HomeStyle Renovation Loan ADU: 2026 Rules, the December 2025 Update, and When It Actually Fits

By The Dwelling Index Editorial Team · · Last verified May 19, 2026 · ~40 min read

Independent ADU resource · Not a lender or broker · Editorial standards →

The bottom line on a HomeStyle Renovation loan ADU

Yes, the Fannie Mae HomeStyle Renovation loan can finance an accessory dwelling unit — including a detached, new-construction ADU, which the current FHA 203(k) program does not. As of March 31, 2026, lenders using Fannie Mae’s UAD 3.6 policy can finance up to three ADUs on a single-unit primary residence and add ADUs to 2–3 unit properties up to four total dwellings, per Selling Guide Announcement SEL-2025-10. The renovation-cost ceiling is 75% of the as-completed appraised value (or 75% of the lesser of purchase price plus renovation costs or as-completed value for purchases);50% when the primary dwelling is a manufactured home. The 2026 conforming loan limit is $832,750 in standard counties and $1,249,125 in high-cost counties per the FHFA November 25, 2025 announcement.

HomeStyle fits best when you’re buying a home and adding an ADU in the same transaction, you don’t have enough current equity for a HELOC, or your existing first-mortgage rate is at or above today’s market. HomeStyle fits worst when you have a sub-5% pandemic-era first mortgage and meaningful current equity, your project is a tear-down-and-rebuild (not allowed), or you can’t tolerate the contractor-approval, draw-schedule, and lender-recourse complexity.

See what you can build before you call a lender → Get your free ADU report in 60 seconds

Two rule lanes exist in 2026: read this before the comparison

Fannie Mae’s public ADU policy currently runs on two parallel tracks, and conflating them is the single biggest source of confusion on this topic.

- Standard ADU rules — limits ADUs to a 1-unit primary residence, generally one ADU, and excludes 2–4 unit properties, manufactured-home primary dwellings, and multiple ADUs. See Fannie Mae’s ADU policy page.

- UAD 3.6 expanded rules — effective March 31, 2026 for lenders that have adopted UAD 3.6 policy, permits up to three ADUs on a 1-unit primary residence, up to four total dwellings on a 2–3 unit property, and ADUs on single-wide manufactured-home primaries. See SEL-2025-10.

The expanded multi-ADU and MH-ADU eligibility throughout this guide applies to the UAD 3.6 lane. Ask any HomeStyle lender directly whether they have implemented UAD 3.6 policy. If they haven’t, the standard ADU rules apply to your file.

Should you test HomeStyle first? A one-screen decision

| Your situation | Test HomeStyle first? | Why |

|---|---|---|

| Buying a home and adding an ADU in the same transaction | Yes | One loan combines purchase + renovation; underwriting uses as-completed value. |

| Refinancing a home with strong value upside and a mortgage rate near or above today’s market | Yes | HomeStyle replaces your first mortgage anyway — no rate sacrifice. |

| You have a sub-5% pandemic-era first mortgage and meaningful current equity | No | A HELOC or home equity loan preserves your rate and is simpler. |

| Detached new ADU + limited current equity | Yes, but compare with CHOICERenovation and construction-to-perm | All three can lend against as-completed value; HomeStyle has the clearest detached new-construction path. |

| You need ADU rental income to qualify and the ADU does not yet exist | Maybe — ask the lender | Fannie Mae’s current published rule clearly addresses existing ADUs on a 1-unit primary residence; treatment of proposed ADU rent is a lender-confirmation item. |

| You want to use FHA 203(k) for a detached new ADU | No — current 203(k) policy doesn’t list detached new ADUs as eligible | HomeStyle (or CHOICERenovation) is your path. |

| You’re an investor or owner on a 2–4 unit property and want to add an ADU | Yes, effective March 31, 2026 for UAD 3.6 lenders | SEL-2025-10 opened ADUs on 2–3 unit properties up to four total dwellings. |

Not sure which side of this table you’re on? Run our free 60-second ADU feasibility check → We check zoning, setbacks, lot coverage, fire-zone status, HOA, and ADU classification on your parcel before you spend a dollar on plans or call a lender.

What we verified for this guide

- Fannie Mae Selling Guide B5-3.2-01 — eligibility, 15-month completion rule, lender recourse, ADU permission. B5-3.2-01

- Fannie Mae B5-3.2-02 — the 75% / 50% renovation-cost caps. B5-3.2-02

- Fannie Mae B5-3.2-06 — 15-month deadline, extensions up to 18 months in limited cases. B5-3.2-06

- Fannie Mae B3-3.8-01 Rental Income (10/08/2025) — ADU rental-income rules and the 30% qualifying-income cap. B3-3.8-01

- Fannie Mae B3-5.1-01 — credit-score requirements for manually underwritten loans vs DU casefiles. B3-5.1-01

- Fannie Mae Selling Guide Announcement SEL-2025-10 (Dec 10, 2025) — multi-ADU eligibility, 50% upfront disbursement, HomeStyle Refresh, MH ADU expansion. SEL-2025-10

- Fannie Mae SEL-2025-08 — ADU rental-income policy. SEL-2025-08

- Fannie Mae Desktop Underwriter 12.1 Release Notes (Feb 18, 2026) — DU automation of the 30%-of-income ADU cap. DU 12.1

- FHFA 2026 conforming loan limit announcement (November 25, 2025) — $832,750 / $1,249,125. FHFA limits

- HUD Mortgagee Letter 2024-13 — Limited 203(k) cap raised to $75,000; Standard 12-month / Limited 9-month rehab periods.

- HUD Mortgagee Letter 2023-17 — current FHA ADU policy and eligible 203(k) improvements.

- Freddie Mac CHOICERenovation page and Bulletin 2026-1 — CHOICERenovation rental-income restriction effective May 4, 2026.

- Pennymac Announcement 26-33 — lender-level HomeStyle Refresh implementation.

Last verified: May 19, 2026 · Last updated:

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Can you use a HomeStyle Renovation loan for an ADU?

Yes. Fannie Mae Selling Guide B5-3.2-01 expressly permits HomeStyle Renovation to fund “accessory units, garages, recreation rooms, and swimming pools” when local zoning allows. The Fannie Mae ADU product page confirms borrowers purchasing or refinancing a one-unit property and constructing or installing a new ADU can use a renovation loan, and Selling Guide Announcement SEL-2025-10 (December 10, 2025) significantly expanded the property configurations eligible for ADU financing. HomeStyle isn’t a separate ADU loan product. It’s a conventional first-mortgage with a renovation escrow attached. The ADU is one of many improvements the program supports. What makes HomeStyle particularly relevant for ADU borrowers is that the appraisal is done on an “as-completed” basis: the property is valued as if the ADU were already built.

The “accessory unit” vs “another dwelling” distinction nobody explains clearly

From the HomeStyle Renovation FAQ: “Funds may not be used to construct another residential dwelling on the property.” That sounds like a contradiction with “Yes, you can build an ADU.” It isn’t. The distinction is accessory versus independent. An ADU is, by definition, subordinate and accessory to the primary residence on the same parcel. A second primary dwelling on the same lot is something else — it’s effectively a duplex.

The practical test the appraiser and the lender apply: is the new structure ancillary to the primary, properly subordinate, and permitted as an ADU under local code? If yes, HomeStyle is in. If you’re trying to build two roughly equivalent dwellings on a parcel zoned for one, you’re outside the program.

Which ADU types HomeStyle will finance

- Detached new-construction ADU — backyard cottage, DADU, separate-structure granny flat.

- Attached new-construction ADU — addition to the primary home with an independent entrance.

- Interior conversion — basement ADU, attic ADU, garage-to-ADU conversion.

- Modular or factory-built ADU — site-installed and permanently affixed; treated under standard ADU rules.

- Manufactured-home (HUD-code) ADU — must be classified as real property per Selling Guide B5-2-05; expanded eligibility under SEL-2025-10 effective March 31, 2026 for lenders using UAD 3.6.

