ADU Loan Requirements in 2026: Credit, Equity, Permits, and Program-by-Program Rules

By The Dwelling Index Editorial Team · Last updated: · Last verified: May 20, 2026 · Editorial standards →

The bottom line up front.

ADU loan requirements split into five gates: borrower qualification (credit, DTI, income, reserves), usable value (current equity or after-completed value), a legal or legalizable ADU, a documented project plan, and an appraisal that supports the value and any rent you're counting on. Across nearly every path, the program-set credit floor is roughly 580 (FHA) and the practical sweet spot is 680–720 to access best pricing. DTI ceilings cluster at 43%–50%. Most second-lien products cap combined loan-to-value (CLTV) at 80%–85%. As of November 16, 2025, Fannie Mae removed the published 620 minimum credit score from Desktop Underwriter® (DU) for new casefiles;7 manually underwritten loans still follow the published score minimums.

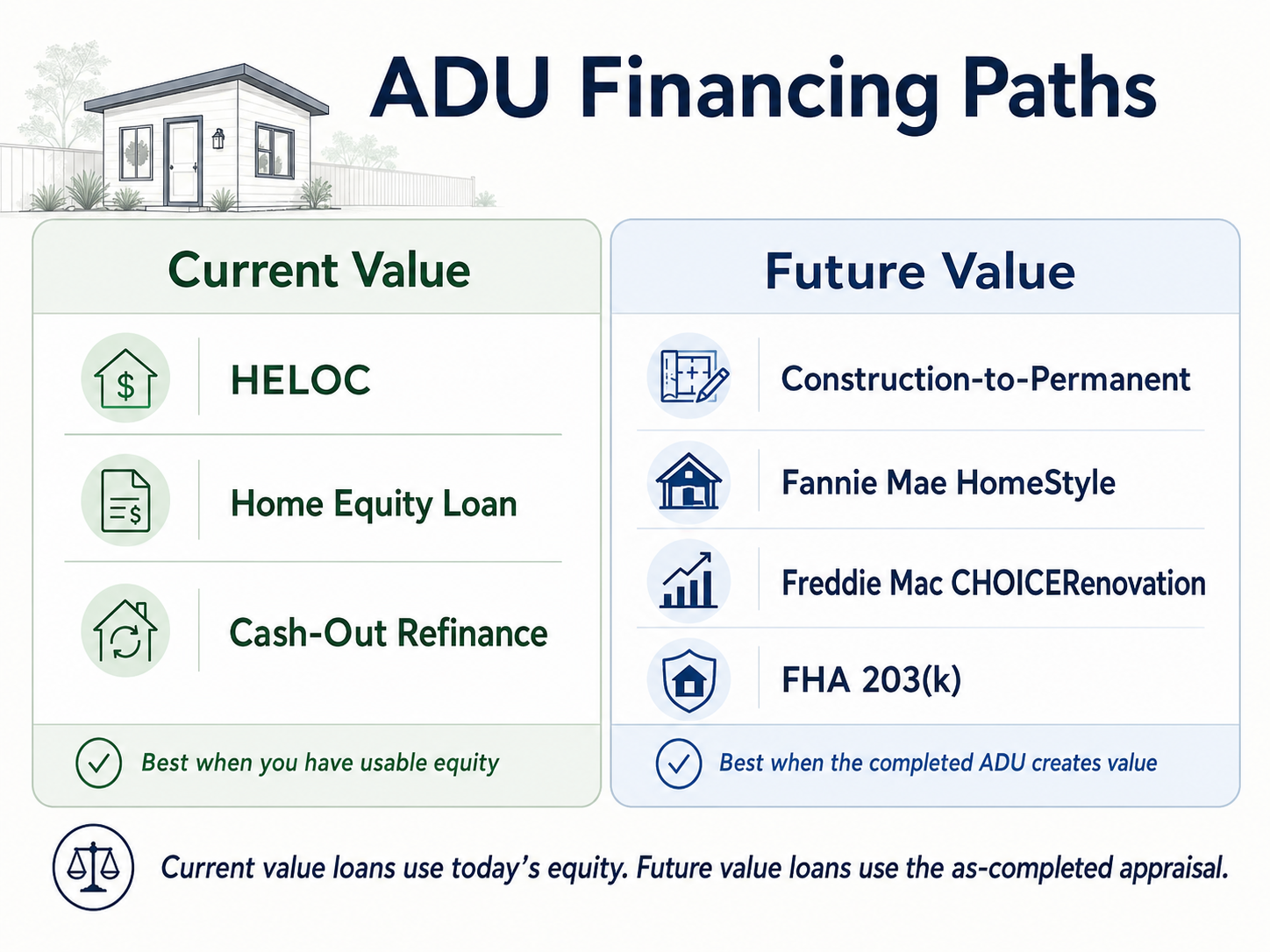

If you have strong current equity and a low first mortgage to protect, start with a HELOC or home equity loan. If your equity isn't enough, a construction-to-permanent loan, Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, or FHA 203(k) can underwrite against the property's future value. As of March 21, 2026, Fannie Mae's DU 12.1 lets you count up to 30% of qualifying income from one ADU's rental income on a 1-unit primary residence (purchase or limited cash-out refinance only).1

Who this is for: homeowners, ADU investors, and small builders researching which loan path fits their credit, equity, and project type.

See what your lot can actually support before any lender call.

Get your free ADU report — 60 seconds, no obligation.

Get your free ADU report — 60 seconds →

ADU loan requirements at a glance (May 2026)

| Path | Main approval test | Keeps 1st mortgage? | Value basis | Typical credit (overlay) | ADU rental income |

|---|---|---|---|---|---|

| HELOC | Current equity & CLTV (≤80–85%) | ✅ Yes | Current | 680–720 | Helps post-build, not pre-build |

| Home equity loan | Current equity + defined budget | ✅ Yes | Current | 620–680 | Same as HELOC |

| Cash-out refinance | Refinance underwriting | ❌ Replaced | Current | 620 conv. / 580 FHA | Eligible per program; FHA cash-out cannot use ADU rental income as effective income2 |

| Construction-to-permanent | Full project package | ❌ Usually replaced | Future (as-completed) | 680–720 conv. | Lender-specific |

| Fannie Mae HomeStyle Renovation | Renovation + 75% cost cap | ❌ Replaced | Future | DU: no published floor since Nov 16, 20257; manual UW: 620; lenders typically 620 | Up to 30% of total qualifying1 |

| Freddie Mac CHOICERenovation | Renovation + ADU appraisal rules | ❌ Replaced | Future | LPA Accept: no minimum Indicator Score; lenders typically 620 | 75% of lease, capped at 30% of total3 |

| FHA 203(k) Standard / Limited | FHA rehab + ADU rules | ❌ Replaced | Future, subject to FHA limits | 580 (3.5% down) / 500 (10% down) | 75% existing ADU / 50% new ADU under 203(k)4 |

| VA construction or renovation | VA eligibility + occupancy | ❌ Usually replaced | Future | No VA floor; lenders 580–620 | Generally not counted5 |

| USDA SFHGLP | Income, location, occupancy | ❌ Replaced | Future | Lender 640 | ⏳ Pending — proposed rule RHS-26-SFH-01006 |

Sources & verification dates in the Sources block.

⚠ The credit-score gotcha.

As of November 16, 2025, Fannie Mae removed the 620 minimum representative credit score from DU for new casefiles per Selling Guide Announcement SEL-2025-09.7 Freddie Mac's LPA Accept route also operates without a minimum Indicator Score. Manually underwritten loans still carry published minimum-score rules, and individual lenders, mortgage insurers, and specialty programs still impose their own overlays — most retail conventional lenders still apply a 620 floor. Always ask whether a number you're being quoted is an agency rule, an automated-underwriting outcome, or a lender overlay.

What we verified for this guide

Sources cross-checked on May 20, 2026.

