New York ADU Grant: Plus One Program Status, Amounts & How to Apply in 2026

· · Last verified: May 26, 2026

By the Dwelling Index research team — an independent research resource covering ADU financing, costs, and regulations.

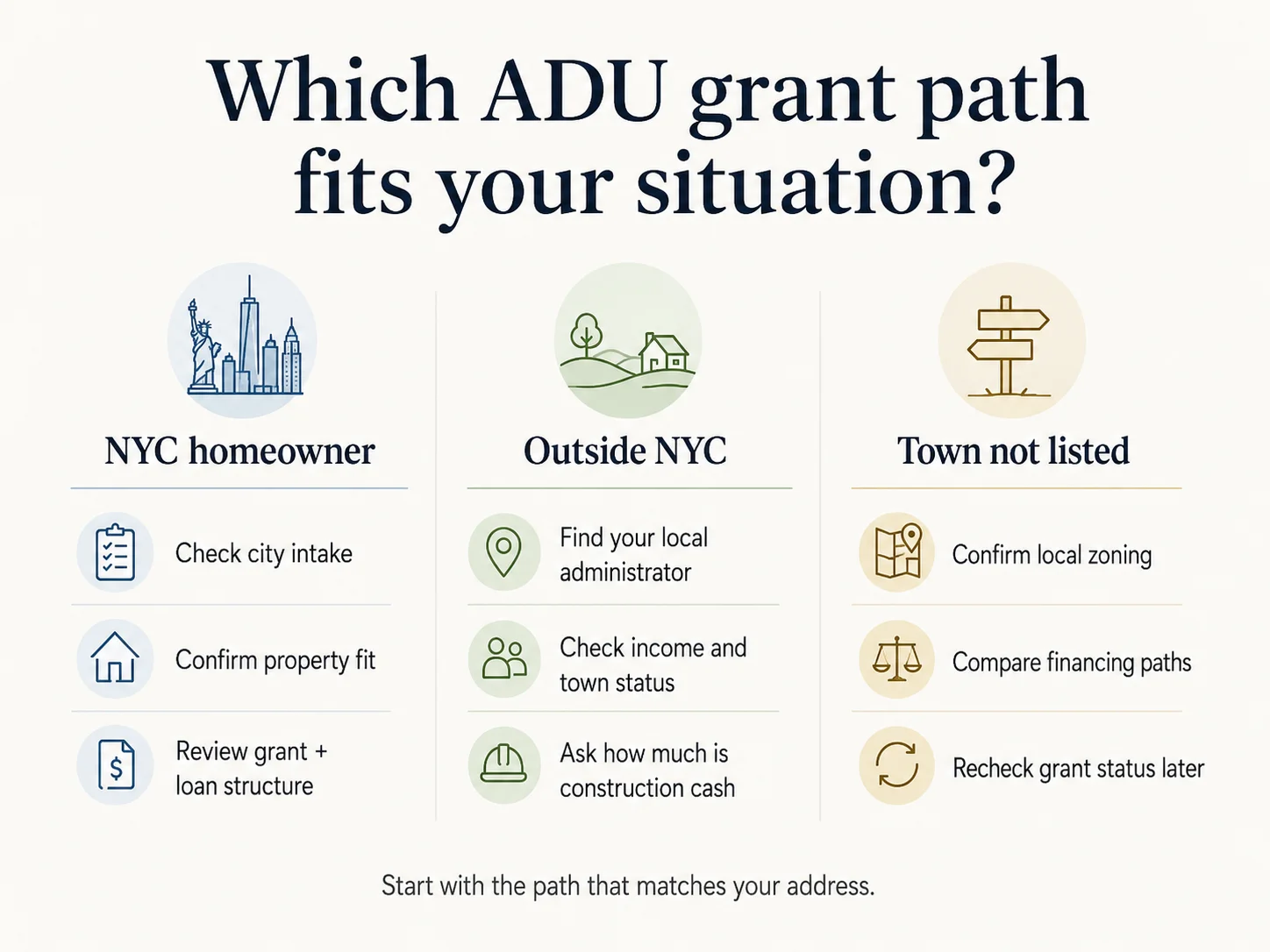

Which New York ADU grant path are you in?

| Your situation | Your first move | Why |

|---|---|---|

| NYC homeowner | Submit the HPD intake survey before June 12, 2026 | NYC has a separate up-to-$395,000 package, but the interest window is closing |

| Your town is on HCR’s list | Apply through the listed local administrator | The state routes all homeowners through local administrators |

| Your town isn’t listed | Don’t wait — check zoning, file HCR’s interest form, compare financing | Plus One can’t help an unlisted town yet, but you can still build |

| You want short-term rental income | The grant is the wrong tool | Plus One requires permanent housing; Airbnb use is barred |

We built this page because the results for “new york adu grant” tend to do one of two things: cover only New York City, or flatten two very different programs into a single wrong number. A homeowner in Buffalo and a homeowner in Brooklyn type the same words and need opposite answers — and the Brooklyn searcher has a clock running. The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations, and what follows routes you to your track, with every figure traced to its source and dated.

