Construction to Permanent Loan for ADU: When It Works, When It Doesn’t, and Who Actually Offers It in 2026

By The Dwelling Index Editorial Team · · Last verified May 19, 2026 against Fannie Mae, Freddie Mac, HUD/FHA, USDA RHS, CFPB, California HCD, and the official program pages cited below · 32 min read

Independent ADU resource · Not a lender or broker · Editorial standards →

The bottom line on a construction to permanent loan for ADU

A construction to permanent loan for an ADU is a single mortgage product that funds the build in staged draws and then converts to a long-term permanent mortgage once the ADU passes final inspection — one underwriting, one set of closing costs, and in true single-close versions, one closing date. Yes, the product exists, but the agency-labeled path depends on whether you’re building a new home with an ADU or adding an ADU to a home you already own. Fannie Mae’s explicit construction-to-permanent ADU use case is building a new 1-unit property with an ADU; for existing homes, the agency points borrowers to HomeStyle Renovation (Fannie), CHOICERenovation (Freddie), or FHA 203(k) — products that function similarly to single-close C2P with draws and as-completed value underwriting.

Specialty construction lenders, mortgage brokers, credit unions, community banks, and a few state and city housing finance agencies do issue true single-close C2P for ADUs on existing properties. The product is the right tool when your current equity won’t cover the build and your existing first-mortgage rate isn’t worth protecting. The right first move isn’t calling a lender — it’s confirming what you can actually build.

| Your situation | First path to test | Why |

|---|---|---|

| Building a new primary home with an ADU from the ground up | Single-close construction-to-permanent loan | Fannie Mae’s explicit C2P ADU use case |

| Already own the home, adding an ADU, low equity, current first mortgage at or above market | HomeStyle Renovation, CHOICERenovation, or a portfolio construction-to-permanent | Single closing, draws, as-completed value underwriting |

| Already own the home, adding an ADU, strong equity, sub-5% first mortgage | HELOC or home equity loan | Protects your favorable first-mortgage rate |

| Garage, basement, or interior conversion under $100K | HELOC or FHA 203(k) Limited | Renovation logic fits better than ground-up C2P |

| FHA borrower converting or adding an attached ADU | FHA Standard 203(k) | HUD ML 2023-17 lists ADU as an eligible improvement |

| VA-eligible veteran building a new home + ADU | VA One-Time Close construction loan | Available through select VA-approved lenders |

| Eligible in City of San Diego, Massachusetts, Long Beach, or other public ADU program | Local public ADU loan first | Below-market terms with income, occupancy, and rent restrictions |

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

See What You Can Build

Check your lot, zoning, and likely financing lane in about 60 seconds. Setbacks, height, lot coverage, and fire-zone rules decide whether you’re funding a 600 sq ft unit or a 1,200 sq ft one — and that changes which financing lane fits.

Get Your Free ADU Report (60 sec)

What we verified for this guide

- Fannie Mae ADU page distinguishing construction-to-permanent (new construction) from HomeStyle Renovation (existing-property ADU additions); Selling Guide B5-3.1-02 (Conversion of Construction-to-Permanent Financing: Single-Closing Transactions); current B2-3-04 (Special Property Eligibility); Selling Guide Announcement SEL-2025-10 (December 10, 2025) and its multi-ADU expansion effective March 31, 2026 for lenders using UAD 3.6 policy only; Announcement SEL-2025-08 (ADU rental-income qualification, effective October 8, 2025); Desktop Underwriter 12.1 released the weekend of March 21, 2026. Verified via singlefamily.fanniemae.com and selling-guide.fanniemae.com on May 19, 2026.

- Freddie Mac CHOICERenovation page including the limitation, effective for applications received on or after May 4, 2026, that rental income from any unit included in the renovation project funded by CHOICERenovation mortgage proceeds cannot be used to qualify. Verified via sf.freddiemac.com on May 19, 2026.

- HUD/FHA Mortgagee Letter 2023-17 (dated October 16, 2023) — ADU definition, Standard 203(k) eligible ADU improvements, rental-income rules (75% with rental history, 50% for Standard 203(k) without rental history), the 30% cap on ADU rental income as a share of effective income, and the exclusion of ADU rental income on FHA cash-out refinances. Verified via hud.gov on May 19, 2026.

- USDA Rural Housing Service proposed rule RHS-26-SFH-0100 (Single Family Housing Guaranteed Loan Program — Income-Producing ADU Provisions), published in the Federal Register March 31, 2026; comment period closes June 1, 2026.

- CFPB consumer guidance describing construction loans as short-term loans funded in advances as construction progresses. Verified via consumerfinance.gov on May 19, 2026.

- California Government Code § 66315 prohibiting local owner-occupancy requirements on ADUs, made permanent by AB 976. Verified via the California HCD ADU Handbook (2025 update) on May 19, 2026.

- State and local programs: San Diego Housing Commission ADU Finance Program, MassHousing ADU Loan Program, City of Long Beach Backyard Builders second round. Each verified against the official program page on May 19, 2026.

- FTC endorsement guidance on disclosure of material connections. Verified via ftc.gov on May 19, 2026.

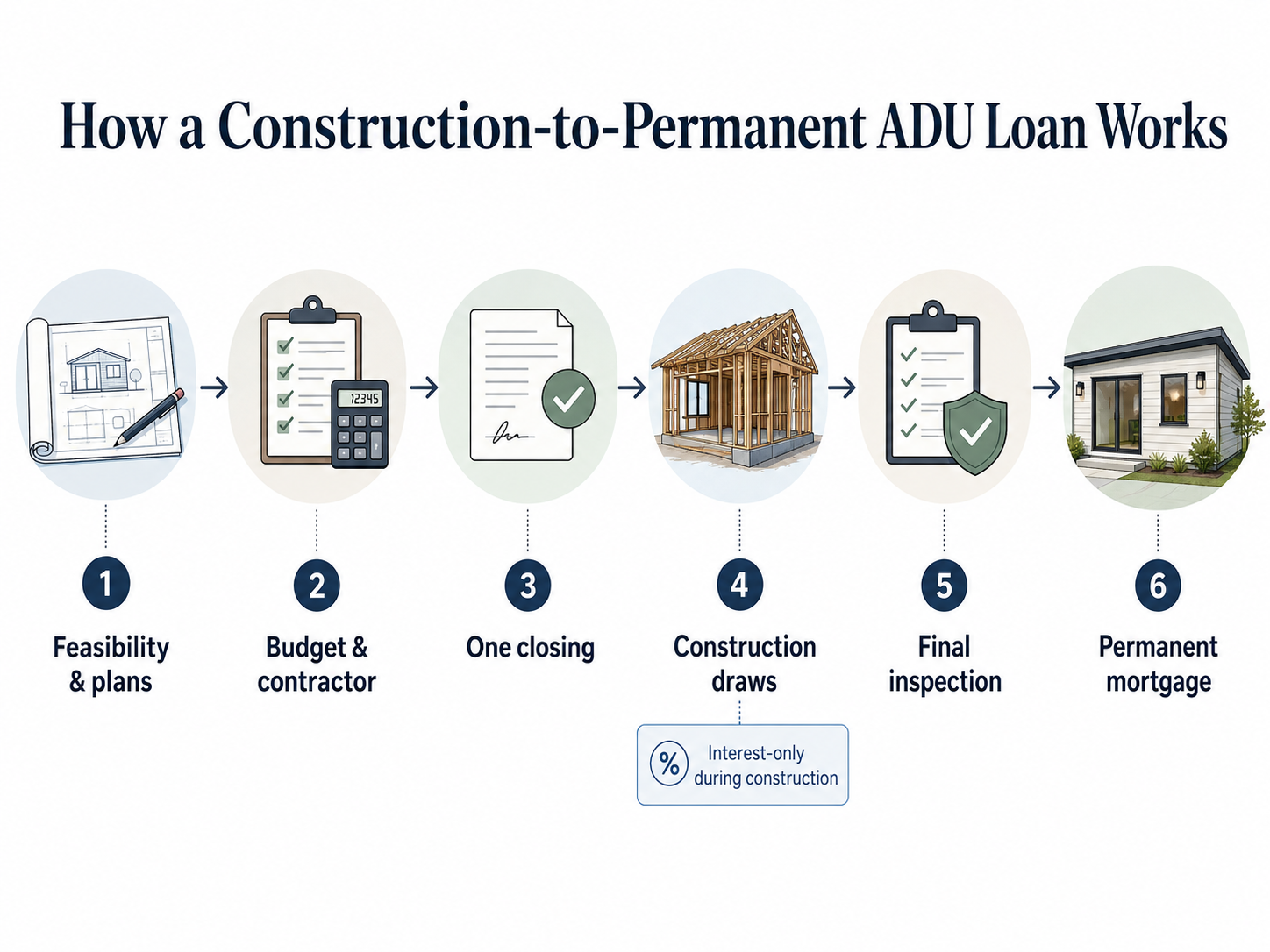

What is a construction to permanent loan for an ADU?

