· By The Dwelling Index Editorial Team

Home Equity Loan for ADU: When a Fixed Second Mortgage Actually Works

Short answer

A home equity loan — a fixed-rate, lump-sum second mortgage — is one of the most predictable ways to finance an ADU when your equity is strong, your scope is locked, and you want a single payment that never changes. It is not the right product for every ADU project. This page tells you when it works, when it doesn't, how to calculate your borrowing room, which lenders offer ADU-specific products, and what the tax rules say in 2026.

Is a home equity loan right for your ADU project?

Answer capsule. A home equity loan is the right starting point when you have meaningful existing equity (enough to cover the ADU build plus a 15–20% contingency at 80–85% combined loan-to-value), a locked ADU scope and contractor bid, a first-mortgage rate you refuse to give up, and a preference for payment certainty over construction flexibility.

The table below maps common homeowner situations to the right product lane. If your situation lands in the left column with a strong or possible fit, keep reading. If it points you elsewhere, follow that link — the wrong product is more expensive than the right one, even if the interest rate looks lower.

| Your situation | Fit | Direction |

|---|---|---|

| Strong equity, locked scope, signed fixed-bid contractor | Strong | This page applies |

| Strong equity, scope still in design or cost-plus contract | Possible but HELOC often better | See HELOC for ADU guide |

| Low first-mortgage rate (sub-4%), want to preserve it | Strong vs. cash-out refi | Second lien — first mortgage untouched |

| Weak equity relative to ADU cost | Not yet | Look at ARV or after-renovation-value products |

| Uncertain scope, milestone-draw contractor | Not ideal | HELOC or renovation loan |

| No equity, recent purchase | Not yet | See How to Finance an ADU With No Equity |

| Cash flow constrained, can't service new payment | Not suited | Consider a home equity investment (HEI) |

What is a home equity loan for an ADU?

Answer capsule. A home equity loan is a fixed-rate, lump-sum second mortgage secured by your home. You borrow a single amount, receive it in full at closing, and repay it in fixed principal-and-interest installments over a term of 5 to 30 years. Unlike a cash-out refinance, it leaves your existing first mortgage completely intact — rate, term, and payment unchanged. Unlike a HELOC (home equity line of credit), it doesn't revolve and carries a fixed rate rather than a variable one.

The Consumer Financial Protection Bureau and Federal Trade Commission both classify the home equity loan as a "second mortgage" and note that the loan is secured by your home — which means that if you fall behind on payments, the lender may seek foreclosure. That risk is real and is not unique to ADU projects. Managing it comes down to borrowing an amount your household can service without depending on ADU rental income that hasn't started yet.

For an ADU, the mechanics work like this: you close the loan, the full balance lands in your bank account, you manage disbursements to your contractor across the build, and you begin repaying from day one regardless of when the ADU is finished or rented. The payment doesn't change when rates move. The payment doesn't reset when a draw period ends. If you can tolerate paying interest on funds sitting in the bank waiting for the framing draw, the certainty of a fixed payment over a 15- or 20-year term is a genuine trade worth making.

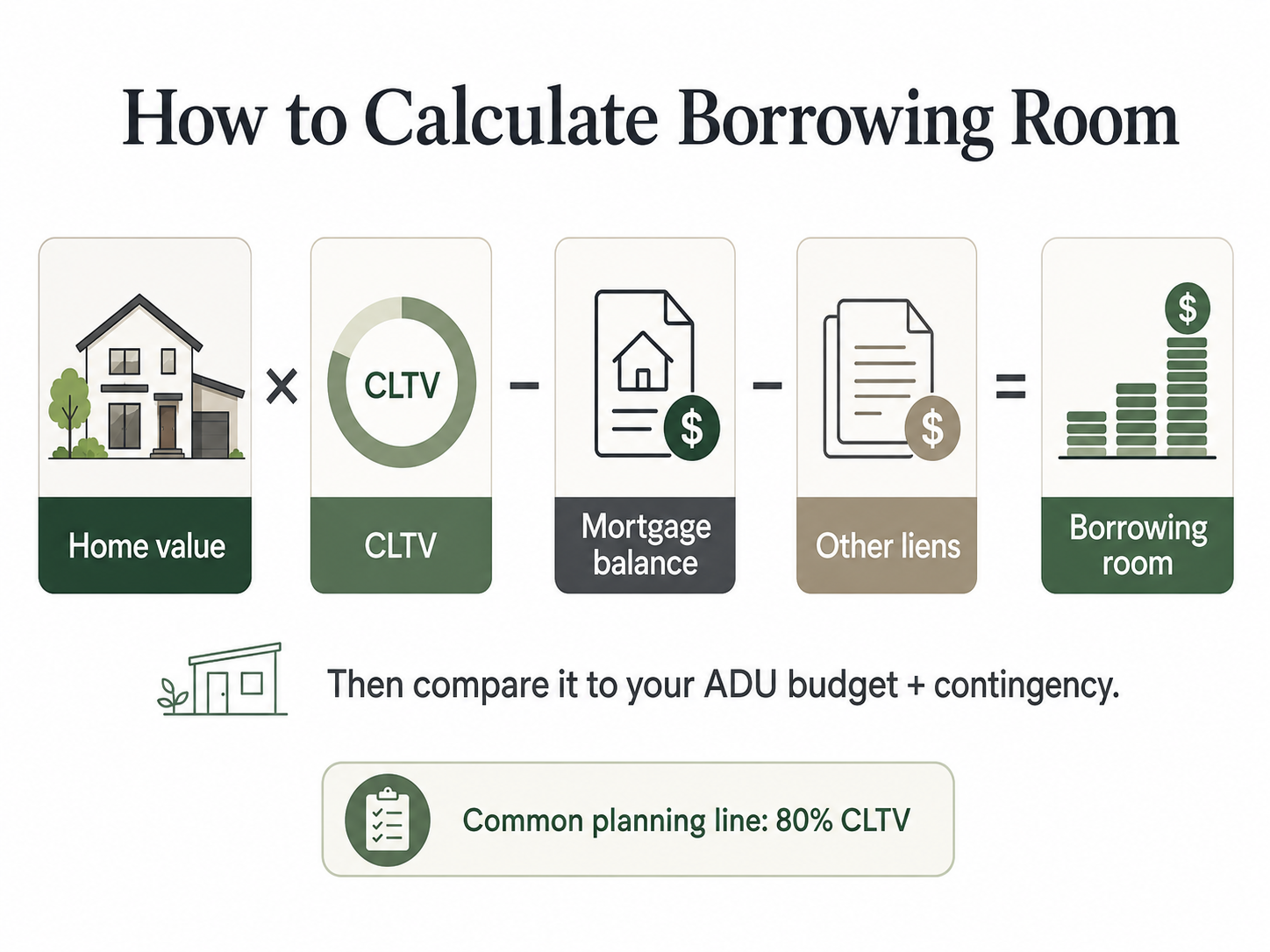

How much equity do you need? Borrowing room and the CLTV formula

Answer capsule. The formula is straightforward: (home value × maximum combined loan-to-value ratio) − existing mortgage balance − other liens = borrowable room. Most lenders cap the CLTV at 80–85% for a standard home equity loan. The result tells you the maximum amount you can borrow in a new second mortgage, which is the same as your usable equity for this purpose.

