How to Qualify for ADU Financing in 2026: The Real Thresholds, Decoded Agency Rules, and the 30–180 Day Fixes If You Don't Qualify Today

By The Dwelling Index Editorial Team · · Last verified May 20, 2026

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

60-Second Answer

ADU financing qualification is controlled by four gates simultaneously: borrower strength (credit score, DTI, income documentation, cash reserves), equity or future-value collateral, property eligibility (legal ADU, zoning compliance, no blocking HOA), and project documentation (licensed contractor, itemized scope, draw schedule). A strong credit score does not override an illegal ADU. Enough equity does not fix undocumented income. All four gates must clear at the same time.

General thresholds across major ADU loan products: credit score floors run from 580 (FHA 203(k) with 10% down) to 620 (most conventional products) to 660+ (DSCR); DTI is typically capped at 43–50%; equity requirements range from zero (renovation and construction loans that underwrite against after-improved value) to 15–20% post-close equity for HELOC/HELOAN/cash-out refi products. As of October 8, 2025, Fannie Mae (B3-3.8-01) allows existing ADU rental income to count toward qualifying income on a one-unit principal residence, capped at 30% of total qualifying income — the most significant ADU financing rule change in years.

What We Verified

Qualification thresholds verified against Fannie Mae Selling Guide B3-3.8-01 (effective October 8, 2025) and B5-3.2-02; Fannie Mae DU 12.1 release notes (weekend of March 21, 2026); Freddie Mac Seller/Servicer Guide Chapter 5306; HUD Mortgagee Letter 2023-17 and ML 2024-13; FHA Handbook 4000.1; USDA proposed rule (Federal Register, March 31, 2026); CalHFA ADU Grant Program status (allocated December 28, 2023). Market rates and lender overlays verified via current lender rate sheets.

Sources and methodology: Editorial Standards · Methodology · Affiliate Disclosure

Qualification Threshold Matrix: All 11 ADU Financing Paths

The table below covers the 11 most-used ADU financing paths. These are published program guidelines, not lender overlays — individual lenders may add stricter requirements.

| Product | Min FICO | Max DTI | Equity / LTV | Income docs | ADU rent counts? | Key constraint |

|---|---|---|---|---|---|---|

| HELOC | 620 (680+ best rates) | 43% | 80–85% CLTV cap (current value) | W-2 or 2yr self-employed | No (secondary income only) | Variable rate; draw period ends |

| Fixed home equity loan (HELOAN) | 620 | 43% | 80–85% CLTV cap (current value) | W-2 or 2yr self-employed | No (secondary income only) | Lump sum; no redraw |

| Cash-out refinance | 620 | 45% | 80% LTV cap (current value) | W-2 or 2yr self-employed | Program-specific (not FHA cash-out) | Replaces first mortgage rate |

| Fannie Mae HomeStyle Renovation | 620 | 45% | Up to 75% of after-improved value (renovation costs) | Full conventional docs | Existing ADU only (B3-3.8-01), 30% cap | Plans, GC bid, draw schedule required |

| Freddie Mac CHOICERenovation | 620 | 45% | After-improved value; Freddie LTV matrix | Full conventional docs | Existing ADU only; 30% cap; landlord ed. required | Landlord-education certificate at purchase |

| FHA Standard 203(k) | 580 (500+ with 10% down) | 43–57% with compensating factors | After-improved value; 96.5% LTV (purchase) | FHA standard income docs | To-be-built: 50% of rent; 30% Effective Income cap; not cash-out | HUD consultant, work write-up, FHA MIP |

| Construction-to-permanent | 680+ (typical) | 43–45% | After-improved value; varies by lender | Full docs; 2yr history | Lender-specific | Single close; GC license, draw schedule |

| Conventional purchase w/ ADU rent (Fannie B3-3.8-01) | 620 | 45% | Per Fannie Eligibility Matrix | Full conventional docs | Yes — existing ADU only; 30% cap; purchase or limited cash-out | One ADU only; ADU must be legal |

| DSCR (investor) | 660+ | No personal DTI (DSCR ≥ 1.0–1.25) | 20–25% equity or down payment | Property cash flow (no personal income) | Core qualification metric | Non-owner-occupied; rates above conventional |

| Bank-statement loan | 640–660+ | 43–50% | Typically 80–85% LTV/CLTV | 12–24 months business bank statements | Program-specific | Self-employed only; rates above conventional |

| HEI / shared-appreciation | 500–600+ (provider-specific) | Varies; may skip traditional DTI | Equity-primary; no monthly loan payment in some structures | Equity-primary; may not require income docs | Not typically | Share of future appreciation; CFPB risk flag; state availability varies |

Thresholds reflect published program guidelines and are subject to lender overlays. These are not guarantees of approval. Verify current terms directly with a licensed lender.