A construction to permanent loan for an ADU is a single mortgage that funds the ADU’s construction phase in staged draws and then converts to a long-term permanent mortgage when the ADU is complete. The CFPB describes construction loans as short-term financing released in advances as work progresses; the “to permanent” part means the same loan amortizes as a 15- or 30-year mortgage after final inspection, rather than requiring a separate refinance.

The industry uses overlapping labels for this category, and it pays to be precise:

- Construction-only loan — short-term financing for the build only. Must be paid off with cash or a separate refinance. Two loans, two closings, two sets of fees.

- Construction-to-permanent loan, two-time close — coordinated construction and permanent financing, but conversion requires a second closing (and often re-underwriting and a new appraisal). Two closings, two sets of fees.

- Construction-to-permanent loan, single-close (also “one-time close” or “OTC”) — one loan, one closing, one set of fees. Permanent rate is typically set at the original closing. Loan converts automatically when the ADU passes final inspection.

For an ADU, the structure most homeowners want — and the one this guide focuses on — is single-close construction-to-permanent (or its renovation-mortgage cousins, HomeStyle Renovation and CHOICERenovation, which behave similarly). Single-close eliminates the two biggest risks of the two-close version: getting re-qualified mid-build and being blocked at conversion by an intervening lien.

How the construction phase works for an ADU

Once the loan closes, the lender doesn’t hand you a check for the whole amount. Funds sit with the lender and get released in draws tied to construction milestones, after a third-party inspector verifies the work. A typical ADU draw schedule:

| Draw # | Milestone | Typical % of construction budget |

|---|---|---|

| 1 | Mobilization, demolition, deposits, permits | 5–10% |

| 2 | Foundation, underground utilities, site work | 15–25% |

| 3 | Framing, sheathing, roofing dry-in | 20–25% |

| 4 | Mechanical, electrical, plumbing rough-ins | 15–20% |

| 5 | Insulation, drywall | 10–15% |

| 6 | Interior finishes, cabinets, flooring, fixtures | 15–20% |

| 7 | Final inspection, certificate of occupancy, punch list | 5–10% |

Illustrative draw schedule based on common lender practice and the USDA Combination Construction-to-Permanent reference. Actual schedules depend on lender, builder, contract, and inspection protocol.

During construction you pay interest only on the cumulative drawn balance — not on the full loan. So in month one, with 10% drawn, your interest is on 10% of the loan. By month six, with 70% drawn, you’re paying interest on 70%. This is the structural reason construction loans are cheaper to carry early in the build.

How the permanent phase converts

In a single-close structure, conversion happens at the end of construction once the city issues the certificate of occupancy and the lender’s final inspection (Fannie Mae Form 1004D) confirms the ADU was built to the approved plans. The loan transitions from interest-only construction to a fully amortizing 15- or 30-year mortgage at the permanent rate set at original closing.

Fannie Mae Selling Guide B5-3.1-02 governs the mechanics. Key rules borrowers should know:

- A Fannie Mae single-closing C2P loan may be a purchase transaction or a limited cash-out refinance transaction; pure cash-out refinances are not eligible.

- No single construction-loan period may exceed 12 months, and the total construction period may not exceed 18 months. Builds that run longer must be processed as two-closing transactions.

- Income, employment, and credit documents must be no more than 4 months old at conversion — extended to 18 months if the original closing met two conditions (LTV/CLTV at or below 95% and an Approve/Eligible Desktop Underwriter recommendation).

- The permanent loan’s interest rate, loan amount, term, and amortization type may be modified at conversion within Fannie Mae’s tolerances; major changes can trigger re-underwriting.

Single-close C2P reduces — but doesn’t fully eliminate — the re-qualification risk. As long as the build wraps inside the construction-period limits and the borrower’s income, employment, and credit stay stable inside the 4/18-month window, the permanent phase is not a fresh second-closing qualification event.

Single-close vs. two-time close construction to permanent loans for an ADU

A single-close construction-to-permanent loan closes once, typically sets the permanent rate at the original closing, and converts when the ADU is complete. A two-time close requires a second closing with new fees, potentially a new appraisal, and full re-underwriting. Single-close substantially reduces the risk of re-qualification, rate movement, or appraisal failure mid-build and removes the intervening-lien risk that can block conversion in a two-close structure.

Land Gorilla, a construction-lending platform widely used by lenders to administer draws, defines an intervening lien as a lien — typically a mechanics lien filed by an unpaid subcontractor — recorded against the property between the construction-loan closing and the permanent-loan closing. In a two-close transaction, that lien must be paid off or subordinated before the new permanent loan can record in first lien position. In a single-close transaction, the loan is already in first position from day one; any mechanics lien filed during construction sits in second position behind it, and the build continues without the conversion being held hostage.

Side-by-side decision matrix

| Feature | Single-close C2P | Two-time close C2P | HomeStyle Renovation | FHA 203(k) Standard |

|---|---|---|---|---|

| Number of closings | 1 | 2 | 1 | 1 |

| Permanent rate set at original closing | Usually (Fannie permits limited modifications) | No (set at second closing) | Yes | Yes |

| Re-qualification at conversion | Limited (4/18-month rule) | Yes (full re-underwrite) | Not required | Not required |

| Intervening-lien risk at conversion | No | Yes | No | No |

| ADU on existing primary residence | Yes, but renovation mortgages are the cleaner agency path | Yes | Yes (Fannie Mae’s explicit existing-property ADU path) | Yes (HUD ML 2023-17) |

| Underwrites against as-completed value | Yes | Yes | Yes | Yes |

| Typical credit minimum | 680+ | 680+ | 620 | 580 |

| Typical max LTV of as-completed value | 95% | 95% | 97% (HomeReady-eligible) | 96.5% |

| Cash-out refinance eligible | No (purchase or limited cash-out only per B5-3.1-02) | Varies | Limited (HomeStyle has specific LCOR rules) | Standard 203(k) is not cash-out |

| Best fit | Larger ground-up ADU builds, strong income | Borrowers with a specific exit refi plan | Most ADU additions on existing homes | FHA borrowers, lower credit, conversions |

Why most lenders steer ADU borrowers to a renovation loan

Here’s the practical reality: when you call a national retail mortgage lender and say “I want a construction-to-permanent loan to build a backyard ADU on my existing home,” the loan officer often steers you toward HomeStyle Renovation, CHOICERenovation, or FHA 203(k). That’s because for an existing single-unit primary residence adding an ADU, those renovation products are the GSE-blessed path. Fannie Mae’s ADU page expressly says borrowers building a new 1-unit property with an ADU can use a Construction-to-Permanent loan, while borrowers purchasing or refinancing a 1-unit property and constructing or installing a new ADU can use a renovation loan.

This doesn’t mean a true single-close C2P is unavailable for an ADU on an existing home. It means you’ll have better luck with a specialty construction lender, a mortgage broker with construction-lending capability, a community bank, or a credit union. Functionally, HomeStyle Renovation behaves like a single-close C2P for the ADU use case: one closing, draws, as-completed value underwriting. Different label, similar experience.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Explore mortgage-based ADU financing options → MortgageResearch.com

MortgageResearch.com connects homeowners with mortgage-based financing resources and licensed loan officers. Construction, renovation, and ADU-specific options depend on lender, property, borrower, and state. Loan approval, terms, rates, and program availability are not guaranteed.

Can you use a construction to permanent loan to build an ADU on a home you already own?

