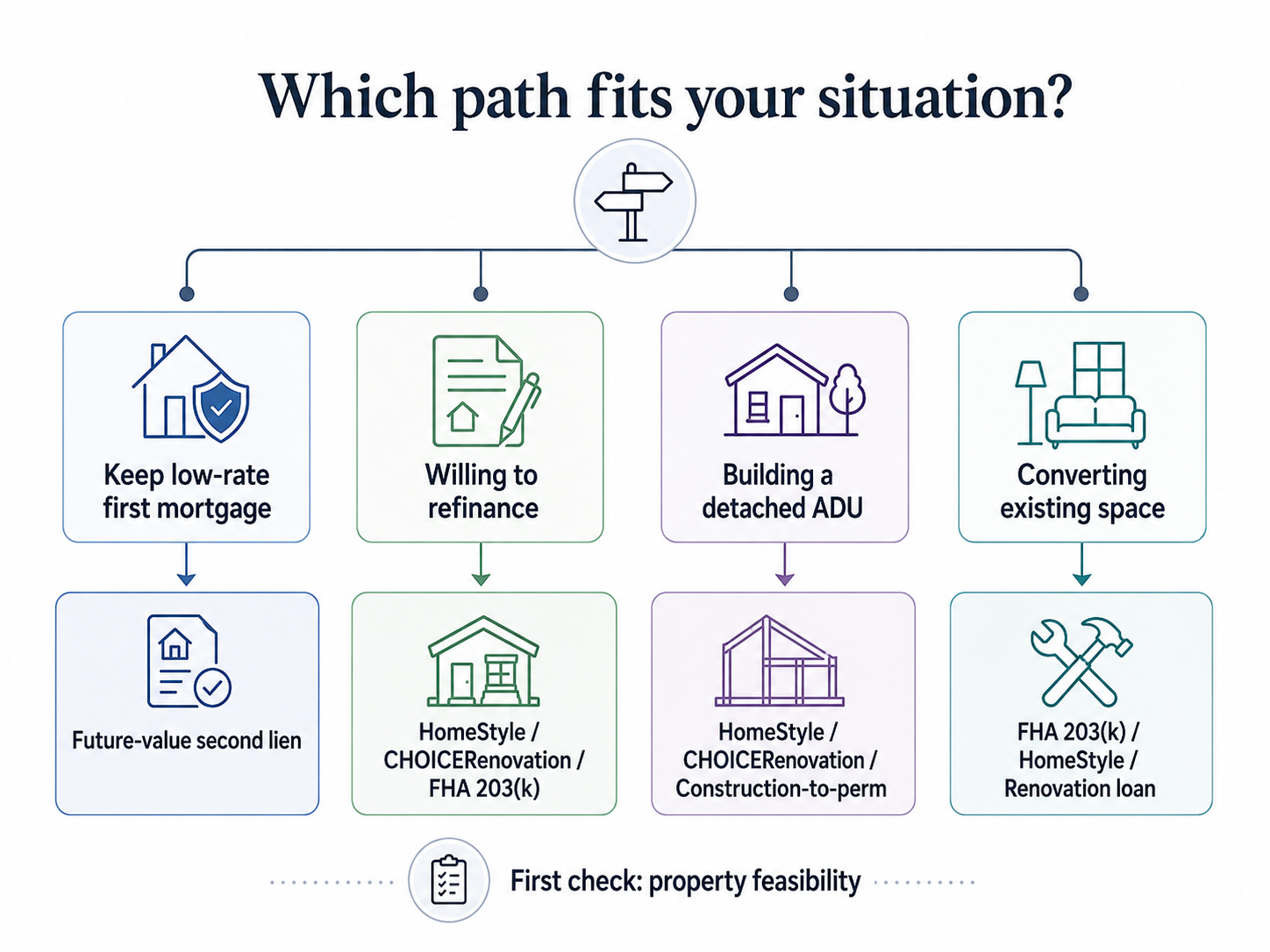

If you have no equity, check this first

This table is your fast triage. The rest of the page explains the why behind each row and the math you’ll need before you call a lender.

| Your situation | First path to test | Why |

|---|---|---|

| You have a low-rate first mortgage and don't want to refinance | After-renovation-value second-lien loan (renovation HELOC) | May preserve your low rate while underwriting against future value |

| You're willing to refinance, or you're buying the home | Fannie HomeStyle, Freddie CHOICERenovation, FHA 203(k), or construction-to-permanent | These underwrite against as-completed value |

| You're building a new detached ADU from the ground up | HomeStyle, CHOICERenovation, or construction-to-permanent | FHA 203(k) is best for attached additions or rehab of an existing ADU |

| You're converting a garage, basement, or interior space | FHA 203(k), HomeStyle, CHOICERenovation, or a renovation loan | Conversions are usually easier to underwrite than ground-up detached builds |

| You want no required monthly payment | Home Equity Investment (HEI) — but read the section below first | HEIs require equity; they're not a no-equity product |

| You don't know if your lot can legally support an ADU | Run a feasibility check first | No loan fixes a property that won't pass zoning, setbacks, or utilities |

Can you finance an ADU with no equity? Yes — but “no equity” usually means three different things

Answer capsule

Yes, you can finance an ADU without traditional home equity if the loan uses the property’s after-renovation or as-completed value, or if you qualify through a program that bypasses equity. The path that fits depends on which of three problems you actually have: not enough current tappable equity, an unwillingness to refinance a low-rate first mortgage, or a need for financing without monthly payments.

When homeowners say they have “no equity,” they almost always mean one of these three things — and each one has a different solution.

Not enough current tappable equity

The most common case. You bought your home in the past 1–5 years, your loan-to-value (LTV) is already 90%+, and a standard Home Equity Line of Credit (HELOC) — which underwrites against your current home value — has nothing to lend you. Per Urban Institute analysis presented to the California Assembly, conventional home equity products typically cap at 80% of current market value and “don’t consider future rental income the ADU will generate.” For a recent homebuyer with 3% equity on a $600,000 home, a standard HELOC has $0 of borrowing capacity. Your fix: future-value loans — renovation mortgages, ARV second liens, construction-to-permanent loans.

You have equity, but you don’t want to lose your low first mortgage

A significant share of U.S. mortgages were originated when rates were near historic lows. Refinancing into today’s rates to fund an ADU can erase the financial benefit of building the ADU at all. If that’s you, you don’t have a “no-equity” problem — you have a “preserve-my-first-mortgage” problem. Your fix: second-lien products that sit behind your existing mortgage. The most relevant category is the after-renovation-value home-equity loan offered through specialty lenders that operate as brokers connecting borrowers to credit-union partners.

You want financing without monthly payments

This isn’t a no-equity problem — it’s a cash-flow problem. Companies like Hometap, Unlock, and Point offer Home Equity Investments (HEIs): lump-sum cash today in exchange for a share of your home’s future appreciation, with no monthly payments. But HEIs require meaningful existing equity to qualify — Hometap publicly states a minimum of 25% equity, and Point requires “sufficient” equity plus a 500+ credit score. We cover HEIs honestly in their own section below.

Naming the problem correctly is the first work of this page.

Most homeowners think they have Problem 1 when they really have Problem 2 — or vice versa. The financing paths that solve each are different.

Run the feasibility check first — before any lender conversation

See What You Can Build → Get Your Free ADU Report

Check your property before you spend time comparing loan options. About 60 seconds. No phone call.

