NYC Plus One ADU Program (2026): Up to $395,000 to Build an ADU — Who Qualifies, the Real Catch, and How to Apply

· · Last verified: May 26, 2026

By the Dwelling Index Research Team — an independent research resource covering ADU financing, costs, and regulations.

Should you apply? Read this table first

Find yourself in one row and know your move before reading another word. This is the verdict; the rest of the page is the proof.

| Your situation | What it likely means | Your next step |

|---|---|---|

| You own and live in a 1–2 unit NYC home, you’re current on your mortgage and city charges, and you want long-term housing or rental income | You’re the core candidate for Plus One | Submit interest now, then run a feasibility check on your lot |

| You have a basement, attic, garage, or backyard idea but haven’t checked flood maps or zoning | Eligibility is plausible but not confirmed | Verify flood zone, zoning district, ceiling height, and access before you spend on plans |

| You want short-term rental (Airbnb) income, want to rent both units, or expect to move or sell within a few years | Plus One is likely a poor fit — owner-occupancy and rent rules conflict with your goal | Consider building privately instead |

| Your income is above the priority band or your property can’t legally add a unit | You may not be selected, but you may still build | Compare private financing lanes |

| You need the unit fast | Selected projects run a multi-year process | Be realistic about timeline before applying |

This is not free money, and we’ll say so plainly. Plus One can be one of the strongest ADU funding deals available to NYC homeowners — for the right owner-occupant. It is the wrong tool for someone trying to build a fast, flexible, restriction-free short-term-rental asset. Knowing which one you are is the single most valuable thing this page can give you.

See what you can build at your address → Get your free ADU report in 60 seconds.

Check your NYC property before you spend a dollar on drawings or the $200 application step.

Affiliate disclosure: The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation.

What we verified

Everything in this guide is built from primary government sources, not press rewrites. Here’s exactly what we checked and when.

- Program is open, with a hard deadline. The HPD/DOB press release dated March 18, 2026 confirms the reopening and states interest submissions run “through Friday, June 12, 2026,” subject to limited funding. (Source: NYC HPD/DOB press release 017-26.)

- The $395,000 structure. The Plus One ADU FAQ (last updated September 4, 2025) states eligible homeowners receive “grant funding through HCR, up to $175,000, and a loan from the City of New York, up to $220,000, for a combined $395,000.” (Source: HPD Plus One ADU FAQ; Term Sheet.)

- Income priority caveat. The FAQ states eligibility runs to 165% AMI, and that “currently, homeowners earning up to 100% AMI are being prioritized.” The main program page separately references preference at or below 120% AMI. We present both rather than guess. (Source: HPD Plus One ADU page; FAQ.)

- AMI dollar figures. Pulled directly from HPD’s official Area Median Income chart, which currently publishes 2025 figures (verified live on May 26, 2026). (Source: NYC HPD AMI page.)

- Zoning, size, height, flood, and code rules. Confirmed against the HPD FAQ, the NYC Department of Buildings ADU page (last revised 09/30/25), and City of Yes for Housing Opportunity materials (adopted December 5, 2024). (Source: HPD FAQ; NYC DOB; NYC Dept. of City Planning.)

- Pre-approved plan costs. We opened the official ADU for You Pre-Approved Plan Library and recorded each plan’s published construction-cost range used in the funding-gap table below, verifying low and high endpoints directly on the plan pages. (Source: ADU for You PAPL, verified May 26, 2026.)

- Loan strings. 270-day residency, 10-/15-year terms, rent restriction on forgivable loans, and repayment on sale/cash-out confirmed in the FAQ and Term Sheet. (Source: HPD FAQ; Plus One ADU Term Sheet.)

Last updated: May 26, 2026. Last verified: May 26, 2026.

Is the NYC Plus One ADU Program open right now?

Yes. The NYC Plus One ADU Program reopened on March 18, 2026 — the first new intake since the original pilot survey closed in February 2024 — and HPD is accepting interest submissions through Friday, June 12, 2026, while limited funding lasts. The first step is a free online interest survey; homeowners who appear eligible are then invited to submit a full application with a $200 non-refundable fee.

If you’ve seen pages saying the program is closed, here’s why: it genuinely was, for over two years. The original Plus One pilot opened in November 2023, drew more than 1,300 submissions in roughly two weeks, and closed to new applicants in February 2024. Then two things changed everything. In December 2024, the City Council adopted City of Yes for Housing Opportunity, which defined ADUs in the zoning code for the first time and made far more properties eligible. And on March 18, 2026, the City reopened Plus One alongside a new homeowner toolkit called ADU for You — a guidebook, a budgeting tool, and a library of pre-approved designs.

What the interest survey does — and doesn’t — do

Submitting the interest survey signals you want in and starts the screening process. It is not an acceptance, not a funding commitment, and not permission to build. HPD reviews submissions and conducts an initial site-feasibility review; only homeowners who appear eligible are invited to the formal application. Think of the survey as getting in line, not crossing the finish line.

Why the June 12 deadline actually matters

Funding is explicitly limited, and the program is operating on a fixed interest window that closes June 12, 2026. Given that the first round attracted over 1,300 submissions in about two weeks, demand reliably outruns supply. Treat this as an urgent, finite window — not a standing entitlement you can return to next year.

| Program item | Current status (verified May 26, 2026) | What it means for you |

|---|---|---|

| Interest intake | Open | You can submit now |

| Interest deadline | Friday, June 12, 2026 | A real, finite window — not permanent |

| Funding availability | Limited | Submitting interest ≠ getting selected |

| Application fee | $200, non-refundable (only if invited to apply) | Run basic feasibility first |

| Timeline to completion | Multi-year | Not a fast cash or fast-rental play |

The HPD survey is free and is not an approval. Running a feasibility check first takes two minutes and can save you the $200 fee on a lot that can’t qualify.

Is the $395,000 a grant, a loan, or a forgivable loan?

It is both a grant and a loan — never a single $395,000 cash gift. Per HPD, eligible homeowners receive up to $175,000 in grant funding from New York State HCR plus a loan of up to $220,000 from the City, for a combined maximum of $395,000. The City loan can be structured as an amortizing (repayable) loan with no regulatory agreement, or as a deferred-forgivable loan that carries a rent restriction on the new ADU.

This is the single most misunderstood fact about the program, and it changes your decision completely. Here is the money, decoded.

The Plus One Money Decoder

| Component | Maximum | Do you repay it? | Strings attached |

|---|---|---|---|

| HCR grant | Up to $175,000 | No repayment on the grant portion | Program occupancy, rent, and monitoring obligations still apply |

| City (HPD) loan | Up to $220,000 | Depends on which loan you choose (see below) | Rent restriction only on the forgivable version |

| Combined ceiling | $395,000 | Partly | Maximum support ≠ guaranteed full project coverage |

Source: HPD Plus One ADU FAQ (Sept. 4, 2025); Plus One ADU Term Sheet.

