Personal Loan for ADU: When It Works, When It Doesn't

By The Dwelling Index Editorial Team · ·

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder.

Quick answer: yes — but only in 4 specific situations

Yes, you can use a personal loan for an ADU — but it's the right tool in only four specific situations: (1) your total project cost is under roughly $100,000 like a one-car garage conversion, (2) you're a recent buyer with little equity but strong income and credit above 700, (3) you need short-term gap or soft-cost funding layered on top of another loan, or (4) you need to move fast on a deposit or permit fee.

Home-improvement personal-loan APRs run roughly 6%–36% with an average of 12.27% (Bankrate Monitor, May 13, 2026), and most mainstream lenders cap unsecured loans at $100,000. If your ADU is a full detached build or any project over $100,000, a HELOC, home equity loan, or renovation loan will almost always cost less over the life of the loan.

Above-the-fold verdict — find your situation

| If you're… | Personal loan verdict | Read this section |

|---|---|---|

| Funding a one-car garage conversion under $100k | Likely fits | Scenario 1 |

| A recent buyer with no equity but strong income | Likely fits | Scenario 2 |

| Funding permits, design, deposits, or a small gap | Strong fit | Scenario 3 |

| Racing a builder deadline and your credit is solid | Conditional fit | Scenario 4 |

| Building a full detached ADU over $100k | Wrong tool | Walk away |

| Credit below 670 | Wait and fix credit first | Walk away |

60 seconds, no obligation, before you compare loans.

What we verified for this guide

We built this page so you can stop searching. Here's what we checked, where, and when:

- Average personal-loan rate of 12.27% APR — Bankrate Monitor, dated May 13, 2026.

- 24-month commercial-bank personal-loan rate of 11.40% (February 2026 observation; 11.65% was November 2025) — Federal Reserve FRED series TERMCBPER24NS.

- Home-improvement personal-loan range of approximately 6%–36% APR — NerdWallet 30-day pre-qualification aggregate, May 2026.

- Typical home-improvement personal-loan size of $1,000–$100,000 with terms of 1–7 years — Bankrate, March 2026.

- LightStream/Truist home-improvement loans of $5,000–$100,000 with terms 24–240 months and current public APR range of 6.74%–20.94% with AutoPay — Bankrate and Truist/LightStream, May 2026.

- SoFi personal-loan APR range of 7.74%–35.49% after discounts — SoFi disclosure, March 24, 2026.

- HFS Financial is not a direct lender — it markets access to home-improvement personal loans through third-party lenders, with a stated max amount of $450,000, rates as low as 7.8%, and terms from 1–30 years — hfsfinancial.net, March 2026.

- BHG Financial unsecured personal loans of $20,000–$250,000, terms 3–10 years, APR range 8.72%–28.89%, minimum credit 640, not available in Illinois or Maryland — bhgfinancial.com, May 2026.

- Patelco ADU HELOC posted APR of 8.25% (California only, most qualified applicant, CLTV up to 125%) — patelco.org, May 5, 2026.

- Fannie Mae rental income from an existing ADU on a one-unit principal residence, capped at 30% of qualifying income, for purchase and limited cash-out refinance only — Fannie Mae Selling Guide B3-3.8-01 and SEL-2025-08 (October 8, 2025).

- Fannie Mae HomeStyle Renovation permits up to 50% of total renovation costs disbursed at closing including permit fees, design, and architectural services — Fannie Mae HomeStyle FAQs.

- CFPB guidance on secured vs. unsecured loans and consequences of default — consumerfinance.gov.

- FTC guidance on advance-fee loan scams — consumer.ftc.gov.

- IRS rules on home-mortgage and home-equity interest deduction — IRS Publication 936.

- MassHousing ADU Loan Program — up to $250,000 detached / $150,000 attached, income-eligible — masshousing.com/adu, announced January 14, 2026.

- NYC Plus One ADU — up to $395,000 combined financing, reopened March 2026 — nyc.gov/hpd.

- CalHFA ADU Grant status — fully allocated since December 28, 2023; reservation portal closed — CalHFA Program Bulletin 2023-14.

- Garage conversion ADU national average of $110,000 — one-car range $36,000–$96,000; two-car range $45,000–$120,000 — Angi 2026 data.

- Detached new-construction ADU range of $110,000–$285,000 — Angi 2026 ADU cost data.

- California ADU median construction cost of approximately $150,000 / ~$250 per square foot — Terner Center for Housing Innovation.

- Los Angeles ADU costs of approximately $300–$400 per square foot, $250/sf minimum, permits/fees $5,000–$20,000 — GreatBuildz 2026 LA cost guide.

Anything in this guide we couldn't verify against a primary or highly reliable source is explicitly marked [needs verification] so you know to check it yourself before acting on it.

Can you use a personal loan to build an ADU?

Answer capsule: Yes. Personal loans are commonly used for home improvement, and ADU construction can qualify — but each lender's use-of-funds clause controls. For projects under approximately $100,000, typically one-car garage conversions and small basement finishes, a personal loan can be a defensible choice. For full detached ADUs or projects above $100,000 where the homeowner has equity, a HELOC or renovation loan will almost always cost less.

Most ADU-financing articles you'll read fall into two camps. Lender-funnel pages call personal loans “the best option” because that's what they sell. Renovation-loan companies call them “one of the dumbest things homeowners do.” Both are conflicts of interest dressed up as advice. The truth sits in the middle, and it depends on numbers you already know about your own situation.

Damaging admission, since we're being honest: a personal loan creates a real cash-flow squeeze that secured loans usually don't. A $100,000 personal loan at the May 2026 average rate of 12.27% APR over seven years is roughly a $1,780 monthly payment — fixed, no interest-only period, no flexibility if a slow construction month hits. That 's not a small commitment, and we'd be lying if we pretended it was. But here's the upside that nobody else writes down clearly: for the right project, a personal loan funds in 24–72 hours instead of six weeks, doesn't put your home at risk of foreclosure, and lets a recent buyer with no equity actually move forward instead of waiting three years to build equity they may never have. Used in the four scenarios below, that trade is the right one. Used as a default because nobody told you about better paths, it isn't.

A quick precision point most ADU pages skip: a personal loan being “for home improvement” doesn't automatically mean the lender will fund ADU construction. The use-of-funds clause controls. Truist/LightStream, for example, explicitly allows paying contractors, supplies, and permit fees. SoFi offers home-improvement loans but restricts certain real-estate uses. Confirm ADU construction, permits, deposits, and contractor payments are permitted before you apply, not after.

By the end of this guide, you'll know exactly whether a personal loan fits your specific ADU scope — and if it doesn't, which financing path actually does. We don't sell personal loans, we're not paid by any of the lenders named on this page, and we'll tell you to walk away from this product if a HELOC or renovation loan would serve you better. That's the standard.