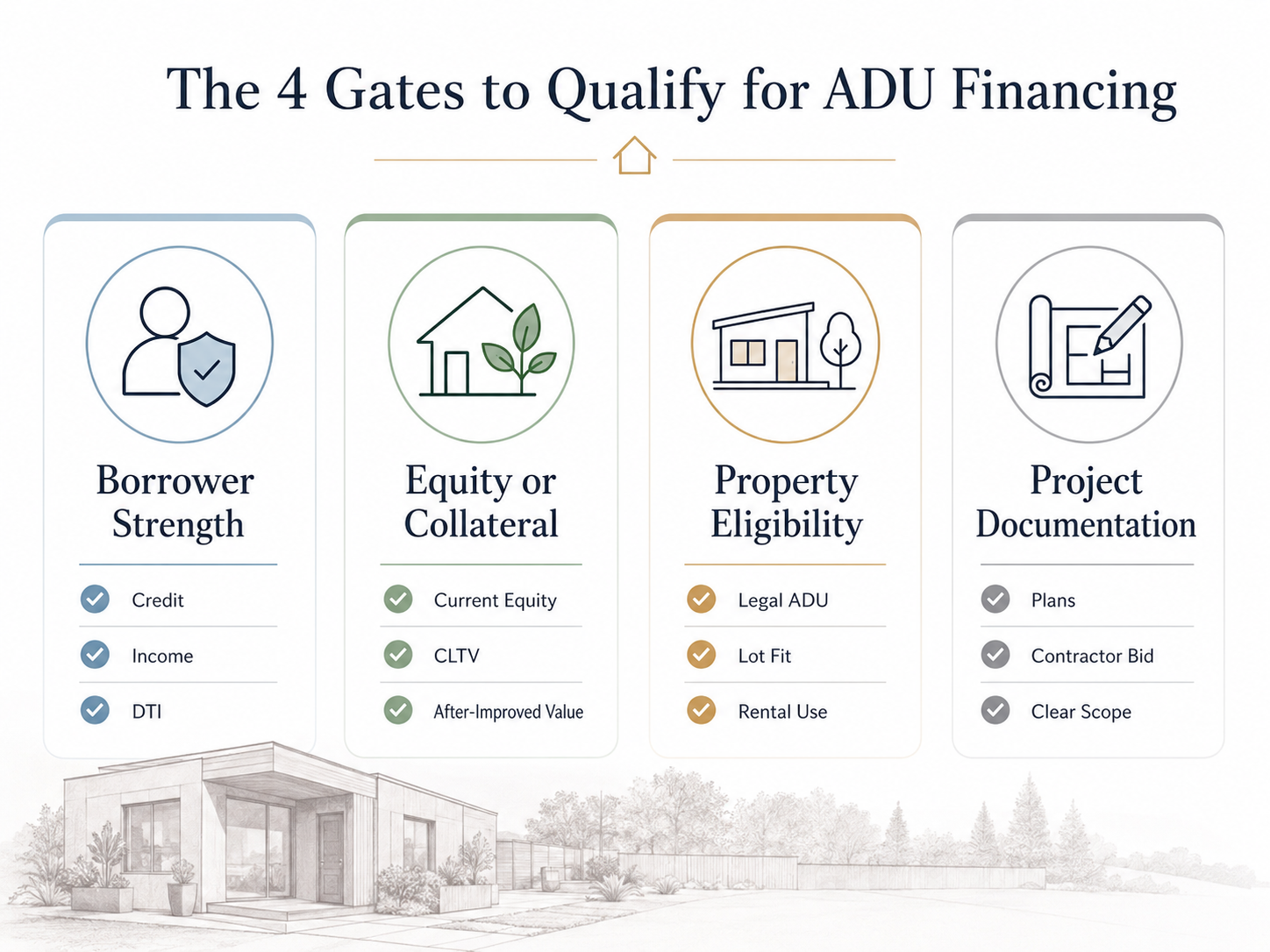

The four gates you must clear simultaneously

You qualify for ADU financing when four gates clear at the same time: borrower strength (credit, income, DTI, reserves), equity or future-value collateral, property eligibility (the ADU is legal or legally permittable), and project documentation (plans, contractor, scope). A strong credit score does not fix an illegal ADU. Enough equity does not fix unsupported income. And a high rent estimate does not help if the loan program does not allow rental income on that loan purpose.

This four-gate model is how lenders actually structure the underwriting file. A loan can pass borrower strength and equity and still fail because the ADU isn't legal on the lot, or because the contractor's bid doesn't break out the work in a way the underwriter can map to a draw schedule.

Gate 1 — Borrower readiness

Across major ADU loan products, typical floors are:

- Credit score: generally 620 minimum, with best rates reserved for 740+. FHA 203(k) accepts 580 with the standard 3.5% down payment, and 500–579 with 10% down. HELOC pricing improves meaningfully at 680 and again at 720.

- Debt-to-income ratio (DTI): typically capped at 43% for most ADU loans, with flexibility up to 45–50% for borrowers with strong compensating factors (large reserves, high credit, low LTV).

- Income documentation: two years of W-2s and 30 days of pay stubs for wage earners; two years of tax returns plus a year-to-date profit-and-loss and 12 months of business bank statements for the self-employed.

- Cash reserves: for construction and renovation loans, lenders typically want 2–6 months of mortgage payments in liquid reserves after closing.

Gate 2 — Equity or future-value collateral

Equity-based products (HELOC, home equity loan, cash-out refinance) underwrite against your home's current appraised value. Renovation and construction products (HomeStyle, CHOICERenovation, FHA 203(k), construction-to-permanent) underwrite against the home's projected value after the ADU is complete.

A homeowner with 8% current equity can still get fully funded — they're using the wrong product if they're trying for a HELOC, but they're a strong candidate for a renovation mortgage that uses after-improved value.

Gate 3 — Property and ADU eligibility

The lot has to legally support the ADU:

- Zoning permits the ADU type (detached, attached, or junior ADU).

- Setbacks, height, and lot-coverage rules can be met by the design.

- Utility laterals (water, sewer, electrical) either exist or can be brought in within budget.

- No HOA covenant or deed restriction effectively prohibits the ADU. In California, Civil Code § 4751 limits HOA and deed-restriction provisions that effectively prohibit or unreasonably restrict ADUs or JADUs on qualifying single-family residential lots, while allowing reasonable restrictions. Other states vary.

- If you're using rental income to qualify, the ADU must be legal, not just physically present. Freddie Mac explicitly prohibits using rental income from an illegal ADU.

Gate 4 — Project and documentation readiness

The gate that surprises homeowners who passed everything else. Lenders need to underwrite the specific project:

- Detailed scope of work or a pre-approved ADU plan

- Licensed general contractor's itemized bid (or, for some renovation loans, an approved consultant's work write-up)

- Expected timeline with draw milestones

- For HUD-related programs, contractor licensing, bonding, and FHA's required forms

- Cost contingency built into the bid (most lenders require 10–20%)

The four-gate scorecard

Run yourself through this before you call a lender:

| Gate | Green light | Caution | Red flag |

|---|---|---|---|

| Borrower | Stable W-2 or 2+ years self-employed, FICO 680+, DTI under 40%, 3+ months reserves | Variable income, FICO 620–679, DTI 40–45%, thin reserves | FICO under 620, DTI over 50%, income can't be documented |

| Equity / collateral | 25%+ equity OR a real plan to use future-value financing | Borderline equity OR future-value path not yet selected | Underwater or zero equity with no construction/renovation product in play |

| Property | ADU is legal under current zoning, no HOA block | Zoning unclear, HOA covenant ambiguous | ADU prohibited, lot can't physically support the build |

| Project | Plans drawn, licensed GC under bid, scope itemized | Rough budget, no contractor yet | No plans, no contractor, no scope |

Green across all four? You're ready to apply. Caution on any one? Fix that gate first — most homeowners can move a single caution to green in 30–90 days. Red flag on any gate? That gate has to resolve before any lender will fund.

What do lenders actually look at first: credit, income, DTI, or equity?

Lenders look at all four, but the order shifts by product. A HELOC or fixed home equity loan starts with current equity and your CLTV cap, then runs DTI, then verifies credit and income. A renovation or construction loan starts with the project — plans, contractor, after-improved appraisal — then verifies borrower strength. A mortgage that's counting ADU rental income to qualify starts with whether the program even allows that income on this loan purpose, then verifies the rent through the appraiser's Form 1007 or Form 1000.

Many homeowners spend time fixing the wrong number. Polishing your FICO from 720 to 740 saves basis points on the rate but doesn't move you from denied to approved if your CLTV is already at 85%. Nudging DTI from 43% to 41% doesn't help if the appraiser can't support the contractor's projected after-improved value.

Qualification factor by loan type

| Factor | HELOC / HELOAN | Cash-out refi | Renovation loan | Construction-to-perm | Conv./FHA w/ ADU rent |

|---|---|---|---|---|---|

| Credit score | Important | Important | Important | Very important | Important |

| DTI | Important | Important | Important | Important | Important |

| Current equity | Very important | Very important | Less central | Less central | Important |

| After-improved value | Less central | Less central | Very important | Very important | Depends |

| ADU legality | Important | Important | Very important | Very important | Critical |

| Rental income / Form 1007 or 1000 | Usually secondary | Program-specific | Program-specific | Lender-specific | Critical |

| Plans, scope, GC | Not required | Not required | Required | Required | Not required |

Why “blended cost” beats the advertised rate

A lender quotes you a rate on the new loan. That isn't the comparison that matters. What matters is the total cost across all your liens combined. Replacing a low-rate first mortgage with a higher-rate cash-out refi to get $200,000 in ADU money often loses to keeping the first mortgage intact and adding a $200,000 second-lien HELOAN, because the blended cost on the latter is lower across your full balance. Model both scenarios in a spreadsheet — current first mortgage rate, proposed cash-out refi rate, proposed second-lien rate, and the blended cost across the combined principal — before signing anything.

How much equity do I really need for ADU financing?

For equity-based products (HELOC, home equity loan, cash-out refinance), you generally need to keep 15–20% equity untouched after the loan closes — meaning your CLTV ends up at 80–85% or lower. For renovation mortgages (HomeStyle, CHOICERenovation, FHA 203(k)) and construction-to-permanent loans, the equity test runs against the home's after-improved value, which can unlock financing even for homeowners with 5–10% current equity. There is no single equity number that fits every ADU loan.

The single most useful formula:

Estimated home value

× lender's allowed CLTV cap (typically 80%–85%)

− current mortgage balance

= estimated borrowing room before fees, overlays, and underwriting

Worked example A — High-equity owner

You bought your home in 2014, it's now worth $800,000, and you owe $250,000.

