How to Finance an ADU for Aging Parents

By the Dwelling Index Editorial Team · Last updated: · Last verified: · Editorial standards · Methodology · ~35 min read

This guide is educational and is not financial, legal, tax, lending, or Medicaid-planning advice. The Dwelling Index is an independent research resource. We are not a lender, broker, builder, or attorney.

The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Full disclosure.

The fast answer: best first financing path by family situation

There is no single best ADU loan for aging parents. The best path is set by your family’s structure — who owns the land, who holds the equity, and who can safely make a payment. The table below maps the most common family situations to the financing lane to test first. Find your row, then read that path’s full breakdown below.

We present financing as paths organized by your situation — never ranked by compensation. We don’t quote rates, APRs, or monthly payments, and we never guarantee qualification. Full disclosure.

| Your family’s situation | First path to test | Why it fits | Don’t use it when |

|---|---|---|---|

| Adult child owns the property, has equity + steady income | HELOC or home equity loan on the child’s home | Simplest current-value path; ties the loan to the property gaining the ADU | The payment would strain your caregiving budget |

| Adult child owns property but has low current equity | Renovation loan that lends on after-renovation value | Underwrites against the home’s completed value, not today’s | You need a fast, low-documentation close |

| Parent is 62+ and owns/occupies their home with equity | Reverse mortgage (HECM) on the parent’s home — with HUD counseling | No required monthly payment; built for fixed-income owners 62+ | The parent will move out of that home (see the occupancy trap below) |

| Parent has equity, limited income, wants no new payment | Home Equity Investment (HEI) or HECM, compared side by side | Solves the cash-flow constraint without a monthly bill | The family can’t tolerate sharing future appreciation or estate uncertainty |

| Parent is on / near Medicaid or SSI | STOP — structure first. Line of credit, not lump sum; settle rent; consult an elder-law attorney | Protects benefit eligibility (see the two benefit sections below) | Funds would sit unspent past month-end, or the parent will live rent-free |

| Parent sells their home and contributes cash | Documented family contribution agreement | Avoids debt and monthly payments | Gift/loan terms, title, siblings, and Medicaid aren’t settled in writing |

| Multiple siblings chipping in | Shared contribution agreement with estate equalization | Spreads cost, reduces resentment | Repayment and inheritance terms are left informal |

| Parent already needs memory care or 24/7 nursing | Do not finance yet — care-first planning | An ADU doesn’t replace trained medical staff | You’re using construction to postpone a care decision |

Last verified: . Cost and program details change; we re-check financing and regulatory sources at least quarterly.

See what you can build → get your free ADU report. Before you compare a single loan, confirm your lot can support the ADU your parent actually needs — zoning, setbacks, size limits, and a ballpark cost, personalized to your address in about 60 seconds.

See What You Can Build → Get Your Free ADU ReportHow to finance an ADU for aging parents by family situation: the five-question filter

