to sell or refinance within two to four years

- Anyone in a market they expect to appreciate rapidly

- Anyone who would not be able to repay the balloon at end of term

- Anyone uncomfortable with contract complexity

We do not currently have an affiliate relationship with Hometap, Unlock, or Point. If you decide to apply, you’ll go directly to the provider — we don’t earn anything on that click.

Which HEI providers serve your state?

Answer capsule: HEI/HEA products are not available nationwide. As of , Hometap publishes availability in 16 states and is no longer originating in Massachusetts. Point publishes approximately 25–28 states plus DC. Unlock publishes approximately 25 states. Unison publishes approximately 29 states plus DC. State availability changes frequently — always confirm directly with the provider before applying.

| Provider | Published 2026 state list (verify directly before applying) | Notes |

|---|---|---|

| Hometap | Arizona, California, Florida, Indiana, Michigan, Minnesota, Missouri, Nevada, New Jersey, New York, Ohio, Oregon, Pennsylvania, South Carolina, Utah, Virginia | 16 states, verified . Not currently originating in Massachusetts during ongoing AG litigation. |

| Point | Arizona, California, Colorado, Connecticut, Florida, Georgia, Hawaii, Illinois, Indiana, Kentucky, Maryland, Michigan, Minnesota, Missouri, Nevada, New Jersey, New York, North Carolina, Ohio, Oregon, Pennsylvania, South Carolina, Tennessee, Utah, Virginia, Washington, Wisconsin, plus Washington DC | Some availability is regional within a state. |

| Unlock | Arizona, California, Florida, Hawaii, Idaho, Indiana, Kentucky, Michigan, Missouri, Montana, Nevada, New Hampshire, New Jersey, New Mexico, North Carolina, Ohio, Oregon, Pennsylvania, South Carolina, Tennessee, Utah, Vermont, Virginia, Wisconsin, Wyoming | Funds investment properties (uncommon for HEI). Partial buyouts allowed during the term — also uncommon. |

| Unison | Approximately 29 states plus DC | See regulatory risk section below. |

States where you’ll likely have multiple HEI providers to compare: Arizona, California, Florida, Nevada, New Jersey, Ohio, Oregon, Pennsylvania, South Carolina, Utah, and Virginia consistently appear in three or more major providers’ state lists.

States where no major HEI provider currently operates include several Plains and Mountain West states, parts of New England, and several Midwest states. If you’re in one of these states, skip to the HECM, local deferred program, and cash/family sections below.

HECM reverse mortgages for ADU construction

Answer capsule: A HECM is the FHA-insured reverse mortgage available exclusively to homeowners age 62 and older. The 2026 HECM maximum claim amount is $1,249,125, set by HUD effective . Per HUD Mortgagee Letter 2023-17 and the Single Family Housing Policy Handbook 4000.1, a single-family home with one ADU can qualify for a HECM provided the ADU is subordinate to the main home, complies with zoning requirements, and the borrower occupies the main unit.

Who qualifies

- Age: the homeowner must be 62 or older. If you have a spouse under 62, ask the HUD-approved counselor about eligible non-borrowing spouse protections.

- Primary residence: the home must be your primary residence and you must continue to occupy it.

- Mortgage status: the HECM must be in first-lien position. Existing mortgages typically must be paid off at closing using HECM proceeds.

- Property charges: you must demonstrate the ability to pay property taxes, homeowners insurance, and any HOA fees on an ongoing basis (residual-income test, not DTI).

- Property type: single-family homes, FHA-approved condos, 2–4 unit properties with borrower occupying one unit, manufactured homes meeting FHA minimum property standards, and — per HUD Mortgagee Letter 2023-17 — single-family properties with one ADU.

- Counseling: HUD requires every prospective HECM borrower to complete pre-loan counseling with a HUD-approved agency before applying. This is non-negotiable.

The 2026 HECM maximum claim amount

HUD raised the 2026 HECM maximum claim amount to $1,249,125, up from $1,209,750 in 2025, for FHA case numbers assigned on or after . This is the cap on the home value HUD will use to calculate your principal limit — homes appraised above $1,249,125 don’t yield additional HECM proceeds beyond what the cap supports. For high-value markets (parts of California, Washington, Hawaii, the New York City area, Massachusetts), this is a real constraint.

What HUD Mortgagee Letter 2023-17 means for ADU builders

- Single-family properties with an ADU can be eligible for HECM financing

- The ADU must be subordinate to the main home and comply with zoning requirements, including any legal nonconforming use status

- The borrower must occupy the main unit as their primary residence

- The appraiser reports the ADU separately, including its size, features, and whether it’s legally rentable

How accrued interest actually adds up

Interest doesn’t disappear because you don’t pay it monthly — it compounds against your equity. Compounding over a decade or more meaningfully reduces the equity available to heirs at sale or estate transfer. The headline structural trade is monthly cash flow for back-end equity reduction. Walk through a current amortization with a HUD-approved counselor using today’s rates and your actual draw plan before deciding.

HECM is best for

- Homeowners 62+ planning to stay 10+ years

- Multigenerational families housing aging parents via an ADU

- Homeowners on fixed income who can’t qualify for traditional financing

- Borrowers with heirs comfortable with the equity-reduction trade

HECM is a bad fit for

- Anyone planning to move within five to seven years

- Anyone with heirs who plan to keep the home without refinancing

- Borrowers unable to maintain property tax and insurance obligations

- Anyone uncomfortable with long-term equity-reduction math

Local deferred-payment ADU programs

Answer capsule: A small number of cities fund ADU construction through truly deferred loans where the homeowner makes no payment during the build or for years afterward, until a defined trigger event. The strongest 2026 example is Boston’s ADU Financial Assistance Program — up to $50,000 at 0% interest, deferred until sale, ownership transfer, or cash-out refinance. These programs are geographically narrow, but where you qualify they are the cheapest no-payment money on this page.