- Fannie Mae HomeStyle Renovation Selling Guide B5-3.2-01 and B5-3.2-02 — 15-month completion window; 75% renovation-cost cap; manufactured-home renovation costs capped at 50% of as-completed value (prior $50,000 cap removed in SEL-2025-10)8·19

- Fannie Mae Selling Guide Announcements SEL-2025-08, SEL-2025-09, SEL-2025-10 and Pennymac Announcement 26-29 confirming DU 12.1 effective March 21, 20261·7·19

- Freddie Mac Accessory Dwelling Units Fact Sheet (February 2026) and Guide Bulletins 2025-15 and 2026-13·25

- HUD Mortgagee Letter 2023-17 (FHA ADU rental income, appraisal forms, 203(k) ADU treatment)4

- HUD's November 4, 2024 FHA 203(k) program changes raising the Limited cap to $75,000 and extending Standard/Limited completion to 12/9 months9

- Federal Register notice RHS-26-SFH-0100 (USDA proposed rule on income-producing ADUs; comments must be received by June 1, 2026)6

- Freddie Mac Primary Mortgage Market Survey (30-year fixed averaged 6.36% as of May 14, 2026)10

- Curinos / Yahoo Finance HELOC and home equity loan rate averages as of May 12, 202611

- CFPB consumer guidance on HELOCs and construction loans12

- California AB 2533 (signed September 28, 2024; effective January 1, 2025; applies to unpermitted ADUs and JADUs built before January 1, 2020)21

What are the five approval gates for an ADU loan?

An ADU loan is approved or denied on five things at once: you (borrower), the property, the ADU itself, the project plan, and the appraisal or rental analysis that supports value and income. Different loan paths weight these gates differently, but no path skips them.

Equity-based products (HELOC, home equity loan, cash-out refinance) live or die on the property's current value. Future-value products (construction-to-permanent, HomeStyle, CHOICERenovation, FHA 203(k)) live or die on the as-completed appraisal and the project package supporting it. A loan officer's first 15 questions are almost always pre-screening which gate is going to be the hardest one for your file. If you know the answer before you call, you save weeks.

- Gate 1 — Borrower.

- Credit score, debt-to-income ratio (DTI = monthly debt payments ÷ gross monthly income), income stability, employment history, assets, reserves, and any prior derogatory events (foreclosure, short sale, bankruptcy, late payments).

- Gate 2 — Property.

- Title, liens, occupancy plan, property type, insurance, and zoning. The ADU has to be on a lot that legally allows one — or that can be legalized — under your jurisdiction's rules.

- Gate 3 — ADU legality.

- The ADU must be legal, legal nonconforming ("grandfathered"), or in a no-zoning jurisdiction. Freddie Mac has a narrow exception path for illegal-zoning ADUs on 1-unit subject properties; most other programs do not.3 An illegal ADU usually has to be legalized before financing.

- Gate 4 — Project plan.

- Required when the loan funds construction or renovation. Plans, scope of work, line-item budget, signed construction contract, contractor's license and insurance, permit status, draw schedule, and contingency reserve. The CFPB describes construction loans as short-term loans funded "in advances as work progresses,"12 which is why the project package matters as much as your W-2s.

- Gate 5 — Appraisal & rental analysis.

- Equity-based products need a current-value appraisal that supports your CLTV. Future-value products need an as-completed appraisal. If you're counting on ADU rent to qualify, the appraisal must include market-rent analysis — and for Freddie Mac — at least one comparable sale with an ADU plus at least three comparable rentals, one of them with a rented ADU.3

How to know which gate matters most for you:

- Strong equity, low first mortgage → equity gate is easy; protecting the first mortgage should drive your path.

- Low equity, recent purchase → future-value gate; you need a real project package or a renovation/construction loan.

- Need rental income to qualify → Fannie/Freddie/FHA rule-set is your blocker.

- Unsure the lot can legally support an ADU → start with feasibility, not a lender.

Skip the guesswork. Confirm what your lot can actually support before any lender call.

Get your free ADU feasibility report →Credit score, DTI, and reserves — what lenders actually test

No single credit score is "the ADU loan requirement." FHA 203(k) accepts as low as 500 with 10% down or 580 with 3.5% down; HomeStyle and CHOICERenovation no longer carry a published agency floor on automated-underwriting paths as of November 16, 2025, though most lenders still overlay 620; HELOCs typically require 680–720 for the best pricing; the most competitive pricing across products usually opens at 740+.

Credit score thresholds: agency rule vs. lender overlay

| Program | Agency rule (May 2026) | Typical lender overlay |

|---|---|---|

| Fannie Mae HomeStyle / conventional (DU casefile) | No representative-credit-score minimum since Nov 16, 2025 for new DU casefiles7 | 620; 680–740 for best pricing |

| Fannie Mae (manually underwritten) | 620 minimum retained in the Selling Guide | 620+ |

| Freddie Mac CHOICERenovation / conventional (LPA Accept) | No minimum Indicator Score on LPA Accept | 620; 680–740 for best pricing |

| FHA 203(b), 203(k) Standard, 203(k) Limited | 500 with 10% down; 580 with 3.5% down4 | 580–620; many lenders won't go below 620 |

| VA (purchase, cash-out, construction) | No VA-set floor | 580–620 |

| USDA SFHGLP | No USDA-set floor | 640 |

| Home equity loan | None | 620–680 |

| HELOC | None | 680–720 for competitive pricing11 |

| Cash-out refinance | Program-set; FHA permits 500–579 within published LTV caps | 620 conventional; 580 FHA |

A lender overlay is a stricter rule the lender adds on top of the program rule. Even though Fannie and Freddie dropped published score floors on automated paths, retail lenders broadly continue to apply at least a 620 floor in practice on conventional ADU files.

DTI ceilings by program

- HomeStyle Renovation: Up to 50% via Desktop Underwriter (DU).

- CHOICERenovation: 45% typical; LPA decisions vary.

- FHA 203(k): 31% front-end / 43% back-end standard; up to 47/57 with documented compensating factors.13

- HELOC and home equity loan: 43% standard; some lenders flex to 50% with strong credit and income.

- VA: 41% benchmark plus residual income test (which can let you exceed 41%).

- USDA SFHGLP: 41%.

A common DTI mistake: forgetting to include the new loan's projected payment in the math. For a HomeStyle or 203(k), it's the new full PITIA (principal, interest, taxes, insurance, association dues). If you're at 42% today and the new loan adds another 4% of debt to income, you're over the line for everything but FHA with compensating factors.

Reserves and assets

- Conventional renovation (HomeStyle / CHOICERenovation): 2–6 months PITIA, depending on automated-underwriting findings and number of financed properties.

- FHA 203(k): 1 month PITIA for 1–2 unit; 3 months PITIA for 3–4 unit. If FHA ADU rental income is used to qualify on a 1-unit with ADU, HUD requires reserves equivalent to at least 2 months of PITI after closing.4

- HELOC and home equity loan: Lender-specific; many require 2 months PITIA.

- Construction-to-permanent: Typically 6+ months PITIA, plus the 10–15% contingency reserve required for two-to-four-unit HomeStyle files.8

If your ADU project will require you to live elsewhere during construction, your reserves also need to support the alternate housing cost.

How much equity (or future value) do you actually need?

The right question isn't "what's the down payment?" — it's "what value am I borrowing against?" Equity products lend against your home's current value at 80–85% combined loan-to-value. Future-value products (construction, HomeStyle, CHOICERenovation, 203(k)) lend against the home's as-completed value, typically capped at 95–110% of that future appraisal, with down payments as low as 3% on conventional and 3.5% on FHA.

Current-value lending: HELOC, home equity loan, cash-out refinance

Most lenders require CLTV at 85% or less for a HELOC.14

Max combined loan balance @ 80% CLTV = $700,000 × 0.80 = $560,000

Less your existing first mortgage = – $400,000

Usable HELOC / home equity loan limit = $160,000

Worked example. Your home appraises at $700,000. Your first mortgage balance is $400,000. Usable HELOC limit is $160,000 at 80% CLTV. If your ADU is going to cost $300,000 to build, current equity at this property doesn't cover it on a first-or-second-position equity product. You either pivot to a future-value loan, contribute personal cash, or stage the build.

