Fannie Mae vs Freddie Mac ADU Rules: 2026 Side-by-Side Guide

The bottom line on Fannie Mae vs Freddie Mac ADU rules (read this first)

Both GSEs now allow rental income from one ADU on a one-unit principal residence toward qualifying income, capped at 30% of total qualifying income. Fannie’s change took effect October 8, 2025 (SEL-2025-08); Desktop Underwriter 12.1 applies it automatically since March 21, 2026. Freddie has allowed it since 2022 under Section 5306.1. The rules diverge on property type, multiple ADUs, manufactured homes, appraisal evidence, zoning exceptions, and renovation-funded rent.

Fannie operates in two lanes in 2026: a standard lane (UAD 2.6) — one ADU on one-unit properties only — and an expanded UAD 3.6 lane (effective March 31, 2026) that opens up to three ADUs on a one-unit property, ADUs on 2- and 3-unit properties, and ADUs on single-section manufactured homes. Freddie under standard policy allows one ADU on 1-, 2-, and 3-unit properties and added multi-wide manufactured-home primaries under Bulletin 2025-15.

Articles published before October 2025 that say “Freddie allows ADU income, Fannie doesn’t” are now out of date.

Quick decision table: find your row

| Your situation | Where to start |

|---|---|

| One-unit primary + one existing legal ADU + need rent to qualify | Either GSE — compare the rental-income rules below |

| One-unit property + two or three legal ADUs | Fannie UAD 3.6 lane, if your lender supports it |

| Duplex or triplex + one ADU | Freddie today; Fannie UAD 3.6 once your lender adopts it |

| Fourplex + ADU | Not eligible either GSE — ask about non-agency/portfolio options |

| Planning to build an ADU with renovation proceeds and count future rent | Caution — restricted on both GSEs; see the renovation section |

| ADU rental income from a separate investment property | Freddie explicitly covers this; Fannie may under general rental rules |

| Illegal or non-conforming ADU | Check legality and appraisal support first; Freddie 5601.2(c) may help on a 1-unit |

Free. No signup required. Results in 60 seconds.

By the Dwelling Index Editorial Team · Last updated: May 21, 2026 · Last verified: May 21, 2026 · ~45 min read

Independent editorial comparison. The Dwelling Index is not a lender, broker, or builder. See our affiliate disclosure below.

A note on what this page is and isn’t

We built this page for one reader: someone with an existing or planned ADU who needs to know which conventional rule lane — Fannie standard, Fannie UAD 3.6, or Freddie Mac — fits their file. We did not build it as a generic “what is an ADU” primer or a “best ADU loan” review. If you’re earlier in the journey, our What Is an ADU and ADU Grants by State guides will serve you better.

The rules below come straight from the Fannie Mae Selling Guide and the Freddie Mac Single-Family Seller/Servicer Guide, with every claim tied to a section or announcement number. We are not a lender, broker, or builder. We do not give legal, tax, or financial advice. Verify every rule with your loan officer before making a financing decision. Both GSEs publish regular guide, bulletin, and release-note updates — we re-verify this page quarterly and immediately after any update that touches ADU-related sections.

Fannie Mae vs Freddie Mac ADU Rules: 2026 Comparison Matrix

| Rule | Fannie Mae (Standard / UAD 2.6) | Fannie Mae (UAD 3.6 lane, eff. Mar 31, 2026) | Freddie Mac | Source |

|---|---|---|---|---|

| ADU definition | Independent living/sleeping/cooking/bath; same parcel as a primary one-unit dwelling; access without going through the primary; kitchen needs cabinets, countertop, sink with running water, and stove or stove hookup | Same definition, expanded structural eligibility | Living area independent of primary dwelling with separate entrance; same lot; full kitchen + bath + sleeping | Fannie B4-1.3-05; Freddie 5601.2 |

| ADUs on a 1-unit property | 1 ADU | Up to 3 ADUs | 1 ADU | SEL-2025-10; Freddie 5601.2 |

| ADUs on a 2- or 3-unit property | Not eligible | Eligible, provided total dwelling units + ADUs ≤ 4 (a duplex may add up to two ADUs; a triplex may add one) | 1 ADU (since 2022) | SEL-2025-10; Freddie 5601.2 |

| ADUs on a 4-unit property | Not eligible | Not eligible | Not eligible | — |

| Primary dwelling type when ADU is present | Must be site-built or modular; the ADU itself may be site-built, factory-built, modular, or HUD-Code manufactured if classified as real property | Adds manufactured-home primaries (see MH row) | Site-built, modular, or (per Bulletin 2025-15) multi-wide manufactured home | Fannie B2-3-04; Freddie 5601.2; Bulletin 2025-15 |

| Manufactured-home primary with an ADU | Addressed in the UAD 3.6 expansion, not the standard lane | Single-section standard MH (excl. MH Advantage): 1 ADU. Multi-section MH or single-section MH Advantage: up to 3 ADUs, subject to the dwelling-unit-plus-ADU limit | Multi-wide MH including CHOICEHome (eff. settlements ≥ Feb 9, 2026) | SEL-2025-10; Bulletin 2025-15 |

| Count ADU rent (subject 1-unit primary) | Yes — purchase + limited cash-out refi; one ADU’s rent only; 30% of total qualifying income cap | Yes — same rule, automated in DU 12.1 (live since Mar 21, 2026) | Yes — purchase + no-cash-out refi; lease-documented income capped at 75% of lease; 30% of total qualifying income cap | SEL-2025-08; B3-3.8-01; Freddie 5306.1 |

| Count ADU rent from a non-subject investment property | Not under the ADU carveout; may be eligible under Fannie’s general non-subject rental-income rules if documented and otherwise eligible | Same | Explicitly eligible — Freddie names this context directly | B3-3.8-01; Freddie 5306.1 |

| Rent calculation (lease or market rent) | 75% of gross monthly rent or market rent (B3-3.1-08) | Same | 75% of the lease amount or market rent | B3-3.1-08; Freddie Rental Income Matrix |

| First-time landlord (subject 1-unit primary) | If borrower has <12 months property-management experience and a current housing payment, qualifying ADU rent cannot exceed the subject property’s PITIA. If the borrower has no current primary housing payment, ADU rental income may not be used to qualify | Same | Landlord education required for purchase use unless ≥1 year landlord/property-management experience | Fannie B3-3.1-08; Freddie 5306.1 |

| Multiple ADUs: how many ADUs’ rent can count? | One (subject 1-unit primary), even if multiple ADUs exist | One, even if up to three ADUs exist | One on a subject 1-unit primary | SEL-2025-08; Freddie 5306.1 |

| Appraisal forms (1-unit + ADU) | Form 1004 + Form 1007; appraiser may use non-ADU comps with adjustments if no ADU comps exist | Same forms, UAD 3.6 data standard | Full appraisal required when subject 1-unit ADU rent is used; at least 1 ADU comparable sale; 3 rent comps including at least 1 rented ADU | B3-3.1-08; Freddie 5601.12 |

| Value acceptance / appraisal waiver | Not available when rental income from the subject property is used to qualify; otherwise file-dependent | Same | ACE (Automated Collateral Evaluation) not acceptable when subject 1-unit ADU rent is used | Fannie B4-1.4-10; Freddie 5601.12 |

| Zoning compliance | Legal, legal non-conforming, or unzoned; an ADU not allowed under zoning may be eligible if the lender confirms it doesn’t jeopardize insurance and appraisal conditions are met | Same; UAD 3.6 appraisal policy also addresses non-compliant zoning with comparable-sales support | Legal, legal non-conforming, or unzoned; illegal-zoning exception for 1-unit + ADU under 5601.2(c) with 2 similarly non-compliant comps | B2-3-04; B4-1.4-10; Freddie 5601.2(c) |

| Single-close construction/renovation product | HomeStyle Renovation; HomeStyle Refresh (eff. Mar 31, 2026; smaller-scope, can add or renovate an ADU within its scope) | Same | CHOICERenovation; CHOICEReno eXPress (small projects) | Fannie B5-3.2, B5-3.3-01; Freddie Chapter 4607 |