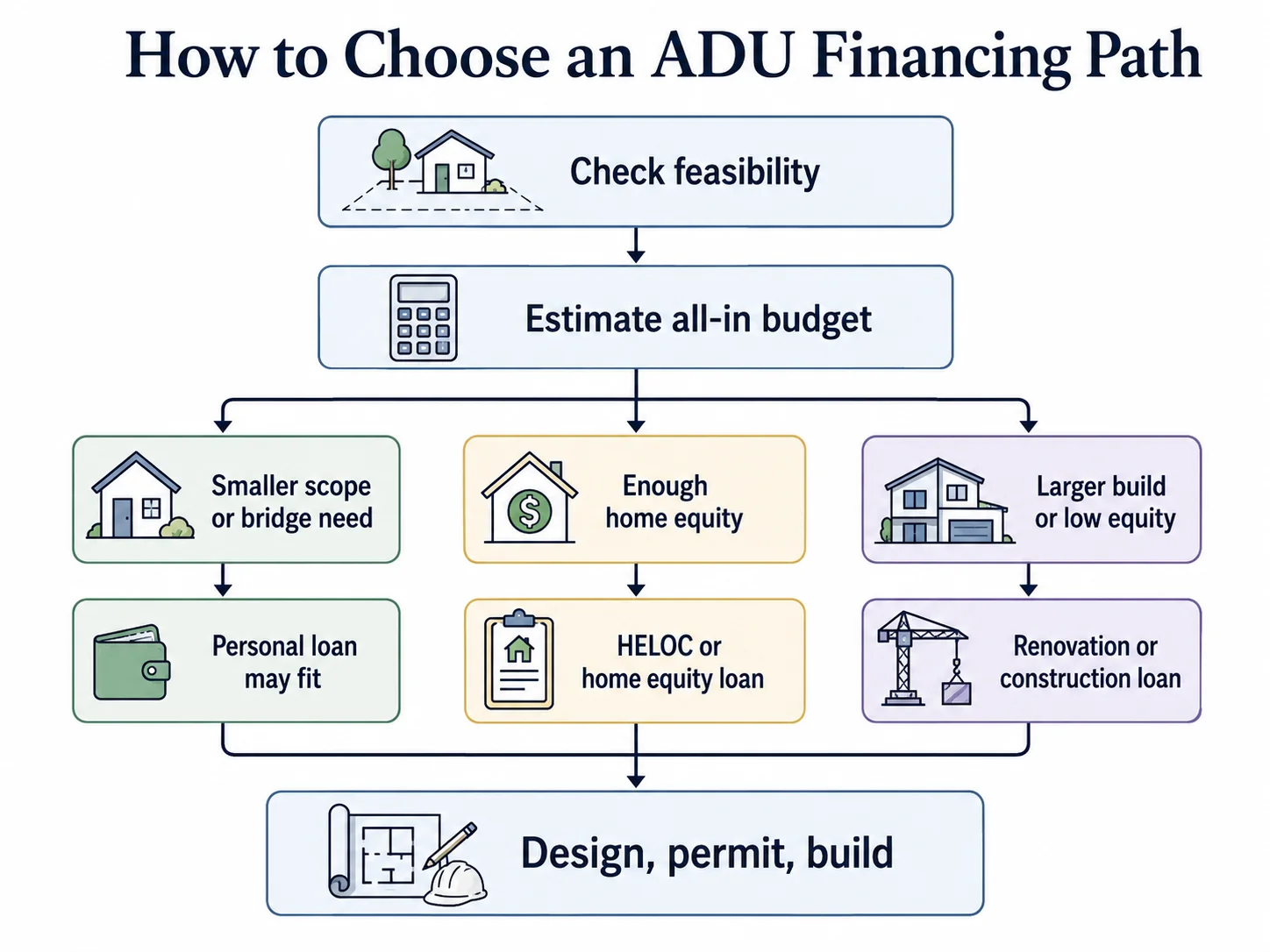

Before you compare a single lender, verify your lot can support the ADU you want. Zoning, setbacks, utility hookups, and lot coverage rules can change your budget by tens of thousands of dollars or rule out the project entirely. Every dollar you borrow before you check feasibility is a dollar at risk.

Free, 60 seconds, your zip code and address.

When a personal loan IS the right tool for an ADU — 4 scenarios

Answer capsule: A personal loan is the right tool for an ADU in four specific situations: (1) the total project cost is under approximately $100,000, typically a one-car garage conversion or basement finish, (2) you're a recent buyer with little home equity but strong income and credit above roughly 700, (3) you're using the loan as short-term gap or soft-cost funding layered on top of another loan, or (4) you need to move fast on a builder deposit or permit deadline and your credit can absorb the higher rate. Outside these four scenarios, a home-equity product or renovation loan will almost always serve you better.

Below is the framework no other ADU page has assembled. We built it by combining current personal-loan size and rate data with verified ADU cost ranges by project type. If your situation maps to one of these four scenarios, a personal loan deserves a serious look. If it doesn't, skip to the alternatives section.

Scenario 1 — Your total ADU project cost is under approximately $100,000

The mainstream personal-loan ceiling is $100,000. LightStream, SoFi, and most major online lenders cap unsecured loans there. The ADU project types that consistently fit under $100,000 are:

- One-car garage conversions at the lower end of the cost range. Angi's 2026 data puts the one-car range at $36,000–$96,000 depending on whether utilities, structural work, and finishes are simple or complex. Note: $96,000 plus a recommended 15% contingency ($14,400) lands above $100,000 — so for high-end one-car conversions you'd be a small surprise away from the cap.

- Basement finishes that are already plumbed. Existing rough plumbing and adequate ceiling height bring the cost down dramatically.

- Interior conversion ADUs that don't require utility laterals, foundation work, or structural changes.

If your contractor estimate plus a 15% contingency plus soft costs lands under $100,000, a personal loan is in the running. Above that, you have two options: layer the loan on top of another source, or move to a different product entirely.

A note on lender claims of higher ceilings. HFS Financial markets access to home-improvement personal loans up to $450,000 through third-party lenders (HFS is a marketplace, not a direct lender — see their disclaimer). BHG Financial offers personal loans up to $250,000, but the program is structured for high-income borrowers — a $100,000 minimum income, minimum credit score of 640, and APR range of 8.72%–28.89% per BHG's published terms. BHG personal loans are not currently available in Illinois or Maryland. Treat the higher ceilings as lender-specific exceptions, not the market baseline.

Scenario 2 — You're a recent buyer with little equity but strong income

This is the homeowner the rest of the internet ignores. You bought your home in the last three to five years. You have less than 15%–20% equity. You make $150,000+. Your credit score is 720 or higher. You can't get a HELOC because HELOCs require equity — most lenders want 80%–85% combined loan-to-value, which you don't have.