Yes, the structure exists for existing-home ADU additions — but the cleaner agency path is usually a renovation mortgage. Fannie Mae’s official ADU guidance points borrowers building a new 1-unit property with an ADU to construction-to-permanent financing, and routes borrowers purchasing or refinancing a 1-unit property and constructing or installing an ADU to HomeStyle Renovation. Freddie Mac uses CHOICERenovation for the same case. FHA permits ADU construction under Standard 203(k) per HUD Mortgagee Letter 2023-17. All three function as one-loan, single-closing, draw-based, as-completed-value financing — which is what most homeowners actually mean when they say “construction-to-permanent loan for an ADU.”

When you tell a loan officer “I want a construction loan for my ADU,” they often hear “build me a new house.” If you’re adding to an existing home, the more accurate request is: “I want a one-time-close renovation mortgage or single-close C2P that underwrites against the as-completed value of my property with the new ADU.” That phrasing routes you to the right product faster.

How official programs classify your ADU project

| Project type | The label the agency uses | Why this matters |

|---|---|---|

| Build a new primary home plus an ADU together | Construction-to-Permanent (Fannie Mae) | One-loan, draw-based, true new construction |

| Already own the home; add a detached ADU | HomeStyle Renovation (Fannie) or CHOICERenovation (Freddie) | Renovation mortgage, single closing, as-completed value |

| Already own the home; add an attached ADU | HomeStyle, CHOICERenovation, or FHA 203(k) | Same renovation logic; ML 2023-17 lists attached ADU as eligible |

| Convert a garage, basement, or attic to an ADU | HomeStyle, CHOICERenovation, FHA 203(k), or HELOC | Conversion is closer to renovation than new construction |

| Purchase a home and add an ADU at the same time | HomeStyle, CHOICERenovation, FHA 203(k) | Renovation mortgage rolls purchase + improvement into one transaction |

| Build a new home that includes an ADU on the same lot | True Construction-to-Permanent | Cleanest C2P use case |

When a true single-close C2P fits an existing-home ADU

There’s a narrow but real set of cases where a true single-close C2P — not a renovation mortgage — is the better fit:

- The build is large enough (typically $300K+) that the lender wants the formal controls of a construction loan (third-party inspections, builder approval, formal draw schedule).

- The borrower has limited current equity, and the ADU will substantially change the property’s as-completed appraisal.

- The borrower wants a separate construction-phase rate structure rather than a renovation mortgage’s blended approach.

- The lender’s overlays allow C2P for ADU-on-existing-property — usually a specialty construction lender, a credit union, a community bank, or a state housing finance agency program.

Construction to permanent loan requirements for an ADU

Many construction-to-permanent lenders use overlays such as a minimum credit score around 680, a debt-to-income ratio at or below 45%, roughly 20–25% effective equity in the as-completed value, a fixed-price construction contract with a licensed and lender-approved general contractor, stamped plans and permits, and a “subject-to-completion” appraisal that supports the loan amount. FHA 203(k) Standard accepts credit scores as low as 580 with 3.5% down. SDHC requires 680. Lender overlays vary; the numbers below are typical, not universal.

Credit

| Program | Minimum credit score | Source |

|---|---|---|

| Conventional construction-to-permanent (Fannie / Freddie) | 680 typically; some lenders push to 720 for best pricing | Lender disclosures reviewed May 2026 |

| Fannie Mae HomeStyle Renovation | 620 | Fannie Mae Selling Guide |

| Freddie Mac CHOICERenovation | 620 | Freddie Mac Seller Guide |

| FHA 203(k) Standard | 580 with 3.5% down; 500–579 with 10% down (lender overlays often stricter) | HUD Handbook 4000.1 |

| VA One-Time Close | 620+ at most participating lenders (VA itself sets no minimum) | VA-approved lender programs reviewed May 2026 |

| SDHC ADU Finance Program (City of San Diego) | 680 | sdhc.org/housing-opportunities/adu/ |

The lender’s overlay almost always exceeds the GSE or HUD minimum. “We’ll do 620 FHA” often becomes “we want 660+ for a 203(k) Standard” in practice.

Debt-to-income

Most C2P programs cap DTI at 45% total monthly debt-to-income, though Fannie Mae’s Desktop Underwriter can approve some borrowers up to 50% with compensating factors. The DTI includes:

- The proposed permanent-loan principal, interest, taxes, and insurance.

- All other monthly debts (auto, student, credit cards, child support).

- Any second mortgage that will remain after closing.

Note that the construction-phase interest-only payment is not usually used in the DTI calculation — lenders qualify you based on the permanent payment, since that’s what you’ll carry after conversion.

Equity and down payment

Equity math for a C2P ADU loan is different from a regular mortgage because the lender underwrites against the as-completed appraised value, not today’s value:

| Item | Calculation |

|---|---|

| As-completed value | Subject-to-completion appraisal of property with the new ADU |

| Maximum loan amount | Up to 95% of as-completed value (conventional); up to 96.5% (FHA) |

| Existing first-mortgage balance | What you owe today |

| Construction budget | Hard costs + soft costs + contingency |

| Cash to close | Construction budget − (max loan − existing balance) |

Worked example

A $750,000 current home with a $400,000 existing first mortgage and a $250,000 ADU build planned:

- Lender’s appraiser issues a subject-to-completion appraisal at $1,050,000.

- At 90% LTV of as-completed value: $945,000 maximum loan.

- Subtract the $400,000 existing balance the C2P loan will pay off: $545,000 of available loan room.

- ADU build budget: $250,000. Cash to close: roughly $0–$15,000 (closing costs only).

Illustrative example, not a loan offer. Actual numbers depend on lender, appraisal, credit, LTV caps, and lien structure.

Property eligibility

Fannie Mae’s current B2-3-04 (for lenders not yet on UAD 3.6) permits one ADU on a one-unit primary residence, with the ADU construction method including site-built, factory-built, modular, or HUD-code manufactured homes legally classified as real property. If the ADU is a manufactured home, the primary dwelling must be site-built or modular, and the manufactured home must be on a permanent foundation with towing hitch, wheels, and axles removed.

For lenders using Fannie Mae’s UAD 3.6 policy, Selling Guide Announcement SEL-2025-10 (December 10, 2025) expands ADU eligibility effective March 31, 2026:

- One-unit properties: up to three ADUs (where local zoning permits).

- Two- to three-unit properties: ADUs permitted provided the total of primary units plus ADUs does not exceed four.

- Manufactured home as primary residence: one ADU permitted on single- or multi-section HUD-code manufactured homes classified as real property.

Ask any lender directly whether they’re on UAD 3.6 if a multi-ADU, manufactured-home, or two-to-three-unit configuration matters to your project. All lenders must use UAD 3.6 for new appraisal reports submitted to the Uniform Collateral Data Portal on or after November 2, 2026.

Contractor and contract requirements

Lenders almost always require:

- Licensed general contractor. State licensing verified (CSLB in California, CSL in Massachusetts, etc.).

- General liability and workers’ comp insurance with the lender named as additional insured.

- Fixed-price construction contract. Cost-plus contracts are typically rejected.

- Detailed scope of work, plans, specs, and itemized budget with a 5–15% contingency line.

- Lender-approved draw schedule tied to milestones.

- No owner-builder exemption at most lenders, even where state law allows it. A handful of credit unions and portfolio lenders make narrow exceptions.

Appraisal

The appraisal for a C2P ADU loan is a subject-to-completion appraisal — also called an “as-completed” appraisal. The appraiser values the property as if the ADU were already built, based on the approved plans and specs. If your loan uses projected ADU rental income for qualification, the appraiser also completes Form 1007 (Single-Family Comparable Rent Schedule).

A second, “final” inspection appraisal (Form 1004D) happens at completion to confirm the ADU was built to the approved plans before the loan converts to permanent. The biggest risk is the as-completed appraisal coming in below the build cost — most often when the appraiser can’t find ADU rental comparables in the local market.

What disqualifies your project

Four real-world disqualifiers stand out across agency rules and lender workflows:

- The lot fails local zoning, setbacks, owner-occupancy, fire-zone, or HOA rules at the as-completed configuration. Lenders won’t fund a build the city won’t permit.

- As-completed appraisal comes in below the loan amount. Especially common in markets with few comparable ADU sales.

- Income, employment, or credit changes between original closing and conversion exceed the 4-month or 18-month tolerance in Selling Guide B5-3.1-02.