| Renovation cost cap | Up to 75% of as-completed value (site-built); manufactured-home renovations capped at 50% of as-completed value | Same | Up to 75% of as-completed value | SEL-2025-10; B5-3.2; Freddie 4607 |

| Upfront disbursement at closing (renovation loan) | Up to 50% of renovation funds (since Dec 10, 2025) | Same | Standard escrow holdback | SEL-2025-10; Freddie 4607 |

| Renovation completion deadline | 15 months | Same | 450 days standard; 180 days CHOICEReno eXPress | Fannie B5-3.2; Freddie 4607 |

| Counting renovation-funded ADU rent to qualify | ADU rental-income rule is framed around an existing ADU | Same | For CHOICERenovation applications received ≥ May 4, 2026, rental income from any unit included in the funded renovation project cannot be used to qualify | Freddie Bulletin 2026-1 |

| Minimum down payment with ADU (1-unit primary) | As low as 3% with HomeReady | Same | As low as 3% with Home Possible or HomeOne | Fannie B5-6; Freddie 4501 |

| Automated underwriting system | Desktop Underwriter (DU) — version 12.1 applies ADU income automatically (live since Mar 21, 2026) | Desktop Underwriter 12.1 | Loan Product Advisor (LPA) — Asset and Income Modeler accepts rental income for submissions ≥ Mar 1, 2026; CHOICERenovation update live in LPA Apr 12, 2026 | DU 12.1 Release Notes; Bulletin 2025-15; Bulletin 2026-1 |

| UAD 3.6 status | Optional through Nov 1, 2026 | Required for the expanded ADU eligibility above; mandatory for all new appraisals submitted to UCDP on or after Nov 2, 2026 | Freddie moving to UAD 3.6 on its own appraisal path in 2026 | UAD 3.6 Policy Supplement |

See your lot fit, size cap, and city fees first — then you’ll know which financing ceiling you actually need.

