Salt Lake City ADU Loan Program (Backyard Keys): Who Qualifies, the Real 2026 Terms, and How to Apply

By the Dwelling Index Editorial Team · Last updated: May 27, 2026 · Last verified: May 27, 2026 · ~18 min read

Published May 27, 2026 · Last verified against CRA, CDCU, and SLC code: May 27, 2026

The Short Answer

The Salt Lake City ADU loan program — branded Backyard Keys — is a city-funded, nonprofit-administered construction loan offering up to $200,000 at a 3% fixed rate to owner-occupants whose property sits west of Interstate 15 inside Salt Lake City limits. It's administered by the Community Development Corporation of Utah (CDCU) for Salt Lake City's Community Reinvestment Agency (CRA), funded at $2,913,215 — enough for an estimated 15 to 20 ADUs — and the adopted term sheet directs CDCU to make reasonable efforts to disperse the funds by June 30, 2027, after which undistributed money reverts to the CRA.

If your property is east of I-15, or you can't live on the property, you don't qualify — jump to the financing paths that work citywide. And read the forgiveness section carefully: the city's two official pages don't agree on whether any of this loan is forgivable. (Sources: cra.slc.gov; cdcutah.org; Building Salt Lake. Verified May 27, 2026.)

🔎 The Dwelling Index ADU Loan Fit Check

Before you pay for a single drawing or builder bid, run your address, income band, and ADU type through our free SLC ADU Loan Fit Check. In about 60 seconds it tells you (1) whether your parcel falls on the eligible side of I-15, (2) which rent lane your household income puts you in, and (3) whether $200,000 is likely to cover your build type — or leave a funding gap to plan around.

Check your property, income lane, and funding gap before you spend money on plans or bids.

Fast eligibility check: is Backyard Keys worth your time?

Most people who land here want one thing first: a fast yes-or-no read on whether this program is even in play for them. Here it is, before anything else.

| Question | Fast answer | What to do |

|---|---|---|

| Is it real? | Yes. It's an official Salt Lake City CRA program administered by the nonprofit CDCU. | Verify current funding before you plan around it. |

| How much can I borrow? | Up to $200,000 per property. | Compare your full project budget to the cap. |

| Where does my property have to be? | West of I-15, inside Salt Lake City limits. The 9-Line area gets funding priority. | Confirm which side of I-15 your parcel is on. |

| Do I have to live there? | Yes — owner-occupancy is required. | Confirm the property is your primary residence. |

| What's the rate? | 3% fixed, under the published program terms. | Strong for construction money, but tied to this program only. |

| What's the term? | 5 years, with a 5-year extension option — amortized over 30 years. | Ask CDCU what happens at the end of the term. |

| Are there rent restrictions? | Depends on income. At or below 80% AMI: none. Above 80% AMI: you must rent one unit affordably. | Find your AMI lane below. |

| Is any of it forgivable? | The city's two official pages disagree. The CRA page lists up to 10%; CDCU's page lists no forgiveness. | Don't budget around it — see the conflict table below. |

| Best first step? | Confirm address, income lane, and budget fit. | Use the Fit Check, then join the CDCU interest list. |

(Sources: cra.slc.gov ADU Loan Program page; cdcutah.org ADU financing page; Building Salt Lake, March 2025. Verified May 27, 2026.)

Here's the honest framing we owe you up front, because no builder landing page will give it to you. Based on the published $200,000 cap, the 3% fixed rate, and the public-program structure, this is — in our editorial judgment — one of the most favorable ways to finance an ADU available to qualifying Salt Lake City homeowners right now. But it is not a set-and-forget 30-year mortgage. The five-year term, the affordability compliance, the owner-occupancy rule, the limited funding pool, the energy-design requirement on detached units, and an unresolved conflict over forgiveness all matter more than the headline 3% rate. None of those are dealbreakers for the right homeowner. They're just the parts the headlines skip — and the parts that decide whether this loan actually fits your situation. We'll walk through every one.

Is the Salt Lake City ADU loan program real and open in 2026?

Answer capsule. Yes. The Salt Lake City ADU loan program, branded Backyard Keys, is an official program of the city's Community Reinvestment Agency, administered by the Community Development Corporation of Utah and its affiliate, the Utah Community Investment Fund. The adopted term sheet allocates $2,913,215 for ADU construction loans west of I-15 — enough to finance an estimated 15 to 20 ADUs — with funds to be dispersed by mid-2027. Applications are accepted on a rolling basis as funding allows.

Let's define the players, because “city-backed loan” gets thrown around loosely and the structure here actually matters for trust.

The Community Reinvestment Agency (CRA) is Salt Lake City's redevelopment arm — the entity that captures a slice of property-tax growth in designated districts and reinvests it locally. The CRA funded this program. The Community Development Corporation of Utah (CDCU) is a long-standing local nonprofit that administers it — meaning CDCU is who you'll actually talk to, apply through, and sign documents with. CDCU's affiliate, the Utah Community Investment Fund, is the lending vehicle. Salt Lake City did not hand this to a bank or a builder; it routed it through a nonprofit with a housing-counseling mission. That's a meaningful signal if you're worried this is a sales funnel in disguise.

Why the program exists (and why the geography isn't random)

Salt Lake City studied what was actually stopping homeowners from building ADUs and found the bottleneck wasn't zoning — it was money. As CRA project manager Austin Taylor put it to the City Council, the city was trying to solve a market failure: the two normal ways to finance an ADU — a home-equity loan or a cash-out refinance — both depend on having enough equity, and many west-side homeowners simply don't have it. (Source: Building Salt Lake, July 2024.)

That's why the eligibility line is drawn at I-15. The funding originated from the 9-Line Community Reinvestment Area — a tax-increment district created in 2021 along the 900 South corridor between I-15 and the Jordan River, covering parts of the Poplar Grove and Glendale neighborhoods. Because the money came from the west side, it has to be spent on the west side.

How limited is the funding, really? The math, not the marketing.

| Funding fact | Figure | What it means for you |

|---|---|---|

| Total adopted allocation | $2,913,215 | A pilot-scale pool, not an open-ended citywide program. |

| Reserved for the 9-Line priority area | $1,913,215 | The larger share is set aside for 9-Line applicants. |

| Available elsewhere west of I-15 | $1,000,000 | The remainder, for the rest of the eligible west side. |

| Maximum loan per property | $200,000 | If everyone maxed out, the fund covers ~14–15 full loans. |

| Local reporting estimate | 15–20 ADUs | The CRA's project manager's own estimate, across internal, attached, and detached units. |

| Dispersal target | June 30, 2027 | The term sheet directs reasonable efforts to disperse by then; undistributed funds revert to the CRA. |

(Sources: Salt Lake City CRA adopted ADU loan term-sheet modification, January 2026; Building Salt Lake, March 2025; KSL NewsRadio, March 2025. Verified May 27, 2026.)

