ADU Financing in Texas: 7 Ways to Pay for a Backyard Home, Garage Apartment, or Casita

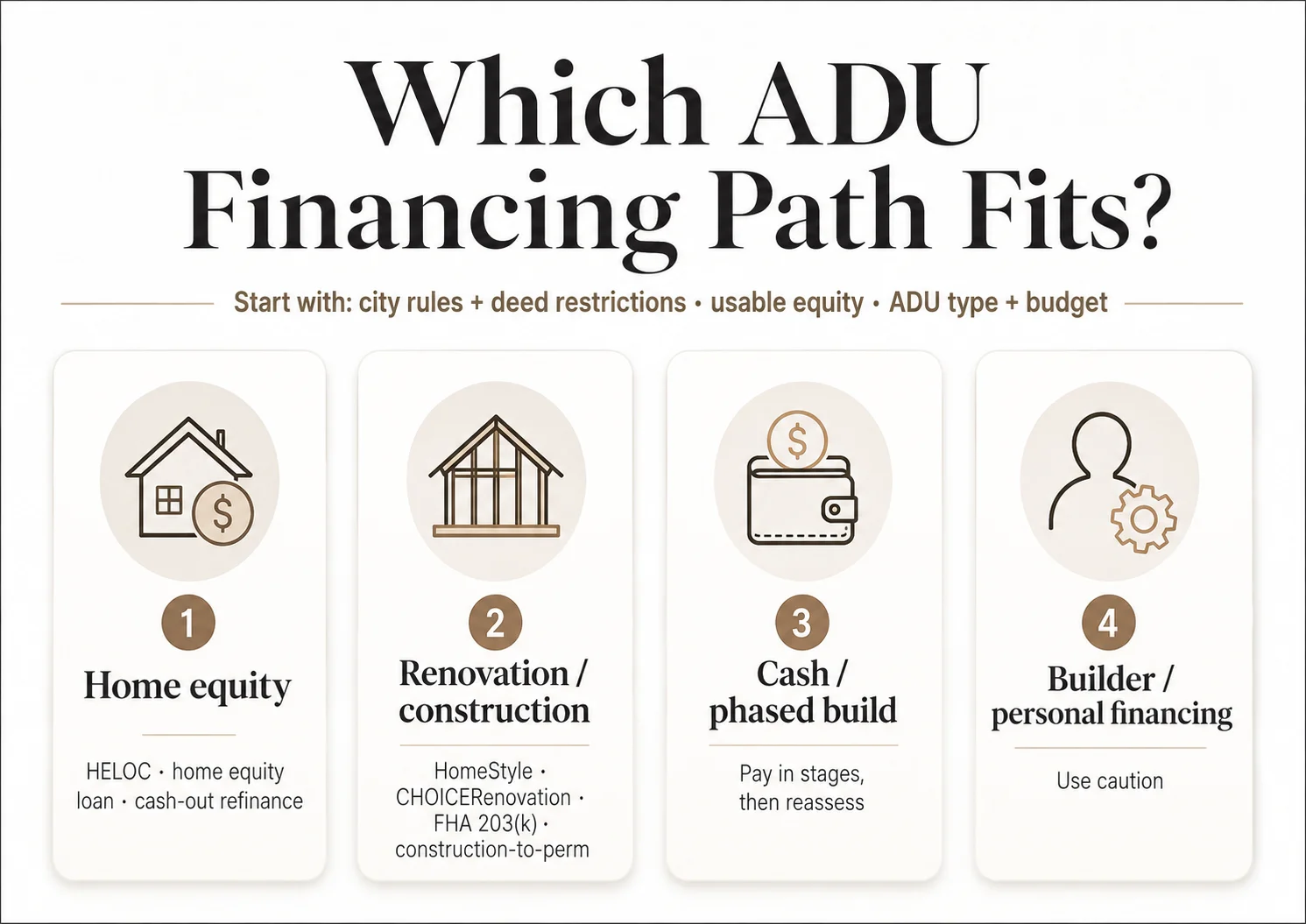

ADU financing in Texas usually comes down to four lanes: home equity (a HELOC, a home equity loan, or a cash-out refinance), a renovation or construction mortgage that lends against the home’s finished value, cash or a phased build, or higher-risk builder/personal financing. For most homeowners with equity who want to keep their current first mortgage, a home equity loan or HELOC is the first lane to test. For homeowners without enough equity today, a renovation loan (Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, or FHA 203(k)) or a construction-to-permanent loan is usually the better fit, because those products qualify you against what the property will be worth after the ADU is built.