Find Your Conventional ADU Path in 60 Seconds

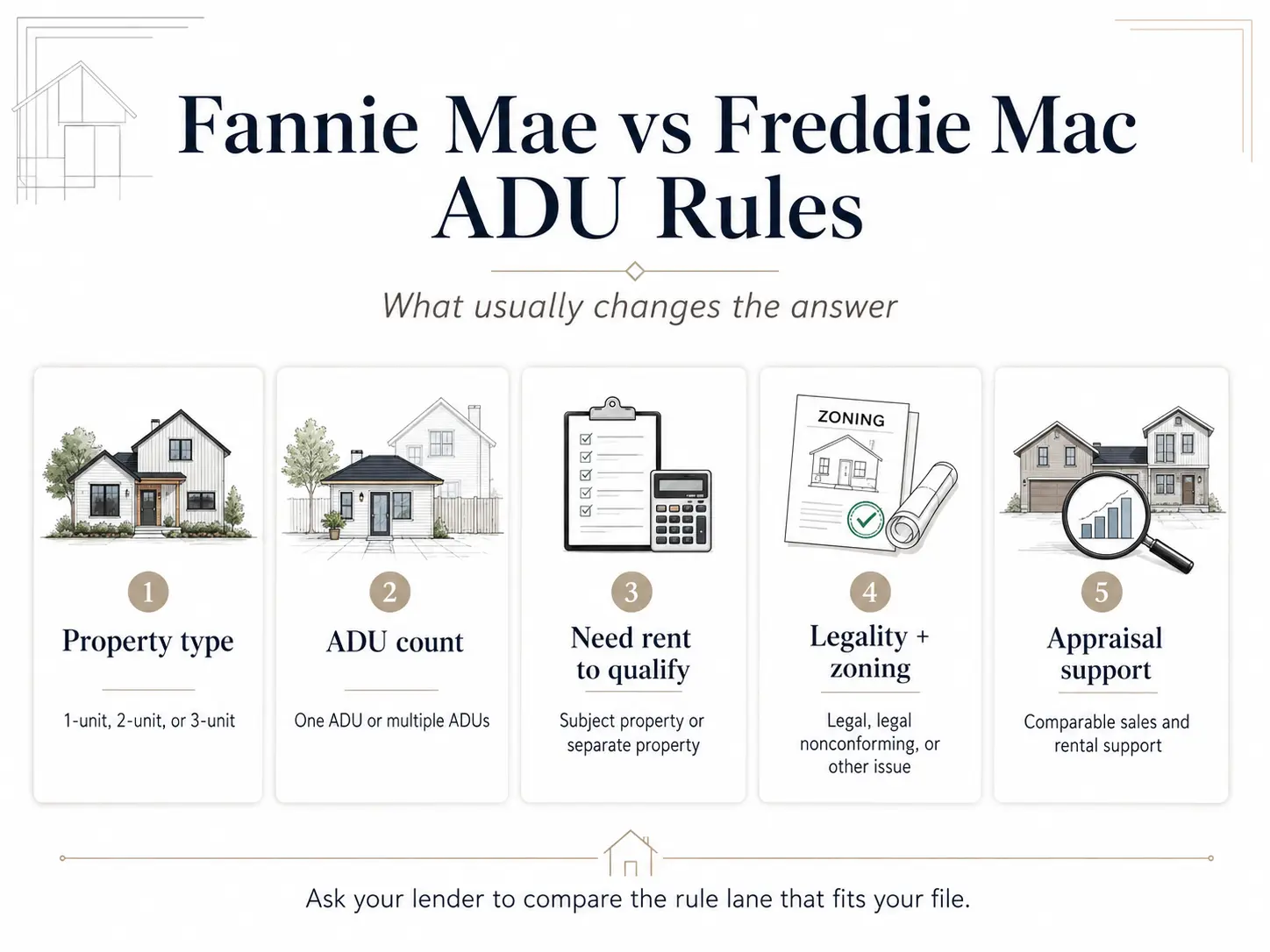

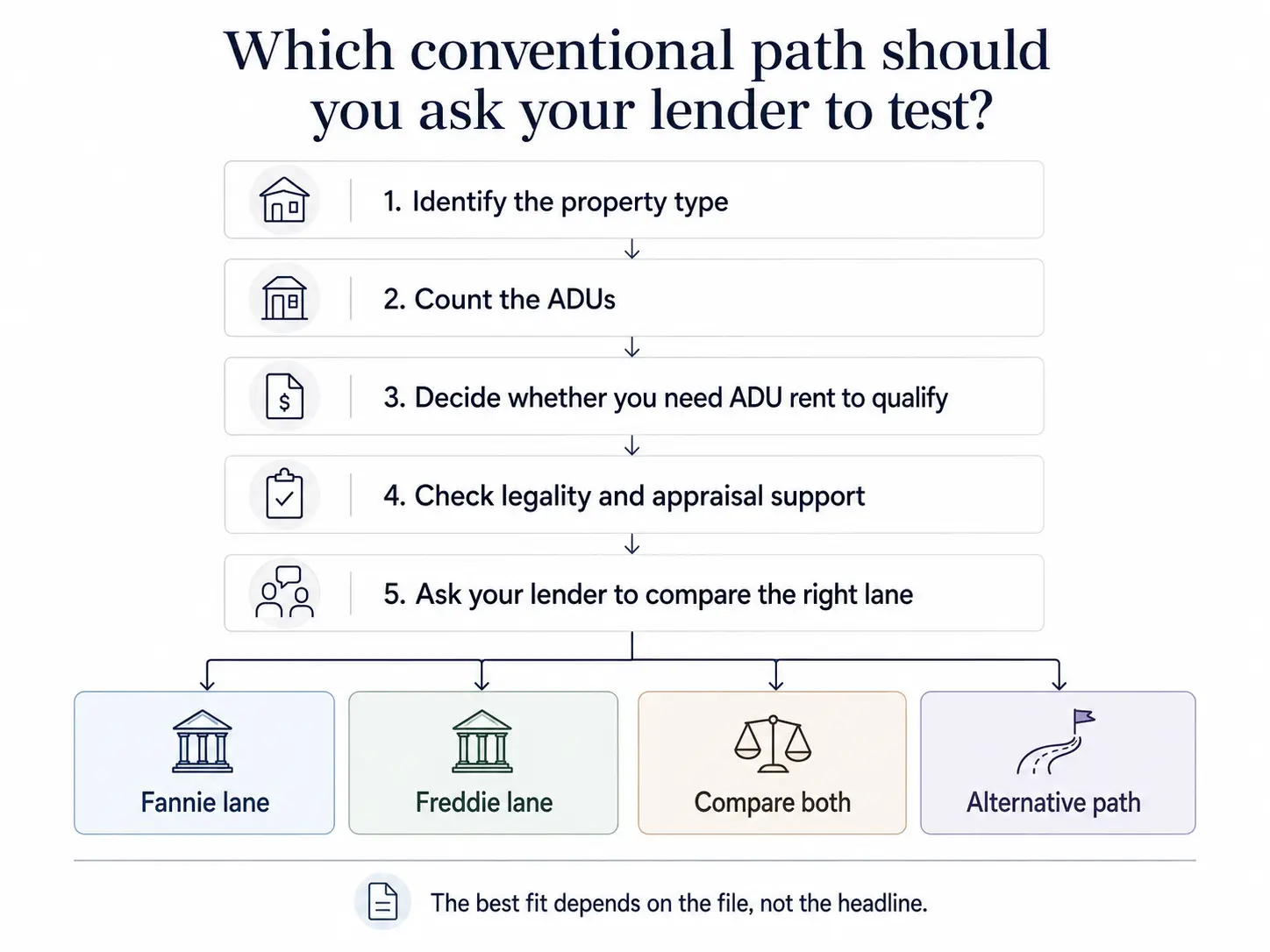

Five questions to find your lane

- Property type: Is the subject property a 1-unit, 2-unit, 3-unit, 4-unit, or manufactured home? (4-unit is ineligible either GSE; MH requires specific lanes.)

- ADU count: How many ADUs exist or are planned? (One ADU: any lane. Two or three ADUs: Fannie UAD 3.6 only. Four+: not eligible.)

- Need rent to qualify? If yes, which context — subject property, non-subject investment property, or future rent from a unit being renovated? (Future renovation rent is restricted on both GSEs.)

- ADU legal status: Legal, legally non-conforming, unzoned, or not permitted? (Illegal ADU rent may not be used; see Freddie 5601.2(c) for the one-unit exception.)

- Landlord experience: Fewer than 12 months of property-management experience triggers additional restrictions under both GSEs.

The exact question to ask your lender:

“Are you running this under Fannie standard, Fannie UAD 3.6, or Freddie — and which guideline section applies to the ADU rental-income treatment on my file?”

Free, no signup, 60 seconds.

What changed in 2025–2026 (the updates that rewrote this topic)

October 8, 2025 — Fannie Mae SEL-2025-08

For the first time, Fannie allowed rental income from one ADU on a one-unit principal residence to count toward qualifying income. Cap: 30% of total qualifying income. Eligible loan purposes: purchase and limited cash-out refinance. Lenders with manual underwriting authority could apply it immediately. Sections updated: B3-3.1-08 and B3-3.2-02.

November 5, 2025 — Freddie Mac Bulletin 2025-15

Freddie expanded manufactured-home ADU rules: the primary dwelling may now be a multi-wide manufactured home (including CHOICEHome) with an ADU. Effective for mortgages with settlement dates on or after February 9, 2026 (lenders permitted to implement immediately). The same bulletin added rental income as an eligible income type for Asset and Income Modeler automated assessments using tax data, effective March 1, 2026.

December 10, 2025 — Fannie Mae SEL-2025-10

The biggest single ADU expansion in Fannie’s history. Three structural changes, all effective March 31, 2026 and gated to lenders using UAD 3.6 appraisals:

- Up to three ADUs allowed on a one-unit property.

- ADUs newly allowed on 2- and 3-unit properties, provided total dwelling units plus ADUs does not exceed four. A duplex may add up to two ADUs; a triplex may add one.

- ADUs newly permitted on single-section standard manufactured homes (one ADU); multi-section MH and single-section MH Advantage primaries may include ADUs up to the four-unit ceiling.

The same announcement introduced HomeStyle Refresh (replacing HomeStyle Energy), removed the $50,000 renovation cap on manufactured-home renovations (now capped at 50% of as-completed value), and allowed HomeStyle Renovation to disburse up to 50% of renovation funds at closing — effective December 10, 2025.

February 4, 2026 — Freddie Mac Bulletin 2026-1

Freddie clarified construction-to-permanent and renovation mortgage requirements and — critically for ADU planners — added specificity to CHOICERenovation. For applications received on or after May 4, 2026, rental income from any unit included in the renovation project funded by the mortgage proceeds cannot be used to qualify the borrower. Only rental income from units not included in the renovation project may count. Loan Product Advisor was updated April 12, 2026 to support the change. If you planned to build an ADU with CHOICERenovation and rely on the new ADU’s future rent to qualify, this rule closes that door.

March 21, 2026 — Fannie Mae DU Version 12.1

Desktop Underwriter 12.1 went live the weekend of March 21, 2026 and now applies SEL-2025-08’s ADU rental-income rule automatically. New loan casefiles submitted on or after that weekend run the updated logic — including the 30% cap calculation — while older casefiles continue under DU 12.0.

November 2, 2026 — UAD 3.6 becomes mandatory

All new appraisal reports submitted to the Uniform Collateral Data Portal (UCDP) must use UAD 3.6 on or after this date. Until then, UAD 3.6 is optional. That’s why Fannie’s December 2025 structural expansion is gated: lenders that haven’t adopted UAD 3.6 early can’t use the expanded eligibility yet.

Free, no signup, 60 seconds.

Fannie Mae ADU rules in 2026, decoded

How Fannie Mae defines an ADU

Selling Guide Section B4-1.3-05 defines an ADU as “an additional living area independent of the primary dwelling that may have been added to, created within, or detached from a primary one-unit dwelling.” It must include living, sleeping, cooking, and bathroom facilities on the same parcel and be accessible without going through the primary residence, with some expectation of privacy.

Fannie spells out kitchen minimums: cabinets, a countertop, a sink with running water, and a stove or stove hookup. A finished basement with a microwave and a hot plate is not an ADU. We flag this because appraisers routinely reclassify “ADUs” as ordinary finished space when the kitchen requirements aren’t met — and that reclassification can shift the property’s eligibility entirely.

How many ADUs Fannie Mae allows

Under standard rules (UAD 2.6 lane), Fannie allows one ADU on a one-unit property and no ADUs on a 2-, 3-, or 4-unit dwelling. Under the UAD 3.6 lane effective March 31, 2026 (SEL-2025-10):

- One-unit property: up to three ADUs.

- Two- or three-unit property: ADUs allowed provided total dwelling units + ADUs ≤ 4.

- Single-section standard MH as primary (excl. MH Advantage): one ADU classified as real property.

- Multi-section MH or single-section MH Advantage as primary: up to three ADUs, subject to the dwelling-unit-plus-ADU limit.

These limits are gated to lenders using UAD 3.6. Until November 2, 2026, UAD 3.6 is optional — many lenders haven’t adopted it yet. The first practical question to ask any lender is whether their appraisal workflow is on UAD 3.6.

Using ADU rental income with Fannie Mae

Under SEL-2025-08, effective October 8, 2025, Fannie allows rental income from one ADU toward qualifying income on a one-unit principal residence, provided all of the following:

- The property is a one-unit, principal residence.

- The transaction is a purchase or a limited cash-out refinance.

- The rental income is derived from only one ADU, even if multiple ADUs exist.

- The amount used for qualifying does not exceed 30% of the borrower’s total qualifying income.

- Standard documentation under B3-3.1-08 applies — typically a Form 1004 appraisal plus a Form 1007 Single-Family Comparable Rent Schedule, or a current lease.

Two sub-rules catch borrowers off guard. First, under B3-3.1-08, when the borrower has fewer than 12 months of property-management experience and a current housing payment, qualifying ADU rent cannot exceed the subject property’s PITIA (principal, interest, taxes, insurance, and association dues). Second — and this is a hard stop — if the borrower has no current primary housing payment, rental income from a one-unit principal residence with an ADU may not be used to qualify at all.

