Best ADU Financing Options in 2026: The 7 Paths, Real Rules, and Which One Fits

By The Dwelling Index Editorial Team · Last verified · Last updated · Editorial standards →

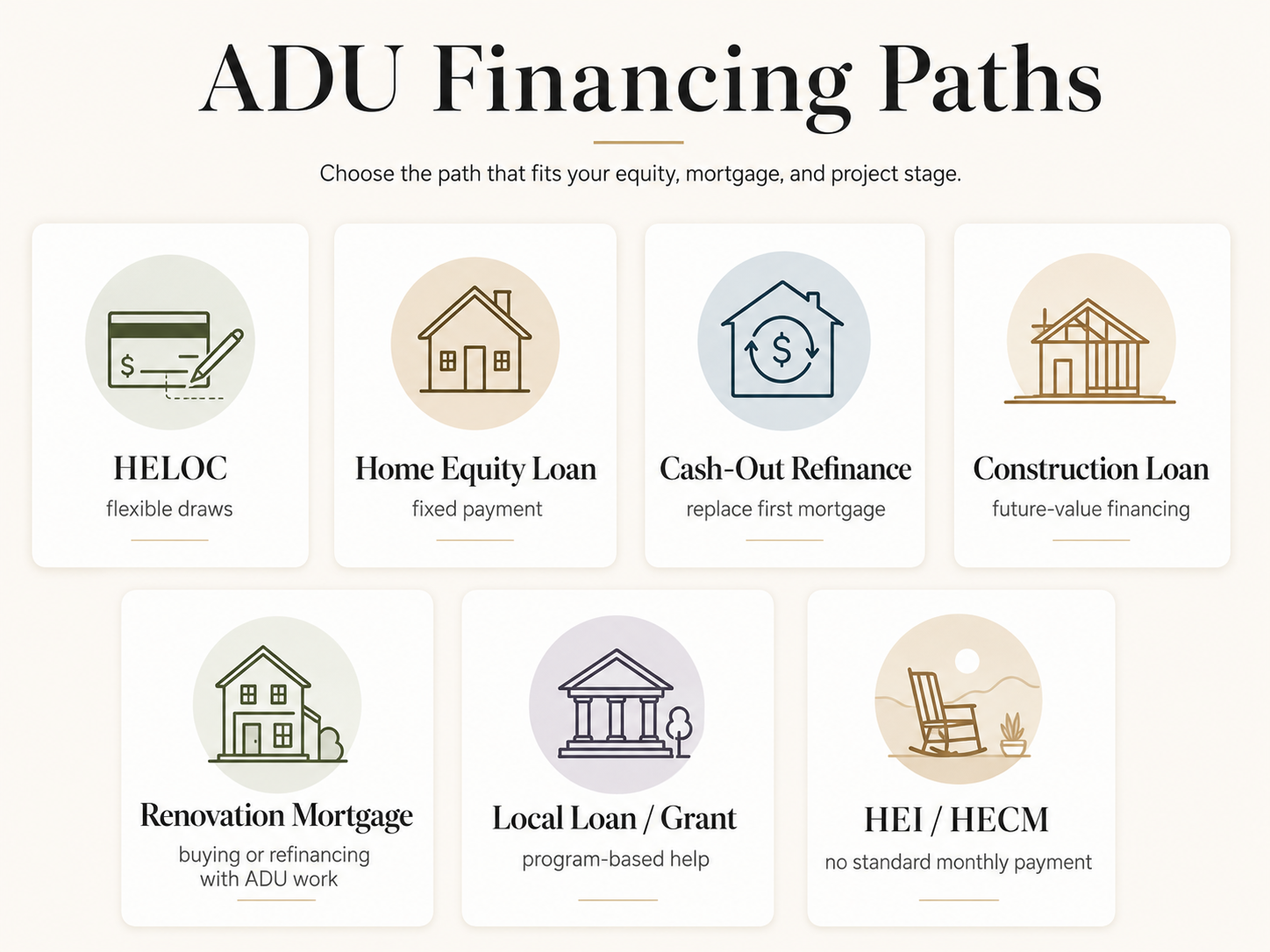

The best ADU financing options in 2026 split into seven paths, and the right one for you depends on three variables: how much equity you have, what your current first-mortgage rate is, and what kind of ADU you’re building. If you have meaningful equity and a first-mortgage rate well below the mid-6% benchmark that Freddie Mac’s Primary Mortgage Market Survey reported for May 14, 2026,4 a HELOC or home equity loan keeps that rate intact while funding the build. If you don’t have enough current equity, a construction loan or one of three renovation mortgages — Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, or FHA 203(k) — can underwrite against the home’s value after the ADU is built. Skip a cash-out refinance unless your existing rate is already at or above today’s market. Grants exist in a handful of states and cities, but most are local, income-restricted, or fully allocated. Confirm your lot is actually buildable before calling any lender.

Best ADU Financing Option by Situation (May 2026)

| Your situation | First path to test | Why it fits | Avoid if | Verification needed |

|---|---|---|---|---|

| Strong equity, low first-mortgage rate | HELOC or fixed home equity loan | Keeps the first mortgage intact; funds the ADU as a second lien | You can’t tolerate variable-rate exposure (HELOC only) | Current equity, CLTV cap, draw schedule, rate type |

| Strong equity, want payment certainty | Fixed home equity loan | Predictable payment; no rate risk | Your ADU budget is fluid or staged | Final budget, contingency, contractor draw schedule |

| Current first-mortgage rate is at or above today’s market | Cash-out refinance | Consolidates into one payment | You’d give up a sub-5% rate | Blended-cost comparison vs. second-lien option |

| Low current equity but completed ADU adds value | Construction-to-permanent loan | Underwrites against future value | You can’t supply plans, bids, permits, contractor docs | Plans, bids, permits, builder license, draw schedule |

| Buying or refinancing while adding an ADU | Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, or FHA 203(k) | Bundles purchase/refi + renovation in one loan | You need to keep a low existing rate | Program-specific eligibility and rental-income rules |

| Want no required monthly payment | Home equity investment (HEI) or HECM if 62+ | No standard monthly payment | You don’t have an exit plan in 10–30 years | State availability, term sheet, share of appreciation |

| You’re in a city or state with an active program | Local loan, grant, or fee waiver | Reduces total borrowing | You can’t accept income or rent restrictions | Program status, eligibility, deed covenant terms |

Sources: Fannie Mae Selling Guide B5-3.2 and SEL-2025-10; Freddie Mac Guide Section 5601.2, Bulletin 2025-15, and Bulletin 2026-1; HUD Mortgagee Letters 2023-17 and 2024-13; Curinos / Yahoo Finance and Bankrate national rate surveys (May 2026). See full source list at the bottom →

Before you compare loans, make sure the ADU is actually buildable on your lot.

See what you can build at your address — get your free ADU report in 60 seconds →Which of the 7 best ADU financing options fits your situation?

There is no single “best” ADU financing option. The best path is the one that funds the build without creating a bigger financial problem — and that depends on four variables: usable equity, your current first-mortgage rate, whether the loan can use the ADU’s completed value, and whether rental income or a local program can offset the borrowing.

Researchers at the Terner Center for Housing Innovation at UC Berkeley have documented that second-lien products — HELOCs and fixed home equity loans — are the most common mortgage method among California homeowners who have built ADUs.1 That’s the most predictable path when equity is available. When equity isn’t available, the picture changes completely.

We narrow your decision in four steps:

- Do you have at least 20–25% equity in your home today? If yes, equity-based products are usually the cleanest start. If no, jump to step 3.

- Is your current mortgage rate well below the mid-6% benchmark? If yes, keep it. Use a HELOC or fixed home equity loan that sits as a second lien. If no, consider a cash-out refinance.

- Do you have a defined ADU plan, budget, contractor, and permits? If yes, a construction loan or renovation mortgage can underwrite against your home’s completed value, which is how lower-equity homeowners actually get to “fully funded.”

- Are you in a city or state with an active ADU program? Many programs have meaningful gap funding, but most are local, restricted, and limited. Check the program tracker below before banking on one.

If you can’t answer any of these — particularly whether your lot can even legally support the ADU you’re imagining — that’s the place to start, not a lender call.

Skip the guessing.

Get your free ADU report — see what’s possible at your address →Should you keep your current mortgage or replace it?

If your existing first mortgage is meaningfully below the mid-6% benchmark, protecting it is usually more important than chasing the lowest-advertised ADU loan rate. A HELOC or fixed home equity loan can leave the first mortgage alone. A cash-out refinance replaces it entirely. That single choice often costs or saves more than the rate on the ADU money itself.