- Existing ADU renovation or substantial remodel — improving a pre-existing accessory unit.

What HomeStyle won’t do

- Tear down and reconstruct the primary dwelling. A complete teardown to the foundation is excluded by Selling Guide B5-3.2-01.

- Construct a second residential dwelling that isn’t classified as an ADU. See the accessory-vs-independent test above.

- Pay for anything not permanently affixed to the real property. Movable structures, freestanding sheds without utilities, and most “tiny homes on wheels” don’t qualify.

- Cover DIY work above 10% of as-completed value. The lender approves plans in advance and inspects items costing more than $5,000. No DIY is permitted on manufactured homes, and sweat-equity labor is never reimbursable.

HomeStyle Renovation loan ADU requirements: what has to be true?

To use HomeStyle Renovation for an ADU, the property, the borrower, the contractor, and the project must all qualify under Fannie Mae’s published rules. The property must be an eligible 1–4 unit, condo, PUD, or manufactured home; the borrower needs sufficient credit history (Fannie Mae’s published manually-underwritten minimum is 620), an acceptable DTI, and standard documentation; the contractor must be licensed, bonded, and approved by the lender; and the project must complete within 15 months of closing.

Property eligibility

- 1-unit primary residence, 1-unit second home, 1-unit investment property

- 2–4 unit primary residence (a contingency reserve is required)

- Condo unit / co-op unit (subject to project approval)

- One-unit manufactured home as primary dwelling (subject to MH-specific rules)

- PUD (Planned Unit Development)

- The property must be at least one year old

- It does not need to be habitable at closing — up to six months of PITI can be financed into the loan to cover the uninhabitable period

Borrower credit and DTI

Fannie Mae’s B3-5.1-01 sets a published minimum credit score for manually underwritten fixed-rate loans at 620 and manually underwritten ARMs at 640. Most HomeStyle Renovation transactions run through Desktop Underwriter, which assesses the file holistically. Most lenders impose overlays that effectively raise the floor to 640, 680, or even 700 for renovation transactions because of construction-period risk.

Standard DTI ceilings apply (typically 45%, with compensating factors permitted in DU).

Contractor requirements

- Licensed, bonded, and insured general contractor — subject to lender approval

- Detailed scope of work, signed contract (Fannie Mae Form 3730), and itemized cost estimates

- For 2–4 unit properties: 10% contingency reserve required and funded

- DIY work permitted on 1-unit only, capped at 10% of as-completed value, with lender approval and inspection on items >$5,000; DIY not permitted on manufactured homes

Can HomeStyle finance a detached new ADU?

Yes. HomeStyle Renovation can finance a detached new-construction ADU on an eligible property. Under Fannie Mae Selling Guide B5-3.2-01, HomeStyle “may be used to construct various outdoor buildings and structures when allowed by local zoning regulations,” and the listed examples include accessory units. The detached ADU must qualify as an accessory dwelling unit (independent living, sleeping, cooking, and bathroom facilities; accessible without going through the primary dwelling; expectation of privacy from the primary) and must be subordinate to the primary residence rather than functioning as a separate non-accessory second dwelling.

This is the single most important practical advantage HomeStyle has over the current FHA 203(k) for ADU borrowers. Under HUD Mortgagee Letter 2023-17, eligible ADU work under the 203(k) program is limited to ADUs “attached to an existing Structure” or renovation of an existing ADU — detached new-construction ADUs are not listed as eligible 203(k) uses. If your project is a new backyard cottage, HomeStyle (or Freddie Mac’s CHOICERenovation, or a construction-to-permanent loan) is your conventional path.

The detached-ADU eligibility doesn’t change the rules of the rest of the program. You still need the 75% renovation-cost cap to clear, the appraisal to support the as-completed value, the contractor to be approved, the local zoning to allow the ADU, and the build to complete within 15 months.

What changed in December 2025: SEL-2025-10 and DU 12.1, decoded

On December 10, 2025, Fannie Mae issued Selling Guide Announcement SEL-2025-10. Effective immediately, lenders can disburse up to 50% of total renovation costs at closing for documented costs such as materials, permits, and architect/design fees. The $50,000 renovation cap on manufactured-home transactions was replaced with a 50%-of-as-completed-value ceiling. Limited cash-out refinances can now be used to buy out a co-owner’s interest while renovating. Effective March 31, 2026 for lenders using UAD 3.6 policy, Fannie Mae expanded ADU property eligibility to allow up to three ADUs on a single-unit primary residence and up to four total dwellings on 2–3 unit properties, and explicitly permitted ADUs on single-wide manufactured-home primaries. Desktop Underwriter 12.1, implemented the weekend of March 21, 2026, automates ADU rental-income qualification under the 30%-of-income cap from SEL-2025-08.

| Rule change | Effective | Source | What it means for ADU borrowers |

|---|---|---|---|

| Up to 3 ADUs on a single-unit property (subject to local zoning) | Mar 31, 2026 — UAD 3.6 lenders only | SEL-2025-10 | A 1-unit primary residence can host multiple ADUs and still qualify for HomeStyle financing if zoning allows. |

| Up to 4 total dwellings on 2–3 unit property (including ADUs) | Mar 31, 2026 — UAD 3.6 lenders only | SEL-2025-10 | A duplex or triplex with an ADU is now financeable; previously ineligible. |

| Single-wide manufactured home as primary, with one ADU classified as real property | Mar 31, 2026 — UAD 3.6 lenders only | SEL-2025-10 | Rural and lower-density markets gain an ADU financing path that didn’t exist. |

| Up to 50% upfront disbursement of total renovation costs at closing | Immediate (Dec 10, 2025) | SEL-2025-10 | Contractor can be paid for documented materials, permits, and design fees at closing instead of waiting for the first milestone draw. |

| $50,000 cap removed for manufactured-home renovations; new ceiling is 50% of as-completed value | Immediate | SEL-2025-10 | MH primary-dwelling owners can do substantial renovations, including ADU additions, under a cleaner rule. |

| Limited cash-out refinance allowed to buy out a co-owner’s interest while renovating | Immediate | SEL-2025-10 | A spouse keeping the home in a divorce can refinance out the other partner and build the ADU in one transaction. |

| DU 12.1 automates ADU rental-income qualification with 30%-of-income cap | Mar 21, 2026 | DU 12.1 Release Notes + SEL-2025-08 | DU enforces the 30% cap automatically on eligible 1-unit primary purchase or limited cash-out refi transactions. |

| HomeStyle Refresh replaces HomeStyle Energy; finances up to 15% of as-completed value for resiliency and cosmetic work; 180-day completion | Applications on/after Mar 31, 2026 | SEL-2025-10 + B5-3.3-01 | A streamlined product for smaller-scope upgrades. Not a full ADU-financing path — completion window is just six months. |

Source: Fannie Mae Selling Guide Announcement SEL-2025-10, Dec 10, 2025; DU 12.1 Release Notes, Feb 18, 2026; Pennymac Announcement 26-33. Verified May 19, 2026.

Who actually wins from these changes

Contractors and cash-constrained homeowners. The 50% upfront disbursement is the single most operationally meaningful improvement. Before SEL-2025-10, contractors often fronted material costs, permit fees, and architect deposits for weeks before the first milestone draw. On a $200,000 ADU, that’s commonly $30,000 to $50,000 the contractor had to float — a documented bottleneck on renovation-loan projects.

Owners of duplexes and triplexes (UAD 3.6 lane). Previously, a duplex or triplex with an ADU was ineligible. As of March 31, 2026, lenders using UAD 3.6 policy can finance a duplex or triplex with ADUs up to four total dwellings on the parcel.

Manufactured-home primary owners in rural markets (UAD 3.6 lane). Single-wide MH primaries can now host an ADU classified as real property. The $50K cap removal on manufactured-home renovations means substantial work is financeable.

What kinds of ADUs can HomeStyle finance?

