How to Finance an ADU Rental: Every Loan Path (and Whether the Rent Counts) in 2026

By the Dwelling Index Editorial Team · Last updated: · Last verified: · Editorial standards · Methodology · ~40 min read

This guide is educational and is not financial, legal, tax, or lending advice. The Dwelling Index is an independent research resource. We are not a lender, broker, or builder.

Editorial disclosure: The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations — not a lender, broker, or builder. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Read our full affiliate disclosure and methodology →

Start Here: Which ADU Rental Financing Path Fits Your Situation?

An ADU — accessory dwelling unit — is a smaller, self-contained second home on the same lot as a primary residence (a backyard cottage, garage conversion, or basement apartment). When you want that unit to generate rent, your financing question splits in two: how you’ll pay for construction, and whether the future rent can help you qualify for the loan. Those are different problems, and most “ways to finance an ADU” lists only answer the first one.

This is the fastest way to find your lane. Find the row that sounds like you, then read the matching section below for the full breakdown.

| Your situation | Path to test first | Why it fits | Watch out for |

|---|---|---|---|

| Strong equity, low-rate first mortgage you want to keep | HELOC or home equity loan | Adds a second loan without touching your first mortgage | Usually can’t use future ADU rent to qualify; HELOC rate is typically variable |

| Fine replacing your first mortgage, or current rate is high | Cash-out refinance | One loan, one payment | Resets your rate and term; FHA cash-out specifically cannot use ADU rent as income |

| Not enough equity yet; need construction draws | Renovation loan or construction-to-permanent loan | Lends against the home’s after-build value, not today’s | More paperwork, inspections, contractor controls; higher rate than a simple HELOC |

| Buying a home that already has a legal, permitted ADU | Conventional or FHA purchase mortgage | Existing, leased ADU rent can help you qualify | Rent is haircut to 75% and capped at 30% of qualifying income |

| Non-owner-occupied investment property | DSCR loan | Qualifies on the property’s cash flow, not your W-2 | Business-purpose only; some lenders require comparable ADU sales/rentals before counting the rent |

| The math only works with optimistic Airbnb numbers | Don’t finance yet | Lenders and many cities won’t support transient-rental income | Validate legal use and long-term rent first |

Sources: Fannie Mae Selling Guide B3-3.8-01 and SEL-2025-08 (Oct 8, 2025); Freddie Mac Single-Family Seller/Servicer Guide §5306.1(g) and ADU fact sheet; HUD Mortgagee Letter 2023-17 (FHA). DSCR comparable requirement reflects common non-QM lender overlays. Verified . General program rules — individual lenders apply their own overlays.

Want a path matched to your exact numbers? Answer a few questions about your property, equity, income, and rental plan and you’ll get a ranked likely path, a rent-counting flag specific to your inputs, and the questions to bring to a lender.

Run the ADU Rental Financing Path Finder →Which ADU Rental Financing Path Should You Test First?

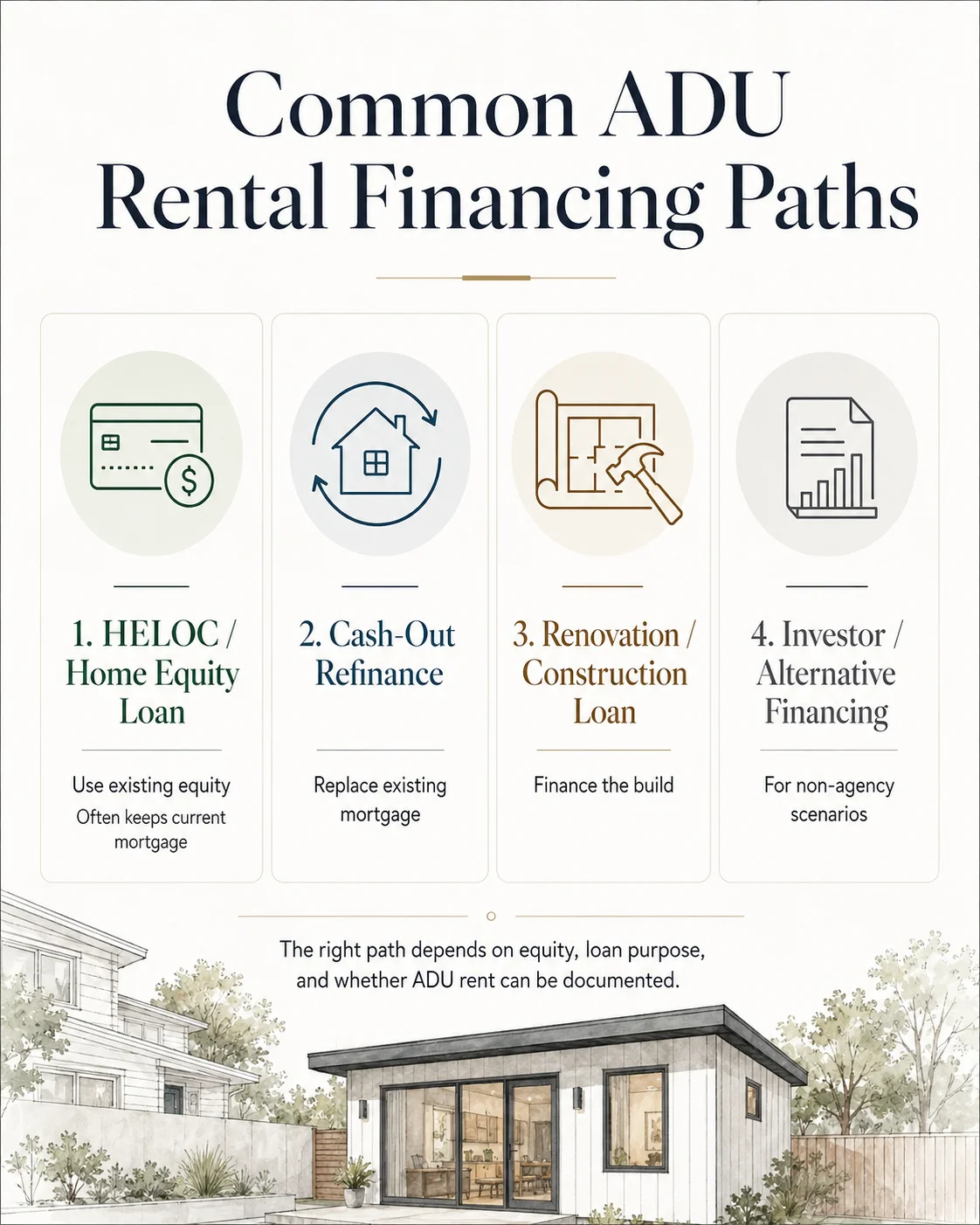

Most homeowners should test financing in this order: first, whether existing equity can fund the project without disturbing the first mortgage; second, whether renovation or construction financing is needed because the project depends on the home’s future value; third, whether documented ADU rent can help you qualify; and fourth — only if those don’t fit — investor or private-credit options with a clear exit plan. This sequence works because each step is cheaper, simpler, and lower-risk than the next.