Worked example: Fannie Mae ADU rental income math

Illustrative scenario: W-2 borrower, $6,000/month income, more than 12 months of landlord experience, current housing payment, buying a one-unit primary with an existing legal ADU. Lease: $2,000/month; Form 1007 supports $2,000 market rent.

- Step 1 — Apply the 75% rental-income calculation: $2,000 × 75% = $1,500/month usable rent.

- Step 2 — Apply the 30% cap: ADU rent can’t exceed 30% of total qualifying income. Solve X ≤ 0.30 × (6,000 + X), which gives X ≤ $2,571. The $1,500 fits.

- Step 3 — First-time landlord check: not triggered here (more than 12 months experience). If triggered, qualifying rent would also be capped at the subject PITIA.

Total qualifying income: $6,000 + $1,500 = $7,500/month.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Building an ADU with Fannie Mae: HomeStyle Renovation

HomeStyle Renovation is Fannie’s single-close purchase-or-refinance plus renovation product. The appraisal is performed on an “as-completed” basis — the appraiser values the property as if the renovation, including the ADU, is finished, based on plans, specifications, and contractor bids. Site-built renovation costs may go up to 75% of the as-completed value; manufactured-home renovations are capped at 50% of as-completed value. Effective December 10, 2025 (SEL-2025-10), HomeStyle Renovation now allows up to 50% of total renovation costs to be disbursed at closing. Down payments can be as low as 3% when combined with HomeReady on a one-unit primary. Renovation completion deadline: 15 months from closing. See our Fannie Mae HomeStyle Renovation for ADUs guide for full details.

HomeStyle Refresh: a smaller-scope option that can include an ADU

HomeStyle Refresh, effective March 31, 2026, replaces HomeStyle Energy. It finances improvements up to 15% of the as-completed appraised value — cosmetic and functional upgrades, energy efficiency, resiliency, disaster preparedness, and environmental remediation. Fannie’s B5-3.3-01 expressly lists adding or renovating an accessory dwelling unit as an eligible improvement when the work fits within the 15% cap and the product’s scope. It carries a 180-day completion timeline and doesn’t require special lender approval. For larger ADU construction, HomeStyle Renovation remains the main Fannie lane.

HomeReady with an ADU

HomeReady is Fannie’s affordable-lending product — a 3% down option for borrowers at or below 80% of area median income. ADUs are eligible, and ADU rental income may be used under the SEL-2025-08 rules. Boarder income is also allowed under HomeReady up to 30% of qualifying income, documented under Selling Guide Section B3-3.4-04. In a high-cost market, if your income is within the limits, HomeReady is often the cleanest path for a first-time buyer who wants an ADU.

Freddie Mac ADU rules in 2026, decoded

How Freddie Mac defines an ADU

Section 5601.2 defines an ADU as a living area independent of the primary dwelling unit, with a separate entrance, that includes living, sleeping, cooking, and bathroom facilities, on the same lot as the primary residence. Shared walls or utilities don’t disqualify it — independence and the separate entrance do the work. ADUs are acceptable on 1-, 2-, and 3-unit properties. A 2- or 3-unit property with an unpermitted basement or attic unit treated as a fourth dwelling is not eligible.

Freddie’s zoning treatment and the 5601.2(c) exception

Under Section 5601.2, ADUs on 1-, 2-, and 3-unit properties must be legally permissible by jurisdiction, legally non-conforming, or located in an area without zoning.

Freddie’s narrow exception — Section 5601.2(c) — allows an ADU on a one-unit dwelling that does not comply with zoning to remain eligible if the appraisal demonstrates marketability by presenting at least two comparable sales that are similarly non-compliant. The exception does not extend to 2- to 4-unit properties; a 2- or 3-unit property with an illegal accessory unit is not eligible regardless of comparable sales.

Do not treat 5601.2(c) as legalization. It is only a loan-eligibility path. The underlying ADU may still be illegal under local ordinance, with consequences that loan approval does nothing to fix — fines, mandatory removal, insurance gaps, title problems. Keep the legalization question separate, and resolve it with your local jurisdiction.

Using ADU rental income with Freddie Mac

Under Guide Chapter 5306 and Section 5306.1, Freddie allows ADU rental income in three named contexts: a subject one-unit primary residence (purchase or no-cash-out refinance), a subject one-unit investment property, and a non-subject investment property. The rules:

- Lease-documented rental income may not exceed 75% of the gross monthly rent or market rent.

- Qualifying rental income cannot exceed 30% of total qualifying income.

- The ADU must be legal, legally non-conforming, or in an unzoned area. Rental income from an illegal ADU may not be used.

- For purchase use, landlord education is required unless the borrower has at least one year of property-management or ADU rental-management experience.

- For subject one-unit primary transactions where ADU rent is used, a full appraisal is required (ACE is not acceptable), with at least one ADU comparable sale and a rental analysis containing at least three rent comparables, including at least one rented ADU.

The non-subject investment property context is Freddie’s distinguishing feature. If you own a separate investment property with an ADU and you want to buy a primary residence, Freddie explicitly names that ADU’s rental income as usable under Chapter 5306. Fannie’s ADU-specific carveout is limited to the subject one-unit primary — but Fannie’s general non-subject rental-income rules carry no property-type restriction, so a non-subject property’s income may still be eligible if documented and otherwise qualifying.

Worked example: Freddie Mac ADU rental income math

Illustrative scenario: Same borrower — $6,000/month W-2 — buying a one-unit primary with an existing legal ADU, lease at $2,000/month, appraisal supporting the rent with one ADU sales comp and three rent comps including one rented ADU.

- Step 1 — Apply Freddie’s 75% rule: $2,000 × 75% = $1,500/month usable rent.

- Step 2 — Apply the 30% cap: X ≤ 0.30 × (6,000 + X), so X ≤ $2,571. The $1,500 fits.

- Step 3 — Confirm landlord education. With fewer than 12 months of property-management experience, landlord education must be completed before the rent may be used for a purchase.

Total qualifying income: $7,500/month — the same numeric result as Fannie in this scenario, but the documentation path and the landlord-education requirement differ.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Where Freddie and Fannie produce different outcomes

The two GSEs converge on the headline math (30% cap, 75% haircut) but diverge in three places that matter:

- Non-subject investment property ADU rent. Freddie names it explicitly; Fannie’s ADU carveout doesn’t, though its general non-subject rental rules may apply. Freddie is the cleaner explicit path.

- One-unit dwelling with an illegally zoned ADU. Freddie’s 5601.2(c) exception is explicit when comparable non-conforming sales support marketability. Fannie can also allow it under standard insurance/appraisal conditions, but the rule path differs.

- First-time landlord constraints. Fannie caps qualifying rent at PITIA (and blocks it entirely with no current housing payment); Freddie requires landlord education for purchase use absent a year of experience. Different mechanisms, different paperwork.

Building an ADU with Freddie Mac: CHOICERenovation

CHOICERenovation is Freddie’s single-close renovation product. Like HomeStyle, it uses an as-completed appraisal and lets renovation costs go up to 75% of the as-completed value. It combines with Home Possible (3% down) or HomeOne for first-time buyers. Standard completion timeline is 450 days; the streamlined CHOICEReno eXPress option carries a 180-day timeline with lighter documentation. See our Freddie Mac CHOICERenovation ADU rules guide for full details.

CHOICEHome and manufactured-home ADUs

Under Bulletin 2025-15, effective for settlement dates on or after February 9, 2026, a multi-wide manufactured home — including CHOICEHome — may serve as the primary dwelling with an ADU. CHOICEHome is Freddie’s program for manufactured homes built to near-site-built specifications; the ADU expansion gives manufactured-home owners a conventional path for adding a backyard cottage or in-law unit.

