HELOC vs Construction Loan for ADU: The 2026 Decision Guide

By The Dwelling Index Editorial Team · · Last verified May 21, 2026

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, builder, CPA, or law firm.

The short answer (read this first)

If your current home equity covers the ADU budget plus a reasonable contingency, start with a HELOC. It is faster, cheaper to set up, leaves your low first-mortgage rate alone, and lets you draw funds as the build progresses. If your current equity does not cover the build, start with a construction loan or a renovation loan — Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, FHA 203(k) Standard, or an after-renovation-value HELOC.

The 60-second test:

(Home value × 0.80) − current mortgage balance = your usable second-lien equity room.

If that number is larger than your ADU budget plus a 10–15% contingency, the HELOC lane is open. If it is smaller, you need a loan that uses the home’s future value.

Quick verdict table

| If this describes you | Test first | Why |

|---|---|---|

| Enough current equity + low first-mortgage rate | HELOC | Keeps your first mortgage; draw as needed |

| Not enough current equity for full build | Construction or renovation loan | Lends against future as-completed value |

| Nervous about paying the contractor too soon | Construction loan | Lender controls scheduled draws and inspections |

| Small garage or basement conversion | HELOC or home equity loan | Simpler if your equity covers the budget |

| Large detached ADU over $300K | Construction or renovation loan | More likely to exceed current-equity room |

| Need ADU rent to qualify | Renovation loan via Fannie Mae or FHA | HELOC underwriting usually doesn't credit rent |

Rates and rules verified May 21, 2026 against the Federal Reserve H.15 release, Curinos national averages via Yahoo Finance, Fannie Mae Selling Guide, Freddie Mac ADU materials, and HUD Mortgagee Letter 2023-17.

Check your lot, likely ADU type, setbacks, and probable size limit before you talk to a single lender. A HELOC against an ADU your zoning won’t allow is the most expensive mistake in this category — and the easiest to avoid.

See What You Can Build → Get Your Free ADU ReportWhat we verified for this guide

- HELOC and home equity loan rates: Curinos national averages reported via Yahoo Finance on May 20, 2026 — HELOC 7.21%, home equity loan 7.36%. Bankrate’s separate survey reports HELOCs near 7.26% in the same period.

- Prime rate: 6.75% per the Federal Reserve H.15 release dated May 15, 2026.

- Construction loan rate context: Per the Consumer Financial Protection Bureau, construction loans generally price higher than long-term mortgage loans and vary by lender and product.

- Fannie Mae ADU rental income rule: Selling Guide Announcement SEL-2025-08 allows ADU rental income on eligible one-unit principal-residence purchase and limited cash-out refinance transactions, capped at 30% of total qualifying income, implemented in Desktop Underwriter Version 12.1 the weekend of March 21, 2026.

- Freddie Mac ADU policy: Freddie Mac’s ADU fact sheet confirms ADU rental income may be used to qualify on an eligible 1-unit primary residence.

- FHA ADU rental income rule: HUD Mortgagee Letter 2023-17 allows 75% of lesser of appraiser fair market rent or lease; 50% projected rent in eligible 203(k) cases; capped at 30% of monthly effective income.

- IRS interest deductibility: Per the IRS FAQ, HELOC and home equity loan interest may be deductible only when funds are used to buy, build, or substantially improve the home securing the loan.

- California contractor down-payment law: Per the California CSLB, a home-improvement down payment cannot exceed $1,000 or 10% of the contract price, whichever is less.