Personal loans don't price you on equity. They price you on income, credit, and debt-to-income ratio (DTI). For this profile, the rate spread between a personal loan and a HELOC may still favor the HELOC if you could qualify — but you can't. So the relevant comparison isn't personal loan vs. HELOC. It's personal loan vs. doing nothing for three more years while you build equity you may never have.

If you can comfortably absorb the monthly payment without pushing your DTI above 40%, and you're funding a project that genuinely makes sense, a personal loan can move you forward when the equity products lock you out. See also: how to finance an ADU with no equity.

Scenario 3 — You need short-term gap or soft-cost funding

Many ADU projects need money in two phases that traditional construction loans don't always cover cleanly:

- Pre-construction soft costs. Architectural plans, permit fees, surveys, soils reports, feasibility studies. [needs verification] These can run roughly $8,000–$25,000 before a contractor breaks ground, based on common builder estimates, but the actual range varies by jurisdiction.

- Builder deposits. Many ADU builders require 10%–30% upfront before mobilization, often before your construction or renovation loan funds.

- Change-order and contingency overruns. A site condition you didn't expect — bad soil, an undersized electrical panel, a sewer lateral that needs replacement — can blow past the contingency in your main loan.

A personal loan used as a bridge to cover these gaps and paid off aggressively from rental income or refinanced into the permanent financing is a defensible play. The pattern works when you have a clear payoff plan and a primary loan already committed.

One worth flagging: Fannie Mae's HomeStyle Renovation program allows up to 50% of total renovation costs to be disbursed at closing, with permit fees, architect fees, and design/planning costs eligible per Fannie Mae's HomeStyle FAQs. If you're already moving toward a HomeStyle loan, that bridge may be covered by the main product — no separate personal loan needed. Confirm with your lender before adding unsecured debt.

Scenario 4 — You need speed and your credit can absorb the rate

HELOCs typically take 3–6 weeks to close. Construction loans take 6–10 weeks. Renovation loans can take 60–90 days. Personal loans fund in 24–72 hours after approval. LightStream and SoFi both advertise same-day funding for qualified applicants.

If your builder has a slot opening next month, you need to lock a permit fee within two weeks, or your design team needs payment to start drafting plans, the speed premium can be worth the rate. Quick math: a $30,000 personal loan at 12% APR for 24 months has a monthly payment of approximately $1,412 and costs roughly $3,893 in total interest. If waiting eight weeks for a HELOC means losing the builder slot and pushing the project six months, the time cost may exceed the rate premium.

This scenario only works if the deposit-sized loan can be paid off fast — typically two to four years — and if your credit profile keeps the rate in the single digits or low teens. If your rate would push above 18%, the speed premium evaporates.

If none of these four scenarios describes you, a personal loan probably isn't your best path. The rest of this guide walks you through what is — including a side-by-side cost comparison with HELOCs and a decision tree for what to do when your ADU budget is too large for unsecured financing.

Free ADU Starter Kit

Costs by state, financing path decision tree, and the questions to ask any builder.

Download the Free ADU Starter Kit →Verify your project before you borrow.

When a personal loan is NOT the right tool — 3 scenarios to walk away

Answer capsule: Don't use a personal loan as your sole ADU funding source if (1) your total project cost exceeds approximately $100,000 and you have any meaningful home equity, (2) your credit score is below 670, where personal-loan APRs typically push above 18% and the monthly payment becomes punishing, or (3) you're already carrying high-interest debt that has pushed your DTI above 40%. In each of these cases, a HELOC, home equity loan, or renovation loan will almost always produce a lower lifetime cost, even accounting for closing costs and the longer underwriting timeline.

Walk away if your ADU is a full detached build

A detached ADU in most U.S. markets runs $110,000–$285,000 per Angi 2026 ADU cost data. In high-cost markets like Los Angeles, GreatBuildz's 2026 LA cost guide puts ADU construction at approximately $300–$400 per square foot, with $250/sf as an absolute minimum and permits/fees of $5,000–$20,000. The mainstream personal-loan ceiling is $100,000. The math doesn't work.

Yes, specialty lenders like BHG can extend higher. But the rate spread between an unsecured loan and a HELOC at this size is meaningful. On a $200,000 loan over seven years, the difference between 12% (current personal-loan average) and 8.25% (a current ADU HELOC rate from Patelco, May 2026) is approximately $32,600 in total interest. That's a meaningful sum no matter how you frame it.

If you have equity, use it. If you don't have equity, look at renovation loans like Fannie Mae HomeStyle or Freddie Mac CHOICERenovation, which underwrite to the after-renovation value — meaning your current low equity isn't a blocker.

Walk away if your credit score is below 670

Personal-loan APR is steeply tiered by credit band. At 720+, you're in the high single digits to low teens. At 700–719, you're in the low to mid-teens. Below 670, you can expect 18%–36% based on Bankrate's current personal-loan rate data. Many online lenders' APR ranges top out near 36%; federal credit unions are legally capped at 18%, which is one reason credit-union membership becomes valuable at this credit profile.

At 24% APR, a $50,000 loan over five years costs roughly $36,300 in interest. The monthly payment is $1,438. That's not financing an ADU — that's mortgaging the next five years of your life. If your credit is below 670, fix it first (or look at a co-signed loan with a creditworthy family member through a lender like SoFi that allows joint applications).

Walk away if you're already at high DTI

Most personal-loan lenders cap approved borrowers at 40%–45% DTI [needs verification on exact thresholds — varies by lender]. Specialty lenders like BHG underwrite higher DTIs when income is substantial per BHG's stated criteria. But the rate they offer at 50% DTI will be brutal.

DTI math is straightforward: total monthly debt payments divided by gross monthly income. If you make $8,000/month and your existing debt payments total $3,500, your DTI is 43.75%. Adding a personal loan payment will likely push you outside the comfort range at most mainstream lenders, and any approval is likely to come at higher pricing or a smaller approved amount.

There's also a downstream consequence. If you're planning to refinance your mortgage or apply for a HELOC after the ADU is built and renting, the personal-loan payment will count against your DTI on that application. Sequence matters.

Is “no lien on my house” the same as “low risk”?

Answer capsule: No. A personal loan is unsecured, meaning the lender does not place a lien on your home and cannot foreclose if you default. But the consumer-protection consequences of default are still serious: missed payments damage your credit, the lender can send the debt to collections, and the lender can sue and obtain a judgment against you per CFPB consumer guidance on unsecured loans. The “no collateral” benefit is real, but it does not eliminate financial risk — it changes the form of the risk.

What a personal loan does protect

- ✓No appraisal required in most cases — you don't need to prove what your home is worth.

