Prefab ADU Financing in 2026: The 7 Paths and the Factory-Deposit Trap

By the Dwelling Index Editorial Team · Last updated: · Last verified: · Editorial standards · Affiliate disclosure · ~38 min read

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, appraiser, builder, or zoning authority, and nothing here is financial, legal, tax, or lending advice.

Disclosure: The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. We are not a lender, broker, or builder. Read the full disclosure.

If you’ve already gotten a prefab quote, you may recognize the feeling that brought you here. You were excited — prefab is fast, the pricing looked clean — and then you read the contract and saw a deposit due now, with more due before anything lands in your yard. Maybe your loan officer went quiet when you mentioned it. Maybe you’re weighing a HELOC against a cash-out refinance and dreading giving up the low mortgage rate you locked years ago. Maybe a builder advertised “100% financing” and you can’t tell if that’s real. Those are the right worries to have. This guide is built to resolve every one of them, in order, with sourced numbers and a checklist you can take to a lender.

See What You Can Build → Get Your Free ADU Report

Free, no obligation. See your size, likely path, and financing questions before you commit a dollar.

Get your free ADU report →Which prefab ADU financing path should you compare first?

The fastest way to narrow seven options to one is to start with your biggest constraint, not the product names. Equity-rich owners who want to keep a low first mortgage usually compare a HELOC or home equity loan first; owners short on equity compare finished-value renovation or construction loans; and prefab buyers facing a tight factory deadline compare manufacturer financing or a lender that can fund deposits before installation. Find your row below — that’s the lane to compare first.

Quick definitions before you read it. An ADU (accessory dwelling unit) is a self-contained second home on the same lot as a single-family house — a backyard cottage, in-law suite, or converted garage; a detached one is sometimes called a DADU, a smaller interior one a JADU (junior ADU). LTV (loan-to-value) is the loan amount divided by the home’s value. A draw is a release of loan funds tied to a construction milestone.

| Your situation | First path to compare | The prefab-specific catch | Your next step |

|---|---|---|---|

| Strong equity, want to keep your low first mortgage | HELOC or home equity loan | May not cover the all-in cost; some lenders balk at funding a factory deposit | Confirm equity; ask about deposit timing |

| Want one loan, a larger amount, and you’re refinancing anyway | Cash-out refinance | Replaces your current mortgage — painful if your rate is low | Compare the blended lifetime cost vs. a second lien |

| Buying or refinancing and adding the ADU | Renovation loan (HomeStyle, CHOICERenovation, FHA 203(k)) | Agency rules, appraisals, draw controls; manufactured units need extra docs | Ask the lender about ADU + prefab eligibility |

| Building ground-up or want one closing | One-time-close construction-to-permanent | Must use a lender that writes factory deposits into the draw schedule | Find a modular-experienced lender |

| Have equity, want no monthly payment, can tolerate a later settlement | Home equity investment (HEI) | Requires existing equity (often ~25%+); limited states; balloon settlement | Check availability in your state |

| The provider offers in-house financing | Manufacturer-linked financing | Built around the factory schedule, but brand- and state-specific | Compare it against an independent option |

| Little or no equity | Finished-value renovation/construction loan, or manufacturer financing | Each has tradeoffs; future rent may not count automatically | See our no-equity path below |

Comparison sorted by borrower situation and neutral criteria (equity required, payment structure, eligibility) — never by any business relationship.

Still not sure which of these seven is you? Our free Prefab ADU Financing Path Finder takes four inputs — your home equity, your credit comfort, whether you own your land outright, and your prefab type — and returns the paths worth discussing with a lender, plus your personal deposit-coverage gap: the cash you’ll likely need on hand before any loan releases a dollar. It’s an educational tool, not a lender recommendation, and it doesn’t store your answers.

Run the free Path Finder →

See which paths fit your situation and your deposit gap.