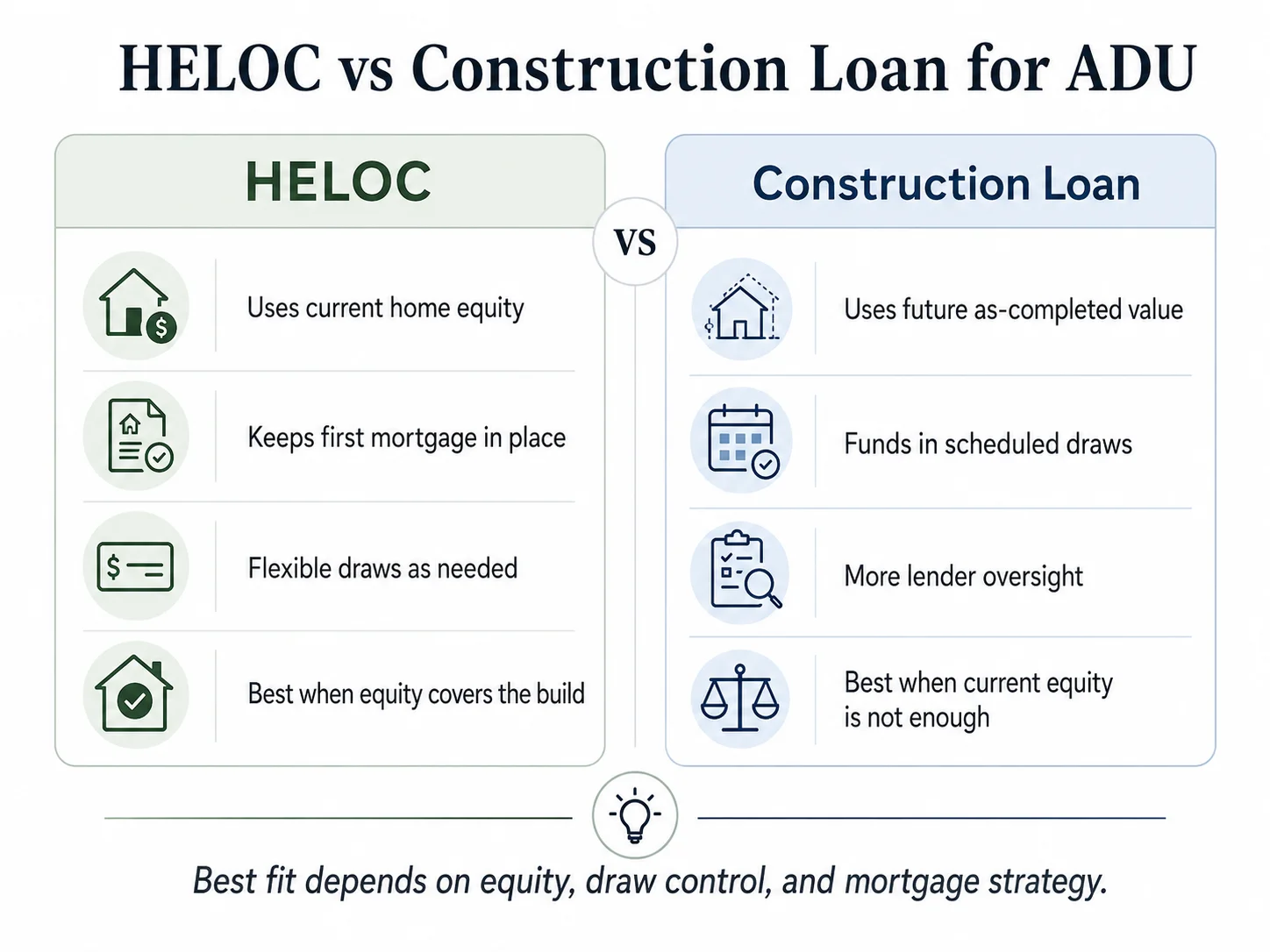

What’s actually different between a HELOC and an ADU construction loan?

Four mechanical differences matter. Get these straight and the rest of the decision follows.

Appraisal basis — current value vs future value

A HELOC is appraised against what your home is worth today. The lender takes today’s value, multiplies it by their combined loan-to-value (CLTV) cap (usually 80–90%), subtracts your current mortgage balance, and that is your line. A construction loan is appraised “subject to completion” — the appraiser looks at the plans, the bid, and comparable homes with similar finished improvements, and produces an as-completed value or after-renovation value (ARV). For ADU projects where the build adds 20–40% to the home’s value, that future-value lens often unlocks $100,000 or more in additional borrowing power.

Funds delivery — open line vs scheduled draws

A HELOC sits open. You draw whatever you need, whenever you need it, up to the limit. There is no inspection between draws and no third party deciding when the money releases. A construction loan delivers money in scheduled draws — usually four to six over the project — tied to specific milestones like foundation, framing, mechanical rough-in, drywall, and final inspection. Each draw requires the lender (or a third-party inspector) to verify completion. That friction is also protection.

What happens to your primary mortgage

A HELOC is a second lien. Your existing mortgage stays exactly where it is — same rate, same balance, same payment. That matters enormously if your first mortgage is at 3% or 4% from a 2020–2022 lock. A construction loan can be a second lien too, but the most common ADU construction products — the one-time-close construction-to-permanent loan, Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, and FHA 203(k) — either replace your first mortgage or wrap it, eliminating that low rate.

Rate type and exposure

Most HELOCs carry a variable rate equal to prime plus a margin. With prime at 6.75% per the Federal Reserve H.15 release of May 15, 2026, a typical HELOC margin of 0.25%–1.75% puts most borrowers in roughly the 7.0%–8.5% range. That rate moves when the Federal Open Market Committee moves. Construction loans are quoted as either variable during the build (then refinanced or converted) or fixed for the permanent term.

The shorthand: HELOC = current value, open line, second lien, variable. Construction loan = future value, scheduled draws, often replaces first mortgage, fixed or hybrid. Everything else flows from those four.

For a deeper product-specific walkthrough, see our companion guides on the HELOC for ADU and the broader ADU loan vs HELOC comparison.

Which ADU loan structure fits my situation in 2026?

This is the single asset we wish existed when we started researching this question two years ago.

| Loan structure | Rate type | May 2026 typical rate | Appraised against | Funds delivery | Touches first mortgage? | Typical close | Best fit |

|---|---|---|---|---|---|---|---|

| HELOC (standard) | Variable, prime + margin | ~7.0–8.5% | Current value | Open line, draw anytime | No (second lien) | 2–4 weeks | Equity-rich, phased build, want flexibility |

| Home equity loan | Fixed | ~7.3–8.5% | Current value | Single lump sum | No (second lien) | 2–4 weeks | Equity-rich, want fixed payment from day one |

| ARV HELOC (after-renovation-value) | Variable | Varies; ask lender | Future as-completed value | Open line, draw anytime | No (second lien) | 4–8 weeks | Equity-thin, want HELOC flexibility on a future-value basis |

| Construction-to-permanent (one-time-close) | Hybrid (variable during build, fixed at conversion) | Varies by lender/product | Future as-completed value | Scheduled draws during build; converts to permanent mortgage at completion | Yes (replaces or wraps) | 45–60 days | Large build, equity-thin, want one closing |

| Two-close construction loan | Variable during build; separate permanent loan later | Varies by lender/product | Future as-completed value | Scheduled draws; refinance into permanent loan at completion | Yes at takeout | 30–45 days | Owners who expect rates to drop before conversion |

| Renovation loan (HomeStyle / CHOICERenovation / FHA 203(k) Standard) | Fixed-rate or ARM executions available | Varies by lender/program | Future as-completed value | Scheduled draws via lender-controlled escrow | Yes (replaces or first-lien for purchase) | 60–90 days | Buy + build, refi + build, lower equity, lower credit (FHA route) |

Rate ranges reflect Curinos national averages via Yahoo Finance on May 20, 2026 (HELOC 7.21%, home equity loan 7.36%); Federal Reserve H.15 prime rate 6.75% on May 15, 2026. Construction and renovation loan pricing varies widely; see the CFPB explainer. We re-verify the matrix monthly.

Our editorial read: For many ADU homeowners who hold a sub-5% first mortgage and meaningful current equity, the standard HELOC is the right tool. For equity-thin owners or large builds, a renovation loan (HomeStyle or CHOICERenovation for conventional borrowers, 203(k) Standard for FHA-eligible borrowers) or a one-time-close construction-to-perm is the strongest fit. The ARV HELOC is the underused middle-ground option that deserves more attention than most builder blogs give it.

Want a lender who handles more than one lane?

Most banks specialize in one product. The Mortgage Research Center matched-advisor service connects you with licensed lenders in your state for mortgage, refinance, and construction-loan paths.

Compare your matched lender options →Affiliate disclosure applies. Mortgage Research Center, LLC (NMLS #1907) operates a lead-routing and marketing service; The Dwelling Index earns a commission if you ultimately take a loan from a matched lender. Never any cost to you.