The CLTV formula in plain English

If your home is worth $750,000 and your existing mortgage balance is $450,000, the math at an 80% CLTV ceiling looks like this:

$750,000 × 0.80 = $600,000 (max total secured debt)

$600,000 − $450,000 = $150,000 borrowable room

At 85% CLTV, the same home gives you $187,500 of room. At 90% — available only from specialty lenders or after-renovation-value products — the room grows to $225,000. The difference between lenders that cap at 80% and those that allow 90% can be the difference between a project that fits and one that doesn't.

Borrowing room matrix — by home value, mortgage balance, and CLTV

| Home value | Mortgage balance | Room @ 80% CLTV | Room @ 85% CLTV | Room @ 90% CLTV |

|---|---|---|---|---|

| $500,000 | $300,000 | $100,000 | $125,000 | $150,000 |

| $600,000 | $350,000 | $130,000 | $160,000 | $190,000 |

| $750,000 | $400,000 | $200,000 | $237,500 | $275,000 |

| $750,000 | $500,000 | $100,000 | $137,500 | $175,000 |

| $900,000 | $500,000 | $220,000 | $265,000 | $310,000 |

| $1,000,000 | $600,000 | $200,000 | $250,000 | $300,000 |

| $1,200,000 | $700,000 | $260,000 | $320,000 | $380,000 |

Illustrative examples only. Actual appraised value may differ from purchase price or estimated value. Other liens reduce available room.

Why the 10–20% contingency matters

Closing on the exact loan amount that matches your contractor's bid is a structurally bad idea. Site work surprises — buried utilities, soils that need engineering, foundation depth changes — routinely add 5–15% to actual hard costs. Utility-lateral runs (the underground line carrying water, sewer, gas, or electric to the new ADU) often surprise homeowners; budget $10,000–$30,000, with the high end common when the ADU is far from existing service or trenches must cross hardscape or mature trees.

The Dwelling Index recommends a 15% contingency above the contractor bid for conversions and 20% for detached new construction, sized into the loan. If your borrowable room can't cover the full bid plus contingency, the right move is rarely "stretch the loan." It's usually "switch products" or "scope down."

ADU Home Equity Loan Borrowing Room Calculator

Enter your numbers to see borrowable room at 80 %, 85 %, and 90 % CLTV. We don't store or transmit your inputs.

Now connect equity math to your specific lot

See What You Can Build → Get Your Free ADU ReportIs a home equity loan or HELOC better for an ADU?

Answer capsule. A home equity loan (fixed lump sum, fixed rate, fixed payment) is the better fit when your ADU budget is firm and you value payment certainty. A HELOC (revolving line, typically variable rate, draw as needed) is usually the better fit during ADU construction because costs arrive in stages and a HELOC lets you avoid paying interest on funds you don't yet need. The CFPB and FTC both note that HELOCs typically carry variable rates and draw-period mechanics, while home equity loans are usually fixed-rate, lump-sum products.

Lump sum vs revolving line — what that actually means for an ADU

A home equity loan funds at closing. The day your loan closes, the full balance hits your bank account and the clock starts on principal-and-interest payments. Your contractor probably won't bill for a foundation pour for another four to six weeks, and the framing draw might be three months out. In the meantime, you're paying interest on the entire loan balance.

A HELOC opens a credit line at closing but doesn't fund anything until you draw. You ask for $25,000 when the contractor invoices for foundation. You ask for $40,000 at framing. You ask for $30,000 at mechanicals. During the typical 10-year draw period, most HELOC products require interest-only payments on the outstanding balance. You're never paying interest on money you haven't yet pulled.

Fixed payment vs variable-rate exposure

Where the home equity loan wins is in payment certainty. Your rate is locked. Your payment is locked. If prime moves up 150 basis points over the next two years, your monthly payment doesn't move with it. The Federal Reserve's H.15 release puts the prime rate at 6.75% as of mid-May 2026. Curinos rate data (published by Experian) puts the average home equity loan rate at 7.53% and the average HELOC rate at 7.50% for May 2026. Bankrate's separate survey puts the home equity loan average at 8.03% as of May 15, 2026.

HELOC vs home equity loan — side-by-side

| Feature | Home equity loan | HELOC |

|---|---|---|

| Disbursement | Lump sum at closing | Draw as needed, revolving |

| Rate type | Fixed | Typically variable (prime + margin) |

| Payment structure | Principal-and-interest from day one | Interest-only during draw period; P&I in repayment |

| Term | 5–30 years | 10-year draw + 10–20-year repayment, typically |

| First mortgage preserved? | Yes (second lien) | Yes (second lien) |

| Best for | Known-budget builds, conversion ADUs, signed fixed-bid contracts | Phased construction, uncertain scope, multiple draws |

| Main risk | Paying interest on idle funds from day one | Variable-rate movement during repayment period |

When to use a HELOC during construction and refinance later

There's a hybrid play worth naming: use a HELOC during construction to manage draws and avoid paying interest on idle balances. Once the ADU is complete and the property has been re-appraised — typically reflecting a meaningful value lift — refinance the outstanding HELOC balance into a fixed second mortgage to lock the rate before variable-rate exposure becomes painful. This works when you have enough HELOC headroom to cover the full build and the discipline to actually refinance once the project finishes. If your scope is locked and you don't want to manage two financing decisions, skip the hybrid and take the fixed home equity loan now. For the staged-construction path, see our HELOC for ADU guide.