HomeStyle can finance attached ADUs, detached ADUs, garage and basement conversions, modular and factory-built ADUs, and manufactured-home ADUs (subject to real-property classification), provided the unit qualifies as an accessory dwelling unit under Fannie Mae’s definition, complies with local zoning, and satisfies the lender’s appraisal and underwriting requirements.

| ADU type | HomeStyle fit | Main catch | Source |

|---|---|---|---|

| Basement ADU (interior conversion) | ✅ Strong | Must have independent ingress/egress, expectation of privacy, and required living/sleeping/cooking/bathroom facilities | B2-3-04 + B4-1.3-05 |

| Attic ADU (interior conversion) | ✅ Strong | Same independence requirements; head-height and egress code compliance | B2-3-04 |

| Garage conversion ADU (attached) | ✅ Strong | Local code compliance; utilities; appraisal classification | B2-3-04 |

| Attached new-construction addition ADU | ✅ Strong | Permits, plans, contractor bid, as-completed appraisal | B5-3.2-01 / B5-3.2-02 |

| Detached site-built ADU (new construction) | ✅ Strong | Must remain classified as accessory; cannot become a non-accessory second dwelling | Fannie Mae ADU page + B2-3-04 |

| Modular / factory-built ADU | ✅ Strong with proper classification | Must be permanently affixed; appraisal classification per modular rules | B2-3-04 |

| Manufactured (HUD-code) ADU | ⚠️ Allowed but technical | Must be real property per B5-2-05; permanent foundation, affidavit of affixture, security instrument description; ALTA 7/7.1/7.2 title endorsement; eligible on single-wide MH primary effective Mar 31, 2026 (UAD 3.6 lenders) | B5-2-05 + SEL-2025-10 |

| Multiple ADUs on a single-unit property (up to 3) | ✅ Allowed under UAD 3.6 lane effective Mar 31, 2026 | UAD 3.6 lenders only; subject to local zoning | SEL-2025-10 |

| ADU on a 2–3 unit primary residence | ✅ Allowed under UAD 3.6 lane effective Mar 31, 2026 | Up to 4 total dwellings on the parcel; UAD 3.6 lenders only | SEL-2025-10 |

Verified May 19, 2026 against Fannie Mae Selling Guide B5-3.2-01, B2-3-04, B5-2-05, and SEL-2025-10.

Fannie Mae’s precise ADU definition

“A smaller additional living space on the same lot as a single-family home. It must include space for living, sleeping, cooking and bathrooms independent of the primary residence. While the ADU may or may not include access to the primary residence, it must be accessible without going through the primary residence and there must be some expectation of privacy from the home.”

Three test phrases: smaller, independent facilities, and expectation of privacy.

Not sure if your unit qualifies as an ADU on your specific lot? Get your free 60-second ADU feasibility report → We check zoning, setbacks, lot coverage, fire-zone status, HOA, and ADU classification on your parcel before you spend a dollar on plans or call a lender.

How much can you borrow with HomeStyle for an ADU?

A HomeStyle Renovation loan is capped at the 2026 conforming loan limit — $832,750 for a 1-unit property in standard areas and $1,249,125 in high-cost areas, per FHFA’s November 25, 2025 announcement. Loan-to-value can reach 97% in eligible Desktop Underwriter cases on a 1-unit primary residence purchase or limited cash-out refinance. The key constraint most borrowers miss is the renovation-cost ceiling: renovation costs cannot exceed 75% of the lesser of (purchase price + renovation costs) or the as-completed appraised value for purchase transactions, or 75% of the as-completed appraised value for refinance transactions. The manufactured-home cap is 50% of as-completed value when the primary dwelling is a manufactured home.

The 75% renovation-cost cap, in plain English

For a purchase transaction:

Renovation cost cannot exceed 75% × the lesser of (purchase price + renovation costs) or as-completed appraised value.

For a refinance transaction:

Renovation cost cannot exceed 75% × as-completed appraised value.

For manufactured-home transactions (primary dwelling is a manufactured home):

Renovation-cost ceiling is 50% of as-completed value per Selling Guide B5-3.2-02.

The Maximum Mortgage Worksheet (Form 1035), decoded

HomeStyle uses Form 1035 to calculate the loan amount. The lender plugs in:

- Purchase price (or current value for refi)

- Planned renovation costs (contractor’s contract price)

- Soft costs (architect, engineering, permit fees) — financeable

- Contingency reserve (10% required and funded on 2–4 unit; optional on 1-unit)

- Inspection and plan-review fees

- Up to six months of financed PITI if the home is uninhabitable during construction

- As-completed appraised value (the appraiser values the property subject-to the planned renovations)

The output is the smaller of: the program LTV ceiling for your transaction type, the conforming loan limit, or the 75% renovation-cost test.

Three worked scenarios

| Scenario | Current home value | Existing mortgage | ADU build cost | As-completed value (illustrative) | 75% reno-cost test | HomeStyle outcome |

|---|---|---|---|---|---|---|

| Low-equity refi + build | $625,000 | $475,000 | $200,000 | $775,000 (subject-to) | $200K vs 75% × $775K = $581K → passes | Refi loan up to 97% of $775K = ~$751K assuming high-LTV LCOR eligibility conditions met. Less existing $475K = ~$276K headroom for the $200K ADU plus closing costs and reno fees. |

| High-equity refi + build | $900,000 | $250,000 | $300,000 | $1,150,000 | $300K vs 75% × $1.15M = $862K → passes | Often not the best path — a HELOC or home equity loan preserves the existing rate and avoids HomeStyle complexity. |

| Purchase + immediate ADU | $650,000 purchase price | None | $185,000 (rolled in) | $850,000 (subject-to) | $185K vs 75% × min($835K, $850K) = $626K → passes | New first mortgage up to ~97% of $850K covers purchase plus ADU. Strong fit for a new buyer. |

Illustrative only. Not loan offers. Actual approval depends on credit, DTI, lender overlays, appraisal support, contractor bids, Form 1035, and the applicable conforming loan limit.

Down payment requirements by property type

| Occupancy / property | Minimum down payment* |

|---|---|

| 1-unit primary residence (HomeReady-eligible) | 3% |

| 1-unit primary residence | 5% (eligible DU casefiles may go up to 97% LTV / 3% down with HomeReady) |

| Single-unit second home | 10% |

| Single-unit investment property | 15% (purchase) / 25% (refinance) |

| 2–4 unit primary residence | 5% |

| Manufactured home (primary) | Subject to standard MH requirements |

*Subject to DU recommendation, lender overlays, and the Fannie Mae Eligibility Matrix.

The 2026 conforming loan limit reality check

The FHFA announced the 2026 conforming loan limits on November 25, 2025: $832,750 for a 1-unit property in standard areas and $1,249,125 in high-cost areas. Multi-unit limits scale up to $1,601,750 for a 4-unit standard and $2,402,625 in high-cost areas. Alaska, Hawaii, Guam, and the U.S. Virgin Islands have higher limits up to $1,873,687 for a one-unit property.

A high-cost ADU build in a standard-cost county can pass the 75% renovation test and still hit the conforming loan limit. If you’re financing a $750,000 home in an $832,750-limit county and want to add a $250,000 ADU, your renovation cost passes the cap, but the combined loan likely exceeds the limit — pushing you toward a jumbo non-conforming product rather than HomeStyle.

Mortgage insurance

Cancellable PMI applies when LTV exceeds 80%. By law, PMI is removed once the borrower reaches 22% equity (78% LTV). This is a meaningful advantage versus FHA 203(k), which carries permanent FHA Mortgage Insurance Premium that survives the life of the loan unless refinanced.

If you’ve worked through the math and HomeStyle’s process feels heavier than your project needs, a straightforward cash-out refinance can sometimes be the simpler route — especially if your current first-mortgage rate is already at or near today’s market. We work with Mortgage Research Center (NMLS #1907) as a partner for broader mortgage / refinance / cash-out content; they do not originate HomeStyle Renovation loans, so this route is for borrowers who decide HomeStyle isn’t their fit.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Explore mortgage-backed ADU financing options →Mortgage Research Center — affiliate disclosure applies. Not a guarantee of approval.

