Renovation HELOC for ADU (2026): How After-Renovation-Value Lending Works, Who Offers It, and When It’s the Wrong Tool

By The Dwelling Index Editorial Team · · Last verified May 19, 2026 · 28 min read

Independent ADU resource · Not a lender or broker · Editorial standards →

The 60-second answer

A renovation HELOC for ADU construction — also called an ARV HELOC or after-renovation-value HELOC — is a second-position home equity line of credit underwritten against your home’s projected post-construction value instead of its current value. For a homeowner whose standard HELOC won’t cover their ADU budget, that one change in math can multiply borrowing power. RenoFi advertises an average of 11× more borrowing power than a standard home equity loan; the worked scenarios on this page show roughly 3× to 11×, depending on how much value the completed ADU adds to your home.

The catch: it’s offered by a small group of credit unions and renovation-finance platforms, underwriting takes roughly twice as long as a standard HELOC, and product availability is uneven by state.

- Use it when: you have limited current equity, a high-value ADU project, and a first mortgage you don’t want to lose.

- Skip it when: a standard HELOC already covers your budget — or your project is small enough that the extra paperwork and fees aren’t worth it.

- Verify before you commit: product availability by lender in your state, current rate, and the as-completed appraisal outcome.

| Your situation | First lane to test | Why |

|---|---|---|

| Recent buyer, low current equity | Renovation HELOC | ARV math, keeps your first mortgage |

| Ample current equity, low first-mortgage rate | Standard HELOC | Simpler, faster, fewer fees → Standard HELOC guide → |

| Ground-up detached ADU, willing to refinance | Construction-to-permanent loan | One loan that converts to a fixed permanent mortgage |

| Buying + building combined; want one fixed-rate first lien | Fannie HomeStyle or Freddie CHOICERenovation | ARV underwriting in a single first-lien renovation mortgage |

| FHA-eligible borrower converting or adding attached ADU | FHA 203(k) Standard | Per HUD ML 2023-17 |

| First-mortgage rate ≥ 6% and ample current equity | Cash-out refinance | May consolidate if new terms beat blended cost |

| Standard HELOC won’t cover and renovation HELOC unavailable in your state | HomeStyle, CHOICERenovation, or construction-to-perm | All use as-completed value, replace first mortgage |

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

See What You Can Build

Check your lot, zoning, and likely financing lane in about 60 seconds.

Get Your Free ADU Report (60 sec)

What this guide is — and what it isn’t

This is a single-product deep-dive on the renovation HELOC, written for the homeowner who has already discovered that a regular HELOC won’t fund their ADU and wants to know whether after-renovation-value lending can close the gap.

If you’re earlier in the journey, our How to Finance an ADU in 2026: 7 Paths Compared → is the better starting point. If you have enough current equity for a standard HELOC, see Best HELOC for ADU: Decision Guide →

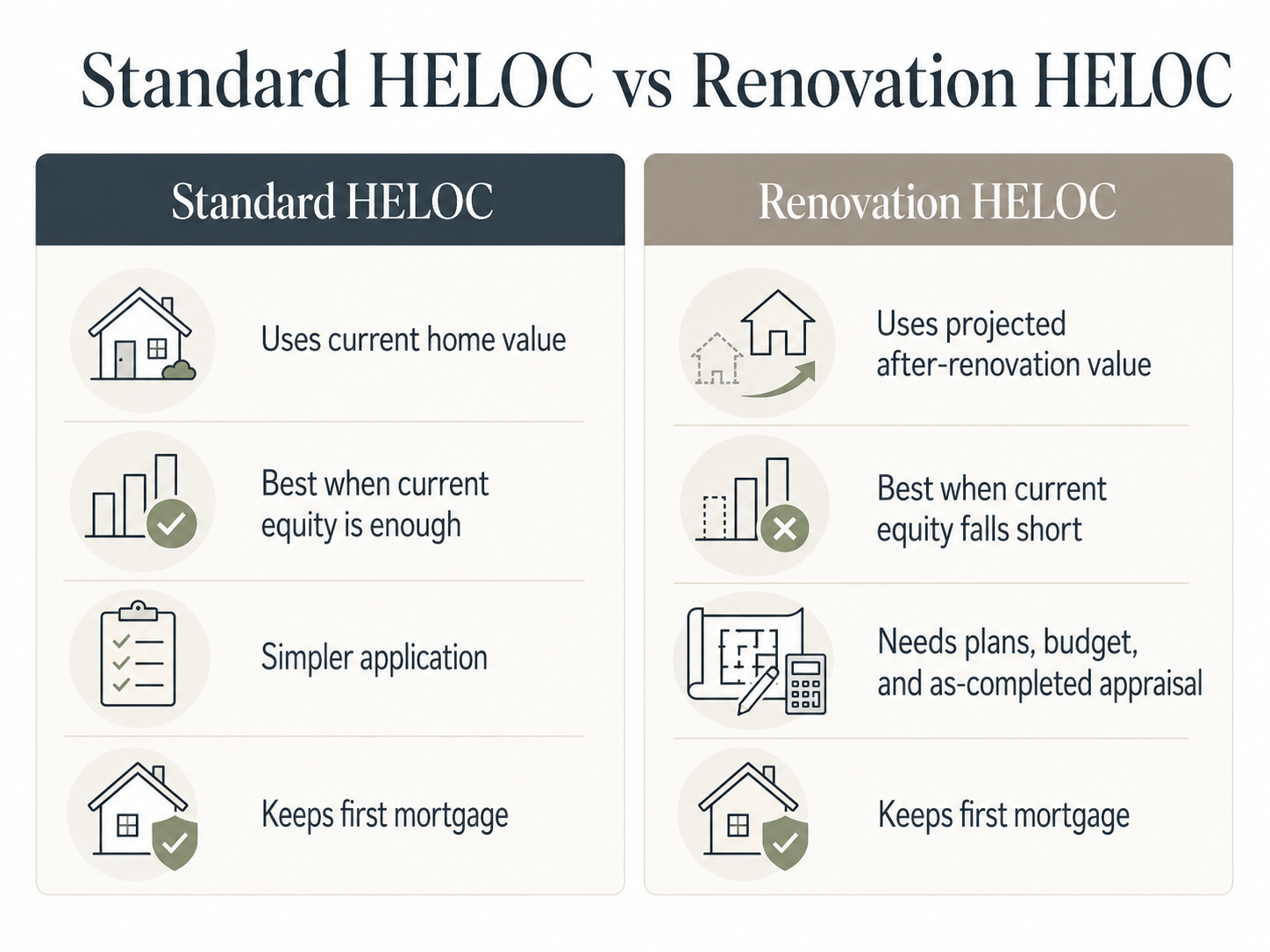

1. What is a renovation HELOC for an ADU?

A regular HELOC asks one question: how much is your home worth today, and how much can we lend against that? A renovation HELOC asks a different question: how much will your home be worth after the ADU is finished, and how much can we lend against that future value?