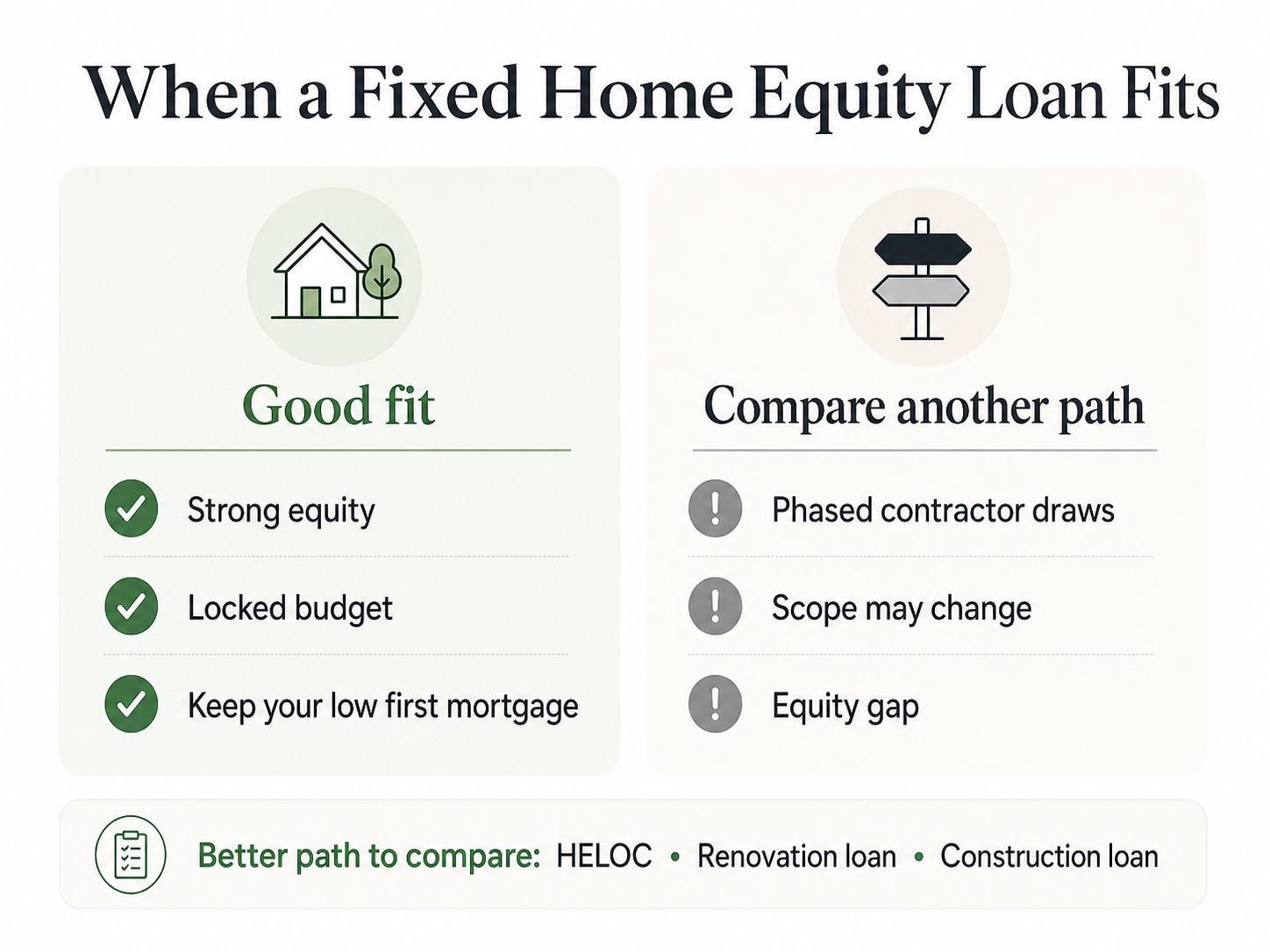

When does a fixed home equity loan actually win for an ADU?

Answer capsule. A fixed home equity loan is the right product when four conditions stack: strong current equity, a first mortgage rate worth preserving, a firmly locked ADU scope and cost, and a preference for payment predictability over construction flexibility.

Profile 1 — Strong equity and a locked scope

The cleanest fit. You own a home worth $900,000 with $400,000 left on a 3.5% first mortgage. Your contractor has signed a $180,000 fixed-bid contract for a permitted garage conversion. You have $40,000 in savings as your contingency reserve. You take an $180,000 home equity loan at a fixed rate, keep your 3.5% first mortgage in place, and pay a known monthly amount for the next 15 or 20 years. This profile is more common than most articles suggest. Garage conversion ADUs, basement ADUs, and small attached ADUs all tend to come in below $200,000 in many markets. For these projects, the fixed loan's predictability is a feature, not a constraint.

Profile 2 — Low first mortgage rate you refuse to refinance

Freddie Mac data shows nearly 60% of borrowers hold a mortgage rate at or below 4%, and the Federal Housing Finance Agency has documented that mortgage-rate lock-in significantly reduced fixed-rate home sales between 2022 and 2024. If you're one of those lock-in-affected borrowers, a cash-out refinance is a non-starter — replacing a 3.25% first mortgage with a 6.5% one to extract $200,000 wipes out years of cumulative savings. A home equity loan sits as a second lien. Your first mortgage is untouched. For lock-in-affected borrowers, this is almost always the right framework, and the choice within the framework is between fixed (home equity loan) and variable (HELOC).

Profile 3 — Signed fixed-bid contract

If your contractor's contract is firm — fixed bid, all-inclusive of site work, utilities, permits, materials, and labor — your scope is locked. The draw flexibility of a HELOC isn't worth giving up the payment certainty of a fixed home equity loan. You know what you'll spend. Borrow exactly that, plus contingency, and don't think about it again. If your contractor's contract is cost-plus, time-and-materials, or open-ended on allowances, your scope is not locked, no matter what the bid sheet says. That's a HELOC profile.

Profile 4 — Predictable repayment over draw flexibility

Some borrowers — often retirees, fixed-income households, or families managing tight cash flow — value payment predictability above almost everything else. A fixed home equity loan delivers that. The principal-and-interest payment on day one is the same payment in year ten. There is no resetting payment when the draw period ends. There is no variable rate. The trade-off — paying interest on the full balance from day one, including the portion sitting in the bank waiting for the contractor — is the price of certainty.

Worth noting: lender attitude toward ADUs

Most banks underwrite home equity loans without asking what the proceeds are for. As long as the property's value supports the loan and you qualify, the bank approves. Some lenders — especially regional credit unions like Patelco, Foothill, and a growing list of others — have built ADU-aware programs that include construction-management oversight, projected rental income consideration, and longer terms structured for the build phase. We cover those specifically in the lender section below.

When is a home equity loan the wrong move for an ADU?

Answer capsule. A fixed home equity loan is the wrong product when your scope or cost is uncertain, your current equity can't cover the full budget plus contingency, your contractor requires milestone draws, you're relying on projected ADU rent to make the payment work, or your DTI is already tight before the new payment is added. This section is the one most lender pages skip. If you're in any of the situations below, picking a fixed home equity loan is how good projects get into bad financial structures.

Your final ADU cost is uncertain

If your contractor's quote is preliminary, if the city hasn't fully approved the plans, if your soils report hasn't come back, or if your design includes allowances rather than final selections — your cost is uncertain. A fixed loan delivers one number at closing. If your actual cost lands 15% higher, you're funding the overrun from cash, from credit cards, or from a second loan application that may not happen quickly enough. A HELOC with headroom, or a renovation loan based on after-renovation value, is built for uncertainty. A fixed loan is not.