Run the Path Finder →Why prefab financing is different: the factory-deposit trap

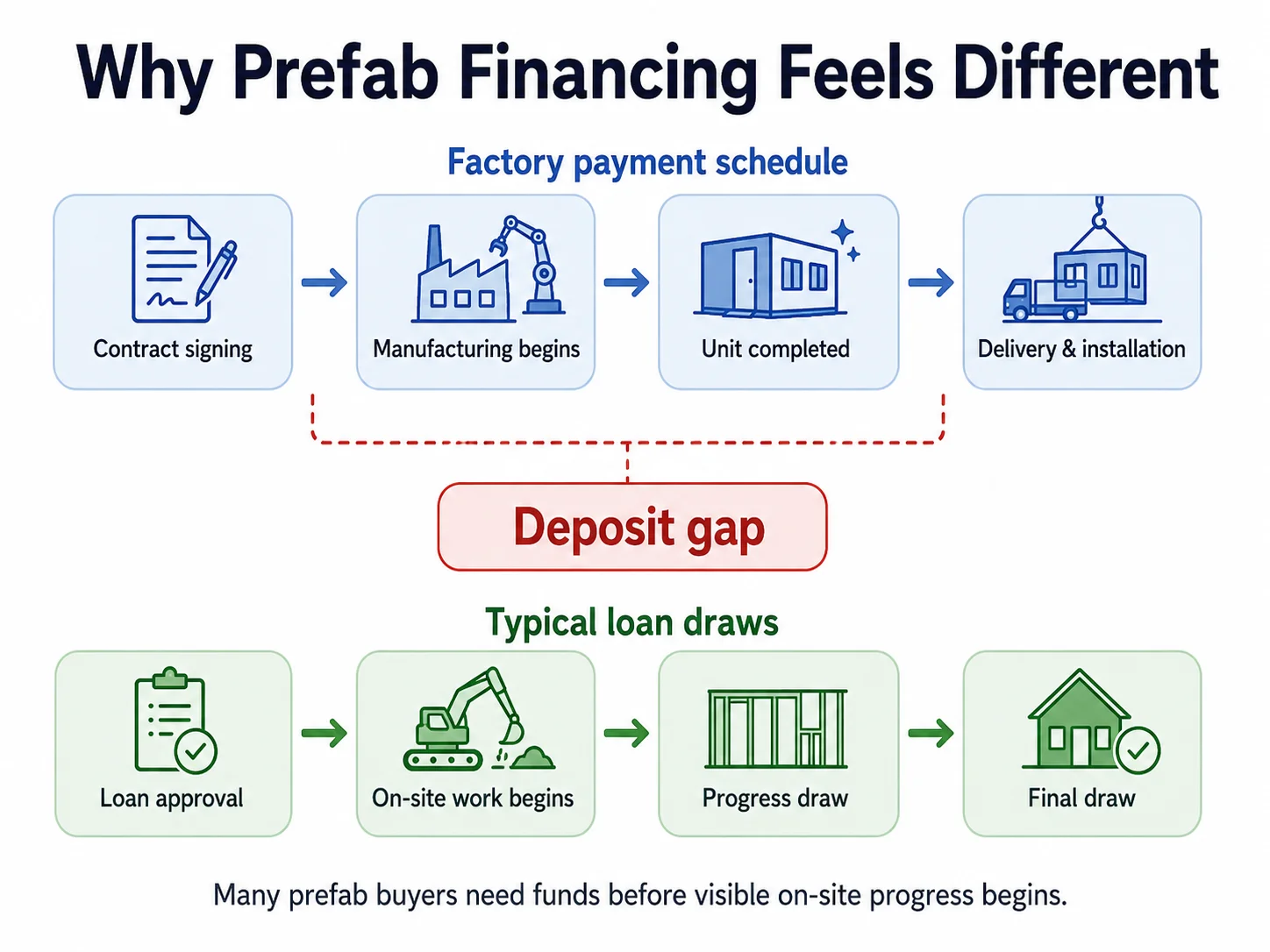

Prefab ADU financing differs from site-built financing mainly in payment timing, not loan type. Manufacturers typically tie large payments to factory milestones — often the entire unit cost is due before the unit is delivered — while most construction and renovation loans release money against progress an inspector can see on the property. That mismatch between the factory’s payment schedule and the lender’s draw schedule is the single most common reason a prefab project stalls. Solve the timing and you’ve solved 80% of the problem.

This is the part nearly every competing article skips, so we’re going to prove it with a real, published payment schedule — then show you the three clean ways out.

A real-world payment schedule, decoded

Abodu, one of the most established prefab ADU companies in California, publishes its payment schedule openly. The cost of an Abodu is split into a Unit Contract (the factory unit) and a Site Work Contract (getting your yard ready). Here’s the published schedule, with our plain-English translation of why each step is a financing landmine:

| Stage | When | Payment due | What it means for your loan |

|---|---|---|---|

| On-site assessment | At start | $250 (non-refundable) | Trivial — but it’s the first dollar, and it’s non-refundable. |

| Contract signing | After you sign the all-in contract | 10% of Unit Contract | You’re committing real money before any lender draw exists. |

| Manufacturing begins | ~1 month later | 40% of Unit Contract | The factory now wants 50% total — and nothing is on your lot yet. |

| Manufacturing completed | ~4 months later | Final 50% of Unit Contract | The entire unit is now paid for — still sitting in the factory. |

| Ready for installation | ~2 weeks later | 50% of Site Work Contract | Now site work begins — the part lenders are comfortable funding. |

| Project completion | ~2 weeks later | Final 50% of Site Work Contract | Certificate of occupancy issued; the ADU is ready to use. |

Source: Abodu published payment schedule (abodu.com/pricing), verified May 31, 2026. Schedules vary by manufacturer — treat this as a representative example, not a universal rule.

Look at the fourth row. By the time the unit leaves the factory, you’ve paid 100% of the Unit Contract — and there is still nothing on your property for an appraiser or inspector to look at. A traditional construction loan releases money through “draws” tied to on-site progress: foundation poured, framing up, roof on. A unit being assembled in a factory two counties away produces zero on-site progress for months. That is the trap, in one sentence: the most expensive moment of a prefab build comes before there’s anything in your yard to pay against.

What the gap looks like in dollars

Let’s run it. Take Abodu’s 500-square-foot one-bedroom, which the company lists at an average all-in price of $352,500 (base $326,800 plus average upgrades of $25,700), before permit fees and taxes that average about $17,000. Suppose — for illustration only; your real split comes from your signed quote — that contract breaks into a $280,000 Unit Contract and a $72,500 Site Work Contract. Here’s the cash the factory expects, and when:

- At signing: 10% of the unit = $28,000

- ~1 month in, manufacturing begins: 40% of the unit = $112,000 (running total $140,000)

- ~4 months in, manufacturing complete: the final 50% of the unit = $140,000 (running total $280,000 — the entire unit, paid, before delivery)

- Only then does the $72,500 of site work get billed, as the unit lands and the yard gets finished.

A standard construction loan would have released roughly $0 against that $280,000, because none of it produced on-site progress. So your job is to line up a funding source that puts that money in your hands — or a lender that explicitly agrees to fund factory milestones — before you sign. Miss that, and you’re the homeowner who’s pre-approved for a loan they can’t actually use.

Why this is a documented industry pattern, not one company’s quirk

This isn’t an Abodu thing. Analysis from the Construction Financial Management Association (CFMA) explains the underlying economics: because manufacturers must buy materials and reserve factory line time months ahead — materials alone can be 60% or more of total job cost — modular projects commonly require a non-refundable letter-of-intent deposit of around 5% roughly six months ahead of production, followed by a 25%-or-greater material deposit about three months ahead, with manufacturers often requiring upfront deposits “as high as 30% or more of the off-site contract.” A site-built project funds in lockstep with visible progress; a factory build front-loads the cash. The federal government has even acknowledged the problem by name: California’s 2022 state budget listed “deposits on factory-built ADU products” as an eligible use of dedicated ADU financing funds.

The Urban Institute puts the consequence bluntly: most ADUs today are financed “by relatively affluent homeowners,” because tapping home equity demands strong credit and existing equity — and second mortgages tailored for ADU construction are “virtually non-existent,” since lenders see them as risky and hard to resell without government backing. That’s the landscape. Now here’s how to navigate it.

The three clean ways out of the trap

- 1. Put cash in your hands up front. A HELOC, home equity loan, cash-out refinance, or home equity investment hands you money you control, so you can pay the factory on its schedule without waiting on a draw. This is why equity-rich homeowners have the easiest time with prefab — and why so much existing ADU financing quietly favors them.

- 2. Use a renovation loan that allows large upfront disbursements. As of Fannie Mae Selling Guide Announcement SEL-2025-10 (December 10, 2025), HomeStyle Renovation now lets lenders disburse up to 50% of total renovation costs at closing — explicitly including materials, permits, architectural and design fees, and reimbursement of a borrower’s deposit (when the borrower intends to finance all renovation costs). The same announcement removed the prior $50,000 renovation-cost cap for manufactured homes. That 50%-at-closing rule is, in practice, the closest thing to an agency-backed bridge for a prefab factory deposit — and it’s recent enough that most articles haven’t caught up.

- 3. Use a one-time-close construction-to-permanent loan with a modular-experienced lender. These lenders write factory deposits directly into the draw schedule and release funds against a factory invoice plus a review of the manufacturer, rather than demanding on-site progress for that payment. The catch is that you have to find them — a generalist loan officer at a big retail bank often can’t do it.

A note on honesty, because you’ll thank us later.

Prefab is not automatically easier to finance than site-built. It’s faster to build and easier to price, but if your lender can’t fund off-site factory progress, it can be harder. And as the Urban Institute data shows, the conventional equity paths were largely built for high-FICO, high-equity homeowners. That’s the bad news. The good news is everything below: the 2025 rule changes, finished-value loans, and the lender checklist at the end exist precisely to level that field — and homeowners with modest equity are building prefab ADUs right now using exactly these tools.