Why “blended cost” matters more than advertised rate

A loan officer will quote you a rate on the new product. That’s not the comparison that matters. What matters is the total interest you’ll pay across the full debt stack — existing mortgage plus any new financing — over the realistic time you’ll hold the debt.

A simplified example with verified May 2026 rate context:

- Existing mortgage: $400,000 balance at 3.25% (locked in 2020–2021)

- ADU budget: $250,000

- Option A — Keep the first mortgage, add a second-lien HELOC at ~7.25%. Curinos’s national HELOC average was 7.21% on May 17, 2026 (the 30-day low was 7.19% in mid-March);2 Bankrate’s national survey reported 7.26% on May 6, 2026.3 Your first mortgage’s 3.25% rate stays intact on the $400,000. You pay ~7.25% on the $250,000 ADU money only.

- Option B — Cash-out refinance into one $650,000 loan at ~6.50%. With 30-year first-mortgage rates in the mid-6% range — Freddie Mac’s PMMS showed 6.36% on May 14, 20264 — a cash-out tier typically sits 25–75 basis points higher. You now pay roughly 6.50% on the entire $650,000, including the $400,000 you used to pay only 3.25% on.

For most owners who locked sub-5% rates between 2020 and 2022, the math of Option B is far worse than the headline rate suggests. The 3.25-point spread on $400,000 over the remaining mortgage term is real money. We’ve seen homeowners come out meaningfully ahead by keeping a HELOC versus accepting a “lower” cash-out refinance rate.

This is the most expensive decision in ADU financing. Ask every lender for a side-by-side comparison of total debt-stack interest over the remaining term, not just monthly payment.

When a cash-out refinance still wins

It’s not always wrong. A cash-out refi can be the right answer when:

- Your existing rate is already at or above today’s mid-6% market (e.g., you bought in late 2023 or 2024 at 7%+)

- Your remaining balance is small (under ~$150,000), so the cost of replacing it is limited

- You want one payment and one closing

- You qualify for a meaningfully better rate than your current one

Most cash-out refinances allow borrowing up to roughly 80% of current home value, capped by your lender’s combined loan-to-value (CLTV) rules.5

The rate-lock trap

We see this routinely. A homeowner with a sub-4% first mortgage assumes the only way to access a six-figure ADU budget is to refinance. The lender quotes them a cash-out refi. The monthly payment looks manageable. They sign. A year later, after rates haven’t moved meaningfully, they realize they’ve replaced a generational asset — their low-rate mortgage — to fund a project a second-lien product could have covered.

Ask every lender for a side-by-side debt-stack comparison. Compare APR, not just rate. Compare total interest over the remaining term, not just year-one payments.

If you want to compare mortgage-backed ADU financing across multiple lenders without making each call yourself, our financing-lane partner Mortgage Research Center connects homeowners to lenders for cash-out refi, construction, and renovation loans.

Compare mortgage-backed ADU financing paths →Dwelling Index is reader-supported. We may earn a commission when you use this link. Approval, rate, and terms depend on lender underwriting, credit, income, and property details and are not guaranteed.

How much equity do you need to finance an ADU?

For current-value lending (HELOC, home equity loan, cash-out refi), you typically need at least 15–20% equity above your existing mortgage to access meaningful funds. For after-completion lending (construction loan, renovation mortgage), you may be able to qualify with little or no current equity because the lender appraises your home based on its projected value with the ADU already built.

The simple usable-equity formula

Most lenders cap second-lien CLTV around 80–85% of current home value:

(Home value × max CLTV %) − Existing mortgage balance = Available second-lien equity

A worked example assuming 80% max CLTV:

| Field | Value |

|---|---|

| Current home value | $700,000 |

| Existing mortgage balance | $400,000 |

| Assumed max CLTV | 80% |

| $700,000 × 80% | $560,000 |

| Minus existing mortgage | −$400,000 |

| Available second-lien borrowing | $160,000 |

That $160,000 covers a garage conversion or a smaller detached ADU comfortably. It doesn’t cover a $300,000–$450,000 detached build on its own.

Why current value and completed value are different

After-completion appraisals are how lower-equity homeowners actually finance an ADU. Construction loans, Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, and FHA 203(k) all allow underwriting against the as-completed appraised value — what the property will be worth with the ADU finished.

The same $700,000 home from the example above might appraise at $900,000 with a permitted, well-designed detached ADU. With the same 80% CLTV assumption:

$900,000 × 80% = $720,000 − $400,000 existing mortgage = $320,000 of borrowing capacity

That’s the difference between “can’t afford it” and “fully funded.” It’s also why these products require more paperwork — the lender is taking on more risk by underwriting against something that doesn’t exist yet.

The 2026 conforming loan limits matter

For conventional loans (HomeStyle Renovation, CHOICERenovation), the Federal Housing Finance Agency’s 2026 conforming loan limit is $832,750 for a single-unit property in standard-cost areas and $1,249,125 in designated high-cost or special-area counties.6 FHA’s 2026 limits are $541,287 (floor) and $1,249,125 (ceiling) for one-unit properties.7 If your purchase price or refinance balance plus renovation costs exceeds those limits, you’re in jumbo or non-conforming territory.

What lenders want to see before they’ll quote you

For any path more complex than a HELOC, have these ready before the first call:

- Plans or design drawings

- Two or more written contractor bids

- Proof that permits are obtainable (zoning verification, lot dimensions, setback compliance)

- Your current mortgage statement and rate

- Credit score and income documentation

- A realistic budget with a 10–15% contingency

The Urban Institute has flagged ADU appraisal friction — particularly the shortage of comparable ADU sales in many markets — as a persistent issue that can come back to bite low-equity construction-loan applicants when appraisals come in below build cost.8 Document everything.

HELOC vs home equity loan for an ADU: which is better?

A HELOC (home equity line of credit — a revolving credit line secured by your home) usually fits ADU construction better than a fixed home equity loan, because you draw only what you need as construction progresses and pay interest only on the drawn balance. A fixed home equity loan (a lump-sum loan with a fixed rate) wins when your ADU budget is fully defined and rate certainty matters more than flexibility.

Side-by-side

| Feature | HELOC | Fixed home equity loan |

|---|---|---|

| Rate type | Variable (tied to prime — currently 6.75% as of mid-May 20269) | Fixed for the life of the loan |

| Funding | Revolving line — draw as needed | One-time lump sum at closing |

| Year-1 interest base | Drawn balance only | Full borrowed amount |

| National average rate (May 2026) | ~7.21–7.26%2,3 | ~7.36–8.03%2,3 |

| Best fit for | Phased construction, uncertain final cost | Defined budget, payment certainty |

| Biggest risk | Variable-rate exposure | Interest paid from day one, even on unspent funds |

| Typical CLTV cap | 80–90% (lender-dependent) | 80–85% |

| Closing costs | Often low or none | Comparable to a refi |

When a HELOC fits ADU construction

ADU projects rarely match their original budget exactly. Soft costs (plans, permits, soils reports, utility hookups) and site work can shift by 10–20% mid-project. A HELOC lets you draw what you actually need as contractor invoices arrive — and pay interest only on what you’ve drawn. We routinely see homeowners save thousands by using a HELOC for construction and refinancing into a fixed product only after the project is complete and the costs are known.

When a fixed home equity loan wins

If your build is prefab or modular with a confirmed all-in price, or if you have a fixed-price contract with a licensed general contractor and a contingency built in, a fixed home equity loan removes rate uncertainty entirely. The payment never changes. The lender’s underwriting is also typically simpler.

Stress-test the variable rate

If you choose a HELOC, model your payment at the rate plus three percentage points. If your projected post-draw payment at, say, 10.25% would push your debt-to-income ratio over your comfort zone, the HELOC isn’t the right product even if today’s rate looks low.

For a deeper breakdown of HELOC mechanics, draw periods, and repayment terms specific to ADUs, see our HELOC for ADU guide →

What are the seven ADU financing paths in detail?

Here’s the honest breakdown of each path: who it fits, who it doesn’t, how it actually works, the biggest upside, and the biggest downside. Rates and limits are current as of May 2026.

1. HELOC for an ADU

- Best fit: Homeowners with at least 20–25% equity who want to keep their current first mortgage and draw funds as construction progresses.

- Bad fit: Recent buyers with minimal equity, or anyone who can’t tolerate a variable rate.

