ADU Financing for Low Income Homeowners: Real Help, Loan Paths, and Closed Grants in 2026

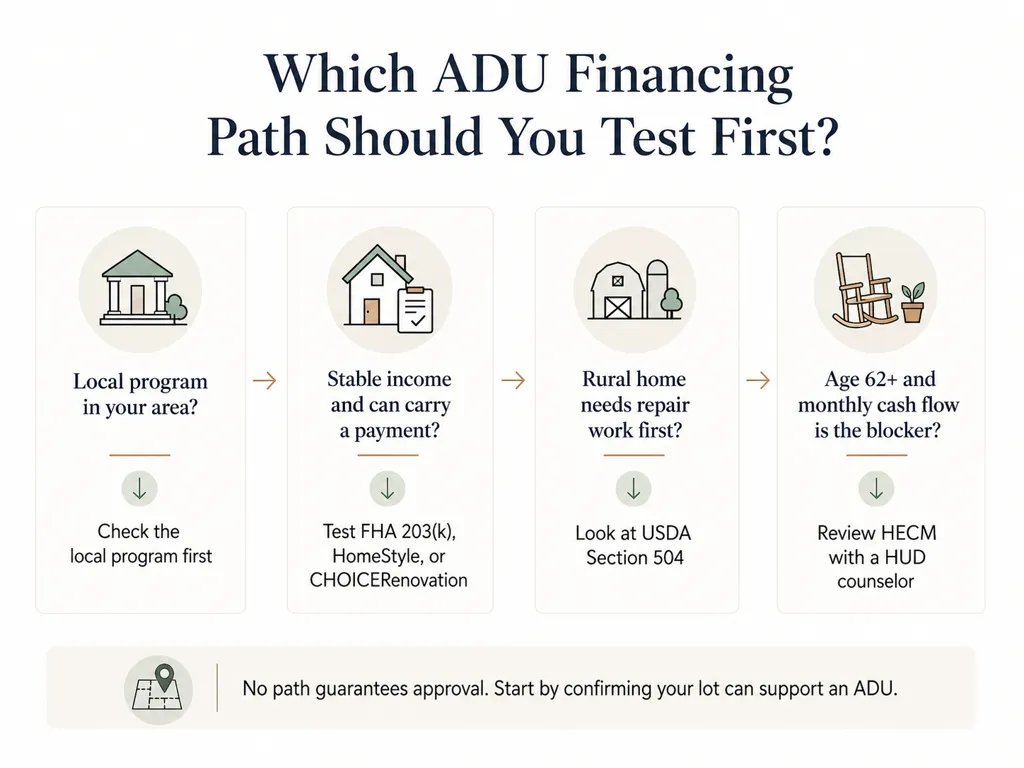

ADU financing for low income homeowners almost never comes from one big grant — it comes from matching your situation to one of four lanes: a local forgivable-loan or rebate program if your city or state runs one, a renovation or future-value mortgage like an FHA 203(k) or Fannie Mae HomeStyle if you can carry a payment, a repair program like USDA Section 504 for smaller rural work, or a senior equity path if you’re 62 or older and understand the risks. Most income-tested help draws its line around 80% of Area Median Income (AMI), though some programs test the homeowner’s income, some test the tenant’s, and some use higher local limits. The number that surprises people most: the most generous verified municipal construction loans we found — the San Diego Housing Commission’s program and Massachusetts’s MassHousing program — go up to $250,000, while the most-cited “grant,” California’s CalHFA ADU Grant, has been closed since December 2023, and the agency now warns that anyone promising to get it for you is likely running a scam. The right first move isn’t picking a loan — it’s confirming your lot can legally support an ADU before you spend a dollar on plans.

An ADU (accessory dwelling unit) is a smaller, self-contained second home on the same property as a primary residence — a detached cottage, garage conversion, basement unit, or attached addition. Depending on local rules, it can sit beside a single-family home or, in some cities, a duplex. A JADU (junior ADU) is a smaller unit, up to 500 sq ft in California, carved out of the existing house.

Start here — match your situation to a lane:

| Your situation | First path to test | The catch to check |

|---|---|---|

| Your city or state runs an active ADU assistance program | The local program | Often requires affordable rent, income-qualified tenants, or 5–15 year covenants |

| Low income but documented, stable, and you can carry a payment | FHA 203(k), HomeStyle/HomeReady, or CHOICERenovation/Home Possible | Not 'easy approval' — depends on credit, debt-to-income ratio, appraisal, ADU type |

| Rural property needing repairs or safety work first | USDA Section 504 | Caps at $40,000 loan / $10,000 grant — not full ADU construction |

| You're 62+ and the blocker is monthly cash flow | HECM reverse mortgage review with a HUD counselor | Debt grows, equity falls, taxes/insurance/occupancy still required |

| You only found an old CalHFA grant page | Do not plan around it | CalHFA warns the 'grant' is fully allocated and scam-targeted |

See what’s possible at your address → Get your free ADU report. Check zoning, likely ADU types, a rough cost range, and financing-path flags before you spend money on design. Start your free ADU report

Disclosure: The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations — not a lender, broker, or builder. Read our full affiliate disclosure and methodology.