See What You Can Build → Get Your Free ADU Report

Confirm what your lot supports and which financing lane fits before you talk to a lender.

Get your free ADU report →The 7 prefab ADU financing paths, compared

The seven realistic ways to finance a prefab ADU are cash, a home equity line of credit (HELOC), a home equity loan, a cash-out refinance, a renovation or construction loan (including Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, and FHA 203(k)), a home equity investment (HEI), and manufacturer-linked financing. They differ on three things that matter most for prefab: how much equity they require, whether they let you keep your existing mortgage, and — critically — whether they can fund the factory deposit before installation. There is no universal “best”; there’s the one that fits your equity, your current mortgage rate, and your manufacturer’s payment schedule.

Let’s define the jargon once:

- HELOC (home equity line of credit): a revolving credit line secured by your home; you draw what you need, usually at a variable rate.

- Home equity loan: a fixed lump sum secured by your home, repaid at a fixed rate — a “second mortgage.”

- Cash-out refinance: you replace your existing mortgage with a new, larger one and pocket the difference.

- Renovation loan: a mortgage that finances the home plus improvements, underwritten partly on the home’s after-completion (finished) value.

- One-time-close (OTC) construction-to-permanent: a single loan that covers construction and automatically converts to a permanent mortgage when the build is done — one closing, one set of costs.

- HEI (home equity investment, a.k.a. home equity agreement): a lump sum of cash in exchange for a share of your home’s future value, with no monthly payments and a balloon settlement later. It is not a loan, and it requires existing equity.

| Path | Funds the factory deposit early? | Keeps your first mortgage? | Built on current or finished value? | Best-fit prefab buyer | The honest catch |

|---|---|---|---|---|---|

| Cash | Yes | Yes | N/A | High liquidity, wants simplicity | Opportunity cost; ties up reserves |

| HELOC | Usually, once the line is open | Yes | Current value | Equity-rich; wants flexible, keep low rate | Variable rate; capped at current value |

| Home equity loan | Usually, as a lump sum | Yes | Current value | Equity-rich; wants fixed payments; known-cost turnkey | Same current-value ceiling; second-lien rate |

| Cash-out refinance | Yes, after closing | No — replaces it | Current value | Refinancing anyway; needs a larger sum | Can torch a low first-mortgage rate |

| Renovation loan (HomeStyle / CHOICERenovation / 203(k)) | Yes — up to 50% at closing on HomeStyle | Varies | Finished value | Low-equity owners; anyone who needs finished value to qualify | Paperwork, appraisals, draw controls, agency rules |

| One-time-close construction | Only with a modular-experienced lender | Converts to (sets) your mortgage | Finished value | Ground-up or one-closing projects | Must find a lender who funds factory draws |

| HEI | Yes, if funded | Yes | Equity-share product | Equity-rich; wants no monthly payment | Requires ~25%+ equity; limited states; balloon settlement |

| Manufacturer financing | Usually — designed around the factory schedule | Often yes | Brand-specific | Buyer of that specific provider | Brand- and state-specific; compare total cost |

Sorted by fit to the prefab cash-flow problem and neutral criteria — never by any business relationship or payout. “Best-fit” notes are our editorial conclusions, based on the verified facts in What we verified.

1. Cash

Punchline: if you have it, cash sidesteps the entire factory-deposit problem — there’s no draw schedule to clash with. You still verify permits, code, and zoning before you spend a dollar, and you give up liquidity and the chance to leverage rising home value, but no path is faster to the manufacturer’s milestones. Most homeowners pair cash with one other path: the Urban Institute notes the lopsided reality that, absent good financing options, a large share of homeowners drain savings or borrow from family to fund home projects. If you’d rather not, read on.

2. HELOC or home equity loan

Punchline: for equity-rich homeowners, a second lien is often the cleanest way to cover a factory deposit, because the cash lands in your account and you control the timing — and you keep your existing first mortgage untouched, which is a real advantage if you locked a low rate years ago. A HELOC gives flexible, draw-as-you-go access at a usually-variable rate; a home equity loan gives a fixed lump sum with fixed payments, which pairs neatly with a known-cost turnkey prefab.

The honest tradeoffs: your home is the collateral, so default puts the house at risk. A HELOC’s rate is typically variable, so the payment can move. And here’s the constraint that surprises people — home equity lending is generally capped around 80% of your home’s current value and ignores the future value the ADU will add, so your available equity may simply not reach an all-in prefab budget north of $250,000. The Urban Institute’s data underlines who this path really serves: the average HELOC borrower’s credit score exceeds 760. We never quote specific rates as promises — your rate depends on your credit, your lender, and the market on the day you lock.

3. Cash-out refinance

Punchline: a cash-out refinance rolls everything into one new mortgage and one payment, which is tidy — but it replaces your existing loan, so it’s painful if your current rate is well below today’s market. It shines when you were going to refinance anyway, or when you need a larger sum than a second lien comfortably allows. Like every equity path, the cash arrives up front, so the factory-deposit problem disappears. The math to run before you sign: compare the blended lifetime cost of refinancing your whole balance at today’s rate against keeping your low first mortgage and adding a smaller second lien. For a homeowner sitting on a sub-4% mortgage, a cash-out refinance can quietly cost more over time than the ADU itself.

Once you’ve got your prefab quote and payment schedule in hand, the next move is comparing real financing lanes with people who understand construction lending. Loan availability, terms, and approval are never guaranteed, and we present lanes — not lender rankings.

Affiliate link — we may earn a commission at no extra cost to you; it never affects our recommendations.

Explore ADU mortgage, refinance, and construction-loan options →

Independent financing-lane education. We don’t quote rates or guarantee approval.

Explore financing options →4. Renovation loan — HomeStyle, CHOICERenovation, FHA 203(k)

Punchline: renovation loans let you borrow partly against your home’s finished value rather than only its current value, which can sharply reduce how much equity you need today — and a 2025 rule change made them far more prefab-friendly. The price of admission is paperwork: appraisals, contractor documentation, draw controls, and agency-specific eligibility. You’ll still face loan-to-value limits, cash-to-close requirements, credit standards, and lender overlays. Three programs matter:

- Fannie Mae HomeStyle Renovation. Fannie Mae confirms HomeStyle can be used to purchase or refinance a one-unit property and construct or install a new ADU, and per its HomeStyle Renovation FAQ it can even cover a manufactured-home ADU when all standard manufactured-home requirements are met, “including but not limited to conversion to real property.” As covered above, SEL-2025-10 (Dec. 10, 2025) raised the allowable upfront disbursement to 50% of total renovation costs and removed the prior $50,000 renovation cap for manufactured homes — both directly useful for prefab. Note the program requires a construction contract and inspections for work items over $5,000.

- Freddie Mac CHOICERenovation. Freddie Mac states CHOICERenovation can be used “to add a new ADU or renovate an existing ADU,” with its ADU requirements applying across Freddie Mac mortgage products. It’s the second agency path to put in front of a lender.