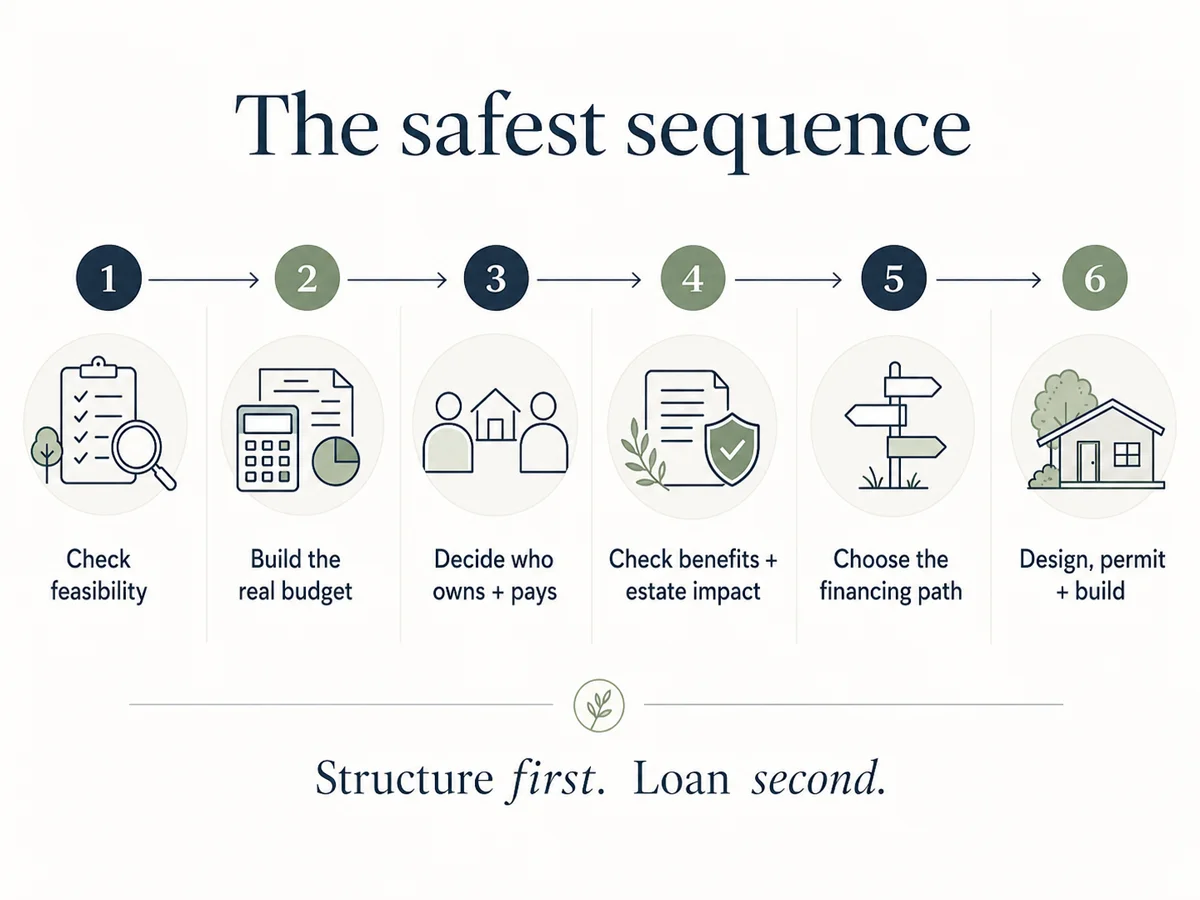

The best ADU financing path for an aging parent is the one that matches who owns the land, who has usable equity, who can carry payments, whether the parent relies on needs-based benefits, and what the exit plan is if care needs grow. Families who pick the loan before answering those questions are the ones who end up refinancing, retitling, or unwinding a benefits problem later. Loan product is the last decision, not the first.

We organize everything that follows into paths by situation, not products ranked by who pays us. On a financing page, that ordering is the whole game: “best for you” should never quietly mean “best for our commission.”

Run these five questions in order. Each one eliminates paths that can’t work, so by the end you’re choosing among two or three real options instead of ten theoretical ones.

- Who legally owns the property where the ADU will sit? The owner of record usually borrows, and the ADU becomes part of that parcel’s collateral.

- Who will actually borrow or contribute the money — the adult child, the parent, or both?

- Can the borrowing household carry payments during construction, when you’re paying a mortgage and a build at the same time?

- Is the parent largely independent, or already needing daily care? This decides whether a six-figure build even makes sense.

- What happens to the financing and the ADU after the parent no longer lives there — rental, guest house, caregiver suite, or sale?

The honest admission up front: financing an aging-parent ADU is more tangled than financing a rental ADU, because two generations’ money, benefits, and estates collide in one project. None of it is a reason to abandon the plan — it’s a reason to sequence it correctly. Thousands of families build these every year and get it right; they just decide the structure before they sign anything.

What are the financing options for an ADU for elderly parents? The Family-Fit Matrix

Six financing lanes cover almost every aging-parent ADU: (1) HELOC or home equity loan, (2) cash-out refinance, (3) renovation or construction loan, (4) reverse mortgage (HECM), (5) Home Equity Investment (HEI), and (6) cash or pooled family contributions. Which one fits is driven by who is paying and what constraint you’re solving — income, equity, monthly-payment tolerance, or benefit protection.

Definitions first, because the acronyms do real work here:

- HELOC (home equity line of credit): a revolving credit line secured by your home; you draw what you need and pay interest on the balance.

- Cash-out refinance: you replace your existing mortgage with a larger one and take the difference in cash — only smart if your current rate isn’t already low.

- Renovation / construction loan: financing sized to the project, often underwritten against the home’s after-renovation value (ARV) — the appraised value the home is expected to reach once the ADU is built.

- HECM (Home Equity Conversion Mortgage): the FHA-insured reverse mortgage for owners 62+, with no required monthly payment, secured by the borrower’s primary residence.