See What You Can BuildHow much equity do you need to finance an ADU?

Answer capsule

None — if you use a loan that underwrites against your home’s future or as-completed value. For products that use current value (standard HELOCs, conventional cash-out refinance), you typically need at least 15–20% existing equity above your mortgage balance. The distinction between current-value and future-value lending is the entire reason this page exists.

| Loan type | Equity required (typical) |

|---|---|

| Standard HELOC, conventional home equity loan, conventional cash-out refinance | Enough to keep Combined LTV (CLTV) at or under the lender’s ceiling — typically 80–90%. For most homeowners, this means at least 15–20% existing equity. |

| Renovation HELOC / ARV second-lien, Fannie HomeStyle, Freddie CHOICERenovation, FHA 203(k), construction-to-permanent | No traditional equity required. The lender underwrites against the home’s as-completed value with the ADU built. |

If your equity math doesn’t work today, that doesn’t mean your project is dead. It means you’re shopping a different category of loan. The next section walks through the math.

Why a standard HELOC usually fails for an ADU — and the simple math behind it

Answer capsule

A standard HELOC underwrites against your home’s current value minus your current mortgage balance, capped at a Combined Loan-to-Value (CLTV) ceiling that’s typically 80–90%. If your existing mortgage already uses most of that ceiling, the available HELOC room is too small to cover an ADU. The fix isn’t a different lender — it’s a different product category that values your home at what it will be worth after the ADU is built.

Run the math before you make a single phone call.

The HELOC formula

A typical recent-homebuyer profile:

- •Home value: $600,000

- •Lender's max CLTV: 80%

- •Existing mortgage balance: $580,000

- •Math: $600,000 × 0.80 = $480,000 − $580,000 = −$100,000

Borrowing room from a standard HELOC: $0

The first-mortgage balance has already exceeded what the lender will allow at 80% CLTV. Even a more generous 90% CLTV ($540,000 ceiling) gives this homeowner $0 of HELOC capacity once the existing mortgage is netted out. That’s the entire reason “no-equity ADU financing” is a real category.

When a standard HELOC does work

You have substantial existing equity (CLTV after the new draw stays under 80%), the ADU budget is modest, you want to preserve a low-rate first mortgage, and the monthly payment is comfortable. Garage conversions and basement ADUs in the $60,000–$150,000 range are the most common fit. Per Angi’s 2026 ADU cost data, basement and garage conversions average $60,000–$150,000 nationally — a budget a HELOC may cover for an equity-rich homeowner.

For a deeper look at HELOC mechanics for ADUs, see our HELOC for ADU guide or the full ADU Financing Options Guide.

When to stop forcing a HELOC

Your CLTV math returns under your project budget. You bought in the last 1–5 years. Your first mortgage balance is high relative to value. Your home’s current appraisal won’t support the size of HELOC you need. Any of those, and you’re looking at a future-value path instead.

The No-Equity ADU Financing Decision Matrix (2026)

Answer capsule

Seven financing paths can fund an ADU without traditional home equity. Each has a different borrowing basis, a different rental-income rule, and a different best-fit homeowner. This matrix is the master tool for narrowing your options to one or two before you call a lender.

Which path fits depends on whether you want to preserve your first mortgage, your ADU type, and your state.

| Path | Borrowing basis | Approx. max | ADU rental income for qualifying? | Min. credit |

|---|---|---|---|---|

| Fannie Mae HomeStyle Renovation | As-completed appraised value (up to 97% LTV on purchase); renovation costs capped at 75% of as-completed value | 2026 conforming limit: $832,750 single-family; $1,249,125 high-cost | Yes, with conditions; ADU rental income capped at 30% of total qualifying income per SEL-2025-08 | Lender-set; DU casefiles no agency floor as of Nov 16, 2025; manually underwritten: 620 (fixed) / 640 (ARM) |

| Freddie Mac CHOICERenovation | As-completed appraised value; renovation costs up to 75% of as-completed value | Same conforming limits as HomeStyle | For applications received May 4, 2026 or later: rental income from any unit funded by CHOICERenovation proceeds cannot be used to qualify | Lender-set; typically 620–680 |

| FHA 203(k) Standard | As-completed value: 96.5% LTV for purchase, 97.75% LTV for refinance | 2026 FHA one-unit limits: $541,287 floor; $1,249,125 ceiling (county-specific) | Yes; 50% of estimated rent (no prior rental history), or 75% (existing ADU), both subject to 30% cap on total monthly effective income; not usable for FHA cash-out refinance | 580 with 3.5% down; 500–579 with 10% down |

| FHA 203(k) Limited | As-completed value (same LTV factors) | Rehabilitation cost cap of $75,000 per HUD ML 2024-13 (effective Nov 4, 2024) | Same 30% cap on total effective income | Same as Standard 203(k) |

| Construction-to-permanent loan | As-completed value (drawn in stages) | Lender-dependent | Sometimes — depends on lease-start timing and lender | Typically 680+ |

| ARV home-equity loan (renovation HELOC category) | After-renovation value (RenoFi publicly describes up to 90% of after-renovation value) | Loan amount depends on partner credit union; minimums typically $25,000 | Lender-dependent; commonly not used | 620+ (lender-dependent); higher for larger loans |

| Local construction-to-permanent or forgivable-loan programs (SDHC, NYC Plus One, MassHousing, Boston, Vermont VHIP) | Program-defined; often as-completed value or income-based | $7,500–$395,000 depending on program | Some programs do; verify per program | Program-dependent (typically 640–680 where credit applies) |

| Unsecured personal loan | Income + credit only | Typically capped at $50,000–$100,000 | Not applicable (loan isn't real-estate secured) | 660+ for best terms |

Cell-level terms, rates, and availability change quarterly and vary by lender, state, and borrower profile. We re-verify this matrix quarterly. These are not loan offers. The Dwelling Index is an independent research resource — not a lender or broker. We do not rank lenders by commission and do not sort the table above by any compensation factor.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Ready to talk to a lender about renovation, construction, or FHA loan options?

Explore Mortgage-Backed ADU Financing Options →

Compare renovation, construction-to-permanent, and FHA 203(k) paths that use as-completed value.

Our partner Mortgage Research Center connects homeowners with lenders offering renovation, construction-to-permanent, and FHA loan products.

Explore Mortgage-Backed ADU Financing OptionsAffiliate link — we may earn a commission at no extra cost to you; we do not rank by commission.

How after-renovation-value (ARV) and as-completed-value loans work

Answer capsule

An after-renovation-value or as-completed-value loan underwrites against what your home will be worth after the ADU is built, not what it’s worth today. This is the single mechanism that lets a recent buyer with 3% equity borrow a meaningful sum against the future value. The three main products that use this mechanism are Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, and after-renovation-value home-equity loans through specialty lenders.

If you remember one concept from this page, remember this:

Future-value lending is real, federally regulated, and the specific reason no-equity ADU financing exists as a category. Lenders aren’t doing you a favor — they’re doing standard underwriting against a different appraised value.

Fannie Mae HomeStyle Renovation: how it works for an ADU

Fannie Mae’s HomeStyle Renovation product finances “the purchase or refinance of an existing dwelling and includes funds in the loan amount to cover the costs of repairs, remodeling, renovations, or energy improvements.” Fannie Mae’s ADU page explicitly confirms HomeStyle can be used to “construct or install a new ADU.”

