ADU After-Renovation Value Loan: How Future-Value Financing Works in 2026

At a glance: which path should you test first?

The full breakdown comes later. This table exists so you can find your situation in fifteen seconds.

| Your situation | First path to test | Why | Watch out for |

|---|---|---|---|

| Enough current equity and a low first-mortgage rate | Standard HELOC or home-equity loan | Keeps your first mortgage untouched | Current-value cap may not cover the ADU budget |

| Little current equity, want to keep your first mortgage | Second-lien after-renovation-value (ARV) HELOC / home-equity product | Uses future value without refinancing the first mortgage | Availability varies by state and lender; credit, DTI, and appraisal still gate it |

| Buying or refinancing anyway and want to wrap the ADU in | Fannie Mae HomeStyle or Freddie Mac CHOICERenovation | One conventional mortgage covers the home and the ADU build | More documents, contractor draws, completion rules |

| Using FHA, lower credit or down payment | FHA Standard 203(k) | FHA-insured rehab loan; funds attached/eligible ADU work | Best for attached ADUs; not the first path for a new detached unit |

| Large ground-up detached ADU | Construction-to-permanent loan | Funds the build in stages, then converts to a mortgage | Single close, but tight draw management matters |

| Not sure the lot even qualifies | Feasibility check first | Financing fails if the ADU can’t be permitted | Zoning, setbacks, utilities, parking, owner-occupancy, HOA |

The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation.

Check your property before you shop loans. A future-value loan only helps if the ADU itself is legal, buildable, and likely to support the appraisal.

By the Dwelling Index Editorial Team · Last updated: · Last verified: · ~35 min read

An independent guide from Dwelling Index — an independent research resource covering ADU financing, costs, and regulations. We are not a lender, appraiser, builder, or zoning authority.

What is an ADU after-renovation value loan?

An ADU after-renovation value loan is any financing where the lender considers the projected value of your property after the ADU is complete — its “as-completed” appraised value — rather than only your current equity. It is not a single product. It’s an underwriting idea used inside several different loan types: renovation mortgages, construction loans, and certain home-equity products. Fannie Mae’s HomeStyle Renovation program sizes loans against “as-completed” appraised value. So does Freddie Mac’s CHOICERenovation, FHA’s Standard 203(k), and so-called RenoFi-style ARV home-equity products. These are all different products that share the same underwriting idea.

That single distinction — concept, not product — is the thing nearly every competing page gets wrong, and it’s why homeowners end up confused. You can’t “apply for an after-renovation value loan.” You apply for a HomeStyle Renovation mortgage, or a RenoFi-arranged renovation home-equity loan, or an FHA 203(k), and those products use after-renovation value as the number they lend against.

A quick vocabulary reset, because lenders use four words for the same idea and it makes people feel lost when they shouldn’t:

| Term you’ll see | What it actually means |

|---|---|

| After-renovation value (ARV) | What your home is expected to be worth once the ADU is finished |

| As-completed value | The appraisal industry’s term for that same finished value |

| After-improved value | Another synonym used in renovation lending |

| Subject-to-completion appraisal | An appraisal that values the home as if the planned ADU is already built |

| LTV / CLTV | Loan-to-value / combined loan-to-value — your total loans divided by the home’s value |

| DTI | Debt-to-income ratio — your monthly debts divided by gross monthly income |

| Draw schedule | Construction money released in stages as work passes inspection |

| Lien position | Whether a loan sits first (your primary mortgage) or second (behind it) against your home |

Why this matters right now: financing is one of the central barriers limiting ADU construction, especially for homeowners without enough cash or current equity. UC Berkeley’s Terner Center for Housing Innovation maps this financing gap and finds that most ADU builders rely on cash and mortgage debt, while recommending reforms to renovation-loan underwriting, appraisal, and ADU rental-income treatment. The reason the gap bites hardest here is structural: the people with the highest need to build ADUs — recent buyers, families in high-cost markets — are precisely the ones with the least current equity.

Is this the same as an ADU renovation loan, construction loan, or HELOC?

No — these terms overlap but they are not interchangeable. A standard HELOC or home-equity loan for an ADU is almost always based on your current value. A renovation mortgage (HomeStyle, CHOICERenovation, FHA 203(k) loan for an ADU) wraps the ADU into a first-lien mortgage based on future value. A ADU construction loan funds the build through draws. A RenoFi-style ARV home-equity product uses future value while keeping your first mortgage in place. The labels collapse into one practical question: does this lender size my loan against what the property is worth today or what it will be worth after the ADU is built?

Here’s the decoder that resolves most of the confusion:

| Loan label | Current or future value? | First or second lien? | Replaces your current first mortgage? | Best use |

|---|---|---|---|---|

| Standard HELOC | Current value | Second lien | No | Enough equity; you want to keep a low first-mortgage rate |

| Home-equity loan | Current value | Second lien | No | Fixed lump sum, you already have equity |

| ARV HELOC / ARV home-equity (RenoFi-style) | Future / as-completed | Usually second lien | Usually no | Little current equity, want to preserve the first mortgage |

| Renovation mortgage (HomeStyle / CHOICERenovation) | Future / as-completed | First lien | Usually yes | Buying or refinancing and building the ADU |

| FHA 203(k) | Future / as-completed | First lien | Usually yes | FHA borrower, lower credit/down payment |

| Construction loan | Future project value | Varies | Varies | Ground-up detached ADU |

| Construction-to-permanent | Future value | First lien | Usually yes (new mortgage) | Large build or purchase-plus-build |

Read that “replaces your first mortgage” column carefully, because it’s the most expensive mistake in ADU financing. If you locked a 3% mortgage in 2021 and you refinance into a 2026 HomeStyle loan to fund your ADU, you don’t just borrow for the ADU — you re-price your entire existing balance at today’s rate. For a homeowner with a large, low-rate balance, that can cost more over time than the ADU itself. The second-lien ARV products exist precisely so you don’t have to make that trade.