The fork in the road: repayable vs. deferred-forgivable

Your loan terms are set by underwriting — household income, credit score, debt-to-income ratio, and age all factor in. Per the Term Sheet, the starting interest rate is 5%, reducible in quarter-point steps to as low as 0% to make payments affordable, and the 15-year term can be extended up to 30 years if needed. Monthly payments are sized so the household keeps at least $200 in monthly cash flow after debts. Then you choose:

- Repayable (amortizing) loan — maximum flexibility. You repay the City loan on standard terms, but there is no regulatory agreement and no rent cap on your ADU. You can charge market rent. This is the path for owners who want the money but not the restrictions.

- Deferred-forgivable loan — maximum subsidy, real strings. The loan is forgiven over time, but in exchange the new ADU must be rent-restricted at 100% of AMI with annual increases capped at 2%, under a 15-year regulatory agreement. If underwriting determines you can’t afford even a 0%, 30-year repayable loan, HPD assigns the deferred-forgivable structure.

Plain-English translation: the “freer” the money, the more control you give up over how much rent you can charge. Family members occupying the unit may be exempt from some of those rent provisions — which matters enormously if your goal is housing an aging parent or adult child rather than maximizing rent.

Who qualifies for NYC Plus One ADU funding?

Plus One is for NYC owner-occupants of 1–2 unit homes earning up to 165% of Area Median Income. You must occupy the property as your primary residence, carry valid homeowner’s insurance, be current on your mortgage, and have no outstanding municipal arrears (or be on an active payment plan). HPD’s FAQ states homeowners up to 100% AMI are currently prioritized, while the program page references preference at or below 120% AMI — verify the live threshold before applying. Submitting interest does not guarantee selection.

There are four gates. Miss any one and you’re likely out — so check all four before you invest time.

The income gate, in real dollars

Here are the NYC AMI thresholds from HPD’s official chart (currently published as 2025 figures, verified live on May 26, 2026) at the levels that matter for Plus One — the 100% and 120% priority references and the 165% ceiling.

| Household size | 100% AMI (current priority band) | 120% AMI (program preference) | 165% AMI (eligibility ceiling) |

|---|---|---|---|

| 1 person | $113,400 | $136,080 | $187,110 |

| 2 people | $129,600 | $155,520 | $213,840 |

| 3 people | $145,800 | $174,960 | $240,570 |

| 4 people | $162,000 | $194,400 | $267,300 |

| 5 people | $175,000 | $210,000 | $288,750 |

Source: NYC HPD Area Median Income chart (2025 figures, verified May 26, 2026). Note: rental income from the new ADU is counted toward your household income. HUD updates regional AMI annually; re-check the HPD chart when you apply.

The priority caveat, resolved. Plan around the 100% AMI figures if you want to be in the strongest position today, treat 120% as the program’s stated preference ceiling, and know that 165% is the hard eligibility cap. Before you apply, confirm the current threshold on HPD’s latest materials or by emailing PlusOneADU@hpd.nyc.gov.

The other three gates

- Owner-occupant. You must live in the home as your primary residence. The City enforces this with annual affidavits if you receive financing.

- Mortgage and municipal standing. Current on your mortgage; no outstanding arrears with the Department of Finance or DEP, or enrolled in an active payment plan. Valid homeowner’s insurance required.

- Eligible property (covered in full in the next section).

Two useful nuances from the FAQ: you can apply even if the space you intend to convert is currently occupied, and you can apply even if you have an existing illegal basement unit (that routes through the Basement Legalization Program — more below). What you cannot do is get reimbursed for an ADU you already finished building yourself.

See whether your NYC home is a Plus One fit → Get your free ADU report.

We’ll flag the likely disqualifiers before you spend the $200 application fee.

What properties and ADU types can use Plus One?

Eligible Plus One properties are existing 1–2 unit homes — semi-attached, semi-detached, or fully detached — in a zoning district that allows up to three residential units, outside FEMA’s Special Coastal Risk District. HPD recognizes five ADU types: attached structures, detached existing structures (like a garage), newly built detached structures, basement conversions, and attic conversions. Basement ADUs carry significant extra flood and ceiling-height requirements.

One source conflict worth knowing. HPD’s live program page and FAQ describe eligible homes as 1–2 unit detached, semi-detached, or semi-attached. The older Plus One term sheet still uses narrower “one-unit, single-family detached” language. If you own a two-family or semi-attached home, treat the broader HPD/FAQ rule as current — but confirm your specific property with HPD before relying on funding.

ADU type matrix

| ADU type | Plus One possibility | The main thing to verify first |

|---|---|---|

| Backyard cottage (new detached) | Possible — program’s primary focus | Zoning district, rear-yard limits, flood/historic/Special Bay Ridge restrictions, 5-ft setbacks, access |

| Garage or shed conversion | Possible if structure & zoning fit | Existing structure condition, code, utilities (garage conversions are not “Backyard ADUs” so they’re not blocked in restricted districts) |

| Attached addition | Possible | Building Code, egress, and Multiple Dwelling Law if it becomes a 3rd unit |

| Attic conversion | Possible | Ceiling height, egress, fire safety |

| Basement conversion (new) | Possible but highly constrained | Ceiling height (7 ft) and multiple flood layers |

| Existing illegal basement | Separate narrow path | Basement Legalization Program limits — applications not currently being accepted (see below) |

The size, height, and placement rules, decoded

- Maximum size: 800 square feet of zoning floor area. There’s no minimum, but the unit still has to meet Housing Maintenance Code room-size rules. For a detached backyard ADU, the structure also can’t cover more than one-third of your required rear yard (NYC Zoning Resolution §23-341). In practice, most NYC backyards hit the rear-yard limit long before the 800-square-foot limit.

- Height: one story / 15 feet — unless you put a parking space below part of the ADU, in which case two stories / 25 feet is allowed. Height is measured from Base Flood Elevation.

- Setback: at least 5 feet from the lot line for a new detached ADU.

- Separate entrance required, and the owner must reside on the zoning lot at the ADU’s initial occupancy.

- No front-yard ADUs. Period.

Where backyard (detached) ADUs are NOT allowed

Per the NYC DOB ADU page (last revised 09/30/25), backyard ADUs are not permitted in:

- Historic Districts (unless converting an existing structure)

- R1-2A, R2A, and R3A districts outside the Greater Transit Zone

- The Special Bay Ridge District, west of Ridge Boulevard or south of Marine Avenue

Important exception: converting an existing garage to an ADU is not classified as a “Backyard ADU” under Zoning §12-10, so garage conversions are not blocked in those restricted districts. If a backyard cottage is off the table for your lot, an existing-garage conversion may still be on it.

