Hard Money Loan for ADU: When It Works, When It Traps You, and How to Exit in 2026

Last updated: · Last verified: May 20, 2026 · By The Dwelling Index Editorial Team — an independent research resource covering ADU financing, costs, and regulations.

The bottom line.

A hard money loan for ADU construction is a short-term, asset-based loan from a private lender — typically priced at 9.5%–12.5% interest plus 1–3 points, capped at roughly 65%–75% of after-repair value (ARV), with 6–24 month terms and funding in 5–14 days. It fits two situations well: an investor building or rehabbing on a non-owner-occupied property with a verified DSCR refinance or sale exit, and a buyer who must close on a property with strong ADU upside before slower financing can clear. For an owner-occupied primary residence where proceeds are primarily for personal, family, or household use, the loan is generally classified as consumer-purpose credit under federal consumer-mortgage rules — which restricts the number of lenders willing to write it, lengthens funding, and is usually a wrong fit anyway. A construction loan, cash-out refinance, HELOC, or renovation loan almost always costs less and protects you better.

Who this is for: homeowners, ADU investors, and small builders anywhere in the United States researching whether to use hard money to fund an ADU.

One key number to anchor the decision: every percentage point of rate on a $250,000 ADU loan held for 12 months is $2,500 in interest. The gap between a 7.5% construction loan and an 11% hard money loan on that same balance is $8,750 in one year — before points, extension fees, or refinance costs.

Next step (below): the free Property Eligibility Check confirms whether your lot can host an ADU and matches you to the financing lane that fits your equity, income, and timeline.

See What You Can Build → Get Your Free ADU Property & Financing Report.

Confirm what your lot can legally support before you borrow against it. Free, 60 seconds, no obligation.

Run the Property Eligibility Check →What we verified for this page

Sources cross-checked on May 20, 2026.

- 2026 hard money rate ranges (9.5%–12.5%) confirmed across Gauntlet Funding (May 2026), North Coast Financial (May 2026), Gelt Financial (Feb 2026), and Capital Direct Funding (April 2026).

- Mortgage benchmarks from the Freddie Mac PMMS: 30-year FRM 6.36%, 15-year FRM 5.71% as of May 14, 2026.

- Published ADU hard money transaction data from Mortgage Vintage public deal records (2022–2025) — a representative public-source sample, used as illustrative examples, not as quotes or endorsements.

- Dodd-Frank framework and consumer-purpose classification verified against CFPB Regulation Z and its §1026.43 ATR/QM rule.

- DTI thresholds from the Fannie Mae Selling Guide §B3-6-02 (manual DTI 45% maximum; DU casefile up to 50%).

- State and federal ADU finance programs verified against primary sources: CalHFA, MassHousing, San Diego Housing Commission, and the USDA Federal Register rulemaking (comment period through June 1, 2026).

Editorial framing of "fit" — when hard money is right and wrong — is our editorial conclusion based on the verified data above. Your situation may differ. The Property Eligibility Check maps your specifics.

Should you even consider hard money for your ADU?

| Your situation | Hard money fit | What to do first |

|---|---|---|

| Investor building or rehabbing ADUs on a non-owner-occupied rental, with a planned DSCR refinance | ✅ Strong fit | Pre-qualify the DSCR refi before signing the bridge |

| Buying a property at auction or in a competitive market with strong ADU upside | ✅ Strong fit | Confirm permits are achievable; close fast, then refi |

| Homeowner with 20%+ equity, W-2 income, and 700+ credit, building an ADU on a primary residence | ❌ Wrong fit | Run a construction loan or cash-out refi instead |

| Homeowner with little equity who recently bought the home and wants to build an ADU | ❌ Wrong fit | Use a renovation loan that values the home at after-construction value |

| Self-employed or non-QM income, primary residence, willing to pay a premium for speed | ⚠️ Last-resort fit | Only via a licensed consumer-purpose hard money lender; verify the refi exit first |

| Fix-and-flip + ADU addition by an investor on a 6–12 month timeline | ✅ Strong fit | Confirm the after-repair appraisal supports your exit |

| Family ADU for parents/aging-in-place on the home you live in | ❌ Wrong fit | HELOC, specialty ADU HELOC, or renovation loan |

If your row says "Wrong fit," keep reading — we show you exactly which alternative to use and how the numbers compare. If your row says "Strong fit," skip ahead to What does a hard money loan for ADU cost in 2026? and How do you pay off a hard money ADU loan after construction?

Is a hard money loan for ADU better than a HELOC, construction loan, or renovation loan?

We assembled this from four 2026 hard money rate trackers (Gauntlet, North Coast Financial, Gelt, Capital Direct Funding), the Freddie Mac PMMS, Bankrate national averages, and published rate sheets from Patelco, Meriwest, KeyPoint, Lighthouse, JVM Lending, and CrossCountry Mortgage. Rates and terms are illustrative 2026 ranges. Your actual quote depends on credit, equity, lien position, property type, and market.

| Financing tool | Typical 2026 rate | Points / fees | Max leverage | Term | Time to fund | Owner-occ OK | ADU rent counted | Best for |

|---|---|---|---|---|---|---|---|---|

| Hard money — 1st lien, business-purpose | 9.5%–12.5% | 1–3 points | 65–75% ARV | 6–24 mo | 5–14 days | Rarely (consumer-purpose only via licensed lender) | Sometimes | Investors, near-completion bridges |

| Hard money — 2nd lien | 12%–14% | 1–3 points | 50–65% CLTV | 6–24 mo | 7–21 days | Same as above | Sometimes | Preserving a low first mortgage |

| Construction-to-permanent loan | ~7.5%–9% | 0.5–1 point | Up to 80% of as-completed value | 12 mo build → 30 yr | 30–60 days | Yes | Yes (Fannie/Freddie, with caps) | Ground-up or significant ADU builds |

| Cash-out refinance | ~7%–8% | 0.5–1 point | Up to 80% of current value | 15–30 yr | 30–45 days | Yes | N/A | High-equity owners with a higher-than-market existing rate |

| HELOC (standard) | ~7.25%–9% variable | $700–$3,000 setup | Up to 85% CLTV | 10 yr draw + 20 yr repay | 15–30 days | Yes | Some lenders | Equity-rich homeowners preserving a low first mortgage |

| Specialty ADU HELOC (e.g., Patelco CA) | 8.25%–9.00% APR | Setup fees | Up to 125% as-is value and 90% post-construction value | 2-yr draw + 20-yr repay | 15–30 days | Yes | Yes | Low-equity CA homeowners on a primary residence |

| Renovation loan (Fannie HomeStyle, Freddie ChoiceRenovation, FHA 203(k)) | ~7.5%–8.5% | 0.5–1 point | Up to ~95%+ of as-completed value | 30 yr | 45–60 days | Yes | Yes (with caps; 30% of qualifying income on Fannie one-unit ADUs) | Low-equity owners; future-value underwriting |

| DSCR loan | ~8%–10% | 1–2 points | Up to 75–80% LTV | 30 yr | 21–30 days | No (investment only) | Yes (qualifies on rent) | Investor exit after build |