- A mechanics lien is recorded against the property during construction — usually only an issue in two-time-close transactions.

See What You Can Build

Before you call any lender, run your address through the free Feasibility Engine. It checks setbacks, height limits, lot coverage, and fire-zone status — and tells you which financing lane is realistic for your project.

Get Your Free ADU Report (60 sec)How much does a construction to permanent loan for an ADU cost in 2026?

Construction-loan rates typically sit above 30-year fixed mortgage rates. According to AmeriSave’s 2026 construction-loan guide citing FHFA data, third-quarter 2025 averages were 8.34% on construction loans against 6.89% on 30-year fixed — a 1.45 percentage-point spread. For 2026, expect construction-phase rates running noticeably above the prevailing 30-year fixed and permanent-phase rates roughly in line with the conventional fixed-rate market, plus origination fees of about 1% of the loan amount, a subject-to-completion appraisal of $800–$1,200, draw inspection fees of $150–$400 per draw across 5–7 draws, title insurance of roughly 0.5–1% of loan amount, and interest-only payments on the drawn balance during construction. None of these figures is a loan offer; verify with a lender’s Loan Estimate.

Construction-phase rate vs. permanent-phase rate

In a single-close structure, both rates are set at the original closing.

- The construction-phase rate applies to the drawn balance during the build. It’s often slightly higher than the permanent rate and is sometimes floating (tied to the Wall Street Journal prime rate — 6.75% as of May 19, 2026).

- The permanent-phase rate is locked at original closing for the post-conversion amortizing mortgage. This protects the borrower against rate movement during construction.

In a two-close structure, only the construction-phase rate is set at closing; the permanent rate is set at the second closing. That’s a real risk if rates rise during the build.

Interest-only construction payments — modeled

For a $250,000 ADU C2P loan, assuming a 6-month build with a typical draw curve and an illustrative 8% construction-phase rate:

| Month | Cumulative drawn | Monthly interest payment |

|---|---|---|

| 1 | $25,000 (10%) | ~$167 |

| 2 | $62,500 (25%) | ~$417 |

| 3 | $112,500 (45%) | ~$750 |

| 4 | $162,500 (65%) | ~$1,083 |

| 5 | $212,500 (85%) | ~$1,417 |

| 6 | $250,000 (100%) | ~$1,667 |

After conversion, assuming a 7% permanent rate over 30 years, the $250,000 principal amortizes at roughly $1,663/month principal and interest. Illustrative only — not a loan offer.

Origination, appraisal, inspection, and draw-administration fees

For a typical $250,000 ADU C2P loan, expect roughly:

| Cost item | Typical range | Source / basis |

|---|---|---|

| Origination fee | ~1% of loan amount ($2,500 on $250K) | Industry lender disclosures reviewed May 2026 |

| Subject-to-completion appraisal | $800–$1,200 | Includes Form 1007 if rental income used; appraiser fee schedules reviewed May 2026 |

| Construction-phase interest | Pay-as-you-draw on drawn balance | Loan structure (CFPB construction-loan guidance) |

| Draw inspection fees | $150–$400 × 5–7 draws | Construction-lending administrator fee schedules |

| Title insurance | 0.5–1% of loan amount | Standard construction-loan title premium |

| Recording, processing, underwriting | $1,000–$2,500 | Standard lender fees |

| Final inspection (Form 1004D) | $250–$500 | Appraiser fee schedules |

| Interest reserve (some lenders) | Up to ~10% of construction costs | USDA Combination Construction-to-Permanent reference; some private lenders mirror this |

Illustrative cost stack from industry sources — not a loan offer. Verify exact fees with your Loan Estimate.

What this looks like compared to a HELOC

For context, Curinos national averages verified May 17, 2026:

- HELOC national average: 7.21%

- Home equity loan national average: 7.36%

- 30-year fixed mortgage (FHFA Q3 2025): 6.89%

- Construction loan (FHFA Q3 2025): 8.34%

- Wall Street Journal prime: 6.75%

The C2P structure costs more in interest during the build than a HELOC. But it lets you borrow against as-completed value, which a HELOC can’t. That tradeoff is the central decision of this guide.

What each agency allows: Fannie Mae, Freddie Mac, FHA, VA, USDA

Each agency handles construction-to-permanent loans for ADUs differently. Fannie Mae expressly supports C2P for new construction with an ADU and routes existing-property ADU additions to HomeStyle Renovation; SEL-2025-10 expands ADU eligibility effective March 31, 2026 for lenders using UAD 3.6 policy. Freddie Mac CHOICERenovation is the renovation-mortgage equivalent, with a limitation effective May 4, 2026 barring rental income from CHOICE-funded units. FHA permits ADU construction under Standard 203(k) per Mortgagee Letter 2023-17. VA One-Time Close construction loans are available through select VA-approved lenders, primarily for new home construction. USDA RHS published proposed rule RHS-26-SFH-0100 on March 31, 2026 to amend the Single Family Housing Guaranteed Loan Program to finance income-producing ADUs; comment period closes June 1, 2026.

Fannie Mae

Two governing references:

- Selling Guide B5-3.1-02 — Conversion of Construction-to-Permanent Financing: Single-Closing Transactions. Sets the framework for true single-close C2P.

- Fannie Mae ADU page at singlefamily.fanniemae.com — expressly states: “Borrowers building a new 1-unit property with an ADU can use a Construction-to-Permanent loan to finance both the home and ADU construction” and “Borrowers looking to purchase or refinance a 1-unit property and construct or install a new ADU can use a renovation loan to finance it.”

Key updates effective March 31, 2026 for lenders on UAD 3.6 (Selling Guide Announcement SEL-2025-10):

- Up to three ADUs on a 1-unit primary residence (where local zoning permits).

- ADUs on 2- to 3-unit primary residences, provided total units + ADUs do not exceed four.

- ADUs on single- or multi-section manufactured-home primary residences, classified as real property.

ADU rental-income qualification was authorized by Selling Guide Announcement SEL-2025-08 (effective October 8, 2025) and automated in Fannie Mae’s Desktop Underwriter (DU) version 12.1, released the weekend of March 21, 2026. Rental income from an ADU on a one-unit primary residence is calculated using the standard rental-income method and capped at 30% of total qualifying income.

Freddie Mac

Freddie Mac’s CHOICERenovation product is the closest equivalent to Fannie Mae HomeStyle Renovation. It permits purchase or refinance transactions with ADU construction or installation, underwrites against the as-completed appraised value, releases funds in draws, and converts to permanent financing in a single closing.

A 2026 limitation: for applications received on or after May 4, 2026, rental income from any unit included in the renovation project funded by CHOICERenovation mortgage proceeds cannot be used to qualify the borrower. Rental income from units not included in the funded renovation project may still be treated under Freddie Mac’s applicable rental-income rules. Confirm the current language on sf.freddiemac.com at application.

FHA — HUD Mortgagee Letter 2023-17

HUD Mortgagee Letter 2023-17, dated October 16, 2023, was the most consequential FHA ADU policy change in over a decade. Decoded into plain English:

- An ADU is eligible as part of new construction on a single-family property.

- Standard 203(k) eligible improvements expressly include converting a 1-family dwelling to a 1-family dwelling with an ADU, adding an ADU attached to the existing structure, and renovating an existing ADU (attached or unattached).

- For a one-unit property with rental history, lenders may use 75% of the lesser of fair market rent or lease as effective income.

- For a one-unit property without rental history (Standard 203(k) scenarios), lenders may use 50% of the lesser of fair market rent or lease.

- ADU rental income used as effective income is capped at 30% of the total monthly effective income.

- ADU rental income cannot be used as effective income for an FHA cash-out refinance — a hard exclusion in the mortgagee letter.

- Documentation: Form 1004 URAR, Form 1007 (Single Family Comparable Rent Schedule), and prospective leases when available.

ML 2023-17 doesn’t speak to a detached new-build ADU under 203(k); the eligible improvements list focuses on conversion, attached addition, and renovation of existing ADUs. Detached new-build ADU financing through 203(k) should be verified directly with the lender.

