ADU Financing California: How to Pay for an ADU in 2026

ADU financing California starts with one fact most pages get wrong: there is no open statewide grant in 2026. California’s $40,000 CalHFA ADU Grant has been fully allocated since December 28, 2023, and is closed to new applications (CalHFA.ca.gov/adu, verified May 25, 2026). If you own a California home and you’re planning an ADU — a detached backyard unit, a garage conversion, or a junior ADU (a unit of 500 sq ft or less inside your existing home) — the realistic way to pay for it is home equity or a construction loan, sized to a build that typically runs $140,000 to $400,000+ in California metros. A handful of California cities still offer rebates, fee waivers, and below-market loans, and several state laws now cut your costs and widen your borrowing. Your fastest next step is to confirm what your lot allows, then match the financing lane to your equity and current mortgage rate.

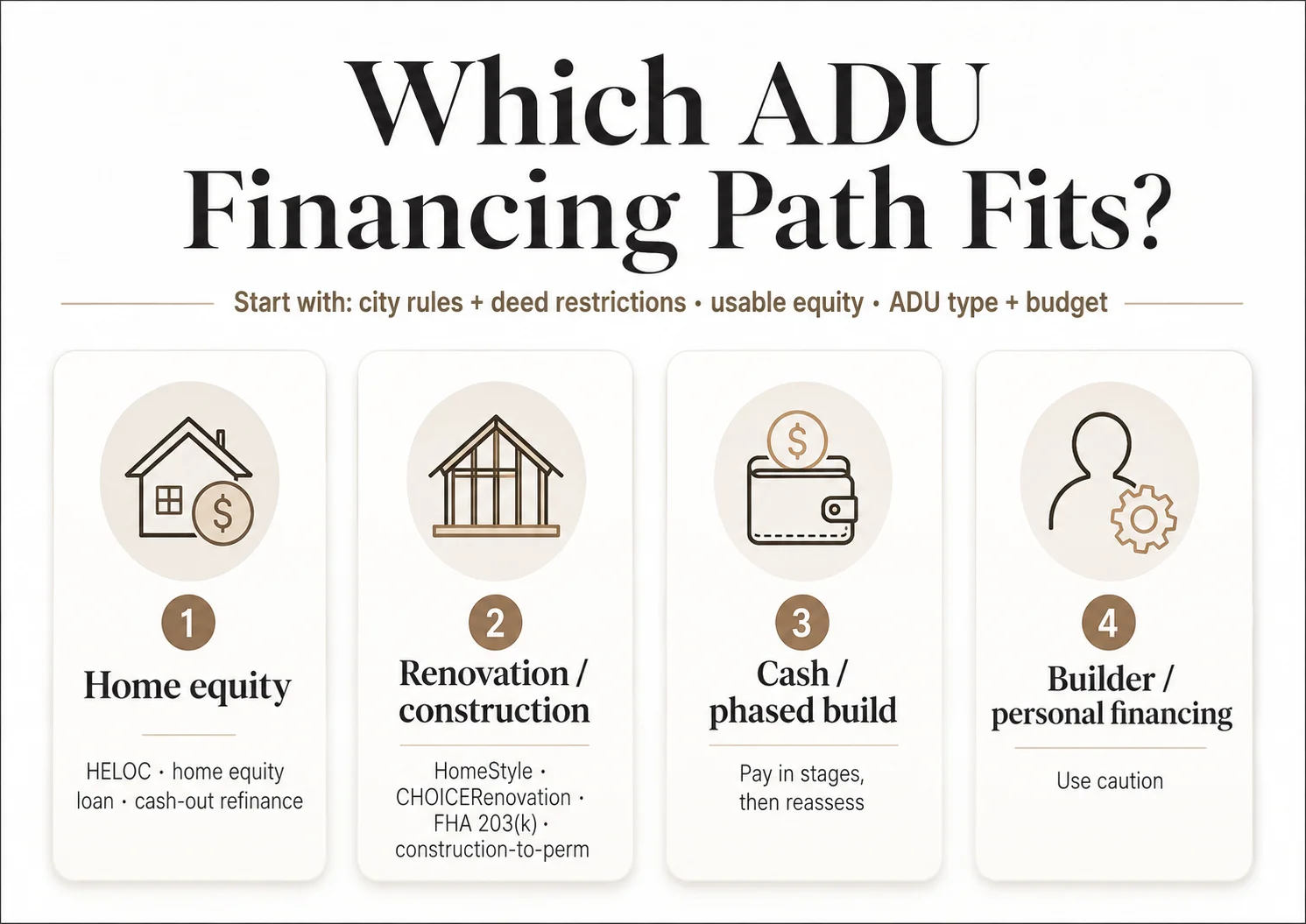

Match your situation to a lane:

| Your situation | First lane to test | Keeps your low mortgage rate? |

|---|---|---|

| Strong equity + a low (2020–2022) first mortgage | HELOC or home equity loan | ✅ Yes |

| Equity, but you want a fixed payment | Home equity loan | ✅ Yes |

| Not enough equity today; high value after the ADU | Construction or renovation loan | Depends on structure |

| City of San Diego, income-qualified | SDHC ADU Finance loan | n/a — program loan |

| Lower-income Long Beach owner, can rent affordably | Long Beach Backyard Builders loan | n/a — program loan |

| Can't take on a monthly payment | Home equity investment (confirm CA availability) | ✅ Yes |

See what you can build before you talk to a lender.

Setbacks, lot coverage, height limits, and local rules can change which financing path works — or whether you should borrow at all. Our free Feasibility Engine checks your address and returns a personalized ADU report in about 60 seconds. No phone call, no commitment.

See What You Can Build → Get Your Free ADU ReportHere’s the thing the grant-chasing pages bury: even when the CalHFA grant was open, it never paid for construction. It reimbursed soft costs — plans, permits, soil tests, impact fees — and capped at $40,000 against a six-figure project. That sounds like bad news. It’s actually freeing. Your ADU was never going to live or die on a government program. California homeowners build thousands of ADUs every year with ordinary financing, and the state has spent the last three legislative sessions making that easier — removing owner-occupancy rules, exempting smaller units from impact fees, and letting lenders count ADU rent toward your qualification. You have more room than you think.

This guide is the California-specific layer: the state and local money that actually exists right now, how California’s ADU laws change your financing and tax picture, and the lane to test first. For the full mechanics of how each loan type works — HELOCs, construction loans, the Fannie Mae rule, equity formulas, the keep-or-replace-your-mortgage math — we go deep in our ADU Financing Options Guide, and we point you there at each decision point rather than repeat it here.

ADU financing California: the quick answer

There is no special “California ADU loan.” Lenders fund California ADUs with the same standard products used nationwide, and the core mechanics don’t change at the state line. What does change in California is the money available to you and the laws that govern it — and that’s where this page earns its place.

| Path | Best when… | Keeps current mortgage? | California note |

|---|---|---|---|

| HELOC (revolving credit line secured by equity) | You have equity and a low first-mortgage rate | ✅ Yes | Strong fit for equity-rich owners protecting a low pandemic-era rate |

| Home equity loan (fixed lump sum, fixed payment) | You have equity and want payment certainty | ✅ Yes | Pairs well with a phased California build budget |

| Cash-out refinance (replaces your whole mortgage) | Your current rate is already at/above market | ❌ No | Rarely wins if you locked a 2020–2022 rate |

| Construction / construction-to-permanent loan | Low current equity, strong income, ground-up build | Depends on structure | Underwrites against after-completion value |

| Renovation loan (HomeStyle / CHOICERenovation / FHA 203(k)) | Buying + building, or low-equity refi-plus-build | ❌ No | FHA 203(k) is a fit for CA garage/attached conversions |

| California state/local program | Income-qualified in a participating city/county | Varies | Most are below-market loans or rebates with rent restrictions |

| Home equity investment (HEI) | You can't carry another monthly payment | ✅ Yes | Confirm the provider serves California before relying on it |

Definitions: A construction-to-permanent loan funds the build in inspected stages, then converts to a regular mortgage. A renovation loan bundles purchase or refinance with construction funding and underwrites against the home’s after-completion value. A home equity investment (HEI) gives you cash now for a share of your home’s future value, with no required monthly payment. Ministerial approval means staff approve against fixed standards, with no discretionary hearing.

Compare every financing path, with worked examples and the questions to ask any lender.

Our independent guide walks through all eight paths and the full keep-vs-replace-your-mortgage math — the deep version of the mechanics this page links out to.

Explore Your ADU Financing Options →Is there a grant to build an ADU in California in 2026?