- HEI (Home Equity Investment): a company gives a lump sum today in exchange for a share of the home’s future value — no monthly payment, no interest, but a settlement is owed at the term’s end or on sale.

| Lane | Who borrows | Monthly payment? | Fixed-income parent fit | Medicaid/SSI impact | Best for |

|---|---|---|---|---|---|

| HELOC / home equity loan | Adult child (usually) | Yes | Poor — needs income to qualify | Child’s loan on child’s home → no parent-benefit issue | Child owns the lot, has equity + income |

| Cash-out refinance | Adult child | Yes (new full mortgage) | Poor | Same as above | Child’s existing rate is already high |

| Renovation / construction (ARV) | Adult child | Yes | Poor | Same as above | Child’s current equity is too low to cover the build |

| Reverse mortgage (HECM) | Parent (62+) | No required payment | Strong | Bona-fide loan proceeds aren’t income; unspent funds can become a countable resource | Parent owns home, 62+, staying in that home |

| Home Equity Investment (HEI) | Parent (or child) | No | Strong on cash flow | Newer contract category — benefit treatment not assured; verify with an attorney | Parent has equity, no income, wants no payment |

| Cash / pooled family funds | Family | No | N/A | Gifts/transfers can trigger the Medicaid look-back | Parent sells/downsizes; siblings contribute |

Path order reflects fit to common situations, not lender compensation. We don’t rank lenders or sort by payout.

Path 1 — The adult child has equity and steady income: HELOC, home equity loan, or cash-out refi

If the ADU goes on the adult child’s property and the child has usable equity plus income to support a payment, a HELOC or home equity loan is typically the most straightforward path because the financing stays tied to the property that gains the ADU. The home secures the debt, so the payment has to stay safe even if construction runs long or over budget.

The decision inside this lane is whether to preserve your current first mortgage or replace it. Here’s the rule, made concrete:

| Your situation | Preserve the first mortgage (HELOC / home equity loan) | Replace it (cash-out refinance) |

|---|---|---|

| Current mortgage rate is low | Yes — add a second lien for the ADU amount only | No — refinancing would reprice your whole balance higher |

| Current rate is already high | Either works; compare total cost | Often yes — consolidate into one loan |

| You want the smallest monthly add | HELOC (interest only on what you draw) | Usually higher payment |

| ADU budget is large relative to the mortgage | Either; compare | Cash-out can be cleaner administratively |

The decision rule that protects caregiving budgets: compare total interest cost over the life of the loan, not just the monthly payment. A lower monthly payment that runs five years longer can cost more — money that could have gone toward your parent’s care.

Explore your mortgage-backed ADU financing options. If you’re financing on your own property, compare HELOC, home equity loan, cash-out refinance, and construction-loan paths in one place — education first, then verify terms with a licensed lender. No rate quotes, no approval assurances.

Affiliate link — we may earn a commission at no extra cost to you. Never affects our recommendations.

Compare ADU financing paths →Path 2 — The adult child has low current equity: lend on after-renovation value

When a family can’t borrow enough against the home’s current value, the next lane to test is renovation financing that underwrites against the home’s after-renovation value (ARV) — what the home will be worth once the ADU is complete. This lets you access financing based on the finished project rather than today’s appraisal.

| Product | What it can do for an aging-parent ADU | Note |

|---|---|---|

| Fannie Mae HomeStyle Renovation | Finance adding an ADU (including an in-law suite) as part of a purchase or refinance | Fannie Mae’s HomeStyle program expressly covers adding an ADU; subject to lender and program requirements |

| Fannie Mae construction-to-permanent | Build a newly constructed one-unit home with an ADU under a single financing | Per Fannie Mae Selling Guide product descriptions |

| Freddie Mac CHOICERenovation | Add or renovate an ADU in a single-closing structure | Freddie Mac markets it for aging-in-place and multigenerational needs |

| FHA 203(k) | Roll certain ADU-related improvements into one FHA-insured loan | More documentation; FHA overlays apply |

| ARV renovation HELOC (e.g., RenoFi-style) | Lend against the home’s projected after-renovation value | Offered through third-party lending partners, not a direct lender; availability varies by lender and state — confirm before applying |

The tradeoff to know going in: these products require defined plans, contractor documentation, draw schedules, and inspections. They’re more paperwork than a simple home-equity line, and the lender controls disbursement against construction milestones.

See whether after-renovation-value financing fits your build. If today’s equity won’t cover the ADU but the finished unit will add real value, ARV-based renovation financing may bridge the gap. Availability varies by lender and state — check what’s available where your parent lives.

Affiliate link — we may earn a commission at no extra cost to you. Never affects our recommendations.

Explore renovation financing →

Path 3 — The parent is 62+ and owns the home: reverse mortgage (HECM)

A Home Equity Conversion Mortgage (HECM) is the FHA-insured reverse mortgage that lets a homeowner 62 or older convert part of their equity into cash with no required monthly mortgage payment — repaid only when the borrower sells, permanently moves out, or passes away. For a parent whose wealth is in the house but whose income is Social Security, it’s frequently the only path that doesn’t add a monthly bill they can’t afford.

