ADU Loan vs HELOC: How to Pick the Right One in 2026 (Verified Rates + Free Fit Calculator)

By The Dwelling Index Editorial Team · Editorial standards · Methodology

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder.

Last updated: · Last verified: May 20, 2026 · 18 sources cited

The bottom line on ADU loan vs HELOC

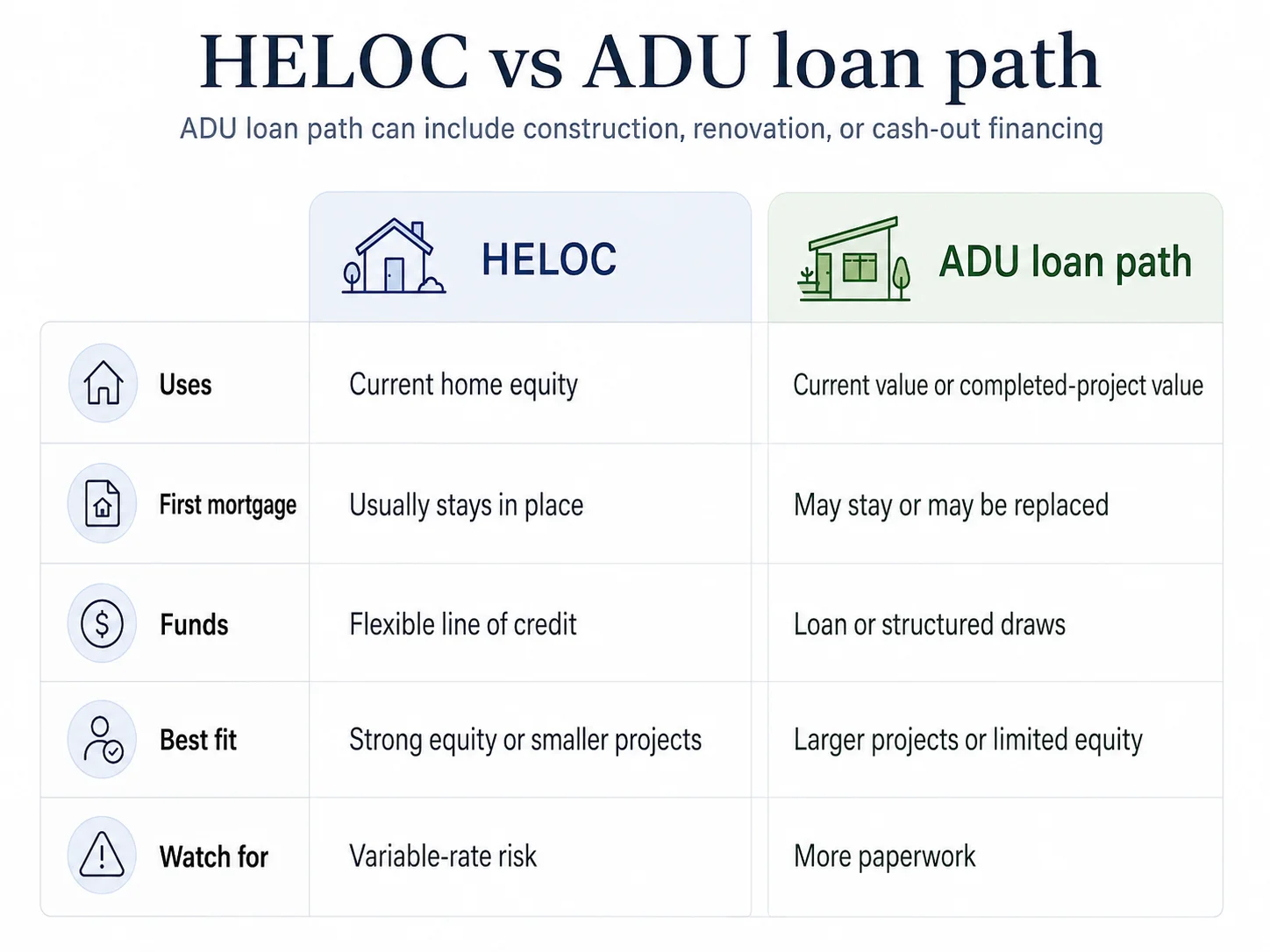

ADU loan vs HELOC comes down to one formula and one fact. The formula: current home value × 80% − first mortgage balance − any other liens equals your likely HELOC borrowing room. The fact: an “ADU loan” is not one product — it usually means a construction loan, a renovation mortgage (Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, or FHA 203(k)), a lender-branded ADU product, or a cash-out refinance. If your HELOC room covers the ADU budget plus a 10–15% contingency, a HELOC is usually the cleanest path. If it falls short, you need a loan that underwrites against the home’s after-completion value.

| HELOC | “ADU loan” (four products) | |

|---|---|---|

| What it really is | Revolving second-lien line of credit | Construction loan, renovation mortgage, lender-branded ADU product, or cash-out refi |

| Keeps first mortgage? | Yes | Construction: depends on structure. Renovation: no. Cash-out: no. ADU-branded: depends. |

| Underwrites against | Current home value | Often the after-completion value |

| Rate type | Usually variable (prime + margin) | Usually fixed |

| Benchmark rate, May 17, 2026* | ~7.21% (Curinos) / 7.26% (Bankrate) | Construction: ~7.0–9.0% · Renovation: ~6.8–7.5% · Cash-out: varies by profile |

| Typical close time | 2–6 weeks | 30–60 days (construction); 45–60 days (renovation) |

| Biggest watch-out | Variable rate; line can be frozen or reduced | Lender-controlled draws; may replace your first mortgage |

*Curinos national HELOC average via Yahoo Finance, May 17, 2026; Bankrate national HELOC survey, May 6, 2026. Construction and renovation rate ranges from publicly published lender pages verified May 2026. Rates are not loan offers; actual pricing varies by lender, credit, LTV, lien position, property type, occupancy, and state.

