Freddie Mac CHOICERenovation ADU Loan: 2026 Rules, Limits & Fit Matrix

By The Dwelling Index Editorial Team · · Last verified May 20, 2026 · ~45 min read

Independent ADU resource · Not a lender or broker · Editorial standards →

The bottom line on CHOICERenovation and ADUs

Yes, Freddie Mac CHOICERenovation can finance an accessory dwelling unit — including a brand-new detached ADU, a garage conversion, a JADU, or a renovation of an existing ADU, on 1-, 2-, or 3-unit properties. It is one of the most flexible conventional renovation products for ADU work.

The critical 2026 change: Under Freddie Mac Bulletin 2026-1 (effective May 4, 2026), rental income from any unit included in the renovation project funded by CHOICERenovation proceeds cannot be used to qualify the borrower. If you need the new ADU’s future rent to pass debt-to-income, this product does not work for you right now.

The five numbers that matter most:

| Factor | Rule (2026) |

|---|---|

| What it finances | New or renovated ADU on 1-, 2-, or 3-unit properties |

| Max LTV (1-unit primary) | 95% standard; 97% with Home Possible or HomeOne only |

| Rental income from funded ADU | Cannot qualify — Bulletin 2026-1 (May 4, 2026) |

| Max renovation cost | 75% of as-completed appraised value (purchase or refi) |

| Completion deadline | 450 days from note date |

Before you call a lender, confirm what your lot is allowed to build. Free, 60 seconds.

What is Freddie Mac CHOICERenovation in plain English?

Answer capsule: CHOICERenovation is a Freddie Mac conventional mortgage that wraps the purchase or refinance of a property and the renovation budget into a single loan, sized against the home’s after-improvement value rather than its current value. You close on the loan, the renovation funds sit in a completion escrow account, and you have 450 days to complete the work. The lender releases draws as construction milestones are hit and verified.

For ADU purposes, this matters in two ways. First, it lets you borrow against what the property will be worth after the ADU is built — not what it’s worth today — which is how the math pencils on a large renovation. Second, it means you only need one loan, one closing, and one set of paperwork, rather than a construction loan that you later refinance into permanent financing.

CHOICERenovation is a purchase or no-cash-out refinance product. You cannot use it as a cash-out refinance to extract existing equity. If you already own the home and have equity, you’re likely looking at a CHOICERenovation no-cash-out refinance — one that pays off your existing first mortgage, folds in the renovation budget, and sizes the new loan against the as-completed value.

Key structural features, per the Freddie Mac CHOICERenovation product page and Guide Chapter 4607:

- Loan Product Advisor (LPA) “Accept” risk classification required — no manual underwriting

- Max LTV 95% on a 1-unit primary residence; 97% only with Home Possible or HomeOne program rules

- Renovation costs capped at 75% of the as-completed appraised value (or the relevant purchase-price test for purchases)

- 10–20% contingency reserve required; minimum is 15% if utilities are not operable

- Completion deadline: 450 days from note date

- Funds disbursed via draw-release schedule from a completion escrow account

- Eligible for luxury renovations (pools, outdoor kitchens, landscaping) unlike FHA 203(k)

- Up to 50% of material costs may be advanced at closing to secure suppliers

- Up to 6 months of principal, interest, taxes, insurance, and association dues (PITIA) may be financed into the loan if the property will be uninhabitable during renovation

Sources: Freddie Mac ADU Fact Sheet (February 2026); CHOICERenovation Fact Sheet; Guide Chapter 4607.

What does Freddie Mac count as an ADU for CHOICERenovation?

Answer capsule: Freddie Mac defines an ADU as a habitable living unit with its own entrance, kitchen, and bathroom — a complete, self-contained dwelling. It must be permitted or legal non-conforming under local zoning (or in a no-zoning area). One ADU is allowed per property under CHOICERenovation for 1-, 2-, and 3-unit subject properties. An ADU added to a 4-unit property is not eligible. (Guide Section 5601.2; ADU Fact Sheet, February 2026.)

Project types Freddie recognizes

| ADU project type | Freddie eligible? | Notes |

|---|---|---|

| Detached new-build ADU | Yes | Must comply with local zoning; requires permit |

| Attached addition (new ADU) | Yes | Added to existing structure |

| Garage or basement conversion | Yes | Must produce full kitchen, bath, separate entrance |

| JADU (Junior ADU) | Yes | Interior to existing structure; must meet Freddie’s habitable-unit definition |

| Renovation of existing legal ADU | Yes | ADU must be legal, legal non-conforming, or in a no-zoning area |

| Renovation of existing legal non-conforming ADU | Yes | Must have been legally built; keep original permit and CO records |

| ADU on a 4-unit property | No | CHOICERenovation ADU eligibility is limited to 1-, 2-, and 3-unit properties |

| Ground-up teardown + new construction | No | CHOICERenovation may not be used to raze a structure and rebuild; use construction-to-permanent instead |

The zoning exception for illegal ADUs on 1-unit properties

For 1-unit subject properties only, Guide Section 5601.2 allows an ADU that does not comply with current zoning to make the property eligible under specific conditions — including appraiser confirmation that the property is acceptable as a one-unit residence without the ADU. Rental income from an illegal ADU may not be used to qualify the borrower under any circumstances.

The 2026 rental-income rule: what Bulletin 2026-1 actually says

Answer capsule: Effective May 4, 2026, Freddie Mac Bulletin 2026-1 prohibits lenders from using rental income from any unit included in the renovation project funded by CHOICERenovation proceeds to qualify the borrower. This means if you’re building an ADU with CHOICERenovation proceeds, you cannot use that ADU’s projected future rent in your debt-to-income calculation. (Freddie Mac Bulletin 2026-1.)

Three examples

Example 1 — Blocked: New detached ADU funded by CHOICERenovation

You’re purchasing a house and financing a new detached ADU using CHOICERenovation proceeds. You want to count $2,100/month projected ADU rent toward qualifying income. Under Bulletin 2026-1, this is not permitted. The ADU is “included in the renovation project funded by the mortgage proceeds.”

Example 2 — Borderline: Existing multi-unit with one unit renovated

You own a 3-unit property. You use CHOICERenovation to renovate Unit 3 into an ADU. Unit 1 and Unit 2 are not being renovated. The rental income from Units 1 and 2 may be used to qualify (subject to standard documentation rules). The income from Unit 3 — the renovated unit — may not.

Example 3 — Permitted: Existing ADU not in the funded project

You own a property with an existing, permitted ADU. You use CHOICERenovation proceeds only to renovate the main house (new roof, kitchen, HVAC). The existing ADU is not part of the funded renovation project. Its documented rental income may be used to qualify, up to 75% of the lease amount and capped at 30% of total qualifying income on a 1-unit primary residence.

Why Freddie added this rule

Freddie Mac has not published a detailed policy rationale for Bulletin 2026-1, but the practical effect is clear: it prevents borrowers from qualifying for a CHOICERenovation loan based on rental income that does not yet exist and that comes from a unit being funded by the same loan. This is a layered-risk concern — the borrower’s qualification depends on a future income stream from an asset being created by the very loan under review. The rule is an underwriting safety valve.

What income IS still permitted

| Income source | Permitted? | Cap / condition |

|---|---|---|

| New ADU funded by CHOICERenovation proceeds | No | Blocked entirely by Bulletin 2026-1 (effective May 4, 2026) |

| Existing ADU not part of funded project (1-unit primary) | Yes | 75% of documented lease amount; max 30% of total qualifying income |

| Non-renovated existing units (2–3 unit property) | Yes | Standard rental income documentation rules apply |

| Borrower’s own W-2 / self-employment income | Yes | Standard income documentation |

| Rental income from illegal ADU | No | Always prohibited under Guide Section 5601.2 |

Landlord education requirement

For purchase transactions where rental income from an ADU on a 1-unit primary residence is used to qualify, at least one qualifying borrower must complete landlord education — unless that borrower has at least one year of investment property management or ADU rental management experience.