How the numbers actually work, decoded:

- The 2026 HECM maximum claim amount is $1,249,125 (HUD, for case numbers assigned during calendar year 2026). This is the maximum home value FHA will count — not the amount your parent receives.

- Borrowing power, called the principal limit, equals the Maximum Claim Amount multiplied by an HUD-published Principal Limit Factor (PLF) set by the youngest borrower’s age and the expected interest rate. Older borrowers and lower rates produce higher proceeds.

- The first-year disbursement limit: during the first 12 months, your parent can generally draw the greater of 60% of the principal limit, or mandatory obligations plus 10% of the principal limit (HUD). That can create a real construction-timing problem if the ADU build needs more cash up front than the HECM can release in year one — so the construction draw schedule has to be coordinated between the lender and builder before you start.

- The home does not need to be owned free and clear; an existing mortgage can be paid off at closing if there’s enough equity.

- HUD-approved counseling is required before application, and your parent must keep property taxes and homeowner’s insurance current and maintain the home.

⚠️ The occupancy trap — read this twice if your parent plans to move into an ADU on your land

A HECM is secured by the borrower’s principal residence. The Consumer Financial Protection Bureau is explicit: if the borrower is away from that home for more than 12 consecutive months — including a move into a healthcare facility or into an ADU on someone else’s property — with no co-borrower or eligible non-borrowing spouse still living there, the home stops being their principal residence and the loan becomes due and payable (CFPB, reverse mortgage rules).

A HECM works cleanest when the ADU is built on the parent’s own property. If the plan is for your parent to take a HECM on their house and then move into an ADU on your land, ask a HUD-approved counselor and the lender whether that move triggers repayment before any money moves. Families miss this constantly, and it can force a sale of the very home they were trying to keep.

The other honest tradeoffs: a HECM carries origination fees, an upfront and ongoing mortgage insurance premium, and compounding interest that reduces the estate over time — the loan balance grows rather than shrinks. It’s the wrong tool if your parent may move within a few years or can’t reliably cover taxes and insurance.

Our role here: The Dwelling Index does not partner with any reverse-mortgage lender, so there’s no link to push and no incentive in either direction. The neutral next step is HUD’s own counselor directory — find a HUD-approved HECM counselor at hud.gov, and run your parent’s numbers (including the occupancy question above) before committing.

Path 4 — The parent has equity but no income and wants no payment: Home Equity Investment

A Home Equity Investment (HEI) provides a lump sum today in exchange for a share of the home’s future value, with no monthly payments and no interest during the term, settled when the home sells or the term ends. For a fixed-income parent who can’t qualify for a HELOC (lenders verify income) and isn’t 62 yet (the HECM floor), an HEI is sometimes the only no-payment door.

Terms vary by provider. The Consumer Financial Protection Bureau describes home equity contract terms as typically running 10 to 30 years; some providers use shorter terms. The CFPB has also flagged real risks: repayment is usually a single future lump sum that can be hard to predict, may reach into the hundreds of thousands of dollars, and can force a sale if the homeowner can’t pay at the trigger event (CFPB Issue Spotlight on Home Equity Contracts, 2025). HEI providers operate only in select states, not nationwide — availability has to be checked for your parent’s specific state before treating it as a live option.

Two questions to ask any HEI provider, because the answers swing the cost by tens of thousands: (1) Does the company share in the value the ADU itself adds, or only the home’s baseline appreciation? (2) What exactly triggers settlement, and what happens if my parent can’t pay at term?

Benefit caution

A HECM’s proceeds are treated as loan proceeds under Social Security’s rules, but an HEI is a newer contract category — the CFPB notes these products are often marketed as “not a loan.” Do not assume HEI proceeds get the same SSI or Medicaid treatment as a bona-fide loan. If your parent is on or near needs-based benefits, verify the treatment with a state-licensed elder-law attorney before funds move.

Explore no-monthly-payment ADU financing. If your parent has equity but can’t take on a payment, an HEI provides a lump sum with no monthly bill. These products are state-restricted and the benefit interaction is nuanced — check what’s available where your parent lives and confirm the SSI/Medicaid treatment first.

Affiliate link — we may earn a commission at no extra cost to you. Never affects our recommendations.

See no-monthly-payment options →Path 5 — Cash and pooled family money

When a parent downsizes or sells, contributing cash to a build on the adult child’s land can avoid debt entirely — but it is never “just family helping family,” because the contribution carries gift, loan, title, sibling, and Medicaid consequences that must be documented before money moves. A common, workable combination: the parent’s sale proceeds cover part of the build while the adult child finances the balance with a HELOC.

