From Dwelling Index, an independent research resource covering ADU financing, costs, and regulations.

The bottom line, up front:

There is no single, universal “Colorado ADU loan” that hands homeowners cash to build. A Colorado ADU loan almost always means one of seven financing paths — a HELOC, a home equity loan, a cash-out refinance, a construction-to-permanent loan, a renovation mortgage, state-backed CHFA financing delivered through a participating lender, or a local public program like Eagle County’s. Which one you should test first comes down to two things above all: how much equity you have, and whether you want to keep your current mortgage rate. Most Colorado ADUs run roughly $150,000 to $420,000 all-in (some detached Denver custom builds go higher), so many homeowners need a financing plan, not just a savings plan. The single most expensive mistake is choosing financing before you confirm your lot, your city’s rules, and your true total cost. Your next step: verify what your property can actually support, then match the financing lane to your situation.

If you’ve landed here, you’ve probably already pictured the ADU — an accessory dwelling unit, the legal term for a second, self-contained home on the same lot as your house. Maybe it’s a backyard cottage for your mom. Maybe it’s a garage conversion that finally makes the mortgage feel survivable. Maybe a neighbor broke ground and you thought, wait, I have a lot too. And then a number landed — a build quote, a lender’s offhand comment — and the dream hit the same wall it does for almost everyone in Colorado right now: how on earth do you pay for it?

That’s the real question behind “Colorado ADU loan,” and we’re going to answer it completely. Not with a generic list of loan types you could find anywhere, but with the Colorado specifics that actually change your decision: what the new state programs really do (and don’t), which city rules quietly raise the amount you need to borrow, and a plain framework for picking your first path. We verified every program, legal, and fee claim against primary state, agency, and city sources, and we date-stamped all of it. Let’s get you oriented.

Run the Colorado ADU Financing Path Finder → See your first path to test.

Answer a few questions about your equity, mortgage rate, city, ADU type, and goals, and we’ll point you to the financing lane to test first, the strongest backup, and the city-specific blockers to verify before you apply. You get your personalized result on the tool.

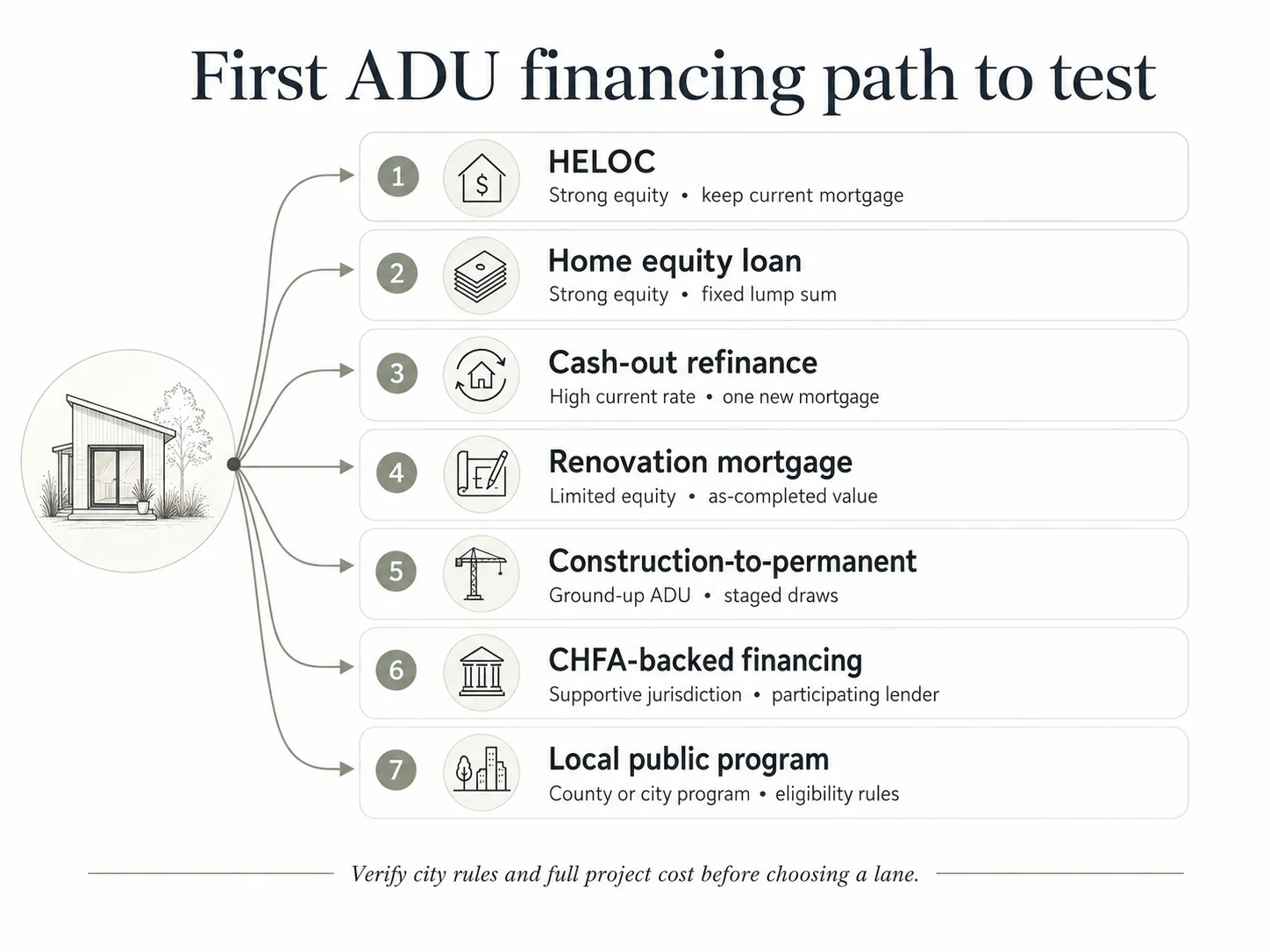

Start the Path FinderFirst Colorado ADU loan to test, by situation

Answer capsule: The best first financing path for a Colorado ADU depends on your equity, your current mortgage rate, the ADU type, your city’s rules, and whether documented rental income can help you qualify. Homeowners with strong equity who want to keep a low first mortgage typically start with a HELOC or home equity loan; those with limited equity often need a renovation or construction loan that lends against the home’s as-completed value; income-eligible owners in a DOLA-certified ADU Supportive Jurisdiction should check CHFA-backed and local programs before assuming private financing is the only option.