- $800,000 × 80% CLTV = $640,000 total liens permitted

- $640,000 − $250,000 existing mortgage = $390,000 in equity-product borrowing room

You can fully fund a $300,000 ADU with a single HELOC or home equity loan, keep your existing first mortgage rate, and stay under the 80% CLTV ceiling.

Worked example B — Recent buyer with 12% equity

You bought in late 2024, the home is now worth $700,000, and you owe $616,000 (12% equity).

- $700,000 × 80% CLTV = $560,000

- $560,000 − $616,000 = negative $56,000

You have zero current borrowing room for a HELOC or HELOAN. But an FHA 203(k) Standard or Fannie Mae HomeStyle Renovation underwrites against after-improved value. If a $280,000 detached ADU is projected to raise the appraised value to $1,050,000, the after-improved CLTV math becomes: $1,050,000 × 75% = $787,500 − $616,000 = $171,500 of future-value renovation budget you can finance, plus whatever you bring in cash.

Worked example C — Zero current equity, new construction

You're buying a property and want to build a new detached ADU. Down payment is 5%, current equity is essentially zero. A construction-to-permanent loan or an FHA 203(k) Standard underwrites against the projected post-construction value. The lender requires detailed plans, a licensed GC, a draw schedule, and 10–20% cost contingency. The biggest gating factor isn't your equity — it's whether the appraiser can support the after-improved value the contractor's bid implies.

The “preserving a low first mortgage” question

Many homeowners locked in 30-year fixed rates between 2020 and 2022 at meaningfully below-market rates. A cash-out refinance gives them ADU money but replaces that first mortgage at today's rate. A second-lien HELOC or HELOAN keeps the first mortgage intact at the cost of a higher rate on the second loan. For homeowners with a first mortgage well below today's market rate, second-lien products are usually mathematically superior — even when the HELOAN rate looks higher than the cash-out rate on paper. The blended cost across the entire balance determines the actual lifetime interest expense. Run both scenarios, including the cash-out refi's closing costs (typically 2–5% of the new loan amount), before signing.

Not sure your equity covers the project? Check your property and financing readiness in one step.

Does the ADU have to exist before rental income can count?

It depends on the program. Conventional Fannie Mae rules require an existing ADU. Conventional Freddie Mac's rental-income rule for the subject one-unit primary residence is similarly oriented around an existing ADU on the property at qualification. FHA Standard 203(k) is the main path that allows rental income from a to-be-built ADU to count — at 50% of the lesser of appraiser rent or lease, capped at 30% of total Effective Income. Construction-to-permanent and DSCR lenders set their own rules and vary widely.

| Program | Existing ADU rent? | To-be-built ADU rent? | Loan purpose | Cap on rent | Primary source |

|---|---|---|---|---|---|

| Fannie Mae conventional (B3-3.8-01) | Yes | No — existing ADU on subject property only | Purchase or limited cash-out refi; one-unit principal residence; one ADU only | 30% of total qualifying income; 75% of gross rent | Fannie B3-3.8-01 |

| Freddie Mac (Guide Ch. 5306) | Yes — subject one-unit primary residence | Confirm with lender; structured around existing ADU at qualification | Purchase or no-cash-out refi | 30% of total income; 75% of lease amount | Freddie Guide Ch. 5306 |

| FHA — existing ADU (ML 2023-17) | Yes — 75% of lesser of appraiser rent or lease | n/a | Purchase or rate-and-term refi; not cash-out | 30% of total monthly Effective Income | HUD ML 2023-17 |

| FHA Standard 203(k) — to-be-built ADU (ML 2023-17) | n/a | Yes — 50% of lesser of appraiser rent or lease | Eligible 203(k) renovation scope; not cash-out | 30% of total monthly Effective Income | HUD ML 2023-17; ML 2024-13 |

| FHA cash-out refinance | n/a | Not allowed as Effective Income | Cash-out excluded | n/a | HUD ML 2023-17 |

| HomeStyle / CHOICERenovation | When paired with agency ADU rental-income rule | Conservatively assume no — confirm with lender for specific scenario | Per agency rules | Per agency caps | Fannie B3-3.8-01; Freddie Guide Ch. 5306 |

The clean read: if you need projected rent from an ADU you haven't built yet to qualify, FHA Standard 203(k) is the established path. Conventional Fannie/Freddie rules require an existing ADU. Construction-to-permanent loans are lender-specific — some will count projected ADU rent in their own underwriting, but it isn't a Fannie or Freddie rule and shouldn't be assumed.

Can ADU rental income help me qualify? (The 2025–2026 rule changes, decoded)

Yes — and this is where the most important shift in ADU financing in years happened. As of October 8, 2025, Fannie Mae allows rental income from an existing ADU to count toward qualifying income on a one-unit principal residence (Selling Guide B3-3.8-01) — capped at 30% of total qualifying income, one ADU only, purchase or limited cash-out refinance only. Fannie's Desktop Underwriter version 12.1 picks the rule up automatically on new casefiles submitted on or after the weekend of March 21, 2026. FHA has allowed 75% of an existing ADU's estimated rent (or 50% for a to-be-built ADU under Standard 203(k)) since HUD Mortgagee Letter 2023-17. Freddie Mac follows a similar 30% cap with a landlord-education requirement for purchase borrowers without prior investment property management or ADU rental management experience.

The Fannie Mae rule, decoded

What changed. Before October 8, 2025, conventional Fannie Mae loans on one-unit principal residences could not use ADU rental income to help the borrower qualify. The updated B3-3.8-01 reversed that for existing ADUs:

- Property type: one-unit principal residence with an existing ADU.

- Loan purpose: purchase or limited cash-out refinance only. Standard cash-out refinances are excluded.

- One-ADU limit: even if your property has multiple ADUs, rental income from only one can count.

- The 30% cap: qualifying rental income from the ADU is limited to 30% of total qualifying income (measured against total income used to qualify, not against your non-ADU income).

- Documentation: Schedule E where applicable, current lease or Form 1007/Form 1025 where permitted, and 75% of gross rent when current leases or market rents are used.

The 30% cap math, worked correctly

The 30% cap is measured against your total qualifying income — which includes the ADU rent in the total once it's added.

Example 1: non-ADU income $5,000/month, appraiser supports $2,000/month ADU rent.

- 75% of $2,000 = $1,500 qualifying rent.

- Total qualifying income: $5,000 + $1,500 = $6,500. ADU share = $1,500 / $6,500 = 23%. Under the cap — the full $1,500 counts.

Example 2: non-ADU income $4,000/month, appraiser supports $3,000/month ADU rent.

- 75% of $3,000 = $2,250 program-calculated rent.

- Total: $4,000 + $2,250 = $6,250. ADU share = $2,250 / $6,250 = 36%. Over the 30% cap.

- Maximum ADU income that satisfies the cap: solve rent / (rent + $4,000) ≤ 30% → cap of $1,714/month.

Do not treat the cap as “30% of your non-ADU income” — it's measured against total qualifying income with the ADU rent included in the denominator.

The FHA rule, decoded (Mortgagee Letter 2023-17)

FHA was first. HUD's Mortgagee Letter 2023-17 (case numbers assigned on or after October 31, 2023):

- Existing ADU: 75% of the lesser of the appraiser's fair market rent on Form 1007/1000 or the actual lease amount counts toward qualifying income.

- To-be-built ADU under FHA Standard 203(k): 50% of the lesser of appraiser fair market rent or the lease counts.

- 30% cap: ADU rental income used as Effective Income cannot exceed 30% of total monthly Effective Income.

- Cash-out exclusion: ADU rental income is not allowed as Effective Income on an FHA cash-out refinance.

