How to Finance a Garage Conversion ADU in 2026: The 8 Financing Paths, Ranked by Your Situation

By the Dwelling Index Editorial Team · Last updated: · Last verified: · Editorial standards · Affiliate disclosure · ~40 min read

The Dwelling Index — an independent research resource covering ADU financing, costs, and regulations. We are not a lender, appraiser, builder, or zoning authority.

Disclosure: The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you — and it never changes our recommendations. Read the full disclosure.

Start here: which garage conversion financing path should you test first?

Find the row that sounds like you. That’s the lane to test first. We explain every one in depth below — this table is the map, not the whole journey.

| Your situation | First path to test | Why it usually fits | The catch to watch |

|---|---|---|---|

| Strong equity + a low first-mortgage rate you want to keep | HELOC or home equity loan | Borrows against equity behind your existing mortgage — your low rate stays untouched | Rates run higher than a first mortgage; HELOCs are variable |

| Strong equity + your current rate is already high | Cash-out refinance | One consolidated payment; a first-lien rate that’s often priced lower than second-position debt | Replaces your mortgage; closing costs apply |

| Limited equity today, but the ADU adds real value | Renovation loan (HomeStyle / CHOICERenovation / 203(k)) | Lends against the home’s after-completion value, not today’s | More paperwork, contractor draws, longer timeline |

| Limited equity + larger or detached build | Construction-to-permanent loan | Funds released in draws; doesn’t require big existing equity | New first mortgage; you lose a low existing rate |

| Small one-car conversion or a funding gap | Cash, savings, or a personal loan | Fast, no equity required, no lien on the home | Higher rate, short term; rarely covers a full permitted ADU |

| Can’t qualify for a loan but have equity | Home equity investment (HEI) | No monthly payment | You owe a share of future appreciation; available in limited states |

Loan mechanics verified against CFPB consumer guidance on HELOCs and home equity loans; Fannie Mae and Freddie Mac ADU/renovation program pages; HUD’s 203(k) program guidance; and U.S. Department of Veterans Affairs cash-out guidance. Cost band from Angi 2026 garage-conversion data and regional builder cost references. Last verified .

See your personalized path in about 60 seconds. Our free Financing Path Matcher takes a handful of inputs — your state, rough home value and mortgage balance, garage type (attached or detached), project scope, and whether you plan to rent the unit — and returns the single lane to test first for your property, the disqualifier to watch, and an estimated monthly cost band.

What is the best way to finance a garage conversion ADU?

The best way to finance a garage conversion ADU depends on five variables: how much equity you have, your current mortgage rate, your garage’s condition, whether the project is permit-ready, and whether the ADU will generate rent. For homeowners with enough equity to cover a permit-ready budget and a low first mortgage worth keeping, a home equity line of credit or home equity loan is generally the most efficient starting point because it leaves the existing mortgage in place. For homeowners short on current equity, a renovation or construction loan that underwrites the home’s after-completion value is often more realistic. There is no single best loan — there is a best loan for your situation.