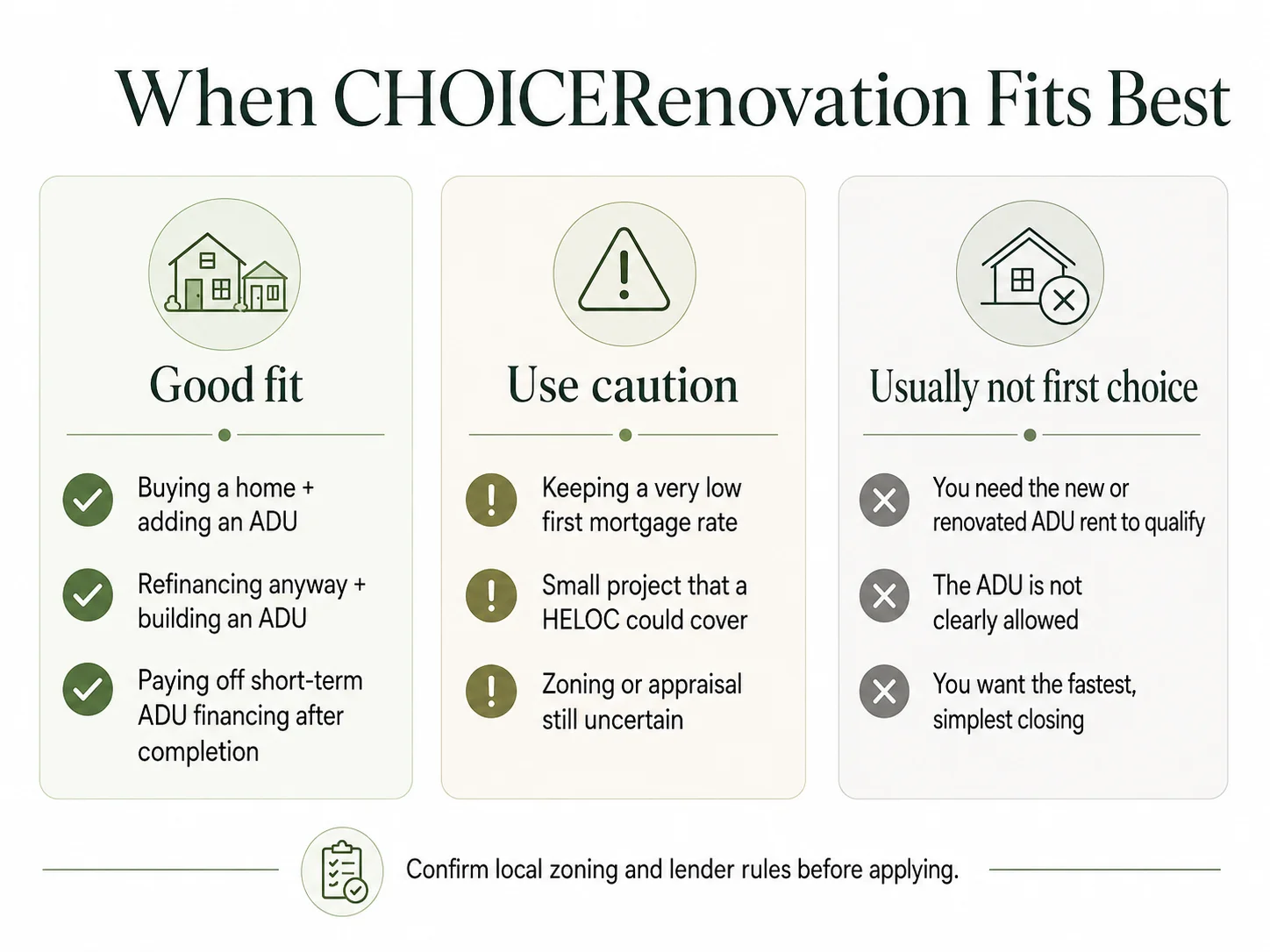

Fit matrix: when CHOICERenovation works and when it doesn’t

Answer capsule: CHOICERenovation works best for buyers and owners who don’t have a low existing first-mortgage rate to preserve, who have enough income to qualify without the new ADU’s rent, and who are making a substantial addition or conversion rather than a small finish-out. It works worst when you need the new ADU’s rent to qualify, when your existing first mortgage rate is significantly below today’s market, or when the ADU isn’t legally buildable on your lot.

When CHOICERenovation fits best — and when it doesn’t

| Scenario | Fit | Reason |

|---|---|---|

| Buying a home + adding an ADU in the same transaction | ✓ Green | Consolidates into one loan, one closing, as-completed appraisal |

| Refinancing with current rate ≥ today’s CHOICERenovation rate | ✓ Green | First-mortgage replacement not a loss; one-loan simplicity |

| Don’t have equity for a HELOC but ADU adds significant value | ✓ Green | Sizes against as-completed value, not current equity |

| Qualify without the new ADU’s rent (income self-sufficient) | ✓ Green | Bulletin 2026-1 restriction is irrelevant to your file |

| Investor or second-home property + ADU | ✓ Green | CHOICERenovation allows 1-unit investment and second home (FHA 203k does not) |

| Major renovation scope (kitchen, HVAC, addition + ADU) | ✓ Green | CHOICERenovation handles large-scope projects; eXPress would be too small |

| Need new ADU’s future rent to qualify | ✗ Red | Bulletin 2026-1 blocks this (May 4, 2026 effective) |

| Existing first-mortgage rate significantly below today’s market | ✗ Red | Replacing a 3% rate with a 7% rate to fund an ADU rarely pencils; consider HELOC |

| ADU not legally buildable on the lot | ✗ Red | Zoning blocks the project; no financing product can override local code |

| Credit score below 620 | ✗ Red | Most lenders treat 620 as the floor; FHA 203(k) goes to 580 |

| Down payment below 5% and not eligible for Home Possible/HomeOne | ✗ Red | Minimum is 5% standard; 3% only with affordable-overlay programs |

| Ground-up new construction (teardown + rebuild) | ✗ Red | CHOICERenovation may not be used to raze an existing structure; use construction-to-perm |

| Small renovation scope (under ~$30K) fitting eXPress | ~ Yellow | CHOICEReno eXPress may be faster and simpler; ask lender to compare |

| Lender offers HomeStyle but not CHOICERenovation | ~ Yellow | HomeStyle is the closest conventional alternative; rules are similar but not identical |

What dates matter for CHOICERenovation and ADUs?

Several rule-effective and deadline dates govern CHOICERenovation ADU loans. Here’s the timeline:

| Date | What changed / what it means | Source |

|---|---|---|

| Feb 2026 | Freddie Mac ADU Fact Sheet updated; confirms CHOICERenovation eligible for ADUs on 1-, 2-, 3-unit properties; codifies rental-income caps | ADU Fact Sheet |

| May 4, 2026 | Bulletin 2026-1 effective: rental income from funded ADU unit cannot qualify borrower | Bulletin 2026-1 |

| Nov 25, 2025 | 2026 conforming limits announced: $832,750 (standard) / $1,249,125 (high-cost) | FHFA |

| 2025-15 (Bulletin) | Manufactured-home ADU multiwide-primary requirement established; non-structural cap of $50K or 50% of as-completed value | Bulletin 2025-15 |

| 2025-16 (Bulletin) | CHOICEReno eXPress: 15% renovation-cost cap (up from 10%) in Duty to Serve high-needs areas | Bulletin 2025-16 |

| 450 days | Maximum completion window from note date (per-loan deadline, not a calendar date) | CHOICERenovation Fact Sheet |

The 75% renovation cap: how the math works with three worked examples

Answer capsule: The 75% cap limits total renovation costs to 75% of the as-completed appraised value (for refinances) or 75% of the lesser of (purchase price + renovation costs) or as-completed appraised value (for purchases). “Renovation costs” in this context include hard construction costs, soft costs (architect, engineering, permits), contingency reserve, and up to six months of PITIA during an uninhabitable renovation period. The CHOICERenovation Maximum Mortgage Worksheet calculates this precisely. (Guide Chapter 4607.)