Boston ADU Financial Assistance Program

Boston’s program, administered by the Boston Home Center, offers up to $50,000 at 0% interest, deferred until sale of the home, ownership transfer, or cash-out refinance. Eligibility centers on income limits, owner occupancy, working with a licensed architect, and meeting Boston’s specific ADU rules. The deferred structure means no monthly payment ever, until one of the trigger events occurs.

For Boston homeowners with permitted plans and an income within the program’s bands, this is functionally the cheapest $50,000 in residential financing in 2026. The trade is the recorded lien on the property and the eventual repayment at the trigger event.

True deferred-payment programs are rare

The CalHFA ADU Grant Program, which previously offered up to $40,000 in pre-development reimbursement, has been fully allocated and paused since , per CalHFA’s official program bulletin. No relaunch date has been confirmed. Several California cities run smaller pilot programs at the local level — we maintain the current inventory on our verified ADU grants and incentives table.

See what’s possible at your address → Program eligibility usually depends on a specific ADU scope and location. Confirm your build is realistic before applying. (60 seconds, no commitment)

Get Your Free ADU ReportReduced-payment and hybrid public ADU financing alternatives

Answer capsule: Several municipal and state programs offer subsidized ADU financing that meaningfully reduces — but does not eliminate — the monthly burden. San Diego Housing Commission’s ADU Finance Program provides up to $250,000 at 1% interest during construction, converting to 4% fixed for 15 years with amortizing monthly payments. MassHousing’s ADU Loan Program offers up to $250,000 for detached ADUs or $150,000 for attached, structured as a hybrid of amortizing and zero-interest deferred financing. Portland, Oregon waives system development charges for qualifying ADUs. New York City’s Plus One program reopened in March 2026 offering up to $395,000 in combined financing. These are not no-monthly-payment paths, but in the right geography they may be the cheapest option you’ll find.

San Diego Housing Commission ADU Finance Program

The SDHC ADU Finance Program provides up to $250,000 structured as construction-to-permanent financing. The construction-phase loan is at 1% interest; the permanent loan after construction is at 4% fixed for 15 years with amortizing monthly payments.

Eligibility requirements:

- Owner-occupied detached single-family residence in the City of San Diego

- Income up to 150% of Area Median Income (AMI)

- Minimum 680 FICO

- Owner contribution of 1% of the construction loan amount

- $2,500 application fee at construction-loan closing

- A 7-year affordability covenant requiring the ADU to be rented to households at or below 80% AMI at affordable rents (30% or less of renter’s monthly household income)

- During the 7-year covenant period, the owner cannot rent the ADU to a family member

MassHousing ADU Loan Program (ADULP)

MassHousing offers up to $250,000 for detached ADUs or $150,000 for attached ADUs, structured as a combination of an amortizing interest-bearing loan and a zero-interest deferred component. This isn’t fully no-monthly-payment — there’s an amortizing piece. But the deferred component meaningfully reduces the monthly burden. If you’re in Massachusetts, this is worth a direct conversation with a MassHousing-approved lender before considering an HEI — especially given Hometap’s MA pause during ongoing AG litigation.

Portland ADU SDC Waiver Program

Portland’s ADU SDC Waiver Program waives system development charges — the upfront utility, transportation, and parks fees that can total tens of thousands of dollars — for qualifying ADUs. The waiver applies to ADUs that are owner-occupied or rented month-to-month or longer; short-term-rental ADUs are excluded. The waiver requires a binding 10-year agreement recorded against the property. Portland also has a separate temporary SDC exemption for newly created housing units issued from through under certain conditions.

New York City Plus One ADU Program

NYC’s Plus One program reopened in in partnership with Restored Homes HDFC, offering up to $395,000 in combined financing through NYC Housing Preservation and Development (HPD) and NY State Homes and Community Renewal (HCR) for qualified homeowners. Interest submissions were open through per the city’s published timeline.

For the current state-by-state inventory of active grant and incentive programs, see our verified ADU grants and incentives table, which we update monthly.

How do funds arrive during construction?

Answer capsule: HEIs and HEAs typically deliver one lump sum at closing. HECM proceeds can be structured as a lump sum, a line of credit drawn over time, or a tenure/term payment. Local construction-to-permanent loans use staged draws aligned to construction milestones. Cash and family contributions can be staged or lump-sum at the homeowner’s discretion. The mismatch between a lump-sum HEI and a milestone-billing builder is the single most common construction-phase financing complication.

| Funding mechanism | When funds arrive | Practical considerations |

|---|---|---|

| HEI / HEA (lump sum) | Single wire at closing | Park funds in a high-yield savings or short-duration treasury — never the operating checking account. Coordinate with your builder's payment schedule so funds are available at each draw request. |

| HECM line of credit | Available on demand as you draw | The remaining unused line grows at an annual growth rate per HUD's HECM formula. Draw progressively as the builder bills, not all at once. |

| HECM lump sum | Single advance at closing | Treat like a one-time draw on equity — same parking discipline as HEI proceeds. |

| Local construction-to-permanent (e.g., SDHC) | Staged draws aligned to construction milestones | Funds disburse only as inspections confirm progress. Matches the way builders bill, but may slow projects if inspections lag. |

| Cash / family contribution | Whatever schedule you and family agree | Document the schedule in writing — particularly for intrafamily contributions where vague timing creates disputes. |

The mismatch between a lump-sum HEI and a milestone-billing builder is the single most common construction-phase financing complication we see. The fix isn’t financial — it’s operational. Sit down with your builder before signing the HEI and agree on how funds will move from your account to theirs over the project timeline, in writing.

