ADU Financing Washington: 8 Ways to Pay for a Legal ADU in 2026

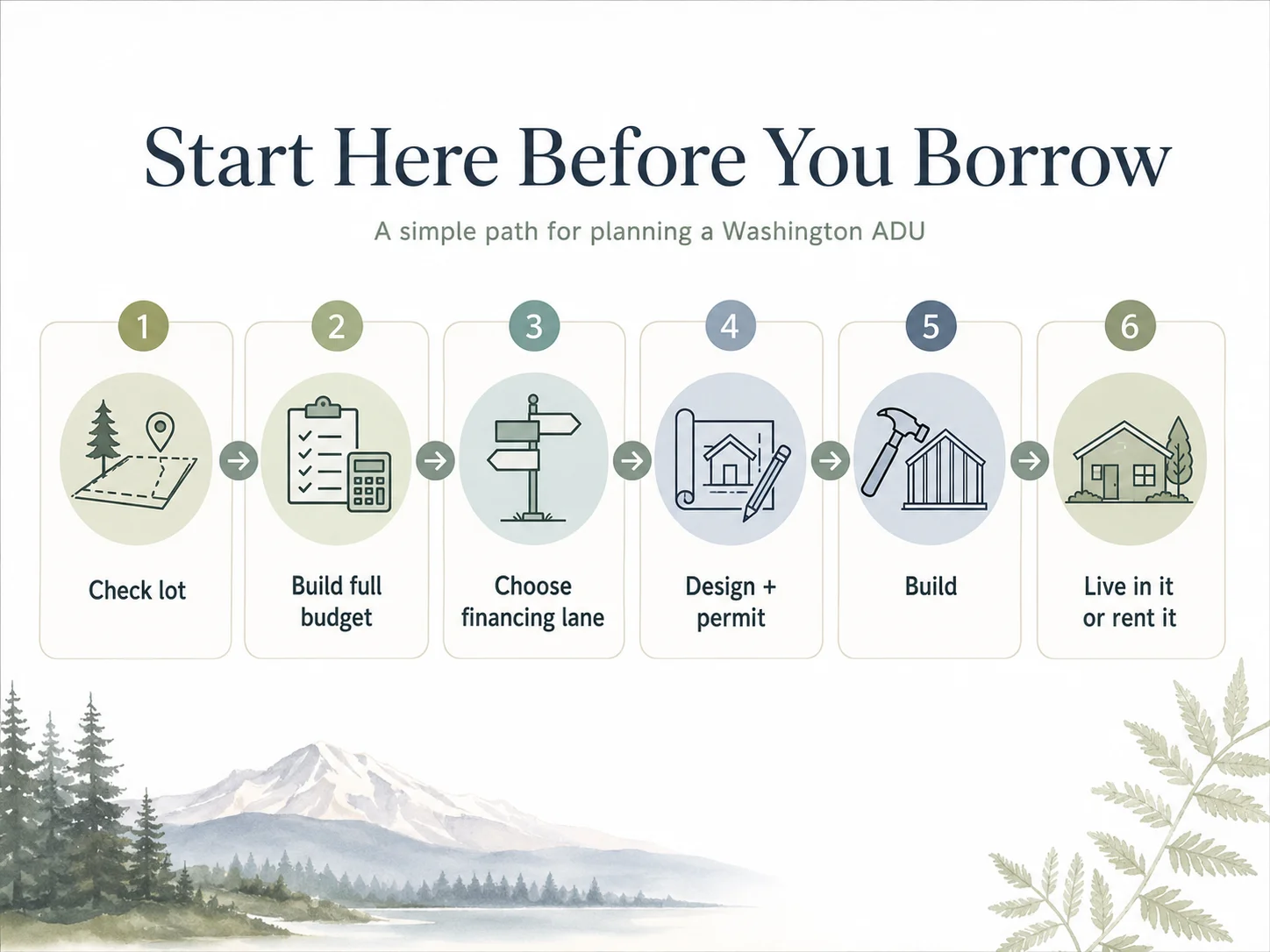

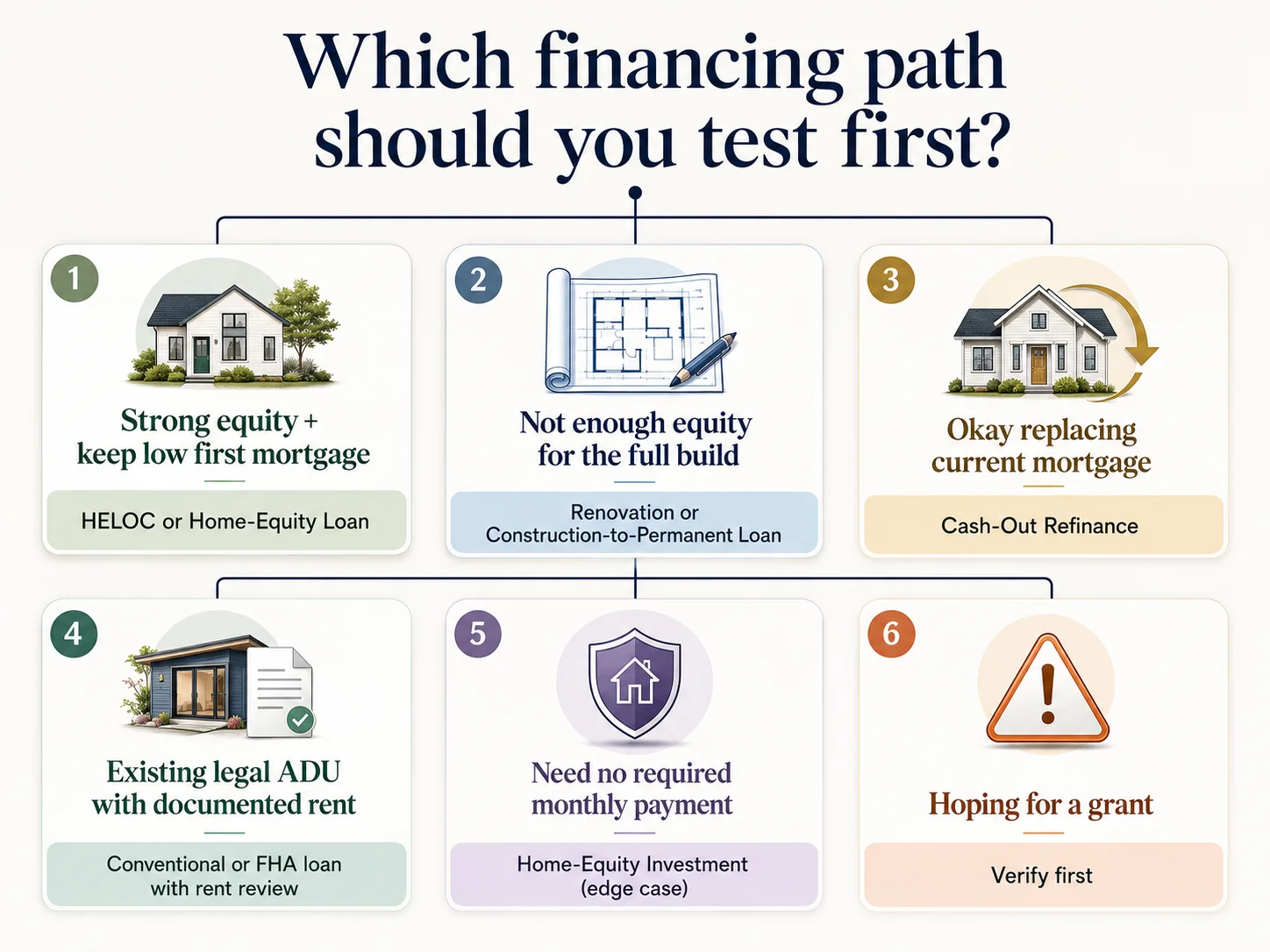

For ADU financing Washington homeowners usually test one of three lanes first, and which one fits is decided by your equity and your current mortgage rate — not by the lender with the best ad. If you have enough usable equity and a low first mortgage worth protecting, test a HELOC or home-equity loan first. If your budget is bigger than your equity, test a renovation or construction-to-permanent loan that lends against the finished value. A cash-out refinance only makes sense if your current mortgage rate is already close to today's rates. Budget realistically: a detached ADU in the Seattle and Eastside market commonly runs $300,000–$650,000+ all-in, while a Seattle garage conversion can run closer to $100,000–$150,000. New for the 2026 underwriting rollout: under Fannie Mae, rental income from an existing ADU may help you qualify on a one-unit principal residence for a purchase or limited cash-out refinance, from one ADU only, capped at 30% of qualifying income. The right first move isn't picking a loan — it's confirming your lot can actually be built on.

A quick, honest admission before you read further: Washington made ADUs dramatically easier to permit. It did not make them cheap, automatic, or automatically lendable. The biggest financing mistakes in this state happen before anyone fills out a loan application — choosing a loan before confirming the lot is buildable, underbudgeting for sewer and utilities, or assuming future rent will carry the deal. The whole point of this guide is to keep you out of those traps. There's good news on the other side of each one, and a clear path through.

We are not a lender, broker, or builder. We don't rank lenders by who pays us, and we'll tell you plainly when a popular option is wrong for your situation — including when it costs us a referral.

Why trust this page (and what we verified)

We built this guide from primary Washington law (the Revised Code of Washington and the Department of Commerce), official city permit pages for Seattle, Tacoma, Kirkland, Bellevue, and Spokane, federal mortgage underwriting sources (Fannie Mae, Freddie Mac, and HUD/FHA), public program pages (USDA, Washington Commerce), and clearly labeled builder- and lender-published cost signals. Where a number is a market estimate rather than a guarantee, we say so and give the range. Forum comments were used only to understand how homeowners describe the problem — never as proof of law, cost, or loan terms. Every factual claim links to its source, and the full source list with verification dates is in the "What we verified" box near the end.

