FHA 203(k) Loan for ADU: What Works, What Doesn’t, and When to Use Another Loan

By The Dwelling Index Editorial Team · · Last verified May 19, 2026 against HUD Mortgagee Letters 2023-17 and 2024-13, HUD Handbook 4000.1, Fannie Mae, and Freddie Mac guidance · ~38 min read

Independent ADU resource · Not a lender or broker · Editorial standards →

The bottom line on the FHA 203(k) loan for an ADU

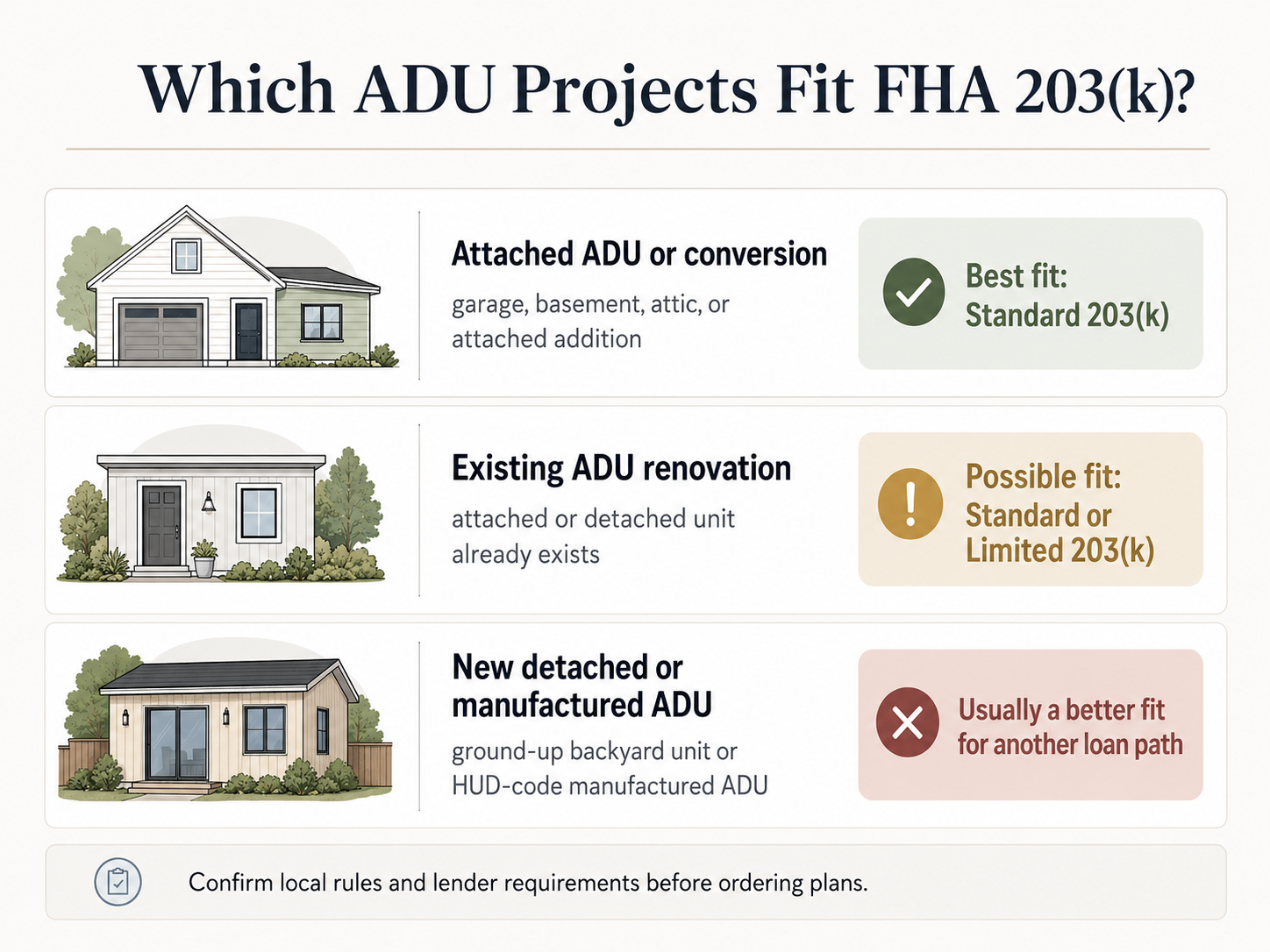

Yes — the FHA 203(k) loan can finance ADU work, but only specific kinds. The Standard 203(k) is the cleanest path for adding a new ADU attached to your existing home (including garage, basement, attic, or interior conversions) and for renovating an existing ADU — attached or detached. A brand-new, ground-up detached ADU is the danger zone: HUD’s official list of Standard 203(k) eligible improvements adds new ADUs only when they “will be attached to an existing Structure,” which leaves new detached construction outside the program for most buyers.

The Limited 203(k) is capped at $75,000 and prohibits structural or major remodeling work, so it almost never covers a full ADU build — only minor finish-out on an existing one. The total Standard 203(k) loan is subject to your county’s 2026 FHA loan limit — $541,287 in low-cost counties and up to $1,249,125 in high-cost counties — and also passes through a Loan-to-Value test (96.5% LTV for purchases, 97.75% for refinances).

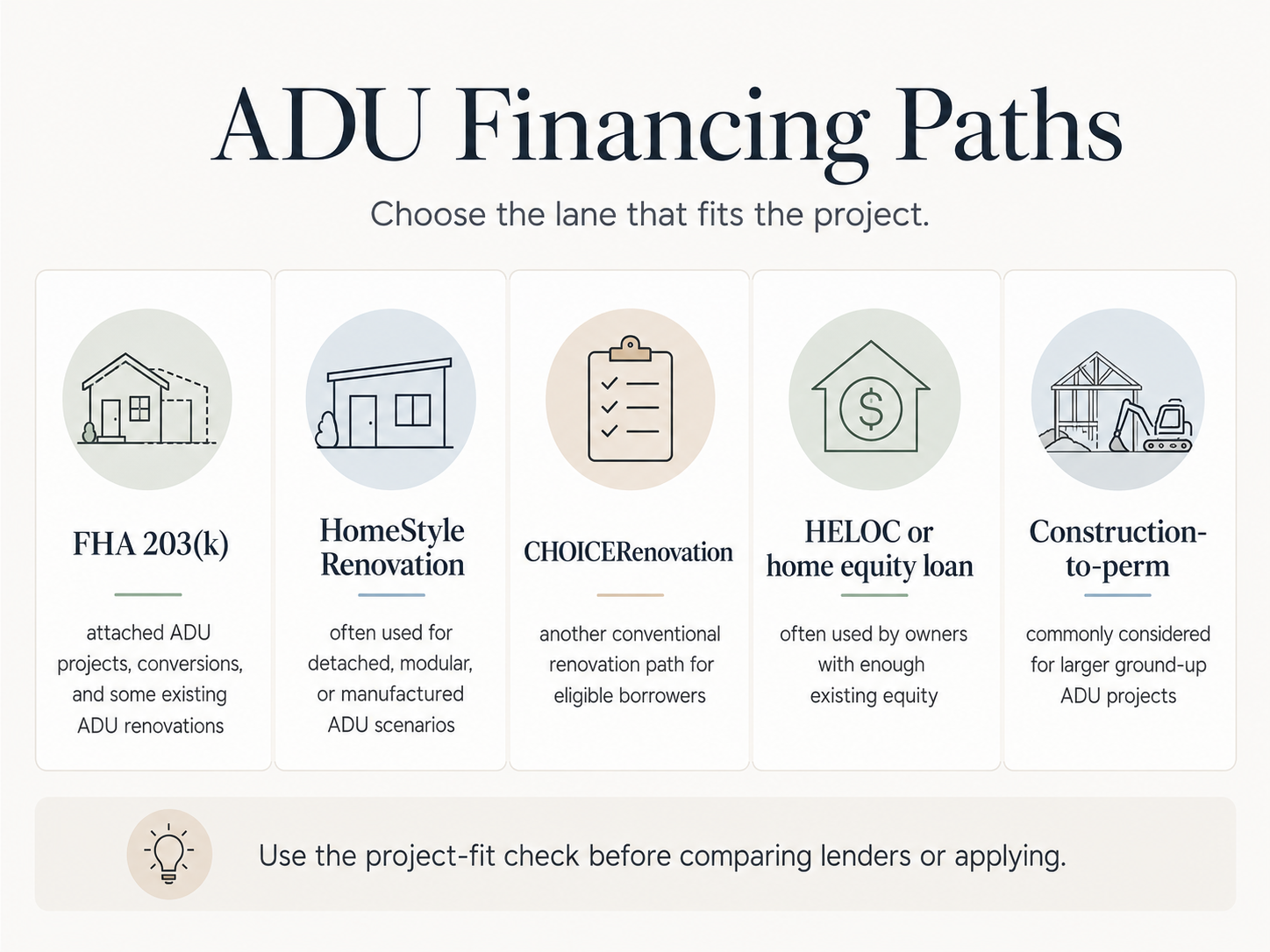

If you have a strong credit score, decent equity, and need a brand-new detached ADU, Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, or a construction-to-permanent loan will fit better. If you’re a first-time buyer with limited cash and a 580+ credit score adding an attached ADU, the FHA Standard 203(k) is the loan that opens this door wider than any other product on the market.