- FHA 203(k). FHA’s Standard 203(k) rehabilitation mortgage can finance certain ADU work — generally adding an ADU attached to the existing structure, or renovating an existing attached or detached ADU — under HUD Mortgagee Letter 2023-17 (effective Oct. 16, 2023). That same letter lets a lender count up to 75% of the estimated fair-market rent from an existing ADU, or 50% of the estimated rent from a new ADU built via 203(k), toward qualifying income in defined cases. Because FHA’s treatment of factory-built and manufactured units carries extra requirements, confirm your specific unit type with an FHA-approved lender before relying on 203(k).

5. One-time-close construction-to-permanent (OTC)

Punchline: an OTC loan combines construction financing and your permanent mortgage into a single closing — locking your permanent rate before the build starts and saving a second set of closing costs — but for prefab it only works if your lender writes factory deposits into the draw schedule. Fannie Mae explicitly allows Construction-to-Permanent financing to fund both a home and an ADU. The make-or-break detail is finding a modular-experienced lender: one who releases funds against a factory invoice and a review of the manufacturer, rather than waiting for on-site progress. Credit unions and regional banks with a modular track record are the usual home for this; a national retail call center usually is not. (One current wrinkle worth confirming: many lenders pulled back from VA one-time-close construction programs in 2025, so veterans should verify VA OTC availability specifically before relying on it.)

6. Home equity investment (HEI)

Punchline: an HEI hands you a lump sum with no monthly payment, which preserves cash flow during a build — but it requires meaningful existing equity, you settle later with a share of your home’s future value (often via a balloon), and it’s available in only a limited set of states. It is an equity-access product, not a no-equity solution. Providers like Hometap, Unlock, and Point offer them; most require roughly 25% or more equity and will accept lower credit scores than many HELOC lenders. State availability differs by provider and changes often, so check current availability in your state before counting on it.

The honest negative: the Consumer Financial Protection Bureau (CFPB) describes home equity contracts as complex, often expensive compared with traditional home-secured financing, and hard to compare — and warns they can leave a homeowner facing a large repayment or a forced sale if they can’t settle. Because there’s no monthly payment, the settlement at the end can be large, and if your home appreciates strongly, an HEI can cost more than a conventional loan would have. If you don’t know when you’ll sell or whether you’ll have cash to settle, a traditional equity product is usually safer.

7. Manufacturer-linked financing

Punchline: because the prefab company designed the product, its in-house or partner financing is often built to match the factory payment schedule — which can neatly solve the deposit-timing trap — but it’s frequently brand-specific, state-specific, and not portable, so always compare it against an independent option. To illustrate how these programs work: Samara lists its 800-square-foot Backyard XL 8 starting at $249,000 plus installation (verified May 31, 2026), and states that financing is offered through third-party partners, with terms that can include as little as no money down and no payments or interest for 180 days while you keep your existing mortgage. Treat that as a single-provider illustration of the structure of manufacturer financing — not a national availability claim or a rate quote.

When you evaluate any manufacturer financing, ask: Who is the actual lender? Is it available in my state? Does it cover site work, permits, taxes, foundation, delivery, and craning — or only the unit? Can I use my own lender instead?

Run the free Path Finder →

Four inputs, and you’ll see the paths worth discussing with a lender plus your personal deposit-coverage gap.

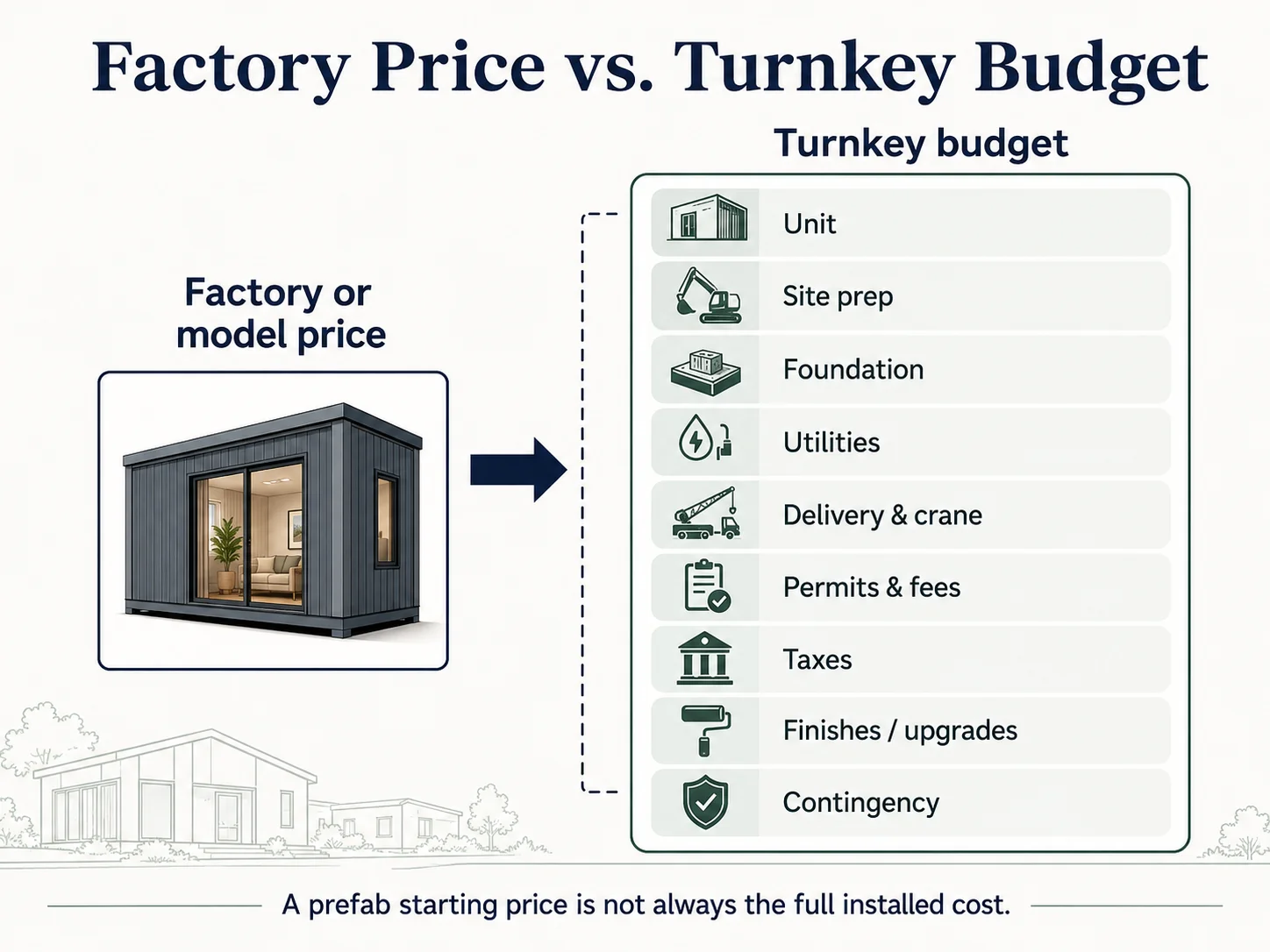

Run the Path Finder →Modular quote vs. turnkey total: what the sticker price hides

A prefab “starting at” price almost always covers the factory unit alone. The turnkey total adds foundation, delivery, craning, utility hookups, permits, taxes, site prep, and sometimes demolition or engineering — frequently 40% to 100%+ on top of the unit price. Financing the sticker price instead of the all-in installed budget is the single most expensive prefab mistake, because it leaves the project under-funded mid-build, exactly when more money is hardest to get.