Here’s the whole decision on one screen. Find the row that sounds like you, then read that path’s full breakdown below.

| Your situation | First path to test | Why it fits | Watch out for |

|---|---|---|---|

| Strong equity, want to keep your current first mortgage | HELOC or home equity loan | Adds borrowing without touching your existing mortgage rate | Variable rates (HELOC), draw limits, payment shock when repayment begins |

| Limited equity but a strong, well-scoped project | Renovation or construction-to-permanent loan | Can lend against the home’s as-completed value, not just today’s equity | More paperwork, appraisals, and inspection-based draws |

| You already have a high mortgage rate | Cash-out refinance | Rolls everything into one mortgage, possibly at a better rate | Resets your entire first mortgage — a poor move if your rate is low |

| Low-to-moderate income in an ADU Supportive Jurisdiction | CHFA-backed financing via a participating lender | May lower your rate or improve access through state support | Not a direct homeowner grant; income limits and jurisdiction rules apply |

| Planning a long-term rental | A mortgage path that can document ADU rental income | Some agency rules now allow ADU rent toward qualifying | Caps (Fannie Mae’s 30% rule), documentation, legality, appraisal support |

| Counting on short-term rental income | Verify your city’s rules before anything | Some cities restrict short-term rentals on ADU lots | Boulder and Colorado Springs limit ADU short-term rentals |

Cost ranges and city-rule sources are cited in the relevant sections below. Last verified May 26, 2026.

See What You Can Build → Get Your Free ADU Report.

Confirm your lot’s ADU potential before sizing a loan.

Is there a Colorado ADU loan or grant in 2026?

Answer capsule: As of May 2026, Colorado does not offer a single statewide “ADU loan” that pays homeowners directly. The state’s ADU finance ecosystem, created by House Bill 24-1152, includes CHFA-administered programs that support lenders (through credit enhancement, interest-rate buydowns, down-payment assistance or principal reduction, and loans to nonprofits and CDFIs), a separate DOLA grant program for local governments, and local programs such as Eagle County’s Aid for ADUs (loans up to $150,000). For a homeowner, the practical question is not whether a Colorado ADU loan exists, but which public or private lane fits your property, city, income, and intended use.

This is the most misunderstood part of ADU financing in Colorado — so let’s decode it carefully. There are really three separate things people lump together when they say “the Colorado ADU program,” and they work very differently.

What Colorado’s ADU law (HB24-1152) actually changed

Answer capsule: Colorado House Bill 24-1152, signed in May 2024, requires “subject jurisdictions” to allow at least one ADU as an accessory use to a single-unit detached dwelling, through an administrative approval process, on or after June 30, 2025. Under the statute, a subject jurisdiction is generally a municipality with a population of 1,000 or more within a metropolitan planning organization, or the portion of a county that is both within a census-designated place of 40,000 or more and within a metropolitan planning organization. The law also created funding structures — a grant program for local governments and a financing program administered by CHFA — but it did not create a universal homeowner loan.

The law (codified at C.R.S. § 29-35-401 through 405) does several practical things. It forces subject jurisdictions to permit one ADU wherever single-family detached homes are allowed, using administrative approval — meaning a planner checks your plans against objective standards, rather than a discretionary public hearing. On or after June 30, 2025, it bars subject jurisdictions from enacting or enforcing local laws that restrict ADU construction or conversion. In practice that generally means a subject jurisdiction may not require a new off-street parking space for an ADU (with narrow exceptions the statute preserves), may not impose blanket owner-occupancy requirements (subject to limited exceptions tied to short-term-rental and application rules), and may not apply restrictive design or dimension standards. Local authority over impact fees, historic-district procedures, and short-term-rental laws is preserved. (Source: Colorado General Assembly, HB24-1152; C.R.S. § 29-35-403. Verified May 26, 2026.)

What the law does not do is write you a check. The money lives in two separate programs.

What CHFA’s ADU Finance Programs really do — and the part everyone gets wrong

Answer capsule: Under HB24-1152, the state authorized $8 million for the Colorado Economic Development Commission to contract with the Colorado Housing and Finance Authority (CHFA) to operate ADU finance programs for low- and moderate-income residents of supportive jurisdictions. The statute authorizes four tools: credit enhancement that supports lenders offering affordable loans, interest-rate buydowns, down-payment assistance or principal reduction, and loans or revolving lines of credit to nonprofits, public housing authorities, and Community Development Financial Institutions (CDFIs) who then lend to homeowners. Critically, this money flows to lenders and intermediaries — not directly from CHFA to homeowners.

Here is the mechanism, decoded — and it’s the single fact most competing pages get wrong. You don’t apply to CHFA for an ADU loan. The $8 million backs the lenders, nonprofits, and CDFIs who then make affordable loans to eligible borrowers. To benefit, you must be income-eligible (the programs target low- and moderate-income borrowers) and located in a supportive jurisdiction — a city or county that DOLA has certified. (Source: Colorado General Assembly, HB24-1152, Sections 3–4; CHFA ADU Finance Programs page; OEDIT Accessory Dwelling Unit Finance Program page. Verified May 26, 2026.)

CHFA announced its ADU finance programs in late 2025, and the borrower-facing pieces are rolling out through participating lenders during 2026. Because the exact rollout dates can shift, confirm current status directly on CHFA’s ADU Finance Programs page before building a plan around it.

How to check whether your city is an ADU Supportive Jurisdiction

Answer capsule: A supportive jurisdiction is a local government that DOLA has certified for complying with HB24-1152 and adopting one or more ADU-supportive strategies. Certification is what makes a jurisdiction’s residents eligible for CHFA’s homeowner-facing ADU financing. You can confirm your city or county’s status through DOLA’s Division of Local Government ADU pages or by asking your local planning department directly.

Two quick questions resolve this. Ask your planning department: “Is our jurisdiction a subject jurisdiction under HB24-1152, and is it a DOLA-certified ADU Supportive Jurisdiction?” The first tells you whether the state’s by-right ADU allowance applies to you; the second tells you whether CHFA-backed financing can reach you. As of October 3, 2025, DOLA reported that 82% of the local governments subject to the ADU law were compliant or pursuing compliance, with additional jurisdictions voluntarily opting in. (Source: DOLA Division of Local Government; Governor’s Office press release, November 2025. Verified May 26, 2026.)

What DOLA’s grant program does — and why it’s not for you directly

Answer capsule: DOLA runs the Accessory Dwelling Unit Fee Reduction and Encouragement Grant Program, funded by a $5 million transfer under HB24-1152. It awards grants to local governments — not homeowners — to develop pre-approved ADU plans, provide technical assistance, and waive, reduce, or offset ADU-associated fees. A jurisdiction must be a DOLA-certified supportive jurisdiction to receive these grants.

This is a separate pot of money from the $8 million CHFA financing program, and conflating the two is the most common error you’ll see online. DOLA’s grant money helps cities lower the systemic costs of building ADUs — pre-approved plans, fee reductions — which can indirectly save you money. But you can’t apply for it as a homeowner. DOLA directs residents interested in financing to contact CHFA at askchfa@chfainfo.com. (Source: Colorado General Assembly, HB24-1152, Section 1; DOLA ADU Grant Program page. Verified May 26, 2026.)

So, is the state program real? Yes — it’s real and active in 2026. But it works through your jurisdiction and your lender, not as a check from the state. Before you build a plan around it, confirm your city is a certified supportive jurisdiction and that you’re within the low-to-moderate income targets.