The honest admission we owe you first

Here’s the truth most pages bury: most low income homeowners will not find a grant large enough to build a full ADU. The programs that exist are usually local, capacity-limited, funding-round based, capped well below construction cost, restricted by income, paid as reimbursements after you’ve already spent the money, or structured as forgivable loans with multi-year deed covenants that limit who you can rent to and how much you can charge.

That sounds discouraging. It isn’t meant to be. It’s meant to save you from the most expensive mistake we see: paying for architectural plans for a project funded by a grant that turns out to be closed, geographically restricted, or three sizes too small.

Because here’s the other half of the truth: the project is usually still possible — you just need to test the right lane first. Across the country, lower-income homeowners build ADUs every month using renovation mortgages that underwrite against the home’s future value, city forgivable-loan programs, repair programs, and senior equity paths. The Terner Center for Housing Innovation at UC Berkeley documented exactly why this is hard for households like yours: banks have been “slow to design appropriate types of loans,” and lower-income households are “less likely to have the assets needed to fund the construction of an ADU.” That’s a market gap, not a personal failing — and this page exists to walk you through it.

What ADU financing can low income homeowners actually use?

Low income homeowners have four realistic ADU financing lanes: local or state assistance programs, mortgage-backed renovation or future-value loans, repair and accessibility programs, and senior equity options. Grants help at the margins, but most are too small, too local, or too restricted to fund a full ADU on their own. The right lane depends on where you live, whether you can carry a monthly payment, and whether you’ll accept rent or tenant restrictions in exchange for cheaper money.

This is the part nobody assembles in one place, so we will. Each lane solves a different blocker.

Lane 1 — Local ADU assistance, if your city or state has a program

This is the lane that produces real below-market help, and it’s worth checking first because the terms can be dramatically better than a private loan. Local programs come in five flavors, and the words matter:

- A grant is money you don’t repay. Rare, and almost always covers only “soft costs” (design, permits, soil tests), not construction.

- A forgivable loan is money you repay only if you break the rules — usually by selling early or renting above the allowed rent. Most “ADU grants” you’ll see advertised are actually forgivable loans.

- A rebate reimburses you after you’ve paid, so you still need cash or financing upfront.

- A fee waiver reduces or eliminates permit and impact fees — real savings, usually a few thousand dollars on a six-figure project.

- A subsidized loan is below-market financing from a housing agency.

We’ve verified the major programs in the matrix below. The headline numbers: San Diego and Massachusetts offer construction loans up to $250,000; Vermont offers up to $50,000 forgivable; Charlotte offered up to $80,000 forgivable but has closed its application window; Orlando offers up to $10,000 plus fee relief.

Lane 2 — A renovation or future-value mortgage, if your project appraises

If your income is low but documented and stable, the most realistic non-grant path is a mortgage that underwrites against your home’s as-completed value — what it will be worth after the ADU is built — rather than your current equity. This is the critical distinction for anyone told “you don’t have enough equity for a HELOC.” A HELOC (home equity line of credit) lends against today’s value; a renovation mortgage lends against tomorrow’s. The main products are the FHA 203(k), Fannie Mae HomeStyle Renovation (often paired with HomeReady for borrowers at or below 80% AMI), and Freddie Mac CHOICERenovation (paired with Home Possible). We break these down below.

Lane 3 — Repair and accessibility help, when a full ADU loan isn’t realistic yet

If a six-figure construction loan is out of reach, smaller programs can fund the work that keeps your home safe and livable — fixing a roof, upgrading an electrical panel, repairing a foundation. USDA Section 504 (rural) and HUD Title I property-improvement loans live here. They are repair tools, not full-ADU construction loans, and we’ll be clear about their caps.

Lane 4 — Senior equity, when monthly cash flow is the only blocker

If you’re 62 or older, own significant equity, and the problem is that you can’t add a monthly payment on a fixed income, a HECM (Home Equity Conversion Mortgage — the FHA-insured reverse mortgage) can convert equity to cash with no required monthly payment. It is not free money, and the risks are real. We cover them honestly below.

What counts as “low income” for ADU financing?

“Low income” is not self-defined — it’s measured against your county’s Area Median Income (AMI), adjusted for household size, and the threshold varies by program. Many programs draw the line at 80% of AMI, but some test the homeowner’s income, some test the future tenant’s income, and some allow higher local limits. Before you assume you do or don’t qualify, look up your county’s AMI and check which income each program actually measures.

Here’s why the distinction matters, with verified examples:

- The San Diego Housing Commission tests the homeowner’s household income (its published ceiling has shifted across program phases — confirm the current figure on its site), and separately requires the tenant to earn ≤80% AMI for seven years.