The math change is dramatic for recent homebuyers. In April 2024, the Urban Institute identified the gap between what standard HELOCs offer and what ADUs cost as one of the biggest structural barriers to ADU construction in the United States. The renovation HELOC was built specifically to close that gap.

“Renovation HELOC,” “ARV HELOC,” and “After-Renovation-Value HELOC” are the same category

Different lenders brand the product differently. RenoFi calls it a Renovation HELOC. Quorum FCU calls it a Renovation HELOC. Tower FCU calls it the Dreamline Renovation HELOC. Patelco calls it the ADU HELOC. The category logic is the same — borrow against future value, keep first mortgage intact — but lender-specific products differ in lien structure, draw rules, fees, state availability, and underwriting. Treat them as variations on a theme, not as one identical instrument.

The four-actor structure most platform-mediated renovation HELOCs use

Many renovation HELOCs — especially those powered by a tech platform like RenoFi — involve four parties. Knowing the structure upfront saves a lot of confusion later:

- You, the borrower — homeowner with a defined ADU project.

- The underwriting platform or broker (often RenoFi). RenoFi is not a lender. The company itself is explicit about this in its NMLS disclosures.

- The actual lender — a credit union such as Quorum Federal Credit Union, USALLIANCE Financial, Ardent Credit Union, Chartway Credit Union, or First Community Credit Union, all named as RenoFi partner credit unions in RenoFi’s March 3, 2026 announcement.

- The construction management vendor — a third party that releases construction draws to your contractor and confirms project milestones. This is the source of the monthly admin fee at some lenders.

When someone says, “I got a renovation HELOC from RenoFi,” what they actually got is a HELOC from one of RenoFi’s partner credit unions, packaged through RenoFi’s underwriting platform.

Sources: Urban Institute, “To Increase the Housing Supply, Focus on ADU Financing” (April 2024); RenoFi NMLS disclosure on renofi.com; RenoFi Series B announcement, PRNewswire (March 3, 2026).

2. How is a renovation HELOC different from a standard HELOC?

| Feature | Standard HELOC | Renovation HELOC |

|---|---|---|

| Value used to set credit line | Current appraised value | After-renovation value (ARV), via “as-completed” appraisal |

| Typical max CLTV | 80–85% of current value | 90% of ARV (some lenders 95%; some allow 125–150% of current value inside the ARV cap) |

| Refinances first mortgage? | No | No |

| Time to close | 2–3 weeks typical | 4–8 weeks typical |

| Construction-management fee during build? | No | Yes at most lenders — typically $50–$100/month |

| Rate type | Variable, prime + margin | Variable, prime + margin (some fixed-rate lock options) |

| Documents required at application | Income, mortgage statement, AVM or full appraisal | Income, mortgage statement, full as-completed appraisal, contractor info, itemized cost estimate, plans, signed contract |

| Available in all 50 states? | Yes, depending on lender | No — state exclusions apply |

Both products are variable-rate because both are tied to the prime rate, which moves with the Federal Reserve’s federal funds rate. Per Federal Reserve H.15 data released May 15, 2026, the bank prime loan rate is 6.75% and the federal funds effective rate is 3.63% (target range 3.50%–3.75% per the Fed’s April 29, 2026 FOMC statement). That’s the index your renovation HELOC margin gets added to. The shorthand: the value of a renovation HELOC is borrowing power, not rate.

Sources: Federal Reserve H.15 (May 15, 2026); Federal Reserve FOMC statement (April 29, 2026); RenoFi, Quorum FCU, Tower FCU, Patelco product pages (verified May 19, 2026).

3. What is after-renovation value — and what makes the appraisal come in too low?

The formula every renovation HELOC borrower needs to understand

ARV = current appraised value + estimated added value of the completed ADU

The trap: “added value” is not the same as “construction cost.” The 2025 Cost vs. Value Report (Journal of Light Construction / Zonda) lists the ADU project at $166,406 average job cost and $68,656 resale value — about 41% cost recouped at resale on a national average basis. Local recovery rates vary — high-demand California markets often outperform the national average; rural and lower-density markets may underperform.

Why the as-completed appraisal might come in too low

This is the section most renovation HELOC pages skip. Five things drive ARV down — sometimes invisibly until the appraisal lands:

- Lack of permitted-ADU comps within ~1 mile. Appraisers need recent sales to support the value uplift. In markets where ADUs are uncommon, there’s no comp evidence and the appraiser will be conservative.

- The neighborhood ceiling. Your ARV is capped by what comparable homes in your neighborhood actually sell for. Building a $400K ADU in a neighborhood where homes top out at $700K will not produce a $1.1M appraisal.

- The appraiser values rent differently than you do. Even in markets with strong rental demand, the appraiser uses sale comps as the primary anchor, not the gross-rent multiplier you might calculate in a spreadsheet.

- Unpermitted or illegal ADUs in the area. If recent ADU sales in your area were unpermitted, they may not count as comps.

- Over-building for the neighborhood. A high-finish, large detached ADU on a lot in a modest neighborhood produces diminishing returns.

A worked ARV example — San Diego homeowner

| Starting home value | $600,000 |

| Comparable homes with permitted ADUs (~1 mile, last 12 months) | Selling for ~$760,000 |

| ADU build budget | $280,000 |

| As-completed appraisal | $760,000 — capped at the comp ceiling, not cost-plus |

| Maximum renovation HELOC (90% ARV − $250K first mortgage) | $434,000 available |

Notice the appraised value is lower than current value + cost ($600K + $280K = $880K). That’s the neighborhood-ceiling effect. The borrower still has plenty of borrowing room — but the math doesn’t work the way most first-time applicants assume.

Build your own ARV comp worksheet before you apply

| Field | What to enter |

|---|---|

| Current home value | From recent sales of your home type within ~1 mile |

| ADU budget | All-in, with 15% contingency |

| Comparable sale 1 | Address, sale date, sale price, ADU size, distance |

| Comparable sale 2 | Same fields |

| Comparable sale 3 | Same fields |

| Average comp sale price | The number your appraisal will likely cluster around |

| Adjustments | Lot size, ADU size delta, finish-level delta, location quality |

| Resulting estimated ARV | Cluster around comp average, then adjust |

If you can’t find three permitted-ADU comps within a mile, that’s your signal: the appraisal will likely come in conservative. Plan around that, or talk to a local appraiser before committing to a lender that requires a non-refundable appraisal fee.

Sources: JLC/Zonda 2025 Cost vs. Value Report; RenoFi ARV explainer (verified May 19, 2026); IRS Publication 936.

