ADU Financing for Multifamily Property: Your 2026 Loan Path by Unit Count

An independent research guide from Dwelling Index — an independent research resource covering ADU financing, costs, and regulations.

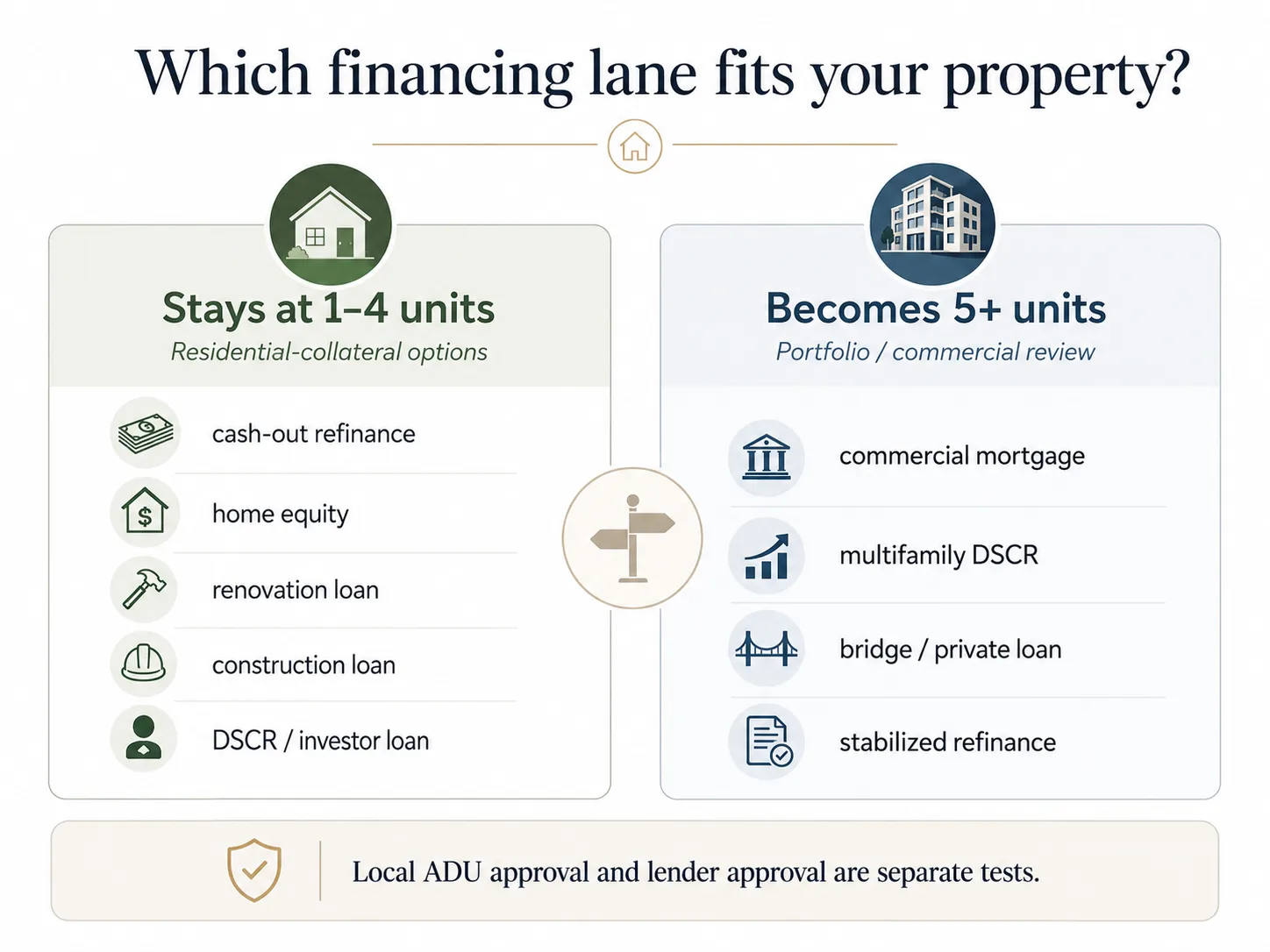

The short answer: ADU financing for multifamily property depends on one number above all others — your unit count after the ADU is built. If your property stays at 1–4 units, you stay in the residential-collateral world: owner-occupants test cash-out refinance, renovation loans, construction-to-permanent, or home equity, while investors test DSCR, investor construction, or private/bridge loans. The moment a fifth legal unit appears — or you already own a 5+ unit building — the ordinary residential agency lane generally disappears and you move to portfolio, bridge, or commercial multifamily financing, with a higher debt-service-ratio bar (typically DSCR 1.15+) and often lower LTV (~75%). Confirm your after-build unit count with a lender before you pay for plans.