What if the ADU is not legal or permitted?

Answer capsule: No-monthly-payment financing does not solve a legal or zoning problem. HECM eligibility per HUD’s published guidance requires the ADU to comply with zoning, including any legal nonconforming use status. HEI providers underwrite to the property as it stands; an unpermitted ADU may not be credited as improvement value at settlement. Fannie Mae and Freddie Mac will not include rental income from an illegal ADU in qualifying calculations. If your ADU is unpermitted, the financing question is downstream of the legalization question.

The legalization path varies by city. Some jurisdictions offer amnesty pathways for unpermitted ADUs that meet current building codes — California, Oregon, and several California cities have explicit amnesty programs in 2026. Other jurisdictions require full code-compliant retrofit, which can run from $20,000 to well over $100,000 depending on the unit’s condition.

Order of operations if your ADU is unpermitted:

- Pull the property’s permit history through your county recorder

- Engage a designer or attorney experienced with your jurisdiction’s amnesty or legalization path

- Determine the cost to legalize before assuming the unit’s value will count

- Only then comparison-shop the financing

What we have to tell you about HEI regulatory risk in 2026

Answer capsule: Home equity investment products are under active regulatory scrutiny in 2026. On , Massachusetts AG Andrea Joy Campbell filed a complaint against Hometap alleging HEIs are illegal reverse mortgages; on , a Massachusetts judge denied Hometap’s motion to dismiss. In Olson v. Unison, the Ninth Circuit issued an unpublished memorandum in August 2025 concluding the specific Unison agreement at issue could be treated as a reverse mortgage under Washington law. The CFPB’s Issue Spotlight on home equity contracts flagged consumer confusion about HEI costs and disclosures. None of this means HEIs are illegal — but prospective HEI customers should read contracts carefully, run scenarios at multiple appreciation rates, and consult independent counsel before signing.

Massachusetts v. Hometap Equity Partners, LLC

On , Massachusetts Attorney General Andrea Joy Campbell filed a complaint against Hometap in Suffolk County Superior Court. The complaint alleges Hometap “pervasively and systematically violated the state’s consumer protection laws, including mortgage and foreclosure prevention laws.” Specifically, the AG’s complaint alleges Hometap’s HEI product functions as an unlawful reverse mortgage; includes a 10-year balloon payment that puts house-rich, cash-poor homeowners at risk; and markets to financially vulnerable homeowners without the disclosures Massachusetts requires for reverse mortgages.

Hometap responded that its product is an option contract rather than a loan. On , Suffolk County Superior Court Justice Debra Squires-Lee denied Hometap’s motion to dismiss, finding the products could plausibly be considered loans and that the legal questions should be tested in court. The case continues. Hometap is no longer originating new HEIs in Massachusetts during the proceedings.

Olson v. Unison Agreement Corp.

A private plaintiff suit against Unison in Washington state resulted in an unpublished Ninth Circuit Court of Appeals memorandum in August 2025 concluding that the specific Unison agreement at issue could be treated as a reverse mortgage under Washington law. The memorandum was designated “not for publication” and “not precedent” except as provided by Ninth Circuit Rule 36-3. The case subsequently settled, the appeal was voluntarily dismissed, and the procedural disposition of the underlying opinion is described differently across public sources. The practical takeaway: the ruling is not broadly controlling law, but it does demonstrate judicial willingness to characterize an HEI as a reverse mortgage in a specific factual context.

CFPB Issue Spotlight on Home Equity Contracts (January 2025)

The Consumer Financial Protection Bureau’s Office of Mortgage Markets published an Issue Spotlight reviewing the home equity contracts market. The published findings noted that the four largest HEI companies inked deals totaling approximately $1.1 billion in the first 10 months of 2024, that complex terms and nonstandard disclosures cause consumer confusion about true costs and risks, and that effective costs of HEIs can exceed those of traditional home-secured credit under common scenarios.

What this means for you, practically

- Read your specific contract. The contract — not the marketing page — controls. Ask for the contract before you commit to an appraisal so you can review the actual terms.

- Run scenarios at multiple appreciation rates. Ask the provider for their published scenario table covering 0%, 3%, 5%, and 8% annual appreciation, including the ADU-improvement contribution.

- If you’re 60 or older and live in Massachusetts, the HECM is your no-payment path right now. Hometap is not originating; Unison’s product was challenged in Olson. Use the HECM’s Massachusetts reverse-mortgage protections.

- Have an attorney review the agreement before signing. Not a real estate agent. Not the provider’s “investment manager.” A real estate or consumer protection attorney whose only role is your interest.

- Don’t take this as a verdict. The Mass case has not been decided on the merits. Hometap, Unlock, and Point all maintain their products are legitimate. The point of this section is informed consent — not a recommendation to avoid the category.

What can go wrong with no-monthly-payment ADU financing

Answer capsule: The risks are not monthly cash-flow risks — they are exit risks. The most common failure patterns are a settlement amount larger than expected due to home appreciation, an appraisal dispute at settlement, ADU-created value being included in the provider’s share, local program covenants becoming inconvenient, HECM balance growth reducing estate equity beyond what the family expected, and construction overruns that consume the funded amount before the project is complete.

1. The settlement is bigger than expected. A homeowner signs a $200,000 HEI when their home is worth $800,000. Ten years later, the market has been kind — the home is worth $1.4 million, and the new ADU added $250,000 of that. The provider's contract gives them a percentage of the final value. The amount owed at settlement is well above what the owner mentally modeled. This isn't a violation of the contract — it's exactly how the contract works. The owner didn't run the upside scenarios before signing.