4. Who offers a renovation HELOC for ADU construction in 2026?

2026 Renovation HELOC Lender Comparison Matrix

| Feature | RenoFi (via partner CUs) | Quorum FCU | Tower FCU Dreamline | Patelco ADU HELOC |

|---|---|---|---|---|

| Max loan amount | Up to $750,000 | Driven by ARV math + Quorum CLTV | $50,000–$350,000 (up-to-80% LTV tier; 80.01–90% tier capped at $250K) | $10,000–$400,000 |

| Max % of ARV | Up to 90% (some partners 95%) | Up to 95% LTV combined with ARV | 90% of ARV | 90% of post-construction value |

| Max % of current value | Up to 125% (some up to 150%) | — | — | 125% of current value |

| Verified APR | Variable, prime + margin (set by partner CU) | As low as 6.625%; floor 4.95%; max 18% (verified Dec. 11, 2025) | Variable, prime + margin; max 18% (verified May 19, 2026) | 8.25%–9.00% APR (verified May 18, 2026) |

| Draw / repayment | Typically 10-yr draw + 15–20 yr repay | 10-yr draw + 20-yr repay | 15-yr interest-only draw + 15-yr repay; construction sub-period up to 12 months ($500/mo extension to 18 months) | 2-yr interest-only draw + 20-yr repay |

| Construction-period fees | Some partner lenders charge monthly management fees | — | $300 processing + CM vendor origination; closing costs $500–$5,500 for loans up to $250K | $250 lender fee + $50/mo (lines ≤$100K) or $100/mo (>$100K) |

| State footprint | 48 states per RenoFi; Bankrate (Feb. 27, 2026): HI, NY, MA unavailable | Not available in Texas per Quorum’s product disclosure | MD, VA, DC, DE, PA, NC, SC, FL only | California only — primary residences only |

| Minimum credit score | Most partner lenders ~640+ | 640+ typical | Standard FCU HELOC underwriting | Standard FCU HELOC underwriting |

| First-mortgage refinance required? | No (second lien) | No | No | No |

| Counts projected ADU rental income? | Lender-dependent | Lender-dependent | Lender-dependent | Yes — Patelco explicitly states this |

Verified May 19, 2026. Every cell sourced from the lender’s own product page or an independent third-party review. Cells marked — are where the lender does not publicly disclose the data point.

Lender profiles

RenoFi

The broker / underwriting platform with the largest renovation HELOC footprint. RenoFi is not a lender — its proprietary Renovation Underwriting platform powers loans originated by partner credit unions. Per RenoFi’s March 3, 2026 PRNewswire announcement, the platform has facilitated more than 8,000 renovation loans totaling over $1.5 billion funded. RenoFi states it’s licensed in 48 states; Bankrate’s February 27, 2026 review lists Hawaii, New York, and Massachusetts as unavailable.

Quorum Federal Credit Union

RenoFi’s most-visible partner credit union. APR as low as 6.625% (verified December 11, 2025), floor rate 4.95%, maximum APR 18%. Quorum says loan underwriting is typically 1–2 days after a complete application package — but the overall timeline still depends on appraisal and project documentation. Membership open to anyone joining the American Consumer Council (free). Not available in Texas per Quorum’s product disclosure.

Tower Federal Credit Union — Dreamline

Available on primary and second homes in MD, VA, DC, DE, PA, NC, SC, and FL only. Loan limits $50,000–$350,000. Draw period: 15 years interest-only followed by 15 years fully-amortizing repayment. Construction sub-period up to 12 months, extendable to 18 months at $500 per month. Funds advanced directly to the contractor in four equal 25% disbursements. Closing costs typically $500–$5,500 for loans up to $250,000. Maximum APR 18%.

Patelco Credit Union

California only, primary residences only. APR range 8.25%–9.00% for the most qualified applicant (verified May 18, 2026). Min 4.00%, max 17.00%. Line: $10,000–$400,000. Draw period: 2 years interest-only, then 20-year repayment. Fee: $250 lender fee plus $50/mo (lines ≤$100K) or $100/mo (>$100K). Patelco specifically states it will consider projected rental income from the ADU to help you qualify — a feature most renovation HELOC lenders do not advertise.

Sources: RenoFi.com /start-adus (verified May 19, 2026); Quorum FCU product page (verified May 19, 2026); Tower FCU Dreamline product page (verified May 19, 2026); Patelco ADU HELOC product page (verified May 19, 2026); Bankrate RenoFi review (Feb. 27, 2026); CrossCountry Mortgage product page (verified May 19, 2026); PRNewswire RenoFi Series B announcement (March 3, 2026).

5. How much can you borrow with a renovation HELOC for an ADU?

These are illustrative examples, not guarantees of approval, borrowing capacity, or returns. Construction cost ranges from Angi’s 2026 garage conversion guide, GatherADU’s 2026 California cost guide, Cali ADU’s 2026 LA guide, and Custom Home Builders’ 2026 California guide.

Scenario A — Recent California buyer, detached site-built ADU

| Current home value | $500,000 |

| First mortgage balance | $400,000 |

| ADU type / budget | Detached site-built / $260,000 |

| Expected ARV | $760,000 |

| Standard HELOC (85% CLTV) | $25,000 |

| Renovation HELOC (90% ARV) | $284,000 |

| Borrowing power multiplier | 11.4× |

The textbook case. The standard HELOC math fails — it doesn't even cover design fees. The renovation HELOC math works with margin for cost overruns.

Scenario B — Recent Midwest buyer, garage conversion

| Current home value | $325,000 |

| First mortgage balance | $260,000 |

| ADU type / budget | Garage conversion / $110,000 |

| Expected ARV | $385,000 |

| Standard HELOC (85% CLTV) | $16,250 |

| Renovation HELOC (90% ARV) | $86,500 |

| Borrowing power multiplier | 5.3× |

The multiplier is smaller because garage conversions typically add less value than detached new builds. But the renovation HELOC still closes the gap.

Scenario C — 5-year owner, prefab/modular ADU

| Current home value | $625,000 |

| First mortgage balance | $440,000 |

| ADU type / budget | Prefab modular / $200,000 |

| Expected ARV | $805,000 |

| Standard HELOC (85% CLTV) | $91,250 |

| Renovation HELOC (90% ARV) | $284,500 |

| Borrowing power multiplier | 3.1× |

Five years of equity-building shrinks the multiplier but the standard HELOC still falls short of the budget — a renovation HELOC is the right tool.

Scenario D — 10-year owner with strong equity (standard HELOC wins)

| Current home value | $725,000 |

| First mortgage balance | $200,000 |

| ADU type / budget | Garage conversion / $130,000 |

| Expected ARV | $830,000 |

| Standard HELOC (85% CLTV) | $416,250 |

| Renovation HELOC (90% ARV) | $547,000 |

| Borrowing power multiplier | Not applicable — standard HELOC wins |

This is the scenario where a renovation HELOC is the wrong tool. The standard HELOC already covers the ADU budget more than three times over. For this homeowner, our standard HELOC guide is the better destination.