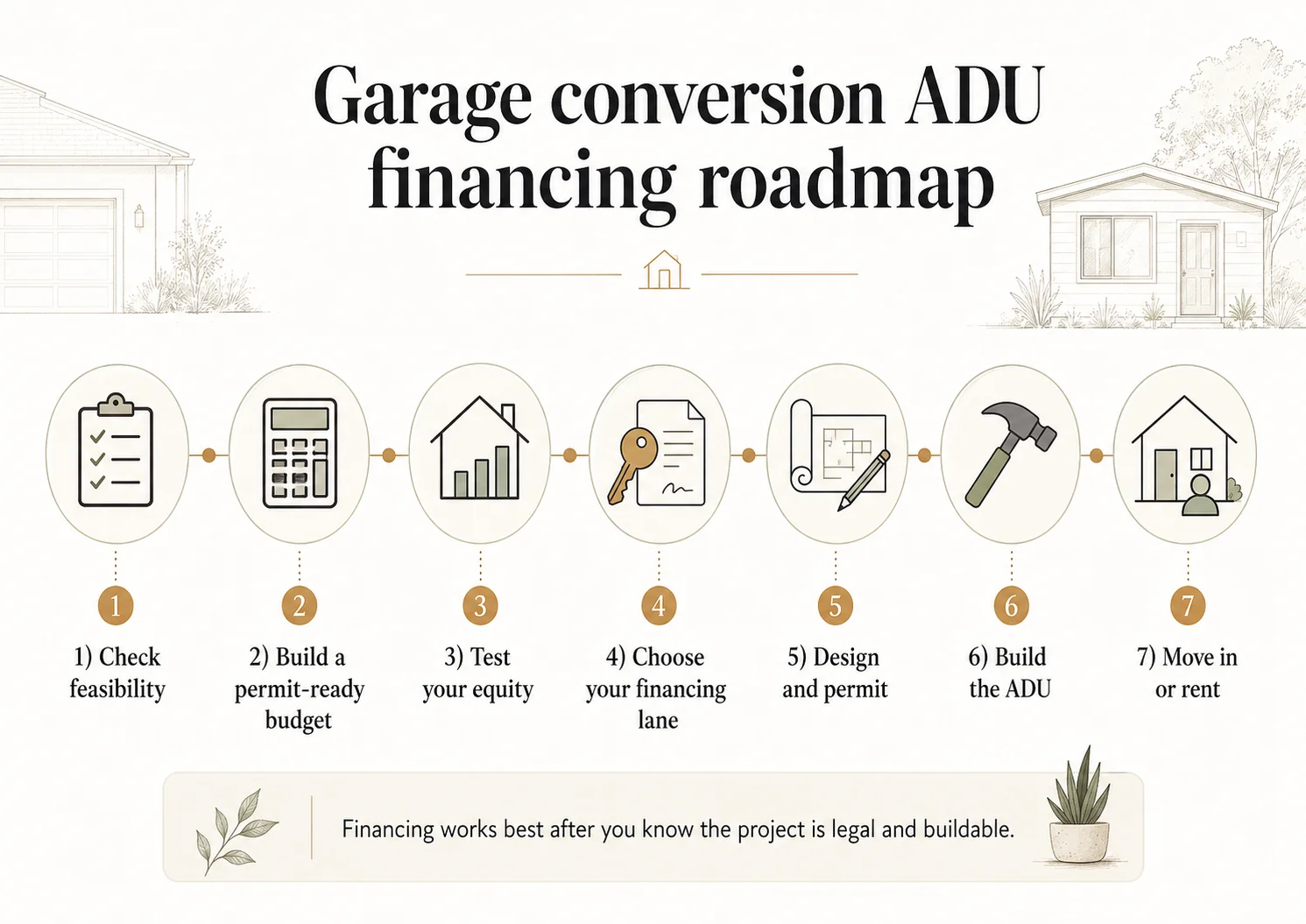

This is where most homeowners get stuck. Financing a garage conversion isn’t a single yes/no door (“do I have enough equity?”). It’s a decision tree, and there’s a viable branch for nearly every situation. The branch you need depends on how your equity, your rate, and your garage interact. Here’s the order we recommend working through it.

The five-step decision rule

- Confirm the garage can legally become an ADU. Zoning, lot eligibility, owner-occupancy rules, and parking replacement vary by city. Lenders and appraisers care whether the unit is legal or legally permissible — an unpermitted conversion creates appraisal, insurance, resale, and enforcement problems later.

- Build a permit-ready budget, not a rough contractor number. Add design, engineering, permit and plan-check fees, utility work, code upgrades, inspections, and a contingency reserve to the construction estimate.

- Run the 60-second equity test (below) to see whether current equity can realistically cover that budget.

- Decide whether to keep or replace your first mortgage — this single decision eliminates half the loan menu.

- Only then choose the loan lane.

Current-value financing vs. future-value financing

This is the distinction that decides everything.

Current-value financing — HELOCs, home equity loans, and cash-out refinances — lends against your home’s value today and the equity you’ve already built. If your home is worth $600,000 and you owe $300,000, you have roughly $300,000 in equity, and lenders let you borrow against a portion of it (commonly up to a combined loan-to-value, or CLTV, around 80–85%). CLTV is the total of all loans on the home divided by its value; a lower CLTV means lower risk to the lender and usually a better rate.

Future-value (renovation) financing — FHA 203(k), Fannie Mae HomeStyle Renovation, and Freddie Mac CHOICERenovation — can underwrite the home’s value after the ADU is finished. That matters enormously for a recent buyer or anyone whose current equity falls short of the project cost, because the after-completion appraisal can unlock far more borrowing power than today’s value alone. After-renovation value, sometimes abbreviated ARV, is the appraised value the home is expected to reach once the work is complete.

If you remember nothing else from this page, remember this: for most garage conversion ADUs, the first financing question isn’t “which lender is best?” It’s “can current equity cover a permit-ready budget, or do I need a future-value loan?”

The 60-second equity test

Estimate your home’s value, subtract your mortgage balance, and you have your rough current equity:

Home value − mortgage balance = current equity.

Then ask the question that actually matters: can that equity cover the permit-ready ADU budget, your soft costs, a contingency, and still stay within the lender’s CLTV cap? If yes, you’re a current-value candidate (HELOC, home equity loan, cash-out refi). If no, you’re a future-value candidate (renovation or construction loan) — and that’s not a failure, just a different branch of the tree.

How much should you borrow for a garage conversion ADU?

Borrow for the permit-ready total, not the cheapest construction estimate. A realistic budget includes design and drafting, engineering, permit and plan-check fees, utility work, kitchen and bath systems, code upgrades, inspections, a contingency reserve, and financing reserves for draws or change orders. Published costs for a standard one- to two-car conversion commonly land in the $80,000–$160,000 range, but the figure that should drive your loan amount is the all-in permitted number — typically 15–25% above the bare construction quote.

The most expensive mistake we see is borrowing against a verbal quote. A contractor’s “about $125,000” rarely includes the soft costs, and when those land after closing, homeowners discover their loan is too small to finish the unit legally. Size the loan for the real project.

2026 Garage Conversion ADU financing fit matrix

This table cross-references the type of conversion against published cost signals, a contingency-adjusted budget to actually finance, the first lane to test, and the proof a lender will want.