See what you can build before you talk to a lender. The cheapest financing path is the one that matches the ADU you can actually permit. Most homeowners who get blocked don’t get blocked by financing — they get blocked by setbacks, fire-zone rules, lot coverage limits, height limits, or owner-occupancy ordinances. Confirm your lot is buildable first.

See What You Can Build → Get Your Free ADU Report

What we verified for this guide (as of May 20, 2026)

- HELOC mechanics — Federal Trade Commission (FTC) consumer guidance on home equity lines of credit, and Consumer Financial Protection Bureau (CFPB) HELOC consumer booklet (12 CFR §1026.40(e)).

- Benchmark rates — Curinos national HELOC average of 7.21% (May 17, 2026 via Yahoo Finance); Bankrate national HELOC survey at 7.26% and home equity loan at 8.03% as of May 6, 2026; Federal Reserve H.15 bank prime loan rate at 6.75% (May 2026).

- Fannie Mae ADU rules — Selling Guide B3-3.8-01 (updated 10/08/2025) and Announcement SEL-2025-08; Desktop Underwriter (DU) version 12.1, effective the weekend of March 21, 2026.

- Freddie Mac CHOICERenovation rules — Bulletin 2026-1: for applications received on or after May 4, 2026, rental income from any unit included in the renovation project funded by the mortgage proceeds may not be used to qualify the borrower.

- FHA / HUD — Mortgagee Letter 2023-17 on ADU rental income, property eligibility, and appraisal protocols; HUD’s Limited 203(k) and Standard 203(k) program guidance.

- IRS rules — Publication 936 (2025) on home mortgage interest deduction and the “buy, build, or substantially improve” rule for HELOC interest, with the $750,000 acquisition-debt cap.

- HEI products — CFPB issue spotlight on home equity contracts (2025) and CFPB guidance on consumer risk.

Why “ADU loan vs HELOC” is the wrong question — until you fix the terminology

Most people searching this comparison are stuck on a vocabulary problem. They’ve heard “ADU loan” from a builder, a podcast, or a lender ad, and they assume it refers to a single product. It doesn’t. There is no standardized national “ADU loan” with one rate, one structure, and one set of rules. When a builder, lender, or finance writer says “ADU loan,” they usually mean one of four things:

- A construction loan or construction-to-permanent loan, structured for ground-up ADU builds with staged draws gated by inspections.

- A renovation mortgage — Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, or FHA 203(k) — that underwrites against the home’s after-completion value.

- A lender-branded ADU product — for example, Patelco Credit Union’s ADU HELOC in California, Griffin Funding’s ADU loan offering, or specialty programs at credit unions and nonbank lenders.

- A cash-out refinance marketed as “ADU financing” — a regular cash-out refi with the marketing tilted toward ADU buyers.

How to tell which “ADU loan” your lender or builder actually means

| If they described it as… | They most likely mean… |

|---|---|

| Funds disbursed in draws with inspections at foundation, framing, rough-in, and finish | A construction loan (often construction-to-permanent) |

| One loan that replaces your mortgage and includes both your purchase/refi and the ADU build | Fannie Mae HomeStyle Renovation or Freddie Mac CHOICERenovation |

| Backed by FHA with a 3.5% minimum down and a renovation escrow | FHA 203(k), Limited or Standard |

| A second mortgage that uses your home's future (after-renovation) value | An ARV HELOC, typically through a specialty lender like RenoFi via partner credit unions |

| Replaces your existing mortgage and gives you cash for the ADU | A cash-out refinance |

| A line of credit secured by your home that you draw from as needed | A standard HELOC — they meant this all along |

| A 'specialty ADU loan' from a specific lender | Usually one of the above wrapped in a marketing label |

If your builder’s preferred lender pitched you “an ADU loan” and you can’t slot it into one of those rows, the right move is to ask the lender for the actual product name and program guide before signing anything. Words like “draws,” “as-completed appraisal,” “renovation escrow,” and “construction-to-permanent” tell you which row you’re in.

How HELOCs actually work — the parts that change the comparison

A home equity line of credit (HELOC) is a revolving, home-secured second mortgage with a draw period followed by a repayment period. During the draw period (typically 5–10 years), you borrow against an approved credit limit as needed and usually make interest-only payments on the drawn balance. When the draw period ends, the line closes and you enter the repayment period (typically 10–20 years) when principal and interest payments begin.

Three HELOC features change the head-to-head against an “ADU loan” more than the rate does:

That third feature — current-value underwriting — is the spine of the entire decision. It’s also where the formula in the next section earns its keep.

The one formula that decides most cases

Likely HELOC room = (current home value × 0.80) − first mortgage balance − any other liens

We use 80% combined loan-to-value as the conservative default because it’s the most common HELOC cap. Some lenders go to 85% for top-tier borrowers; you can rerun the math at 85% as a stretch case, but plan around 80%.

Compare that result to your ADU budget plus contingency — not the builder’s sticker price. We use 15% as the default contingency layer because ADU projects routinely encounter sitework, utility lateral, permit, and impact-fee costs that don’t appear in the initial bid.