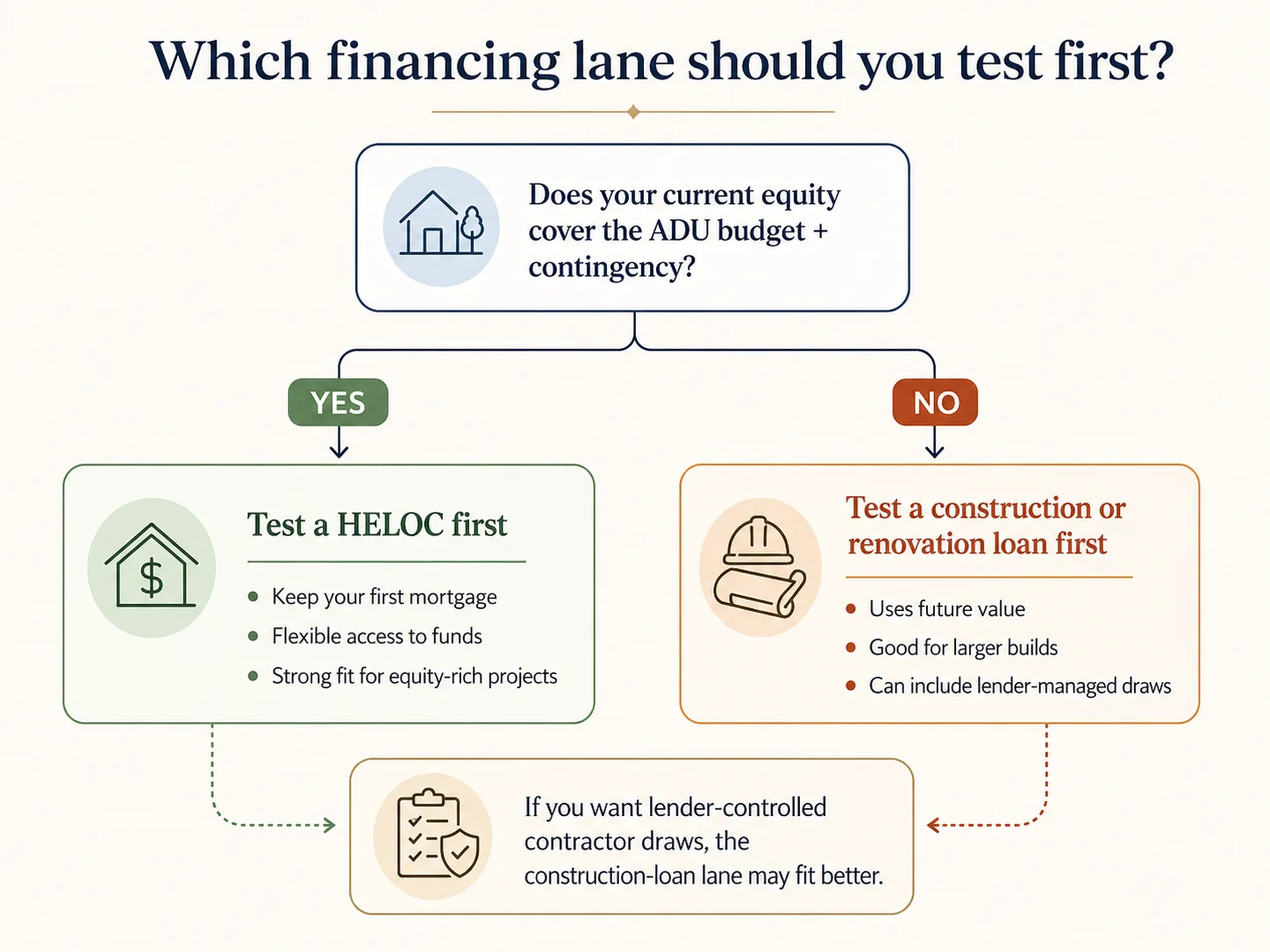

How do I pick my lane in 60 seconds?

(home value × 0.80) − current mortgage balance. If that number is larger than your ADU budget plus 10–15% contingency, the HELOC lane is open. If it is smaller, you need a future-value loan. If your first mortgage is below 5%, prefer second-lien structures that preserve it.The framework runs in four steps. Each step rules in or rules out at least one option.

Step 1 — Calculate your usable current equity

Take your home’s current value (use a recent appraisal, refinance estimate, or a conservative Zillow/Redfin reading minus 5–7%). Multiply by 0.80. Subtract your current mortgage balance. That is the rough upper bound on what a typical second-lien HELOC or home equity loan will offer.

Worked example: Home value $750,000 · Mortgage $400,000 → Usable equity = ($750,000 × 0.80) − $400,000 = $200,000. ADU build $250,000 → short. ADU build $180,000 → room available.

Step 2 — Compare to your project budget plus contingency

We recommend financing with a 10–15% contingency built in. If your builder bid is $250,000, finance $280,000.

- Equity ≥ project + contingency → HELOC or home equity loan lane

- Equity 60–95% of project + contingency → ARV HELOC, HomeStyle, or CHOICERenovation lane

- Equity < 60% of project + contingency → one-time-close construction-to-permanent or FHA 203(k) Standard lane

Step 3 — Check your first-mortgage rate

Below 5%, protect it. A sub-5% first mortgage saves you tens of thousands in avoided interest. Any product that replaces or refinances that mortgage at a 6.5–7% current rate eats years of arithmetic. That rules out, for most owners, the full cash-out refinance, the one-time-close construction-to-perm that wraps the first mortgage, and HomeStyle/CHOICERenovation/203(k) when used as refinance vehicles. It leaves the standard HELOC, the home equity loan, the ARV HELOC, and second-lien construction structures.

Step 4 — Match to your contractor and timeline

Does your contractor want progress payments aligned to milestones, or do they prefer flexibility? Are you the kind of homeowner who will police a draw schedule? If the contractor wants milestone-based progress payments and you want third-party oversight, the construction loan structure is doing you a favor. If your contractor is a known quantity and you want to write checks on your own schedule, a HELOC is doing you a favor by getting out of the way.

The Dwelling Index ADU Financing Fit Check asks for your home value, mortgage balance, project budget, first-mortgage rate band, contractor status, and timeline — and returns your recommended first lane, borrowing-room gap, the two questions to ask a lender first, and the documents to gather this week. Free, no email required.