The reason almost everyone searches for “ADU grant California” is the CalHFA program — and it is genuinely closed. CalHFA’s own page confirms its ADU funding was fully allocated and the reservation portal closed as of December 28, 2023, with no relaunch date announced (CalHFA.ca.gov/adu, verified May 25, 2026).

Two things are worth saying plainly, because they cost real homeowners real money.

First, be skeptical of any page telling you the grant is open. As of early 2026, multiple builder and zoning blogs still claimed the CalHFA grant was “still going strong into 2026” or “renewed with expanded funding.” CalHFA’s official page contradicts this directly. If you’re budgeting around a $40,000 grant based on a builder blog instead of the administering agency’s page, you’re planning around money that doesn’t exist. Our rule, and the one we’d urge on you: verify grant status on the administering agency’s official page, and check the date.

Second, the scam warning is official. CalHFA explicitly warns that anyone who approaches you offering to help you obtain an ADU grant is operating a financial scam, and asks that you report it to marketing@calhfa.ca.gov (CalHFA.ca.gov/adu, verified May 25, 2026). Federal grant-fraud guidance echoes the broader principle: legitimate government grant programs don’t ask you to pay an upfront fee to “release” free money (grants.gov grant-scam alerts).

For context that matters to your budget: CalHFA’s $40,000 reimbursed pre-development soft costs only — architectural plans, permit and plan-review fees, impact fees, soil tests, site surveys, energy reports, and in some cases a construction-loan interest-rate buydown. It never paid for framing, drywall, labor, materials, or utility hookups. The number that actually funds your ADU is the loan behind it.

For the national picture — every state’s grant, forgivable loan, and rebate, with status badges and sources — see our dedicated ADU Grants tracker.

Which California ADU programs are still open by city?

We assembled the California money picture below by checking each program against its official administering page. Every row carries a status badge and a verification date, because these open and close on funding cycles.

Status legend: ✅ Open · ⚠️ Limited (open but funding-constrained) · 📋 Waitlist / upcoming · ⛔ Closed

| Geography | Program | Type | Max | Status | The catch you need to know | Source · verified |

|---|---|---|---|---|---|---|

| California (statewide) | CalHFA ADU Grant | Grant (pre-development costs) | $40,000 | ⛔ Closed | Fully allocated since Dec 28, 2023; no relaunch; CalHFA warns of "grant help" scams | calhfa.ca.gov/adu · May 2026 |

| San Diego (City) | SDHC ADU Finance Program | Construction loan (repaid after construction) | Up to $250,000 | ⚠️ Limited | City of San Diego only; 3% fixed; max 75% LTV; ~680 min FICO; ~$2,500 fee at closing; income up to 80% AMI; 7-year affordable-rent restriction; loan must be repaid or refinanced after the build | sdhc.org · May 2026 |

| Long Beach | Backyard Builders (Round 2) | Below-market loan + free project management | Up to $250,000 | 📋 Opens Summer 2026 | 2% below-market rate, 30-year term, payments deferred for the life of the loan (or until sale/transfer); 0% during construction and affordability period, then 3% after; lower-income owner-occupants; lottery if oversubscribed | longbeach.gov/aduloan · May 2026 |

| East Bay (SD7 region) | SD7 ADU Accelerator | Rebate (sliding scale by size) | $7,500 base / $15,000 deed-restricted | ⚠️ Varies by city | Regional program across multiple Senate District 7 cities; higher tier requires an affordability deed restriction; reimbursement after final inspection | participating city pages · May 2026 |

| Dublin | ADU permit-fee waiver | Permit-fee waiver | ~$2,500–$6,000 savings | ✅ Open through Dec 31, 2026 | ADUs under 750 sq ft qualify; units 750 sq ft or larger qualify only if deed-restricted for lower-income households for 55 years; no short-term rentals | dublin.ca.gov · May 2026 |

| Lafayette | SD7 ADU Accelerator | Rebate | $7,500 / $15,000 | ✅ Open | Program period through Sept 30, 2026 (or until funds run out); $15,000 tier requires a 20-year affordability deed restriction; reimbursed after final inspection | lovelafayette.org · May 2026 |

| Walnut Creek | ADU Acceleration | Rebate | $7,500 / $15,000 | 📋 Waitlist | All rebates claimed as of July 15, 2025; backup list only; program period through Aug 31, 2026; low-income tier carries a 20-year deed restriction | walnutcreekca.gov · May 2026 |

The SD7 ADU Accelerator spans multiple East Bay (Senate District 7) jurisdictions — including Antioch, Brentwood, Clayton, Concord, Dublin, Lafayette, Livermore, Moraga, Oakley, Orinda, Pittsburg, Pleasanton, San Ramon, and Walnut Creek. Some cities add a local match — Antioch, for example, can raise the low-income deed-restricted rebate as high as $30,000. Terms differ by city; confirm with your jurisdiction.