A damaging admission, because you deserve the truth before you spend money on plans: future-value financing is not easy money. The phrase “borrow against what your home will be worth” sounds like a loophole, and some lenders market it that way. But the loan still fails if the finished appraisal doesn’t support the value, if the ADU can’t be legally permitted, if your contractor can’t meet the lender’s documentation and draw requirements, or if your income and credit don’t qualify.

If you’re exploring this because you want to finance an ADU with no equity, future-value underwriting is the place to look — but the caveats above apply in full. For the broader landscape, see our guide to the best ADU financing options.

How does borrowing against future value actually work?

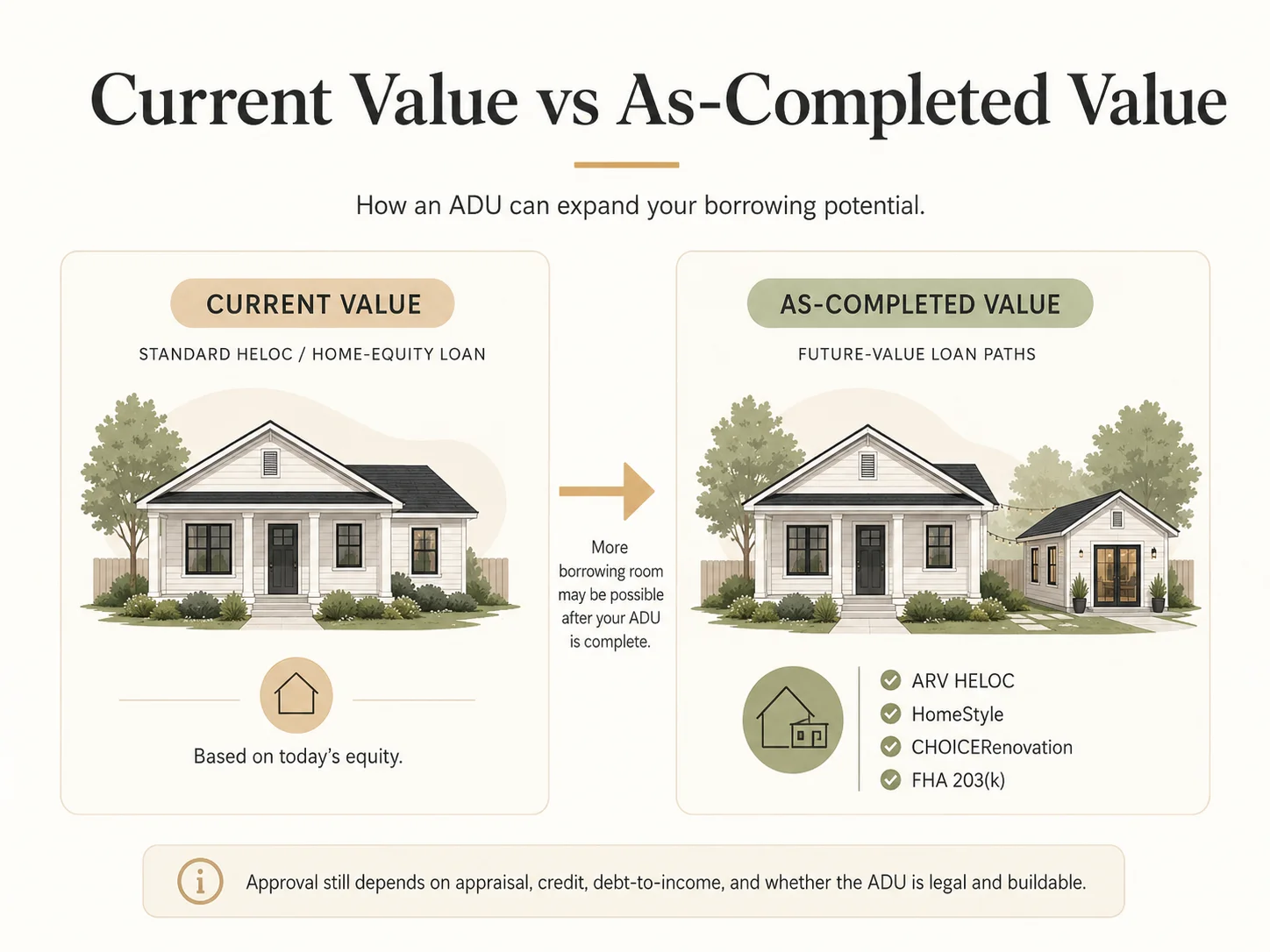

A traditional HELOC caps you near 80% of your home’s current value minus what you owe — which can leave a recent buyer with literally $0 to borrow. An after-renovation-value product instead lets you borrow up to roughly 90% of the as-completed value, unlocking the future equity the ADU itself creates. The mechanism is a “subject-to-completion” appraisal: the appraiser values your home as if the documented ADU is already built, and the lender lends against that number.

Let’s run it with real arithmetic, because “you can borrow more” is meaningless until you see the dollars. This is an illustrative example, not a guarantee — your actual numbers depend on the appraisal, your credit, DTI, the lender, and loan limits.

Scenario: You bought two years ago. Home is worth $600,000, you owe $480,000. Your ADU quote is $175,000, and a subject-to-completion appraisal projects the finished property at $750,000.

| Financing approach | Formula | Borrowing room |

|---|---|---|

| Standard 80% current-value HELOC | $600,000 × 80% − $480,000 | $0 |

| 85% current-value home-equity product | $600,000 × 85% − $480,000 | $30,000 |

| 90% after-renovation-value product | $750,000 × 90% − $480,000 | $195,000 |

That’s the whole story in three rows. At 80% of current value you cannot build at all. At 90% of the as-completed value, the ADU becomes fundable — and the $195,000 of room comfortably covers a $175,000 project. RenoFi, the platform that popularized this structure for ADUs, publishes the same logic: it says most of its partner lenders allow loans covering up to $750,000 in renovation costs, with borrowing up to 125% of current home value and up to 90% of after-renovation value.