Worked example 1 — Purchase: Detached ADU on a $600K house

Purchase price: $600,000

ADU construction cost (all-in with contingency): $180,000

As-completed appraised value: $820,000

Test 1 — lesser of (purchase + reno) vs. as-completed: $600K + $180K = $780,000 < $820,000 as-completed. Use $780,000.

Test 2 — 75% of $780,000: $585,000.

Can the $180,000 renovation be financed? $180,000 ≤ $585,000. Yes — passes the 75% cap.

Max loan amount (95% of $780,000): $741,000.

Worked example 2 — Refinance: Garage conversion ADU on a $550K home

Current home value: $550,000

Existing first mortgage balance: $320,000

Garage conversion cost: $95,000

As-completed appraised value: $680,000

75% of as-completed for refinance: 75% × $680,000 = $510,000.

Can the $95,000 renovation be financed? $95,000 ≤ $510,000. Yes — easily passes.

Max loan amount (95% of $680,000): $646,000. Existing first mortgage of $320,000 is rolled in. Additional borrowing capacity up to $226,000 (within max LTV).

Worked example 3 — Purchase: When the 75% cap actually binds

Purchase price: $400,000

Planned renovation cost (all-in): $380,000

As-completed appraised value: $650,000

Test 1 — lesser of (purchase + reno) vs. as-completed: $400K + $380K = $780,000 > $650,000 as-completed. Use $650,000.

Test 2 — 75% of $650,000: $487,500.

Can the $380,000 renovation be financed? $380,000 ≤ $487,500. Yes — passes, but barely. If the as-completed appraisal comes in at $500,000 instead of $650,000, the cap would be $375,000 and the project fails or must be scaled back.

Pattern across examples

The 75% rule almost never kills an ADU project on its own. What kills CHOICERenovation deals is usually (1) the as-completed appraisal coming in lower than projected, (2) the borrower’s DTI failing once the new mortgage payment is included, or (3) the May 2026 rental-income rule removing income the borrower was counting on.

These examples are illustrative, not loan quotes or approval guarantees. Actual loan amount, LTV, DTI, appraisal, mortgage insurance, and lender overlays determine eligibility.

The contingency reserve

Freddie Mac requires a contingency reserve deposited into the renovation escrow account. The minimum is 10% of total renovation costs. If the property’s utilities are not operable as referenced in the construction contract or plans, the minimum increases to 15%. The maximum is 20%. Contingency funds may come from loan proceeds or directly from the borrower. Any unused contingency, after the renovation is complete, is either applied to additional eligible renovations or used to reduce the principal balance.

For an ADU build, budget toward the higher end of contingency. Site work, utility connections, and septic surprises are the most common cost overruns on detached ADU builds. A 15–20% contingency on a $180K project is the difference between a clean close-out and a mid-build cash crunch.

Worried your project might not fit the 75% cap?

Run a free property eligibility check before spending on plans. We screen what your lot can support and surface the financing constraints to discuss with a lender.

Get Your Free Property Report →The 11 eligibility rules that determine whether your loan funds

Answer capsule: The most important: an LPA “Accept” is required (no manual underwriting); maximum LTV is 95% on a 1-unit primary (97% only with affordable-product overlay); minimum down payment is 5% (3% with affordable overlay); and lender credit-score overlays are typically 620. (Freddie Mac CHOICERenovation product page; Guide Chapter 4607.)

Rule 1: LPA “Accept” is required — no manual underwriting

Every CHOICERenovation mortgage must be submitted to Loan Product Advisor and receive an “Accept” risk classification. Manual underwriting is not permitted. If your file does not Accept, the deal is dead in CHOICERenovation.

Rule 2: Maximum LTV — 95% on a 1-unit primary; 97% only with affordable-product overlay

For a 1-unit primary residence, the maximum loan-to-value is 95%. The 97% LTV is available only with Home Possible (income-limit tied to AMI) or HomeOne (first-time homebuyers). For 2-unit owner-occupied purchases, typically 85%. For 3-4 unit, typically 80%. Investment properties: 75–80%.

Rule 3: Minimum down payment

5% on a 1-unit primary residence (3% with Home Possible or HomeOne for eligible borrowers). On 2- to 4-unit properties, typically 15% or more. Investor 1-unit purchases require 15% minimum.

Rule 4: Credit score — Freddie sets no hard floor, but 620 is the practical minimum

Freddie does not publish a hard minimum credit score; the requirement is LPA “Accept.” In practice, correspondent lender materials treat 620 as the floor. Some lenders impose higher overlays — 660 or 680 — particularly for investment properties.

Rule 5: Minimum loan amount

Some lender matrices impose minimum loan amounts (we’ve seen $50,000, and $75,000 for manufactured singlewide homes). These are lender overlays, not universal Freddie Mac rules. Confirm with your lender.

Rule 6: Maximum renovation cost — 75% of the relevant value test

Covered in detail above. For manufactured homes, an additional cap applies: non-structural improvements are limited to the lesser of $50,000 or 50% of the as-completed appraised value when the primary dwelling is a manufactured home.

Rule 7: Contingency reserve — 10% minimum (15% if utilities not operable), 20% maximum

Required on every CHOICERenovation loan. Sits in the completion escrow account and is released per the lender’s draw procedures.

Rule 8: Completion deadline — 450 days from note date

All renovations must be completed within 450 days of the note date. Plan for 12 months and build in buffer. Lenders with prior written Freddie approval may, in limited circumstances, request extensions — do not count on extension flexibility.

Rule 9: Contractor requirements — Form 1202 review; borrower-as-contractor only if licensed

The lender must review the contractor using the contractor profile report (Form 1202). Plans and specifications must be prepared by a registered, licensed, or certified professional. The borrower may not be employed by the contractor, and they cannot be in a related-party relationship.

Rule 10: Mortgage insurance required if LTV exceeds 80%

Standard conventional rule: if LTV is above 80%, you’ll carry PMI until you reach the cancellation threshold. PMI is generally cancellable, unlike FHA mortgage insurance premium.

Rule 11: Property type — 1- to 4-unit primary, 1-unit second home, 1-unit investment, manufactured

CHOICERenovation is eligible on 1- to 4-unit primary residences, 1-unit second homes, 1-unit investment properties, and certain manufactured homes. Multi-unit investment is not eligible. For ADU-specific rules, one ADU is permitted on 1-, 2-, or 3-unit properties.

What this means in practice

If your credit score is under 620, your DTI without the new ADU’s rent fails LPA Accept, or your down payment is under 5% and you don’t qualify for Home Possible or HomeOne, CHOICERenovation is probably not your first path. FHA 203(k) has a lower 580 credit floor and 3.5% down.