Future-value lending: construction-to-permanent, HomeStyle, CHOICERenovation, FHA 203(k)

These products are scored against the appraised value after the ADU is built.

- Fannie Mae HomeStyle Renovation: Eligible renovation funds capped at 75% of the lesser of (purchase price + renovation cost) or the as-completed appraised value for purchases; 75% of as-completed appraised value for refinances. For manufactured homes, renovation costs are limited to 50% of the as-completed appraised value (the prior $50,000 cap was removed in SEL-2025-10).8·19 LTV up to 97% on a 1-unit primary residence. Renovation work must be completed within 15 months of closing.8

- Freddie Mac CHOICERenovation: Comparable structure; up to 97% LTV on 1-unit primary; new specificity on qualifying rental income for CHOICERenovation applications received on or after May 4, 2026 per Bulletin 2026-1.15

- FHA 203(k) Standard: Loan amount limited to lesser of (purchase + reno) or 110% of as-completed value, subject to FHA county loan limits. 2026 FHA limits range from $541,287 in low-cost counties to $1,249,125 in high-cost counties for single-family.13

- FHA 203(k) Limited: Cap raised to $75,000 in renovation funds (effective for FHA case numbers assigned on or after November 4, 2024); completion within 9 months; HUD consultant not required.9

For new-construction ADUs financed under construction-to-permanent, Fannie Mae allows a construction period not to exceed 12 months in a single phase and not to exceed 18 months total across phases.16

The qualification matrix — by program

The eight ADU financing paths each have their own credit, DTI, equity/LTV, occupancy, documentation, ADU-specific overlay, and rental-income rule. The matrix below is assembled from primary-source documentation. Use it as a shortlist tool, not a substitute for an underwriter.

Fannie Mae HomeStyle Renovation

| Item | Requirement | Source |

|---|---|---|

| Property (lenders not using UAD 3.6) | 1-unit primary residence with one ADU; ADU not eligible on 2-4 unit primary; multiple ADUs not allowed17 | Fannie Mae ADU page |

| Property (lenders using UAD 3.6, effective March 31, 2026)19 | 1-unit primaries may have up to three ADUs; 2–3 unit may include ADUs up to four total dwelling units; standard MH primary may include one real-property ADU; MH Advantage may include multiple ADUs up to four total dwellings | SEL-2025-10; UAD 3.6 Policy Supplement |

| Credit score | DU: no representative-credit-score minimum since Nov 16, 20257; manually underwritten: 620 minimum retained; lender overlay typically 620. Best pricing 740+ | SEL-2025-09; lender disclosures |

| DTI | Up to 50% via DU | Lender disclosures |

| Down payment | 3% with HomeReady + HomeStyle at 95.01%–97% LTV (does not require first-time-buyer status)8; 5% standard on 1-unit primary; 15% on 2-unit; 25% on investment | Selling Guide B5-3.2-028 |

| LTV | Up to 97% on 1-unit primary | Fannie Mae HomeStyle product page |

| Renovation funds cap | 75% of (purchase + reno) or as-completed value, whichever is less (purchase); 75% of as-completed value (refinance). Manufactured-home renovation costs capped at 50% of as-completed value (prior $50,000 cap removed in SEL-2025-10)19 | HomeStyle FAQs8; SEL-2025-10 |

| Completion | 15 months from closing | Selling Guide B5-3.2-018 |

| Contractor | Required (limited DIY on 1-unit owner-occupied at ≤10% of as-completed value; inspections required on items >$5,000). Not related to borrower | HomeStyle FAQs8 |

| ADU rental income | Up to 30% of total qualifying income from one ADU's rent on a 1-unit principal residence; purchase or limited cash-out refinance only. DU 12.1 enforces effective March 21, 20261 | Selling Guide B3-3.1-08; Pennymac 26-29 |

| Appraisal | As-completed; market rent reported on Form 1007 (UAD 2.6) or in the Rental Information section / Rental Comparison Grid (UAD 3.6) when ADU income is used22 | Fannie Mae Appraiser Update |

Plain-English decoder of the 75% cap. If you're buying a $400,000 fixer with $200,000 in renovations and the as-completed appraisal values the property at $640,000, your eligible renovation funds are capped at 75% of $600,000 (lesser of purchase+reno or as-completed) = $450,000 — well above your $200,000 budget, so the cap won't bite. The cap prevents renovations bigger than the property can support.

Freddie Mac CHOICERenovation

| Item | Requirement | Source |

|---|---|---|

| Property | 1-, 2-, or 3-unit eligible; legal, legal nonconforming, or no-zoning OK; illegal ADUs OK in narrow exception on 1-unit subject properties | Freddie ADU Fact Sheet (Feb 2026)3 |

| Loan purpose (ADU income used on 1-unit primary) | Purchase or no-cash-out refinance only | Freddie ADU Fact Sheet3 |

| Credit score | LPA Accept: no minimum Indicator Score; lender overlay typically 620 | Freddie Guide Section 5203.2 |

| DTI | 45% typical via LPA | Lender disclosures |

| LTV | Up to 97% on 1-unit primary | Freddie Selling Guide |

| ADU rental income | Up to 75% of lease, capped at 30% of total qualifying income; landlord education required on purchase unless borrower has ≥1 year investment-property or ADU rental-management experience3 | Freddie ADU Fact Sheet3 |

| Appraisal | At least 1 comparable sale with ADU; at least 3 comparable rentals (1 with rented ADU); automated collateral evaluation (ACE) not acceptable when ADU rental income is used | Freddie ADU Fact Sheet3 |

| New CHOICERenovation rental income specificity | Applications received on or after May 4, 2026 | Bulletin 2026-115 |

FHA 203(k) Standard

| Item | Requirement | Source |

|---|---|---|

| Property | 1-unit Single Family with ADU treated as 1-unit; 2+ unit with ADU treated as additional unit per HUD 4000.1.18 Property must be ≥1 year old | HUD Handbook 4000.1 |

| Credit score | 500 with 10% down / 580 with 3.5% down4 | NerdWallet; HUD 4000.1 |

| DTI | 31/43 standard; up to 47/57 with compensating factors13 | Plaza FHA 203(k) Guidelines |

| Down payment | 3.5% | HUD |

| Maximum loan | Lesser of (purchase + reno) or 110% of as-completed value, subject to FHA limits ($541,287 low-cost to $1,249,125 high-cost in 2026)13 | Rocket Mortgage; The Mortgage Reports |

| Completion | 12 months for Standard (effective Nov 4, 2024)9 | Diamond Residential |

| HUD consultant | Required for Standard | HUD; Plaza |

| Reserves (ADU rental income used) | At least 2 months PITI after closing required when ADU rental income is used to qualify on 1-unit with ADU4 | HUD ML 2023-17 |

| ADU rental income | 75% of FMR or lease (existing ADU); 50% of lesser of FMR or lease when new ADU added under 203(k).4 Capped at 30% of total monthly effective income20 | HUD ML 2023-17 |

| Eligible improvements | Standard 203(k) explicitly lists adding an ADU attached to the existing structure and renovating an existing ADU4 | HUD ML 2023-17 |

FHA 203(k) Limited

| Item | Requirement | Source |

|---|---|---|

| Scope | Minor remodeling and nonstructural repairs only. Major work, structural changes, and adding an attached ADU to the existing structure require Standard 203(k)18·21 | HUD 203(k) program page |

| Renovation cap | $75,000 (raised from $35,000 effective November 4, 2024); includes reserves and inspection fees9 | Diamond Residential |

| Completion | 9 months | Diamond Residential |

| HUD consultant | Not required (optional) | HUD |

Decoder. For most ground-up detached ADU builds, 203(k) Limited won't fit — the scope rules out structural work and major additions. Limited is best for a finished interior remodel paired with a cosmetic garage conversion where the conversion itself doesn't trigger structural work. Standard 203(k) is the right fit for major rehab + ADU addition.

