ADU Financing for Fixed-Income Homeowners: 9 Paths Ranked by Risk

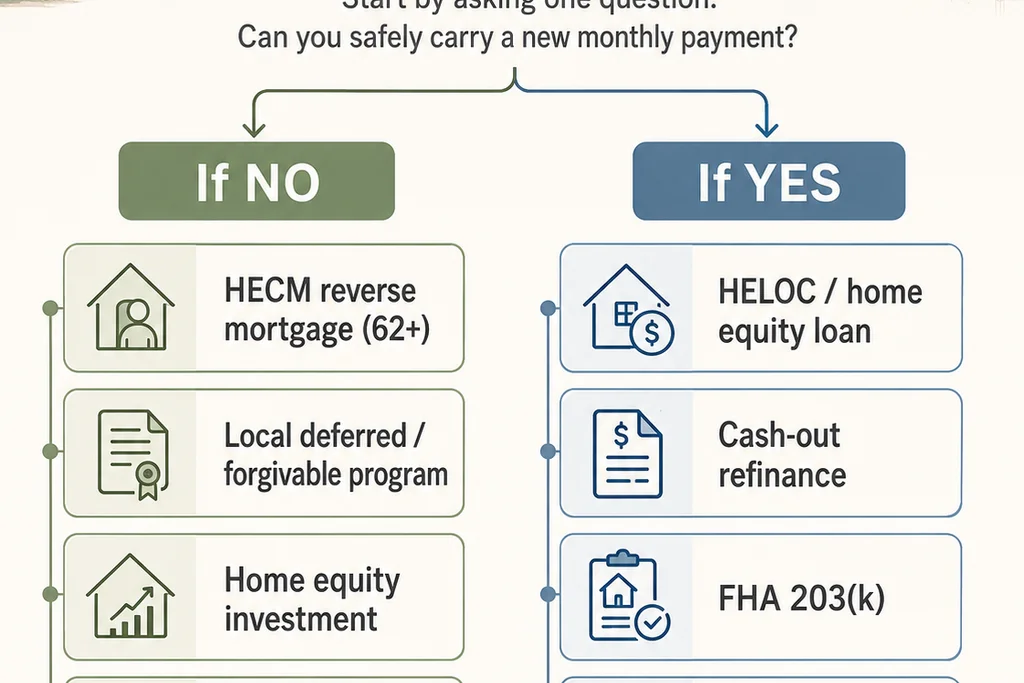

The short answer: ADU financing for fixed-income homeowners comes down to one question before any other — can you safely carry a new monthly payment? If the honest answer is no, start with the no-required-payment paths: a HECM reverse mortgage for eligible homeowners age 62 and older, a local deferred or forgivable program where one is funded, a home equity investment, or cash and family funding. If you can carry a payment, compare a HELOC, home equity loan, renovation loan, or cash-out refinance — but only after you confirm your lot can legally support the unit. The single most expensive mistake on a fixed income is choosing the path that approves the largest amount instead of the one that survives a cost overrun, a six-month vacancy, and a property-tax increase. Next step: confirm feasibility, stress-test the payment against zero rental income, then talk to a lender or counselor.

This page is for the homeowner who is “house-rich but cash-flow-constrained” — living on Social Security, a pension, disability, VA, or retirement-account income — and for the adult child researching on a parent's behalf. Almost every “ways to finance an ADU” article assumes you have a paycheck a lender will count. You may not. So we reorganized every major path around the constraint that actually matters to you: monthly-payment exposure and the risk to your home, your benefits, and your equity.

| Your situation | Test these paths first | Why |

|---|---|---|

| Can't add a monthly payment | HECM (62+), local deferred/forgivable program, home equity investment, cash/family | No required monthly payment — the exposure a fixed income can least afford |

| Can carry a safe payment | HELOC, home equity loan, renovation loan, cash-out refinance | Lower total cost when the payment survives a vacancy and a cost overrun |

| Need ADU rent to qualify | Verify FHA, Fannie Mae, and Freddie Mac caps before applying | Projected rent is capped and often unavailable for the exact loan you want |

See What You Can Build → Get Your Free ADU Report

Before you compare a single loan, see whether your lot can legally support the ADU you have in mind. It's the step that keeps a financing plan from collapsing later.

Get Your Free ADU Report →Free · No commitment

ADU Financing for Fixed-Income Homeowners: The Safety Matrix

Answer capsule: For a homeowner on a fixed income, ADU financing paths divide into two groups: those that require a new monthly payment (HELOC, home equity loan, cash-out refinance, FHA 203(k), conventional renovation loans) and those that don't (HECM reverse mortgage, certain local deferred or forgivable programs, home equity investments, and cash or family funding). No path is “free” — each shifts the cost somewhere, whether to your equity, your heirs, an affordability covenant, or your liquidity. The table below sorts every major path by the factors that decide whether it is safe for your situation.