- Appraisal requirements: appraiser must identify, analyze, and report on the ADU's characteristics, legality, marketability, and estimated rent.

The Freddie Mac rule, decoded — and the landlord-education requirement

Freddie's ADU rental-income provisions for a subject one-unit primary residence parallel Fannie's in most respects: one ADU, 30% cap on total income used to qualify, full appraisal required (no ACE), documented lease rent capped at 75% of lease amount. Loan purpose: purchase or no-cash-out refinance. Appraisal requirements include at least one comparable sale with an ADU, plus at least three rental comps with at least one rented ADU.

The provision that trips applicants: Freddie requires that at least one qualifying borrower participate in a landlord-education program for purchase transactions — unless the borrower has at least one year of investment property management experience or ADU rental management experience. The course typically runs a few hours; the completion certificate is required in the loan file. If a Freddie path is in play, complete the course before the appraisal is ordered.

The USDA proposed rule (Federal Register, March 31, 2026)

On the horizon, not yet active. The USDA Rural Housing Service published a proposed rule on March 31, 2026, that would expand the Single Family Housing Guaranteed Loan Program to allow income-producing ADUs on financed properties. The public comment period is open through June 1, 2026. It is not final as of the publication date of this guide. If you're in a USDA-eligible rural area, this rule is worth tracking. We will update this page within 30 days of any finalization.

Damaging admission — what rental income won't fix

Rental-income inclusion has real ceilings. For a $300,000 detached ADU on a $750,000 home, you might be adding $1,500–$2,500/month of qualifying income — meaningful, but capped at 30% of total qualifying income. If your DTI is already deeply over the program ceiling before any ADU rent, the rule almost never gets you across the line on its own. It pulls borderline files into approval. It doesn't rescue files that are far from the threshold.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

See if ADU rent may matter for your financing path.

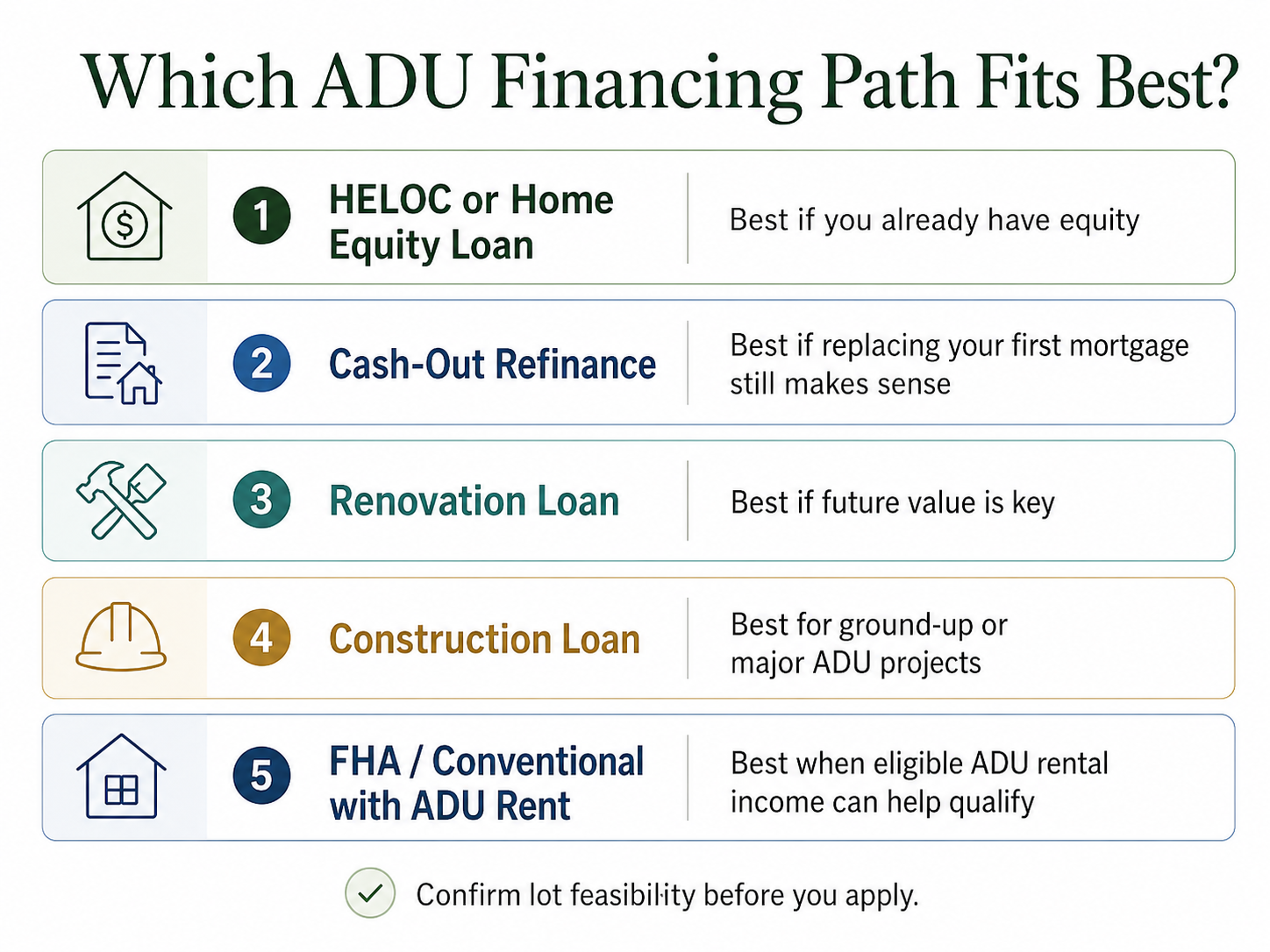

Which ADU financing path is easiest to qualify for?

The easiest path is the one that matches your strongest asset. If your asset is current equity, a HELOC or home equity loan is the cleanest path — typically pre-qualifying with a soft pull, closing in 2–6 weeks. If your asset is income strength but not equity, a renovation mortgage or construction-to-permanent loan unlocks future-value underwriting. If your asset is the property itself (a home you're buying with an existing legal ADU), a conventional purchase or FHA loan with rental income counted may be the strongest fit. If your asset is none of these, a home equity investment may be the only path — at the cost of a share of future appreciation.

| Situation | Path most worth testing first | Why it fits | What to verify before applying |

|---|---|---|---|

| 25%+ equity, first mortgage well below today's market | HELOC or fixed HELOAN | Preserves the low first mortgage; second lien adds the ADU money | CLTV cap, draw schedule, fixed vs. variable rate |

| 25%+ equity, payment certainty wanted | Fixed home equity loan | Predictable monthly payment, no rate risk | Total fees, prepayment penalty terms |

| Current first mortgage at or above today's market | Cash-out refinance | Consolidates into one payment at one rate | Closing costs (commonly 2–5% of new loan), DTI on new payment |

| 5–15% current equity, recent buyer, strong income | HomeStyle, CHOICERenovation, or FHA 203(k) | Future-value underwriting unlocks budget | Plans, GC bid, after-improved appraisal feasibility |

| Buying a home with an existing legal ADU | Conventional or FHA purchase with ADU rent counted | Rental income offsets DTI from day one | Whether the ADU is legal, rent comps, Form 1007 |

| Building new construction with an ADU | Construction-to-permanent | Single close, future-value underwriting | GC license, reserves, draw schedule |

| Self-employed, ADU primarily for rental income | DSCR loan | No traditional personal-income underwriting; property cash flow qualifies | Projected DSCR ratio, prepayment penalties |

| Payment-sensitive | HEI / shared appreciation | No traditional monthly loan payment in some structures | Share of appreciation given up, state availability, term length |

| Zero equity, no future-value product works | Smaller ADU scope (garage conversion, JADU) or wait | The right answer is sometimes "not yet" | Whether the timeline allows waiting |

For product-by-product comparisons with rates, fees, and tradeoffs, see our Best ADU Financing Options 2026 and our ADU Financing Options 2026 (8-path interactive finder). For HELOC specifics, see our HELOC for ADU guide.