HELOC (home equity line of credit)

| Item | Typical requirement | Source |

|---|---|---|

| Credit score | 680–720 at most lenders for best pricing11 | LendEDU; Curinos |

| DTI | 43% standard; 50% with compensating factors | LendEDU |

| CLTV | 80–85% standard | Bank of America14 |

| Rate type | Variable, tied to Prime | CFPB |

| Risk | CFPB notes HELOCs use the home as collateral and may be frozen or reduced if home value or finances change12 | CFPB |

May 2026 rate snapshot (not an offer; subject to borrower/lender/property terms). As of May 12, 2026, the national average was 7.21% on HELOCs and 7.36% on fixed home equity loans per Curinos data via Yahoo Finance.11 Variances of 200–300 basis points across lenders for the same applicant are common. Shop at least three lenders.

Home equity loan (fixed-rate second mortgage)

| Item | Typical requirement |

|---|---|

| Credit score | 620–680 (some lenders 740 for best pricing)23 |

| DTI | 43% standard |

| Equity | At least 15–20% remaining after the loan; CLTV typically 80–85% |

| Rate type | Fixed; lump sum at closing |

| Best when | Budget is defined; you want payment certainty |

Cash-out refinance

| Item | Typical requirement | Source |

|---|---|---|

| Credit score | 620 conventional; 580 FHA; 620 VA | Lender disclosures |

| DTI | 43–50% | Lender disclosures |

| LTV | Up to 80% conventional; FHA per published cash-out caps; up to 100% on VA cash-out for eligible vets | HUD 4000.1; VA |

| ADU rental income | Eligible under Fannie's limited cash-out refi (per March 2026 rule, not full cash-out); FHA cash-out refi cannot use ADU rental income as effective income on a 1-unit with ADU2 | HUD ML 2023-17; Pennymac 26-29 |

| Closing costs | 2–5% of new loan amount | Lender disclosures |

⚠ The first-mortgage trap.

A cash-out refi replaces your first mortgage at today's market rate. The 30-year fixed averaged 6.36% as of May 14, 2026.10 If you locked at 3% in 2021, the blended cost of "cheap" ADU money can vaporize the rental upside for years. Run the all-in math before pulling the trigger.

Construction-to-permanent loan

| Item | Typical requirement |

|---|---|

| Credit score | 680–720 conv. / 580 FHA / 620 VA (lender) |

| Down payment | 10–25% conv.; 0% VA; 3.5% FHA |

| DTI | 43–45% |

| Project package | Detailed plans, signed contractor bid, permits or proof permits are in process, draw schedule, contingency reserve |

| Contractor | Licensed, lender-approved, not a relative |

| Fannie Mae rule | Construction period not to exceed 12 months in a single period, not to exceed 18 months total16 |

VA construction or renovation

| Item | Requirement | Source |

|---|---|---|

| Eligibility | Active duty / veterans / surviving spouses with a Certificate of Eligibility (COE) | VA |

| Credit score | No VA-set floor; lenders 580–620 | Lender overlays |

| DTI | 41% benchmark + residual income test | VA Lenders Handbook |

| Down payment | $0 for entitlement | VA |

| Occupancy | Required: the borrower must occupy the property as a primary residence5 | VA |

| ADU rental income for qualifying | Generally not counted on VA loans for the subject property's ADU5 | Lender practice; verify with your lender |

USDA Single Family Housing Guaranteed Loan Program

| Item | Current rule | Proposed (RHS-26-SFH-0100) |

|---|---|---|

| Income-producing ADUs | Not allowed | Would be allowed (single or multiple income-producing ADUs)6 |

| Non-income (multigenerational) ADUs | Already allowed | Continues |

| Status (as of May 20, 2026) | — | Published March 31, 2026; comments must be received by June 1, 2026. Final rule not yet published6 |

| Lender overlay | 640 | — |

| DTI | 41% | — |

Practical answer for May 2026: USDA currently blocks income-producing ADUs. Multigenerational (family) ADUs are allowed. Watch for the final rule before banking on USDA for a rental ADU.

Affiliate link — see disclosure above. Approval depends on credit, income, property, ADU scope, appraisal, and lender underwriting; not guaranteed.

Compare mortgage and renovation financing paths through our research partner.

Explore mortgage-backed ADU financing options →Can ADU rental income help you qualify for a loan?

Yes, under specific conditions — and this is the most consequential change in ADU lending in years. As of March 21, 2026 (Desktop Underwriter® version 12.1), Fannie Mae allows up to 30% of qualifying income to come from one ADU's rental income on a 1-unit principal residence (purchase or limited cash-out refinance only).1 Freddie Mac allows 75% of lease, capped at 30% of total qualifying.3 FHA allows 75% on existing ADUs or 50% on a new ADU added under a 203(k), capped at 30% of total monthly effective income.4 VA generally does not count ADU rental income for qualifying. USDA's current rule blocks income-producing ADUs; the proposed rule (RHS-26-SFH-0100) would change that.6

Side-by-side: the three big rule-sets

| Element | Fannie Mae | Freddie Mac | FHA |

|---|---|---|---|

| Effective | DU 12.1 weekend of March 21, 2026 (manual UW allowed since SEL-2025-08, Oct 8, 2025)1 | Already in effect; new specificity for CHOICERenovation 5/4/202615 | HUD ML 2023-17 in effect4 |

| Property | 1-unit principal residence only | Subject 1-unit primary residence (for ADU income carve-out) | 1-unit Single Family with ADU |

| Loan purpose | Purchase or limited cash-out refi only | Purchase or no-cash-out refinance only when ADU income on subject 1-unit primary is used3 | Purchase, refi, 203(k); FHA cash-out refi cannot use ADU rental income as effective income2 |

| Rent calculation | 75% of gross monthly rent (via Form 1007 / Form 1025); then capped at 30% of total qualifying1·24 | 75% of lease3 | 75% (existing ADU) / 50% (new ADU under 203(k))4 |

| Cap on qualifying income | 30% of total qualifying1 | 30% of total qualifying3 | 30% of total monthly effective income20 |

| Landlord experience | Not required for purchase; PITIA cap applies for first-time landlords | Required (purchase) unless ≥1 year investment-property or ADU rental-management experience3 | Not required |

Plain-English decoder

If your household gross income is $8,000/month and you're buying a 1-unit primary with an existing ADU using a Fannie HomeStyle loan:

- The ADU rent you can count is capped at 30% of your total qualifying income post-rule. Total qualifying becomes up to $10,400 ($8,000 base + $2,400 in counted ADU rent).

- The ADU itself might rent for $3,000 — but only $2,400 counts for DTI math.

- That additional $2,400 typically expands your maximum loan amount by roughly $50,000–$120,000, depending on rate and DTI room.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Why your expected ADU rent may not count at all

The rent you expect from the ADU is not automatically lender-usable income. If any of these is true, it may be ignored or reduced:

- The ADU is not legally rentable in your jurisdiction.

- The ADU is illegal-zoning (not legal nonconforming) — Freddie has a narrow exception, others don't.3

- The appraisal cannot find ADU rental comps in your market.

- The transaction type isn't eligible (Fannie cash-out refi; FHA cash-out refi).2

- The program caps the income (the 30% rule applies even when the rent could be much higher).

- You're using a VA loan (generally not counted).5

- You're using a USDA loan (currently blocked by 7 CFR 3555 pending final rule).6

See whether ADU rent could realistically help you qualify in your zip code.