Key 2025–2026 mechanics:

- Up to 97% LTV against as-completed value on purchase transactions.

- Renovation costs capped at 75% of the applicable as-completed value calculation (50% for manufactured homes) per Fannie Mae §B5-3.2-02.

- Up to 50% of renovation costs can be disbursed at closing for materials, permit fees, design, and deposits per the December 2025 Selling Guide update (SEL-2025-10).

- Renovation must complete within 15 months of loan closing.

- Per Fannie Mae's SEL-2025-10, for lenders using UAD 3.6, single-unit properties may include up to three ADUs. Until your lender is on UAD 3.6, confirm eligibility.

- Borrower may complete renovations themselves on one-unit properties, capped at 10% of as-completed value.

- 2026 conforming loan limit: $832,750 for a single-family home in standard areas; $1,249,125 in high-cost areas.

Honest tradeoff

If you’re using HomeStyle as a refinance, it replaces your first mortgage. For a homeowner with a 3% rate locked in 2021, going to a current-market rate to fund an ADU can wipe out years of rental-income return. Run the rate-differential math. If you’re using HomeStyle on a purchase, this concern doesn’t apply — there’s no existing low-rate loan to lose.

Freddie Mac CHOICERenovation: how it works for an ADU — with the critical 2026 change

Freddie Mac’s ADU page confirms CHOICERenovation “can be used to add a new ADU or renovate an existing ADU.” Renovation costs can finance up to 75% of as-completed value. Same conforming limits as HomeStyle.

The 2026 update you can’t miss

Per Freddie Mac Bulletin 2026-1, for mortgages with application received dates on or after May 4, 2026, rental income from any unit included in a CHOICERenovation project funded by the mortgage proceeds cannot be used to qualify the borrower. Only rental income from units not in the renovation project may be considered. Loan Product Advisor was updated April 12, 2026 to support the change.

In plain English: if you’re using CHOICERenovation proceeds to build the ADU, the lender cannot count that new ADU’s projected rent toward your income on applications dated May 4, 2026 or later. If your numbers depended on counting that rent, HomeStyle Renovation (which still allows ADU rental income up to the 30% cap) or FHA 203(k) (which still allows the 50%/75% mechanism) may be a better fit.

FHA 203(k) Standard and Limited: the rule changes that opened the door for ADUs

In October 2023, HUD published Mortgagee Letter 2023-17 — the most significant change to FHA ADU policy in a decade. The letter added ADUs as eligible improvements under both the Standard 203(k) and Limited 203(k) Rehabilitation Mortgage and created ADU rental-income qualifying mechanics with a hard cap.

The rental-income rules for FHA loans on properties with ADUs, all subject to a 30% cap on total monthly effective income:

- For a Standard 203(k) one-unit property with an ADU and no rental history: 50% of the lesser of the appraiser's estimated market rent or the lease rent, subject to the 30% cap.

- For an existing ADU on a property: some borrower scenarios allow 75% of estimated ADU rental income, subject to the 30% cap.

- FHA cash-out refinance: ADU rental income cannot be used to qualify under HUD ML 2023-17.

Worked example

Projected ADU rent of $1,200/month. Under the Standard 203(k) one-unit-with-ADU-and-no-prior-rental-history rule, the borrower can add $600/month to qualifying income — provided the resulting figure doesn’t push ADU-derived rental income above 30% of total monthly effective income. The 30% cap is the ceiling you have to design around.

Key 203(k) mechanics:

- Maximum LTV: 96.5% for purchase, 97.75% for refinance per HUD's 203(k) calculator instructions.

- 2026 FHA loan limits: $541,287 floor and $1,249,125 ceiling for one-unit properties (county-specific limits control) per HUD ML 2025-23.

- 3.5% minimum down with 580+ credit; 10% with 500–579 credit.

- Limited 203(k) rehabilitation cost cap raised from $35,000 to $75,000 per HUD ML 2024-13, effective for FHA case numbers assigned on or after November 4, 2024. Rehab period extended to nine months for Limited 203(k); twelve months for Standard 203(k).

- A 203(k) consultant is required for Standard 203(k); not required (but optional) for Limited 203(k).

- Lifetime mortgage insurance premium when the down payment is under 10%.

- Borrower must occupy the main house or the ADU as primary residence within 60 days of closing and for at least one year.

- New detached ADUs are not the clean 203(k) fit — the program is structured for attached additions, conversions, and existing ADU rehab.

After-renovation-value home-equity loans (the renovation HELOC category)

These are second-lien loans that sit behind your existing first mortgage — meaning you don’t lose your low rate. They underwrite against ARV. RenoFi, the most-cited example of this category, publicly describes its model as borrowing up to 90% of after-renovation value. RenoFi operates as a mortgage broker connecting homeowners to a network of credit-union partners. Per Bankrate’s RenoFi review, the typical minimum loan is $25,000 with credit floors starting at 620. State availability varies and changes — confirm with the lender directly before designing a project around it.

Honest tradeoff

The lender network is smaller than for conventional HELOCs. Underwriting takes longer. You pay for the as-completed appraisal whether or not you’re ultimately approved. Per the Terner Center for Housing Innovation, only about 6% of California ADU owners have used a renovation or construction loan, despite the products being “well-suited for homeowners without significant equity” — low adoption is partly an awareness problem and partly a lender-comfort problem. Ask a candidate lender how many ARV ADU loans they’ve actually closed.

Construction-to-permanent loans

Per Fannie Mae’s construction products page, construction-to-permanent financing supports both single-closing and two-closing transactions, and an ADU can be part of the construction project. The loan funds the build in scheduled draws, then converts (or refinances) into a permanent mortgage at completion. Best fit for ground-up detached ADUs and for borrowers who don’t have a low first-mortgage rate to preserve.

See which renovation or construction loan path fits your numbers.

Explore Mortgage-Backed ADU Financing Options →

Compare renovation, construction-to-permanent, and FHA 203(k) paths that use as-completed value.

Our partner Mortgage Research Center connects homeowners with lenders offering renovation, construction-to-permanent, and FHA loan products.

Explore Mortgage-Backed ADU Financing OptionsAffiliate link — we may earn a commission at no extra cost to you; we do not rank by commission.

Can projected ADU rental income help you qualify? The 2026 rules, decoded

Answer capsule

Sometimes — and the rules changed materially between 2023 and 2026. Federal loan programs now allow borrowers to count projected ADU rental income toward qualifying income with specific caps: FHA’s percentage rules under HUD ML 2023-17 are subject to a 30% cap on total monthly effective income; Fannie Mae caps ADU rental income at 30% of total qualifying income; Freddie Mac CHOICERenovation effectively does not allow rental income from units funded by loan proceeds on applications dated May 4, 2026 or later. Treat projected rent as a possible boost, not the foundation of your approval.

This is the section most pages get wrong. The rules are specific, recent, and worth reading slowly.

The FHA rule (HUD Mortgagee Letter 2023-17)

Published . ADUs are now eligible improvements under both Standard and Limited 203(k), and rental income from ADUs may be counted toward qualifying income under specific rules — all subject to a 30% cap on total monthly effective income:

- For some Standard 203(k) borrowers on a one-unit property with an ADU and no prior rental history: 50% of the lesser of estimated market rent or lease rent, subject to the 30% cap.