Will HomeStyle make you refinance your current mortgage?

Usually yes if you already own the home and are using HomeStyle to fund a new ADU. HomeStyle Renovation is a conventional first-mortgage structure, and a limited cash-out refinance can include payoff of the existing first mortgage plus eligible renovation costs — but the borrower cannot receive cash proceeds beyond the standard limited-cash-out allowances. If your existing first-mortgage rate is well below today’s market, replacing it to fund an ADU is often more expensive than the ADU itself.

The low-rate-first-mortgage trap

A large share of U.S. homeowners with a mortgage carry a rate at or below 4.0%, almost entirely from 2020–2022 purchases and refinances. For those borrowers, replacing the first mortgage to fund an ADU can cost more in lifetime interest than the ADU itself. The break-even point depends on assumed rates, fees, and prepayment behavior, but the math typically only works when the existing rate is at or above today’s market.

Illustrative example only, not a guarantee of returns. Actual results depend on your specific rate, loan terms, fees, prepayment behavior, and market conditions.

Keep-first vs replace-first matrix

| Your situation | Likely first path to test | Why |

|---|---|---|

| Low existing first rate + enough current equity for ADU | HELOC or home equity loan | Keeps the first mortgage intact; sits as a second lien. |

| Low existing first rate + not enough current equity | Compare HELOC + cash gap funding vs HomeStyle | Future-value financing may be the only way to bridge the gap, even with the rate penalty. |

| Higher or similar existing first rate + want one payment | HomeStyle, cash-out refi, or CHOICERenovation | The rate sacrifice is small or zero. |

| Buying a home and adding ADU in one transaction | HomeStyle, CHOICERenovation, or construction-to-perm | No existing rate to protect. |

| You bought in the last 12 months at today’s rates | HomeStyle, cash-out refi, or HELOC | You haven’t locked in a below-market rate yet. |

| Major ground-up ADU with permitting + build likely > 15 months | Construction-to-permanent loan | HomeStyle requires completion within 15 months of closing per B5-3.2-01. |

Protecting a low first-mortgage rate? Read our HELOC for ADU guide first.

Can ADU rental income help you qualify for HomeStyle?

For Fannie Mae HomeStyle, the clearly verified rule is rental income from an existing ADU on a one-unit principal residence (purchase or limited cash-out refinance only, one ADU only), capped at 30% of total qualifying income per Selling Guide B3-3.8-01. The 75%-of-gross-rent vacancy calculation applies to lease or market rent (Form 1007). Since Desktop Underwriter 12.1 went live the weekend of March 21, 2026, DU automates this rule for eligible casefiles. Whether projected rent from a not-yet-built ADU can be counted is a lender-confirmation item — Fannie Mae’s published rental-income section expressly addresses existing ADUs, and your lender’s specific underwriting treatment of proposed ADU rent should be confirmed before you rely on it.

The 30% cap, walked through

Example 1 — cap doesn’t bind

Gross monthly salary: $6,000 · ADU market rent: $1,600/month

- 75% × $1,600 = $1,200 (vacancy-adjusted rent)

- 30% × ($6,000 + $1,200) = $2,160 (the income cap)

- $1,200 < $2,160 → full $1,200 counts → total qualifying income = $7,200/month

Example 2 — cap bites

Gross monthly salary: $3,000 · ADU market rent: $2,500/month

- 75% × $2,500 = $1,875

- 30% × ($3,000 + $1,875) = $1,463 (the income cap)

- Only $1,463 counts → total qualifying income = $4,463/month

Illustrative only — not guarantees of returns. Actual results depend on local market conditions, financing terms, and regulatory approvals.

Lender script for the rental-income conversation

“I’m evaluating a HomeStyle Renovation transaction for an ADU on a 1-unit primary residence. For underwriting purposes, the ADU is [existing / proposed]. Are you running this through Desktop Underwriter 12.1? For an existing ADU, are you applying the 30%-of-income cap from B3-3.8-01 and the 75% gross-rent calculation? What’s your documentation requirement — Form 1007, lease, Schedule E? For a proposed ADU, how do you treat projected rental income — is it eligible at your shop, and what documentation supports it? Do you have any lender overlay that changes the standard rental-income treatment?”

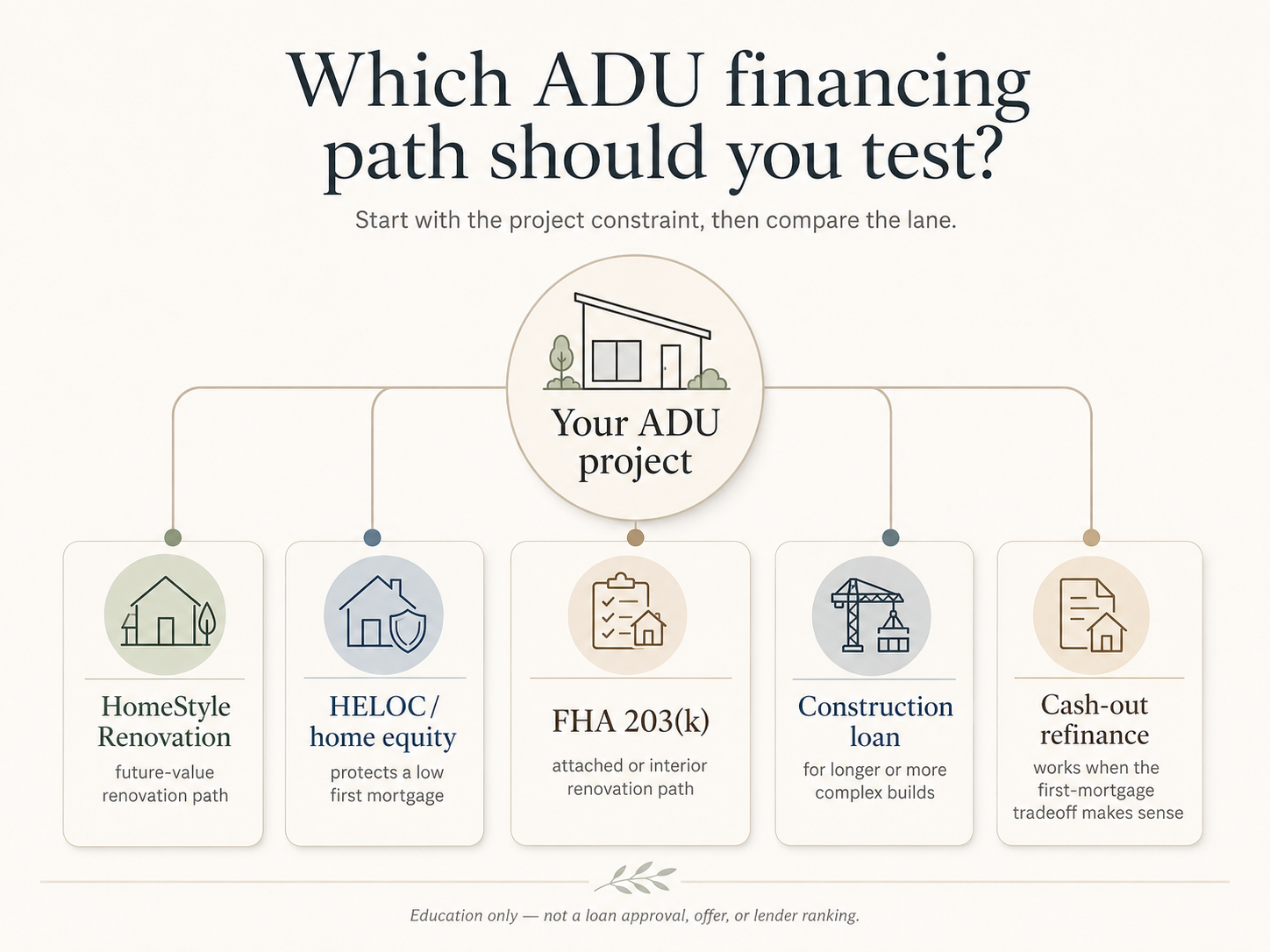

HomeStyle vs FHA 203(k) vs Freddie Mac CHOICERenovation: which renovation loan for your ADU?