This matrix is the asset we assembled that doesn't exist in this combined form anywhere else. To reproduce it, a homeowner would have to read HUD's Mortgagee Letter 2023-17, Fannie Mae's October 2025 Selling Guide announcement, Freddie Mac's CHOICERenovation guidance, the San Diego Housing Commission program page, and several lender disclosures — then build their own spreadsheet. We did that and dated every cell.

| Financing path | New monthly payment? | Income pressure | Equity needed? | Can projected ADU rent help you qualify? | Best fit | Pause or avoid if |

|---|---|---|---|---|---|---|

| HECM reverse mortgage | No required monthly mortgage payment (you must still pay property charges) | Lower monthly-payment pressure; lender still runs a HECM financial assessment and may require a set-aside for property charges | Yes — significant equity | ADU income may factor into the HECM financial assessment; case-specific | Age 62+, meaningful equity, plans to stay long-term, no room for a new payment | You may move soon, can't keep property charges current, have unresolved spouse/heir questions, or want to preserve equity |

| Local deferred / forgivable program | Often deferred, low-interest, or forgivable | Often income-limited | Sometimes | Usually not the core question; rent restrictions apply | Income-eligible owner in a city/county with active funding | You need market-rate rent, want to rent to family where prohibited, or can't meet the affordability covenant |

| HELOC / home equity loan | Yes (HELOC rate is usually variable) | High — payment must fit current income | Yes, based on current value | Generally no, for a not-yet-built ADU | Owner with strong equity, stable income, and a real payment buffer | A variable payment or DTI would strain your retirement budget |

| Cash-out refinance | Yes — replaces your existing mortgage | High | Yes | No for FHA cash-out (HUD prohibits ADU rent for qualifying income); limited for conventional | Owner without a low-rate first mortgage, whose full new payment is clearly affordable | You have a low first-mortgage rate worth keeping, or the payment only works with perfect rent |

| FHA 203(k) renovation loan | Yes | Moderate to high | Renovation/as-completed framework | Yes — 50% of the lesser of appraiser fair-market rent or lease for a new attached ADU, within the 30%-of-income cap | Attached additions, garage/basement conversions, renovating an existing ADU | You're building a detached ADU from scratch and need its projected rent to qualify |

| Fannie Mae HomeStyle / conventional renovation | Yes | Moderate to high | Renovation/as-completed framework | Only for an existing ADU on a one-unit principal residence, purchase or limited cash-out; one ADU; capped at 30% of qualifying income | Documented-income borrower with a renovation lender that supports ADUs | You assume rent from an ADU you're building will count, or the project fails lender overlays |

| Freddie Mac CHOICERenovation | Yes | Moderate to high | Renovation/as-completed framework | Limited; ADU must be legal or legal-nonconforming, and rent from units in the renovation project may be restricted | Borrower using a Freddie-eligible renovation path with a legal ADU scope | You need rent from the ADU being built to qualify and the rules don't allow it |

| Home equity investment (HEI) | Usually no required monthly loan payment | Lower monthly-payment pressure | Yes | Not typically about ADU rent; approval and state availability vary | Under-62 or payment-sensitive owner with equity who accepts the appreciation-share tradeoff | You may sell soon, dislike sharing appreciation, or the provider doesn't serve your state |

| Cash, family loan, or family contribution | No lender payment (a family agreement may create one) | Low lender pressure; high family/estate pressure | Not required if cash exists | Not applicable | Family housing need where relatives can document terms safely | An informal deal could create tax, estate, Medicaid/SSI, or family-conflict problems |

Verified May 24, 2026. Agency rules and program terms change; see “What we verified” for the refresh cadence.

Explore your options → Get your free ADU report

The matrix shows which paths fit which situations. To see which ones your specific address and property support, start with a free feasibility report.

Get Your Free ADU Report →Free · No commitment

Can you finance an ADU if you're retired or on a fixed income?

Answer capsule: Usually yes, but a fixed income does not remove the normal financing gates. Lenders and programs still evaluate documented income, equity, property eligibility, project documentation, credit, and existing debt. The safest first move is not to apply everywhere — it is to sort options by monthly-payment exposure and confirm the property can legally support an ADU before borrowing.

Here is the distinction that trips people up. Being retired does not disqualify you. Lenders routinely count Social Security, pension, annuity, VA, and documented retirement-account distributions as income. What disqualifies a plan is when the only way the numbers work is to assume the ADU rents instantly and forever. We've seen homeowners get approved for financing that wasn't safe — a payment that cleared underwriting in month one and then collided with a roof repair, an insurance hike, or a tenant who gave notice.

Can I get ADU financing on Social Security?

Answer capsule: Yes — Social Security, pensions, VA and disability benefits, annuities, and documented retirement-account distributions can all be used in a mortgage application. Many lenders can “gross up” non-taxable income such as Social Security, treating it as worth more than its face value because it isn't taxed. The deciding factor is whether the payment is safe without relying on unrealistic future rent, not the income source itself.

Gather these before you call a lender. A ready file is the single biggest thing that turns a “we're not sure” into a “yes,” and it tells you which paths fit before you spend an application fee:

| Income or asset type | Document usually requested | Continuance / notes |

|---|---|---|

| Social Security | Award letter, recent bank statements, SSA-1099 | May be grossed up; ask the lender |

| Pension | Pension statement, 1099-R, deposit history | Confirm whether it continues for at least 3 years |

| VA / disability income | Award letter, deposit history, benefit documentation | Often grossed up; document expected duration |

| Retirement-account withdrawals | Account statements, distribution history | Lender may require evidence of remaining assets |

| Existing rental income | Lease, tax returns, bank deposits | Documented per the lender's standard rental rules |

| Home equity | Mortgage statement, value estimate, property-tax bill | Drives LTV and available paths |

| ADU project | Contractor bid, plans, scope, permit status, feasibility report | Required for renovation/construction paths |

| Property carrying costs | Insurance, property taxes, HOA dues, utilities | The numbers your stress test runs against |

Ask the lender directly: “How will you document my income, and do you gross up non-taxable income?” The answer can change what you qualify for by hundreds of dollars a month.