These are illustrative examples, not guarantees of approval, loan amount, monthly payment, interest rate, or return. Actual results depend on appraisal, income, credit, lender rules, loan limits, local market conditions, construction costs, and regulatory approvals.

A word of caution on value-add math: don’t underwrite your project using a generic “ADU adds X%” percentage you read online. The as-completed appraisal controls your borrowing room, and an appraiser may not credit the ADU dollar-for-dollar against what you spend, especially in markets where ADUs are less common. The gap between what you spend and what the appraisal supports is the single most important risk in this entire category.

See your own number

You don’t have to do this math by hand for your own home. Our ADU Financing Worksheet takes your current value, mortgage balance, ADU budget, and ADU type, then shows your current-value borrowing room beside your possible future-value borrowing room — so you can see your personal gap and which path your numbers point toward, plus the document checklist you’ll need.

Includes your current-equity room vs. possible future-value room and a lender-question script.

Which ADU future-value loan products are real in 2026?

The main future-value ADU financing paths are Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, FHA Standard 203(k), RenoFi-style ARV home-equity products, construction-to-permanent loans, and a small number of local credit-union and state programs. The single biggest difference between them is lien position — whether the product replaces your first mortgage or sits behind it as a second lien. Everything else (rate, term, draw process) is secondary to that one fork.

The 2026 ADU Future-Value Loan Fit Matrix below covers value basis, lien position, ADU type, rent-qualification rules, and state availability. To assemble the equivalent yourself, you’d have to read Fannie Mae’s Selling Guide, Freddie Mac’s bulletins, HUD’s Mortgagee Letters, FHFA’s limit tables, and RenoFi’s disclosures, then reconcile the conflicting and often stale numbers floating around builder blogs.

| Path | Future / as-completed value? | Lien position | New detached ADU fit? | Can projected ADU rent help qualify? | 2026 limit / cap | State / availability watch-out | Best for | Last verified |

|---|---|---|---|---|---|---|---|---|

| Fannie Mae HomeStyle Renovation | Yes — as-completed value | First lien (usually replaces) | Yes (one-unit; expanded multi-unit/multiple-ADU needs UAD 3.6) | Per Fannie ADU rental-income rules and caps | Conforming: $832,750 baseline / $1,249,125 high-cost (2026); reno ≤ 75% of as-completed value | Expanded 2026 rules only for lenders on UAD 3.6 | Conventional borrower wrapping the ADU into a purchase or refi | May 22, 2026 |

| Freddie Mac CHOICERenovation | Yes | First lien (usually) | Yes, subject to program rules | No for any unit included in the renovation project (applications on/after May 4, 2026) | Conforming limits as above | Funded-unit rent exclusion (Bulletin 2026-1) | Conventional borrower; the Freddie sibling to HomeStyle | May 22, 2026 |

| FHA Standard 203(k) | Yes — as-completed value | First lien (usually) | Best for attached; not the first path for a new free-standing detached unit | Yes — 50% rule for new ADU (no history); see rent table | HUD consultant required; FHA MI applies | Verify detached eligibility in writing | FHA borrower, lower credit/down payment | May 22, 2026 |

| FHA Limited 203(k) | Limited (minor/non-structural) | First lien (usually) | No | Limited | Rehab cap $75,000 (2024 update) | Not for additions, structural work, or new builds | Small attached/existing ADU rehab | May 22, 2026 |

| RenoFi-style ARV HELOC / home-equity | Yes — up to 90% of ARV | Often second lien | Depends on lender/state/scope | Lender-dependent | Up to $750K project (most lenders) | Lender programs vary by state; NY mortgage-solicitation limitation noted | Equity-light owner who wants to keep a low first mortgage | May 22, 2026 |

| Construction-to-permanent | Yes — future appraised value | First lien (new mortgage) | Yes | Lender-dependent | Lender-set | Local/regional lender verification | Larger / detached builds | May 22, 2026 |

| Standard HELOC / home-equity | No — current value | Second lien | Funds any legal ADU if proceeds allow | Generally no projected-rent boost | Lender-set | May not provide enough room | Owner with ample existing equity + a low first mortgage | May 22, 2026 |

| Cash-out refinance | Usually current value | First lien (replaces) | Funds any legal ADU | Per agency rules | Lender-set | Replaces first mortgage — painful with a low existing rate | Borrower already planning to refinance | May 22, 2026 |

2026 conforming limits are the FHFA baseline ($832,750) and high-cost ceiling ($1,249,125) for one-unit properties; confirm your county’s limit. Sources: FHFA; Fannie Mae; Freddie Mac Bulletin 2026-1; HUD ML 2023-17; HUD ML 2024-13; RenoFi. Verified May 22, 2026.

Fannie Mae HomeStyle Renovation — and what just changed

Fannie Mae HomeStyle Renovation is a conventional first mortgage that bundles a home purchase or refinance with the cost of building an ADU into a single loan, underwritten against the as-completed appraised value. Because it’s conventional, there’s no upfront mortgage-insurance premium and no monthly mortgage insurance once your loan-to-value drops below 80%. It supports internal, attached, detached, and certain manufactured ADUs on eligible properties; for expanded multi-unit or multiple-ADU scenarios, confirm your lender is using Fannie Mae’s UAD 3.6 policy. (Source: Fannie Mae ADU page, verified May 22, 2026.)

Fannie Mae overhauled HomeStyle Renovation in late 2025 — changes most competing pages haven’t caught up to:

- Bigger upfront draws. Lenders may now disburse up to 50% of total renovation costs at closing for materials, permits, architectural and design expenses, and borrower deposits. For ADU builders this matters: contractors can procure materials early instead of fronting them. (Source: Fannie Mae SEL-2025-10, Dec. 2025.)