All three are renovation loans that can fund ADU work, but they aren’t interchangeable. The decision usually comes down to four factors: detached vs attached, credit score, rental-income strategy, and conventional vs FHA structure. Under current HUD policy, the FHA 203(k) does not list detached new-construction ADU as an eligible use — attached ADUs and existing ADU renovation are the ADU paths HUD identifies. Freddie Mac CHOICERenovation will, for applications received on or after May 4, 2026, restrict the use of rental income from units funded by CHOICERenovation proceeds for qualifying per Freddie Mac Bulletin 2026-1. HomeStyle has the broadest detached new-construction ADU eligibility of the three.

| Feature | HomeStyle (Fannie Mae) | FHA 203(k) Standard | FHA 203(k) Limited | CHOICERenovation (Freddie) |

|---|---|---|---|---|

| Funds a new detached ADU | ✅ Yes [B5-3.2-01] | ❌ Not listed as eligible [ML 2023-17] | ❌ No | ✅ Yes |

| Funds attached or interior ADU | ✅ Yes | ✅ Yes | ✅ Yes (non-structural only) | ✅ Yes |

| Funds a manufactured-home ADU | ✅ Yes, with real-property classification; expanded UAD 3.6 Mar 31, 2026 | ⚠️ Limited | ⚠️ Limited | ⚠️ Limited |

| ADU on 2–3 unit property | ✅ Yes, up to 4 total dwellings — UAD 3.6 only, Mar 31, 2026 | 1–4 unit primary residence eligible | 1–4 unit primary | 1, 2, or 3-unit + 1 ADU |

| Rental income for qualifying | Existing ADU only on 1-unit primary, 75% gross rent, 30% qualifying-income cap (DU 12.1) | 75% of estimated rent on existing ADU; 50% on new attached/conversion ADU per ML 2023-17 | 75% / 50% same as Standard | Restricted: rental income from units funded by CHOICERenovation proceeds cannot be used for qualifying for applications received on/after May 4, 2026 (Bulletin 2026-1) |

| Minimum credit score | 620 manually underwritten (B3-5.1-01); DU assessed holistically; lender overlays apply | 580 with 3.5% down; 500–579 with 10% down | 580 with 3.5% down | 660 typical (overlays vary) |

| Max LTV (1-unit primary) | Up to 97% in eligible DU cases | Up to 96.5% | Up to 96.5% | Up to 97% |

| Renovation cost ceiling | 75% of as-completed (refi); lesser of purchase+reno or as-completed (purchase); 50% if primary is MH | Within FHA county loan limit | $75,000 cap (raised from $35,000 per HUD ML 2024-13, effective Nov 4, 2024) | 75% of as-completed value |

| Completion deadline | 15 months from closing (extensions up to 18 months in limited cases per B5-3.2-06) | 12 months from closing (per ML 2024-13) | 9 months from closing (per ML 2024-13) | Per Freddie Mac CHOICERenovation terms |

| Upfront disbursement at closing | Up to 50% of total renovation costs (SEL-2025-10) | Standard draws | Two-draw structure | Varies |

| Contingency reserve required | Not required on 1-unit; 10% required and funded on 2–4 unit | 10–20% required | Optional | Required, varies |

| DIY work allowed | 1-unit only, ≤ 10% of as-completed value, lender approval and inspection for items > $5,000; not on MH | Generally not | Generally not | Generally not |

| Tear-down and rebuild | ❌ Not allowed | ❌ Not allowed (foundation must remain) | ❌ Not allowed | ❌ Not allowed |

| Consultant required | No | Yes (HUD-approved 203(k) Consultant) | Optional (financeable under ML 2024-13) | No |

| 2026 max loan amount (1-unit) | $832,750 standard / $1,249,125 high-cost | $541,287 low-cost / $1,249,125 high-cost | Same as Standard, plus $75K rehab cap | Same as Fannie Mae conforming limits |

| Mortgage insurance | Cancellable PMI when LTV ≤ 78% | Permanent FHA MIP; 1.75% upfront MIP | Permanent FHA MIP; 1.75% upfront MIP | Cancellable PMI |

| Best fit for an ADU borrower | Detached new ADU; low-equity refi-and-build; purchase + ADU; MH ADU; investor 1–4 unit | Attached/interior/conversion ADU; lower-credit borrower; foundation intact | Smaller attached/interior ADU work ≤ $75K | Existing ADU on 2–3 unit property without depending on ADU rental for qualifying |

Verified May 19, 2026 against Fannie Mae Selling Guide B5-3.2-01, B5-3.2-02, B3-3.8-01, B3-5.1-01, B5-3.2-06; SEL-2025-10; HUD Mortgagee Letter 2023-17; HUD Mortgagee Letter 2024-13; Freddie Mac CHOICERenovation page and Bulletin 2026-1; FHFA November 25, 2025. Lender overlays may apply.

Decision tree: which renovation loan for your ADU?

- Detached new ADU + credit qualifies for conventional? → HomeStyle Renovation

- Attached or interior-conversion ADU + credit 580–619 + needs FHA? → FHA 203(k) Standard

- Smaller attached or conversion project ≤ $75K + credit 580+? → FHA 203(k) Limited (consultant optional and financeable per HUD ML 2024-13)

- Existing ADU on a 2–3 unit primary, don’t need ADU rent to qualify? → Freddie Mac CHOICERenovation

- VA-eligible + livability/safety repairs (no major structural)? → VA Renovation (very limited lender availability)

- Want to preserve a current low first-mortgage rate? → Skip all four; consider a HELOC or home equity loan

The FHA 203(k) gap for detached new ADUs

Under current HUD policy, eligible ADU work under the 203(k) program is limited to ADUs “attached to an existing Structure” or renovation of an existing ADU, per Mortgagee Letter 2023-17. A new detached ADU is not listed among eligible 203(k) uses. If you want to build a new backyard cottage from scratch, the 203(k) is out — HomeStyle, CHOICERenovation, or a construction-to-permanent loan is your path.

HomeStyle Renovation rates and total project costs in 2026

HomeStyle Renovation is a conventional first mortgage and is generally priced in line with conventional 30-year fixed and ARM products, subject to lender-specific renovation-loan adjustments. Closing costs run higher than a standard conventional refinance because of the renovation escrow, inspections, plan review, and contingency. We don’t publish promised rates or guaranteed spreads — get a written Loan Estimate from a Fannie Mae-approved HomeStyle lender for your specific scenario.

Cost components most lender pages bury

- Renovation escrow setup and servicing fees — set by the lender; ask for the fee schedule in writing

- Plan review fee for architect/engineer documents — set by the lender or third-party plan reviewer

- Per-draw inspection fees — a typical detached ADU build has 4–6 draw inspections (foundation, framing, rough-in, drywall and finishes, final)

- Contingency reserve — 0% required on 1-unit; 10% required and funded on 2–4 unit

- Six months of financed PITI if the home is uninhabitable during build — added to loan balance

- Architect / engineer / permit fees — financeable into the loan

- Title insurance endorsement for MH ADU — ALTA 7, 7.1, or 7.2 for manufactured-home accessories

Rate, fee, and APR information is not a loan offer, not guaranteed, varies by lender, credit, LTV, lien position, property, and state, and may not reflect APR with all fees. Always request the full Loan Estimate with renovation-loan-specific fees itemized.