Why a local program might matter more than the statewide ones

Answer capsule: Some Colorado counties run their own ADU loan programs that can be more generous than statewide options for the right homeowner. Eagle County’s Aid for ADUs program offers up to $150,000 as a loan, requires a 15-year deed restriction, requires leasing to an eligible local household earning no more than 100% of Area Median Income (AMI), and strictly prohibits short-term rentals.

If you live in a resort or mountain county, check your county housing authority first. Eagle County’s program is the clearest example: a substantial local loan, but with strings — you generally must rent to a qualifying local worker at restricted rates, and you can’t run it as a short-term rental. (Source: Housing Eagle County, Aid for ADUs. Verified May 26, 2026.) That’s an excellent deal for a homeowner who wants stable long-term tenants and a poor fit for someone banking on nightly-rental income. Exactly the kind of trade-off you want to know before you borrow.

Public program not a fit? Explore your ADU mortgage and home-equity options.

Explore ADU mortgage and home-equity options →Which Colorado ADU loan path should you test first?

Answer capsule: The first financing path to test depends on five questions: whether your property can legally support the ADU type you want, how much equity you have, whether your current mortgage rate is worth preserving, what kind of ADU you’re building, and how you plan to use it. Equity-rich owners with a low first mortgage often start with a HELOC; equity-light owners typically need a renovation or construction loan that uses as-completed value; income-eligible owners in supportive jurisdictions should check CHFA-backed financing first.

Run yourself through the fork before reading each path. Your answers narrow seven options to one or two fast.

The five-question financing fork

- Can your property legally support this ADU type? Detached, attached, garage conversion, basement, or prefab — each triggers different city rules and costs.

- How much equity do you have? Roughly: your home’s value minus what you still owe.

- Is your current mortgage rate worth protecting? If you locked 3% in 2021, almost certainly yes.

- What is the ADU — and how big? A $90,000 garage conversion and a $380,000 detached build call for completely different financing.

- How will you use it? Family, long-term rental, or another use — this affects both qualifying income and city legality.

Now the seven paths. We present these as financing lanes, not ranked lenders — we don’t rank by anyone’s compensation, and we never promise rates or approval.

Path 1: HELOC (home equity line of credit)

A HELOC is a revolving line of credit secured by your home — like a credit card backed by your equity, with a “draw period” (often 10 years) where you borrow as needed and typically pay interest only, followed by a repayment period of principal and interest. Best for: owners with solid equity who want to keep their existing first mortgage untouched and like drawing funds as construction bills arrive. The honest catch: most HELOCs carry variable rates tied to the Prime Rate, so your payment can move, and a large detached ADU may exceed what your available equity supports. Lenders generally want you to retain meaningful equity after the draw. Some Colorado lenders market ADU-relevant equity products — Urban ADU, for example, describes a Community Banks of Colorado HELOC and a second-position renovation/construction term-loan option for ADU projects; confirm current terms directly with the lender. (Source: Urban ADU finance options page; Community Banks of Colorado home-equity page. Verified May 26, 2026.)

Path 2: Home equity loan (HELOAN)

A home equity loan is a second mortgage that gives you a single lump sum at a fixed rate, repaid on a set schedule. Best for: owners who know their total budget up front and prefer predictable fixed payments over a variable line. The honest catch: you take the whole amount — and start paying interest on all of it — immediately, even if construction spans many months. Less efficient than a HELOC’s draw-as-you-go for a long build.

Path 3: Cash-out refinance

A cash-out refinance replaces your existing first mortgage with a new, larger one and hands you the difference in cash to fund the ADU. Best for: owners whose current mortgage rate is higher than today’s market, so refinancing improves their terms while funding the build. The honest catch — and it’s a big one in Colorado: if you have a low pandemic-era rate, a cash-out refi resets your entire mortgage at today’s higher rate. That’s the “low-rate trap,” and it’s why we steer most Front Range homeowners who bought before 2022 toward second-position options instead.

Path 4: Construction-to-permanent loan

A construction-to-permanent loan is a single loan that funds the build through scheduled “draws” — releases of money tied to inspection milestones — then converts to a standard permanent mortgage when the ADU is finished. Best for: larger detached or new-build ADUs where cost exceeds available equity and the project needs structured funding. The honest catch: more documentation, appraisals, inspections, and lender oversight than an equity product, and often a higher rate during the construction phase.

Path 5: Renovation mortgage (the equity-light homeowner’s friend)

A renovation mortgage lets you borrow against your home’s after-renovation value — its estimated worth once the ADU is built — rather than just today’s equity. This category includes Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, and FHA 203(k) products. Fannie Mae confirms that its Selling Guide products can be used to purchase a home with an ADU, renovate, or add an ADU, including HomeStyle Renovation and construction-to-permanent structures. Best for: owners who bought recently and don’t yet have much equity, or who need the future value to make the numbers work. The honest catch: the loan amount hinges on an appraiser’s projection of as-completed value, and the documentation is heavier than an equity product. (Source: Fannie Mae, Accessory Dwelling Units product page. Verified May 26, 2026.)

One note on a product you’ll see advertised: renovation-focused HELOCs that lend against after-renovation value exist, but availability, lender participation, property eligibility, and state coverage should be checked before you rely on them.

Path 6: CHFA-backed or local public program

Covered in detail above. Best for: low-to-moderate income homeowners in a DOLA-certified supportive jurisdiction, or anyone in a county with its own program (like Eagle County). The honest catch: eligibility is restricted by income, jurisdiction, and often use (workforce or long-term-rental requirements), and the homeowner-facing CHFA pieces are still rolling out through 2026.

Path 7: Cash or hybrid funding

Many real Colorado ADU projects don’t use one neat loan — they stack sources. Best for: owners who can pay for design and permits in cash, then finance construction; or who combine a HELOC for early phases with a construction loan for the build. The honest catch: more moving parts, and you need to sequence draws carefully so you’re never paying interest on money you’re not using yet.

Here’s the full comparison assembled in one place — something you’d otherwise have to build yourself across half a dozen lender and builder sites.

Seven Colorado ADU financing paths compared

| Path | Preserves your existing first mortgage? | Can use as-completed (future) value? | Best fit | Primary watch-out |

|---|---|---|---|---|

| HELOC | Usually yes | Usually no | Strong equity, flexible draws, keep low first mortgage | Variable rate; payment shock at repayment |

| Home equity loan (HELOAN) | Usually yes | Usually no | Known budget, wants fixed payments | Interest on full sum from day one |

| Cash-out refinance | No | Based on current value | High existing mortgage rate | Resets entire mortgage — avoid if your rate is low |

| Construction-to-permanent | Not always | Often yes | Larger detached / new-build ADUs | Draws, inspections, more paperwork |

| Renovation mortgage | Varies | Often yes | Limited equity; ADU added via renovation scope | Hinges on appraised future value |

| CHFA-backed / local program | Varies | Varies | Income-eligible owners in supportive jurisdictions | Restricted by income, jurisdiction, and use |

| Cash / hybrid | Yes (if no new lien) | N/A | Owners stacking multiple funding sources | Complex sequencing |

Assembled from CHFA/OEDIT program materials, HB24-1152, Fannie Mae product guidance, and lender product disclosures. Educational only — not a lender ranking and not financial advice. Verified May 26, 2026.