An ADU — an accessory dwelling unit (New York City’s program now officially calls it an “ancillary” dwelling unit) — is a second, self-contained home on a lot that already has a house. In New York that can mean a basement apartment, a garage conversion, an attic unit, an attached addition, or a detached backyard cottage. The Plus One ADU Program exists to help low-to-moderate-income owner-occupants build or legalize one.

Is there really a New York ADU grant in 2026?

Answer capsule: Yes. New York’s Plus One ADU Program is a state-backed initiative funded by an $85 million allocation in the 2022–2023 state capital budget, administered through selected local governments and nonprofit partners rather than a single statewide homeowner portal. Homeowners apply through a local program administrator only if their municipality is one of the participating areas.

The program traces back to the 2022–2023 New York State capital budget, which made $85 million available to create and upgrade accessory dwelling units across the state as part of a five-year housing plan (NYS HCR Plus One ADU page, verified May 26, 2026). New York State Homes and Community Renewal — HCR, the state’s housing agency — doesn’t hand checks to homeowners. It funds Local Program Administrators (LPAs): nonprofits and municipal governments that run community-specific programs. As of HCR’s January 2026 Gap Loan funding documents, HCR’s Housing Trust Fund Corporation had contracted with 14 LPAs working across more than 80 communities, and the March 2026 NYC announcement cited 14 partners building more than 550 ADUs statewide.

This structure is the single most misunderstood thing about the program, and HCR’s own page causes the confusion. The official site lists “eligible applicants” as partnerships between a non-profit housing organization and a municipal or county government — which reads, to a homeowner, like they’re shut out. They’re not. That language describes who applies to the state for funding. As a homeowner, you apply to the administrator for your town. If your town isn’t covered, there is currently no way to apply directly to New York State for Plus One money.

Why “grant” doesn’t always mean a no-strings check

Here’s the honest part you’ll find nowhere on page one: the word “grant” is doing a lot of work. Outside NYC, the money is generally a forgivable grant — you don’t repay it if you keep meeting the rules for a regulatory period of at least 10 years. Break the rules or sell early, and a declining-balance repayment can kick in. Inside NYC, a big chunk of the “$395,000” is actually a loan. We decode all of it below. None of this is a reason to walk away — for the right homeowner this is one of the highest-dollar public ADU subsidy paths published anywhere in the country — but you should know what you’re signing before you spend a dollar on design.

How much can you get from the New York ADU grant?

Answer capsule: Outside New York City, local Plus One programs commonly publish up to $112,500–$125,000 in total forgivable grant support, but that figure includes design, permitting, oversight, and administration — leaving less for construction. In New York City, the combined package reaches up to $395,000: up to $175,000 in HCR grant funds plus up to a $220,000 HPD loan, subject to income limits and underwriting.

The dollar figure depends on which track you’re in, and even within the statewide track, administrators set their own caps. Here is the comparison no single official page assembles:

| Statewide Plus One (outside NYC) | NYC Plus One | |

|---|---|---|

| Maximum assistance | Up to $125,000 (some LPAs cap at $112,500) | Up to $395,000 total |

| Structure | Forgivable grant | $175,000 grant + $220,000 loan |

| Repayment | Not repaid if rules are kept; declining-balance recapture on early sale/non-compliance | Grant not repaid; loan repaid at 0–5%, or deferred-forgivable if you can’t afford payments |

| Income cap | ≤120% AMI (county-adjusted) | ≤165% AMI (preference to ≤120% AMI) |

| Regulatory period | At least 10 years | 10-year primary-residence obligation; up to 15 years for some rent-restricted loan paths |

| Administered by | Local nonprofits & municipalities (LPAs) | NYC HPD + Restored Homes HDFC |

| Status (May 2026) | Varies by town — several open | Interest window OPEN — closes June 12, 2026 |

Sources: HCR Plus One Gap Loan RFA (Jan 2026); NYC HPD live Plus One page, term sheet & FAQ; CDLI; RUPCO. Figures are program maximums and eligibility ceilings, not guarantees — your actual award depends on project scope, underwriting, and current funding. Verified May 26, 2026.

The number nobody tells you: headline amount vs. construction cash

This is the most valuable thing on this page, and it comes straight from the administrators’ own published rules. “Up to $125,000” is not $125,000 of construction money.

Community Development Long Island (CDLI), which runs Plus One for Babylon, East Hampton, Shelter Island, and Southampton, states it plainly: the program may provide up to $125,000 in forgivable grant funds, but that total includes CDLI program support — design, permitting, construction oversight, closeout, and ongoing compliance. The amount actually available for construction is up to $115,000 — and you only reach that ceiling if you cover your own pre-development costs, like hiring your own architect (CDLI Plus One FAQ, verified May 26, 2026).