Worked example

| Current home value | $900,000 |

| Conservative CLTV cap | 80% |

| Max combined debt at 80% | $720,000 |

| First mortgage balance | $600,000 |

| Other liens | $0 |

| Estimated HELOC room | $120,000 |

| ADU budget (builder quote) | $215,000 |

| 15% contingency | $32,250 |

| ADU budget plus contingency | $247,250 |

| Verdict | HELOC room is short by ~$127k. Test future-value ADU loan paths first. |

If your HELOC room covers the budget plus contingency comfortably, a HELOC is usually the cleanest path. If it falls short, you need a loan that underwrites against the home’s after-completion value.

Run your own numbers

The numbers above are illustrative. To run the test against your home, your mortgage balance, and your actual ADU scope, use our free fit calculator. It returns your likely HELOC room, your budget gap, and which loan path to test first.

This is an educational fit check, not a loan approval, rate quote, or financial advice. Rate assumptions are refreshed on the page’s verification cadence and labeled with source and date.

What about a home equity loan instead of a HELOC?

A home equity loan (sometimes called a HELOAN) is the fixed-rate, lump-sum cousin of the HELOC. Same security (home as collateral). Same lien position (second). Same first-mortgage preservation. Different mechanics: you receive the full loan amount at closing, your rate is fixed for the life of the loan, and you start principal-and-interest payments immediately.

For an ADU project, a home equity loan fits when you already know your final ADU budget, want payment certainty for the full construction period, and don’t mind paying interest on the full borrowed amount from day one. A HELOC fits when costs arrive in waves and you only want to pay interest on funds actually drawn.

| HELOC | Home equity loan | |

|---|---|---|

| Funds | Draw as needed up to limit | Lump sum at closing |

| Rate | Usually variable | Fixed for the life of the loan |

| Interest accrues on | Only what you've drawn | Full borrowed amount from day one |

| Payment structure | Interest-only during draw, P&I during repayment | Principal + interest from month one |

| Best for | Phased construction with variable cash needs | Known final budget; payment certainty |

| Benchmark rate, May 2026 | 7.21% (Curinos) / 7.26% (Bankrate) | 7.36% (Curinos) / 8.03% (Bankrate) |

ADU loan vs HELOC, head-to-head by product

The formula tells you whether to test current-value or future-value financing first. Now the question becomes which specific product within each lane. We compare HELOC against each of the four real meanings of “ADU loan” below, with current rate data and the genuine tradeoffs.

HELOC vs construction loan

A construction loan funds a ground-up ADU build through staged draws gated by lender inspections at milestones like foundation, framing, rough-in, and finish. A construction-to-permanent (C-to-P) loan converts to a long-term mortgage when the build is complete, typically replacing your first mortgage at conversion.

| Dimension | HELOC | Construction / C-to-P loan |

|---|---|---|

| Underwrites against | Current home value | After-completion value |

| Keeps your first mortgage? | Yes | Depends on structure; often no at conversion |

| Typical close time | 2–6 weeks | 30–60 days |

| Draw control | Homeowner-controlled | Lender-controlled with inspections |

| Rate (May 17, 2026) | ~7.21% national avg (Curinos) | ~7.0–9.0% range, per published lender pages |

| Equity / down payment | 15–20% existing equity | Often 20–25% of as-completed value |

| Credit floor | 620–680 for best pricing | 680+, many lenders prefer 700+ |

| Documentation | Income, equity, appraisal | Plans, contractor agreement, draw schedule, budget |

HELOC vs renovation mortgage (HomeStyle, CHOICERenovation, 203(k))

Renovation mortgages bundle the home purchase or refinance with the cost of improvements — including building an ADU when zoning allows — into a single loan that underwrites against the home’s after-completion value.

| Dimension | HELOC | Renovation mortgage |

|---|---|---|

| Underwrites against | Current home value | After-completion value |

| Keeps your first mortgage? | Yes | No — replaces it |

| Typical close time | 2–6 weeks | 45–60 days |

| Funds disbursement | Draw as needed up to limit | Renovation escrow with lender-serviced draws |

| Rate (May 2026) | ~7.21% national avg (Curinos) | ~6.8–7.5% range, per published lender pages |

| Best fit | Existing low first mortgage you want to keep | Buying + building, or thin current equity |

HELOC vs lender-branded ADU product

A growing number of lenders market “ADU loans” as a distinct product. In our review of lender pages, these usually reduce to one of three underlying structures: (a) a standard HELOC or home equity loan with ADU-friendly marketing, (b) a construction or construction-to-permanent loan adapted for ADU scopes, or (c) a renovation mortgage routed through the lender’s program partnership with Fannie Mae, Freddie Mac, or FHA.

Patelco Credit Union’s ADU HELOC in California, for example, is structurally a HELOC with a 2-year draw period followed by a 20-year repayment period, designed around typical ADU construction timelines. Griffin Funding offers fixed-rate HELOCs alongside DSCR loans aimed at ADUs intended as rentals. New American Funding markets an ADU loan program that routes borrowers into the underlying conventional product that fits their situation.

HELOC vs cash-out refinance

A cash-out refinance replaces your existing first mortgage with a new, larger one and gives you the difference in cash for the ADU. It consolidates financing into one payment and a single rate — but at the cost of your existing first mortgage.

| Dimension | HELOC | Cash-out refinance |

|---|---|---|

| Keeps your first mortgage? | Yes | No — replaces it |

| Rate (May 2026) | ~7.21% national avg (Curinos) | Bankrate May 2026 national 30-year refi APR ~6.78%; cash-out pricing varies by lender, profile, LTV, fees |

| Rate type | Usually variable | Fixed |

| Closing costs | Often low | Typically 2–5% of loan amount |

| Best fit | Existing low first mortgage worth preserving | Existing rate at or above current market |

Mortgage Research Center connects you with mortgage lenders so you can compare quotes. We earn a commission if you proceed. This does not change the rates lenders show you. Read our partner vetting policy.