For context on demand: Salt Lake City residents filed 98 ADU permit requests in 2024 alone, plus another 15 in early 2025. (Source: Building Salt Lake, March 2025.) That doesn't mean all those people want this loan — many had equity and didn't need it — but it tells you appetite for ADUs far exceeds 15–20 funded units. If you qualify, treating this as scarce is rational, not hype.

That's a real reason to move deliberately — and a good reason not to let a contractor stampede you into a contract before you've confirmed eligibility. The genuine scarcity here is a fixed public fund with a 2027 deadline, not a builder's “only a few slots left this quarter.”

The pool is limited. Confirm your property and budget belong in this lane before you shop for plans.

Check your SLC ADU loan fit → get your free ADU report.

See What You Can Build → Get Your Free ADU ReportDo I qualify for Backyard Keys?

Answer capsule. You may qualify if you own and live in a primary residence west of I-15 within city limits, can meet CDCU's underwriting and program requirements, complete the required Good Landlord training and financial counseling, and accept the program's rent restrictions if your household income is above 80% of Area Median Income. Properties in the 9-Line Community Reinvestment Area receive funding priority.

Eligibility runs through four gates, in order. Fail an early one and the later ones don't matter — which is exactly why we sequence them this way. Most disqualifications happen at gate one.

The eligibility decision gate

| Gate | Requirement | You PASS if… | You're likely OUT if… |

|---|---|---|---|

| 1. Location | Property west of I-15, inside SLC limits | Your parcel is on the west side; bonus priority in the 9-Line area | Your property is east of I-15 or outside city limits |

| 2. Occupancy | Owner-occupied primary residence | You live in the main home (or will live in the ADU) | You own it purely as an investment and won't live on-site |

| 3. Program steps | Good Landlord training + financial counseling | You'll complete both | You won't or can't complete the required training |

| 4. Income lane | Sets your rent obligation, not your eligibility | Any income level can participate | (No one is disqualified by income — but it sets your rules) |

(Source: cra.slc.gov ADU Loan Program page; cdcutah.org. Verified May 27, 2026.)

Gate 1: The I-15 line and the 9-Line priority area

The dividing line is literal: Interstate 15. If your property is west of it and inside Salt Lake City's municipal boundary, you clear the geographic gate. The strongest position is inside the 9-Line Community Reinvestment Area, which runs along 900 South between I-15 and the Jordan River and reaches into Poplar Grove and Glendale — that area has $1,913,215 set aside, so applications there get priority. (Source: cra.slc.gov. Verified May 27, 2026.)

If you're not sure which side of I-15 you're on, or whether your address is inside city limits versus an unincorporated pocket or a neighboring city, that's the single most important thing to confirm first — and exactly what our Fit Check resolves in seconds.

Gate 2: Owner-occupancy — and the exceptions nobody mentions

Both the loan program and Salt Lake City's zoning code require owner-occupancy for an ADU on a single-family lot. Either the main house or the ADU has to be your primary residence; you can rent one and live in the other, but you can't rent out both and live elsewhere under a standard ADU approval. (Source: SLC Code §21A.40.200.)

The owner-occupancy requirement has real flexibility built in. It permits a bona fide temporary absence of three years or less for things like military service, a temporary job assignment, a sabbatical, or voluntary service. The code also accommodates ownership through a deed owner, a related person living on site, or a trustor of a family trust, and addresses situations involving hospitalization, nursing, or assisted-living care. (Source: SLC Code §21A.40.200, as amended by Ord. 17-23, 2023.) So a reservist deploying, a professor on a one-year sabbatical, or a family holding the home in a trust isn't automatically knocked out. If your ownership situation is unusual, confirm directly with the Salt Lake City Planning Division before you invest in design work.

Gate 3: Good Landlord training and financial counseling

Two non-financial requirements you complete as part of qualifying: Salt Lake City's Good Landlord training and CDCU's financial counseling. Under the adopted term-sheet language, the Good Landlord step for higher-income borrowers is tied to obtaining a business license for the rental. (Sources: cra.slc.gov; SLC CRA adopted term-sheet modification, January 2026. Verified May 27, 2026.) These aren't obstacles so much as paperwork — but they take time, so start them early rather than discovering them at closing.

Gate 4: Your income lane sets your rent obligation

This is the gate people misunderstand most. Your income doesn't disqualify you — it determines what you can do with the ADU once it's built. There are two lanes.

| Household income | What you can do with the ADU |

|---|---|

| At or below 80% AMI | No rent restriction. Live in it, let family use it, or rent it to anyone at any price. |

| Above 80% AMI | You must rent either the ADU or the main home at a rent affordable to a household earning 80% AMI or less. |

(Source: cra.slc.gov ADU Loan Program page; cdcutah.org. Verified May 27, 2026.)

“AMI” stands for Area Median Income — the midpoint household income for the Salt Lake City metro area, published annually by HUD and adjusted for household size. Here are Salt Lake City's published 2026 figures, so you can find your lane without leaving this page.

Salt Lake City 80% AMI thresholds (2026)

| Household size | 80% AMI income limit |

|---|---|

| 1 person | $70,650 |

| 2 people | $80,750 |

| 3 people | $90,850 |

| 4 people | $100,900 |

| 5 people | $109,000 |

| 6 people | $117,050 |

| 7 people | $125,150 |

| 8 people | $133,200 |

(Source: Salt Lake City Housing Stability Division, 2026 HUD income limits for the Salt Lake City HUD Metro FMR Area. HUD updates these every spring; confirm the current figures with CDCU's AMI calculator before you rely on them. Verified May 27, 2026.)

The practical takeaway: if you're above 80% AMI, this loan comes with a real obligation — you're agreeing to rent one of your two units below market and document it every year. For some homeowners — housing an aging parent or an adult child in the ADU while renting the main house affordably — that's a fine trade. For an owner who wanted market-rate rental income from day one, it changes the math. Know which lane you're in before you fall in love with a floor plan.

We'll help you confirm your lot, your AMI lane, and your build options at your specific address.

Check your income lane and lot fit → get your free ADU report.