The fixed-income problem isn't qualification — it's survivability

Answer capsule: For fixed-income homeowners, the biggest financial risk is not loan rejection. It is being approved for a path that only works if everything goes right — no cost overrun, no vacancy, no rate increase, no tax or insurance jump. The safe assumption is that the ADU produces no rent for the first six to twelve months and that costs run over.

This is why we lead with payment exposure instead of loan type. A homeowner with a paid-off house and $3,200 a month in combined Social Security and pension income can technically qualify for several loans. The question that matters is whether the payment still works in the month the water heater fails, the tenant moves out, and the county reassessment lands in the same envelope.

| Your concern | What to verify before you borrow |

|---|---|

| "Will my Social Security count?" | Ask how income is documented and whether it can be grossed up |

| "Can I use future ADU rent to qualify?" | Ask which program allows it, what percentage counts, and the cap |

| "Can I avoid a new monthly payment?" | Compare HECM, HEI, deferred local programs, and cash/family |

| "Will I lose my low mortgage rate?" | Don't start with a cash-out refinance unless the full new payment is clearly safe |

| "Will this affect my benefits?" | Talk to a benefits, tax, or elder-law professional before counting rent or transferring ownership |

Not sure whether your real obstacle is income, equity, or property eligibility? Read: ADU financing qualification gates →

What's the safest ADU financing path if you can't afford another monthly payment?

Answer capsule: If a new monthly payment would strain a retirement budget, start with no-required-payment or deferred-payment paths rather than a HELOC or cash-out refinance. The main options are a HECM reverse mortgage for eligible homeowners 62 and older, a local deferred or forgivable program, a home equity investment, and cash or family funding. None is free — each shifts the cost to equity, future appreciation, an affordability restriction, or liquidity.

We'll be blunt: the HELOC is the path most often recommended online and the path most often wrong for a fixed income, precisely because it demands a monthly payment — usually at a variable rate. If carrying a new payment is the thing keeping you up at night, the no-payment group is where you should look first, and there's real relief in seeing that two or three legitimate paths never touch your monthly budget.

Each no-payment path trades the monthly payment for a different obligation:

| No-required-payment path | Monthly payment? | The hidden cost | Best next step |

|---|---|---|---|

| HECM reverse mortgage | None required | Property charges, occupancy rules, reduced heir equity | HUD-approved HECM counseling |

| Local deferred / forgivable program | Usually deferred or limited | Income caps, rent caps, funding limits | Check your city/county program |

| Home equity investment | Usually none | A share of future appreciation; payoff at sale/refinance | Verify state availability and payoff scenarios |

| Cash / family | None to a lender | Liquidity, taxes, family conflict | Written agreement + advisor review |

Check your property first → Get your free ADU report

A no-payment path still depends on the ADU being legal and buildable on your lot. Confirm feasibility before you choose one.

Get Your Free ADU Report →Free · No commitment

Does a reverse mortgage make sense for ADU construction?

Answer capsule: A HECM reverse mortgage can make sense for an ADU when the homeowner is 62 or older, has substantial equity, plans to stay in the home, can keep property charges current, and needs to avoid a required monthly payment. It is a poor fit when the homeowner may move soon, needs to preserve equity for heirs or future care, or cannot reliably keep up with property charges. HUD-approved counseling is required before a HECM can be originated.

The HECM is the path most likely to fit the literal fixed-income homeowner, because it is the one that doesn't ask for monthly payments and has no minimum credit score. The only reverse mortgage insured by the U.S. federal government is the Home Equity Conversion Mortgage, available through FHA-approved lenders, and borrowers may stay in their homes as long as they keep property taxes and homeowner's insurance current.

A practical pattern worth knowing: a homeowner 62 or older can take a HECM and use the proceeds to build an ADU — frequently for a family member. If your plan is to move into the ADU yourself and rent the main house, verify the occupancy treatment with a HUD-approved counselor and lender before relying on HECM proceeds — the principal-residence rules are specific.

How a HECM helps a fixed-income ADU borrower

- No required monthly mortgage payment, which protects monthly cash flow

- Proceeds are loan proceeds, not income — and the IRS treats reverse-mortgage payments as nontaxable loan advances, not taxable income

- You keep the title and ownership of your home

- It is a nonrecourse loan, so you or your heirs are never required to repay more than the home is worth when the loan comes due

HECM red flags — pause before you proceed if any of these are true

We won't soften this. The U.S. Government Accountability Office, reviewing the program, described it as relatively complex and costly for a population that is often vulnerable — which is exactly why the counseling step below exists. Pause if:

- You may move or need assisted living within a few years — the loan becomes due and payable when the last borrower permanently leaves the home

- You cannot reliably keep property charges current — these include property taxes, hazard insurance, flood insurance where applicable, HOA/condo/PUD fees, ground rents, and special assessments, and missing them can trigger default

- A spouse, co-owner, or heirs are not aligned on the plan

- You want to preserve home equity as an inheritance or for future care

- The ADU plan isn't yet permitted or financially feasible

- You receive needs-based benefits such as SSI or Medicaid — proceeds you hold rather than spend can affect eligibility, so confirm with a benefits or elder-law professional before you draw funds

The counseling step that protects you

Answer capsule: Before a HECM application can be funded, federal rules require every borrower — and certain non-borrowing spouses — to complete a session with a HUD-approved counselor. The counselor is an independent educator, not a lender. Counseling may be free, reduced-fee, or fee-waived based on hardship, though HUD permits agencies to charge a reasonable and customary fee.