The loan would leave you with no contingency

If your maximum borrowing room is $200,000 and your contractor bid is $200,000, you cannot borrow $200,000 and feel safe. You're zero-padded. The first surprise wipes the project. The right move is to borrow less than your max — leaving 10–20% room for contingency — or to switch to a product that includes future-value underwriting.

You're counting on projected ADU rent to make the payment work

Even where lenders allow some consideration of ADU rental income for qualifying, nobody approves a fixed home equity loan on the assumption that you'll be collecting rent in month four. The build alone often takes 6 to 12 months. Lease-up takes another 30 to 60 days. Vacancy happens. If the loan only works because the rent is hitting your account, you've built a structure that fails the moment the rent doesn't. Lenders underwrite to current household income, not projected rental income on an unbuilt ADU.

Your DTI is already tight

The general industry benchmark for a home equity loan is a debt-to-income ratio at or below 43%, including the new loan payment. Some lenders go to 50% for borrowers with strong compensating factors. If you're already at 38% before the new payment, a $1,600 monthly home equity loan payment can push you to or beyond 43%. The fix is rarely "find a more flexible lender." The fix is usually "reduce existing debt before applying" or "borrow less."

Your contractor requires milestone draws

Some contractors won't take a single up-front payment. They expect a deposit at signing, draws at foundation, framing, mechanicals, drywall, and final. If you take a fixed home equity loan, you're managing a $200,000 lump sum across those milestones from your own bank account. The interest you pay on the unused portion is real. A HELOC or renovation loan structures the draws against the loan itself.

Your lot may not qualify in the first place

Cities have setbacks, height limits, lot-coverage limits, fire-zone overlays, FAR caps, and short-term rental ordinances that constrain what you're allowed to build. Borrowing $200,000 against your home and then discovering the lot can't accept the design you wanted is a particularly painful sequence. Run feasibility before financing.

Honest negative paragraph

No financing decision on this page eliminates the underlying risk that a home equity loan is secured by your home. The CFPB is explicit: "Like a mortgage, a home equity loan, also called a ‘second mortgage,’ uses your home as collateral. If you fall behind in repaying your home equity loan, your lender may take steps to foreclose on your home." That risk doesn't disappear with the right product choice. It's reduced by borrowing less than your maximum, by keeping a real contingency, and by verifying the project is buildable before you sign. We'd rather you scope down to a garage conversion you can fund safely than borrow against the house for a detached ADU you can't actually afford to finish.

How does ADU type change the financing decision?

Answer capsule. ADU type changes the financing decision because the cost gap between conversions and detached new construction often spans $200,000 or more, and that gap determines whether your current equity can cover the build. Garage and basement conversions often fit inside borrowable equity at standard CLTVs. Detached ADUs in high-cost markets often don't, and frequently push borrowers toward after-renovation-value products or construction loans.

Garage conversion ADU

A garage conversion repurposes an existing attached or detached garage into a self-contained dwelling unit. Because the structure, foundation, and roof already exist, hard costs run lower than new construction. Dwelling Index planning estimates (2026):

- High-cost coastal metros (LA, Bay Area, Seattle, Boston): $120,000–$180,000

- Mid-cost metros (Portland, Denver, Austin, Tampa): $90,000–$140,000

- Lower-cost markets (much of the South and Midwest): $80,000–$125,000

Basement ADU

Cost is typically similar to a garage conversion if the basement already has adequate ceiling height (most codes require a 7-foot minimum) and reasonable egress. If not, the project balloons fast: digging out for ceiling height, cutting in a legal egress window or door, and waterproofing for habitable use can push the total well past $150,000. Basement ADUs are not legal in all jurisdictions.

Attached ADU

An attached ADU connects to the primary home, often sharing a common wall and utility connections. Dwelling Index planning ranges:

- High-cost coastal: $200,000–$320,000

- Mid-cost: $150,000–$245,000

- Lower-cost: $130,000–$200,000

Detached ADU

A detached ADU — sometimes called a DADU or backyard cottage — is a freestanding new structure. Cost is highest because everything is new. Dwelling Index planning ranges:

- High-cost coastal: $300,000–$600,000

- Mid-cost: $200,000–$400,000

- Lower-cost: $150,000–$300,000

Above-garage ADU

A second-story addition built over an existing garage. One important wrinkle: the existing garage's foundation often needs structural reinforcement to carry the new load. Budget $20,000–$60,000 for reinforcement work. Total project ranges typically run $150,000–$275,000 in most markets.

Prefab or modular ADU

Factory-built and delivered to your lot for installation. Hard cost on the unit alone can run 15–30% lower than fully site-built equivalents. The catch: site work, foundation, utility connections, crane delivery, and installation often add $40,000–$100,000 to the manufactured unit's price. Prefab can fit a fixed home equity loan well if the all-in installed cost is known up front and the manufacturer's deposit schedule matches your loan timing.

Decision table by ADU type

| ADU type | Typical national cost range | Fixed home equity loan fit |

|---|---|---|

| Garage conversion | $80,000–$180,000 | Often strong |

| Basement ADU | $90,000–$180,000 if egress and height work; $250,000+ if not | Possible if scope is locked |

| Attached ADU | $130,000–$320,000 | Possible with strong equity |

| Above-garage ADU | $150,000–$275,000 | Mixed — structural contingency critical |

| Detached ADU | $150,000–$600,000+ | Often needs more borrowing room than a standard fixed loan provides |

| Prefab / modular | $80,000–$300,000 all-in installed | Depends on all-in installed price |

What if a home equity loan does not cover the full ADU cost?

Answer capsule. If a fixed home equity loan based on current value can't cover your ADU plus contingency, you have six honest next moves: a HELOC with more headroom, a renovation or after-renovation-value (ARV) loan, a construction-to-permanent loan, a cash-out refinance if your first mortgage isn't worth preserving, a smaller-scope ADU that fits inside your current equity, or a home equity investment (HEI) if cash flow is your hard constraint.

Option 1 — HELOC with more headroom

If a fixed home equity loan caps your borrowing room, a HELOC at the same CLTV ceiling gives the same total room but better cash-flow ergonomics during construction. You only pay interest on what you actually draw. Trade-off: variable rate. Some HELOC products offer a fixed-rate conversion option for portions of the balance — Figure's HELOC structures around this — which mitigates but doesn't eliminate the variability. See our HELOC for ADU guide.