A note on HEI (home equity investment) products

Companies like Hometap, Unlock, and Point offer agreements where they give you cash today in exchange for a share of your home's future appreciation. The CFPB has flagged in its Issue Spotlight on home equity contracts that these contracts can involve complex terms, non-standardized disclosures, repayment triggers tied to specified events, and potential forced-sale or foreclosure risk if the homeowner cannot repay at the end of the term. State availability is uneven. If you're considering an HEI, read the full term sheet before signing, model the worst-case scenario across the contract's full term, check availability in your state, and consider a fiduciary financial planner's input.

What can stop an ADU loan approval — and how to fix each one

ADU loans fail for five reasons most of the time: insufficient equity, DTI too high, FICO too low, missing or invalid construction documents, and zoning or permit problems with the lot itself. Each has a specific fix and a realistic timeline. If you were denied between January 2024 and October 2025 because rental income wasn't allowed to help your file, your borrower-and-property profile may be worth re-running under current Fannie rules — especially if it's recreated as a current DU casefile and the property, appraisal, documentation, and loan purpose still qualify.

CFPB HMDA analysis has historically shown HELOC and home equity denial rates materially higher than closed-end mortgage denial rates — not because homeowners are bad credits, but because product-fit and documentation problems are common.

The denial-recovery decision tree

| Denial reason | What it really means | The fix | Realistic timeline | What to do this week |

|---|---|---|---|---|

| Insufficient equity | Your CLTV after the new loan exceeds the lender's cap (typically 80–85%) | Switch to a future-value product (HomeStyle, CHOICERenovation, FHA 203(k), construction-to-permanent) — or wait/pay down for 12–24 months | 0 days (product switch) to 24 months (build equity) | Get re-quoted on a renovation or construction loan instead |

| DTI too high | Monthly debts plus the new loan payment exceed 43–50% of gross income | Pay down highest-utilization revolving balances; consolidate; if eligible, add ADU rental income under current Fannie/FHA/Freddie rules | 30–90 days | Calculate your current DTI; identify the single debt with the biggest monthly payment |

| FICO too low | Score below the product's floor (typically 620, sometimes 580 for FHA) | Dispute reporting errors; lower revolving utilization below 30% (ideally 10%); pause new credit applications | 60–120 days for a meaningful score move; 30 days for utilization corrections | Free soft-pull credit check, then attack the top 1–2 negative items |

| Missing or invalid construction docs | Contractor's bid isn't itemized, contractor isn't licensed, or plans don't match the loan program | Get a CSLB-licensed (or state-equivalent) GC; use a pre-approved ADU plan where the city offers one; itemize the bid to lender spec | 0–60 days | Confirm whether your city offers pre-approved ADU plans |

| Zoning / permit issue | Lot doesn't legally support the ADU | Run a feasibility check before any lender call; revise design if a different ADU type fits | 0–90 days | Run the Feasibility Engine — 60 seconds, no commitment |

| Rental income disallowed by program | You applied on a standard cash-out refi (FHA bars it; Fannie limits to purchase or limited cash-out; Freddie to purchase or no-cash-out) | Re-apply on the right loan purpose: purchase, limited cash-out (Fannie), no-cash-out (Freddie), or 203(k) | 0 days (product switch) | Confirm the loan purpose with a Fannie/Freddie/FHA-experienced lender |

| Appraiser can't support the rent | Appraiser's Form 1007/1000 fair market rent came in lower than the lease, or no ADU comparable rentals in the area | Submit additional rent comps; appeal the appraisal with documented comparables; in some markets, work with a lender who orders a different appraiser | 30–60 days | Pull 3–5 comparable ADU rentals in your zip code |

| Pre-October 2025 Fannie denial that hinged on ADU rental income | Old Fannie rule didn't allow it — your file was on the cusp | Ask whether the file is worth re-running under current B3-3.8-01; a new DU casefile may be required | 0 days — ask your lender | Call the same lender; ask if they have implemented current B3-3.8-01 and DU 12.1 |

Damaging admission — applying repeatedly hurts you

If you've been denied twice in 90 days, applying again immediately compounds the problem. Each hard credit pull drops your FICO by 2–5 points and stays on your report for up to 24 months. The disciplined response is to identify the specific gate that caused the denial, fix that one gate, and re-apply only after the number has moved.

Rate-shopping windows are an exception. Per myFICO and CFPB guidance, multiple mortgage-related inquiries within a focused 14–45 day window are treated as a single inquiry for credit-scoring purposes. Rate-shopping the same product across 3–5 lenders within that window doesn't compound the way separate denied applications do.

Ready to test a real pre-qualification on a national mortgage marketplace?

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Explore ADU financing options through Mortgage Research Center →

Subject to lender approval; credit-pull type, rates, terms, and availability vary by lender and state. Affiliate link — see disclosure above.

What documents do I need before I apply?

Plan for two packets: a borrower packet (income, assets, debts, identity) and an ADU project packet (plans, contractor bid, scope, permits, rent support). A clean digital package reduces back-and-forth; missing documents are a common delay point. Self-employed borrowers add two years of tax returns and a year-to-date P&L. Borrowers using ADU rental income add Form 1007 (or Form 1000) and either a lease or comparable rent schedule.

The borrower packet

- Government-issued photo ID

- The last 30 days of pay stubs (W-2 employees)

- The most recent two years of W-2s (W-2 employees)

- The most recent two years of federal tax returns, including all schedules (anyone using rental income, self-employment income, or 1099 income)

- A year-to-date profit-and-loss statement (self-employed)

- The most recent 12 months of business bank statements (self-employed or bank-statement loan applicants)

- The last two months of personal bank statements

- Retirement, brokerage, and investment account statements (for reserves)

- The most recent mortgage statement

- Property tax statement and homeowner's insurance declaration page

- A complete list of monthly debt payments (credit cards, auto loans, student loans, child support, alimony)

- HOA dues statement, if applicable

The ADU project packet

- Full property address and parcel number

- ADU type designation — detached ADU (DADU) is a standalone structure; attached ADU shares one or more walls with the main house; junior ADU (JADU) is a California-specific category, generally up to 500 square feet of interior livable space, created within or attached to the primary dwelling

- Preliminary zoning and permit feasibility confirmation

- Final or near-final floor plan and site plan (or the pre-approved plan number if your city offers one)

- Licensed general contractor's itemized bid (or consultant's work write-up for 203(k))

- Contractor license verification (CSLB number in California, equivalent state license elsewhere)

- Contractor liability and workers' compensation insurance certificates

- Project timeline with draw milestones

- Utility lateral status — the underground connections from the public utility lines in the street to your structure (water, sewer, electrical, gas). New laterals can materially increase project cost. Verify assumptions with the local utility and your contractor before finalizing financing.

- Cost contingency (most lenders require 10–20% above the contractor bid)

The rental-income packet (only if you're using ADU rent to qualify)

- An executed lease (if the ADU already exists and is currently rented)

- Schedule E from the most recent two years of tax returns (if rental history exists)

- Form 1007 (Fannie Mae Single-Family Comparable Rent Schedule) or Form 1000 (Freddie Mac equivalent) — the appraiser completes this and supports market rent with three or more comparable rentals

- For Fannie or Freddie loans counting ADU rent: at least one ADU comparable sale included in the appraisal

- For Freddie Mac purchase borrowers: landlord-education completion certificate (unless one year of prior investment property management experience or ADU rental management experience is documented)

Most ADU loan files stall not on borrower income but on a missing comparable rental, an appraiser who didn't include the right addendum, or a contractor bid that doesn't break out site work from construction. Get the project packet to the lender at the same time as the borrower packet, and the file moves at lender speed instead of homeowner speed.