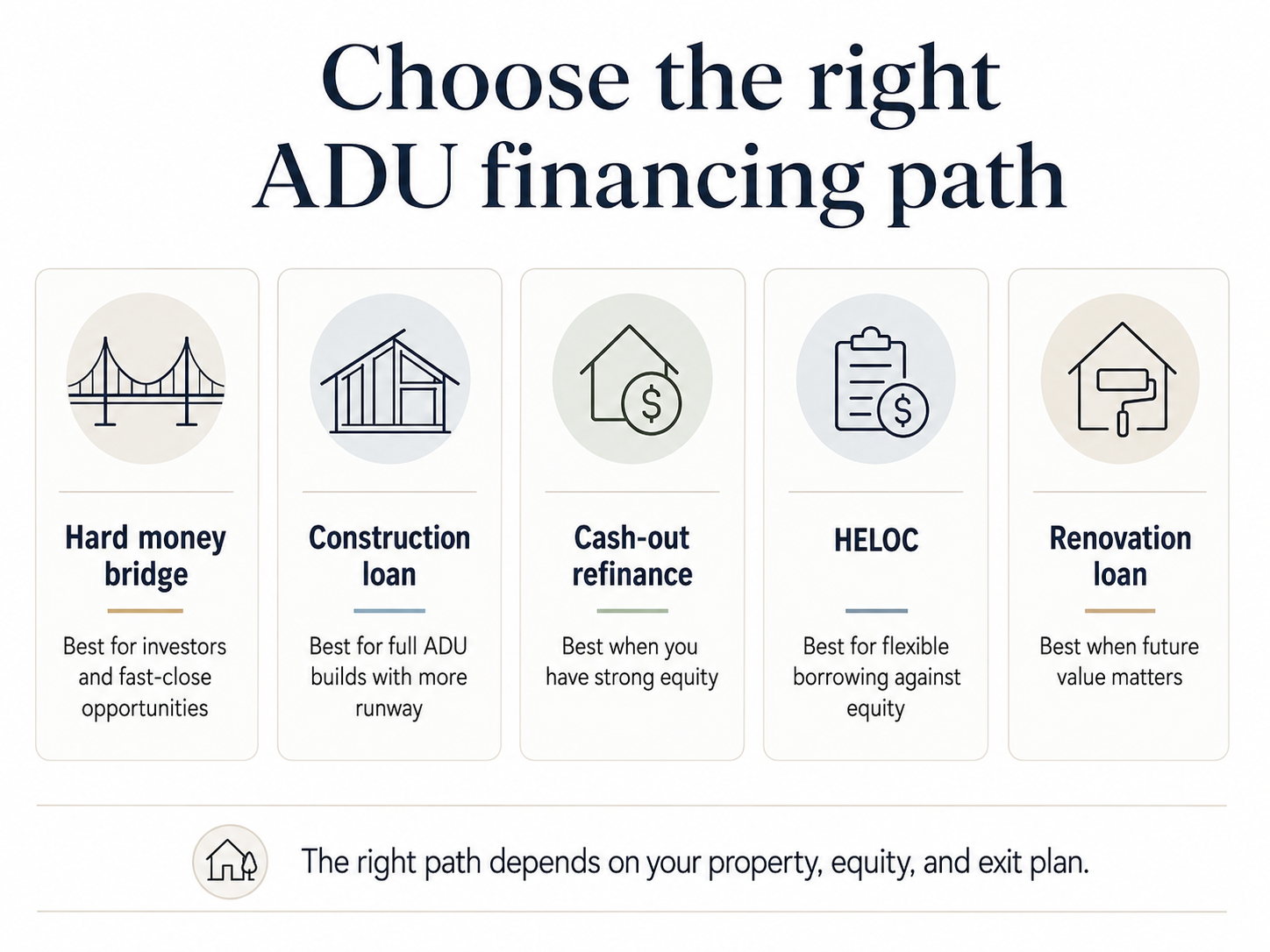

Choose the right ADU financing path — 2026 rate comparison across eight tools.

What a hard money loan actually is — and what it means for an ADU build

Why it's called "hard" money

The "hard" refers to the hard asset — the property — that secures the loan, not the rate or the difficulty of getting one. Gelt Financial, a 36-year direct lender that has funded more than 10,500 hard money loans, explains it the same way.

Hard money sits inside a broader category called private money. Capital Direct Funding's 2026 fix-and-flip financing guide distinguishes them: hard money is typically asset-based, short-term, and priced off a rate card; private money is a relationship-based category that can include longer terms and creative structures. In 2026, hard money commonly sits between 8.5% and 11.2% on the lowest end and 12.5%+ on the high end. Origination fees average 1 to 3 points.

A quick decision map for ADU borrowers

| Borrower profile | Where hard money sits | Right next move |

|---|---|---|

| Investor — rental property, ADU added for cashflow | Most common fit; business-purpose loan, DSCR refi exit | Vet lenders against the 12-question checklist below |

| Owner-occupied family ADU on primary residence | Rare and expensive; consumer-purpose rules slow the close | Run the alternatives section first |

| Acquisition bridge — buying a property with ADU upside | Strong fit when a 30-day conventional close would lose the deal | Pre-arrange the take-out refi before you sign |

Why investors specifically reach for hard money on an ADU

- Speed. Gelt Financial reports closing hard money loans in 3–5 days, versus 30–45 days for traditional financing.

- Underwriting flexibility. Most hard money lenders weigh property value far more than personal credit. Borrowers with 600+ scores can qualify; the property and the exit drive the decision.