ADU financing Washington: which path should you test first?

Answer capsule: The best first financing path for a Washington ADU is the one that matches your usable home equity, protects a low first mortgage if you have one, covers the full city-specific budget including permits and utilities, and does not depend on rental income a lender won't count. For homeowners with substantial equity, that usually means a home-equity line of credit (HELOC) or home-equity loan; for those with thinner equity or a larger detached build, it usually means a renovation or construction-to-permanent loan that lends against the project's completed value.

Here's the decision in one screen. Find your situation, see the first lane to test, and note what to watch out for.

| Your situation | First path to test | Why it fits | Watch out for |

|---|---|---|---|

| Strong equity + a low first mortgage you want to keep | HELOC or home-equity loan | Leaves your first mortgage untouched | Borrowing room is based on today's value, not the finished value; HELOC rates are usually variable |

| Not enough equity for the full build | Renovation loan or construction-to-permanent loan | Can lend against the as-completed value | More paperwork, inspections, contractor requirements, and draw schedules |

| You're fine replacing your current mortgage | Cash-out refinance | One consolidated loan, fixed for up to 30 years | A costly mistake if it replaces a sub-5% pandemic-era mortgage |

| Buying or refinancing a home that already has a legal ADU | Conventional / FHA loan with ADU rent review | Existing, documented rent may help you qualify | Rent is discounted (typically to 75%) and capped (30% of income); illegal-ADU rent can't count |

| You need no required monthly payment | Home-equity investment (HEI), edge case only | No monthly payment during the term | Complex repayment, Washington regulatory scrutiny, limited provider availability |

| You're hoping for a grant | Verify first — don't build the plan around it | A few narrow programs exist | No broad statewide homeowner ADU-construction grant is currently verified in Washington |

Definitions: A HELOC (home-equity line of credit) is a revolving credit line secured by your home, usually at a variable rate. A DADU is a detached accessory dwelling unit — a standalone backyard cottage. An AADU is an attached accessory dwelling unit, like a basement or addition. An HEI (home-equity investment, also called a HESA or home-equity sharing agreement) gives you cash today in exchange for a share of your home's future value, with no monthly payment but a lump-sum settlement later.