Basement and cellar conversions: the extra hurdles

New subgrade ADUs face the strictest conditions and are not permitted in high-risk flood areas. Per DOB, subgrade ADUs are prohibited in areas demarcated by FEMA’s Special Flood Hazard Area, the Coastal Flood Risk Area, and DEP’s 10-Year Rainfall Flood Risk Area. HPD’s program materials add ceiling-height (7-foot minimum) and no-recent-flooding requirements. Because HPD’s live page and FAQ use slightly different coastal-year labels for these layers, check your address against the current official flood-risk maps before filing.

The Multiple Dwelling Law trap (this one is expensive)

For a two-family home, adding a basement, cellar, attic, or attached ADU can legally turn the building into a three-family dwelling subject to the New York State Multiple Dwelling Law (MDL) — which can require sprinklers, egress upgrades, and other potentially cost-prohibitive work. Per the FAQ, MDL is not triggered if the ADU is: (1) fully detached from the main structure, (2) attached but separated by a fire-rated wall, or (3) a basement unit legalized through the Basement Legalization Program. If you own a two-family and want an interior ADU, ask about MDL before you pay for design — it’s the difference between a feasible project and a financial wall.

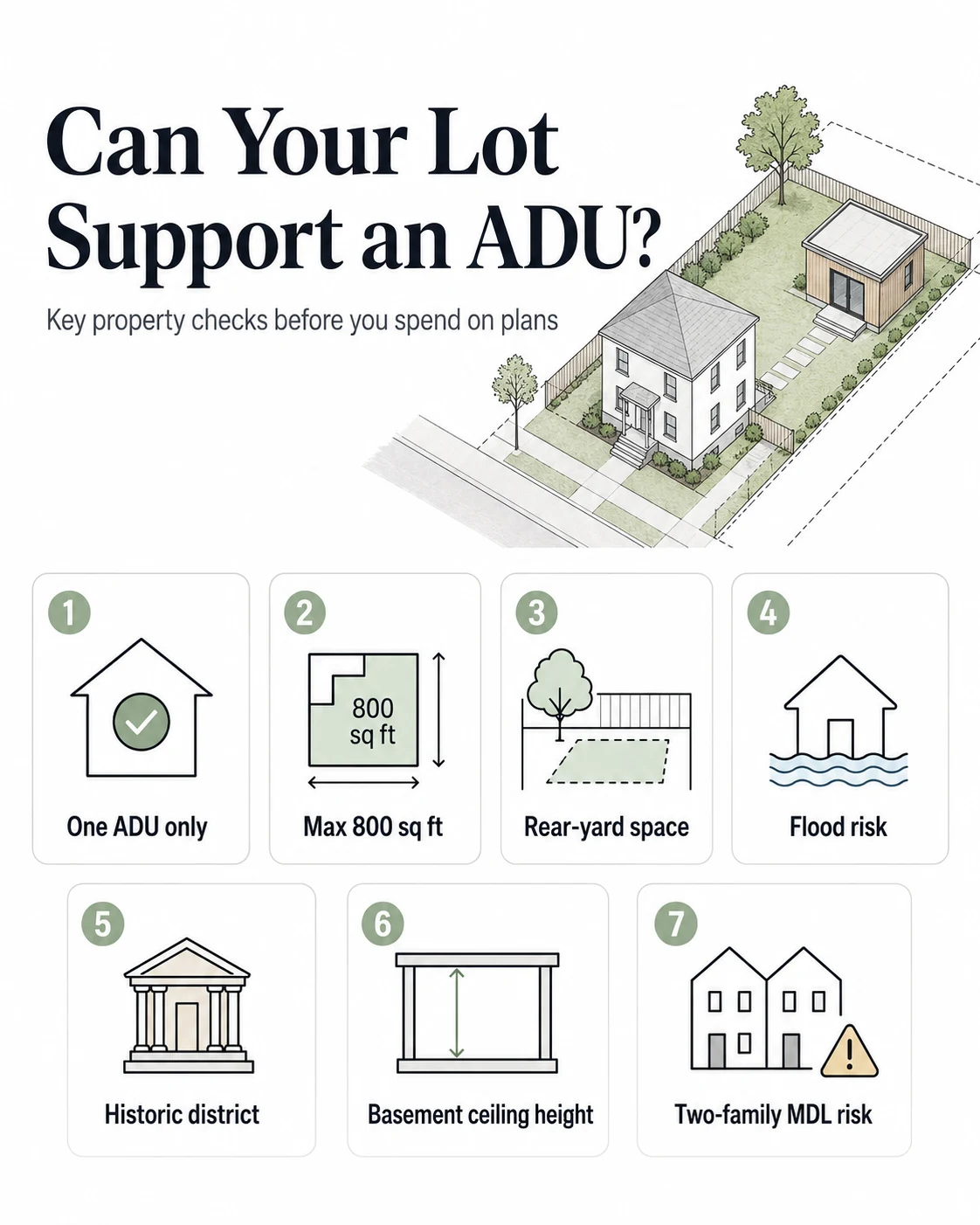

Can my NYC lot legally support an ADU? (The kill-switch checklist)

Under City of Yes, NYC generally allows one ADU per 1–2 family lot, capped at 800 square feet, with the owner residing on the lot at initial occupancy. But zoning district, flood maps, historic-district status, the Special Bay Ridge District, and the Multiple Dwelling Law can each independently block or shrink a project — so legal eligibility must be confirmed lot by lot, not assumed from the citywide rule.

Run down this list. Any single “yes” in the blocker column is a reason to stop and verify before spending money.

| Possible blocker | Why it matters | Where to verify |

|---|---|---|

| You want more than one ADU | NYC allows only one per 1–2 family residence | DOB / Zoning Resolution |

| ADU over 800 sq ft | Hard cap under City of Yes | Zoning Resolution §23-341 |

| Subgrade unit in a high-risk flood area | Basement/cellar ADUs prohibited (FEMA SFHA, Coastal Flood Risk, DEP 10-Year Rainfall) | DOB / DEP flood maps |

| In a Historic District | Backyard ADUs restricted (existing-structure conversions may be OK) | DOB / Zoning Resolution |

| In R1-2A, R2A, or R3A outside Greater Transit Zone | Backyard ADUs not permitted in these districts | DOB / Zoning Resolution |

| In the Special Bay Ridge District (west of Ridge Blvd or south of Marine Ave) | Backyard ADUs not permitted here | DOB ADU page |

| Two-family adding a 3rd interior/attached unit | May trigger MDL (sprinklers, egress) | DOB / HPD FAQ |

| No 5-ft setback or access for a backyard ADU | Required for new detached ADUs | Zoning Resolution |

| Open violations or major repair needs on the property | HPD may require resolution first; inspection may fail | NYC HPD Online; DOB BIS |

| Basement under 7-ft ceiling or with recent flood history | Disqualifies a basement conversion | HPD FAQ / DOB |

A sobering data point: an analysis by the Regional Plan Association found that only about 68,000 of roughly 565,400 NYC 1–2 family homes (around 12%) would be eligible to build or legalize an ADU under current restrictions. We mention it not to discourage you, but so you check your specific lot rather than assuming the citywide “yes” applies to you. (Source: Regional Plan Association.)