| Conversion scenario | Published cost signal | Budget to finance (after contingency) | First financing lane to test | Proof needed before applying |

|---|---|---|---|---|

| One-car attached garage, simple studio | $36,000–$96,000; garage-conversion average ~$110,000 ¹ | ~$41,000–$120,000+ | Cash, HELOC, home equity loan, or a small personal-loan gap | Contractor scope, permit feasibility, utility plan, kitchen/bath layout |

| Standard two-car conversion (CA/LA-type market) | ~$125,000–$175,000; simple ~$125,000–$150,000 ² | ~$144,000–$219,000+ | HELOC/home equity if equity allows; renovation mortgage if not | Written bid, permit status, plans, equity estimate, current mortgage terms |

| Older garage w/ slab, framing, or utility risk | ~$150,000–$200,000 ² | ~$173,000–$250,000+ | Future-value renovation loan, or home equity loan if equity is strong | Structural inspection, utility trenching plan, engineer notes, contingency reserve |

| High-cost / high-condition-risk market (e.g., Portland) | ~$175,000–$250,000+, excluding design & permitting ³ | ~$220,000–$325,000+ | Renovation mortgage, construction-to-permanent, or high-equity HELOC | Local designer/builder budget, permit-fee estimate, appraisal/rent support |

| Three-car or larger conversion | Up to ~$225,000 ¹; $175,000+ ² | ~$201,000–$281,000+ | HELOC/home equity if equity is high; otherwise renovation or construction | Detailed construction budget, appraisal, permit-ready scope |

| Above-garage unit / second-story add | Conversion starts ~$150,000 ⁴; above-garage/new-garage ADUs run ~$350,000–$500,000+ in San Diego County ⁵ | $350,000+ plausible in high-cost markets | Construction-to-permanent or renovation mortgage — treat as major construction | Engineering, foundation/framing review, full plans, builder estimate |

¹ Angi, 2026 garage-conversion cost data. ² Regional Southern California / Los Angeles builder cost references, 2026. ³ Portland-area architect cost reference (excludes design and permit fees). ⁴ Maxable garage-conversion starting point. ⁵ SnapADU San Diego County above-garage/new-garage ADU range (regional, not national). Contingency-adjusted budgets are Dwelling Index editorial estimates applying a 15–25% contingency to published construction signals; local figures vary by market — confirm against contractor bids in your area. Last verified .

Editorial note: the above-garage row is the trap. Homeowners assume “it’s still my garage, so it’s still a conversion,” but adding a second story is structural construction — different scope, different cost, different financing lane. Don’t carry a conversion budget into a project that’s really a small build.

Soft costs to include before you apply

These line items turn a $125,000 quote into a $155,000 loan. Budget for them up front so your financing covers the whole project.

| Soft / hidden cost | Why it matters to your loan amount |

|---|---|

| Design and drafting | Required for permit-ready plans an appraiser and lender can review |

| Engineering | Common when modifying structure, adding openings, or building above a garage |

| Permit and plan-check fees | Required before legal occupancy; vary widely by city |

| Utility work | Electrical, plumbing, sewer, gas, HVAC, water — and possible trenching to a utility lateral (the line connecting your property to the municipal main) |

| Fire separation / life safety | Critical when an attached garage becomes habitable space |

| Contingency reserve | Garage condition surprises (slab, moisture, framing) are common |

| Temporary storage / disruption | If the garage’s contents must be relocated during construction |

| Financing reserves | For draws, delays, or change orders on renovation/construction loans |

Get a property-specific starting point before you borrow against your home. Our feasibility report estimates what you can legally build at your address and a realistic budget band — so you’re not comparing loans for a project your lot can’t support.

See what’s possible at your address →“I don’t want to lose my low mortgage rate.” Here’s how to keep it.

If you locked a low first-mortgage rate, you can finance a garage conversion without giving it up by using a second-position loan — a HELOC, a home equity loan, or a renovation HELOC — that sits behind your existing mortgage and leaves it untouched. A cash-out refinance, by contrast, replaces your entire mortgage at today’s rate, which can add hundreds of dollars a month to a loan you already had under control. For homeowners with a sub-5% rate, protecting that first mortgage is usually the single most valuable financial move in the whole project.

This is the objection we hear most, and it’s a rational one. Here’s a hypothetical to show why it matters — a homeowner pulling $75,000 for a conversion:

- Cash-out refinance of a $200,000 balance into a new $275,000 loan at roughly 6.75% creates a new payment near $1,784/month — versus the old $955 payment. That’s about $829 more per month, much of it extra interest on the original $200,000 that never needed a new rate.

- HELOC for the same $75,000 at roughly 8.5%, interest-only during the draw period, runs about $531/month while the first mortgage stays at $955 — a total of $1,486/month, nearly $300 less than the cash-out path, and the low first mortgage survives.

Hypothetical math example, principal and interest only; excludes taxes, insurance, mortgage insurance, points, closing costs, and any HELOC fees. Not a loan offer, rate quote, or approval. Your numbers depend on credit, CLTV, and current market rates.

The takeaway isn’t “always use a HELOC.” It’s that when you hold a genuinely low first mortgage, the second-position math frequently wins — and it deserves a real comparison before anyone talks you into a refinance.

When a HELOC fits

A HELOC is a revolving line of credit secured by your home; you draw what you need, pay interest only on the drawn balance during the draw period, then repay principal and interest afterward. It fits when:

- You have meaningful equity and a first mortgage worth keeping.

- Your costs arrive in stages (design, permits, then construction draws).

- You can handle a variable rate — most HELOCs track the prime rate, so the payment can rise if prime rises.

Read our full breakdown of using a HELOC and home equity loan for an ADU.

When a home equity loan fits

A home equity loan (sometimes called a HELOAN or “second mortgage”) gives you a fixed lump sum at a fixed rate with predictable payments. The CFPB draws the line this way: a home equity loan is a specific borrowed amount, while a HELOC is an open line you can draw from repeatedly — and if you already have a mortgage, both sit in second position behind it. A home equity loan fits when you have a firm contractor bid, want payment certainty, and don’t want to replace your first mortgage.

The low-equity workaround that still protects your rate

If your current equity is thin but the ADU will lift your home’s value substantially, a renovation HELOC that lends against after-renovation value can sit in second position — keeping your low first mortgage — while still giving you access to the future value the ADU creates. These products are worth understanding as a category. Availability is limited and some renovation HELOCs are not offered in every state — including Texas — so confirm availability where you live before counting on this path.