How to read this honestly. Even the strongest programs here — San Diego’s and Long Beach’s up-to-$250,000 loans — are loans, not free money, and both are restricted to income-qualified owner-occupants who accept a multi-year affordable-rent requirement. The rebates are reimbursements you collect after you’ve paid. The fee waivers reduce permit costs but hand you no cash. None fund the bulk of a build. Treat any California local program as a discount on top of your real financing plan, not as the plan itself.

If you’re in Greater San Diego and weighing the SDHC program against simply building, it helps to get a real local cost picture first. San Diego County–focused builders such as SnapADU work across the county — San Diego, Chula Vista, Oceanside, Carlsbad, Escondido, El Cajon, Vista, and unincorporated San Diego County among them — and can frame what your specific project would actually cost before you decide whether a program’s restrictions are worth it.

Affiliate disclosure (repeated near comparison content): The Dwelling Index may earn a commission when you use our links to explore financing or request builder pricing, at no extra cost to you. We organize options by fit, never by payout. Full disclosure.

Find out which California program — if any — fits your address.

Eligibility turns on geography, income, and what you’re allowed to build. Our Feasibility Engine checks your lot’s rules and flags local program availability in one personalized report.

Check What’s Possible at Your Address →How most Californians actually finance an ADU

The single most expensive decision is whether to preserve your existing first mortgage. If you locked a rate during the 2020–2022 low-rate window, replacing it with a cash-out refinance to fund an ADU can cost more in additional lifetime interest than the ADU itself. The general guidance: if your current rate is well below today’s market, use a second-lien product — a HELOC or home equity loan — so only the new ADU money carries the higher rate, and your low first mortgage stays untouched. We run the full dollar math on this in the financing guide.

Rather than re-explain national loan mechanics, here is the California-specific decision table — match your situation to the lane to test first.

| If you’re a… | Your first lane to test | Why it fits in California |

|---|---|---|

| High-equity owner with a low first-mortgage rate | HELOC or home equity loan | Protects your sub-market rate; you borrow only the ADU money at today's rate |

| Owner with little equity now but high after-ADU value | Construction or construction-to-permanent loan | California's high values mean the after-completion appraisal often jumps enough to fund the build |

| City of San Diego owner, income up to 80% AMI | SDHC ADU Finance loan, then refinance | 3% fixed, up to $250K, plus free technical help — repaid or refinanced after the build |

| Lower-income Long Beach owner who can rent affordably | Long Beach Backyard Builders loan | 2% below-market, deferred payments, 0% while affordably rented |

| Owner with an existing ADU planning to rent it | Standard loan using ADU rental income to qualify | California removed owner-occupancy, so rent-to-qualify is practically usable here |

| Owner of a pre-2020 unpermitted ADU | Legalize first (AB 2533), then refinance | A legal unit becomes financeable; an unpermitted one is not |

A California-specific timing tip that saves weeks: under AB 1332 (effective 2025), every local agency must run a preapproved-plan program, and a detached-ADU application that uses a qualifying preapproved plan must be approved or denied ministerially within 30 days of a complete application (Gov. Code § 65852.27). That compresses the permit step lenders wait on — so start the construction-loan conversation before you submit for permit, not after.

Compare every ADU financing path, with worked examples.

Our ADU Financing Options Guide is the deep version of this section: all eight paths, the math, the document checklist, and the twelve questions to ask any lender.

Explore Your ADU Financing Options →How California’s ADU laws change your financing math

California has reshaped its ADU rules across the last several legislative sessions, and several of those changes quietly improve your financing position. The table decodes each law into plain English, then states the financing consequence.