ADU rental income: how much actually counts

Side-by-side rental-income mechanics

| Mechanic | Fannie Mae | Freddie Mac |

|---|---|---|

| Eligible contexts | Subject 1-unit primary (ADU carveout); non-subject property may qualify under general rental rules | Subject 1-unit primary; subject 1-unit investment property; non-subject investment property |

| Eligible loan purposes (subject 1-unit primary) | Purchase + limited cash-out refinance | Purchase + no-cash-out refinance |

| Cap as % of total qualifying income | 30% | 30% |

| Calculation of usable income | 75% of market rent (Form 1007) or current lease | 75% of lease or market rent |

| Number of ADUs whose rent may count | One — even if multiple ADUs exist | One |

| Documentation | Form 1004 + Form 1007; current lease if available | Full appraisal (ACE blocked) + 1 ADU sales comp + 3 rent comps including 1 rented ADU |

| Value acceptance / appraisal waiver | Not available when subject-property rental income is used | ACE not acceptable when subject 1-unit ADU rent is used |

| First-time landlord | Qualifying rent capped at subject PITIA when <12 months experience and a current housing payment; not usable at all with no current housing payment | Landlord education required for purchase use unless ≥1 year experience |

| Future rent from a unit being renovated | Rule framed around existing ADU | Blocked for CHOICERenovation funded units (Bulletin 2026-1) for applications ≥ May 4, 2026 |

Three illustrative scenarios

Scenario A — High income, modest rent

Borrower earns $12,000/month. Buying a one-unit primary with a $1,500/month leased ADU. Usable rent at 75% = $1,125. The 30% cap is 0.30 × (12,000 + 1,125) ≈ $3,937 — the $1,125 fits with room to spare. Result: identical with both GSEs. Total qualifying income: $13,125.

Scenario B — Moderate income, strong rent

Borrower earns $4,500/month. Buying a one-unit primary with a $2,400/month leased ADU. Usable rent at 75% = $1,800. The 30% cap: X ≤ 0.30 × (4,500 + X), so X ≤ $1,929 — the $1,800 fits, but only just. Result: identical with both GSEs. Total qualifying income: $6,300.

Scenario C — Non-subject investment-property ADU rent

Borrower owns an investment property with a permitted ADU generating $1,800/month. Wants to buy a separate one-unit primary. Freddie: rental income from a non-subject investment property is explicitly eligible under Chapter 5306. Fannie: the subject-property ADU carveout doesn’t apply, but the non-subject property’s rental income may still be eligible under Fannie’s general rental-income rules if documented and otherwise eligible. Result: Freddie is the clearer explicit path; confirm with your lender on the Fannie side.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Talk to a Lender About ADU Financing → Compare mortgage options from lenders who finance properties with ADUs

Explore ADU Financing Paths →Disclosure: we may earn a commission if you proceed. Rates and approval depend on your lender, credit profile, and property. Not a guarantee of approval or rate.

Which property types are eligible: single-family, duplex, triplex, fourplex, manufactured home

One-unit home with one ADU

The cleanest scenario for both GSEs. Eligible under Fannie standard, Fannie UAD 3.6, and Freddie. ADU rental income may be used on a purchase or limited cash-out refi (Fannie) or purchase or no-cash-out refi (Freddie). Choose by lender pricing and AUS findings.

One-unit home with multiple ADUs

Fannie standard: one ADU only. Fannie UAD 3.6: up to three ADUs on a one-unit property. Freddie: one ADU. If your one-unit property has two or three permitted, legal ADUs, the Fannie UAD 3.6 lane is the path — provided your lender has adopted UAD 3.6. Rental income from only one ADU counts on either GSE.

Duplex or triplex with an ADU

Fannie standard: not eligible. Fannie UAD 3.6: ADUs allowed provided total dwelling units + ADUs ≤ 4. Freddie: one ADU under Section 5601.2, allowed since 2022. For now, Freddie is the simpler path for a 2- or 3-unit property with an ADU unless your lender has implemented Fannie UAD 3.6.

Fourplex with an ADU

Not eligible for ADU treatment under either GSE — both cap at four total dwelling units, and a fourplex is already at the ceiling. If you’re trying to finance a fourplex with an extra unit characterized as an ADU, you need a non-agency or portfolio lender.

Manufactured-home ADUs

Fannie standard: the primary dwelling must be site-built or modular; the ADU itself may be a HUD-Code manufactured home if classified as real property. Fannie UAD 3.6 (effective March 31, 2026): single-section standard MH may serve as the primary dwelling with one ADU; multi-section MH and single-section MH Advantage may include ADUs up to the four-unit ceiling. Freddie (Bulletin 2025-15, effective for settlements on or after February 9, 2026): multi-wide manufactured homes, including CHOICEHome, may serve as the primary dwelling with an ADU.

Manufactured-home ADUs require the ADU to be classified as real property, with proper foundation, title (converted from a vehicle title to real property), and documentation. Expect title attorneys, surveyors, foundation engineers, and a longer underwriting timeline.

ADU types: detached, attached, garage conversion, basement, prefab, modular

Neither guide draws fundamental eligibility distinctions by construction type — what matters is the ADU definition (independent living/sleeping/cooking/bath, separate entrance, same parcel) and legality. Detached ADU (DADU — a standalone structure): eligible. Attached ADU (addition or conversion sharing walls): eligible. Garage conversion ADU: eligible if permitted as habitable space. Basement ADU: eligible with the same tests, though many fail the separate-entrance requirement until that’s added. Prefab or modular ADU: eligible — construction method doesn’t change the rule. JADU (Junior ADU) under California state law: GSE treatment depends on whether the unit meets the ADU definition; JADUs that share a bathroom with the main dwelling may not qualify as Fannie/Freddie ADUs even if legal under state law.

What counts as an ADU: classification traps

| What it’s marketed as | Appraiser classification risk | Fannie treatment | Freddie treatment | Document to gather |

|---|---|---|---|---|

| Second kitchen / wet bar | High — no independent living/sleeping/bath = not an ADU | Not an ADU without full facilities | Not an ADU without full facilities | Floor plan, photos of kitchen + bath |

| Guest house, casita, pool house | Medium — fails if no kitchen, no bath, or no independent entrance | ADU only if it meets B4-1.3-05 | ADU only if it meets 5601.2 | Floor plan, separate-entrance photo |

| In-law suite inside the main home | Medium — JADU/shared-bath units may not qualify | ADU only with independent kitchen + bath | ADU only with independent facilities | Permit, floor plan |

| Unit with separate postal address | High — may signal a second dwelling unit | May shift property to 2-4 unit (ineligible standard lane) | May shift to multi-unit analysis | Postal records, tax card |

| Unit with separate utility meter | Medium-high — duplex indicator | Same risk of reclassification | Same risk | Utility records |

| Tiny home on wheels | High — not real property | Not eligible | Not eligible | Title, foundation status |

| HUD-Code manufactured ADU | Medium — must be real property | Eligible if classified as real property | Eligible under conditions | HUD Data Plate, foundation report, title |

| Garage conversion | Medium — must be permitted habitable space | Eligible if permitted + meets definition | Eligible if permitted + meets definition | Permit, certificate of compliance |

What happens if the ADU is unpermitted, illegal, or legally non-conforming

Legal vs. legally non-conforming vs. illegal

Legal: permitted under current zoning and compliant with current rules. Fully eligible.

Legally non-conforming: legally permitted when built, but current zoning wouldn’t allow it today. Common in older neighborhoods where setbacks or use rules have tightened. Both GSEs treat this as eligible, addressed through the appraisal and lender review.

Illegal (non-conforming): never permitted, or built in violation of current rules and not legalizable. The unit may rent at market rates and still not be legal. This is the dangerous category.

What to ask the building department before applying

- Request the building permit history and any certificate of occupancy or certificate of compliance.

- Ask whether the structure is recorded as habitable space, accessory dwelling, or something else.

- Ask whether the jurisdiction has an ADU amnesty or legalization pathway.

- Ask the tax authority how the unit is taxed — discrepancies between tax records and physical reality are a red flag for underwriting.

What to ask the appraiser

Ask whether the appraiser has experience finding ADU comparables in your market, and whether they can identify two non-conforming ADU comparable sales if you need Freddie’s 5601.2(c) path. If not, find an appraiser who specializes in properties with ADUs before ordering the report.