Compare ADU mortgage and home-equity options → Explore your financing paths.

Explore financing paths →How much should you plan to borrow for a Colorado ADU?

Answer capsule: Most Colorado ADUs cost roughly $150,000 to $420,000 all-in. By size, Olerra’s Colorado cost guide reports about $150,000–$240,000 for a 245-square-foot studio, $220,000–$300,000 for a ~490-square-foot one-bedroom, and $300,000–$420,000 for a ~735-square-foot two-bedroom; some custom Denver-area detached builds run higher. A right-sized ADU loan must cover design, permits, utility work, site work, construction, city fees, and a contingency — not just the contractor’s construction bid.

A surprise that catches almost everyone: ADU cost does not scale neatly with square footage. A tiny ADU still needs a full kitchen, a bathroom, electrical service, and utility connections — the expensive parts — so per-square-foot cost actually rises as units shrink. An older national ADU cost dataset (heavily Portland-based, useful for the fixed-cost dynamic rather than current Colorado pricing) pegged the per-square-foot range at $162–$682, averaging about $305/sq ft. (Source: BuildinganADU.com dataset — older/national; cited for cost dynamics, not Colorado benchmarking.)

Colorado ADU cost ranges by type and size

| ADU type / size | Planning range to budget | Financing implication | Source (verified May 26, 2026) |

|---|---|---|---|

| Garage conversion | ~$100,000–$130,000 | May fit a HELOC or contained renovation loan | Denver Dream Builders (Denver) |

| Small detached / studio (~245 sq ft) | ~$150,000–$240,000 | Equity may cover it; still verify site & utilities | Olerra Colorado ADU cost guide |

| Mid-size detached (~490 sq ft, 1-BR) | ~$220,000–$300,000 | A HELOC alone may fall short; compare renovation/construction | Olerra Colorado ADU cost guide |

| Larger detached (~735 sq ft, 2-BR) | ~$300,000–$420,000 | Construction-to-permanent or hybrid often needed | Olerra Colorado ADU cost guide |

| Detached, ~900 sq ft, well-designed (Denver) | ~$350,000–$450,000 (premium higher) | Detailed scope, contingency, and utility budget required | Denver Dream Builders (Denver) |

An honest note on the numbers: sources disagree, and that disagreement is itself useful. The gap reflects site conditions (alley access, sloped lots, century-old utility lines), finish levels, and whether your design fights local geometry rules. Budget toward the higher end if your lot is tight, your alley is complicated, or you want anything beyond builder-grade finishes.

The Colorado fee-and-utility costs that quietly raise your loan amount

Answer capsule: City review fees and utility connection charges can add tens of thousands of dollars beyond construction. Fort Collins states that its Basic Development Review fee is $6,925 and that total ADU fees often reach $20,000–$25,000. In Denver, Denver Water confirms that adding an ADU may require a new water supply license and an additional System Development Charge to run water service to the unit. Detached ADUs frequently need separate utility connections, which is among the largest hidden costs.

These are the line items that blow up budgets after the loan is already sized. Plan for them up front:

- Plan review and permit fees — Fort Collins reports total ADU fees frequently reaching $20,000–$25,000, with a Basic Development Review fee of $6,925. (Source: City of Fort Collins ADU page.)

- Water/sewer connection (“tap”) charges — Denver Water confirms an ADU may need a separate water supply license plus an additional System Development Charge; check Denver Water’s current SDC schedule for the dollar amount that applies to your application date. (Source: Denver Water, Accessory Dwelling Units.)

- Parking replacement — if a garage conversion eliminates required off-street parking, you may have to rebuild it elsewhere on the lot, which Denver builders estimate at roughly $10,000–$30,000.

- Site work — grading, tree removal, and utility laterals (the underground lines connecting your ADU to water, sewer, and electric) add cost on difficult lots.

Our rule of thumb for early loan sizing: add at least a 10–15% contingency on top of your best total-cost estimate unless your builder, lender, and city review give you a concrete reason to use a different number.

Illustrative-planning disclaimer: These are planning ranges, not quotes, loan offers, or guarantees. Actual costs depend on site conditions, design, contractor pricing, utility requirements, and local approvals.

For a full city-by-city construction-cost breakdown, see our companion guide on the full city-by-city construction-cost breakdown.

See what your lot can support before you price a loan → Get your free ADU report.

Which Colorado city rules can change your loan amount?

Answer capsule: Colorado’s HB24-1152 opens the door statewide, but individual city rules — size caps, utility and fee requirements, parking, wildfire-overlay restrictions, and short-term-rental rules — can materially change your ADU’s cost and the loan you need. Denver expanded citywide ADU eligibility effective December 16, 2024; Boulder dropped owner-occupancy on March 8, 2025, but restricts short-term rentals; Fort Collins reports total fees of $20,000–$25,000; and Colorado Springs uses administrative review while restricting short-term rentals on ADU lots after June 30, 2025.

This is where a national financing page can’t help you. Here’s what changes the math in the major Front Range markets.

Denver

Answer capsule: Denver’s citywide ADU text amendment expanded ADU eligibility across residential zone districts and took effect December 16, 2024, allowing ADUs with administrative approval in many residential zones. More Denver properties are now eligible, but height, bulk-plane, setback, and placement standards vary by zone and lot, and Denver Water charges a separate System Development Charge — so verify your property’s exact zone standards before assuming a detached or two-story ADU will fit.

Denver allows ADUs through administrative approval (no discretionary public hearing) in eligible residential zones. Don’t assume a single universal height or placement rule, though — Denver’s zone-specific standards for setbacks, height, and bulk plane (the angled envelope that limits how tall a structure can be near property lines) differ by district, and they drive structural engineering complexity. Builders also report that permit review can run several months in practice even though approval is administrative; treat that as a builder-reported timeline, not a legal rule. (Source: City and County of Denver, Citywide ADUs; Denver Water; Denver builder guides. Verified May 26, 2026.)

Boulder

Answer capsule: As of March 8, 2025, Boulder no longer requires owner-occupancy for ADUs and reviews them through the building-permit process. Boulder generally prohibits short-term rental use (stays under 30 days) of either the ADU or the main house unless both the ADU and a short-term-rental license were established before February 1, 2019. Detached ADU size limits and fire-sprinkler requirements can apply and affect your budget.

Boulder is now friendlier for long-term rental and family use than for nightly-rental strategies. If your plan depends on short-term-rental income, Boulder will likely break it unless you hold that pre-2019 grandfathered status. Size caps and sprinkler requirements are the budget items to confirm before sizing a loan. Note that modular ADUs still require local permits and must comply with local codes and zoning. (Source: City of Boulder, Accessory Dwelling Units. Verified May 26, 2026.)