Free property check

See what you can build → Get your free ADU report

Before you choose a loan, check your lot. Our free property check flags likely buildability issues, the ADU type your parcel supports, and the financing questions worth bringing to a lender.

Check my property for free →Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

What's the best way to finance an ADU in Washington?

Answer capsule: The best way to finance an ADU in Washington is to start from your own constraints rather than from lender shopping. The path that fits matches four things: how much usable equity you have today, whether your current first mortgage is worth protecting, whether the project needs construction draws or after-build value to pencil, and whether you need rental income to qualify. For many Washington owners that means a HELOC or home-equity loan first; for larger detached units or lower-equity homes, a renovation or construction-to-permanent loan.

There is no single "best loan." There's a best loan for your numbers. We see homeowners waste weeks shopping lenders before they've answered the five questions that actually determine the answer. Run these first.

The five-question Washington financing fork

- 1

Do you have enough usable equity today?

Most home-equity lenders will lend up to roughly 80–85% of your home's current value minus your existing mortgage balance. If you bought recently or prices have softened, your borrowing room may fall short of a $400,000 detached build. That single fact pushes many people toward after-build-value products.

- 2

Is your current first mortgage worth protecting?

If you locked a rate in the 3% range during 2020–2021, a cash-out refinance would re-price your entire mortgage balance at today's rates just to extract ADU cash. That's usually the most expensive way to fund a backyard cottage. A HELOC or home-equity loan sits behind your first mortgage and leaves it alone.

- 3

Does the project need construction draws or as-completed value?

Ground-up detached units usually need a construction or renovation loan that releases money in stages tied to inspections and lets you borrow against what the home will be worth after the ADU exists.

- 4

Do you need rent to qualify?

If your debt-to-income ratio only works when you count the ADU's future rent, you're in a narrower lane with specific rules (covered in the rent section below).

- 5

Is the property actually buildable under your city and site conditions?

This is the question most people answer last and should answer first. We'll explain why in the next section.

The City of Kirkland's own ADU Toolkit lists the same core menu homeowners reach for — HELOCs, home-equity loans, cash-out refinances, construction loans, and personal loans — and pairs it with a blunt warning we'll echo throughout: many banks will not count potential rental income when they assess what you qualify for. (Source: City of Kirkland, "Paying for Your ADU," accessed May 2026.)

For the mechanics of each loan type — how a HELOC draw period works, how construction-to-permanent loans convert, how the Fannie Mae HomeStyle and Freddie Mac CHOICERenovation programs differ — see our national ADU Financing Options and HELOC vs. Construction Loan guides. This page tells you which lane to test first as a Washington homeowner, then hands you off to those for the nuts and bolts.

Explore mortgage-backed ADU financing

Compare ADU loan options through our financing research partner →

Mortgage Research Center (NMLS #1907; WA Consumer Loan Company License #CL-1907). Educational resource only — loan approval, terms, and availability depend on lender underwriting, your credit, income, equity, the property, and applicable state rules. No rate, payment, or approval is guaranteed.

Explore mortgage-backed ADU financing options →Before you borrow: does your Washington lot even qualify?

Answer capsule: Washington's House Bill 1337 (codified at RCW 36.70A.680, .681, and .696) requires cities and counties planning under the Growth Management Act to allow at least two ADUs on most residential lots inside urban growth areas that already permit single-family homes. But RCW 36.70A.680 expressly does not force approval where development is limited by on-site sewage capacity, critical areas, wetlands, floodplains, geologic hazards, lack of public sewer, or public-health and building-code constraints. A lot can be "legal for an ADU in Washington" and still fail a site check — which is why feasibility comes before loan selection.

The Dwelling Index — Washington ADU: start here before you borrow

The damaging admission, stated plainly because it saves the most money: Legal to build is not the same as buildable, and buildable is not the same as financeable. Here's the hopeful part — once you clear the site check, Washington's law is genuinely one of the most ADU-friendly frameworks in the country, and clearing it early is cheap insurance against a five-figure surprise.

For the full city-by-city rules, see our companion guide on Washington ADU laws.

What Washington state law gives you (the financing tailwind)

House Bill 1337, signed in 2023, applies to each jurisdiction through the Growth Management Act periodic comprehensive-plan update schedule. Once it applies, HB 1337 requires GMA-planning jurisdictions to:

- ✓Allow at least two ADUs per lot on residential lots inside urban growth areas that permit single-family homes — attached, detached, or a combination. (RCW 36.70A.681; WA Dept. of Commerce ADU guidance, accessed May 2026.)

- ✓Permit detached ADUs (DADUs), not just attached units.

- ✓Not cap ADU size below 1,000 square feet of gross floor area.

- ✓Not impose owner-occupancy requirements in most cases — meaning you can rent both the main house and the ADU, which materially expands financing flexibility.

- ✓Cap ADU impact fees at 50% of those charged on the principal unit. (WA Dept. of Commerce; HB 1337 summary, accessed May 2026.)

- ✓Not require off-street parking for an ADU within one-half mile walking distance of a major transit stop, and limit parking elsewhere.

- ✓Not prohibit selling an ADU as a condominium separately from the principal unit solely because it began life as an ADU.