The structure question is the whole ballgame. There are five legitimate ways to frame a parent’s contribution — they are not interchangeable:

| Structure | What it means | Who signs | Main risk | Professional to involve |

|---|---|---|---|---|

| Gift | Parent gives money with nothing owed back | Gift letter; possible gift-tax filing | Counts as a transfer for Medicaid look-back; reduces parent’s assets | Tax advisor + elder-law attorney |

| Loan | Parent lends; child repays on terms | Promissory note | Must be bona fide and documented to be treated as a loan | Attorney |

| Rent prepayment | Parent pre-pays occupancy | Written lease/agreement | Affects parent’s resources and possibly SSI | Attorney |

| Occupancy right / lease for life | Parent funds build, gets legal right to live there for life | Recorded agreement | Survives a sale/divorce only if drafted right | Elder-law attorney |

| Estate equalization | Other siblings’ inheritance is adjusted to offset | Estate-plan documents | Fails if left informal | Estate attorney |

Will financing an ADU affect my parent’s Medicaid or SSI? The structure tripwire

A reverse mortgage or any bona-fide loan is treated as loan proceeds, not income — so it does not reduce Medicaid or SSI by itself. But money that sits unspent in your parent’s bank account past the end of the month it arrives can convert from an exempt loan into a countable resource the following month, which can push your parent over the asset limit and suspend benefits. The federal SSI resource limit is $2,000 for an individual and $3,000 for a couple; Medicaid asset limits are set by state and program.

The same-month rule, in plain English

Social Security’s program manual is explicit. Under POMS SI 00815.350, proceeds of a bona-fide loan are not income to the borrower because of the obligation to repay. But under the companion resource rule POMS SI 01120.220 (updated May 28, 2024), any of those loan proceeds still sitting in the account after the month of receipt count as a resource going forward.

The practical effect: money that is invisible to Medicaid and SSI on the last day of the month it arrives can become a disqualifying asset on the first day of the next month. AARP states the same principle from the homeowner’s side — a reverse mortgage is a loan, not a countable asset, when spent in the same month it’s received (AARP Policy Book).

Lump sum vs. line of credit — why structure beats source

For a parent on or near Medicaid/SSI, how the money is taken matters more than where it comes from:

- A lump sum is the dangerous form. A $50,000 reverse-mortgage draw deposited in January and not fully spent by January 31 can be counted as a resource in February — and a single deposit can blow past the $2,000 SSI limit many times over.

- A line of credit is the protective form. Elder-law guidance widely recommends taking a HECM as a line of credit rather than a lump sum, drawing only what’s spent that month, so unspent funds never accumulate. A draw made and paid to the builder within the same month never becomes a countable resource.

- Paying a contractor directly in the month of the draw — rather than parking the money — keeps the funds from ever sitting as a resource.

SSI and Medicaid are not the same limit — and the state matters

The $2,000 / $3,000 figures are the federal SSI resource limits. Medicaid asset limits are state- and program-specific, especially for long-term-care Medicaid, and they can be far higher. California is the clearest current example: after eliminating its asset test entirely, California reinstated a Medi-Cal asset limit on January 1, 2026 — $130,000 for one person, plus $65,000 for each additional household member — for non-MAGI programs covering seniors, people with disabilities, and long-term care (California DHCS; Justice in Aging; CANHR, verified ). California also applies a 30-month look-back for certain nursing-home transfers made on or after January 1, 2026. The lesson is that you must verify your own state’s current Medicaid asset and look-back rules before structuring a parent-funded build.

The unsoftened limitation

These rules are state-variable, and getting them wrong can disqualify a parent from care they genuinely need at the worst possible moment. If your parent receives or might apply for Medicaid or SSI, talk to a state-licensed elder-law attorney before any money moves. A Medicaid planner can help organize documents, but should not replace legal advice unless they’re also licensed to give it.

Download the free 2026 ADU Starter Kit

It includes the family-money worksheet, a parent-contribution checklist, and the exact questions to bring to an elder-law attorney before a gift, loan, or reverse-mortgage draw — so the benefit conversation starts organized.

Get the free ADU Starter Kit →Can living rent-free in my ADU reduce my parent’s SSI?

Yes, potentially — and this surprises almost every family. Even when ADU financing doesn’t count as income, letting a parent who receives SSI live rent-free or below market can be treated as “in-kind support and maintenance” (ISM) and reduce their monthly SSI check. If your parent is on SSI, decide whether they’ll pay fair-share rent before you assume the arrangement has no benefit impact.

Here’s how Social Security handles it. ISM is shelter someone else provides for you, and it can reduce an SSI payment by as much as $351.33 per month in 2026 — the “presumed maximum value,” equal to one-third of the federal benefit rate plus $20 (SSA, Understanding SSI 2026 edition). If a parent lives in a unit you own and pays nothing toward shelter, SSA can count that free housing as ISM and dock the check up to that cap.