Run the Fit Check → Find My ADU Financing LaneHow a construction loan really works for an ADU (the mechanics most pages skip)

The future-value (as-completed) appraisal

Instead of appraising your home today, the appraiser looks at your plans, your contractor’s bid, and comparable sales of similar homes with finished improvements, and produces an “as-completed value.” For HomeStyle Renovation purchase transactions, Fannie Mae caps total renovation financing at the lesser of “purchase price plus renovation costs” or the as-completed appraised value. For ADU projects where the build adds 20–40% to the home’s value, that future-value lens often unlocks $100,000 or more in borrowing power.

Draw schedules — how money actually arrives

A typical ADU construction loan releases funds in four to six draws:

| Draw | Trigger milestone | Typical % of total |

|---|---|---|

| Draw 1 | Site preparation, demolition, foundation pour | 15–20% |

| Draw 2 | Framing, sheathing, roof dry-in | 20–25% |

| Draw 3 | Mechanical, electrical, plumbing rough-in | 15–20% |

| Draw 4 | Insulation, drywall, exterior finish | 15–20% |

| Draw 5 | Interior finish, cabinets, fixtures | 15–20% |

| Draw 6 | Final inspection, certificate of occupancy | 5–10% |

Schedules are illustrative. Your lender will issue a specific draw schedule signed by you, your contractor, and the lender at closing.

One-time-close vs two-close

A two-close construction loan funds the build, pays off at completion, and forces you to apply for a separate permanent mortgage — two closings, two sets of closing costs, rate risk between start and finish. A one-time-close construction-to-permanent loan does both at a single closing — it disburses as a construction loan during the build, then automatically converts to a 15-, 20-, or 30-year permanent mortgage. One closing, one set of fees, one rate. For most ADU owners, the one-time-close is the right structure unless you have a specific reason to believe rates will drop materially before your build ends.

Interest during the build — the interest reserve trick

During construction, most lenders charge interest only on the funds drawn to date, not on the full loan amount. A $250,000 construction loan that has released $75,000 by month three charges interest only on that $75,000. Some lenders capitalize the construction-phase interest into the loan itself — meaning the interest gets added to the principal balance and you do not write monthly checks during the build. Ask whether your lender offers this.

What lenders require from your builder

For FHA Standard 203(k), the lender selects a HUD-approved consultant who oversees the rehabilitation work plan and draws. For HomeStyle and CHOICERenovation, the contractor must pass the lender’s review — typically a state-issued license in good standing, proof of insurance, references, and a fixed-price contract with a detailed scope and draw schedule. In California, an active license with the Contractors State License Board.

What does each loan really cost on a $150K, $250K, and $400K ADU?

The $150,000 ADU

A small garage conversion or basement ADU — the project size where HELOCs dominate.

| Structure | Term assumed | Build-phase monthly | Post-build monthly | Est. total interest | Notes |

|---|---|---|---|---|---|

| HELOC at 7.21% variable | 10-yr IO draw + 20-yr repay | ~$901 IO at full draw | ~$1,182 P&I | ~$242,000 over 30 yr | Rate moves with prime |

| Home equity loan at 7.36% fixed | 20-yr fully amortizing | ~$1,196 from day 1 | Same | ~$137,000 over 20 yr | No surprises |

| Construction-to-perm 7.0% blended | 12 mo IO build + 30-yr fixed perm | ~$875 IO during build | ~$998 P&I after | ~$220,000 over total | Replaces or wraps first mortgage |

| HomeStyle Renovation 7.25% fixed | 30-yr fixed | Folded into mortgage | ~$1,023 P&I on incremental balance | ~$218,000 over 30 yr | Lower monthly, longer tail |

The $250,000 ADU (the typical case)

| Structure | Term assumed | Build-phase monthly | Post-build monthly | Est. total interest | Notes |

|---|---|---|---|---|---|

| HELOC at 7.21% variable | 10-yr IO draw + 20-yr repay | ~$1,502 IO at full draw | ~$1,970 P&I | ~$403,000 over 30 yr | Variable rate exposure |

| Home equity loan at 7.36% fixed | 20-yr fully amortizing | ~$1,993 from day 1 | Same | ~$228,000 over 20 yr | Stable payment |

| Construction-to-perm 7.0% blended | 12 mo IO build + 30-yr fixed perm | ~$1,458 IO during build | ~$1,663 P&I after | ~$366,000 over total | Includes 12 months of build-phase interest |

| HomeStyle Renovation 7.25% fixed | 30-yr fixed | Folded into mortgage | ~$1,705 P&I on incremental balance | ~$364,000 over 30 yr | Lower monthly, longer tail |

The $400,000 ADU (large detached or coastal-California build)

At this size, current-value equity loans are out of reach for most owners. Future-value products dominate.

| Structure | Term assumed | Build-phase monthly | Post-build monthly | Est. total interest | Notes |

|---|---|---|---|---|---|

| HELOC at 7.21% (if equity supports) | 10-yr IO draw + 20-yr repay | ~$2,403 IO at full draw | ~$3,152 P&I | ~$645,000 over 30 yr | Requires substantial existing equity |

| Construction-to-perm 7.0% blended | 12 mo IO build + 30-yr fixed perm | ~$2,333 IO during build | ~$2,661 P&I after | ~$586,000 over total | Most common path at this size |

| HomeStyle Renovation 7.25% fixed | 30-yr fixed | Folded into mortgage | ~$2,729 P&I on incremental balance | ~$582,000 over 30 yr | Uses as-completed value |

| FHA 203(k) Standard at 7.5% fixed | 30-yr fixed (with MIP) | Folded into mortgage | ~$2,797 P&I + MIP | ~$607,000 over 30 yr (excl. MIP) | Lower credit/equity hurdle; MIP duration depends on LTV |

What these numbers reveal: Cheaper-per-month does not mean cheaper-total. The HomeStyle Renovation’s monthly payment is meaningfully lower than the home equity loan’s because the term is longer — a 30-year payment is smaller than a 20-year payment by definition, but the interest accrues for an extra decade. Pick the structure that matches your equity and your first mortgage; pay attention to the term length when you do.

Get this math on your actual scenario

Plug your home value, mortgage balance, and project size into the Mortgage Research Center matched-advisor service and they will route you to lenders licensed in your state who quote mortgage, refinance, and construction-loan paths.