VA — One-Time Close construction

VA One-Time Close construction loans through specialty construction lenders allow up to 100% LTV for eligible veterans on new construction. Most VA OTC programs target new home construction, not adding an ADU to an existing primary residence — though some lenders will package an ADU as part of a new construction loan if the primary dwelling is also being built. For a VA-eligible veteran adding an ADU to an existing home, a VA cash-out refinance or a VA renovation loan is usually the better path.

USDA — proposed rule for income-producing ADUs

On March 31, 2026, the USDA Rural Housing Service published proposed rule RHS-26-SFH-0100 in the Federal Register, amending the Single Family Housing Guaranteed Loan Program to allow financing for single-family homes with one or multiple income-producing ADUs. Comment period closes June 1, 2026. As of this guide’s verification date, the rule is not yet final. If you’re in a USDA-eligible rural area considering an ADU, monitor regulations.gov for the final rule.

The single-page agency matrix

| Agency | Product name | ADU on existing primary | Multi-ADU eligibility | Rental income for qualifying |

|---|---|---|---|---|

| Fannie Mae | C2P (new construction); HomeStyle Renovation (existing) | Yes — HomeStyle is the cleaner path | Up to 3 ADUs on 1-unit; 1 ADU on 2–3 unit (UAD 3.6 only, eff. Mar 31, 2026); 1 ADU otherwise under B2-3-04 | Yes — 30% cap of qualifying income, automated in DU 12.1 (Mar 21, 2026) |

| Freddie Mac | CHOICERenovation | Yes | One ADU | Restricted — rental from CHOICE-funded unit barred on applications from May 4, 2026 |

| FHA | Standard 203(k); New Construction | Yes (conversion, attached addition, existing renovation) | One ADU | Yes — 75% with rental history, 50% without; 30% cap; not on cash-out refi |

| VA | One-Time Close | Limited — primarily new construction | One ADU as part of new build | Varies by lender |

| USDA RHS | Combination C2P (proposed ADU rule) | Pending — final rule not yet effective | Pending | Pending |

Find Your ADU Financing Path

Answer five questions about equity, your current mortgage, ADU type, credit, and rental plans. We return the financing lane to test first plus the disqualifiers that could block your build — and exactly which agency program fits your project.

Get Your Free ADU Report (60 sec)Who actually offers construction to permanent loans for ADUs in 2026?

True single-close construction-to-permanent loans for an ADU on an existing primary residence are most commonly issued by specialty construction-lending platforms, mortgage brokers with construction-lending capability, a few state and city housing finance agencies, and some credit unions and community banks. Most national retail banks and the largest mortgage call centers steer ADU borrowers toward HomeStyle Renovation, CHOICERenovation, or HELOC rather than a true single-close C2P.

The Dwelling Index lender-channel scan (May 2026)

For this guide, we reviewed public origination and product pages across the lender channels listed below. Inclusion criteria: lender publishes a construction-loan, construction-to-permanent loan, renovation mortgage, or HELOC product page that mentions ADUs or supports an ADU use case. We categorized each lender’s actual product offering — not just what it markets.

| Lender channel | Typical product for ADU | True single-close C2P for ADU on existing primary? | What they push instead |

|---|---|---|---|

| National retail bank (big-bank call center) | Conventional HomeStyle / HELOC | Rarely | HomeStyle Renovation, HELOC |

| Mortgage broker with construction specialty | Conventional, FHA OTC, VA OTC, single-close | Often yes | Depends on borrower file |

| Specialty construction-lending platform | FHA OTC, VA OTC, Conventional OTC, Jumbo | Often yes | Two-time close as fallback |

| Credit union (regional) | Renovation-construction; ARV HELOC | Sometimes | After-renovation value HELOC |

| Community bank (regional / portfolio) | Portfolio C2P with builder approval | Sometimes — strong for local builder networks | Bank’s standard HELOC or renovation product |

| State housing finance agency (SDHC, MassHousing) | Program-specific C2P | Yes (within geographic / income limits) | N/A |

| Digital-first national mortgage retailer | HomeReady / HomeStyle | Rarely | Renovation mortgage |

This is a directional scan, not an exhaustive list. Lender programs change; verify with the lender at the time you apply.

State and city public ADU construction-to-permanent programs

These are verified informational references, not affiliate offers.

San Diego Housing Commission (SDHC) ADU Finance Program

City of San Diego only. Construction-to-permanent loan up to $250,000, 1% fixed during construction, then converted to a 4% fixed permanent loan. Maximum 75% LTV. Seven-year affordability covenant with rents capped at the 80% AMI affordable level; the property owner cannot rent to a family member during the covenant. Minimum 680 credit score. $2,500 application fee at construction-loan closing. Owner-occupied detached single-family residence in the City of San Diego required. Income up to 150% of AMI. Verify exact terms directly with SDHC. sdhc.org/housing-opportunities/adu/ →

MassHousing ADU Loan Program

Massachusetts statewide. Announced January 14, 2026 and launched March 2026. Fixed-rate second-mortgage construction-to-permanent product up to $250,000 for detached ADUs and $150,000 for attached ADUs. 20-year amortization with additional zero-percent deferred-repayment funding stacked on top to lower the effective rate. Designs and permits must be in hand before application. masshousing.com →

Long Beach Backyard Builders Loan Program (Round 2)

City of Long Beach designated areas. Up to $250,000 at 2% interest with deferred payments up to 30 years to eligible lower-income homeowners. Applications expected Summer 2026; specific eligibility requirements being finalized. Short-term rentals not permitted on funded units. Verify at longbeach.gov.

Why your first call shouldn’t be a national bank’s call center

We’ve seen this pattern repeatedly: a homeowner calls a big national lender, asks for a “construction to permanent loan for ADU,” gets routed through three departments, and ends up with either (a) a HELOC pitch, (b) a HomeStyle Renovation referral, or (c) a flat “we don’t do that for ADUs, only new home construction” decline. The faster path is to identify the channel that actually issues the product for your situation — specialty construction lender, mortgage broker with construction capability, a state HFA program if you qualify, or a credit union with after-renovation-value lending — and start there.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Explore mortgage-based ADU financing options → MortgageResearch.com

MortgageResearch.com connects homeowners with mortgage-based financing resources and licensed loan officers. Use this after you’ve identified the channel that fits your situation. Approval, rates, and loan availability are not guaranteed and depend on lender, property, borrower, and state.

Can you keep your existing mortgage when financing an ADU?

Sometimes yes, sometimes no — and this is the question that determines whether C2P is worth pursuing. A single-close construction-to-permanent loan from Fannie Mae’s framework is structured as a purchase or limited cash-out refinance, which means it typically replaces your existing first mortgage with the new permanent loan. HomeStyle Renovation and CHOICERenovation work the same way. HELOCs and home equity loans sit behind your existing first mortgage in second lien position, preserving your current rate. If you have a sub-5% pandemic-era first mortgage, replacing it to finance an ADU is almost always a worse total-cost decision than carrying a second-lien product on top — even with the second’s higher rate.

The math, in plain English

Replacing a 3.5% first mortgage on a $400,000 balance with a 7% C2P loan costs you the interest-rate spread on the full $400,000 for the entire remaining life of the loan — that’s tens of thousands of dollars in extra interest, easily exceeding the cost of the ADU itself for many homeowners.

Carrying a 7.5% HELOC or home equity loan as a second lien against the same property, by contrast, only applies the higher rate to the new amount being borrowed for the ADU — not to your existing first-mortgage balance.

The breakeven moment for replacing the first mortgage is when your existing rate is at or above today’s market rate. If your current rate is meaningfully below market, protect it.