Start with your free ADU feasibility report →The ADU loan documentation checklist — what each loan type actually requires

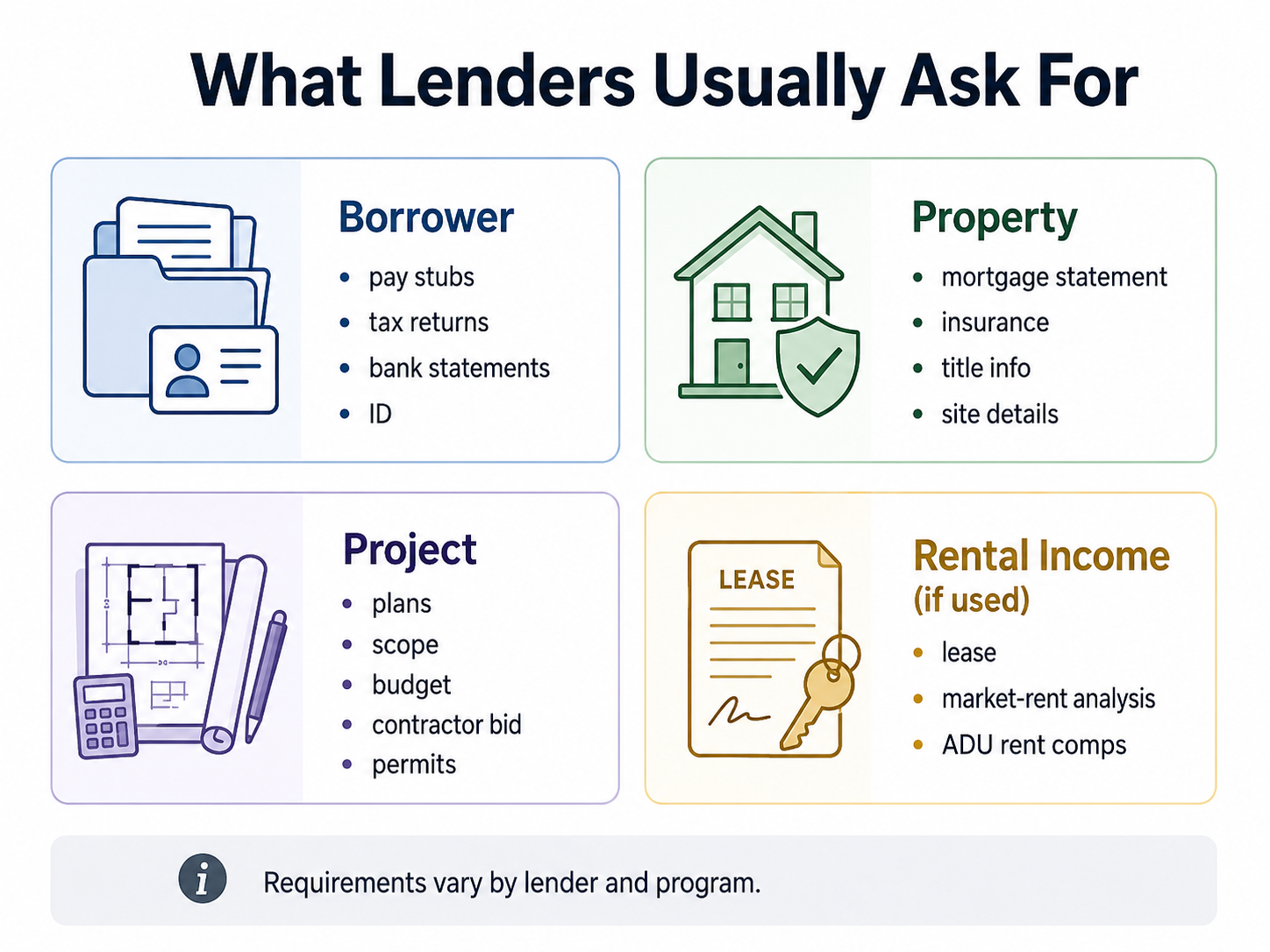

Documentation falls into three buckets: about you, about the property, and about the project. Equity loans (HELOC, home equity loan) need primarily the first two. Construction and renovation loans (HomeStyle, CHOICERenovation, FHA 203(k), construction-to-permanent) add a project package of 8–12 additional documents. If you're using ADU rental income to qualify, add another 4–5 items.

Universal stack — about you (always required)

- Government-issued photo ID

- Social Security number

- Two most recent pay stubs

- W-2s for the past 2 years

- Federal tax returns for the past 1–2 years (2 years if self-employed)

- Two months of bank statements for all accounts

- Two-year residential history

- Two-year employment history (gaps explained)

- Documentation of any non-W-2 income (pensions, Social Security, child support, existing rental income)

- Credit authorization

- Statements for any other liabilities or properties

About the property

- Current homeowners insurance declarations page

- Most recent property tax bill

- Current mortgage statement(s)

- Legal description / title commitment

- HOA documentation, if applicable

About the project (renovation, construction, future-value loans)

- Signed construction contract with contractor

- Detailed scope of work and line-item budget

- Contractor's license, insurance, references

- Stamped architectural plans + elevations

- Site plan

- Local building permit (or proof permits are in process)

- Project timeline with milestones tied to draws

- Contingency reserve calculation (typically 10–15%)

- Plans for utility connections (sewer/septic/water/electric)

When ADU rental income is used to qualify

- Existing lease (signed, dated, in U.S. dollars)

- Appraisal with Form 1007 / Form 1025 (UAD 2.6) or UAD 3.6 Rental Information section + Rental Comparison Grid22

- Rental history (12 months of cancelled checks or bank deposits) if existing rental

- Schedule E from federal tax returns (if previously declared rental income)

- For Freddie Mac CHOICERenovation purchase + rental-income use: proof of landlord education completion OR documentation of ≥1 year management history

Additional for FHA 203(k) Standard

- HUD consultant write-up (Specification of Repairs)

- Energy or structural reports as required by the lender

- Termite report (in most states)

Save 10–15 hours assembling the right docs the first time.

Download the Free ADU Starter Kit — document checklist, budget worksheet, and lender question script.

Download the Free ADU Starter Kit →Will your ADU itself qualify? Zoning, permits, appraisal, and the illegal-ADU trap

Your personal qualifications are only half the test. The ADU must clear three gates of its own: zoning compliance (legal, legal nonconforming, or in a no-zoning jurisdiction), a structural definition that meets the program's ADU rules (independent living, sleeping, cooking, and bathroom facilities with separate ingress/egress), and an appraisal that finds at least one comparable sale with an ADU within a reasonable distance. The illegal-ADU question is the single most common dealbreaker.

Zoning compliance — the four categories

- Legal ADU. Built with a permit, complies with current zoning. ✅ All programs accept.

- Legal nonconforming ("grandfathered") ADU. Built legally under prior rules; protected. ✅ All programs accept.

- No-zoning jurisdiction. Some rural areas. ✅ Freddie Mac explicitly allows.3 Verify the others.

- Illegal ADU. No permit or in violation of current rules. ❌ Fannie, FHA, VA, USDA reject. Freddie Mac has a narrow exception path on 1-unit subject properties in specific cases.3

If you inherited or bought a property with an "unpermitted in-law unit," pull the building department records before you call a lender. California's AB 2533 — signed September 28, 2024, effective January 1, 2025 — creates a statewide amnesty for unpermitted ADUs and JADUs built before January 1, 2020, subject to Health and Safety Code §17920.3 substandard-housing limits.21 See our California ADU laws guide →

The ADU structural definition by program

Fannie Mae defines an ADU as a smaller additional living space on the same lot as a single-family home that includes "space for living, sleeping, cooking and bathrooms independent of the primary residence," accessible without going through the primary residence, with some expectation of privacy.17

| Element | Fannie Mae (UAD 2.6) | Fannie Mae (UAD 3.6 lenders, effective Mar 31, 2026)19 | Freddie Mac | FHA / HUD |

|---|---|---|---|---|

| Independent kitchen | Required | Required | Required | Required |

| Independent bathroom | Required | Required | Required | Required |

| Separate ingress/egress | Required | Required | Required | Required |

| Primary may be a manufactured home | ❌ | ✅ (single ADU on standard MH; multiple on MH Advantage)19 | ✅ if multiwide MH (Bulletin 2025-15)25 | ❌ |

| Multiple ADUs on property | ❌ | ✅ (1-unit primary: up to 3 ADUs; 2-3 unit: up to 4 total dwellings)19 | One ADU on 1-, 2-, 3-unit | Per HUD 4000.1 |

The appraisal problem nobody warns you about

When ADU rental income is being used to qualify, the appraiser must find a comparable sale with an ADU, and — for Freddie Mac — at least three comparable rentals with at least one rented ADU.3 In high-ADU markets (much of California, Portland, Seattle, Denver), this is workable. In markets with few documented ADU sales, the appraiser can fail to find comps, and your loan goes from approved to suspended mid-process.