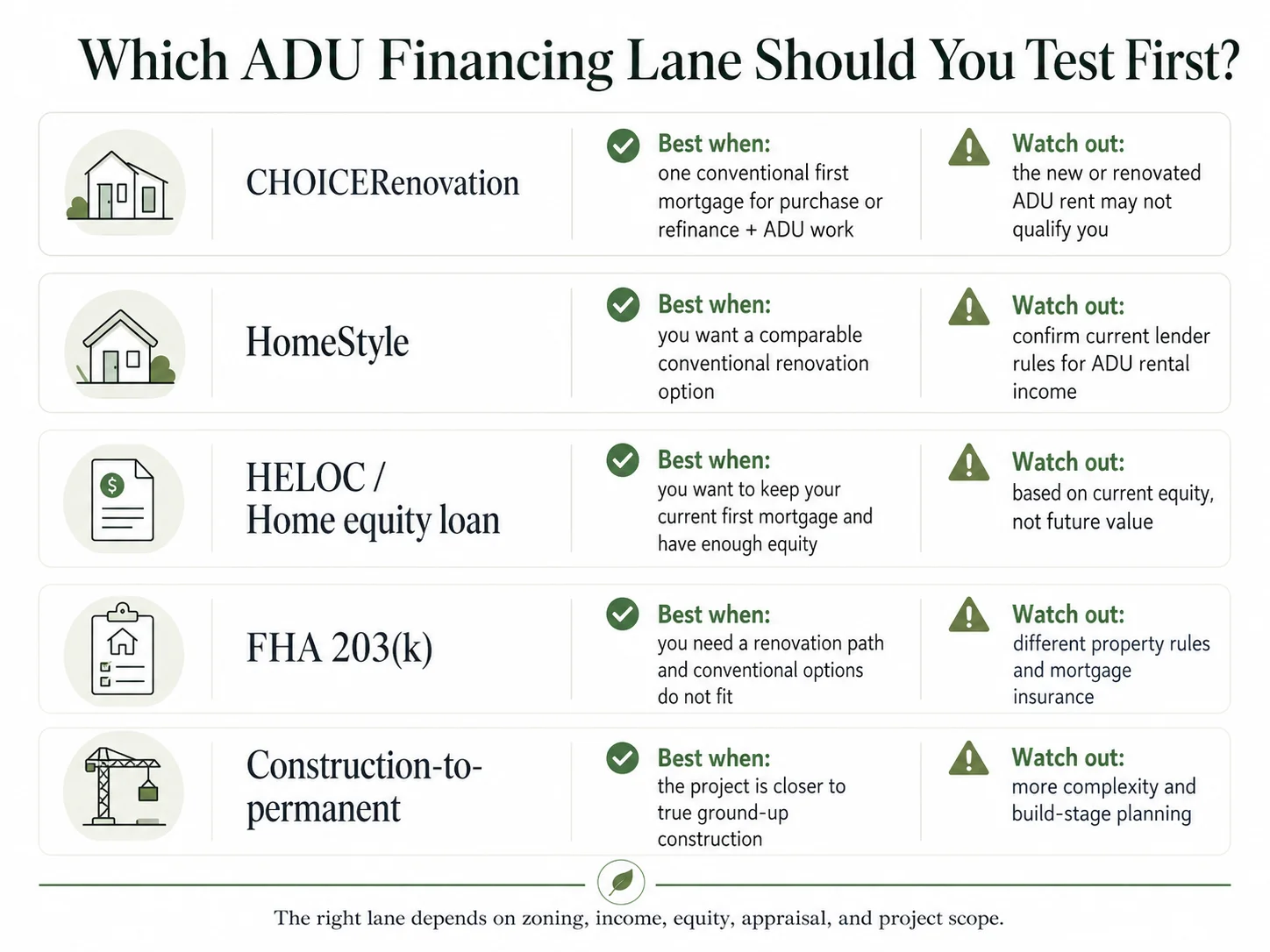

CHOICERenovation vs HomeStyle vs FHA 203(k): the full comparison

Answer capsule: For an ADU build, all three programs let you size the mortgage against the home’s after-improvement value, but they differ in critical ways. CHOICERenovation and HomeStyle are conventional cousins — 95% LTV, 75% renovation cap, 620 credit floor. FHA 203(k) has a lower credit floor (580) and lower down payment (3.5%), but Standard 203(k) requires new ADUs to be attached to the existing structure per Mortgagee Letter 2023-17, and FHA mortgage insurance is more expensive and longer-lasting. CHOICERenovation, alone among the three, carries the May 2026 rental-income restriction on the funded unit. (Sources: HUD Mortgagee Letter 2023-17; HUD Mortgagee Letter 2024-13; Fannie HomeStyle Renovation Selling Guide B5-3.2-01.)

Which ADU financing lane should you test first?

| Dimension | Freddie CHOICERenovation | Fannie HomeStyle | FHA 203(k) Standard |

|---|---|---|---|

| New detached ADU eligible? | Yes | Yes | No — ML 2023-17 limits new ADUs to attached construction only |

| Existing ADU renovation (attached or detached) | Yes | Yes | Yes — attached or detached existing ADU may be renovated |

| Max renovation cost | 75% of relevant value test | 75% of relevant value test | Up to FHA county loan limit; Standard for projects above Limited threshold |

| Max LTV (1-unit primary) | 95% (97% with Home Possible / HomeOne only) | 95% (97% with HomeReady or affordable overlay) | 96.5% |

| Min credit score (typical) | 620 | 620 | 580 (FHA floor) |

| Min down payment | 5% (3% with overlay product) | 5% (3% with overlay product) | 3.5% |

| Mortgage insurance | Required >80% LTV; cancellable PMI | Required >80% LTV; cancellable PMI | Upfront 1.75% MIP + monthly MIP; generally for loan life on current loans |

| Investor / second-home eligible | Yes (with LTV caps) | Yes (with LTV caps) | No — primary residence only |

| Future ADU rent to qualify | No — Bulletin 2026-1 (May 4, 2026 effective) | Lender-dependent; confirm current Fannie treatment | Up to 50% of projected ADU rent on new ADUs per ML 2023-17; capped at 30% of total effective income |

| Existing ADU rental income (not in project) | Up to 75% of lease; max 30% of total qualifying income on 1-unit primary | Per Fannie Selling Guide rules | Per FHA ADU appraisal protocols; 75% of fair market rent with rental history; 30% cap |

| Completion deadline | 450 days from note date | 15 months from closing | 12 months Standard; 9 months Limited per ML 2024-13 |

| Underwriting | LPA Accept required; no manual UW | DU Approve required | Manual UW common; HUD consultant required on Standard 203(k) |

| Luxury items (pools, outdoor kitchens) | Permitted | Permitted | Restricted |

| 2026 max loan amount | $832,750 / $1,249,125 high-cost | $832,750 / $1,249,125 high-cost | County-specific FHA limit (lower in most areas) |

Sources: Freddie Mac CHOICERenovation Fact Sheet; ADU Fact Sheet (February 2026); Bulletin 2026-1; Fannie Mae HomeStyle Renovation (B5-3.2-01); HUD Mortgagee Letters 2023-17 and 2024-13. Verified May 20, 2026.

Which one to pick, by borrower profile

Profile 1 — 5%+ down, 680+ credit, building a detached ADU

Pick CHOICERenovation or HomeStyle based on which your lender actually offers and is fluent in. If you need the new ADU’s rent to qualify, the May 2026 rule blocks CHOICERenovation. Confirm directly with your lender how HomeStyle treats projected rent from a newly built ADU.

Profile 2 — Credit 580–640, or only 3.5% down

FHA 203(k) is probably your path — but watch the attachment rule. Under ML 2023-17, new ADUs financed by Standard 203(k) must be attached to the existing structure. Renovating an existing ADU is fine attached or detached. If you must build detached and your credit is sub-620, you’re in a narrow corner of the market.

Profile 3 — Investor or second-home property

CHOICERenovation or HomeStyle. FHA 203(k) is out — primary residence only.

When to skip all three and look elsewhere

If you have a low first-mortgage rate (under ~5.5%) that you don’t want to lose, none of the three renovation mortgages is your best path. Replacing your first mortgage to finance an ADU at the cost of giving up a sub-5% rate frequently doesn’t pencil. Run the comparison math: calculate the additional interest over the life of the loan from the higher rate, and compare it to the cost of a separate-financing path (HELOC, home equity loan). In most cases, preserving the low first mortgage wins.