- ✓No home-equity requirement — recent buyers and homeowners with low equity can still qualify.

- ✓No new mortgage lien at origination — your title stays clean.

- ✓Often faster funding than home equity, renovation, or construction loans.

- ✓Fixed rate for the life of the loan — unlike a HELOC, your payment doesn't move with prime.

- ✓No prepayment penalty at most major lenders — pay off early from rental income with no fee.

What a personal loan does not protect

- ✗Your credit score. A serious delinquency (60+ days) can drop a score meaningfully.

- ✗Your monthly cash flow. A $100,000 loan at 12% over five years is approximately $2,225/month.

- ✗Your DTI. Future mortgage and home-equity applications will count this payment.

- ✗Collection actions. Unsecured doesn't mean uncollectable. Lenders can pursue the debt aggressively, including wage garnishment after a court judgment.

- ✗Project underfunding. Borrowing $100,000 for a $150,000 project leaves you with a half-built ADU.

The honest read: a personal loan reduces the type of risk that scares most homeowners (losing the house) and replaces it with a different type of risk (cash-flow pressure and credit damage). For some homeowners that swap is the right call. For most, it isn't.

Personal loan vs. HELOC for an ADU — 7-year cost comparison

Answer capsule: For homeowners with sufficient equity, a HELOC is meaningfully cheaper than a personal loan over a 7-year horizon. Using May 2026 rate midpoints — a personal-loan average of 12.27% APR (Bankrate Monitor, May 13, 2026) and a current ADU HELOC posted rate of 8.25% APR (Patelco Credit Union, May 5, 2026) — the personal loan costs approximately $8,800 more in interest on a $50,000 loan, $14,000 more on $80,000, and $17,500 more on $100,000 over seven years.

The table below assumes a fully amortized loan with no rate changes over the seven years. HELOC rates are variable and tied to prime — they can rise during the term, which is the major risk a personal loan's fixed rate avoids. Real-world HELOC payments may also start lower during an interest-only draw period and rise during repayment.

Side-by-side cost comparison (illustrative, May 2026 rates)

| Loan amount | Personal loan @ 12.27%, 7-yr | HELOC @ 8.25%, 7-yr (variable, assumed flat) | Difference (interest paid) | Time to funding |

|---|---|---|---|---|

| $50,000 | ~$890/mo, ~$24,750 total interest | ~$786/mo, ~$15,990 total interest | Personal loan costs ~$8,760 more | 24–72 hrs vs. 3–6 wks |

| $80,000 | ~$1,424/mo, ~$39,600 total interest | ~$1,257/mo, ~$25,580 total interest | Personal loan costs ~$14,020 more | Same |

| $100,000 | ~$1,780/mo, ~$49,500 total interest | ~$1,571/mo, ~$31,975 total interest | Personal loan costs ~$17,525 more | Same |

These are illustrative examples, not guarantees of returns. Actual rates depend on your credit profile, lender, state, and current market conditions. Personal-loan rates assume fixed APR throughout; HELOC math assumes the posted rate holds for seven years, which is unlikely — variable rates can rise.

Where the personal loan actually wins

Three legitimate wins, in order of how often they matter:

- You can't qualify for the HELOC. No equity, recent purchase, denied application. If the HELOC isn't on the table, the comparison is academic.

- Fixed-rate certainty. If you believe prime is likely to rise meaningfully during the loan term, the fixed personal-loan rate buys you predictability. The premium you pay over the HELOC's current rate is effectively the cost of that insurance.

- No foreclosure risk. For some homeowners, this is the deciding factor regardless of cost. It's a legitimate preference, but the trade is real money.

Where the HELOC wins (most of the time)

- Lower APR over the life of the loan.

- Higher loan-to-value limits — Patelco's ADU HELOC goes up to 125% CLTV for qualified applicants in California.

- Interest-only payments during the draw period can ease cash flow during construction.

- Larger total available borrowing power for projects above $100,000.

If you have equity and a low-rate first mortgage you want to keep, a HELOC for an ADU, home equity loan, or after-renovation-value (ARV) HELOC is almost certainly your cheapest path.

The Dwelling Index is reader-supported. The link below is an affiliate link to Mortgage Research Center, LLC (NMLS #1907), and we may earn a commission if you use it. Our editorial recommendations are based on independent research and are never influenced by compensation. Read our full disclosure.

Compare HELOC, home equity loan, cash-out refinance, and renovation loan options through Mortgage Research Center, LLC, NMLS #1907.

Is a personal loan better than a construction loan for an ADU?

Answer capsule: Usually no for a full ground-up build. Construction loans are designed for large projects, disburse funds in draws tied to construction milestones, and typically convert to a permanent mortgage upon completion. They're slower (6–10 weeks to close), require more documentation, and add inspection and draw-management overhead. But for projects above $100,000 — especially detached ADUs and additions requiring foundation work and utility laterals — a construction or construction-to-permanent (C2P) loan is almost always the better fit. Personal loans only beat construction loans on small scopes, soft costs, or speed-critical gap funding.

The trade-off is structural. A construction loan disburses in stages, with the lender (and often a third-party inspector) verifying construction progress before each draw. That's friction. But it's friction that protects you: the lender is checking that work has actually been done before more money goes out. A personal loan hands you the full lump sum on day one, and what happens after that is entirely on you.

Three situations where the personal loan still wins against a construction loan:

- Pre-build soft costs the construction loan won't cover until origination. Plans, permits, surveys, and deposits before the construction loan closes.

- Small scopes (under ~$100k) where the construction loan's overhead isn't worth it. A $60,000 garage conversion doesn't need a draw schedule.

- Time-critical situations where waiting 8–10 weeks for the construction loan means losing a builder slot.

For anything larger or more complex, the construction loan or C2P is the right structural fit — even though it's slower and more paperwork.

Is a personal loan better than a renovation loan for an ADU?

Answer capsule: Usually no when the project is over $100,000, especially if you don't have enough equity for a HELOC. Renovation loans like Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, and FHA 203(k) underwrite to the after-renovation value of the property — meaning your post-ADU home value, not your current equity, determines borrowing capacity. That alone makes them the right tool for many recent buyers building larger ADUs. HomeStyle also permits up to 50% of total renovation costs disbursed at closing, including permit fees, architect fees, and design costs, which can eliminate the soft-cost gap that drives many homeowners to personal loans in the first place (Fannie Mae HomeStyle FAQs).

Structural advantages of a renovation loan

- After-renovation value underwriting. Not stuck with current equity as your limit.

- Soft-cost coverage at closing. Up to 50% of total renovation costs (HomeStyle) can be disbursed at closing.

- Single loan structure. No personal-loan payment stacked on top of a future refinance.