A second-position loan against existing equity (a HELOC or home equity loan) is the least disruptive move because it doesn’t replace your first mortgage — which matters enormously if you locked a low rate in 2020–2021. Among California homeowners who used mortgage products to finance an ADU, 56% used a HELOC or home equity loan, 35% used a cash-out refinance, and 6% used a construction or renovation loan (Urban Institute analysis of UC Berkeley Terner Center data, 2024).

Equity-based loans have a ceiling: lenders generally let you borrow up to 80–85% of your home’s value minus your existing mortgage balance, and they typically want you to keep 15–20% equity after closing. If your project costs more than that gap, renovation and construction loans underwrite against the finished property value.

The four-question decision filter

Before you call a single lender, answer these four questions. Your answers determine which path to test first.

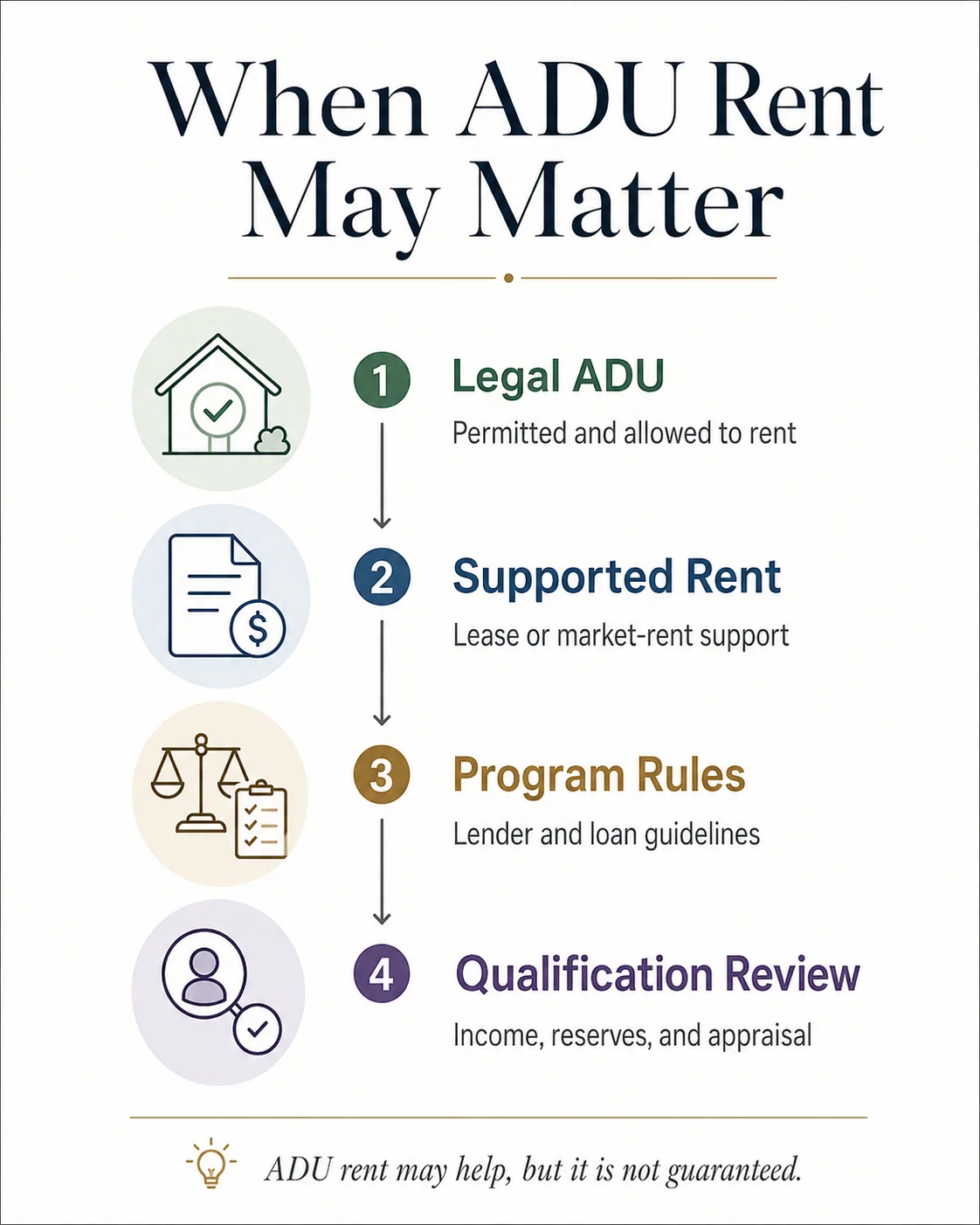

- Will the ADU be legal to rent? If your city won’t permit it as a rentable unit, the rental income can’t support an appraisal or a loan. Freddie Mac explicitly bars rental income from an illegal ADU from being used to qualify.

- Do you need the ADU rent to qualify? If yes, agency rules and appraisal support matter far more than any lender’s marketing. If your salary alone qualifies you, you have more freedom.

- Are you protecting a low-rate first mortgage? If yes, a second-lien option (HELOC, home equity loan) usually deserves the first look so you don’t surrender that rate.

- Do you need construction draws or after-renovation value? If yes, a renovation loan or construction-to-permanent loan is built for exactly that.