The honest tradeoff: second-position loans carry higher rates than a first mortgage, and a HELOC’s variable rate means your payment isn’t fixed. If rate certainty matters more to you than protecting a low first mortgage — and your current rate isn’t especially low — a cash-out refinance or a fixed renovation mortgage may serve you better. There’s a path either way, and the next two sections walk both.

Want to see real second-mortgage and refinance options without prematurely touching your first mortgage? You can compare mortgage, refinance, and home-equity pathways through our research partner.

Affiliate link — we may earn a commission at no extra cost to you. This is financing-path education, not a loan offer, rate quote, or approval guarantee.

Explore your financing options →Should you use a cash-out refinance for a garage conversion ADU?

A cash-out refinance replaces your existing mortgage with a new, larger one and gives you the difference in cash — and it can be an excellent ADU financing pathif your current mortgage rate is at or above today’s rates. It consolidates everything into one payment, and because it’s a first-lien mortgage it’s often priced differently than second-position or unsecured debt, though the all-in cost depends on today’s rate, closing costs, and the mortgage you’re replacing. Many conventional cash-out refinances cap a one-unit primary residence around 80% loan-to-value, but exact limits vary by program, occupancy, property type, and lender. It’s a poor fit if you hold a low pandemic-era rate and only need ADU funds, because replacing that rate can cost more than the ADU itself over time.

A cash-out refinance generally takes about 30–45 days to fund, the same timeline as any refinance. On a refinance of a primary residence where the right of rescission applies, federal rules give you until midnight of the third business day after closing to cancel before funds are disbursed.

When a cash-out refinance makes sense

- Your current first-mortgage rate is already at or above today’s rates, so the rate tradeoff is smaller than replacing a low-rate loan.

- You want one payment instead of a first mortgage plus a second lien.

- The ADU budget is large enough to justify the closing costs of a full refinance.

- You’re already considering a refinance for other reasons.

When to avoid it

- You hold a low first-mortgage rate (the most common reason to skip it).

- You only need a modest amount — closing costs outweigh the benefit.

- Your equity is too thin to reach the budget within the ~80% LTV cap.

A note for veterans

Eligible veterans and service members may consider a VA-backed cash-out refinance to fund home improvements, including ADU work. The VA notes you still qualify through a private lender, that closing costs can add up to thousands of dollars, and to watch for misleading refinance solicitations. If you have VA entitlement and your current rate isn’t especially low, it’s worth comparing.