This is the most valuable, least-marketed step in the process. The HECM statute requires counseling, and spouses participate even if they won't be on the mortgage. HUD-approved counselors don't represent lenders — their role is to serve the homeowner. Bring these questions:

- How much could I actually access, given my age and home value?

- What happens if construction costs run over the proceeds?

- Exactly which property charges must I keep paying?

- What happens to my spouse or heirs if I move into care or pass away?

- Can ADU rental income be considered in my financial assessment?

- What happens if the ADU can't be permitted after I've borrowed?

Find a HUD-approved HECM counselor →

Counseling is required before a reverse mortgage, the counselor works for you (not a lender), and it may be free or reduced-fee based on hardship. Talk to one before treating a HECM as ADU financing.

Find a HUD-Approved HECM Counselor →Can projected ADU rental income help you qualify?

Answer capsule: Sometimes — but this is where many ADU financing articles become misleading. Projected ADU rent is capped, limited to specific transaction types, or unavailable for the exact loan many homeowners want. Under current federal rules, FHA allows 75% of the lesser of appraiser fair-market rent or the lease for an existing ADU (capped at 30% of effective income, with two months' PITI reserves), 50% for a new attached ADU built via a 203(k), and none for an FHA cash-out refinance. Fannie Mae allows rent only from an existing ADU on a one-unit principal residence for purchase or limited cash-out, one ADU, capped at 30% of qualifying income.

Do not assume a lender will count 100% of your future rent. The rules are specific and recent, and getting them right is what separates a reliable page from a guess. Here is what we verified directly against the agencies' own documents:

| Program / path | ADU rent treatment (verified) | Practical meaning |

|---|---|---|

| FHA — existing ADU, no rental history | 75% of the lesser of appraiser fair-market rent or the lease; capped at 30% of total monthly effective income; two months' PITI reserves required | Helpful, but bounded — and it's for an ADU that already exists |

| FHA — new attached ADU via Standard 203(k) | 50% of the lesser of fair-market rent or lease | Helps attached additions, garage/basement conversions, and renovations of existing attached or unattached ADUs — not projected rent on a new detached build |

| FHA — cash-out refinance | ADU rental income may not be used for qualifying income | Don't count on ADU rent to make a cash-out work |

| Fannie Mae (SEL-2025-08) | Existing ADU only; one-unit principal residence; purchase or limited cash-out; one ADU; capped at 30% of total qualifying income | Don't assume rent from an ADU you're building with HomeStyle can qualify |

| Freddie Mac CHOICERenovation | ADU must be legal or legal-nonconforming; rent from units in the renovation project may be limited | Don't assume projected rent from the unit you're building will count |

| HELOC / home equity loan | Lender-specific; usually based on current income and equity | Future rent generally won't solve a current DTI problem |

| HECM | ADU income can factor into the financial assessment under HUD's ADU policy | Requires counselor and lender verification |

The federal facts behind that table, from the agencies directly: FHA's Mortgagee Letter 2023-17 allows projected ADU rental income for qualifying, caps it at 30% of total monthly effective income, requires two months' PITI in reserves, and makes ADU rent ineligible for cash-out refinances. On the conventional side, Fannie Mae's Selling Guide Announcement SEL-2025-08 permits ADU rental income only when the property is a one-unit principal residence, the transaction is a purchase or limited cash-out refinance, the income comes from a single existing ADU, and the amount used does not exceed 30% of total qualifying income. The change takes full effect in automated underwriting with the Desktop Underwriter version 12.1 release over the weekend of March 21, 2026.

The safe assumption. Plan as if the ADU produces zero rent for the first six to twelve months after financing starts. If the loan only works with immediate, full-market rent, it is not fixed-income safe. These are illustrative rules, not guarantees. Actual qualification depends on local market conditions, construction costs, financing terms, lender overlays, and regulatory approvals.

Should you use a HELOC, home equity loan, or cash-out refinance on a fixed income?

Answer capsule: A HELOC or home equity loan can preserve your existing mortgage but adds a new monthly payment that's harder to carry on a fixed income, often at a variable rate. A cash-out refinance consolidates the debt into one mortgage but can replace a low first-mortgage rate and raise your entire housing payment. For fixed-income homeowners, the best option is the one that survives a vacancy, a cost overrun, and a tax or insurance increase — not the one with the largest approval.

The Urban Institute, in its research on why ADU financing is hard, notes that many existing channels are constrained by current home value and that a cash-out refinance may force borrowers to give up a below-market first mortgage rate. The math is concrete: as of May 21, 2026, Freddie Mac's Primary Mortgage Market Survey put the 30-year fixed-rate average at 6.51%. If you locked a 3% mortgage years ago, refinancing your whole balance to fund an ADU can cost far more in added interest on the existing debt than the ADU itself.