- Expanded ADU eligibility, on a clock. Fannie expanded ADU eligibility for certain multi-unit properties, multiple ADUs on single-unit properties, and manufactured-home scenarios effective March 31, 2026 — but those expanded rules are only available to lenders using UAD 3.6 policy. All lenders must use UAD 3.6 for new appraisal reports submitted on or after November 2, 2026. (Source: SEL-2025-10, verified May 22, 2026.)

- HomeStyle Refresh. A companion product effective for application dates on or after March 31, 2026, capped at 15% of as-completed appraised value. It is not the path for a full ADU build — treat it as a lighter-touch option for smaller scopes. (Source: Fannie Mae HomeStyle Refresh B5-3.3-01, verified May 22, 2026.)

The practical takeaway: if a lender or blog quotes you HomeStyle rules from 2023 or 2024, the draw structure they describe is out of date. The newer rules are friendlier to ADU cash flow.

Freddie Mac CHOICERenovation — the conventional sibling

Freddie Mac’s CHOICERenovation is the Freddie equivalent of HomeStyle: a conventional renovation mortgage that, per Freddie Mac, can be used to add a new ADU or renovate an existing one, in a single-closing purchase or refinance structure. If your lender doesn’t offer HomeStyle, they may offer CHOICERenovation, and the borrower experience is broadly similar.

There is one 2026 rule you must know before you count on rental income: effective for CHOICERenovation mortgages with application received dates on or after May 4, 2026, rental income from any unit included in the renovation project funded by the mortgage proceeds cannot be used to qualify the borrower. Only rental income from units not included in the renovation project may be considered. In plain English: if you’re using a CHOICERenovation loan to build the ADU, you generally can’t lean on that new ADU’s projected rent to qualify. (Source: Freddie Mac Bulletin 2026-1, verified May 22, 2026.)

FHA Standard 203(k) — the lower-barrier path, with one hard limit

FHA’s Standard 203(k) is a rehabilitation mortgage that lets lower-credit or lower-down-payment borrowers finance both a home and eligible ADU work in one FHA-insured loan, based on the as-completed value. Per HUD Mortgagee Letter 2023-17, eligible improvements include adding an ADU that will be attached to the existing structure, and renovating an existing ADU that is attached or detached to the primary residence.

Here’s the damaging admission you need, stated plainly: do not use FHA 203(k) as your first path for a brand-new, free-standing detached ADU unless your lender gives you written FHA/HUD-backed confirmation. HUD’s own guidance is read by industry experts as not permitting the 203(k) to create a new detached unit, even as it lists improvements like garage construction as eligible — the line is genuinely blurry, and you don’t want to discover that mid-project. If you’re building a detached backyard ADU, HomeStyle, CHOICERenovation, or a construction loan are cleaner paths; keep 203(k) for attached additions, garage/basement conversions, and existing-ADU renovations. (Sources: HUD ML 2023-17; NAHB; Shelterforce. Verified May 22, 2026.)

The FHA Limited 203(k) is a separate, smaller product: capped at $75,000 in rehabilitation costs (raised in HUD’s 2024 update) and for minor, non-structural rehabilitation. Don’t position it for ADU additions, major garage conversions, foundation or structural work, or new ADU construction — that’s Standard 203(k) territory, which requires a HUD consultant. (Source: HUD ML 2024-13, verified May 22, 2026.)

RenoFi-style ARV home-equity products — keep your first mortgage

A RenoFi-style ARV product is a renovation home-equity loan or HELOC that lets you borrow against your home’s after-renovation value — up to 90% of it, on projects up to $750,000 with most lenders — usually as a second lien that leaves your existing first mortgage untouched. That last part is the entire appeal for anyone holding a low pandemic-era rate.

RenoFi is not a lender; it works with partner third-party lenders (NMLS #1802847). RenoFi says lender programs vary by lender and by state, and its site states that no mortgage solicitation or loan applications for New York properties can be facilitated through the site — so check state availability before you rely on it. (Source: RenoFi, verified May 22, 2026.)

We’re naming RenoFi because it would be dishonest not to — it’s the most relevant product to this exact search. We are not linking to it as a financing partner on this page.

Local and state ADU finance programs

A growing number of state programs offer ADU-specific or future-value financing, but rules vary heavily by market — treat these as examples, not a national guarantee. Two verified examples:

| Program | State | Max assistance | Who qualifies | Status note | Last verified |

|---|---|---|---|---|---|

| MassHousing ADU Loan Program | Massachusetts only | Offered through participating lenders; combines amortizing and deferred financing | Owner-occupant of a single-family primary residence, meets income guidelines, and already has plans, permits, and predevelopment materials in hand | Active through participating lenders | May 22, 2026 |

| Colorado ADU Finance Programs (HB24-1152) | Colorado, ADU-supportive jurisdictions | $8 million through CHFA — down-payment assistance, affordable loans, and interest-rate buydowns | Homeowners in ADU-supportive jurisdictions | Confirm current CHFA/OEDIT consumer-application availability | May 22, 2026 |

Sources: MassHousing ADU Loan Program; Colorado HB24-1152 / CHFA. Verified May 22, 2026. Call the program before you count on it.

How much more can future-value underwriting unlock?

Future-value underwriting matters when today’s equity is too small but the completed ADU will lift the appraised value. The result is never guaranteed — appraisal, lender caps, loan limits, DTI, credit, and the ADU’s legal feasibility all gate it. In the worked example above, the difference was $0 versus $195,000. In practice it’s usually the difference between “can’t build” and “can.”

The honest version of value-add: an appraiser controls the number, not a rule of thumb. Treat any “ADUs add 18–35%” figure you see online as a single regional builder’s estimate, not a national appraisal standard — useful as a hint, useless as an underwriting assumption. Your subject-to-completion appraisal is the only number your lender will lend against.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, appraisal outcomes, and regulatory approvals.