The brand-new 2026 piece: rural lots get a path (HB 1345)

If your property sits outside an urban growth boundary — the gap HB 1337 left open — there's fresh news. House Bill 1345 was signed by Governor Bob Ferguson on March 27, 2026, and takes effect June 11, 2026. It allows counties planning under the Growth Management Act to permit detached ADUs on rural properties outside urban growth areas. (Source: Washington State Legislature, accessed May 2026.) Whether it applies to your rural parcel depends on your county opting in, so confirm current status with your county planning department before assuming a rural ADU — and therefore its financing — is viable.

What state law does not give you

This is where loans fall apart. State law does not hand you:

- ✕Automatic sewer or septic approval

- ✕Automatic buildability on critical-area, wetland, or steep-slope lots

- ✕Automatic lender approval

- ✕Guaranteed rental-income treatment in underwriting

- ✕Guaranteed short-term-rental legality

- ✕A guaranteed construction cost

- ✕Guaranteed separate-sale economics

Free property check

See what you can build → Get your free ADU report

The check flags likely buildability issues — sewer, critical areas, lot fit — and the ADU type your parcel supports, so you don't pick a loan for a project your site won't allow.

Check my property for free →How much should you budget before choosing a Washington ADU loan?

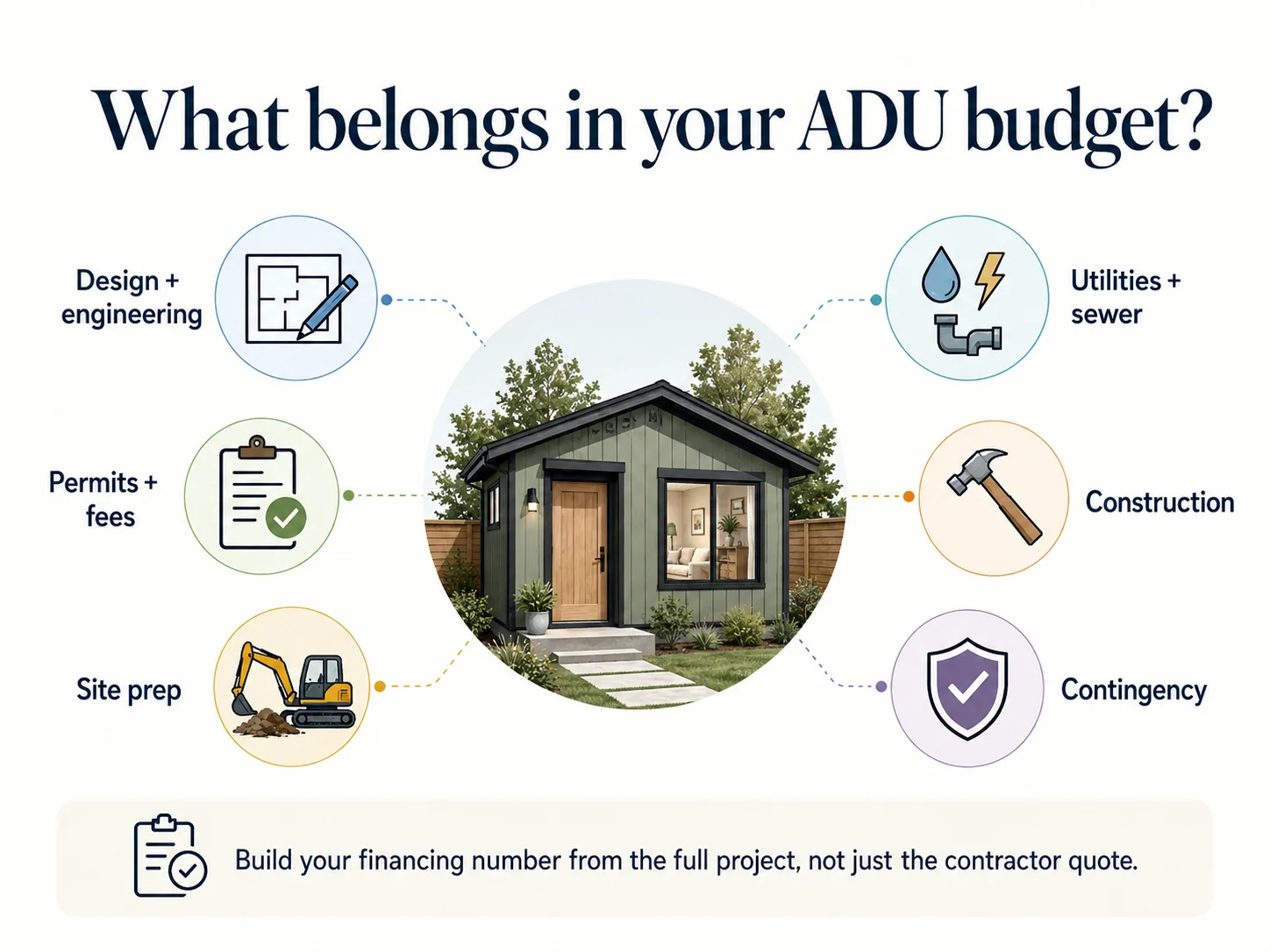

Answer capsule: A Washington ADU borrowing budget should never come from a construction-only estimate. It needs to include design and feasibility, permits and city fees, utility and sewer work, site preparation, Washington sales tax on construction, a contingency, financing costs, and post-build reserves. Published 2026 cost signals range widely: from roughly $150,000–$250,000 for smaller ADUs to $300,000–$650,000+ for detached Seattle-area units.