Fort Collins

Answer capsule: Fort Collins allows ADUs across its zone districts when property requirements are met, but size caps, utility requirements, stormwater, and review fees add up — the city states its Basic Development Review fee is $6,925 and that total ADU fees often reach $20,000–$25,000. Detached ADU size is capped relative to the primary home, ADUs generally require their own electric meter, and stormwater treatment can be triggered by new impervious surface.

Translation for your loan: in Fort Collins, build the fee-inclusive budget before you shop financing, because review and utility-related costs alone can shift your borrowing need by $20,000 or more. Confirm the current detached-ADU size cap and stormwater threshold with the city for your specific lot. (Source: City of Fort Collins ADU page. Verified May 26, 2026.)

Colorado Springs

Answer capsule: Colorado Springs adopted an ADU ordinance aligning with HB24-1152 (Colorado Springs Code § 7.3.304) that allows ADUs where single-family detached homes are permitted, using administrative approval with posted notice. Current code generally limits most lots to one ADU, requires the owner to demonstrate residence on the property when applying unless the ADU is built simultaneously with the primary dwelling, requires an additional off-street parking space, restricts detached and attached ADUs in the Wildland-Urban Interface overlay (while integrated ADUs may be allowed), and caps ADU size. Short-term rental use on ADU lots is restricted after June 30, 2025 unless grandfathered.

The practical takeaways for financing: a short-term-rental pro forma is risky here, parking and wildfire-overlay rules can change feasibility, and adequate water/wastewater capacity is required. An ADU approval may be appealable under the city’s Unified Development Code. Confirm the current parking, size, height, and overlay rules against § 7.3.304 for your parcel before sizing a loan. (Source: City of Colorado Springs Code § 7.3.304. Verified May 26, 2026.)

Aurora

Answer capsule: Aurora’s ADU regulatory status requires direct verification before you rely on it for loan sizing. The city has worked through HB24-1152 compliance updates that have been subject to council debate, so confirm current ADU allowances with Aurora’s planning department rather than assuming a specific rule.

If you’re in Aurora, call the planning department and confirm current ADU allowances before sizing a loan. (Source: Engage Aurora zoning-update materials. Status requires direct municipal-code verification, May 26, 2026.)

Colorado ADU city financing friction matrix

| City / county | Key rule that affects financing | What it does to your budget or loan |

|---|---|---|

| Denver | Administrative approval; zone-specific height/bulk-plane/setbacks; Denver Water SDC | More lots eligible; engineering + utility costs raise total; verify zone standards |

| Boulder | No owner-occupancy (since 3/8/2025); STR banned <30 days unless ADU + license predate 2/1/2019; sprinklers/size caps | Underwrite long-term rent only; sprinklers add cost |

| Fort Collins | Allowed across zones; fees often $20K–$25K total; separate electric meter; stormwater threshold | Build fee-inclusive budget before loan shopping |

| Colorado Springs | § 7.3.304: one ADU/lot; owner-residence at application; +1 parking space; WUI overlay limits; STR restricted after 6/30/2025 | STR pro formas risky; confirm parking, WUI, water/wastewater |

| Aurora | Compliance status contested — verify directly | Confirm current allowances before borrowing |

| Eagle County | Aid for ADUs loan up to $150K, 15-yr deed restriction, ≤100% AMI tenant, no STR | Generous local loan, but use-restricted |

Sources: respective city ADU pages and ordinances (Denver, Boulder, Fort Collins; Colorado Springs Code § 7.3.304); Housing Eagle County. Verified May 26, 2026. Aurora flagged for direct verification.

Run the Colorado ADU Financing Path Finder → Check your city, ADU type, and first funding path.

Start the Path FinderCan Colorado ADU rental income help you qualify?

Answer capsule: Sometimes. Fannie Mae now allows rental income from one ADU to count toward qualifying income on a one-unit principal residence, for purchase or limited cash-out refinance transactions only, capped at 30% of the borrower’s total qualifying income. When current leases or appraiser market-rent forms are used, Fannie Mae generally calculates qualifying rental income at 75% of gross monthly rent. This became automatic in Fannie Mae’s Desktop Underwriter (DU) version 12.1 over the weekend of March 21, 2026, though lenders could apply it earlier under manual underwriting. The ADU must be legal, permitted, and supported by appraisal and rent documentation.

This is a meaningful 2026 change worth understanding precisely.

Existing ADU rental income

Answer capsule: To count rental income from an existing ADU, lenders generally require a lease and an appraiser’s market-rent estimate, the ADU must be legal and permitted, and the property must be a one-unit principal residence. Under Fannie Mae’s policy, qualifying ADU rental income cannot exceed 30% of the borrower’s total qualifying income, and lease or market-rent figures are generally counted at 75% of gross rent.

There are extra guardrails for first-time landlords. Fannie Mae’s published scenarios show that if a borrower has fewer than 12 months of property-management experience and a housing payment, the qualifying rental income generally can’t exceed the property’s housing payment (PITIA — principal, interest, taxes, insurance, and association dues). (Source: Fannie Mae Selling Guide, B3-3.8-01 Rental Income; Selling Guide Announcement SEL-2025-08. Verified May 26, 2026.)

Projected (future) ADU rental income

Answer capsule: Income from an ADU you haven’t built yet is far more constrained than income from an existing, leased ADU. Whether projected rent can support a loan depends on the specific loan program, appraiser support, and the ADU’s legal and permitted status — confirm with your lender before relying on it.

Don’t assume the rent a contractor or rent-estimate site quotes will count toward qualifying. Get it confirmed in writing by your loan officer for your specific program.

Freddie Mac and short-term-rental cautions

Answer capsule: Freddie Mac states that ADU rental income may be used as qualifying income when its requirements are met; its ADU fact sheet provides that lease-documented rental income must not exceed 75% of the lease amount and that qualifying rental income cannot exceed 30% of total qualifying income. Short-term-rental income is risky for underwriting and is restricted outright in some Colorado cities, including Boulder and Colorado Springs.

If your plan depends on nightly-rental income, two things can sink it: the lender may not count projected short-term-rental income at all, and your city may not let you run a short-term rental on an ADU lot. (Source: Freddie Mac ADU resources/fact sheet; city ordinances above. Verified May 26, 2026.)

Illustrative-examples disclaimer: These are illustrative examples, not guarantees of returns or approval. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Planning to rent it out? Explore financing paths that may consider ADU rental income.

Explore rental-income financing paths →Should you use a HELOC, cash-out refinance, or construction loan?

Answer capsule: Use a HELOC or home equity loan when you have enough equity and want to preserve a favorable first mortgage; use a cash-out refinance only when replacing your current mortgage is acceptable or improves your rate; use a renovation or construction-to-permanent loan when the project needs larger funding, draw management, or as-completed value. The right product should follow feasibility, not precede it.