Mitigation: ask your lender three questions upfront — (1) does your appraisal panel include ADU-experienced appraisers in this zip code; (2) what's the recent ADU comp count; (3) what's the rebuttal process if the as-completed value comes in low? If they can't answer, you're shopping the wrong lender for an ADU file.

The 75% vacancy haircut

When you submit a lease or market-rent estimate, Freddie Mac and FHA's appraisal-based paths apply a 25% vacancy/expense haircut — meaning they count 75% of the rent. A $2,000/month lease counts as $1,500/month for DTI math, then is further capped at 30% of total qualifying. This isn't a lender's choice; it's program-baked.

Which ADU loan requirements change by project type?

Detached ADUs, garage conversions, attached additions, prefab/modular ADUs, manufactured-home ADUs, basement ADUs, and Junior ADUs (JADUs) trigger different requirements around appraisal, zoning, building code, and program eligibility. The path that's cheapest on a detached ADU may not be available for a JADU at all, and vice versa.

For detailed cost ranges by ADU type and market, see our ADU cost per square foot guide and how much does an ADU cost? — the requirements section here focuses on what changes for the loan, not the build.

Detached ADU (DADU — a standalone backyard unit)

- Highest project complexity: site work, foundation, utility laterals, setbacks, and the deepest project documentation.

- Best-fit lanes: HELOC or home equity loan if equity is strong; construction-to-permanent or HomeStyle / CHOICERenovation if future value is needed.

- Appraisal challenge: rural and suburban markets with few DADU sales can produce low as-completed values.

Garage conversion

- Typically the lowest-cost ADU type because the foundation, walls, and roof exist.

- Triggers parking replacement, fire-separation, ceiling-height, and habitability rules.

- Best-fit lanes: HELOC, home equity loan, FHA 203(k) Limited only when the work is eligible nonstructural / minor, stays within the $75,000 Limited cap, and can be completed in the 9-month window.

Attached ADU (addition off the primary home)

- HUD Mortgagee Letter 2023-17 explicitly lists adding an attached ADU under Standard 203(k) eligible improvements.4

- Triggers exterior matching, structural review, and possible second-egress requirements.

- Best-fit lanes: HomeStyle Renovation, CHOICERenovation, FHA 203(k) Standard.

Prefab or modular ADU

- Classification (real property vs. personal property/chattel) controls financing.

- Fannie Mae HomeStyle: Manufactured-home renovation costs capped at 50% of as-completed value under SEL-2025-10 (the prior $50,000 dollar cap was removed).19

- Freddie Mac CHOICERenovation: MH ADU permitted with a multiwide MH primary per Bulletin 2025-15.25

- Best-fit lanes: HELOC if owned outright; construction-to-permanent if first-time install; HomeStyle Renovation or CHOICERenovation for new-build packages.

Junior ADU (JADU)

- Defined in California law as an interior conversion (typically a converted bedroom + efficiency kitchen) up to ~500 sq ft within the existing single-family home footprint.

- Lenders treat a JADU as an ADU only if it meets the full structural test (independent kitchen, bath, sleeping area, separate ingress/egress).

- Best-fit lanes: HELOC or home equity loan (lowest friction); HomeStyle Renovation and FHA 203(k) Limited can work when the scope stays small and program rules fit.

Basement ADU

- Triggers ceiling height, egress window, and waterproofing rules under the International Residential Code (IRC).

- In flood-prone jurisdictions (e.g., NYC's Plus One ADU program), basement ADU eligibility is restricted to non-Special Coastal Risk District properties and outside specific flood zones.26

Special cases: VA loans, USDA's pending rule, manufactured-home ADUs, JADUs, investment property

VA loans and ADUs

Eligible veterans can use VA financing to buy or refinance a property with an ADU and rent the unit not used as their primary residence. Mechanics in practice:

- $0 down for entitlement-eligible borrowers.

- Occupancy of the property as a primary residence is required.5

- ADU rental income from the subject property generally doesn't count for qualifying on a VA loan; confirm with your VA-experienced lender.5

- VA construction loans technically exist; very few lenders offer them.

The most common VA + ADU pattern: buy with VA financing, occupy for the required period, then use a HELOC or other equity product to fund the ADU.

USDA's proposed rule (RHS-26-SFH-0100)

The USDA's Single Family Housing Guaranteed Loan Program is in the middle of rulemaking that, if finalized, would change ADU treatment substantially. The proposed rule:

- Amends 7 CFR 3555.102(b) and 7 CFR 3555.201(b)(2) to permit financing of single-family homes with single or multiple income-producing ADUs.6

- Was published in the Federal Register March 31, 2026; comments must be received by June 1, 2026. The final rule has not been published as of May 20, 2026.

Manufactured-home ADUs

- Fannie Mae HomeStyle (UAD 2.6): MH ADU allowed when the primary residence is stick-built. The MH ADU must be classified as real property after installation per Selling Guide B5-2-05.8

- Fannie Mae HomeStyle (UAD 3.6 lenders, effective March 31, 2026): Standard MH primaries may include one real-property ADU; MH Advantage primaries may include multiple ADUs up to four total dwellings.19

- Freddie Mac (Bulletin 2025-15): Allows the primary dwelling to be a multiwide manufactured home (including a CHOICEHome) with an MH ADU, effective February 9, 2026.25

Junior ADUs (JADUs) — financing tips

JADUs are usually the cheapest ADU to permit and build because they reuse existing walls and foundation. Most JADU files close on a HELOC or home equity loan because the scope is small enough to fit comfortably within current equity. For HomeStyle Renovation or 203(k), confirm the JADU meets the full ADU structural test before counting on its rental income.

Investment property ADUs

- Fannie Mae's March 2026 rule applies only to 1-unit primary residences. Investment properties with ADUs are not eligible for the new 30%-of-qualifying-income rule.1

- Freddie Mac is more permissive — ADU rental income may be considered on investment properties under Guide Chapter 5306.3

- FHA generally requires owner-occupancy.

Lender overlays: the gap between agency rules and reality

A lender overlay is a stricter requirement the lender adds on top of the program rule. Even though Fannie and Freddie removed published score floors on their automated paths, retail lenders broadly continue to require at least 620 conventional on a HomeStyle / CHOICERenovation file in practice. Even though FHA permits 500 with 10% down, most lenders won't go below 580. Knowing what overlays your lender uses — before you apply — is the single fastest way to avoid a wasted month.

Common ADU-specific overlays

| Overlay | Why lenders apply it |

|---|---|

| FICO floor of 620 conventional, 580 FHA | Risk management beyond the agency floor |

| 24-month rental history before counting ADU income | Risk of first-time landlord vacancy |

| No manual underwriting | Process efficiency |

| No FHA 203(k) Standard | Complexity of HUD consultant management |

| No manufactured-home ADUs | Appraisal and title complexity |

| Local-market overlay (no ADU files in zip codes with limited ADU comp sales) | Appraisal risk |

| Self-employed requires 2 years of returns even when DU says 1 | Risk |

| 3–6 months PITIA reserves on top of program rule | Risk |

Three questions that flush out overlays before you apply

- "What's your minimum FICO for a HomeStyle Renovation (or CHOICERenovation, or 203(k)) with an ADU?"