- Lien-position flexibility. Hard money lenders routinely write second-position loans behind a low-rate first mortgage, something most banks won't do. For an ADU, this matters when an investor wants to keep a 3% legacy mortgage in place and stack a short-term bridge on top.

Where hard money stops being useful for ADUs

It is not designed for borrowers who plan to keep the property forever, can qualify for a bank loan, and don't need to close in two weeks. That's most ADU builders. Most homeowners researching "hard money loan for ADU" land here because a builder said it was the fastest path, a bank said no, or they assumed it was the only product that lends without significant current equity. Each of those reasons has a better answer than hard money, and we walk through them below.

What does a hard money loan for ADU cost in 2026?

The 2026 rate environment has been kinder to private lending than to conventional mortgages. Gauntlet Funding's 2026 outlook puts hard money in a 9.5% to 12.5% band. North Coast Financial agrees: first-position hard money rates are 9.5%–12%, second-position 12%–14%. Capital Direct Funding describes 2026 as a "rate compression" period — the lowest hard money rates have come down meaningfully from 2023–2024 double-digit floors, especially for seasoned investors with documented track records.

What "points" actually cost in dollars

One point equals 1% of the loan amount, paid upfront at closing. On a $200,000 ADU hard money loan with 2 points, that's $4,000 in fees before you owe the first dollar of interest. Most hard money loans charge 1–3 points; a few will go higher for stretch leverage or thin exits.

By comparison, a typical bank construction loan in 2026 carries 0.5–1 point in origination. The point gap alone — $4,000 to $6,000 on a $200K loan — is one reason the cost-of-capital math so often favors conventional paths.

Three worked-dollar examples — what your money actually does

Illustrative examples, not guarantees of available loan terms, returns, or specific lender offers. Actual results depend on lender underwriting, market conditions, construction costs, and regulatory approvals.

| Scenario | Loan amount | Rate | Points | Term | Monthly interest-only | Total interest | Points cost | True cost of capital |

|---|---|---|---|---|---|---|---|---|

| A — Investor, BRRRR ADU build, 1st lien at 70% ARV | $200,000 | 10.5% | 2 | 12 mo | $1,750 | $21,000 | $4,000 | $25,000 |

| B — Investor, fix-and-flip + ADU addition | $350,000 | 11.5% | 3 | 9 mo | $3,354 | $30,188 (9 mo) | $10,500 | $40,688 |

| C — Homeowner using a 2nd-lien consumer-purpose hard money loan | $150,000 | 12.0% | 2.5 | 24 mo | $1,500 | $36,000 (full term) | $3,750 | $39,750 over 24 mo |

Examples assume interest-only payments, no prepayment penalty, and a clean exit at maturity.

What drives your rate up or down

- LTV / ARV. Lower leverage almost always wins a lower rate. A 65% ARV deal will price below a 75% ARV deal at the same lender.

- Lien position. Second-position rates run 200–400 basis points above first-position.

- Borrower track record. Repeat investors with documented successful exits routinely access the lower end. Gauntlet Funding's 2026 outlook puts this explicitly: "your track record of successful projects is now a direct negotiating asset."

- Property condition and location. Stabilized properties in strong markets price below distressed properties or rural locations.

- Business-purpose vs. consumer-purpose. Consumer-purpose loans on a primary residence carry full federal consumer-mortgage compliance and tend to price higher and fund slower.

- Construction risk. Ground-up new construction is priced above renovations or completion loans on already-permitted projects.

Why a 12% short-term loan can still pencil out

A $200,000 hard money loan at 12.5% for 9 months costs roughly $18,750 in interest plus $4,000 in points = $22,750. If that loan unlocks an ADU build that adds $250,000 of value and $24,000/year in projected gross rental income, the math can work for the right investor over a multi-year hold. Important caveat: gross rent is not net operating income — vacancy, operating expenses, property taxes, insurance, maintenance, management, and refinance costs all reduce what flows to your pocket. For a homeowner with no rental thesis, the financing premium is pure friction.

The published ADU hard money deal tracker — what real ADU private money loans actually look like

| Location & date | Project use | Loan structure | Leverage and controls | Exit strategy | Lesson |

|---|---|---|---|---|---|

| Duarte, LA County, CA — Jan 2025 | Add two ADUs to convert rental to four detached units | $345,000 2nd trust deed at 12.50% | 53.59% CLTV; $300,000 funds control; 18-month term; 6 months prepaid + guaranteed interest | DSCR refinance | Investor exit, controlled construction funds, ample interest reserve |

| Fontana, CA — April 2024 | Complete a fully permitted 460 sq ft ADU | $105,000 at 11.99%; 2nd TD | 60% CLTV; $84,650 funds control; 18-month term; ~3-month GC completion estimate | Conventional refinance | Near-completion, fully permitted = strongest fit |

| Palmdale, CA — Oct 2022 | Build 730 sq ft ADU behind existing home | $234,750 2nd TD at 10.50% | 65% LTV on ARV; $206,000 funds control; 7-month GC completion estimate | Conventional refinance | ARV/appraisal support is everything; exit depends on post-build value |

| Costa Mesa, CA — Sept 2023 | Fund another ADU on an SFR + JADU + ADU property | $500,000 2nd TD at 11.75% | 64% CLTV; $200,000 funds control; experienced investor-developer | Not fully specified in public listing | Investor experience and existing rental income meaningfully change terms |

| Los Angeles, CA — April 2024 | Reconfigure duplex and add two fully permitted ADUs | $600,000 2nd TD at 12.00% | 61.52% CLTV; 100% of proceeds into funds control | Truncated in public listing | Controlled construction funds dominate ADU hard money structures |

Source: Mortgage Vintage public transaction pages (2022–2025), accessed May 2026. Used as illustrative published examples, not as offers, endorsements, or rate quotes for any current or future loan.

Five patterns from the deal tracker

- They're all second trust deeds. Hard money for ADU construction usually sits behind a first mortgage the borrower wants to preserve. That's part of what makes the math hard to escape — you're stacking 11%–12% money on top of a 4%–6% legacy mortgage rate.

- Leverage is conservative. Despite "12% hard money" headlines, the actual loan-to-value ratios run 53.59% to 65% in this sample. The lender isn't lending against thin air.

- Funds control is the norm. All five loans use funds control — money held by the lender or a third party and released against verified construction milestones.