- Fannie Mae HomeReady and Freddie Mac Home Possible test the borrower’s income, capped at 80% of AMI.

- Orlando’s rebate condition tests the tenant’s income, allowing up to 120% AMI.

- New York’s Plus One ADU Program sets homeowner-income eligibility through its local administrators, with priority for lower-income applicants.

- USDA Section 504 tests the homeowner’s household income and requires “very low income” — below 50% of AMI.

To find your number, search “HUD income limits [your county]” or ask the program administrator directly. The same dollar income can be “low income” in one county and over the limit in another, because AMI is local.

Verified ADU programs and loan paths: the triage matrix

The best ADU assistance in 2026 isn’t a national grant — it’s a patchwork of state, city, and local programs, each with its own income limits, owner-occupancy rules, rent restrictions, funding windows, and compliance requirements, sitting alongside federal mortgage paths. Some are open, some have closed their application windows, and several widely-cited programs are discontinued. Budgeting around a closed grant is not a financing plan.

Below is our verified, source-linked snapshot. We built it because no single competing page assembles federal loan paths, active local programs, and closed-program warnings in one fit-first table. Every row was checked against the official administering agency.

Status legend: ✅ Open · ⚠️ Limited / funding-round based · 🛑 Applications closed · ⛔ Discontinued · 🏛️ Federal loan path (not a grant) · 🌐 Local administrator varies

Low-Income ADU Financing Triage Matrix — verified May 2026

| Program / Path | Status | Whose income? | Help type / amount | Key restriction | Wrong fit if… |

|---|---|---|---|---|---|

| San Diego Housing Commission ADU Finance Program | ⚠️ Limited | Homeowner (tenant ≤80% AMI separately) | Construction-to-permanent loan up to $250,000; ~1% during construction, converting to ~4% fixed; free technical assistance | City of San Diego only; 680 min credit score; 7-year covenant (tenants ≤80% AMI); no renting to family | Outside San Diego, want to rent to family, or can’t qualify for takeout financing |

| MassHousing ADU Loan Program | ✅ Open (via approved lenders) | Homeowner (income guidelines) | Fixed-rate second mortgage up to $250,000 detached / $150,000 attached | Must already have plans, permits, and pre-development materials before applying | You need pre-development money before you have plans and permits |

| New York Plus One ADU Program | 🌐 Local administrator varies | Homeowner (set by local administrator) | Low/no-interest loans or construction financing; amount varies (one LPA, CDLI, lists up to ~$125,000) | Multi-year regulatory period; recorded deed covenant; no short-term rentals | Your municipality doesn’t participate, or you won’t accept long-term affordability monitoring |

| Vermont VHIP 2.0 | ✅ Open | Tenant (fair-market-rent rules) | 0% forgivable loan up to $50,000 | 20% match (can be in-kind); reimbursement basis; forgiven over 5 or 10 years; fair-market-rent rules | You can’t front costs or won’t accept rental restrictions |

| Charlotte Queen City ADU Program | 🛑 Applications closed | Tenant (≤80% AMI); no owner income limit | Up to $80,000 / 50% of cost; 0% interest, forgivable at $10,000/yr of compliance | Closed to new applicants Oct 31, 2025; 50% owner match; annual recertification | You need it open today or can’t provide the 50% match |

| Orlando ADU Incentive Program | ✅ Open | Tenant (≤120% AMI for rental condition) | Up to $10,000 build-out rebate plus 100% rebate of impact and permit fees | City of Orlando only; must rent to ≤120% AMI household for 12 of first 24 months (waived if resident is 62+) | You need full construction financing |

| CalHFA ADU Grant | ⛔ Closed | — | Previously up to $40,000 for pre-development costs | Fully allocated December 2023; CalHFA warns anyone offering to “get” it is likely a scam | You’re planning 2026 financing around a CalHFA reopening |

| Orange County (CA) OCHFT Affordable ADU Loan | ⛔ Discontinued | — | — | Discontinued by board vote May 21, 2025 | You’re relying on older pages that still list it |

| USDA Section 504 (Repair) | 🏛️ Federal (repair, not ADU build) | Homeowner (very low income, <50% AMI) | Loan up to $40,000 at 1% fixed/20 yr; grant up to $10,000 for owners 62+ | Repairs and health/safety hazard removal only — not full ADU construction; rural areas only | You need six-figure new-build ADU funding |

| FHA 203(k) Renovation Mortgage | 🏛️ Federal loan path | Borrower (no income maximum) | Limited 203(k) rehab cap raised to $75,000 (case numbers on/after Nov 4, 2024); Standard for larger/structural work | Owner-occupied; 580 score for 3.5% down; FHA county limits $541,287–$1,249,125 (2026) | You want a ground-up detached ADU and a pure construction product |