Will an after-renovation value loan make you refinance your current mortgage?

Sometimes — and this is the decision gate most pages skip. First-lien renovation mortgages (HomeStyle, CHOICERenovation, FHA 203(k)) and cash-out refinances usually replace or create your main mortgage. Second-lien ARV home-equity products usually preserve your existing first mortgage. If you hold a low rate, this question outranks every other consideration. Refinancing a $480,000 balance from a pandemic-era rate to a 2026 rate to fund a $175,000 ADU means re-pricing the whole balance, not just the new money — often far more costly than the ADU.

Use this no-rate comparison to narrow your options before you talk to anyone:

| Path | Current or future value? | Replaces first mortgage? | Lose existing first-lien structure? | Best first test for… |

|---|---|---|---|---|

| Standard HELOC / home-equity | Current | No | No | Owners with enough equity and a rate worth protecting |

| ARV HELOC / home-equity (RenoFi-style) | Future | Usually no | No | Equity-light owners protecting a low first mortgage |

| HomeStyle / CHOICERenovation | Future | Usually yes | Yes | Buyers/refinancers wrapping the ADU into one loan |

| FHA 203(k) | Future | Usually yes | Yes | FHA borrowers with attached/eligible scope |

| Construction-to-permanent | Future | Usually yes (new) | Yes | Large or detached ground-up builds |

| Cash-out refinance | Usually current | Yes | Yes | Borrowers already planning to refinance |

No rates, APRs, or payments are shown here by design — those depend entirely on your lender, credit, and the market on the day you lock. This table is about structure, which is what actually drives the right choice.

This is the natural moment to talk to a lender — but only once you know whether you’re testing a first-lien path (renovation mortgage, refi) or a second-lien path (ARV HELOC). Walking into a bank without that clarity is how people end up refinancing a great mortgage by accident.

The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our recommendations are based on independent research and are never influenced by compensation.

Use this once you know whether you’re testing a first-lien renovation/refi path or a second-lien equity path. Financing-path education, not a lender ranking — no approval, terms, rates, or loan amount are guaranteed.

Which ADU types can future-value loans finance?

ADU type changes which products will fund you. A garage conversion, basement unit, attached addition, detached backyard ADU, prefab/modular unit, and manufactured-home ADU are each treated differently by each program. A DADU is a detached accessory dwelling unit (a freestanding backyard structure). A JADU (junior ADU) is a smaller category: in California, a JADU is generally up to 500 square feet created within an existing or proposed single-family dwelling or attached garage — but outside California, don’t assume the term or the 500-square-foot rule applies to your jurisdiction. Conventional renovation mortgages (HomeStyle, CHOICERenovation) tend to be the most flexible across ADU types; FHA 203(k) has the most eligibility nuance.

| ADU type | Future-value paths that may fit | Main gotcha |

|---|---|---|

| Garage conversion | HomeStyle, CHOICERenovation, FHA 203(k), ARV HELOC | Must be legally permitted and meet habitability/egress/code |

| Basement / internal ADU | HomeStyle, CHOICERenovation, FHA 203(k), ARV HELOC | Separate entrance, kitchen/bath, egress, fire safety, local code |

| Attached ADU addition | HomeStyle, CHOICERenovation, FHA 203(k), construction loan | Most broadly eligible across programs |

| Detached site-built ADU | HomeStyle, CHOICERenovation, construction loan, some ARV products | Not the first choice for FHA 203(k) — confirm eligibility in writing |

| Prefab / modular ADU | HomeStyle, CHOICERenovation, construction loan, some ARV products | Must meet local code, permanent foundation, title, and lender rules |

| Manufactured-home ADU | Certain Fannie/Freddie paths | Real-property conversion, foundation, title, and zoning can block it |

| Existing unpermitted ADU (legalization) | Case-by-case | Lender may require legal status, permits, or a correction plan |

On prefab specifically: don’t assume every factory-built unit qualifies. Lenders care whether the unit is legally permitted, permanently installed, appraised correctly, and — when applicable — converted to and titled as real property. Fannie Mae will finance manufactured-home ADUs under HomeStyle Renovation provided all standard manufactured-home requirements (including conversion to real property) are met. (Source: Fannie Mae ADU page, verified May 22, 2026.)

Plans checklist, permit-document list, and a financing-path worksheet.

Can projected ADU rent help you qualify?

Sometimes — but don’t assume it, and never let projected rent be the thing that makes an unaffordable project look affordable. Some programs allow ADU rental income under specific rules, especially for legal existing ADUs. Projected rent from a planned ADU is far more rule-dependent and varies by loan program, appraisal/rent analysis, your borrower profile, and whether the unit is legally rentable. Below is the original side-by-side assembled from the agencies’ own current rules.

| Program | Projected new-ADU rent | Existing-ADU rent | Income cap | Other requirements |

|---|---|---|---|---|

| FHA Standard 203(k) | 50% of the lesser of appraiser fair-market rent (Form 1007) or the lease — when there’s no rental history | Higher allowances apply for some borrowers with an existing ADU (up to 75% of the lesser of appraiser-supported rent or lease) | ADU rental income capped at 30% of total monthly effective income | FHA generally requires two months of PITI reserves when ADU rent is used; ADU rent is ineligible on cash-out refinances |

| Freddie Mac | Lease-documented ADU rental income capped at 75% of the lease amount | Same 75% lease cap framework | Qualifying ADU rental income capped at 30% of total qualifying income | Appraisal required; rental analysis must include at least three comparable rentals, and at least one must include a rented ADU |

| Freddie Mac CHOICERenovation | Not usable if the unit is included in the renovation project funded by the mortgage (applications on/after May 4, 2026) | Rent from units not in the funded project may still count | As above | This is the rule most likely to surprise you — see below |

Sources: HUD ML 2023-17; Freddie Mac February 2026 ADU fact sheet and Bulletin 2026-1. Verified May 22, 2026.