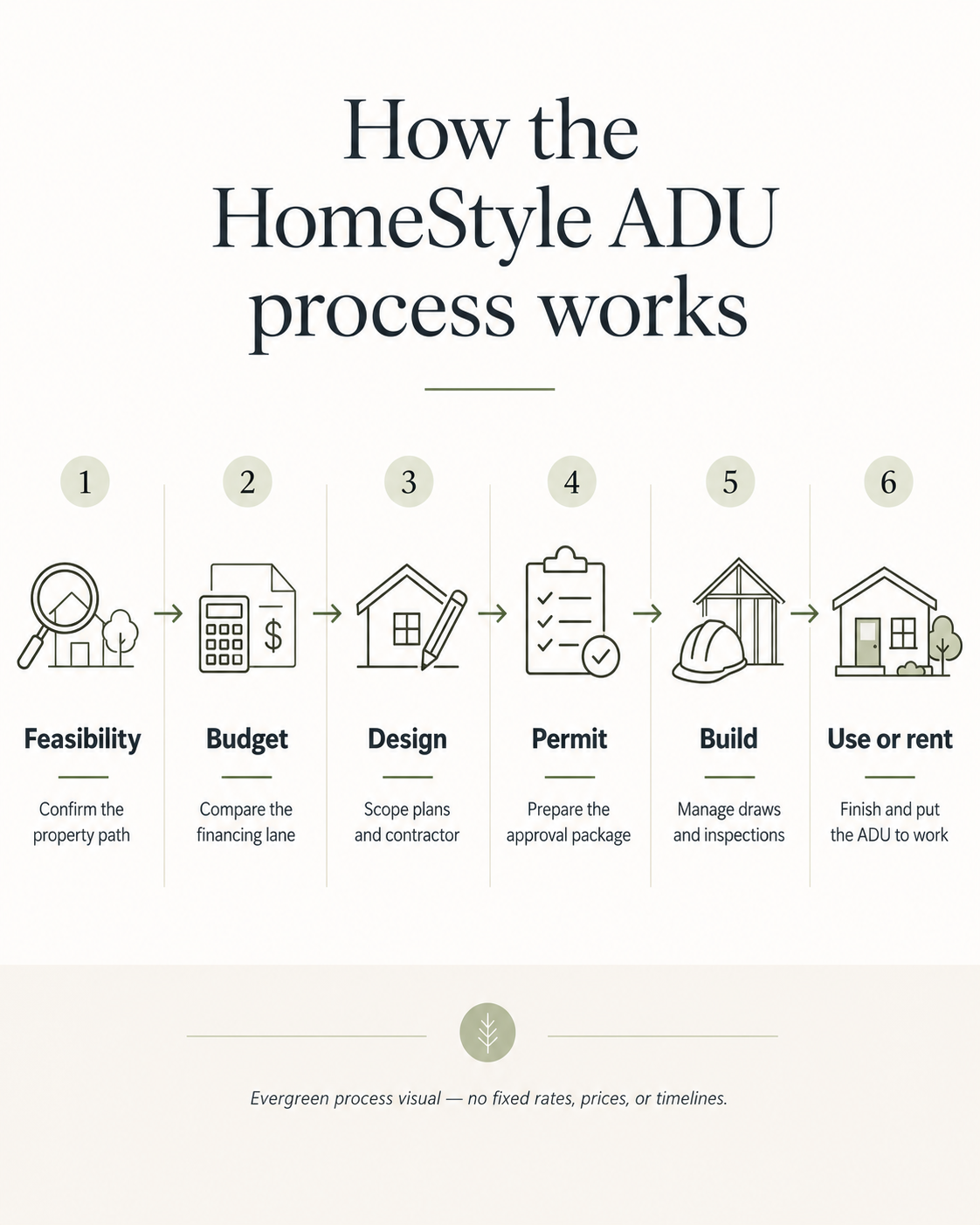

How the HomeStyle Renovation ADU process actually works

HomeStyle is a single-close loan: one application, one underwrite, one closing, one monthly payment that combines purchase or refinance with the renovation. The lender escrows renovation funds at closing and releases them in draws as the contractor hits documented milestones. Renovation work must be completed within 15 months of closing per Selling Guide B5-3.2-01, with extensions limited to no later than 18 months after closing in extenuating circumstances beyond the borrower’s control, per B5-3.2-06.

The 7 phases of a HomeStyle ADU project

- Pre-application. Confirm the lot is buildable. Run our property eligibility check to verify zoning, setbacks, lot coverage, fire-zone status, HOA covenants, and ADU classification before you spend a dollar on plans.

- Lender selection. Find a Fannie Mae-approved HomeStyle lender. Not every conventional mortgage lender offers this product — we cover availability below.

- Contractor and plans. The lender approves your general contractor. You submit detailed plans, specifications, a signed contract (Form 3730), and itemized cost estimates.

- Subject-to appraisal. The appraiser values the property “as completed” — as if the ADU were already built. The appraiser must review the ADU plans before producing the as-completed value. ADU comp availability matters here: in some counties, appraisers are still building their comp database for ADUs, which can compress the as-completed valuation.

- Underwriting and closing. The lender runs the Maximum Mortgage Worksheet (Form 1035), determines the final loan amount, schedules closing. Renovation contract and renovation loan agreement attach. Security instrument riders 3732 and 3733 record.

- Construction. Renovation must begin promptly per the renovation loan agreement. Up to 50% of total renovation costs may be disbursed at closing under SEL-2025-10. The remainder releases via milestone-triggered draws — typically 4 to 6 draws on an ADU build (foundation, framing, rough-in, drywall and finishes, final). Per-draw inspections verify progress before each disbursement.

- Completion and recourse removal. Final inspection, appraiser completion certificate on Form 1004D, lender obtains title update and certificate of occupancy where local authorities require one. Per B5-3.2-05, the lender submits the completion package to Fannie Mae to remove recourse. Any unused contingency reserve applies to loan principal.

Required document checklist

- ADU scope of work and detailed plans

- Contractor’s signed contract (Form 3730) and itemized bid

- Contractor profile / lender-required documentation (license, bonding, insurance)

- Permits or documented permit path

- Local zoning confirmation

- As-completed appraisal report (Form 1004 with subject-to addendum)

- Renovation loan agreement

- Lien waiver from contractor and subcontractors at final disbursement (Form 3739)

- Title endorsements where required (ALTA 7 / 7.1 / 7.2 for MH ADU)

- Certificate of occupancy at completion, where local code requires it

- Property insurance certification post-completion

Lender script for the program-fit conversation

“I’m evaluating a Fannie Mae HomeStyle Renovation loan for an ADU. The project is [detached new construction / attached addition / garage conversion / basement conversion / manufactured-home ADU]. Do you originate HomeStyle Renovation loans, and do you have the Fannie Mae special approval to deliver loans before renovation completion? Have you adopted UAD 3.6 policy? What ADU documentation do you require — plans, permits, contractor bid, soils report? How do you handle the 50% upfront disbursement under SEL-2025-10? Do you allow ADU rental income, and under what documentation — Form 1007, lease, Schedule E? Do you have lender overlays on detached ADUs, manufactured-home ADUs, or local permit status? What’s your expected timeline from application to closing, and what are your renovation-escrow and per-draw inspection fees in writing?”

What slows the process

- Missing or incomplete contractor bids (most common kill)

- Plans that don’t comply with local zoning surfacing late

- Appraisal challenges — ADUs are still comp-thin in many counties

- HOA covenants or owner-occupancy requirements not surfaced until late

- Title issues, especially for MH ADU transactions

- Contractor without renovation-loan prior experience underestimating draw paperwork

How to find a HomeStyle Renovation lender

Fannie Mae Selling Guide B5-3.2-01 requires lenders to obtain special approval to deliver HomeStyle Renovation loans before renovation completion. Not every mortgage lender carries the program, and the lenders that do tend to be banks, credit unions, and renovation-specialty shops rather than the largest online mortgage retailers. Rocket Mortgage’s own learning center confirms it does not offer HomeStyle Renovation loans.

How to verify a lender’s HomeStyle Renovation availability

- Check the lender’s current product page for “HomeStyle Renovation” or “Fannie Mae HomeStyle.” If the program isn’t listed, it’s a strong signal they don’t originate it.

- Call the lender and ask: “Do you originate Fannie Mae HomeStyle Renovation loans, and do you have the Fannie Mae special approval to deliver them before renovation completion?”