See What You Can Build

Before you apply for any loan, confirm what your lot can support. Setbacks, lot coverage, fire-zone rules, owner-occupancy, and HOA restrictions change which financing path is even relevant.

Get Your Free ADU Report →

What we verified for this guide

- HUD Mortgagee Letter 2023-17 (October 16, 2023) — the controlling FHA ADU policy, including Standard 203(k) eligible improvements, ADU rental-income rules, reserve requirements, and appraisal protocols. hud.gov ML 2023-17 PDF.

- HUD Mortgagee Letter 2024-13 (effective for FHA case numbers assigned on or after November 4, 2024) — the $75,000 Limited 203(k) cap, the 12-month Standard / 9-month Limited rehab periods, the updated Consultant fee schedule, and financeable Mortgage Payment Reserve rules. hud.gov ML 2024-13 PDF.

- HUD Handbook 4000.1 — the FHA Single Family Housing Policy Handbook, including the formal ADU definition and one-unit-with-ADU property classification.

- HUD 203k Calculator and HUD Form 92700 — the maximum-mortgage worksheet specifying the 96.5% purchase / 97.75% refinance LTV factors and the financeable origination fee formula.

- HUD-No. 25-145 — the 2026 FHA Single Family forward mortgage loan limits announcement.

- Pennymac Correspondent Announcement 23-88 — industry implementation of ML 2023-17.

- Fannie Mae Selling Guide B3-3.8-01 (Rental Income) and B2-3-04 — HomeStyle Renovation ADU rules and ADU rental-income calculation framework.

- Freddie Mac Single-Family Seller/Servicer Guide — CHOICERenovation ADU and manufactured-home renovation guidance, including the limitation effective May 4, 2026, on using rental income from a unit funded with CHOICERenovation proceeds for qualifying.

- Terner Center for Housing Innovation / Casita Coalition — California ADU Owner Survey (median statewide ADU construction cost).

- The Mortgage Reports — benchmarking the FHA 203(k) rate premium over standard FHA.

- Shelterforce (2023) — reporting on the Bipartisan Policy Center webinar discussion of detached-ADU eligibility under 203(k).

Last verified: May 19, 2026 · Last updated:

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

FHA 203(k) loan for ADU: which projects fit?

Here is the entire decision compressed into one table. Every row is sourced from HUD Mortgagee Letter 2023-17, Mortgagee Letter 2024-13, and Handbook 4000.1.

| Your ADU project | FHA 203(k) fit | Likely 203(k) path | Better alternative if FHA is wrong |

|---|---|---|---|

| Garage conversion (attached garage → ADU) | ✅ Strong fit | Standard 203(k) | HomeStyle or HELOC if you have equity |

| Basement conversion → ADU | ✅ Strong fit | Standard 203(k) | HomeStyle / HELOC |

| Attic conversion → ADU | ✅ Strong fit | Standard 203(k) | HomeStyle / HELOC |

| Attached addition (new ADU sharing a wall) | ✅ Strong fit | Standard 203(k) | HomeStyle (if conventional fits) |

| Renovating an existing attached ADU | ✅ Strong fit | Standard or Limited (scope-dependent) | HELOC for simpler finish-out |

| Renovating an existing detached ADU | ✅ Eligible | Standard or Limited (scope-dependent) | HELOC or HomeStyle |

| Brand-new, ground-up detached ADU | ❌ Not on HUD’s eligible-improvements list | None — pick a different loan | HomeStyle, CHOICERenovation, or construction-to-perm |

| New ADU above a detached garage | ⚠️ Gray area, lender-dependent | Ask lender directly; many will decline | HomeStyle / construction loan |

| JADU (Junior ADU within main house) | ⚠️ Case-specific | Standard or Limited if it meets HUD’s ADU/living-unit standard and local code | Verify with lender — state JADUs that allow shared sanitation may not meet FHA’s separate-ingress/egress requirement |

| Prefab / HUD-code manufactured ADU (new) | ❌ Not eligible under 203(k) | None | HomeStyle (allows manufactured ADU on permanent foundation); CHOICERenovation also has manufactured-home renovation paths |

| Buying a home that already has an ADU + light renovation | ✅ Strong fit | Standard or Limited | HomeStyle for higher loan amounts |

Sources: HUD Mortgagee Letter 2023-17 (Standard 203(k) Eligible Improvements, II.A.8.a.vi(A)(1)); HUD Mortgagee Letter 2024-13 (Limited 203(k) Eligible Improvements, II.A.8.a.vii); HUD Handbook 4000.1; Fannie Mae Selling Guide. Verified May 19, 2026.

If your row says ✅ Strong fit, keep reading — we go deep on each path below. If it says ❌, jump to What to use instead of 203(k) for a detached or prefab ADU.

Run our free FHA 203(k) ADU Fit Check →

Answer six questions about your project type, county, and credit profile. The tool returns the likely 203(k) lane (Standard or Limited), your county FHA loan-limit ceiling, projected ADU rent treatment under the 203(k)-specific rule, and the better alternative if FHA is the wrong door.

Run the FHA 203(k) ADU Fit Check →Can you use an FHA 203(k) loan for an ADU?

Yes. Under HUD Mortgagee Letter 2023-17 (October 16, 2023), the Standard 203(k) Rehabilitation Mortgage Insurance Program explicitly added accessory dwelling units to its list of eligible improvements — but only in specific forms: adding an ADU that will be attached to the existing structure, and renovating an existing ADU whether attached or unattached to the main home. New ground-up detached ADU construction is not on the list. The Limited 203(k) is generally too small and too restrictive to handle a real ADU build because it caps total rehabilitation costs at $75,000 and prohibits structural or major remodeling work.

What HUD changed in 2023 — and why it matters

Before October 2023, FHA programs allowed financing for properties that included a single ADU, but lenders couldn’t count any rental income from that ADU when underwriting your loan. That made ADU-equipped homes harder to qualify for, especially for first-time buyers and lower-income borrowers — the exact people FHA was designed to serve.

Mortgagee Letter 2023-17 changed three things at once. First, it updated the FHA appraisal protocol so appraisers are now required to analyze and report ADU market rent on appraisals. Second, it allowed lenders to include a portion of ADU rental income in the borrower’s Effective Income — meaning that ADU rent can help you qualify for the loan. Third, it added ADU-related work to the list of improvements eligible under the Standard 203(k) program and added single-family homes with ADUs to FHA’s New Construction-eligible property types.

How HUD defines an ADU for FHA purposes

HUD Handbook 4000.1 defines an Accessory Dwelling Unit as “a single habitable living unit with means of separate ingress and egress that meets the minimum requirements for a living unit.” Critically, an ADU “is a private space that is subordinate in size and can be added to, created within, or detached from a primary one-unit Single Family dwelling, which together constitute a single interest in real estate.”

That last clause matters. An ADU is part of your property, not a separate parcel — it cannot be sold separately under FHA rules (state laws like California’s AB 1033 allow this in limited cases through a multi-step process, but that’s a state-specific track, not an FHA permission). FHA also keeps the one-unit-with-ADU property classification distinct from a true two-unit property: “A Single Family residential one-unit Property with a single ADU remains a one-unit Property.”

The “separate ingress and egress” requirement matters more than most homeowners realize. California’s Junior ADU (JADU) statutes, for example, allow a JADU to share sanitation facilities with the main home. That arrangement may satisfy state law but can fall outside HUD’s FHA ADU definition. Confirm with your lender that your specific unit configuration meets HUD’s standard.

The eligible-improvements list, verbatim

For a Standard 203(k), HUD’s eligible-improvements list includes — among other items — converting a one-family structure to a one-family structure with an ADU, adding an ADU attached to an existing structure, renovating an existing ADU whether attached or unattached, and rehabilitating, improving, or constructing a garage. The list does not include new ground-up detached ADU construction. This is the exact wording where the industry confusion starts, which we address head-on next.

Does FHA 203(k) work for a detached ADU?

The FHA 203(k) does not currently allow building a brand-new detached ADU on your property. It does allow renovating an existing detached ADU. Shelterforce reported in 2023 that Casita Coalition and other ADU advocates were lobbying HUD to add new detached ADU construction to the eligible-improvements list and to raise the projected-rent factor for new ADUs from 50% to 75%. As of this page’s verification date, HUD’s published 203(k) ADU materials still limit new ADU construction under 203(k) to attached scopes.

Why blogs disagree about detached ADUs

If you’ve spent any time researching this, you’ve seen contradictions. Some lender pages flatly say “FHA 203(k) cannot be used to build a detached ADU.” Others say it can. Still others say “the ADU must be attached.” The contradictions are real and trace back to specific source material.