Want this as a take-along reference before your first lender call?

Download the free 2026 ADU Starter Kit →

Qualification thresholds, document checklist, denial-recovery framework, and city-by-city permit timelines. No spam.

Should I talk to a lender before or after permits?

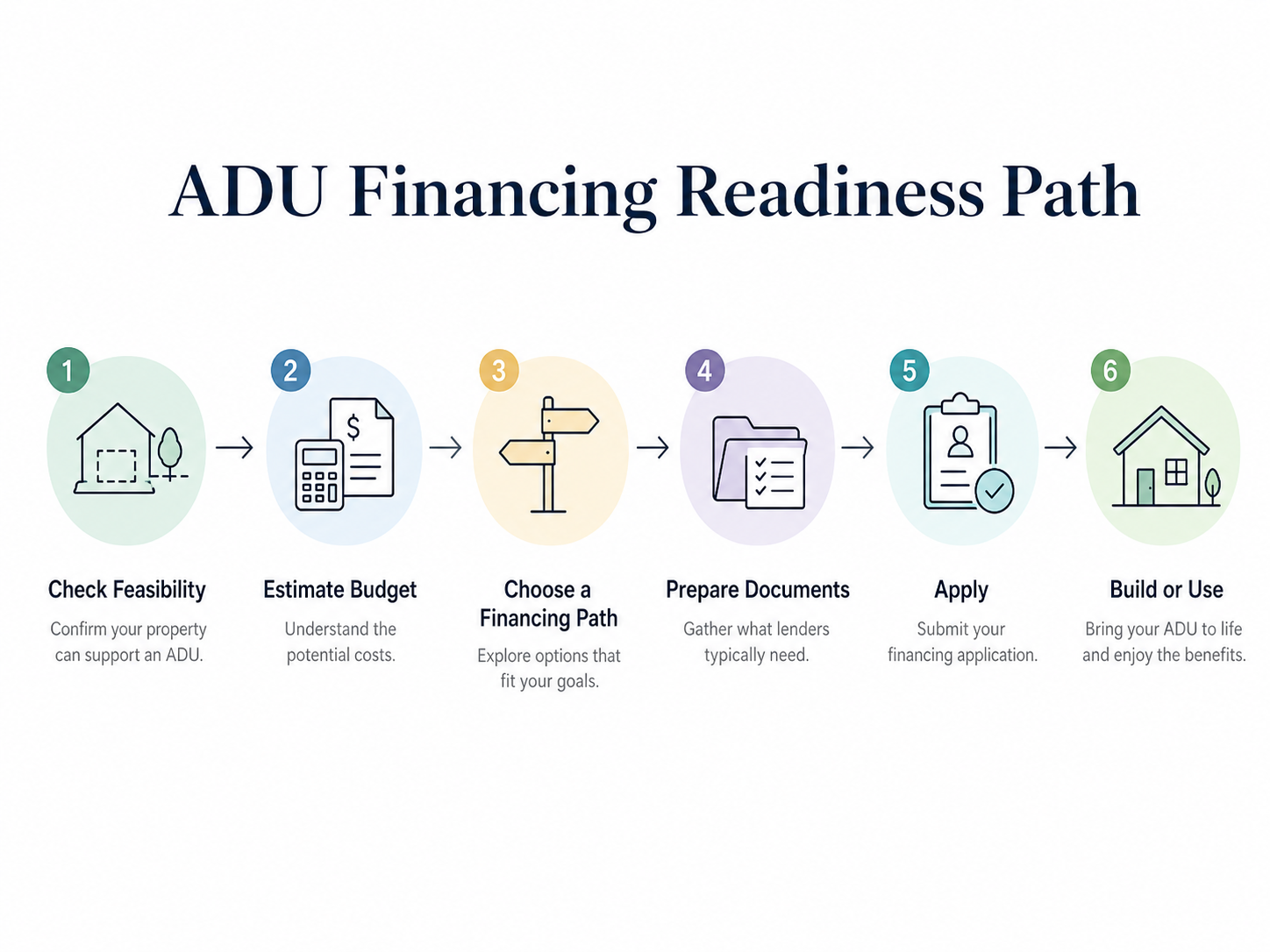

Talk to a lender after a basic feasibility and budget check, but before you spend heavily on final architectural plans or pay permit fees. Most lenders need rough scope, a preliminary bid, and a feasibility-confirmed property — they do not need an issued permit at application. However, FHA 203(k) and construction-to-permanent loans typically require an approved permit application or issued permit before construction funds are released.

The sequence that minimizes wasted spending:

- Confirm basic ADU feasibility on the lot. Free 60-second check using a Dwelling Index property report or your city's online ADU eligibility tool.

- Estimate the rough ADU budget. Use our ADU cost per square foot guide or how much does an ADU cost overview.

- Calculate your equity and DTI. Use the formula in the equity section above. Pull a free soft-check FICO.

- Pre-qualify with one national lender and one local credit union. Soft pull where available. Compare.

- Hire a designer or select pre-approved plans. Several California cities now offer pre-approved or pre-reviewed plans that compress permit timelines and reduce design cost.

- Get 2–3 licensed contractor bids. Itemized. Side by side. Same scope, same finishes.

- Submit your permit application. Your designer or GC typically handles this.

- Close the loan and start draws. For renovation and construction loans, the lender controls the draw schedule and orders inspections at each milestone.

For FHA 203(k) specifically, the process adds a HUD-approved consultant (for Standard 203(k)), a formal work write-up, lender-controlled escrow for rehabilitation funds, and inspections tied to draw releases. This isn't a flaw of the program — it's why the program works for low-equity borrowers — but it's why starting the lender conversation early helps you understand the program's flow before committing.

Qualifying when you're self-employed, retired, or building primarily for rental income

Self-employed, retired, and rental-focused homeowners can qualify for ADU financing — but the documentation burden is heavier and the products that work are narrower. Self-employed borrowers typically provide two years of tax returns plus a year-to-date P&L and 12 months of business bank statements. Retired borrowers qualify on pension, Social Security, IRA distributions, and asset depletion. Investor borrowers building specifically for rental can use DSCR loans that ignore traditional personal-income underwriting and qualify on the property's projected cash flow vs. debt service.

Self-employed homeowners

The challenge isn't your income — it's that your tax returns may understate what you actually earn. Aggressive write-offs (Section 179, home-office deduction, vehicle depreciation) reduce your AGI, which is what the lender uses. Two approaches help:

- Bank-statement loans. These use 12 or 24 months of business deposits instead of tax returns. Rates are typically higher than conventional but qualifying income is often dramatically higher.

- DSCR (debt service coverage ratio) loans. Designed for real estate investors. The lender uses the property's projected cash flow vs. debt service rather than traditional personal-income underwriting. Typical thresholds: a DSCR ratio of 1.0–1.25, 660+ FICO, 20–25% equity or down payment. DSCR rates typically run above conventional rates, but the qualifying logic is fundamentally different — often the only path for high-write-off self-employed borrowers.

Retired homeowners

Lenders can qualify retirement and asset income through several documented paths:

- Social Security and pension income — recurring, reliable, documented through award letters and 1099-SSAs.

- IRA and 401(k) distributions — recurring distributions can count as ongoing income; lump-sum withdrawals generally cannot.

- Asset depletion — for borrowers with substantial liquid retirement assets but limited monthly income. A $1.2 million portfolio depletes to roughly $3,300/month of qualifying income on a standard 360-month formula.