The clean fix: pay rent ≥ $351.33 (2026 PMV)

The clean workaround SSA itself describes: if your parent pays rent at least equal to the presumed maximum value ($351.33 in 2026), SSA generally treats it as a bona-fide business arrangement and applies no ISM reduction, no matter how far below true market rent that figure is (20 C.F.R. § 416.1130(b); SSA).

One useful recent change in your parent’s favor: as of September 30, 2024, food is no longer counted in ISM calculations — only shelter is. The practical move for an SSI parent in your ADU is a simple, documented monthly rent set at or above the PMV.

This is genuinely good news wrapped in a rule: a small, documented rent solves the problem. But it has to be deliberate, and it’s exactly the kind of detail an elder-law attorney should confirm for your state and your parent’s situation.

Can my parent pay to build an ADU on my property?

Yes — but it should be documented before any money moves, as a gift, loan, rent prepayment, ownership contribution, or estate-plan adjustment, because a parent putting six figures into an asset on a child’s land raises gift-tax, sibling-equity, and Medicaid look-back questions all at once. A parent contributing cash to a build on your land is converting their money into value on your property. That can be entirely reasonable — it just can’t be informal.

The structures and who-signs-what are in the Path 5 table above. The risk that makes documentation non-negotiable is the Medicaid look-back: federal law (the Deficit Reduction Act) sets a 60-month (5-year) look-back for long-term-care Medicaid, during which transfers of assets for less than fair market value can create a penalty period of ineligibility (CMS; 42 U.S.C. § 1396p). A parent who gifts money toward your ADU and then needs nursing care within five years can face a penalty — even though the money is gone.

There is a narrow, documented exception built for exactly the caregiving situation many of these families are in: the Child Caregiver Exemption can let a parent transfer their home to a son or daughter without a look-back penalty if that child lived in the home for at least two years immediately before the parent entered care and provided care that allowed the parent to delay institutionalization (42 U.S.C. § 1396p; elder-law practice guidance). State documentation standards matter, and the relationship interpretation can vary — this is attorney territory.

Adding a child to the title as joint owner generally does not provide the protection families expect — the parent’s interest is usually still counted. A lease for life can give a contributing parent the legal right to occupy the ADU even if you later sell, refinance, divorce, or pass away — without transferring ownership. Estate-recovery rules (the state’s right to recover Medicaid costs from an estate after death) vary significantly by state.

Have an elder-law attorney structure any transfer or parent-funded build before construction money moves. The single document that separates a protected transfer from a penalized one is worth far more than the consult costs.

Can ADU rental income help us qualify for financing if the ADU is for a parent?

Sometimes — but usually not when the parent will live there rent-free or below market. Mortgage programs that let you count ADU rental income to help qualify generally require a lease, a market-rent appraisal, and documentation, and a parent living rent-free is family housing, not rental income. FHA’s Mortgagee Letter 2023-17 requires documentation of proposed ADU rental income and caps ADU rental income used as effective income at 30% of total monthly effective income; FHA also expects lease/market-rent support and, where rental income is used, reserve requirements may apply (HUD ML 2023-17).

| ADU use | Can it help you qualify? | Practical note |

|---|---|---|

| Existing ADU with a documented lease | Possibly | Depends on the loan program and documentation |

| New ADU intended for market rent | Possibly | Appraisal/market-rent documentation typically required |

| Parent lives rent-free | Usually not as rental income | It’s family housing, not qualifying rent |

| Parent pays an informal family amount | Uncertain | Lenders may not treat informal payments as qualifying rent |

| Future rental after the parent moves out | Not for current qualification | Useful for long-term planning, not underwriting today |

These are illustrative examples, not guarantees of returns or qualification. Actual results depend on local market conditions, construction costs, financing terms, lender programs, and regulatory approvals.

Is financing an ADU cheaper than assisted living?

For a parent who is still largely independent, an ADU can beat assisted living on a multi-year cost comparison — because it’s a one-time investment rather than a recurring bill, and it leaves a permanent asset behind — provided build cost, financing, taxes, insurance, maintenance, and care needs stay within your assumptions. Assisted living’s 2025 national median is $6,200/month, or $74,400/year (CareScout 2025 Cost of Care Survey, data collected July–November 2025).

The crossover math, run honestly on the simple pre-financing comparison: at $74,400/year, a $200,000 ADU breaks even in roughly 2.7 years; a $350,000 ADU in roughly 4.7 years; a $400,000+ build crosses later. Financing costs, property taxes, insurance, maintenance, and any escalation in your parent’s care needs all move that line — so treat these as starting points, not promises. The full 10-year model is in our main ADU for Aging Parents guide.