First path by borrower profile

| Borrower profile | First path | Backup path | Bad fit |

|---|---|---|---|

| Equity-rich owner, low first-mortgage rate | HELOC / home equity loan | Home equity investment (HEI), where available in your state | Cash-out refi that needlessly replaces a low-rate loan |

| Low equity, strong income, large build | Renovation or construction loan | Construction-to-permanent | A HELOC that’s too small for the project |

| Buying a property with an existing legal ADU | Purchase mortgage with ADU-rent review | FHA, conventional, or portfolio lender | Assuming all the rent will count |

| Investor building/buying for yield | DSCR / portfolio / private | Conventional investment-property loan | An owner-occupant-only product |

| Airbnb-first plan | Verify local STR legality first | Long-term rent as the fallback base case | Financing that depends only on nightly-rate assumptions |

Not sure which lane is realistic for your lot? It’s free, and it tells you what you can build before you spend a dollar on plans.

See what’s possible at your address →Can ADU Rental Income Help You Qualify for the Loan?

Yes — but only under specific program rules, and the rent is almost always discounted and capped. Fannie Mae, Freddie Mac, and FHA each allow ADU rental income to count toward a borrower’s qualifying income on a one-unit principal residence, and when lease or appraiser-supported market rent is used, they apply a 75% calculation and cap how much ADU rent can contribute at 30% of total qualifying income. The single most important practical point on this entire page: the rent may help, but it will never carry the whole loan by itself.

Fannie Mae

In Selling Guide Announcement SEL-2025-08 (published October 8, 2025), Fannie Mae expanded ADU rental income to all conventional programs — previously it was limited to HomeReady. Desktop Underwriter (DU) version 12.1, released the weekend of March 21, 2026, automated the calculation. Key conditions:

- The property must be a one-unit principal residence.

- Purchase or limited cash-out refinance transactions only.

- Rental income may come from only one ADU, even if the property has more.

- ADU rent used to qualify cannot exceed 30% of the borrower’s total qualifying income.

- When current lease or market rent is used, qualifying income is at 75% of gross rent (Form 1007 “Monthly Market Rent” on appraisal). Borrowers with a rental history may instead document income from tax returns.

- First-time-landlord limit: fewer than 12 months of landlord experience means qualifying rental income cannot exceed the borrower’s PITIA (principal, interest, taxes, insurance, association dues).

Sources: Fannie Mae Selling Guide B3-3.8-01; SEL-2025-08; Fannie Mae ADU rental-income fact sheet (Nov 2025).

Freddie Mac

Freddie Mac’s rules (Single-Family Seller/Servicer Guide §5306.1(g)) closely mirror Fannie’s, with a few distinct wrinkles:

- ADU rental income allowed on a one-unit primary residence, for purchase or “no cash-out” refinance.

- Rent documented with a lease must not exceed 75% of the lease amount; qualifying rental income must not exceed 30% of total stable monthly income.

- Appraisal requirement: a full appraisal is required. The sales-comparison approach must include at least one comparable sale with an ADU, and the ADU rental analysis must include a minimum of three comparable rentals, with at least one comparable rental that includes a rented ADU.

- Landlord education: for a purchase, at least one qualifying borrower must complete a landlord-education program unless they have at least one year of landlord experience.

- Illegal ADU rental income may not be used.

Sources: Freddie Mac Single-Family Seller/Servicer Guide §5306.1(g); Freddie Mac ADU fact sheet.

FHA

FHA’s ADU rental-income policy comes from HUD Mortgagee Letter 2023-17 (issued October 2023):

- 75% of the appraiser-estimated ADU rent included in effective income for certain existing/limited-history scenarios, up to a maximum of 30% of total monthly income.

- Two months of PITI reserves required when ADU income is used.

- Special FHA Standard 203(k) treatment: for certain one-unit-with-new-ADU scenarios with no rental history, up to 50% of the estimated ADU rent may be used.

- Critical limit: in an FHA cash-out refinance, ADU rental income cannot be used as effective income.

- The appraiser’s market rent must be for a unit that is legally rentable and non-transient — FHA guidance excludes hotel/transient comparables and rentals under 30 days.

Source: HUD Mortgagee Letter 2023-17.

USDA and VA

USDA: As of this writing, USDA’s Single Family Housing Guaranteed Loan Program (SFHGLP) cannot finance a property that is income-producing — and a property with a rental ADU is generally treated as exactly that. That may change: on March 31, 2026, USDA’s Rural Housing Service published a proposed rule (docket RHS-26-SFH-0100) to allow financing of homes with income-producing ADUs, with public comments due June 1, 2026. This is proposed, not final, as of May 24, 2026.

VA: Treatment of ADU rental income under VA loans is not clearly established by a current nationwide official rule. Verify with the current VA Lender’s Handbook and your lender before relying on any ADU rental-income treatment for a VA loan.

Agency rental-income rule matrix

| Program | ADU rent can help qualify? | Transaction / property | Haircut / cap | Source (verified May 24, 2026) |

|---|---|---|---|---|

| Fannie Mae | Yes — existing ADU | One-unit primary; purchase or limited cash-out refi; one ADU | 75% of gross rent; 30% cap; first-time-landlord rent ≤ PITIA | Selling Guide B3-3.8-01; SEL-2025-08 |

| Freddie Mac | Yes, conditions apply | One-unit primary; purchase or no-cash-out refi | 75% of lease; 30% cap; full appraisal + comps | Guide §5306.1(g); ADU fact sheet |

| FHA | Yes, conditions apply | Existing rent; certain new-ADU 203(k) | 75% (or 50% in 203(k) no-history); 30% cap; 2 mo. reserves | HUD ML 2023-17 |

| USDA | No (currently) — proposed rule pending | N/A until finalized | N/A | Federal Register 03/31/2026 |

| VA | Verify — no clear nationwide rule confirmed | Lender-specific | Lender/handbook-specific | Verify before relying |

Agency rules change, and individual lenders apply additional overlays. This is regulatory information, not a promise of approval.

Whether your salary plus your projected rent clears the 30% cap depends entirely on your numbers.

Run the ADU Rental Financing Path Finder → check whether your rent may countHow Much ADU Rent Can Lenders Actually Count?

The rent you expect is rarely the rent a lender can use. After the standard 75% haircut and the 30%-of-income cap, the amount of ADU rent that meaningfully boosts your qualification is often smaller than homeowners assume — and in higher-rent metros, the 30% cap can bind before the 75% haircut even matters, unless your other income is substantial.