First, the national picture, so you don’t anchor on any one market. Across the U.S., ADUs average roughly $180,000, with a wide range of about $60,000 to $285,000 depending on type, region, and finish (2025 industry data). Prefab and modular construction typically runs $150–$300 per square foot and tends to save 10%–25% versus custom site-built, mostly through factory efficiency. The unit alone can start far lower — independent benchmark HomeGuide pegs prefab/modular units around $80–$160 per square foot (2026) — but the installed project is another matter. Maxable reports installed prefab studios running roughly $190,000–$304,000 and one-bedrooms around $219,000–$320,000 (verified May 31, 2026). The pattern is consistent across every source: the unit is a fraction of the finished project.

Now the granular proof, using Abodu’s published 2026 California figures (verified May 31, 2026):

| Abodu model | Size | Base price | + Avg. upgrades | = Avg. price | + Permits/taxes |

|---|---|---|---|---|---|

| Studio | 340 sq ft | $278,800 | $21,700 | $300,500 | ~$17,000 avg. |

| One (1 bd / 1 ba) | 500 sq ft | $326,800 | $25,700 | $352,500 | ~$17,000 avg. |

| Two (2 bd / 1 ba) | 610 sq ft | $360,800 | $31,700 | $392,500 | ~$17,000 avg. |

| Two+ (2 bd / 2 ba) | 800 sq ft | $426,800 | $52,000 | $478,800 | ~$17,000 avg. |

| Dwell House (1 bd / 1 ba) | 540 sq ft | $439,000 | $59,500 | $498,500 | ~$17,000 avg. |

Source: Abodu published pricing (abodu.com/pricing), verified May 31, 2026. These are California numbers and run high for the market; nationally, prefab ADUs span a wider range.

Abodu is unusually transparent — its base price includes a project manager, the unit, permit services, pre-approved plans, delivery and installation, foundation, and standard utility connections. And it still excludes utility trenching beyond 50 feet, craning beyond 100 feet, building demolition, tree removal, unique site engineering, and sales tax and permit fees. If even a company that bundles foundation and utilities has a list of exclusions this long, a provider quoting a bare “unit only” price has a far longer one.

The takeaway: borrow against the turnkey total, plus a contingency. Under-borrow on the sticker price and you’ll be calling your lender mid-project asking for more.

Hidden costs to budget before you apply

These line items routinely turn a $300,000 quote into a $380,000 project:

- Permit fees and plan-review fees

- Utility trenching, sewer/septic work, and electrical panel upgrades

- Foundation (if not included)

- Delivery and craning

- Demolition and tree removal

- Fire sprinklers and stormwater requirements

- Sales tax

- Financing reserves

- A contingency — we suggest 10%–15%

Download the free ADU Starter Kit →

Get the printable budget worksheet that lists every line item lenders expect — plus our prefab deposit-timing checklist.

Download the Starter Kit →Does the lender care if it’s modular, panelized, or manufactured?

Yes — “prefab” is a marketing umbrella, but lenders treat the underlying construction types very differently. Modular and panelized units built to the state building code are generally financed much like site-built homes once permitted and permanently installed. HUD-code manufactured units carry extra requirements — a permanent foundation, conversion to real property, title work, and HUD certification documents. Tiny homes, RVs, and park models often don’t qualify as real property at all, which can make them ineligible as mortgage collateral. This single distinction can be the difference between a normal mortgage and a high-rate personal loan — or no financing at all.

Fannie Mae’s UAD 3.6 policy (2026) draws the line cleanly:

- Modular homes are financed as loans “secured by modular homes built in accordance with the International Residential Code [IRC] administered by state agencies” — treated essentially like site-built. (The IRC is the model residential building code most states adopt; building to it is what lets a factory-built unit be valued like a stick-built one.)

- Prefabricated, panelized, and sectional homes are eligible and “do not have to satisfy HUD’s Federal Manufactured Home Construction and Safety Standards” — again, more like site-built.

- HUD-code manufactured homes are a separate category — built to the federal manufactured-housing standard (24 CFR Part 3280) — with their own real-property, foundation, and certification requirements.

| Prefab type | Plain-English meaning | What the lender worries about | Documents to collect |

|---|---|---|---|

| Modular ADU | Factory-built modules assembled on-site to the state/local code (IRC) | Usually easiest — treated like site-built once permitted, affixed, and titled as real property | Approved plans, permits, specs, foundation details, contract, appraisal support |

| Panelized ADU | Wall/roof/floor panels built in a factory, assembled on-site | Often handled like construction/renovation; generally lender-friendly | GC contract, draw schedule, inspections, permits |

| HUD-code manufactured ADU | Built to the federal manufactured-housing standard (24 CFR Part 3280) | Needs permanent foundation, conversion to real property, title work, HUD label/data plate | HUD certification label & data plate, foundation certification, title/ALTA docs |

| Tiny home / RV / park model | Often built to RV or park-model standards; may be on wheels | May be personal property, not mortgageable; may not qualify as an ADU under zoning | Local zoning confirmation, title status, foundation/code documentation |

| Container or foldable unit | Varies widely by product and jurisdiction | Must satisfy local code, foundation, permits, and collateral rules | Engineering, code compliance, permits, foundation, appraisal support |

Sources: Fannie Mae UAD 3.6 policy (2026) and Selling Guide property-eligibility provisions, verified May 31, 2026.

The five words that decide everything

Legal real property on a foundation.

A modular unit that’s permitted, permanently affixed, and titled as real property clears that bar easily. A “portable,” “mobile,” or “RV-style” unit on wheels usually does not. (Real property simply means land and anything permanently attached to it — as opposed to personal property like a vehicle, which mortgages can’t be secured against.)

Red flags before you sign

Pause, or walk away, if:

- The seller calls the unit “mobile,” “portable,” or “RV-like”

- There’s no clear permit path

- There’s no permanent-foundation plan

- Nobody can answer the real-property/title question

- HUD certification labels or the data plate are missing for a manufactured unit

- The provider can’t hand your lender the specs, contract, payment schedule, and installation scope

Can ADU rental income help you qualify?