Screen your lot before you spend on plans → Get your free ADU report.

Flood zone, zoning district, Special Bay Ridge, setbacks, and rear-yard math — checked against your actual address.

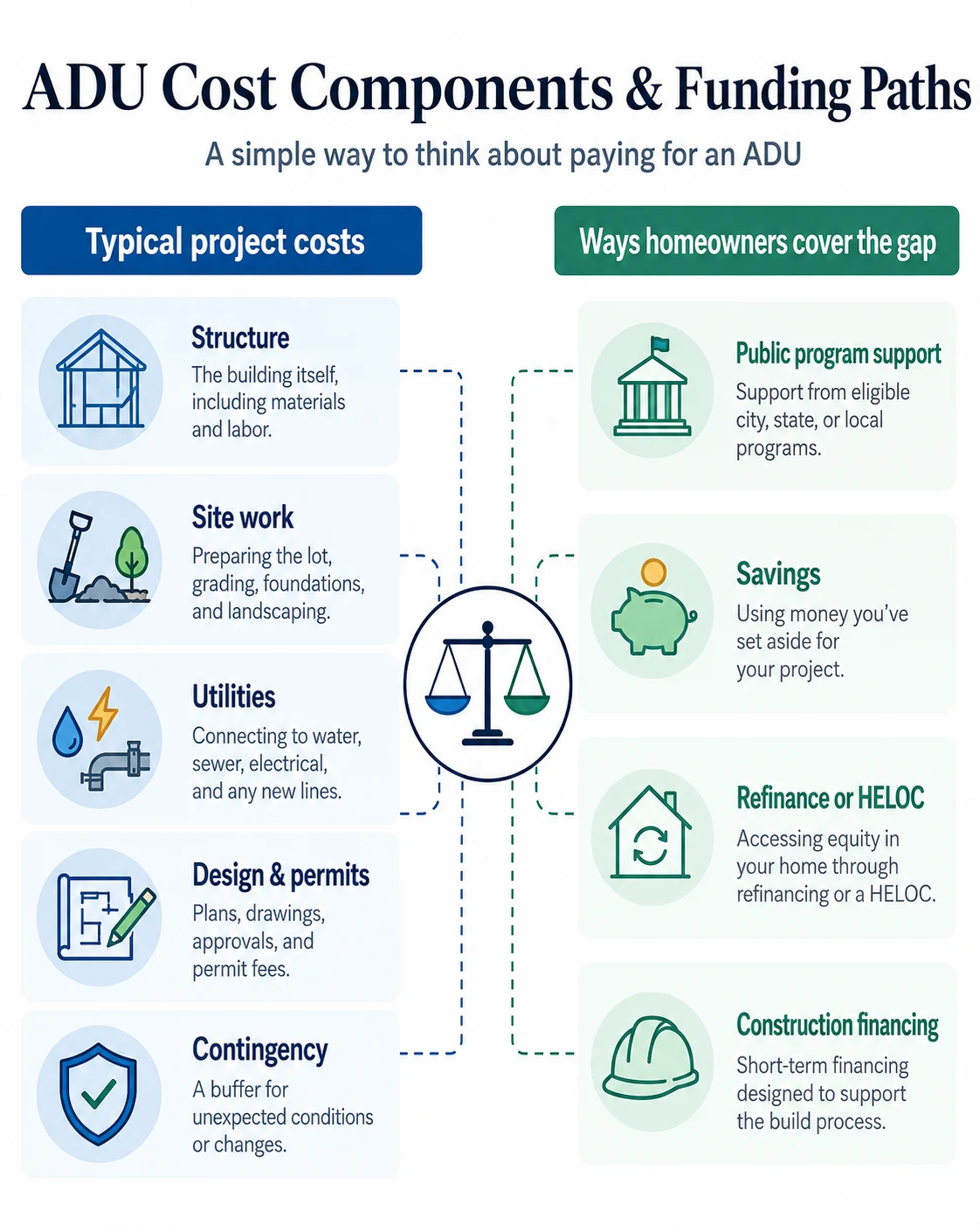

Will Plus One funding cover the cost of a NYC ADU?

Sometimes, but never assume it. The City’s official pre-approved plan estimates range from $85,000–$100,000 for the smallest detached studio to $550,000–$650,000 for the largest — and every estimate excludes site connections and site-specific costs. The $395,000 program maximum is a ceiling, not a promise.

This is the section that prevents the most expensive mistake homeowners make: budgeting off a sticker price that was never meant to be all-in.

Our verified Plus One Funding Gap table

We opened the official ADU for You Pre-Approved Plan Library and recorded each plan’s published construction-cost range, then calculated the midpoint and midpoint cost per square foot, and compared each to the $395,000 maximum. These are construction estimates only — they exclude site connections (water, sewer, gas, electric laterals) and site-specific costs like excavation, foundation, drainage, and flood-resistant work. We verified the low and high endpoints directly on the plan pages.

| Pre-approved plan | Size / type | Published cost range | Midpoint | Midpoint $/sf | vs. $395K max (before site costs) |

|---|---|---|---|---|---|

| Xanadu | 300 sf detached studio | $85k–$100k | $92.5k | ~$308 | Well under max |

| SMART LOFT | 343 sf detached studio | $100k–$120k | $110k | ~$321 | Well under max |

| Still Point | 472.5 sf detached 1BR | $100k–$140k | $120k | ~$254 | Well under max |

| Grand ADU | 785 sf detached 2BR over garage | $160k–$230k | $195k | ~$248 | Under max |

| Studio ADU NYC | 439 sf detached studio | $185k–$265k | $225k | ~$513 | Under max |

| Roof for Two | 406 sf attached 1BR | $215k–$275k | $245k | ~$603 | Under max |

| SITU ADU | 280 sf prefab detached studio | $220k–$280k | $250k | ~$893 | Under max |

| CDA Studio | 336 sf attached studio | $250k–$310k | $280k | ~$833 | Under max |

| CDA One Bed | 600 sf detached 1BR | $360k–$430k | $395k | ~$658 | At the edge; high end exceeds max |

| Far Nordic ADU | 600 sf detached 1BR over garage | $390k–$450k | $420k | ~$700 | Exceeds max before site costs |

| Maisel House | 400 sf detached studio/1BR over garage | $550k–$650k | $600k | ~$1,500 | Above max before site costs |

Source: NYC ADU for You Pre-Approved Plan Library, plan pages, verified May 26, 2026. Plan costs exclude site connections and site-specific costs and are not bids or guarantees; the library expands as DOB approves more designs.