See What You Can Build → Get Your Free ADU Report

What are the actual loan terms — and what changed in the 2026 term sheet?

Answer capsule. Under the published program terms, the Salt Lake City ADU loan offers up to $200,000 at a 3% fixed rate, amortized over 30 years on a 5-year term with a 5-year extension option. Borrowers make interest-only payments during the first 12 months, pay a $2,000 origination fee and a $200 annual compliance fee, and contribute at least $1,000 of their own funds. The biggest open question is forgiveness: the CRA's public page lists up to 10%, but CDCU's page and the adopted 2026 term sheet do not.

Here's where we earn our keep, because the most-repeated fact about this program is the most misleading one. News stories and builder pages routinely call this a “30-year loan.” It isn't, exactly. Read the terms carefully.

Headline vs. reality: the corrected term sheet

| Term | What the headlines say | What the official terms actually say |

|---|---|---|

| Loan amount | "Up to $200,000" ✓ | Up to $200,000 per property — accurate |

| Interest rate | "3% fixed" ✓ | 3% fixed — accurate |

| The "30-year" part | "30-year loan" ✗ | 30-year amortization — your payment is calculated as if over 30 years |

| The actual term | (usually omitted) | 5-year term, with a 5-year extension option |

| First 12 months | (usually omitted) | Interest-only payments; construction-period interest is capitalized from loan proceeds as an interest reserve |

| Origination fee | (usually omitted) | $2,000 ($200 is the application fee; the rest can roll into the loan) |

| Compliance fee | (usually omitted) | $200 per year, for affordability verification |

| Close-out admin fee | (usually omitted) | CDCU may collect a $1,000 administrative fee at loan close-out |

| Your cash in | (usually omitted) | Minimum $1,000 of your own liquid funds |

| Forgiveness | "up to 10%" (sometimes) | Disputed across official sources — see the conflict table below |

(Sources: cra.slc.gov ADU Loan Program page; cdcutah.org ADU financing page; SLC CRA adopted term-sheet modification, January 2026; Building Salt Lake, March 2025. Verified May 27, 2026.)

Why “30-year amortization” is not “30-year term”

Amortization is the schedule used to calculate your monthly payment — spreading the loan over 30 years keeps the payment low. Term is how long the loan agreement actually lasts before it comes due. Backyard Keys pairs a low 30-year-amortized payment with a much shorter 5-year term, extendable once to ten years total.

In plain terms: your monthly payment is small, like a 30-year mortgage, but the loan doesn't run for 30 years. At the end of the term, the balance has to be addressed. The single most important question to ask CDCU: “At the end of the five-year term — and at the end of the extension — does the remaining balance come due as a balloon, re-amortize, or have to be refinanced?” The official written sources confirm the term and the extension; they don't spell out the payoff mechanics, so get that answer from CDCU directly.

The first-year payment structure most people miss

For the first 12 months — the construction window — you make interest-only payments, and the construction-period interest is capitalized from the loan proceeds as an interest reserve. (Source: SLC CRA adopted term-sheet modification, January 2026.) That's borrower-friendly: it keeps your out-of-pocket low while the unit isn't yet generating any rent. Just know that capitalized interest adds to your principal, so the amount you ultimately repay is a bit higher than the cash you receive for construction.

The fees, all in one place

- $2,000 origination fee — $200 is a non-refundable application fee; the remaining $1,800 can roll into the loan. (cdcutah.org.)

- $200 per year compliance fee — covers ongoing affordability verification over the term. (cra.slc.gov.)

- $1,000 close-out administrative fee — CDCU may collect this from loan principal and interest payments at close-out. (Adopted term sheet, January 2026.)

- $1,000 minimum borrower contribution — your own liquid funds in the deal. (cdcutah.org.)

Is the loan forgivable? Read this carefully — the official sources conflict.

This is the most important thing on the page to get right, so we're going to be precise.

| Official source | What it says about forgiveness | Verified |

|---|---|---|

| CRA public Backyard Keys page | Lists “Loan Forgiveness: Up to 10% for rent-restricted ADUs” | We confirmed this is currently on the page |

| CDCU ADU financing page (the administrator) | Lists the full loan terms — and does not mention any forgiveness | We confirmed forgiveness is absent from CDCU's term list |

| CRA adopted term-sheet modification (Jan 2026) | Reported to omit a partial loan-forgiveness option from the amended/restated terms | Reported from the adopted resolution; confirm wording with CDCU |

(Sources: cra.slc.gov; cdcutah.org; SLC CRA adopted term-sheet modification, January 2026. Verified May 27, 2026.)

What this means for you, plainly: there is a documented disagreement between the city's own pages, and the administrator who will actually write your loan — CDCU — does not list forgiveness at all. On a maxed $200,000 loan, “up to 10%” would be up to $20,000, which is enough to make or break a budget. Do not finalize your project budget assuming you'll receive any forgiveness unless CDCU confirms it in writing in your final loan documents, with the conditions that trigger it.

What changed in the 2026 term sheet — the short version

The adopted 2026 term-sheet modification: (1) gives the exact funding split — $1,913,215 for the 9-Line area, $1,000,000 for the rest of the west side; (2) sets the June 30, 2027 dispersal target with reversion of undistributed funds; (3) spells out the interest-only first 12 months and construction-interest reserve; (4) adds the $1,000 CDCU close-out fee and the tenant-verification compliance mechanics; (5) requires detached ADUs to meet the CRA's sustainability standard; and (6) is the source of the forgiveness conflict above. (Source: SLC CRA adopted term-sheet modification, January 2026. Verified May 27, 2026.)

The sustainability requirement on detached ADUs

Under the adopted term sheet, detached ADU projects must comply with the CRA's Sustainable Development Policy: the unit must be “Designed to Earn the ENERGY STAR” with a score of 90 or higher and must have no on-site fossil-fuel combustion — meaning electric heat pumps and water heaters rather than gas. Attached and internal ADUs may receive a waiver under the term-sheet language. (Source: SLC CRA adopted term-sheet modification and Sustainable Development Policy, 2025–2026. Verified May 27, 2026.)

Practically, this shapes your HVAC, water-heating, and appliance choices on a detached build, which affects both cost and builder selection. Ask early: “My ADU is detached — what does the Energy Star 90+ and all-electric requirement add to my budget?”

Is this a grant, a forgivable loan, or a regular loan?

Answer capsule. The Salt Lake City ADU loan program is a loan you repay, not a grant. A partial-forgiveness provision is listed on the CRA's public page but is absent from the administrator's page and the adopted 2026 term sheet, so it should be treated as unconfirmed until it appears in your loan documents.