- How it works: A revolving line of credit secured by your home equity. You’re approved for a maximum amount and draw what you need during the draw period (typically 10 years), paying interest only on the drawn balance. After the draw period, you enter repayment (typically 20 years).

- Current rate context: National averages around 7.21–7.26% (May 2026).2,3 Best-credit borrowers can find sub-7% offers; some credit unions advertise introductory rates in the 5.99–6.50% range.10

- Biggest upside: Flexibility plus rate protection on your first mortgage.

- Biggest downside: Variable-rate exposure. Your payment can rise if the Fed moves.

2. Fixed home equity loan for an ADU

- Best fit: Homeowners with significant equity and a fixed, well-defined ADU budget.

- Bad fit: Anyone with a fluid scope or who wants to draw funds gradually.

- How it works: A second-lien fixed-rate lump-sum loan, typically 5–30 years.

- Current rate context: National averages around 7.36–8.03% (May 2026).2,3

- Biggest upside: Rate certainty — same payment every month.

- Biggest downside: Less flexible than a HELOC; you start paying interest on the full amount at closing.

3. Cash-out refinance for an ADU

- Best fit: Homeowners whose current mortgage rate is at or above today’s mid-6% market, or owners with very small remaining balances.

- Bad fit: Anyone sitting on a sub-5% first mortgage. The blended cost almost never pencils.

- How it works: You refinance your entire first mortgage for a larger amount and take the difference as cash. Most cash-out refis allow up to 80% LTV.

- Biggest upside: One loan, one payment, one closing. If your existing rate is high, you might even improve it.

- Biggest downside: You replace your first mortgage. For most owners who refinanced or bought in 2020–2022, this is the most expensive way to fund an ADU.

4. Construction loan (or construction-to-permanent loan) for an ADU

- Best fit: Homeowners without enough current equity for second-lien products, but with strong income, good credit, plans, permits, and a licensed contractor.

- Bad fit: DIY / owner-builder projects (most construction lenders won’t underwrite them), or anyone unwilling to manage staged draws and inspections.

- How it works: The lender appraises your home based on its future value with the ADU completed. Funds are released in stages (draws) as construction milestones are verified by an inspector. A construction-to-permanent loan automatically converts to a long-term mortgage when construction is finished — saving you a second closing. A construction-only loan requires a separate refinance into permanent financing after completion.

- Biggest upside: Lets you borrow against what the home will be worth, not what it’s worth today. The unlock for low-equity owners.

- Biggest downside: Paperwork, draw schedules, contractor approval, inspections, higher rates, and tighter project oversight.

5. Renovation mortgages — Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, FHA 203(k)

- Best fit: Homebuyers adding an ADU at the time of purchase, or homeowners willing to refinance to fund a renovation.

- Bad fit: Anyone with a sub-5% existing rate that they need to protect.

- How they work: Each program bundles purchase or refinance funds with renovation costs in one mortgage, underwritten against the home’s after-completion value. We break each program down in the renovation-mortgage deep dive below.

- Biggest upside: Lets you borrow against future value, with potentially smaller down payments than construction loans.

- Biggest downside: Strict timelines, contractor requirements, agency-specific rental-income limits, and a refinance of your first mortgage.

6. State and local ADU programs

- Best fit: Income-qualified homeowners in participating cities or states willing to accept affordability covenants or rent restrictions.

- Bad fit: Anyone counting on California’s CalHFA grant (fully allocated since December 28, 202311) or assuming most cities have one.

- How they work: Vary widely. Some are grants. Some are deferred-forgivable loans. Some are construction-to-permanent loans with subsidized rates. Many require an affordability covenant (rent restricted to ≤80% AMI tenants for 5–10 years).

- Biggest upside: Real money. New York City’s Plus One ADU Program offers up to $395,000 combined per homeowner;12 Charlotte’s Queen City ADU Program offers up to $80,000 forgivable, capped at 50% of project costs;13 Salt Lake City’s Backyard Keys construction loan goes up to $200,000 at 3% fixed.14

- Biggest downside: Geographic and income restrictions; programs open and close; deed covenants reduce future flexibility. See the full snapshot below.

7. Non-debt and alternative options

- Cash: Avoids all interest cost. The tradeoff is opportunity cost on the deployed capital.

- Home equity investment (HEI): Also called a home equity agreement (HEA). A lump sum in exchange for a share of your home’s future appreciation. No monthly payments, but a large lump-sum repayment due at sale, refinance, or term end (typically 10–30 years). The CFPB has published an Issue Spotlight on home equity contracts warning that these products can be complex, often lack standardized disclosures, and may create sale/refinance/default pressure — read the term sheet carefully.15 See the no-monthly-payment section below for details.

- HECM (reverse mortgage): For homeowners 62 or older. Can provide tax-free funds without a monthly payment, but the balance grows over time and the loan must be repaid when you sell or no longer occupy the home as a primary residence.

- Family loan: Document it with a written promissory note, register it appropriately, and set an interest rate at or above the IRS Applicable Federal Rate to avoid imputed-income issues.

How do you finance an ADU with little or no equity?

You finance an ADU with little or no equity by using a loan that underwrites against your home’s as-completed value rather than its current value. The four products that do this are construction-to-permanent loans, Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, and FHA 203(k). All four require more paperwork than a HELOC, but they’re how lower-equity homeowners actually get to “fully funded.”

We see this constantly. A homeowner bought in 2023 or 2024 at today’s prices. They have maybe 5–10% equity. A standard HELOC won’t get them anywhere close to a $300,000 detached ADU budget. The lender’s response is almost always: “We’ll appraise the home subject to completion.”

That phrase — “subject to completion” — is what unlocks low-equity ADU financing. The appraiser models what the property will be worth with the ADU built. Lenders then size your loan against that future number, not today’s.

The four “future value” options compared

| Path | Down payment / equity needed | Max LTV against future value | First mortgage | Property types |

|---|---|---|---|---|

| Construction-to-permanent (conventional) | Typically 10–20% down for purchase; equity-dependent for owner-occupied refinance | Up to ~80–95% depending on lender and product | Replaces or converts | All ADU types |

| Fannie Mae HomeStyle Renovation | 3% down for first-time buyers; standard for refinance | Up to 75% of as-completed appraised value16 | Replaces | Detached, attached, modular, manufactured (with conditions) |

| Freddie Mac CHOICERenovation | 5% down for 1-unit primary residences (3% if combined with Home Possible)17 | Up to as-completed value tier | Replaces | Detached, attached, modular, manufactured (with conditions) |

| FHA 203(k) Standard | 3.5% down (FICO 580+); 10% (FICO 500–579) | Capped by FHA county loan limits | Replaces | Attached ADUs, conversions; not the natural fit for ground-up detached ADUs |

What makes these loans harder

- Plans, permits, and bids required upfront. No “we’ll figure it out later.”

- Licensed, insured contractor required. Most programs don’t accept owner-builder.

- Staged draws and inspections. Your contractor doesn’t get paid until inspections confirm the work.

- Strict timelines. HomeStyle Renovation requires completion within 15 months of closing.18 FHA 203(k) Standard now allows up to 12 months (extended from 6 in November 2024).19

- Refinances your first mortgage. If your rate is low, this is the trade.

The Terner Center has noted that only about 6.3% of California ADU owners actually use renovation loans, despite the fact that renovation loans are “theoretically well-suited for homeowners without significant equity.”1 The gap is mostly friction — paperwork and lender familiarity — not eligibility.

If your equity is tight and a construction or renovation loan looks like the right lane, comparing offers across multiple lenders at once is faster than calling each individually.

Compare mortgage-backed ADU financing paths via Mortgage Research Center →We may earn a commission when you use this link. Approval depends on credit, income, property, and lender underwriting; not guaranteed.

Are HomeStyle, CHOICERenovation, or FHA 203(k) better for an ADU?

It depends on whether you’re buying a home, refinancing, the ADU type you’re building, and whether you need rental income to qualify. We compare all three side by side, then break down the recent rule changes that most ADU financing guides on the internet haven’t updated.