What the numbers tell you: across these verified plans, the median midpoint is about $245,000 and the average midpoint is roughly $267,000. Eight of the eleven plans carry a published high-end estimate at or below $395,000 before site costs; three exceed it. Translation: many efficient detached cottages and conversions fit comfortably inside the program ceiling on construction alone — but the plan price is a starting point, not an all-in bid.

Why “under $395,000” is not the same as “fully covered”

The plan estimate may exclude utility laterals, grading and drainage, excavation, foundation surprises, flood-resistant elevation, and main-house electrical upgrades. For many smaller PAPL designs, the published estimate leaves real room under $395,000 before site work. For larger or complex builds — anything needing serious site work, flood elevation, or MDL upgrades — expect a funding gap you ’ll need to cover with savings, a HELOC, or a construction loan. The program is generous; it is not bottomless.

Run the NYC Plus One Funding Gap Checker → see if your project lands “likely covered,” “near the edge,” or “likely gap.”

Pick a plan, add your borough and a site-cost risk flag, choose your loan path, and see where your numbers fall against the $395,000 ceiling.

Check the funding gap for your project →If your project may exceed the ceiling, understand how homeowners cover the gap. We maintain a plain-English guide to NYC ADU financing lanes — construction loans, cash-out refinances, and renovation financing — written as path education, not lender rankings.

Explore NYC ADU financing paths → Compare construction-loan, refinance, and renovation options.

Affiliate disclosure (repeated near financing content): The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our recommendations are based on independent research and are never influenced by compensation. We present financing as educational lanes; we do not rank lenders by compensation, and nothing here is a quote, an offer, or a guarantee of any rate, payment, or approval.

What strings come with the money?

Selected homeowners take on real, multi-year obligations: a primary-residency requirement of at least 270 days per year, an ownership/occupancy commitment of 10 years (or 15 years under a regulatory agreement), a prohibition on renting out both units, mandatory landlord training, and — on the deferred-forgivable loan — a 15-year rent restriction. Selling to a non-eligible buyer or doing a cash-out refinance during the loan term triggers repayment.

Read this carefully, because these strings are exactly why Plus One is perfect for some owners and wrong for others.

| Restriction | What it actually requires | Who should think twice |

|---|---|---|

| Owner-occupancy | You must occupy the main home or the ADU as your primary residence | Investors; anyone planning to move out |

| 270 days/year residency | The home must genuinely be where you live | Seasonal or part-time residents |

| No renting both units | Owner occupies one; only the other can be rented | Owners wanting two full rental incomes |

| Rent cap (forgivable loan only) | New ADU rented at 100% AMI; increases capped at 2%/year; for 15 years | Owners seeking maximum market rent |

| 10-/15-year ownership hold | Maintain ownership & primary residence for the term | Owners likely to sell within a decade |

| Sale / cash-out refi trigger | Selling to a non-eligible buyer or cash-out refinancing repays the loan immediately | Owners planning to tap equity or sell soon |

| Approved professionals only | You cannot bring your own architect or contractor | Owners with a builder they trust already |

| Mandatory training & affidavits | Landlord training class + annual residency certifications | Owners wanting zero public oversight |

A few of these deserve emphasis:

- You cannot use your own contractor or architect. Per the FAQ, Restored Homes HDFC provides the list of program-approved architects and general contractors. This is non-negotiable inside Plus One.

- A cash-out refinance triggers repayment. If part of your long game was to pull equity out of the house in a few years, Plus One conflicts with that.

- Family occupancy can soften the rent rules. If you’re housing a parent or adult child rather than a market tenant, family members occupying the unit may be exempt from certain rent provisions.

Here’s the hope, because there genuinely is some. If those strings stop you, you are not stuck — you’ve simply learned that the repayable loan path (no regulatory agreement, no rent cap) or building privately is your better road. For the owner who wants to create stable long-term housing, keep their home, and bring in steady income, these “strings” are mostly just the shape of a public program doing what it’s designed to do: up to $175,000 you never repay, plus a loan that can drop to 0% interest.

See whether Plus One fits your long-term plan → Get your free ADU report.

If the strings don’t work for you, we’ll point you to the path that does.