2. The appraisal at settlement is disputed. The settlement appraisal becomes a fight. The provider's appraiser comes in materially lower than the owner's. Most HEI contracts include dispute-resolution procedures, but those procedures often favor the party with the more conservative appraisal. Owners who didn't document the ADU improvement value during construction often lose this fight.

3. The ADU-created value gets pulled in. This is the failure this guide is built around. Check the contract before signing — not after.

4. The local program covenant becomes inconvenient. A San Diego homeowner who took SDHC funding now needs to relocate for a job five years in. The 7-year affordability covenant requires the unit to remain rent-restricted; the homeowner can sell or move, but the buyer inherits the covenant. The property is harder to sell at full value during the covenant period.

5. The HECM balance compounds further than the family modeled. A 67-year-old draws $300,000 from a HECM to fund an ADU. They live in the home until age 92. The compounded balance at sale by the estate is much larger than the original draw. The home is worth more, too, but the remaining equity to heirs is meaningfully less than the heirs expected because they didn't model the compounding.

6. Construction goes over budget and consumes the funded amount. A homeowner draws $200,000 from an HEI. The project quoted at $250,000 finishes at $340,000 because of utility upgrades, site work, and finishes. The homeowner now needs another $90,000 mid-build. The HEI funded a lump sum 12 months ago and can't be redrawn. The homeowner takes a HELOC at today's rates — and now they have both products on the home.

Our damaging admission: No-monthly-payment financing can be the more expensive choice. If you can comfortably carry a traditional payment and your ADU is likely to add meaningful value, an equity-sharing or reverse-mortgage agreement may trade short-term cash-flow relief for long-term upside you would otherwise keep. That doesn’t mean these products are wrong — it means cash flow has to be the binding constraint for them to be the right answer. If, after reading this, you decide a payment-bearing path is the better trade: that’s an honest conclusion.

Can you carry a monthly payment?

For homeowners who can carry a payment, mortgage-backed options may preserve more of the value the new ADU creates.

Compare HELOC, home equity loan, cash-out refi, and construction loan options →via Mortgage Research Center, an active Dwelling Index partner

How to build an exit plan before signing

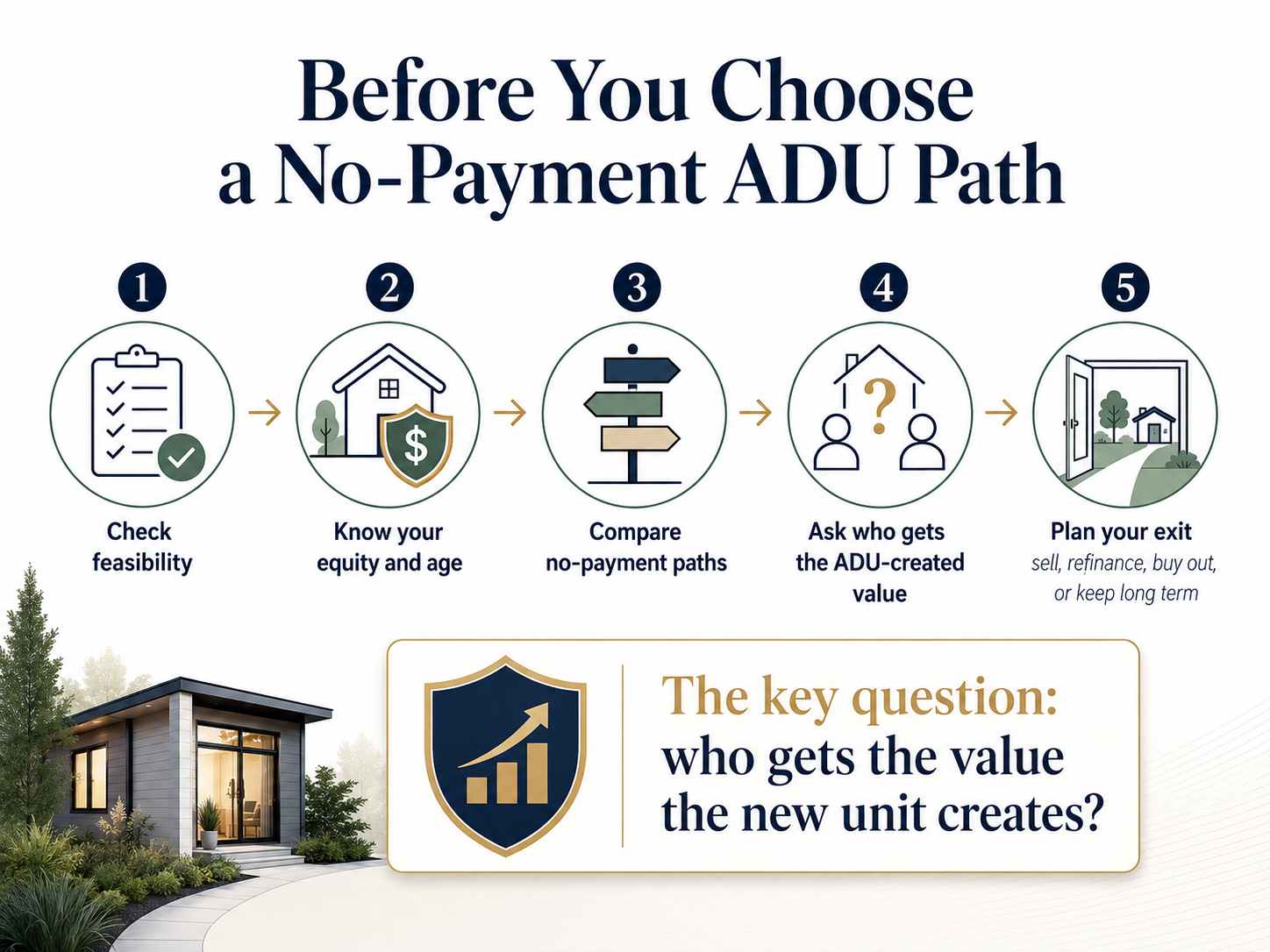

Answer capsule: Before signing any no-monthly-payment financing agreement, the homeowner should have a specific exit plan: how the agreement will end, what event will trigger settlement, and what funding source will cover the settlement amount. Common exit paths include sale of the home, cash buyout, refinance into a payment-bearing loan, family buyout, and — for HECM — estate sale or refinance. A vague exit plan is the single most common reason these agreements produce regret.