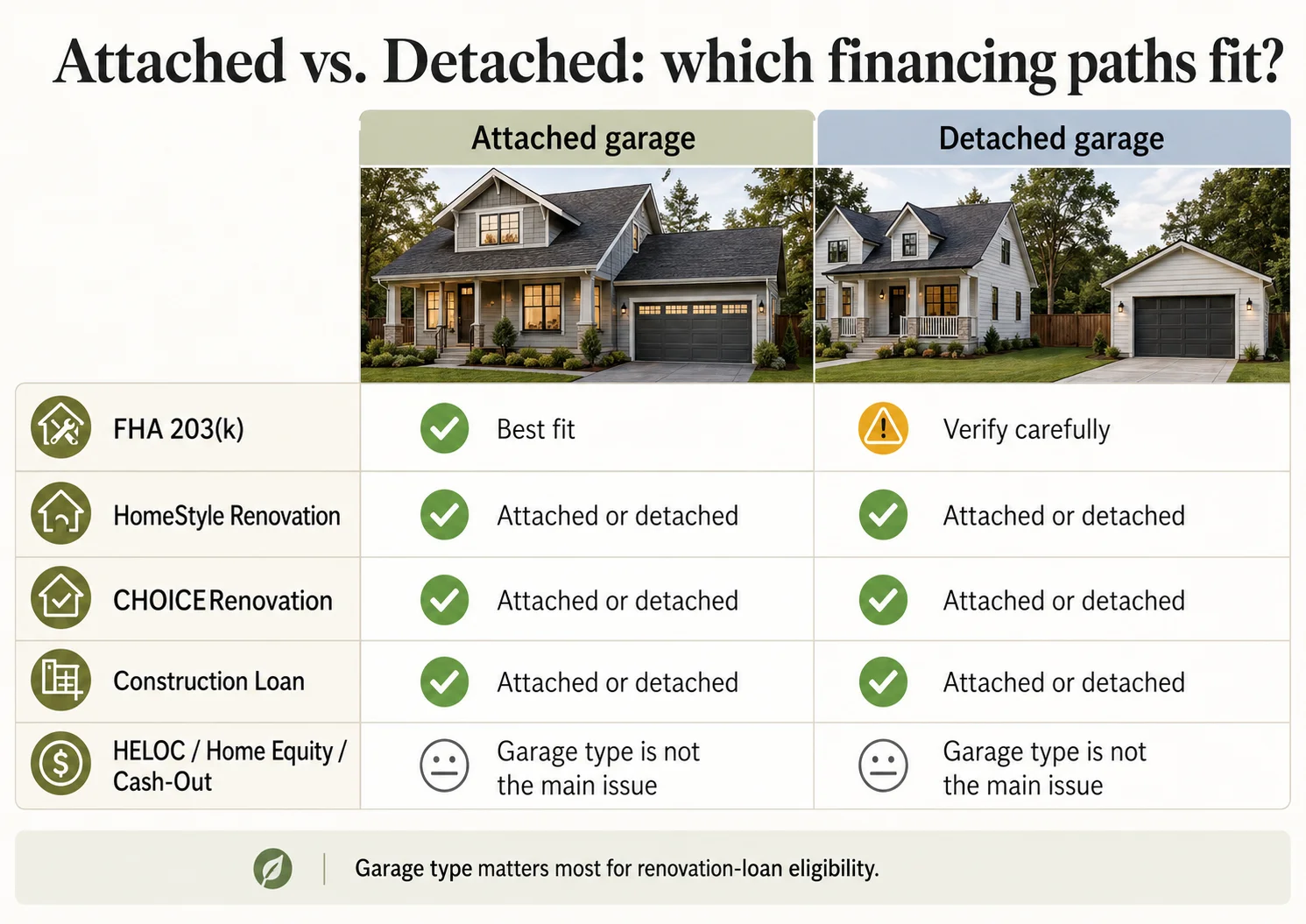

Can renovation mortgages — FHA 203(k), HomeStyle, CHOICERenovation — finance a garage conversion ADU?

Yes — renovation mortgage programs are often the best path when your current equity isn’t enough, because they underwrite the home’s after-completion value rather than today’s value alone. The three main programs are FHA’s 203(k), Fannie Mae’s HomeStyle Renovation, and Freddie Mac’s CHOICERenovation. Each can fund eligible ADU work, but they differ on one detail that decides whether your specific garage qualifies: how they treat a detached structure. This is the most expensive surprise in garage-conversion financing, and we’ll make it impossible to miss.

Can FHA 203(k) finance a detached garage conversion ADU?

For an FHA 203(k), a new ADU must be attached to the existing structure — so converting a detached garage into a brand-new ADU generally does not qualify. But renovating an ADU that already exists is eligible whether it’s attached or unattached. In plain terms: if your detached garage is currently just a garage and you want to turn it into a first-ever ADU, 203(k) usually isn’t your lane. If a legal ADU already exists and you’re renovating it, detached is fine. HUD’s own 203(k) eligible-improvements list spells this out: a one-family structure may be converted to include an ADU, a new ADU may be constructed attached to an existing structure, construction of a new detached ADU is not eligible, and renovating an existing ADU (attached or unattached) is eligible.

Because a garage conversion is, by definition, creating a new ADU, the attached requirement is what most converters run into. If your garage is detached, verify with the lender and 203(k) consultant before building your plan around this program — and know that Fannie Mae HomeStyle and Freddie Mac CHOICERenovation both allow detached units, so you have strong alternatives.

| Loan product | Convert ATTACHED garage to new ADU | Convert DETACHED garage to new ADU | Lends against future value? |

|---|---|---|---|

| FHA 203(k) | ✓ Yes (new ADU attached to existing structure is eligible) | ✗ Generally no for a new ADU; ✓ only if renovating an existing unattached ADU | ✓ Yes (after-improved value) |

| Fannie Mae HomeStyle Renovation | ✓ Yes | ✓ Yes (detached accessory units allowed) | ✓ Yes (renovation costs capped at 75% of as-completed value) |

| Freddie Mac CHOICERenovation | ✓ Yes | ✓ Yes (garage/barn/shed conversions cited, if legally permissible) | ✓ Yes |

| Construction-to-permanent | ✓ Yes | ✓ Yes | ✓ Yes (as-completed appraisal) |

| HELOC / home equity loan / cash-out refi | ✓ Yes | ✓ Yes (not structure-dependent) | ✗ No (current value only) |

Sources: HUD 203(k) program guidance and the FHA 203(k) eligible-improvements list (new ADU must be attached; new detached ADU ineligible; renovating an existing attached or unattached ADU eligible); Fannie Mae HomeStyle Renovation product page and FAQ; Freddie Mac Accessory Dwelling Units page. Last verified .

FHA 203(k) — Limited vs. Standard

The 203(k) combines a purchase or refinance with rehabilitation funds in one loan, released as work is completed. Two flavors:

- Limited 203(k): for minor remodeling and nonstructural repairs; total rehabilitation costs may not exceed $75,000 (raised from the old $35,000 cap under HUD Mortgagee Letter 2024-13). Faster and simpler.

- Standard 203(k): for larger or structural rehabs, including eligible attached garage-to-ADU conversions. Requires a HUD 203(k) consultant and more documentation.

Across both: it’s for owner-occupied primary residences, allows credit scores as low as 580 (or 500 with 10% down), needs a minimum 3.5% down payment, and typically takes 60+ days to close — longer than a standard FHA loan because of the contractor bids and consultant review.

Rental income on a 203(k): if your one-unit property will have an ADU and you have no rental history from it, HUD requires the lender to use 50% of the lesser of the appraiser’s market rent or the lease rent to calculate effective income. ADU rental income cannot be used to qualify for an FHA cash-out refinance.

Fannie Mae HomeStyle Renovation

HomeStyle Renovation can fund renovations to any part of the home, including adding accessory dwelling units, and it allows detached ADUs. Renovation costs must not exceed 75% of the lesser of purchase price plus renovation costs, or the “as-completed” appraised value (for purchases), and 75% of the as-completed value for refinances. It’s a conventional loan, so borrowers who put enough down can avoid FHA mortgage insurance — making it the natural home for a detached garage conversion that needs after-completion value.

Freddie Mac CHOICERenovation

Freddie Mac’s CHOICERenovation similarly funds renovations using after-completion value and explicitly contemplates converting a garage, barn, or shed into an ADU — provided the ADU is legal or legally permissible. It’s a strong alternative to HomeStyle for borrowers whose lender prefers Freddie Mac products.