Scenario E — New buyer in Hawaii, New York, or Massachusetts

| Current home value | $700,000 |

| First mortgage balance | $560,000 |

| ADU type / budget | Detached / $300,000 |

| Expected ARV | $1,000,000 |

| Standard HELOC (85% CLTV) | $35,000 |

| Renovation HELOC (90% ARV) | Not available via RenoFi-network products (Bankrate Feb. 2026) |

| Alternative path | Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, or construction-to-permanent loan |

If you're in HI, NY, or MA and need ARV-based borrowing, RenoFi's network won't serve you. You'll need a different product structure. Section 8 walks through those alternatives.

See What You Can Build

California homeowners get the highest-fidelity feasibility output because our database is densest here.

Get Your Free ADU Report (60 sec)6. The Renovation HELOC Fit Check

🧮 The Renovation HELOC Fit Check

Inputs:

- Current home value

- Current mortgage balance

- Expected after-renovation value

- Total ADU budget including contingency

- ADU type (Garage / Basement / Attached / Detached / Prefab)

- Your state

Outputs:

- Standard HELOC at 85% CLTV — what it allows

- Renovation HELOC at 90% ARV — what it allows

- Whether the project pencils

- Lender options available in your state

The tool models the math two products use to set borrowing ceilings. Income, DTI, credit, and the specific appraisal outcome are what actually determine whether you get the loan.

Run the Fit Check →7. When is a renovation HELOC the wrong tool?

This is the one section RenoFi, Quorum, Tower, and Patelco won’t write. Their job is to sell the product. Our job is to tell you when you don’t need it.

You already have enough current equity

If your standard HELOC at 85% CLTV minus your mortgage balance covers your ADU budget plus 15% contingency, stop. Go to Best HELOC for ADU: Decision Guide → It closes in 2–3 weeks instead of 4–8. There’s no construction-management fee. The application is shorter. You don’t need to commission an as-completed appraisal.

Your project is small relative to the fees

Construction-management fees of $50–$100 per month for 6–12 months equal $300–$1,200 before other closing/appraisal/vendor fees. For modest garage conversions, JADU additions, or basement bedroom conversions where the total budget is small enough that those fixed fees become a meaningful share of the build, an unsecured personal loan, a standard HELOC, or cash usually wins on total cost.

Your state isn’t covered

- RenoFi network: HI, NY, MA unavailable (Bankrate, Feb. 2026)

- Quorum FCU: not available in Texas

- Tower Dreamline: MD, VA, DC, DE, PA, NC, SC, FL only

- Patelco: California primary residences only

Your first mortgage is at 6%+ and you’d happily refinance

If you locked in your current mortgage at a rate above 6%, the protective value of keeping that first mortgage in place is smaller. Compare a cash-out refinance or a construction-to-permanent loan that consolidates everything into a single fixed-rate first mortgage.

You can’t yet produce plans, contractor bid, and itemized budget

The most common reason renovation HELOC applications stall is the construction documentation requirement. The lender cannot order an as-completed appraisal without your project scope. Sequence matters: builder bid → application → appraisal → close → first draw.

You’re planning to sell within 18 months

Renovation HELOC closing costs ($1,000–$2,500 typical, up to $5,500 at Tower), monthly construction-management fees ($300–$1,200 over a typical project), and the non-refundable as-completed appraisal ($500–$1,000) add up to real money. ADUs work as a long-term play more reliably than as a short-term flip.

You need fixed monthly payments more than flexibility

A renovation HELOC is variable-rate by default. If predictable monthly payments matter to you more than draw flexibility, a fixed-rate home equity loan or a construction-to-permanent loan with a fixed-rate permanent phase is a cleaner fit.

Compare ADU lenders

Explore current ADU financing options from lenders who understand ADU construction, organized by loan type and scenario fit.

Compare ADU lenders → (Mortgage Research Center, our approved national mortgage education partner)8. Renovation HELOC vs. the four major alternatives

| Path | Underwrites against | Replaces first mortgage? | Rate type | Best fit |

|---|---|---|---|---|

| Renovation HELOC | After-renovation value | No | Variable (prime + margin) | Limited current equity, low first-mortgage rate, ADU adds substantial value |

| Standard HELOC | Current value | No | Variable (prime + margin) | Ample current equity, wants the simplest product |

| Home equity loan | Current value | No | Fixed | Wants fixed rate, has enough current equity, prefers lump sum |

| Cash-out refinance | Current value | Yes | Fixed or adjustable | First mortgage rate ≥ 6%, wants to consolidate into one payment |

| Construction-to-permanent loan | As-completed value | Yes | Fixed permanent phase | Ground-up detached ADU, willing to refinance first mortgage |

| Fannie Mae HomeStyle Renovation | As-completed value | Yes | Fixed or adjustable | Buying + building, or refinancing with attached ADU on 1–4 unit properties |

| Freddie Mac CHOICERenovation | As-completed value | Yes | Fixed or adjustable | Similar to HomeStyle; Bulletin 2026-1: rental income from CHOICERenovation units cannot be used to qualify |

| FHA 203(k) Standard | As-completed value | Yes (FHA) | Fixed | FHA-eligible borrower, conversion or attached ADU; cannot fund new detached ADU ground-up (HUD ML 2023-17) |

Fannie Mae HomeStyle Renovation

Covers up to $750K construction cost, 75% of as-completed value. Available on 1- to 4-unit properties including attached ADUs and detached ADUs where local zoning permits. The 2025–26 Selling Guide updates allow up to three ADUs on a 1-unit property under UAD 3.6 where local zoning permits. Interest rates are often higher than standard conventional loans — refinancing later into a lower rate is a common strategy.

Freddie Mac CHOICERenovation

Available on 1-, 2-, and 3-unit properties including ADU conversions and new construction. Effective May 4, 2026 (Bulletin 2026-1), rental income from any unit funded by CHOICERenovation proceeds cannot be used to qualify the borrower. This is a material rule change that affects how you model post-construction cash flow qualifying.

FHA 203(k) Standard

Per HUD Mortgagee Letter 2023-17 (October 2023), eligible improvements include (a) converting an existing structure to include an ADU, (b) adding an attached ADU, or (c) renovating an existing attached or unattached ADU. HUD ML 2023-17 generally does not cover constructing a brand-new detached ADU from the ground up. For that, HomeStyle, CHOICERenovation, or a construction-to-permanent loan are typically the cleaner paths.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Compare ADU lenders → Explore ADU-Friendly Lenders

Current financing options from lenders who understand ADU construction, organized by loan type and scenario fit. (Mortgage Research Center — our approved national mortgage education partner.)