The Long Island Housing Partnership (LIHP), which runs the program for Huntington and other Suffolk towns, publishes the same split — up to $125,000 with $112,500 usable for construction — and adds the figure that should reset every Long Island homeowner’s expectations: the average cost of a new ADU build can exceed $175,000 (LIHP Huntington program guidelines, verified May 26, 2026). TAP Inc., the Albany/Troy administrator, discloses that up to 10% of the grant can go to administration and optional in-house design. RUPCO, covering the Hudson Valley, publishes a lower headline cap of $112,500 to start (rupco.org, verified April 8, 2026).

| Administrator | Published cap | Usable for construction | The reality |

|---|---|---|---|

| CDLI (Babylon, E. Hampton, Shelter Is., Southampton) | Up to $125,000 | Up to $115,000 | Full $115K only if you pay your own pre-development |

| LIHP (Huntington + Suffolk) | Up to $125,000 | Up to $112,500 | Average new ADU build can top $175,000 |

| TAP Inc. (Albany/Troy) | Up to $125,000 | ~90% | Up to 10% goes to admin/design |

| RUPCO (Hudson Valley) | Up to $112,500 | Varies | Lower headline cap; county-specific windows |

| NYC HPD/HCR | Up to $395,000 | Grant + loan | $220,000 of it is a loan, not grant |

The lesson: ask your administrator one specific question — “How much of this is construction cash after your fees?” — before you build a budget around the headline number. On Long Island, the gap between a ~$113K–$115K grant and a $175K+ build is the gap you’ll need to finance. That’s not a reason to skip the grant; it’s a reason to plan the rest.

How NYC’s money is structured

NYC’s “$395,000” is two things stacked: up to a $175,000 grant from HCR that isn’t repaid, and up to a $220,000 loan from HPD that is. These loan terms are the government program’s own — interest can drop to 0% and the term can stretch toward 30 years based on income, and if you genuinely can’t carry payments, the loan can convert to a deferred-forgivable loan with no monthly payments and forgiveness over time (NYC HPD term sheet and FAQ, verified May 26, 2026). Treat the grant as the gift and the loan as financing.

Before you chase a grant, confirm your lot can host an ADU and what it would cost — free, about 60 seconds, and we’ll tell you honestly if it doesn’t qualify.

See What You Can Build → Get Your Free ADU ReportIs NYC’s ADU grant different from the rest of New York?

Answer capsule: Yes, substantially. New York City runs a higher-dollar, higher-income-cap version of Plus One ($395,000 combined; 165% AMI) administered by HPD and Restored Homes HDFC, with an intake window that closes June 12, 2026. The rest of the state runs the $125,000 / 120% AMI version through local administrators on rolling, town-by-town windows.

NYC’s program reopened on March 18, 2026 after being closed to new applicants since February 2024 — a two-year pause (NYC Mayor’s Office release, March 2026). When it first launched in late 2023, it drew more than 1,300 submissions in two weeks before closing. That history is the honest basis for urgency: HPD reviews on a rolling basis, funding is limited, and the last window stayed shut for two years.

One precision point that matters: the open step right now is an intake survey, not an application. You submit the survey to convey interest; HPD then runs a site-feasibility review and, if you’re eligible, sends a formal application that carries a $200 non-refundable fee. The intake survey is not an offer, approval, or guarantee of funding. The interest window closes June 12, 2026.

NYC also launched an “ADU for You” resource hub and a DOB-reviewed Pre-Approved Plan Library of ADU designs, which can speed early review. It does not replace project-specific professional design or DOB filing, and it does not guarantee approval — every NYC ADU still needs site-specific work and a permit. (Worth knowing: the December 2024 “City of Yes for Housing Opportunity” zoning reform formally defined ADUs in NYC’s zoning code for the first time, which is why some previously ineligible properties were reconsidered.)

NYC eligibility and property rules

NYC allows eligible homeowners up to 165% AMI, and HPD’s live program page says preference goes to households at or below 120% AMI. (An older HPD FAQ still references a 100% AMI priority — if the threshold matters to your application, confirm the current number with HPD/Restored Homes.)

| NYC Plus One term | Published detail |

|---|---|

| Income cap | Up to 165% AMI; preference to ≤120% AMI |

| HCR grant | Up to $175,000 (not repaid) |

| HPD loan | Up to $220,000 (0–5%, or deferred-forgivable) |

| Eligible property | Detached, semi-detached, or semi-attached homes with 1–2 existing units |

| Owner occupancy | Required as primary residence |

| Regulatory period | 10-year primary-residence obligation; up to 15 years on rent-restricted loan paths |

| Rent restriction | Deferred-forgivable path sets initial rent within a 100% AMI limit |

| Architect/contractor | Restored Homes provides approved architects and general contractors — you generally cannot bring your own |

| Basement conversions | Must meet ceiling-height rules and sit outside the 2050 stormwater flood area and 2080 100-year coastal flood zone |

| Application | Intake survey → site review → formal application with $200 non-refundable fee; window closes June 12, 2026 |

Sources: NYC HPD live Plus One page, FAQ, term sheet; NYC Mayor’s Office release (Mar 2026). Verified May 26, 2026.