Compare HELOC paths before you replace your first mortgage →

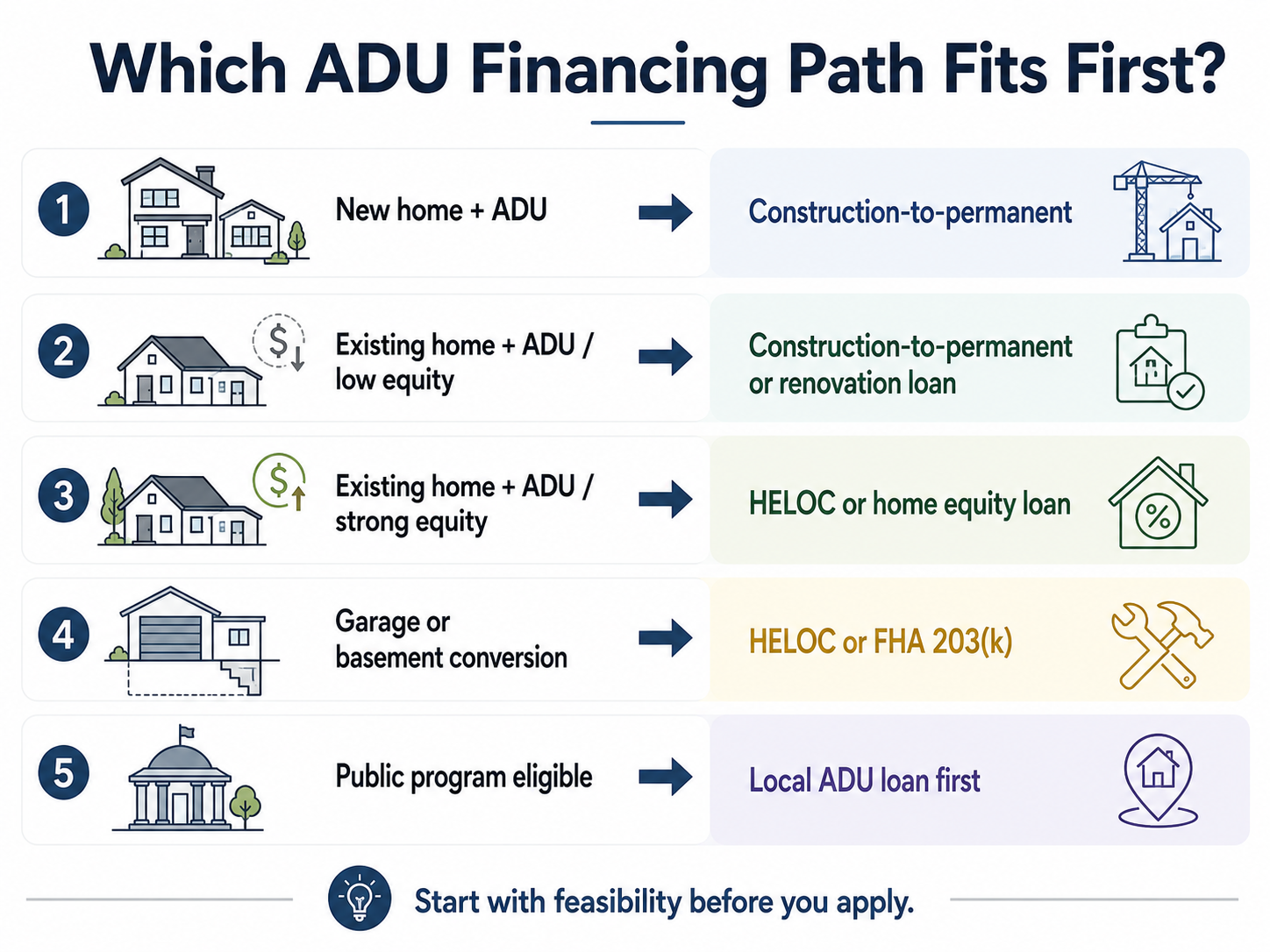

HELOC for ADU: Rates, Lenders, and When It Beats Construction Lending in 2026 →Construction to permanent loan vs. HELOC, renovation loan, and cash-out refinance for an ADU

A construction-to-permanent loan wins when you have limited current equity, a higher build budget, and your existing first-mortgage rate is at or above current market. A HELOC wins when you have strong equity and a low first-mortgage rate worth protecting. A HomeStyle Renovation, CHOICERenovation, or FHA 203(k) wins when you want single-closing renovation-mortgage mechanics for an existing-home ADU addition. A cash-out refinance wins only when your existing rate is already at or above current market and you want one consolidated loan. The right path depends on four variables: current equity, current first-mortgage rate, ADU budget size, and whether ADU rental income matters for qualifying.

The five-question financing fork

- Do I have enough usable current equity? Take your home’s current market value × 80%, subtract your existing first-mortgage balance. If that number covers your ADU budget, current-value products (HELOC, home equity loan) are on the table. If not, you need future-value products (C2P, HomeStyle, CHOICERenovation, 203(k)).

- Is my current first mortgage worth protecting? If you locked a rate below today’s market — common for anyone who refinanced or bought 2020–2022 — don’t replace it with a cash-out refi or a C2P that pays off your existing loan.

- Does the ADU budget exceed my current-equity borrowing room? If yes, you need a lender who will underwrite against as-completed value.

- Will ADU rental income help me qualify? Fannie Mae and FHA allow it under specific rules; Freddie Mac restricts it post-May 4, 2026 on CHOICE-funded units.

- Can I carry another monthly payment during the build? If not, look at construction loans with interest reserves (USDA Combination Construction-to-Permanent and some specialty C2P lenders fund up to ~10% interest reserve at closing).

The decision matrix

| Reader situation | Right first path | Why |

|---|---|---|

| Strong equity, sub-5% first mortgage, ADU < $200K | HELOC or home equity loan | Protects the favorable first mortgage; flexible draws |

| Strong equity, sub-5% first mortgage, ADU $200K+ | HELOC plus a renovation-loan alternative; compare both | Preserve first; add capacity |

| Low equity, current first mortgage ≥ market rate, ADU $200K+ | True single-close C2P or HomeStyle Renovation | As-completed value underwriting |

| Buying a home and adding an ADU at the same time | HomeStyle Renovation or 203(k) | Single transaction for purchase + improvement |

| Garage or interior conversion, < $100K | HELOC or 203(k) Limited | Renovation logic fits better |

| FHA borrower, low credit, low equity | FHA 203(k) Standard | 580 credit min, 96.5% LTV of as-completed |

| Building new home plus ADU together | True single-close C2P | Cleanest C2P use case |

| Eligible for SDHC / MassHousing / Long Beach program | Public program first | Below-market terms with restrictions |

For the full path comparison, see How to Finance an ADU in 2026: 7 Paths Compared →

A realistic timeline: month by month with a construction to permanent loan for an ADU

From initial feasibility check to the first permanent mortgage payment, the realistic timeline for a construction-to-permanent ADU loan runs 10–14 months for a detached ground-up build. The table below shows the eight phases, typical calendar range, and the most common risk event at each stage.

| Phase | Typical calendar | Key milestone | Risk callout |

|---|---|---|---|

| 1. Feasibility & lot check | Months −3 to −2 | Confirm ADU type, zoning, setbacks, HOA, fire zone | Project not permittable at desired size |

| 2. Plans, permits, contractor | Months −3 to −1 | Stamped plans, permit application filed, lender builder approval initiated | Permit review extends 4–12 weeks; builder approval adds 1–3 weeks |

| 3. Loan application & docs | Month 1 | Loan application, income/asset docs submitted, appraisal ordered | Incomplete package delays underwriting 2–4 weeks |

| 4. Underwriting & appraisal | Months 1–2 | Subject-to-completion appraisal (Form 1004 + 1007); lender conditional approval | As-completed appraisal below build cost; requires scope reduction or more cash |

| 5. Closing | Month 2 | Loan closes; lien recorded in first position; existing mortgage paid off | Rate-lock expiration if underwriting runs long |

| 6. Construction & draws | Months 3–10 | 5–7 milestone draws; interest-only payments on drawn balance | Builder delays, change orders, draw-inspection lag, budget overruns |

| 7. Final inspection & CO | Month 11 | Lender Form 1004D; city certificate of occupancy issued | ADU deviates from approved plans; punch-list delays conversion |

| 8. Permanent conversion | Month 12 | Loan converts to fully amortizing 15/30-year mortgage | Income, employment, or credit change outside 4/18-month window (Selling Guide B5-3.1-02) |

What documents do lenders need for a construction to permanent ADU loan?