Explore ADU-Friendly Lenders →Sources: Fannie Mae ADU product page and HomeStyle Renovation guide (verified May 19, 2026); Freddie Mac ADU fact sheet (February 2026); HUD Mortgagee Letter 2023-17 (October 2023); CFPB HELOC consumer guide.

9. Can ADU rental income help you qualify?

The rule for renovation HELOCs specifically

For most renovation HELOC applications covering construction of an ADU that doesn’t exist yet, projected rental income generally cannot be used to qualify. The Urban Institute identified this as one of the structural barriers to ADU financing in its April 2024 report. The notable exception: Patelco Credit Union’s ADU HELOC product page explicitly states the credit union will consider projected ADU rental income. Other lenders may make case-by-case exceptions on application, but it’s not advertised. Ask directly.

Freddie Mac’s framework

Per Freddie Mac’s ADU fact sheet (February 2026) and Bulletin 2022-11, rental income from an ADU on a 1-unit primary residence can qualify under specific conditions:

- Transaction must be a purchase or no cash-out refinance

- ADU rental income cannot exceed 30% of total stable monthly qualifying income

- Only 75% of the lease amount or appraised market rent counts

- The appraisal must include an ADU rental analysis with comps

FHA’s framework

Per HUD Mortgagee Letter 2023-17 (October 2023), FHA allows 75% of the lesser of market rent or the lease/rental agreement as effective income, capped at 30% of total monthly effective income. For new ADUs added through Standard 203(k) without rental history, FHA uses 50% of the lesser of fair market rent or lease/rental agreement. ADU rental income may not be used for FHA cash-out refinances.

The practical takeaway

For the renovation HELOC initially: assume no rental income credit unless you’re using Patelco (which explicitly advertises it) or your lender confirms in writing they’ll count it. Build your financing plan so the project works on your current income.

For the post-build refinance: rental income from a now-built and rented ADU is much more useful — under Freddie’s framework, FHA’s purchase or rate-term refi scenarios, or Fannie’s eligible products. The Two-Step Strategy in section 13 walks through this play.

Sources: Freddie Mac Bulletin 2022-11 (June 1, 2022); Freddie Mac ADU fact sheet (February 2026); HUD Mortgagee Letter 2023-17 (October 2023); Fannie Mae Selling Guide B3-3.8-01 (verified May 19, 2026); Patelco ADU HELOC product page (verified May 18, 2026); Urban Institute, “To Increase the Housing Supply, Focus on ADU Financing” (April 2024).

10. Documents to gather before you apply

Personal and financial documents

- Government-issued ID

- Two most recent pay stubs (W-2) or two years of tax returns (self-employed)

- W-2s or 1099s from the past two years

- Two most recent months of bank statements

- Homeowners insurance declarations page

- Most recent first mortgage statement

- Documentation of other debts or obligations

Property and title documents

- Property tax statement

- Title or deed reference

- Recent home value evidence (comps, online valuations, or recent appraisal)

ADU project documents — where applications stall

- Signed contractor agreement with licensed builder

- Itemized cost estimate broken into materials and labor by phase

- Architectural plans or selected pre-approved plan set

- Detailed scope of work

- Construction timeline with major milestones

- Permit application status

- Contingency budget (typically 10–20% above hard construction cost)

What actually delays your first draw

| Delay cause | How to avoid it |

|---|---|

| Plans/contractor not finalized | Finalize before you apply, not after |

| Appraiser can't find ADU comps | Pull comps yourself first; if there are none, talk to a local appraiser before paying for the as-completed |

| Itemized budget shows lump sums only | Break into materials and labor by phase before submitting |

| Permit uncertainty | Run a feasibility check; have your builder confirm permit path |

| Construction-management vendor onboarding delay | Ask the lender for the CM vendor name and confirm processing timeline |

| State availability not confirmed | Verify the lender lends in your state before you spend time on the application |

| Title/lien issues from prior work | Order a title check before applying |

12 questions to ask the lender before submitting

- Are you currently making renovation HELOC loans in my state?

- What’s your typical underwriting timeline from application to first draw?

- What’s your minimum credit score and DTI threshold?

- What as-completed CLTV will you allow on my profile?

- Do you allow recently purchased homes, or is there a seasoning requirement?

- What’s the floor rate, margin, and maximum APR on the variable rate?

- Is there a fixed-rate conversion option, and what does it cost?

- What’s the construction-management vendor fee structure?

- What’s the maximum construction draw period?

- What’s the extension policy and cost if the project runs long?

- Are there prepayment penalties?

- Can I see a sample draw schedule and contractor payment process in writing?

If a lender won’t answer any of these in writing before you apply, that’s a meaningful signal.

Download the Free 2026 ADU Starter Kit

Budget worksheets, lender question checklist, contractor vetting checklist, and a step-by-step planning sequence. No commitment, no spam.

Download the Free ADU Starter Kit →Sources: Quorum FCU document checklist (verified May 19, 2026); Tower FCU Dreamline process page (verified May 19, 2026); Fannie Mae HomeStyle Renovation process documentation.