Found your lane? Get rate quotes for that specific product.

Explore options through Mortgage Research Center →Current rates as of May 17–20, 2026

Here is what national benchmarks and lender data show. Note the spread between Curinos and Bankrate methodologies — we cite both because they reflect different lender samples and assumptions.

| Product | Source | Rate (May 2026) |

|---|---|---|

| HELOC (variable, national average) | Curinos via Yahoo Finance, May 17, 2026 | 7.21% |

| HELOC (variable, national average) | Bankrate national survey, May 6, 2026 | 7.26% |

| Home equity loan (fixed, national average) | Curinos via Yahoo Finance, May 17, 2026 | 7.36% |

| Home equity loan (fixed, national average) | Bankrate national survey, May 6, 2026 | 8.03% |

| Federal Reserve H.15 bank prime loan rate | Federal Reserve, May 2026 | 6.75% |

| Federal funds rate target range | Federal Reserve / Moody's H.15 data, April 2026 | 3.50%–3.75% |

| Construction loan (range) | Published lender pages and aggregator data | ~7.0–9.0% |

| Renovation mortgage (HomeStyle, CHOICERenovation, 203(k)) | Published lender pages | ~6.8–7.5% |

| Cash-out refinance | Bankrate national 30-year refinance APR, May 2026 | ~6.78%; cash-out pricing varies by profile, LTV, fees |

What your monthly payment could actually look like

A HELOC and a home equity loan generate very different monthly payments on the same borrowed amount because HELOCs typically allow interest-only payments during the draw period. Here are two illustrative scenarios using a $200,000 borrowed amount at a 7.21% rate.

Principal is not being repaid; the balance remains $200,000 entering the repayment period.

Total interest over the 20-year repayment period (after a 10-year draw period of interest-only) is substantial.

Total interest paid over 20 years ≈ $183,338 (illustrative).

These are illustrative payment scenarios using current rate benchmarks. Actual payments depend on your specific rate, draw amount, repayment term, lender fees, taxes, insurance, and other variables. Confirm your specific numbers with the lender’s loan estimate.

Which loan keeps your existing first mortgage (and which doesn’t)

This is the single most consequential factor for homeowners with a pandemic-era mortgage and the one most competitor pages skip past too quickly.

| Loan type | Sits in | First mortgage survives? |

|---|---|---|

| HELOC | Second lien | ✓ Yes |

| Home equity loan | Second lien | ✓ Yes |

| Home equity investment (HEI) | Not a traditional loan; recorded interest varies | Usually yes, but mechanics and lien recording vary by provider |

| Cash-out refinance | Replaces first lien | ✗ No |

| Construction loan (one-time close C-to-P) | Often replaces first lien at conversion | Usually no |

| Construction loan (two-loan structure) | Construction loan + new permanent at conversion | Depends; often no |

| Fannie Mae HomeStyle Renovation | Replaces first lien | ✗ No |

| Freddie Mac CHOICERenovation | Replaces first lien | ✗ No |

| FHA 203(k) | Replaces first lien | ✗ No |

| Lender-branded ADU HELOC (e.g., Patelco) | Second lien | ✓ Yes |

| Lender-branded ADU construction/renovation product | Varies | Varies — ask the lender |

Worked example: keep the 3.25% first mortgage + HELOC vs cash-out refi

Suppose a homeowner has a $400,000 first mortgage at 3.25% with 25 years remaining and wants to borrow $200,000 for an ADU.

First mortgage payment unchanged. New HELOC interest on $200,000 at 7.21% ≈ $1,201/month during draw period (interest-only). The 3.25% rate on the original $400,000 is preserved.

New loan reprices the entire $400,000 portion from 3.25% to 6.95%. Annual extra interest cost on the original $400,000 alone is approximately $14,800 in year one (illustrative).

These calculations are illustrative and do not reflect taxes, insurance, mortgage insurance, points, or all fees. Confirm your specific numbers with a licensed loan officer.

Qualification floor — what each loan actually requires

| Requirement | HELOC | HEL | Construction | HomeStyle / CHOICEReno | FHA 203(k) | Cash-out refi |

|---|---|---|---|---|---|---|

| Min credit (best pricing) | 680+ | 680+ | 680–700+ | 680+ | 580+ | 680+ |

| Min credit (acceptable) | 620–640 | 620–640 | 660+ | 660+ | 500–579 (10% down) | 620–640 |

| Equity / down payment | 15–20%+ equity | 15–20%+ equity | 20–25% as-completed | Per program | 3.5% down (580+) | 15–25% remaining equity |

| Max DTI | ~43–45% | ~43–45% | ~43–45% | Per agency guide | Per FHA guide | ~43–50% |

Can ADU rental income help you qualify? The rules in 2026

Whether your future ADU rental income can help you qualify for the loan that builds the ADU is itself a deciding factor — and the rules changed multiple times in early 2026. The headline-friendly summary of “ADU rental income now counts” is much narrower in the actual agency text.

Fannie Mae — DU 12.1 (effective March 21, 2026)

Per Fannie Mae Selling Guide B3-3.8-01 (updated 10/08/2025) and Announcement SEL-2025-08, Fannie Mae allows rental income from an existing ADU to be considered for qualifying purposes, provided all of the following are met:

- The subject property is a one-unit principal residence.

- The transaction is purchase or limited cash-out refinance only (no standard cash-out).

- Rental income may be derived from only one ADU, even if multiple ADUs exist.

- ADU rental income used for qualifying is capped at 30% of the borrower’s total qualifying income.