A specific note for retired ADU builders: variable-rate HELOCs and HEI products with appreciation-share triggers can be the wrong product for a fixed-income retiree. Model the worst-case payment scenario before signing.

Building primarily for rental income

If the ADU is fundamentally an investment, three paths work better than conventional ones:

- DSCR loan — qualifies on projected property cash flow.

- Fannie Mae HomeStyle Renovation with ADU rent counted — under B3-3.8-01, the conventional ADU rental-income rule applies on a one-unit principal residence with an existing ADU. If you plan to rent the main house, the property classification shifts — talk to a lender experienced in two-to-four-unit treatment.

- Conventional purchase of a property with an existing ADU — the cleanest qualifying scenario under the current Fannie rule.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

What to do if you don't qualify yet (the 30/60/90/180-day plans)

“Not yet” is not the same as “no.” Most ADU financing problems fall into one of five categories — equity, DTI, credit, property, or documentation — and each has a typical remediation window between 30 and 180 days. The right answer for many homeowners is to fix one specific gate and re-apply, not to give up on the project or pick a worse product.

The 30-day plan (fast fixes)

- Reduce revolving credit utilization. Pay credit card balances down below 30% of their limits (10% is ideal). Most issuers report balances on the statement closing date; a payment posted before that date shows on the next month's score.

- Dispute credit-report errors. Wrong addresses, paid-off accounts still showing balances, identity-mix errors. A successful dispute can lift a score 10–30 points in a single cycle.

- Get itemized contractor bids. Most “vague budget” denials clear with a properly itemized scope — separating site work, foundation, framing, finishes, and utility laterals.

- Switch loan products. If equity is the block, request a re-quote on a renovation or construction product instead.

The 60–90 day plan

- Pay off a small installment loan. Reduces DTI by removing a monthly payment. Confirm credit-score impact before closing the account — closing a long-held account can shorten your average credit-age.

- Wait out a hard inquiry. Inquiries lose most of their score impact within 6 months, even though they remain on the report for 24.

- Complete a landlord-education course. Required for Freddie Mac purchase borrowers using ADU rental income without one year of investment property management experience.

- Build reserves. Construction and renovation loans typically want 2–6 months of liquid reserves after closing. Divert 60–90 days of income into reserves before applying.

The 6-month plan

- Build current equity. Additional principal payments are the only equity source in a flat market. In a rising market, time plus appreciation does some of the work.

- Repair credit through positive history. New positive payment history layered over old negatives can move a score meaningfully over 4–6 months of disciplined behavior.

- Resolve a zoning or HOA issue. Some restrictions can be appealed, varianced, or invalidated under state law. In California, Civil Code § 4751 limits HOA/deed restrictions that effectively prohibit or unreasonably restrict ADUs/JADUs on qualifying single-family lots.

When the answer is “build a smaller project”

A garage conversion ADU or a JADU (in California, up to 500 square feet of interior livable space, created within or attached to the primary dwelling) costs a fraction of a detached new build. In many markets, a converted garage ADU rents for two-thirds to three-quarters of what a new detached ADU rents for in the same zip code — at a fraction of the build cost. Sometimes the right financial answer isn't a bigger loan but a smaller project that funds easily with what you already have.

ADU grants — do you actually qualify, and should you wait?

Most homeowners should not plan around grants. CalHFA's $40,000 ADU Grant Program has been fully allocated since December 28, 2023, with no confirmed reopening date — and CalHFA has warned that anyone claiming to help you access the grant is running a scam. A handful of city and state programs remain active (New York's Plus One ADU Program; Vermont's VHIP 2.0; Boston offers ADU soft-cost grants plus a separate ADU loan; Portland offers ADU system development charge waivers tied to non-short-term-rental use), but the typical homeowner builds with home equity products and renovation loans, not grants.

While statewide California funding is exhausted, ADUs are still being built every day. The financing ecosystem is more accessible than it's been in two decades. The October 2025 Fannie Mae rule alone has materially expanded who can qualify on existing properties. The right move isn't to wait for a grant that may not reopen — it's to pre-qualify for the right product, fix any gates blocking you, and start the build.

We maintain a verified tracker of every active ADU grant program with status badges and verification dates at ADU Grants 2026. If a grant fits your situation, apply — but build the financing plan that funds 100% of the project without it.

Whether or not a grant fits, the qualification path starts the same way.

Honest tradeoffs and edge cases

What if I have an illegal or unpermitted ADU already?

You can still finance a primary mortgage on the property in most cases, but rental income from an illegal ADU cannot be used to qualify. Freddie Mac explicitly prohibits it; Fannie Mae's rules effectively prohibit it through the legality requirement; FHA appraisal protocols flag it. The fix is to legalize the existing ADU through a city legalization process, then re-apply. In California, AB 2533 creates a legalization pathway for certain unpermitted ADUs/JADUs constructed before January 1, 2020, subject to health-and-safety and substandard-building limits and local implementation. See the relevant city-specific guides for local procedures.

What if I have multiple ADUs?

Conventional Fannie Mae rules count rental income from only one ADU, even if multiple ADUs exist. Freddie Mac is similar. FHA's rules vary by property classification. If you have two ADUs and need both rents to qualify, you're likely outside conventional and FHA — talk to a portfolio lender or a DSCR specialist. California's AB 1033 authorizes separate conveyance of ADUs as condominiums only where the local agency has adopted an implementing ordinance (opt-in by jurisdiction); where active, it can change the financing math for some investors. Confirm whether your city has opted in.

What if I'm in a coastal zone, fire-risk zone, or HOA-restricted property?

These add overlays, not absolute blocks. A California coastal-zone ADU may still require a Coastal Development Permit. AB 462 (chaptered 2025) sets 60-day processing deadlines for completed ADU coastal development permit applications, but coastal-zone eligibility still depends on the local coastal program, Coastal Commission jurisdiction, and site conditions. WUI (Wildland-Urban Interface) fire zones add construction-cost overlays for fire-resistant construction — verify with your local building department and contractor. HOA restrictions are increasingly limited by state law (in California, Civil Code § 4751), but limits and exceptions vary. Our coastal zone ADU guides and city-specific law guides cover these overlays in detail.

What if rates move materially before I close?

Rate locks are the answer. Most ADU loan products offer 30–60 day rate locks at application, with extension options at additional cost. Float-down provisions exist on some products. If rates are moving fast, lock at application and pay the extension fee if needed — the lock typically costs less than a meaningful rate swing during your closing window.

Frequently asked questions

Do I need 20% equity to build an ADU?

Not for every loan. Equity-based products (HELOC, home equity loan, cash-out refinance) generally require you to keep 15–20% equity untouched after the loan closes — a CLTV ceiling of 80–85%. But renovation mortgages (HomeStyle, CHOICERenovation, FHA 203(k)) and construction-to-permanent loans underwrite against the home's after-improved value, so homeowners with 5–10% current equity often qualify when matched to the right product. The short version: 20% equity makes the equity-based path easy. Less than that means a different product, not no product.

What's the minimum credit score for an ADU loan?

Product-specific floors are 620 for most conventional HELOCs, home equity loans, and renovation mortgages; 580 for FHA 203(k) with 3.5% down (500–579 with 10% down); typically 660+ for DSCR loans; and 680+ for the cleanest construction-to-permanent terms. Best pricing on most products starts at 720–740. Lenders may add overlays to these floors.

Can I use FHA financing to build an ADU?