HUD ML 2023-17’s eligible-improvements list, in plain language, makes “adding an Accessory Dwelling Unit (ADU) that will be attached to an existing Structure” eligible, and “renovating an existing ADU that is attached or unattached to an existing Structure” eligible. That same list includes “rehabilitating, improving, or constructing a garage” as a separate line item. At a 2023 Bipartisan Policy Center webinar reported by Shelterforce, an FHA official stated that the 203(k) program “cannot be used to create a new, detached unit.” Yet the eligible-improvements list permits constructing a garage — which raised the obvious advocate question: could a homeowner build a new detached garage with an ADU above it under 203(k)? The official answer has remained ambiguous, and lender practice has filled the vacuum cautiously.

What this means for you, today

For new ground-up detached ADU construction with no existing structure being repurposed, the safe assumption in 2026 is that the FHA 203(k) is the wrong loan. Lenders will overwhelmingly decline this scope. If you’re building a new detached ADU, move to a Fannie Mae HomeStyle Renovation loan, a Freddie Mac CHOICERenovation loan, or a construction-to-permanent loan.

For an ADU above a new detached garage that you’re constructing through 203(k), expect this to be a case-by-case lender judgment call. Some FHA-approved 203(k) lenders will decline the request entirely; others may approve under the “rehabilitating, improving, or constructing a garage” line item with the ADU above it treated as part of the garage structure. Get this in writing from a 203(k)-experienced lender before you pay for plans.

For existing detached ADUs — say, a backyard cottage built in 1958 that needs new plumbing, electrical, kitchen, and code-compliance work — the 203(k) is on the table. The eligible-improvements list explicitly includes renovating an existing ADU “attached or unattached.” This is the part most blog posts miss.

Not sure your ADU type qualifies? Run your address through the Property Eligibility Check before you spend a dollar on plans. Last verified: May 19, 2026.

Standard 203(k) vs. Limited 203(k): which one fits your ADU project?

Almost every real ADU project belongs in the Standard 203(k) conversation, not the Limited. The Limited 203(k) is capped at $75,000 in total rehabilitation costs, prohibits structural and major remodeling work, must complete within nine months, and cannot fund anything that requires a HUD-approved 203(k) Consultant or architectural plans. Standard 203(k) handles the major work, requires a HUD-approved Consultant, allows up to 12 months for rehabilitation, and has no separate renovation-cost cap beyond the FHA county loan limit and LTV factor.

What changed in 2024

For years, the Limited 203(k) was capped at $35,000. HUD Mortgagee Letter 2024-13, effective for case numbers assigned on or after November 4, 2024, raised that cap to $75,000 and extended the Limited rehabilitation period to 9 months. The same letter extended the Standard 203(k) rehabilitation period to up to 12 months. The Limited 203(k) cap will now be evaluated annually alongside the FHA’s national forward-mortgage loan-limit announcement, so it may rise again.

For most ADU work, the new $75,000 cap still isn’t enough. A 2022 California ADU owner survey by the Terner Center for Housing Innovation in partnership with the Casita Coalition reported a $150,000 median statewide construction cost, with 71% of new California ADUs costing under $200,000. National numbers run higher in expensive markets and lower in some rural areas — but the point holds: Limited 203(k) becomes interesting for ADU buyers only in two specific scenarios — minor finish-out on a property where the ADU shell already exists, or cosmetic refresh of an inherited or recently-purchased existing ADU.

Standard vs. Limited 203(k) for ADU work

| Rule | Limited 203(k) | Standard 203(k) |

|---|---|---|

| Best ADU fit | Minor, non-structural updates on an existing ADU shell | Major ADU build, full conversion, structural work |

| Total rehabilitation cost limit | $75,000 (effective Nov 4, 2024) | No separate cap; total loan must fit FHA county limit |

| Minimum repair cost | No minimum | $5,000 minimum |

| Structural work allowed? | ❌ No | ✅ Yes |

| HUD 203(k) Consultant required? | ❌ No (optional; fee now financeable) | ✅ Yes — selected from FHA Consultant Roster |

| Architectural plans/exhibits allowed? | ❌ If required, project becomes Standard | ✅ Yes |

| Maximum rehabilitation period | 9 months | 12 months |

| Mortgage Payment Reserve financeable? | ❌ No | ✅ Up to 12 months PITI when home is uninhabitable |

| Contingency reserve | Optional; lender-established | Required under HUD Handbook; financeable up to 20% of repair costs |

| New attached ADU eligible? | Usually no — exceeds cap or requires plans | ✅ Yes |

| Existing ADU renovation eligible? | ✅ If minor and non-structural | ✅ Yes |

| Borrower may not occupy during rehab | Maximum 30 days | Allowed for longer periods |

Source: HUD Mortgagee Letter 2024-13, II.A.8.a.i(A)(2), II.A.8.a.vi(F), II.A.8.a.vii. Verified May 19, 2026.

Why Limited 203(k) usually fails for ADU work

Several Limited 203(k) rules quietly disqualify most ADU projects. The Limited 203(k) cannot fund any project that requires more than two payments per specialized contractor, requires plans or architectural exhibits, requires a Consultant to develop a Work Write-Up, or prevents you from occupying the property for more than 30 days total during the rehabilitation period. ADU work typically requires architectural plans (city plan check requires them), structural review (cutting into load-bearing walls for egress, kitchen, or bath additions), and contractor draws that exceed the two-payment-per-trade rule for plumbing, electrical, framing, and finish carpentry.

If your project requires any of those things, FHA reclassifies it as a major remodel — which forces you into Standard 203(k) regardless of how big the renovation budget is.

When Limited 203(k) does work for ADU buyers

A real example: you buy a house that already has a permitted ADU above the garage, but the interior is dated — old kitchen, original bathroom fixtures, worn flooring, no in-unit washer/dryer hookups. Total scope is $40,000 in cosmetic updates with no structural work, no plans required, completable in three months. That’s a clean Limited 203(k) candidate. The newer benefit under Mortgagee Letter 2024-13 is that the Consultant fee — if you choose to engage one for guidance — is now financeable under the Limited program, where it wasn’t before.

How much can you borrow with an FHA 203(k) for an ADU in 2026?

For 2026, the FHA loan limit on a single-unit property — including a one-unit home with one ADU — ranges from $541,287 in low-cost counties to $1,249,125 in high-cost counties. The total Standard 203(k) loan is calculated through HUD’s 203k Calculator using three checks: (1) the lower of acquisition cost plus rehabilitation cost OR 110% of after-improved value, (2) multiplied by the applicable LTV factor — 96.5% for a purchase, 97.75% for a refinance, (3) and capped at your county FHA limit. The lowest of those three governs your maximum base loan amount.

2026 FHA loan limits — the four tiers

| Property type | 2026 FHA floor (low-cost county) | 2026 FHA ceiling (high-cost county) |

|---|---|---|

| 1 unit (including 1 unit with one ADU) | $541,287 | $1,249,125 |

| 2 units | $693,050 | $1,599,375 |

| 3 units | $837,700 | $1,933,200 |

| 4 units | $1,041,125 | $2,402,625 |

Source: HUD-No. 25-145, FHA’s 2026 forward mortgage loan limit announcement. Verified May 19, 2026.

Alaska, Hawaii, Guam, and the U.S. Virgin Islands have special-exception FHA limits adjusted for higher construction costs; use HUD’s county lookup for the final number in those areas. For everyone else, use the FHA Mortgage Limits lookup tool on entp.hud.gov to find your county’s specific 2026 limit. Many mid-tier counties fall between the floor and the ceiling.

The three-step max-loan math, decoded

Per HUD’s 203k Calculator and HUD Form 92700, the maximum Standard 203(k) mortgage is determined in this sequence:

Step 1 — The lower-of-two value test.

Take the lower of:

- (a) Acquisition cost (or existing debt for refinance) + total rehabilitation cost + eligible fees, OR

- (b) 110% of the appraised after-improved value of the property.

Step 2 — Apply the LTV factor.

- 96.5% for an owner-occupant purchase, or

- 97.75% for an owner-occupant refinance.

Step 3 — Apply the FHA county loan limit.

The final base mortgage cannot exceed your county’s 2026 FHA loan limit. Whichever number is lowest across the three steps becomes your base mortgage amount.

Worked purchase example

You’re buying a $400,000 home in a county with a $541,287 FHA limit, planning a $150,000 attached garage-conversion ADU.

- Acquisition + rehab: $400,000 + $150,000 = $550,000

- 110% of after-improved value (assume $580,000 appraised): $580,000 × 110% = $638,000

- Lower of those two: $550,000

- Apply 96.5% LTV factor: $550,000 × 96.5% = $530,750 base mortgage

- County limit check: $530,750 is below $541,287. ✅

- Your maximum base mortgage is approximately $530,750.

Additions for financeable repairs, fees, and reserves may modify this slightly per the HUD calculator. Illustrative only — not a loan offer.