Freddie Mac — CHOICERenovation (effective May 4, 2026)

Per Freddie Mac Bulletin 2026-1: for mortgages with application received dates on or after May 4, 2026, rental income from any unit included in the renovation project funded by the mortgage proceeds cannot be used to qualify the borrower. Only rental income from units not included in the renovation project may be considered.

FHA — Mortgagee Letter 2023-17

| Scenario | Rule |

|---|---|

| Standard FHA loan, property with existing ADU, no prior rental history | Mortgagee uses 75% of the lesser of fair market rent or the lease agreement |

| FHA Standard 203(k), adding a new ADU with no prior rental history | Mortgagee uses 50% of the lesser of fair market rent or the lease agreement |

| Cap (both scenarios) | ADU rental income used cannot exceed 30% of total monthly effective income |

| Cash-out refinance | ADU rental income is ineligible as effective income |

HELOC and home equity loan

HELOCs and home equity loans don’t have ADU-specific rental income rules. Qualification is based on your existing documented income, debts, and equity. If you need future ADU rental income to help you qualify, the FHA Standard 203(k) path (under ML 2023-17) is currently the most flexible mainstream option for building a new ADU, with the 50% rule and 30% cap.

Compliance note: these are illustrative examples, not guarantees of returns. Rental-income figures used for qualification are subject to lender, agency, and appraisal requirements. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

When your HELOC isn’t big enough: the after-renovation-value (ARV) path

If your HELOC pre-qualification came in below your ADU budget, you have three options that underwrite against the home’s future value instead of its current value:

Option 1 — An ARV HELOC

ARV HELOCs are second-lien lines of credit underwritten against your home’s after-completion appraisal. They preserve your existing first mortgage — the major advantage for homeowners holding low pandemic-era rates. RenoFi is the most prominent specialty provider; the company partners with credit unions to deliver renovation HELOCs underwritten against ARV. Check availability in your state before assuming this option is open to you — ARV HELOC availability is materially narrower than standard HELOC availability.Option 2 — A renovation mortgage

Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, and FHA 203(k) all underwrite against after-completion value. They replace your existing first mortgage but reach borrowing levels a current-value HELOC can’t.Option 3 — A construction-to-permanent loan

C-to-P loans use the as-completed appraisal to size the loan. They typically replace your existing first mortgage at conversion but work for ground-up detached ADU builds where the project scope is well-defined upfront.Rate type risk: variable HELOC vs fixed ADU loan

A standard HELOC is variable-rate. The rate is the prime rate plus a lender margin, and it adjusts when the prime rate moves. A fixed-rate ADU loan — home equity loan, fixed construction-to-perm, renovation mortgage, or cash-out refinance — locks the rate for the life of the loan.

Two considerations decide which rate type fits:

The right rate type depends less on your prediction of where rates are going and more on whether your budget can absorb payment changes during the 12–18 months of construction.

Speed to close, draw structure, and going over budget

The operational differences between products are sometimes more important than the rate differences:

| HELOC | Construction loan | Renovation mortgage | |

|---|---|---|---|

| Typical time to close | 2–6 weeks | 30–60 days | 45–60 days |

| Draw structure | Homeowner draws as needed | Lender inspections at foundation, framing, rough-in, finish | Renovation escrow with lender-serviced draws |

| Contractor approval required? | No | Yes — licensed builder, signed agreement | Yes — agency-approved contractor process |

| Over-budget mechanism | Credit-line increase (subject to re-underwriting) | Change order requires lender approval, may push project 30+ days | Change order requires lender + program approval |

| Inspection cadence | None lender-required | At each draw milestone | At each escrow disbursement |

Timeline ranges are typical industry benchmarks; actual close times vary by lender, file complexity, appraisal turnaround, and state. If your contractor is fast, experienced, and you have a clear scope, a HELOC’s flexibility usually wins. If your project is large or novel, the inspection cadence on a construction or renovation loan protects you from paying for work that hasn’t been done correctly.

Free ADU Starter Kit

We built a starter kit for homeowners moving from “comparing financing” to “talking to lenders.” It includes: a 14-document lender checklist, a draw-schedule template for construction loans, a contractor-bid comparison sheet, the 12-question lender script (below) as a printable PDF, and the complete ADU Loan vs HELOC decision framework.