Sometimes — and the rules just expanded — but the details are specific, so don’t assume rent will count. As of Fannie Mae Selling Guide Announcement SEL-2025-08 (Oct. 8, 2025), rental income from an existing ADU on a one-unit principal residence can count toward qualifying income, but only on purchase and limited cash-out refinance transactions, only from one ADU, and capped at 30% of the borrower’s total qualifying income. FHA and Freddie Mac have their own separate ADU rental-income rules. Treat any rental figure as conditional until your lender confirms it for your specific loan.

The rules, program by program

Fannie Mae. Per SEL-2025-08 and the current Selling Guide (B3-3.8-01), a lender may use rental income from an existing ADU on a one-unit principal residence toward qualifying income when all of these hold: the transaction is a purchase or limited cash-out refinance, the income comes from only one ADU (even if more exist), and the amount used is capped at 30% of the borrower’s total qualifying income, with standard rental-income documentation. Desktop Underwriter support arrived with version 12.1 in Q1 2026 (the weekend of March 21, 2026). Separately, the December 2025 update (SEL-2025-10 / UAD 3.6) expanded ADU property eligibility — including allowing up to three ADUs on certain one-unit properties — which widens what can be financed even if it doesn’t change the income cap. One nuance worth repeating: this is about an ADU on a principal residence; it is not a blanket rule that a not-yet-built prefab unit’s projected rent will automatically qualify you.

FHA. Mortgagee Letter 2023-17 allows, in certain cases, up to 75% of the estimated fair-market rent from an existing ADU, or 50% from a new ADU added via Standard 203(k), to count as effective income — subject to FHA rules and appraisal/rent-schedule documentation.

Freddie Mac. Permits rental income from an ADU on a subject one-unit primary residence to be used for certain purchase or no-cash-out refinance transactions, subject to documentation and limits.

The practical distinctions

- An existing ADU with a signed lease is the strongest case.

- A planned rental with no tenant is weaker and program-dependent.

- A family-use ADU generates no qualifying income.

- A short-term rental is often not treated like long-term rent.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, lender guidelines, appraisals, and regulatory approvals.

No equity? Here’s your realistic prefab path

With little or no home equity, the realistic prefab ADU financing options narrow to a renovation or construction loan underwritten partly on the after-completion value, manufacturer-linked financing structured around the factory schedule, an active local program where one exists, or savings and partner capital. Home equity products — HELOCs, home equity loans, and home equity investments — all require existing equity, so they are not no-equity solutions. This is the hardest scenario in prefab financing, and we won’t pretend otherwise — but you still have moves.

- 1. Renovation and construction loans underwritten on finished value. Because HomeStyle Renovation, CHOICERenovation, FHA 203(k), and construction-to-permanent loans factor in what the property will be worth finished, they can reduce how much equity you need today. They don’t erase borrower requirements — you’ll still face LTV limits, cash-to-close, credit standards, and appraisals — but they’re the most realistic ground-up path for a low-equity owner. The new 50%-upfront-disbursement rule on HomeStyle Renovation (SEL-2025-10) makes them meaningfully more viable for prefab deposits than they were a year ago.

- 2. Manufacturer-linked financing. Built around the factory schedule and sometimes carrying lower equity requirements, this can be among the more accessible paths for a low-equity buyer — just confirm it covers site work, not only the unit, and compare the total cost.

- 3. An active local program, if one serves you (see below).

The truth about grants and the SUPPLY Act

We’ll be straight with you, because misinformation here wastes months and money:

- California’s CalHFA $40,000 ADU Grant is fully allocated and paused. CalHFA’s program page confirms the latest funding round was exhausted (the original $100 million ran out, and the program has not accepted new applications since roughly December 28, 2023), with no confirmed relaunch date — and CalHFA has even posted warnings about scammers claiming they can still secure the grant. You may see a stray blog claiming it’s “still going strong”; the weight of current evidence says it is not. Don’t build a plan around it. (Verified May 31, 2026.)

- San Diego homeowners have one notable live program. The San Diego Housing Commission (SDHC) ADU Finance Program offers up to $250,000 in construction-loan assistance plus no-cost technical assistance — but eligibility is specific: it’s for low-income homeowners in the City of San Diego, on an owner-occupied detached single-family residence, generally requiring a minimum credit score around 680 and roughly 75% maximum loan-to-value, with affordability restrictions for seven years. If you fit that profile, it’s worth checking. (Verified May 31, 2026.)

- The federal SUPPLY Act (H.R. 4568) would direct the FHA to insure second mortgages specifically for ADU construction, let Fannie Mae and Freddie Mac purchase and securitize them, and allow up to 50% of projected ADU rent to count toward qualification — squarely aimed at homeowners without enough equity. It was introduced July 18, 2025 by Reps. Sam Liccardo and Andrew Garbarino, is endorsed by the National Association of Home Builders, the Mortgage Bankers Association, and the Casita Coalition, and was referred to the House Financial Services Committee, where it remains — a proposal, not a program you can use today. (Verified May 31, 2026.)

The honest, useful frame: most grant programs are exhausted or narrow, and the federal bill is still pending — yet homeowners are building prefab ADUs every single day. They’re doing it with the financing lanes above, not with grants. Don’t wait for a program that may never arrive; build the plan around what exists now.

Affiliate link — we may earn a commission at no extra cost to you; it never affects our recommendations.

Explore ADU mortgage, refinance, and construction-loan options →

Financing-lane education for low-equity and finished-value paths. No guaranteed rates or approvals.

Explore financing options →Will a prefab ADU appraise — and is it really cheaper?

Modular and panelized ADUs that are permitted and permanently affixed generally appraise much like site-built construction; HUD-code manufactured units can appraise lower and limit your lender options. Prefab is often modestly cheaper per square foot on the unit, but once foundation, craning, utilities, and site work are added, the all-in total can approach site-built — prefab’s most reliable advantages are speed and price predictability, not always the bottom-line cost.

Will it appraise? For modular and panelized units treated under the IRC, generally yes — appraisers value them like comparable site-built ADUs, consistent with Fannie’s UAD 3.6 treatment. For HUD-code manufactured units, the appraisal can come in lower and fewer lenders participate, which is exactly why the real-property and foundation documentation matters so much. Whether an ADU adds enough value to “pay for itself” at resale depends heavily on your local market and comparable sales — ask a local appraiser or agent for ADU comps in your area rather than trusting a national rule of thumb.

Is it cheaper? Sometimes, modestly, on the unit itself — and the savings often shrink once you add site-specific hard costs. The reliable wins from prefab are speed (the factory build runs in parallel with site prep) and price certainty (a fixed unit contract reduces surprises). If your priority is maximum customization or squeezing the lowest possible all-in number on an easy lot, site-built can sometimes match or beat it. We’d rather you hear that now than after you’ve signed.

Edge cases worth a thought before you commit

- Selling mid-term. With an HEI, a sale triggers settlement; with an OTC loan, the construction phase has its own rules — confirm both before you sign.

- Owner-occupancy rules. Some jurisdictions require you to live on the property; this affects both zoning eligibility and some loan products. Confirm your local rule.