Is my city or town in the Plus One ADU program? New York ADU grant status by city and town

Answer capsule: Maybe — Plus One’s network spans more than 80 New York communities through 14 local administrators, clustered in NYC, Long Island, the Hudson Valley, Westchester, the Capital Region, Buffalo, and Central New York. If your municipality isn’t covered by an active administrator, you generally cannot apply for Plus One funds.

This is the table that would otherwise cost you five to ten browser tabs. We assembled it from HCR’s official municipality roster and cross-checked status against each administrator’s own page. Where we confirmed a live window, we say so; where we couldn’t, we say “confirm” honestly rather than guess.

| Region / municipality | Administrator | Status (verified) | Next action | Verified |

|---|---|---|---|---|

| NYC — all five boroughs | NYC HPD + Restored Homes | Open — closes Jun 12, 2026 | Submit intake survey | May 26, 2026 |

| Long Island — Shelter Island, Southampton | CDLI | Open | Apply (See If You Qualify) | May 26, 2026 |

| Long Island — East Hampton | CDLI | CDLI: open, limited funding; HCR: pending contract | Confirm with CDLI before applying | May 26, 2026 |

| Long Island — Babylon | CDLI | Closed — waitlist | Submit interest form for waitlist | May 26, 2026 |

| Long Island — Huntington | LIHP | Guidelines live; verify intake | Confirm intake with LIHP | May 26, 2026 |

| Long Island — Brookhaven, Islip, Southold | LIHP | Participates per HCR roster | Confirm with LIHP | May 26, 2026 |

| Westchester — Cortlandt, Croton-on-Hudson, Dobbs Ferry, Hastings-on-Hudson, Irvington, Yorktown | Habitat NYC & Westchester | Active service area | Pre-qualify with Habitat | May 26, 2026 |

| Westchester — Bedford | per HCR roster | Confirm | Confirm | May 26, 2026 |

| Westchester — Tarrytown, Lewisboro, Pleasantville | Housing Action Council | Annual window Nov 1 – Mar 1 | Apply in window | May 26, 2026 |

| Hudson Valley — Ulster, Columbia, Orange, Sullivan counties (Kingston, Saugerties, Woodstock, Chatham, Rosendale + 25 more towns) | RUPCO | Open | Apply by county | Apr 8, 2026 |

| Hudson Valley — Amenia | Hudson River Housing | Open — rolling | Submit pre-application; ~10 business days response | May 26, 2026 |

| Hudson Valley — Clinton, Northeast, Pine Plains, Pleasant Valley, Stanford, Unionvale | Hudson River Housing | Participates per HCR roster | Confirm with HRH | May 26, 2026 |

| Hudson Valley — Poughkeepsie (town), Rhinebeck (village), Beacon | Town / HRH / City of Beacon | Confirm | Confirm | May 26, 2026 |

| Capital Region — Albany, Troy | TAP Inc. | Active | Confirm intake with TAP | May 26, 2026 |

| Western NY — City of Buffalo | Buffalo Urban Renewal Agency | Closed | Check back / express interest | May 26, 2026 |

| Western NY — Amherst | Town of Amherst | Confirm | Confirm | May 26, 2026 |

| Central NY — Ithaca | Ithaca Neighborhood Housing Services | Confirm | Confirm | May 26, 2026 |

| Central NY — Utica | Utica Center for Development | Confirm | Confirm | May 26, 2026 |

Sources: hcr.ny.gov/adu roster; CDLI, LIHP, RUPCO, Habitat NYC & Westchester, Hudson River Housing (Amenia), Housing Action Council (Tarrytown), TAP, BURA — each verified at the date shown. Statuses change quickly; “confirm” means the town participates per HCR’s roster but the live window should be confirmed with the administrator before you rely on it.

Don’t see your town? HCR maintains a program-expansion interest form, linked directly from its official Plus One ADU page. It won’t get you a grant today, but municipal demand factors into where HCR onboards next.

What are the income limits for the New York ADU grant?

Answer capsule: Income caps are set per administrator and tied to county Area Median Income — generally up to 120% AMI outside NYC and up to 165% AMI inside NYC. Because AMI varies by county and household size, the binding number is always your administrator’s current chart. CDLI’s Long Island threshold for a four-person household, for example, is $197,160.

AMI — Area Median Income — is the midpoint household income for your county, published annually by the federal government and adjusted for household size. “120% AMI” means your household can earn up to 1.2 times that midpoint. Because the midpoint in Westchester is far higher than in Sullivan County, the dollar cutoff that binds you is your county’s.

We pulled CDLI’s actual published income table for Nassau/Suffolk — most pages won’t give you hard numbers:

| Household size | Maximum annual income |

|---|---|

| 1 person | $138,012 |

| 2 people | $157,728 |

| 3 people | $177,444 |

| 4 people | $197,160 |

| 5 people | $212,933 |

| 6 people | $228,706 |

Source: CDLI Plus One income guidelines, verified May 26, 2026. CDLI cites $197,160 as its current Nassau/Suffolk four-person threshold.