The simple screening formula

- Start with supported monthly rent (what an appraiser or lease can document — not what you hope to get).

- Apply the program haircut: multiply by 0.75 for existing/market rent under Fannie, Freddie, and FHA (FHA Standard 203(k) uses 0.50 in certain no-history cases).

- Check the 30% cap: the counted rent can’t exceed 30% of your total qualifying income. To fully use a given amount of counted ADU rent, your non-ADU monthly income generally needs to be at least the counted rent × 70 ÷ 30 — roughly 2.33× the counted rent.

- Remember: actual underwriting uses lender and program documents (Form 1007, leases, rental analyses), not a blog formula.

Worked example

Say the appraiser supports $2,000/month in ADU market rent.

- 75% haircut → $1,500 of potentially countable rent.

- For that full $1,500 to count under the 30% cap, your other qualifying income must be at least $1,500 × 2.33 ≈ $3,500/month ($42,000/year). If you earn more, the full $1,500 counts. If you earn less, the cap trims the usable rent.

That’s the mechanism nobody explains: in a strong rental market, your salary — not the rent — often becomes the limiting factor.

2026 ADU rental underwriting snapshot (sample metros)

HUD Fair Market Rent (FMR) benchmarks combined with the 75% haircut and the income threshold at which the 30% cap begins to bind. HUD FMRs are annually published monthly gross-rent estimates used in housing programs; lenders do not automatically accept HUD FMR — they require an appraisal, lease, or program-specific documentation — but FMR is a useful neutral starting benchmark.

| HUD FMR area (FY2026 sample) | 1BR FMR (sample) | 75% countable | Non-ADU monthly income before 30% cap binds |

|---|---|---|---|

| Los Angeles–Long Beach–Glendale, CA HMFA | $2,328 | $1,746 | ~$4,074 |

| San Diego–Carlsbad, CA MSA | $2,459 | $1,844 | ~$4,303 |

| San Jose–Sunnyvale–Santa Clara, CA MSA | $2,982 | $2,236 | ~$5,217 |

| Seattle–Bellevue, WA HMFA | $2,146 | $1,610 | ~$3,757 |

| Portland–Vancouver–Hillsboro, OR-WA MSA | $1,677 | $1,258 | ~$2,935 |

| Denver–Aurora–Lakewood, CO MSA | $1,754 | $1,316 | ~$3,071 |

| Austin–Round Rock, TX MSA | $1,562 | $1,172 | ~$2,735 |

| Miami–Miami Beach–Kendall, FL HMFA | $1,995 | $1,496 | ~$3,491 |

| Atlanta–Sandy Springs–Roswell, GA HMFA | $1,660 | $1,245 | ~$2,905 |

| Charlotte–Concord–Gastonia, NC-SC MSA | $1,538 | $1,154 | ~$2,693 |

| Minneapolis–St. Paul–Bloomington, MN-WI MSA | $1,405 | $1,054 | ~$2,459 |

| Salt Lake City, UT MSA | $1,456 | $1,092 | ~$2,548 |

| New York, NY HMFA (Kings County sample) | $2,655 | $1,991 | ~$4,646 |

| Chicago–Joliet–Naperville, IL HMFA | $1,581 | $1,186 | ~$2,767 |

FMR figures are illustrative samples drawn from HUD’s published FY2026 Fair Market Rent program data, rounded; HUD revises FMRs during the year and uses Small Area FMRs (by ZIP) in some metros, so confirm your exact area against the live HUD User FY2026 dataset before relying on a figure. The “income needed” column is our calculation: 75% countable rent × (70 ÷ 30). This is a screening tool, not an approval estimate, payment estimate, or guarantee.

Illustrative-example disclaimer: These are illustrative examples, not guarantees of returns or loan approval. Actual results depend on local market conditions, appraiser-supported rent, construction costs, borrower qualifications, lender overlays, and regulatory approvals.

What If You Don’t Have Enough Equity Yet?

If you don’t have enough equity to cover the build, renovation and construction-to-permanent loans solve the problem by underwriting against the home’s after-build value rather than today’s value — letting you borrow against equity you don’t have yet. This is the single most important escape hatch for homeowners who get a build quote that exceeds their current borrowing power.

A standard HELOC or cash-out refinance lends against your home as it stands today. So if your home is worth $500,000, you owe $300,000, and a lender caps you at 80% loan-to-value, you can borrow against roughly $100,000 — often not enough for a $250,000 detached ADU. A renovation or construction loan instead underwrites the after-renovation value (ARV): your home plus the finished ADU.

The main products in this lane:

- Fannie Mae HomeStyle Renovation and Freddie Mac CHOICERenovation — conventional renovation mortgages that fold the construction cost into one loan based on completed value.

- FHA 203(k) — an FHA renovation loan with more flexible credit requirements; the Standard 203(k) has its own ADU rent treatment (the 50% rule above).

- Construction-to-permanent loan — one loan that funds the build in stages (draws, released as construction milestones are inspected), with interest-only payments during construction, then converts to a permanent mortgage when the ADU is done.

- ARV-based renovation loans — some specialty lenders lend against future value through a renovation home equity loan, HELOC, or refinance. Availability is state-specific, so confirm your state.

Honest tradeoff: These loans give you more borrowing power, but they cost you in other ways: more documentation, contractor approvals, draw schedules, and inspections — and rates are typically higher than a simple HELOC.

Affiliate disclosure: The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation.

Want to compare construction-loan and renovation-loan paths side by side?

Explore your options with Mortgage Research Center →HELOC, Home Equity Loan, Cash-Out Refinance, Renovation, or Construction Loan?

A HELOC or home equity loan is usually the cleanest first test when you have enough equity and want to preserve a low first mortgage. A cash-out refinance works when replacing the first mortgage is acceptable or your current rate is already high. Renovation and construction loans matter when the project needs future value, formal construction draws, or one-loan financing.

Quick definitions:

- HELOC (home equity line of credit): a revolving line secured by your home. Draw funds as needed during a draw period (often ~10 years, interest-only), then repay in a repayment period. Rates are usually variable.

- Home equity loan (HELOAN): a one-time lump sum, usually at a fixed rate.