- For some borrowers on properties with an existing ADU: 75% of estimated ADU rental income, subject to the 30% cap.

- FHA cash-out refinance: ADU rental income cannot be used to qualify.

The follow-up letter, HUD Mortgagee Letter 2025-04 (published ), addresses boarder income (renters of space inside the home) — distinct from ADU income. ML 2025-04 explicitly notes that “a renter of an ADU is not a Boarder.”

The Fannie Mae rule (SEL-2025-08 and SEL-2025-10)

Per Fannie Mae’s Selling Guide announcements, policy now allows income from an ADU to be considered toward qualifying income on a one-unit principal residence when specific requirements are met. The hard cap: ADU rental income used for qualifying cannot exceed 30% of the borrower’s total qualifying income. Desktop Underwriter (DU) Version 12.1, effective , automatically recognizes the new policy.

Required documentation: Fannie Mae Form 1004/Freddie Mac Form 70 (Uniform Residential Appraisal Report) plus Fannie Form 1007 (Single Family Comparable Rent Schedule). Note: Fannie Mae removed minimum credit-score requirements for DU loan casefiles created on or after — but manually underwritten Fannie loans still require 620 (fixed-rate) or 640 (ARM), and individual lenders may apply credit-score overlays.

The Freddie Mac rule (Bulletin 2026-1)

This is the one most homeowners — and even some lenders — don’t know about yet

Per Freddie Mac Bulletin 2026-1 (issued ):

“For CHOICERenovation Mortgages, rental income from any unit included in the renovation project funded by the Mortgage proceeds cannot be used to qualify the Borrower. Only rental income from units not included in the renovation project may be considered for qualifying purposes.”

Effective date: applications received on or after . Loan Product Advisor was updated to support the change.

If your numbers depended on counting that ADU rent, you’ll need HomeStyle Renovation (which still allows ADU income up to the 30% cap) or FHA 203(k) (which still allows the 50%/75% mechanism subject to the 30% cap).

Side-by-side: can ADU rent help me qualify?

| Loan program | Counts projected ADU rent? | Cap or limit | Source |

|---|---|---|---|

| FHA 203(k) Standard, one-unit with ADU, no rental history | Yes | 50% of estimated rent, subject to 30% cap on total monthly effective income | HUD ML 2023-17 |

| FHA, existing ADU on property (some borrower scenarios) | Yes | 75% of estimated rent, subject to 30% cap on total monthly effective income | HUD ML 2023-17 |

| FHA cash-out refi | No | — | HUD ML 2023-17 |

| Fannie Mae HomeStyle / standard purchase / refi | Yes, with conditions | Cap: 30% of total qualifying income | Fannie SEL-2025-08 |

| Freddie Mac CHOICERenovation, ADU funded by loan proceeds, application May 4, 2026+ | No | — | Freddie Bulletin 2026-1 |

| Freddie Mac CHOICERenovation, ADU not funded by loan proceeds | Yes, with lease-start-date rule | Per Freddie ADU FAQ | Freddie ADU FAQ |

| Renovation HELOC / ARV second-lien | Lender-dependent; commonly no | — | Lender policy |

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals. We do not guarantee approval, qualification, or specific outcomes.

The Equity Math Decoder: how much you can actually borrow under each path

Answer capsule

The same homeowner profile produces wildly different borrowing capacity depending on which path they pursue. Most articles give you LTV ratios in the abstract; this section gives you dollars against a single hypothetical homeowner so you can apply the math to your own numbers.

We’re going to run one homeowner through every path. Use it as a template — substitute your own numbers and you’ll see your real options sharpen quickly.

Illustrative borrowing capacity for the hypothetical homeowner below — not loan offers or guarantees.

The hypothetical homeowner

Current home value

$600,000

First mortgage balance

$580,000 (3% fixed, locked 2021)

Equity

$20,000 (3.3%)

Credit score

720

Household income

$135,000

DTI before any new loan

32%

ADU project total cost estimate

$200,000 (mid-range detached, ~700 sq ft)

As-completed home value (with ADU)

$780,000 — hypothetical assumed appraised value used solely to illustrate borrowing-capacity math

Projected ADU rent

$2,000/month (Terner Center California median)

State

California

Borrowing capacity by path

| Path | Borrowing math (illustrative) | Net cash to project |

|---|---|---|

| Standard HELOC (80% CLTV) | $600,000 × 0.80 − $580,000 = −$100,000 | $0 — disqualified |

| Cash-out refinance (80% LTV) | $600,000 × 0.80 − $580,000 payoff = $0 | $0 — disqualified |

| HEI (Hometap requires 25%+ equity) | Doesn't meet equity threshold | $0 — disqualified |

| ARV home-equity loan (~90% of $780K ARV) | $780,000 × 0.90 − $580,000 = $122,000 | $122,000 (would need to source remaining $78,000) |

| Fannie HomeStyle Renovation (97% as-completed) | $780,000 × 0.97 − $580,000 payoff = $176,600 | ~$177,000 |

| Freddie CHOICERenovation | Similar math; renovation costs capped at 75% of as-completed | ~$170,000–$180,000 |

| FHA 203(k) Standard (refi, 97.75% LTV) | $780,000 × 0.9775 − $580,000 payoff = ~$182,450. Can use 50% of $2,000 = $1,000/month projected rent for qualifying (subject to 30% cap) | ~$182,000 |

| Construction-to-permanent loan | Lender-dependent; commonly ~90% of as-completed less payoff = ~$122,000 | ~$122,000 |

| SDHC ADU Finance Program (City of San Diego only) | Program-defined; up to $250,000 | Up to $250,000 — covers full project |

| Unsecured personal loan | Income/credit-based; typically $50,000–$100,000 cap | Partial — gap funding only |

These are illustrative borrowing-capacity examples for a single hypothetical homeowner, not loan offers or guarantees. Actual capacity depends on lender underwriting, appraisal results, debt-to-income ratios, county-specific FHA limits, closing costs, upfront mortgage insurance premiums, and other factors. The hypothetical $780,000 as-completed value is an assumption used only to illustrate the math; the lender’s appraisal controls. We do not guarantee approval, qualification, or specific outcomes.

What the numbers actually tell you

The highest single-source path that preserves the low first mortgage is the ARV home-equity loan, but it leaves a roughly $78,000 gap for our hypothetical homeowner.

The highest borrowing capacity overall comes from FHA 203(k) refinance (97.75% LTV) — but it replaces the 3% rate, adds lifetime mortgage insurance, and is subject to FHA county-specific limits. Run the rate-differential math against rental income before committing.

In a covered city like San Diego, the SDHC ADU Finance Program completely changes the picture — up to $250,000 covers the entire project at a 1% construction rate stepping up to 4% permanent, in exchange for a 7-year affordability covenant.

Want to run this math on your own numbers?

Download the Free ADU Starter Kit →

Includes the Equity Math Decoder worksheet, the lender-document checklist, and the ADU feasibility prep sheet.

Download the Free ADU Starter KitHow to stack two paths when one isn’t enough

Answer capsule

Many no-equity ADU projects work only when two financing paths combine — typically a primary loan that handles 60–80% of the budget plus a secondary source (personal loan, grant, or cash) that fills the gap. Lenders rarely design a stack for you; you have to do it yourself or work with a broker who specializes in renovation financing.