Most homeowners get stuck on one of four real problems. Here’s how each points to a path.

The low-rate mortgage problem

If you locked a 2–3% mortgage during the pandemic, a cash-out refinance is usually the wrong move — it forces you to refinance your whole loan at today’s higher rate just to access cash. Second-position options (a HELOC, a home equity loan, or an after-renovation-value renovation loan) let you keep the cheap first mortgage and borrow on top of it. This is the most common Front Range situation, and it’s why we rarely lead with cash-out refi here.

The equity problem

If you bought recently, your equity may not cover a six-figure detached build. That’s the renovation mortgage’s moment: it underwrites against what your home will be worth after the ADU is finished, not just today’s value.

The documentation problem

Construction and renovation loans require plans, a detailed budget, contractor documentation, appraisals, inspections, and draw schedules. HELOCs and home equity loans are lighter on paperwork. If you value simplicity and have the equity, the equity products win on hassle.

The sequencing problem

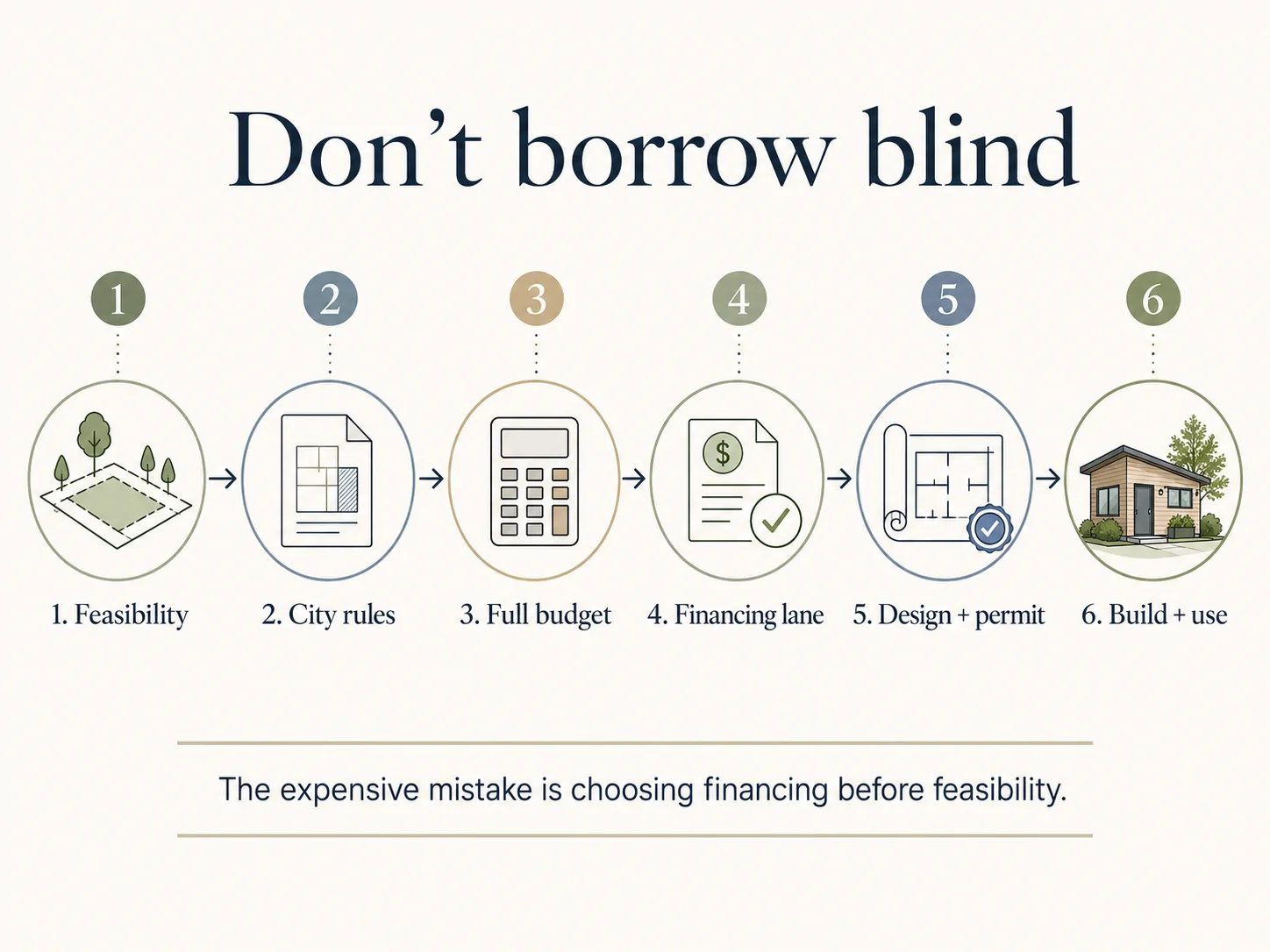

This is the most valuable thing on this page: the loan is usually not the hardest part of an ADU. The expensive mistake is choosing financing before you’ve confirmed the ADU type, the city rules, the utility and fee costs, and a realistic total project cost. We’ve seen the pattern repeatedly — a homeowner sizes a HELOC to a construction bid, then discovers a five-figure tap charge and a parking-replacement requirement the line of credit can’t cover, and the project stalls mid-build. The good news: that mistake is completely avoidable, and avoiding it is exactly what the rest of this page is built to help you do. Verify feasibility first; let the financing follow.

Which loan protects your first mortgage?

| Financing path | Preserves existing first mortgage? | Uses as-completed value? | Best fit |

|---|---|---|---|

| HELOC | Usually yes | Usually no | Strong equity, flexible draws |

| Home equity loan | Usually yes | Usually no | Fixed lump sum, known budget |

| Cash-out refinance | No | Based on current value | Owners with a high existing rate |

| Construction-to-permanent | Not always | Often yes | Larger detached / new builds |

| Renovation mortgage | Varies | Often yes | Limited equity; ADU via renovation |

| Public / local program | Varies | Varies | Eligibility-restricted projects |

Educational comparison, sorted by neutral criteria. Not a lender ranking. Verified May 26, 2026.

Not sure which path fits? Run the Colorado ADU Financing Path Finder.

Start the Path FinderWhere do you find a CHFA participating lender — and what should you ask?

Answer capsule: Because CHFA’s ADU finance support flows through lenders, nonprofits, and CDFIs rather than directly to homeowners, you access it by working with a participating institution. CHFA maintains a network of participating lenders for its homeownership programs and can be contacted at askchfa@chfainfo.com; as the ADU finance programs roll out through 2026, confirm directly with CHFA which lenders or nonprofits are offering ADU-specific products in your area.

When you talk to a lender, ask these five questions: Are you participating in CHFA’s ADU finance programs? Is my jurisdiction a DOLA-certified ADU Supportive Jurisdiction? Do I meet the program’s low-to-moderate income criteria? Can you do an after-renovation-value renovation loan or a construction-to-permanent loan for an ADU? And will my project’s documentation — plans, budget, permits — be enough to firm up terms? You won’t apply to CHFA directly; the lender is your point of entry. (Source: CHFA Homeownership and ADU Finance Programs pages. Verified May 26, 2026.)