- Exits are pre-baked. Three of the five cases specify the planned exit (DSCR refi or conventional refi) in the listing. The lender wants the exit identified before the loan funds, not figured out afterward.

- Projects are permitted or near-permitted. Hard money lenders on ADU deals heavily prefer permitted projects. "Conceptual" ADUs without permits are far harder to finance.

This tells you that hard money for ADUs in real life is closer to moderate-leverage second-position investor financing than to the headline "fast cash" pitch.

Why is hard money different for an owner-occupied ADU?

Business-purpose vs. consumer-purpose — the line that decides everything

- Business-purpose loan: Property is a rental, fix-and-flip, or held by an LLC. The ADU income is the point. Loan funds finance business activities. → Hard money is widely available and lenders compete on terms.

- Consumer-purpose loan: Property is the borrower's primary residence. ADU is for family use, aging-in-place housing, or even a rental that supports the household budget (this can still be consumer-purpose). → Hard money is restricted; only a small number of licensed lenders will write it.

The CFPB's commentary makes clear: just labeling the loan "business-purpose" doesn't make it one. Classification is determined by facts — who occupies the property, how the proceeds are used, and whether the borrower's intent and conduct align with a business purpose.

The ATR/QM rule and what it means for consumers

A covered consumer-purpose mortgage generally triggers federal consumer-mortgage compliance, including the Ability-to-Repay / Qualified Mortgage (ATR/QM) requirements when applicable. Under CFPB Regulation Z §1026.43, temporary or bridge loans of 12 months or less, construction phases of 12 months or less, HELOCs, and housing-finance-agency program loans can be exempt from certain ATR/QM provisions. So a consumer-purpose owner-occupied loan isn't automatically pulled into the full ATR/QM regime — but it does sit inside a tighter compliance frame than business-purpose lending.

The prepayment-penalty diagnostic

Federal rules restrict most prepayment penalties on consumer-purpose primary-residence loans. Business-purpose hard money loans frequently include 6–12 month minimum interest periods or prepayment penalties.

The "we'll just call it business-purpose" trap

Some lenders will offer to write your loan as business-purpose even though you're the owner-occupant, to skip the consumer-purpose process. Scott B. Umstead, P.A., a Florida real-estate attorney, summarizes the exposure: if a loan is for a consumer purpose and a lender misclassifies it, both lender and borrower face enforcement, rescission, refund of borrower costs, restitution, and the borrower may even gain an affirmative defense in foreclosure. It is not a workaround. It is a future legal problem dressed up as a closing convenience.

How long owner-occupied loans actually take to close

North Coast Financial reports that owner-occupied private money loans on a primary residence "typically take about 2.5 weeks" — meaningfully slower than the 5-day business-purpose hard money pitch, because the lender has to verify income, debts, and ability-to-repay under federal rules. TRID timing requirements also apply, including a 3-day Closing Disclosure waiting period before consummation.

Hard money for ADU construction most commonly funds investor-held, non-owner-occupied detached units with a clear DSCR refinance exit.

When hard money is the right tool for an ADU — and when it isn't

Strong-fit scenario one: investor building with a verified DSCR exit

This is the sweet spot. The deal mirrors the Duarte case from our deal tracker: a rental property, ADUs added to multiply rentable units, and a DSCR refinance lined up against post-stabilization rent. Hard money buys you speed and underwriting flexibility a bank can't match, and the higher cost is recovered through faster project execution and rent ramp-up — assuming your refinance qualifies on the projected DSCR and the appraisal supports the loan amount.

Strong-fit scenario two: the acquisition bridge with ADU upside

You found a property where adding an ADU dramatically improves value or cashflow. A conventional 30-day close means a cash buyer beats you. A 5-to-14-day hard money close lets you win the property. You then refinance into a construction-to-permanent loan, DSCR loan, or cash-out refi once you own it.

What has to be true before this works:

- You've confirmed the property can legally host the ADU (zoning, setbacks, utilities).

- Your take-out lender has already issued a term sheet or pre-qualification, contingent on acquisition.

- Your timeline math works: hard money close (5–14 days) → permits and construction (4–9 months) → refinance (30–45 days). Hard money term should be 12–18 months with extension provisions in writing.

- You have a cash reserve for the carry — interest-only payments accrue from day one.

The five scenarios where hard money is the wrong tool

- Owner-occupied homeowner with 20%+ equity and W-2 income. A cash-out refinance at ~7% or a construction-to-permanent loan at ~7.5%–9% is cheaper and easier. Consumer-purpose hard money is slower than the business-purpose marketing line.

- Recent buyer with little equity, building an ADU on a primary residence. The right answer is a renovation loan — Fannie Mae HomeStyle, Freddie Mac ChoiceRenovation, or FHA 203(k) — which underwrites against the home's as-completed value after the ADU is built. The Terner Center for Housing Innovation specifically calls renovation loans "well-suited for homeowners without significant equity, but underused" — the Center's research found only 6.3% of ADU owners used them.

- Self-employed or non-QM income on a primary residence. A bank statement loan, a non-QM lender, or a DSCR loan (if the ADU will be rented) usually beats consumer-purpose hard money on rate and term.

- Family ADU for parents or aging-in-place. A short-term balloon loan with a 12–24 month maturity creates the exact opposite of long-term stability. A HELOC, specialty ADU HELOC, or renovation loan matches the project's actual time horizon.

- No real exit strategy. The American Association of Private Lenders notes that loans without a viable exit are a common decline reason. If you can't write down on paper what loan will replace this loan, you don't have an exit — you have a hope.

The biggest mistake homeowners make

A $200,000 ADU loan at 11% hard money for 12 months costs $22,000 in interest plus ~$4,000 in points = $26,000. The same $200,000 at 7.5% on a Fannie HomeStyle Renovation loan over the same 12 months costs $15,000 in interest plus ~$1,500 in points = $16,500. The gap is $9,500 in 12 months — and the renovation loan keeps amortizing for 30 years instead of demanding a balloon at month 12.

Compare Mortgage-Backed ADU Financing Paths →

Talk with a licensed mortgage advisor about cash-out refinance, construction loan, HELOC, and renovation loan options before you sign anything. Approval depends on lender underwriting and is not guaranteed.

Get a free financing path consultation →Affiliate link — see disclosure above. Read our full affiliate disclosure.