A lot of people arrive searching “Salt Lake City ADU grant,” so let's be direct: Backyard Keys is a loan you pay back, not free money. It feels grant-like because a 3% fixed rate is well below market for construction financing, and because of the forgiveness language on the CRA page. But you borrow it, and you repay it.

The safe mental model: a below-market public construction loan, with a possible small forgiveness component you must confirm in writing. If a true grant is what you're after, most ADU “grants” nationally are paused, waitlisted, or tiny — we cover the verified ones in our ADU grants database.

The questions to ask CDCU before you rely on this program

Bring this list to your first call. It's the fastest way to turn “sounds great” into “confirmed for my situation.”

- Is funding currently available for new applicants?

- Is my specific address eligible, and am I in the 9-Line priority area?

- At maturity (and after the extension), does the balance balloon, re-amortize, or require a refinance?

- Is any loan forgiveness available to me, and what exactly triggers it?

- What rent restriction applies to my income lane, and how is compliance verified each year?

- Does the Energy Star 90+ / all-electric requirement apply to my ADU type?

- What happens if I sell, refinance, move out, or stop renting before the term ends?

- How is a funding gap handled if my project costs more than $200,000?

- What's the realistic timeline from application to a permit-ready loan?

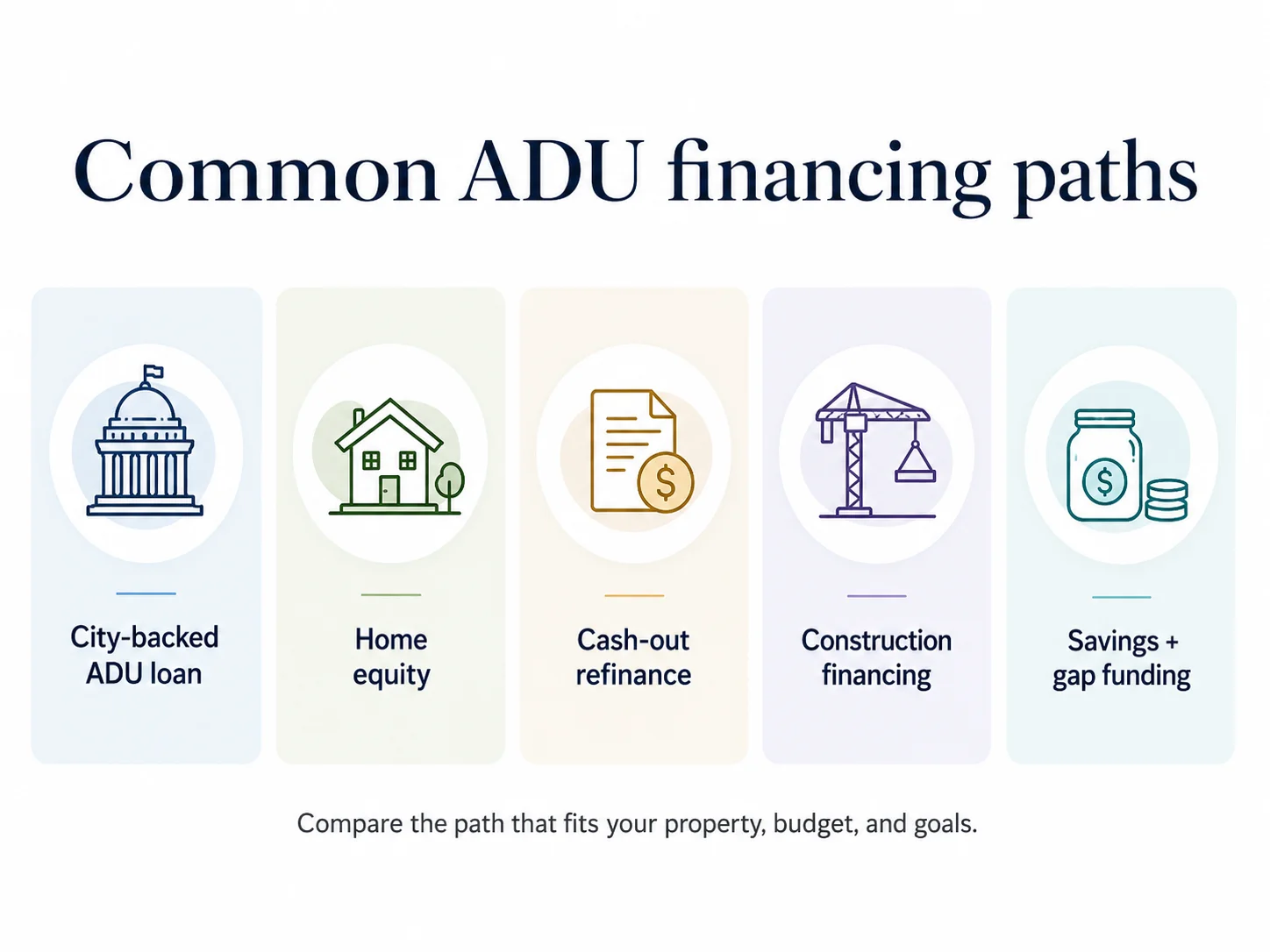

Backyard Keys isn't the only way to fund an ADU. If the geography, rent rules, funding limit, or 5-year term don't fit, it's worth comparing mortgage, refinance, home-equity, and construction-loan paths side by side.

No single path is best for every ADU. Compare the route that fits your property, budget, and goals.

Can my Salt Lake City lot legally have an ADU?

Answer capsule. Salt Lake City allows one accessory dwelling unit where ADUs are permitted under zoning Chapter 21A.33, subject to the standards in §21A.40.200. A 2023 ordinance moved detached ADUs to staff-level administrative review and set clear dimensional rules: a 1,000-square-foot cap on detached units, 3-foot side and rear setbacks, and a 17-foot default height. Owner-occupancy is required and short-term rental is prohibited. Qualifying for the loan does not guarantee your specific lot can physically and legally fit an ADU.

Qualifying for the money is one thing. Getting an ADU approved on your actual parcel is another — and you need both.

The 2023 change that made detached ADUs easier

In 2023, Salt Lake City adopted Ordinance 17-23, which moved detached ADUs in single-family zones to staff-level administrative review — eliminating the discretionary conditional-use approval that used to slow projects down, while keeping owner-occupancy in place. Administrative review does not mean “no rules.” It means the path is predictable rather than discretionary, as long as you meet every standard below. (Sources: SLC Code §21A.40.200; KSL, April 2023.)