Published Washington ADU cost signals (2026)

| ADU type / area | Published cost signal | Source type | How to use it |

|---|---|---|---|

| Smaller Washington ADUs (general) | $150,000–$250,000 depending on size and finishes | Local lender-published (Olympia Federal Savings, accessed May 2026) | A reasonable lower-to-mid planning signal, not a statewide guarantee |

| Washington DADUs (general) | $250,000–$450,000 | Builder-published (Goodwin Construction, accessed May 2026) | A broad detached-unit planning range |

| Garage conversion (Seattle) | ~$100,000–$150,000 | Builder-published (multiple Seattle sources, accessed May 2026) | The most affordable common path |

| Seattle detached ADUs | $300,000–$650,000+; roughly $400–$700/sq ft all-in | Builder-published (multiple Seattle/Eastside builders, accessed May 2026) | The realistic Seattle DADU budgeting band |

| Seattle DADU vs. AADU split | DADU $250,000–$650,000; attached $80,000–$450,000 | Builder-published (Nine8 Redevelopment, accessed May 2026) | Use to separate detached from attached/converted budgets |

All cost figures above are planning signals from lender- and builder-published sources accessed January–May 2026. They are not guaranteed costs or bids. Get at least two to three written quotes for your specific site before locking a loan amount.

Notice the spread. A garage conversion and a two-story detached cottage are both "ADUs," but they're a quarter-million dollars apart. Do not apply a generic national "$100K–$300K" range to a Seattle detached build, and don't apply a Seattle detached budget to a Spokane garage conversion. Matching the cost band to your actual project and city is the difference between a loan that closes and one that comes up short mid-build.

The Washington-specific costs most borrowers forget

Sewer treatment / capacity charges

Seattle's SDCI reports new ADUs to King County for sewer treatment capacity charges, and a new detached unit can trigger a side-sewer connection. As of October 1, 2025, Seattle Public Utilities — not SDCI — handles side-sewer permitting.

Electrical service upgrades

Seattle City Light service changes are common for detached units. Factor this into your loan amount from day one.

Water, sewer line work & stormwater

Drainage and stormwater review add cost on many Seattle lots, especially those with tree coverage or slope.

Site work & tree-protection rules

Seattle's tree-protection rules can add significant cost on lots with exceptional trees. Don't underestimate grading and access prep.

Washington sales tax on construction

Washington applies retail sales tax to the total contract price on custom residential construction. The combined Seattle rate is 10.55% as of January 1, 2026 — routinely missing from headline quotes.

Contingency (10–20%)

Most experienced builders advise a 10–20% contingency for the unknowns. Smaller ADUs often carry a higher cost per square foot because fixed costs spread across less area.

The Dwelling Index — Washington ADU budget components: what belongs in your loan amount

Free download

Download the free ADU Starter Kit →

Get the budgeting worksheet, a Washington permit-and-utility cost checklist, and the lender-question list — so the number you borrow against includes the costs most quotes leave out.

Get the free ADU Starter Kit →How does ADU financing change between Seattle, Tacoma, Kirkland, Bellevue, and Spokane?

Answer capsule: The loan products are national, but the cash you need is local. City-level differences — Seattle's sewer capacity charges, Tacoma's site-specific review of pre-approved plans, Kirkland's low pre-approved-plan license fee, Bellevue's still-developing plan program, and Spokane's lower fees and faster review — change both how much you must borrow and how much contingency to carry.

| Jurisdiction | Verified process detail | What it means for your loan budget |

|---|---|---|

| Seattle | ADUs aren't legal until permitted and must meet current code; SDCI reports ADUs to King County for sewer treatment capacity charges; pre-approved DADU plans (ADUniverse) can cut review to roughly 1–6 weeks vs. months for custom; permit fees commonly $4,000–$12,000 plus school impact fees. (City of Seattle SDCI; Seattle Services Portal, accessed May 2026.) | Budget specifically for sewer-capacity and utility work and Seattle's 10.55% sales tax; a standard plan can lower preconstruction uncertainty and soft costs. |

| Seattle standard-plan path | The expedited pre-approved DADU path requires NR-zoned lots, no environmentally critical areas, and less than 750 sq ft of total ground disturbance. (Seattle Services Portal, accessed May 2026.) | Don't assume your lot qualifies for the fast path; wrong site conditions push you back to custom review and higher soft costs — size your contingency accordingly. |

| Tacoma | Offers four pre-approved DADU base models; the city is explicit that plans streamline permitting but are not pre-permitted and still require site-specific review for utilities, critical areas, historic districts, and fire access. (Tacoma Permits, accessed May 2026.) | Pre-approved plans can cut design cost, but lenders still need a full project budget and site-specific approvals before funding. |

| Kirkland | Pre-approved plan program with a license fee of no more than $1,000; pre-approved plans can permit in a few weeks versus roughly three months for custom. (City of Kirkland ADU Toolkit, accessed May 2026.) | A strong 'pre-approved plan + financing path' example with low plan-license cost folded easily into a loan budget. |

| Bellevue | 2025 middle-housing code changes allow ADUs and DADUs on residential lots; a pre-approved-plan program has been in development. (City of Bellevue, accessed May 2026.) | Confirm current pre-approved-plan status with the city before assuming plan-cost savings. |

| Spokane | Allows detached ADUs; review commonly runs about 6 weeks with fees frequently in the low thousands; Spokane has used temporary ADU permit-fee waivers/reductions in recent years. (City of Spokane / MRSC; permit-data aggregators, accessed May 2026.) | Lower land costs and fees plus faster review can improve the budget and rental return — confirm current fee-waiver status, which has expiration dates. |

City-specific property check

Check your city's ADU friction → Get your free ADU report

Enter your address to see the likely site and utility flags for your specific parcel before you size a loan.

Check my property for free →Can Washington ADU rental income help you qualify for a loan?

Answer capsule: Sometimes — but never assume future rent will carry the project. Under the Fannie Mae Desktop Underwriter 12.1 update (effective the weekend of March 21, 2026), rental income from an existing ADU can count toward qualifying income on a one-unit principal residence for a purchase or limited cash-out refinance, capped at 30% of the borrower's total qualifying income, from one ADU only. Freddie Mac and FHA allow ADU rental income in their own scenarios with their own guardrails: rent is typically discounted to 75% of market or lease rent and capped at 30% of qualifying income.

This is one of the most important — and most misunderstood — financing facts in 2026, and it's genuinely new. Here's how it actually works, by program.