A HELOC or home equity loan may fit when: your existing low rate is worth preserving, the new payment is safe without counting ADU rent, your equity is strong, you understand the rate structure, and the project has a contingency reserve.

A cash-out refinance may fit when: your existing mortgage rate isn't worth keeping, the full new payment is clearly affordable, you want a single payment, the ADU cost is well documented, and the appraisal supports the loan.

The fixed-income stress test

Run your plan through every row. If it fails any of them, shrink the scope or change the path:

| Stress test | Pass standard |

|---|---|

| 10–20% construction overrun | You still have reserves or can reduce scope |

| Six months of zero ADU rent | The payment is still safe |

| Higher insurance and property taxes | Housing costs remain manageable |

| Unexpected utility-lateral or site-work cost | A contingency covers it |

| Family occupies the ADU rent-free | The financing still works |

| Appraisal comes in low | You have a backup plan |

Explore mortgage-backed ADU financing paths with Mortgage Research Center →

If you have income a lender can document and the stress test passes, comparing HELOC, cash-out refinance, renovation, and construction-loan paths is a smart next step. Compare the path, not promised rates — and ask how your fixed income and any ADU rent would be documented. This won't fit homeowners with no qualifying income; if that's you, go back to the no-payment paths above.

Compare Mortgage-Backed Paths with MRC →What if you have equity but your income is too low for a traditional ADU loan?

Answer capsule: If you have equity but not enough qualifying income to safely carry a loan payment, your realistic paths narrow: a HECM if you're 62 or older, a local deferred or forgivable program if one is funded near you, a home equity investment where available, cash or family funding, or simply a smaller, lower-cost ADU such as a garage conversion. Check them in order of safety, not size.

The order we'd check them in:

- Is the property even ADU-feasible? Confirm before anything else.

- Is there a local deferred or forgivable program you qualify for?

- Are you 62+ and willing to sit through HECM counseling to see the numbers?

- Is a no-payment home equity investment available in your state?

- Can the project be reduced to a lower-cost conversion — garage, basement, attached — instead of a detached new build?

- Is family funding possible with written, advisor-reviewed terms?

- If none of those work, pause. Not borrowing yet is a valid, often wise, outcome.

On home equity investments specifically: the no-monthly-payment feature is genuinely attractive for a payment-sensitive owner, but it is not free money. You're selling a share of your home's future value, the eventual buyout can be costly, and these products are typically capped around current market value — which can leave a gap for an ADU whose value won't be realized until it's built. Treat an HEI as a real option to compare, not a default, and verify the provider serves your state before you spend time on an application.

If your real obstacle is equity rather than income, read: ADU financing with no equity →

Are there ADU grants, deferred loans, or forgivable programs for fixed-income homeowners?

Answer capsule: Yes, but they are local, limited, and rule-heavy. Fixed-income homeowners should check for local ADU funding early, because these programs can dramatically reduce monthly-payment risk — but they typically carry income limits, owner-occupancy requirements, affordability covenants, rent caps, construction deadlines, contractor requirements, and restrictions on renting to family. Funding also runs out, so status matters as much as terms.

We assembled a sampler of real programs across the country so you can see the shape of what exists and the questions to ask your own city and county. Read the status column as carefully as the terms — a generous program with no open funding is a historical example, not a path.

| Program | What it offers | Key restrictions | Status (as of May 24, 2026) |

|---|---|---|---|

| San Diego Housing Commission ADU Finance Program City of San Diego | Construction loan up to $250,000; 1% fixed during construction, converting to a 4% fixed, 15-year permanent loan (term due in 30); up to 75% LTV; free technical assistance | Homeowner income up to ~150% of AMI (~$236,600); owner-occupied detached single-family home in the City of San Diego; 680 minimum credit score; $2,500 application fee at construction-loan closing; the tenant's rent must stay affordable to households at 80% of AMI for 7 years; no renting to family during that period | Income-eligible only; confirm current funding round directly with SDHC |

| NYC Plus One ADU | Up to $395,000 in financial support plus technical assistance and pre-approved designs; established with city funding and NY State HCR grants, operated with Restored Homes HDFC | Owner-occupancy, income and property rules; application does not guarantee acceptance | Active program; verify intake before relying on it |

| MassHousing ADU Loan Program | Up to $250,000 for detached ADUs / $150,000 for attached ADUs, combining an amortizing interest-bearing loan with additional zero-interest, deferred-repayment financing | Income-eligible homeowners; plans, permits, and pre-development materials must be ready before applying | Active; lender and program criteria apply |

| CalHFA ADU Grant California | Previously reimbursed up to $40,000 in predevelopment costs (design, permits, soft costs) | Income-limited (last phase ≤80% AMI for the borrower) | Paused — latest funding fully allocated as of Dec. 28, 2023. Historical example only unless CalHFA announces new funding. |

| Habitat Monterey Bay “My House My Home” Santa Cruz, CA | Partnership helping senior homeowners build or renovate an ADU | Senior-, income-, and locality-targeted | Confirm intake status with Habitat Monterey Bay before treating it as currently available |

Sources: SDHC; NYC Mayor's Office; MassHousing; CalHFA; Habitat Monterey Bay. Verified May 24, 2026.