Salt Lake City ADU rule cheat sheet (current code)

| Rule | What SLC Code §21A.40.200 says | What it means for your project |

|---|---|---|

| Number of ADUs | One ADU per property, where permitted under Chapter 21A.33 | No stacking multiple units on one parcel |

| Owner-occupancy | Required on single-family lots (3-year temporary-absence and family-trust/care exceptions) | You live in the house or the ADU |

| Detached ADU size | May not exceed 1,000 square feet | Don't design past 1,000 sq ft on a detached unit |

| Internal ADU size | No maximum floor area (must meet habitability code) | Basement conversions aren't size-capped, but must meet egress, ceiling-height, and light rules |

| Setbacks (detached) | At least 3 ft from rear and side property lines; corner-side setback is the lesser of 20% of lot width or 10 ft | Tight setbacks help small lots — confirm utility easements |

| Height (detached) | 17 ft default; up to 24 ft (pitched roof) or 20 ft (flat roof) with increased setbacks; up to the principal building's permitted height if within the buildable area | A tall two-story prefab may not fit without extra setback |

| Parking | One on-site stall, unless in a no-minimum-parking area, within ¼ mile of a transit stop, or within ½ mile of a city-recognized bike lane/path | Many west-side lots qualify for an exemption |

| Lot/yard coverage | Subject to the building- and yard-coverage limits of the applicable zoning district | Big units need lots that can carry the coverage |

| Alley activation | Detached ADUs near a public alley must include lighting for an alley segment | A small design item to budget for |

| Permit + zoning certificate | Building permit and zoning certificate required before construction | No permit, no legitimate (or financeable) project |

| Restrictive covenant | Must be recorded with the Salt Lake County Recorder | Runs with the property; a future buyer inherits the ADU rules |

| Short-term rental | Prohibited — no stays under 30 days | This is a long-term-rental path, not an Airbnb play |

(Source: Salt Lake City Code §21A.40.200, including Ord. 17-23 (2023); corroborated by KSL's April 2023 reporting. Verified May 27, 2026. We rely on Salt Lake City code only for city setback and dimensional rules — county guidance does not govern city lots.)

A note on Utah state law

Utah's 2025 recodification moved the municipal ADU framework into Title 10, Chapter 21. Internal-ADU provisions sit at Utah Code §10-21-303, and detached-ADU provisions at §10-21-304 take effect October 1, 2026. (Source: Utah Legislature, Utah Code Title 10 Ch. 21.) For your project, though, Salt Lake City's local code and the Backyard Keys terms are what govern the practical path — don't let a state-level headline override what the city requires on your lot.

Pre-approved plans can speed things up — but won't skip the permit

Salt Lake City Building Services maintains a library of pre-approved ADU standard plans that have already cleared building-code review, which can shorten plan check. Salt Lake City lists a Nest Tiny Homes 775-square-foot (2B-775) ADU plan among its pre-approved standard plans. But the city is explicit: a site review is still required to get a permit, and you still pay all applicable permit fees. The city also states it does not endorse any specific design, contractor, architect, or engineer. (Source: slc.gov Building Services ADU Standard Plans page. Verified May 27, 2026.)

Can $200,000 actually cover an ADU in Salt Lake City?

Answer capsule. Sometimes. In Salt Lake City, garage conversions, basement (internal) ADUs, and compact detached or prefab units are the most likely to fit inside the $200,000 cap, while larger detached new-construction ADUs — which local builders estimate at roughly $300 to $350 per square foot — frequently exceed it once site work, utilities, permits, and contingency are added.

What ADUs actually cost in Salt Lake City

Detached new construction in Salt Lake City runs roughly $300 to $350 per square foot or more, per a local Utah builder's estimate — you're building a complete small house: foundation, framing, full utilities, kitchen, and bath. (Source: Marshall Homes Utah, April 2025 — a local builder estimate, not a market-wide audited average.) At $325/sq ft, a 600 sq ft detached unit is about $195,000 — right at the cap before fees and contingency. An 800 sq ft unit is about $260,000 — over the cap.

A key dynamic: cost per square foot drops as size rises, because fixed costs (foundation, utility hookups, kitchen, bath) spread across more square footage. (Source: BuildinganADU.com development-cost analysis.) That's why builders often advise building closer to the allowable maximum when budget and lot allow — the marginal square footage is comparatively cheap.

How the $200K cap maps to ADU type

| ADU type | Typical SLC fit with $200K | Why |

|---|---|---|

| Garage conversion | Often fits | Existing shell (walls, roof, slab) cuts cost — though habitability upgrades can add up |

| Internal / basement ADU | Often fits | No new footprint; cost is in egress, ceiling height, fire separation, and utilities |

| Compact detached (≤~600 sq ft) | Can fit | Best when design is simple and site work is minimal |

| Larger detached (700–1,000 sq ft) | Risky | Size + foundation + utilities + Energy Star compliance can push past the cap |

| Prefab / modular | Can fit | Predictable factory pricing helps; delivery, site work, and permitting still count |

| Luxury / custom | Weak fit | The cap likely becomes partial financing only |

(Editorial framework by The Dwelling Index, built from the SLC-specific builder estimate and SLC code size limits. These are directional planning ranges, not quotes. Verified May 27, 2026.)

Where the $200,000 quietly disappears

Builders quote a “base” price. The cap gets eaten by what that base price leaves out:

- Design and engineering (often excluded from a base unit price)

- Building permit and impact fees

- Utility laterals — the pipes and wires connecting your ADU to city water, sewer, gas, and power; trenching and service upgrades can run into the tens of thousands

- Foundation and site work (grading, drainage, excavation) — drain grade and slope is a major up-front issue

- Fire-access or code upgrades

- The Energy Star / all-electric items on a detached build

- Contingency (budget 10–15%; site surprises are the norm, not the exception)

The most important piece of advice: site work can move your budget after you've already fallen for a design. A clean, flat lot with utilities at the property line is a very different number than a sloped lot needing a new sewer lateral. Get an all-in bid (sitework, permits, utilities, foundation, delivery, and contingency) before you sign, so the surprises happen on paper, not in a trench.