What should you gather before applying for a Colorado ADU loan?

Answer capsule: Before applying, assemble documents that prove both financial capacity and project feasibility: a current mortgage statement, an estimate of your home’s value, your preliminary ADU type and concept, zoning/city evidence that the ADU is allowed, a rough fee-inclusive budget, a contractor or prefab estimate, income documentation, and your intended use. A stronger feasibility package reduces the odds you borrow the wrong amount.

Walk into the lender conversation with these in hand and you’ll get a faster, more accurate answer.

- Property and mortgage documents: mortgage statement, property tax bill, homeowner’s insurance, an estimate of current value, and parcel information.

- City feasibility documents: zoning confirmation, ADU type, setbacks, size limits, utility requirements, parking rules, short-term-rental rules, and any floodplain or Wildland-Urban Interface (WUI) constraints.

- Construction documents: a concept plan, a contractor bid or prefab quote, a site-work allowance, a utility allowance, and a contingency line.

- Income and rental documents: pay stubs, tax returns, and — if you’ll rent the ADU — a lease or appraiser’s market-rent estimate plus your long-term rental plan.

Colorado-specific add-ons: a DOLA supportive-jurisdiction check; a city ADU-eligibility confirmation; a Denver Water SDC/license question if you’re in Denver; a Fort Collins fee-and-utility review if you’re in Fort Collins; a Colorado Springs § 7.3.304 parking/WUI/water statement if you’re in Colorado Springs; and a Boulder short-term-rental grandfather check if you’re in Boulder.

Download the Free ADU Starter Kit → Get the document checklist.

The checklist above, formatted and ready to hand to your lender.

Get the Starter KitWhat can go wrong if you finance before checking feasibility?

Answer capsule: The costliest ADU financing mistakes aren’t about choosing the wrong lender — they’re about borrowing against a project that later changes due to city rules, utility constraints, short-term-rental limits, fee schedules, or construction-cost surprises. The four most common failures are under-borrowing, assuming unusable rental income, choosing the wrong loan structure, and applying before the project is financeable.

You under-borrow

A loan sized only to the construction bid misses design, permitting, water/sewer connections, utility laterals, stormwater, city fees, and contingency. That’s how a “fully funded” project runs out of money at framing.

You assume rental income that can’t be used

Future rent may not qualify under your loan program, and short-term-rental assumptions can fail outright in cities like Boulder and Colorado Springs.

You choose the wrong loan structure

A cash-out refinance can needlessly reset a great mortgage; a HELOC may not cover a large detached ADU; a full construction loan may be overkill for a simple garage conversion.

You apply before the project is financeable

Lenders frequently need plans, budgets, permits, appraisals, and contractor documents before they’ll firm up terms. Applying too early just earns a “come back later.”

See What You Can Build → Get Your Free ADU Report.

Know your lot’s potential before you talk to a lender.

Colorado ADU loan examples

Answer capsule: The right financing path shifts with each homeowner’s profile — equity, mortgage rate, city, and intended use. The following are decision models, not predictions, guarantees, or offers.

- Denver homeowner with strong equity and a low first mortgage. Likely first test: a HELOC or home equity loan to preserve the cheap mortgage. Verify Denver eligibility, zone-specific bulk-plane and setback standards, and Denver Water’s System Development Charge before sizing the loan.

- Boulder homeowner planning long-term rental. Likely first test: a home equity or renovation loan with conservative rent assumptions. Don’t build the plan around short-term-rental income — Boulder restricts it unless the ADU and license predate February 1, 2019.

- Fort Collins homeowner surprised by fees. Likely first test: feasibility plus a full, fee-inclusive budget before loan shopping, because review and utility costs can reach $20,000–$25,000.

- Colorado Springs homeowner counting on nightly-rental income. Likely first test: revise the use case before financing — short-term-rental restrictions on ADU lots can dismantle a nightly-rental pro forma, and § 7.3.304 parking and WUI rules may apply.

- Eagle County homeowner willing to provide workforce housing. Likely first test: the Aid for ADUs program (up to $150,000, 15-year deed restriction, ≤100% AMI tenant), then private financing only if the workforce-rental and no-short-term-rental restrictions fit.

Illustrative-examples disclaimer: These scenarios are illustrative, not guarantees of returns, loan approval, or program eligibility.

What we verified for this guide

Answer capsule: This guide was built from official Colorado state, program, agency, and city sources first, then supplemented with Colorado-specific cost sources where official construction-cost data was unavailable. Each fact below was confirmed on the verification date shown.

| Topic | Source type | Last verified |

|---|---|---|

| HB24-1152 statewide ADU law; subject-jurisdiction definition; $5M DOLA grant + $8M CHFA via OEDIT; supportive-jurisdiction HOA provision | Colorado General Assembly (primary statute) | May 26, 2026 |

| CHFA ADU Finance Programs (four tools; lender-/intermediary-facing) | CHFA; OEDIT (state agencies) | May 26, 2026 |

| DOLA grant program to local governments; 82% compliance | DOLA; Governor’s Office | May 26, 2026 |

| Denver citywide ADU expansion (eff. 12/16/2024); Denver Water license + SDC | City and County of Denver; Denver Water | May 26, 2026 |

| Boulder owner-occupancy removal (3/8/2025); STR pre-2/1/2019 grandfather; size/sprinkler | City of Boulder | May 26, 2026 |

| Fort Collins fees ($6,925 BDR; $20K–$25K total); size/meter/stormwater | City of Fort Collins | May 26, 2026 |

| Colorado Springs ADU rules (Code § 7.3.304) | City of Colorado Springs municipal code | May 26, 2026 |

| Eagle County Aid for ADUs (up to $150K, 15-yr deed restriction, ≤100% AMI, no STR) | Housing Eagle County | May 26, 2026 |

| Fannie Mae ADU rental income (30% cap; 75% of rent; DU 12.1, weekend of 3/21/2026) | Fannie Mae Selling Guide; SEL-2025-08 | May 26, 2026 |

| Freddie Mac ADU rental documentation (75% lease; 30% cap) | Freddie Mac ADU resources | May 26, 2026 |

| Colorado ADU cost ranges | Olerra; Denver Dream Builders; BuildinganADU (national/older) | May 26, 2026 |

| Aurora ADU code status | Engage Aurora — requires direct municipal-code verification | Pending |

We separate verified legal and program facts from editorial financing guidance. We are not a lender or financial advisor, and we do not guarantee loan approval, rates, program eligibility, rental income, construction costs, or ADU approval.

Frequently asked questions

Can I get an ADU loan in Colorado?

Answer capsule: Yes, but “Colorado ADU loan” almost always means choosing among home equity, renovation, construction, refinance, CHFA-backed, or local-program paths. There is no single universal statewide loan available to every homeowner.