Where to check for local ADU funding in your area

Answer capsule: Most ADU grants and deferred loans are run at the city, county, or state level, so the fastest way to find money you qualify for is to check five places: your city housing or planning department, your county housing agency, your state housing finance agency, local housing nonprofits, and a HUD-approved housing counseling agency. Programs open and close on annual funding cycles, so confirm current status before you build a plan around one.

| Where to check | What you're looking for |

|---|---|

| City housing / planning department | ADU loan or grant programs, fee waivers, pre-approved plans |

| County housing agency | County forgivable or deferred ADU loans (e.g., Napa-style programs) |

| State housing finance agency / HCD | Statewide ADU grants, second-mortgage programs, predevelopment grants |

| Local housing nonprofits | Gap financing, senior-specific ADU help, application assistance |

| HUD-approved housing counseling agency | Free or low-cost guidance on programs and financing fit |

Local-program red flags

Before you build a plan around a program, confirm: funding may already be exhausted; income limits may disqualify you in either direction; you may not be able to charge market rent; you may not be able to rent to family; you may have to keep the unit affordable for 7, 10, or 15 years; you may need a licensed contractor and a hard completion deadline; and you may need clean property-tax, mortgage, and municipal-account status.

See if your ADU plan is program-ready → Get your free ADU report

Local programs usually require a real, buildable project scope — not just interest. Start by confirming what your property can support.

Get Your Free ADU Report →Free · No commitment

If you're building for — or as — an aging parent

Answer capsule: Two common fixed-income patterns involve family. In the first, a homeowner 62 or older builds an ADU (often funded with a HECM or cash) so an aging parent or adult child can live close. In the second, an adult child co-signs or contributes because the parent's income alone won't qualify. Both can work, but family money and shared ownership create tax, estate, and benefits questions that a written agreement and professional review should resolve before construction.

This is where the “fixed income” search often really comes from — not a rental-income play, but a caregiving need. A daughter pricing a backyard cottage for her mother. A retired couple wanting their son nearby. When no rent is involved, every “the rent will cover it” assumption disappears, and the plan must work on the household's actual income alone. The table below maps who to consult for each family arrangement so the financing doesn't quietly create a tax or benefits problem:

| Family arrangement | Main risk to resolve | Who to consult first |

|---|---|---|

| Parent owns home, parent borrows | Payment fit on fixed income; HECM property charges | Lender or HUD-approved HECM counselor |

| Adult child co-borrows | Child's name and credit on the debt and title | Lender + estate/tax professional |

| Adult child gifts funds | Gift-tax reporting; effect on the parent's benefits | Tax or elder-law professional |

| Adult child loans funds | Documentation, interest, repayment terms | Tax professional; written agreement |

| 62+ owner uses HECM for family unit | Occupancy rules; reduced heir equity | HUD-approved HECM counselor |

| Rent-free family occupancy | No rent to offset cost; benefits interaction | Benefits or elder-law professional |

Building specifically for a parent or family member? Read: financing an ADU for aging parents →

What can go wrong if you build an ADU on a fixed income?

Answer capsule: The most damaging fixed-income ADU mistakes are borrowing before confirming the ADU is legal on the lot, assuming future rent will cover everything, choosing a loan that strains monthly cash flow, ignoring property taxes, insurance, and benefit effects, and failing to budget for cost overruns. For a fixed-income household, a construction contingency reserve is not optional — it is the line between a home improvement and a retirement-risk event.

Different paths fail in different ways. The red flag that should stop you depends on which path you're on:

| Path | The red flag that should make you pause |

|---|---|

| HECM reverse mortgage | You can't reliably keep property charges current, or you may move within a few years |

| HELOC | The variable payment strains the budget the moment rates or balances rise |

| Cash-out refinance | You'd surrender a low first-mortgage rate to fund the build |

| FHA 203(k) | You're counting on projected rent from a new detached ADU (not allowed) |

| Local program | Funding is closed, or the affordability/family-rental rules don't fit your plan |

| Home equity investment | You may sell soon, or the appreciation share costs more than expected at payoff |

| Family funding | The arrangement is informal and could trigger tax, estate, or benefits problems |

The do-not-proceed checklist

Pause before financing if any of these is true: you can't afford the payment without ADU rent; you don't know whether the ADU is legal on your property; you haven't checked utility-lateral and site-work costs; you have no construction contingency; you're relying on a program that isn't currently funded; you haven't confirmed whether family rental is allowed under your program; you're considering a HECM but can't keep property charges current; you're tapping retirement funds without tax advice; you receive SSI, Medicaid, VA, or property-tax relief and haven't asked how rent or ownership changes could affect them; or your spouse, co-owner, or heirs aren't aligned.

The safety-reserve principle

We won't hand you a universal dollar figure — that would be a number without a methodology, and on a fixed income a wrong number is worse than none. The principle: set a contingency reserve with your contractor and lender before you commit, sized to your specific scope, and treat it as untouchable. ADU budgets move when the lot reveals a utility surprise, when permitting adds a requirement, or when material costs shift mid-build. On a paycheck you can absorb that. On a fixed income, the reserve is the absorption.