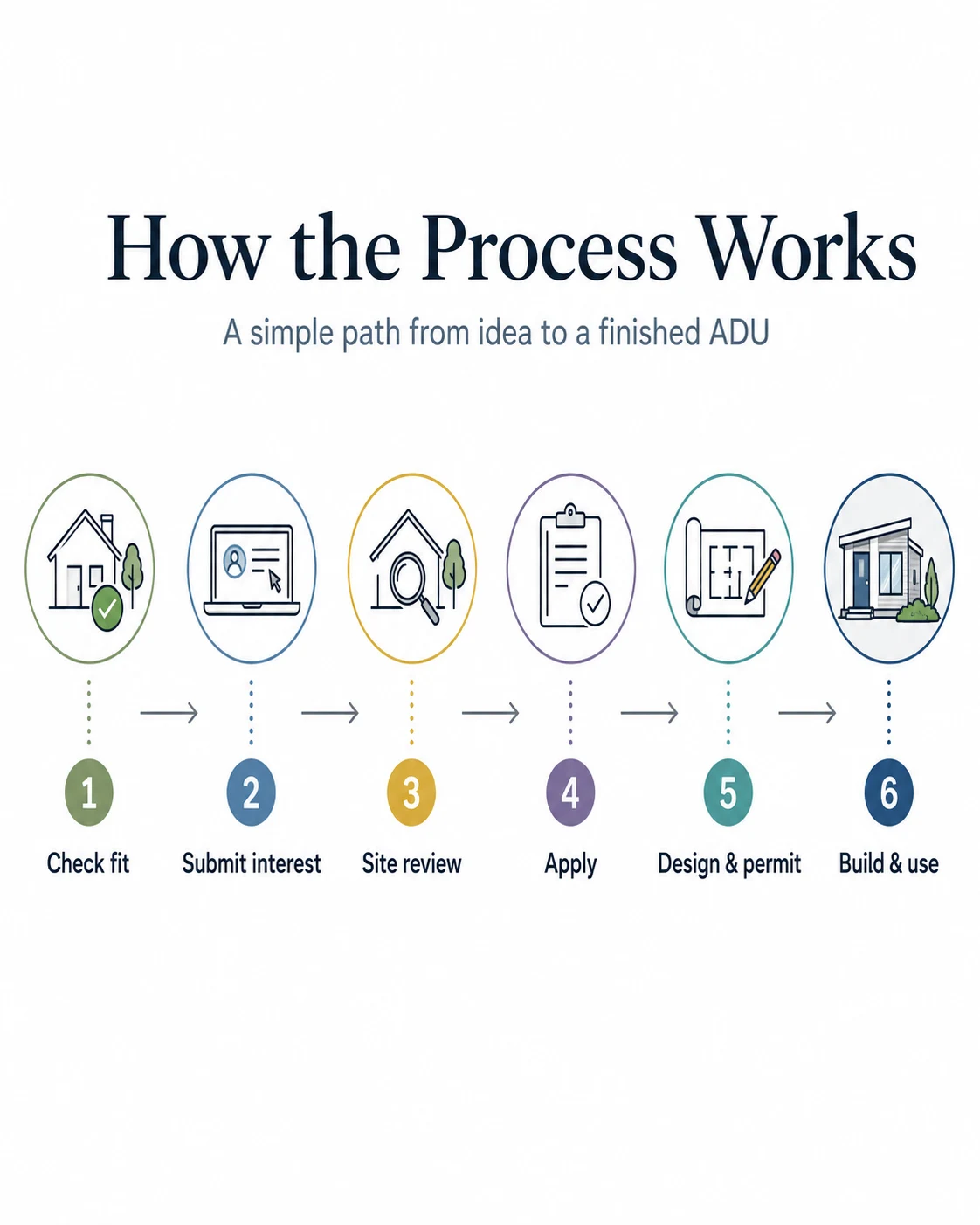

How do I apply without wasting the $200 fee?

Start with the free online interest survey on HPD’s Plus One ADU page — never with the paid application. HPD conducts an initial site-feasibility review; only homeowners who appear eligible are invited to submit the full application, which includes the $200 non-refundable fee. Submit early: HPD reviews on a rolling basis, funding is limited, and the interest window closes June 12, 2026.

The order of operations is the whole game here. The $200 fee comes after the free screen — so the smart move is to make sure your property can plausibly qualify before you ever reach a paid step.

The 10-step Plus One sequence

Per the FAQ, selected participants should expect this multi-year path. Completing these steps does not guarantee funding or approval.

- 1

Online interest survey (free)

You submit basic info about you and the property on HPD’s Plus One ADU page

- 2

Program application + $200 fee

Only if invited after HPD’s initial feasibility review. Non-refundable.

- 3

Financial review

Income, debt, mortgage, obligations reviewed to determine loan structure

- 4

Home inspection

If the property fails due to unforeseen barriers, you cannot proceed

- 5

Program approval letter + Developer Agreement

Formal terms begin here

- 6

Pre-development: design

Using program-approved architects (from Restored Homes’ list)

- 7

Pre-development: contractor bidding

Program-approved general contractors only

- 8

Pre-development: loan processing & closing

Loan documents prepared and signed

- 9

Construction

Restored Homes provides pre- and post-construction support including a one-year warranty

- 10

Tenant approval & monitoring

Ongoing annual residency certifications and rent compliance

You’ll also complete a homeownership training class during the process, and Restored Homes provides a one-year post-construction warranty.

Documents to have ready (so you’re not scrambling)

- The $200 non-refundable fee

- Completed Plus One ADU application form + Right of Entry form

- Proof of primary residence and a homeowner occupancy affidavit

- Proof of valid homeowner’s insurance

- Proof of income: four consecutive paystubs, a W-2, and income tax returns for the last two years (plus documentation of any supplemental, self-employment, or unemployment income)

- Absent Deed Holder form / death certificate for a deceased deed-holder, if applicable

- Designated Communication form

Our free pre-application checklist (before you pay anything):

- Resolve any obvious municipal arrears or building violations

- Pull your flood-zone and zoning-district status

- Confirm your basement ceiling height if a basement ADU is your plan

- Decide which unit you’ll occupy

Doing this first is how you avoid burning the $200 on a project that can’t clear feasibility.

Run a free feasibility check before the paid step → Get your free ADU report.

Find your likely disqualifiers now, while the fix is still free.

How do NYC ADU permits work after City of Yes?

ADU applications under Local Law 127 of 2024 are filed in DOB NOW: Build, which went live for ADU filings on September 30, 2025. You (or your licensed professional) create an Alt-CO-GC or New Building-GC job, and a registered design professional handles the plans. Choosing a pre-approved design from the City’s library simplifies approval because DOB has already reviewed the design generically for code compliance.

- Filing path: Alt-CO-GC (alteration with a new or amended Certificate of Occupancy) or New Building-GC, submitted in DOB NOW: Build. The application asks whether the scope includes an ADU and, if so, the pre-approved plan number, ADU location, and where the main entrance opens.

- Who files: a Registered Design Professional (RDP) — a licensed architect or professional engineer. Even homeowners who don’t use Plus One can hire an RDP to file plans and pull permits, building as-of-right if the project complies.

- Occupancy classification: the ADU is recorded under Residential Occupancy Group R-2 or R-3 on the Schedule of Occupancy.

- Pre-approved plans: launched with nine DOB-reviewed detached-cottage designs in March 2026 and expanding; choosing one connects you with the RDP who created it for site-specific approval.

What building-code issues can make a NYC ADU fail?

Beyond zoning, several NYC Building Code requirements can make an ADU infeasible or far more expensive: sprinkler triggers (especially via the Multiple Dwelling Law), emergency escape and rescue openings, a separate entrance, shared utilities with separate shutoffs, minimum habitable-room ceiling heights, radon and vapor testing for basement/cellar units, Fire Department access paths, and building-separation requirements. These are governed by Building Code Appendix U and 1 RCNY §105-08.

Zoning tells you whether you can build; the Building Code often decides what it costs. The items that most often derail a project:

- Sprinklers. Triggered most commonly when a two-family conversion falls under the MDL. Retrofitting sprinklers can be one of the single most expensive line items.

- Egress and emergency escape/rescue openings. Every habitable ADU needs compliant means of egress; basements and attics are where this gets hard.

- Separate entrance and Fire Department access. ADUs require their own entrance and an accessible path.

- Utilities. Shared utilities are allowed but generally need separate shutoffs/controls for the ADU.