Can CHOICERenovation rent from the new ADU help me qualify?

No — not if the unit is included in the renovation project funded by the CHOICERenovation mortgage proceeds, for applications received on or after May 4, 2026. If you’re building the ADU with the loan, you generally can’t use that new ADU’s projected rent to qualify; only rent from units not part of the funded project counts. Plan your debt-to-income around that, or choose a path (like an FHA 203(k) for attached scope, where the 50% rule can apply) that treats projected rent differently. (Source: Freddie Mac Bulletin 2026-1, verified May 22, 2026.)

These are illustrative examples, not guarantees of returns. Actual rental results depend on local market conditions, lease restrictions, tenant demand, operating costs, vacancy, taxes, insurance, and regulatory approvals.

What can stop an after-renovation value ADU loan from working?

The most common blockers are legal feasibility, appraisal value, borrower qualification, documentation, contractor/draw requirements, first-mortgage replacement risk, and product availability in your state. Every red flag below is tied to a verified rule or a documented program limitation, not guesswork.

| Red flag | Why it matters | Source basis | What to do instead |

|---|---|---|---|

| ADU isn’t legal on your lot | A loan can’t fix a zoning or buildability problem | Local zoning / ministerial-review rules | Run feasibility first |

| Appraisal won’t support the finished value | Your future-value borrowing room shrinks or vanishes | Agency as-completed appraisal + comparable-rental requirements (Freddie: 3 comps, 1 with a rented ADU) | Reduce scope, add cash/equity, or seek another valuation path |

| Your current mortgage is too valuable to replace | A first-lien refi/reno mortgage can cost more than the ADU | Lien-position structure (see refinance table) | Test second-lien ARV paths first |

| FHA borrower wants a new detached ADU | 203(k) is read as not creating a new detached unit | HUD ML 2023-17 (attached-ADU language) | Use HomeStyle, CHOICERenovation, or a construction loan |

| Counting on new-ADU rent with CHOICERenovation | Funded-unit rent can’t be used to qualify | Freddie Bulletin 2026-1 (eff. May 4, 2026) | Re-run DTI without that rent, or choose another path |

| Lender isn’t on Fannie UAD 3.6 yet | Expanded multi-unit/multiple-ADU rules may not apply | Fannie SEL-2025-10 (eff. Mar 31, 2026; UAD 3.6 required) | Ask the lender directly; UAD 3.6 is mandatory for new appraisals from Nov 2, 2026 |

| Prefab unit isn’t treated as real property | Some lenders won’t finance it as planned | Fannie manufactured-home requirements | Verify title, foundation, code, and appraisal treatment up front |

| DTI / credit / reserves fall short | Project value alone doesn’t qualify you | FHA two-month PITI reserve rule when ADU rent is used | Reduce budget, document more income, or wait |

| Product unavailable in your state | ARV/home-equity availability varies | RenoFi state-variation + NY solicitation note | Use a national mortgage path or a local lender search |

Find the zoning, scope, and financing red flags before you spend on plans.

What documents do lenders need before funding an ADU?

Every future-value ADU loan requires the standard income, credit, and asset documents — but on top of that, each program has its own project documentation. Getting these wrong is the most common reason a ready borrower stalls mid-approval.

| Program | Key document requirements |

|---|---|

| HomeStyle Renovation | Renovation contract; plans/specs; draw schedule; contractor license + insurance; permits; completion certificate |

| FHA Standard 203(k) | HUD consultant engagement; consultant work write-up; permits; inspections; rehabilitation escrow account; draw schedule; contractor documentation |

| Freddie Mac CHOICERenovation | Renovation contract; appraisal; cost estimates; completion/delivery requirements; draw documentation |

| RenoFi-style ARV | Contractor bid; plans/scope; after-renovation-value appraisal; lender/state availability confirmation; standard income/credit docs |

Two terms worth defining here: a setback is the minimum distance your ADU must sit from property lines (set by local zoning), and ministerial approval means that, in ADU laws that use it, a compliant application is reviewed and approved without discretionary public hearings. Both affect feasibility — which affects whether your loan ever funds.