Worked refinance example

You currently owe $350,000 on a home worth $475,000 in the same $541,287-limit county and want to add a $200,000 attached ADU.

- Existing debt + rehab cost + eligible closing costs/prepaids: ~$555,000

- 110% of after-improved value (assume $650,000 appraised): $650,000 × 110% = $715,000

- Lower of those two: $555,000

- Apply 97.75% LTV factor: $555,000 × 97.75% = $542,512.50 — exceeds the $541,287 county limit

- County limit governs: $541,287 base mortgage

- The gap of approximately $13,000+ would need to be brought to closing or absorbed by scaling back the project.

Illustrative only — not a loan offer.

Why FHA county limits often disqualify ADU buyers in expensive markets

In coastal California, parts of Hawaii, the New York and DC metros, and a handful of mountain-resort counties, the 2026 FHA ceiling of $1,249,125 sounds high until you price the actual project. A $900,000 home purchase plus a $300,000 attached ADU build totals $1,200,000 — fits the ceiling on paper, but only barely, and any appraisal weakness or cost overrun blows the deal. In those markets, conventional Fannie Mae HomeStyle Renovation often gives you more flexibility — not because the loan amount cap is higher (conforming limits also peak at $1,249,125 for one-unit properties in high-cost areas) but because the underwriting framework is conventional rather than FHA, which lets the right borrower avoid the FHA MIP burden we cover in the cost section.

Can ADU rental income help you qualify for an FHA 203(k) loan?

Yes — but the percentage of projected rent you can use depends on which FHA rule applies to your transaction. For an FHA 203(k) transaction on a one-unit property with an ADU where you don’t have a history of rental income from the subject property since the previous tax filing, HUD’s 203(k)-specific rule uses 50% of the lesser of appraiser fair-market rent or lease/rental agreement. For other FHA transactions on a one-unit-with-ADU property (non-203(k)) with no rental history, FHA’s general rental-income rule uses 75% of the lesser. In both cases, ADU rental income is capped at 30% of total monthly effective income, the borrower must document 2 months of PITI reserves, and ADU rental income cannot be used to qualify for an FHA cash-out refinance.

The 203(k)-specific 50% rule

Per HUD ML 2023-17, Section II.A.8.a.ii, when the subject property is a one-unit home with an ADU and the borrower does not have a history of rental income from the subject property since the previous tax filing, the lender must use 50% of the lesser of:

- fair market rent reported by the Appraiser; or

- the rent reflected in the lease or other rental agreement.

Worked example — 50% rule, illustrative only

You earn $6,000/month W-2. You’re buying a $400,000 home and using Standard 203(k) to add a $150,000 attached garage-conversion ADU. The appraiser reports fair-market rent of $1,800/month.

- 50% of $1,800 = $900/month of qualifying ADU rent

- Add to base income: $6,000 + $900 = $6,900/month effective income

- 30% cap check: 30% of $6,900 = $2,070. The $900 sits well under the $2,070 cap. ✅

That $900/month of additional effective income lowers your DTI meaningfully. If your DTI was sitting at 47% — too high for FHA without compensating factors — adding the $900 in qualifying ADU income could drop it to 43% or below and turn a decline into an approval.

Illustrative only — not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

The general FHA 75% rule (non-203(k))

For other FHA transactions on a one-unit-with-ADU property where the borrower has limited or no history of rental income from the subject property since the previous tax filing, FHA’s general rental-income section (HUD ML 2023-17, II.A.4.c.xii(I) and II.A.5.b.xii(I)) uses 75% of the lesser of fair-market rent or the lease rent.

So which percentage applies to your deal depends on which lane you’re in. Buying a property that already has a permitted ADU and not doing 203(k) renovation work? The general FHA rule applies and your lender uses 75%. Buying or refinancing through 203(k)? The 203(k)-specific rule applies and your lender uses 50%. Confirm the exact underwriting lane with your lender because some scenarios — purchase plus light renovation — could be structured either way and your qualifying income changes meaningfully depending on the choice.

The 30% effective income cap — when it bites

The 30% rule from ML 2023-17 reads, in HUD’s exact framing: “The amount of the Rental Income from an ADU used as Effective Income must not exceed 30 percent of the total monthly Effective Income used to qualify the Borrower.” This cap applies under both the 203(k) 50% rule and the non-203(k) 75% rule. It was designed to prevent borrowers from leaning too heavily on speculative rental income.

The cap only bites in scenarios where the base income is low relative to the projected rent. Example under the 75% non-203(k) rule: base income $3,500/month, projected ADU rent $1,800/month → 75% × $1,800 = $1,350 of qualifying rent. 30% of total effective income ($3,500 + $1,350 = $4,850) = $1,455. The $1,350 sits just under, so you keep it all. But push the rent higher — say $2,400/month projected — and the math shifts: 75% × $2,400 = $1,800. Total effective income would be $5,300, 30% cap is $1,590, so you lose $210 of qualifying rent to the cap.

Reserves, documentation, and the cash-out exclusion

Three documentation rules from ML 2023-17 you should know before you talk to a lender:

- Reserves. If ADU rental income is being used to qualify, the mortgagee must verify and document reserves equivalent to two months’ PITI after closing for one-unit-with-ADU properties. This is liquid cash, not equity.

- Form 1007. The appraisal package requires the URAR (Fannie Mae Form 1004 / Freddie Mac Form 70) and Fannie Mae Form 1007 / Freddie Mac Form 1000 (Single Family Comparable Rent Schedule). The appraiser will determine fair-market rent by pulling comparable rental properties.

- No cash-out refi. Per ML 2023-17, “rental income from the ADU cannot be used as Effective Income to qualify for a cash-out refinance.” This is a hard rule with no exceptions. If you’re a current homeowner trying to fund an ADU build through a cash-out refi and lean on the projected rent to qualify, FHA is the wrong door — go to Fannie Mae HomeStyle or a HELOC instead.

Why ADU rent comps can be hard in ADU-sparse neighborhoods

Here’s a real friction point most blogs ignore. The appraiser’s fair-market-rent figure depends on comparable rentals nearby. In neighborhoods where ADUs aren’t common — most of the United States outside of California, Oregon, Washington, Colorado, and a few East Coast cities — comparable ADU rents are scarce, and appraisers often pull comps from small studios, garage apartments, or in-law suites in nearby buildings. Sometimes those comps come in lower than what your ADU will actually rent for once built. If the Form 1007 comes in low, your qualifying rent drops with it. This is the single most underappreciated risk in 203(k) ADU underwriting and is why some lenders quietly steer detached or unusual ADU projects toward HomeStyle, where the appraisal protocols are slightly more flexible.

Explore mortgage and refinance options for your ADU project. A 203(k)-experienced lender can review your qualifying scenario before you order full plans.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Eligibility, rates, loan limits, and program availability vary by borrower, property, lender, and location. The Dwelling Index does not guarantee loan approval, financing terms, rental income, or construction outcomes.

Compare FHA renovation and refinance paths →Mortgage Research Center — affiliate disclosure applies.

What does an FHA 203(k) ADU loan actually cost? (The full cost stack)

An FHA 203(k) ADU loan costs more than a vanilla FHA mortgage because of five stacking items: FHA Mortgage Insurance (the upfront 1.75% premium plus annual MIP), a financeable supplemental origination fee, the HUD 203(k) Consultant fee (Standard only), a contingency reserve held in escrow (required on Standard, optional on Limited), and a renovation-loan interest rate premium of roughly 0.75 to 1.0 percentage points above standard FHA rates.

The 203(k) ADU cost stack — verified line items

| Cost item | Standard 203(k) | Limited 203(k) | Vanilla FHA loan |

|---|---|---|---|

| Down payment | 3.5% (FICO 580+) / 10% (500–579) | Same | Same |

| Upfront MIP | 1.75% of base loan | 1.75% | 1.75% |

| Annual MIP | Per FHA schedule (LTV & term) | Same | Same |

| HUD 203(k) Consultant fee | Required — fee schedule below | Optional, now financeable | Not applicable |

| Financeable supplemental origination | Greater of $350 or 1.5% of (repair costs + fees + financeable contingency + financeable Mortgage Payment Reserves) | Greater of $350 or 1.5% of (repair costs + fees + financeable contingency) | Not applicable |

| Contingency reserve | Required; financeable up to 20% of repair costs | Optional, lender-established | Not applicable |

| Renovation-loan rate premium | ~0.75–1.0% above vanilla FHA rate (The Mortgage Reports, 2026) | Slightly less | Not applicable |

| Form 1007 + URAR appraisal | Required; ADU-specific protocols apply | Required | Standard URAR only |

Sources: HUD Mortgagee Letter 2024-13 (Consultant Fee Schedule, II.A.9.c); HUD 203k Calculator and HUD Form 92700; The Mortgage Reports (rate premium benchmarking, January 2026). Verified May 19, 2026.