- Basement/cellar specifics. Minimum ceiling height (7 ft), plus radon and vapor certification for subgrade units.

- One-family vs. two-family basement nuance. A basement/cellar ADU may be possible in an existing one-family home under Building Code Appendix U, or in a new one-family home under 1 RCNY §105-08 — but in a two-family home, a basement/cellar ADU can trigger R-2 classification and the MDL. (Source: NYC DOB ADU FAQ.)

The practical takeaway: have your RDP flag sprinkler and MDL exposure before you commit to a design. It’s the cheapest insurance you’ll buy on the whole project.

Should I use a pre-approved plan or a custom ADU design?

A pre-approved plan from the City’s library speeds up permitting because DOB has already reviewed it generically for code compliance, but it is not an automatic approval — you still need a registered design professional and site-specific review. A custom design makes sense for odd lots, basements, tight access, or family-specific layouts, but carries more design uncertainty and potentially higher cost.

| Option | Best for | Watch out for |

|---|---|---|

| Pre-approved plan (PAPL) | Standard backyard or garage-style concepts on a lot that fits an existing design | Still needs site-specific review; published cost excludes site work |

| Custom design | Odd lots, basements, tight access, existing-structure conversions, family layouts | More design uncertainty, potentially higher cost and longer timeline |

| Wait / don’t build | Lots with major flood, MDL, violation, or occupancy conflicts | The smart “no” — saves you from a project that can’t qualify |

A “pre-approved” plan saves time on the front end of permitting, but it never removes the need to prove it works on your specific lot. Treat it as a head start, not a finish line.

What if I don’t qualify, funding runs out, or I miss the deadline?

Not qualifying for Plus One does not mean you can’t build an ADU. Per HPD’s own FAQ, any homeowner can move forward independently by hiring a licensed professional engineer or registered design professional to file plans and pull permits with DOB — as long as the project complies with City of Yes zoning and the Building Code. ADUs are now allowed as-of-right on most qualifying 1–2 family lots, which means no variance and no community-board hearing.

| If your blocker is… | Your best next path | Where we send you |

|---|---|---|

| Income above the priority band | Compare private financing lanes | NYC ADU financing guide |

| Funding window closed | Join HPD’s update list + compare private financing | NYC ADU financing guide |

| You want no rent/occupancy restrictions | Private financing + build as-of-right | Best ADU financing options |

| Senior or fixed-income homeowner | Lower-payment / no-monthly-payment education | ADU financing for seniors · Fixed-income homeowners |

| Low-income but not selected | Grant and subsidy alternatives | ADU financing for low-income homeowners |

Explore ADU financing paths → Compare refinance, renovation, and construction-loan options.

Use this if Plus One isn’t a fit, funding’s gone, or you simply want a private path with fewer program restrictions. Financing lanes explained plainly — no rankings, no rate promises.

Can I legalize an existing illegal basement apartment?

Possibly — through a separate, narrow path, but not right now. Local Law 126 of 2024 created a basement/cellar legalization pathway (run by DOB) for currently illegal but occupied units that existed before April 20, 2024. The statutory deadline to enter is April 20, 2029 — but DOB is not currently accepting legalization or new cellar ADU applications until the Housing Maintenance Code amendment and DOB rules are promulgated and DOB NOW functionality is available.

This is a real opportunity for a specific group of owners, with two hard limits to understand. First, it isn’t open yet — DOB’s ADU page (last revised 09/30/25) states legalization and new cellar ADU applications “are not currently being accepted” pending rulemaking. Second, it has geographic limits. Eligibility is restricted to specific Community Districts:

Bronx

CDs 9, 10, 11, 12

Brooklyn

CDs 4, 10, 11, 17

Manhattan

CDs 2, 3, 9, 10, 11, 12

Queens

CD 2

The unit must also sit outside the coastal flood zone and the 10-year rainfall flood-risk area. Required upgrades (once the program opens) include hardwired smoke/CO detectors, water sensors and alarms, automatic sprinklers, a compliant stairwell and at least one means of egress, a 7-foot minimum ceiling height, vapor/radon certification, and an amended legal Certificate of Occupancy — with all code upgrades completed within 10 years. One upside: basement units legalized through this program are exempt from MDL triggers. Homeowners in this program may also be eligible for Plus One financing. If your property isn’t in one of the listed Community Districts, this specific path isn’t open to you.

What mistakes make NYC ADU projects more expensive?

The costliest mistake is treating the $395,000 maximum as guaranteed, all-in money before verifying property eligibility. In NYC, flood maps, the Multiple Dwelling Law, basement ceiling and flood rules, utility connections, open violations, lot access, and site work routinely affect the budget as much as the published ADU plan price.

| Mistake | What it costs you | How to prevent it |

|---|---|---|

| Assuming $395,000 is guaranteed and all-in | Bad budgeting, stalled project | Treat it as a ceiling minus site costs |

| Picking a plan before a feasibility check | Plan may not fit lot or zoning | Screen the property first |

| Ignoring flood maps | Subgrade/backyard ADU gets blocked | Check FEMA SFHA, Coastal Flood Risk, and DEP 10-year layers |

| Banking on Airbnb income | Owner-occupancy and rent rules conflict | Plan for long-term housing |

| Planning to rent both units | Violates owner-occupancy rule | Decide which unit you’ll live in before applying |

| Overlooking the MDL | Two-family conversions can become cost-prohibitive | Ask about MDL and sprinklers before design |

| Forgetting site costs | Plan estimate understates true cost | Add utility, drainage, foundation, and access allowances |

| Applying with arrears/violations unresolved | Application stalls or fails inspection | Clear municipal/mortgage/violation issues early |

How will an ADU affect my property taxes?

Adding an ADU will increase your property’s assessed value and therefore your property taxes over time, but Plus One participants benefit from a partial tax exemption during the first ten years after construction is completed. Owners may also apply separately for homeowner property-tax exemptions and benefits through the NYC Department of Finance.

The increase phases in rather than hitting all at once, thanks to the ten-year partial exemption. As with everything tax-related, your actual outcome depends on your assessment and your specific exemptions, so confirm the details with the NYC Department of Finance for your property. (Source: HPD Plus One ADU FAQ; NYC Department of Finance.)

Is the Plus One ADU program legitimate? Who runs it?

Yes, it’s a legitimate government program. Plus One is administered by NYC Housing Preservation and Development (HPD) in partnership with Restored Homes HDFC, with grant funding from New York State Homes and Community Renewal (HCR). It’s part of New York State’s $85 million statewide Plus One ADU initiative, which HCR reports now spans 14 partners working to create more than 550 ADUs statewide, including 37 projects in New York City.