When to pause and legalize before applying

In markets where the appraiser can support marketability with comparable sales showing the same non-compliant zoning use, the conventional exceptions can matter. But where legalization is available, it’s often faster and cheaper than expected — a finished garage conversion may qualify for a non-permitted-construction pathway with a structural sign-off, a fire-separation check, and a permit fee.

Check What Your Property Can Support → Get Your Free ADU ReportFree, no signup, 60 seconds.

Appraisal evidence each program requires

| Evidence | Fannie Mae | Freddie Mac |

|---|---|---|

| Description of the ADU | Required | Required |

| Value and marketability analysis | Required | Required |

| ADU comparable sales | Marketability support needed; not a fixed minimum | Required when subject 1-unit primary rent is used: 1 comp |

| ADU rent comparables | Form 1007 or Form 1025 with rental analysis | 3 rent comps, ≥1 rented ADU |

| Appraisal waiver / value acceptance | Not available when subject-property rental income is used; otherwise file-dependent | ACE not acceptable when subject 1-unit primary ADU rent is used |

Why appraisers may struggle

ADU comparables can be hard to find outside major coastal metros. Appraisers in less-active markets may be unfamiliar with ADU classification rules, and MLS data often doesn’t tag ADUs consistently. If your subject is in a market where ADUs are uncommon, expect longer appraisal turnaround and a wider comp search. Some lenders maintain rosters of ADU-experienced appraisers; ask before ordering.

What homeowners can prepare before appraisal

Have these ready when the appraiser arrives: building permits and certificate of occupancy (or a permit-history report), the ADU floor plan with dimensions, photos of every room including kitchen and bath, the current lease and past 12 months of rent receipts (if applicable), the property tax record showing classification, and any prior appraisal that addressed the ADU. The more the appraiser can document about legality, classification, and rental history, the less likely the report comes back with conditions that derail underwriting.

Should you ask your lender to try Fannie, Freddie, FHA, or another path?

When Fannie may be the better fit

- One-unit primary with a single existing legal ADU and rental income you want to count — and your lender has adopted DU 12.1.

- One-unit property with two or three permitted ADUs (UAD 3.6 lane only).

- Single-section standard manufactured home as primary with an ADU (UAD 3.6 lane only).

- 2- or 3-unit property with one or two ADUs, total dwelling units + ADUs ≤ 4 (UAD 3.6 lane only).

When Freddie may be the better fit

- 2- or 3-unit property with one ADU (allowed since 2022; doesn’t require UAD 3.6).

- One-unit property with an illegally zoned ADU where two non-conforming comparable sales exist (5601.2(c)).

- Borrower wants to use ADU rental income from a non-subject investment property (explicitly named context).

- Multi-wide manufactured home as primary with an ADU (settlement on or after February 9, 2026).

When FHA or another path may be needed

- Properties that fit neither GSE — fourplex with an extra unit, illegal ADU on a 2-3 unit property, units that fail the kitchen-or-bath test.

- Credit, DTI, or down-payment situations that fail both DU and LPA.

- Borrowers who need to count rental income from a unit being constructed with renovation proceeds. FHA 203(k) has its own ADU rules under HUD Mortgagee Letter 2023-17 and we cover it separately.

Scenario-specific lender script

| Your scenario | What to ask your lender |

|---|---|

| One-unit + one existing ADU | “Are you running this under Fannie or Freddie, and are you counting the ADU rent under SEL-2025-08 / Section 5306.1? What’s the 30% cap on my file?” |

| One-unit + two or three ADUs | “Is your appraisal workflow on UAD 3.6? If so, can we use the Fannie multi-ADU one-unit eligibility under SEL-2025-10?” |

| Duplex or triplex + one ADU | “Can we use Freddie’s 5601.2 (allowed since 2022), or are you on Fannie UAD 3.6 for a 2-3 unit ADU?” |

| Non-subject investment-property ADU rent | “Can we use the ADU rental income from my investment property — Freddie names this in 5306.1; how does Fannie’s general non-subject rental rule treat it?” |

| Illegal / non-compliant zoning | “Can we support 5601.2(c) with two non-conforming comps, or meet Fannie’s insurance/appraisal conditions?” |

| Building an ADU with renovation proceeds | “Given Freddie Bulletin 2026-1, can we count the new ADU’s rent at all, or do we need to build first and refinance with the lease in place?” |

A loan officer who can answer the row that fits you is one worth working with. A loan officer who waves it off probably hasn’t read the post-October-2025 updates.

Compare Conventional ADU Financing Paths → Explore mortgage options from lenders experienced with ADU files

Explore Conventional ADU Financing Paths →Affiliate disclosure: we may earn a commission if you complete a loan via this link. Rates depend on lender, credit, and property. Not a guarantee of approval or rate.

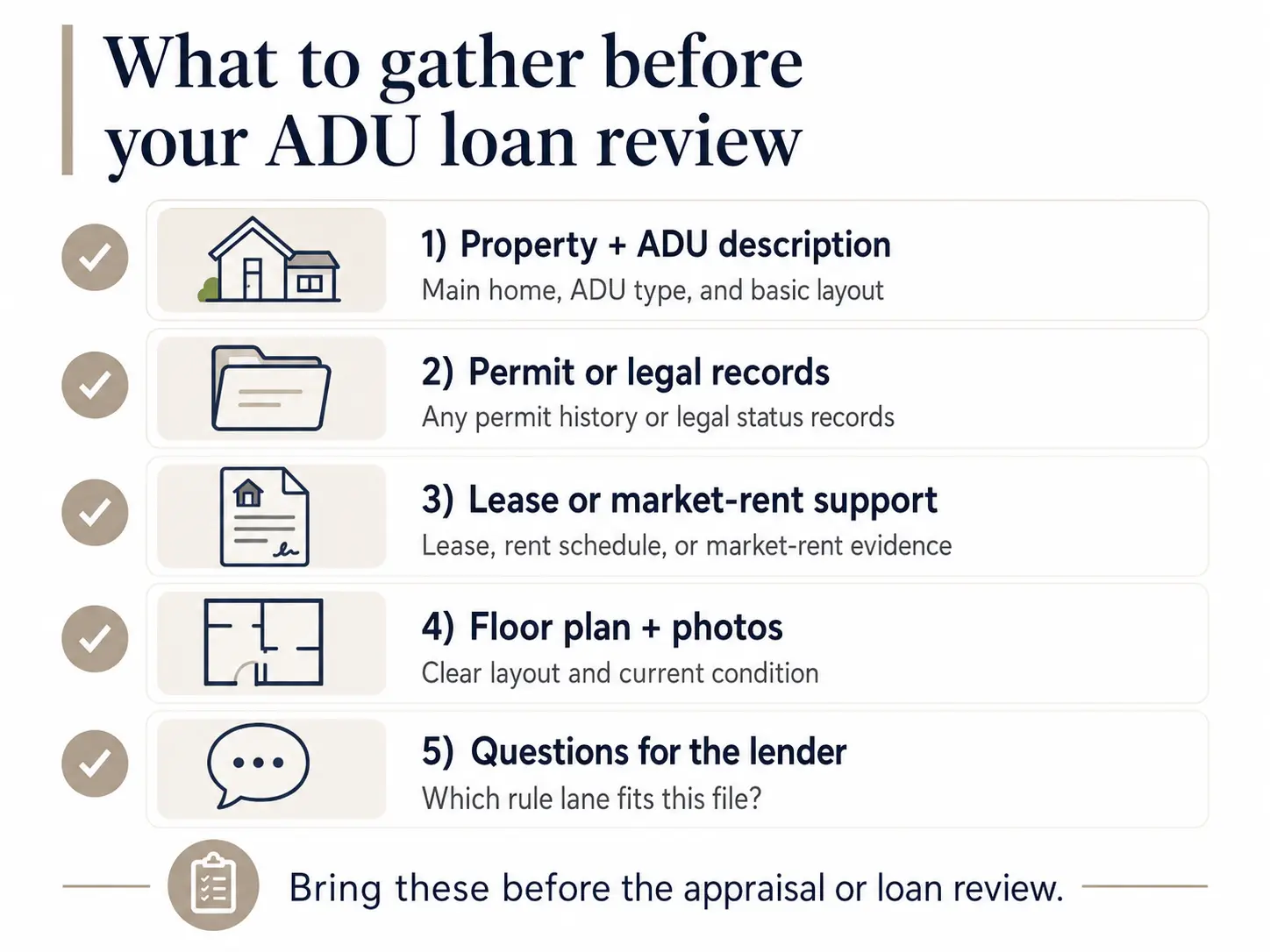

Documents to collect before applying

| Document | Rule it supports |

|---|---|

| Building permits, certificate of occupancy, certificate of compliance, or permit-history record | Freddie 5601.2 / Fannie B2-3-04 legality and zoning compliance |