The HUD 203(k) Consultant fee schedule (verified from ML 2024-13)

| Service | Maximum allowable fee |

|---|---|

| Feasibility Study (if requested) | $375 |

| Work Write-Up — repairs ≤ $50,000 | $1,000 |

| Work Write-Up — repairs $50,001–$85,000 | $1,200 |

| Work Write-Up — repairs $85,001–$140,000 | $1,400 |

| Work Write-Up — repairs > $140,000 | Lesser of 1% of repair cost or $2,000 |

| Additional Dwelling Unit (per unit) | +$25 |

| Draw inspection fee (per draw) | Maximum $375 (reasonable & customary for area) |

| Change order fee | $120 per request |

| Reinspection fee | $225 |

| Mileage (if Consultant >15 miles from property) | Current IRS mileage rate |

Source: HUD Mortgagee Letter 2024-13, II.A.9.c Consultant Fee Schedule. Verified May 19, 2026.

For a typical garage-conversion ADU with a $150,000 budget, expect approximately: Work Write-Up $1,400 + four to six draw inspections at ~$375 each ($1,500–$2,250) + likely one or two change orders ($120–$240) = total Consultant fee in the $3,000 to $4,000 range over the life of the project. On a $250,000 attached ADU build with more draws, plan for $4,500–$6,000+.

The financeable supplemental origination fee

For both Standard and Limited 203(k) loans, FHA allows lenders to charge a supplemental origination fee in addition to the standard origination charge. Per HUD’s 203k Calculator, the fee is the greater of $350 or 1.5% of the sum of repair/improvement costs, eligible fees, financeable contingency reserves, and (for Standard 203(k)) financeable Mortgage Payment Reserves. On a $200,000 renovation portion with $20,000 in contingency reserves, that’s approximately $3,300 added to your closing costs.

The contingency reserve — required on Standard, optional on Limited

Standard 203(k) loans require a contingency reserve held in escrow alongside the renovation funds. Per the HUD calculator, the financeable contingency reserve cannot exceed 20% of the repair/improvement costs; the actual percentage required is set by the appraiser and Consultant based on project complexity (older homes often require closer to 20%; newer ones may set 10%). This is not an extra fee you pay — it’s a portion of your renovation budget held back to cover unexpected costs that emerge mid-build. Any unused contingency at the end of the project is applied to your loan’s principal balance.

Mortgage Payment Reserves — the financeable safety net most blogs miss

Per HUD ML 2024-13, on Standard 203(k) loans, a mortgagee may establish a financeable Mortgage Payment Reserve of up to 12 months of mortgage payments to cover the period when you cannot occupy the property during rehabilitation. If you’re buying a house and adding an ADU that requires extensive structural work — and you can’t move in during construction — you can finance up to 12 months of PITI into the loan rather than paying out of pocket on top of your current rent or mortgage. This is genuinely useful and almost never mentioned on lender blogs.

The interest rate premium

FHA 203(k) loans typically run 0.75 to 1.0 percentage points above a vanilla FHA loan rate, per The Mortgage Reports’ January 2026 analysis. That premium reflects the additional risk and complexity of renovation lending. Current rates are not provided here because they change weekly — confirm benchmark FHA and 203(k) rate ranges with your lender at the time you apply.

The total cost-stack vs. a HELOC for the same project

For a homeowner with strong equity who has a low first-mortgage rate (sub-5%) locked in from 2020–2022, the 203(k) cost stack usually adds up to more than a HELOC. A back-of-envelope comparison on a $200,000 ADU build:

| Cost element | 203(k) Standard | HELOC + existing mortgage preserved |

|---|---|---|

| Required equity | None (after-improved value rule) | 20%+ typically |

| Upfront MIP | 1.75% of base loan amount | None |

| Supplemental origination | ~1.5% of repair + fees + reserves | None |

| HUD Consultant total | ~$3,000–$6,000 | None |

| First-mortgage rate effect | Replaces existing first mortgage | Preserves existing first mortgage |

| Mortgage insurance after closing | Annual MIP (often for life of loan) | None |

The 203(k) wins where the HELOC fails: when you don’t have enough equity, don’t have the FICO for a strong conventional loan, or are buying a fixer-upper-with-ADU-potential as your primary residence. It loses where the HELOC wins: when you already have the equity and a good first-mortgage rate worth preserving. Match the loan to your starting position, not to a generic recommendation.

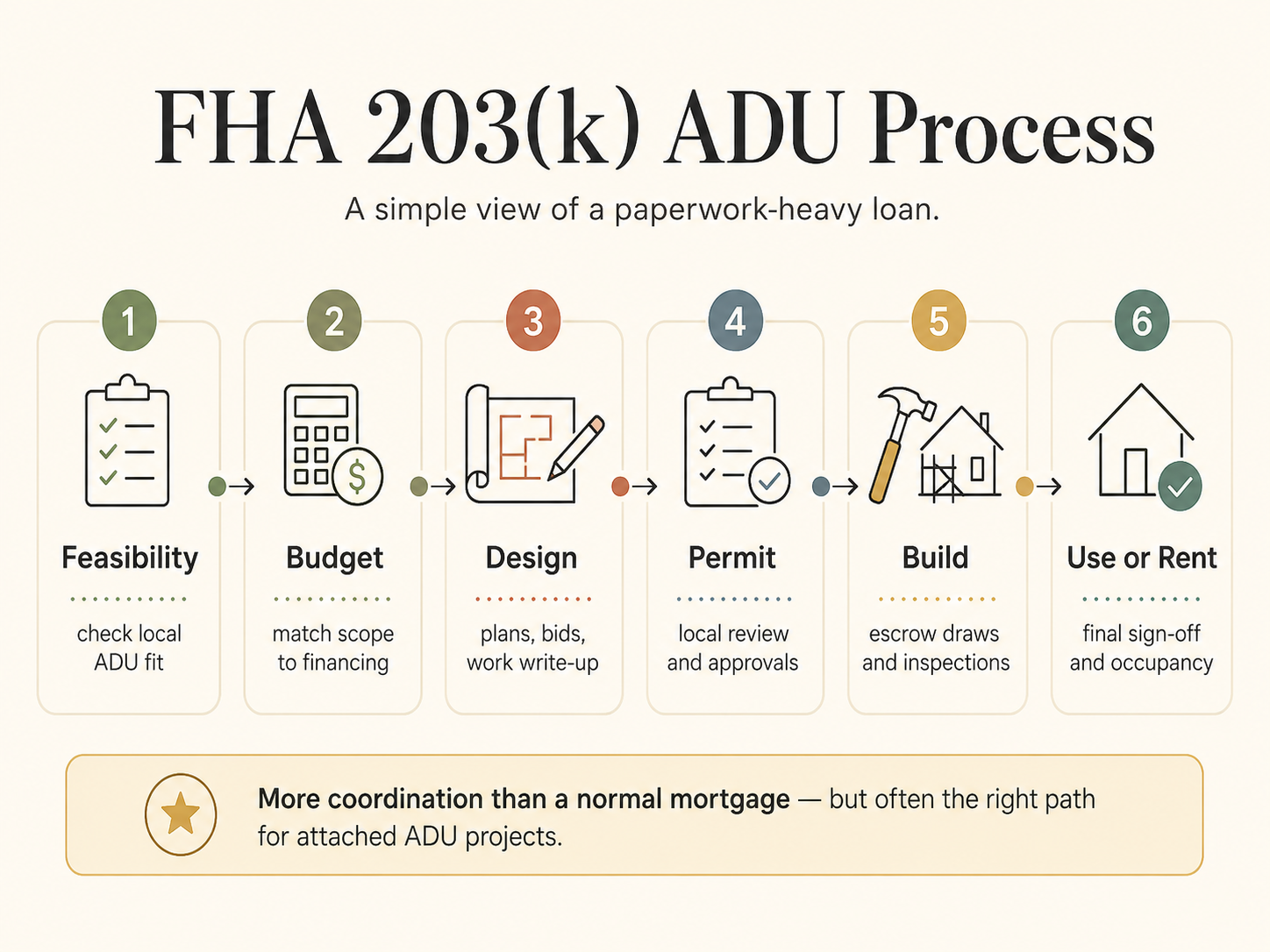

How long does an FHA 203(k) ADU loan take?

Plan for 60 to 90 days from application to closing, then up to 12 months from closing to complete construction on a Standard 203(k) ADU loan. Rehabilitation must begin within 30 days of closing under HUD’s loan agreement rules. Most ADU projects complete within 4 to 8 months of construction once permits and contractors are aligned — the 12-month cap (Standard) and 9-month cap (Limited) are regulatory ceilings, not typical timelines.