Definitions: JADU = junior accessory dwelling unit, 500 sq ft or less, created within the existing home; owner-occupancy requirement = a rule that the owner must live on-site; impact fee = a one-time municipal charge to fund infrastructure serving new development.

| California law (effective date) | What it actually means | Why it changes your financing |

|---|---|---|

| AB 976 (chaptered Oct 11, 2023; operative Jan 1, 2024) | Permanently barred local agencies from imposing owner-occupancy requirements on non-junior ADUs. You can rent both your primary home and your ADU and don't have to live on the property. Local agencies may still require rental terms of 30 days or longer. | Removes a barrier to financing investment-oriented ADUs and makes rent-to-qualify practically usable (see the Fannie Mae rule below). |

| AB 1033 (effective Jan 1, 2024; opt-in) | Lets a local agency adopt an ordinance permitting the separate sale of an ADU as a condominium. It is opt-in — it applies only where the city or county has adopted an ordinance. | In an adopting jurisdiction, condo-conversion potential can change appraisal comparables and your exit math. See the verified city-status table below before relying on it. |

| AB 2533 (effective Jan 1, 2025) | Created a pathway to legalize certain unpermitted ADUs and JADUs built before January 1, 2020; agencies may still require corrections needed to address substandard health-and-safety conditions. | A legally permitted unit can be financed or refinanced; an unpermitted one cannot. Legalizing an old informal unit can be the single highest-return move available to an owner. |

| AB 1332 (effective 2025) | Every local agency must run a preapproved-plan program; a detached ADU using a qualifying preapproved plan must be approved or denied ministerially within 30 days of a complete application. | Compresses the permit step lenders depend on — start the lender conversation before permit submission so financing and approval move in parallel. |

| SB 1211 (effective Jan 1, 2025) | Allows up to eight detached ADUs on a lot with an existing multifamily dwelling — but not more than the number of existing primary units. Lots with a proposed multifamily dwelling remain limited to two detached ADUs. | Opens larger income-property financing scenarios for multifamily owners — a more complex lending conversation than a single backyard unit. |

| AB 1154 (effective Jan 1, 2026) | JADU owner-occupancy applies only when the JADU shares sanitation facilities with the main home; a JADU with its own bathroom no longer triggers owner-occupancy. | More JADUs escape owner-occupancy, widening rent-to-qualify scenarios. |

| SB 543 (effective Jan 1, 2026) | Sets JADU size at 500 sq ft of interior livable space and the impact-fee exemption threshold at 750 sq ft of interior livable space or less; measures by interior space, excluding exterior walls and stairs. | Interior-only measurement effectively gives you more usable square footage within the same cap, and the 750-sq-ft rule can erase thousands in fees (see below). |

Sources: California legislative text and official local pages — AB 976 (leginfo.legislature.ca.gov); AB 1154 (LegiScan); SB 543 (LegiScan); SB 1211 (summarized by Best Best & Krieger); AB 1332 (Gov. Code § 65852.27); AB 2533 implementation per San Diego County PDS. Verified May 25, 2026. The statutory facts are sourced to legislative text and official implementation pages; how any of them applies to your specific loan is our editorial framing, not legal advice.

Owner-occupancy is gone — here’s the financing payoff

Because AB 976 permanently removed owner-occupancy for non-junior ADUs, you can rent both units. That’s a financing lever, not just a lifestyle change. Lender rules now allow rental income from an existing ADU to help you qualify on eligible transactions — Fannie Mae automated this check in its Desktop Underwriter 12.1 release in March 2026. The qualifying calculation uses 75% of gross monthly rent, capped at 30% of your total qualifying income, on a one-unit principal residence with an existing ADU in eligible purchase or limited cash-out refinance transactions (Fannie Mae Selling Guide B3-3.8-01). Note that this is for an existing ADU — proposed or future ADU rent is treated differently and isn’t automatically countable. The full agency rules — including Freddie Mac’s CHOICERenovation limitation effective May 4, 2026, and FHA’s treatment under HUD Mortgagee Letter 2023-17 — are documented in our ADU Financing Options Guide.

These are illustrative examples, not guarantees of returns or qualification. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Which California cities have adopted AB 1033 (separate ADU sale)?