- Cash-out refinance: replace your existing mortgage with a larger one and take the difference in cash.

- Renovation loan: finances the build based on the home’s completed value.

- Construction-to-permanent loan: funds the build in inspected draws, then becomes a standard mortgage.

- DSCR loan: an investment-property loan qualified on the property’s rental cash flow, not your personal income.

- HEI (home equity investment): a lump sum in exchange for a share of your home’s future value — no monthly payment, but you give up appreciation. State availability is limited.

Rental-first financing decision matrix

| Financing path | Best when | Future ADU rent can help qualify? | Protects first mortgage? | Funds construction draws? | Biggest drawback |

|---|---|---|---|---|---|

| HELOC | Strong equity, flexible draw needs | Usually no | Yes | Informally, via line access | Variable rate; equity ceiling |

| Home equity loan | Strong equity, want a fixed lump sum | Usually no | Yes | No formal draw control | You borrow it all at once |

| Cash-out refinance | First mortgage is replaceable / high-rate | Limited; FHA cash-out cannot use ADU rent | No | No | May reset rate and term |

| Renovation loan (HomeStyle, CHOICERenovation, 203k) | Future value matters | Program-specific (203k: 50% in some cases) | Usually no | Yes | Contractor, escrow, inspections |

| Construction-to-permanent | Larger ground-up build | Lender-specific | Usually no | Yes | Complexity, overrun risk |

| Purchase mortgage w/ existing ADU | Buying a home with a legal ADU | Yes, if rules met (75% / 30%) | Depends | No | Rent haircut, cap, documentation |

| DSCR / private / bridge | Investor / non-agency | Property-income focused | Depends | Sometimes | Higher cost; exit-risk discipline |

| HEI | Equity-rich, cash-flow constrained | No | Yes | No | Shares future value; limited states |

| Cash / family funds | Avoiding lender friction | N/A | Yes | N/A | Liquidity / relationship risk |

Sources as cited throughout. Organized by structure and borrower fit, not by any payout. Verified .

When preserving a low mortgage matters

If you locked a sub-4% mortgage in 2020–2021, that rate is an asset. Replacing it with a cash-out refinance at today’s higher rates to fund an ADU can cost you far more over time than the ADU loan itself. In that case, a second-position loan — HELOC, home equity loan, or an HEI — usually wins because it leaves the first mortgage alone. Compare the total cost of debt across both loans, not just the size or rate of the new one.

When replacing the first mortgage still makes sense

A cash-out refinance can be the right call when your current rate is already high, when you want a single loan and payment, when you’re consolidating other debt, or when you need a renovation/construction structure a HELOC can’t provide. Just remember the FHA carve-out: FHA cash-out refinances cannot use ADU rental income as effective income (HUD ML 2023-17).

Affiliate disclosure: When you use our links to explore financing options, we may earn a commission at no extra cost to you.

Ready to compare a mortgage-backed path?

Compare ADU financing options with Mortgage Research Center →Financing an ADU as an Investor: DSCR Loans

If the property is not your primary residence, the Fannie Mae and FHA owner-occupant rules don’t apply — investors typically use a DSCR (debt-service-coverage-ratio) loan that qualifies on the property’s rental cash flow instead of personal tax returns or W-2 income. The catch most investors don’t see coming: in emerging-ADU neighborhoods, the appraiser may not be able to count the ADU’s rent at all.

How DSCR works: the lender calculates gross monthly rent ÷ PITIA(principal, interest, taxes, insurance, association dues). A ratio of 1.0 means rent exactly covers the payment; most lenders want 1.0–1.25, and some specialty programs go down to 0.75 or offer “no-ratio” options. Typical parameters: credit score around 620+, down payment 20–25%, and cash reserves of several months of payments.

DSCR loans are business-purpose, non-owner-occupied only. If you plan to live in the property, you need a traditional owner-occupied mortgage instead.

The DSCR appraisal catch-22

DSCR is a non-QM (non-qualified-mortgage) product, so the rules are lender-specific — but a common overlay requires the appraiser to document comparable ADU sales and/or rentals nearby before the ADU’s income can be included. If local ADU comps are thin, that lender may discount or exclude the ADU income entirely from the DSCR calculation. The result is a real catch-22: even a legal, permitted, income-producing ADU can be invisible to underwriting if ADUs are still uncommon in your specific neighborhood. Confirm the comp rule with your lender before you rely on the rent.

On the upside, many DSCR programs are explicitly ADU-friendly where comps exist: some allow income from up to three ADUs per single-family unit, which is significant in markets where state ADU laws permit stacking units.

Check whether your property pencils as a rental before you talk to a DSCR lender. It shows what you can build and what it might rent for — the inputs every DSCR conversation starts with.

Get your free ADU report →Can Projected ADU Rent Count Before the ADU Is Built?

Sometimes — but this is exactly where many ADU rental plans break. The agencies are far more comfortable with an existing, legal, appraiser-supported ADU than with rent from a unit that doesn’t exist yet. FHA’s Standard 203(k) has a specific 50% treatment for certain new-ADU, no-rental-history scenarios, but conventional and portfolio lenders require program-by-program confirmation. Never assume projected rent automatically counts.

Existing ADU vs. new ADU

- Existing ADU: the strongest position. You can show a lease, rent history, and appraisal support — and Fannie Mae and Freddie Mac both allow rental income from an existing ADU on a one-unit principal residence under the rules above.

- New ADU (being built): the lender must rely on program rules, the appraiser’s market-rent estimate, and your contractor’s scope. FHA’s Standard 203(k) explicitly contemplates a new-ADU scenario; conventional and portfolio products vary, so do not treat a not-yet-built ADU as automatically eligible.

- Unpermitted ADU: high risk. Freddie Mac bars rental income from an illegal ADU from being used to qualify, and an unpermitted unit can also create insurance, resale, and liability problems.

FHA 203(k) treatment

The FHA Standard 203(k) renovation loan can finance creating or renovating ADU space, and HUD ML 2023-17 permits up to 50% of the estimated ADU rent to be used in certain one-unit-with-ADU scenarios that have no rental history. This is the closest thing to a “future rent counts” rule among the agencies — but it is narrow, not universal.