Exit Plan Checklist

| Question | Why it matters |

|---|---|

| What exact event will trigger repayment? | HEIs typically require settlement at sale, refinance, or end of term. HECMs become due at borrower death, move-out, or sale. Local deferred loans typically trigger at sale, transfer, or cash-out refinance. Confirm the exact triggers in your contract. |

| Can I buy out the agreement early without penalty? | Most HEI providers say yes. Confirm in your specific contract. Buyout cost is calculated at then-current appraised value. |

| How is the settlement value determined? | Third-party appraisal in most cases. Confirm appraisal method, dispute procedures, and who pays the appraisal cost. |

| Does the provider share in ADU-created value? | The central ADU-specific question. Get this in writing before signing. |

| What documents do I need to keep to prove improvement value? | Permits, contractor invoices, before-and-after appraisals, plans, completion certificates. Start keeping these the day construction begins. |

| What happens if the home value falls? | Most major HEI providers share in downside risk to some extent. Confirm the specific formula. |

| Can I refinance into a payment-bearing loan to settle the HEI? | Yes, in most cases. The refinance happens at then-current rates and your then-current equity. |

| What happens if I rent the ADU short-term? | Some contracts restrict commercial or short-term use. Check your specific terms. |

| What happens if I transfer the home to a trust or heirs? | Both HEI and HECM contracts have transfer provisions. Estate planning matters. |

| Who reviews the contract before I sign? | Not the provider. Not your real estate agent. An attorney whose only role is your interest. |

The four legitimate exit paths for HEIs

- Sale of the home — the most common and cleanest exit. Settlement comes out of sale proceeds at closing.

- Refinance into a payment-bearing loan — works if your then-current equity and DTI support the refinance amount including the HEI buyout.

- Cash buyout from accumulated savings — rare but possible if you’ve meaningfully built liquid assets during the term.

- Partial buyout (Unlock only, currently) — Unlock allows partial buybacks during the 10-year term, letting homeowners chip away at the obligation as cash becomes available. Other major providers do not currently offer partial buybacks.

See what’s possible at your address → A financing exit plan only works if the ADU itself produces what you expected. We recommend running the feasibility check first. (60 seconds, no commitment)

Get Your Free ADU ReportIs no-monthly-payment ADU financing actually cheaper than a HELOC?

Answer capsule: Not always. No-monthly-payment financing protects cash flow but can cost more over a 10–30-year holding period than a HELOC or home equity loan if the home and the new ADU appreciate meaningfully. The CFPB’s January 2025 Issue Spotlight on home equity contracts noted that HEIs can be more expensive than traditional home-secured credit under common scenarios. For homeowners who can carry a monthly payment, a HELOC may preserve more of the long-term upside the ADU itself creates.

| Option | Monthly payment | Cost trajectory | Keeps ADU-created value? | Better when |

|---|---|---|---|---|

| HEI / HEA | None | Variable; back-loaded as a balloon. Effective IRR can range from single digits to 20%+ depending on appreciation | Provider-dependent — see ADU-created-value section | Cash flow is the binding constraint |

| HELOC | Yes (variable, interest-only during draw period) | Predictable; capped by the rate and draw amount | Yes — homeowner keeps 100% | You can carry the payment and want to preserve appreciation upside |

| Home equity loan | Yes (fixed) | Predictable; capped | Yes — homeowner keeps 100% | You want payment certainty |

| Cash-out refinance | Yes (replaces first mortgage) | Predictable but may replace a low first-lien rate | Yes — homeowner keeps 100% | Current first-mortgage rate is close to today's rates |

| Renovation / future-value loan (FHA 203(k), Fannie HomeStyle, etc.) | Yes | Predictable; complex underwriting | Yes | Current equity is insufficient and after-improvement value supports the loan |

| HECM reverse mortgage | No required mortgage payment | Compound interest against equity over time | No investor share, but equity reduces | Age 62+, long-term hold, comfortable with estate impact |

Illustrative example — model assumptions

| Equity available | $400,000 in a $900,000 California home |

| ADU build cost | $300,000 |

| Path A: HEI investment | $150,000 |

| Path B: HELOC drawn | $150,000 |

| Path B: HELOC rate (assumed) | 7%, interest-only during 10-year draw period |

| Path B: Monthly payment | ~$875/month (interest-only) |

| Path B: Total interest over 10 years | ~$105,000 (assumes no draws repaid until end of period; fees excluded) |

| Path A: Settlement amount at 10-year exit | Variable; range commonly $300,000–$400,000 depending on appreciation and contract terms |

Illustrative only. Not a quote or offer. Actual outcomes depend on specific provider terms, fees, appraisal results, and market conditions.

The structural takeaway: the HELOC costs less in scenarios where the home appreciates strongly because the homeowner keeps all of that upside. The HEI costs less in scenarios where appreciation is flat or modest. If you can carry the payment, the comparison is worth running honestly.

Can you carry a monthly payment?

If yes, comparing payment-bearing options may preserve more of the value your new ADU creates.