| Fannie Mae HomeStyle + HomeReady | 🏛️ Federal loan path | Borrower (HomeReady ≤80% AMI) | HomeStyle finances ADU renovation/construction; HomeReady allows 3% down for ≤80% AMI borrowers | Renovation costs generally capped at 75% of as-completed value; completion-timing rules apply | You can’t qualify for the payment or the ADU won’t meet code |

| Freddie Mac CHOICERenovation + Home Possible | 🏛️ Federal loan path | Borrower (Home Possible ≤80% AMI) | CHOICERenovation can add or renovate an ADU; Home Possible for ≤80% AMI borrowers | For applications on/after May 4, 2026: rent from renovation-funded unit cannot be used to qualify | Your project depends on a use that won’t be permitted |

| HUD Title I Property Improvement Loan | 🏛️ Federal loan path | Borrower | Insured property-improvement loan; single-family maximum $25,000 | Caps at $25,000 for a single-family property — gap or repair funding, not full detached ADU construction | You need to fund a six-figure detached ADU |

| HECM / Reverse Mortgage | 🏛️ Federal (62+ only) | Homeowner (62+) | FHA-insured reverse mortgage; no required monthly payment | Debt rises, equity falls; must keep taxes, insurance, occupancy, and maintenance current; HUD counseling required | You may move soon, can’t keep property charges current, or don’t understand foreclosure triggers |

Disclosure (repeated near comparison table): The Dwelling Index is reader-supported and may earn a commission when you use our links to explore financing options, at no extra cost to you. Editorial conclusions are independent. Full disclosure.

The local-program landscape is fragmented by design — see which rows can actually apply to your address. → Check your address with a free ADU report

Does the program cover the full ADU cost?

Most ADU assistance covers a slice of the budget, not the whole thing. Detached ADUs commonly run well into six figures, so a $10,000 rebate or a $50,000 forgivable loan is a meaningful down payment on the project — not the project. Match the assistance to the gap it actually closes:

| Program | Max assistance | Typical role in a six-figure build |

|---|---|---|

| Orlando ADU Incentive | Up to $10,000 + fee rebates | Offsets soft costs and permit/impact fees |

| USDA Section 504 | $40,000 loan / $10,000 grant (62+) | Repairs that make a future ADU possible; not the build |

| Vermont VHIP 2.0 | Up to $50,000 forgivable | Large slice of a modest conversion; reimbursement basis |

| Charlotte Queen City (closed) | Up to $80,000 / 50% of cost | Up to half the project — when open |

| SDHC / MassHousing | Up to $250,000 | Can cover a full build, with heavy eligibility and repayment rules |

Closed, paused, or discontinued — don’t plan around these

A closed grant is not a financing plan. Two programs deserve special attention because outdated builder blogs still cite them:

- California CalHFA ADU Grant — The famous $40,000 grant exhausted its funding in December 2023. CalHFA’s own site warns that anyone claiming they can help you access the grant is likely operating a scam. Don’t build a 2026 budget assuming it reopens.

- Orange County (CA) Housing Finance Trust Affordable ADU Loan — Discontinued by board vote on May 21, 2025. OCHFT states it’s not aware of an alternative government-funded ADU finance program in its area.

How to verify your local ADU program in 10 minutes

Program pages go stale, and builder blogs repeat dead programs for years. Verify status yourself before you spend money.

- Search

[your city or county] ADU loan programand addsite:.govto filter to official pages. - Open the administering agency page — a housing authority, finance agency, or planning department — not a builder or lender blog.

- Confirm applications are open today (a current funding round, not an archived announcement).

- Note the income limit and whose income it tests, the owner-occupancy rule, rent/tenant restrictions, and repayment/forgiveness triggers.

- Call or email the administrator before paying for plans: “Is the program accepting applications right now, and what’s the current waitlist?”

- Save a PDF or screenshot of the rules with the date.

Download the free Low-Income ADU Financing Checklist — the exact questions to ask your city, housing agency, or lender, so you don’t miss the detail that changes the answer. Get the free checklist

What if your income is low but you can still handle a mortgage payment?

If your income is modest but documented and stable, the most realistic non-grant path is usually a mortgage-backed renovation or construction loan that underwrites against your home’s as-completed value. These aren’t “easy approval” products — they depend on income, credit, debt-to-income ratio, appraisal, ADU legality, and contractor documentation — but they don’t require the existing equity a HELOC demands. Several of these products were built specifically for lower-income borrowers.

Two facts matter most here: the FHA 203(k) has no maximum income limit — a relief for anyone who assumed they earn “too little” — and Fannie Mae HomeReady and Freddie Mac Home Possible are designed for borrowers at or below 80% AMI.

FHA 203(k): best for attached ADUs, conversions, and existing-ADU rehab

The FHA 203(k) is a government-insured renovation mortgage that rolls a home purchase or refinance together with renovation costs into one loan, with a down payment as low as 3.5% for borrowers with a 580 credit score (or 10% down for scores of 500–579). It’s the most accessible renovation loan for lower-credit, lower-down-payment borrowers, and HUD has explicitly made ADU-related work eligible.