Ask your lender, verbatim: “For this exact program, occupancy, ADU status, and loan purpose, can any ADU rent be used to qualify? If yes, what form, lease, appraisal, reserve, and cap rules apply?”

What Makes an ADU Financeable as a Rental?

A financeable ADU rental isn’t just buildable — it must be legal (or acceptably documented), rentable under local rules, supportable by appraisal or lease evidence, and consistent with the loan program’s occupancy and income rules. Miss any one of those and the rent stops counting, even if the unit itself is perfectly nice.

Legal rentability

What lenders and appraisers look for: local zoning permission, building permits, a certificate of occupancy (or local equivalent) where applicable, legal nonconforming status for older units, HOA allowances, owner-occupancy requirements where your jurisdiction imposes them, and any short-term-rental (STR) restrictions. In California, the statewide ADU framework is codified in Government Code Sections 66310–66342 (renumbered in 2024), which set by-right approval rules.

Appraisal support

The appraiser typically completes a Form 1007 (single-family comparable rent schedule) or Form 1025, documents comparable ADU rentals, and establishes market rent. Remember: gross market rent is the appraiser’s number; qualifying rent is what’s left after the 75% haircut and 30% cap.

- Fannie Mae: Form 1007 / comparable rent schedule supports the market rent used.

- Freddie Mac: a full appraisal with at least one ADU sale comp, plus a rental analysis of three comparable rentals (at least one with a rented ADU).

- FHA: the appraiser’s estimated market rent must be for a legally rentable, non-transient unit.

Rental use type

- Long-term rent (12-month leases) is the easiest to document and the safest base case for underwriting.

- Short-term rent (under 30 days) may be excluded entirely — FHA appraiser guidance bars transient and sub-30-day comparables.

- Mid-term rent (30+ days, furnished) still must be validated under the lender’s rules.

Financeable rental ADU checklist

| Requirement | Why it matters | Where to verify |

|---|---|---|

| Legal ADU status | Illegal-ADU rent can’t be used to qualify (Freddie Mac) | City planning/building department |

| Rental allowed | Some cities restrict separate or short-term rental | Local ordinance |

| Appraiser-supported rent | Lender needs documented market rent (Form 1007; Freddie comps) | Appraisal |

| Lease or market-rent support | Determines usable rent | Lease, rent comps |

| Borrower reserves | FHA requires 2 months PITI; many lenders require more | Loan program / lender |

| Insurance + tax impact | Affects cash flow and assessed value | Insurer, county assessor |

| Utility plan | Affects build cost and operating cost | Contractor / utility |

What If You Want Short-Term or Mid-Term Rental Income?

Don’t build the financing plan around Airbnb-style revenue unless your lender, your city, and the appraisal documentation all support it. Most underwriting paths strongly prefer legally rentable, appraiser-supported, long-term monthly rent — and FHA explicitly excludes transient and sub-30-day comparables from ADU market-rent support. Short-term rental upside is real, but it’s the wrong foundation for a loan.

Why STR income is risky in underwriting: many cities ban or cap short-term rentals or require scarce permits; STR revenue is seasonal and volatile; platform policies can change; and lenders frequently won’t accept projected nightly-rate income at all.

The safer approach: underwrite the deal on long-term rent as the base case — that’s the number that has to make the loan and the cash flow work. Treat any short-term or mid-term premium as optional upside you capture only if it’s legal and permitted in your jurisdiction. That way, a change in local STR rules dents your upside instead of breaking your loan.

Before you bank on any rental strategy, check what’s allowed at your address. Local rental rules vary block by block, and it’s free to find out where you stand.

Check what’s allowed at your address →How Should You Model the Rental Before You Borrow?

Model the ADU like a small rental business, not just a construction project. The rent has to cover far more than the loan payment — vacancy, maintenance, insurance, taxes, utilities, management, and reserves all come out of it before anything reaches your pocket. A unit that “covers the mortgage” in a perfect month can still lose money across a real year.

Agency rent calculations already haircut rent to 75% to account for vacancy and expenses — and your own cash-flow model should separately budget for those same realities rather than assuming the haircut covers them.

Rental cash-flow stress test

| Line item | Conservative modeling note |

|---|---|

| Gross rent | Use supported long-term rent first, not best-case STR |

| Vacancy | Budget for it even in strong markets |

| Maintenance | Plan for ongoing repairs and capital items |

| Utilities | Confirm separate meters or a reimbursement structure |

| Insurance | Get a quote before construction |

| Property tax | Adding an ADU can raise assessed value (typically the added value is reassessed — verify locally) |

| Management | Include software cost or your own time |

| Reserves | Keep cash for overruns and vacancy |

| Loan payment | Use real, current terms — not a temporary teaser |

| Permits & impact fees | Verify locally; they vary widely by city |

Illustrative-example disclaimer: These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, vacancies, and regulatory approvals.

Planning to rent it out? Set up the rental side before you borrow. Knowing your real operating costs makes every financing conversation sharper.

Explore landlord and rental-accounting tools with Buildium →When Should You Not Finance an ADU Rental Yet?

Some ADU rental projects shouldn’t be financed yet. If the only way the numbers work is by assuming unverified rent, unpermitted rental use, zero cost overruns, no vacancy, or a refinance exit you haven’t pre-screened, the safer move is to fix feasibility, reduce scope, or pick a different path before you borrow.

The reassuring part: almost every item below is fixable before you borrow. Catching it now is exactly how you avoid the painful version — the homeowner who spends thousands on stamped architectural drawings, then learns they qualify for far less financing than the design requires, and has to start over on a smaller plan.

Red flags to resolve first

- The ADU isn’t legal to rent under local zoning. → See your regulations hub.

- Your city restricts the rental use you’re counting on (often STR).

- The lender won’t count the rent you need. → See the agency rules above.

- Your current mortgage is too valuable to replace without a clear reason.

- The plan depends on a post-construction refinance but you haven’t identified the takeout lender.

- The builder’s rent or value estimate isn’t independently supported.

- There’s no reserve for overruns or vacancy.

- You need short-term rental income to qualify but only long-term rent is supportable.

If the blocker is equity, look at renovation/construction financing. If it’s qualification, revisit the agency rules and consider a co-borrower or a larger down payment. If it’s cost, scope down or change ADU type. If it’s local legality, start with a feasibility check. None of these means “no ADU” — they mean “not this loan, this way, yet.”