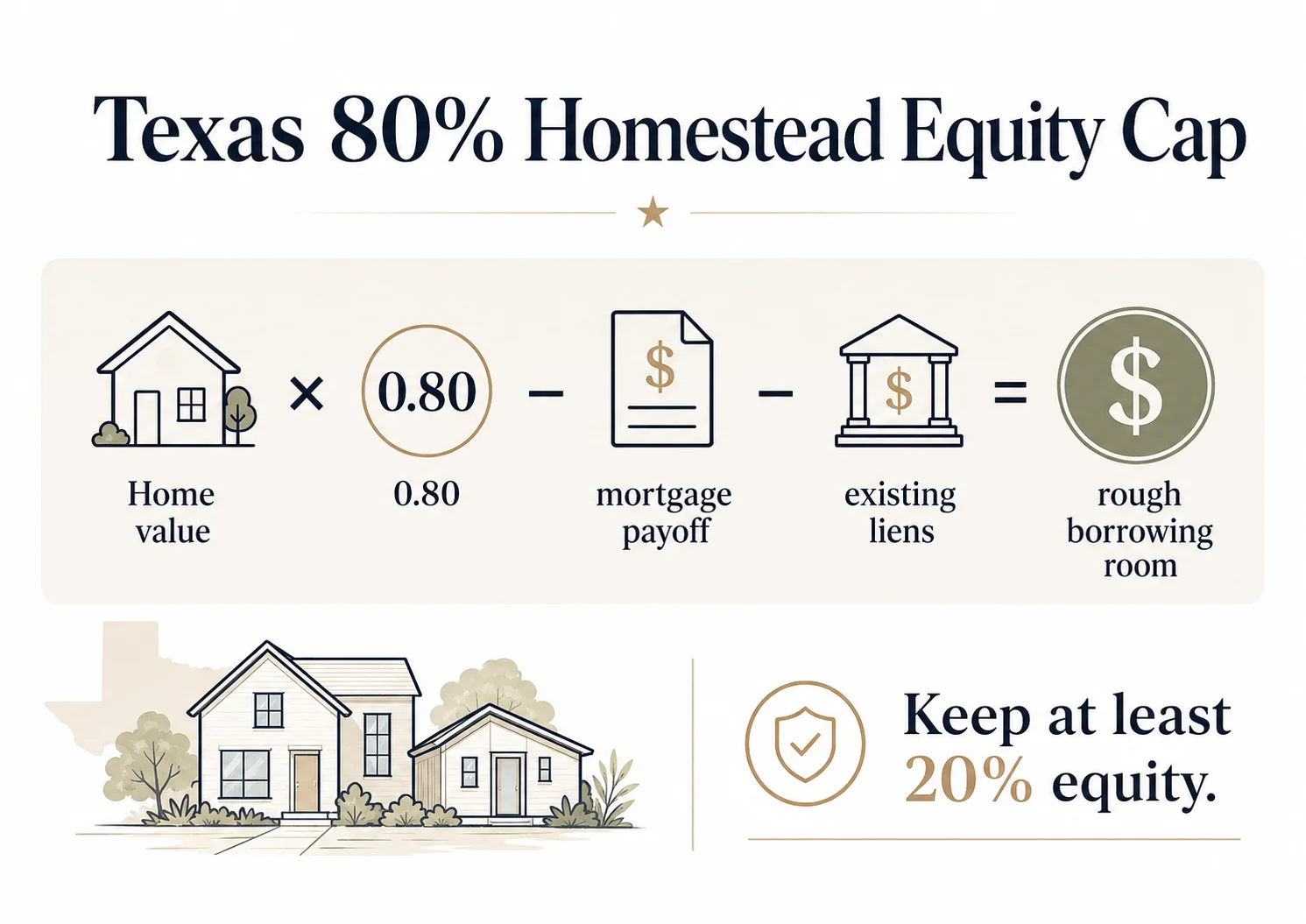

Here’s the part almost every other guide skips: in Texas, the first question is not “which lender is cheapest?” — it’s whether your city, your deed restrictions, and the Texas Constitution’s 80% homestead-equity cap make the project financeable at all. The number to memorize: under Section 50(a)(6) of the Texas Constitution, the total of all loans against your homestead can’t exceed 80% of its appraised value, so you must keep at least 20% equity. Plan on a Texas ADU costing roughly $125,000–$350,000 for a detached build, with garage conversions and small prefab units coming in lower. Start by confirming your city allows the ADU, estimate your usable equity, then pick a lane.

Not sure if your lot even qualifies? See what’s possible at your address — get your free ADU report.

A fair warning before we go further. “ADU financing in Texas” is rarely one clean product. You can have plenty of income and still be blocked — by a local ordinance, a deed restriction, an HOA, the Texas home-equity cap, or a lender that won’t count your projected rent. That’s the hard part. The good news: every one of those is knowable before you spend a dollar on plans, and this guide walks you through each gate in order. Texas can be an excellent ADU state. You just have to clear the checkpoints in the right sequence.

ADU financing in Texas: which path should you test first?

The right financing path depends on three things: whether your city allows the ADU, how much usable equity you have under Texas’s 80% cap, and whether you need to borrow against the home’s finished value. Homeowners with strong equity who want to keep a low first-mortgage rate typically start with a HELOC or home equity loan. Homeowners who need more than current equity supports typically start with a renovation or construction-to-permanent loan. Use the table below to find your starting lane, then read the full breakdown for your situation further down the page.

| Your situation | Path to test first | Main Texas watch-out | Your next move |

|---|---|---|---|

| Strong equity, want to keep your current first mortgage | HELOC or home equity loan | 80% combined-lien cap; 12-day waiting period; documentation | Estimate usable equity before applying |

| You need more than your current equity supports | Renovation loan or construction-to-permanent loan | More paperwork, draw schedules, contractor review | Get plans/bid + city feasibility first |

| Buying or refinancing a home and adding an ADU | HomeStyle, CHOICERenovation, FHA 203(k), or construction-to-perm | Appraisal "subject to completion," rent-counting rules, legal ADU status | Confirm lender program fit |

| You can fund design/permitting but not the full build | Cash + phased plan, then mortgage-backed financing | Phasing can cost more if sequenced poorly | Use a feasibility report before committing |

| A builder is offering "easy" financing | Treat as higher-risk until terms are reviewed | May hinge on a future refinance or short payoff window | Compare against mortgage-backed options |

| Income-qualified and building in San Antonio | City Casita forgivable-loan incentive, stacked with your own financing | Reimbursed at completion; you must show proof of funds/financing first | Check eligibility at sa.gov/ADU |

Financing options are presented as educational lanes, not lender rankings. Availability and terms depend on your profile, your property, and lender review.

Check your address, ADU type, and likely next steps before you talk to a lender.

Our free Feasibility Engine checks city rules, lot eligibility, and returns a personalized ADU report in about 60 seconds. No phone call, no commitment.

See What You Can Build → Get Your Free ADU ReportWhat is the best way to finance an ADU in Texas?

The best Texas ADU financing path depends on three gates: local permission, usable equity, and whether a lender can underwrite the project as a home-equity loan, a renovation loan, a construction loan, or a purchase/refinance mortgage. For many homeowners the first lane to test is a HELOC or home equity loan if they have enough equity; for those who don’t, a renovation or construction-to-permanent loan that lends against the home’s completed value is usually the stronger fit. There is no single “best” loan — there’s a best loan for your equity position, your city, and your build type.

Let’s define the four lanes plainly, because the search results are full of jargon that hides simple ideas. We’ve added the Texas-specific catch for each, since that’s what a national “7 ways to finance an ADU” article will never tell you.