CDLI, LIHP, TAP, and Habitat each publish their own local tables, so don’t assume Long Island’s numbers apply upstate. For NYC, HPD’s published 165% AMI figure for a two-person household is roughly $186,450; HPD’s live AMI chart is the binding reference for your exact household size.

The “too rich or too poor” worry

Two opposite fears come up constantly. Higher earners assume they’re over the cap — and outside NYC, the 120% line is genuinely tight, which is exactly why NYC’s 165% ceiling drives such heavy demand. On the other end, lower-income owners assume the program “isn’t for them” — but the statewide track is built for low-to-moderate-income owner-occupants, and several administrators give scoring preference to lower-income applicants. If you own your home and live in it, you’re in the target zone. The only way to know your exact standing is your administrator’s chart.

Includes our New York eligibility checklist and the exact document list administrators request — pay stubs, tax returns, bank statements, mortgage and insurance statements — so you walk in ready instead of guessing.

Download the Free ADU Starter Kit →What ADU types can the grant pay for?

Answer capsule: Plus One can fund new ADUs and the legalization of existing ones, but the permitted type depends on local zoning and site conditions. Eligible types across New York programs include detached backyard cottages, garage and carriage-house conversions, basement apartments, attic conversions, and attached additions. In NYC, ADUs are capped at 800 square feet and every project requires DOB permits and professional filing.

HCR’s own description covers small detached units on single-family lots, basement apartments, garage conversions, and “other permitted units” — with the key qualifier that what you can build is whatever your locality permits. A few decoded definitions:

- Detached ADU / DADU: a free-standing structure, like a backyard cottage. Usually the most expensive because it needs its own foundation and utility laterals (the pipes and lines connecting to municipal water, sewer, and power). In NYC, detached units carry rear-yard, height, and setback (the required distance from property lines) constraints.

- Garage conversion: turning an existing garage into living space — often the cheapest path because the structure already exists.

- Basement or attic conversion: legalizing or finishing interior space. In NYC, basements face extra scrutiny for ceiling height (a 7-foot minimum), egress, and flood-zone rules.

- Attached ADU: an addition that shares a wall with the main house.

In New York City, ADUs are capped at 800 square feet under the zoning code, and every project requires Department of Buildings permits and filing by a registered design professional (NYC HPD FAQ and ADU guide).

A warning worth its own sentence: do not buy a prefab or tiny-home unit before confirming local code, zoning, foundation, utility, and permit requirements — and before confirming your administrator will fund that approach. The grant funds code-compliant units your municipality allows, not whatever you can order online.

What are the strings attached if you accept the grant?

Answer capsule: The money is real, but it carries long-term housing-use obligations. Depending on location and structure, homeowners accept owner-occupancy, a prohibition on short-term rentals, a regulatory period of at least 10 years (up to 15 on some NYC loan paths), a recorded deed covenant, and declining-balance repayment if you sell early or break the rules.

This is the section that doesn’t sell, which is exactly why most pages skip it. We include it because hiding it would be the fastest way to lose your trust — and because for most people building long-term housing, these terms are entirely livable once understood.

Drawing from CDLI’s, LIHP’s, Habitat’s, and HPD’s published terms (verified May 26, 2026):

- A regulatory period of at least 10 years. You enter a regulatory agreement with monitoring that can include site visits roughly every two years. Some NYC rent-restricted loan paths run 15 years.

- Owner-occupancy. You must keep living on the property. This is not a vehicle for an absentee investor. In NYC, one unit must remain your primary residence — you generally cannot rent out both the main home and the ADU.

- Not an Airbnb path. Local administrators like Habitat and TAP bar short-term and vacation rental use outright. In NYC, separate citywide short-term-rental rules bar renting a unit for fewer than 30 days unless the host lives there — making ADU Airbnb use highly restricted regardless.

- A recorded deed covenant. CDLI requires a deed covenant filed with the County Clerk. It runs with the property and shows up in title searches.

- Declining-balance recapture. Per CDLI, on early sale or non-compliance within the regulatory period, grant funds are subject to repayment on a simple annual declining-balance basis — the longer you comply, the less you could owe.

- Reimbursement-only disbursement. An operational reality almost no page mentions: CDLI pays grant funds on a reimbursement basis only — no advance payments to contractors. Funds flow in progress payments at 50% and 100% completion, with 10% held until a Certificate of Occupancy is issued. You or your contractor often need working capital to float the job before reimbursement arrives.