- Generally lower rates than unsecured personal loans because the loan is secured by the property.

Real trade-offs

- Longer time to close — typically 60–90 days.

- More documentation — appraisal, plans, contractor bids, scope of work.

- Stricter contractor approval requirements.

- Disbursement happens in draws during construction.

For homeowners who can wait for the underwriting timeline and have a clear scope, HomeStyle and similar ADU renovation loans are usually a better tool than a personal loan for ADU projects above $100,000.

Which ADU projects fit a personal loan — the 2026 Fit Matrix

Answer capsule: A personal loan fits ADU projects where the verified total cost — including design, permits, utilities, construction, and a 15% contingency — lands under approximately $100,000. That generally limits the tool to one-car garage conversions at the lower end of the cost range, simple basement finishes, and soft-cost or gap funding on larger projects. Most attached and detached ADUs exceed the personal-loan ceiling once utility, structural, and site-work realities are priced in.

Sources: Angi's 2026 garage conversion data, Angi's 2026 ADU cost data, Terner Center for Housing Innovation, GreatBuildz 2026 LA cost guide, and owner-reported BuildingAnADU averages (older dataset).

The 2026 ADU Personal Loan Fit Matrix

| ADU project type | Verified 2026 cost range | Personal loan fit | Why | Better first path if not fit |

|---|---|---|---|---|

| Plans, design, feasibility, permits | $8,000–$25,000 typical [needs verification] | Strong fit | Bridge funding before main loan funds; manageable repayment. | Cash reserve, or HomeStyle upfront disbursement. |

| Small gap or contingency funding | $10,000–$40,000 | Strong fit | Layered on top of secured main financing. | Main loan contingency or builder change-order reserve. |

| One-car garage conversion (low end) | $36,000–$65,000 (Angi 2026) | Strong fit | Sits comfortably under the $100k cap with contingency. | HELOC if equity available; personal loan is sensible. |

| One-car garage conversion (high end) | $65,000–$96,000 (Angi 2026) | Conditional | With 15% contingency, top of range approaches $110k. | HELOC, home equity loan, or specialty lender. |

| Two-car garage conversion | $45,000–$120,000 (Angi 2026) | Conditional | Above the loan cap if scope creeps; utilities can push cost. | HELOC, home equity loan, or renovation loan. |

| National average garage ADU conversion | $110,000 (Angi 2026) | Marginal | Just over the standard $100k cap. | HELOC, home equity loan, or renovation loan; specialty lender if equity-blocked. |

| Basement / internal ADU | $75,000–$220,000 [needs verification] | Usually no | Plumbing, egress, fire separation can push costs up. | HomeStyle, CHOICERenovation, FHA 203(k), or HELOC. |

| Attached ADU / home addition | $120,000–$250,000 [needs verification] | Usually no | Behaves like major construction; exceeds unsecured comfort. | HomeStyle, CHOICERenovation, FHA 203(k), C2P loan. |

| Detached backyard ADU (national) | $110,000–$285,000 (Angi 2026); $180,833 owner-reported avg (BuildingAnADU, older dataset) | Rarely | Almost always exceeds personal-loan ceilings and contingency needs. | Renovation loan, construction loan, HELOC if equity available. |

| Detached ADU, high-cost market (LA) | ~$300–$400/sf typical; $250/sf minimum; permits/fees $5,000–$20,000 (GreatBuildz 2026) | No as sole loan | Loan-size mismatch too large; rate spread too costly. | HomeStyle, CHOICERenovation, HELOC, or HEI. |

| Prefab / modular ADU | $100,000–$300,000+ installed | Deposit only | Sticker price ≠ installed cost; site work and utilities add meaningfully [needs verification on exact uplift %]. | Manufacturer financing + secondary product; HomeStyle for full installed cost. |

How to read this matrix

- “Total cost” means installed and permitted, not just the construction contract. Pre-build soft costs and site work both add to the all-in number.

- Contingency. Build a 15% contingency into every estimate. Construction surprises are common.

- Loan size includes contingency. If the contractor quote is $90,000 before soft costs and contingency, add those before sizing the loan.

Match your lot to a realistic ADU scope before you size a loan.

How much can you actually borrow with a personal loan for an ADU?

Answer capsule: Most mainstream personal-loan lenders cap unsecured loans at $100,000, including LightStream/Truist and SoFi. A small set of specialty lenders go higher: BHG Financial offers up to $250,000 for high-income borrowers (minimum income $100,000, minimum credit 640, APR 8.72%–28.89%, not available in IL or MD), and HFS Financial markets access to home-improvement personal loans up to $450,000 through third-party lenders. The amount you actually qualify for depends on credit score (typically 670+ for the higher end), verifiable income, debt-to-income ratio (lenders generally prefer under 40%), and state availability.

Personal-loan options for an ADU (May 2026)

Listed alphabetically. None are paid placements. Dwelling Index has no affiliate relationship with any lender in this table.

| Lender or platform | Type | Loan amount | Term | Published APR (May 2026) | Credit min. | ADU use-of-funds notes |

|---|---|---|---|---|---|---|

| BHG Financial | Direct lender | $20k–$250k | 3–10 yrs | 8.72%–28.89% | 640 | Permits ADU use under home-improvement; not available in IL or MD. |

| HFS Financial | Marketplace (not a lender) | Up to $450k | 1–30 yrs (platform-stated) | As low as 7.8% | Varies | Marketed for home improvement and ADU; HFS is not itself the lender. |

| LightStream (Truist) | Direct lender | $5k–$100k | 24–240 mos (home improvement) | 6.74%–20.94% w/ AutoPay | 660+ typical | Truist confirms contractor pay, supplies, permit fees permitted. |

| SoFi | Direct lender | $5k–$100k | 2–7 yrs | 7.74%–35.49% | Not published | Home improvement permitted; certain real-estate-purchase uses restricted — confirm ADU specifics directly with SoFi. |

| Upgrade | Direct lender | $1k–$50k | Up to 84 mos | Lender-published range | 600 | Origination fee applies; accepts co-signed and secured loans. |

Two important caveats

- “Rate floor” is what virtually nobody pays. LightStream's published 6.74% AutoPay floor requires excellent credit, the right loan purpose, and the right term. Treat floors as aspirational; pre-qualify with a soft inquiry to see your actual offer.

- HFS Financial is a marketplace, not a direct lender. HFS connects borrowers with third-party lenders; HFS itself does not fund loans. Verify the actual lender and approval terms before relying on HFS's advertised ceilings.

How much you'll actually get approved for

Three variables drive your approval amount:

- Credit score. 720+ unlocks the highest loan amounts and the lowest rates. 670–719 narrows your options and pushes rates into the low to mid-teens. Below 670, expect higher rates and lower approved amounts.