What every renovation program will require

| Requirement | Why it matters |

|---|---|

| Contractor bid | The lender needs a defined scope and cost |

| Plans / specifications | Supports the appraisal and renovation review |

| Appraisal (often as-completed) | Establishes the value the loan is sized against |

| Permit path | The ADU must be legal or legally permissible under program rules |

| Draw process | Funds release in stages tied to construction milestones |

| Certificate of occupancy / final inspection | Renovation programs require evidence the work is complete and signed off |

| Contingency reserve | Required or strongly recommended for construction uncertainty |

Use our research partner to explore whether a refinance or renovation pathway fits your project. Availability and qualification depend on your state, credit, income, property, and lender rules.

Affiliate link — we may earn a commission at no extra cost to you. Not a loan offer or approval guarantee.

Compare garage ADU mortgage paths →Can the future rent help you qualify? The 2026 rule change explained

Yes, for eligible loans. Under Fannie Mae Selling Guide Announcement SEL-2025-08, rental income from one ADU can now count toward qualifying income on a one-unit principal residence — but only on purchase or limited cash-out refinance transactions, capped at 30% of your total qualifying income, using 75% of the market or lease rent. Lenders could apply this manually starting October 8, 2025; the automated system caught up with Desktop Underwriter (DU) version 12.1, implemented the weekend of March 21, 2026, which now applies the ADU-income rules to new loan casefiles. FHA has a parallel allowance for some borrowers. This is the change that can tip a borderline applicant into qualifying — though the caps and documentation are specific.

The 2026 rule, in dollars

Say your qualifying income is $6,000/month and the ADU’s market rent is $1,200/month.

The lender counts 75% of that rent = $900.

The rule caps usable ADU income at 30% of your total — and $900 added to $6,000 brings your total to $6,900, with the $900 sitting comfortably inside that 30% cap.

Your qualifying income becomes $6,900/month.

Illustrative example, not a guarantee of returns or approval. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

What the lender will need

- A traditional Form 1004 (URAR) appraisal plus a Single-Family Comparable Rent Schedule (Form 1007) specific to the ADU.

- A lease, or tax returns if there’s existing rental history.

- Evidence the ADU is legal or legally permissible.

- Standard borrower income and debt documentation.

The honest caveats

The rule is real, but adoption is lender-by-lender for manually underwritten loans, so ask your lender directly whether they’re applying it. And mind the boundaries: it applies to purchase and limited cash-out refinance transactions on one-unit principal residences only, counts one ADU even if you have several, and — on the FHA side — ADU rent generally can’t qualify a cash-out refinance. Projected rent can genuinely help, but it’s capped and document-heavy. Don’t build your plan on “the unit pays for itself” until a lender confirms the rule applies to your loan.

What if you don’t have enough equity?

If you don’t have enough current equity, don’t start with a HELOC — start with a future-value renovation loan, a construction-to-permanent loan, a local housing program, or a scope-down plan. Renovation mortgages (HomeStyle, CHOICERenovation, 203(k)) and construction loans underwrite the home’s after-completion value, which can dramatically increase borrowing power versus today’s equity. If repayment capacity — not equity — is the real constraint, reducing scope or waiting is safer than forcing the project.

Construction-to-permanent loans deserve a specific mention. A construction-to-permanent loan funds the build in stages (draws) tied to verified milestones — foundation, framing, rough-in, finishes — then converts to a permanent mortgage at completion without a second closing. Because it’s sized to the as-completed value, it doesn’t require large existing equity, which makes it a strong fit for recent buyers or larger/detached builds where a HELOC would fall short. The tradeoffs: more paperwork, lender-controlled draws and inspections, and it creates a new first mortgage (so you’d lose a low existing rate).

| If your situation is… | A better path than a HELOC |

|---|---|

| Recent purchase, little equity built | FHA 203(k), HomeStyle, CHOICERenovation, or construction-to-permanent |

| Rental-income-driven ADU | A program that allows documented ADU rent (see the 2026 rule above) |

| Quote is simply too high | Scope down, phase nonessential finishes, or revisit feasibility |

| Income is the constraint, not equity | Avoid overleveraging; model rent conservatively, or wait |

| Property may not even qualify | Run a feasibility check before applying for anything |

There’s also the home equity investment (HEI) category for owners who can’t qualify for loans: an investor gives you cash today in exchange for a share of your home’s future value, with no monthly payment. It’s a real option for the loan-constrained, but you owe a share of future appreciation, and these products are available in limited states — check availability where you live.

If little equity is your situation, we go deeper here: how to finance an ADU with no equity.

What should you verify before applying for garage conversion ADU financing?

Before you apply, verify three things: that the garage can legally become an ADU, that your budget includes soft costs and a contingency, and that you have the documents a lender will ask for. Financing before feasibility is where homeowners waste the most time — applying for a loan on a project the property can’t legally support, or for an amount that won’t finish the unit. The two checklists below are the ones to run first.