- You’ll likely contribute your own money. Administrators expect a homeowner contribution once grant funds are exhausted, and may require proof of that funding before construction. If your project exceeds the grant, you either reduce scope or document additional funds.

| String attached | Practical meaning | Bad fit if… |

|---|---|---|

| No short-term rentals | Must be permanent housing | You planned Airbnb/seasonal income |

| Owner occupancy | You must keep living there | You expect to move soon |

| Rent cap (NYC deferred path) | Initial rent within a 100% AMI limit | You need market rent to pencil out |

| Recapture on early sale | Declining-balance repayment within the regulatory period | You may sell within a few years |

| Reimbursement-only | No upfront cash; 10% held to C of O | You can’t float construction costs |

| Admin/soft-cost carveout | Headline amount isn’t all construction | Your budget is already tight |

The damaging admission, stated plainly: for a higher-income homeowner, someone planning to sell or refinance soon, or anyone counting on short-term rental income, the New York ADU grant may be the wrong money. Cheap money with restrictions can cost more than flexible money if it blocks your actual plan. If that’s you, the financing section is the cleaner path. If your goal is housing a family member or earning steady long-term rental income while you stay put, these terms are very livable — and this is among the best ADU money available.

How do I apply for the New York ADU grant?

Answer capsule: You apply through the administrator serving your municipality, not a single statewide form. NYC homeowners start with the HPD/Restored Homes intake survey; everyone else starts with HCR’s participating-municipality list and the local administrator’s application or interest form.

A clean seven-step path:

- Find your municipality in the status table above (or HCR’s roster).

- Confirm intake is open — “open,” “waitlist/closed,” “rolling,” and “pending contract” are very different states. Babylon is waitlist-only right now while two other CDLI towns are open; Amenia takes rolling pre-applications.

- Check your income band against the administrator’s current AMI chart.

- Confirm zoning and property type — even with grant money, your local zoning has to allow the unit. (For NYC zoning and rules specifically, see our New York ADU laws and NYC zoning rules guide.)

- Gather documents — typically consecutive pay stubs, tax returns, bank statements, mortgage statement, proof of insurance, and proof that taxes are current.

- Do not start reimbursable work without program clearance. Grant funds reimburse approved work; spending ahead of approval risks getting nothing back.

- Ask the right questions before you sign (below).

Questions to ask your local program administrator

- Is intake open, or is this an interest form/waitlist?

- What is the current maximum award — and how much of it is construction cash after your fees?

- What income limit applies to my household size this year?

- What happens if my project costs more than the grant?

- Can I use my own contractor and architect? (NYC answer: generally no — Restored Homes provides approved architects and general contractors. CDLI and Habitat may allow homeowner-selected vendors if program requirements are met.)

- What deed covenant or regulatory agreement gets recorded?

- What exactly triggers repayment, and how does the declining balance work?

- Are family occupants treated differently from tenants?

- How and when are funds disbursed — and do I need to float costs before reimbursement?

Can the grant legalize an existing basement, garage, or illegal ADU?

Answer capsule: Sometimes. HCR explicitly allows Plus One to support bringing an existing ADU into compliance with local and state code, and NYC addresses basement legalization — but flood zones, a 7-foot ceiling-height minimum, egress, and zoning issues can make some units infeasible, and reimbursement is never automatic.

The program was designed partly to convert New York’s large stock of informal and unpermitted units into safe, legal, code-compliant housing. HCR’s language covers improving an existing ADU “that needs to be brought into compliance.” In NYC, basement legalization is a recognized use, but it’s also where projects most often die on feasibility: HPD requires the basement space to meet ceiling-height rules and sit outside the 2050 stormwater flood area and the 2080 100-year coastal flood zone before conversion. A cellar that fails height or egress, or sits in the wrong flood zone, may simply not qualify. Before spending money to legalize, get a feasibility read on the specific space — the grant won’t rescue a unit that can’t meet code.

Will the grant cover the full cost of an ADU?

Answer capsule: Outside NYC, often no. A $112,500–$125,000 grant — with only ~$112,500–$115,000 usable for construction — rarely covers a detached new build, which can exceed $175,000 in the downstate market per LIHP’s own figures. NYC’s larger combined package goes further but is still bounded by scope, underwriting, and the loan/grant split.

A detached backyard cottage with its own foundation and utility laterals is the priciest ADU type, and in much of downstate New York the all-in cost outruns the grant — LIHP puts the average new ADU build above $175,000. Garage and basement conversions fit a grant far more comfortably because the shell already exists. When a project exceeds the grant, your administrator gives you two choices: reduce scope, or document additional funds. That’s where financing comes in — and where the grant should be your first path checked, not your only one. See what an ADU actually costs to build before finalizing your budget.

When the grant doesn’t cover the gap, mortgage-backed ADU financing options exist — and some don’t require touching your existing mortgage.

Grant not enough? Explore mortgage-backed ADU financing options →Path education; no lender rankings or rate promises.

What if my town isn’t listed, intake is closed, or the grant isn’t enough?

Answer capsule: If your town isn’t on HCR’s roster, Plus One likely can’t help yet — but homeowners build ADUs across New York every day without a grant. The practical next moves are to verify local zoning, submit any official expansion/interest form, and compare non-grant financing paths such as cash-out refinance, renovation loans, construction loans, or home equity.