- "Do you have ADU-type or zip-code overlays in [your market]?"

- "What's the appraisal panel's experience with ADU comparable sales here?"

Get the answers by email. Shop three lenders before submitting any hard credit pull.

Affiliate link — see disclosure. Approval depends on credit, income, property, ADU scope, appraisal, and lender underwriting; not guaranteed.

Compare mortgage and renovation financing paths and current lender requirements.

Explore mortgage and renovation loan options →Why ADU loan applications get delayed or denied

ADU financing is genuinely harder than financing a primary residence. Renovation loans add a contractor-coordination layer most borrowers underestimate. Construction loans are draw-managed. Appraisals can fail in markets without ADU comps. These aren't reasons to abandon the project — they're reasons to plan. Most homeowners who close on ADU financing work through at least one of these issues during the process.

| Blocker | Why it matters | What to do |

|---|---|---|

| Not enough current equity | HELOC / home equity loan / cash-out can't cover the project | Test as-completed-value financing (HomeStyle, CHOICERenovation, 203(k), construction loan) |

| Existing low first-mortgage rate | Refi-based loan can wipe out the rental upside | Compare second-lien (HELOC, HEL) vs. renovation/construction blended cost |

| Missing permits or plans | Renovation / construction lender can't underwrite scope | Push feasibility and design forward before applying |

| Contractor not lender-acceptable | Draws require license, insurance, and lender vetting | Pre-vet contractor before underwriting |

| ADU not legally rentable | Rental income won't count | Confirm zoning + rental rules; legalize if possible (in California, see AB 2533) |

| Appraisal lacks ADU comps | Value or rent support is weak | Ask lender for ADU-experienced appraiser; document recent local sales |

| FHA Limited scope mismatch | Limited 203(k) can't fund major or structural work | Switch to Standard 203(k) or another lane |

| Self-employed <2 years | Conventional renovation likely blocked | Wait or use a non-QM / bank-statement program |

| Recent quitclaim or title change | Refinance and limited cash-out seasoning rules can block | Confirm seasoning before applying |

If any of these is your situation, the right next step usually isn't to apply for a different loan — it's to fix the underlying issue. Most can be solved in 30–90 days.

Start by confirming what your lot can actually support — that resolves half the issues above.

Get your free ADU feasibility report →How long does ADU loan approval take?

Equity loans are usually faster than construction and renovation loans. Exact timing depends on borrower-document completeness, permit and design stage, contractor readiness, appraisal scheduling, rent-comparable availability, draw administrator setup, and title/lien review. The ranges below are editorial planning estimates assembled from current lender-published timelines reviewed May 2026; your jurisdiction can add or remove weeks.

| Path | Editorial planning range (application → first disbursement) |

|---|---|

| HELOC | 2–4 weeks |

| Home equity loan (fixed) | 3–5 weeks |

| Cash-out refinance | 30–45 days |

| FHA 203(k) Limited | 30–45 days |

| Fannie Mae HomeStyle | 45–60 days |

| Freddie Mac CHOICERenovation | 45–60 days |

| FHA 203(k) Standard | 60–90 days |

| Construction-to-permanent | 60–90 days from application; first draw at construction kickoff |

These are not guarantees. Permits, appraisal scheduling, contractor readiness, and lender backlog can each add 2–6 weeks.

The 30-day pre-application protocol

The fastest-approved borrowers usually spend the 30 days before application doing five things. Use it as a checklist.

Week 1 — Documents and credit

- Pull free credit reports from all three bureaus.

- Dispute errors.

- Pay down credit cards to <30% utilization.

- Avoid new credit inquiries.

- Gather the borrower-stack documents (items 1–11 above).

Week 2 — Property and feasibility

- Run your feasibility check on the lot.

- Pull building department records for any existing ADU.

- Confirm zoning and ADU permitting path.

- Get 2–3 contractor bids if building.

Week 3 — Lender shopping

- Identify three lenders (at minimum one bank, one credit union, one mortgage broker).

- Ask each the three overlay questions.

- Compare APRs (not just headline rates).

Week 4 — Submit and underwrite

- Submit to the best fit.

- Respond to every document request within 24 hours.

- Lock the rate at the right milestone (typically once the appraisal is in).

Frequently asked questions

- What credit score do I need for an ADU loan?

- It depends on the program. FHA 203(k) accepts as low as 500 with 10% down or 580 with 3.5% down. Conventional renovation loans on automated underwriting (HomeStyle DU, CHOICERenovation LPA Accept) no longer carry a published agency floor as of November 16, 2025, but manually underwritten conventional loans still carry the 620 minimum and most lenders still overlay 620 in practice. Home equity loans typically require 620; HELOCs typically require 680–720 for the best pricing. Best pricing across nearly all products opens at 740+.

- How much equity do I need to finance an ADU?

- For HELOCs and home equity loans, you typically need at least 15–20% equity remaining after the new loan (CLTV at 80–85%). For future-value loans (HomeStyle, CHOICERenovation, 203(k), construction-to-permanent), the loan size is governed by the post-completion appraisal, with HomeStyle eligible renovation funds capped at 75% of the lesser of (purchase + reno) or as-completed value.

- Can I get an ADU loan with no equity?

- Yes, if you can support the loan against the future value of the home after the ADU is built. Construction-to-permanent loans, Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, and FHA 203(k) all use as-completed value. They require more documentation (plans, bids, permits, draw schedules) than equity products.

- Can projected ADU rental income help me qualify?

- Often, yes. As of March 21, 2026, Fannie Mae's DU 12.1 allows up to 30% of qualifying income from one ADU's rental income on a 1-unit primary residence (purchase or limited cash-out refinance only). Freddie Mac allows 75% of lease, also capped at 30% of total qualifying. FHA allows 75% on existing ADUs or 50% on a new ADU under a 203(k). VA generally does not count ADU rental income; USDA's current rule blocks income-producing ADUs entirely.

- Do I need permits before applying for an ADU loan?

- For HELOCs and home equity loans secured against the existing home, no — but you'll need them before construction starts. For renovation and construction loans, your lender will want either issued permits or evidence the permit application is in process before disbursing construction draws. Local rules vary.

- Do lenders require a licensed contractor?

- For HomeStyle Renovation, CHOICERenovation, FHA 203(k), and construction-to-permanent loans, yes. Fannie Mae HomeStyle allows limited DIY on 1-unit owner-occupied homes (capped at 10% of as-completed value, with lender inspections for items over $5,000). Manufactured homes are not eligible for DIY.

- Can I use an FHA 203(k) loan for an ADU?

- Yes. HUD Mortgagee Letter 2023-17 recognizes ADUs as eligible improvements under Standard 203(k), including adding an attached ADU to the existing structure and renovating an existing ADU. Limited 203(k) is for minor remodeling and nonstructural repairs up to $75,000 with a 9-month timeline; major or structural ADU work requires Standard 203(k).

- Can a HELOC be used to build an ADU?

- Yes, if you have enough current equity. Most lenders cap CLTV at 80–85% of current value. Some California credit unions offer ADU-specific HELOCs. HELOCs use the home as collateral, are typically variable-rate (tied to Prime), and can be frozen or reduced if home value or finances change.

- Does a prefab ADU qualify for financing?

- It depends on classification and program. Prefab ADUs that are permanently affixed and titled as real property are widely financeable. Manufactured-home ADUs have program-specific rules — Fannie Mae HomeStyle Renovation caps manufactured-home renovation costs at 50% of as-completed value under SEL-2025-10 (the prior $50,000 dollar cap was removed); Freddie Mac allows MH ADU on multiwide MH primaries per Bulletin 2025-15.

- What if my ADU is legal nonconforming?

- Legal nonconforming ("grandfathered") ADUs are accepted by Fannie Mae, Freddie Mac, and FHA. Confirm with your VA-experienced lender for VA files.

- Can a HELOC be frozen during my ADU build?