The better alternatives most homeowners qualify for (and which one fits you)

Cash-out refinance

Best for owners with 20%+ equity who have a higher-than-market existing rate. Rates around 7%–8% (30-year fixed, May 2026). You retire the first mortgage and take the difference in cash. The ADU build proceeds from the equity you pull out. Downside: you lose your existing rate if it's below market.

Construction-to-permanent loan

A single loan that funds construction in draws, then converts automatically to a 30-year mortgage at completion. Rates ~7.5%–9%. Underwritten against as-completed value, so it works for borrowers with modest current equity. The best one-loan solution for significant ADU builds.

HELOC and specialty ADU HELOC

A standard HELOC draws up to 85% CLTV at ~7.25%–9% variable and keeps your existing first mortgage untouched. For homeowners with less current equity, specialty ADU HELOCs like Patelco's ADU Line of Credit (California) lend up to 125% of as-is property value at 8.25%–9.00% APR — removing the equity gap that pushes some homeowners toward hard money.

Renovation loan (Fannie HomeStyle / Freddie ChoiceRenovation / FHA 203(k))

These programs underwrite against the home's as-completed value — what the property will be worth after the ADU is built. That means a borrower with little current equity can still qualify for a meaningful loan. JVM Lending puts it clearly: "Building an ADU without home equity is possible with both Fannie Mae's Homestyle Renovation Loan and Freddie Mac's ChoiceRenovation Loan. This is because you can appraise your property 'subject to completion,' as if the ADU is already constructed." Rates run ~7.5%–8.5% on a 30-year term. This is the product most homeowners researching hard money actually need.

State and local ADU finance programs to check before hard money

California — CalHFA ADU Grant Program

CalHFA offers up to $40,000 in predevelopment cost assistance (design, permits, site prep) for income-qualified homeowners building ADUs on their primary residence. Not a loan — this is a grant that does not require repayment if you meet program conditions. Always verify current availability and income limits at calhfa.ca.gov/adu. Read our full guide to ADU grants and what's actually fundable in 2026.

California — SDHC ADU Finance Program (San Diego)

- Up to $250,000 construction-to-permanent loan.

- 1% fixed interest rate during construction, converting to a 4% fixed-rate permanent loan (15-year amortization, due in 30) up to 75% LTV.

- Eligibility: income up to $236,600 (150% of San Diego AMI), detached single-family residence in the City of San Diego, main home owner-occupied, minimum 680 FICO, $2,500 application fee, 1% owner contribution of construction loan amount.

- 7-year affordability covenant: rent must remain affordable to tenants at ≤80% AMI.

This is materially cheaper than any private option for qualifying owners — and significantly more restrictive. The 7-year affordability covenant rules it out for owners planning market-rate rent. Verify current details at sdhc.org.

Massachusetts — MassHousing ADU Loan Program

Launched March 17, 2026. Fixed-rate second mortgages structured as construction-to-permanent: up to $250,000 for detached ADUs and $150,000 for attached ADUs, at 5.25% interest with a 20-year amortization, paired with additional zero-interest deferred-repayment financing to lower the effective borrowing cost (MassHousing official program page). Income limits up to 135% of area median income. This is the largest dedicated state ADU finance launch of 2026 and Massachusetts homeowners in the income window should compare this against any private option first.

Federal — USDA SFHGLP rulemaking

USDA's Rural Housing Service has proposed amending the Single Family Housing Guaranteed Loan Program to allow financing properties with income-producing ADUs and to count ADU rental income. The public comment period closes June 1, 2026. This is a proposed rule, not an active loan feature yet. If finalized, it would meaningfully expand USDA-backed ADU financing in rural and small-town markets.

Note: state and local program eligibility, funding status, and rates change. Always verify current details at the program's official site (CalHFA.ca.gov, MassHousing.com, SDHC.org, Federal Register) before relying on the numbers above. Last verified May 20, 2026.

Get organized before you talk to any lender.

The free ADU Starter Kit includes: the financing path decision tree, our 12-question lender vetting checklist, a one-page worked-numbers comparison, and the state-program cheat sheet. Emailed once, no spam.

Download the Free ADU Starter Kit →How do you pay off a hard money ADU loan after construction?

The hard money exit plan: secure the take-out lender first, then close the bridge.

The two clean exits

DSCR refinance. A Debt Service Coverage Ratio loan qualifies the borrower on the property's rental income, not personal income. Investor-friendly. Rates run roughly 8%–10% in May 2026 with 30-year terms. This is the natural exit for a hard money investor build — once the ADU is leased and you can show 1.0+ DSCR, the refi qualifies.

Conventional cash-out refinance. Once construction is complete and the appraisal reflects the ADU's added value, an owner-occupied homeowner refinances into a 30-year fixed at the prevailing rate (6.36% as of May 14, 2026 for the 30-year FRM, 5.71% for the 15-year). The new loan retires the hard money balance.

The DTI math homeowners forget

Even if the appraisal supports the new loan amount, conventional cash-out refinance still requires you pass a debt-to-income (DTI) test. Per the Fannie Mae Selling Guide §B3-6-02, a loan is not eligible for delivery if recalculated DTI exceeds 45% for manual underwriting or 50% for a DU casefile; Freddie Mac generally treats mortgages with monthly DTI above 45% as ineligible for sale. Run that math before you take hard money. If your DTI doesn't pencil at the refi, you have no exit.

Stress-test your exit before signing

| Exit plan | What has to be true before you close the hard money loan |

|---|---|

| Conventional refinance | Projected appraisal supports the new loan; your income and DTI qualify at refi |

| Cash-out refinance | You accept losing your existing first mortgage rate; CLTV at or below 80% |

| DSCR refinance | Projected rent meets the lender's DSCR threshold (typically 1.00–1.25) |

| HELOC or home equity loan after completion | Post-construction equity supports the line |

| Sale | Market value supports payoff plus selling costs (5–8% friction); buyer demand is real |

| ⛔ No exit yet | Do not close the hard money loan. Stop here. |

When the exit goes wrong

Hard money lenders generally allow extensions — for an additional 1–3 points and sometimes a rate bump. If extensions run out and you can't refinance or sell, the loan goes into default, the lender can foreclose, and you can lose the property.

A BiggerPockets commenter warned about exactly this on a 2024 ADU thread: their post-construction appraisal came in at "property purchase price + $20,000" — far below the ADU's build cost — and they cautioned others against assuming hard-money-to-refinance math will pencil if a HELOC alternative is on the table.