The four financing lanes — and the Texas catch in each

Lane 1 — Home equity

You borrow against equity you already have. Three products live here. A home equity loan is a fixed lump sum at a fixed rate as a second lien (it sits behind your first mortgage). A HELOC (home equity line of credit) is a revolving line you draw from as needed, usually at a variable rate — you can borrow, repay, and reborrow during the draw period. A cash-out refinance replaces your entire first mortgage with a larger one and hands you the difference in cash. The Texas catch: all three are capped at 80% combined loan-to-value on your homestead, carry a 12-day waiting period, and — critically — you can’t hold a home equity loan or HELOC at the same time as an active Texas cash-out refinance. We decode all of this below.

Lane 2 — Renovation or construction mortgage

These products lend against the home’s after-completion value — what it will be worth once the ADU exists. That’s the magic for homeowners who don’t have enough equity today. Fannie Mae’s HomeStyle Renovation, Freddie Mac’s CHOICERenovation, FHA’s 203(k), and construction-to-permanent loans all live here. The Texas catch: the ADU generally has to be legally permissible for the appraisal and the loan to work, so city feasibility comes first.

Lane 3 — Cash or phased build

You pay for some or all of the project out of pocket, sometimes in phases (design and permitting first, then construction). Slower, but no lender overlays and no interest. Often combined with a later mortgage-backed loan once there’s something to appraise. The Texas catch: if you’re income-qualified in San Antonio, the city’s Casita incentive reimburses you after completion — so you still need your own financing or funds lined up first.

Lane 4 — Higher-risk bridge, builder, or personal financing

Unsecured personal loans, builder-arranged financing, or bridge loans. Useful in narrow cases, but treat any builder financing as higher-risk until you understand the exit — many depend on you refinancing within a short window. The Texas catch: a builder-financed plan that assumes a later Texas cash-out refi inherits all the 80%-cap and waiting-period constraints below.

Why Texas is different

Three reasons a national guide will lead a Texan astray. First, Texas home-equity restrictions cap how much you can borrow against your homestead and add a mandatory waiting period. Second, local ADU rules vary wildly — what’s allowed in Austin may be prohibited or sharply limited a few miles away, because Texas has no statewide ADU law forcing cities to permit them. Third, deed restrictions and HOAs can override a permissive city — a city “yes” is not the same as a recorded-covenant “yes.”

When not to apply yet

Don’t start a financing application if any of these are still unknown: you haven’t confirmed your city allows the ADU, you haven’t checked your deed restrictions and HOA, you don’t have a realistic cost range with a contingency built in, or you’re assuming projected rent will qualify you without confirming the lender will count it. Applying before these are settled is how homeowners end up paying for plans on a project that can’t be built — or getting denied after committing money.

Find your Texas ADU financing path — run the free 2-minute check. You’ll see which lane to test first, what could block financing, and what to verify before paying for plans. Get your free ADU report →

What Texas home-equity rules change the ADU financing decision?

Here’s the decoder. This table assembles rules that are normally scattered across the Texas Constitution, Fannie Mae’s Selling Guide, and a stack of lender and legal sources into one place. (LTV = loan-to-value, the loan amount divided by the home’s appraised value. CLTV = combined LTV, all liens added together divided by value.)

Texas homestead lending rules, decoded

| Texas rule | What it means for your ADU loan | Source (verified) |

|---|---|---|

| 80% LTV / CLTV cap on homestead equity loans and cash-out refis | Total of all loans on your home can't exceed 80% of appraised value. A homeowner with "lots of equity" on paper may have less usable borrowing room than they expect. | Fannie Mae Selling Guide B5-4.1-03 (updated 03/04/2026): max LTV/CLTV for any Texas 50(a)(6) loan is 80%, regardless of automated-underwriting findings. Texas Const. Art. XVI §50(a)(6); Texas Real Estate Research Center (TRERC). |

| 2% lender-fee cap | Certain lender fees on a 50(a)(6) loan are capped at 2% of the loan amount (appraisal, survey, and title premiums are generally excluded). | TRERC; Texas Admin. Code Title 7 §153, verified 2026. |

| 12-day waiting period + 3-day rescission | The loan can't close fast. Texas mandates a cooling-off window (the "12-day letter") and a 3-day right to cancel after closing. Plan your timeline around it. | TRERC; Texas United Mortgage, verified 2026-02. |

| You can't stack a home-equity loan/HELOC on top of an active Texas cash-out | If you already have a Texas cash-out refinance in place, you generally can't add a separate home equity loan or HELOC until it's paid off. Pick the right Lane 1 product the first time. | Capital Home Mortgage; Defy Mortgage, verified 2025–2026. |

| "Once a Texas cash-out, always a Texas cash-out" | After one 50(a)(6) loan, the 80% cap follows your home on every future refinance — even a no-cash-out one — until you sell. | The Mortgage Reports, verified 2026-01-07. |

| No FHA or VA cash-out refinance on a Texas homestead | Government-backed cash-out refinances are blocked here. A 2018 Texas Attorney General Opinion treats the VA guaranty as "additional collateral," which §50(a)(6)(H) prohibits; FHA and VA loans are also treated as recourse loans. (A 203(k) renovation loan is a different transaction — see Lane 2.) | Polunsky Beitel Green (law firm), citing 2018 TX AG Opinion; Plaza Home Mortgage 50(a)(6) program guide. |

| Primary residence only | 50(a)(6) protections apply to homesteads, not investment properties or second homes. Investor ADU financing follows different rules. | Hurst Lending; Texas United Mortgage, verified 2026. |

A note on manufactured homes: some lender and program guides apply a lower maximum LTV (around 65%) when a manufactured home is the collateral. This is program-specific rather than a universal constitutional rule — confirm the limit with your specific lender’s program guide.

Texas equity quick math

Estimated home value × 0.80 − current mortgage payoff − any existing home-equity liens = approximate maximum secured borrowing room

(Before transaction-specific rules, underwriting, closing costs, and lender limits.)

Example, illustrative only: a $400,000 home with a $220,000 mortgage balance. $400,000 × 0.80 = $320,000. Minus the $220,000 payoff leaves roughly $100,000 of usable equity to tap — before costs and underwriting. If your ADU quote is $200,000, that gap is your signal to look at Lane 2 (renovation/construction financing against the finished value) instead of trying to force the whole project into a home-equity loan.