The grant is narrow by design, and plenty of New Yorkers fall just outside it — over the income cap, in a non-participating town, or facing a build that outruns the cap. Here are the main financing lanes, framed by situation rather than ranked. For the full New York ADU financing lane breakdown, see our New York ADU financing guide.

| Financing path | Fits best when… | Watch for |

|---|---|---|

| Cash-out refinance | You have substantial equity and replacing your mortgage makes sense | Resets your whole mortgage; closing costs |

| Renovation / construction loan | You’re building new and want financing tied to the project | Draw schedules, inspections, more paperwork |

| HELOC / home equity loan | You want to borrow against equity without touching your first mortgage | Variable rates (HELOC); your home is collateral |

| Grant + financing stacked | You qualify for Plus One but face a gap above the cap | Confirm the program allows your other funding source |

A HELOC is a home equity line of credit — a revolving credit line secured by your home. A cash-out refinance replaces your existing mortgage with a larger one and gives you the difference in cash. These put your home up as collateral, so they’re tools, not free money. Recheck the grant roster quarterly, too — HCR keeps onboarding new municipalities, and your town may join.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Also useful: ADU financing for lower-income homeowners · financing an ADU on a fixed income · compare New York with other state ADU grant programs

Can the ADU grant affect my taxes, rent, or ability to sell or refinance?

Answer capsule: Yes. An ADU can raise your assessed value, and the grant’s covenant restricts rent, occupancy, and resale flexibility for the regulatory period. But several New York counties now offset the tax hit: Albany and Ulster counties each adopted ADU property-tax exemptions in 2025 that fully exempt the added assessed value for five years, then phase it out over five more.

Building an ADU typically increases your home’s assessed value, which can raise property taxes. New York’s ADU exemption is tied to Real Property Tax Law § 421-p, which counties, cities, towns, villages, and some school districts must opt into locally before it helps a homeowner. Two counties have done so with nearly identical structures:

- Albany County (Local Law “C” of 2025): the increase in assessed value from adding an ADU is fully exempt for five years, then partially exempt over the next five at 75%, 50%, 25%, 15%, and 5%. It applies to value increases between $3,000 and $200,000, and Albany’s version bars short-term rentals from qualifying. Effective January 1, 2026.

- Ulster County (Local Law No. 5 of 2025): the same five-year-full, five-year-phase-out structure, capped at $200,000 of added value, amended to exclude short-term rentals.

These are local opt-ins, so they don’t exist everywhere — but they’re a real, stackable benefit in the regions that have them, and they pair naturally with the grant’s own no-short-term-rental rule. Always confirm with your local assessor, because the exemption and its fine print vary by jurisdiction. Note too that the grant’s covenant can complicate an early sale or cash-out refinance during the regulatory period; factor that into your timeline.

What should I do before I apply?

Answer capsule: Before applying, confirm your municipality is active, check your income band against the current AMI chart, verify owner-occupancy and property type, confirm local zoning and (in NYC) flood/ceiling/egress feasibility, clear any open violations, and decide whether you can accept the regulatory period. Then ask your administrator how much of the award is construction cash.

A 10-minute pre-application gut check:

- Is my town listed and intake open?

- Is my household income under the cap for my size?

- Do I own and live in the home?

- Does my zoning allow the ADU type I want?

- Are there open violations on the property?

- Can I float construction costs given reimbursement-only disbursement?

- Am I comfortable with a 10-year (or longer) covenant and no short-term rentals?

- Do I have a realistic plan for costs above the grant?

If you answered yes down the line, you’re a strong candidate. If a few are “no,” the financing path may serve you better than the grant. Either way, the next step is the same: confirm what your specific lot can actually support. Also useful: paying for an ADU to house aging parents and financing an ADU built for rental income.

Not sure where to start? See what’s possible at your address — free, about 60 seconds.

See What You Can Build → Get Your Free ADU ReportWhat we verified

We verified the program structure from official state and city sources, then cross-checked practical homeowner details against local administrator pages. Program status changes quickly, so each major figure is dated.

- Statewide structure, $85M allocation, LPA model, 14 LPAs across 80+ communities, municipality roster — NYS HCR Plus One ADU page and January 2026 Gap Loan RFA. Verified May 26, 2026.

- Statewide $125,000 cap / 120% AMI — HCR Gap Loan RFA. Verified May 26, 2026.

- Construction-cash caveat ($115,000), reimbursement-only disbursement, CDLI income table, deed covenant, declining-balance recapture, 10-year residency — CDLI Plus One FAQ. Verified May 26, 2026.

- LIHP split ($125,000 / $112,500 construction) and $175,000+ average new-build cost — LIHP Huntington program guidelines. Verified May 26, 2026.

- Hudson Valley $112,500 cap, open windows — RUPCO. Verified April 8, 2026.

- Amenia open/rolling, ~10-business-day response — Town of Amenia / Hudson River Housing. Verified May 26, 2026.