Find out which blocker applies to you — and what to do instead.

Check my property, free →Step by Step: How to Finance an ADU Rental Safely

The safest order is feasibility first, rent proof second, financing path third, loan application fourth. Borrowing before you’ve confirmed legal rentability and basic cash-flow resilience is where most ADU rental plans turn fragile.

- Confirm the ADU can be legally built and rented. Check your city planning page, your state ADU law, and (if relevant) your HOA documents.

- Estimate realistic rent. Use HUD FMR as a benchmark, then local comps, a property manager’s estimate, and appraiser-supported rent where needed — with long-term rent as your base case.

- Estimate total project cost. Include design, permits, site work, utility upgrades, construction, contingency, financing costs, and rental setup.

- Decide whether to protect your first mortgage. Compare your current rate, balance, and term against the cost of a refinance versus a second-lien option.

- Choose the financing lane to test first. Use the decision matrix above.

- Ask the lender the rental-income questions before applying. Use the checklist below.

- Build the draw and contingency plan. Map contractor milestones, inspection timing, permit risk, an overrun cushion, and your takeout strategy.

- Set up the rental business before move-in. Lease, tenant screening, accounting, insurance, and a maintenance process.

Step 1 is the cheapest and most important move you can make.

See what’s possible at your address → get your free ADU report.

Get my free ADU report →Want all of this in one place? A financing checklist, the lender-question list, and pre-approval prep, in one PDF.

Download the free ADU Starter Kit →What Should You Ask Lenders Before Applying?

The right question isn’t “Do you finance ADUs?” — it’s “For my occupancy, loan purpose, ADU status, and rental plan, what ADU rent can you use, what documents do you require, and what limits apply?”

- Do you allow ADU rental income for this loan type?

- Does the ADU need to already exist?

- Can projected rent be used?

- What percentage of the rent can be counted?

- Is there a cap on how much ADU rent can contribute to qualifying income?

- Do you require Form 1007, Form 1025, a lease, or another rent schedule?

- Do you require ADU rental comparables?

- Can short-term rental income be used?

- Does the ADU need to be legal, legal nonconforming, or separately permitted?

- Are cash reserves required, and how many months?

- Does the loan allow construction draws?

- Will this replace my first mortgage?

- What happens if the project costs more than expected?

- What's the takeout/refinance plan after completion?

- Do you apply overlays beyond Fannie/Freddie/FHA rules?

What Documents Do You Need to Finance an ADU Rental?

Expect to document the property, the project, the rent, the borrower, and the legal use — and the more your financing leans on ADU rent, the more proof the lender will want.

| Category | Documents | Who typically asks for it |

|---|---|---|

| Property | Mortgage statement, tax bill, insurance, HOA docs, title information | All lenders |

| ADU legality | Zoning confirmation, permits, plans, certificate of occupancy | All lenders; local permit office issues them |

| Project | Contractor bid, scope of work, plans, budget, timeline | Renovation/construction lenders |

| Rent support | Lease, rent schedule, Form 1007/1025, rent comps | Fannie, Freddie, FHA, DSCR (when using rent) |

| Borrower | Income, assets, debts, credit, reserves | Owner-occupied loans (Fannie/Freddie/FHA) |

| Loan-specific | Renovation paperwork, draw schedule, appraisal, contractor approval | Renovation/construction lenders |

| Rental setup | Lease template, screening criteria, insurance, accounting system | You (for operations); lenders may ask for the lease |

How the Answer Changes: Owner-Occupant vs. House Hacker vs. Investor

Owner-occupants care most about protecting a low first mortgage and whether ADU rent can help them qualify. House hackers care about rent offset and flexibility. Investors care about DSCR, exit value, and whether the property’s cash flow supports the loan — and they play by different rules entirely.

Owner-occupant

Best paths: HELOC or home equity loan (preserve the first mortgage), renovation loan (if you need future value), cash-out refinance (only if replacing the first mortgage makes sense), or a conventional/FHA purchase mortgage if you’re buying a home with an existing legal ADU. The Fannie Mae and FHA owner-occupant rent rules are written for you.

House hacker

You live in one unit and rent the other. Best paths: a purchase mortgage with ADU-income review, a renovation mortgage, or FHA 203(k) where appropriate. Underwrite on a conservative long-term-rent base case so a soft rental month doesn’t sink you.

Investor (non-owner-occupied)

The agency owner-occupant rules don’t apply. Best paths: DSCR or portfolio loans, hard money/bridge only with a clear exit, or a conventional investment-property loan where the rules fit. Plan for property management and reserves from day one.

The Biggest ADU Rental Financing Mistakes

The single biggest mistake is borrowing based on the rent you hope to get instead of the rent a lender, an appraiser, and your local ordinance will actually support. Almost every other mistake on this list is a version of that one.

- Assuming all expected rent counts as qualifying income (it’s haircut to 75% and capped at 30%).

- Assuming projected rent counts before the ADU exists.

- Ignoring the 30% qualifying-income cap.

- Replacing a low-rate first mortgage without comparing total debt cost.

- Building an ADU that’s legal to occupy but not legal to rent as planned.

- Using short-term rental revenue as the base case without verifying city and lender rules.

- Forgetting vacancy, maintenance, insurance, taxes, utilities, and management.

- Taking a short-term construction or bridge loan with no takeout plan.

- Trusting builder rent/value claims without independent proof.

- Leaving no contingency for cost overruns.

What We Verified

Last verified:

We verified, against primary or highly authoritative sources:

- Fannie Mae ADU rental-income conditions — existing ADU on a one-unit principal residence, purchase/limited cash-out refi, one-ADU limit, 30% qualifying-income cap, 75% gross-rent treatment, first-time-landlord PITIA limit, and the DU 12.1 rollout (weekend of March 21, 2026). (Fannie Mae Selling Guide B3-3.8-01; SEL-2025-08; Fannie Mae ADU fact sheet.)

- Freddie Mac ADU rules — one-unit primary residence, purchase/no-cash-out refi, 75% lease treatment, 30% cap, full-appraisal requirement (≥1 ADU sale comp + ≥3 rental comps, ≥1 rented ADU), landlord-education requirement, and illegal-ADU income exclusion. (Freddie Mac Guide §5306.1(g); Freddie Mac ADU fact sheet.)