Compare your matched lender options →Affiliate disclosure applies. Mortgage Research Center, LLC (NMLS #1907) operates a lead-routing service.

When does a HELOC beat a construction loan for an ADU?

You have enough current equity

The simplest check: (home value × 0.80) − current mortgage balance ≥ ADU budget × 1.10. If that holds, the HELOC lane is open. Many California owners — especially anyone who bought before 2020 or has paid down meaningful principal — sit comfortably in this zone.

Your first mortgage rate is worth protecting

Anything under 5%, and the math gets ugly fast on products that refinance the first. A 30-year mortgage at 3.5% with $400,000 remaining balance generates roughly $200,000 less in lifetime interest than the same balance at 7.0%. The HELOC preserves that asset; the cash-out refinance and most full construction-to-perm structures destroy it.

You can tolerate variable-rate exposure

A HELOC tied to prime moves when the Federal Reserve moves. The prime rate was 6.75% as of the H.15 release dated May 15, 2026, and the FOMC’s path from here will move it. If that exposure keeps you up at night, the home equity loan (fixed) or a fixed renovation loan is a better fit.

Your ADU build is small or phased

A $120,000 garage conversion in three phases is HELOC-shaped. A $400,000 ground-up detached ADU on a complex coastal lot is not. The HELOC’s strength is flexibility — drawing for an invoice, paying it down, redrawing later.

You have a vetted contractor and can manage payments yourself

No lender inspector is going to second-guess your draw schedule on a HELOC. That is freedom if you and your contractor have a tight working relationship and a clear written milestone schedule. The single biggest avoidable failure mode in HELOC-funded ADU projects is paying too much too early to a contractor who then stops showing up. A construction loan’s inspection-gated draws prevent that; a HELOC does not.

The Urban Institute analysis of ADU financing found that home equity loans and HELOCs were among the most common products used by mortgage-financed ADU builders — particularly among owners with substantial existing equity.

When does a construction loan beat a HELOC for an ADU?

Your current equity is not enough

Recent buyers, owners in markets where prices have flattened, and owners with sizable existing mortgages often run the current-value formula and come up short. A construction or renovation loan opens the future-value lane. A property worth $750,000 today that will appraise at $980,000 after a $250,000 ADU is worth $230,000 more to the future-value lender — and that difference is the borrowing power you need.

You want a fixed rate locked through the project

HELOCs are variable. Construction-to-perm and renovation loans typically lock at fixed terms. If the rate environment is uncertain and you want certainty in your monthly payment, the fixed-rate construction lane delivers it.

You are buying a home and adding an ADU simultaneously

This is the killer use case for renovation loans. A HomeStyle Renovation or 203(k) Standard mortgage can finance the home purchase and the ADU construction in a single first-lien loan, using the as-completed value as the appraisal basis. A standalone HELOC cannot do this — you cannot tap equity you do not yet own.

You want lender-controlled draws

The inspector who verifies foundation pour before draw #1 releases is also the inspector who catches a contractor who poured a deficient footing. Owners building their first ADU, owners working with a contractor they have not used before, and owners who do not want to spend their evenings reviewing invoices benefit from the structural oversight a construction loan enforces.

You need to count ADU rental income to qualify

This is new in 2026 and matters enormously. Standard HELOCs generally do not credit future ADU rent. Fannie Mae, Freddie Mac, and FHA renovation and construction paths can. We cover this in detail in the rental income section below.

The honest tradeoff. Construction and renovation loans are slower (45–90 days to close vs 2–4 weeks), require more paperwork, and put your contractor through a separate approval. The right question is not “which is easier?” but “which friction can I live with?”

What if I have a low first-mortgage rate I don’t want to lose?

Why your low first mortgage is an asset, not just a payment. A 30-year fixed mortgage at 3.5% with $400,000 remaining principal accrues roughly $246,000 in lifetime interest. The same balance at 7.0% accrues $558,000. The $312,000 difference is real money you owe to a bank if you replace that mortgage — and it is gone if the new product is a refinance.

Compact reference — what each loan does to your first mortgage

| Product | What it does to your first mortgage |

|---|---|

| Standard HELOC | Sits behind it as a second lien |

| Home equity loan | Sits behind it as a second lien |

| ARV HELOC (after-renovation-value) | Sits behind it as a second lien |

| Two-close construction (then refinance) | Construction sits as second lien; refinance at takeout replaces first |

| One-time-close construction-to-perm | Varies — can replace, wrap, or sit behind; ask specifically |

| HomeStyle / CHOICERenovation (refinance) | Replaces your first mortgage at current rates |

| HomeStyle / CHOICERenovation (purchase) | Becomes the new first mortgage on the purchased home |

| FHA 203(k) Standard (refinance) | Replaces your first mortgage at current rates |

| Full cash-out refinance | Replaces your first mortgage at current rates |

The question to ask your lender, in writing: “Will this loan replace, refinance, or sit behind my existing first mortgage? Provide me the lien position and the impact on my current first-mortgage rate.” Get it in writing before you pay for an appraisal.

Run the numbers before you refinance

Before any product that touches your first mortgage, compare second-lien options head-to-head. The Mortgage Research Center matched-advisor service routes you to lenders who quote both second-lien options and construction-to-perm structures.

Compare lender paths before replacing your first mortgage →Affiliate disclosure applies.

Can ADU rental income help me qualify for either loan?

This is the single biggest underwriting change in ADU lending in the last decade, and most pages have not caught up to it.

Worked example

Borrower has $6,000/month in qualifying employment income. The appraiser estimates the ADU’s fair market rent at $1,500/month. Under either Fannie or FHA’s 75% factor: $1,500 × 0.75 = $1,125 of countable rental income. Adding $1,125 to the $6,000 base yields $7,125 total — the 30% cap check clears. The borrower’s qualifying income becomes $7,125/month instead of $6,000/month, which can be the difference between approval and denial on a stretch budget.