Assemble this packet before you apply. Incomplete applications are the most common cause of underwriting delays on construction loans.

| Packet item | Why it matters |

|---|---|

| ADU type (detached, attached, conversion, prefab, modular, manufactured) | Determines product fit and agency eligibility |

| Property address and jurisdiction | Determines zoning, permit, and local program eligibility |

| Current mortgage statement, payoff, and rate | Determines whether replacing the first mortgage is sensible |

| Current home appraisal or recent market estimate | Sets the baseline for as-completed math |

| Project budget with contingency line (5–15%) | Determines loan size and risk |

| Stamped architectural plans | Lender’s appraiser needs them for as-completed value |

| Building permit status (issued, in review, ready to submit) | Lender may require permits before closing |

| Fixed-price construction contract | Lender review of price and scope |

| Detailed scope of work | Tied to draw schedule |

| Builder license and proof of insurance | Lender approval gate |

| Lender-approved draw schedule | How funds release tied to milestones |

| Rental income plan (if used to qualify) | Affects DU/AUS treatment under SEL-2025-08 and HUD ML 2023-17 |

| Exit / permanent financing plan | Critical for two-close transactions |

ADU Construction Loan Document Checklist

The exact list of documents your lender will request — fixed-price contract, stamped plans, permit checklist, contractor licensing checks, draw-schedule template — plus a one-page summary of which agency program fits which ADU type. Free, no spam.

Download the ADU Starter Kit →What questions should you ask lenders before applying?

Don’t start with rate. Start with whether the lender finances your exact ADU type, property status, draw structure, permit status, contractor model, and permanent conversion plan. Then compare written answers. Two lenders quoting the same “construction-to-permanent loan” can deliver radically different experiences for an ADU.

| Question | Why it matters |

|---|---|

| Do you finance ADUs on existing single-family homes, or only new construction with an ADU? | Filters out the lenders who’ll say no after wasting your week |

| Do you finance detached, attached, conversion, modular, prefab, and manufactured ADUs? | ADU type drives eligibility |

| Is this single-close or two-time close? | Determines re-qualification and rate risk |

| Are you currently using Fannie Mae UAD 3.6 policy for ADU eligibility? | Decides whether the expanded multi-ADU and manufactured-home rules apply to your loan |

| Do you underwrite against current value or as-completed value? | Critical for low-equity borrowers |

| What are your max LTV/CLTV limits on the as-completed value? | Determines cash needed |

| Do I need permits issued before closing, or do you allow conditional approval? | Determines timing |

| What builder approval do you require, and what’s the typical turnaround? | Prevents contractor surprises |

| How many draws is typical, and who orders the inspections? | Affects cash flow and timeline |

| Who receives draw funds — builder, escrow, or borrower? | Prevents payment confusion |

| Can projected ADU rental income help me qualify, and what percentage will you use? | Underwriting depends on product (DU 12.1, FHA ML 2023-17, CHOICE rules) |

| What happens if construction runs over time or budget? | Reveals the real risk profile |

Ask these in writing. Loan officers use these terms loosely, and a written response is the only way to compare apples to apples.

Can ADU rental income help you qualify?

Yes, under specific rules — and the rules differ by product. Fannie Mae’s Desktop Underwriter 12.1 (released the weekend of March 21, 2026) automates ADU rental-income qualification for one-unit primary residences on eligible transactions, capped at 30% of total qualifying income. HUD Mortgagee Letter 2023-17 allows FHA borrowers to use 75% of fair market rent with rental history, 50% on Standard 203(k) scenarios without rental history, capped at 30% of total monthly effective income — and excludes ADU rental income entirely on FHA cash-out refinances. Freddie Mac CHOICERenovation restricts rental income from any unit included in the renovation project funded by the mortgage proceeds on applications received on or after May 4, 2026.

Rental income at a glance

| Product | Can ADU rent help qualify? | Calculation | Cap |

|---|---|---|---|

| Fannie Mae C2P / HomeStyle (DU 12.1) | Yes | Standard rental-income method (75% of fair market rent or lease) | 30% of total qualifying income |

| Freddie Mac CHOICERenovation | Restricted for applications from May 4, 2026 — rent from any unit included in the funded renovation excluded | N/A on excluded units | N/A on excluded units |

| FHA Standard 203(k) with rental history | Yes | 75% of lesser of fair market rent or lease | 30% of total monthly effective income |

| FHA Standard 203(k) without rental history | Yes | 50% of lesser of fair market rent or lease | 30% of total monthly effective income |

| FHA cash-out refinance | No | Excluded entirely | N/A |

| VA OTC | Varies by lender | Lender-specific | Lender-specific |

These are illustrative, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, lease execution, vacancy, and regulatory approvals.

What happens if the as-completed appraisal comes in low?

A low appraisal is one of the most common ADU construction-to-permanent failures. If the appraiser values the as-completed property below your build cost, the lender reduces the maximum loan amount in proportion to its LTV cap. You then face three options: bring more cash to close, reduce the construction scope, or restructure the financing. Low appraisals happen most often in markets with few comparable ADU rental or sale data points.

Practical mitigations before the appraisal:

- Provide the appraiser with comparable ADU sales you’ve identified (especially recent permits in the same zip code).

- Include a Form 1007 Single-Family Comparable Rent Schedule with realistic rental comps if rental income matters.

- Use a pre-approved or pre-permitted plan where the city has already approved the design — it signals lower risk to the appraiser.

- Ask your lender whether they allow a desk review or second appraisal if the first comes in low.

Which public ADU construction loan programs are open in 2026?

A handful of city and state housing finance agencies offer ADU-specific construction-to-permanent loans with below-market terms. As of May 2026, the most established programs are the San Diego Housing Commission ADU Finance Program (City of San Diego, up to $250,000), the MassHousing ADU Loan Program (Massachusetts statewide, up to $250,000 detached or $150,000 attached), and the City of Long Beach Backyard Builders Loan Program (Long Beach, up to $250,000, second round opening Summer 2026). All carry eligibility restrictions on income, geography, owner-occupancy, rent affordability, and program funding status.

| Program | Geography | Amount | Construction rate | Permanent rate | Key restrictions |

|---|---|---|---|---|---|

| SDHC ADU Finance Program | City of San Diego | Up to $250,000 | 1% fixed | 4% fixed (confirm term with SDHC) | Owner-occupied SFR, 680+ credit, 75% LTV, income to 150% AMI, 7-year affordability covenant at 80% AMI rents, no family rental, $2,500 application fee |

| MassHousing ADU Loan | Massachusetts statewide | $250,000 detached / $150,000 attached | Fixed-rate, second-mortgage C2P | 20-year amortization + zero-percent deferred component | Designs and permits in hand before application; income limits apply |

| Long Beach Backyard Builders (Round 2) | City of Long Beach designated areas | Up to $250,000 | 2% | Deferred up to 30 years | Lower-income eligibility; applications open Summer 2026; no short-term rentals |

Verify the official program page before assuming availability — program funding status changes.

Edge cases: owner-occupancy, HOA, lot size, utility hookups, multi-ADU, manufactured homes

Even when a construction-to-permanent loan is the right product on paper, edge cases derail real builds. The most common: owner-occupancy requirements (California prohibits local ADU owner-occupancy requirements under Government Code § 66315; other states differ), HOA architectural review, lot-size minimums (preempted by state law in some states; verify your state’s statute), utility hookup costs (often $5K–$50K and frequently buried in change orders), lender-specific rental-income overlays, multi-ADU eligibility (Fannie Mae’s expansion to 3 ADUs is UAD 3.6-specific effective March 31, 2026), and manufactured-home ADUs.

Owner-occupancy

Many public ADU programs (SDHC, MassHousing) require the homeowner to live in the primary residence or the ADU after construction. In California, Government Code § 66315 prohibits local agencies from imposing owner-occupancy requirements on ADUs — a rule made permanent by AB 976. Junior ADU (JADU) rules are different, and AB 1154 (effective October 10, 2025) narrowed JADU owner-occupancy treatment. Owner-occupancy treatment in other states varies; verify your state’s statute and local ordinance.

HOA architectural review

Even if your city allows the ADU by right, your HOA may have architectural review authority that delays or modifies the project. In California, HCD has issued guidance that third-party reviews by HOAs in the ADU approval process can violate state ADU law (Gov. Code § 66315) — but covenants can still impose design or color rules. Verify HOA standing before paying for plans.

Lot size and setbacks

State ADU laws in California (Government Code Chapter 13), Oregon, Washington, and Massachusetts override many local lot-size minimums for ADUs in specified circumstances. But local setback rules, building-code height limits, fire-zone restrictions, lot coverage maximums, and floor-area ratios (FAR) still bind. Verify your state’s statute and your specific city’s ordinance before assuming a lot is buildable.