This is the law most often misreported online, so we verified it against official sources. AB 1033 does not automatically apply statewide — your city or county must opt in by ordinance (San José ADU Condominium Conversions; San Diego County PDS).

| Jurisdiction | AB 1033 status (verified May 2026) |

|---|---|

| San José | ✅ Adopted (Ordinance No. 31095, 2024); first condo sales closed Aug 2025 |

| City of San Diego | ✅ Adopted (Aug 2025) |

| Santa Monica | ✅ Adopted (early 2025) |

| City of Santa Cruz | ✅ Allows ADU condominium mapping |

| Unincorporated San Diego County | ✅ Adopted Mar 4, 2026; effective Apr 4, 2026 |

| Los Angeles (City & County) | ⛔ Not adopted as of early 2026 |

| Sacramento, Long Beach, Oakland, Berkeley | 📋 Studied / in process; not adopted |

Because adoption changes month to month, confirm your specific city’s status with its planning department before counting on a separate-sale exit. The conversion itself also carries real cost — condo map, CC&Rs, HOA formation, and lienholder consent — commonly estimated at $15,000–$40,000 in legal and filing fees.

Are California ADUs under 750 square feet exempt from impact fees?

This is one of the highest-value cost facts in California ADU planning, and it directly affects how much you need to finance. Impact fees — one-time municipal charges for parks, transportation, sewer capacity, and the like — can run into five figures on a larger unit. By keeping a detached ADU at or under 750 square feet of interior livable space, you can eliminate them entirely (SB 543 text, LegiScan). For a smaller backyard unit or a garage conversion, that’s thousands of dollars you simply don’t borrow. It’s also why SB 543’s switch to interior measurement matters: excluding exterior walls and stairs gives you more usable space under the same 750-square-foot ceiling.

The exemption does not cover utility connection fees or capacity charges, which are separate line items — so budget those independently. Confirm your city’s current fee schedule, since some jurisdictions layer additional local rules on top of the state floor.

Will an ADU raise your California property taxes?

This is one of the most common fears California homeowners bring to an ADU, and the answer is genuinely reassuring — though you should plan for it. The Santa Clara County Assessor’s office explains the mechanics clearly: your existing home is not reassessed, the new ADU construction is assessed at its market value, and that new assessment is simply added to your existing assessment; in a conversion, only the altered areas may be assessed.

So your tax bill rises — but by the ADU’s incremental value at your local rate, not by re-rating your whole property at today’s market value. On a unit that adds, say, $200,000 in assessed value, the incremental tax is your local rate applied to that $200,000 — meaningful, but a fraction of what people fear when they picture their entire home being reassessed. (Illustrative example only.) Rules and exemptions vary by county, and some areas carry additional Mello-Roos or special assessments, so confirm specifics with your county assessor.

This section is general context, not tax advice; consult a qualified tax professional.

What you’re actually financing: California ADU costs in 2026

Your financing amount is the whole game, so you need a realistic target before you pick a lane. The ranges below are planning ranges compiled from private California ADU cost sources — not statewide averages or quotes.

| Item | Typical 2026 California range | Source |

|---|---|---|

| Garage conversion | ~$140,000 – $250,000 | CALI ADU (Apr 2026); LADU |

| Attached ADU (500–1,000 sq ft) | ~$175,000 – $325,000 | LADU; BFPM (Apr 2026) |

| Detached new-build ADU | ~$225,000 – $400,000+ (LA: $219K–$459K) | BFPM; CALI ADU (Apr 2026) |

| Per square foot (metro CA) | ~$300 – $500 / sq ft (~$250 floor for large units) | GreatBuildz (Mar 2026); BFPM |

| City plan check + permit + fees | ~$5,000 – $20,000 (can be $0 impact fees under 750 sq ft per SB 543) | GreatBuildz (Mar 2026) |

| 2025 Energy Code compliance | ~$10,000–$20,000 for heat-pump + insulation + (often) solar | GatherADU (Apr 2026) |

Verified May 25, 2026. These are illustrative ranges, not quotes; actual cost depends on site conditions, scope, finishes, and local fees.

Two California realities most pages skip:

The energy code raises your up-front cost — and it’s the 2025 Energy Code, effective for permits submitted on or after January 1, 2026. Under California’s 2025 Energy Code, newly constructed detached ADUs generally must meet strict standards, and newly constructed detached ADUs require solar PV unless an exception applies; attached ADUs are treated as additions and do not require solar PV (California Energy Commission). Private builders estimate the heat-pump, insulation, and solar package can add roughly $10,000–$20,000 to a detached build. It lowers a tenant’s operating costs later, but you finance it up front.