The protection is simple: secure the exit before the bridge, not after. A pre-qualified DSCR term sheet, a conditional construction-to-permanent commitment, or written HELOC approval changes the risk profile of the entire project.

Run the exit before the bridge.

Use the Property Eligibility Check to see if your lot supports the project — and to map exit-financing options against your real numbers before you sign anything.

Get Your Free ADU Property & Financing Report →How hard money ADU loans are actually structured

Lien position

A first trust deed sits in first position on the property; the lender gets paid first in a foreclosure or sale. A second trust deed sits behind an existing first mortgage. The five published Mortgage Vintage cases we reviewed were all second trust deeds, reflecting the most common ADU hard money structure: investor preserves a low-rate first mortgage and takes a second-position bridge to fund the ADU build.

LTV, CLTV, and ARV — the leverage vocabulary

- LTV (loan-to-value): the new loan as a percent of the property's current value.

- CLTV (combined loan-to-value): all loans secured by the property as a percent of current value.

- ARV (after-repair value): the property's projected value once the ADU is finished. Hard money lenders frequently lend up to 65%–75% of ARV rather than current value — which is what lets them lend on properties with low current equity.

Funds control and draw schedules

Funds control means a third party (often the lender or an escrow firm) holds loan proceeds and releases them against verified construction milestones. All five Mortgage Vintage cases used funds control, and the dollars in control were significant — $84,650 in Fontana, $206,000 in Palmdale, $300,000 in Duarte.

Why this matters: it protects the lender from a borrower spending construction money before completing the project, and it protects you from paying a general contractor for work that isn't done. It also adds process — every draw requires documentation, inspection, and lender approval.

Interest-only payments, points, and balloon maturity

Most hard money loans require interest-only monthly payments during the term, with the entire principal due as a balloon at maturity. Some lenders also prepay months of interest at closing — six months of guaranteed interest reserves, for example — meaning that interest is deducted from the loan proceeds even if you pay off the loan early. The Duarte case explicitly listed "6 months prepaid and guaranteed interest" in its public structure.

Terms to get in writing before you sign

| Term to confirm | Question to ask the lender |

|---|---|

| Note rate | Fixed for the entire term, or variable? |

| Points | Charged upfront, financed into the loan, or deducted from proceeds? |

| Draws | Who controls funds and what triggers each release? |

| Extension | What rate/points apply if construction runs past maturity? |

| Exit | What evidence of refinance or sale do you require before funding? |

| Lien | First, second, or cross-collateralized? |

| Prepay | Is there a minimum interest period or prepayment penalty? |

| Default | What's the default rate, and how soon does it trigger? |

The hard money lender vetting checklist for ADU projects

The 12-question vetting checklist

- What is your NMLS license number, and which states are you licensed for consumer-purpose loans? Verify the answer on NMLS Consumer Access.

- Will you classify my loan as business-purpose or consumer-purpose, and on what basis? If they reflexively want to call your owner-occupied loan business-purpose, stop the conversation.

- What is your maximum LTV, and is it calculated on current value, as-completed value, or ARV? This single number drives everything else.

- What is your rate today for my exact scenario, and what's the rate on day one after extension? Extension pricing is where lenders make their money on deals that slip.

- What are the points and all origination, closing, and junk fees in dollars — not percentages — on my exact loan amount? Gauntlet Funding's 2026 outlook specifically flags transparency on closing fees as a 2026 vetting concern.

- Do you charge a prepayment penalty? On a consumer-purpose primary-residence loan, this is the regulatory red flag we described above.

- What's your average actual close time on a loan like mine — not the "as fast as 5 days" marketing line?

- What's the draw schedule and inspection cadence during construction?

- Who is the actual lender — you, or a capital partner you're brokering to? Some "lenders" are brokers and add a layer to your cost.

- What is your default rate over the last 24 months, and how do you handle extensions or defaults?

- Will you talk to my exit lender directly to confirm the refi take-out is real? Lenders who say yes are taking your exit seriously. Lenders who refuse are signaling they don't.

- Can I see three references from borrowers who closed an ADU project with you in the last 12 months?

Red flags

- Pressure to sign before you've read the full term sheet

- Vague or evasive answers about regulatory licensing

- Prepayment penalties on consumer-purpose primary-residence loans

- "Don't worry, we'll classify it as business-purpose" coaching from the lender

- Junk fees that appear at closing but weren't on the original term sheet

- No NMLS number, no verifiable references, no public transaction history

- Loan documents emailed without an attorney review window

Honest tradeoffs: the real downsides of using hard money for an ADU

The damaging admission, owned plainly: the ADU industry is full of pages telling you hard money is fast and flexible. Few tell you what happens when it goes wrong. Perfectly viable ADU projects derail when the refinance appraisal comes in under expectation, rates move against the borrower during construction, or DTI math that worked on paper fails at the closing table.

Compounding interest-only carry

A $250,000 hard money loan at 11% interest-only costs $2,292 per month in interest alone, plus $5,000–$7,500 in points upfront. Over 18 months, that's roughly $41,250 in interest plus points — and you still owe the full $250,000 at maturity.

Extension fees

When construction takes longer than expected (and ADU construction often does — utility hookups, inspector availability, supply chain), the lender will extend you for additional points (typically 1–2 points) and sometimes a rate increase. Two extensions can add $5,000–$10,000 to your cost on a $250,000 loan.

The refinance squeeze

Mortgage rates can move 50–100 basis points during a 12-month construction window. If you locked your project around a refi at 7% and rates are at 8% when construction finishes, the new monthly payment on the refi can blow up your DTI or your projected cashflow on the rental. This is real risk, not speculation.

What you'll need before you apply for hard money on an ADU

- Permit or plan-check status with the city

- Site plan and ADU drawings (architect or designer)

- Contractor's state license number and proof of insurance

- A fixed-scope, fixed-price bid from a licensed contractor

- Construction timeline with inspection milestones

- Current mortgage statement showing payoff and lien priority

- Property tax statement

- Title commitment with no surprises

- Realistic rent estimate or signed lease assumptions (for DSCR exits)

- Refinance pre-qualification or DSCR pre-check letter from your exit lender

- Cash reserve for construction overruns (a 10–15% buffer is conventional)

- A written Exit Plan A and Exit Plan B

HCS Equity, a California bridge-loan lender writing on ADUs, summarizes the same essential thing: bridge-loan borrowers should provide "a comprehensive project plan, including timeline and budget" before approaching a lender. The complete file is what gets you to the lower end of the rate range.