Can ADU rent help qualify?

| Loan path | Can ADU rent help qualify? | Key limits |

|---|---|---|

| Standard HELOC | Usually no | Underwritten on current income and DTI |

| Home equity loan | Usually no | Same |

| Fannie Mae conventional (purchase or limited cash-out refi) | Yes, with existing ADU | 75% of market rent, capped at 30% of total qualifying income, one-unit principal residence only |

| Freddie Mac conventional / CHOICERenovation-related scenarios | Yes, on eligible 1-unit primary residence | Subject to Freddie Mac Single-Family Seller/Servicer Guide requirements |

| FHA loan (purchase, with existing ADU) | Yes | 75% of lesser of appraised rent or lease, capped at 30% of total monthly effective income |

| FHA 203(k) Standard (planned ADU in eligible cases) | Yes | 50% of projected market rent in eligible no-history scenarios, capped at 30% |

| Cash-out refinance (any flavor) | No (Fannie and FHA both exclude) | Verify with lender |

These are illustrative examples, not guarantees of approval. Verify ADU rental income eligibility with your specific lender in writing before relying on it for qualification.

How much could I actually borrow with each option?

(home value × 0.80) − current mortgage balance. For a future-value construction loan: (future as-completed value × 0.75–0.80) − current mortgage balance. The 80% CLTV is a planning assumption — some lenders go higher, many go lower. Contingency belongs in the borrowing number, not just the construction budget.The current-value formula

(Home value × 0.80) − current mortgage = current-value second-lien room

The future-value formula

(After-completed value × 0.75 or 0.80) − current mortgage = future-value loan room

Four worked scenarios

| Scenario | Home value | Mortgage balance | Project + 12% contingency | Current-value room (80%) | Expected as-completed value | Future-value room (80%) | Likely first lane |

|---|---|---|---|---|---|---|---|

| High-equity owner, 3.5% first mortgage | $900,000 | $350,000 | $246,000 | $370,000 | $1,100,000 | $530,000 | HELOC (preserves first mortgage) |

| Recent buyer, equity gap | $700,000 | $595,000 | $280,000 | $0 | $950,000 | $165,000 | Future-value loan; may still need cash |

| Garage conversion | $600,000 | $300,000 | $134,000 | $180,000 | $720,000 | $276,000 | HELOC |

| Large detached ADU | $800,000 | $500,000 | $392,000 | $140,000 | $1,100,000 | $380,000 | Construction or renovation loan |

Illustrative examples only. Actual results depend on appraisal, credit, DTI, lender overlays, and regulatory approvals.

For your specific numbers, see our ADU equity calculator or our full comparison in ADU Financing Calculator: 7 Loan Paths.

What are the honest tradeoffs?

What is hard about a HELOC for an ADU

- Variable rate exposure. A 1% rate move on a $250,000 drawn balance is roughly $2,500 in additional annual interest.

- Repayment-period payment shock. HELOCs convert from interest-only to principal-and-interest after 5–10 years. The monthly payment usually increases meaningfully at that conversion.

- Lenders can freeze or reduce limits. During 2008–2009, banks froze and reduced HELOC limits widely, sometimes mid-build.

- Foreclosure risk is real. Per the FTC, failing to repay can lead to losing the home.

- Draw discipline is yours. No one will stop you from paying a contractor who has not finished the work.

What is hard about a construction loan for an ADU

- Slower close. 45–90 days versus 2–4 weeks for a HELOC.

- Contractor approval can rule out your choice. If your contractor cannot meet the lender’s requirements, you change contractor or lender.

- Inspection-gated draws can delay payment. If framing finishes on a Friday and the inspector is booked for two weeks, your draw releases two weeks late.

- Most full-replacement structures cost you your low first mortgage.

- Cost overruns above contingency are your problem. The loan amount is fixed at closing.

The damaging admission we will not dress up

At a $250,000 full-draw balance, the interest-only carrying cost is roughly $1,502 per month at 7.21% versus about $729 per month at 3.5% — approximately 106% higher. That is the actual headwind in this market, not which loan you pick. The HELOC vs construction loan decision is the right decision to optimize; it is not the decision that determines whether your project pencils. If your build only pencils at 3.5% rates, no loan structure will save it. If your build pencils at current rates with the right structure, the wrong loan still costs you tens of thousands of dollars.

How should I handle contractor payments and draw schedules?

HELOC draw discipline — what good looks like

- A written payment schedule tied to milestones, not weeks

- A legal initial deposit — in California, capped at the lesser of $1,000 or 10% of the contract

- Progress payments that never exceed the value of work completed and materials delivered

- A holdback (5–10% of total contract value) released only at final inspection and certificate of occupancy

- Lien waivers collected from contractor and any subcontractors before each progress payment

Red flags from your contractor — fire-the-contractor list

- “I need 30% up front before I order materials.” (In California, this is flatly illegal under CSLB rules.)

- “Pay me every two weeks based on time, not milestones.”

- “I don’t do lien waivers.” (Subcontractors and suppliers can place mechanic’s liens on your property.)

- “Inspections slow things down — let’s skip the inspector.” (Skipping permits or inspections voids most insurance and creates resale problems forever.)

- “My license is being renewed.” (Verify current license status with CSLB before signing.)

Get the draw schedule template we use

The Free ADU Starter Kit includes our HELOC-vs-construction loan comparison worksheet, a milestone-payment schedule template, a contractor-vetting checklist, and the document list lenders ask for. Email required to download.

Download the Free ADU Starter Kit →What documents should I gather before talking to a lender?

| Document | HELOC | Home equity loan | Construction-to-perm | HomeStyle / CHOICERenovation | FHA 203(k) |

|---|---|---|---|---|---|

| Income docs (paystubs, W-2s, returns) | ✅ | ✅ | ✅ | ✅ | ✅ |

| Two months bank statements | ✅ | ✅ | ✅ | ✅ | ✅ |

| Current mortgage statement | ✅ | ✅ | ✅ | ✅ | ✅ |

| Homeowners insurance dec page | ✅ | ✅ | ✅ | ✅ | ✅ |

| Property tax statement | ✅ | ✅ | ✅ | ✅ | ✅ |

| Contractor bid + fixed-price contract | — | — | ✅ | ✅ | ✅ |

| Contractor license + insurance | — | — | ✅ | ✅ | ✅ |

| ADU plans (permit-ready preferred) | — | — | ✅ | ✅ | ✅ |

| Signed draw schedule | — | — | ✅ | ✅ | ✅ |

| HUD-approved 203(k) consultant work writeup | — | — | — | — | ✅ |

| Form 1004/70 + Form 1007/1000 (rental income) | — | — | If using ADU rent | ✅ | ✅ |

| Existing ADU lease (if applicable) | — | — | If using ADU rent | If using ADU rent | If using ADU rent |

Questions to ask in writing before you spend money on plans

- “What is the maximum I qualify for under your HELOC product, and what is the rate at full draw today?”