Larger units are cheaper per square foot. California’s inspection and permitting burden is similar for an 800- and a 1,200-square-foot unit, so fixed costs spread over more space. If your lot and budget allow, a larger unit often produces a better cost-per-foot and a stronger after-completion appraisal — which directly improves your borrowing room on a future-value loan. The trade-off: stay at or under 750 square feet of interior space and you keep the impact-fee exemption. Run both scenarios.

For the full breakdown by type, region, and line item, see How Much Does an ADU Cost?. For modular and prefab pricing — often faster and sometimes lower-cost than site-built — modular options can be compared through providers like Modular Home Direct (national modular/prefab), or, for the Central Coast and Bay-Area-adjacent service area within roughly 150 miles of Monterey County, Framework First for California modular ADUs.

Set your borrowing target against your actual property.

Knowing the range is step one; knowing what your lot supports is step two. Get a personalized ADU report for your address before you size a loan.

Get Your Free ADU Report →Financing edge cases California homeowners actually hit

Low or no current equity

If your home’s value times 80%, minus your mortgage balance, doesn’t cover your ADU budget, no current-value product (HELOC, home equity loan, standard cash-out refi) will fully fund it. Your realistic paths are future-value loans — construction, construction-to-permanent, or renovation loans — that underwrite against the after-completion appraisal. They’re more involved (approved plans, contractor bids, draw schedules, inspections) and take longer to close, but in high-value California markets the after-completion jump often makes the math work. The step-by-step is in our financing guide.

A previously unpermitted ADU

Lenders and appraisers won’t finance a unit that isn’t legally permitted. California’s AB 2533 (effective January 1, 2025) created a pathway to legalize certain unpermitted ADUs and JADUs built before January 1, 2020, with agencies limited to requiring corrections needed for health and safety. Legalizing the unit first can convert it from unfinanceable into a refinanceable asset — often the highest-return move available to an owner who built informally years ago.

A non-owner-occupied or investment property

Because AB 976 permanently removed owner-occupancy for non-junior ADUs, you can build and rent on a property you don’t live in. But lender rules for investment properties are stricter — expect higher rates, larger down payments, and narrower product options (DSCR loans, portfolio products from regional banks and credit unions). The state law removes the occupancy barrier; it doesn’t soften the lending terms. If you’ll be renting the unit, a property-management platform like Buildium handles tenant screening, rent collection, and tax-ready records once you’re built.

No monthly payment

If another monthly payment isn’t feasible — common for retirees or owners housing an aging parent — a home equity investment (HEI) trades cash now for a share of your home’s future value, with no required monthly payment. The honest caveat: HEIs are state-limited, so confirm the provider serves California before relying on one, and over a long hold the cost of sharing appreciation can exceed traditional interest. We cover the trade-offs in the financing guide.

No path here is a dead end, but none is free of trade-offs — and pretending otherwise is how homeowners get blindsided mid-project. If a limitation applies to you, confirm feasibility first and pick the lane that fits your real constraints, not the one a single lender happens to sell.

What we verified for this guide

Source categories and verification (verified May 25, 2026):

- Grant and program status: CalHFA ADU Grant (calhfa.ca.gov/adu), San Diego Housing Commission (sdhc.org), Long Beach Backyard Builders (longbeach.gov/aduloan), and Dublin, Lafayette, and Walnut Creek official city pages.

- California ADU statutes: AB 976, AB 1154, SB 543, AB 1332 (Gov. Code § 65852.27), SB 1211, and AB 1033 implementation via San José and San Diego County official pages.

- California cost data: BFPM, CALI ADU, GreatBuildz, GatherADU, and LADU (Mar–Apr 2026 California cost guides), cross-checked across sources and labeled as private planning ranges.

- Energy code: California Energy Commission, 2025 Energy Code (effective for permits submitted on/after Jan 1, 2026).

- Property tax: Santa Clara County Assessor (Prop 13 ADU reassessment mechanics).

- Financing mechanics and agency rules: Fannie Mae Selling Guide B3-3.8-01, plus our ADU Financing Options Guide, which sources Fannie Mae, Freddie Mac, HUD, CFPB, and FTC primary documents.

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We do not originate loans, act as a broker, or sort financing options by compensation. We never quote rates as guarantees, never publish fake reviews or schema for content not on the page, and re-verify California program status monthly and statutes quarterly.