- Utility hookup surprises. Long trenching runs and panel upgrades are classic budget-blowers — get them quoted, not estimated.

- Crane access. A prefab unit has to physically reach your backyard. Tight lots, overhead wires, and long set distances add cost.

Documents to collect before you apply

A lender-ready prefab ADU file includes the all-in (turnkey) contract, the manufacturer’s payment schedule, unit specifications, the ADU construction classification, the foundation plan, permit status or path, the site plan, the utility scope, the contractor/manufacturer agreement, title and real-property documents (especially for manufactured units), and any lease or rent estimate if you plan to rent. Assembling this before you apply — and before you pay a deposit — prevents the most common prefab financing failures.

| Document | Why the lender needs it |

|---|---|

| All-in (turnkey) quote | Shows the total to finance, not just the unit price |

| Payment schedule | Reveals factory deposit and draw timing — the make-or-break detail |

| Unit specifications | Supports the appraisal and eligibility determination |

| ADU type / classification | Tells the lender whether to treat it as modular, manufactured, or site-built |

| Foundation plan | Supports permanence and real-property status |

| Permit or permit path | Confirms the project is a legal ADU |

| Site plan | Shows placement, setbacks, utilities, and access |

| Utility scope | Prevents under-budgeting on trenching and hookups |

| Contractor / manufacturer agreement | Shows who's responsible for which work |

| Title / real-property documents | Critical for manufactured ADUs |

| Lease or rent estimate | Only useful if the lender's program allows rental income |

| Insurance / warranty info | Supports collateral and project-risk review |

Seven questions to ask your lender before paying a prefab deposit

- Can this loan fund factory deposits before the unit is installed?

- Can it disburse design, permits, plans, materials, and deposits at closing? (Recall HomeStyle Renovation now allows up to 50% upfront.)

- Do you require inspections before each draw — and how do you handle off-site factory progress?

- Do you treat this as modular, manufactured, or site-built construction?

- Can the appraiser include the completed ADU value?

- Will the unit be encumbered as part of the real property?

- What documents do you need from the manufacturer?

Pair this checklist with a property feasibility report so you know your likely ADU size, path, and financing questions before you apply.

See What You Can Build → Get Your Free ADU Report

Bring the report and your all-in quote to a lender to map your financing path.

Get your free ADU report →What can go wrong with prefab ADU financing

The most common prefab ADU financing failures are financing only the unit’s sticker price instead of the all-in installed cost, paying a non-refundable deposit before the lender confirms it can fund the factory schedule, discovering the unit can’t be classified as real property, under-budgeting site work, and counting on rental income the lender hasn’t approved. Each is preventable with the documents and questions above.

- 1. Financing the sticker, not the all-in. You borrow $300,000 for a unit that becomes a $380,000 project. Mid-build, you’re short — and emergency money is the most expensive money.

- 2. Paying a non-refundable deposit before lender review. You commit 10% (or more) and then learn the lender can’t fund the schedule. Now you’re choosing between losing the deposit and scrambling for worse financing.

- 3. Assuming every prefab is treated like modular real estate. A “tiny home on a trailer” is not the same collateral as a foundation-set modular unit. Confirm classification first.

- 4. Ignoring site-work exclusions. Trenching, craning, demolition, engineering — the fine print is where budgets die.

- 5. Counting rental income before the lender confirms it. The Fannie change helps, but it’s for an existing ADU, capped at 30% of qualifying income, on specific transaction types. Don’t pre-spend it.

Honest dealbreakers — and where to go if you hit one

- • Unit can’t be permitted as an ADU → reconsider the product or location; start with a feasibility check.

- • Unit can’t be classified as real property → revisit the prefab classification section above and consider a different unit type.

- • No equity and a finished-value loan won’t stretch → see our no-equity ADU financing guide.

- • Cost is the blocker → compare options in our prefab ADU cost and cost-per-square-foot guides.

- • The whole point was rental income → run realistic numbers in our ADU rental income guide.

What to do before you pay a prefab ADU deposit

Before paying any prefab ADU deposit, get the full installed (turnkey) quote, confirm exactly what’s excluded, obtain the manufacturer’s payment schedule, identify the unit’s construction classification, verify permit and zoning feasibility, and ask lenders whether they can fund the factory payments on time. Sign only after both your financing and your deposit risk are clear. Done in order, the factory-deposit trap stops being a trap and becomes a checklist.

- 1.Get the all-in quote — turnkey, not the unit sticker.

- 2.Ask for the payment schedule — and map it against any loan’s draw schedule.

- 3.Identify the ADU type and code path — modular, panelized, manufactured, or other.

- 4.Confirm permit and zoning feasibility — is it even a legal ADU on your lot?

- 5.Ask lenders whether they can fund factory payments — use the seven questions above.

- 6.Compare financing paths — not by headline rate, but by which one funds your schedule.

- 7.Sign only when financing and deposit risk are clear — never the other way around.

The fastest way to start is to confirm what your lot can support, then bring that report and your all-in quote to a lender.

What homeowners are actually worried about

This box reflects language from homeowner forums and groups, gathered to understand the real questions behind prefab ADU financing. It is not a source for any financial, legal, or cost claim, and it is not a testimonial.

Homeowners aren’t just asking “what loan can I get?” They’re asking whether they can avoid refinancing, whether “100% financing” is real, whether a clean prefab quote will balloon once site work lands, and whether a lender will even understand the project before they risk a deposit. Every one of those questions has an answer above. As San Diego real-estate agent Sherry Chen put it to NerdWallet, the appeal of an ADU is often deeply personal — keeping aging parents or adult children close while the property helps pay for itself. The financing exists to make that possible; the trick is matching it to the factory’s clock.

What we verified (and when)

Verified May 31, 2026. Every factual claim about lender rules, costs, and program status on this page is sourced inline and summarized below. Provider prices and lender rules change; anything that requires individual confirmation is flagged in context.

| Claim category | Sources |

|---|---|

| Agency lending rules (ADU eligibility, rental income, renovation disbursement) | Fannie Mae Selling Guide (B3-3.8-01; B5-3.2-04 HomeStyle costs/escrow), Announcements SEL-2025-08 (Oct. 8, 2025) and SEL-2025-10 (Dec. 10, 2025), HomeStyle Renovation FAQ, and UAD 3.6 policy; Freddie Mac ADU/CHOICERenovation pages; HUD/FHA Mortgagee Letter 2023-17 |

| Consumer-protection framing for home equity contracts | Consumer Financial Protection Bureau (CFPB) — home equity contracts overview |

| Modular construction deposit/cash-flow mechanics | Construction Financial Management Association (CFMA) |

| Who ADU financing serves; ADU-specific second mortgages | Urban Institute (ADU financing barriers); corroborated via CNBC |

| Named prefab provider pricing and payment schedules | Abodu (abodu.com/pricing) and Samara (samara.com) published pages |

| Independent cost benchmarks | HomeGuide and Maxable (2026 data); national averages (industry data, 2025) |

| Government program status | CalHFA, San Diego Housing Commission (SDHC), and Congress.gov (H.R. 4568) |

| Voice-of-customer language | Homeowner forums and groups — used only to understand questions and objections, never as a source for any financial, legal, or cost claim |

Two items we flag for confirmation: current VA one-time-close construction availability (which tightened in 2025), and the exact unit/site-work split on any specific prefab contract (use the figures from your signed quote).