Does Colorado have ADU grants?

Answer capsule: Colorado has ADU-related grant and finance programs, but the main grant program — DOLA’s Accessory Dwelling Unit Fee Reduction and Encouragement Grant Program, funded by a $5 million transfer under HB24-1152 — awards money to local governments, not directly to homeowners. A separate $8 million CHFA program supports lender-facing financing. DOLA directs residents seeking ADU financing to contact CHFA at askchfa@chfainfo.com. (Source: HB24-1152; DOLA. Verified May 26, 2026.)

What is the CHFA ADU program?

Answer capsule: The CHFA ADU Finance Programs are backed by $8 million authorized under HB24-1152 to provide credit enhancement, interest-rate buydowns, down-payment assistance or principal reduction, and loans to nonprofits and CDFIs — all to support affordable ADU financing for low- and moderate-income borrowers in DOLA-certified supportive jurisdictions. Homeowners access it through a participating lender or intermediary, not directly from CHFA. (Source: HB24-1152, Section 3; CHFA; OEDIT. Verified May 26, 2026.)

How much does an ADU cost in Colorado?

Answer capsule: A useful early planning range is roughly $150,000 to $420,000 for many installed Colorado ADUs depending on size and site conditions, with some detached or custom Denver-area projects running higher. Always add design, permits, utilities, city fees, and contingency before sizing a loan. (Source: Olerra; Denver Dream Builders. Verified May 26, 2026.)

Is a HELOC a good way to build an ADU in Colorado?

Answer capsule: A HELOC can fit homeowners with enough equity who want to preserve their current first mortgage and like drawing funds as construction bills arrive. It may not fit larger projects, owners with limited equity, or borrowers who need to borrow against the home’s as-completed value.

Can I use future ADU rent to qualify for a loan?

Answer capsule: Sometimes. Fannie Mae allows rental income from one ADU on a one-unit principal residence (purchase or limited cash-out refinance only) toward qualifying income, capped at 30% of total qualifying income and generally counted at 75% of gross rent, effective automatically in Desktop Underwriter 12.1 from the weekend of March 21, 2026. Documentation, legality, appraisal support, and lender overlays apply, so confirm with your lender. (Source: Fannie Mae SEL-2025-08; B3-3.8-01. Verified May 26, 2026.)

Can my HOA stop a Colorado ADU?

Answer capsule: In a DOLA-certified supportive jurisdiction, HB24-1152 (Section 6) makes a unit-owners’ association’s prohibition on ADUs, or its restrictive ADU design or dimension standards, void as a matter of public policy — subject to a reasonable-restriction exception. Outside supportive jurisdictions, an HOA’s authority depends on its governing documents and local law, so confirm both your jurisdiction’s status and your association’s current rules. (Source: HB24-1152, Section 6. Verified May 26, 2026.)

Can I use a Colorado ADU as a short-term rental?

Answer capsule: It depends on your city. Boulder generally prohibits short-term rentals (stays under 30 days) of ADUs unless the ADU and its short-term-rental license were established before February 1, 2019, and Colorado Springs restricts short-term rental use on properties with ADUs after June 30, 2025 unless grandfathered. Confirm your municipality’s current rules before underwriting any short-term-rental income. (Source: City of Boulder; City of Colorado Springs § 7.3.304. Verified May 26, 2026.)

Should I get loan preapproval before permits?

Answer capsule: You can talk to lenders early, but you should not finalize a financing plan before confirming property feasibility, city rules, a rough fee-inclusive construction cost, utility requirements, and whether your intended use is allowed. Financing should follow feasibility, not precede it.

Before you go

The honest takeaway is the one we’d give a neighbor over the fence: don’t shop for a Colorado ADU loan in the abstract. Confirm what your specific lot, in your specific city, can support — then match the financing lane to your equity, your mortgage rate, and how you’ll use the unit. Get that order right, and the money question, the one that stops most Colorado homeowners cold, becomes the easy part.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

Get Your Free ADU Report →Sources & citations

- Colorado General Assembly, HB24-1152 (C.R.S. § 29-35-401–405) — subject-jurisdiction definition; June 30, 2025 effective date; $5M to DOLA grant fund (Sec. 1); $8M to CHFA via OEDIT for four program types (Secs. 3–4); supportive-jurisdiction HOA/unit-owners-association void provision (Sec. 6). leg.colorado.gov/bills/hb24-1152

- C.R.S. § 29-35-403 — subject-jurisdiction ADU requirements; parking/owner-occupancy/design limits with exceptions. (Justia 2024 Colorado Revised Statutes.)

- CHFA ADU Finance Programs — chfainfo.com/accessory-dwelling-unit-adu-finance-programs; CHFA Newsroom (program announcement).

- OEDIT Accessory Dwelling Unit Finance Program — $8M loans/buydowns/credit enhancement framing. oedit.colorado.gov.

- DOLA — ADU Grant Program (to local governments); ADU Supportive Jurisdictions; dlg.colorado.gov. Governor’s Office press release, Nov 2025 (82% compliance).

- City and County of Denver — Citywide ADUs text amendment, effective 12/16/2024. denvergov.org.

- Denver Water — Accessory Dwelling Units: water supply license + additional System Development Charge required. denverwater.org.

- City of Boulder — ADU page: owner-occupancy removed 3/8/2025; STR grandfather (ADU + license before 2/1/2019); modular ADUs need local permits. bouldercolorado.gov.

- City of Fort Collins — ADU page: $6,925 Basic Development Review; total fees $20K–$25K; size/meter/stormwater. fortcollins.gov.

- City of Colorado Springs — Municipal Code § 7.3.304 (Accessory Uses): administrative approval; one ADU/lot; owner-residence at application; +1 parking space; WUI overlay limits; size/height caps; STR restriction after 6/30/2025. codelibrary.amlegal.com.

- Housing Eagle County — Aid for ADUs: up to $150K loan, 15-yr deed restriction, ≤100% AMI tenant, no STR. housingeaglecounty.com.

- Fannie Mae — Accessory Dwelling Units product page; Selling Guide B3-3.8-01 Rental Income; Announcement SEL-2025-08 (30% cap; 75% of rent; one-unit principal residence; purchase/limited cash-out only; one ADU; DU v12.1 effective weekend of 3/21/2026, manual underwriting earlier). singlefamily.fanniemae.com.

- Freddie Mac — Accessory Dwelling Units resources/fact sheet (75% lease; 30% cap). sf.freddiemac.com.

- Cost data — Olerra Colorado ADU cost guide (size bands); Denver Dream Builders (garage conversions ~$100K–$130K; detached ~$350K–$450K); BuildinganADU.com (older/national $162–$682/sq ft, ~$305 avg).

- Urban ADU / Community Banks of Colorado — ADU finance options; general HELOC/home-equity terms (verify current terms with lender).

Aurora ADU code status flagged for direct municipal-code verification before publishing city-specific loan guidance.