Prefab and pre-approved plans as a cost-and-time lever

Predictable pricing and pre-cleared plans both reduce risk, so a prefab or modular ADU built from a plan that's already on Salt Lake City's pre-approved list can cut both cost uncertainty and permitting time. Salt Lake City lists a Nest Tiny Homes 775-square-foot (2B-775) ADU plan among its pre-approved standard plans — a verifiable detail, since the city itself shows the plan as code-reviewed — though the city is explicit that it does not endorse any specific contractor or plan. (Source: slc.gov Building Services ADU Standard Plans page. Verified May 27, 2026.)

Use any published model price as a starting point only. Ask for an all-in Salt Lake City quote that includes site work, permits, utilities, delivery, foundation, and contingency — and get at least two local bids.

Cost and rental figures on this page are illustrative examples for planning, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

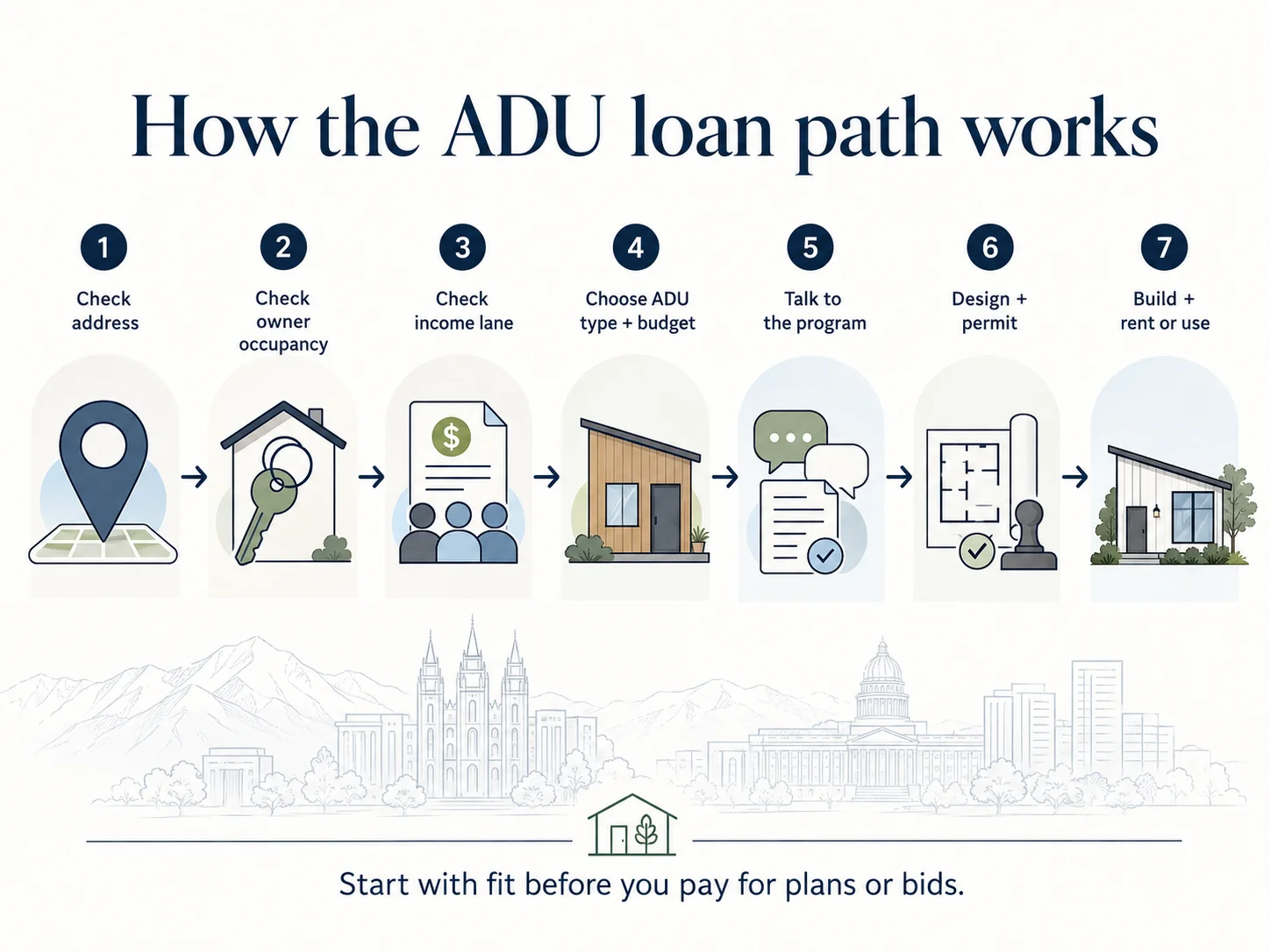

How do I apply for the Salt Lake City ADU loan?

Answer capsule. To apply, confirm your property is west of I-15 and owner-occupied, estimate your AMI rent lane, then join the CDCU interest list as your official first step. From there you complete Good Landlord training and financial counseling, develop plans and a scoped budget, apply through CDCU, record the required covenant, pull a city building permit, and review your final loan documents before closing.

Applications are accepted on a rolling basis as funding allows, so the honest first move is to get on the official interest list — that's how you learn when a window opens and receive the program's own guidance. (Source: cra.slc.gov. Verified May 27, 2026.)

Step-by-step application path

| Step | What you do | What it gets you |

|---|---|---|

| 1 | Confirm property is west of I-15, inside SLC limits | Geographic eligibility |

| 2 | Confirm owner-occupancy (now or planned) | Occupancy eligibility |

| 3 | Estimate your AMI lane (table above + CDCU's calculator) | Your rent-restriction rules |

| 4 | Decide if you can accept the rent/compliance terms | A clear go / no-go before spending money |

| 5 | Choose ADU type (internal, attached, detached, garage, prefab) | Cost range + code path |

| 6 | Review §21A.40.200 standards and pre-approved plan options | Permit feasibility on your lot |

| 7 | Join the CDCU interest list | Your official program entry point |

| 8 | Complete Good Landlord training (+ business license if >80% AMI) and financial counseling | Program readiness |

| 9 | Get plans, contractor bids, and a scoped budget; confirm how any gap above $200K is covered | A financeable project |

| 10 | Apply through CDCU; record the restrictive covenant | Loan + zoning compliance |

| 11 | Read final loan documents before closing | Confirm term, extension, payoff, forgiveness, and compliance obligations |

(Sources: cra.slc.gov; cdcutah.org; SLC CRA adopted term-sheet modification. Verified May 27, 2026.)