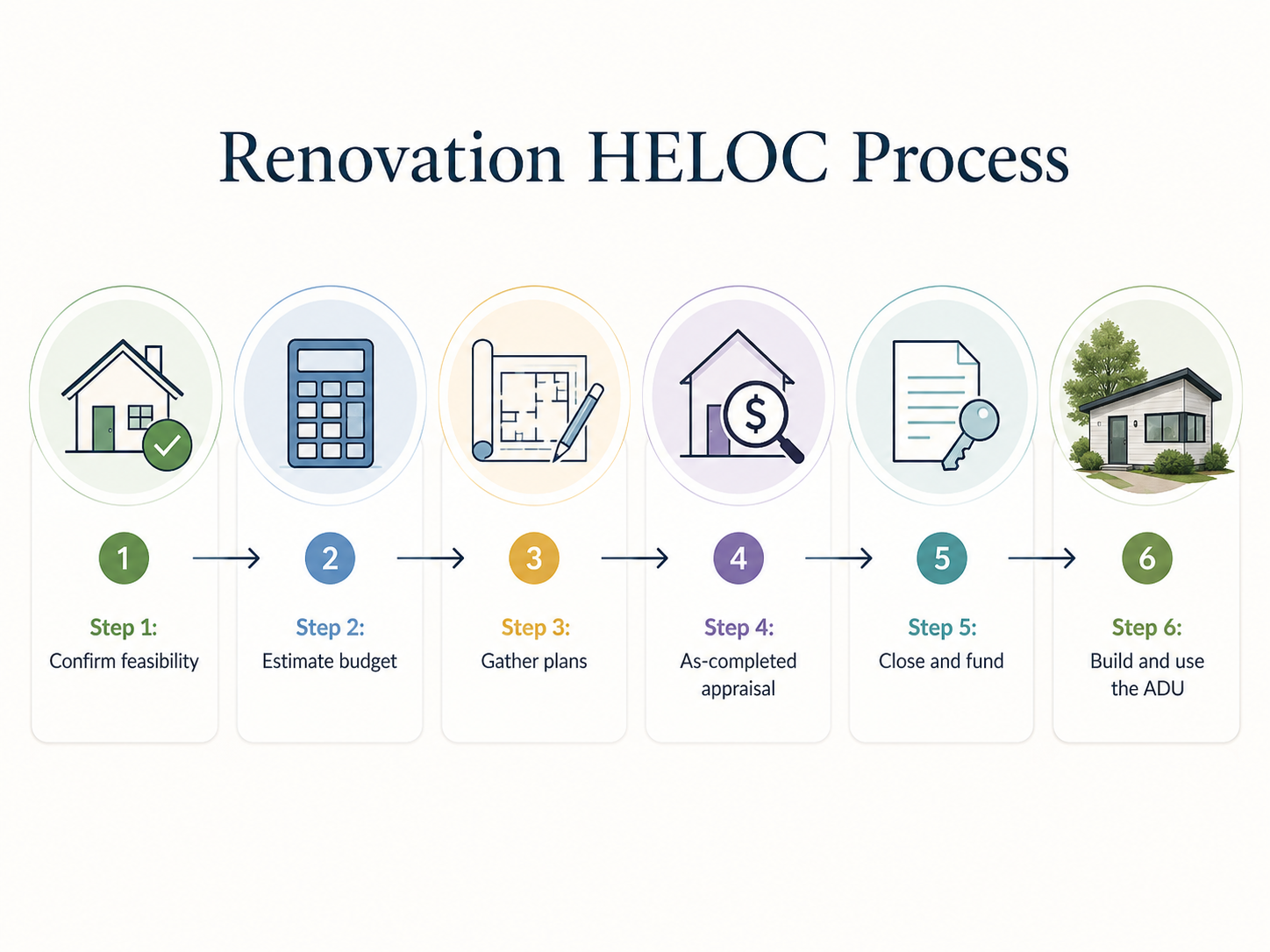

11. The application process, step by step

Confirm your ADU is permittable on your property

Before talking to any lender, verify your lot, zoning, and (if applicable) HOA actually allow the ADU type you want. Run a free 60-second feasibility check →

Get written bids from at least two to three licensed builders

A single bid is a starting point, not a budget. Three bids let you triangulate the real cost. Verify each builder's license in your state.

Estimate your after-renovation value using local comps

Pull recently sold properties within a mile that have permitted ADUs of similar size. If your market has few ADU comps, plan for a conservative appraisal.

Run the Renovation HELOC Fit Check on this page

Confirm whether the standard HELOC or renovation HELOC produces enough borrowing power for your project budget plus 15% contingency.

Pre-qualify with one or two lenders

Most renovation HELOC platforms offer a soft-pull pre-qualification. This is a free signal of whether your credit profile and DTI will support the loan.

Finalize your contractor selection and signed agreement

This is the document that unlocks the formal application.

Submit the full application

Submit with the documentation from section 10.

Order and pay for the as-completed appraisal

Typical cost: $500–$1,000 depending on region. This fee is non-refundable. Even if your loan is ultimately denied or the appraisal comes in lower than needed, you pay. Do steps 1–6 well before paying for the appraisal.

Close on the line

After underwriting completes and the lender issues a commitment letter, you sign closing documents. At Tower FCU, the first 25% draw is released to the contractor at closing.

Plan your post-construction refinance evaluation

Section 13 walks through this.

Realistic timeline

| Phase | Typical duration | Notes |

|---|---|---|

| Feasibility + builder bids | 2–6 weeks | Independent of lender |

| Pre-qualification | 1–3 days | Soft-pull check |

| Full application + document gathering | 1–2 weeks | Depends on borrower readiness |

| As-completed appraisal | 2–3 weeks | Often the longest single step |

| Underwriting + commitment | 1–2 weeks | Quorum says 1–2 days for underwriting after complete docs; appraisal extends overall timeline |

| Closing | 1 week | Standard |

| First draw to contractor | At closing | Some lenders release the first 25% at closing |

Total: 4–8 weeks from application to first draw.

12. Real rates, fees, and timelines (verified May 19, 2026)

| Product | Verified APR | Floor | Max APR | Verification date |

|---|---|---|---|---|

| Quorum FCU Renovation HELOC | As low as 6.625% APR | 4.95% | 18% | December 11, 2025 (quorumfcu.org) |

| Patelco ADU HELOC | 8.25% to 9.00% APR | 4.00% | 17% | May 18, 2026 (patelco.org) |

| Tower FCU Dreamline | Prime + margin (posted rate sheet) | n/d | 18% | May 19, 2026 (towerfcu.org) |

| RenoFi (set by partner CU) | Variable; not published by RenoFi itself | Varies | Varies | n/a |

Verify the current rate directly with the lender before you apply. Posted rates can become stale between verification dates.

Renovation HELOC fee stack

| Fee type | Typical amount | Verified examples |

|---|---|---|

| Lender / processing fee | $250–$300 | Patelco $250; Tower $300 |

| As-completed appraisal | $500–$1,000 | Varies by region; non-refundable |

| Construction-management vendor origination | Varies | Paid at closing at most lenders |

| Monthly construction admin fee during build | $0–$100/mo | Patelco: $50/mo (≤$100K) or $100/mo (>$100K); Tower: $500/month for extensions beyond 12 months |

| Title and recording fees | $300–$1,500 | Standard, varies by state |

| Total closing costs | $500–$5,500 typical at Tower for loans up to $250K |

Sources: Federal Reserve H.15 (May 15, 2026); Federal Reserve FOMC statement (April 29, 2026); Bankrate HELOC rate survey (May 6, 2026); Quorum FCU (verified December 11, 2025); Patelco (verified May 18, 2026); Tower FCU Dreamline (verified May 19, 2026).

13. Taxes and the post-build refinance strategy

Tax deductibility, accurately stated

1. The use-of-funds test. The IRS allows a deduction for HELOC interest only if the proceeds are used to “buy, build, or substantially improve” the home securing the loan. Building an ADU on the property securing the HELOC qualifies as a substantial improvement.

2. The dollar limit. For loans secured after December 15, 2017, the combined home acquisition debt limit is $750,000 ($375,000 if married filing separately). Loans secured before that date may be grandfathered at the older $1 million / $500,000 limit.