The 2026 rent-counting matrix

| Program | When ADU rent may help | The key limits |

|---|---|---|

| Fannie Mae | Existing ADU on a one-unit principal residence; purchase or limited cash-out refinance only | One ADU only (even if the property has more); ADU rent capped at 30% of total qualifying income; documented via lease + Form 1007 or tax returns; DU 12.1 applies the cap automatically as of ~March 21, 2026. (Fannie Mae Selling Guide SEL-2025-08 / DU 12.1, accessed May 2026.) |

| Freddie Mac | ADU rent may help on a subject one-unit primary residence under its ADU requirements, including purchase and no-cash-out refinance scenarios | Lease-supported rent limited to 75%; qualifying ADU rent capped at 30% of total qualifying income; appraisal and comparable-rent (Form 1000) requirements apply. (Freddie Mac ADU fact sheet, accessed May 2026.) |

| FHA | One-unit dwelling with an existing ADU; new ADU via 203(k) rehab | 75% of the lesser of appraiser market rent or lease for an existing ADU (50% of estimated rent for a proposed ADU under 203k); capped at 30% of total monthly effective income; not eligible on cash-out refinances; Form 1007/1000 and two months PITIA reserves required. (HUD Mortgagee Letter 2023-17, accessed May 2026.) |

These rules are summarized for education only. Individual lenders apply their own overlays and may be stricter. This is not a loan approval, a rate quote, or a guarantee that ADU rent will qualify in your case.

The honest version: existing ADU vs. the one you haven't built yet

Here's the catch homeowners miss. These programs count rent from an ADU that already exists and can be documented — a lease, a comparable-rent schedule, an appraisal. Future rent from a unit you're about to build is far harder to use to qualify, which is exactly why the City of Kirkland warns that many banks will not count potential rental income when sizing your loan. If your debt-to-income math only works with the future rent, you may need a renovation or construction-to-permanent product that underwrites the as-completed value, or you may need to qualify on your income alone and treat the rent as upside.

A worked Washington example (illustrative)

Say you're buying or refinancing a one-unit Seattle home that already has a legal, rented ADU. A Seattle one-bedroom rents for roughly $2,100/month in mid-2026 (Apartments.com Seattle rent market trends, accessed May 2026). A lender applying the 75% haircut would count about $1,575/month — but only up to 30% of your total qualifying income. If your total qualifying income is $6,000/month, the 30% cap is $1,800, so the full $1,575 fits. If your qualifying income were $5,000/month, the cap drops to $1,500 and the usable rent is trimmed to that ceiling.

In Tacoma (one-bedroom around $1,656/month, RentCafe, accessed May 2026) or Spokane (around $1,160–$1,280/month, current rental-market sources, accessed May 2026), the dollar amounts shrink accordingly.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

The Dwelling Index — Washington ADU financing path decision guide

If you're building to rent: the management side

If your plan is income, remember the loan is only half the equation — you'll be a landlord under Washington's Residential Landlord-Tenant Act, and you'll report net rental income on your taxes. Property-management software like Buildium can handle leases, screening, rent collection, and bookkeeping once the unit is occupied.

Disclosure: Buildium is an affiliate partner; see disclosure above.

For the full federal rule comparison and which forms you'll need, see our ADU Financing Options guide.

Washington's ADU-relevant money levers: the 3-year exemption, sales tax, and fee cuts

Answer capsule: Washington offers a handful of financial levers that change the real cost of an ADU build. One easy-to-miss lever: under a Department of Revenue program, owners can apply for a three-year property-tax exemption on the value of qualifying improvements — including an ADU — to a single-family dwelling, when the remodel does not exceed 30% of the structure's pre-remodel assessed value, and the application is filed before the work is complete. HB 1337 also caps ADU impact fees at 50% of the principal unit's. Working against you: Washington charges sales tax on construction (10.55% in Seattle as of January 2026), which most quotes omit.

| Lever | What it is | What it means for your budget |

|---|---|---|

| 3-year improvement exemption | A property-tax exemption on the assessed value of qualifying improvements to a single-family dwelling, including an ADU, administered through the WA Dept. of Revenue. Two conditions: the remodel must not exceed 30% of the structure's pre-remodel assessed value, and the application must be filed before the remodel is complete. (WA Dept. of Commerce; WA Dept. of Revenue, accessed May 2026.) | Can soften the short-term property-tax hit of adding an ADU — but only if you apply before completion. Miss the timing and you lose it. |

| 50% impact-fee cap | HB 1337 caps ADU impact fees at 50% of those charged on the principal unit. (WA Dept. of Commerce, accessed May 2026.) | Lower upfront fees in jurisdictions that charge them; fold the reduced figure into your loan budget. |

| Owner-occupancy removed | Most jurisdictions can no longer require you to live on-site. (RCW 36.70A.681, accessed May 2026.) | Expands financing and rental flexibility; you can rent both units or hold the property as an investment. |

| Construction sales tax (cost, not saving) | Washington taxes the total contract price on custom residential construction; the combined Seattle rate is 10.55% as of January 1, 2026. (WA Dept. of Revenue, accessed May 2026.) | Adds materially to the all-in number; budget it into the loan amount from the start. |

For very-low-income and senior homeowners, the state also offers property-tax assistance and deferral programs, and some jurisdictions offer local low-income ADU property-tax exemptions, depending on eligibility. (WA Dept. of Revenue; MRSC, accessed May 2026.)

Are there ADU grants in Washington?

Answer capsule: As of May 2026, we did not verify a broad statewide grant for individual Washington homeowners to build a new ADU. The verified public programs are narrower: USDA's Section 504 program offers repair and improvement loans for very-low-income homeowners and grants for elderly very-low-income homeowners to remove health-and-safety hazards — not general new-ADU construction — and Washington Commerce's ADU-adjacent infrastructure funding is applicant-limited (cities, counties, and public utility districts), not a direct homeowner ADU grant.