| Property tax record | Classification (ADU vs additional finished space vs second unit) |

| ADU floor plan with dimensions | Fannie B4-1.3-05 / Freddie 5601.2 ADU definition and appraiser classification |

| Photos of kitchen, bath, sleeping area, separate entrance | The definitional facilities and separate-entrance requirement |

| Current lease agreement (when using lease-documented rent) | Fannie B3-3.8-01 / Freddie 5306.1 rental income |

| Form 1007 or Form 1025 (lender/appraiser provides) | Fannie ADU rental-income documentation |

| Three rent comps with at least one rented ADU (Freddie) | Freddie 5601.12 subject 1-unit ADU rental income |

| Two non-conforming ADU comparable sales (Freddie) | Freddie 5601.2(c) illegal-zoning exception |

| Separate utility meter / postal address records | Heads off reclassification as a second unit |

| Landlord education certificate | Freddie purchase-use requirement (unless ≥1 year experience) |

| Property-management track record (LLC docs, other leases, tax returns) | Supports waiving Fannie’s first-time-landlord PITIA cap |

| Contractor bids and as-completed plans (renovation product) | HomeStyle Renovation / CHOICERenovation as-completed appraisal |

Some of these take weeks — building permit histories from older jurisdictions without digital records, foundation engineering reports, and Form 1007 rent schedules in thin markets. Start early.

Download the Free ADU Starter Kit → Every document checklist, every fee category, and the questions to ask before you sign — updated quarterly.

Get the Free ADU Starter Kit →We’ll notify you when GSE rules change. No spam, unsubscribe anytime.

The most common Fannie/Freddie ADU deal-killers

| Deal-killer | Why it matters | What to do |

|---|---|---|

| ADU is unpermitted with no non-conforming comparable sales | Illegal-ADU rent can’t be used under Freddie; Fannie requires lender insurance + appraisal conditions | Legalize, or finance without counting the rent (HELOC, cash-out refi on equity alone) |

| Borrower has no current primary housing payment | Fannie B3-3.1-08: ADU rental income may not be used to qualify in this case | Restructure the income picture, or pursue the Freddie path |

| First-time landlord, current housing payment, ADU rent exceeds PITIA | Fannie caps qualifying rent at the subject PITIA | Reduce reliance on ADU rent, or use Freddie with landlord education |

| Multiple ADUs, lender not on Fannie UAD 3.6 | Standard Fannie and Freddie cap at one ADU | Find a lender on UAD 3.6, or scope to one rentable ADU |

| Duplex/triplex + ADU, lender not on Fannie UAD 3.6 | Standard Fannie doesn’t permit ADUs on 2-4 units | Use Freddie (allowed since 2022), or a Fannie lender on UAD 3.6 |

| Need future rent from an ADU built with renovation proceeds | Bulletin 2026-1 blocks this for CHOICERenovation apps ≥ May 4, 2026; Fannie rule framed for existing ADU | Build with another product, lease the ADU, then refinance with rent in place |

| Appraiser can’t find ADU comparable sales | Freddie requires ≥1 ADU comp on subject 1-unit ADU rent files; Fannie needs marketability support | Use an ADU-experienced appraiser; pre-research comps in MLS |

| Subject 1-unit + ADU rent file uses ACE/value acceptance | Freddie blocks ACE; Fannie blocks value acceptance when subject rental income is used | Order a full appraisal up front |

| Kitchen doesn’t meet Fannie’s minimums | Appraiser may reclassify as ordinary finished space; property loses ADU status | Bring the kitchen to specification before appraisal |

| Fourplex with an extra “ADU” | Both GSEs cap at four total dwelling units | Recharacterize as four-unit or use non-agency lending |

The pattern in every row: the rule is knowable, the friction is predictable, and the fix is usually possible — but only if you address it before the appraisal is ordered, not after the file is denied.

See Whether Your Property Fits a Conventional ADU Path → Get Your Free ADU ReportFree, no signup, 60 seconds.

The honest limitations to plan around

- UAD 3.6 adoption is uneven. Fannie’s expanded structural eligibility is gated to lenders using UAD 3.6 appraisals. UAD 3.6 doesn’t become mandatory until November 2, 2026. Ask your loan officer directly whether their appraisal workflow is on UAD 3.6 before assuming the new rules apply.

- The 30% cap binds more often than you’d think. It’s a cap on usable ADU income relative to total qualifying income, including the ADU’s contribution. In moderate-income markets with strong ADU rents, the cap — not the appraisal or the lease — is the constraint.

- First-time landlords face additional caps. Fannie’s PITIA cap (and the no-current-housing-payment exclusion) and Freddie’s landlord-education requirement both apply to borrowers with less than 12 months of property-management experience.

- Only one ADU’s rent counts. Even under Fannie’s UAD 3.6 lane permitting three ADUs on a one-unit property, only one ADU’s rent flows into qualifying income on either GSE.

- Future rent from a unit being built with renovation proceeds is restricted. Freddie’s Bulletin 2026-1 blocks it explicitly for CHOICERenovation applications received on or after May 4, 2026. Fannie’s published ADU-income rule is framed around an existing ADU.

- Appraisal comps can be hard to find. Freddie’s requirement for at least one ADU sales comp and three rent comps (including one rented ADU) is a real constraint in markets without dense ADU activity.

- Lender overlays exist. GSE rules are the floor. Individual lenders often add overlays — stricter DTI, higher reserves, ADU-experience requirements, lower LTV limits. If one lender says no, another with different overlays may say yes, within the same GSE rule set.

- The trajectory is clearly positive. None of the friction above changes the bigger picture: conventional ADU financing is more accessible in 2026 than in any previous year. SEL-2025-08 removed the single biggest restriction in the conventional ADU market. SEL-2025-10 expanded the structural footprint dramatically.

How GSE choice actually works in practice

Behind every conventional mortgage in the U.S. is the same secondary-market logic: a lender originates the loan, then sells it to Fannie or Freddie based on which guidelines the file meets and which offers the better execution price. The borrower experiences a “conventional” mortgage; the routing is invisible.

That routing runs through DU and LPA, which apply the published guide rules to your file’s data — income, credit, property, occupancy, ADU treatment — and return a recommendation plus conditions. Many lenders can test both DU and LPA, but workflows vary; ask whether your file has been run through both engines and which rule lane produced the cleaner findings.

This is why knowing the rules matters even though you can’t pick the GSE directly. If your file is on the borderline — say you need ADU rental income but the appraisal won’t support Freddie’s comparable-sale requirement — you and your loan officer can adjust the strategy. Switch the path from “we need this Freddie ADU comp” to “we’ll proceed under Fannie, which doesn’t require an ADU sales comp,” and the file moves.

Frequently asked questions

- Does Fannie Mae allow ADU rental income in 2026?

- Yes. Effective October 8, 2025 under SEL-2025-08, Fannie allows rental income from one ADU on a one-unit principal residence as qualifying income, capped at 30% of total qualifying income, for purchase and limited cash-out refinance transactions. Desktop Underwriter 12.1, live since March 21, 2026, applies the rule automatically.

- Does Freddie Mac allow ADU rental income?