Renovation mortgage comparison (May 2026)

| Feature | Fannie Mae HomeStyle | Freddie Mac CHOICERenovation | FHA 203(k) Standard |

|---|---|---|---|

| Minimum down payment | 3% (first-time buyers); 5% standard | 5% (3% with Home Possible) | 3.5% (FICO 580+); 10% (FICO 500–579) |

| Property types | 1–4 units; ADUs eligible on 1, 2, and 3-unit properties; up to 3 ADUs on single-unit eff. March 31, 2026 for UAD 3.6 lenders20 | 1–4 units; ADUs allowed on 2–3 unit properties; manufactured-home ADUs on multi-section / CHOICEHomes eff. Feb 9, 202621 | 1–4 units; ADUs eligible for attached/conversion projects |

| Renovation cap | Up to 75% of as-completed value | Up to as-completed value tier | Capped by FHA county limits (2026: $541,287 floor / $1,249,125 ceiling7) |

| Detached new-build ADU | ✓ Yes | ✓ Yes | ⚠ Provisions oriented toward conversions and attached units |

| Upfront disbursement | Now up to 50% of total renovation costs at closing for materials, permits, design, and deposits (per SEL-2025-10, eff. Dec 10, 2025)22 | Lender-dependent draw structure | Drawn through 203(k) consultant; consultant fee now eligible within Limited program |

| Completion timeline | 15 months | Typically 12 months | 12 months for Standard (extended from 6, eff. Nov 4, 202419); 9 months for Limited |

| Limited variant cap | N/A | N/A | $75,000 (raised from $35,000, eff. Nov 4, 202419) |

| ADU rental income for qualifying | Yes, with conditions | Tightened — for applications on/after May 4, 2026, rental income from any unit included in the CHOICERenovation project funded by mortgage proceeds cannot be used to qualify23 | Yes, with conditions; cannot be used on FHA cash-out refi24 |

What changed in 2024–2026 that most guides don’t reflect

Fannie Mae SEL-2025-10 (announced December 10, 2025):

- HomeStyle Renovation upfront disbursements at closing increased to 50% of total renovation costs for materials, permits, architectural and design expenses, and borrower deposits.22

- The previous $50,000 renovation cap for manufactured homes was removed; renovation costs can now reach 50% of the as-completed appraised value.22

- For lenders using UAD 3.6 policy, ADU property eligibility expanded: up to 3 ADUs on a single-unit property where local zoning allows, ADUs allowed on 2–3 unit properties, and ADUs explicitly permitted on single-wide manufactured homes (effective March 31, 2026).20

- HomeStyle Renovation used with a limited cash-out refinance does not allow cash proceeds to the borrower, including proceeds typically permitted under standard limited cash-out rules.22

Freddie Mac Bulletin 2025-15 (announced November 5, 2025; effective February 9, 2026): Mortgages secured by multi-section manufactured homes — including CHOICEHomes — are now eligible with one ADU or one manufactured-home ADU on the property.21

Freddie Mac Bulletin 2026-1 (announced February 4, 2026): For applications received on or after May 4, 2026, rental income from any unit included in a CHOICERenovation project funded by the mortgage proceeds cannot be used to qualify the borrower.23 This is a real tightening — if you were counting on your future ADU’s rent to help you qualify for a CHOICERenovation loan, that lane just closed for the renovation-funded unit itself.

FHA 203(k) modernization (HUD Mortgagee Letter 2024-13; effective November 4, 2024):

- 203(k) Limited cap raised from $35,000 to $75,000 nationwide.19

- 203(k) Standard rehabilitation period extended from 6 to 12 months.19

- 203(k) Consultant fee now includable in the Limited mortgage amount; HUD’s maximum consultant fee schedule applies (typically $400–$1,000+ depending on repair amount).19

These changes are why we don’t recommend reading 2023 or pre-2024 ADU financing guides as current. The rules moved.

Can ADU rental income help you qualify for financing?

Sometimes — and the rules depend on which agency is underwriting the loan, whether the ADU already exists, and whether you’re buying or refinancing. Both Fannie Mae and Freddie Mac allow some ADU rental income to count toward qualifying income on one-unit principal residence transactions with a 30% cap, but the eligible transaction types differ between agencies.

Fannie Mae’s rental-income treatment for ADUs

Per the Fannie Mae Selling Guide, Section B3-3.8-01:

- Rental income from one ADU on a one-unit principal residence may be used as qualifying income for purchase and limited cash-out refinance transactions.25

- ADU rental income is capped at 30% of total qualifying income.25

- A signed lease or a Single-Family Comparable Rent Schedule (Form 1007) is required.

- Borrowers with fewer than 12 months of property management experience face additional limits — qualifying rental income cannot exceed the borrower’s housing payment (PITIA).

- Under HomeReady, ADU rental income can help qualifying lower-income borrowers access better terms.

Freddie Mac’s rental-income treatment for ADUs

Per the Freddie Mac Single-Family Seller/Servicer Guide Section 5601.2 and the February 2026 ADU Fact Sheet:

- ADU rental income is permitted on purchase and no-cash-out refinance transactions on one-unit principal residences.26 (Note: Freddie Mac uses “no-cash-out” where Fannie Mae uses “limited cash-out.” The eligible transaction wording differs between agencies.)

- Lease-supported income is capped at 75% of the lease amount.26

- Total qualifying rental income is capped at 30% of total income used to qualify.

- A comparable-rent analysis is required.

- For purchase transactions, borrowers may need to complete landlord education.

Important May 4, 2026 change: For applications on or after May 4, 2026, if you’re using CHOICERenovation to add or renovate an ADU, rental income from that ADU cannot be used to qualify, because that unit is “included in the renovation project funded by mortgage proceeds.”23 Rental income from a separate, existing, unmodified unit on the property may still count.

FHA’s rental-income treatment for ADUs

Per HUD Mortgagee Letter 2023-17:

- For an FHA mortgage on a property with an existing ADU (purchase or rate-and-term refinance), lenders can use 75% of the estimated ADU rental income for certain borrowers when calculating effective income.24

- For a new ADU being added under the Standard 203(k) Rehabilitation program (such as a garage or basement conversion), lenders may use 50% of the estimated rental income.24

- ADU rental income may not exceed 30% of total monthly qualifying income.24

- ADU rental income cannot be used on FHA cash-out refinance transactions.24

What homeowners get wrong about ADU rental income

You can’t project any number you want. Lenders require documented market-rate evidence (Form 1007 or equivalent comparable rent schedule), not optimistic estimates. And “future” rent from an ADU that doesn’t yet exist is treated differently than rent from an existing leased ADU.

Illustrative rental-income examples below and in the scenarios section are not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

The bottom line: ADU rental income can meaningfully improve your qualification odds — especially for borrowers who are close to qualifying but need a debt-to-income (DTI) boost. It’s a real tool. It’s not a blank check.

Can you finance an ADU without monthly payments?

Yes — through a home equity investment (HEI) or, for homeowners 62 or older, a HECM reverse mortgage. Both provide cash without a standard monthly loan payment. Both also carry real costs that may exceed traditional financing over a long hold period, and the CFPB has specifically flagged home equity contracts as a product category with complexity, repayment, and disclosure risks worth understanding before signing.15

Home equity investments (HEIs) — what they are

An HEI (also called a home equity agreement or home equity sharing agreement) is a lump-sum payment to the homeowner in exchange for a share of the home’s future appreciation. There’s no monthly payment. Instead, you repay the investment plus a share of appreciation when you sell the home, refinance, or hit the contract’s term limit (usually 10–30 years).

Major HEI providers (current snapshot — verify each provider’s state list, current investment range, and credit requirement on the provider’s site before applying):

- Hometap — investments roughly $15,000–$600,000; 10-year term; available in a limited set of states plus DC.

- Point — investments roughly $25,000–$600,000; terms up to 30 years; available in a limited set of states.

- Unison — investments up to $500,000; terms up to 30 years; broader state availability than most HEI providers.

- Unlock — investments roughly $30,000–$500,000; 10-year term with partial-buyout option.

- Splitero, EquiFi, Aspire HEI — more limited geographic footprints (EquiFi is California-only).

State availability changes; coverage in this category can shift quarterly. Always verify on each provider’s official site before relying on a specific provider for your project.

Why “no monthly payment” doesn’t mean “no cost”

The catch with HEIs is what happens at settlement. The investor typically takes a percentage of your home’s appreciation — and on a 10-year contract in an appreciating market, that math can exceed the total interest you’d pay on a traditional loan, even at higher rates.

The CFPB’s Issue Spotlight on home equity contracts highlights specific risks:15

- Contract terms vary widely from provider to provider, with no standardized disclosure framework

- Repayment is often a balloon payment at sale, refinance, or term end

- If a homeowner can’t repay, the contract can force a sale

- Some contracts discount the homeowner’s starting home value before calculating the investor’s share — the CFPB cites examples of 25% and 30% starting-value discounts in real contracts, which materially increases the eventual repayment

- Default provisions may resemble those of a mortgage even though the product isn’t underwritten like one

Treat the term sheet like any other major financial contract. Read every page. Have a real estate attorney review it before signing if six figures are involved.