The document pack to bring

- Property address and parcel verification (which side of I-15)

- Owner-occupancy proof (ID, tax records, utility bills)

- Household income and household-size documentation (for your AMI lane)

- Good Landlord training completion and business license (if >80% AMI)

- CDCU financial-counseling confirmation

- Preliminary scope, site plan, and at least one contractor bid

- The recorded restrictive covenant

- Your written questions on the term, forgiveness, and sustainability requirements

Bring this checklist to your CDCU call, your designer, and your builder bid review so nothing falls through the cracks.

Download the Free ADU Starter Kit →You can join the official interest list directly through CDCU or the CRA's Backyard Keys page — that step is free and non-commercial, and it's the right place to start. Our role is to get you to that conversation already knowing whether you qualify and what to ask.

What if I don't qualify, or the funds run out?

Answer capsule. If you don't qualify for the Salt Lake City ADU loan — because your property is east of I-15, you can't owner-occupy, you won't accept the rent restriction, or the funding is exhausted — you can still build an ADU using conventional financing. Most ADUs nationwide are funded through construction loans, cash-out refinances, home equity lines of credit, or renovation loans rather than public programs.

If Backyard Keys isn't a fit, the answer isn't to abandon the ADU — it's to match the reason it didn't fit to the right alternative. The vast majority of Salt Lake City homeowners — everyone east of I-15, plus anyone who can't meet owner-occupancy — were never eligible for this program, and they build ADUs all the time.

Your alternative-path matrix

| Why Backyard Keys didn't fit | Your better next step |

|---|---|

| Property is east of I-15 | Compare home-equity, cash-out refinance, renovation, or construction-loan paths |

| You don't owner-occupy | Look at investor / non-owner-occupied ADU financing |

| You're above 80% AMI and won't accept rent restrictions | Compare conventional financing and model market-rate rental economics |

| Project costs more than $200,000 | Ask CDCU how a gap is handled, or go fully conventional |

| Funds are unavailable | Join the interest list, but build a backup financing plan now |

| You want short-term rental income | SLC's ADU code prohibits STR — rethink the use or the property |

| You need a larger or custom ADU | Rework scope, add equity, or compare financing alternatives |

(Editorial framework by The Dwelling Index. Verified May 27, 2026.)

The financing lanes, explained (not ranked)

We present these as lanes, not a ranked “best lender” list — because the right lane depends on your equity, your timeline, and whether you're keeping the property long-term.

- Construction loan. Funds the build in draws as work completes, then converts to or is replaced by permanent financing. Fits ground-up detached ADUs where you don't have enough equity to borrow the full amount upfront. See ADU construction loans explained.

- Cash-out refinance. Replaces your existing mortgage with a larger one and gives you the difference in cash. Fits homeowners with substantial equity whose current mortgage rate isn't dramatically below market. See cash-out refinance for ADUs.

- HELOC (home equity line of credit). A revolving credit line secured by your equity; you draw as needed. Fits phased projects and owners who want flexibility and have a low first-mortgage rate worth keeping. See HELOC for ADUs.

- Renovation loan. Wraps the project cost into financing based on the home's projected after-completion value. Fits owners who don't yet have the equity but will once the ADU is built. See renovation loans for ADUs.

For homeowners who want to compare these mortgage, refinance, cash-out, and construction-loan lanes in one place, our financing partner Mortgage Research Center provides education across all of them. We point you there for path comparison, not for a rate quote. A note on newer products: home equity investment (HEI) products exist, but availability varies by state and several providers have limited or no Utah availability. Confirm it operates in Utah before you count on it. See also: compare ADU financing paths and our estimate your ADU funding gap tool.

No single path is best for every ADU. Compare the route that fits your property, budget, occupancy plan, and rental strategy.

This is educational information, not a guarantee of loan approval, eligibility, interest rates, monthly payments, or returns. The Dwelling Index is not a lender, broker, city agency, law firm, or tax advisor.

What are the risks and dealbreakers?

Answer capsule. The main risks are limited funding, the 5-year term structure, the rent and compliance obligations for higher-income borrowers, the owner-occupancy requirement, the detached-ADU sustainability requirement, ADU permit and code constraints, construction cost overruns above the $200,000 cap, the prohibition on short-term rentals, and the unresolved forgiveness conflict.

We'd rather you walk in clear-eyed than excited and surprised. Here's the honest risk ledger.

| Risk | Why it matters | How to reduce it |

|---|---|---|

| Limited funding | A strong program can still run out ($2.9M pool, 15–20 ADUs) | Verify availability before paying for plans |

| 5-year term | It's not a settled 30-year loan; the balance gets addressed at maturity | Get written maturity/extension/payoff terms from CDCU |

| Forgiveness conflict | Official sources disagree; CDCU's page lists none | Treat forgiveness as a confirmed bonus only, never an assumption |

| Rent restrictions | Above-80%-AMI borrowers must rent one unit affordably and document it annually | Model conservative rent and the compliance burden |

| Owner-occupancy | Moving out can affect compliance (3-year/care/trust exceptions aside) | Ask what happens if your life circumstances change |

| Sustainability requirement | Detached ADUs must meet Energy Star 90+ and run all-electric | Have your designer price compliance from the start |

| Short-term rental ban | No Airbnb income under SLC code | Underwrite on long-term rent only |

| Permit / code issues | Setbacks, height, parking, utilities, and the covenant can reshape the project | Run a zoning/site review before committing to a model |

| Cost overruns | The $200K cap may not cover all-in costs | Require all-in bids plus a 10–15% contingency line |

(Sources: cra.slc.gov; cdcutah.org; SLC CRA adopted term-sheet modification; SLC Code §21A.40.200. Verified May 27, 2026.)

None of these is a reason to walk away if the program fits you. They're the reasons to ask the nine questions, get the all-in bid, and read your loan documents — the three habits that separate the homeowners who finish their ADU on budget from the ones who stall halfway.