Compare all ADU financing paths →CHOICEReno eXPress: the sibling product and when to consider it

Answer capsule: CHOICEReno eXPress is Freddie Mac’s streamlined renovation product, intended for smaller-scale renovations with a 180-day completion period and lower renovation-cost caps — generally 10% of as-completed value, or 15% in designated Duty to Serve high-needs areas per Bulletin 2025-16. eXPress is rarely the right product for a full new-build ADU, but it can fit for limited-scope ADU finish-outs, accessibility improvements to an existing ADU, or small garage or basement conversions within the 180-day window and cost cap. (Freddie Mac CHOICEReno eXPress materials.)

| Feature | CHOICERenovation | CHOICEReno eXPress |

|---|---|---|

| Best for | Major renovations, full ADU builds | Small-scale renovations, minor ADU improvements |

| Completion deadline | 450 days from note date | 180 days from note date |

| Renovation-cost cap | Up to 75% of relevant value test | 10% of as-completed value; 15% in Duty to Serve areas (Bulletin 2025-16) |

| Prior lender approval | Required for pre-completion delivery | Not required for standard delivery |

| Recourse | May be sold pre-completion with recourse + Freddie approval | Sold without recourse if rules met |

| ADU fit | Strong for new builds and significant ADU renovations | Possible for limited-scope ADU finish work; usually too small for a new ADU |

Source: Freddie Mac CHOICEReno eXPress comparison materials and Bulletin 2025-16. Verified May 20, 2026.

The honest take: If your ADU project is large enough to materially change the home’s footprint or value, you’re in CHOICERenovation territory. If your project is more of an ADU touch-up — finishing an unpermitted ADU into a permitted one with minor work, an accessibility retrofit, or refreshing an existing rentable ADU — eXPress may save you documentation and time. Anything in between, ask your lender to model both.

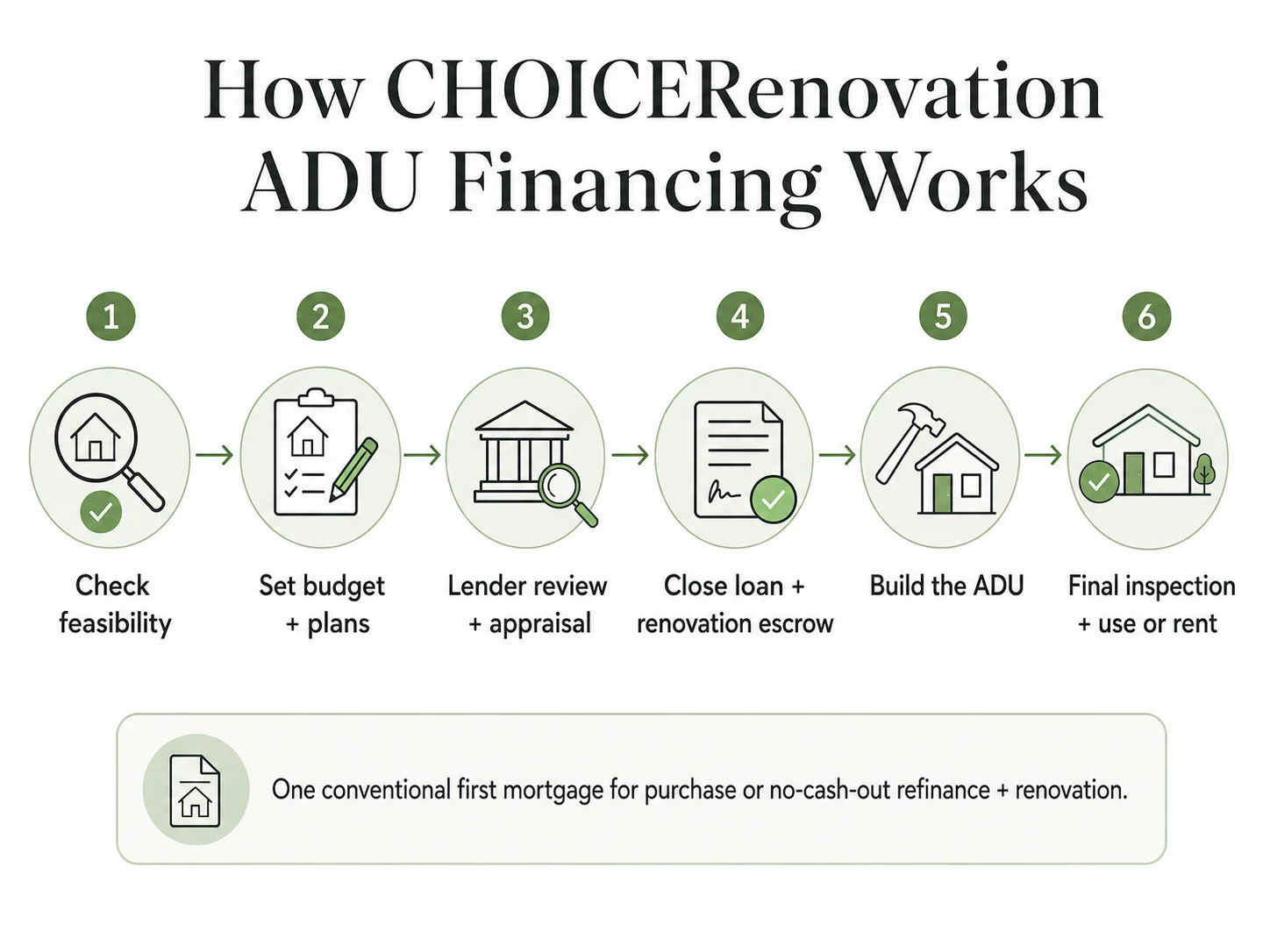

How to get a CHOICERenovation loan: the 7-step process

Answer capsule: From application to funding, expect 60–90 days for a CHOICERenovation loan, with construction starting after closing and completing within 450 days. The biggest gating step is finding a Freddie Mac-approved Seller/Servicer that delivers CHOICERenovation — many lenders only deliver Fannie HomeStyle.

How CHOICERenovation ADU financing works, step by step

- 1

Find a lender that delivers CHOICERenovation

Ask directly: “Do you currently originate Freddie Mac CHOICERenovation mortgages, and have you closed one with an ADU component in the last six months?” If the answer is no to either, find a different lender or accept HomeStyle as the alternative.

- 2

Confirm zoning before spending on plans

This is the single most important step, and it’s not the lender’s job. Confirm with your local planning department that an ADU is permitted on your lot, the size and setback rules, the parking and owner-occupancy requirements, and any HOA or coastal-zone restrictions.

- 3

Get a soft pre-qualification

Income, credit, debt, and rough as-completed value goal. The lender can run a preliminary LPA submission and tell you whether the structure is likely to work before you spend on plans.

- 4

Hire a licensed GC and get sealed plans and specifications

Plans must be prepared by a registered, licensed, or certified general contractor, a renovation consultant, or an architect. The lender will use Form 1202 to evaluate your contractor. The borrower and contractor cannot be in a related-party or employer-employee relationship.

- 5

Submit the full loan application

Contractor profile (Form 1202), full plans and specifications, contractor bid with itemized draw schedule, permit pathway, income and asset documentation, and existing first-mortgage statements if refinancing.

- 6

Lender orders the subject-to-completion appraisal

The appraiser values the property as if the ADU is already built, using the plans and specifications. This is the most consequential step — if the as-completed appraisal comes in below projections, the loan amount may need to be reduced or the deal restructured.

- 7

Close, then renovate within 450 days

Renovation funds and contingency reserve sit in a completion escrow account. Draw release procedures are governed by the lender’s CHOICERenovation draw process. Lenders may advance up to 50% of material costs at any time after closing to secure suppliers. All work must be completed within 450 days of the note date, evidenced by Form 442 and any required local certificates of occupancy.