Stage-by-stage breakdown

| Stage | Typical duration | What happens | Where ADUs tend to delay |

|---|---|---|---|

| 1. Pre-approval | 1–7 days | Credit pull, income verification, county loan-limit confirmation | Rare delays |

| 2. Find 203(k)-experienced lender | 1–3 weeks | Many FHA-approved lenders don’t do 203(k); fewer have done ADU-scope 203(k)s | Lender shortage in some metros |

| 3. Engage HUD 203(k) Consultant | 1–2 weeks | Consultant inspects property, prepares Work Write-Up | Consultant scheduling in rural areas |

| 4. Contractor bids | 2–4 weeks | Contractor bids must match Consultant scope | Contractors unfamiliar with 203(k) draw paperwork |

| 5. Appraisal (URAR + Form 1007) | 1–2 weeks | After-improved valuation; comparable rent analysis | Form 1007 comparable rent challenges in ADU-sparse areas |

| 6. Underwriting | 3–4 weeks | Lender reviews complete file | Lender overlays beyond FHA minimums |

| 7. Closing | 1 week | Renovation funds escrowed | Last-minute appraisal questions |

| 8. Permit submission & construction start | Within 30 days of closing | Construction begins per HUD agreement | City plan check delays |

| 9. Draws & inspections | 4–8 months typical | Funds released as work milestones complete | Contractor cash flow; weather; site conditions |

| 10. Final inspection & closeout | 2–4 weeks | Certificate of occupancy if applicable | City final inspection scheduling |

The five things that delay 203(k) ADU closings the most

- The appraisal comes in low. The after-improved value didn’t support the loan amount. Mitigation: order a preliminary appraisal feasibility study before you finalize the contractor bid.

- The contractor backs out of 203(k) paperwork. Mid-project, the contractor decides the draw documentation is too much hassle and walks. Mitigation: hire a contractor who has completed at least three prior 203(k) jobs.

- The Form 1007 comparable rent is too low. No comparable ADU rents in the neighborhood drag the figure down, which collapses your qualifying rent and your DTI. Mitigation: pull your own rent comps from local apartment listings and bring them to the appraiser.

- The scope creeps mid-bid and the budget exceeds your county FHA limit. Mitigation: lock the Consultant’s Work Write-Up before getting more than two contractor bids.

- Permits delay the construction start past 30 days. HUD allows extensions but it requires lender approval. Mitigation: submit your permit application before closing if your city allows it.

What can stop an FHA 203(k) ADU loan?

The most common blockers are not the word “ADU” — they’re local zoning, the attached-vs-detached mismatch, a Limited-vs-Standard scope mismatch, FHA county loan-limit shortfalls, weak appraisals, contractor unwillingness to work with 203(k) paperwork, reserve shortfalls, lender overlays beyond FHA minimums, and HOA or private-covenant restrictions that block your ADU regardless of state law. FHA financing cannot make an illegal ADU legal.

Local zoning is the first gate, and FHA does not override it

Many states have expanded ADU rights significantly since 2017, but FHA financing still does not override local zoning, permits, CC&Rs, fire zones, or building code. Every property still has to satisfy local setbacks, lot coverage limits, fire-zone rules, parking requirements, and historic-overlay rules where applicable. FHA cannot insure a loan for an illegal or unpermitted ADU. Before you talk to a lender, confirm your project can actually be permitted. Our Property Eligibility Check screens for common local ADU blockers and points you to the right code and permit checks for your jurisdiction.

HOAs and private covenants — the dealbreaker most homeowners don’t think to check

If you live in an HOA, some HOA conditions, covenants, and restrictions (CC&Rs) can still apply even where state law limits HOA bans on ADUs. Outside of states with HOA-override laws, HOA bans on ADUs can be enforceable. Pull your CC&Rs before you spend a dollar on plans.

Owner-occupancy: FHA requires you to live there

All FHA loans require you to occupy the property as your primary residence within 60 days of closing and to live there for at least 12 months. You cannot use a 203(k) to build a pure investment-rental ADU; the main home or the ADU must be your primary residence.

Contractor pushback is real

Some contractors will not work with 203(k) because of the draw inspection schedule, the documentation requirements, and the slower cash flow compared to private construction contracts. This is especially common in hot construction markets where contractors have plenty of cash-funded work. Mitigation: ask any contractor candidate point-blank, “How many 203(k) projects have you closed in the past 3 years?” If the answer is fewer than three, find another bidder.

Lender overlays beyond FHA minimums

FHA’s published rules are the floor — lenders are free to add stricter overlays. Common 203(k) overlays include minimum FICO of 620–640 (above FHA’s 580), maximum DTI of 43% (FHA technically allows higher with compensating factors), and refusal to fund ADU scopes that include detached construction or above-detached-garage ADUs. Always ask any lender for their 203(k) overlay sheet in writing before you commit.

What to use instead of FHA 203(k) for a detached or prefab ADU

If your ADU is brand-new detached, prefab, manufactured, or too expensive to fit inside your county’s FHA loan limit, compare four alternatives: Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, a HELOC or home equity loan, and a construction-to-permanent loan. HomeStyle is the most common 203(k) alternative for detached new-construction ADUs and supports manufactured ADUs on permanent foundations. CHOICERenovation also has ADU addition/renovation and manufactured-home renovation pathways subject to guide requirements. The right pick depends on your credit profile, equity position, and whether you need to use projected ADU rent to qualify.

The four alternatives, head-to-head

| Dimension | FHA 203(k) Standard | Fannie Mae HomeStyle Renovation | Freddie Mac CHOICERenovation | Construction-to-Permanent Loan |

|---|---|---|---|---|

| Min credit score (typical) | 580 (FHA min); 620–640 (lender overlay) | 620+ | 620+ | 680+ |

| Min down payment | 3.5% | 5% (3% in some cases) | 5% (3% in some cases) | 10–20% |

| Max LTV (primary, 1-unit) | 96.5% | 97% | Per Freddie guide | Lender-set |

| Detached new ADU eligible? | ❌ Not on HUD list | ✅ Eligible | ✅ Eligible | ✅ Eligible |

| Manufactured/HUD-code ADU? | ❌ | ✅ With permanent foundation | ✅ Renovation paths available subject to guide | ✅ |

| Use ADU rental income to qualify? | 50% under 203(k)-specific rule, 30% cap | Existing ADU on one-unit primary residence, purchase or limited cash-out refi, 30% cap | ❌ Banned May 4, 2026 for units funded by CR proceeds | Lender-dependent |

| Mortgage insurance | FHA MIP (upfront + annual, often for life of loan) | Conventional PMI (drops off at 78–80% LTV) | Conventional PMI (drops off at 78–80% LTV) | Permanent-phase only |

| HUD Consultant required? | ✅ Standard only | ❌ | ❌ | ❌ |

| Best for | Lower-credit, lower-cash buyers; attached/conversion ADUs | Detached ADUs; manufactured ADUs; conventional borrowers | Similar profile to HomeStyle | Large detached builds, strong credit/income |

Sources: HUD Mortgagee Letter 2023-17 and 2024-13; Fannie Mae Selling Guide B2-3-04, B3-3.8-01, B5-3.2; Freddie Mac Single-Family Seller/Servicer Guide. Verified May 19, 2026.

When to switch from FHA 203(k) to HomeStyle

- Your ADU is detached and new construction (HomeStyle allows it; 203(k) does not).

- You want a manufactured or HUD-code prefab ADU on a permanent foundation.

- Your credit score is 620+ and you’d rather have conventional PMI that drops off than FHA MIP that often persists for the life of the loan.

- Your county FHA loan limit is too tight for your total purchase + ADU budget.

When to switch to CHOICERenovation — and the May 4, 2026 caveat

Freddie Mac’s CHOICERenovation is functionally similar to HomeStyle but with one critical 2026 catch. For CHOICERenovation applications received on or after May 4, 2026, rental income from a unit funded with CHOICERenovation proceeds cannot be used to qualify the borrower. If using projected ADU rent for qualifying is a make-or-break for your approval, HomeStyle remains the more flexible conventional option until further notice.

When to skip renovation loans entirely and use a HELOC

A HELOC (home equity line of credit) keeps your existing first mortgage in place and pulls funds against your current equity — not the after-improved value. If you have 20%+ equity, a low pandemic-era first-mortgage rate worth preserving, and a credit score in the mid-700s or better, the HELOC is usually the cheapest and simplest path. The downside is variable-rate exposure during the draw period and no use of projected ADU rent for qualification. Read our deep-dive on HELOC for ADU for the full breakdown.

When the construction-to-permanent loan is the right answer

For large, ground-up detached ADUs over $300,000 in expensive markets, a construction-to-permanent loan often provides more room than a renovation loan. C-to-perm loans fund the build in stages, underwrite against the after-improved property value, and convert automatically to a permanent first mortgage at completion. The trade-off is higher credit and down-payment requirements (typically 680+ FICO and 10–20% down) and more lender oversight during the build. See our guide on construction-to-permanent loan for ADU for the full breakdown.

Compare FHA renovation and refinance paths with a mortgage specialist.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Eligibility, rates, loan limits, and program availability vary by borrower, property, lender, and location.

Explore mortgage and refinance options for your ADU →Mortgage Research Center — affiliate disclosure applies.