Option 2 — Renovation loan based on after-renovation value (ARV)

A renovation or ARV HELOC underwrites against the home's future value after the ADU is finished, not its current value. This can dramatically expand borrowing room. Key lenders offering ARV products:

- Tower Federal Credit Union's Dreamline Renovation HELOC — lends up to 90% of after-renovation value; available in Maryland, Virginia, Washington D.C., Delaware, Pennsylvania, North Carolina, South Carolina, and Florida only. Lines $50,000–$350,000; 15-year interest-only period plus 15-year repayment; 12-month draw window with extensions up to 18 months at $500/month.

- Spring EQ's HELOC — higher CLTVs than typical standard products, draw periods up to 20 years on some structures (May 2026).

- RenoFi — partners with credit unions across 49 states (Texas excluded as of May 2026); often allows total borrowing up to 90% of post-ADU value.

For a borrower whose home is worth $700,000 today with $500,000 on the first mortgage and a $250,000 detached ADU that will lift value to $900,000 — a standard 80% CLTV loan provides $60,000 of room. A 90%-of-ARV loan against $900,000 provides $310,000 of room. Same project, same equity position, two different products: one works, one doesn't.

Option 3 — Construction-to-permanent loan

Funds the construction phase against the project's future value, then converts into a permanent first-position mortgage when the build is complete. Fannie Mae's Selling Guide references construction-to-permanent financing as compatible with ADUs. Trade-off: this is a replacement of your first mortgage. If your current rate is sub-5%, the math usually doesn't pencil.

Option 4 — Fannie Mae HomeStyle or Freddie Mac CHOICERenovation

Both agencies have ADU-aware renovation mortgage products that let you finance ADU construction inside a single mortgage based on the as-completed value. Useful for buyers acquiring a home and building an ADU simultaneously. The catch: they replace your existing first mortgage, which means rate-lock-in borrowers usually pass.

Option 5 — Scope down

Sometimes the right answer is to build the ADU you can fund safely. A garage conversion at $140,000 that fits inside your current equity at 80% CLTV is a better financial decision than a $400,000 detached ADU that requires stretching to 90% CLTV with a specialty lender and leaving no contingency.

Option 6 — Home equity investment (HEI)

If cash flow is the hard constraint — you have equity but cannot service a new monthly payment — a home equity investment (HEI) exchanges a share of your home's future appreciation for cash today, with no monthly payments. The trade-offs are significant and are covered in our Home Equity Investment for ADU guide.

Not sure which path fits your situation?

Compare ADU financing paths — home equity, renovation, and construction loan options — side by side.

Compare ADU Financing Paths → Explore Mortgage & Renovation Loan OptionsAffiliate link — Mortgage Research Center. We may earn a commission; you pay nothing extra. Full disclosure.

Can ADU rental income help you qualify for a home equity loan?

Answer capsule. In limited circumstances, and rarely at a level that fully solves a qualifying gap on an unbuilt ADU. Fannie Mae allows ADU rental income for qualifying on a one-unit principal residence with documentation, capped at roughly 30% of total qualifying income (Fannie Mae Selling Guide B3-3.8-01). Patelco's ADU HELOC explicitly considers projected ADU rental income. Most standard home equity loans do not credit projected rental income on an unbuilt ADU.

Lenders are underwriting to the risk that an unbuilt ADU produces zero rent for a year or more. No honest lender assumes your ADU will be built, permitted, and rented on time. If your DTI only works with projected ADU rent, you are building a structure that fails the moment any piece of the plan slips.

The right question is whether your household's current income — without the ADU rent — can service the combined first mortgage and home equity loan payment. If it can, the ADU rent is upside. If it can't, you need to borrow less, add income, or switch products.

Is home equity loan interest tax deductible when used to build an ADU?

Answer capsule. In most cases, yes — if the loan is secured by your home, the proceeds are used to build the ADU on that same property, your total qualified mortgage debt stays within the $750,000 cap, and you itemize deductions on Schedule A. The One Big Beautiful Bill Act, enacted in 2025, made the TCJA's home equity interest restriction permanent. There is no longer a future date at which the broader pre-2018 rule returns.

The IRS rule in plain English

IRS Publication 936 (2025 tax year, published October 28, 2025) sets the framework. Interest on home equity loans is deductible only if the borrowed funds are used to buy, build, or substantially improve the taxpayer's home that secures the loan. Building an ADU on the property that secures the loan satisfies the "build" or "substantially improve" test. The IRS defines a substantial improvement as one that adds value to the home, prolongs its useful life, or adapts it to a new use. Adding a new dwelling unit clearly qualifies.

The $750,000 aggregate cap

The deduction applies to interest on up to $750,000 in total qualified mortgage debt across your main home and one second home ($375,000 if married filing separately). This is an aggregate cap — your existing first mortgage and the new home equity loan are added together. If you owe $650,000 on your first mortgage and take a $200,000 home equity loan to build an ADU, only the interest on $750,000 of total debt is deductible.

You have to itemize

This is the catch most homeowners miss. For 2026, the IRS has set the standard deduction at $32,200 for married filing jointly, $16,100 for single filers and married filing separately, and $24,150 for head of household (IRS Rev. Proc. 2025-32). If your total itemized deductions don't exceed this threshold, the mortgage interest deduction has no practical value for you.

Mixed-use proceeds and the tracing rule

If you use part of the home equity loan for the ADU and part for something else, only the portion used to build the ADU generates deductible interest. The IRS calls this "tracing." Keep clean records: contractor invoices, permits, and final inspection records. If the IRS questions the deduction, the burden of proof is on you.

Three claims circulating that are wrong in 2026

- "You can deduct up to $325,000 if filing single." Incorrect. The cap for married filing separately is $375,000 (IRS Pub 936, 2025 tax year).

- "The TCJA expiration in 2025 means the old broader deduction returns." No longer true. The OBBBA made the TCJA restriction permanent.

- "Rates are expected to decline through 2024." Stale guidance. Average rates as of May 2026 are 7.53% (Curinos/Experian) and 8.03% (Bankrate).

Tax disclaimer. The above is a summary of publicly available IRS guidance as of May 2026. Your specific deduction depends on your filing status, whether you itemize, your aggregate qualified mortgage debt, and how you trace loan proceeds. Tax rules change. The Dwelling Index is not a tax advisor or law firm. Consult a CPA or enrolled agent before claiming any deduction described here.

Get the full pre-build checklist — budget, permit, and financing

Download the Free ADU Starter Kit →What does a home equity loan for an ADU cost in 2026?

Answer capsule. Rate surveys differ by lender panel and method. Curinos data (published by Experian) put the average home equity loan rate at 7.53% in May 2026. Bankrate's separate survey put the average at 8.03% as of May 15, 2026. The Federal Reserve's H.15 release puts the prime rate at 6.75%. Closing costs typically run 2% to 5% of the loan amount, plus appraisal, lender, and title fees.