What the rules actually say, decoded:

- HUD Mortgagee Letter 2023-17 added ADUs as eligible improvements — including converting a one-unit home into a one-unit home with an ADU, attaching an ADU, and renovating existing attached or detached ADUs.

- HUD Mortgagee Letter 2024-13 (effective for case numbers assigned on or after November 4, 2024) raised the Limited 203(k) rehabilitation cap from $35,000 to $75,000 and extended completion timelines to 12 months (Standard) and 9 months (Limited). That $75,000 ceiling can cover a limited, nonstructural garage or internal-conversion scope — but the Limited program cannot be used for structural work.

- Standard 203(k) handles larger and structural work, requires an FHA-approved 203(k) consultant, carries a $5,000 minimum repair cost, and must stay within FHA county loan limits — $541,287 in low-cost areas up to $1,249,125 in high-cost areas for 2026 (effective for case numbers assigned on or after January 1, 2026).

The honest limitation: a ground-up detached ADU isn’t the cleanest fit for a 203(k). The program shines for conversions, attached units, and rehabbing an existing ADU. For a pure detached new build, a construction-to-permanent loan or a HomeStyle/CHOICERenovation loan is usually the better tool.

Fannie Mae HomeStyle Renovation + HomeReady

Fannie Mae’s HomeStyle Renovation loan finances the purchase or refinance of a home plus renovation or construction costs in a single conventional mortgage, and it can fund ADU work — including detached and manufactured ADUs — when the unit meets real-property and local code requirements. Renovation costs are generally capped at 75% of the as-completed appraised value (50% if the primary dwelling is a manufactured home).

For low-income borrowers, the key pairing is HomeReady, Fannie Mae’s affordable-lending program for borrowers at or below 80% of AMI, which allows a 3% down payment and reduced mortgage-insurance costs. Separately, since the Desktop Underwriter 12.1 release the weekend of March 21, 2026, Fannie Mae automates the treatment of ADU income in eligible one-unit primary-residence purchase and limited-cash-out-refinance scenarios, including a check on whether ADU qualifying income exceeds 30% of total qualifying income. ADU rent can factor into qualifying — but only under specific rules, never automatically, and never as a blanket assumption for an unbuilt unit.

Freddie Mac CHOICERenovation + Home Possible

Freddie Mac’s CHOICERenovation loan lets borrowers add a new ADU or renovate an existing one within a conventional mortgage, provided the ADU is legally permissible, legal nonconforming, or fits Freddie’s stated exception framework. Paired with Home Possible (Freddie’s affordable program for borrowers at or below 80% AMI), it’s the Freddie-side equivalent of HomeStyle + HomeReady.

One watch-out we verified: for applications received on or after May 4, 2026, rental income from any unit included in the renovation project funded by mortgage proceeds cannot be used for qualifying — only rental income from units not included in the renovation project may be considered. If your qualification math leans on the new ADU’s rent, confirm the current rule with your lender first.

HUD Title I property improvement loans

HUD Title I insures lender loans for property improvements, capped at $25,000 for a single-family property — useful for smaller, ADU-adjacent scopes, but not the tool for six-figure detached ADU construction. Treat it as gap or repair funding.

Explore mortgage-backed ADU financing paths. Compare FHA 203(k), renovation, construction-to-permanent, and refinance options with a mortgage partner. Approval, terms, and loan fit depend on your income, credit, equity, property eligibility, project scope, and underwriting — we present lanes, not guarantees.

→ Explore mortgage-backed financing paths (Mortgage Research Center)

Can ADU rental income help you qualify for a loan?

Sometimes — but never assume the future rent from your ADU will count. FHA, Fannie Mae, Freddie Mac, and individual lenders each use different rules, caps, documentation standards, and ADU-type limitations, and several rules changed in 2026. For a low-income borrower, projected rent can be the difference between approval and denial, which is exactly why you need to get the rule right. Here’s how the three big programs handle it:

| Program | Existing ADU rent | New / projected ADU rent | Key limit |

|---|---|---|---|

| FHA Standard 203(k) | Treated under standard rental-income rules with documentation | When there’s no rental history, uses 50% of the lesser of appraiser-estimated market rent or the lease/rental agreement | Conservative by design |

| Fannie Mae (DU 12.1) | Documented existing rent considered | ADU income automated in eligible one-unit primary-residence purchase / limited-cash-out refi scenarios | Checks whether ADU income exceeds 30% of total qualifying income |

| Freddie Mac CHOICERenovation | Rent from units not in the renovation may count | For applications on/after May 4, 2026, rent from a unit funded by the renovation cannot be used to qualify | Renovation-funded unit rent excluded |

The practical takeaway for a low-income borrower: build your plan on the conservative number, not the optimistic one. Projected rent may stretch your qualifying income, but it doesn’t erase the underwriting, reserves, appraisal, permit, and documentation requirements. → Can ADU Rental Income Help You Qualify for a Mortgage?