- Ask about UAD 3.6 policy adoption if your project depends on the expanded multi-ADU or MH-ADU rules effective March 31, 2026.

- Cross-check with Pennymac correspondent announcements if you’re working through a smaller broker — many smaller lenders deliver HomeStyle through correspondent relationships with aggregators like Pennymac, and the aggregator’s announcements (e.g., Pennymac Announcement 26-33) reveal program availability.

- Verify lender state availability — some lenders are licensed in limited states, and renovation programs sometimes have narrower state availability than the lender’s main products.

Lenders whose current product pages list HomeStyle Renovation (verified May 19, 2026)

| Lender | Source | Notes |

|---|---|---|

| Huntington Bank | huntington.com | Min reno $5K, max $250K per lender page; renovations within 12 months of close per their stated policy |

| PrimeLending | primelending.com | HomeStyle and Freddie Mac CHOICERenovation |

| CMG Home Loans | cmghomeloans.com | HomeStyle Renovation product page |

| Society Mortgage | societymortgage.com | 620 credit floor per their product page |

| Pennymac (correspondent) | corr.pennymac.com | HomeStyle Renovation correspondent product |

| Pennsylvania Housing Finance Agency (PHFA) | phfa.org | Through PHFA participating lenders; Pennsylvania only |

| Clear Lending | clearlending.com | Renovation Program product page |

| Waterstone Mortgage | waterstonemortgage.com | 3% down for first-time buyers (HomeReady-paired) |

| Andes Mortgage | andesmortgage.com | HomeStyle Renovation product page |

Lender product portfolios change. Always confirm HomeStyle availability by direct phone call before applying. This list is provided for borrower benefit, not for affiliate revenue.

Lenders who confirm they do not offer HomeStyle Renovation

| Lender | Source |

|---|---|

| Rocket Mortgage | Rocket Mortgage learning center states they do not currently offer renovation mortgages |

| Navy Federal Credit Union | Navy Federal’s Home Project Financing Center lists HELOCs, home equity loans, and personal loans — HomeStyle not listed; verify directly with NFCU before applying |

Three reliable places to find a HomeStyle Renovation lender

- Local credit unions and community banks — many smaller lenders carry the program because they specialize in the construction-period oversight that big retail shops avoid.

- Mortgage brokers who handle renovation loans — independent brokers often have correspondent relationships with HomeStyle-approved aggregators.

- Builder-recommended lenders, with verification — ADU builders in active markets work with HomeStyle-experienced loan officers regularly. Verify the program is HomeStyle (and not a non-conforming in-house product) before relying on a builder referral.

We don’t have a compensated relationship with any HomeStyle Renovation originator. This list exists to help you find a lender, not to route you to one we earn from.

The honest downsides

HomeStyle Renovation isn’t the right product for most ADU borrowers. Renovation lending has historically had higher denial rates than standard purchase or refinance lending, and lender participation is narrower because lenders bear recourse to Fannie Mae for delays, cost overruns, and poor-quality workmanship during the renovation period. If you have meaningful equity and a low-rate first mortgage, a HELOC or home equity loan is almost always the better path.

Specific dealbreakers

- You bought your home in 2020–2022 at a sub-5% rate. Replacing that mortgage with a HomeStyle refi often costs more in lifetime interest than the ADU itself.

- Your local appraiser pool can’t pull ADU comps. Without a defensible as-completed valuation, the 75%-of-as-completed-value renovation cap may not give you enough loan room.

- You want to tear down and rebuild. Not allowed. A complete teardown to the foundation is excluded by B5-3.2-01.

- Your contractor isn’t bondable. Many smaller ADU specialists operate without bonding; HomeStyle lenders typically require it for the construction period.

- Your permitting plus build is likely to exceed 15 months. The 15-month completion rule from B5-3.2-01 is real. Extensions are at Fannie Mae’s sole discretion and capped at 18 months per B5-3.2-06.

Roadblock-to-action matrix

| Roadblock | Why it matters | What to do next |

|---|---|---|

| Local zoning doesn’t allow the ADU | Fannie Mae eligibility and appraisals still depend on legal/zoning treatment | Verify zoning and permit path before lender application |

| Unit would be classified as a separate dwelling, not an ADU | Detached doesn’t automatically mean eligible accessory unit | Ask lender / appraiser how the property will be classified |

| Appraisal can’t support the as-completed value | Loan math may fail even if the program permits the project | Pull realistic comps and avoid overbuilding for the market |

| County loan limit is too low | Renovation budget can pass the 75% cap but loan amount can still exceed conforming limit | Check county limit at the FHFA loan limit lookup |

| Existing first mortgage is below market | Refinancing destroys the economics | Compare HELOC or home equity loan first |

| Contractor can’t operate with the draw process | Renovation loans require milestone documentation and inspections | Pre-screen contractor for HomeStyle or 203(k) prior experience |

| Manufactured ADU classification not real property | MH ADU eligibility is technical | Confirm permanent foundation, title, HUD data plate, and B5-2-05 compliance |

| Rental income assumption too aggressive | Existing-ADU rules are clearer than proposed-ADU rules | Ask lender how they’ll treat ADU rent before relying on it |

| Timeline likely exceeds 15 months | Permit and build cycles can break program fit | Consider construction-to-permanent or phased strategy |

We’ve written this section to help you decide. We are not the lender. We don’t earn money when you originate a HomeStyle loan. The 7-path comparison on our ADU Financing Options 2026 hub covers the alternatives in similar depth.

Is HomeStyle Renovation right for your ADU? A 6-question fit check

Run this six-question check before you call a lender. If you answer yes to questions 1–3 and yes to at least one of 4–6, HomeStyle is worth a serious conversation. If you answer no to question 1 or 2, a different financing path will probably serve you better.

- Does your credit and debt profile meet the lender’s HomeStyle Renovation underwriting (Fannie Mae’s published manually-underwritten minimum is 620; most lenders impose overlays in the 640–680 range)?

- Is your ADU project (a) detached new construction, (b) a substantial attached or interior renovation, (c) a manufactured-home ADU, or (d) a purchase-plus-ADU bundle on a 1–4 unit property?

- Are you OK replacing your current first mortgage (or originating a new one as part of a purchase)?

- Is your current first-mortgage rate at or above today’s market — or are you a buyer without an existing mortgage to protect?

- Do you need to borrow against the home’s future value because your current equity isn’t enough?

- Will you use the ADU’s rental income to qualify, and is the ADU existing (clearly covered by Fannie’s rental rules) — or are you prepared to confirm proposed-ADU income treatment with the lender directly?

See what you can build before you call a lender

The fit check above is rules-only. It doesn’t know whether your specific address can host the ADU you’re planning. That’s what our free property report does — in 60 seconds, we check zoning, setbacks, lot coverage, fire zone, HOA, coastal status, and ADU classification on your actual parcel before you commit to any financing path.

Get your free ADU report in 60 seconds →Step by step: how to test HomeStyle before you apply

Don’t start with a full loan application. Start with a rule check: ADU legality on your parcel, project classification, rough budget, as-completed value estimate, loan-limit fit, current-mortgage tradeoff, and lender availability.

- Confirm your city or county allows the ADU type you want.

- Confirm the unit will be classified as an accessory dwelling unit, not a separate non-accessory dwelling.

- Get a preliminary contractor scope and cost from a builder with renovation-loan experience.

- Estimate as-completed value using comparable sold ADU properties in your zip code.

- Run the 75% (or 50% for MH-primary) renovation-cost cap against your project.

- Check the applicable county conforming loan limit at the FHFA tool.

- Decide whether replacing your current first mortgage is acceptable economically.

- Ask the lender directly whether they originate HomeStyle Renovation loans, whether they have UAD 3.6 policy adopted, and what their current renovation-loan rate band and fee schedule are.

- Ask how they’ll treat ADU rental income for qualification.