- FHA ADU treatment — 75% of supported rent up to a 30% cap, two months PITI reserves, FHA Standard 203(k) 50% rule for certain no-history cases, and the FHA cash-out exclusion. (HUD Mortgagee Letter 2023-17.)

- USDA status — current SFHGLP prohibition on income-producing ADUs, plus the proposed rule (docket RHS-26-SFH-0100, Federal Register 03/31/2026, comments due 06/01/2026; proposed, not final). (Federal Register; USDA Rural Development.)

- California ADU statutory framework now codified at Government Code §§66310–66342 (renumbered in 2024). (California HCD ADU Handbook, updated March 2026.)

- DSCR structure and the common comparable-ADU lender overlay. (Griffin Funding, New American Funding, theLender, OfferMarket — 2026.)

- ADU financing-mix statistic — among California owners using mortgage products, 56% HELOC/home-equity, 35% cash-out refi, 6% construction/renovation. (Urban Institute analysis of UC Berkeley Terner Center data, 2024.)

- HUD FY2026 Fair Market Rent dataset and methodology. (HUD User.)

Reader caveats we want to be transparent about:

- HUD FMR figures in our sample table are rounded benchmarks; HUD revises FMRs during the year and uses Small Area FMRs by ZIP in some metros — confirm your exact area on the live HUD dataset.

- VA ADU rental-income treatment is not established by a clear nationwide rule we could confirm; verify with the VA Lender’s Handbook and your lender.

- All program rules are subject to individual lender overlays. None of this is a promise of approval, a rate quote, or financial advice.

Methodology

This guide was built by The Dwelling Index, an independent research resource covering ADU financing, costs, and regulations. We prioritized official agency guidance for lending rules, HUD data for rent benchmarks, and homeowner discussions only for identifying real questions and decision friction — never for legal, lending, or cost claims.

We reviewed primary and authoritative sources from Fannie Mae, Freddie Mac, HUD/FHA, USDA, the California Department of Housing and Community Development, and HUD User’s FY2026 Fair Market Rent dataset, then translated those rules into a rental-first decision framework and an original rent-underwriting screening table that combines the FMR benchmark, the 75% haircut, and the 30% cap in one place.

We do not rank lenders by payout. Financing paths are organized by borrower situation, property use, documentation requirements, and practical risk. We present financing as path education, not “best lender” rankings, and we never quote specific rates, APRs, or payments as guarantees.

Affiliate disclosure: The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Full disclosure →

Frequently Asked Questions

What is the best way to finance an ADU rental?

For many homeowners, the first path to test is a HELOC or home equity loan — if you have enough equity and want to preserve a low first mortgage. If you need future value or construction draws, a renovation or construction-to-permanent loan often fits better. If the ADU already exists and is legally rentable, a conventional or FHA mortgage may let some of the rent help you qualify (at 75% of rent, capped at 30% of qualifying income).

Can ADU rental income help me qualify for a mortgage?

Yes, under specific program rules. Fannie Mae, Freddie Mac, and FHA each allow ADU rental income on a one-unit principal residence, and when lease or appraiser-supported market rent is used they apply a 75% calculation and cap it at 30% of your total qualifying income. Don't assume all your expected rent will count.

Can I use future ADU rent before the ADU is built?

Sometimes, but it's program-specific. FHA's Standard 203(k) allows up to 50% of estimated rent in certain no-history new-ADU cases. Conventional and portfolio lenders are most comfortable with an existing, appraiser-supported ADU, so verify the not-yet-built scenario with your lender. Never assume projected rent always counts.

Does Fannie Mae count ADU rental income?

Yes, for an existing ADU under conditions set in SEL-2025-08 (Oct 2025): one-unit principal residence, purchase or limited cash-out refinance, one ADU, 75% of gross rent, capped at 30% of qualifying income, with a first-time-landlord limit. Desktop Underwriter automated the rule with version 12.1 the weekend of March 21, 2026.

Does Freddie Mac count ADU rental income?

Yes, under §5306.1(g): a one-unit primary residence, purchase or no-cash-out refinance, 75% of the lease amount, capped at 30% of total stable monthly income, with a full appraisal (one ADU sale comp plus three rental comps, at least one a rented ADU) and a landlord-education requirement unless you have a year of landlord experience.

Does FHA count ADU rental income?

Yes, per HUD Mortgagee Letter 2023-17: 75% of appraiser-supported rent, capped at 30% of monthly income, with two months of PITI reserves — and a special 50% rule under Standard 203(k). FHA cash-out refinances cannot use ADU rental income.

Can I use a HELOC to build an ADU rental?

Yes, if you have enough equity and qualify for the line. A HELOC's big advantage is that it preserves your existing first mortgage. Its limit: it usually won't help you qualify on future ADU rent — that comes through agency purchase/refinance rules instead.

Is a cash-out refinance good for an ADU rental?

It can be, especially if your current rate is high or you want a single loan. It's a poor fit if it would replace a valuable low-rate first mortgage, or if you're counting on ADU rent that the program won't allow — notably, FHA cash-out refinances can't use ADU income.

Can I use Airbnb income to qualify?

Usually not. Many lenders won't accept projected short-term rental income, and FHA appraiser guidance excludes transient and sub-30-day comparables from ADU market-rent support. Underwrite on long-term rent and treat short-term revenue as optional upside.

What if my ADU is unpermitted?

That's a serious financing and rental problem. Freddie Mac states that rental income from an illegal ADU can't be used to qualify, and an unpermitted unit raises insurance, resale, and liability risks. Bringing it into compliance can unlock both financing and value.

Do I need landlord experience?

For some scenarios, yes. Freddie Mac requires at least one qualifying borrower to complete a landlord-education program for a purchase using ADU rent, unless they have at least one year of landlord experience. Fannie limits first-time-landlord qualifying rent to no more than the borrower's PITIA.

Should I finance an ADU rental if the rent barely covers the loan?

Only after stress-testing vacancy, maintenance, insurance, taxes, utilities, management, reserves, and cost overruns. Rent covering the loan in a perfect month is not the same as a rental that holds up across a real year.

Not sure where to start?

See what’s possible at your address — get your free ADU report in about 60 seconds.