What if you have little equity or a standard HELOC won’t work?

A standard HELOC or home equity loan underwrites against your home’s value today, so without substantial equity you’ll be told “no” — but that’s the wrong question. The right question is which future-value or local-program path can fund a project your current equity can’t. For low-income homeowners, equity and income are two separate blockers that need different solutions.

| Funding type | Value it uses | Problem it solves | Problem it doesn’t solve | Low-income risk |

|---|---|---|---|---|

| Current-value lending (HELOC, home equity loan, cash-out refi) | Today's appraised value | Quick access if you already have equity | Doesn't help if you have little/no equity | Often a dead end for thin-equity owners |

| Future-value lending (203(k), HomeStyle, CHOICERenovation, construction-to-perm) | As-completed value | Unlocks borrowing room you don't have yet | Doesn't fix limited repayment capacity | You can over-borrow into a payment you can't carry |

| Local-program funding (forgivable loans, subsidized loans, rebates) | Program rules, not equity | Below-market cost; sometimes 0–1% | Limited availability; covenant strings | Covenants can restrict rent and tenants for years |

This is a simplified illustration, not a valuation, approval estimate, or loan quote.

Here’s the math in one example: your home is worth $400,000, you owe $320,000, and an ADU will cost $180,000. A HELOC capped at 80% of current value leaves essentially nothing. But a renovation or construction loan that underwrites against an as-completed value of, say, $560,000 can lend against that higher number — unlocking room your current equity never could. That’s why “I don’t have equity” is rarely the end of the story.

When equity is the only blocker and your income can carry a payment, the no-equity playbook is its own topic. → How to Finance an ADU With No Equity

When low income — not equity — is the real constraint, future-value lending solves the equity problem, not the repayment problem. If you genuinely can’t carry another monthly payment, no appraisal trick fixes that. Your best moves are the local forgivable and subsidized programs (which often carry 0–1% rates — USDA Section 504 is 1% fixed, Vermont VHIP is 0% forgivable), repair programs that shrink the scope, or — if you’re 62+ — a no-monthly-payment senior equity path. Stretching into a construction loan you can’t service is how good intentions become foreclosures.

Before you compare loans, confirm your lot can support the ADU type a lender would finance. → Get your free ADU report

What if you’re 62 or older and need no required monthly payment?

For some homeowners 62 and older with significant equity, a reverse mortgage can solve a monthly cash-flow problem by converting equity to cash with no required monthly payment — but it is not free money. The loan balance grows over time, your home equity falls, and you must keep paying property taxes, homeowners insurance, and maintenance, and keep living in the home, or you can face foreclosure. It’s a serious tool for a narrow situation.

Should a HECM be on your list? A quick gut-check

| ✅ A HECM may fit if… | ⛔ A HECM probably doesn’t fit if… |

|---|---|

| You're 62+, have substantial equity, and plan to stay in the home long-term | You may move or sell within a few years |

| You can reliably keep taxes, insurance, and maintenance current | Keeping property charges current is already a stretch |

| You complete HUD-approved counseling and involve your heirs | A contractor or salesperson is pushing you toward it |

| The monthly-payment burden — not equity — is your only blocker | You don't fully understand how the growing balance affects your estate |

The risks, plainly: debt rises and equity falls as interest accrues; you still owe property charges, and falling behind can trigger foreclosure; and high-pressure sales are a red flag — the FTC and CFPB both warn about reverse-mortgage pressure tactics, especially when tied to a contractor’s pitch.

A safer sequence before considering a HECM: talk to a HUD-approved housing counselor first (required anyway); confirm your ADU is legally permittable; get a written construction scope and bid; compare local assistance programs first (a 0–1% forgivable loan beats spending equity); and involve heirs or a trusted advisor if the home is part of your estate plan. → Find a HUD-approved housing counselor

Which ADU grant claims should you ignore?

Ignore any ADU “grant” claim that promises guaranteed approval, asks for upfront money to “hold your spot,” says a closed program is secretly still available, or uses a non-government website as the only proof for a supposed government grant. Real government grants don’t charge you to apply and don’t get “unlocked” by middlemen.

The CalHFA scam warning, stated plainly: California’s CalHFA ADU Grant — the $40,000 program that drives most “ADU grant” searches — fully allocated its funding in December 2023. CalHFA’s own website warns that anyone claiming they can help you secure the ADU Grant is likely running a scam. If someone offers to “get you the California ADU grant” in 2026, that is the scam.

General government-grant scam signs, per the FTC and Grants.gov: a request to pay a fee to receive or “guarantee” a grant; a request for personal or financial information through social media or text; an official-sounding but fake agency name; or a promise of free government money you didn’t apply for.

Old city pages stay online after programs close. The Orange County (CA) Housing Finance Trust discontinued its Affordable ADU Loan Program by board vote on May 21, 2025 — but older references still surface in search. Always confirm a program’s current status with the administering agency, not a cached page or builder blog.