Download the Free ADU Starter Kit →

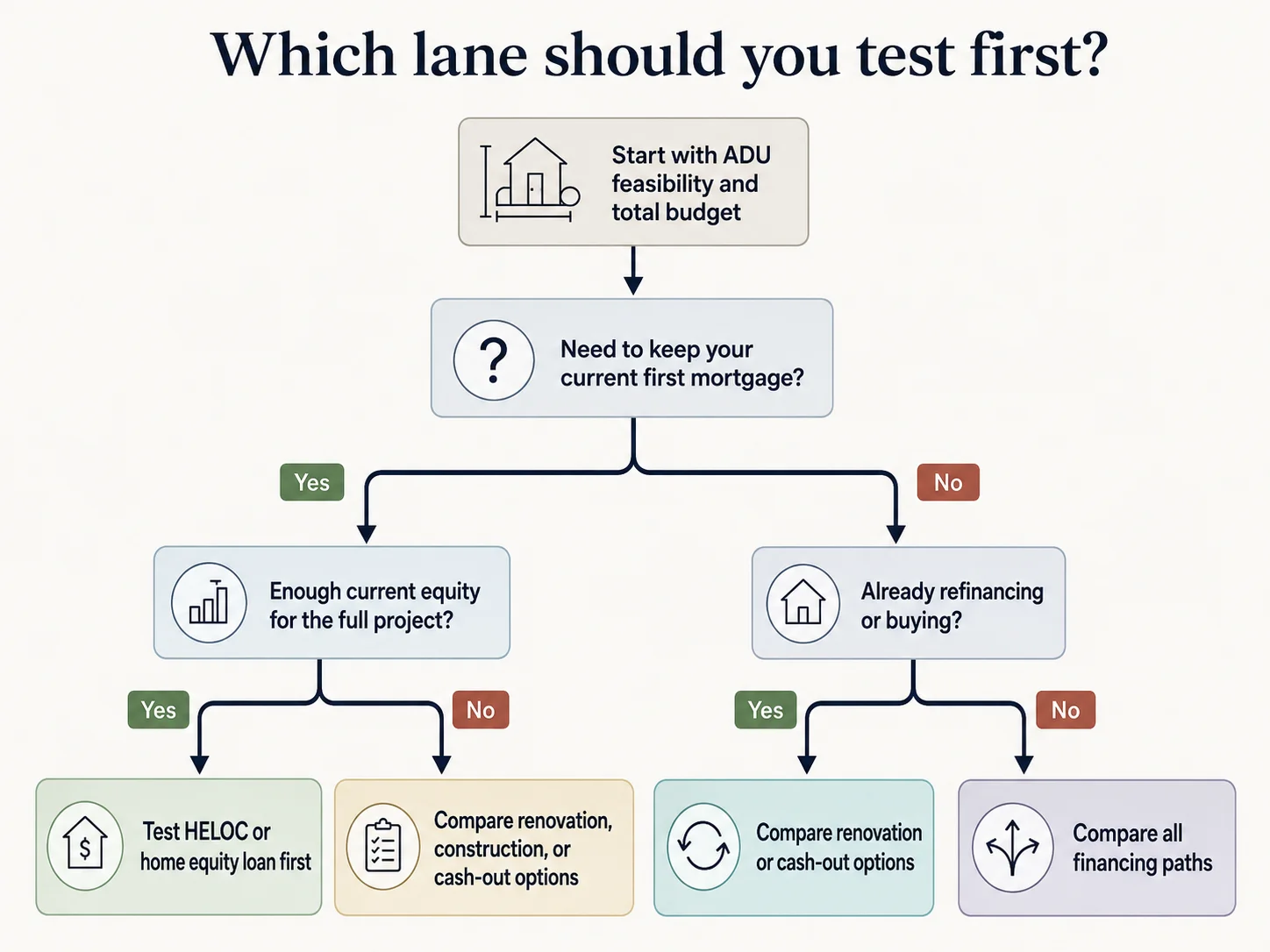

Pick your lane — decision matrix by situation

Most ADU homeowners fall into one of six patterns. Find yours and we’ll point you at the path to test first.

Pattern 1: Strong equity + low first mortgage + modest ADU budget

You have $200k+ of current home equity, a sub-5% first mortgage you want to keep, and an ADU budget under $200k.

- Test first: HELOC or home equity loan

- Alternative: Lender-branded ADU HELOC if available in your state

- Why: Your HELOC room covers the budget comfortably; the variable-rate risk is manageable on a balance you'll repay quickly; you preserve a valuable first mortgage.

Pattern 2: Strong equity + low first mortgage + larger ADU budget that still fits HELOC room

You have substantial equity, a low first mortgage, and an ADU budget between $200k and $400k that still fits inside your 80%-CLTV HELOC room.

- Test first: Home equity loan (for payment certainty) or HELOC (for flexibility)

- Alternative: Fixed-rate HELOC conversion if your lender offers it

- Why: Fixed payment on a larger balance during a 12–18 month build offers material peace of mind.

Pattern 3: Thin current equity + low first mortgage you want to keep

You have less than 15–20% existing equity, a sub-5% first mortgage worth preserving, and you need future-value underwriting to reach your ADU budget.

- Test first: ARV HELOC (if available in your state)

- Alternative: Reassess whether you can scale the project to fit current-equity HELOC room, or accept replacing the first mortgage with a renovation loan

- Why: ARV HELOC is the only mainstream path that uses after-completion value while preserving your existing first mortgage.

Pattern 4: Thin equity + market-rate first mortgage + larger ADU budget

You bought within the last few years, have limited equity, and your existing first mortgage is at or above current market rates.

- Test first: Fannie Mae HomeStyle Renovation or Freddie Mac CHOICERenovation

- Alternative: FHA 203(k) Standard if your credit profile makes FHA the better fit

- Why: Renovation mortgages use after-completion value, reach the needed borrowing capacity, and you're not protecting an existing rate.

- Watch out: If you're applying for CHOICERenovation on or after May 4, 2026, you cannot use future rental income from the unit funded by CHOICERenovation proceeds to qualify.

Pattern 5: Buying a home and planning an ADU at the same time

You're in the home-buying process and want to finance the ADU build in the same loan.

- Test first: Fannie Mae HomeStyle Renovation or FHA Standard 203(k)

- Alternative: Freddie Mac CHOICERenovation

- Why: Renovation mortgages explicitly bundle purchase and renovation into one loan that underwrites against post-renovation value. If you need ADU rental income to qualify, FHA 203(k) under ML 2023-17 allows 50% of projected rent (capped at 30% of effective income) for a new ADU.

Pattern 6: Home owned free and clear

No mortgage at all. Substantial equity by definition.

- Test first: HELOC or home equity loan

- Alternative: Cash-out from a new first mortgage if you want one consolidated payment

- Why: Without a first mortgage to preserve, the comparison reduces to flexibility (HELOC) vs payment certainty (home equity loan) vs structure (construction loan if you want lender oversight on draws).

You picked a lane — now confirm your lot is buildable. Most ADU projects fail in zoning, not in financing. Run a free property eligibility check and see what you can actually build before you sign any loan documents.