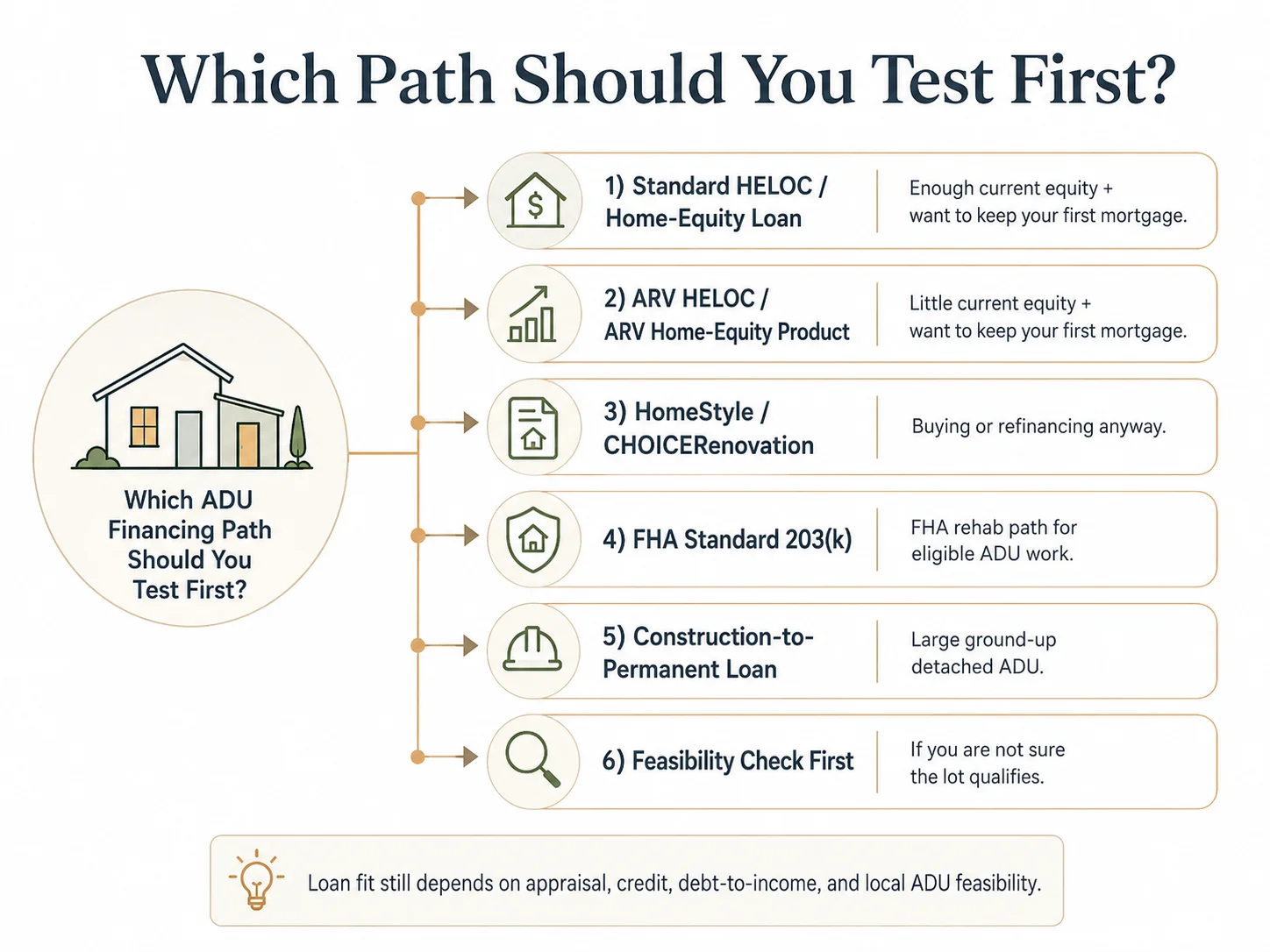

Which path should you test first? (the decision matrix)

Start with the path that solves your biggest constraint without creating a bigger one. If you have enough current equity and a low first mortgage, test a HELOC or home-equity loan. If equity is short but you want to keep that first mortgage, test a second-lien ARV product. If you’re buying or refinancing anyway, test HomeStyle, CHOICERenovation, FHA 203(k), or construction-to-permanent. Pick the path, then prove feasibility, then apply — in that order.

| Your situation | Test first | Avoid first |

|---|---|---|

| Enough current equity + low first mortgage | HELOC or home-equity loan | Cash-out refi that replaces a low first mortgage |

| Little equity + want to keep first mortgage | ARV HELOC / home-equity product | First-lien refi unless the numbers justify it |

| Buying a home and adding an ADU | HomeStyle, CHOICERenovation, FHA 203(k), construction-to-perm | A standard HELOC with no equity history |

| Refinancing anyway | HomeStyle, CHOICERenovation, FHA 203(k), cash-out refi | Second-lien-only thinking |

| FHA borrower, attached/eligible ADU work | FHA 203(k) Standard or Limited | Assuming detached-new-ADU eligibility |

| New detached ADU | HomeStyle, CHOICERenovation, construction loan, local ADU loan | Banking on FHA 203(k) for a detached new build |

| Unsure the lot qualifies | Feasibility first | Loan shopping before the zoning check |

| Rental-income-driven project | Feasibility + a rent/operating-cost model | Assuming rent will automatically qualify you |