The hypothetical homeowner above had a $78,000 gap on the cleanest no-equity path (ARV home-equity loan preserving the low first mortgage). Real-world stacks that close that kind of gap:

1Recent buyer, preserve low first-mortgage rate, $200K project

This stack preserves the 3% first mortgage. The blended cost of capital is higher than a single low-rate loan, but the rental income from the ADU often covers the new debt service in California markets. These are illustrative examples, not guarantees of returns.

2Buying a home with intent to build an attached ADU

One close, lower credit thresholds, lifetime mortgage insurance as the tradeoff.

3In a covered city (San Diego, Boston, NYC)

For homeowners in covered cities, the local program is almost always the right primary lane because the borrowing cost is so much lower than market-rate alternatives.

Local programs that bypass equity entirely: the 2026 map

Answer capsule

A small number of municipal and state programs underwrite ADUs through construction-to-permanent or forgivable-loan structures that don’t require existing home equity. They come with affordability covenants and income limits, so they’re not for everyone — but for homeowners in covered geographies, they’re often the strongest path.

Local programs verified . Coverage is geographic; most homeowners won’t have one in their area.

The verified national snapshot, as of :

| Program | Geography | Status (verified May 19, 2026) | Max support |

|---|---|---|---|

| SDHC ADU Finance Program | City of San Diego, CA | Open | Up to $250,000 construction-to-permanent |

| NYC Plus One ADU Program | New York City | Open — EOI window through | Up to $395,000 combined financing + technical support |

| MassHousing ADULP | Massachusetts statewide | Open | Up to $250,000 for detached; up to $150,000 for attached |

| Boston ADU Financial Assistance Program | City of Boston | Open | $7,500 soft-cost grant + up to $50,000 deferred 0% loan |

| Vermont VHIP 2.0 | Vermont statewide | Competitive | Up to $50,000 no-interest forgivable loan |

| Portland, OR System Development Charge (SDC) waiver | City of Portland | Open | SDC waiver — saves thousands per project |

| CalHFA $40,000 ADU Grant | California statewide | Closed — fully allocated since | $40,000 toward pre-development costs (when funded) |

For City of San Diego homeowners, the SDHC program offers one of the most aggressive borrowing structures in this verified table — and it requires no traditional equity. Inside the SDHC service area, SnapADU is a verified ADU builder in Greater San Diego. (SnapADU is an affiliate partner of The Dwelling Index for Greater San Diego only.)

For our full state-by-state and city-by-city grant database — updated quarterly against each administering agency — see Dwelling Index’s ADU Grants resource.

What’s coming: the SUPPLY Act and what it could change

Answer capsule

H.R. 4568, the bipartisan Supporting Upgraded Property Projects and Lending for Yards (SUPPLY) Act, was introduced in July 2025 and would direct HUD to insure second-lien mortgages specifically for ADU construction — letting homeowners keep a low first mortgage while financing the ADU as a separate loan. As of the bill is in the House Financial Services Committee and is not yet law. Do not plan your project around it.

The SUPPLY Act would do three structurally important things if passed:

HUD-insured second mortgages

Specifically for ADU construction. Per GovInfo, H.R. 4568 was introduced in the House and referred to the Committee on Financial Services. The bill text establishes HUD insurance for certain ADU second liens.

Up to 50% of anticipated ADU rental income

Could be considered for loan qualification.

Preserve the first mortgage

The same structural advantage as today's after-renovation-value second-lien products, but with federal insurance backing that brings more lenders into the market.

Endorsements: National Association of Home Builders (NAHB), Mortgage Bankers Association, California and Nevada Credit Union Leagues, Casita Coalition. Status as of : in committee. Not law. We’ll update this page when the status changes.

The 2023–2026 ADU lending unlock timeline

| Date | Action | Impact |

|---|---|---|

| Oct 16, 2023 | HUD Mortgagee Letter 2023-17 published | FHA 203(k) Standard and Limited add ADUs as eligible improvements; ADU rental-income qualifying mechanics created with 30% cap |

| Jul 9, 2024 | HUD Mortgagee Letter 2024-13 published | Limited 203(k) rehab cost cap raised from $35,000 to $75,000; rehab periods extended; consultant fees can be financed under Limited 203(k); effective for case numbers assigned on or after Nov 4, 2024 |

| Jan 13, 2025 | HUD Mortgagee Letter 2025-04 published | Boarder-income rules clarified; explicit separation of boarder vs. ADU renter |

| Jul 18, 2025 | SUPPLY Act (H.R. 4568) introduced in House | Federal second-lien ADU insurance bill enters legislative pipeline |

| Nov 16, 2025 | Fannie Mae removes minimum credit-score floor for DU casefiles | Underwriting moves to overall-risk evaluation for DU loans; manual underwriting retains 620/640 floors; lenders may still apply overlays |

| Dec 2025 | Fannie Mae announces SEL-2025-10 | HomeStyle Refresh launches; ADU eligibility expanded (tied to UAD 3.6 lender adoption) |

| Dec 11, 2025 | HUD ML 2025-23 sets 2026 FHA loan limits | One-unit floor rises to $541,287; ceiling rises to $1,249,125 |

| Feb 4, 2026 | Freddie Mac Bulletin 2026-1 published | CHOICERenovation rental-income restriction announced for May 4, 2026 effective date |

| Mar 21, 2026 | Fannie Mae DU Version 12.1 released | Automated underwriting recognizes new ADU rental-income policy |

| Mar 31, 2026 | Fannie SEL-2025-10 effective | Expanded ADU property-eligibility rules take effect (UAD 3.6 lenders) |

| May 4, 2026 | Freddie Mac Bulletin 2026-1 effective | CHOICERenovation no longer allows rental income from units funded by loan proceeds for new applications |

If you’re applying for a loan in 2026, your lender should be familiar with every line of this table. If they’re not, they may not be the right lender for your project.

Home Equity Investments (HEI) vs no-equity ADU financing: don’t confuse them

Answer capsule

A Home Equity Investment is not a no-equity product. HEIs from companies like Hometap, Unlock, and Point provide a lump sum in exchange for a share of your home’s future appreciation, with no monthly payments — but they require meaningful existing equity to qualify. If your problem is “I don’t have enough equity for a HELOC,” HEIs don’t solve it. If your problem is “I have equity but can’t afford a monthly payment,” they might.

This distinction matters because HEI marketing often emphasizes “no monthly payments” in ways that imply they’re a no-equity solution. They’re not. Hometap publicly states a minimum of 25% equity. Point requires sufficient equity plus a 500+ credit score. The CFPB has noted that home equity contracts can have widely varying repayment outcomes that homeowners should understand carefully before signing.

When HEIs actually fit

- You have substantial existing equity (provider-specific minimums).

- You can't comfortably carry a new monthly payment (fixed income, retirement, irregular income).

- You're willing to give up a share of future appreciation in exchange for upfront cash.

- You plan to stay in the home long enough that the appreciation share isn't catastrophic.

- Your state is on the provider's eligibility list.

When HEIs don’t fit a no-equity ADU project

You don’t have enough current equity to meet the minimum threshold. The product simply isn’t available to you. We mention HEIs here for completeness because so many homeowners read about them and assume they’re a no-equity solution — they aren’t.

Hometap, Unlock, and Point are pending partners of The Dwelling Index. We do not currently route primary CTAs to HEI products and do not earn commissions on HEI placements in this article. We mention them as the major category players for educational completeness only.