See What You Can Build → Get Your Free ADU ReportFree 60-second property check. Flags setback, lot coverage, height, owner-occupancy, and fire-zone disqualifiers.

Edge cases that change the answer

Honest tradeoffs and what could go wrong

Every financing path has a downside that doesn’t show up in the rate sheet.

What to ask lenders before choosing — the 12-question script

When you call lenders, don’t ask “what rate can I get?” first. Rate is a small part of total cost, and the first call is where you should be qualifying the lender for fit, not the other way around. Run this script:

- Do you finance the specific ADU type I'm building (detached, attached, garage conversion, JADU, prefab/modular)?

- Is this loan underwritten against my home's current value or after-completion value?

- What's the maximum combined loan-to-value (CLTV) you'll allow for this product in my state?

- What credit score gets your best pricing, and what's the floor for approval?

- What documentation do I need to provide upfront (income, equity, plans, contractor agreement)?

- Are funds disbursed in draws with inspections, or do I have homeowner-controlled access?

- Can you use rental income from this ADU to qualify me? Under which program (Fannie DU 12.1 existing-ADU rule, FHA 203(k) 50% rule, lender policy)?

- What happens to my existing first mortgage with this product?

- What's the all-in cost — interest rate, APR, origination fees, draw fees, annual fees, prepayment penalties, appraisal, inspection?

- If the project scope changes mid-build, what's your change-order process and timeline?

- Is this product available in my state and for my property type (primary, second home, investment)?

- What's your typical close-to-funding timeline for this loan type?

Get those answers in writing before you compare rates. A lender that can’t answer questions 2, 7, and 10 cleanly isn’t the right lender for an ADU project even if their rate looks best.

Is HELOC interest tax-deductible if I use it to build an ADU?

Per IRS Publication 936 (2025), interest on a home equity loan or HELOC is deductible only if the borrowed funds are used to buy, build, or substantially improve the home that secures the loan, subject to the $750,000 acquisition-debt cap ($375,000 if married filing separately). This restriction was made permanent by the One Big Beautiful Bill Act.

Building an ADU on the property securing the HELOC generally qualifies as “substantially improving” the home, which means HELOC interest used for ADU construction may be deductible — subject to itemization, the $750k cap, and IRS documentation requirements (Form 1098, contractor invoices, permits, receipts).

Key conditions:

- The HELOC must be secured by the home being improved.

- You must itemize deductions on Schedule A. For 2026, the standard deduction is $32,200 for joint filers and $16,100 for single filers.

- If only part of the HELOC is used for ADU construction (and part for other purposes), only the portion used to substantially improve the home generates deductible interest.

- The label doesn’t matter; how you use the money does. Home equity loans and HELOCs follow the same “buy, build, or substantially improve” test.

- Keep all documentation — contractor invoices, permits, lien waivers — to substantiate the deductible portion.

This is general information based on IRS Publication 936 (2025) and the IRS FAQ on home equity loan interest deductibility. Tax situations vary materially by individual; consult a qualified tax professional before claiming the deduction.

Frequently asked questions

- Can I use a HELOC to build an ADU?

- Yes, if your lender allows the use of proceeds for ADU construction and your current home equity is enough to cover the project plus contingency. The larger issue is sizing — many HELOC pre-qualifications come in below the actual ADU budget because the lender underwrites against your home's current value, not its after-completion value. Run the formula (home value × 80% − mortgage balance − liens) before assuming a HELOC will work.

- Is an ADU loan the same as a construction loan?

- Not exactly. "ADU loan" isn't a standardized national product; it usually refers to a construction loan, a renovation mortgage (Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, or FHA 203(k)), a lender-branded ADU product, or a cash-out refinance marketed for ADU buyers. When a lender or builder uses the phrase, ask which specific product they mean before signing anything.

- How much equity do I need for a HELOC to build an ADU?

- Most lenders require at least 15–20% equity in the home, with combined loan-to-value capped at 80% (some lenders go to 85% for top-tier borrowers). To estimate your HELOC room, calculate: home value × 80% − first mortgage balance − any other liens. Compare that to your ADU budget plus a 10–15% contingency.

- Do I have to refinance my mortgage to get an ADU loan?

- Sometimes. HELOCs, home equity loans, and home equity investments preserve your existing first mortgage. Cash-out refinances and renovation mortgages (HomeStyle, CHOICERenovation, 203(k)) replace it. Construction-to-permanent loans can go either way depending on structure. For homeowners with pandemic-era sub-5% mortgages, preserving the first mortgage is often the single most consequential factor in the decision.

- What credit score do I need for an ADU loan versus a HELOC?

- Best HELOC pricing typically requires 680+; some lenders accept down to 620 with rate penalties. Construction loans typically require 680+ with many lenders preferring 700+. Renovation mortgages follow agency floors (HomeStyle and CHOICERenovation: 620+; FHA 203(k): 580+ with 3.5% down, or 500–579 with 10% down). Lender overlays often add additional requirements.

- Can I use future ADU rental income to qualify for the loan?

- It depends on the program — and the rules are narrower than the marketing suggests. Fannie Mae's DU 12.1 rule allows rental income from an existing ADU on a one-unit principal residence, purchase or limited cash-out refi only, capped at 30% of qualifying income. It does not allow projected rent from an ADU you intend to build. Freddie Mac CHOICERenovation, for applications received on or after May 4, 2026, prohibits using rental income from any unit included in the renovation project funded by the mortgage proceeds. FHA Standard 203(k) under ML 2023-17 allows 50% of projected rent for a new ADU you're building, capped at 30% of total monthly effective income, and not on cash-out refinances. HELOCs and home equity loans don't have ADU-specific rental income rules — qualification is based on your existing documented income.