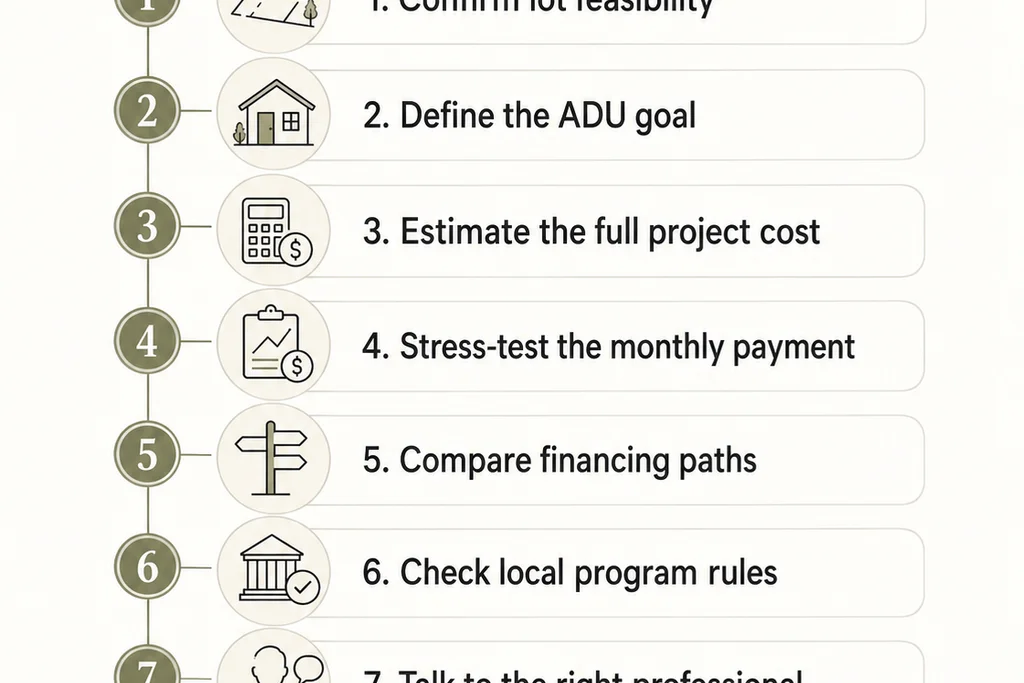

How to choose your ADU financing path in 7 days

Answer capsule: Don't start with lender shopping. Start by proving the project can legally exist, then test whether the financing survives your real monthly budget with zero rent, then match the path to the right professional. A feasibility check and a cash-flow stress test — both free — come before any loan application.

Day 1 — Check property feasibility. Confirm zoning, the ADU type your lot allows, setbacks (the minimum distance a structure must sit from property lines), parking rules, utility access, HOA limits, and any owner-occupancy requirement. Definitions: a DADU is a detached ADU — a standalone backyard unit; a JADU, or junior ADU, is a small unit (often up to 500 sq ft) carved out of the existing home; ministerial approval means the city must approve a compliant application without discretionary review — faster and more predictable.

Day 2 — Define the ADU's purpose. Rental income, family housing, caregiving, downsizing into the ADU, aging in place, or property value. This decides whether rent is even part of the math.

Day 3 — Estimate scope. Garage conversion, attached ADU, detached ADU, or prefab/modular; plus utility work, design, and permitting. Conversions are usually the lowest-cost path.

Day 4 — Calculate payment tolerance. The payment you can carry with zero ADU rent, plus property taxes, insurance, reserves, and maintenance.

Day 5 — Sort the financing paths. Use the safety matrix at the top of this page: no-payment paths, mortgage-backed paths, local programs, family/cash, or reduced scope.

Day 6 — Talk to the right professional:

| Path | Who to talk to |

|---|---|

| HECM reverse mortgage | HUD-approved HECM counselor (required) |

| HELOC / cash-out / renovation loan | Mortgage or lending professional |

| Local ADU program | City/county housing agency |

| Home equity investment | Provider + an independent advisor |

| Benefits / tax / estate questions | Tax, estate, elder-law, or benefits professional |

| Construction feasibility | ADU designer, builder, or feasibility service |

Day 7 — Choose one next step. Get a feasibility report, call a local program, book a counselor, compare mortgage-backed options, reduce scope, or pause. One step is enough.

Start with the property check → Get your free ADU report

Day 1 of the plan is feasibility. Do it now, free, and every decision after it gets easier.

Get Your Free ADU Report →Free · No commitment

What we verified

What we verified on

- HUD HECM basics, counseling, and property-charge obligations — HUD.gov HECM page; HUD Handbook 7610.1 (counseling fees and certificate language); 24 CFR Part 206 (financial assessment, set-asides, property-charge definition); Congressional Research Service report R44128 (counseling mandate)

- FHA ADU rental-income rules — FHA Mortgagee Letter 2023-17 (HUD.gov): 75% existing / 50% new attached via 203(k) / 30% effective-income cap / cash-out prohibition / two months' PITI reserves

- Fannie Mae ADU income rules — Selling Guide Announcement SEL-2025-08 (existing ADU, one-unit principal residence, purchase or limited cash-out, one ADU, 30% cap, DU 12.1 effective the weekend of March 21, 2026; property-management-experience PITIA limit)