One more Texas nuance worth a lender conversation

Fannie Mae’s guidance also flags a use-of-proceeds caution: a Texas 50(a)(6) cash-out loan’s proceeds generally shouldn’t be used to acquire or improve the homestead if a different Texas constitutional provision (such as a Section 50(a)(5) home-improvement lien) could have been used instead. In plain terms: for actually building an ADU, a 50(a)(6) cash-out is not automatically the cleanest tool, and a purpose-built renovation or construction loan may be both simpler and more compliant. Put this question to your lender, title company, and — if the dollars are large — a real estate attorney before you sign. We’re a research resource, not your lawyer; this is the one section where professional confirmation genuinely matters.

Check your ADU equity room → Our Feasibility Engine flags when your project likely needs a renovation or construction path instead of current-equity financing. Get your free ADU report.

Can I use a HELOC, home equity loan, or cash-out refinance for a Texas ADU?

Home-equity fit matrix

| Path | Best fit | Main Texas caution | Don’t use it when |

|---|---|---|---|

| HELOC | Flexible draw schedule, enough equity, first mortgage worth keeping | Texas 80% cap; variable rate means payment can rise | Your borrowable room can't cover the bid plus contingency |

| Home equity loan | You want a fixed payment and have a firm budget | Texas 80% cap; lump-sum timing vs. construction draws | Project cost is still uncertain |

| Cash-out refinance | Your current first mortgage isn't worth preserving and you need a large sum | Replaces first mortgage; "once A6, always A6"; blocks future second liens until paid off | Your current rate is materially better, or another lane fits |

| Renovation/construction (Lane 2) | Not enough current equity, or you need after-completion value | More underwriting controls and draw management | You can't tolerate process complexity and want speed |

The decision most Texas homeowners get wrong: doing a cash-out refinance when they have a low first-mortgage rate. If you locked a sub-5% mortgage and current rates are higher, refinancing the entire balance to access equity can cost far more over time than a second-lien HELOC or home equity loan that leaves your first mortgage untouched. Run both before you commit. And remember: a Texas cash-out permanently caps future refinances of that home at 80% LTV and blocks a separate second-lien HELOC or home equity loan until it’s paid off.

Explore mortgage-backed ADU financing options.

Compare refinance, second-lien, and construction paths with a lender network that works in Texas. (Affiliate link. This is education, not an offer or a guarantee of approval; availability and terms depend on your profile and property.)

Compare ADU Financing Paths →Can I use a renovation loan or construction-to-permanent loan for a Texas ADU?

Here’s why Lane 2 changes the math. With a home-equity loan you can only borrow against equity you’ve already built. With a renovation or construction loan, the appraiser values the property “subject to completion” — as if the ADU already exists. That means homeowners with little equity today can still finance a six-figure ADU, because the loan is sized against tomorrow’s value.

The agency renovation and construction lanes

Fannie Mae HomeStyle Renovation

A conventional mortgage that bundles purchase or refinance with renovation in a single loan and closing, based on the as-completed appraised value. Fannie Mae confirms HomeStyle can construct or install a new ADU on a one-unit property. In Selling Guide Announcement SEL-2025-10, Fannie Mae expanded its renovation and ADU policy: lenders may now disburse up to 50% of total renovation costs at closing, and ADU eligibility was broadened — for lenders using the newer UAD 3.6 appraisal format (effective March 31, 2026), a one-unit property may have up to three ADUs. These expansions roll out by lender and appraisal format, so confirm what your specific lender supports for your file.

Freddie Mac CHOICERenovation

Freddie Mac’s counterpart, which borrowers purchasing or refinancing can use to add a new ADU or renovate an existing one — including converting an old barn, garage, or shed into an ADU. Freddie Mac requires the ADU to be legally permissible, legal non-conforming, or located in an area without zoning (with a narrow exception path for one-unit dwellings under Guide Section 5601.2(c)).

FHA Standard 203(k)

The FHA renovation product folds rehab costs into the mortgage. Per HUD’s Mortgagee Letter 2023-17, a Standard 203(k) may be used to convert a one-family dwelling into a one-family dwelling with an ADU, to add an ADU that will be attached to the existing structure, or to renovate an existing attached or unattached ADU. If your plan is a brand-new detached ADU, confirm program fit with your lender. Remember: Texas prohibits FHA cash-out refinances on a homestead, but a 203(k) renovation loan is a different transaction.

Construction-to-permanent (single-close) loan

This finances the build then automatically converts to a standard mortgage when construction finishes — one closing, not two, which saves a set of closing costs. The rate is typically locked at closing. Lenders commonly want roughly 20%–25% down measured against the completed project value. Fannie Mae confirms borrowers building a new one-unit property with an ADU can use a construction-to-permanent loan to finance both the home and the ADU.

Programs exist; approval is not guaranteed

These programs can support ADU financing, but the lender still reviews borrower qualification, contractor documentation, permits, appraisal, local legality, and program overlays. Do not assume projected rent or after-completion value will be accepted until a lender confirms it in writing for your specific property.

A practical note on “legal ADU.” To a lender, an ADU that isn’t permitted — or sits in a jurisdiction that doesn’t allow it — may not be financeable at all, or may be appraised as something less valuable than a legal second unit. This is why the city-feasibility step comes before the financing step, not after.

Compare renovation and construction paths — explore your options. (Affiliate link — see disclosure above.) Explore ADU financing options →

How much does a Texas ADU cost before financing?

These numbers matter for financing because they determine your lane. A modest garage conversion might fit inside a home-equity loan or even a phased-cash approach. A $250,000+ detached build almost always needs Lane 2 (renovation or construction financing against the finished value).