Feasibility checklist — and what it means for your loan

We added a column most checklists skip: what actually happens to your financing if a given item fails. That’s the part that costs money.

| Check | Why it matters | Loan impact if it fails |

|---|---|---|

| ADU allowed on the property | Lenders and appraisers care whether the ADU is legal or legally permissible | Appraisal and rental-income support can fail; some programs won’t lend at all |

| Garage condition (slab, framing, moisture, ceiling height) | Determines whether this is a simple conversion or major construction | A required structural rebuild raises gap risk on a HELOC/personal loan and may force a renovation or construction loan |

| Separate entrance + independent living facilities | ADUs must be independently habitable | Without them the unit may not meet the program’s ADU definition |

| Kitchen and bathroom plan | Required for legal ADU use | Missing facilities can disqualify the unit as an ADU |

| Utilities (electrical, plumbing, sewer, HVAC) | Can materially change cost; trenching to a utility lateral is a common surprise | Underestimating this is the most common reason a loan ends up too small |

| Fire / life safety separation | Especially important for attached garages | Code-required upgrades add to scope and must be financed |

| Parking / parking replacement | Varies by local rules | Can block the permit, which blocks legal completion |

| Certificate of occupancy / final sign-off | Renovation loans need proof the work is complete | The renovation phase can’t fully close until inspection/CO evidence is obtained |

| HOA or deed restrictions | May block or complicate the project | Can stop the project regardless of financing |

| Rental rules | Matters if you’re counting on rental income | Limits whether projected rent can be used to qualify |

Lender document checklist

| Bring this | Why |

|---|---|

| Current mortgage statement | Helps assess equity and refinance implications |

| Estimated home value | Needed for the equity test and CLTV |

| Contractor estimate | Supports the loan amount and scope |

| Plans or preliminary drawings | Supports appraisal and renovation review |

| Permit status | Shows whether the project is feasible |

| Tax returns / W-2s / pay stubs | Income qualification (P&L if self-employed) |

| Insurance information | Some renovation loans require coverage review |

| Rent estimate or lease support | Only if using rental income to qualify |

| HOA documents | If HOA restrictions apply |

Use this before your lender call so you’re not comparing loans for a project your property can’t support. Our feasibility report checks what you can legally build at your address and gives you a realistic budget band to bring to the conversation.

See What You Can Build → Get Your Free ADU ReportWhich financing path fits your situation? A quick segmentation

Match your project type and primary constraint to the first lane to test. The right answer for a homeowner with a low-rate mortgage and high equity differs from the right answer for a recent buyer with little equity, which differs again for someone counting on rent to qualify. Use this as a fast self-sort, then verify with a feasibility check and a lender.

- Strong equity + want to keep your first mortgage → HELOC or home equity loan.

- Equity + your current rate is already high → compare a cash-out refinance against home equity options.

- Recent buyer or limited equity → a renovation/future-value loan (HomeStyle, CHOICERenovation, 203(k)) or construction-to-permanent.

- Attached garage + lower credit or down payment → FHA 203(k) is worth a look.

- Detached garage → verify FHA 203(k) first; if it’s not already an existing ADU eligible for renovation, route to HomeStyle, CHOICERenovation, construction, or home-equity products.

- Small one-car conversion or a funding gap → cash, savings, or a personal loan, only if the permitted total is modest. (When does a personal loan actually make sense?)

- Building for family, not rent → prioritize payment stability and feasibility over rental-income assumptions.

- Building for rental income → model rent conservatively and confirm whether your lender can use the 2026 ADU rent rule.

- Can’t qualify for a loan but have equity → a home equity investment (check state availability).

Run your exact numbers. The Financing Path Matcher turns this list into a single recommended lane for your property.

See what’s possible at your address →What garage conversion financing mistakes should you avoid?

The biggest mistakes are financing before confirming feasibility, borrowing from a rough quote instead of a permit-ready budget, using the wrong loan type for the scope, and counting on rental income before a lender confirms it qualifies. Each is avoidable with one extra step of verification, and each can cost five figures if skipped.

- Mistake 1 — Financing before feasibility. Don’t borrow against your home until you’ve confirmed the garage can legally become an ADU. An unpermitted conversion creates appraisal, insurance, resale, rental, and enforcement risk.

- Mistake 2 — Borrowing from a rough contractor quote. A real ADU budget includes permits, plans, utilities, code work, contingency, and soft costs — typically 15–25% over the bare construction number.

- Mistake 3 — Using a personal loan for a full ADU budget. Personal loans (often up to ~$100,000) fit small scopes or gap funding, but many permitted garage ADUs exceed practical unsecured limits, and rates run higher than home-secured options.

- Mistake 4 — Replacing a good first mortgage without comparing alternatives. A cash-out refi can be the right call — but not just because it’s simple. Run the second-position comparison first.

- Mistake 5 — Assuming projected rent will qualify you. The 2026 rules help, but they’re capped (30% of income, 75% of rent on the Fannie side), limited to purchase and limited cash-out refinances, and rent generally can’t qualify an FHA cash-out refinance.

- Mistake 6 — Misreading the FHA detached-garage rule. Building around FHA 203(k) for a detached garage that isn’t already an ADU is a common dead end, because a new ADU must be attached. Check structure eligibility before you choose a program.

What we verified

We built this page from primary and authoritative sources, not competitor paraphrasing. Verified for this edition ():

- HELOC and home equity loan definitions and differences — CFPB consumer guidance.

- Right-of-rescission timing on refinances — CFPB.

- FHA 203(k) mechanics, the eligible-improvements list, the $75,000 Limited cap, and the 50% rental-income calculation — HUD 203(k) program guidance and HUD Mortgagee Letter 2024-13.

- FHA cash-out ADU rental-income limitation — HUD.

- Fannie Mae HomeStyle Renovation ADU eligibility (including detached units) and the 75%-of-as-completed-value cap — Fannie Mae HomeStyle product page and FAQ.

- The 2026 ADU rental-income rule (one-unit principal residence, purchase or limited cash-out refinance, one ADU, 30% cap, 75% of rent) and DU 12.1 implementation (weekend of March 21, 2026) — Fannie Mae Selling Guide Announcement SEL-2025-08 and the DU Version 12.1 release notes.