Which lane is yours? (start here)

| Your property | Your financing lane |

|---|---|

| 1-unit home + ADU | Owner-occupant residential (refi, renovation, construction, home equity) |

| Duplex or triplex + ADU, staying ≤ 4 units | 2–4-unit residential lane |

| Fourplex + ADU | Fifth-unit risk → portfolio/commercial review |

| Non-owner-occupied 2–4 unit rental + ADU | Investor lane (DSCR, investor construction, private/bridge) |

| Existing 5+ unit apartment building | Commercial multifamily lane |

Most guides about ADU financing quietly assume one thing: that you live in a single-family house and can tap your home equity. If you own a duplex, a fourplex, or a small apartment building, that advice collapses on contact. We built this page for the people the cracks swallow — the multifamily owner-occupants and investors who keep reading "just get a HELOC on your home" and thinking, that's not my situation.

Here's what's actually true, verified against Fannie Mae's own Selling Guide, Freddie Mac and FHA guidance, the FHFA's 2026 loan limits, and California's codified ADU statute: a multifamily property can absolutely support an ADU loan. But the rules fork hard at the four-unit line, and a lot of owners spend money on plans and permits before discovering which side of that line their project lands on. The goal of this guide is to put you on the right side of it before you spend a dollar.

A quick term, defined once: an accessory dwelling unit (ADU) is a self-contained additional living unit — typically with its own cooking, sleeping, bathing facilities, and access — on a lot that already has housing. It can be detached (a standalone backyard unit, sometimes called a DADU), attached (sharing a wall with the main building), or a conversion (turning a garage, basement, or storage room into living space). A JADU (Junior ADU) is a California-specific category that converts space within the main dwelling and is generally limited to 500 sq ft.

Can you get ADU financing for multifamily property?

Answer: Usually yes — but the loan you'll use is decided by how a lender classifies your property, not by the word "ADU." Properties at 1–4 units use residential financing (conventional, FHA, renovation loans, construction loans, and DSCR loans for investment cases). Properties at 5+ units use commercial financing. The single biggest factor is whether the finished property stays at four units or fewer.

The obstacle is rarely whether financing exists. It's matching your specific property to the right lane, because the wrong lane wastes weeks and sometimes thousands of dollars in plans for a loan you were never going to get.

The fork is simple to state and expensive to ignore. Conventional loans backed by Fannie Mae and Freddie Mac, and FHA loans, are built around one- to four-unit residential properties. That's the entire residential agency framework — the loan limits, the appraisal forms, the underwriting. Stay at four units or fewer and you have a deep menu of options. Cross into five units and that menu is replaced by commercial real estate lending, which underwrites the property's income, not your household income — and comes with tighter LTV, higher minimum DSCR, and shorter amortization.

That's the whole map. Everything else on this page is the detail inside one of those two lanes.

See what's possible at your address before you pick a lane. A property check confirms what your specific parcel may support — so you walk into a lender conversation knowing your unit count, not guessing it.

See What You Can Build → Get Your Free ADU ReportCan you build an ADU on a multifamily property?

Answer: In a growing number of states and cities, yes — ADUs are now permitted on lots with existing multifamily buildings, not just single-family homes. In California, Government Code § 66323 (as amended by SB 1211, effective January 1, 2025) requires local agencies to allow up to eight detached ADUs on a lot with an existing multifamily dwelling — capped at the number of existing units — plus interior-conversion ADUs equal to at least one unit or up to 25% of existing units.

Two government systems answer two different questions. Zoning answers "can this be built here?" Lending answers "can this collateral and this borrower fit a loan program?" They are not the same test, and one can say yes while the other says not yet.

California is the clearest example of the gap. Under § 66323, a four-unit apartment building can add up to four detached ADUs; a twelve-unit building can add up to eight (capped at eight regardless of building size). Separately, owners can convert non-livable space — storage rooms, boiler rooms, passageways, attics, basements, garages — into ADUs equal to at least one unit or up to 25% of the existing unit count, approved ministerially. That sounds like a feast for an investor. The catch is that state law can hand you the right to build far more units than a residential mortgage lender will finance through an ordinary loan.

Outside California, multifamily ADU allowances vary widely by state and municipality. Some states have followed California's lead; many still write ADU rules around single-family lots only. Do not assume your duplex or fourplex qualifies until your city's planning department confirms it.