Don't build your financing plan around a grant that may not exist for your situation. If a Washington ADU grant is paused, income-restricted, organization-only, or limited to repair rather than new construction, treat it as a possible bonus, not a foundation. The good news is you don't need to wait — homeowners across the state are building ADUs right now by matching the project to a real financing lane.

Before you believe any "ADU grant" claim, check:

USDA Section 504 in Washington is a real and open program — but it's repair and hazard-removal help for very-low-income homeowners, not building a backyard rental. (USDA Rural Development, accessed May 2026.) And for context on why grants vanish: California's well-known CalHFA ADU grant (up to $40,000 toward predevelopment costs) was fully allocated and stopped accepting new reservations in late 2023 — a cautionary tale about planning around grant money. (CalHFA, accessed May 2026.)

Don't wait for a grant

See which financing lane is realistic without waiting for a grant →

Explore the mortgage-backed paths Washington homeowners actually use, through Mortgage Research Center. Educational only; no approval or rate guaranteed.

Explore mortgage-backed ADU financing options →Do home-equity investments (HEIs) or no-monthly-payment options work in Washington?

Answer capsule: Some no-monthly-payment home-equity products may be available to Washington homeowners, but they are not the default ADU financing path and carry distinct risks. A home-equity investment (HEI), also called a home-equity sharing agreement, gives you cash today for a share of your home's future value, repaid as a lump sum later — typically at sale or end of term. Provider availability in Washington is uneven, and the state's Department of Financial Institutions has had open rulemaking on these agreements, so verify both availability and current rules before pursuing one.

The Consumer Financial Protection Bureau describes home-equity contracts as relatively new and complex, with repayment due as a future lump sum tied partly to your home's value — an amount that can be hard to predict. (CFPB issue spotlight, accessed May 2026.) That's not a reason to dismiss them, but it is a reason to go in with eyes open and ideally a second opinion from an attorney or financial professional.

Availability snapshot (confirm on each provider's current state page before pursuing):

- • Point publicly lists Washington among its active regions.

- • Hometap's current published state list does not include Washington.

- • Unlock's current published state list also does not show Washington.

- • Washington's DFI has active home-equity-sharing-agreement rulemaking.

(Point, Hometap provider pages; WA DFI; accessed May 2026.) We do not route primary financing CTAs to HEI providers.

An HEI might be worth researching if:

- ✓ You have strong equity

- ✓ Genuinely can't support another monthly payment

- ✓ Understand the future repayment formula

- ✓ Have a realistic exit plan

- ✓ Get legal/financial review first

Avoid or delay it if:

- ✕ You have no clear payoff plan

- ✕ You're depending on optimistic future rent

- ✕ You plan to sell soon

- ✕ You can't follow the repayment math

- ✕ You're using it to paper over an underbudgeted project

What documents should you gather before talking to a lender?

Answer capsule: Walking into a lender conversation prepared changes the outcome — the goal isn't to get approved fastest, it's to avoid being routed into the wrong product. Bring your property documents, project documents, and financial documents. The borrower who arrives with a complete picture controls the conversation.

Property documents

- □Current mortgage statement (balance, rate, term)

- □Property tax assessment

- □Survey or site plan, if you have one

- □Zoning/parcel lookup for your address

- □HOA or covenant documents, if any

Washington-specific add-ons

- □Public sewer vs. septic confirmation — and in Seattle, the side-sewer/capacity-charge picture

- □Critical-area / environmentally critical area lookup

- □Pre-approved standard-plan eligibility for your city

- □Stormwater/drainage review status

- □Your city's permit-intake requirements

Project & financial documents

- □ADU type (detached, attached, garage/basement conversion)

- □Concept plan or floor plan + city pre-approved plan number if applicable

- □Contractor estimate (ideally two to three) with permit and utility assumptions

- □Pay stubs, W-2s or 1099s, recent tax returns

- □Asset/bank statements and current list of debts

Free download

Download the free ADU Starter Kit →

It includes this exact document checklist, the questions to ask a lender, and a city-verification worksheet — everything to walk in prepared.

Get the free ADU Starter Kit →What mistakes make Washington ADU financing fall apart?

Answer capsule: Most failed Washington ADU financing plans break before the loan application. The five recurring mistakes are: choosing a loan before confirming the lot is buildable, underbudgeting for sewer and utilities, assuming future rent will count toward qualifying, applying Seattle cost assumptions statewide, and waiting on a grant instead of validating a real financing lane. Each is avoidable with verification up front.

Choosing a loan before checking the lot

RCW 36.70A.680 lets jurisdictions decline ADUs on critical-area and sewer-constrained lots, and RCW 36.70A.681 doesn't apply to critical areas or their buffers; Seattle and Tacoma both require site-specific review. Confirm buildability first. (RCW 36.70A.680–.681; city sources, accessed May 2026.)

Ignoring sewer and utilities

Seattle's sewer treatment capacity charges and City Light service changes are common, real, and routinely left out of early budgets. (City of Seattle SDCI, accessed May 2026.)

Assuming rent will qualify

Many banks won't count future rent, and even existing-ADU rent is discounted to 75% and capped at 30% of income. (City of Kirkland; Fannie/Freddie/FHA, accessed May 2026.)

Using the wrong cost band

A Seattle detached DADU ($300K–$650K+) and a Spokane garage conversion ($100K–$150K) are different financial planets, and Seattle's 10.55% sales tax compounds the gap. Match the band to your project and city. (Builder-published; WA Dept. of Revenue, accessed May 2026.)

Waiting for a grant

No broad statewide homeowner ADU-construction grant is verified; build the plan on a real lane and treat any incentive as upside.

The encouraging flip side: every one of these is a verification problem, not a money problem. Spend the time (or use the free checks below) and the financing falls into place.