- “What is the maximum I qualify for under your construction or renovation product, and what is the locked rate?”

- “Will this loan replace, refinance, or sit behind my existing first mortgage?”

- “Will you order an as-completed appraisal? At what point in the process?”

Is the interest on a HELOC or construction loan tax-deductible for an ADU?

The deductibility rule is the same for HELOCs, home equity loans, construction loans, and renovation loans — it is about what the money buys, not which loan delivers it.

Why ADU invoices and permit records matter. The IRS wants documentation that the borrowed money actually went into substantial improvements to the qualifying home. Save every invoice, every receipt, the construction contract, the building permit, and the certificate of occupancy.

What changes if the ADU is rented. If the ADU is rented to a third party, the rental activity creates a separate set of rules — rental income and rental expense reporting on Schedule E, depreciation, allocation of mortgage interest between personal-use and rental-use. This is a CPA conversation.

What to ask your CPA

- “Given the ADU is a substantial improvement to my principal residence, can the interest qualify under the home-acquisition-debt rules for my Schedule A itemized deductions?”

- “If I rent the ADU, how should the interest be allocated between Schedule A and Schedule E?”

- “Do my total mortgage balances exceed the applicable cap, and if so, how is interest allocated above the cap?”

- “Are there state tax differences I should know about?”

What happens after the ADU is finished?

Keep the HELOC and pay it down

If rental income covers the payment with cushion, keep the line open and use rental income to pay down the balance during the interest-only draw period. The freed-up capacity can fund future home improvements or stay as an emergency line.

Refinance a two-close construction loan

A two-close construction loan must be replaced at completion. You apply for a permanent mortgage at whatever rate the market offers when your build ends — that is rate risk. Owners who choose two-close are typically betting rates will be better in 12 months than at the start of the build.

Automatic conversion on one-time-close construction-to-perm

One-time-close products convert without a second closing. The rate is either fully locked at the original close or adjusted within a band based on the rate environment at conversion. Read your loan documents carefully — the conversion mechanism varies by lender.

Renovation loans need no post-build action

HomeStyle Renovation, CHOICERenovation, and FHA 203(k) Standard are already permanent mortgages. The renovation portion was escrowed and released in draws; the permanent terms are unchanged.

Planning the post-build refinance?

Once the ADU is complete and you have either a two-close construction loan to take out or a HELOC you want to convert, the Mortgage Research Center matched-advisor service handles refinance and cash-out paths the same way it handles new loans.

Explore post-build refinance options →Affiliate disclosure applies.

Which edge cases change the answer?

Buying the house and adding the ADU at the same time

A HELOC requires existing equity, which you do not have on a home you have not yet bought. The path here is a renovation loan: HomeStyle Renovation, CHOICERenovation, or FHA 203(k) Standard — each combines the purchase mortgage and the ADU construction funds into a single first-lien loan based on the as-completed value. For first-time homebuyers eyeing properties with ADU potential, the 203(k) Standard with 3.5% down is often the only product that makes the math work.

A contractor who wants a 30%+ deposit

In California, per CSLB, home-improvement down payments cannot exceed the lesser of $1,000 or 10% of the contract price — a contractor demanding 30%+ upfront is either in cash-flow stress (a red flag), inexperienced, or simply hoping you will agree. A HELOC can pay any deposit; a construction loan cannot release that large a first draw before work is verified. If your contractor is unwilling to work within state-law deposit limits, change contractors.

A sub-5% first mortgage and an equity gap larger than any second-lien product solves

Painful scenario. Run the lifetime-interest comparison honestly: the ADU’s rent or value lift either justifies the rate sacrifice or it does not. Consider the ARV HELOC as an intermediate step that may close part of the gap while preserving the first mortgage.

Investor building an ADU for day-one rental

Standard owner-occupant products may not be available if you do not plan to live in the primary residence. DSCR (debt service coverage ratio) construction loans qualify based on the property’s projected rental income rather than personal income — useful for investors. DSCR construction is its own corner of the market; rates are typically higher. See our bridge loan for ADU and hard money loan for ADU guides for the next-step lanes.

Building for aging parents or adult children (no rental)

The rental-income rules are moot — you are not renting it. The decision reduces to equity, first-mortgage rate, and timeline. For most owners building a family-use ADU, that means HELOC if the equity is there and a renovation loan if it is not.

Building for rental income? You will need management eventually.

Once the ADU is built and rented, the day-to-day operations — leases, screening, rent collection, maintenance requests, accounting — are their own job. Buildium offers property-management software for landlords with rent collection, maintenance tracking, accounting, and tenant screening.

Explore Buildium for landlords →Affiliate disclosure applies. We earn a commission if you ultimately subscribe; no cost to you.

How do I actually apply — what’s the right order?

Phase 1 — Feasibility (before you spend a dollar on plans)

- Confirm your lot allows an ADU under state and local rules. For California readers, see our California ADU laws guide.

- Calculate your usable current equity using the formula above.

- Estimate your project budget by ADU type. See our ADU cost guide.

- Check your first-mortgage rate and decide whether to preserve it.

Phase 2 — Pre-qualification (before you pay for plans)

- Call two to three lenders. Describe your project, your equity, and your first mortgage. Ask for written pre-qualification.

- Compare offers side by side — rate, term, fees, close timeline, and contractor requirements.

- If using the future-value lane, ask: “Will you order an as-completed appraisal? At what point in the process?”

Phase 3 — Plans, contractor, and contract (before you pay for an appraisal)

- Engage a designer or use a pre-approved plan set. Many California cities — including San Diego, Chula Vista, Encinitas, El Cajon, and San Marcos — offer free or discounted pre-approved ADU plan sets.

- Get one to three contractor bids. Verify license, insurance, and references.

- Sign a fixed-price contract with a milestone-based draw schedule, lien waivers required at each payment, and a 5–10% holdback released at certificate of occupancy.

- Lock your loan rate, if your lender offers rate-lock at this stage.

Phase 4 — Loan close (before construction starts)

- Lender orders appraisal (as-completed for construction/renovation loans; current for HELOC).

- Underwriting completes; clear-to-close issued.