Step-by-step: how to apply for an FHA 203(k) for an ADU

Apply in this order: confirm local ADU legality, verify your 2026 FHA county loan limit, find a 203(k)-experienced lender, engage a HUD-approved 203(k) Consultant, collect contractor bids, order the appraisal package, complete underwriting, close, and begin construction within 30 days. Plan for 60 to 90 days from start to close; allow up to 12 months for the rehabilitation period.

The 9-step sequence

- Confirm your lot can support the ADU you want. Run your address through our Property Eligibility Check to verify setbacks, lot coverage, fire-zone status, owner-occupancy rules, and HOA restrictions. FHA financing cannot make an illegal ADU legal.

- Confirm your county FHA loan limit. Use the HUD FHA Mortgage Limits lookup. Your total Standard 203(k) loan (purchase price or refi balance + ADU renovation + soft costs) must fit inside this number after the 96.5%/97.75% LTV factor is applied.

- Find a 203(k)-experienced lender. Not every FHA-approved lender does 203(k). Even fewer have done ADU-specific 203(k)s post-ML-2023-17. Ask any candidate: How many 203(k) loans have you closed in the past 12 months, and how many of those included ADU work? If they can’t answer specifically, move on.

- Engage a HUD 203(k) Consultant (Standard 203(k) only). The Consultant is selected by the mortgagee from the FHA 203(k) Consultant Roster for your state. The Consultant inspects the property, prepares the Work Write-Up and the Cost Estimate, and signs off on draw inspections throughout construction.

- Collect contractor bids that match the Consultant’s Work Write-Up scope item-for-item. Mismatches between Consultant scope and contractor bid will stall closing.

- Order the appraisal. Your lender orders a URAR (Fannie Mae Form 1004 / Freddie Mac Form 70) plus a Single Family Comparable Rent Schedule (Form 1007 / Form 1000). The appraiser will provide both the after-improved value figure and the fair-market rent estimate for the new ADU.

- Underwriting and closing. The lender reviews your full file — credit, income, assets, reserves (2 months PITI if using ADU rental income), appraisal, Consultant Work Write-Up, contractor bid, and permit status. Plan for 3–4 weeks. Closing happens once the file clears.

- Permit submission and construction start. Construction must begin within 30 days of closing per the Rehabilitation Loan Agreement.

- Draws, inspections, and final closeout. Funds release in stages as work milestones complete and the Consultant inspects each phase. Final inspection and any required certificate of occupancy close the project. Any unused contingency reserve applies to your loan’s principal balance.

Find a 203(k)-experienced lender for your ADU project.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Eligibility and program availability vary by borrower, lender, property, and location.

Explore FHA renovation and refinance paths →Mortgage Research Center — affiliate disclosure applies.

What do FHA 203(k) ADU borrowers wish they knew sooner?

The FHA 203(k) ADU loan is the most paperwork-heavy way to finance an ADU. Between the HUD Consultant Work Write-Up, draw inspections, change-order documentation, contractor coordination, appraisal requirements, and the 30-day construction-start clock, you’ll spend more administrative time on this loan than on almost any other financing path. That’s the price of access — and access is what this loan delivers like nothing else.

The damaging admission

A Standard 203(k) ADU loan moves slower and demands more documentation than a HELOC, a cash-out refinance, or even a standard construction loan run by a borrower with strong credit and equity. You’ll deal with a Consultant on top of your contractor. You’ll wait for draw inspections before each payment release. You’ll fill out change-order forms for scope adjustments mid-build. You’ll watch the 30-day construction-start clock and the 12-month rehabilitation completion deadline. If you have the option of a HELOC with 20%+ equity and a sub-5% first mortgage you want to preserve, that path will be cheaper and faster almost every time.

Why the 203(k) still wins for the right buyer

It is the only government-backed loan that lets you buy a home and finance an attached ADU in the same loan with 3.5% down on a 580 credit score, while using 50% of the projected ADU rent to help you qualify. There’s no conventional alternative that opens this door this wide for first-time buyers and lower-income borrowers. For families combining households across generations, for buyers shut out of single-family pricing in expensive markets who can make the math work with rental income, and for current homeowners with limited equity who refinance into a 203(k) to add an attached unit, the 203(k) is the financing path that turns “we can’t” into “we can.”

When 203(k) does not fit and the better lane is obvious

If any of the following apply, treat this page as a redirect rather than a destination:

- You have 20%+ home equity and a sub-5% existing mortgage → use a HELOC. See our HELOC for ADU guide.

- Your ADU is brand-new detached construction → use HomeStyle or a construction-to-permanent loan.

- Your ADU is a prefab/HUD-code manufactured unit → use HomeStyle or explore CHOICERenovation manufactured-home renovation paths.

- Your total project budget exceeds your county FHA limit by more than 10% even after applying the LTV factor → use HomeStyle or construction-to-perm.

- You’re a current homeowner trying to use projected ADU rent on a cash-out refi → use HomeStyle (FHA cash-out refi excludes ADU rental income).

Edge cases and the things blogs don’t tell you

These are the scenarios that come up in real lender conversations and don’t make it into most published guides.

Multifamily property plus an ADU

If you buy a duplex and convert an attached garage into an ADU, the post-conversion property is classified as a 3-unit property per HUD Handbook 4000.1 (which treats ADUs on properties with two or more units as an additional unit). Your loan limit jumps to the 3-unit FHA ceiling — $837,700 floor to $1,933,200 ceiling in 2026. You can use up to 75% of fair-market rent on units you don’t occupy to help qualify, per existing FHA multi-unit rental income rules.

JADUs (Junior ADUs)

HUD’s FHA ADU definition requires “separate ingress and egress that meets the minimum requirements for a living unit.” Some state JADU laws — including California’s — allow JADUs to share sanitation facilities with the main home. A JADU that shares sanitation may satisfy state law but can fall outside HUD’s FHA ADU classification. Confirm with your lender that your specific JADU configuration meets both HUD’s standard and local code before assuming 203(k) financing is on the table.

Selling later

FHA loans are technically assumable but only with lender approval and underwriting of the assuming buyer. When you sell, you’re released from the mortgage. You cannot sell the ADU separately from the main home under FHA rules — the FHA definition treats both as a single interest in real estate. California’s AB 1033 separate-sale-conversion path is its own multi-step state-specific process and operates independently of the FHA loan.

Utility hookups and site work

203(k) covers eligible improvements but won’t always cover surprise utility upgrades that emerge mid-build — a new electrical service panel, a sewer-lateral replacement, a separate gas meter for the ADU. Build the contingency reserve into your plan deliberately, and ask the Consultant to scope utility work explicitly upfront.

Detached prefab ADUs and the 203(k) gap

Standard 203(k) does not finance new manufactured or HUD-code prefab ADUs. If you’re considering a prefab path, Fannie Mae HomeStyle Renovation is the most common renovation-loan answer, and our prefab ADU cost guide covers the all-in numbers by brand and size.

The “two payments per contractor” rule under Limited 203(k)

This trips up homeowners who think a $60,000 ADU finish-out can squeak under the $75,000 Limited cap. The Limited 203(k) prohibits more than two payments per specialized contractor — meaning the painter, plumber, electrician, and framer can each only be paid twice across the entire project. For most ADU scopes, this rule alone forces you into Standard.

Self-help / borrower-performed work

Contractors must be licensed when required by law, and FHA does recognize a narrow “Self-Help” exception where a borrower performs work under a Rehabilitation Self-Help Agreement (the borrower cannot be reimbursed for labor costs). Most lenders will require approved, licensed contractors for any ADU-scale work and rarely approve borrower self-help for major scope. Don’t plan around this exception as a normal path.

What to ask a lender before choosing FHA 203(k) for an ADU

Take this list to every lender conversation. The lender who answers all of them specifically and confidently is the one you want.

- How many FHA 203(k) loans have you closed in the past 12 months, and how many included ADU scope?

- Will my project be treated as attached new ADU, existing ADU renovation, garage conversion, or detached ADU?

- Does my scope qualify for Limited 203(k), or do I need Standard?

- What’s my county’s 2026 FHA loan limit, and what’s the binding constraint on my max-mortgage calc — the LTV factor, the 110% after-improved value, or the county limit?

- Will you apply the 203(k)-specific 50% ADU rental-income rule or another FHA rental-income section to my deal?

- Will you classify my JADU / internal unit as an FHA ADU under HUD’s separate ingress/egress requirement?

- Will my property be treated as one-unit-with-ADU, two-unit, or another classification?

- What’s your underwriter’s view on Form 1007 comparable-rent estimates in my neighborhood?

- What reserves will you require?

- Will you finance contingency reserves and Mortgage Payment Reserves in this scenario?

- What’s your lender overlay sheet for 203(k) ADU work? May I see it in writing?

- Will you accept my preferred contractor, or do I need to use one from your roster?

- How many draws will be allowed under my Work Write-Up?

- What’s your draw-inspection turnaround time?

- What happens if construction costs exceed my contingency?