How do affordability covenants change the decision?

A forgivable ADU loan can be the cheapest money available, but “forgivable” almost always comes with strings: rent caps, tenant-income limits, annual reporting, resale or repayment triggers, and sometimes a ban on renting to family. Before you take below-market money, make sure you can live with the covenant for its full term — often 5 to 15 years. The savings are real; so are the obligations.

| Program example | Can you rent to family? | Tenant income limit | Rent cap | Repayment trigger |

|---|---|---|---|---|

| San Diego (SDHC) | No, during the 7-year covenant | Tenant ≤80% AMI | Per SDHC rent chart by bedroom size | Breaking affordability rules |

| Charlotte (closed) | Program-specific | Tenant ≤80% AMI | Studio FMR at 70% AMI | Non-compliance forfeits forgiveness ($10k/yr) |

| Vermont VHIP 2.0 | Program-specific | Fair-market-rent rules | Fair-market rent | Selling/non-compliance before forgiveness term |

| Orlando | Program-specific (62+ waiver) | Tenant ≤120% AMI | Per program | Failing the 12-of-24-month rental rule |

The decision framework is simple: if you intended to house an aging parent or adult child, a family-member restriction may be a dealbreaker — route to a market-rate lane instead. If you planned to rent at market rates, a rent cap changes your return math. If the covenant is purely a don’t-sell-early rule, it may cost you nothing. Match the covenant to your actual plan before you sign.

What documents should you gather before you call a program or lender?

Having your paperwork ready is the difference between a 20-minute call that moves you forward and three weeks of back-and-forth. Most programs and lenders ask for the same core documents. Pull these together before you reach out:

- Proof of income (recent pay stubs, two years of tax returns, or benefit award letters)

- Most recent mortgage statement and property-tax bill

- Proof of homeowners insurance

- Deed or title showing ownership

- Government-issued ID

- A rough site plan or property survey if you have one

- A contractor bid or cost estimate, if you’ve gotten one

- Existing architectural plans and permits, if any

- Your assumptions about ADU use (family housing vs. rental) and, if renting, rough rent

- A list of covenant questions: How long is the affordability period? Whose income is tested? Can I rent to family? What triggers repayment?

What should you do before you apply or pay for plans?

The safe order is feasibility first, program verification second, financing third, plans fourth. Paying for architectural drawings before you’ve confirmed your ADU is legal, your local program is open, and your financing lane is realistic is the most common way homeowners waste thousands. Drawings can’t fix a lot that can’t be permitted, and no lender finances a project that can’t get approved.

The 7-day low-income ADU financing action plan:

- Day 1 — Check address-level feasibility. Confirm your lot can legally support an ADU and which types (detached, attached, garage conversion, JADU).

- Day 2 — Find official local/state programs. Use the 10-minute verification method above. Confirm “open today.”

- Day 3 — Check your AMI and household-size eligibility. Look up your county’s AMI and where your household falls.

- Day 4 — Decide your goal. Family housing, rental income, or both? This determines whether covenants are acceptable.

- Day 5 — Pin down ADU type and scope. Garage and internal conversions are the cheapest paths and often the best fit for a Limited 203(k) or a small forgivable loan.

- Day 6 — Make the calls. Talk to the program administrator, a HUD counselor (if 62+), and a mortgage professional, checklist in hand.

- Day 7 — Choose the first lane to test and decide whether buying plans is justified yet.

Start with your address → Get your free ADU report. See likely ADU types, zoning flags, a rough cost range, and financing-path clues before you spend a dollar on design. The same report runs the Low-Income Financing Path Finder — returning your first lanes to test, your likely disqualifiers, covenant warnings, and a document checklist tailored to your situation.

Low-income ADU financing examples

These are illustrations of how the lanes fit different situations — not promises of approval or returns. The right path depends on local rules, construction cost, income, credit, equity, property condition, ADU type, and whether you accept affordability restrictions.

A San Diego homeowner under the SDHC income ceiling.

An income-eligible owner-occupant in the City of San Diego with a 700 credit score builds a detached ADU using the SDHC ADU Finance Program: a construction-to-permanent loan up to $250,000 at roughly 1% during construction, converting to a fixed permanent rate, with free technical assistance. The tradeoff is a 7-year covenant requiring the ADU be rented to tenants earning ≤80% AMI, with no renting to family. Right for a landlord-minded owner; wrong for someone hoping to house a relative.

A Vermont owner willing to rent at fair-market rent.

A Vermont homeowner uses VHIP 2.0’s 0% forgivable loan of up to $50,000, fronting costs on a reimbursement basis and providing a 20% match (some in-kind). On a modest conversion, that $50,000 can be a large share of the budget. In exchange, they accept fair-market-rent rules and a 5- or 10-year covenant — and if they honor the rules for the full term, the loan is never repaid.