- Reverse-mortgage tax treatment — IRS guidance for senior taxpayers (reverse-mortgage payments are nontaxable loan proceeds)

- Mortgage-rate context — Freddie Mac Primary Mortgage Market Survey, 30-year fixed average 6.51% as of May 21, 2026

- Local program terms — San Diego Housing Commission; NYC Mayor's Office (Plus One); MassHousing; CalHFA (funding fully allocated Dec. 28, 2023); Habitat Monterey Bay

- Financing-barrier context — Urban Institute ADU financing research

What you still need to verify for your own property

- Your city's ADU rules, setbacks, utilities, and HOA restrictions

- Current loan pricing and your specific qualification

- Whether ADU rental income can be used for your transaction

- Whether a local program still has open funding

- Tax, SSI, Medicaid, VA, estate, and property-tax implications — confirm with a licensed professional

Refresh cadence: Agency rules (FHA, Fannie, Freddie, HUD) and local program status — quarterly; mortgage-rate references — weekly; HECM rules — quarterly.

Frequently asked questions

Can I finance an ADU if my only income is Social Security?

Possibly. Approval depends on documentation, existing debt, equity, property eligibility, and loan type, and many lenders can "gross up" non-taxable Social Security income. Don't assume Social Security disqualifies you — and don't assume it makes a new monthly payment safe. If a payment is the worry, look first at no-payment paths like a HECM (if you're 62+) or a local deferred program.

Is a reverse mortgage the best ADU financing option for seniors?

Not automatically. A HECM can eliminate a required monthly mortgage payment, which is its biggest advantage on a fixed income, but it creates property-charge obligations and reduces the equity you leave behind. Federal rules require HUD-approved counseling before one can be originated — use it.

Can I use future ADU rent to qualify for a loan?

Sometimes, but usually not 100%. FHA allows 75% of the lesser of appraiser fair-market rent or lease for an existing ADU and 50% for a new attached ADU via a 203(k), both within a 30%-of-income cap, and none for an FHA cash-out refinance. Fannie Mae allows it only for an existing ADU on a one-unit principal residence in a purchase or limited cash-out, capped at 30% of qualifying income.

What's the safest ADU financing option on a fixed income?

The one that works without perfect rental income, protects your monthly cash flow, and matches your property. For some homeowners that's a local program or a HECM; for others it's a smaller ADU, a family arrangement, or waiting until the finances or rules change.

Are there ADU grants for seniors?

Some local programs help low- and moderate-income homeowners, and a few — like Habitat Monterey Bay's "My House My Home" in California — target seniors specifically. They're not universal and usually carry income limits, rent restrictions, and funding caps, so confirm current status before relying on one.

Should I use a HELOC for an ADU if I'm retired?

Only if the payment is safe without ADU rent, you understand the rate risk (HELOC rates are usually variable), and the project has a contingency reserve. A required monthly payment is exactly the exposure a fixed income can least afford, which is why we don't treat the HELOC as the default here.

Should I use retirement savings to build an ADU?

Treat retirement funds as a last resort unless a tax professional and financial advisor have reviewed the liquidity, tax, and long-term-care implications. Borrowing from a retirement account to fund construction is one of the higher-risk moves on a fixed income.

Can I rent the ADU to family if I use a local program?

Sometimes yes, sometimes no. The San Diego Housing Commission program, for example, prohibits renting to a family member during its seven-year affordability period. Always check the specific program's rules before you assume.

Will an ADU affect SSI, Medicaid, VA benefits, or property-tax relief?

It can, depending on the benefit, your ownership structure, the rental income, and your state and local rules. This page cannot give legal or benefits advice — verify with a benefits or elder-law professional before you borrow or rent.

What if my property can't support an ADU?

Don't force the financing. Consider a smaller conversion, a different housing plan, an internal remodel, a family-care alternative, or waiting until rules or finances change. Confirming feasibility first is what prevents a wasted loan application.

Download the Free ADU Starter Kit

Get the fixed-income checklist: documents to gather, questions to ask a lender, the HECM counselor question list, and the local-program red flags — in one PDF.

Download the Free ADU Starter Kit →Free PDF · No commitment

How we researched this guide

Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We built this guide from primary and authoritative sources, not by rewriting other blogs.

Our sources: federal housing and mortgage rules from HUD (HECM program pages, Handbook 7610.1, 24 CFR Part 206), FHA (Mortgagee Letter 2023-17), Fannie Mae (Selling Guide Announcement SEL-2025-08), Freddie Mac, the IRS, and the Congressional Research Service; consumer-protection context from the U.S. Government Accountability Office; mortgage-rate data from Freddie Mac's Primary Mortgage Market Survey; local ADU funding program pages from city, county, and state housing agencies (San Diego Housing Commission, NYC Mayor's Office, MassHousing, CalHFA, Habitat Monterey Bay); and financing-barrier research from the Urban Institute.

Our editorial standard: We do not rank financing paths by commission. We sort them by fit, risk, verification burden, and fixed-income cash-flow exposure. We never promise approval, rates, or rental returns. Rental-income examples are illustrative, not guarantees of returns; actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Not sure where to start? See what's possible at your address — get your free ADU report in 60 seconds.

Get Your Free ADU Report →