What we verified

We built this guide primarily from official Salt Lake City sources — the CRA and CDCU program pages, the adopted CRA term-sheet modification, Salt Lake City Code §21A.40.200, and the city's Housing Stability income limits — supplemented by local reporting and a local builder cost estimate only where official pages don't answer a practical homeowner question. Where official sources conflict, we show the conflict instead of picking a side.

| What we checked | Source(s) | Verified |

|---|---|---|

| Program exists; administered by CDCU / Utah Community Investment Fund | cra.slc.gov; cdcutah.org | May 27, 2026 |

| Loan amount, 3% rate, 30-yr amortization, 5-yr term, fees, $1,000 contribution | cra.slc.gov; cdcutah.org | May 27, 2026 |

| Interest-only first 12 months; $1,000 close-out fee; funding split; June 2027 dispersal | CRA adopted term-sheet modification, Jan 2026 | May 27, 2026 |

| Forgiveness conflict (CRA page lists 10%; CDCU page lists none) | cra.slc.gov vs. cdcutah.org (both confirmed directly) | May 27, 2026 |

| Funding pool $2,913,215; 15–20 ADU estimate | CRA term sheet; Building Salt Lake; KSL | May 27, 2026 |

| West-of-I-15 + 9-Line priority geography | cra.slc.gov | May 27, 2026 |

| Income lanes; 2026 80% AMI thresholds | cra.slc.gov; SLC Housing Stability | May 27, 2026 |

| SLC ADU code: 1,000 sf detached cap, 3-ft setbacks, 17-ft height, parking exemptions, STR ban, covenant | SLC Code §21A.40.200; KSL (Apr 2023) | May 27, 2026 |

| Detached-ADU sustainability requirement (Energy Star 90+, all-electric) | CRA adopted term sheet / Sustainable Development Policy | May 27, 2026 |

| Pre-approved plans incl. Nest Tiny Homes 2B-775; city endorses no provider | slc.gov Building Services | May 27, 2026 |

| Utah Code Title 10 Ch. 21; §10-21-304 detached provisions effective Oct 1, 2026 | Utah Legislature | May 27, 2026 |

| SLC detached cost ~$300–$350/sq ft (local builder estimate) | Marshall Homes Utah, Apr 2025 | May 27, 2026 |

Methodology

We prioritized primary sources — official CRA, CDCU, Salt Lake City code, and city income-limit materials — then used local reporting (Building Salt Lake, KSL) and a local builder estimate only to answer practical questions the official pages leave open. Program terms, zoning rules, and compliance requirements are verified against official sources; cost figures are treated as directional and require project-specific quotes.

Our editorial rules for this page: when official sources conflict — as they do on forgiveness — we surface the conflict and tell you what to confirm rather than picking the more flattering version. We do not present a builder's promotional pricing as a guaranteed all-in cost. We do not rank financing providers by compensation, and we present financing as lanes rather than a “best lender” list. We rely on Salt Lake City code for city zoning facts, not county guidance, and on the Utah Legislature for state-law facts.

This guide was created by the editorial team at The Dwelling Index, an independent research resource covering ADU financing, costs, and regulations. The Dwelling Index is not a lender, broker, city agency, law firm, or tax advisor. Eligibility, underwriting, final loan terms, permit approvals, and rent rules are determined by the relevant agencies and providers.

Frequently asked questions

Is the Salt Lake City ADU loan still available in 2026?

The program accepts applications on a rolling basis as funding becomes available, and the adopted term sheet directs CDCU to make reasonable efforts to disperse the funds by June 30, 2027, with undistributed money reverting to the CRA. Because the pool is limited to an estimated 15–20 ADUs, confirm current availability with CDCU before paying for plans. (Source: cra.slc.gov; CRA term sheet; Building Salt Lake. Verified May 27, 2026.)

Is Backyard Keys only for west-side Salt Lake City homeowners?

Yes. The program serves owner-occupied properties west of I-15 within Salt Lake City limits, with applications in the 9-Line Community Reinvestment Area receiving priority. Properties east of I-15 are not eligible. (Source: cra.slc.gov. Verified May 27, 2026.)

How much can I borrow, and what's the interest rate?

Up to $200,000 per property at a 3% fixed rate, amortized over 30 years on a 5-year term with a 5-year extension option, with interest-only payments in the first 12 months. There's a $2,000 origination fee, a $200 annual compliance fee, a possible $1,000 close-out administrative fee, and a $1,000 minimum borrower contribution. (Source: cra.slc.gov; cdcutah.org; CRA term sheet. Verified May 27, 2026.)

Is the Salt Lake City ADU loan forgivable?

The city's official sources disagree. The CRA's public page lists up to 10% forgiveness for rent-restricted ADUs, but CDCU's administrator page lists no forgiveness, and the adopted 2026 term sheet is reported to omit a partial-forgiveness option. Do not budget around forgiveness unless CDCU confirms it in your final loan documents. (Source: cra.slc.gov; cdcutah.org. Verified May 27, 2026.)

Do I have to live west of I-15?

Yes. Your property must be west of Interstate 15 and inside Salt Lake City limits to qualify, and you must occupy it as your primary residence. (Source: cra.slc.gov; SLC Code §21A.40.200. Verified May 27, 2026.)

Can I rent out my ADU? Can I run it as an Airbnb?

You can rent it long-term (30+ days), subject to your income lane's affordability rule. You cannot use it as a short-term rental — Salt Lake City's ADU code prohibits stays under 30 days. (Source: SLC Code §21A.40.200. Verified May 27, 2026.)

What if I make more than 80% of AMI?

You can still participate, but you must rent either the ADU or the main home at a rent affordable to a household earning 80% AMI or less, and document compliance annually. Below 80% AMI, there's no rent restriction. (Source: cra.slc.gov; cdcutah.org. Verified May 27, 2026.)

How big can my ADU be in Salt Lake City?

A detached ADU may not exceed 1,000 square feet. An internal ADU (such as a basement apartment) has no maximum floor area, as long as it meets habitability code. (Source: SLC Code §21A.40.200. Verified May 27, 2026.)

What does it actually cost to build an ADU in Salt Lake City?

A local Utah builder estimates detached new construction at roughly $300–$350 per square foot; garage conversions and basement units are typically cheaper because they reuse existing structure. A small, efficient ADU can fit inside the $200,000 cap, while larger detached units often exceed it once site work, utilities, permits, and contingency are included. (Source: Marshall Homes Utah, 2025. Verified May 27, 2026.)

What happens at the end of the 5-year term?

The 30-year figure is the amortization (how the payment is calculated), not the term. The official sources confirm a 5-year term and a 5-year extension option but don't spell out the payoff mechanics. Ask CDCU whether the balance balloons, re-amortizes, must be refinanced, or is handled another way. (Source: cra.slc.gov; cdcutah.org. Verified May 27, 2026.)

Do pre-approved ADU plans let me skip permitting?

No. Pre-approved standard plans can speed plan review because the building-code review is already done, but Salt Lake City still requires a site review to issue a permit, and you still pay permit fees. (Source: slc.gov Building Services. Verified May 27, 2026.)

Not sure where to start?

See what's possible at your address → get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU Report