The interest is only deductible if you itemize on Schedule A. Keep documentation: construction invoices, contractor payments, and lender draw records should be retained in case of audit.

The Two-Step Strategy

This is the move most homeowners using a renovation HELOC eventually arrive at on their own.

Step 1 — Build with the renovation HELOC

Variable-rate, no first-mortgage refinance, construction draws aligned with contractor invoices.

Step 2 — Refinance after the ADU is complete and rented

Once your ADU is permitted, complete, and has 6–12 months of documented rental income:

- Your home has a new, higher post-renovation appraisal that’s no longer hypothetical

- The rental income is documented and usable under Freddie Mac’s framework (75% of rent, capped at 30% of qualifying income) or FHA’s framework (HUD ML 2023-17)

- You can evaluate refinancing into a single fixed-rate first mortgage that consolidates both loans

Run the refi math carefully:

- Combined rate before: your current first mortgage rate blended with your renovation HELOC’s variable rate

- Single refi rate after: whatever 30-year fixed rates are at the time of refi

If the single fixed rate is lower than your blended rate, the refi wins on cost. If it’s higher, you may be better off keeping the two-loan structure and aggressively paying down the variable-rate HELOC instead.

Sources: IRS Publication 936 (2025 edition); IRS FAQ on home equity loan interest deductibility (verified May 19, 2026); Freddie Mac ADU rental income framework; HUD Mortgagee Letter 2023-17 (October 2023).

14. California spotlight: why ARV lending is most available here

California ADU laws — decoded for why a lender cares

| Law | Effective | What it does | Why the lender cares |

|---|---|---|---|

| AB 976 (Chapter 751, Statutes of 2023) | January 1, 2024 | Permanently removes owner-occupancy requirements for ADUs (except JADUs) | Makes ADU viable as pure rental from day one — supports rental-income underwriting later |

| AB 1332 (Chapter 759, Statutes of 2023) | January 1, 2024 | Requires local agencies to develop preapproved ADU plan programs by January 1, 2025 | Faster permit timelines mean shorter construction-draw periods, less lender risk |

| AB 2533 | Recent (HCD March 2026 handbook) | Creates legalization pathway for qualifying unpermitted ADUs and JADUs built before January 1, 2020 | Existing unpermitted ADUs can be legalized — but health/safety remediation may still be required |

| SB 1211 | Recent | Authorizes up to 8 detached ADUs on a lot with an existing multifamily dwelling (not exceeding existing unit count) | Expands multifamily ADU eligibility |

| AB 68 (foundational) | Pre-2024 | Streamlined statewide ADU permitting | Established the regulatory base California's renovation HELOC market is built on |

Renovation HELOC availability in California

- RenoFi network — California is one of the covered states.

- Patelco Credit Union ADU HELOC — California’s most clearly disclosed renovation HELOC. Up to 125% of current value OR 90% of ARV. APR 8.25%–9.00% as of May 18, 2026. The only renovation HELOC on this page that explicitly advertises consideration of projected ADU rental income.

- Local California credit unions — offer ARV-based home equity products without the RenoFi underwriting layer.

For City of San Diego homeowners, the San Diego Housing Commission (SDHC) ADU Finance Program offers up to $250,000 in financing, subject to underwriting, income/property/credit/ owner-occupancy requirements, and seven-year affordability restrictions. SDHC’s portal carries a funding-availability warning — verify current funding status directly with SDHC before relying on the program.

California cost realities

| Metro | Typical detached ADU cost (2026) | Typical garage conversion (2026) | ARV opportunity |

|---|---|---|---|

| Los Angeles | $190K–$400K+ | $100K–$225K | Strong — high rental demand, dense ADU comps |

| San Diego County | $200K–$450K+ | $100K–$200K | Strong — high rental demand, dense ADU comps |

| Bay Area | $260K–$450K+ | $130K–$250K | Strong — but neighborhood-ceiling effect can cap ARV in lower-tier neighborhoods |

| Sacramento / Central Valley | $150K–$300K | $70K–$150K | Moderate — fewer ADU comps |

| Inland / Rural California | $140K–$280K | $65K–$160K | Weaker ARV pickup; verify comps carefully |

See What You Can Build

California homeowners get the highest-fidelity feasibility output because our database is densest here.

Get Your Free ADU Report (60 sec)15. Frequently asked questions

What is a renovation HELOC for an ADU?▼

A renovation HELOC for an ADU is a second-position home equity line of credit underwritten against your home's projected after-renovation value rather than its current value. For an ADU project, this typically unlocks more borrowing power without requiring a first-mortgage refinance.

How is a renovation HELOC different from a regular HELOC?▼

A regular HELOC is capped by your home's current appraised value, usually at 80–85% combined loan-to-value minus your mortgage balance. A renovation HELOC is capped by your home's projected post-construction value, usually at 90% of after-renovation value. The renovation version requires construction documentation, takes longer to close, and often has construction-period fees the regular version doesn't.

Can I use a renovation HELOC to build an ADU?▼

Yes — the product is specifically designed for ADU and major renovation projects. Approval depends on the lender's eligibility criteria, your borrower profile, the as-completed appraisal, and your state.

Is RenoFi a lender?▼

No. RenoFi is a renovation-financing platform and licensed mortgage broker that powers loans originated by partner credit unions including Quorum FCU, USALLIANCE Financial, Ardent Credit Union, Chartway Credit Union, and First Community Credit Union. The credit union is the actual lender on your note.

In which states can I get a renovation HELOC?▼

Product availability is uneven and changes. RenoFi states it's licensed in 48 states; Bankrate's February 27, 2026 review lists Hawaii, New York, and Massachusetts as unavailable for RenoFi-network products. Quorum's product disclosure says its Renovation HELOC is not available in Texas. Tower Dreamline is available in MD, VA, DC, DE, PA, NC, SC, and FL only. Patelco's ADU HELOC is California only. Verify directly with the lender before applying.

Why did the as-completed appraisal come in lower than my ADU cost?▼

Several common reasons: lack of permitted-ADU comparable sales within ~1 mile; the neighborhood ceiling effect (your ARV is capped by what comparable homes in your area sell for); the appraiser using sale comps as the primary anchor rather than gross rental yield; unpermitted nearby ADUs that don't count as comps; or over-building for the neighborhood.

How much can I borrow with a renovation HELOC for an ADU?▼

Maximum borrowing is the lesser of (1) 90% of after-renovation value minus your first-mortgage balance and (2) the product's hard cap — typically $750K at RenoFi/Quorum or $350K at Tower. Run the Renovation HELOC Fit Check on this page to see your numbers.

What credit score do I need?▼

Most partner credit unions look for a minimum credit score of around 640. Better rates and higher CLTV approvals generally require 700+. Specific minimums and pricing vary by lender.