- Compare HomeStyle against HELOC, CHOICERenovation, 203(k), construction-to-permanent, and cash-out refi using the matrix above.

Real homeowner perspectives on HomeStyle and ADU financing

Three patterns emerge consistently in homeowner discussion threads: borrowers report difficulty finding lenders who actually originate the product; the friction point that stops most successful applicants from finishing is the contractor approval and draw process, not the underwriting; the homeowners who succeed tend to bring a single experienced general contractor with prior renovation-loan project history.

“I thought this was the hard part — getting ADUs legalized — but it turns out, financing will be my biggest challenge.”

The answer surfacing across forum discussion: yes, HomeStyle works for ADUs — but it works best when you bring an experienced contractor and pair them with a renovation-specialist lender. In markets where ADUs are newer, the lender-contractor pairing is harder to assemble.

This synthesizes patterns from public forum discussion only; it is not a representation that any specific outcome is typical. See our Editorial Standards →

Frequently asked questions

Can a HomeStyle Renovation loan be used to build a detached ADU?

Yes. Fannie Mae Selling Guide B5-3.2-01 permits funding of accessory units when allowed by local zoning. Unlike the current FHA 203(k) program, HomeStyle does not restrict eligibility to attached or interior ADUs — a detached new-construction ADU is an eligible HomeStyle use.

What is the minimum credit score for a HomeStyle Renovation loan?

For manually underwritten fixed-rate Fannie Mae loans, the published minimum credit score is 620; manually underwritten ARMs require 640. Most HomeStyle Renovation transactions run through Desktop Underwriter, which does not apply a single minimum-score gate in the same way. Many lenders impose overlays that raise the effective floor to 640, 680, or higher for renovation transactions.

Can I use ADU rental income to qualify?

For an existing ADU on a 1-unit principal residence, yes — purchase or limited cash-out refinance only, one ADU only, 75% of gross rent applied, capped at 30% of total qualifying income. Desktop Underwriter 12.1 automates this rule for eligible casefiles. Fannie Mae's published rental-income rule expressly addresses existing ADUs; if your ADU is proposed, confirm with your lender how they will treat projected ADU income before relying on it.

How many ADUs can I have on a property with HomeStyle financing?

Under standard Fannie Mae ADU rules, generally one ADU on a 1-unit primary residence. Effective March 31, 2026 for lenders using UAD 3.6 policy, up to three ADUs on a 1-unit primary residence and up to four total dwellings on a 2–3 unit property, provided local zoning allows.

Can I do the ADU work myself with a HomeStyle loan?

On a 1-unit property only, and only if DIY work doesn't exceed 10% of the as-completed value. The lender must review and approve plans in advance and inspect completion of any item costing more than $5,000. You cannot reimburse yourself for sweat-equity labor — only for documented contract labor or materials. DIY is not permitted on manufactured homes.

Does HomeStyle require the home to be habitable at closing?

No. Up to six months of principal, interest, taxes, and insurance can be financed into the loan to cover the uninhabitable period during construction.

What is the maximum HomeStyle Renovation loan amount in 2026?

$832,750 for a 1-unit property in standard areas; $1,249,125 in high-cost areas per FHFA's November 25, 2025 conforming loan limit announcement. Multi-unit limits scale up to $1,601,750 for a 4-unit standard and $2,402,625 for a 4-unit in high-cost areas.

Is HomeStyle Renovation a construction loan?

No. HomeStyle is a permanent first-mortgage loan with a renovation escrow attached. It funds at closing and converts to standard mortgage servicing on completion — no separate construction-to-permanent refinance is required.

Can HomeStyle fund a second home or investment property ADU?

Yes. Standard HomeStyle eligibility extends to 1-unit second homes (10% down) and 1-unit investment properties (15% down to purchase, 25% to refinance). The 30% ADU rental-income cap is specific to 1-unit primary residences; investment-property rental rules under Selling Guide B3-3.1-08 differ.

Does Rocket Mortgage offer HomeStyle Renovation loans?

No. Rocket Mortgage's own learning center states it does not currently offer renovation mortgages.

Is the FHA 203(k) better than HomeStyle for an ADU?

For an attached, interior, or garage-conversion ADU with a borrower who has a 580–619 credit score, the 203(k) is often the better path — particularly the Limited 203(k) if the project is under $75,000 per HUD Mortgagee Letter 2024-13. For a detached new-construction ADU, no — under current HUD policy, detached new-construction ADUs are not listed among eligible 203(k) uses.

How long do I have to complete the renovation?

Renovation work must be completed no later than 15 months from the date the loan is closed, per Selling Guide B5-3.2-01. Extensions are at Fannie Mae's sole discretion in extenuating circumstances beyond the borrower's control and limited to no later than 18 months after closing per B5-3.2-06.

What happens if the ADU project goes over budget?

HomeStyle does not automatically cover overruns. On a 2–4 unit property, the lender funds a 10% contingency reserve that absorbs unforeseen costs. On a 1-unit property, contingency is optional but lender-encouraged. Overruns beyond contingency typically require the borrower to fund out of pocket or pursue a second-lien product post-completion.

Can HomeStyle cover architect, design, and permit costs?

Yes. Eligible renovation-related soft costs — architect and engineering fees, permit fees, plan-review fees — can be financed when documented and within program rules. Under SEL-2025-10, up to 50% of total renovation costs may be disbursed at closing to cover contractor deposits, material expenses, and permit fees.

Does Dwelling Index lend money?

No. The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We publish education, decision tools, and reviews. We are not a lender, broker, or builder, and we do not guarantee approval for any loan product.

How we researched this guide (methodology)

We synthesized Fannie Mae’s primary-source Selling Guide sections (B5-3.2-01, B5-3.2-02, B5-3.2-05, B5-3.2-06, B2-3-04, B4-1.3-05, B5-2-05, B3-3.8-01, B3-5.1-01), Selling Guide Announcement SEL-2025-10 (Dec 10, 2025), Selling Guide Announcement SEL-2025-08, DU 12.1 Release Notes (Feb 18, 2026), the HomeStyle Renovation FAQ, and the Fannie Mae ADU policy page. We cross-referenced HUD Mortgagee Letter 2023-17 and HUD Mortgagee Letter 2024-13 for FHA 203(k) ADU and program-update policy, Freddie Mac CHOICERenovation materials and Bulletin 2026-1, and FHFA’s November 25, 2025 conforming-loan-limit announcement. We checked Pennymac correspondent product profiles for lender-level implementation details. Lender availability was verified by visiting each named lender’s current public product page on the verification date; lender product portfolios change, so always confirm by direct call before applying.

We do not interview Fannie Mae or HUD staff, we do not run loans ourselves, and we do not have a compensated relationship with any HomeStyle Renovation originator. The lender list in this guide is provided for borrower benefit, not for affiliate revenue.

Read our full editorial standards · Read our corrections policy · Read our partner vetting policy

Related Dwelling Index guides

- ADU Financing Options 2026: 7 Paths Compared → — Compare HomeStyle to all other ADU financing paths.

- HELOC for ADU → — Preserve a low first-mortgage rate with a second lien.

- Property Eligibility Check → — Confirm your project is buildable before you call a lender.

- How Much Does an ADU Cost? → — Understand total build cost by ADU type.

- ADU Cost Per Square Foot → — See real $/sq ft by ADU type and state.

- FHA 203(k) Loan for ADU → — Deep dive on the FHA renovation alternative.

- Browse all Financing articles →

Free ADU Financing Starter Kit — every path, every doc requirement, every common gotcha in one PDF.

Building or financing an ADU is a multi-month decision. We put the most-asked questions into a single PDF you can keep on your phone through the process.

Download the Free ADU Financing Starter Kit →Email + ZIP code only. Unsubscribe anytime.

Not sure where to start?

See what’s possible at your address — get your free ADU report in 60 seconds.

See what you can build at your address →Last updated: May 19, 2026 · Last verified: May 19, 2026 · Next scheduled refresh: June 19, 2026 · Affiliate disclosure · Editorial standards · Methodology