Document map: what satisfies which rule

| Document | Why it matters | Rule it satisfies |

|---|---|---|

| Zoning confirmation letter or municipal code excerpt | Establishes the ADU as legal, legal non-conforming, or in a no-zoning area | Guide §5601.2 ADU eligibility |

| Form 1202 contractor profile | Lender reviews contractor qualifications | CHOICERenovation contractor requirements |

| Sealed plans and specifications | Lender, appraiser, and underwriter use to evaluate scope and value | Plans and specs prepared by registered/licensed/certified professional |

| Itemized contractor bid + draw schedule | Establishes total renovation cost and contingency line | 75% cap calculation; escrow funding |

| Subject-to-completion appraisal | Establishes as-completed value; drives loan size | Guide §4607.9 appraisal requirements |

| Completion documentation (Form 442) | Evidence renovation is complete | Renovation must be complete within 450 days |

| Local permit + certificate of occupancy | Required for ADU legality and rental-income eligibility post-completion | Section 5601.2 zoning compliance |

| Two years of W-2s / tax returns | Income verification | LPA Accept on income |

| Existing lease agreements on non-renovated units | If using rental income from a unit not in the funded project | Rental-income documentation rules |

| Landlord education certificate | Required for purchase transactions using ADU rental income on 1-unit primary | ADU Fact Sheet landlord education rule |

Lenders documented to deliver CHOICERenovation

We compiled this list from each lender’s currently published product or guideline materials, listed alphabetically. Inclusion is editorial, not paid, and not exhaustive. Some sources below are wholesale or correspondent channels. Confirm availability and channel directly with each lender before applying.

| Lender | Channel | Source verified |

|---|---|---|

| CrossCountry Mortgage | Direct retail | Renovation product page, verified Jan 2026 |

| eLEND TPO (formerly AFR Wholesale) | Wholesale / TPO | Program guidelines, dated October 22, 2025 |

| Gustan Cho Associates | Broker | Published CHOICERenovation guidelines, verified May 2025 |

| JVM Lending | Direct retail | ADU financing materials, verified March 2026 |

| Plaza Home Mortgage | Correspondent | Guideline document dated July 18, 2025 flagged program as temporarily suspended; verify current status directly |

| The Money Source (TMS) | Correspondent | CHOICERenovation correspondent matrix, dated September 24, 2025 |

Many additional credit unions, regional banks, and correspondent lenders also deliver CHOICERenovation. This list reflects sources we could verify against current published materials.

Explore mortgage paths for your ADU project

The Mortgage Research Center connects you with licensed lenders across conventional mortgage, refinance, and construction-loan paths so you can compare offers in one place. Free initial inquiry.

Explore Mortgage Path Options →Affiliate link. The Dwelling Index may earn a commission. MRC is a broad mortgage-path service — it does not guarantee any lender on its network currently originates CHOICERenovation. Ask each lender whether the next step uses a soft pull or hard credit pull, and confirm product availability before applying.

What documents do you need before applying?

CHOICERenovation is one of the most document-heavy conventional loans available. Assemble three stacks before applying:

Property and zoning documents

- Parcel address and APN

- Zoning district and applicable ADU ordinance citation

- ADU types allowed (detached, attached, JADU, garage conversion)

- Maximum size, setbacks, height, and lot-coverage rules

- Parking requirements (or applicable exemption)

- Owner-occupancy requirements

- Short-term rental restrictions

- HOA, PUD, or CC&R restrictions

- Fire-flow, septic capacity, water meter, or utility-service constraints

- Coastal-zone or overlay-zone requirements, if applicable

- Historic-district review, if applicable

- For Texas borrowers: confirm the transaction is not a Texas Home Equity transaction (excluded from CHOICERenovation)

Project documents

- Plans and specifications signed by a registered, licensed, or certified professional

- Contractor’s written, itemized bid

- Draw schedule with milestones

- Contingency line item (10–20% of renovation cost)

- Permit estimate with realistic timeline

- Site work and utility-hookup line items

- Form 1202 contractor profile (provided by lender, completed with your contractor’s info)

Financing documents

- Current first-mortgage statement and payoff letter (if refinancing)

- Most recent two years of W-2s or 1099s; two years of tax returns if self-employed

- Most recent 30–60 days of pay stubs

- Most recent two months of asset-account statements

- Existing leases for units not included in the renovation project (if using rental income to qualify)

- Homeowners insurance binder for the as-completed property

- Property tax estimate based on as-completed value

The Free ADU Starter Kit includes the complete lender document checklist

Download the Free ADU Starter Kit →Edge cases that trip up CHOICERenovation ADU borrowers

Answer capsule: A handful of niche scenarios reliably cause friction — HOA approval requirements, condo restrictions, Texas Home Equity rules, what happens if you sell mid-renovation, the legal-non-conforming ADU exception, and pre-completion delivery rules.

HOA and condo restrictions

If your property is in an HOA, the HOA must provide written approval for the renovation work. For condominium units, CHOICERenovation renovation work is limited to the interior of the unit — exterior or common-element work is generally not eligible. Loans secured by condo units must follow Freddie Mac’s published Condominium Project Eligibility Guidelines.

Texas Home Equity restrictions

Texas’s constitutional home-equity rules are unique. CHOICERenovation transactions in Texas have specific limitations, and Texas Home Equity transactions are not eligible. If you live in Texas, confirm with your lender that the structure of your transaction (purchase vs. rate-and-term refi vs. cash-out) is not classified as a Texas Home Equity transaction.

What happens if you sell mid-renovation

If you sell the property before the renovation is complete, the loan is paid off through the sale. Funds remaining in the completion escrow account are returned according to the loan documents — typically applied to the payoff. This is why lenders take such care with the as-completed appraisal and the contractor profile; an unfinished CHOICERenovation property is harder to sell.

The legal-non-conforming ADU edge case

A “legal non-conforming” ADU is one that was lawfully built under earlier zoning rules but doesn’t comply with current zoning — for example, an ADU permitted in 1985 with setbacks today’s code would not allow. Freddie accepts legal non-conforming ADUs without special exception treatment, provided documentation shows the ADU was legal when built. Keep the original permit records and certificate of occupancy.

The 5601.2 exception for illegal ADUs on 1-unit properties

For 1-unit subject properties only, Guide Section 5601.2 allows an ADU that does not comply with current zoning to make the property eligible under specific conditions, including appraiser confirmation that the property is acceptable as a one-unit residence without the ADU. Rental income from such an illegal ADU still may not be used to qualify the borrower.

Selling the loan to Freddie before the renovation is complete

By default, CHOICERenovation mortgages are sold to Freddie Mac after the renovation is complete. Lenders that have received prior written Freddie Mac approval and meet certain criteria — including at least two years of renovation-loan origination or servicing experience and eligibility to deliver loans with recourse — may sell the mortgage before completion. This affects lender pricing and process; borrowers won’t see this directly, but it’s why some lenders quote different timelines than others.

Cash-out treatment

CHOICERenovation itself is a purchase or no-cash-out refinance product. Freddie Mac’s broader ADU property eligibility rules may allow cash-out refinances on properties with ADUs under other Freddie Mac mortgage products, but that is not the same as using CHOICERenovation renovation proceeds. If you specifically want a cash-out refinance against an existing ADU’s equity, that’s a different product family.

What can kill a CHOICERenovation ADU approval?

Answer capsule: The most common failure points are zoning problems on the lot, an as-completed appraisal that comes in below projections, needing rental income from the funded unit to qualify (the May 2026 rule), contractor or documentation gaps, DTI failing under LPA on the borrower’s existing income alone, lender overlays imposing additional credit or down-payment requirements, and replacing a low first-mortgage rate when a second-lien product would be cheaper.

| Failure point | Rule / source | Pre-check |

|---|---|---|

| Zoning blocks an ADU on the lot | Local code; Guide §5601.2 | Run a property eligibility check before plans |

| As-completed appraisal below projections | Guide §4607.9 appraisal | Pull comparable sales of homes with ADUs in your zip before finalizing budget |

| Need new ADU rent to qualify | Bulletin 2026-1 (May 4, 2026 effective) | Test FHA 203(k) (50% projected rent), construction-to-permanent, or HomeStyle |

| Contractor / documentation gaps | Form 1202, plans/specs requirements | Use a renovation-loan-experienced GC; confirm they’ll produce required docs |

| DTI fails LPA without new ADU rent | LPA Accept required | Pay down credit-card or auto debt; re-run pre-qual |

| Lender overlays block the file | Lender-specific risk policy | If one lender’s overlay blocks you, your file may fit at another |

| Replacing a low first mortgage | Borrower economics | Run rate-comparison math vs. HELOC or future-value renovation HELOC |

A note on DTI

CHOICERenovation requires an LPA “Accept” classification, not a fixed DTI ceiling. LPA evaluates the full borrower profile — credit, reserves, down payment, income stability, and DTI together. A 47% DTI may Accept on a strong file; a 38% DTI may caution on a thin one. If your new mortgage payment pushes your file beyond what LPA and your lender’s overlays will Accept without the new ADU’s rent, CHOICERenovation may fail.