- Yes — since 2022, under Guide Chapter 5306 and Section 5306.1. Up to 75% of lease or market rent may count, capped at 30% of total qualifying income. Freddie names three eligible contexts: a subject one-unit primary, a subject one-unit investment property, and a non-subject investment property.

- Can I have multiple ADUs on a Fannie Mae loan?

- Under standard rules, no — one ADU per one-unit property and zero on 2-4 unit properties. Under SEL-2025-10's UAD 3.6 lane, effective March 31, 2026, Fannie allows up to three ADUs on a one-unit property. Your lender must have adopted UAD 3.6.

- Does Fannie Mae allow ADUs on duplexes or triplexes?

- Under standard rules, no. Under the UAD 3.6 lane (March 31, 2026), yes — provided total dwelling units plus ADUs do not exceed four. A duplex may add up to two ADUs; a triplex may add one.

- Does Freddie Mac allow ADUs on duplexes or triplexes?

- Yes, since 2022 under Section 5601.2 — one ADU on 1-, 2-, or 3-unit properties.

- What's the difference between HomeStyle Renovation and CHOICERenovation for an ADU?

- Both are single-close conventional renovation mortgages financing ADU construction off an as-completed appraisal up to 75% of value. Fannie's HomeStyle Renovation now allows up to 50% upfront disbursement at closing (since December 10, 2025); Freddie's CHOICERenovation uses standard escrow holdback. HomeStyle's completion window is 15 months; CHOICERenovation's is 450 days (180 days under CHOICEReno eXPress). Freddie's Bulletin 2026-1 blocks rental income from any unit included in a funded CHOICERenovation project for applications received on or after May 4, 2026.

- Can I count rent from more than one ADU?

- No. On a subject one-unit primary residence, only one ADU's rent counts on either GSE, even if multiple ADUs exist.

- Can I use future ADU rent from a planned ADU to qualify?

- This is the most common misconception. Fannie's ADU-income rule is framed around an existing ADU. Freddie's Bulletin 2026-1 explicitly blocks CHOICERenovation applications received on or after May 4, 2026 from using rental income from any unit included in the funded renovation project. The 'build with renovation proceeds and qualify with future rent' combination doesn't work cleanly on either GSE today. A workaround: build with another product — HELOC, cash savings, construction-to-permanent loan — lease the ADU, then refinance with the rent in place.

- Can an illegal ADU still qualify for conventional financing?

- On a one-unit property, Freddie's Section 5601.2(c) exception may allow it if the appraisal demonstrates marketability with at least two similarly non-compliant comparable sales. Fannie's standard rules require lender insurance and appraisal conditions for non-compliant ADUs. On 2-3 unit properties, neither GSE permits illegally zoned accessory units. Rental income from an illegal ADU may not be used to qualify.

- Which is better for ADU loans, Fannie Mae or Freddie Mac?

- Neither is better in the abstract. The right answer depends on property type, ADU count, transaction type, whether you need rental income, where the income comes from, and which system produces cleaner findings for your specific file. Use the scenario guide on this page to get a situation-specific answer.

- Do Fannie and Freddie rules override local ADU zoning?

- No. GSE rules are secondary-market loan-eligibility rules. They don't grant local permits, legalize unpermitted construction, or override setback or use rules. Local zoning compliance is a separate test that must be verified independently with your jurisdiction.

What we verified for this guide

Last verified: May 21, 2026

| Claim type | Source | Last verified |

|---|---|---|

| Fannie ADU property eligibility (standard) | Fannie Selling Guide B2-3-04, B4-1.3-05 | May 21, 2026 |

| Fannie ADU rental-income rule | SEL-2025-08 (Oct 8, 2025); Sections B3-3.1-08, B3-3.2-02, B3-3.8-01 | May 21, 2026 |

| Fannie non-subject rental income (no property-type restriction) | Fannie Selling Guide B3-3.8-01 | May 21, 2026 |

| Fannie value-acceptance ineligibility with subject rental income | Fannie Selling Guide B4-1.4-10 | May 21, 2026 |

| Fannie UAD 3.6 expanded ADU eligibility | SEL-2025-10 (Dec 10, 2025); UAD 3.6 Policy Supplement | May 21, 2026 |

| Fannie DU 12.1 release applying ADU income | Fannie DU Version 12.1 Release Notes (eff. Mar 21, 2026) | May 21, 2026 |

| HomeStyle Renovation (incl. MH 50% cap) and HomeStyle Refresh ADU eligibility | SEL-2025-10; Selling Guide B5-3.2, B5-3.3-01 | May 21, 2026 |

| Freddie ADU property eligibility (1-, 2-, 3-unit) | Freddie Seller/Servicer Guide Section 5601.2; ADU Fact Sheet | May 21, 2026 |

| Freddie 5601.2(c) illegal-zoning exception | Freddie Guide Section 5601.2(c) | May 21, 2026 |

| Freddie ADU rental income (75%/30%; three contexts) | Freddie Guide Chapter 5306, Section 5306.1; ADU Fact Sheet; Rental Income Matrix | May 21, 2026 |

| Freddie manufactured-home ADU expansion | Freddie Bulletin 2025-15 (Nov 5, 2025) | May 21, 2026 |

| Freddie CHOICERenovation rental-income restriction | Freddie Bulletin 2026-1 (Feb 2026); Chapter 4607 | May 21, 2026 |

| Freddie appraisal requirements with ADU rent | Freddie Guide Section 5601.12 | May 21, 2026 |

All claims about ADU treatment, rental income, eligibility, appraisal requirements, and effective dates are tied to the official source above. Editorial conclusions are framed as editorial conclusions based on the verified facts, not as guarantees.

Methodology

We built this page by reading the primary sources — Fannie Mae Selling Guide Announcements, Freddie Mac Single-Family Seller/Servicer Guide Bulletins, the actual Sections each rule lives in, the Desktop Underwriter and Loan Product Advisor release notes, the UAD 3.6 Policy Supplement, and the GSEs’ own ADU product pages and fact sheets — and translating each rule into plain English for a homeowner audience. Where two sources disagreed, we deferred to the more recent official document. We did not rely on news write-ups, lender blogs, or aggregator pages for any factual claim about GSE rules.

This page is for educational purposes only and is not legal, tax, financial, or lending advice. Fannie Mae and Freddie Mac rules are secondary-market guidelines; individual lenders may apply additional overlays. Local zoning, building code, and permit compliance must be verified separately with the relevant jurisdiction. Always confirm rule details with your loan officer before making a financing decision. We update this page on a quarterly cadence and immediately after any Fannie Mae Selling Guide Announcement or Freddie Mac Single-Family Seller/Servicer Guide Bulletin that touches ADU-related sections.

Where to go next

Pick the path that matches where you actually are.

You want to know whether your property fits a conventional ADU path at all.

The Feasibility Engine asks a few questions about your address, zoning, and goals and returns a personalized report — free, no signup required to begin.

See What You Can Build → Get Your Free ADU ReportFree. No signup required. Results in 60 seconds.

You want to talk to lenders about actual financing options.

Explore lenders experienced with conventional ADU files, including HomeStyle Renovation, CHOICERenovation, cash-out refinances, and construction-to-permanent options.

Affiliate disclosure: we may earn a commission if you complete a loan via this link. Rates depend on lender, credit, and property.

You want this page when the rules change.

We re-verify after every update that touches ADU sections. Subscribe to the Free ADU Starter Kit and we’ll send a one-page update each time a material change drops.

Download the Free ADU Starter Kit → Get notified when GSE rules changeYou’re earlier in the journey and want the broader picture.

- What Is an ADU — ADU types, costs, and a national overview of rules.

- ADU Grants 2026 — verified state and city ADU grant programs.

- ADU loan requirements — what lenders look for across all product types.

- Best ADU financing options — the broader comparison across conventional, FHA, HELOC, HEI, and more.

- Fannie Mae HomeStyle Renovation for ADUs — full details on Fannie’s renovation product.

- Freddie Mac CHOICERenovation ADU rules — full details on Freddie’s renovation product.

- Construction-to-permanent loans for ADUs — when a CTP is the right path.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

Free. No signup required. Results in 60 seconds.