Cost planning anchors

| ADU type | Planning anchor | Financing implication | Source / status |

|---|---|---|---|

| Garage / interior conversion | Lower end of the range; varies widely by scope | May fit a smaller home-equity loan or cash hybrid if legal-dwelling requirements are met | Directional; confirm with local Texas builder quotes |

| Detached ADU (Austin) | ~$125,000–$350,000; an 1,100 sq ft unit can reach $300,000+ | Usually needs Lane 2 (renovation/construction against finished value) plus a contingency | Maxable, Austin (named source), verified 2026 |

| Single new water meter | ~$30,000 (Austin) | A frequently underestimated line item that can swing your loan size | Maxable, Austin (named source), verified 2026 |

| Prefab / modular ADU | Often lower base cost, plus site work | Factory deposit timing can break ordinary construction draws; confirm the draw schedule | Directional; confirm with vendor + lender |

| Utility-heavy or rural ADU | Add site-work cost on top of the build | Septic, well, and utility laterals can change loan size and contingency materially | Directional; confirm with county/local quotes |

“Utility lateral” = the pipe or line connecting your ADU to the water, sewer, gas, or electric main. “Site work” = grading, foundation prep, driveways, and utility trenching — the costs that happen before the building goes up and that quotes often understate.

Why “price per square foot” misleads ADU borrowers

A common trap: a homeowner sees “$200/sq ft” and multiplies by 600 square feet to get $120,000 — then is shocked by a $200,000 bid. The reason is that ADUs carry a high share of fixed costs that don’t scale with size: a full kitchen, a bathroom, a separate electrical panel, utility connections, permits, and site work all cost roughly the same whether the unit is 500 or 800 square feet. So smaller ADUs often have a higher cost per square foot, not a lower one. Budget from a real line-item bid, not a per-foot shortcut.

Soft costs lenders care about

Design and architecture, engineering, permit and impact fees, surveys, utility connection fees (remember that ~$30,000 water meter in Austin), and a contingency reserve. A lender financing the build will expect to see these in your numbers, and a 15%–20% contingency is standard for a reason — ADU projects routinely surface surprises once walls open or trenches are dug. Size that contingency before you apply so the loan covers it.

Use a feasibility report before turning a rough quote into a loan application.

See What You Can Build → Get Your Free ADU ReportHow much rent can a Texas ADU realistically support?

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, lease terms, utility costs, and regulatory approvals.

Texas metro rent proxies

| City | Avg rent (all beds) | 1BR proxy | 2BR proxy | How to use it |

|---|---|---|---|---|

| Austin | $1,950 | $1,250 | $1,722 | Conservative starting point; then compare neighborhood ADU/casita listings |

| Dallas | $1,900 | $1,375 | $1,875 | Overlay and owner-occupancy rules may shape what you can legally rent |

| Houston | $1,880 | $1,159 | $1,500 | Deed restrictions and permitting still need checking first |

| San Antonio | $1,610 | $975 | $1,250 | Owner-occupancy affidavit shapes your rental strategy |

| Fort Worth | $2,095 | $1,250 | $1,575 | Confirm permit/zoning feasibility before projecting rent |

Rent figures: Zillow Rental Manager metro data, dated May 23, 2026. These are metro-wide market proxies for all property types, not ADU-specific guarantees. (Fort Worth’s $2,095 is the all-beds average; its 3-bedroom proxy is higher.)

When rent can help you qualify — and the exact numbers FHA uses

Some lenders will count projected ADU rental income toward your debt-to-income ratio, which can help you qualify. Fannie Mae, Freddie Mac, and FHA all have ADU rental-income pathways. FHA’s rules (HUD Mortgagee Letter 2023-17) are unusually specific: for certain cases, FHA counts 75% of the lesser of the appraiser’s estimated fair market rent or the lease amount; caps ADU rental income at 30% of total effective income; and requires two months of mortgage-payment (PITI) reserves when using ADU rental income. For certain 203(k) ADU cases with no rental history, FHA uses 50% of the lesser amount. The takeaway: lenders rarely count 100% of projected rent, and they require documentation — don’t build your plan on full rent counting until a lender confirms it for your file.

Why short-term rental assumptions are risky in Texas

If your plan is to Airbnb the ADU, check the city rules before you bank on it. Austin limits short-term rental use of certain ADUs built after October 1, 2015 to 30 days per calendar year, and the city has signaled it will begin asking platforms to remove unlicensed listings. San Antonio bars short-term rental use of non-owner-occupied ADUs entirely. Long-term rental (leases of 30 days or more) generally faces none of those short-term restrictions. If your financing math depends on nightly rates, a cap like Austin’s can demolish the projection. Verify your specific city and property.

Explore mortgage-backed ADU financing options. Start with education, not a promise of approval. (Affiliate link — see disclosure above.) Compare your options →

Which Texas city rules can make or break ADU financing?

This is the single most common place national guides mislead Texans. They imply “Texas is property-rights friendly, so you can build.” The accurate statement is narrower: your city, HOA, deed restrictions, utility district, and lender all have to say yes — and they don’t always agree. Below, each city gets its own quick reference; verify the specifics with your city before you spend on plans.

Austin ADU financing rules

Austin is comparatively ADU-friendly, but what you can build depends on whether the project is treated as an ADU/two-unit/three-unit use, your lot size, your zoning, and current HOME-initiative standards. Austin’s official ADU page lists SF-1, SF-2, and SF-3 eligibility and references a 5,750-square-foot lot-area threshold for ADU/two-unit/three-unit review; the city’s HOME Phase 1 allows up to three dwelling units on SF-zoned property through two-unit and three-unit residential uses, while HOME Phase 2 small-lot use applies to one-unit residential on lots between 1,800 and 5,750 square feet (not multi-unit ADU stacking). Every dwelling needs a unique address/building number, deed restrictions must be checked, and short-term rental use of post–October 1, 2015 ADUs is limited to 30 days per year. (Source: City of Austin Development Services; HOME amendments page, verified 2026.)

Dallas ADU financing rules

Dallas regulates ADUs through its Accessory Dwelling Unit Overlay, and a key financing detail is that an ADU may not be sold separately from the main building site. Under the Dallas code, a detached ADU has roughly a 200-square-foot minimum and a maximum floor area of the greater of 700 square feet or 25% of the main structure; height is generally limited to one story; one parking space is generally required unless an exemption or reduction applies; owner-occupancy applies when one unit is rented; and if a unit is rented, the rental unit must be registered. (Source: Dallas City Code, ADU Overlay, verified 2026.)