Should homeowners use hard money for a family ADU?

- Family-use ADU. The emotional driver is housing security for a loved one. A 12–18 month balloon undoes that security. Use a 30-year fixed renovation loan, a specialty ADU HELOC with a 22-year total horizon (Patelco's structure), or a cash-out refinance. Match the loan's time horizon to the project's actual life span.

- Rental-use ADU (homeowner with one tenant). Projected rent can support an exit, but projected rent isn't guaranteed. A renovation loan or specialty ADU HELOC absorbs rental fluctuation better than a hard money balloon. Rental figures are illustrative examples, not guarantees of returns; actual rent depends on local market conditions, ADU type, and regulatory approvals.

- Investor-use ADU (multiple rentals). This is the use case where hard money pencils. It is not the same use case as a homeowner thinking of their backyard as an investment.

See What You Can Build → Get Your Free ADU Property & Financing Report.

Confirm what your lot can legally support, then choose the financing path. Free, 60 seconds.

Run the Property Eligibility Check →What to do next if hard money looks too risky

| Your real constraint | Best lane | Why it fits | Internal next step |

|---|---|---|---|

| "Can my lot even host an ADU?" | Feasibility check | A loan can't fix a property that fails zoning, setbacks, utilities, or fire-zone constraints | Run the Property Eligibility Check |

| "I have little equity in the home I just bought" | Renovation loan (Fannie HomeStyle / Freddie ChoiceRenovation / FHA 203(k)) | Values the home on as-completed value, not current value | Compare financing paths |

| "I have a 3% mortgage I don't want to lose" | HELOC or specialty ADU HELOC (Patelco in CA) | Keeps the first mortgage in place | See our ADU financing category |

| "Banks won't take my non-W-2 income" | DSCR loan (if ADU will be rented); bank statement loan otherwise | Qualifies on rent, not personal income | Compare financing paths |

| "I want one loan for build + take-out" | Construction-to-permanent loan | Single close; converts to 30-year at completion | Compare financing paths |

| "I live in San Diego and qualify by income/credit" | SDHC ADU Finance Program | 1% construction → 4% permanent, up to $250K (with 7-year affordability covenant) | SDHC official page |

| "I live in Massachusetts and qualify by income" | MassHousing ADU Loan | 5.25% second mortgage + zero-interest deferred component, up to $250K detached / $150K attached | MassHousing official page |

Start with what your property can legally support — then choose the financing path.

See What You Can Build → Get Your Free ADU Property & Financing Report.

Run the Property Eligibility Check →Frequently asked questions

Can you get a hard money loan to build an ADU?

Yes. A hard money loan can fund an ADU when the lender accepts the property, the project plan, the lien position, the leverage, and the exit strategy. The strongest fit is an investor or small builder working on a non-owner-occupied property with a defined DSCR refinance or sale exit inside 24 months. For owner-occupied primary residences where proceeds are primarily for personal, family, or household use, the loan is generally classified as consumer-purpose credit, which restricts the number of lenders willing to write it and lengthens funding.

Can I use hard money to buy a property and then add an ADU?

Yes — this is one of the genuinely strong-fit cases. An acquisition bridge funded by hard money lets you close in 5–14 days, win a property a conventional buyer would lose, then refinance into a construction-to-permanent loan, DSCR loan, or cash-out refi after closing. Before signing, confirm (1) the property can legally host the ADU, (2) the take-out lender has issued a contingent term sheet, (3) your hard money term is 12–18 months with extension provisions in writing, and (4) you have cash reserves to carry the interest-only payments through construction and refinance.

What happens if the ADU does not appraise for enough after construction?

This is the most common deal-breaker. If the post-construction appraisal falls short of the projected as-completed value, the conventional cash-out refi or DSCR refi may not support a loan large enough to pay off the hard money balance. Your options at that point: bring cash to close the refi, take a smaller refi and pay the difference, extend the hard money loan (and absorb the extension fees), sell the property, or — worst case — default. The protection is to run conservative appraisal assumptions before signing the bridge, ideally pulling realistic comps with a local agent who has sold ADU-equipped properties recently.

Is hard money the same as an ADU construction loan?

No. A construction loan describes how funds are disbursed during a construction project — typically in draws against milestones. Hard money describes a source of capital — private, non-bank, asset-based. Some hard money loans fund construction; many construction loans are funded by banks, credit unions, or agency-backed renovation programs (Fannie HomeStyle, Freddie ChoiceRenovation, FHA 203(k)).

How expensive is a hard money loan for an ADU?

Published ADU hard money cases showed note/yield figures ranging from 10.50% to 12.50%, with 1–3 points in origination fees, on loan amounts from $105,000 to $600,000. Industry-aggregate 2026 ranges put first-position hard money at 9.5%–12.5% and second-position at 12%–14%. These are illustrative ranges, not current offers.

What credit score do you need for a hard money ADU loan?

Hard money lenders weigh property value and exit viability more than credit. Borrowers with 600+ scores can often qualify; the rate moves with the score. Borrowers planning a conventional refinance exit also need to qualify for that refi — typically 620–680+ depending on the loan program.

How fast can you close a hard money ADU loan?

Business-purpose hard money loans on non-owner-occupied properties typically close in 5–14 days. Gelt Financial reports closing hard money loans in 3–5 days on the fast end; Capital Direct Funding cites elite boutique firms at 5–7 days. Consumer-purpose owner-occupied hard money on a primary residence typically takes about 2.5 weeks per North Coast Financial, because the lender must verify income, debts, and ability-to-repay under federal rules, and TRID waiting periods apply.

Can you count ADU rental income on a hard money loan or refinance?

Yes — with caps and program rules. On a DSCR loan, qualification is based directly on rent. Per the Fannie Mae Selling Guide §B3-3.8-01, rental income from an ADU on a one-unit principal residence may be used in qualification up to 30% of total qualifying income, subject to documentation requirements. Freddie Mac permits ADU rental income in specified cases including ChoiceRenovation scenarios, subject to Guide rules. On most hard money loans, the lender cares about asset value and exit, not your personal income.