HECM (reverse mortgage) — for homeowners 62+

A HECM (Home Equity Conversion Mortgage) is FHA-insured and lets owners 62 or older access home equity without a monthly payment. The loan balance grows over time and is repaid when the home is sold or the borrower no longer occupies it as a primary residence. HECMs are tightly regulated and require HUD-approved counseling. They can be relevant for older homeowners building an ADU for aging-in-place or multigenerational housing. They’re not a fit for younger owners.

When to avoid no-payment financing

- You don’t have a clear exit plan in 10–30 years

- You expect significant home-price appreciation that you’d rather keep

- You can qualify for a traditional product (HELOC, home equity loan, construction loan)

- You have a sub-5% existing mortgage rate that you can protect with a HELOC instead

Use no-payment products as a fallback when traditional products don’t work — not as a default just because the monthly payment looks attractive.

Are there ADU grants or local financing programs in 2026?

Yes — but most national readers won’t qualify, many programs are paused or fully allocated, and the largest active programs come with affordability covenants, rent restrictions, and owner-occupancy requirements. The snapshot below was verified May 19, 2026; verify each program at the source before relying on it.

The honest grant reality

There is no reliable nationwide ADU grant. The most-searched program — California’s CalHFA ADU Grant — has been fully allocated since December 28, 2023, with no relaunch date confirmed.11 CalHFA’s own page warns about scammers who claim they can help homeowners “access” allocated funds. Real grants exist locally, but they cover a fraction of demand.

2026 ADU local assistance snapshot (verified May 19, 2026)

| Program | Location | Help offered | Key restrictions | Status |

|---|---|---|---|---|

| CalHFA ADU Grant Program | California | Previously $40,000 toward pre-development costs | Income limits | Fully allocated since Dec 28, 2023; no relaunch date confirmed11 |

| San Diego Housing Commission (SDHC) ADU Finance Program | City of San Diego, CA | Construction-to-permanent loan up to $250,000 (commonly reported: 1% fixed during construction, 4% fixed post-construction)29 | Income limits; 7-year affordability covenant (≤80% AMI tenants); owner-occupancy requirements; verify current rate terms with SDHC at application | Active |

| New York State HCR Plus One ADU Program | Statewide NY (participating municipalities) | Grants and forgivable assistance (up to $125,000 per home)30 | ≤120% AMI; 10-year regulatory agreement; no short-term rental | Active — $85M originally allocated; verify per-home cap with local administrator |

| NYC Plus One ADU Program | New York City | Up to $395,000 combined per homeowner (forgivable loans + grants) | NYC-specific application; ≤165% AMI with preference to ≤120% | Reopened March 18, 2026; application window through June 12, 202612 |

| MassHousing ADU Loan Program | Massachusetts | Up to $250,000 for detached ADUs; $150,000 for attached/conversion ADUs31 | Owner-occupied; income guidelines; plans/permits required | Active |

| Boston ADU Financial Assistance Program | Boston, MA | Up to $7,500 technical assistance grants; up to $50,000 ADU loan gap funding32 | Owner-occupancy; income/assets rules | Active |

| Portland (OR) SDC Waiver | Portland, OR | Waiver of System Development Charges for qualifying ADUs33 | 10-year deed covenant; no short-term rental use | Active |

| Salt Lake City “Backyard Keys” / CDC Utah | Salt Lake City, UT (Westside SLC) | Construction loan up to $200,000 at 3% fixed; 5-year term with possible extension; up to 10% forgiveness possible14 | Westside SLC; owner-occupied; rent restrictions | Active |

| Orlando ADU Incentive Program | Orlando, FL | Up to $10,000 build-out rebate plus permit/impact fee rebates34 | ADU must be rented to tenant earning ≤120% AMI for at least 12 of first 24 months | Active |

| Charlotte Queen City ADU Program | Charlotte, NC | Up to $80,000 or 50% of total project costs (whichever is less), forgivable, interest-free; 50% homeowner match required13 | Affordability and tenant requirements; forgiveness generally 1 year per $10,000, up to 8 years | Active |

Each row verified against the official program page on May 19, 2026. Programs change; re-verify before applying.

How to verify a program before relying on it

- Check the program’s official .gov or housing-agency page. Not a builder’s blog.

- Confirm the funding round is currently open. Most rounds close when funds are allocated.

- Confirm your income falls within the AMI limit. Most programs cap at 80%, 120%, or 165% AMI.

- Read the affordability covenant. A 7- or 10-year deed restriction limiting rent to ≤80% AMI tenants is normal for subsidized programs. It also affects your future flexibility and resale.

- Confirm your project type is eligible. Some programs exclude detached new-builds; others exclude manufactured homes.

If your project doesn’t fit a local program, that’s not a setback — it’s information. Move to the financing path that actually fits your situation.

Local programs are powerful when you qualify.

Check your address against our ADU feasibility tool first →Does ADU type change the best financing path?

Yes. The financing product that fits a $90,000 garage conversion is almost never the same one that fits a $400,000 detached new-build, and prefab and manufactured ADUs have specific eligibility requirements that site-built ADUs don’t. Here’s how to think about it.

By ADU type

Garage conversion ADU — The most affordable type, often $80,000–$160,000. Equity-based products (HELOC, home equity loan) usually cover the entire budget without needing future-value lending. FHA 203(k) is a natural fit because the conversion is within or attached to the existing structure.

Basement or internal conversion / JADU — Similar to garage conversions. A JADU (junior accessory dwelling unit) is typically up to 500 square feet, carved out of the existing primary residence, sharing some utilities. Costs are usually lower. HELOCs, home equity loans, and FHA 203(k) all work cleanly.

Attached ADU addition — All financing paths work. FHA 203(k) Standard is explicitly eligible for attached additions. Construction loans handle the staged-draw process naturally.

Detached new-build ADU — The most flexible for financing. Every path on this page works for a detached site-built ADU. Construction loans and the renovation mortgages (especially HomeStyle and CHOICERenovation) are particularly useful because a detached ADU typically adds the most appraised value.

Prefab or modular ADU — Built to local or state building code in a factory. Lenders generally treat modular ADUs like site-built structures. Fannie Mae explicitly includes modular ADUs as eligible for HomeStyle Renovation. Confirm with your lender that they treat your specific prefab company’s product as modular, not manufactured.

Manufactured (HUD-code) ADU — Built to the federal HUD Manufactured Home Construction and Safety Standards. Conventional financing requires a permanent foundation, legal classification as real property, HUD Data Plate or Certification Label documentation, and manufacturer compliance. Fannie Mae’s HomeStyle Renovation and Freddie Mac’s CHOICERenovation now permit manufactured-home ADUs with these conditions met (Bulletin 2025-15, effective February 9, 2026).21

Owner-builder projects — Most construction loans and renovation mortgages require a licensed, insured general contractor. If you’re acting as your own GC, expect a much smaller universe of lenders. Some local credit unions and specialty lenders will work with owner-builders. Start that lender conversation before you commit to the project structure.

ADU type vs financing fit (quick view)

| ADU type | Best first path | Second-best path | Key watchout |

|---|---|---|---|

| Garage conversion | HELOC / home equity loan | FHA 203(k) | Scope creep — get a detailed bid before borrowing |

| Basement / internal / JADU | HELOC / home equity loan | FHA 203(k) | Egress, ceiling height, separate utilities |

| Attached addition | HELOC or construction loan | FHA 203(k) Standard or HomeStyle | Structural engineering costs often underestimated |

| Detached new-build | Construction-to-perm or HELOC (if equity allows) | HomeStyle / CHOICERenovation | Appraisal comps may be thin in your market |

| Prefab / modular | HELOC or construction loan | HomeStyle / CHOICERenovation | Confirm lender classifies as modular, not manufactured |

| Manufactured (HUD-code) | HomeStyle Renovation | Specialty manufactured-home lender | Real-property classification, permanent foundation |

| Owner-builder | HELOC (if equity allows) | Specialty lender only | Most construction lenders won’t underwrite |

For deeper ADU-type-specific cost data, see our Prefab ADU Cost guide and Best Prefab ADU Companies guide.

What does it actually cost to borrow? Three worked scenarios

The headline rate on a loan rarely tells you which option actually costs the least over the time you’ll hold the debt. Here are three real scenarios at May 2026 market context, with the math worked through.