What if your ADU is detached, prefab, modular, manufactured, or a garage conversion?

Answer capsule

ADU type changes which financing path fits best. Detached ground-up units lean toward HomeStyle, CHOICERenovation, or construction-to-permanent. Attached additions and conversions lean toward FHA 203(k). Prefab and modular ADUs follow special agency rules about permanent foundations and real-property classification.

Acronyms decoded once:

ADU = Accessory Dwelling Unit. DADU = Detached Accessory Dwelling Unit. JADU = Junior Accessory Dwelling Unit (smaller unit inside the existing home, often capped ~500 sq ft). ARV = After-Renovation Value. As-completed value = appraised value of your home assuming the ADU is built per submitted plans. UAD 3.6 = the Uniform Appraisal Dataset version 3.6, tied to recent Fannie Mae ADU-eligibility expansions.

Detached new-construction ADU

Best fit:

- Fannie Mae HomeStyle Renovation — explicitly allows construction of detached ADUs.

- Freddie Mac CHOICERenovation — allows new ADU construction.

- Construction-to-permanent loan — best when ADU is a substantial project relative to home value.

- ARV second-lien (renovation HELOC category) — best if preserving a low first mortgage matters more than cost.

Avoid: FHA 203(k) Standard as your primary path for a ground-up detached unit. The program’s structure is built for attached additions, conversions, and existing-ADU rehab.

Attached ADU or addition

- FHA 203(k) Standard — the cleanest fit; HUD ML 2023-17 specifically addresses attached ADU additions and conversions.

- HomeStyle Renovation or CHOICERenovation as conventional alternatives.

- Construction-to-permanent loan for larger projects.

Garage conversion or basement ADU

- FHA 203(k) — conversions are the program's home turf. Limited 203(k) is well-suited for projects under $75,000.

- HomeStyle Renovation — straightforward conventional option.

- CHOICERenovation — same.

- Standard HELOC if you have enough existing equity (conversion budgets are often $60,000–$150,000).

Prefab, modular, or manufactured ADU

Special rules apply because of factory-built and real-property classification. Per Fannie Mae Special Property Eligibility Considerations §B2-3-04, manufactured home ADUs must be legally classified as real property under applicable state law. Fannie’s December 2025 update (SEL-2025-10) expanded ADU eligibility to allow ADUs on single-wide manufactured homes. Freddie Mac Bulletin 2025-15 included ADU-related updates to manufactured-home mortgages, effective for settlement dates on or after .

For prefab/modular ADUs, work with a lender who’s actually closed manufactured or factory-built ADU loans. Many lenders haven’t, and the underwriting nuances around permanent foundation classification can stall a deal that should have closed.

| ADU type | First financing path to test | Second path |

|---|---|---|

| Detached new construction | HomeStyle / CHOICERenovation / Construction-to-permanent | ARV second-lien |

| Attached ADU / addition | FHA 203(k) | HomeStyle / CHOICERenovation |

| Garage / basement conversion | Limited 203(k) (under $75K rehab) / HomeStyle / CHOICERenovation | Standard HELOC if equity exists |

| Prefab / modular (real-property classified) | HomeStyle / Construction-to-permanent | CHOICERenovation; manufacturer financing |

| JADU (interior, < 500 sq ft) | HomeStyle / CHOICERenovation / Limited 203(k) | Standard HELOC if equity exists |

For an in-depth review of ADU types, definitions, and which one fits which property, see our What Is an ADU? guide.

Can you use a personal loan to build an ADU?

Answer capsule

Yes for smaller scopes (typically under $75,000–$100,000) or as gap funding alongside a primary mortgage-backed loan. Personal loans don’t require home equity and fund fast, but they carry meaningfully higher rates than mortgage-backed renovation loans and shorter repayment terms — which means high monthly payments that can squeeze your DTI for years. They’re rarely the right choice as the only funding source for a full ADU build.

The reasons personal loans aren’t usually the right primary lane:

Loan size

Most unsecured personal-loan products cap at $50,000–$100,000. National ADU build costs commonly run $100,000–$300,000 per Angi's 2026 ADU cost data and the Terner Center's California survey. A $50,000 personal loan funds a soft-cost package, not a finished ADU.

Rate environment

Personal-loan annual percentage rates run materially higher than mortgage-backed renovation or construction loans because the loan isn't secured by the home. Confirm current rates with the specific lender — they vary widely by credit profile.

Repayment term

Personal loans typically amortize over 24–84 months, which compresses the payment relative to a 15- or 30-year mortgage. The monthly payment hit on a $50,000 personal loan can be three to five times what the same amount would be on a renovation mortgage.

When a personal loan does fit

Soft-cost or design-phase funding

Before a primary lender will close (architectural plans, permit fees, deposit on a prefab unit). Many homeowners use a small personal loan to get to permit-ready, then refinance into a construction or renovation mortgage.

Gap funding

Between a primary mortgage-backed loan and the actual project cost (the $78,000 gap in our Equity Math Decoder example).

Small-scope conversions

A $40,000 garage conversion that doesn't justify the closing costs and timeline of a renovation mortgage.

For a full ADU build, treat a personal loan as a supplement, not the foundation.

What documents will lenders need before they take your ADU application seriously?

Answer capsule

Renovation and construction loans require materially more documentation than a simple cash-out refinance because the lender is underwriting against a property that doesn’t yet exist in its final form. Showing up with a complete project package — feasibility, scope, budget, contractor, and lender-ready financials — separates a 30-day close from a 90-day stall.

| Document | Why the lender needs it |

|---|---|

| Current first-mortgage statement showing balance, rate, and payoff figure | Calculates payoff for refinance products and CLTV for second-lien products |

| Property address and recent estimated value | Establishes current-value baseline for appraisal |

| ADU project total cost estimate (hard costs, soft costs, contingency) | Sets the renovation-cost figure for underwriting |

| Written contractor bid | Required for HomeStyle, CHOICERenovation, and 203(k) — Fannie Mae §B5-3.2-01 requires renovation contracts and plans/specs in the loan file |

| Contractor license number and proof of liability/workers' comp insurance | Lender contractor review per agency rules |

| Preliminary architectural plans (or pre-approved plan templates where the city publishes them) | Required for the as-completed appraisal and lender plan review |

| ADU type and square footage (detached / attached / garage / basement / JADU) | Determines program eligibility and appraisal comparables |

| Local feasibility or zoning confirmation | Confirms the ADU is legally buildable |

| Building permit application status (if available) | Demonstrates progress toward an approved scope |

| W-2s for the last 2 years, recent pay stubs, last 2 years of tax returns (more if self-employed), bank statements | Standard income and asset verification |

| Insurance estimate for the completed property + builder's-risk insurance during construction | Lender protection during the construction window |

| Form 1007 (Single Family Comparable Rent Schedule) | Required by Fannie Mae and Freddie Mac when projected ADU rental income is part of qualifying |

| Utility, sewer, and water scope | Separate utility laterals for the ADU can add $5,000–$25,000 depending on jurisdiction |

| Contingency budget | Fannie Mae requires a 10–15% contingency on 2-4 unit properties; lenders often require it on single-unit projects too |

| Construction timeline and draw schedule | Defines the lender's payment milestones during the build |

Get the printable lender-document checklist plus the feasibility prep sheet.