Frequently asked questions

What is the best way to finance an ADU in Washington?+−

For most Washington homeowners with enough usable equity and a low first mortgage worth keeping, a HELOC or home-equity loan is the first path to test. If the project costs more than your current equity supports, a renovation loan or construction-to-permanent loan that lends against the finished value usually fits better. The 'best' path is the one that matches your equity, your mortgage rate, your project size, and whether you need rent to qualify.

Can I use a HELOC to build an ADU in Washington?+−

Yes, if you have enough usable equity and can support the payment. A HELOC keeps your existing first mortgage intact, which matters if you locked a low pandemic-era rate. The limits: HELOC rates are usually variable, and you can typically borrow only against your home's current value (commonly up to 80–85% minus your mortgage), which may fall short of a large detached build.

Can Washington ADU rental income help me qualify for a mortgage?+−

Sometimes. As of 2026, Fannie Mae, Freddie Mac, and FHA all allow rental income from an existing ADU to count toward qualifying under specific rules — typically 75% of market or lease rent, capped at 30% of your total qualifying income. Future rent from an ADU you haven't built yet is much harder to use; many banks won't count it.

Are there ADU grants in Washington State?+−

As of May 2026, we did not verify a broad statewide grant for individual homeowners to build a new ADU. USDA Section 504 offers repair and hazard-removal help for very-low-income homeowners, and Washington Commerce's ADU-adjacent funding goes to local governments and utility districts, not directly to homeowners. Verify any grant claim carefully before planning around it.

How much does it cost to build an ADU in Washington?+−

It depends heavily on type and city. Published 2026 signals run from roughly $100,000–$150,000 for a Seattle garage conversion to $300,000–$650,000+ for detached units in the Seattle and Eastside market, with all-in costs of roughly $400–$700 per square foot in that region. Always include permits, utilities, sales tax, and contingency.

Can I build two ADUs in Washington?+−

On most qualifying lots inside urban growth areas that allow single-family homes, yes — HB 1337 (RCW 36.70A.681) requires GMA-planning jurisdictions to allow at least two ADUs per lot, attached, detached, or a combination, subject to site and code limitations.

Do I have to live on the property to have an ADU in Washington?+−

Generally no. HB 1337 bars most jurisdictions from imposing owner-occupancy requirements, which means you can rent both the main home and the ADU. Cities may still restrict short-term rentals.

Can I sell a Washington ADU separately from the main house?+−

Cities cannot prohibit conveying an ADU as a condominium separately from the principal unit solely because it was originally built as an ADU. Doing so still requires the proper legal and permitting steps, so confirm the process locally.

Does a Seattle pre-approved DADU plan guarantee fast approval?+−

No. Seattle's expedited pre-approved path has eligibility limits — including NR zoning, no environmentally critical areas, and less than 750 square feet of total ground disturbance — and your lot still needs site-specific review.

Should I finance an ADU before checking permits and feasibility?+−

No. Confirm your lot and city constraints first. Washington law allows ADUs broadly but doesn't override sewer, critical-area, or building-code limits, and choosing a loan before confirming buildability is the most common reason ADU financing plans fall apart.

How we researched this (methodology)

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. This page exists to help Washington homeowners avoid choosing a financing path before confirming legal feasibility, city-specific budget friction, and loan-program rules.

We researched it in this order of authority: Washington state law and official Department of Commerce guidance first; official city permit pages (Seattle, Tacoma, Kirkland, Bellevue, Spokane) second; federal mortgage and underwriting sources (Fannie Mae, Freddie Mac, HUD/FHA) third; and clearly labeled local lender- and builder-published cost signals last. Forum language informed only how we describe homeowner concerns — never our statements of law, cost, or financing terms. We present financing as lanes, not ranked lenders; we never sort by compensation; and we quote no rates, APRs, or payments as guarantees. Editorial recommendations are independent and unaffected by affiliate relationships.

What we verified — Last verified: May 25, 2026

- •Washington ADU baseline law: RCW 36.70A.680 / .681 / .696; HB 1337; HB 1345 (signed March 27, 2026; effective June 11, 2026); WA Department of Commerce ADU guidance; MRSC analysis.

- •State financial levers: WA Department of Revenue (3-year improvement exemption; senior/low-income deferral); WA Department of Commerce.

- •City permit/process facts: City of Seattle SDCI and Seattle Services Portal (pre-approved plans; sewer capacity charges; SPU side-sewer transition Oct 1, 2025; permit-fee ranges); Tacoma Permits; City of Kirkland ADU Toolkit; City of Bellevue; City of Spokane / MRSC.

- •Sales tax: WA Department of Revenue local tax tables; Seattle combined rate 10.55% effective Jan 1, 2026.

- •Federal rent-counting rules: Fannie Mae Selling Guide SEL-2025-08 / DU 12.1 (effective ~March 21, 2026); Freddie Mac ADU fact sheet; HUD Mortgagee Letter 2023-17.

- •Grants/programs: USDA Rural Development Section 504; Washington Commerce infrastructure funding; CalHFA (cited only as out-of-state context).

- •HEI availability and risk: Point, Hometap provider state pages; WA Department of Financial Institutions HESA rulemaking; CFPB home-equity-contract spotlight.

- •Cost and rent signals (labeled estimates, not guarantees): Olympia Federal Savings; Seattle/Eastside builder publications (Goodwin, Emerald City, Nine8); Apartments.com, RentCafe for rents.

- •Affiliate partner licensing: Mortgage Research Center (NMLS #1907; WA Consumer Loan Company License #CL-1907).

Not sure where to start?

See what's possible at your address

Get your free ADU report in 60 seconds. We flag likely buildability issues, the ADU type your parcel supports, and the financing questions worth bringing to a lender.

Get my free property check →Content is for informational purposes only and does not constitute financial, legal, tax, construction, or lending advice. Verify all information with qualified local professionals and your city or county planning department before making decisions. The Dwelling Index is not a lender, broker, or builder.