Methodology

We compare total interest paid across the full debt stack — existing first mortgage plus any new ADU financing — over the remaining mortgage term, not just on the ADU money alone. Year-1 monthly payments shown are principal + interest only (excluding taxes, insurance, HOA, and PMI). Construction-loan payments are interest-only during the build phase. Rates reflect Curinos and Bankrate national averages for HELOCs and home equity loans (May 20262,3), Freddie Mac PMMS for 30-year first mortgages (6.36% on May 14, 20264), and roughly 25–75 basis points higher for cash-out tiers. Your actual rate, fees, APR, and approval depend on credit, income, equity, lender, and loan product. These are illustrative comparisons, not offers or guarantees.

Scenario 1: $150,000 garage conversion

Borrower profile: Owner since 2018; home value $700,000; existing mortgage balance $300,000 at 3.5% with ~25 years remaining; FICO 750.

| Option | Rate context | Approx. monthly (year 1, P&I only) | Approx. total interest, full debt stack | Net assessment |

|---|---|---|---|---|

| Keep first mortgage + draw $150K HELOC | First $300K @ 3.5%; HELOC $150K @ ~7.25% variable | ~$1,505 (first) + ~$906 interest-only on HELOC during draw | Approx. ~$281K–$351K total | Protects the 3.5% rate. Wins on blended cost over 25–30 years. |

| Keep first mortgage + $150K fixed home equity loan, 20 years | First $300K @ 3.5%; HEL $150K @ ~7.50% fixed | ~$1,505 (first) + ~$1,209 (HEL) | Approx. ~$291K total | Predictable payment. Keeps the 3.5% rate. |

| Cash-out refinance to $450K, 30 years | Replacement loan $450K @ ~6.50% | ~$2,844 | Approx. $574K total interest over 30 years | Replaces a 3.5% rate. Debt-stack cost materially higher. |

Verdict: For a garage conversion at this borrower’s profile, a fixed home equity loan or HELOC wins by a wide margin over a cash-out refi.

Scenario 2: $250,000 mid-size detached ADU

Borrower profile: Owner since 2020; home value $800,000; existing mortgage balance $400,000 at 3.25% with ~25 years remaining; FICO 740.

| Option | Rate context | Approx. monthly (year 1, P&I only) | Approx. total interest, full debt stack | Net assessment |

|---|---|---|---|---|

| Keep first mortgage + draw $250K HELOC | First $400K @ 3.25%; HELOC $250K @ ~7.25% variable | ~$1,948 (first) + ~$1,510 interest-only on HELOC during draw | Approx. ~$420K–$530K total | Protects the 3.25% first mortgage. Stress-test the variable rate. |

| Keep first mortgage + $250K fixed home equity loan, 30 years | First $400K @ 3.25%; HEL $250K @ ~7.50% fixed | ~$1,948 (first) + ~$1,749 (HEL) | Approx. ~$570K total | Predictable. Higher total because of longer HEL term. |

| HomeStyle Renovation limited cash-out refi to $650K, 30 years | Replacement loan $650K @ ~6.50% | ~$4,109 | Approx. $830K total interest over 30 years | Replaces the 3.25%. Debt-stack cost materially higher. |

| Construction-to-permanent loan, $250K against future value | ~7.75% during build; ~6.50% after conversion | Varies by draw and conversion structure | Comparable to HomeStyle if first mortgage isn’t replaced | Works for owners with insufficient current equity. |

Verdict: For a borrower with adequate equity and a sub-4% first mortgage, the HELOC wins by a meaningful margin over 30 years. For a borrower with insufficient current equity, the construction-to-perm or HomeStyle is the path.

Scenario 3: $400,000 full custom detached ADU on a recent purchase

Borrower profile: Owner since 2024; home purchase price $900,000; current mortgage balance $700,000 at 7.0%; FICO 720.

| Option | Rate context | Approx. monthly (year 1, P&I only) | Approx. total interest, full debt stack | Net assessment |

|---|---|---|---|---|

| Standalone HELOC | Insufficient current equity for second-lien underwriting | N/A | N/A | Most lenders will decline at this LTV. |

| Fannie Mae HomeStyle Renovation refi to $1.1M | Replacement loan $1.1M @ ~6.50% | ~$6,953 | Approx. $1.4M total interest | Replaces 7.0% with 6.50%; captures rate improvement. Note: $1.1M exceeds standard 2026 one-unit limit of $832,750 — requires high-cost county or non-conforming product.6 |

| FHA 203(k) Standard | Total ~$1.0–$1.1M @ ~7.50%; subject to FHA county limits | ~$7,690 | Approx. $1.6M total interest | Higher rate; lower down payment requirement. Less flexible for new-build detached. |

| Construction-to-permanent loan | ~7.75% during build; ~6.75% conversion | Varies by structure | Comparable | Common path for low-equity construction. |

Verdict: For a 2024 buyer already at 7%, replacing the first mortgage with HomeStyle Renovation can actually improve the rate while funding the ADU — but only if the property qualifies under conforming or high-cost limits. The blended math reverses entirely versus Scenarios 1 and 2.

The takeaway across all three: the right financing path is borrower-specific. A path that wins for one homeowner can be the worst choice for another. Run your own math.

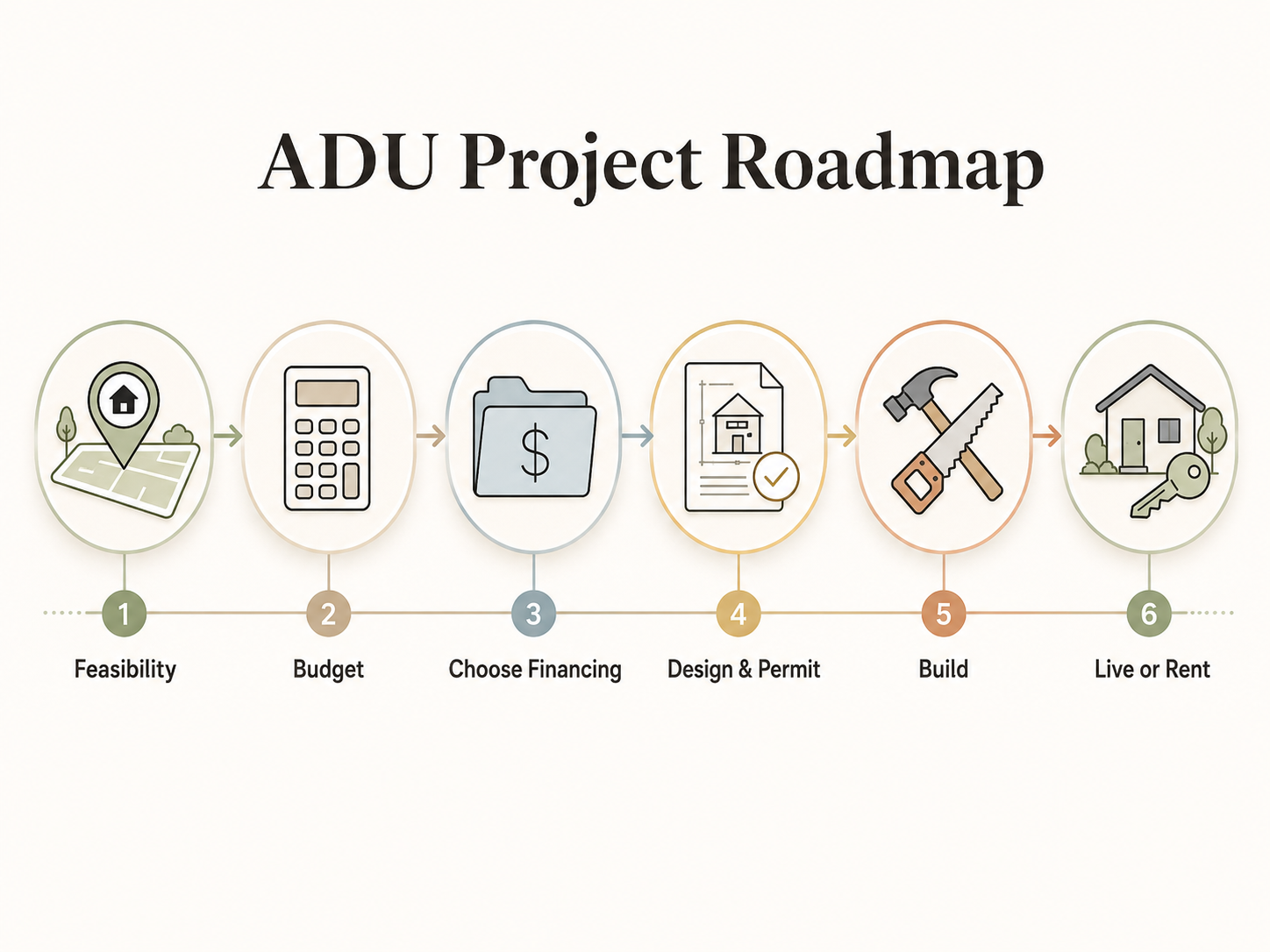

What should you do before applying for ADU financing?