Current rate snapshot

Rates verified May 19, 2026.

| Product | Rate (May 2026) | Source |

|---|---|---|

| Home equity loan, fixed | 7.53% average APR | Curinos via Experian, May 2026 |

| Home equity loan, fixed | 8.03% average APR | Bankrate survey, May 15, 2026 |

| HELOC, variable | 7.50% average APR | Curinos via Experian, May 2026 |

| Prime rate (HELOC index base) | 6.75% | Federal Reserve H.15, May 2026 |

| Patelco ADU HELOC (CA only, most qualified at 125% CLTV) | 8.25%–9.00% APR | Patelco disclosure, rates effective 05/18/2026 |

Rates depend on your credit, CLTV, lender, and market conditions. We refresh this snapshot monthly. These are not guarantees.

Closing cost breakdown

On a typical home equity loan, expect:

- Origination or lender fee. Usually $250–$500 flat or 0.5%–1% of the loan amount.

- Appraisal. $400–$800 for a standard appraisal; higher for after-renovation-value appraisals requiring both as-is and as-completed valuations.

- Title search and title insurance (where required). $300–$1,200.

- Credit report and administrative fees. $50–$150 combined.

- Recording fees (paid to the county). $50–$300 depending on jurisdiction.

Illustrative monthly payment

On a $200,000 home equity loan at 7.53% over 20 years, the monthly principal-and-interest payment is approximately $1,610. The same balance amortized over 15 years runs approximately $1,860. These are illustrative examples only — not guarantees of any specific rate or payment you'll be offered.

Total cost of credit — the number nobody asks about

Monthly payment isn't the right number to compare across loan offers. Total cost of credit is. A 20-year $200,000 home equity loan at 7.53% costs roughly $186,000 in total interest over its life. The same balance at 7.00% costs roughly $172,000 — a $14,000 swing on a half-percent rate difference. When you compare lender offers, ask each lender for the total cost of credit including all closing costs, not just the rate or the monthly payment.

Qualification checklist: credit, DTI, equity, income

Answer capsule. Most lenders want a FICO of 620 or higher (680+ for best rates), DTI at or below 43% including the new loan payment, and a CLTV at or below 80–85% after the new loan. Some specialty ADU products require higher credit scores (700+) but allow higher CLTVs in exchange. Income documentation typically requires two years of tax returns, recent pay stubs, and bank statements.

Credit score

Most lenders set a 620 FICO floor for home equity loans. Below 620, options narrow significantly and rates add 1–3 percentage points above the prime-qualified rate. Above 680 you start to see the best-tier rates. Above 740 you typically qualify for the lowest available rates. ADU-specific HELOC products tend to set higher floors (700+) because they're underwriting against the future value of an unbuilt project.

Debt-to-income (DTI)

DTI is calculated by adding all monthly debt payments — first mortgage, the proposed new home equity loan, credit cards, auto loans, student loans, child support — and dividing by gross monthly income. Most lenders cap at 43%. Some go to 50% for borrowers with strong compensating factors. A worked example: gross income $9,000/month, existing mortgage $2,200/month, car payment $400/month, credit card minimums $200/month. Existing DTI: 31%. Add a $1,610/month home equity loan and DTI rises to 49% — likely a decline at most lenders.

Income documentation

Standard documentation for a home equity loan application:

- W-2s for the past two years

- Federal tax returns for the past two years

- Pay stubs covering the last 30 days

- Bank statements (typically 60 days, all accounts)

- Photo ID, current mortgage statement, homeowners insurance declaration page, most recent property tax bill

For ADU-specific or after-renovation-value products, expect to also provide preliminary ADU plans, a contractor estimate or budget, and evidence of lot eligibility.

Qualification benchmarks by product type

| Requirement | Home Equity Loan | Standard HELOC | ADU-Specific HELOC (Patelco) | ARV HELOC (Tower Dreamline) |

|---|---|---|---|---|

| Minimum FICO | 620 | 680 | 700+ typical | 700+ typical |

| Max DTI | 43% | 43% | 43% | 43% |

| Max CLTV | 80–85% current value | 80–85% current value | 125% current value (CA only) | 90% of after-renovation value |

| Equity floor | 15–20% | 15–20% | Varies | Based on ARV |

| Projected ADU rent considered? | Generally no | Generally no | Yes (Patelco) | Varies by lender |

Which lenders offer ADU-specific home equity products?

Answer capsule. A small but growing list of credit unions and specialty lenders offer products built specifically for ADU construction. Notable examples include Patelco Credit Union and Foothill Credit Union (Southern California ADU HELOCs), Tower Federal Credit Union's Dreamline Renovation HELOC (eight-state coverage), Spring EQ and Figure (national standard HELOCs), New American Funding (national ADU-branded products), and RenoFi (partner credit unions in 49 states, Texas excluded as of May 2026). We list these alphabetically by category; terms verified against each lender's public disclosure page on May 19, 2026.

ADU-specific HELOCs (geographic-limited)

Foothill Credit Union — Southern California only

Public HELOC materials state that HELOC funds may be used for ADU expenses. Property location limited to Orange, Los Angeles, Riverside, San Bernardino, Ventura, and San Diego counties.

Patelco Credit Union — California only

Allows up to 125% of current home value (combining first mortgage and ADU HELOC). 2-year interest-only draw period followed by 20-year repayment period. Explicitly states it will consider projected ADU rental income to help borrowers qualify. Rates effective 05/18/2026: 8.25%–9.00% APR for the 125% as-is / 90% post-construction tier. Available on primary residences only.

After-renovation-value (ARV) products

RenoFi

Operates through partner credit unions across 49 states (Texas not currently served as of May 2026). Renovation home equity loans, HELOCs, and cash-out refinances underwritten against after-renovation value, often allowing total borrowing up to 90% of post-ADU value. Verify state availability directly with RenoFi before planning around it.

Spring EQ

National HELOC provider. Lends against home equity at higher CLTVs than typical standard products and offers draw periods up to 20 years on certain structures (Spring EQ product disclosures, May 2026).

Tower Federal Credit Union — Dreamline Renovation HELOC

Available in Maryland, Virginia, Washington D.C., Delaware, Pennsylvania, North Carolina, South Carolina, and Florida only. Lends up to 90% of after-renovation value. Lines $50,000–$350,000. 15-year interest-only period plus 15-year repayment. 12-month standard construction draw window; extensions up to 18 months at $500/month. $300 processing fee plus construction-management vendor origination fee at closing.

National standard HELOC providers commonly used for ADUs

Figure

Fixed-rate HELOC structure (unusual among HELOC products), 5-year draw period, requires drawing 100% of the credit line up front. Fast online application process. The fixed-rate structure mitigates variable-rate exposure but works poorly for staged construction.