Yes. FHA Standard 203(k) is the FHA renovation path for eligible ADU work — including adding an ADU attached to an existing structure, converting a one-family structure to include an ADU, or renovating an existing attached or detached ADU. Confirm detached new-build scope with an FHA/203(k)-experienced lender before assuming eligibility. Under HUD ML 2023-17, FHA Standard 203(k) allows 50% of the lesser of appraiser fair market rent or lease for a to-be-built ADU to count toward Effective Income, capped at 30% of total Effective Income, and not for cash-out refinance. FHA 203(k) Limited is for minor nonstructural repairs only and caps total rehab at $75,000 — not the typical path for new ADU construction.

Can I qualify for an ADU loan if I'm self-employed?

Yes. The standard documentation path is two years of federal tax returns (including all schedules), a year-to-date profit-and-loss statement, and 12 months of business bank statements. If your tax returns show meaningfully lower income than your actual cash flow due to write-offs, two alternatives unlock the deal: a bank-statement loan (qualifies on business deposits) or a DSCR loan (qualifies on the property's projected cash flow vs. debt service, with no traditional personal-income underwriting).

Do I need permits before I apply for ADU financing?

Usually not at application, but yes before construction draws begin. HELOC and home equity loan products don't require ADU-specific permits at any point — they're secured by your existing home equity. Renovation and construction loans generally accept an application before permits are issued but require an approved permit application or issued permit before the loan funds for the construction phase.

Can I count ADU rental income before the ADU is even built?

Yes, on FHA Standard 203(k) for a to-be-built ADU: 50% of the lesser of appraiser rent or lease counts, capped at 30% of total Effective Income, not for cash-out. Under conventional Fannie Mae rules (B3-3.8-01), ADU rental income is for an existing ADU; do not assume a brand-new to-be-built ADU's projected rent counts on a Fannie HomeStyle Renovation unless the lender confirms current eligibility for that specific scenario. Freddie Mac's subject-property ADU rental-income rule is similarly oriented around an ADU on the property at qualification. Construction-to-permanent lenders set their own rules and vary.

What's the difference between a HELOC and a home equity loan for an ADU?

A HELOC is a revolving line of credit with a variable interest rate and a draw period (typically 10 years) during which you can borrow as needed. A fixed home equity loan delivers a lump sum at closing with a fixed interest rate and a fixed repayment schedule (typically 10–30 years). HELOCs offer flexibility for staged ADU construction; home equity loans offer payment certainty. Qualifying requirements are similar (620+ FICO, 80–85% CLTV cap, sub-43% DTI), but HELOC pricing generally requires a higher FICO (680+ for best rates, 720+ for top tier) than fixed home equity loans (620 floor).

Can I qualify with a co-borrower?

Yes. A co-borrower's income, assets, and credit are evaluated alongside yours. Adding a co-borrower with strong income or credit can move a borderline file to approval. The co-borrower takes on equal legal responsibility for the loan, including the property as collateral on secured products.

Are there ADU loans that skip the income check entirely?

Yes, in a narrow set of products: DSCR loans (qualify on property cash flow), HEI / shared-appreciation agreements (qualify primarily on equity, may not use traditional DTI underwriting; provider-specific terms vary), and asset-depletion loans for high-asset, low-monthly-income borrowers. Each has tradeoffs.

How long does ADU loan approval take?

Typical, not guaranteed: HELOCs and home equity loans close in 2–6 weeks from application. Cash-out refinances close in 30–45 days. Renovation loans (HomeStyle, CHOICERenovation, FHA 203(k)) typically take 45–90 days due to consultant and work-write-up requirements. Construction-to-permanent loans run 45–75 days. Each can stretch if documentation gaps appear mid-process.

Was my pre-October 2025 denial reversible under the new Fannie Mae rule?

If your prior denial was on a one-unit principal residence purchase or limited cash-out refinance with an existing ADU, and the denial was driven by your DTI being just out of range when ADU rental income wasn't allowed to help — yes, the file may be worth re-running under current B3-3.8-01. DU 12.1 applies to new DU casefiles submitted on or after the weekend of March 21, 2026; if your old casefile was DU 12.0, a new casefile may be required. Updated documentation, appraisal, loan purpose, property legality, borrower profile, and lender overlays still control.

Is the CalHFA $40K ADU grant still available in 2026?

No. CalHFA's ADU Grant Program has been fully allocated since December 28, 2023, with no confirmed reopening date. CalHFA has posted warnings that anyone claiming to help you access the grant is running a scam. Monitor CalHFA's official ADU page for updates. See our ADU Grants tracker for the full list of currently open programs nationwide.

What if I'm denied — can I apply again right away?

You can, but applying again within 90 days adds a second hard inquiry (each typically drops FICO by 2–5 points) without fixing the underlying problem. The disciplined response is to identify the specific gate that caused the denial (equity, DTI, FICO, docs, or property), fix it, and re-apply once the number has moved. Per myFICO and CFPB guidance, rate-shopping the same mortgage product across multiple lenders within a focused 14–45 day window is treated as a single inquiry for credit-scoring purposes and doesn't compound the way separate denied applications do.

What to do this week, this month, and this quarter

This week

- Run the free Feasibility Engine to confirm your lot supports the ADU you have in mind.

- Pull your FICO via a soft-check service.

- Calculate your current CLTV and DTI using the formulas in this guide.

- Identify which row of the qualification matrix you fit today.

This month

- Match yourself to one financing product family based on your matrix row.

- If you qualify cleanly, request soft-pull pre-qualifications from one national lender and one local credit union. Compare.

- If you don't qualify on your target product, identify the single gate that's blocking you and start the 30/60/90/180-day fix.

- Begin gathering the borrower document packet — you'll need it whether you apply this month or next quarter.

This quarter

- Execute the fix on the blocking gate (debt paydown, credit repair, product switch, property legalization, or contractor bid revision).

- Re-test against the qualification matrix.

- For many homeowners, 90–180 days of focused work moves a denied file to a clean re-application.

Methodology

We built this page by separating three categories of source:

Official agency rules (primary sources, cited inline):

- Fannie Mae Selling Guide B3-3.8-01 (Rental Income, effective October 8, 2025) and B5-3.2-02 (HomeStyle Renovation eligibility)

- Fannie Mae Desktop Underwriter version 12.1 release notes (weekend of March 21, 2026)

- Freddie Mac Seller/Servicer Guide Chapter 5306

- HUD Mortgagee Letter 2023-17 (case numbers on or after October 31, 2023) and ML 2024-13

- FHA Single Family Housing Policy Handbook 4000.1

- USDA Rural Housing Service proposed rule, Federal Register, March 31, 2026 (comment period open through June 1, 2026)

- CalHFA ADU Grant Program status page (fully allocated December 28, 2023)

- CFPB Issue Spotlight on Home Equity Contracts

- myFICO and CFPB guidance on credit inquiries and rate-shopping windows

Market verification:

FICO floors and DTI caps verified against current lender rate sheets and published program guidelines for each product type. Lender-specific overlays are not reported here — overlays vary and can be stricter than published agency floors.

What we did not include:

Unpublished lender overlays; products with no primary-source documentation; state-specific programs outside the listed examples; any data sourced from marketing materials rather than guidelines or primary agency documents.

For editorial standards and update policies, see our Editorial Standards page.

Related guides on The Dwelling Index

- Best ADU Financing Options 2026: 7 Loan Paths Compared — product-by-product comparison with rates, fees, and tradeoffs

- ADU Financing Options 2026: 8 Paths Compared (Free Finder) — interactive financing-path finder

- HELOC for ADU: Deep Dive — HELOC product specifics

- ADU Grants 2026: Verified Programs by State — current open grant programs

- How Much Does an ADU Cost? — 2026 cost ranges by type and region

- ADU Cost Per Square Foot in 2026 — by ADU type and state

- What Is an ADU? — definitional guide for early-stage researchers

Not sure where to start? See what's possible at your address — get your free ADU report in 60 seconds.

Run your free ADU Feasibility Report →