What's the difference between hard money and private money for an ADU?

Hard money is typically asset-based, short-term, and priced off a published rate card. Private money is a broader category that can include longer-term, more relationship-driven, more creatively structured loans from individuals, family offices, or specialty firms. In 2026, the spread has compressed and the most sophisticated investors often use both — hard money for straightforward acquisitions requiring speed, private lending for complex projects requiring creative structuring.

Is a HELOC cheaper than hard money for an ADU?

Almost always yes, if you qualify. May 2026 HELOC averages run around 7.26% (Bankrate national) versus 9.5%–12.5%+ for hard money. Specialty ADU HELOCs like Patelco's run 8.25%–9.00% APR with leverage up to 125% as-is value, which removes the equity gap that pushes some homeowners toward hard money in the first place. HELOCs also keep your existing low-rate first mortgage intact.

Can I get hard money with no equity?

For an investor on a non-owner-occupied property, yes — hard money is underwritten against ARV, so current equity isn't the limit. For a homeowner with little equity on a primary residence, hard money is rarely the right tool. A renovation loan that values the home at its after-construction value is purpose-built for exactly that situation.

Do hard money loans for ADUs have prepayment penalties?

Federal rules restrict most prepayment penalties on consumer-purpose primary-residence loans. Business-purpose investor loans frequently include a minimum interest period (commonly 6 months) or a fixed prepayment fee in the first 6–12 months. On a consumer-purpose primary-residence loan, the presence of a prepayment penalty is a major compliance red flag — though not by itself conclusive proof of classification, since classification is fact-driven.

What happens if my ADU is delayed?

Most hard money lenders offer extensions for an additional 1–2 points and sometimes a rate increase. Two consecutive extensions can add $5,000–$10,000 to your total cost on a $250,000 loan. If you exhaust extensions and can't refinance or sell, the loan matures and the lender can begin foreclosure. The protection is to negotiate an extension provision into your original term sheet, not to scramble for one when construction is already late.

Do hard money lenders require permits for an ADU?

Most lenders strongly prefer permitted or near-permit-ready projects. All five published Mortgage Vintage ADU cases reviewed were either fully permitted or substantially permitted. Some lenders will fund earlier, but this typically prices higher and adds documentation requirements. No loan fixes a property that legally can't host an ADU — feasibility is the gate that opens every other door.

Is a hard money ADU loan a good fit for an owner-occupied home?

Usually no. Owner-occupied consumer-purpose hard money is restricted, is offered by only a small number of licensed lenders, and the short-term balloon structure is a poor fit for a long-term family-housing project. A specialty ADU HELOC, renovation loan, construction-to-permanent loan, or cash-out refinance almost always wins on cost, risk, and time-horizon match.

What is funds control on a hard money ADU loan?

Funds control is a third-party-managed disbursement structure where loan proceeds are held by the lender or an escrow firm and released against verified construction milestones (typically slab, framing, mechanical rough-in, drywall, certificate of occupancy). It protects the lender from a borrower spending construction funds before completing the project, and it protects you from paying contractors for work that hasn't been done. All five published Mortgage Vintage ADU cases used funds control.

Methodology: how we built this guide

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder. We do not accept payment to influence rankings or recommendations.

Search scope. We pulled and cross-referenced material on the queries "hard money loan for ADU," "ADU hard money loan," "ADU bridge loan," "private money ADU," "DADU hard money loan," and the closest-adjacent regulatory terms (Dodd-Frank consumer-purpose, Regulation Z, TILA, NMLS).

Data extraction. From the five published Mortgage Vintage transactions, we recorded loan amount, published note rate or yield, CLTV / LTV / ARV ratio, funds control amount, ADU type, geography, and exit strategy. Selection criteria: ADU-specific use, public loan amount, public rate/yield, public leverage metric, funds-control detail, and exit/ADU context. Used as illustrative published examples — not as offers, current rate quotes, or endorsements.

Rate ranges. We cross-referenced four 2026 hard money rate trackers (Gauntlet Funding, North Coast Financial, Gelt Financial, Capital Direct Funding) and reported the resulting range. For conventional alternatives, we used the Freddie Mac PMMS (May 14, 2026) and published rate sheets from Patelco, Meriwest, KeyPoint, Lighthouse, JVM Lending, Save Financial, and CrossCountry Mortgage.

Regulatory framework. Federal consumer-mortgage rules, CFPB Regulation Z, §1026.43 ATR/QM, and the consumer-purpose vs. business-purpose distinction were verified against CFPB primary sources, plus practitioner-side coverage by Marquee Funding Group, North Coast Financial, Berlin Patten Ebling, Scott B. Umstead P.A., Fortra Law, and Brad Loans.

Agency rules. Fannie Mae Selling Guide §B3-3.8-01 (ADU rental income), §B3-6-02 (DTI ratios), and Freddie Mac ADU resources.

Forum and voice-of-customer use. BiggerPockets threads were referenced to understand homeowner and investor language and decision friction — never as proof for legal, financial, zoning, or construction claims.

Exclusions. No unsourced lender rankings. No affiliate-driven "best lender" sorting. No fake reviews. No guaranteed rates. No invented testimonials.

Limitations. Published ADU hard money transaction data skews California and investor-heavy. Actual terms vary by state, lender, lien position, credit, equity, and project. The 2026 rate environment is changing; we update this page quarterly for rate data and immediately if regulatory news breaks.

Last verified: May 20, 2026. | Next scheduled review: August 2026.

Disclosures

Editorial disclosure. The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Read the full affiliate disclosure and editorial methodology.

Financial disclaimer. This article is educational information, not legal, tax, or financial advice. Hard money loans, mortgages, construction loans, and ADU financing programs involve significant risk, including the possible loss of your property if you cannot repay. Rates, terms, and program availability change frequently. Before signing any loan, consult a licensed mortgage professional, an attorney in your state, and verify all terms in writing with the lender.

Illustrative-example disclaimer. Worked-dollar examples, rate ranges, rental income figures, and ROI references in this article are illustrative only. They are not guarantees of returns, available loan terms, or specific lender offers. Actual results depend on local market conditions, construction costs, financing terms, lender underwriting, and regulatory approvals.

Not sure where to start?

See what's possible at your address — get your free ADU report in 60 seconds.

Run the Property Eligibility Check →