- The CFPB notes HELOCs can be frozen or reduced if the lender determines the home value has dropped significantly or the borrower's financial circumstances have changed. This is one reason borrowers on lengthy ADU projects sometimes prefer construction-to-permanent or HomeStyle Renovation financing, which lock in the loan amount upfront.

- Can an illegal or unpermitted ADU be financed?

- Generally no. Fannie Mae, FHA, VA, and USDA require zoning compliance (legal or legal nonconforming). Freddie Mac has a narrow exception path for an illegal ADU on a 1-unit subject property in specific cases. The practical path is legalization first, financing second. In California, AB 2533 creates a statewide amnesty path for unpermitted ADUs and JADUs built before January 1, 2020.

- Will an ADU loan replace my current mortgage?

- HELOCs and home equity loans sit as a second lien and keep the first mortgage intact. Cash-out refinances and renovation loans (HomeStyle, CHOICERenovation, 203(k)) replace the first mortgage. Construction-to-permanent typically replaces the existing mortgage at completion.

- What happens if the appraisal doesn't support the ADU value or rent?

- This is one of the most common loan-stage failures. For future-value loans, a low as-completed appraisal shrinks the loan ceiling. For HELOCs, a low current-value appraisal drops the credit line. Options: renegotiate scope, contribute more equity, or pursue an appraisal rebuttal. Ask your lender about rebuttal procedures before signing.

Sources

- Pennymac Correspondent, Announcement 26-29 / 26-25: Fannie Mae Updates to Accessory Dwelling Unit (ADU) Rental Income, March 23, 2026 — confirming DU 12.1 effective March 21, 2026 and 30% qualifying-income cap. Verified May 20, 2026. corr.pennymac.com | Primary source: Fannie Mae Selling Guide B3-3.1-08. fanniemae.com

- HUD Mortgagee Letter 2023-17, Revisions to Rental Income Policies, Property Eligibility… (FHA cash-out ADU effective-income restriction). Verified May 20, 2026. hud.gov

- Freddie Mac, Accessory Dwelling Units Fact Sheet, February 2026. Verified May 20, 2026. freddiemac.com

- HUD Mortgagee Letter 2023-17 (FHA ADU rental income at 75% existing / 50% new under 203(k); URAR/Form 1007 documentation; 2-month PITI reserve requirement on 1-unit + ADU when ADU income is used). Verified May 20, 2026.

- U.S. Department of Veterans Affairs, VA Lenders Handbook (occupancy and rental income guidance). Verified May 20, 2026.

- Federal Register, Single Family Housing Guaranteed Loan Program — Income Producing Accessory Dwelling Unit Provisions (proposed rule), Docket RHS-26-SFH-0100, published March 31, 2026; comments must be received by June 1, 2026. Verified May 20, 2026. federalregister.gov

- Fannie Mae Selling Guide Announcement SEL-2025-09 (effective for new DU casefiles created on or after November 16, 2025 — 620 representative-credit-score minimum removed from DU). Verified May 20, 2026. fanniemae.com

- Fannie Mae, HomeStyle Renovation Mortgages Selling Guide B5-3.2-01 and HomeStyle Renovation FAQs. Verified May 20, 2026. fanniemae.com

- Diamond Residential Mortgage, HUD Announces Changes To Its FHA 203(k) Program (Nov 4, 2024 changes — Limited cap raised to $75,000; Limited completion 9 months; Standard completion 12 months). Verified May 20, 2026. diamondresidential.com

- Freddie Mac, Primary Mortgage Market Survey — 30-year fixed averaged 6.36% as of May 14, 2026 (dated snapshot, not an offer). Verified May 20, 2026. freddiemac.com

- Yahoo Finance / Curinos, HELOC and home equity loan rates today, May 12, 2026 (national averages 7.21% HELOC / 7.36% HEL — dated snapshot, not an offer). Verified May 20, 2026. finance.yahoo.com

- Consumer Financial Protection Bureau, What is a home equity line of credit? and What is a construction loan? Verified May 20, 2026. consumerfinance.gov

- The Mortgage Reports, FHA 203(k) Loan Requirements & Guide 2026. Verified May 20, 2026. themortgagereports.com

- Bank of America, How to Calculate Home Equity (CLTV definition and most-lenders 85% CLTV cap for HELOCs). Verified May 20, 2026. bankofamerica.com

- TENA Companies, Freddie Mac Issues Bulletin 2026-1 (new specificity for qualifying rental income on CHOICERenovation effective May 4, 2026). Verified May 20, 2026. tenaco.com

- Fannie Mae Selling Guide B5-3.1-02, Conversion of Construction-to-Permanent Financing: Single-Closing Transactions. Verified May 20, 2026. fanniemae.com

- Fannie Mae, Accessory Dwelling Units (ADUs) product page. Verified May 20, 2026. fanniemae.com

- HUD, Single Family Housing Policy Handbook 4000.1 and 203(k) Rehabilitation Mortgage Insurance Program. Verified May 20, 2026. hud.gov

- Fannie Mae Selling Guide Announcement SEL-2025-10 and UAD 3.6 Policy Supplement — expanded ADU and MH eligibility effective March 31, 2026 for lenders using UAD 3.6. Verified May 20, 2026. fanniemae.com

- WISA Solutions, Does the FHA Allow Rental Income From an ADU in 2026? (30% cap on ADU income for FHA qualifying). Cross-referenced with HUD ML 2023-17. Verified May 20, 2026. wisadc.com

- California Assembly Bill 2533 — signed September 28, 2024; effective January 1, 2025; applies to unpermitted ADUs and JADUs built before January 1, 2020. Verified May 20, 2026. colma.ca.gov

- Fannie Mae Appraiser Update — UAD 2.6 vs UAD 3.6 reporting requirements for ADU rental income (Form 1007 on UAD 2.6; Rental Information section / Rental Comparison Grid on UAD 3.6). Verified May 20, 2026. fanniemae.com

- LendEDU, HELOC and Home Equity Loan Qualification Requirements: 2026 Guide. Verified May 20, 2026. lendedu.com

- Fannie Mae Selling Guide B3-3.1-08, Rental Income — 75% calculation when using lease or market rent forms; subject-property ADU income cap at 30% of total qualifying. Verified May 20, 2026. fanniemae.com

- TENA Companies, Freddie Mac Issues Bulletin 2025-15: Selling Updates (multiwide MH primary + MH ADU effective Feb 9, 2026). Verified May 20, 2026. tenaco.com

- NYC Housing Preservation & Development, Plus One ADU Program Term Sheet. Verified May 20, 2026. nyc.gov

Methodology

We built this guide by reading the primary documentation that governs ADU lending — the Fannie Mae Selling Guide (Sections B3-3.1-08 Rental Income; B5-3.1Construction-to-Permanent; B5-3.2 HomeStyle Renovation), Selling Guide Announcements SEL-2025-08, SEL-2025-09, and SEL-2025-10, the UAD 3.6 Policy Supplement, the Freddie Mac Single-Family Seller/Servicer Guide (Chapters 4203 and 5306; Section 5601.2), Freddie Bulletins 2025-15 and 2026-1, HUD Mortgagee Letter 2023-17, HUD Handbook 4000.1, HUD's November 4, 2024 FHA 203(k) program changes, the Federal Register entry for USDA proposed rule RHS-26-SFH-0100, the current Freddie Mac Primary Mortgage Market Survey, and CFPB consumer guidance. We cross-referenced rate data against Curinos averages via Yahoo Finance. State-law citations (California AB 2533) are confirmed against multiple municipal and California Department of Housing and Community Development references.

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We do not name specific rates as guarantees, do not rank lenders by payout, and do not endorse a single program over another. The right path depends on the reader's specific facts. This guide is informational and does not constitute financial, legal, tax, or lending advice. Verify all information with qualified local professionals and your lender's specific overlays before making decisions.

Not sure where to start?

See what's possible at your address — get your free ADU report in 60 seconds.

Get my free ADU report →