New American Funding

Licensed in all 50 states plus D.C. and Puerto Rico. Markets ADU loans explicitly under a dedicated product page covering HELOCs, home equity loans, FHA 203(k), and construction loans.

How to evaluate a lender for ADU work

Three things to verify before signing with anyone:

- Does the lender allow proceeds to be used for ADU construction? Some products exclude detached new construction or restrict to renovation of an existing structure. Ask explicitly.

- Does the lender require construction inspection or draw oversight? Some ADU-specific products do; standard products usually don't. Neither is inherently better, but the workflow differs.

- Does the lender allow projected ADU rental income for qualifying? Generally no for standard products; yes for some ADU-specific ones. Confirm before applying if your DTI is tight.

Compare home equity, renovation, and construction loan offers at Mortgage Research Center →

Compare Lender Offers →Affiliate link — Mortgage Research Center. We may earn a commission; you pay nothing extra. Full disclosure.

How to apply for a home equity loan for an ADU without getting boxed in

Answer capsule. Apply only after you've confirmed property feasibility, locked an ADU budget with contingency, and calculated your borrowing room. The application timeline for a standard home equity loan runs two to six weeks; ADU-specific or ARV products take six to ten weeks because of the additional plan and budget review.

1Confirm property feasibility before borrowing

The single most expensive mistake is borrowing against the house and then discovering the city, the HOA, or the lot itself doesn't support what you wanted to build. Setback rules, height limits, lot-coverage caps, fire-zone restrictions, FAR limits, and short-term rental ordinances vary city-by-city. Run feasibility first.

See What You Can Build → Get Your Free ADU Report2Estimate the all-in ADU budget and contingency

The contractor's bid is the starting point, not the final budget. Add 15% contingency for conversions and 20% for new detached construction. Add soft costs: architectural plans ($5,000–$20,000), Title 24 energy compliance (California: $1,500–$3,000), permit fees ($3,000–$25,000 depending on jurisdiction), required impact fees. Get a written breakdown of what's in the bid and what's not.

3Calculate your borrowing room

Use the calculator above or run the formula manually: (home value × max CLTV) − existing mortgage balance − other liens = borrowable room. If your borrowable room covers the all-in budget plus contingency at the 80% CLTV planning line, a standard home equity loan is on the table.

4Compare paths before applying

Even if a fixed home equity loan looks right on paper, get rate quotes for both the fixed home equity loan and a HELOC from at least one shortlisted lender. Sometimes the HELOC ends up cheaper because of how interest accrues only on drawn balances during construction. The right answer depends on your numbers.

5Ask the lender these questions before submitting an application

Before you authorize a credit pull, get answers to all of these in writing:

| Ask the lender | Why it matters |

|---|---|

| What is your maximum CLTV for my property type and state? | Determines maximum loan amount |

| Is the rate fixed for the full term, or does it adjust? | Prevents payment surprises |

| What are all the closing costs — origination, appraisal, title, recording, and any monthly fees? | Total cost matters more than rate alone |

| Is building an ADU an acceptable use of the loan proceeds? | Some products restrict use; confirm explicitly |

| When does the first payment begin? | The ADU may not produce income yet |

| Is there a minimum loan amount? | Some lenders won't fund under $50,000–$75,000 |

| What happens if my appraisal comes in lower than expected? | Your approved loan amount can shrink |

| Is there a prepayment penalty? | You may want to refinance later |

| Do you allow projected ADU rental income to support qualifying? | Matters if your DTI is tight |

| What is the typical close-to-fund timeline for my profile? | Affects construction start date |

6Keep tax and construction records from day one

If you intend to claim deductible mortgage interest on the home equity loan proceeds used for ADU construction (and you plan to itemize), start your documentation file at closing. Save the closing disclosure, every contractor invoice, every receipt for ADU-related expenses, permit documents. The IRS doesn't pay attention until they do, and at that point the burden of proof is on you.

7Recheck the plan before closing

A surprising number of homeowners discover, in the week before closing, that a permit condition has changed, a contractor's pricing has shifted, or their financial picture has evolved. Re-run your borrowing room, your contingency math, and your monthly payment math 48 hours before closing. The 7 days between application and funding are recoverable. The 20 years of loan payments are not.

Typical application timelines

- Standard home equity loan, clean profile: 2–4 weeks application to funding

- Standard HELOC, clean profile: 2–6 weeks

- ADU-specific HELOC with construction management (Patelco, Foothill, similar): 6–10 weeks

- After-renovation-value loan (Tower Dreamline, RenoFi, Spring EQ): 6–12 weeks (two appraisals typically required)

- FHA 203(k) or Fannie Mae HomeStyle: 8–14 weeks

Want help comparing lender offers for the right lane?

Compare Home Equity, Renovation & Construction Loan Options at Mortgage Research Center →Affiliate link — Mortgage Research Center. We may earn a commission; you pay nothing extra. Full disclosure.

The biggest risks of using home equity to fund an ADU

Answer capsule. The largest risks are foreclosure exposure (the loan is secured by your home), cost overruns that exceed your borrowing room and contingency, appraisal shortfalls that reduce your approved loan amount, permit or zoning surprises that block the project after you've borrowed, and over-reliance on projected rental income that may not arrive on the expected timeline.

Foreclosure risk

The Consumer Financial Protection Bureau is direct: "Like a mortgage, a home equity loan, also called a ‘second mortgage,’ uses your home as collateral. If you fall behind in repaying your home equity loan, your lender may take steps to foreclose on your home." A second lien doesn't change that. The protection is not to avoid the loan — it's to not over-borrow, to keep a real cash reserve, and to not stretch the structure so tight that one bad quarter takes the whole thing down.

Cost overrun risk

If your loan amount matches the contractor bid with no contingency and actual costs run 15% over, you're funding the difference from savings, credit cards, or a second loan that may not close in time. Site work surprises, permit changes, material price shifts, and scope evolution during construction are normal. Budget for them before you borrow, not after.

Appraisal shortfall risk

Your approved loan amount is based on an appraised value, not your estimate of your home's value. If the appraisal comes in lower than expected, your maximum loan amount shrinks proportionally. A home you estimated at $850,000 that appraises at $790,000 gives you $63,000 less room at 80% CLTV. Apply with a realistic view of your home's current market value, not its peak Zillow estimate.

Insurance and property-tax changes

Building an ADU almost always raises your property tax assessment. In California, county assessors treat ADU new construction as an assessable event — the new ADU improvement is assessed at market value as of completion and added to your existing assessment (Santa Clara County Assessor guidance). The original home is not automatically reassessed. In other states, rules vary; confirm with your local assessor before budgeting. Insurance also needs re-evaluation: some homeowners policies don't automatically cover a separately occupied accessory unit, and you may need a landlord rider if you're renting the ADU. Tools like Buildium help landlords manage compliance, leases, and bookkeeping once the unit is rented.