- Freddie Mac CHOICERenovation ADU eligibility (garage/barn/shed conversions, legally permissible) — Freddie Mac Accessory Dwelling Units page.

- VA cash-out refinance basics and closing-cost caution — U.S. Department of Veterans Affairs.

- Garage conversion cost ranges — Angi 2026 data, regional California builder references, a Portland-area architect reference, Maxable, and SnapADU (San Diego County, regional).

What we don’t claim: we don’t promise rates, payments, approvals, savings, rental income, or permit approval. Cost bands are early planning estimates that vary by market, and program rules can change after our verification date.

Methodology

This guide was created by The Dwelling Index — an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder. For financing rules, we cite HUD, Fannie Mae, Freddie Mac, the CFPB, and the VA. For costs, we cite multiple published references and mark local estimates as market-specific. For partner links, we disclose material connections and never rank providers by compensation — financing content here presents lanes, sorted by neutral criteria (rate protection, equity required, structure eligibility), not “best lender” rankings. We used homeowner discussion threads only to understand the questions people ask and the language they use, never as proof for legal, lending, or cost claims. We re-verify rates and program rules on a regular cadence.

Frequently asked questions

- Can you get a loan to convert a garage into an ADU?

- Yes. Common paths include HELOCs, home equity loans, cash-out refinances, renovation mortgages (FHA 203(k), Fannie Mae HomeStyle, Freddie Mac CHOICERenovation), construction-to-permanent loans, personal loans for smaller scopes, and cash. The right path depends on your equity, income, garage condition, permit feasibility, and project cost.

- What is the cheapest way to finance a garage conversion ADU?

- Usually the path that avoids unnecessary refinancing and high-cost unsecured debt. For a homeowner with strong equity and a favorable first mortgage, that’s often a HELOC or home equity loan that leaves the low first mortgage in place. For a homeowner without enough current equity, a renovation loan that uses after-completion value is typically more realistic than an expensive personal loan.

- Can I use a HELOC to build an ADU?

- Yes, if you qualify and have enough equity. A HELOC suits staged construction because you draw funds as needed and pay interest only on the drawn balance during the draw period. The main cautions are a variable rate (it tracks the prime rate) and that it’s based on your current equity, not the ADU’s future value.

- Can FHA 203(k) finance a detached garage conversion?

- For a 203(k), a new ADU must be attached to the existing structure, so converting a detached garage into a brand-new ADU generally doesn’t qualify. Renovating an ADU that already exists is eligible whether attached or unattached. For a detached garage that isn’t yet an ADU, look to Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, a construction loan, or home-equity products, all of which allow detached units.

- Can I use Fannie Mae HomeStyle Renovation for a garage conversion ADU?

- Yes. HomeStyle Renovation can fund renovations including adding accessory dwelling units, allows detached units, and underwrites the home’s as-completed value (renovation costs capped at 75% of as-completed value), subject to program and lender rules.

- Can future ADU rent help me qualify for financing?

- Sometimes. Under Fannie Mae’s rule (SEL-2025-08), rental income from one ADU can count toward qualifying income on a one-unit principal residence, but only for purchase or limited cash-out refinance transactions, capped at 30% of total income and using 75% of market or lease rent. DU applied this automatically starting with version 12.1 in March 2026. FHA allows a portion for some borrowers but generally not for cash-out refinances. Confirm your lender’s approach.

- How much does a garage conversion ADU cost?

- Published sources show wide ranges. Angi reports a garage-conversion average around $110,000 with one-, two-, and three-car ranges; regional California and Portland builder sources often place standard two-car ADU conversions in the mid-six figures depending on scope and market. Budget the permit-ready total — typically 15–25% above the bare construction quote.

- Should I use a personal loan for a garage conversion ADU?

- A personal loan may fit a small conversion, design/permit costs, or a funding gap. It’s usually a poor fit for a full permitted ADU, since costs often exceed practical unsecured-loan limits (commonly up to ~$100,000) and rates run higher than home-secured options.

- Do I need permits before getting financing?

- You may not need final permits before the first lender conversation, but you should confirm the ADU is legally feasible. Many renovation and construction loan paths require plans, bids, appraisals, and permit-related documentation before closing or before releasing construction draws.

- What if my garage has to be rebuilt?

- Treat it as major construction, not a simple conversion. That can shift the best financing path from a HELOC or personal loan to a renovation mortgage or construction-to-permanent loan, and it changes the budget materially — confirm scope with an engineer before sizing a loan.

- Is a garage conversion ADU worth it?

- It can be, especially when the garage is structurally usable, legally convertible, and the ADU solves a housing or income need. It’s less attractive when the garage needs major rebuilding, local rules limit rental income, or financing costs make the project too risky. Run a feasibility check before committing.

Get the free ADU Starter Kit

Want the whole roadmap in one place? Download the free ADU Starter Kit — permits, costs, and a garage conversion financing checklist you can take straight to your lender call.

Download the free ADU Starter Kit →Related reading on The Dwelling Index

- Compare all ADU financing options — the full 8-path overview across every ADU type.

- How to finance an ADU with no equity — future-value and low-equity paths in depth.

- Using a home equity loan or HELOC for an ADU — when second-position debt is the right call.

- ADU grants in 2026: verified programs by state — to offset costs before you borrow.

- How much does a garage conversion ADU cost? — full cost breakdowns by type and market.

Not sure where to start?

See what’s possible at your address — get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU Report