Don’t start with a lender call. Start with five steps that determine whether the project is even worth the financing conversation.

Step 1 — Confirm your lot can legally support the ADU

This is the cheapest check that saves the most money. Lot dimensions, zoning, setbacks, and overlay districts (coastal, hillside, fire) determine what you can build before any lender quote matters. We built our Feasibility Engine for this exact step.

Step 2 — Estimate total project cost honestly

Build a budget that includes hard costs (construction), soft costs (design, permits, soils, fees), site work (grading, utilities, foundations), contingency (10–15%), and post-build setup (appliances, landscaping, rental setup if applicable). See our ADU Cost guide for type-by-type budget benchmarks.

Step 3 — Calculate usable equity

Use the formula above to estimate second-lien borrowing capacity at 80% CLTV. If the answer is comfortably above your project budget, equity-based products are your first lane. If it’s below, you need an after-completion product.

Step 4 — Decide whether to protect or replace your first mortgage

If your first mortgage is well below the mid-6% benchmark, default to a second-lien product (HELOC or home equity loan). If your first mortgage is near or above today’s rate or you owe very little, a cash-out refi or renovation mortgage can consolidate.

Step 5 — Document everything before you call lenders

Have ready:

- Property address and jurisdiction

- Current mortgage statement (balance, rate, term, lender)

- Last two months of pay stubs and last two W-2s (or last two years of tax returns if self-employed)

- Credit score (or know it’s been pulled recently)

- ADU plans or designs (or commitment to obtain them)

- Contractor bids (two or three)

- Permit status

- Estimated rent if you plan to lease the ADU

- HOA or covenant documents if applicable

ADU financing pre-application checklist

- Property feasibility confirmed (lot can support intended ADU)

- Realistic all-in project budget with contingency

- Mortgage balance, rate, and term documented

- Estimated home value (recent comparable sales)

- ADU type, size, and design direction chosen

- Two or more written contractor bids

- Plans or designs in progress

- Permit eligibility verified with the local jurisdiction

- Income and credit documentation gathered

- Local program eligibility checked (or ruled out)

- Decision on protecting vs replacing the first mortgage

- Exit plan if using HEI/HEA

If you can check every box, your lender call will go from “I’m just exploring” to a serious quote in a single conversation.

Before you start the paperwork, confirm the build is even buildable.

Get your free ADU report — see what’s possible at your address in 60 seconds →Want the full checklist plus our financing-path comparison worksheet?

Download the Free ADU Starter Kit →How we researched and verified this guide

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We don’t originate loans or act as a broker. We do earn affiliate commissions when readers use our links to explore financing or request pricing — but those payments never change which paths we list, how we rank them, or what we recommend. Paths are ordered by reader fit, not by payout.

We compared ADU financing paths by homeowner scenario rather than ranking lenders. Our primary sources for this guide:

- Fannie Mae Single-Family Selling Guide, including Section B2-3-04 (ADU eligibility), Section B3-3.8-01 (rental income), Section B5-3.2-01 (HomeStyle Renovation), and SEL-2025-10 (December 10, 2025 updates)

- Freddie Mac Single-Family Seller/Servicer Guide, Section 5601.2 (ADU eligibility) and Bulletins 2025-15 and 2026-1

- HUD Mortgagee Letters 2023-17 (FHA ADU rental income) and 2024-13 (203(k) modernization)

- HUD FHA loan limits for 2026

- FHFA conforming loan limits for 2026

- Freddie Mac Primary Mortgage Market Survey (May 14, 2026)

- CFPB Issue Spotlight on Home Equity Contracts

- Curinos / Yahoo Finance and Bankrate national rate surveys (May 2026)

- Wall Street Journal Market Data (prime rate)

- Terner Center for Housing Innovation at UC Berkeley

- Urban Institute Housing Finance Policy Center

- California Department of Housing and Community Development 2025 ADU Handbook

- California State Board of Equalization (new-construction assessment)

- Program pages: CalHFA, San Diego Housing Commission, NYC HPD and NYS HCR, MassHousing, Boston Mayor’s Office of Housing, Portland Permitting & Development, CDC Utah / SLC CRA, City of Orlando, City of Charlotte

What we verified on

- Current HELOC and home equity loan benchmark rates (Curinos; Bankrate)

- Prime rate (WSJ)

- Freddie Mac PMMS 30-year fixed-rate context

- Fannie Mae ADU rental-income rules and SEL-2025-10 effective dates

- Freddie Mac CHOICERenovation rule effective May 4, 2026 and Bulletin 2025-15 effective February 9, 2026

- FHA/HUD ADU rental-income guidance (ML 2023-17) and 203(k) modernization (ML 2024-13)

- CFPB consumer warning on home equity contracts

- Local ADU assistance programs and their current status, max amounts, and restrictions

- 2026 conforming and FHA loan limits

- California impact-fee and new-construction-assessment rules

The financing world moves. We re-verify rate data monthly and program-status data quarterly, and we re-check agency guidance after every published Selling Guide or Mortgagee Letter announcement.

ADU Financing FAQ

What is the best loan for an ADU?

There is no single best ADU loan. For homeowners with strong equity and a low first-mortgage rate, a HELOC or fixed home equity loan typically wins. For homeowners with low equity, a construction-to-permanent loan or one of three renovation mortgages — Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, or FHA 203(k) — is the right starting point. For owners 62+, a HECM reverse mortgage can be an option. The "best" loan depends on your equity, your current mortgage rate, your ADU type, and your need (if any) for rental income to qualify.

Can I use a HELOC to build an ADU?

Yes — a HELOC is one of the most common ADU financing methods when you have at least 20–25% equity in your home. It keeps your existing first mortgage intact, lets you draw funds as construction invoices arrive, and charges interest only on the drawn balance. The variable rate is the main risk; stress-test the payment at current rate plus three percentage points before committing.

Is a home equity loan better than a HELOC for an ADU?

A fixed home equity loan is better when your ADU budget is fully defined and you want payment certainty; a HELOC is better when costs may shift during construction and you want flexibility. Home equity loan rates averaged about 7.36–8.03% nationally in May 2026; HELOC rates averaged about 7.21–7.26%. Both keep your first mortgage intact.

Can I finance an ADU with no equity?

Yes — construction-to-permanent loans, Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, and FHA 203(k) all underwrite against your home's value after the ADU is built rather than today's value. These products require plans, permits, contractor bids, staged draws, and inspections, and most of them replace your first mortgage. They're the path for lower-equity homeowners but they're not simple.

Can ADU rental income help me qualify for a loan?

Sometimes. Fannie Mae allows ADU rental income on one-unit principal residence purchase and limited cash-out refinance transactions, capped at 30% of total qualifying income. Freddie Mac allows ADU rental income on purchase and no-cash-out refinance transactions, with lease-supported income at 75% of lease and the same 30% total cap. FHA uses 75% of estimated rental income for existing ADUs in purchase or rate-and-term refi, and 50% for new ADUs added via Standard 203(k), with the same 30% cap; FHA cannot use ADU rent on cash-out refi. Starting May 4, 2026, rental income from an ADU funded by a CHOICERenovation loan cannot be used to qualify. Rules differ by program and transaction type — confirm with your lender.

Is a cash-out refinance a bad idea for an ADU?

It's not a bad idea if your existing mortgage rate is near or above today's mid-6% market. It's usually a bad idea if your existing rate is well below today's market, because you give up that rate on your entire mortgage balance to fund the ADU. Run the full debt-stack comparison across both options — total interest paid over the remaining mortgage term, not just monthly payment — before deciding.

Are there grants for building an ADU?