California ADU financing FAQ

Is the California ADU grant still available in 2026?

No. The CalHFA ADU Grant has been fully allocated since December 28, 2023, and is closed to new applications, with no confirmed relaunch date. CalHFA warns that anyone offering to help you access the grant for a fee is running a scam. Monitor CalHFA.ca.gov/adu for updates. (Verified May 25, 2026.)

How do most people pay for an ADU in California?

Most California ADUs are funded with home equity products (HELOC or home equity loan) or construction and renovation loans — not grants. Owners with strong equity and a low first-mortgage rate usually use a second-lien product to protect that rate; owners with less equity use a future-value construction or renovation loan.

Does building an ADU increase property taxes in California?

Usually only the ADU's added value is reassessed under Proposition 13, not your entire property. Your existing home keeps its protected base-year value; the county adds the market value of the new unit (or, in a conversion, the altered area). Budget the partial increase and confirm with your county assessor.

Can I use ADU rental income to qualify for a loan in California?

Sometimes. Because California removed owner-occupancy for non-junior ADUs, the rent-to-qualify path is usable here, and Fannie Mae automated ADU rental-income qualification in its March 2026 Desktop Underwriter 12.1 release — 75% of gross rent, capped at 30% of qualifying income, on a one-unit principal residence with an existing ADU in eligible transactions. Exact agency rules are in our financing guide. Illustrative, not a guarantee of qualification.

Are California ADUs under 750 square feet exempt from impact fees?

Yes. Under California law as updated by SB 543, local agencies, special districts, and water corporations cannot charge impact fees on ADUs of 750 square feet of interior livable space or less, or JADUs of 500 square feet or less. Larger ADUs are charged proportionally. The rule excludes utility connection fees and capacity charges.

Can I finance an unpermitted ADU in California?

Generally not until it's legalized. California's AB 2533 (effective January 1, 2025) created a pathway to legalize certain unpermitted ADUs and JADUs built before January 1, 2020, which can make a previously unfinanceable unit eligible for conventional financing or refinancing. Confirm eligibility against current statute and your city's process.

Is there a no-money-down ADU option in California?

There's no universal zero-down ADU loan. Future-value construction and renovation loans can fund a build with limited current equity by underwriting against after-completion value, and HEIs can avoid monthly payments (confirm California availability). Each carries stricter requirements than a standard HELOC.

How much does an ADU cost to build in California?

Roughly $225,000–$400,000+ for a detached new-build and $140,000–$250,000 for a garage conversion in 2026, at about $300–$500 per square foot in metros, plus 2025 Energy Code upgrades. Illustrative ranges, not quotes.

Can I sell my ADU separately in California?

Only in cities that have adopted an AB 1033 ordinance. As of spring 2026 that includes San José, the City of San Diego, Santa Monica, the City of Santa Cruz, and unincorporated San Diego County; Los Angeles and Sacramento had not adopted. Conversion involves a condominium map, CC&Rs, and an HOA, commonly $15,000–$40,000 in fees.

Which California cities offer ADU loans or grants right now?

The City of San Diego (SDHC, up to $250,000 at 3% fixed) and Long Beach (Backyard Builders, up to $250,000 at a 2% below-market deferred rate, opening Summer 2026) offer the most substantial below-market loans. East Bay cities including Dublin, Lafayette, and Walnut Creek offer fee waivers or rebates through the SD7 ADU Accelerator.

Is there a federal ADU grant for California homeowners?

No. There's no dedicated federal ADU grant for individual homeowners. Federal support is indirect — for example, agency policies that let ADU rental income count toward mortgage qualification — not direct cash. See our ADU Grants tracker.

What to do right now

If you want to know what your lot allows and which California rules apply to you — start there. Zoning, setbacks, lot coverage, and the 750-square-foot fee line all interact with financing before any lender does. Our Feasibility Engine returns a personalized ADU report for your address.

If you’re ready to compare loans — move to the full framework: every path, the keep-or-replace-your-mortgage math, and the questions to ask any lender, in our ADU Financing Options Guide.

If you want everything in one place — our free 2026 ADU Starter Kit packages the financing decision tree, the program checklist, and the loan-officer interview script as a download.

Free 2026 ADU Starter Kit

Checklists and tools we didn’t have room for here. No spam, free to download.

Download the Free 2026 ADU Starter Kit →Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.