Download the Free ADU Starter Kit →

Includes the Equity Math Decoder worksheet, the lender-document checklist, and the ADU feasibility prep sheet.

Download the Free ADU Starter KitHow to get financing-ready in seven days

Answer capsule

Most homeowners walk into the lender conversation without a project — they have a wish. Spending one week packaging the project into a lender-ready bundle is the single highest-leverage thing you can do before applying.

Run a feasibility check on your property.

Use Dwelling Index's free property check to confirm your lot can legally support an ADU and what type. If the lot can't support an ADU, no loan will change that. Programs like MassHousing ADULP explicitly require plans, permits, and pre-development materials before applying — feasibility on Day 1 unblocks every later step.

Calculate your equity gap.

Run the HELOC formula above with your real numbers. If the gap is positive (you have enough current equity), check HELOC first. If the gap is negative or thin, you're shopping the future-value path.

Decide: preserve first mortgage, or refinance.

If your first mortgage is under ~4%, lean toward second-lien products (ARV home-equity loan). If you bought recently at a higher rate, the refi-based renovation mortgages (HomeStyle, CHOICERenovation, 203(k)) lose nothing by being on the table.

Lock the ADU type.

Detached / attached / garage / basement / prefab. This decision drives which loan path is best — and which Fannie/Freddie/FHA rule applies.

Get a preliminary scope and budget from at least one builder.

A real number changes the entire conversation with the lender. One of the most common reasons loan applications stall is that the homeowner's budget estimate is half the real cost.

Gather lender documents.

Use the checklist above. Tax returns, pay stubs, bank statements, and the contractor bid are the four things lenders ask for first. If projected rent is part of your qualifying strategy, you'll also need Form 1007 — the Single Family Comparable Rent Schedule.

Ask candidate lenders these exact questions:

- 1.Can you underwrite the ADU using as-completed value? (If they hesitate, they're not your lender.)

- 2.Do you finance my ADU type — detached / attached / prefab / manufactured?

- 3.Can I preserve my current first mortgage with a second-lien product?

- 4.Under what rules can you count projected or existing ADU rent toward qualifying — and are you applying HUD ML 2023-17, Fannie SEL-2025-08, or Freddie Bulletin 2026-1?

- 5.What appraisal, contractor, permit, and draw requirements apply to your renovation loan product?

- 6.What happens if the as-completed appraisal comes in below my budget?

- 7.Are there state, county, or property-type restrictions on this product?

Two lender phone calls answering those seven questions tell you more than two months of website browsing.

Skip directly to Day 1

See What You Can Build → Get Your Free ADU Report

Check your property before you spend time comparing loan options. About 60 seconds. No phone call.

See What You Can BuildWhat can go wrong with no-equity ADU financing — and how to avoid each problem

Answer capsule

Future-value lending depends on assumptions about how the property will appraise after the ADU is built. When those assumptions miss, the loan that looked workable on paper can stall, shrink, or fall apart. The most common failure modes are low as-completed appraisals, lender rejection of the contractor, ADU-type mismatches with the program, rental-income rules the lender won’t apply, and refinances that destroy more value than they create.

The as-completed appraisal comes in low

The most common failure point in renovation/construction lending. The appraiser values the as-completed home at $750,000 when your loan math required $780,000, and your borrowing capacity drops by tens of thousands of dollars overnight.

Mitigation: Order a comparable-sales analysis from a builder familiar with ADUs in your specific market before you submit the loan application. If comparable sales don't support your assumed ARV, redesign or scale the project.

The lender won't count future rent

You designed your DTI math around 75% of $2,000/month FHA rental income — and then learned your lender doesn't actually implement HUD ML 2023-17 yet. Roughly two-and-a-half years after HUD ML 2023-17 was published, adoption is still uneven across FHA lenders.

Mitigation: Ask the question on Day 7 of the seven-day plan. If a lender hedges on whether they apply the federal ADU rental-income rules, find a lender that does.

The project is legal locally but not financeable under the chosen program

A legal nonconforming 'grandfathered' ADU might be permittable by the city and not financeable under FHA 203(k) without lender-specific review. A detached new ADU is legal under most state law but is a structurally poor fit for FHA 203(k) Standard.

Mitigation: Separate two questions — is the project legal (zoning/building) and is the project financeable under this program (mortgage/agency rules). The answers can diverge.

You preserved your low first mortgage but took a worse second-lien product

Sometimes the second-lien path you took to preserve a 3% first mortgage has a much higher second-lien rate and shorter terms, and the math turns ugly fast.

Mitigation: Run the full blended-cost-of-capital math before signing. Model both paths against a 10-year window.

The grant or local program is closed, waitlisted, or restrictive

You designed your stack around the SDHC ADU Finance Program and discovered the program closed for new applications six months ago.

Mitigation: Verify program status with the administering agency directly on the day you apply, not based on a builder's blog from 2023.

Honest admission

If your equity is genuinely sub-3%, your credit is under 620, your DTI is already over 45%, and you live in a state without a local ADU program — there is a reasonable chance no current product will fully fund your project on its own. The honest path forward is often a phased build (garage conversion first, detached unit later) or waiting 18–36 months to build modest equity before applying.

We’d rather tell you that than route you into a financing structure that doesn’t work. A phased build is often cheaper per dollar of finished space than trying to force a full project on day one, and 18–36 months of equity-building plus rule changes tends to expand your options materially.

What about ADU grants?

Answer capsule

Grants are real and can help — but they’re almost never enough to fund a project alone. Treat grant funding as supplemental, not as the financial cornerstone of your ADU plan. Most are local, income-restricted, limited in funding, waitlisted, or paid as reimbursement after you’ve already incurred the cost.

The reality of the ADU grant landscape, verified :

California's CalHFA $40,000 ADU grant

Fully allocated and closed for new applications per CalHFA Bulletin 2023-14, issued December 28, 2023.

New York City's Plus One program

Open with up to $395,000 combined financial and technical support for qualifying projects; the current expression-of-interest window runs through June 12, 2026.

Boston

Offers a $7,500 soft-cost grant + $50,000 deferred 0% loan for income-eligible owner-occupants of 1–3 unit homes who attend required ADU Design and Budget Workshops and work with a licensed architect.

Vermont's VHIP 2.0

Offers up to $50,000 no-interest forgivable loan statewide; competitive scoring, 20% match required, reimbursement-heavy disbursement schedule after the first disbursement, 5- or 10-year affordable-rent covenant.

Portland, Oregon

Waives system-development charges for ADUs that are owner-occupied or rented month-to-month or longer, conditional on the owner signing a 10-year covenant prohibiting short-term rental use.

For our full verified state-by-state and city-by-city grant database — updated quarterly against each administering agency — see Dwelling Index’s ADU Grants resource.

What to verify before counting on a grant:

- Is the program currently open? (Status changes monthly.)

- Is funding currently available, or is it a waitlist?

- Is your specific address in the eligible service area?

- Are there income, AMI, or affordability restrictions?

- Is the program reimbursement or upfront funding? (Reimbursement programs require construction financing in place to bridge the timing.)

- Does the grant combine with your chosen loan product?