The first-mortgage replacement trap

If you have a low existing first-mortgage rate, replacing it to finance an ADU is often the most expensive way to get the ADU. The breakeven math: take your current loan balance, multiply by the rate differential, multiply by the years you’d keep the loan. If that number exceeds the cost of preserving your first mortgage and using a HELOC or future-value renovation HELOC at higher rates on a smaller balance, the HELOC wins. Run that calculation before signing CHOICERenovation paperwork.

When is CHOICERenovation the wrong path?

Answer capsule: CHOICERenovation is wrong when you have a low first-mortgage rate worth preserving, when you need the new ADU’s rent to qualify, when the ADU isn’t legally permissible on your lot, when the project is small enough to fit a second-lien product, or when you’re building ground-up new construction rather than adding to an existing dwelling.

Alternative 1: Keep your first mortgage; use a HELOC

If your current first mortgage is at a low rate, a home equity line of credit (HELOC) preserves that rate while letting you borrow against current equity. HELOCs are typically variable-rate and higher than first-mortgage rates, but you’re only borrowing against equity, not refinancing the entire balance. For ADU projects on homes with substantial current equity, this is often the cheapest path. Constraint: HELOCs typically lend to a CLTV of 80–85%.

HELOC for ADU deep-dive →Alternative 2: Future-value renovation HELOC

Some second-lien products lend against the after-renovation value of your home, similar to CHOICERenovation, without replacing your first mortgage. These typically come with higher rates than a conventional first-mortgage renovation loan. They make sense when you want to preserve your low first mortgage but don’t have enough current equity for a traditional HELOC.

Alternative 3: FHA 203(k)

Pick FHA 203(k) if your credit is 580–620 or your down payment is below 5% and you’re willing to accept FHA mortgage insurance. Watch the attached-ADU rule for new ADUs under Standard 203(k).

FHA 203(k) ADU guide →Alternative 4: Fannie Mae HomeStyle

The conventional alternative. Pick HomeStyle if your lender offers it and not CHOICERenovation, or if HomeStyle’s current treatment of ADU rental income (verified with your specific lender) works better for your scenario.

HomeStyle Renovation ADU guide →Alternative 5: Construction-to-permanent loan

A true construction loan funds the build, then converts to permanent financing once complete. The right path for ground-up new construction or for ADU builds large enough that a renovation mortgage isn’t a clean fit. Downside: more complex underwriting, more inspections, often higher rates during construction.

Construction-to-permanent ADU guide →Alternative 6: Cash-out refinance + separate construction financing

If your home has enough current equity, a cash-out refinance to fund the ADU can work. Trade-off: same as the first-mortgage replacement issue — only pencils if your existing rate isn’t low.

Cash-out refinance for ADU guide →Alternative 7: Home equity investment (HEI)

For borrowers who don’t want additional monthly debt, HEI products provide cash today in exchange for a share of future appreciation. HEI is state-restricted and not available everywhere; the long-term economics are very different from a traditional loan. Requires careful analysis against your specific situation.

What if you already paid for the ADU with short-term financing?

Answer capsule: CHOICERenovation provides an explicit no-cash-out refinance option to pay off short-term financing that funded ADU work completed before the note date, under Guide Section 4607.6(a). The ADU must be complete before the note date, all short-term financing obligations retired at closing, and the file must include documentation of the actual cost of the renovations and the short-term financing payoff calculation.

This scenario is more common than it sounds. A homeowner can’t qualify for CHOICERenovation up front (often because they need the new ADU’s rent to qualify, which Bulletin 2026-1 now blocks). They build the ADU using a short-term construction loan, bridge loan, or private capital. Once the ADU is complete, permitted, and producing documented rental income, they refinance into a CHOICERenovation no-cash-out refinance.

Whether the now-completed ADU is treated as a “unit included in the renovation project funded by the mortgage proceeds” under Bulletin 2026-1 is a question your lender will answer for your specific file. Confirm directly with your lender whether your specific scenario qualifies the completed ADU’s rent for income purposes.

What the file needs (Section 4607.6(a))

- All renovations financed by the short-term financing must be completed prior to the note date

- No obligations related to the short-term financing may remain outstanding

- All renovations must be completed prior to the appraisal

- The file must contain copies of the short-term financing agreement, documentation validating the actual cost of renovations, a calculation of the short-term financing payoff, and the Settlement/Closing Disclosure

When this path works best

- ADU is permitted, finished, and has a certificate of occupancy

- ADU is producing documented rental income or could under a market-rent analysis

- The existing first mortgage is at a rate where refinancing makes sense

- The borrower’s overall profile supports the refinance

Check zoning before calling a lender

Answer capsule: Always. Financing does not override local ADU zoning, building code, utility, septic, fire, HOA, or permitting rules. A loan is only useful if the ADU is legally buildable, appraisable, and permittable on your specific lot. The order is: zoning first, then plans, then financing. Doing it in any other order risks spending money on plans for an ADU that can’t be built.

A lender will not — and cannot — verify whether your lot supports an ADU. That’s the planning department’s job, and it varies city by city, sometimes parcel by parcel.

What to verify by address

- ADU permitted on this lot at all

- Detached, attached, conversion, or JADU permitted

- Maximum size by ADU type

- Setbacks (front, side, rear)

- Maximum height

- Maximum lot coverage and floor area ratio (FAR)

- Parking requirements (or applicable exemption)

- Owner-occupancy requirements

- Short-term rental restrictions or prohibitions

- HOA, PUD, or CC&R restrictions

- Fire-flow, septic capacity, water meter, or utility-service constraints

- Coastal-zone or overlay-zone requirements, if applicable

- Historic-district review, if applicable

- Tree-preservation or environmentally-sensitive-area restrictions

Before you spend a dollar on plans or call a lender, check your lot in 60 seconds.

Our free property eligibility check screens what’s possible at your address and flags the local rules to verify. No commitment, no payment.

Check My Property →Frequently asked questions

Can Freddie Mac CHOICERenovation finance an ADU?

Yes. Freddie Mac's ADU Fact Sheet (February 2026) explicitly permits CHOICERenovation to construct a new ADU or renovate an existing one on 1-, 2-, or 3-unit properties, subject to local zoning compliance and standard CHOICERenovation underwriting rules.

What is the maximum LTV for CHOICERenovation on an ADU loan?

95% for a 1-unit primary residence — or 97% only when the loan meets the applicable Home Possible or HomeOne program requirements. LTV caps are lower for 2- to 4-unit properties (typically 80–85%) and lower still for second homes and investment properties.

What is the 75% rule?

Total renovation costs financed by the loan cannot exceed 75% of the property's as-completed appraised value (for refinances) or 75% of the lesser of (purchase price + renovation costs) or as-completed value (for purchases). Eligible renovation costs include construction, soft costs, contingency reserve, and up to six months of PITIA during the renovation period.

How long do I have to complete the ADU?

450 days from the note date, per Freddie's CHOICERenovation materials. Lenders with prior Freddie approval may, in limited cases, request extensions, but borrowers should plan well within 450 days.

Can I use future ADU rental income to qualify for the loan?

No — not for CHOICERenovation, for applications received on or after May 4, 2026. Under Bulletin 2026-1, rental income from any unit included in the renovation project funded by CHOICERenovation proceeds cannot be used to qualify. Only rental income from units not included in the renovation project may be considered, subject to standard documentation rules.

Can I use rental income from an existing ADU to qualify?