The financing-relevant takeaway: an ADU converts an open-ended monthly drain into a financeable, one-time project that can later generate rent or resale value. That’s exactly why families stretch to fund it — and exactly why the structure decisions above matter so much.

Cost comparisons are illustrative, not guarantees of savings. Actual results depend on care needs, local care and construction costs, financing terms, taxes, and insurance. An ADU is not a substitute for medical care; if your parent needs memory care or skilled nursing, that’s a care decision, not a financing one.

Which financing path fits your family? Use the Path Finder

The fastest way to narrow six lanes down to your real two or three is to answer a short set of family-specific questions — who owns the land, who has equity, who can carry a payment, your parent’s age, benefits status, whether the parent will keep their current home, the ADU budget, and whether your parent will pay rent. The Path Finder runs that logic for your exact combination and surfaces the one or two benefit cautions that apply to your situation — the part a generic article can describe but can’t personalize.

Answer a handful of questions and you’ll get: your first path to test, the paths to rule out, what to verify before applying, which professional to call first (lender, HUD counselor, or elder-law attorney), and the family-documentation checklist to bring to the table. It reads your situation the way an experienced advisor would — including the two traps most families miss: whether a HECM-funded parent will actually keep their home as a primary residence, and whether an SSI parent should pay fair-share rent.

Find your ADU financing path. Answer a few questions about your property and your parent’s situation and get your personalized path plus the benefit rules that apply to you.

Get Your Free ADU Report and Financing Path →What to do before you apply for financing

Do not apply for a loan first. Confirm the ADU is legal and physically possible on your lot, choose the setup that fits your parent’s care needs, build a real all-in budget, decide who owns and who pays, settle any benefit and estate questions with an attorney, and only then match the financing lane. Applying before you know the build cost and lot constraints is how families end up with the wrong product and a second set of closing costs.

- Confirm property feasibility — zoning, setbacks, size limits, utility connections.

- Choose the setup — attached, detached, garage conversion, or internal suite (see the main guide).

- Build an all-in budget — unit + site work + utilities + design + permits + accessibility + 10–15% contingency.

- Decide who owns and who pays — and put parent contributions in writing.

- Clear benefits and estate questions — elder-law attorney if Medicaid/SSI or large transfers are in play, including the HECM occupancy and SSI-rent points above.

- Match the financing lane — using the matrix above.

- Apply only when scope, budget, and documentation are clear.

See what you can build → get your free ADU report. Step one is always the same: confirm what your lot can legally support and what it’s likely to cost, before you compare a single financing offer.

Start with your free feasibility report →What we verified for this guide

| Claim | Source | Verified |

|---|---|---|

| 2026 HECM maximum claim amount $1,249,125 | HUD (2026 HECM limit) | |

| HECM first-year draw = greater of 60% of principal limit or mandatory obligations + 10% | HUD | |

| HECM occupancy: 12+ consecutive months away ends principal-residence status; loan due | CFPB reverse mortgage rules | |

| Loan proceeds aren’t income; unspent funds become a countable resource next month | SSA POMS SI 00815.350 & SI 01120.220 (updated 05/28/2024); AARP Policy Book | |

| Federal SSI resource limits $2,000 / $3,000 | SSA | |

| SSI ISM reduction up to $351.33 (2026 PMV); fair-share-rent workaround; food excluded since 09/30/2024 | SSA, Understanding SSI 2026; 20 C.F.R. § 416.1130 | |

| California Medi-Cal asset limit reinstated 01/01/2026: $130,000 + $65,000 per additional member; 30-month LTC look-back | California DHCS; Justice in Aging; CANHR | |

| Medicaid 60-month look-back; Child Caregiver Exemption | CMS (Deficit Reduction Act); 42 U.S.C. § 1396p | |

| FHA ADU rental income capped at 30% of effective income; documentation/reserves may apply | HUD Mortgagee Letter 2023-17 | |

| Fannie Mae HomeStyle & construction-to-perm cover ADUs; Freddie Mac CHOICERenovation covers ADUs | Fannie Mae & Freddie Mac Single-Family product pages | |

| HEI terms typically 10–30 years; settlement/foreclosure risks; “not a loan” marketing | CFPB Issue Spotlight on Home Equity Contracts (2025) | |

| Assisted living 2025 median $6,200/mo ($74,400/yr); crossover math | CareScout 2025 Cost of Care Survey | |

| Detached ADU $200,000–$400,000+; garage conversion $80,000–$175,000 | The Dwelling Index ADU cost guide |

How we built this guide

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We organized financing by family situation rather than by lender compensation, and we reviewed primary sources — HUD, the Social Security Administration’s POMS manual and Understanding SSI, the CFPB, CMS and 42 U.S.C. § 1396p, California DHCS, AARP, and CareScout — alongside elder-law practitioner guidance and our own existing cost and financing coverage. We used family-forum discussions only to understand how families describe the problem in their own words, never as proof for financing, legal, tax, Medicaid, or zoning claims. Editorial conclusions are based on the verified facts above.