- NYC up to $395,000 ($175K grant + $220K loan), 165% AMI / 120% preference, 1–2 unit property rule, intake-survey-not-application, $200 fee, reopened Mar 18 2026, interest window closes Jun 12 2026, 800 sq ft cap, Restored Homes vendor requirement, basement flood/ceiling rules — NYC HPD live Plus One page, FAQ, term sheet, and Mayor’s Office release. Verified May 26, 2026.

- County ADU tax exemptions (RPTL § 421-p; 5-yr full + 5-yr phase-out, $200K cap, STR exclusion) — Albany County and Ulster County 2025 local-law releases; NYS Tax Department Form RP-421-p-adu. Verified May 26, 2026.

Known source conflicts to confirm for your situation: NYC AMI priority (live page 120% vs. older FAQ 100%); NYC Pre-Approved Plan count (9 vs. 11 across city releases); East Hampton status (CDLI “open” vs. HCR “pending contract”); coastal flood-year references (2080 vs. 2100). For anything affecting your eligibility, the administrator’s pre-screen is the binding answer.

Program status can change before we update this page. Confirm amounts, income limits, deadlines, and participation directly with your administrator or the official HCR/HPD pages before spending money.

Last verified:

Frequently asked questions

- Does New York give grants for ADUs?

- Yes. Through the Plus One ADU Program, eligible owner-occupants can receive forgivable grant support — up to $125,000 in most of the state, or up to $395,000 (grant plus loan) in New York City — administered through local program administrators.

- How much is the New York ADU grant?

- Up to $125,000 statewide (some administrators cap at $112,500, and only about $112,500–$115,000 may be usable for construction after fees), or up to $395,000 in NYC, structured as a $175,000 grant plus a $220,000 loan.

- Is NYC Plus One ADU open right now?

- Yes, as of May 2026. NYC reopened the program March 18, 2026; the interest/intake window closes June 12, 2026. The intake survey conveys interest — eligible homeowners are later sent a formal application with a $200 non-refundable fee.

- Is the NYC ADU grant really $395,000?

- It's a combined figure: up to $175,000 in HCR grant funds that aren't repaid, plus up to a $220,000 HPD loan that is (at 0–5%, or deferred-forgivable if you can't afford payments).

- Who qualifies for the New York Plus One ADU Program?

- Generally, owner-occupants in a participating municipality with household income at or below the AMI cap (120% statewide, 165% in NYC with preference to 120% and below), current on mortgage and taxes, building a code-compliant ADU their zoning allows.

- What are the income limits?

- Up to 120% AMI outside NYC and up to 165% AMI in NYC, adjusted by county and household size. CDLI's Long Island four-person threshold is $197,160; your administrator's current chart is the binding number.

- Do I apply through New York State or my city/town?

- Through your local program administrator, never the state directly. NYC uses HPD/Restored Homes intake; other areas use the administrator listed on HCR's roster.

- What if my town isn't on the HCR list?

- You generally can't apply for Plus One yet. Submit HCR's program-expansion interest form, confirm your local zoning, and compare non-grant financing paths in the meantime.

- Can I use the grant for a detached backyard ADU or a basement apartment?

- Yes, if your local zoning permits it and it meets code. Detached cottages are the costliest type and often exceed the grant; basement and garage conversions fit a grant more comfortably. NYC caps ADUs at 800 square feet.

- Can I use my own contractor?

- Outside NYC, sometimes — CDLI and Habitat may allow homeowner-selected vendors that meet requirements. In NYC, Restored Homes provides approved architects and general contractors, so you generally cannot bring your own.

- Can I use the ADU as an Airbnb?

- No. Plus One requires permanent housing; short-term rentals are barred. NYC's separate citywide short-term-rental rules restrict it further, and Albany and Ulster county tax exemptions also exclude short-term rentals.

- Will I have to pay the grant back?

- The grant is forgivable if you keep the rules for the regulatory period (at least 10 years, up to 15 on some NYC loan paths). Sell early or fall out of compliance and a declining-balance recapture can require partial repayment.

- Can I rent the ADU to a family member?

- Often yes — Plus One supports multigenerational housing as well as affordable rentals. Confirm how your administrator treats family occupants versus tenants.

- Does an ADU raise my property taxes?

- It can, by raising assessed value. Under RPTL § 421-p, counties can opt into an ADU exemption — Albany and Ulster fully exempt the increase for five years, then phase it out over five more. Check whether your county opted in.

Methodology

We started with HCR’s official Plus One ADU page and participating-municipality list, then checked NYC HPD’s live program page, term sheet, and FAQ, and individual local administrator pages (CDLI, LIHP, RUPCO, Habitat NYC & Westchester, Hudson River Housing, Housing Action Council, TAP, BURA) for published intake status, maximum support, income limits, restrictions, and application steps. We cross-checked dollar figures across sources and surfaced the conflicts we found rather than smoothing them over. Where a status changes quickly or a source disagreed with another, we label it for confirmation with the administrator. The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations; we are not a lender, builder, government agency, attorney, or tax advisor. Last verified: May 26, 2026.