- Verifiable income. Most lenders want two years of stable income documentation. Self-employed and 1099 income require additional documentation. BHG and a handful of specialty lenders underwrite complex income profiles more flexibly.

- DTI ratio. Under 40% is generally the comfort zone at most personal-loan lenders; under 30% unlocks the best offers.

Pre-qualifying with two or three lenders via soft inquiry will show you actual offers without affecting your credit. LightStream is a notable exception that doesn't pre-qualify on its own site; check pre-qualified rates through Credible or NerdWallet. A note on hard inquiries: FICO's rate-shopping window deduplicates hard inquiries for mortgages, auto loans, and student loans within a 14–45 day window, but personal-loan inquiries are not currently deduplicated by FICO. Lean on soft-inquiry pre-qualification before any hard pull.

What are current personal loan rates for ADUs in 2026?

Answer capsule: Home-improvement personal-loan APRs range from approximately 6% to 36% as of May 2026 (NerdWallet 30-day pre-qualification data). The Bankrate Monitor reported an average personal-loan APR of 12.27% for the week of May 13, 2026. The Federal Reserve's 24-month commercial-bank personal-loan rate was 11.40% as of February 2026 (down from 11.65% in November 2025). Where your offer lands depends primarily on your credit score.

The honest rate truth

| Credit score band | Typical APR range |

|---|---|

| Excellent (740+) | Roughly 6.5%–10% typical, with autopay and direct-deposit discounts where applicable. |

| Very good (700–739) | Roughly 9%–14% typical. |

| Good (670–699) | Roughly 13%–19% typical. HELOC looks significantly better if you have equity. |

| Fair (620–669) | Roughly 19%–28% typical. Specialty lenders only. |

| Below 620 | Roughly 28%–36% at most online lenders. Consider waiting and improving credit. |

Why the rate matters more than you think

Run the math on a $50,000 ADU loan at three different APRs on a 5-year term:

| APR | Monthly payment | Total interest |

|---|---|---|

| 8% APR | ~$1,014/mo | ~$10,830 |

| 14% APR | ~$1,164/mo | ~$19,820 |

| 22% APR | ~$1,381/mo | ~$32,890 |

The difference between excellent-credit pricing and fair-credit pricing on the same loan is over $22,000 in interest. If your credit is borderline, the single most valuable thing you can do is wait 6–12 months, fix it, and re-apply. Personal-loan applications don't expire — your credit score does.

Who qualifies for a personal loan for an ADU?

Answer capsule: Most personal-loan lenders writing ADU-sized loans (above $25,000) want a credit score of 670+ with 720+ unlocking the best rates, 2+ years of established credit history, verifiable income, and a debt-to-income ratio below 40% for the largest loan amounts. Self-employed borrowers and applicants with complex income profiles face stricter documentation requirements. A recent bankruptcy, current delinquencies, or recent charge-offs typically disqualify you at mainstream lenders.

Credit score thresholds, in plain terms

- 740+: Best rates available. Personal loan is competitive with HELOC for small projects.

- 700–739: Strong rates available at most lenders. Rate spread vs. HELOC is meaningful but tolerable.

- 670–699: Approval available at most lenders, but rates start to change the math. HELOC looks significantly better if you have equity.

- 620–669: Specialty lenders only. Rates often 20%+. Consider waiting and improving credit.

- Below 620: Most personal-loan lenders won't approve. Co-signed loan through a lender like SoFi may be your only path.

Income documentation

Standard package: two most recent pay stubs, two years of W-2s, two years of tax returns if self-employed. Bank statements may be requested for unconventional income. BHG Financial specifically markets to professionals (physicians, attorneys, accountants, dentists) and underwrites complex income — useful if you have multiple income streams or seasonal income that simpler underwriting penalizes.

DTI math, worked example

Imagine you make $9,000/month gross. Your current monthly debts are:

| Mortgage | $2,400 |

| Auto loan | $450 |

| Student loans | $320 |

| Credit card minimums | $180 |

| Total current debt | $3,350 |

Current DTI: $3,350 / $9,000 = 37.2%.

A $100,000 personal loan at 12% APR over 7 years adds approximately $1,765/month. New DTI: $5,115 / $9,000 = 56.8% — likely outside mainstream comfort and may lead to denial, a lower amount, or worse pricing.

What typically disqualifies you

- Bankruptcy in the last 3–7 years (varies by lender).

- Current delinquency on any account.

- Recent charge-offs or accounts in collections.

- Insufficient credit history (typically less than 2 years of established credit).

- State availability — BHG, for example, is not available in IL or MD; confirm at application.

How do you apply for a personal loan for an ADU?

Answer capsule: The right sequence is to verify the project first, get a hard contractor estimate second, pre-qualify with 2–3 lenders via soft inquiry third, compare APR plus fees plus term, then submit a single full application with the best-fit lender. Funds typically arrive 24–72 hours after approval.

The six-step sequence

- 1

Confirm the project is buildable.

Run your address through a feasibility check before you touch a lender. A loan for an ADU that can't legally be built is a loan that wrecks your credit.

Get Your Free ADU Report → - 2

Get a written contractor estimate.

Not a phone quote. A line-item estimate with allowances called out and a contingency stated. This is the number you borrow against — not a guess.

- 3

Pre-qualify with 2–3 lenders via soft inquiry.

Pull the offer with your actual credit, income, and DTI. Don't rely on advertised rates. SoFi and Upgrade allow soft pre-qualification on their own sites; LightStream requires a partner marketplace (NerdWallet, Credible) to pre-qualify.

- 4

Compare on APR plus fees plus term, not advertised rate.

Origination fees can add 1%–7% to the cost of the loan. A 9% APR loan with a 5% origination fee can cost more than a 12% APR loan with no fees.

- 5

Read the use-of-funds clause carefully.

Some lenders restrict funds from being used for real estate. SoFi's terms restrict certain real-estate uses; LightStream/Truist explicitly permits contractor and permit-fee payments per their published product page. Confirm in writing before applying.

- 6

Submit one full application.

This triggers the hard credit pull. Funds typically arrive 24–72 hours after approval. Pay the contractor on the schedule in your contract.

What scams should you avoid when financing an ADU?

Answer capsule: The two most common scams in ADU personal-loan financing are advance-fee loan scams and high-pressure builder-financing tie-ins. Per FTC guidance, real lenders can require application or appraisal fees, but no legitimate lender will tell you that paying a fee guarantees a loan. Verify any lender against the NMLS Consumer Access registry and your state's department of financial institutions before paying anything.

Advance-fee loan red flags

- A promise that paying a fee guarantees a loan. Legitimate lenders may charge an application or appraisal fee, but they cannot guarantee approval in exchange for a fee.