Houston ADU financing rules

Houston has no traditional zoning, and it increased the maximum second dwelling unit size from 900 to 1,500 square feet under Chapter 42 amendments effective November 27, 2023 — but active deed restrictions still control, and they are not overridden. Parking is based on the unit’s size (units up to 1,000 square feet are exempt from an added off-street space). Plan review, site plans, permits, fees, and inspections still apply, and deed restrictions can prohibit an ADU outright even where the city allows it. Houston also offers free permit-ready ADU design resources. (Source: City of Houston Planning & Development Department press release, Sept. 27, 2023; verified 2026.)

San Antonio ADU financing rules

San Antonio allows one ADU in listed zoning districts and requires the property owner to live on site — recording an owner-occupancy affidavit (a covenant) with the Bexar County Clerk — which directly shapes any rental or investor financing plan. The city’s Information Bulletin 402 and Unified Development Code §35-371 set the size, height, setback, parking, and documentation standards. Non-owner-occupied ADUs can’t be used as short-term rentals. Because the affidavit and owner-occupancy requirement are recorded against the property, confirm them with the city before assuming a pure-rental strategy. (Source: City of San Antonio Development Services, Information Bulletin 402 / UDC §35-371, verified 2026.)

Fort Worth ADU financing rules

In Fort Worth, a habitable accessory structure must comply with the building code, lot-coverage and side/rear setback rules, and may not exceed the height of the primary structure — and in one-family districts it may be used only as an ADU, not as a separate independent residence. Additions, detached garages with habitable space, garage enclosures, and other accessory structures require permits and zoning review, so treat Fort Worth as a permit-first city for financing triage. (Source: Fort Worth City Code; Development Services, verified 2026.)

San Antonio’s Casita incentive — the financing help most guides miss

San Antonio is the rare Texas city offering direct financial help to build an ADU. Under the city’s Casita Incentive Pilot Program, funded by the 2022–2027 Affordable Housing Bond, the city’s Casita Incentives page currently shows Application Open.

Two things to understand before you count on it. First, it’s a no-interest forgivable loan for owner-occupied properties, tiered by income — historically up to about $25,000 (5-year forgivable) for owners at 80% AMI or less and up to about $35,000 (10-year forgivable) for owners at 50% AMI or less — plus design-fee help and a waiver of most city permit fees. Second, and crucially: the construction incentive is reimbursed upon completion, not paid upfront, and applicants must show proof of financing or funds greater than the project cost. Short-term rentals under 30 days don’t qualify. In other words, this reduces your net cost — it doesn’t replace your need to finance the build.

Confirm current status, income tiers, and terms at sa.gov/ADU before relying on it. (Source: City of San Antonio, Casita Incentives page; verified 2026.)

Start with city feasibility before you apply for financing — and check your financing gap before counting on any incentive.

See What You Can Build → Get Your Free ADU ReportShould I finance a detached ADU, garage conversion, prefab unit, or casita differently?

Type-to-financing fit

| ADU type | Likely financing fit | Main underwriting friction |

|---|---|---|

| Detached ADU (DADU — free-standing) | Renovation loan, construction-to-permanent, or HELOC if equity is strong | Site work, utility hookups, permit status, appraisal "subject to completion" |

| Garage conversion / garage apartment | HELOC, home equity loan, renovation loan, or cash/phased | Legal-dwelling requirements, parking, fire separation, plumbing upgrades |

| Attached ADU (shares a wall with the main house) | Renovation loan (including FHA 203(k) for attached), or HELOC/home equity | Structural and code review |

| Prefab / modular ADU (built in a factory, installed on site) | Specialized renovation/construction path, or enough cash/equity | Factory deposit timing vs. on-site draws; real-property classification |

| Casita (Texas/Southwest term for a small detached unit) | Feasibility + financing after owner-occupancy affidavit check (San Antonio) | Recorded affidavit and city process |

| Manufactured-home ADU | Specialized lending; some programs apply a lower LTV cap on manufactured-home collateral | Real-property classification; lower equity cap; lender overlays |

The prefab timing issue is worth flagging because it surprises homeowners: modular and prefab manufacturers typically require sizable deposits before anything is installed on your lot — but a standard construction loan disburses against on-site progress an inspector can verify. That mismatch can leave you funding a factory deposit out of pocket while the loan waits for something to appraise. If you’re going prefab, confirm the draw schedule and deposit handling with your lender up front.

For deeper, product-specific guidance, see our pages on prefab ADU financing, garage-conversion financing, and ADU financing options.

What documents will a Texas ADU lender usually ask for?

- •Borrower documents: recent pay stubs, W-2s or tax returns (especially if self-employed), bank and asset statements, and your credit profile. Many Texas cash-out and home-equity programs look for a minimum credit score around 620, with better terms at higher scores.

- •Property and title documents: your deed, current mortgage statement, homeowners insurance, and — critically in Texas — confirmation of any existing homestead liens, since they count against your 80% cap.

- •ADU plans and contractor documents: architectural plans, a detailed contractor bid, the scope of work, and the contractor’s license and insurance.

- •Permit and zoning evidence by city: proof the ADU is permitted or permittable. Austin requires a unique address/building number and a deed-restriction check; Dallas requires ADU Overlay confirmation and rental registration if a unit is rented; Houston requires a deed-restriction check plus site plan, plan review, permits, and inspections; San Antonio requires the recorded owner-occupancy affidavit plus a site plan, foundation plan, energy report, and mechanical calculations; Fort Worth requires building-code and zoning review.

- •Rent support (if using ADU income to qualify): an appraiser’s rent schedule or comparable rents, and any signed or proposed lease — plus, for FHA, the reserve and percentage rules noted above.

- •Insurance and construction-draw documents: builder’s risk insurance and the lender’s draw schedule for construction or renovation loans.

Free 2026 ADU Starter Kit

Includes the lender-document checklist, city pre-check questions, and a budget worksheet. No spam, free to download.

Download the Free 2026 ADU Starter Kit →What are the biggest ADU financing mistakes Texas homeowners make?

The seven we see most often:

- 1Starting with the lender before the city. A loan can't fix a project the city won't permit. Confirm feasibility first.