Compare HELOC, home equity loan, cash-out refi, and construction loan options →via Mortgage Research Center, an active Dwelling Index partner

Cash, family contribution, and hybrid strategies

Answer capsule: The cleanest no-monthly-payment ADU financing in many situations is cash, family contribution, or a hybrid. For calendar year 2026, the IRS annual gift exclusion is $19,000 per donor per recipient per IRS Revenue Procedure 2025-32; gifts above that amount don’t necessarily trigger tax but do require Form 709 reporting and reduce the donor’s lifetime gift/estate exemption. Below-market intrafamily loans must be structured at or above the IRS Applicable Federal Rate (AFR) to avoid imputed interest treatment. Cash and family contributions preserve 100% of the value the new ADU creates.

We don’t list cash and family contribution as a serious option because it’s obvious. We list it because the math frequently beats every financed alternative and homeowners overlook it.

The three intrafamily structures, compared

| Structure | What it is | Tax treatment | Best when |

|---|---|---|---|

| Pure gift | Family member transfers funds with no expectation of repayment | Donor uses annual exclusion ($19,000 per recipient in 2026); excess is reported on Form 709 and applied against lifetime gift/estate exemption | Family member can afford the contribution and estate planning supports the transfer |

| Below-market loan at AFR | Documented promissory note at or above the IRS Applicable Federal Rate, with a real repayment schedule | Treated as a legitimate loan; lender reports received interest as income | Family member wants the money repaid eventually but isn’t trying to charge market rates |

| Hybrid: parent funds ADU and lives in it | Parent contributes funds; documented occupancy agreement governs use | Contribution may be structured as combination of gift and improvement value retained by the property owner | Aging parent needs housing and wants to be near family; property owner has the lot but not the capital |

Cash as a path: If you have $250,000–$400,000 in non-retirement liquid assets sitting in cash or low-yield instruments, deploying that capital to build an ADU may produce a better long-term return than the alternatives, even after accounting for opportunity cost. These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

The single most common reason intrafamily ADU financing falls apart is documentation. Make the loan formal. Use an attorney. Record the note. Pay or receive interest at AFR or above. Sign a written occupancy agreement if a family member will live in the unit.

This is not legal or tax advice. Property tax reassessment rules vary by state. Consult an estate attorney and CPA before structuring any of this.

What if no HEI provider is available in your state?

Answer capsule: If no HEI/HEA provider currently operates in your state and you’re under 62 and outside a city with a deferred-payment ADU program, your no-monthly-payment options narrow significantly. The realistic next steps are checking HECM eligibility, exploring family contribution or below-market intrafamily loans, phasing the ADU project to match available capital, reducing the ADU scope, or accepting that a payment-bearing financing path is the right answer for your situation.

As of May 2026, several Plains, Mountain West, parts of New England, and several Midwest states have limited or no HEI options. If you’re in one of these areas, here’s the decision tree to walk through:

Is the homeowner 62 or older? If yes, the HECM is your path. It's federally insured, available nationwide through HUD-approved lenders, and explicitly permits a single-family home with one ADU to qualify under HUD Mortgagee Letter 2023-17.

Are you in a city with a deferred-payment or subsidized ADU program? Boston (true deferred), San Diego (SDHC reduced-payment), Massachusetts (MassHousing hybrid), Portland (SDC waiver), and New York City (Plus One) are the strongest 2026 examples. Check your city's housing department page directly.

Is there a willing family contribution or intrafamily loan path? An aging parent funding an ADU on a child's property in exchange for occupancy is one of the more common real-world ADU financing structures — and the cleanest financially.

Can you phase the project? A garage conversion done first and a detached unit added later when equity and finances allow is a legitimate strategy. See our ADU cost guide for current cost ranges by ADU type and region.

Can you reduce scope to match cash on hand? A smaller prefab or modular ADU may bring total project cost below the threshold that requires major financing. See our prefab ADU options for current model pricing.

Accept that a payment-bearing path may be the right answer. A HELOC at today's rates, paired with strong ADU rental income, may produce a better lifetime outcome than no project at all.

Compare HELOC, home equity loan, and construction loan options

via Mortgage Research Center, an active Dwelling Index partner

Explore mortgage-backed ADU financing options →Should retirees or families building for aging parents use no-payment financing?

Answer capsule: No-monthly-payment ADU financing is especially relevant for retirees and families building for aging parents because it preserves the household’s monthly cash flow — typically the most fragile element of post-retirement finance. The most common structures are a HECM for owners 62 or older planning to age in place, a parent-funded ADU on an adult child’s property using gift or below-market loan structures, or a hybrid combining family contribution and a smaller HEI or HECM line of credit. Each structure has meaningful estate, tax, and family-dynamic implications that warrant attorney and tax-advisor review before signing.

| Structure | Age requirement | Monthly payment | Investor share of ADU value? | Estate impact | Key consideration |

|---|---|---|---|---|---|

| HECM reverse mortgage | 62+ | None required; taxes, insurance, occupancy remain | None | Loan balance reduces estate equity | HUD-approved counseling required; eligible non-borrowing spouse rules apply |

| HEI on retiree-owned home | None (must be HEI-eligible state) | None | Provider-dependent; check contract for ADU-created-value treatment | Balloon at sale, refinance, or end of term reduces estate proceeds | Subject to state regulatory landscape covered above |

| Parent gift to adult child's property | None | None | None | Reduces parent's lifetime gift/estate exemption above annual exclusion | $19,000 annual gift exclusion per donor per recipient for 2026; Form 709 reporting above that |

| AFR intrafamily loan | None | None required (loan is between family members) | None | Loan principal returns to lender (or estate) at repayment | Must be at or above current AFR to avoid imputed-interest treatment; documented promissory note required |

The honest tradeoffs

- HECM reduces what heirs inherit. This is a feature for some families and a non-starter for others. Discuss before signing.