If your first instinct on hearing “the city will give you $395,000” was this sounds too good to be true — that’s healthy skepticism, and the answer is reassuring. The money flows through established government agencies and a long-standing nonprofit administrator, and it sits inside a multi-year, multi-partner state program with public reporting. The catch isn’t legitimacy; it’s the eligibility gates and strings we’ve detailed above. (Source: NYC HPD/DOB press release 017-26; NYS HCR.)

Frequently asked questions

Is the NYC Plus One ADU Program open right now?

Yes. HPD reopened intake on March 18, 2026, and accepts interest submissions through Friday, June 12, 2026, while limited funding lasts. The first step is a free online interest survey. (Source: HPD/DOB press release, March 18, 2026.)

How much money can I get from Plus One?

Up to $395,000 total — a grant of up to $175,000 from NYS HCR plus a City loan of up to $220,000. The maximum is a ceiling; it does not guarantee approval or full project coverage. (Source: HPD Plus One ADU FAQ.)

Is Plus One a grant or a loan?

Both. The HCR grant portion (up to $175,000) isn't repaid. The City loan (up to $220,000) is either an amortizing loan with no rent restrictions, or a deferred-forgivable loan with a 15-year rent restriction at 100% AMI. (Source: HPD FAQ; Term Sheet.)

Who qualifies?

NYC owner-occupants of 1–2 unit homes earning up to 165% AMI, who are current on their mortgage and city charges and carry valid homeowner's insurance, on a property that can legally add a unit. HPD's FAQ says homeowners up to 100% AMI are currently prioritized; the program page references preference at or below 120% AMI. (Source: HPD FAQ; HPD program page.)

What's the income limit in dollars?

At 165% AMI (current HPD chart): $187,110 (1 person), $213,840 (2), $240,570 (3), and $267,300 (4). The 100% AMI figures are $113,400, $129,600, $145,800, and $162,000 respectively. (Source: NYC HPD AMI chart.)

Can I use my own contractor or architect?

No. Inside Plus One, Restored Homes HDFC provides a list of program-approved architects and general contractors. (Source: HPD FAQ.)

Can I build an ADU if I don't qualify for Plus One?

Yes. You can hire a licensed engineer or registered design professional to file plans and pull DOB permits in DOB NOW: Build, building as-of-right under City of Yes if your project complies. (Source: HPD FAQ; NYC DOB.)

How big can a NYC ADU be?

Up to 800 square feet, with no minimum. A detached ADU also can't cover more than one-third of your required rear yard. (Source: HPD FAQ; Zoning Resolution §23-341.)

How tall can an ADU be?

One story / 15 feet, or two stories / 25 feet if a parking space sits below part of the unit. (Source: HPD FAQ.)

Do I need to add parking?

No. No additional parking is required to build an ADU. (Source: HPD FAQ.)

Can I rent out both my house and the ADU?

No. You must occupy either the main home or the ADU as your primary residence; only the other unit can be rented. (Source: HPD FAQ.)

Can I house my aging parent instead of renting the unit?

Yes — and family members occupying the unit may be exempt from certain rent-restriction provisions that apply to market tenants. (Source: Plus One ADU Term Sheet.)

What happens if I sell or refinance?

Selling to a non-eligible buyer or doing a cash-out refinance during the loan term triggers repayment of the loan. (Source: HPD FAQ.)

How long does the whole process take?

Selected participants should expect a multi-year process across feasibility, application, design, bidding, financing, construction, and lease-up. (Source: HPD FAQ.)

Where do I file the ADU permit?

ADU applications under Local Law 127 are filed in DOB NOW: Build (live for ADUs since September 30, 2025) as an Alt-CO-GC or New Building-GC job. (Source: NYC DOB.)

Are the pre-approved plans automatically approved?

No. Library designs are reviewed by DOB for general code compliance, but you still need a registered design professional and site-specific review. (Source: ADU for You / PAPL.)

Can I legalize an existing illegal basement apartment?

Eventually, through Local Law 126's legalization pathway in specific Community Districts, if the unit existed by April 20, 2024 and you enter by April 20, 2029 — but DOB is not accepting these applications yet, pending rulemaking. (Source: NYC DOB.)

Methodology

Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We built this guide directly from primary government sources: the NYC HPD Plus One ADU program page, the HPD/DOB press release dated March 18, 2026, the Plus One ADU FAQ (last updated September 4, 2025), the Plus One ADU Term Sheet, HPD’s Area Median Income chart, the NYC Department of Buildings ADU page and FAQ, the ADU for You Pre-Approved Plan Library, and City of Yes for Housing Opportunity materials from the NYC Department of City Planning. We used homeowner forums and community discussions only to understand the questions and worries real New Yorkers have — never as a source for laws, costs, eligibility, or financing terms.

For the funding-gap table, we opened the official pre-approved plan pages, recorded each published cost range and square footage, calculated the midpoint and midpoint cost per square foot, and compared each to the published $395,000 maximum. We verified the lowest and highest plan costs directly on their plan pages. Published plan costs are construction estimates that exclude site connections and site-specific work; they are not all-in bids or guarantees. Where official sources differed — the AMI priority band and the labeling of certain flood layers — we presented both and pointed you to the live source to confirm. This page is educational and is not legal, tax, financial, or construction advice.

Last updated: May 26, 2026. Last verified: May 26, 2026.

Sources

- NYC HPD — Plus One Ancillary Dwelling Unit (ADU) Program (program page; eligibility; application status)

- NYC HPD / DOB — Press release 017-26 (March 18, 2026): reopening, $395K, June 12 deadline, nine launch designs

- NYC HPD — Plus One ADU FAQ (last updated September 4, 2025): income/priority, property rules, basement & MDL rules, loan terms, strings, application steps, documents

- NYC HPD — Plus One ADU Term Sheet: loan structure, interest mechanics, residency, rent restriction

- NYC HPD — Area Median Income chart (current published figures)

- NYC Department of Buildings — Ancillary Dwelling Units page (last revised 09/30/25) and ADU FAQ: DOB NOW filing, Special Bay Ridge, subgrade flood areas, Appendix U, legalization status

- NYC ADU for You — Pre-Approved Plan Library and plan pages (verified May 26, 2026)

- NYC Department of City Planning — City of Yes for Housing Opportunity (adopted December 5, 2024)

- New York State Homes and Community Renewal — statewide Plus One ADU initiative

- Regional Plan Association — analysis of NYC lots eligible for ADUs

Not sure where to start?

See what’s possible at your address — get your free ADU report in 60 seconds.

Get My Free ADU Report →Or download the free NYC ADU Starter Kit — the eligibility checklist, document prep list, flood-zone lookup steps, and the Plus One application sequence in one printable guide.