- 2Ignoring deed restrictions or HOA rules. A city "yes" doesn't override a recorded covenant. Houston and Austin guidance both explicitly tell homeowners to verify deed restrictions — and in Houston, an active deed restriction can prohibit an ADU even though the city allows it.

- 3Treating future rent as guaranteed qualifying income. Lenders haircut projected rent (FHA, for instance, counts 75% of the lesser of market or lease rent in certain cases) and require documentation. Don't bank on full rent counting.

- 4Underestimating utility and site-work costs. A single new water meter can run about $30,000 in Austin; septic, well, and utility laterals can move a budget by tens of thousands. Size them in.

- 5Refinancing a good first mortgage unnecessarily. A cash-out refi that wipes out a low locked rate can cost far more than a second-lien option — and triggers the permanent "once a Texas cash-out" 80% cap plus the block on future second liens.

- 6Accepting builder financing without an exit plan. If the offer depends on refinancing within a short window, you're carrying the risk if rates or appraisals move against you.

- 7Building a plan around short-term rental income where the city limits it. See Austin's 30-day cap and San Antonio's ban on non-owner-occupied STR ADUs. Verify before you project.

If one of these is your roadblock, there’s usually a path around it: no equity points you to Lane 2 (renovation/construction against finished value); a prefab timing problem points to a specialized draw structure; an HOA prohibition may mean a different unit type or a conversation with your board. The roadblock is information, not a dead end.

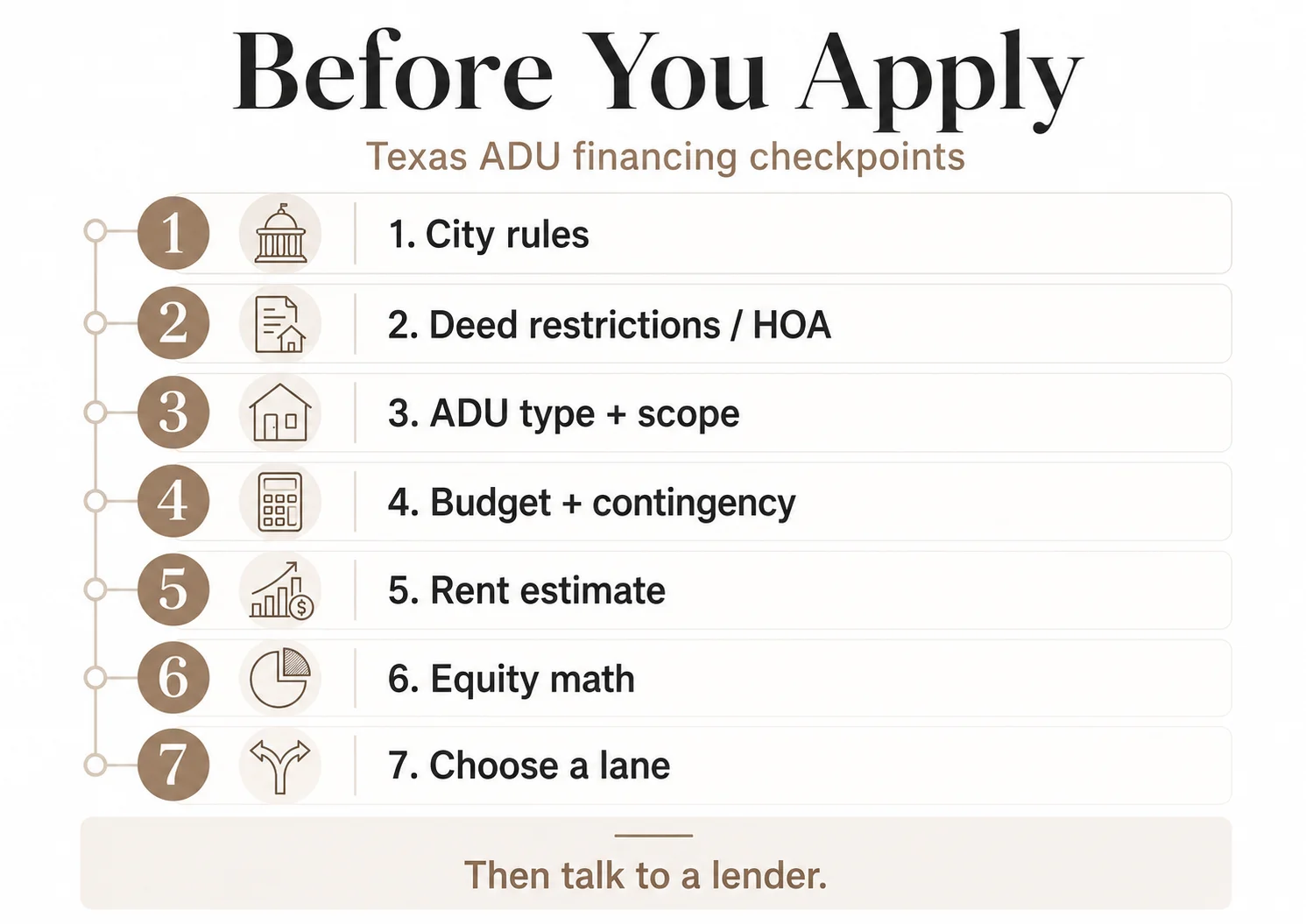

What should I do before I apply for ADU financing in Texas?

The full pre-application sequence:

- 1Check your city's ADU eligibility (zoning, lot size, size caps, setbacks).

- 2Check deed restrictions and HOA rules — separately from city rules.

- 3Choose your ADU type and rough scope.

- 4Get a realistic cost range and size a 15%–20% contingency.

- 5Estimate rent conservatively, using metro proxies as a ceiling, not a floor.

- 6Estimate usable equity: value × 0.80 − payoff − existing liens.

- 7Decide whether to preserve or replace your first mortgage.

- 8Compare the home-equity lane against the renovation/construction lane.

- 9Talk to a lender after steps 1–8 are documented.

- 10Don't sign builder financing until you understand the exit.

Bring the result to your lender, builder, or permit meeting.