- Aging-in-place ADUs may not be designed to generate rental income. If the ADU is single-occupant, ADA-adapted, and located for proximity rather than privacy, it may not be readily rentable after the parent’s lifetime. Plan for both phases.

- Intrafamily contributions need estate-planning structure. Without documentation, what looks like a clean family gift can become a probate dispute, a step-up basis problem, or a Medicaid look-back issue.

- California Proposition 19 and equivalent provisions in other states change how property tax treatment carries across parent-to-child transfers. Get this right before construction.

This is not legal, tax, or estate planning advice. Consult qualified professionals before structuring any of the arrangements described.

What we verified for this guide

We re-verify provider availability and terms quarterly. We re-verify HUD limits annually each December/January. We re-verify state and municipal program status quarterly. If you spot something on this page that contradicts a primary source today, please contact our editorial team.

| Item | Source type | Last verified |

|---|---|---|

| Hometap maximum investment ($600K), 10-year term, no-monthly-payment language, 16-state list, 575 FICO minimum | hometap.com (provider site) | |

| Hometap Massachusetts status and AG litigation | mass.gov AG press release; Suffolk County Superior Court filings | |

| Point maximum investment ($600K), 30-year term, state list, remodel-appreciation treatment | point.com and help.point.com | |

| Unlock $500K cap, 10-year term, partial-buyout feature, 500 FICO minimum, state list, no monthly payments | unlock.com | |

| Unison 15% of home value cap; Olson v. Unison unpublished memorandum (August 2025), Ninth Circuit Rule 36-3 designation, subsequent settlement and dismissal | unison.com; Justia Law; HousingWire; CHEP | |

| HECM 2026 maximum claim amount ($1,249,125) | HUD news release HUD-No-25-145 (December 2025) | |

| HECM age requirement (62 and older); property charges; counseling | CFPB consumer guidance | |

| HUD Mortgagee Letter 2023-17: ADU property eligibility for FHA Title II Forward and HECM programs | HUD published Mortgagee Letter | |

| Boston ADU Financial Assistance Program ($50K, 0%, deferred until sale, transfer, or cash-out refinance) | boston.gov | |

| MassHousing ADU Loan Program ($250K detached / $150K attached; amortizing + zero-interest deferred hybrid) | masshousing.com | |

| SDHC ADU Finance Program (up to $250K, 1% construction / 4% fixed 15-year permanent, 680 FICO, 150% AMI, 7-year affordability covenant, family-rental restriction during covenant) | sdhc.org | |

| Portland ADU SDC Waiver Program (owner-occupancy or month-to-month rental, STR excluded, 10-year recorded agreement); temporary SDC exemption (Aug 15, 2025 – Sep 30, 2028) | portland.gov | |

| NYC Plus One ADU Program reopened March 2026; up to $395,000 combined through HPD and NYS HCR; interest submissions through June 12, 2026 | nyc.gov (HPD news release) | |

| CalHFA ADU Grant Program paused / fully allocated December 2023 | CalHFA Program Bulletin | |

| CFPB Issue Spotlight: Home Equity Contracts: Market Overview (January 2025) | consumerfinance.gov | |

| IRS 2026 annual gift exclusion ($19,000 per donor per recipient) | IRS Revenue Procedure 2025-32 | |

| Fannie Mae ADU rental income (existing ADU on one-unit principal residence, capped at 30% of total qualifying income) | Fannie Mae Selling Guide B3-3.8-01 | |

| Freddie Mac ADU fact sheet (qualifying rental income capped at 30% of total qualifying income; illegal ADU income excluded) | Freddie Mac ADU fact sheet (February 2026) |

Methodology

This guide was researched by reading primary sources — provider websites, HUD published handbooks and mortgagee letters, the CFPB Issue Spotlight on home equity contracts, IRS revenue procedures, official municipal program pages, and court filings in active HEI litigation — and organizing the findings around the ADU-specific question most generic financing pages miss: who keeps the value the new unit creates? Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, financial advisor, contractor, or law firm.

Our source hierarchy, in order of authority:

- Official provider terms, help-center pages, and rate sheets

- HUD, CFPB, IRS, and other federal regulatory sources

- State and municipal program pages

- Court filings in active litigation

- Editorial coverage in established trade and consumer publications

- Voice-of-customer language from forums and reviews — used only to understand reader concerns, never as proof of financial or regulatory facts

Neutral sorting and presentation:

We do not rank lenders by payout. Comparison tables in this guide are organized by neutral documented criteria — path type, provider, published terms, state availability, and ADU-specific relevance. We do not call any provider “best” without an explicit editorial-judgment label naming the criteria we used.

Partner disclosure:

We do not currently have an affiliate relationship with any home equity investment company discussed on this page. Our active financing partner is Mortgage Research Center, which we cite in the sections on payment-bearing alternatives. We have pending partnerships with several HEI providers; until tracking is active, our links to those providers take you directly to their sites and we earn nothing on the click.

This guide is for educational purposes only. Dwelling Index is not a lender, mortgage broker, financial advisor, tax advisor, law firm, or contractor. Financing terms, eligibility, fees, and availability vary by provider, property, borrower, state, and underwriting. Provider availability and terms can change. Always review official documents and consult qualified professionals before using home equity to fund construction. Rental income examples are illustrative only — these are not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Frequently asked questions

Can you finance an ADU without monthly payments?

Yes. The realistic 2026 paths are a home equity investment or home equity agreement from a provider like Hometap, Point, or Unlock; a HECM reverse mortgage if the homeowner is 62 or older; a local deferred-payment ADU program where available (Boston's program is the strongest 2026 example); or cash and family contributions. Each path swaps the monthly payment for a different cost.

Is a home equity investment the same as a loan?