Exit risk if you sell

If you sell the property before the home equity loan is paid off, the loan is typically paid in full at closing from sale proceeds. The exit risk is if the sale price doesn't cover both the first mortgage and the home equity loan plus closing costs — a problem in down markets or when you've borrowed heavily against current value and the home doesn't appreciate as expected.

Which ADU financing path fits your situation?

Answer capsule. The right financing path depends on five factors: ADU type, current equity position, your first-mortgage rate, your cash flow, and whether the lender needs to consider future value. A fixed home equity loan is one of seven viable lanes — not the default for every project.

| If your situation is… | First path to test | Why |

|---|---|---|

| Strong equity, locked scope, low first mortgage rate | Home equity loan (this page) | Predictable fixed payment, preserves first mortgage |

| Strong equity, moving scope, low first mortgage rate | HELOC | Draw flexibility during construction |

| Limited current equity, recent purchase, solid post-ADU value lift | ARV HELOC (RenoFi, Tower Dreamline, Spring EQ) | Underwrites on after-renovation value |

| Limited current equity, building from scratch | Construction-to-permanent or Fannie Mae HomeStyle / Freddie Mac CHOICERenovation | Borrows against as-completed value |

| Current first mortgage rate above ~6.5% | Cash-out refinance | May consolidate to better terms |

| Cash flow constrained, cannot service new payment | Home equity investment (HEI), with state-availability check | No monthly payment, different structure |

| Lot feasibility not yet confirmed | Feasibility check first, no financing | Do not borrow before feasibility |

For the staged-construction path, see our HELOC for ADU guide. For the broader financing-options hub, see our How to Finance an ADU in 2026: 7 Paths Compared.

What we verified

Before publishing, The Dwelling Index editorial team verified the following:

- Home equity loan structure and risk: Consumer Financial Protection Bureau and Federal Trade Commission consumer guidance on home equity loans and HELOCs.

- Tax deductibility rules: IRS Publication 936, 2025 tax year (published October 28, 2025); IRS FAQs on real-estate-related interest deductibility; IRS Rev. Proc. 2025-32 inflation adjustments for 2026 standard deduction amounts; secondary analyses of the One Big Beautiful Bill Act's permanence provisions.

- Current rates: Curinos LLC home equity index as published by Experian (May 2026); Bankrate home equity loan rate survey (May 15, 2026); Federal Reserve H.15 prime rate.

- ADU cost ranges: Angi 2026 ADU cost report; GreatBuildz Los Angeles 2026 cost guide; LA Family Builders California 2026 ADU cost report; SnapADU San Diego cost data; ADU Rules by Zip Code 2026 state-tier benchmarks.

- Lender-specific terms: Patelco ADU HELOC disclosure (rates effective 05/18/2026); Foothill Credit Union ADU HELOC product materials; Tower Federal Credit Union Dreamline Renovation HELOC page (eight-state availability verified); RenoFi public state-availability disclosure (49 states, Texas excluded); New American Funding ADU loan page; Figure HELOC product disclosure; Spring EQ HELOC product information.

- Mortgage agency ADU policy: Fannie Mae Selling Guide (Accessory Dwelling Units); Fannie Mae Selling Guide B3-3.8-01 (Rental Income, 30% ADU income cap); Freddie Mac Single-Family ADU policy.

- FHA ADU policy: HUD Mortgagee Letter 2023-17.

- Property tax assessment of ADUs in California: Santa Clara County Assessor public guidance on ADU new-construction assessment.

Last verified: May 19, 2026. Next scheduled review: June 19, 2026 for rate data; August 19, 2026 for lending-rule and lender-disclosure review; January 2027 for full IRS Publication 936 refresh after the 2026 tax-year publication.

Methodology

This guide is an independent educational resource published by The Dwelling Index. To assemble this article we (1) pulled current rate benchmarks from Curinos via Experian and Bankrate's separate survey, cross-checked against the Federal Reserve H.15; (2) verified the IRS deductibility rule against IRS Publication 936 for the 2025 tax year, and cross-checked the OBBBA permanence provision against post-2025 secondary tax analyses; (3) pulled product-specific terms directly from each named lender's public disclosure page on May 19, 2026; (4) assembled cost ranges from multiple independent builder and industry sources rather than a single one, labeling all numbers that derive from Dwelling Index editorial synthesis rather than a single published figure; (5) verified Fannie Mae, Freddie Mac, and FHA ADU policy directly against published guidance from each agency; and (6) verified state-law claims against primary statute and code citations. Where we couldn't independently verify a specific figure, we either omitted it or labeled it as a Dwelling Index planning estimate. We do not rank lenders by what they pay us; we earn affiliate revenue on Mortgage Research Center referrals only, disclosed inline at every CTA. We are not a lender, broker, or tax advisor, and nothing in this article is financial, tax, legal, construction, or lending advice.

Frequently asked questions

Can I use a home equity loan to build an ADU?

How much equity do I need for an ADU home equity loan?

Is a home equity loan or HELOC better for an ADU?

Will a home equity loan let me keep my current mortgage?

Is a cash-out refinance better than a home equity loan for an ADU?

Can ADU rental income help me qualify?

Is home equity loan interest tax deductible for an ADU?

What happens if the ADU costs more than my home equity loan?

Can I use a home equity loan for a prefab or modular ADU?

Should I apply for the loan before permits?

Will building an ADU raise my property taxes?

How long does it take to close on a home equity loan for an ADU?

Before you do anything else, check the lot

Most of this page assumes the project is buildable. That assumption needs to be tested before you submit a single loan application. Setbacks, lot coverage, fire-zone overlays, septic capacity, utility-lateral feasibility, and city-specific ADU rules vary block by block. The right next step depends on where you landed:

Equity covers the build

Scope is locked → compare lender offers next.

See What You Can Build → Get Your Free ADU ReportNot sure which loan fits

Compare home equity, renovation, and construction loan options.

Compare Options at Mortgage Research Center →Want the full checklist

Budget, permit, and financing checklist before you talk to anyone.

Download the Free ADU Starter Kit →Not sure where to start? See what's possible at your address — get your free ADU report in 60 seconds.

Affiliate disclosure: Some links on this page route to Mortgage Research Center (MRC), a lender-matching platform. The Dwelling Index may earn a commission if you connect with a lender through those links; you pay nothing extra. All affiliate links are labeled. Editorial content is independent and never influenced by affiliate relationships. See our full disclosure.

Financial disclaimer: Nothing on this page is financial, tax, legal, construction, or lending advice. Home equity loan terms, approval, rates, fees, and qualification requirements vary by lender and borrower. Verify all terms directly with licensed professionals before making any financing decision. Home equity loans are secured by your home; failure to repay can result in foreclosure.