A Massachusetts homeowner with plans and permits in hand.

A low/moderate-income Massachusetts owner who already has designs and permits uses the MassHousing ADU Loan — a fixed-rate second mortgage up to $250,000 detached / $150,000 attached, through a participating lender. Because this is construction financing that requires plans and permits up front, it works after the planning stage — which is exactly why feasibility and design come first in the 7-day plan.

A rural senior who needs health-and-safety repairs first.

A very-low-income rural homeowner aged 68 can’t fund a full ADU, but uses USDA Section 504 to fix a failing roof and electrical panel: a $40,000 loan at 1% over 20 years paired with a $10,000 grant (available because they’re 62+), up to $50,000 combined. This isn’t ADU construction — it’s the repair work that keeps the home safe and makes a future conversion possible.

Methodology: what we verified and how

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We built this page from official public-program pages, federal housing-finance guidance, and consumer-protection sources — not third-party summaries. Where we used forums or social posts, it was only to understand how homeowners describe the problem in their own words, never as proof of laws, loan terms, or program availability.

We separate three kinds of claims on purpose: verified program facts (amounts, statuses, income limits) are checked against the administering agency and dated; regulatory facts (FHA, Fannie, Freddie, USDA rules) are sourced to HUD Mortgagee Letters and agency guides; and editorial judgments (which lane may fit which homeowner) are presented as our conclusions based on those facts, not as guarantees.

Frequently asked questions

Are there ADU grants for low income homeowners?

Yes, but they're usually local, limited, and restricted. Many "grants" are actually forgivable loans, rebates, fee waivers, or technical-assistance programs rather than unrestricted cash. The largest verified municipal help we found is a construction loan up to $250,000 (San Diego and Massachusetts), not a cash grant.

Is the CalHFA ADU Grant still available?

No — and no page should tell you to plan around it. CalHFA's funding for the ADU Grant was fully allocated in December 2023, and CalHFA warns that anyone claiming they can help you get the grant is likely running a scam. Verify directly with CalHFA before budgeting any grant money.

Can an FHA 203(k) loan be used for an ADU?

Yes, in specific scenarios. HUD allows ADU-related improvements under the 203(k) program, including converting a one-family home into a one-family home with an ADU, attaching an ADU to an existing structure, and renovating an existing attached or detached ADU. The Limited 203(k) rehab cap rose to $75,000 for case numbers assigned on or after November 4, 2024.

What credit score and down payment do I need for an FHA 203(k)?

Generally a 580 credit score with 3.5% down, or 500–579 with 10% down, for an owner-occupied home. Some lenders set higher minimums (620–640). There is no maximum income limit on the FHA 203(k).

Can USDA Section 504 build a full ADU?

Usually no. Section 504 helps very-low-income rural homeowners repair, improve, or modernize a home or remove health-and-safety hazards. It caps at a $40,000 loan (1% fixed, 20-year term) plus up to a $10,000 grant for owners 62+ — far below typical full ADU construction costs.

Does a forgivable ADU loan mean free money?

Not automatically. Forgiveness typically depends on following affordability, rent, tenant-income, owner-occupancy, documentation, or time-period rules for the full covenant term (often 5–15 years). Break the rules and the loan can become repayable.

Can I rent the ADU to a family member if I use a city program?

Sometimes, but not always. San Diego's ADU Finance Program, for example, states the ADU cannot be rented to a family member during its 7-year covenant. Check each program's covenant before assuming you can house a relative.

Can ADU rental income help me qualify for the loan?

Sometimes, under specific rules. FHA's Standard 203(k) uses 50% of the lesser of appraiser-estimated market rent or the lease when there's no rental history. Fannie Mae automates some ADU rental-income treatment as of its March 21, 2026 Desktop Underwriter 12.1 release, and Freddie Mac limited certain CHOICERenovation-funded rent for applications on or after May 4, 2026. Confirm the current rule with your lender.

What if my city doesn't have an ADU program?

Test the federal and mortgage-backed lanes (FHA 203(k), HomeStyle/HomeReady, CHOICERenovation/Home Possible), check future-value financing if equity is your blocker, and confirm property feasibility before paying for plans.

Should I use a personal loan to build an ADU?

Usually only as gap funding or for a small scope. A personal loan as the sole source for a full ADU tends to create high monthly payments and underwriting stress.

What's the very first thing to check?

Whether your property can legally support the ADU type you want. No financing program fixes an ADU that can't be permitted, which is why feasibility comes before plans, lenders, and programs.

A final word before you start

Most low income homeowners won’t find a single grant that pays for an ADU. But many can still identify a realistic path if they start with feasibility, verify local assistance, understand the covenant tradeoffs, and choose the right financing lane before paying for plans. The market gap is real — but so are the homeowners building ADUs every month on modest incomes.

Not sure where to start? See what’s possible at your address — get your free ADU report in about a minute.

Get your free ADU report →