HEI providers market the product as an investment or option contract rather than a loan, but the practical effect is similar to a non-amortizing loan with a balloon payment at the end. State regulators are actively contesting the loan-vs-investment distinction. Massachusetts AG Andrea Joy Campbell's February 2025 complaint against Hometap argues HEIs are illegal reverse mortgages; the Ninth Circuit's unpublished Olson v. Unison memorandum concluded the specific Unison agreement at issue could be treated as a reverse mortgage under Washington law. Treat HEIs as major home-equity obligations regardless of how they're labeled.

Can I use a reverse mortgage to build an ADU?

Yes, if the homeowner is 62 or older, the home is the primary residence, and HUD-approved counseling is completed. HUD Mortgagee Letter 2023-17 and the Single Family Housing Policy Handbook 4000.1 permit a single-family home with one subordinate, zoning-compliant ADU to qualify for a HECM. The 2026 HECM maximum claim amount is $1,249,125 for FHA case numbers assigned on or after January 1, 2026.

Which HEI providers serve my state?

State availability varies by provider and changes quarterly. As of May 2026, Hometap publishes availability in 16 states (Arizona, California, Florida, Indiana, Michigan, Minnesota, Missouri, Nevada, New Jersey, New York, Ohio, Oregon, Pennsylvania, South Carolina, Utah, and Virginia) and is not currently originating in Massachusetts. Point publishes approximately 25–28 states plus DC. Unlock publishes approximately 25 states. Always verify directly with each provider before applying.

What happens to the value the ADU itself creates?

This is the most important ADU-specific question. Some providers' contracts include improvement-created appreciation in the appreciation share used to calculate settlement — Point's published help center explicitly states that remodel-created appreciation is part of the overall appreciation shared. Others publish improvement-adjustment language that may credit the homeowner. Get the specific contract language in writing before signing.

Is a HELOC better than an HEI for an ADU?

A HELOC may produce a better long-term outcome on a strongly-appreciating property because the homeowner keeps 100% of the new ADU's appreciation contribution. An HEI may produce a better outcome if the homeowner can't carry the monthly payment, the home appreciates modestly, or the holding period is short enough that fees dominate. Run both options through your actual scenario, not the headline rate.

What's the catch with home equity investments?

The cash arrives with no monthly payment, but the cost is a share of your home's future value at settlement, typically 10–30 years out. Effective annualized costs can range from single digits to over 20% depending on appreciation. Origination fees of 3.0%–4.9% are typical. State availability is limited. Litigation in Massachusetts and elsewhere is currently contesting how these contracts should be regulated.

Can I get an ADU loan with no income verification?

HEIs typically do not require income, DTI, or employment documentation — they're underwritten on the property. HECM reverse mortgages have a financial-assessment requirement to confirm the borrower can pay taxes and insurance, but this is a residual-income test, not a traditional DTI test. Local deferred-payment programs typically have income limits as part of eligibility.

Are there ADU grants available with no monthly payments?

A grant is free money — it's not financing — and the available grant programs are narrow and frequently fully allocated. California's CalHFA ADU Grant Program ($40,000) has been fully allocated and paused since December 28, 2023. New York City's Plus One program reopened in March 2026 with up to $395,000 in combined HPD/HCR financing. Boston, Vermont, Juneau, and a handful of California cities have local programs. See our verified ADU grants and incentives table for the current inventory.

Can ADU rental income help me refinance later?

Possibly, with caps. Fannie Mae's Selling Guide allows rental income from an existing ADU on a one-unit principal residence to be used for qualifying in limited cases, capped at 30% of total qualifying income. Freddie Mac's February 2026 ADU fact sheet caps qualifying rental income from an ADU on a subject one-unit primary residence at 30% of total qualifying income; rental income from an illegal ADU may not be used. The ADU must be legally permitted to count.

Can I rent the ADU to a family member if I use SDHC financing?

No, not during the 7-year affordability covenant. The San Diego Housing Commission ADU Finance Program's published terms prohibit renting the ADU to a family member during the seven-year covenant period and require the unit to be rented to a non-family household earning 80% AMI or less at affordable rents. If family-rental is part of your plan, SDHC isn't your path.

Will the CalHFA ADU Grant come back?

The latest funding round was fully allocated as of December 28, 2023. CalHFA has not announced a confirmed relaunch date as of May 19, 2026, though legislative interest in re-funding the program exists. Treat any future CalHFA funding as a bonus to your plan, not a cornerstone. For verified currently-active grants, see our state-by-state grants table.

Get the free ADU Starter Kit

Before you talk to a single lender, builder, or contractor, the Dwelling Index ADU Starter Kit walks you through the cost, financing, and permit-timeline questions in plain language. It’s free.

Download the Free ADU Starter KitFinal take

The honest answer to “ADU financing without monthly payments” is that the category exists, the paths are real, and the products work — but the question every homeowner needs to answer before signing is not “can I get a loan with no monthly payment?” It’s “which path costs me the least over the time I’ll hold this property, and who ends up with the value my new ADU actually creates?”

For homeowners 62 and older, the HECM is usually the cleanest answer. For equity-rich homeowners under 62 in states with active HEI providers, an HEI may fit — provided the contract treats ADU-improvement value fairly and you can model your exit honestly. For homeowners in Boston, the deferred-payment program may beat every private alternative. For homeowners in San Diego, Massachusetts, Portland, or New York City, a reduced-payment or hybrid program may be the strongest option. For everyone else, cash, family contribution, or accepting a payment-bearing path may be the right answer.

If you’ve worked through this guide carefully and you’re still not sure which path fits your situation, that’s the moment to use the feasibility check below — because a financing path is only useful if the ADU itself is feasible.

Not sure where to start?

See what’s possible at your address — get your free ADU report in 60 seconds.

Get Your Free ADU Report →