Yes, if the existing ADU is not part of the renovation project funded by the loan, and provided the ADU is legal, legal non-conforming, or in a no-zoning area. Documented rental income from a lease cannot exceed 75% of the lease amount, and qualifying ADU rental income on a subject 1-unit primary residence cannot exceed 30% of total income used to qualify. Rental income from an illegal ADU may not be used.

What credit score do I need?

Freddie Mac does not publish a hard minimum credit score for CHOICERenovation — the requirement is that Loan Product Advisor returns "Accept." In practice, most lenders set 620 as their floor, and some impose higher overlays.

Can investors use CHOICERenovation?

Yes. 1-unit investment properties are eligible, with stricter LTV caps (typically 75–80%) and higher minimum down payments (typically 15%). FHA 203(k), by contrast, is primary-residence only.

Does CHOICERenovation work for manufactured-home or factory-built ADUs?

Yes, under certain conditions. For mortgages secured by manufactured homes containing an ADU, Freddie Mac Bulletin 2025-15 requires the primary dwelling to be a multiwide manufactured home. The ADU must also meet applicable manufactured-home and real-property requirements. Non-structural improvements are limited to the lesser of $50,000 or 50% of the as-completed appraised value when the primary dwelling is a manufactured home.

Can I be my own contractor?

Generally no, unless you are a licensed contractor qualified to perform the work. Even then, additional documentation and lender approval apply. The borrower and contractor cannot be in a related-party or employer-employee relationship.

What if my lender doesn't offer CHOICERenovation?

Ask whether they offer Fannie Mae HomeStyle Renovation — the closest conventional alternative. For many single-ADU scenarios the products are similar, but ADU and rental-income rules are not identical. If you need CHOICERenovation specifically, several national lenders deliver it; see the lender table in this guide.

Can I refinance an existing ADU construction loan with CHOICERenovation?

Yes. Section 4607.6(a) permits a no-cash-out refinance to pay off short-term financing that funded a completed ADU, provided the ADU is finished before the note date and the file documents the short-term financing amount and renovation costs. Whether the completed ADU's rent is available for qualifying on the refinance depends on lender treatment under Bulletin 2026-1 — confirm directly.

Is CHOICERenovation better than HomeStyle for an ADU?

For many ADU scenarios, the two are functionally similar. The biggest practical differences: which lenders offer which (some only deliver one), the May 2026 rental-income rule applies specifically to CHOICERenovation, and Fannie's UAD 3.6 policy expansion has changed certain ADU treatments for HomeStyle (lender-dependent). Confirm the specific treatment for your scenario with the lender.

Does Freddie Mac require landlord education?

Yes, in one specific case: for purchase transactions where rental income from an ADU on a subject 1-unit primary residence is used to qualify the borrower, at least one qualifying borrower must complete landlord education — unless that borrower has at least one year of investment property management experience or ADU rental management experience.

Can CHOICERenovation be used as a cash-out refinance?

CHOICERenovation itself is a purchase or no-cash-out refinance product. Freddie's broader ADU property eligibility rules may allow cash-out refinances on properties with ADUs under other Freddie Mac mortgage offerings, but that is not the same as using CHOICERenovation renovation proceeds.

What we verified for this guide

This guide is built from primary Freddie Mac sources, current lender materials, and cross-checked against Fannie Mae and HUD documentation. Every factual claim below has been verified against the cited source as of May 20, 2026.

| Claim | Source | Last verified |

|---|---|---|

| CHOICERenovation can construct or renovate ADUs | Freddie Mac ADU Fact Sheet, February 2026 | May 20, 2026 |

| One ADU allowed on 1-, 2-, and 3-unit properties | Freddie Mac ADU Fact Sheet, February 2026 | May 20, 2026 |

| Rental income from funded unit cannot qualify after May 4, 2026 | Freddie Mac Bulletin 2026-1 | May 20, 2026 |

| 450-day completion period | CHOICERenovation Fact Sheet | May 20, 2026 |

| 75% renovation cost cap | CHOICERenovation Maximum Mortgage Worksheet; Guide Chapter 4607 | May 20, 2026 |

| 10–20% contingency (15% if utilities not operable) | CHOICERenovation Fact Sheet | May 20, 2026 |

| Max LTV 95% on 1-unit primary; 97% only with Home Possible/HomeOne | CHOICERenovation Fact Sheet; correspondent matrices | May 20, 2026 |

| LPA Accept required; no manual underwriting | Plaza correspondent guidelines; Freddie product materials | May 20, 2026 |

| Manufactured-home ADU multiwide-primary requirement | Freddie Mac Bulletin 2025-15 | May 20, 2026 |

| ADU rental income limits (75% of lease; 30% cap on 1-unit primary) | Freddie Mac ADU Fact Sheet, February 2026 | May 20, 2026 |

| Landlord education requirement | Freddie Mac ADU Fact Sheet, February 2026 | May 20, 2026 |

| 2026 conforming loan limits ($832,750 / $1,249,125) | FHFA news release, November 25, 2025 | May 20, 2026 |

| HomeStyle 15-month completion | Fannie Mae HomeStyle Renovation (B5-3.2-01) | May 20, 2026 |

| 203(k) Standard 12-month / Limited 9-month rehabilitation period | HUD Mortgagee Letter 2024-13 | May 20, 2026 |

| 203(k) Standard new ADU must be attached; existing ADU may be attached or detached | HUD Mortgagee Letter 2023-17 | May 20, 2026 |

| 203(k) projected ADU rent capped at 50%; 30% of effective income cap | HUD Mortgagee Letter 2023-17 | May 20, 2026 |

| CHOICEReno eXPress 180-day / 10% (15% in Duty to Serve areas) | Freddie Mac CHOICEReno eXPress materials; Bulletin 2025-16 | May 20, 2026 |

Methodology

This page was built by starting with primary Freddie Mac sources — the February 2026 ADU Fact Sheet, the CHOICERenovation Fact Sheet and product page, Guide Chapter 4607, Section 5601.2, Bulletin 2026-1, and Bulletin 2025-15 — then cross-checking against current correspondent lender matrices from eLEND, The Money Source, Plaza Home Mortgage, and CrossCountry. The comparison sections draw on Fannie Mae’s HomeStyle Renovation Selling Guide section and HUD’s Mortgagee Letters 2023-17 (ADU policy) and 2024-13 (203(k) program updates).

When lender summaries disagreed with Freddie Mac’s own documentation, we deferred to Freddie’s published materials. When older industry articles disagreed with current Bulletin language, we used the current Bulletin. When sources appeared inconsistent, we cited both and noted the discrepancy.

This page is not a loan offer, not legal advice, not tax advice, and not a guarantee of approval. ADU rules vary by city, county, and state. Program rules change — sometimes multiple times per year. The “Last verified” date above reflects the most recent source check.

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder. We do not sort lender lists by payout. Our active mortgage-lead partner is the Mortgage Research Center; that partnership covers broad mortgage and refinance education, not specific CHOICERenovation lender placement. Read our editorial standards, methodology, partner vetting policy, and affiliate disclosure for the full picture.

Related guides on The Dwelling Index

- Best ADU Financing Options 2026: 7 Loan Paths Compared — the parent hub comparing all financing paths

- ADU Renovation Loan: Rules, Real Costs & Fit Finder — broader renovation-loan deep dive

- Fannie Mae HomeStyle Renovation ADU 2026 — the closest conventional alternative to CHOICERenovation

- FHA 203(k) Loan for ADU — the lower-credit-score renovation path

- HELOC for ADU — the second-lien alternative if you want to preserve your low first mortgage

- How to Finance an ADU With No Equity — the low-equity path

- Construction-to-Permanent Loan for ADU — ground-up new construction path

- Cash-Out Refinance for ADU — the cash-out alternative

- ADU Rental Income Calculator — estimate your ADU’s market rent

- How Much Does an ADU Cost? — cost planning by ADU type

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

Check My Property →