- Pressure to pay upfront via wire transfer, gift card, or cryptocurrency. These payment methods are nearly impossible to reverse.

- A guarantee of approval regardless of credit. Legitimate lenders price risk; nobody guarantees approval sight unseen.

- Pressure to act in 24 hours or lose the offer.

- The lender uses a free email address (gmail, yahoo) for official communication.

- No verifiable physical address or the address is a virtual mailbox.

- The lender is not registered in your state.

Builder-financing tie-in red flags

- Financing offered before a real budget has been written.

- The builder refers you only to one specific lender with no explanation of why or what the rate is.

- Financing terms are bundled into the construction contract with no ability to shop separately.

- The builder charges a higher construction price when you “use your own financing.”

- No license, bond, or insurance documentation provided before deposit is requested.

Tradeoffs nobody talks about

Answer capsule: Three less-discussed tradeoffs change the personal-loan calculation more than most homeowners realize: (1) personal-loan interest is generally not tax-deductible while home-equity loan or HELOC interest may be deductible if used to substantially improve the home that secures the loan per IRS Publication 936, (2) personal loans are fixed-rate while HELOCs are variable, meaning the personal-loan rate premium partially buys you interest-rate insurance, and (3) most major personal-loan lenders have no prepayment penalty, allowing aggressive payoff from rental income that effectively reduces the all-in cost.

Tax deductibility

Under current IRS rules per Publication 936, interest on personal loans is not tax-deductible. Interest on home-equity loans, HELOCs, and home-equity portions of cash-out refinances may be tax-deductible if the funds are used to buy, build, or substantially improve the home that secures the loan, subject to overall mortgage-interest deduction limits and other requirements. Tax treatment depends on individual circumstances — verify your specific situation with a qualified tax professional before relying on this for financial planning.

Variable-rate risk on HELOCs

HELOCs are usually variable-rate, tied to the prime rate. If prime moves up, your HELOC rate moves up. Over a 7-year term, that exposure is real. The Patelco ADU HELOC posted rate of 8.25% in May 2026 could be 10% or 11% in 2028, depending on Fed action. The fixed personal-loan rate eliminates that risk. The premium you pay over the HELOC's current rate is effectively the cost of rate insurance.

No prepayment penalty = real flexibility

LightStream, SoFi, and most major personal-loan lenders charge no prepayment penalty per their published disclosures. That means once your ADU is built and renting, every dollar of rental income can go toward principal.

Worked example: A $60,000 personal loan at 12% APR over 5 years costs approximately $20,080 in total interest if paid on schedule. If you accelerate payoff by applying $1,500/month in extra principal (roughly $1,800 in rental income minus a buffer), the loan pays off in approximately 24 months, and total interest drops to approximately $7,755. Illustrative examples only — actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

One tradeoff that goes against personal loans

A personal-loan payment is fixed. You can't reduce it during a slow construction month or a vacancy in the rental. A HELOC's interest-only draw period (typically 5–10 years) means you can dial payments up and down based on cash flow. For homeowners with variable income or who are doing a phased ADU build, that flexibility has real value.

Free ADU Starter Kit

Costs by state, financing path decision tree, and the questions to ask any builder.

Download the Free ADU Starter Kit →What to do if a personal loan doesn't fit your ADU

Answer capsule: If a personal loan doesn't fit your ADU project, the right alternative depends on your specific constraint: no equity (renovation or future-value products), wanting to keep a low-rate mortgage (HELOC or home equity loan), needing no monthly payment (Home Equity Investment, with caveats), or needing draw-schedule funding (construction-to-permanent loan). Match the product to your constraint, not the marketing pitch.

| Your real problem | Start here | Why |

|---|---|---|

| No current tappable equity, project >$100k | Future-value / renovation loans (HomeStyle, CHOICERenovation, FHA 203(k)) | These products underwrite to the after-renovation value, not current equity. |

| Want to preserve a low-rate first mortgage | HELOC or home equity loan | Second lien on top of your existing first mortgage; first mortgage rate unchanged. |

| Willing to replace first mortgage for better terms | Cash-out refinance | Single loan, lower combined rate possible if your current mortgage rate is high. |

| Need project-draw funding for ground-up build | Construction-to-permanent loan | Disbursed in draws tied to construction milestones. |

| Want no monthly payment | Home Equity Investment (HEI) | No payment, but you give up a share of future appreciation. State availability matters. |

| Looking for grant or subsidy | State and local ADU programs | Most are limited or paused; treat as bonus, not cornerstone. |

The Dwelling Index is reader-supported. The link below is an affiliate link to Mortgage Research Center, LLC (NMLS #1907), and we may earn a commission if you use it. Our editorial recommendations are based on independent research and are never influenced by compensation. Read our full disclosure.

Compare HELOC, home equity loan, cash-out refinance, and renovation loan paths through Mortgage Research Center, LLC, NMLS #1907.

State and local ADU programs worth flagging

Answer capsule: Four current programs change the financing math meaningfully in their respective regions. MassHousing offers up to $250,000 detached / $150,000 attached for income-eligible Massachusetts homeowners. NYC's Plus One ADU reopened in March 2026 with up to $395,000 in combined financing. Portland, Oregon offers an SDC waiver tied to long-term rental. Boston offers a $7,500 grant plus up to $50,000 in deferred 0% construction financing. California's CalHFA $40,000 grant remains fully allocated since December 28, 2023, with no relaunch date. Verify current eligibility with each program directly before building it into your budget.

MassHousing ADU Loan Program (Massachusetts)

MassHousing's ADU Loan Program provides income-eligible Massachusetts homeowners loans of up to $250,000 for detached ADUs and $150,000 for attached ADUs. The loan combines an amortizing interest-bearing component with additional zero-interest, deferred-repayment financing. Homeowners must have plans, permits, and pre-development materials in hand before applying. For Massachusetts homeowners, this is a meaningfully better option than a personal loan for project sizes under the program caps.

NYC Plus One ADU

NYC HPD's Plus One ADU reopened in 2026 with up to $395,000 in combined financing for qualified homeowners. The statewide Plus One ADU Program provides grants to local governments and nonprofits — homeowners outside NYC apply through local program administrators.

CalHFA ADU Grant — closed

Per CalHFA Program Bulletin 2023-14 (December 28, 2023), all ADU Grant funds were exhausted and the reservation portal closed. There is no announced relaunch date. Be skeptical of any third party claiming to help you access CalHFA funds — the program is closed.

Portland SDC Waiver (Oregon)

The Portland ADU SDC Waiver Program waives system development charges for new ADUs that are owner-occupied or rented month-to-month or longer. Short-term rentals are excluded, and owners sign a 10-year covenant. Verify program status with the Portland Permitting & Development office before assuming the waiver will apply.