How long does the application take?▼

Typically 4–8 weeks from application to first construction draw, compared with 2–3 weeks for a standard HELOC. The bottleneck is the as-completed appraisal, which can't be ordered until you've provided plans, signed contractor agreement, and itemized budget. Quorum says loan underwriting is typically 1–2 days after a complete application package, but appraisal extends the overall timeline.

Are there fees during construction?▼

Yes at most lenders. Patelco charges $50/month (lines ≤$100K) or $100/month (>$100K). Tower FCU charges $500/month for construction extensions beyond a 12-month window. RenoFi-partner lenders' construction-management fees vary.

Is the interest tax-deductible?▼

Per IRS Publication 936, interest on a HELOC used to 'buy, build, or substantially improve' the home securing the loan may be deductible, up to a combined home-acquisition-debt limit of $750,000 for joint filers ($375,000 if married filing separately) for loans secured after December 15, 2017. ADU construction generally qualifies. The deduction requires itemizing on Schedule A. Consult a tax professional for your situation.

Can I use projected ADU rental income to qualify?▼

For most renovation HELOCs, generally no — though Patelco's ADU HELOC product page explicitly states the credit union will consider projected ADU rental income. Other lenders may make case-by-case exceptions. For agency renovation mortgages, Freddie Mac allows up to 75% of market rent (capped at 30% of total qualifying income) for purchase or no-cash-out refinance, and FHA allows up to 75% of ADU rent (capped at 30% of total monthly effective income) per HUD Mortgagee Letter 2023-17.

What if my renovation HELOC application is denied?▼

Real alternatives: a smaller standard HELOC for what your current equity supports; a renovation mortgage (Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, or FHA 203(k)) that replaces your first mortgage but uses similar ARV underwriting; or a construction-to-permanent loan.

Should I get a renovation HELOC or a construction-to-permanent loan?▼

A renovation HELOC keeps your existing first mortgage intact (best when your existing rate is favorable). A construction-to-permanent loan replaces your first mortgage but consolidates into a single fixed-rate loan at the end of the build. Ground-up detached ADU builds where you don't want a low existing rate often lean toward construction-to-permanent. Conversions, attached additions, or builds where you have a sub-5% first mortgage often lean toward a renovation HELOC.

Can I use a renovation HELOC for a prefab or modular ADU?▼

Yes, if the lender allows the specific project type and your borrowing room covers the budget. Confirm lender eligibility — some have specific rules for manufactured or modular structures. Costs are usually more predictable on prefab, which can make underwriting smoother.

16. What we verified

✓ Rates and Federal Reserve data — last verified May 19, 2026

- Bank prime loan rate: 6.75% (Federal Reserve H.15, May 15, 2026)

- Federal funds effective rate: 3.63% (Federal Reserve H.15, May 15, 2026)

- Federal funds target range: 3.50%–3.75% (Fed FOMC statement, April 29, 2026)

- National HELOC average: 7.26% (Bankrate, May 6, 2026)

✓ Lender product terms — last verified May 19, 2026 unless noted

- Quorum FCU Renovation HELOC: APR as low as 6.625%, floor 4.95%, max 18% (verified December 11, 2025); not available in Texas

- Tower FCU Dreamline: $50K–$350K limits, 15-yr draw + 15-yr repay, $300 processing fee, max APR 18%, closing costs $500–$5,500 (loans up to $250K); MD, VA, DC, DE, PA, NC, SC, FL only

- Patelco ADU HELOC: APR 8.25%–9.00% (effective May 18, 2026); California primary residences only; explicitly considers projected ADU rental income

- RenoFi network: 48 states per RenoFi; Bankrate (Feb. 27, 2026) lists HI, NY, MA unavailable

✓ Agency rules — last verified May 19, 2026

- Fannie Mae HomeStyle Renovation ADU eligibility (Fannie Mae ADU page; Selling Guide B3-3.8-01)

- Freddie Mac CHOICERenovation and ADU rental income framework (ADU fact sheet Feb. 2026; Bulletin 2022-11 and Bulletin 2026-1)

- FHA Mortgagee Letter 2023-17 (October 2023): Standard 203(k) ADU-eligible improvements; rental income framework

- IRS Publication 936 (2025 edition): $750,000/$375,000 acquisition debt limit; “buy, build, or substantially improve” test

✓ California law — verified against HCD ADU Handbook (March 2026)

- AB 976 (Chapter 751, Statutes of 2023; effective January 1, 2024)

- AB 1332 (Chapter 759, Statutes of 2023; effective January 1, 2024)

- AB 2533 legalization pathway

- SB 1211 multifamily ADU expansion

✓ Cost and market data

- JLC/Zonda 2025 Cost vs. Value Report — ADU: $166,406 job cost, $68,656 resale, 41% recoup nationally

- 2026 cost ranges from Angi, GatherADU, Cali ADU, Custom Home Builders

- Urban Institute, “To Increase the Housing Supply, Focus on ADU Financing” (April 2024)

- RenoFi Series B platform metrics: PRNewswire (March 3, 2026)

- SDHC ADU Finance Program: City of San Diego only, up to $250,000, subject to income/credit/occupancy/affordability restrictions and current funding availability

Cells in our lender matrix marked — are where the lender does not publicly disclose the data point. We have not estimated. We have not invented.

17. Methodology and editorial standards

What “best” means on this page

“Best” means best fit for your specific situation. We organize by scenario and documented loan features, not by who pays us the most. Several of the lenders we cover most thoroughly — Quorum, Tower, Patelco — are not affiliate partners. We cover them because they’re the most credible offerings in the category.

How affiliate relationships work on this page

The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation.

- Mortgage Research Center (MRC) — our approved active national mortgage education partner. The secondary CTA on this page links to MRC for broad ADU lender exploration.

- RenoFi, Quorum FCU, Tower FCU, Patelco — not currently affiliate partners. We cover these products editorially. We earn no commission on referrals to these lenders.

Update policy

This guide is reviewed quarterly. Rate and product term data is reviewed monthly. All source citations include verification dates. If you notice anything outdated or incorrect, contact us and we’ll verify within 48 hours.

About Dwelling Index

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We’re not a lender, broker, contractor, or builder. Our editorial standards and affiliate disclosure are publicly available.

Related guides

- How to Finance an ADU in 2026: 7 Paths Compared → — every financing path side-by-side

- Best HELOC for ADU: Decision Guide & Lender Checklist → — standard HELOC deep-dive

- How Much Does an ADU Cost? → — national cost ranges by type and size

- California ADU Laws 2025: What to Know → — state legislation summary

- Free Property Eligibility Check → — 60-second feasibility report

Not sure where to start? See what’s possible at your address.

Get your free ADU report in 60 seconds — no commitment, no spam.

Get Your Free ADU Report →