See What You Can Build → Get Your Free ADU ReportWhat we verified

We researched this guide against primary and authoritative sources and last verified it on May 25, 2026. Source categories and verification dates:

- Texas home-equity rules (Section 50(a)(6)): Texas Constitution Article XVI §50; Fannie Mae Selling Guide B5-4.1-03 (updated 03/04/2026); Texas Real Estate Research Center (TRERC); Texas Administrative Code Title 7 §153; Polunsky Beitel Green analysis citing the 2018 Texas Attorney General Opinion on VA/FHA collateral. Verified Jan–May 2026.

- Statewide ADU legislative status: SB 673 (89th Legislature, 2025) passed the Senate and was placed on the General State Calendar; we did not verify it as enacted statewide law, so local rules are controlling. Sources: Texas Municipal League legislative update (April 2025); LegiScan. Recheck Texas Legislature Online before relying on this.

- City ADU rules: City of Austin Development Services and HOME amendments pages; Dallas City Code ADU Overlay; City of Houston Planning & Development Department (Chapter 42 amendments effective Nov. 27, 2023); City of San Antonio Development Services Information Bulletin 402 / UDC §35-371; Fort Worth City Code. Verified 2026.

- San Antonio Casita Incentive Pilot Program: City of San Antonio Casita Incentives page (status: Application Open; reimbursement at completion; proof-of-funds requirement). Verified 2026 — recheck status and income tiers before relying on it.

- Agency financing products: Fannie Mae (HomeStyle Renovation, ADU policy, construction-to-permanent, Selling Guide Announcement SEL-2025-10); Freddie Mac (CHOICERenovation); HUD/FHA (Mortgagee Letter 2023-17). Verified Dec 2025–March 2026.

- Cost anchors: Austin cost data from Maxable (named source), including the ~$30,000 water-meter and 1,100 sq ft → $300,000+ figures. Verified 2026. Other type-level ranges are directional.

- Rent proxies: Zillow Rental Manager metro data, dated May 23, 2026.

We used Reddit and homeowner forums only to understand the questions Texans bring to this decision — never as proof for legal, financing, cost, or zoning claims. This guide is educational and is not financial, legal, tax, lending, or construction advice. Verify your property with your city, lender, title company, attorney, and licensed contractor before applying for financing or starting work.

Frequently asked questions: Texas ADU financing

Can I get a loan to build an ADU in Texas?

Yes. The right path depends on whether your city permits the ADU, how much usable equity you have under the Texas 80% homestead cap, your borrower qualifications, your contractor documentation, and whether the lender finances the project as home equity, renovation, construction, or a purchase/refinance mortgage. Homeowners without much current equity often use a renovation or construction loan that qualifies them against the home's finished value.

Can I use a HELOC for an ADU in Texas?

Often yes, if you have enough usable equity and can handle a variable payment — but a Texas HELOC is subject to the 80% combined-lien cap and lender eligibility review, and you generally can't hold a HELOC at the same time as an active Texas cash-out refinance. It preserves your existing first mortgage, which is an advantage if you have a low locked rate.

Can I use a cash-out refinance for a Texas ADU?

Sometimes, but a Texas cash-out refinance (a 50(a)(6) loan) replaces your entire first mortgage, is capped at 80% LTV, permanently caps future refinances of that home at 80% ("once a Texas cash-out, always a Texas cash-out"), and blocks a separate second-lien HELOC or home equity loan until it's paid off. For actually building an ADU, a purpose-built renovation or construction loan is often cleaner. Compare both, and ask your lender about Texas use-of-proceeds rules.

Can I do an FHA or VA cash-out refinance in Texas?

No. Government-backed cash-out refinances aren't allowed on a Texas homestead. A 2018 Texas Attorney General Opinion treats the VA guaranty as "additional collateral," which the Texas Constitution prohibits for home-equity loans, and FHA/VA loans are treated as recourse loans that aren't eligible. An FHA 203(k) renovation loan is a different transaction and may still be an option.

Can future ADU rent help me qualify for a loan in Texas?

Sometimes. Fannie Mae, Freddie Mac, and FHA all have ADU rental-income pathways. FHA, for example, counts 75% of the lesser of appraiser-estimated market rent or the lease in certain cases, caps ADU income at 30% of effective income, and requires two months of payment reserves. Lenders generally discount projected rent and require documentation, so don't assume full rent counting until a lender confirms it.

Are ADUs legal everywhere in Texas?

No — don't assume that. Texas has no enacted statewide ADU law as of May 2026, so local city rules, deed restrictions, and HOA rules all control. Austin is comparatively ADU-friendly; many other Texas jurisdictions are more restrictive. Verify your specific address.

Is Austin ADU financing easier than Dallas?

Austin has clearer ADU and HOME rules than many Texas cities, but the allowed structure depends on whether the project is treated as an ADU/two-unit/three-unit use, your lot size, your zoning, and current HOME standards. Dallas works through its Accessory Dwelling Unit Overlay with owner-occupancy rules when a unit is rented. "Easier" still depends on your specific parcel and project.

Can I rent out my Texas ADU short-term?

It depends on the city. Austin limits short-term rental use of certain post–October 1, 2015 ADUs to 30 days per calendar year, and San Antonio bars short-term rental use of non-owner-occupied ADUs. Long-term leases (30+ days) generally avoid those restrictions. Verify your city's rules before projecting nightly-rate income.

How much does an ADU cost in Texas?

Detached ADU cost anchors cluster around $125,000–$350,000, with Austin data showing an 1,100-square-foot unit can reach $300,000+ and a single new water meter running about $30,000 (Maxable, Austin, verified 2026). Garage conversions and small prefab units run lower. Budget from a real line-item bid plus a 15%–20% contingency.

Should I finance an ADU if the rent won't cover the payment?

Not necessarily. Treat rental income as an assumption to stress-test, not a guarantee. Many homeowners build ADUs primarily to house family or add long-term property value, with rent as a secondary benefit. Run the numbers with conservative rent and a vacancy allowance before deciding.

What if my HOA or deed restrictions prohibit ADUs in Texas?

That can block or materially change the project even if your city allows ADUs. In Houston especially, an active deed restriction is not overridden by the city's rules. Check your recorded covenants before spending on plans.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.