What we verified

Last verified:

We checked the following primary sources for the rules, figures, and program details in this article:

- HUD Mortgagee Letter 2023-17 (ADU rental income, property eligibility, appraisal protocols)

- HUD Mortgagee Letter 2024-13 (203(k) program revisions including Limited 203(k) $75,000 rehab cap, effective Nov 4, 2024)

- HUD Mortgagee Letter 2025-04 (boarder income revisions)

- HUD Mortgagee Letter 2025-23 (2026 FHA forward mortgage loan limits)

- HUD 203(k) calculator instructions (96.5% purchase LTV; 97.75% refinance LTV)

- Fannie Mae Selling Guide Announcements SEL-2025-08 and SEL-2025-10

- Fannie Mae DU Version 12.1 release notes

- Fannie Mae HomeStyle Renovation FAQ and §B5-3.2-01 / §B5-3.2-02

- Fannie Mae Accessory Dwelling Units guidance page

- Fannie Mae Construction Products page

- Fannie Mae Special Property Eligibility Considerations §B2-3-04

- Freddie Mac CHOICERenovation FAQ and Guide §4607

- Freddie Mac Accessory Dwelling Units FAQ and Guide §5601

- Freddie Mac Bulletin 2026-1 (CHOICERenovation rental-income restriction effective May 4, 2026)

- Freddie Mac Bulletin 2025-15 (ADU + manufactured home updates)

- San Diego Housing Commission ADU Finance Program (sdhc.org/housing-opportunities/adu/)

- NY HPD/HCR Plus One Program announcement

- MassHousing Accessory Dwelling Unit Loan Program page

- City of Boston ADU Financial Assistance Program page

- Vermont VHIP materials via RuralEdge

- City of Portland ADU SDC Waiver page

- CalHFA Bulletin 2023-14

- GovInfo H.R. 4568 (SUPPLY Act)

- Terner Center for Housing Innovation ADU Construction Financing paper (2022) and Statewide ADU Owner Survey (2024)

- FHFA 2026 conforming loan limits

- RenoFi (renofi.com) and Bankrate's RenoFi review

- Hometap application guidance for HEI minimum equity threshold

- Angi's 2026 ADU cost data

We did not rank lenders by compensation, quote guaranteed rates, or treat grant availability as permanent. We are not a lender, broker, or financial advisor. Financing terms depend on individual financial situations; we do not guarantee approval, qualification, or specific outcomes.

Methodology

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender or broker.

For this page, we read the primary-source agency documents listed above and confirmed program-specific details directly with administering agencies where applicable. Where we couldn’t independently verify a figure, we flagged it for re-verification.

Our editorial process explicitly separates three types of claims:

- 1.Verified regulatory facts — agency rules, federal mortgagee letters, conforming loan limits, program eligibility.

- 2.Verified commercial facts — program loan amounts, interest rate structures where published, state availability.

- 3.Editorial recommendations — which path may fit which homeowner profile, framed as editorial conclusions based on the verified facts above.

We re-verify this page quarterly against the source list. Affiliate relationships are disclosed near the first affiliate link and near comparison tables that include affiliate-linked partners. Editorial recommendations are never influenced by compensation. We do not rank lenders by payout.

Frequently asked questions

Can I build an ADU if I have no equity?

Yes — if a lender can underwrite the loan against the property's after-renovation or as-completed value, and your income, credit, project, and ADU type meet the program's requirements. If you have no equity and weak repayment capacity and no eligible local program, financing may not work yet. The path that fits depends on whether your real constraint is equity, a desire to preserve a low first mortgage, or cash flow.

How much equity do you need to finance an ADU?

For future-value loans (HomeStyle, CHOICERenovation, FHA 203(k), construction-to-permanent, ARV second-lien), no traditional equity is required — the lender underwrites against as-completed value. For current-value products (standard HELOC, conventional cash-out refinance), you typically need at least 15–20% existing equity.

What is the best loan to build an ADU with no equity?

There is no single best loan. The starting point depends on whether you want to preserve your first mortgage (look at ARV second-lien loans), whether you're willing to refinance (look at HomeStyle, CHOICERenovation, FHA 203(k), or construction-to-permanent), and the ADU type (detached vs attached vs conversion vs prefab). Use the decision matrix on this page to narrow to one or two options.

Can I use a HELOC to build an ADU if I just bought my house?

Usually not, because standard HELOCs underwrite against your home's current value minus your current mortgage balance. Recent buyers rarely have enough current tappable equity. After-renovation-value loans solve this directly.

Can projected ADU rental income help me qualify?

Sometimes, with specific caps. FHA allows percentage-based qualifying (50% or 75% in different scenarios), all subject to a 30% cap on total monthly effective income, per HUD ML 2023-17. Fannie Mae caps ADU rental income at 30% of total qualifying income (SEL-2025-08). Freddie Mac's CHOICERenovation, for applications dated May 4, 2026 or later, does not allow rental income from any unit funded by loan proceeds to be used for qualifying (Bulletin 2026-1).

Can FHA 203(k) finance a detached ADU?

FHA 203(k) Standard cleanly allows renovation of an existing detached or attached ADU and the addition of a new attached ADU. New detached ground-up ADU construction is not the program's structural fit, so a detached new-build typically goes to HomeStyle, CHOICERenovation, or construction-to-permanent instead.

Can I use a personal loan to build an ADU?

For smaller scopes (typically under $75,000–$100,000) or as gap funding alongside a primary mortgage-backed loan — yes. As the only funding source for a full ADU build — rarely the right answer. Personal-loan rates are meaningfully higher than mortgage-backed renovation loans, and shorter repayment terms produce high monthly payments.

Is a Home Equity Investment (HEI) a no-equity ADU loan?

No. HEIs typically require meaningful existing equity — Hometap publicly requires 25% minimum equity. The 'no monthly payment' feature solves a different problem (cash flow) than the one no-equity homeowners actually have (insufficient current equity for a HELOC).

Should I refinance my first mortgage to build an ADU?

Only if the project value, refinance rate differential, and long-term plan justify giving up the current mortgage. A homeowner with a sub-4% first mortgage should compare second-lien or future-value options against the refinance path before committing. Run the math on a 10-year window, not just a payment-month comparison.

Are ADU grants enough to build an ADU?

Usually not. Grants tend to cover pre-development soft costs ($7,500–$50,000) on a $200,000+ project. NYC Plus One is the notable exception, with up to $395,000 combined financial and technical support. Treat grants as supplemental funding and design your financing plan around the loan path that fills the rest.

What should I do before applying for ADU financing?

Confirm the property can legally support an ADU, calculate your real equity gap, define the ADU type, get a preliminary contractor budget, and ask candidate lenders whether they underwrite against as-completed value. The seven-day plan on this page is the practical sequence.

Does my credit score have to be high?

Most no-equity paths need 620–680. FHA 203(k) goes as low as 580 (3.5% down) or 500 (10% down). Fannie Mae removed its agency-floor minimum credit score for Desktop Underwriter loan casefiles created on or after November 16, 2025; manually underwritten Fannie loans still require 620 (fixed) or 640 (ARM), and individual lenders may apply credit-score overlays. RenoFi-network credit unions typically start at 620, higher for larger loans.

Will the SUPPLY Act help me?

Not yet. H.R. 4568 was introduced in July 2025 and is currently in the House Financial Services Committee. It would create HUD-insured second-lien ADU loans, but it is not law. Do not plan your project around it.

Not sure where to start?

See what’s possible at your address — get your free ADU report in 60 seconds

Check your property before you spend time comparing loan options. About 60 seconds. No phone call.

See What You Can Build