Utility hookups

Utility lateral hookups — the connection from the public main to your ADU’s electrical, water, sewer, and gas — are one of the most underestimated costs in ADU budgets. A separate electrical meter can run $5K–$15K. A sewer lateral extension can run $10K–$30K. Lender-approved construction budgets should include a line item for utility upgrades, and many lenders require a utility-feasibility letter before closing.

Multi-ADU eligibility

Fannie Mae’s expansion to up to three ADUs on a 1-unit primary residence applies to lenders using UAD 3.6 policy, effective March 31, 2026. Outside UAD 3.6, B2-3-04 still permits one ADU per primary parcel. If you’re considering a multi-ADU configuration, ask your lender directly which Fannie Mae policy supplement applies to your loan.

Manufactured-home ADUs

Under current B2-3-04, HUD-code manufactured-home ADUs can be eligible if the ADU is legally classified as real property and the primary dwelling is site-built or modular. SEL-2025-10’s expansion (UAD 3.6 only, effective March 31, 2026) extends eligibility to manufactured-home primary residences with one ADU. The manufactured home must be on a permanent foundation with towing hitch, wheels, and axles removed. Few lenders are set up to underwrite this configuration today; expect to shop several.

Frequently asked questions

Is a construction-to-permanent loan the same as a construction loan?

No. A construction loan funds the build phase only and must be paid off with a separate refinance or cash. A construction-to-permanent loan transitions from construction financing into long-term mortgage financing after completion — automatically in single-close versions, or via a second closing in two-time-close versions.

Can I use a construction-to-permanent loan to build a detached ADU on my existing home?

Yes, technically — but for an existing home, Fannie Mae routes this case to HomeStyle Renovation rather than the construction-to-permanent label. Freddie Mac uses CHOICERenovation. FHA uses Standard 203(k). All three function similarly to single-close C2P: one loan, one closing, draws tied to milestones, underwrites against as-completed value. Some specialty construction lenders, credit unions, and state HFA programs do offer true single-close C2P for an ADU on an existing primary residence.

What credit score do I need for a construction-to-permanent ADU loan?

Conventional construction-to-permanent typically requires 680+. Fannie Mae HomeStyle Renovation accepts 620. Freddie Mac CHOICERenovation accepts 620. FHA 203(k) Standard accepts 580 with 3.5% down. SDHC ADU Finance Program requires 680. Lender overlays often exceed the program minimum.

How much down payment do I need?

In a true C2P loan that underwrites against as-completed value, the cash you bring to close covers what the maximum loan amount (LTV cap) doesn't. Conventional caps at 95% of as-completed value; FHA at 96.5%; HomeStyle and HomeReady reach 97%. For a typical $200K–$250K ADU build, expect $5K–$15K in closing costs out of pocket, sometimes more if the appraisal comes in below build cost.

Will I make payments during the construction phase?

Yes. You pay interest only on the drawn balance — not on the full loan amount. Early draws produce small monthly interest payments; payments rise as the draw schedule progresses. Some lenders fund an interest reserve at closing (up to roughly 10% of construction costs) that covers construction-phase interest, eliminating out-of-pocket monthly payments during the build.

Does Fannie Mae allow construction-to-permanent loans for ADUs?

Yes. Fannie Mae expressly supports construction-to-permanent financing for borrowers building a new one-unit property with an ADU. For existing properties adding an ADU, Fannie Mae routes the borrower to HomeStyle Renovation. Both products are eligible under the Selling Guide, with single-closing transactions governed by B5-3.1-02.

Can I use FHA 203(k) to add or renovate an ADU?

Yes, for the ADU improvements HUD Mortgagee Letter 2023-17 lists: converting a one-family structure to a one-family structure with an ADU, adding an ADU attached to an existing structure, and renovating an existing attached or unattached ADU. HUD also separately lists one-unit properties with ADUs as eligible property types for FHA new construction financing.

Can I use a VA construction loan to build an ADU?

Limited. VA One-Time Close construction loans are primarily for new home construction. Adding an ADU to an existing primary residence is usually better served by a VA cash-out refinance or a VA renovation loan than a VA OTC construction loan.

Can I use proposed ADU rental income to qualify for the loan?

Yes, under specific rules. Fannie Mae's Desktop Underwriter 12.1 (released the weekend of March 21, 2026) automates ADU rental-income qualification for one-unit primary residences on eligible transactions, capped at 30% of total qualifying income. FHA Mortgagee Letter 2023-17 allows 75% with rental history or 50% on Standard 203(k) without rental history, capped at 30% of total monthly effective income. FHA cash-out refinances cannot use ADU rental income. Freddie Mac CHOICERenovation restricts rental income from any unit included in the funded renovation project on applications received on or after May 4, 2026.

Does the loan require a second appraisal at conversion?

In a true single-close construction-to-permanent loan, no — the original subject-to-completion appraisal supports both phases. A Form 1004D final-inspection appraisal confirms the ADU was built to approved plans before conversion, but it's not a full re-appraisal. In a two-time close transaction, a new appraisal may be required for the second closing.

What is an intervening lien and how do I avoid one?

An intervening lien is a lien — typically a mechanics lien from an unpaid subcontractor — recorded against the property between the construction-loan closing and the permanent-loan closing in a two-time close transaction. The intervening lien must be paid off or subordinated before the new permanent loan can record in first lien position. Single-close construction-to-permanent loans eliminate this risk because the loan is already in first lien position from original closing.

What's the interest rate on a construction-to-permanent loan in 2026?

According to AmeriSave's 2026 construction-loan guide citing FHFA data, third-quarter 2025 national averages were 8.34% on construction loans against 6.89% on 30-year fixed mortgages — a 1.45 percentage-point spread. For 2026, expect construction-phase rates above the prevailing 30-year fixed and permanent-phase rates roughly in line with the conventional fixed-rate market. Rates vary by lender, credit, LTV, and lien position; none of these figures is a loan offer.

Who actually offers construction-to-permanent loans for ADUs?

True single-close construction-to-permanent loans for ADUs on existing primary residences are most commonly offered by specialty construction-lending platforms, mortgage brokers with construction-lending capability, some credit unions and community banks, and a small number of state and city housing finance agency programs (SDHC, MassHousing, Long Beach). Most national retail banks and the largest mortgage call centers steer ADU borrowers toward HomeStyle Renovation, CHOICERenovation, or HELOC instead.

Are prefab and modular ADUs eligible?

Modular ADUs (built to International Residential Code, factory-assembled, placed on a permanent foundation) are generally eligible — Fannie Mae treats them the same as site-built for ADU purposes. HUD-code manufactured-home ADUs are eligible under Fannie Mae's current B2-3-04 when classified as real property and the primary dwelling is site-built or modular, and under SEL-2025-10's expanded rules effective March 31, 2026 for lenders on UAD 3.6 policy. Lender overlays vary substantially; ask in writing.

Methodology

This guide was researched by reviewing official federal agency sources (Fannie Mae Selling Guide, Freddie Mac Seller Guide, HUD mortgagee letters, USDA Federal Register filings, CFPB guidance), state and city housing finance agency program pages, FHFA construction-loan data via secondary lender publications, Curinos rate benchmarks, and lender-channel examples from specialty construction-lending platforms, mortgage brokers, credit unions, and community banks. Homeowner forums and discussion threads were used to identify voice-of-customer language and decision friction — not as proof of law, lending terms, zoning, or costs.

Recommendations are framed as editorial conclusions grounded in documented program rules. The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We do not originate loans, broker financing, or build ADUs. We do not rank lenders by compensation or sort comparison tables by affiliate payout. When we link to an affiliate partner, we disclose it in plain language at the point of the link. Read our full methodology →

This guide is for educational purposes only. It is not a loan commitment, rate quote, legal advice, tax advice, or approval guarantee. Loan availability, terms, rates, payments, underwriting, rental-income treatment, and program eligibility vary by lender, property, borrower, jurisdiction, and date. Verify all program details with the official source and your lender before acting.

Related guides

Not sure where to start?

See what’s possible at your address — confirm your lot, financing lane, and ADU type in 60 seconds.

Get Your Free ADU Report in 60 Seconds →