How we researched this guide

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder, and our editorial conclusions are never influenced by compensation.

We built this guide by reviewing official Fannie Mae, Freddie Mac, and FHA/HUD lending guidance first (including Selling Guide B3-3.8-01 and B5-3.2-04, Announcements SEL-2025-08 and SEL-2025-10, the HomeStyle Renovation FAQ, Fannie Mae’s UAD 3.6 policy, and HUD Mortgagee Letter 2023-17); then Consumer Financial Protection Bureau guidance on home equity contracts and Urban Institute analysis of ADU financing barriers; then named prefab provider pricing and payment-schedule pages (Abodu, Samara); then independent prefab cost benchmarks (HomeGuide, Maxable); and finally government program status via CalHFA, SDHC, and Congress.gov. We assembled the factory-payment-timing analysis, the deposit-gap calculation, and the modular-quote-vs-turnkey-total decoder ourselves from these sources. Homeowner forum and group discussions informed our understanding of the questions homeowners actually have, but were never used as a source for any financial, legal, cost, or zoning claim.

We separate three kinds of claims: regulatory facts (from agency and government sources), verified commercial facts (provider pricing and program terms, dated), and editorial conclusions (which path may fit which buyer — labeled as our judgment, based on the verified facts above).

This page is educational and is not financial, legal, tax, or lending advice. Loan eligibility, available products, rates, terms, rental-income treatment, appraisals, and approvals depend on your lender, credit profile, property, state, local regulations, and project documentation. We never quote specific rates, APRs, or payments as guarantees, and we never rank lenders by payout.

Refresh cadence: provider pricing and payment schedules monthly; agency lending rules quarterly and after major bulletins; HEI and partner state availability monthly; grant and federal-bill status quarterly. Last verified: May 31, 2026.

Frequently asked questions

- Can you get a loan for a prefab ADU?

- Yes, if the project meets the lender's property, code, appraisal, legality, and collateral requirements. Fannie Mae confirms ADUs can be financed with its Selling Guide loan products; the practical issue is matching the loan to the unit's construction type and the manufacturer's payment schedule.

- What is the best way to finance a prefab ADU?

- There's no single best way — there's the path that fits your equity, your current mortgage rate, and your factory deposit timing. Equity-rich owners often use a HELOC or home equity loan to keep a low first mortgage; low-equity owners often use a finished-value renovation or construction loan; and buyers facing a tight factory deadline may use manufacturer financing or a modular-experienced construction lender.

- Why is prefab ADU financing different from site-built ADU financing?

- The difference is payment timing, not loan type. A prefab manufacturer often requires most or all of the unit cost before delivery, while most construction loans release funds against on-site progress. Bridging that gap — with an equity product, a renovation loan that disburses upfront, or a modular-savvy construction lender — is the core challenge.

- Can I use a HELOC for a prefab ADU?

- Yes, if you have enough equity and qualify. A HELOC's advantage for prefab is that the cash is in your hands, so you can meet the factory deposit schedule without waiting on draws. The limits are your available equity (generally up to about 80% of current value) and a typically variable rate.

- Can I use a construction loan for a prefab ADU?

- Often — especially with a lender experienced in modular construction who writes factory deposits into the draw schedule and releases funds against a factory invoice. A generalist lender that only funds against on-site progress may not be able to pay the factory milestones.

- Can I use Fannie Mae HomeStyle Renovation for a prefab ADU?

- Yes. Fannie Mae allows HomeStyle Renovation to construct or install a new ADU on a one-unit property, and per its FAQ it can even cover a manufactured-home ADU when all manufactured-home requirements (including conversion to real property) are met. As of SEL-2025-10 (Dec. 10, 2025), it allows up to 50% of renovation costs to be disbursed upfront and removed the prior $50,000 manufactured-home renovation cap.

- Can Freddie Mac CHOICERenovation finance an ADU?

- Yes. Freddie Mac states CHOICERenovation may be used to add a new ADU or renovate an existing one, with its ADU requirements applying across Freddie Mac mortgage products.

- Can FHA 203(k) finance a prefab ADU?

- FHA's Standard 203(k) can finance certain ADU work — generally adding an attached ADU, or renovating an existing attached or detached ADU — under HUD Mortgagee Letter 2023-17, subject to FHA and lender rules. Because factory-built and manufactured units carry extra FHA requirements, confirm your specific unit type with an FHA-approved lender.

- Can I finance delivery, craning, foundation, utility hookups, and permits?

- Often, depending on the loan. Renovation and construction loans are designed to cover site work and soft costs; equity products (HELOC, cash-out refinance, HEI) give you cash you can apply to anything. Always confirm the loan covers the all-in scope, not just the unit.

- Is a modular ADU easier to finance than a manufactured ADU?

- Usually, yes. Modular and panelized ADUs built to the state building code (IRC) are generally treated like site-built construction once permitted and permanently installed. HUD-code manufactured ADUs require additional steps — permanent foundation, conversion to real property, title work, and HUD certification documentation.

- Can future ADU rent help me qualify?

- Sometimes, and the rules recently expanded. Fannie Mae (SEL-2025-08) allows rental income from an existing ADU on a one-unit principal residence on purchase and limited cash-out refinances, from one ADU, capped at 30% of total qualifying income. FHA and Freddie Mac have separate rules. Don't assume rent counts — especially from a not-yet-built unit — until your lender confirms it.

- Is the SUPPLY Act available yet?

- No. The federal SUPPLY Act (H.R. 4568), which would create FHA-insured second mortgages for ADU construction, was introduced in July 2025 and remains in the House Financial Services Committee. It is a proposal, not an available program, as of May 31, 2026.

- Should I pay a prefab deposit before applying for financing?

- Usually no. Confirm first that a lender can finance the unit type, the all-in scope, and the manufacturer's payment schedule. Paying a non-refundable deposit before lender review is one of the most common and costly prefab financing mistakes.

Get the free ADU Starter Kit →

The full roadmap in one place: permits, costs, a prefab deposit-timing checklist, and every document your lender will ask for.

Get the Starter Kit →Related reading on The Dwelling Index

- Compare all ADU financing options — the full overview for any ADU type.

- How much does a prefab ADU cost? — unit vs. turnkey totals, national ranges, and named provider data.

- How to finance an ADU with no equity — finished-value and low-equity paths in depth.

- Using a home equity loan or HELOC for an ADU — when second-position debt is the right call.

- ADU grants in 2026: verified programs by state — what’s actually funded, and what isn’t.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU Report