This page is educational and does not provide legal, tax, lending, Medicaid, or elder-care advice. We are not a lender, broker, builder, or attorney.

By: The Dwelling Index Editorial Team · Last updated: · Last verified: · Editorial methodology · Affiliate disclosure

Frequently asked questions

- Can a reverse mortgage be used to build an ADU for a parent?

- Yes, if the parent is 62 or older, owns and occupies the home, and meets HUD requirements including approved counseling. Proceeds can fund an ADU. The catches: the first-year draw is generally capped at the greater of 60% of the principal limit or mandatory obligations plus 10%, which may limit upfront cash, and the home must remain the parent's principal residence — moving out for more than 12 consecutive months can make the loan due.

- Will a reverse mortgage or HEI disqualify my parent from Medicaid or SSI?

- A bona-fide loan like a HECM is not income (SSA POMS SI 00815.350), but unspent proceeds left past the month received become a countable resource the next month, which can exceed the $2,000 SSI individual limit. Taking funds as a line of credit and spending each draw the same month is the common protective structure. An HEI is a newer contract category whose benefit treatment is not assured — confirm it with an elder-law attorney before relying on it.

- Can my parent pay to build an ADU on my property?

- Yes, but document it first as a gift, loan, rent prepayment, ownership contribution, or estate-plan adjustment. A parent contributing six figures to an asset on a child's land raises gift-tax, sibling-equity, and Medicaid look-back questions, and the 60-month look-back can create a penalty if the parent needs long-term-care Medicaid within five years. An elder-law attorney and tax advisor should review it.

- Will letting my parent live rent-free in the ADU affect their SSI?

- It can. Free or below-market shelter can be counted as in-kind support and maintenance (ISM) and reduce a parent's SSI by up to $351.33 per month in 2026. If your parent pays rent at least equal to that presumed maximum value, SSA generally treats it as a business arrangement with no reduction. Food is no longer counted as ISM as of September 30, 2024.

- What is the cheapest way to finance an ADU for an aging parent?

- The lowest-cost path is usually cash from downsizing combined with the adult child's existing equity, because it avoids interest and fees entirely. Among financed options, a HELOC on the child's home is often cheapest when the child has equity and income. Reverse mortgages and HEIs solve cash-flow problems but carry fees or shared appreciation.

- Can I get a loan in my own name to build an ADU for my parents?

- Yes — if you own the property, you can finance the ADU with a HELOC, home equity loan, cash-out refinance, or renovation loan in your name. This is common when the parent has little income or equity. The loan is your obligation and your home is the collateral, so the payment must fit your budget.

- Does building an ADU raise my property taxes?

- Usually to some degree, though treatment varies by state and county — in some areas only the value of the new construction is added to the assessment. Verify the expected impact with your county assessor before budgeting, especially if a fixed-income parent will share carrying costs.

- Is a HELOC better than a cash-out refinance for an ADU?

- A HELOC or home equity loan preserves a low existing first mortgage by adding only a second lien for the ADU amount. A cash-out refinance replaces the entire mortgage and usually makes sense only when your current rate is already unfavorable. Compare total interest cost over the life of each loan, not just the monthly payment.

- What happens to the ADU financing if my parent moves to a nursing home or passes away?

- With a reverse mortgage, the loan becomes due when the borrower permanently leaves the home — and an absence over 12 consecutive months can trigger that — unless an eligible co-borrower or non-borrowing spouse remains. An ADU financed on the adult child's property simply continues as the child's asset and can become a rental, guest house, or caregiver suite. Plan the exit before you build.

- Are there grants to help finance an ADU for aging parents?

- Some local and state programs exist, but national grant coverage is limited and often paused, income-restricted, or tied to affordability covenants. Treat grants as a possible supplement, not a primary plan, unless you've verified an open program in your jurisdiction. Most families finance through equity, reverse mortgages, HEIs, or family contributions.

Get the free ADU Starter Kit

The full family-financing roadmap in one place: the parent-contribution checklist, the SSI-rent worksheet, the Medicaid question list for your elder-law attorney, and every document your lender will ask for — free, in your inbox.

Download the free ADU Starter Kit →Not sure where to start?

See what’s possible at your address — get your free ADU report in 60 seconds. Structure first. Loan second.

Get Your Free ADU Report →