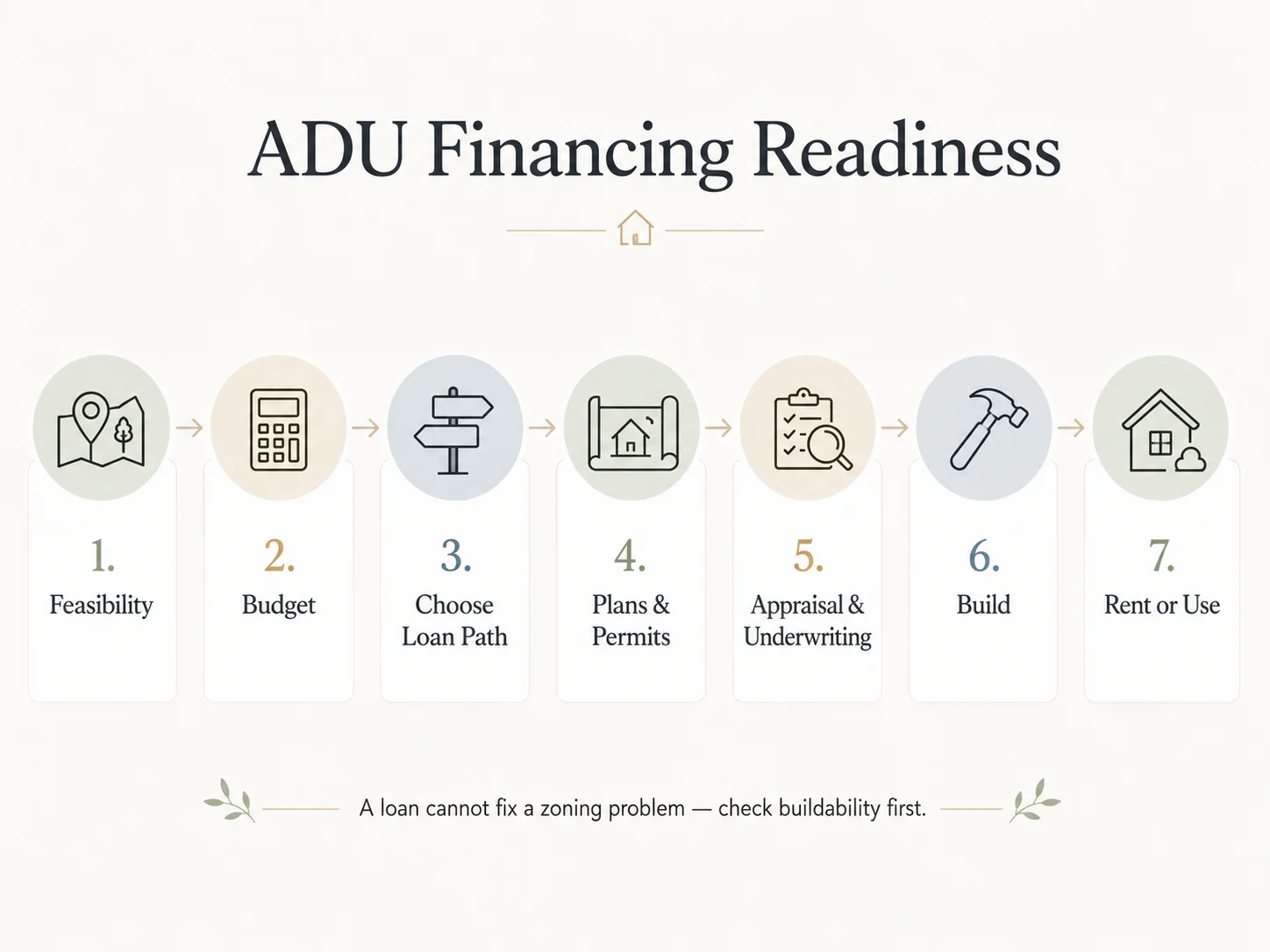

You’ve now got more than most homeowners ever assemble before their first lender call: the value basis, the lien-position consequences, the ADU-type fit, the rent rules, and the red flags. The next move is the cheapest, lowest-risk step you can take — confirm the ADU is actually buildable on your lot before you spend a dollar on plans or applications.

The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our recommendations are based on independent research and are never influenced by compensation.

Final next steps

Start here. Feasibility before financing, every time.

See your options once you know your path. Financing-path education, not a lender ranking.

The document checklist, lender-question script, and project-risk worksheet.

What we verified for this guide

Methodology

We built this as an editorial decision page, not a lender ranking. We reviewed primary agency sources (Fannie Mae’s Selling Guide and announcements, Freddie Mac’s bulletins and ADU guidance, HUD’s Mortgagee Letters, FHFA’s loan limits), product disclosures from RenoFi-style ARV lenders, state housing-finance program pages, and homeowner forums. We used forums only to understand how homeowners describe the problem and what stops them — never as a source for legal, zoning, cost, or loan-rule claims.

We separated three kinds of statements throughout: verified commercial facts (program availability, limits, pricing tiers — dated and sourced), regulatory facts (agency rules and code — cited to primary sources), and editorial judgments (which path may fit which borrower — framed as our conclusions from the verified facts). The comparison tables are sorted by neutral, documented criteria — lien position, value basis, ADU-type fit — never by any commercial arrangement. We don’t quote rates, APRs, or payments, and we don’t rank lenders as “best.” Where current consumer-application status can change (state programs especially), we tell you to confirm before you rely on it. See our best ADU financing options guide for the full landscape, or ADU cost by type and state for budget context.

Frequently asked questions

- What does after-renovation value mean for an ADU loan?

- It’s what your home is expected to be worth after the ADU is finished — also called as-completed value, after-improved value, or ARV. Certain loan products lend against that future number instead of your current equity. It does not guarantee approval or any specific loan amount.

- Is an after-renovation value loan the same as a HELOC?

- No. A standard HELOC is based on your current equity. Some ARV home-equity products use future value, but they’re a different, specialized product — not a normal HELOC.

- Can I get an ADU loan with no equity?

- Possibly. Future-value loans can help when the completed ADU supports the appraisal and you qualify on credit, income, and DTI — but no equity is genuinely hard, and lender limits and project legality still apply.

- Can I use an FHA 203(k) to build a detached ADU?

- Not as your first path. HUD Mortgagee Letter 2023-17 lists adding an attached ADU and renovating an existing ADU as eligible, and the 203(k) is widely read as not being usable to create a brand-new detached unit. For a detached build, look at HomeStyle, CHOICERenovation, or a construction loan, and get any 203(k) detached eligibility confirmed in writing.

- Does Fannie Mae HomeStyle allow ADUs?

- Yes. HomeStyle Renovation can be used by borrowers purchasing or refinancing a one-unit property to construct or install a new ADU. Expanded 2026 rules for multi-unit and multiple-ADU scenarios are available to lenders using Fannie’s UAD 3.6 policy.

- Does Freddie Mac CHOICERenovation allow ADUs?

- Yes — CHOICERenovation can add a new ADU or renovate an existing one. Note the 2026 rule: for applications on or after May 4, 2026, rental income from a unit included in the funded renovation project can’t be used to qualify you.

- Will I have to refinance my current mortgage?

- It depends on the product. First-lien renovation mortgages and cash-out refinances usually replace or create your main mortgage; second-lien ARV HELOC/home-equity products usually preserve your existing first mortgage.

- Can projected ADU rent help me qualify?

- Sometimes. FHA’s Standard 203(k) can allow 50% of projected rent from a new attached ADU (no history), capped at 30% of effective income with reserve requirements; Freddie caps lease-documented ADU rent at 75% and excludes funded-project units under CHOICERenovation. Always confirm with your lender.

- What happens if the appraisal comes in too low?

- Your borrowing room may shrink or the loan may not close. You may need to reduce the ADU scope, bring more cash, choose a different loan type, or wait until you’ve built more equity.

- Can I use future-value financing for prefab or modular ADUs?

- Possibly, but lender treatment varies. The unit usually must meet local code and installation standards, sit on a permanent foundation, and — when applicable — be titled as real property.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.