- Closing. Funds open on the HELOC, or the construction loan begins disbursing per the draw schedule.

Phase 5 — Build and beyond

- Permits pulled. Construction starts.

- Draws release at milestones (construction loan) or you draw against the HELOC as invoices arrive.

- Final inspection. Certificate of occupancy issued.

- ADU rents (if applicable). Loan converts (if construction-to-perm) or refinances (if two-close).

Frequently asked questions

Is a HELOC or construction loan better for an ADU?

Neither is universally better. A HELOC is usually the first choice when your current home equity covers the ADU budget plus contingency and you want to preserve a low first-mortgage rate. A construction or renovation loan is usually the first choice when your equity does not cover the build, when you need a locked fixed rate, or when you want lender-controlled draws.

Can you use a HELOC to build an ADU?

Yes, if your lender allows the use, your equity supports the borrowing room, your income qualifies, and your local jurisdiction permits the ADU. Most HELOC lenders place no restriction on using funds for an ADU; the practical limit is your current equity and your DTI ratio.

Do I need 20% equity for an ADU construction loan?

Not necessarily. Construction and renovation loans typically allow you to borrow up to 75–80% of the future as-completed appraised value — sometimes higher under FHA 203(k) Standard for purchase transactions. The current-value equity requirement is less restrictive on construction loans than on standard HELOCs, which is one of the main reasons equity-thin owners choose the construction lane.

What is the difference between a HELOC and a construction loan?

A HELOC is a revolving second-mortgage line of credit secured by your current home equity, with a variable rate, that you draw on as needed. A construction loan is a short-term loan secured by the home's future as-completed value, released in scheduled draws tied to construction milestones, that either pays off at completion or converts to a permanent mortgage. HELOCs preserve your first mortgage; many construction loans replace it.

Can a construction loan convert to a permanent mortgage?

Yes — if it is a one-time-close construction-to-permanent loan. A two-close construction loan does not convert automatically; you refinance into a separate permanent mortgage at completion.

How long does a construction loan take to close for an ADU?

Typically 45–90 days for construction-to-permanent and renovation loans, depending on the lender, the appraisal, and the contractor approval process. A standard HELOC closes in 2–4 weeks.

Can I use rental income from the ADU to qualify?

Sometimes, depending on the loan program. Fannie Mae's updated rule (SEL-2025-08, implemented in DU 12.1 on March 21, 2026) allows ADU rental income on eligible one-unit principal residences for purchase and limited cash-out refinance transactions, calculated at 75% of market rent and capped at 30% of total qualifying income. Freddie Mac allows ADU rental income on eligible 1-unit primary residences subject to its Single-Family Seller/Servicer Guide. FHA Mortgagee Letter 2023-17 has similar terms with FHA-specific limits, plus a 50% projected-rent allowance in eligible Standard 203(k) cases. Standard HELOCs generally do not credit future rent.

What credit score do I need?

Lender minimums vary. HELOCs typically require higher credit scores for best pricing; some lenders accept lower scores at higher rates. Conventional construction-to-perm and renovation loans generally require stronger credit than entry-level FHA financing. FHA 203(k) Standard's minimum FICO depends on lender overlays and current FHA Handbook requirements. Your actual rate depends on credit, DTI, and CLTV, not just the minimum score — confirm specifics with the lender.

Can I use a HELOC as a down payment on a construction loan?

Sometimes, but it complicates underwriting. Some construction lenders accept HELOC funds for the down payment; others count the HELOC against your DTI and reduce your borrowing capacity. Ask before you tap the HELOC.

What happens if the ADU appraisal comes in low?

Three options: bring more cash to close, scope the project down to fit the lower borrowing room, or appeal the appraisal with supplemental comparable sales. Appeals succeed less often than owners hope. The defensive move is to study three to five recent neighborhood comps before you start.

Is HELOC or construction loan interest tax-deductible for an ADU?

Per the IRS, interest may be deductible when the funds are used to buy, build, or substantially improve the home that secures the loan, subject to the combined mortgage debt limit and other applicable rules. An ADU added to your principal residence can fall under those rules. Document how the funds were used and consult a CPA.

Is RenoFi the same as a construction loan?

RenoFi is a brand that markets after-renovation-value HELOCs and home equity loans through a partner-lender network — products that share the construction loan's future-value appraisal mechanic but the HELOC's structure (second lien, no replacement of your first mortgage). The category is real and useful; specific RenoFi-powered products and state availability vary by partner lender, so check current availability for your state before applying.

Which is faster — HELOC or construction loan?

HELOC, almost always. A standard HELOC closes in 2–4 weeks. A construction-to-perm or renovation loan typically takes 45–90 days.

Should I get a HELOC before I have permits?

Only after you have confirmed feasibility (your lot allows the ADU, the design fits, the cost is realistic). Opening a HELOC before feasibility risks funding a project the city will not approve.

Can I combine a HELOC and a construction loan?

Sometimes, but multiple liens complicate underwriting on the construction loan and complicate refinancing later. Discuss with both lenders before layering products.

Methodology and editorial standards

- We started with the search query and asked: what decision is the reader making, and what are the four to six variables that actually determine the answer? We landed on equity, project size, first-mortgage rate, and contractor-payment comfort.

- We reviewed the top ranking pages and catalogued what they cover, what they miss, and what claims they make without sourcing.

- We verified every regulatory, rate, and program claim against primary sources — Fannie Mae’s Selling Guide, Freddie Mac’s Single-Family Seller/Servicer Guide, HUD Mortgagee Letters, the Federal Reserve H.15 release, the IRS FAQ, the CFPB and FTC consumer guidance, and the California CSLB for contractor-deposit law.

- We assembled the 2026 ADU Loan Structure Decision Matrix from primary-source product descriptions for each loan family.

- We ran the total-cost math on three project sizes ($150K, $250K, $400K) across the four most common structures, calculated from scratch using full-life amortization including draw-period and build-phase interest.

- We checked all internal Dwelling Index pages for cannibalization risk and confirmed this page targets the binary comparison intent.

What we did not do. We did not rank lenders by what they pay us. We did not promise specific rates or approval. We did not invent expert reviewers or fake credentials. We did not present rental-income examples as guarantees.

· · Last verified: May 21, 2026

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

Check your lot, likely ADU type, setbacks, and probable size limit before you talk to a single lender.

Get Your Free ADU Report →