Boston ADU Financial Assistance Program

Boston's ADU Financial Assistance Program provides income-eligible owner-occupants of 1–3 unit homes with a $7,500 technical-assistance grant plus up to $50,000 in deferred 0% construction financing. Eligibility includes income and documentation requirements.

Juneau ADU Grant Program (Alaska)

Juneau's ADU Grant Program offers grants up to $13,500, with rolling applications until all grants are awarded. The official page lists 8 grants currently available (verified May 2026 — grant counts change).

Frequently asked questions

Can you use a personal loan to build an ADU?

Yes. Personal loans are commonly used for home improvement, and ADU construction can qualify — but each lender's use-of-funds clause controls. For projects under approximately $100,000 — typically one-car garage conversions and small basement finishes — a personal loan can be a defensible choice. For full detached ADUs or projects above $100,000 where the homeowner has equity, a HELOC or renovation loan will almost always cost less.

What is the maximum personal loan amount for an ADU?

Most mainstream lenders cap unsecured loans at $100,000 (LightStream, SoFi). Specialty lenders go higher: BHG Financial up to $250,000, HFS Financial markets access up to $450,000 through third-party lenders. The amount you actually qualify for depends on credit, income, DTI, and state.

Can I get an ADU personal loan with no home equity?

Yes. Unsecured personal loans don't require home equity. They're priced primarily on credit score, income, and DTI ratio. Lenders typically want 670+ credit and DTI under 40%.

Is a personal loan or HELOC better for an ADU?

For most homeowners with equity, a HELOC is cheaper. At May 2026 rates, a $100,000 loan over 7 years costs roughly $17,500 more in interest as a personal loan than as a HELOC. The personal loan wins only when you can't qualify for the HELOC, when you need same-week funding, or when you value fixed-rate certainty over the lowest rate.

Is a personal loan better than a construction loan for an ADU?

Usually no for a full ground-up build. Construction loans are designed for large projects and disburse in draws tied to milestones. They're slower and more paperwork-heavy, but they're the right product for projects over $100,000. Personal loans win on small scopes, soft costs, and gap funding only.

Can I use a personal loan for ADU permits and design?

Often yes, and this is one of the stronger use cases — but check the lender's use-of-funds clause. Plans, permits, and feasibility studies typically run $8,000–$25,000 before construction starts. A personal loan can bridge this cost before your main construction or renovation loan funds. Note: Fannie Mae's HomeStyle Renovation allows up to 50% of total renovation costs to be disbursed at closing, including permits, architect fees, and design costs — so if your main loan is HomeStyle, you may not need separate unsecured debt for soft costs.

Can I use a personal loan for a prefab ADU?

Possibly for a deposit or partial payment. Prefab base prices are not installed costs. A '$150,000 prefab' typically lands meaningfully higher once you add foundation, utility laterals, permits, craning, and site work. A personal loan can fund the deposit or a small balance, but it's rarely enough to fund the all-in installed cost.

Will a personal loan affect my mortgage or refinance approval?

Yes. Personal-loan monthly payments count against your debt-to-income ratio on future mortgage and home-equity applications. If you're planning a refinance or HELOC within 24 months, sequence matters — open the larger loan first when possible.

Can ADU rental income help me qualify for financing?

Sometimes. Per Fannie Mae Selling Guide B3-3.8-01, rental income from an existing ADU on a one-unit principal residence can count toward qualifying income on purchase or limited cash-out refinance transactions — capped at 30% of total qualifying income. This rule applies to existing ADUs that can be appraised, not to projected income from an ADU you haven't built yet.

Are personal loan interest payments tax-deductible for an ADU?

Generally no. Personal-loan interest is not deductible per IRS Publication 936. Home-equity-loan and HELOC interest used to buy, build, or substantially improve the home that secures the loan may be deductible subject to limits. Verify your specific situation with a qualified tax professional — this is general information, not tax advice.

What happens if my ADU goes over budget?

You need a gap-financing strategy in place before you break ground. Options include a small personal loan layered on the main loan, a HELOC drawn during construction, builder-financed change orders, or scope reduction. A 15% contingency in your original budget is the minimum buffer.

How fast does a personal loan fund?

LightStream and SoFi advertise same-day funding for qualified applicants. Most major lenders fund within 24–72 hours of approval. This is one of the personal loan's genuine advantages over HELOCs (3–6 weeks to close) and construction loans (6–10 weeks).

Are personal-loan rates negotiable?

Yes, indirectly. LightStream's Rate Beat Program will reduce your APR by 0.10 percentage points if you can prove a competitor approved you at a lower rate on a similar loan. Most lenders won't negotiate APR directly but will negotiate fees and discounts (autopay, direct-deposit). Always pre-qualify with 2–3 lenders before accepting an offer.

Should I just pay cash instead of borrowing?

If you can pay cash without draining emergency reserves or construction contingency, paying cash eliminates borrowing costs entirely. But don't drain reserves before permits, utilities, and contractor scope are verified. A common pattern: pay cash for soft costs and the deposit, finance the construction.

Methodology

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We're not a lender, broker, or builder. We don't take payment from personal-loan lenders to write about them — none of the lenders named in the comparison table on this page are affiliated with Dwelling Index, and they're listed alphabetically with no ranking by payout.

For this guide we reviewed:

- Federal Reserve consumer-credit data (FRED series TERMCBPER24NS).

- Bankrate Monitor weekly personal-loan rate survey.

- NerdWallet 30-day pre-qualification aggregate data on home-improvement loans.

- Lender product pages and disclosures from LightStream/Truist, SoFi, Upgrade, HFS Financial, BHG Financial — verified directly at each lender's site in March–May 2026.

- Patelco Credit Union's posted ADU HELOC rate as the current ADU HELOC benchmark.

- Fannie Mae Selling Guide sections B3-3.8-01 and SEL-2025-08, and HomeStyle Renovation FAQs.

- ADU cost data from Angi (2026), the Terner Center for Housing Innovation, GreatBuildz (2026 LA cost guide), and BuildingAnADU owner-reported averages.

- CFPB and FTC consumer-protection guidance.

- IRS Publication 936 on home mortgage interest deduction.

- State and local program pages from MassHousing, NYC HPD, NYS HCR, CalHFA, Portland Permitting & Development, Boston Department of Housing, and the City and Borough of Juneau.

Where we couldn't verify a claim against a primary or highly reliable source, we marked it [needs verification]. Where rates and program statuses are likely to change, we noted the verification date. The page is re-verified quarterly and any time the Federal Reserve moves rates or a referenced program status changes.

If you spot something on this page that should be updated, email editor@dwellingindex.com.

Not sure where to start?

See what's possible at your address — get your free ADU report in 60 seconds.

Get Your Free ADU Report →Free. No obligation. Your address, 60 seconds.