- What is an ARV HELOC and where can I get one?

- An after-renovation-value (ARV) HELOC is a second-lien line of credit underwritten against your home's after-completion appraisal instead of its current value. It preserves your existing first mortgage while reaching borrowing levels a standard HELOC can't. RenoFi is the most prominent specialty provider, partnering with credit unions to deliver ARV HELOCs. Availability varies by state and by partner credit union; check availability in your state.

- Is HELOC interest tax-deductible when used for an ADU?

- It may be. Per IRS Publication 936 (2025), interest on a HELOC secured by your home is deductible only when proceeds are used to buy, build, or substantially improve that home, subject to the $750,000 acquisition-debt cap ($375,000 if married filing separately). Building an ADU on the property generally qualifies as substantial improvement. You must itemize deductions to claim it. Consult a tax professional for your specific situation.

- How long does it take to close on a HELOC versus an ADU construction loan?

- HELOCs typically close in 2–6 weeks. Construction loans typically close in 30–60 days due to plan review, contractor approval, and detailed budget submission. Renovation mortgages typically close in 45–60 days. These are industry typical ranges; actual close times vary by lender, file complexity, appraisal turnaround, and state.

- What happens if my ADU project goes over budget?

- With a HELOC, you can request a credit-line increase (subject to re-underwriting and current equity); the 15–20% contingency layer in your budget reduces the likelihood you'll need one. With a construction or renovation loan, change orders typically require lender approval and may delay the project 30+ days. This is why we recommend building 15% contingency into the budget calculation rather than relying on a credit-line increase mid-build.

- Can I combine a HELOC with another loan to cover the full ADU cost?

- Sometimes. Some homeowners use a HELOC alongside personal savings, a smaller construction loan, or a HEI product. Lenders typically don't allow stacked second-position lines on the same property, but combining a HELOC with personal funds or a HEI is more common. Confirm with your HELOC lender that the combined financing structure doesn't breach the loan agreement.

- What's the difference between Fannie Mae HomeStyle and Freddie Mac CHOICERenovation?

- Both are conventional renovation mortgages that bundle the home purchase or refinance with renovation costs and underwrite against after-completion value. HomeStyle allows ADU construction when zoning permits. CHOICERenovation, per Freddie Mac Bulletin 2026-1, bars use of rental income from any unit included in the renovation project funded by the mortgage proceeds for applications received on or after May 4, 2026. Your specific situation (credit, equity, occupancy, project scope, rental-income needs) determines which program is the better fit.

Methodology and sources

We built this guide by reconciling primary sources rather than paraphrasing competitor pages. Every numerical claim and regulatory citation in this article has a verifiable source listed below.

Rate data and benchmarks (verified May 17–20, 2026)

- Curinos national HELOC and home equity loan averages (via Yahoo Finance, May 17, 2026)

- Bankrate national HELOC and home equity loan survey (May 6, 2026)

- Bankrate national 30-year refinance APR (May 2026)

- Federal Reserve H.15 Selected Interest Rates, bank prime loan rate at 6.75% (May 2026)

- Federal funds rate target range 3.50%–3.75% (April 2026 per Moody’s H.15 data)

- Construction and renovation loan rate ranges from publicly published lender pages and aggregator data verified May 2026

Agency and regulatory sources

- Fannie Mae Selling Guide B3-3.8-01, Rental Income (updated 10/08/2025)

- Fannie Mae Announcement SEL-2025-08

- Fannie Mae Desktop Underwriter (DU) version 12.1 release (weekend of March 21, 2026)

- Fannie Mae HomeStyle Renovation product page (singlefamily.fanniemae.com)

- Freddie Mac Bulletin 2026-1 (CHOICERenovation rental income rule effective May 4, 2026)

- Freddie Mac CHOICERenovation product page (sf.freddiemac.com)

- HUD Mortgagee Letter 2023-17 (FHA ADU rental income, property eligibility, appraisal protocols)

- HUD 203(k) program guidance (Limited 203(k) and Standard 203(k))

- IRS Publication 936 (2025), Home Mortgage Interest Deduction

- Federal Trade Commission, “Home Equity Loans and Home Equity Lines of Credit” consumer guidance

- Consumer Financial Protection Bureau HELOC consumer booklet (12 CFR §1026.40(e))

- Consumer Financial Protection Bureau, “Issue Spotlight: Home Equity Contracts Market Overview” (2025)

ADU cost benchmarks

- Angi national ADU cost reference

- SnapADU San Diego cost analysis

- cali-adu.com Los Angeles ADU cost breakdown

- Boston.gov ADU planning guide

Independent analysis

- Urban Institute, “To Increase the Housing Supply, Focus on ADU Financing” (April 2024)

- Federal Housing Finance Agency research on mortgage rate lock-in effect

Last updated: May 20, 2026 · Last verified: May 20, 2026 · Next review: June 20, 2026 (or within 7 days of any FOMC rate change)

This page was written and reviewed by The Dwelling Index editorial team. We are not a lender, broker, or builder. We do not accept payment to influence editorial conclusions. The information in this guide is general and educational; it is not lender-specific advice, legal advice, or tax advice.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU ReportReady to compare lender rates for your specific loan type?

Compare Lender Rates via Mortgage Research Center →Affiliate link — verify availability in your state.

Disclosures

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder.

Rates, qualification requirements, product terms, and regulatory rules on this page are sourced from primary lenders, federal agencies, and published benchmarks as of the verification date listed. They are not guarantees of the rate or terms you will be offered. Actual loan terms depend on your credit, equity, income, lender, and state. Consult a qualified lender and financial advisor before making financing decisions.