- What happens if permits delay my construction start past 30 days?

FHA 203(k) ADU pre-application checklist

Before you spend a dollar on plans or pay a single fee, work through this list.

| Step | Done? |

|---|---|

| Verified local ADU is legal at my address (zoning, setbacks, lot coverage) | ☐ |

| Confirmed HOA / CC&R restrictions don’t block the ADU | ☐ |

| Identified ADU type: attached new, conversion, JADU, existing renovation | ☐ |

| Confirmed scope is non-structural (Limited) or structural (Standard) | ☐ |

| Realistic project budget within county FHA loan limit after LTV factor | ☐ |

| 2 months PITI in reserves (liquid) | ☐ |

| Credit score ≥ 580 (3.5% down) or ≥ 500 (10% down) | ☐ |

| Pulled lender 203(k) overlay sheet in writing | ☐ |

| Identified contractor with prior 203(k) experience | ☐ |

| Pulled rent comps for the ADU before appraisal | ☐ |

| Confirmed primary residence within 60 days of closing | ☐ |

| Reviewed HomeStyle as backup if FHA limit or scope falls short | ☐ |

Want the full pre-application package?

Includes the 16-question lender script, the permit-prep checklist, and the ADU financing comparison worksheet — the same tools we use when we research our city-specific guides.

Download the Free ADU Starter Kit →Frequently asked questions

Can you use a 203(k) loan to build a brand-new detached ADU?

No, not under HUD's current Standard 203(k) eligible-improvements list. New detached ADU construction is not on the list — only new ADUs attached to an existing structure and renovations of existing ADUs (attached or detached) qualify. For a new detached ADU, use Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, or a construction-to-permanent loan.

Can you use a 203(k) loan for a garage conversion ADU?

Yes — converting an attached garage into an ADU is one of HUD's named examples of an eligible Standard 203(k) project. The work is typically structural and over $75,000, so it requires Standard 203(k) (not Limited).

What's the maximum FHA 203(k) loan amount for 2026?

The 2026 FHA loan limit for a one-unit property (including a one-unit home with one ADU) is $541,287 in low-cost counties and up to $1,249,125 in high-cost counties per HUD's 2026 loan limits announcement (HUD-No. 25-145). Multi-unit properties have proportionally higher limits. Alaska, Hawaii, Guam, and the U.S. Virgin Islands have special-exception limits adjusted for higher construction costs. The maximum mortgage is also subject to the 96.5% purchase / 97.75% refinance LTV factor and the 110% after-improved-value rule.

How much ADU rental income can I count toward FHA qualifying?

For an FHA 203(k) transaction on a one-unit property with an ADU and no rental history from the subject property since the previous tax filing, the 203(k)-specific rule uses 50% of the lesser of appraiser fair-market rent or lease/rental agreement. For other FHA transactions on a one-unit-with-ADU property (non-203(k)) with no rental history, FHA's general rental-income rule uses 75% of the lesser. Both are capped at 30% of total monthly effective income. ADU rental income cannot be used to qualify for an FHA cash-out refinance. These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

What credit score do I need for a 203(k) ADU loan?

FHA accepts 580 with 3.5% down or 500–579 with 10% down. Most lenders set their own 203(k) overlay at 620–640 because of the additional complexity.

How long does an FHA 203(k) ADU loan take to close?

60 to 90 days from application to closing is realistic for a Standard 203(k) with ADU scope. Construction must start within 30 days of closing and complete within 12 months under HUD Mortgagee Letter 2024-13 (9 months for Limited).

Do I need a HUD Consultant for a 203(k) ADU project?

Yes, for Standard 203(k). The Limited 203(k) does not require a Consultant, but a Consultant fee — if you choose to engage one — is now financeable into the loan under HUD Mortgagee Letter 2024-13. For ADU scopes that need plans or structural work, Standard is the path and a Consultant is mandatory.

Can I do the ADU construction myself with a 203(k)?

Contractors must be licensed when required by law, and most lenders will require approved/licensed contractors for ADU-scale work. FHA recognizes a narrow Self-Help exception where the borrower performs work under a Rehabilitation Self-Help Agreement, but the borrower cannot be reimbursed for labor costs and most lenders won't approve this for major scope.

Is the FHA 203(k) the cheapest way to build an ADU?

Usually not. Between the upfront MIP, supplemental origination fee, HUD Consultant fee, and the 0.75–1.0% rate premium above vanilla FHA, the 203(k) cost stack is meaningful. The 203(k) wins on access — low down payment, low credit minimum, projected-rent qualification — not on absolute cost. For homeowners with strong equity and a low first-mortgage rate, a HELOC is typically cheaper.

Can the FHA 203(k) be used for a JADU (Junior ADU)?

Sometimes — it depends on whether your JADU configuration meets HUD's FHA ADU definition, which requires 'separate ingress and egress that meets the minimum requirements for a living unit.' Some state JADU statutes allow shared sanitation with the main home, which may not satisfy HUD's standard. Verify with your lender before assuming 203(k) financing is available for your JADU.

Does FHA require owner occupancy for a 203(k) ADU loan?

Yes. All FHA loans require you to occupy the property as your primary residence within 60 days of closing and to live there for at least 12 months. The main home or the ADU itself counts as primary occupancy.

Are permits required before construction starts under 203(k)?

Yes. All required local building permits must be in hand before construction begins, and the contractor is responsible for obtaining them. The 30-day construction-start clock begins at closing, so submit your permit application early in the process.

Can I use FHA 203(k) for a prefab or manufactured ADU?

For a new manufactured ADU, no — the 203(k) program doesn't extend to new HUD-code manufactured ADUs. For renovating an existing manufactured ADU already on permanent foundation, eligibility is lender-dependent. For new prefab/manufactured ADU work, use Fannie Mae HomeStyle Renovation, which explicitly allows HUD-code manufactured ADUs on permanent foundations, or explore Freddie Mac CHOICERenovation manufactured-home renovation paths.

What happens if the ADU is not legal under local zoning?

FHA cannot insure a loan for an illegal or unpermitted ADU. The property must satisfy local zoning, setback, lot coverage, and parking requirements before financing can proceed. Run your address through the Property Eligibility Check to verify legality before applying.

Is FHA 203(k) better than HomeStyle for an ADU?

For attached/conversion ADUs and lower-credit, lower-cash buyers: yes. For detached new construction, manufactured ADUs, and higher-credit borrowers who want conventional PMI that drops off: HomeStyle wins.

Sources and methodology

This guide was created by The Dwelling Index, an independent research resource covering ADU financing, costs, and regulations. We reviewed HUD’s primary policy documents (Mortgagee Letter 2023-17, Mortgagee Letter 2024-13, Handbook 4000.1, HUD-No. 25-145, the HUD 203k Calculator and HUD Form 92700, and the HUD 203(k) Comparison Fact Sheet), FHA correspondent-lender announcements implementing those policies (Pennymac Announcement 23-88), Fannie Mae’s HomeStyle Renovation guidance and ADU-specific Selling Guide sections (B2-3-04, B3-3.8-01, B5-3.2), Freddie Mac’s CHOICERenovation guidance, the FHA County Mortgage Limits lookup tool (entp.hud.gov), the Terner Center / Casita Coalition California ADU Owner Survey, The Mortgage Reports rate-premium benchmarking, and policy reporting from Shelterforce on advocacy efforts to expand detached-ADU eligibility. Voice-of-customer signals from borrower forums informed the user-friction analysis but were never used as authority for rules, regulations, or financial claims.

We do not invent expert reviewers, fabricate credentials, or take undisclosed compensation. We do disclose our affiliate relationships and our partner roster transparently — see our Affiliate Disclosure and Partner Vetting Policy. Information on this page is for educational purposes only and is not mortgage, legal, tax, or investment advice. Loan availability, rates, fees, underwriting requirements, reserves, property eligibility, and approval decisions vary by borrower, lender, property, and location. The Dwelling Index does not guarantee loan approval, financing terms, rental income, permit approval, or construction outcomes.

Last updated: · Last verified: May 19, 2026

Related guides on The Dwelling Index

- How to Finance an ADU in 2026: 7 Paths Compared — the pillar that puts FHA 203(k) in context with HELOCs, cash-out refis, construction loans, HomeStyle, CHOICERenovation, HEIs, and local programs.

- HELOC for ADU — the right alternative for homeowners with 20%+ equity and a low first mortgage worth preserving.

- ADU Rental Income: What Can You Earn? — to estimate the projected rent figure your appraiser’s Form 1007 will need to support.

- How Much Does an ADU Cost? — to size the renovation budget before you ask a lender what’s eligible.

- Prefab ADU Cost: Real All-In Prices (2026) — for buyers comparing prefab to site-built, where HomeStyle (not 203(k)) is the right loan.

- California ADU Laws — for California buyers checking state ADU statutes against their lot.

- Construction to Permanent Loan for ADU — the alternative when your ADU is too large or detached for 203(k).

Not sure where to start?

See what’s possible at your address — get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU Report