Yes, but most are local, income-restricted, or fully allocated. The widely-known California CalHFA ADU Grant has been fully allocated since December 28, 2023, with no relaunch date confirmed. Active programs in May 2026 include NYC's Plus One ADU Program (up to $395,000; reopened March 18, 2026; application window through June 12, 2026), NY State HCR Plus One, MassHousing ADU Loan ($250,000 detached / $150,000 attached), Boston's gap funding (up to $50,000), Salt Lake City Backyard Keys (up to $200,000 at 3% fixed), Orlando's $10,000 build-out rebate, and Charlotte Queen City ADU (up to $80,000 forgivable with a 50% match).

Can I finance a prefab or modular ADU?

Yes, in most cases. Prefab and modular ADUs built to local or state building code are typically treated like site-built structures for financing purposes. Fannie Mae HomeStyle Renovation explicitly includes modular ADUs as eligible. Confirm with your lender that they classify your specific prefab company's product as modular (not manufactured), because manufactured/HUD-code units have additional requirements around permanent foundations and real-property classification.

Can I use an FHA 203(k) loan for an ADU?

Yes, with conditions. FHA 203(k) is well-suited for attached ADUs, garage conversions, basement conversions, and renovations of existing ADUs. The 203(k) Standard is the path for substantial work, with a 12-month rehabilitation period (extended from 6 months effective November 4, 2024). The 203(k) Limited cap was raised from $35,000 to $75,000 on the same date. For a brand-new detached ADU, HomeStyle Renovation or CHOICERenovation is generally the better path.

Can I use a personal loan to finance an ADU?

Generally, no — at least not as your core financing. Personal loans are unsecured, which means they carry materially higher rates than home-secured products and shorter terms (typically 2–7 years). They can occasionally make sense for short-term soft-cost bridging (paying for plans before a HELOC closes), but for the main build budget, the math almost never works versus a HELOC, home equity loan, or renovation mortgage.

Should I use builder financing for an ADU?

Tread carefully. Some prefab and modular ADU builders advertise in-house or partner financing as a convenience. Those programs are not always cheaper than independent lenders, and a builder with skin in the financing deal has a conflict you should price into the decision. Get at least one independent lender quote (HELOC, home equity loan, or renovation mortgage) before signing a builder-financed deal so you have a real comparison.

What credit score do I need for an ADU loan?

It varies by path and by lender. FHA 203(k) accepts FICO scores as low as 500 with 10% down, or 580+ with 3.5% down under HUD's published guidelines. Most HELOC lenders look for 680+ for best pricing, though offers exist down to 620. Construction loans typically prefer 700+. Conventional renovation mortgages have no minimum credit score requirement in Fannie Mae and Freddie Mac guidelines as of late 2025, but individual lenders apply their own overlays — most expect 620+. Confirm with the specific lender.

How long does ADU financing take to close?

Typical ranges: HELOC and home equity loan, 2–6 weeks. Cash-out refinance, 30–45 days. FHA 203(k) and conventional renovation mortgages, 45–60 days. Construction-to-permanent loans, 30–60 days plus the construction period. Permit and design dependencies can extend any of these timelines significantly. Your lender's specific underwriting queue and your own documentation readiness drive the actual timing.

What should I do before calling a lender?

Confirm your lot can support the ADU (run our Feasibility Engine or check zoning yourself). Build a realistic budget with contingency. Pull your credit score. Gather pay stubs, tax returns, and your mortgage statement. Get two contractor bids. Decide whether to protect or replace your first mortgage. Lenders who get a complete file return faster quotes with fewer surprises.

Sources

- Terner Center for Housing Innovation, UC Berkeley. ADU Construction Financing. https://ternercenter.berkeley.edu/

- Curinos / Yahoo Finance. HELOC and home equity loan rates, May 17, 2026. National average HELOC: 7.21%. National average home equity loan: 7.36%. https://finance.yahoo.com/

- Bankrate. Current HELOC and Home Equity Loan Rates, May 2026. National average HELOC: 7.26% (May 6, 2026). National average home equity loan: 8.03% (May 6, 2026). https://www.bankrate.com/

- Freddie Mac. Primary Mortgage Market Survey (PMMS). 30-year fixed-rate mortgage at 6.36%, May 14, 2026. https://www.freddiemac.com/pmms

- Fannie Mae Selling Guide. Cash-out refinance LTV requirements. https://selling-guide.fanniemae.com/

- Federal Housing Finance Agency. 2026 Conforming Loan Limits. $832,750 standard; $1,249,125 high-cost. https://www.fhfa.gov/

- HUD. FHA 2026 Loan Limits. $541,287 floor; $1,249,125 ceiling. https://www.hud.gov/

- Urban Institute Housing Finance Policy Center. ADU appraisal friction research. https://www.urban.org/

- Wall Street Journal Market Data. Prime rate 6.75% as of mid-May 2026. https://www.wsj.com/

- Various credit union surveys. Sub-7% introductory HELOC rates, May 2026.

- CalHFA. ADU Grant Program — Fully Allocated December 28, 2023. https://www.calhfa.ca.gov/

- NYC HPD / NYS HCR. Plus One ADU Program. Reopened March 18, 2026; application window through June 12, 2026. https://www.nyc.gov/

- City of Charlotte. Queen City ADU Program. Up to $80,000 forgivable with 50% match. https://www.charlottenc.gov/

- CDC Utah / Salt Lake City CRA. Backyard Keys Program. Up to $200,000 at 3% fixed. https://cdcutah.org/

- CFPB. Issue Spotlight on Home Equity Contracts. https://www.consumerfinance.gov/

- Fannie Mae Selling Guide Section B5-3.2-01. HomeStyle Renovation 75% as-completed value cap. https://selling-guide.fanniemae.com/

- Freddie Mac Single-Family Seller/Servicer Guide. CHOICERenovation down payment requirements. https://guide.freddiemac.com/

- Fannie Mae Selling Guide. HomeStyle Renovation 15-month completion requirement. https://selling-guide.fanniemae.com/

- HUD Mortgagee Letter 2024-13. FHA 203(k) modernization, effective November 4, 2024. https://www.hud.gov/

- Fannie Mae SEL-2025-10, announced December 10, 2025. UAD 3.6 ADU property eligibility, effective March 31, 2026. https://singlefamily.fanniemae.com/

- Freddie Mac Bulletin 2025-15, announced November 5, 2025; effective February 9, 2026. Manufactured-home ADUs. https://guide.freddiemac.com/

- Fannie Mae SEL-2025-10. HomeStyle Renovation upfront disbursements now up to 50% of total renovation costs. https://singlefamily.fanniemae.com/

- Freddie Mac Bulletin 2026-1, announced February 4, 2026. CHOICERenovation rental-income rule effective May 4, 2026. https://guide.freddiemac.com/

- HUD Mortgagee Letter 2023-17. FHA ADU rental income guidelines. https://www.hud.gov/

- Fannie Mae Selling Guide Section B3-3.8-01. ADU rental income qualifying income rules. https://selling-guide.fanniemae.com/

- Freddie Mac Single-Family Seller/Servicer Guide Section 5601.2. ADU rental income and eligibility. https://guide.freddiemac.com/

- Freddie Mac ADU Fact Sheet, February 2026. https://www.freddiemac.com/

- Fannie Mae Desktop Underwriter (DU) version 12.1, released weekend of March 21, 2026. Automated ADU rental-income rules. https://singlefamily.fanniemae.com/

- San Diego Housing Commission (SDHC). ADU Finance Program. https://www.sdhc.org/

- New York State Homes and Community Renewal (HCR). Plus One ADU Program. https://hcr.ny.gov/

- MassHousing. ADU Loan Program. https://www.masshousing.com/

- City of Boston Mayor’s Office of Housing. ADU Financial Assistance. https://www.boston.gov/

- Portland Bureau of Development Services. SDC Waiver for ADUs. https://www.portland.gov/

- City of Orlando. ADU Incentive Program. https://www.orlando.gov/

- California Department of Housing and Community Development. 2025 ADU Handbook. Impact fee exemptions for ADUs under 500 and 750 sq ft. https://www.hcd.ca.gov/

- California State Board of Equalization. New Construction Assessment. ADU additions generally assessable as new construction. https://www.boe.ca.gov/

Related ADU financing guides

- ADU Financing Options 2026: 8 Paths Compared →

- HELOC for ADU: Complete Guide →

- How to Finance an ADU Without Monthly Payments →

- RenoFi vs HELOC for ADU →

- Hometap vs HELOC for ADU →

- How to Finance an ADU With No Equity →

- Fannie Mae ADU Rules →

- Freddie Mac ADU Rules →

- ADU Grants: National & State Programs →

- California ADU Grant 2026 →