If you're not in California, four questions close the loop with your city planning department:

- Does this parcel allow ADUs on a multifamily lot at all?

- Are detached and conversion ADUs both allowed here?

- What's the maximum ADU count for this property?

- Will the ADU be treated as a separate legal unit for permitting, addressing, and utility purposes?

That fourth question quietly determines your financing lane — because a "separate legal unit" is exactly what pushes a fourplex to five. For a starting read on ADU types, see our overview of what an ADU is and the main types.

The 30-second classification test. Before you talk to any lender, answer these eight questions:

- How many legal units exist on the property today?

- How many legal units will exist after the ADU is built?

- Will you (the owner) live in one of the units?

- Is the property owned in your personal name, an LLC, or another entity?

- Is the ADU detached, attached, or a conversion of existing space?

- If you're in California, is the unit rentable for terms longer than 30 days?

- Does projected ADU rent need to help you qualify for the loan?

- Will the total legal unit count exceed four?

That last question is the hinge the whole page turns on.

Which financing path fits your multifamily property — the unit-count fork

Answer: The right financing path depends far less on the ADU itself than on your property's classification before and after the build. Properties at 1–4 units use residential financing; properties at 5+ units use commercial financing with a higher debt-service-ratio bar (typically 1.15+) and a lower loan-to-value cap (~75%). The table below maps every common multifamily scenario to a first lane and a backup lane.

What Fannie Mae, Freddie Mac, and FHA each allow on multi-unit properties

| Agency | What it allows on multi-unit properties | Key condition |

|---|---|---|

| Fannie Mae | Up to 3 ADUs on 1-unit properties; ADUs on 2–3 unit properties if primary units + ADUs ≤ 4 | Effective Mar 31, 2026, only for lenders using UAD 3.6 policy |

| Freddie Mac | One ADU on 1-, 2-, and 3-unit properties | ADU must be legal, legal non-conforming, or in a no-zoning area |

| FHA | Rental-income treatment for a 1-unit-with-ADU or 2–4 unit property; 203(k) can finance adding/renovating an ADU | Appraiser classification and project scope govern eligibility |

Sources: Fannie Mae SEL-2025-10; Freddie Mac ADU Fact Sheet (Feb 2026); HUD Mortgagee Letter 2023-17. Verified May 2026.

If you own an owner-occupied duplex or triplex

This is the most workable scenario, and 2026 made it meaningfully better. Fannie Mae's Selling Guide UAD 3.6 Policy Supplement, announced in SEL-2025-10, allows two- to three-unit properties to include ADUs, provided the number of primary dwelling units plus ADUs does not exceed four — a configuration previously ineligible. It's effective March 31, 2026. Freddie Mac allows one ADU on eligible one-, two-, and three-unit properties when the unit complies with zoning and land-use requirements. (Sources: Fannie Mae SEL-2025-10; Freddie Mac ADU Fact Sheet, Feb 2026. Verified May 2026.)

One critical caveat: Fannie's expanded ADU criteria are only available to lenders utilizing UAD 3.6 policy. If a loan officer tells you a duplex-plus-ADU "can't be done," it may be that their shop hasn't moved to the new policy yet — not that the rule forbids it. Ask directly: "Are you originating under UAD 3.6 policy?" That single question can change your answer.

If you own a fourplex adding an ADU

This is the highest-risk residential category. A fourplex already sits at the top of the 1–4-unit residential band. Add one ADU and you very likely create a fifth legal unit — which can push the entire project out of the conventional and FHA residential world and into portfolio, investor, or commercial financing. Local zoning might happily approve it. The financing conversation is the one that changes.

Before you spend on architectural plans, get a lender to confirm how they'll classify the after-build property. That single question can save you tens of thousands.

If you own a non-owner-occupied 2–4 unit rental

Your first lane is usually a DSCR loan — Debt Service Coverage Ratio financing, which qualifies the loan on the property's rental cash flow rather than your personal income. On 1–4 unit properties, DSCR loans commonly reach up to ~80% LTV and accept a DSCR as low as ~1.0. Investor construction loans, private/bridge debt, and cash-out refinances round out the options. (Sources: Ridge Street Capital, American Heritage Lending, Lendmire DSCR guides, 2025–2026. Verified May 2026.)

Two honest notes. First, Fannie Mae caps second-home and investment-property borrowers at 10 financed one- to four-unit residential properties when the borrower is personally obligated; many DSCR programs don't use that same agency financed-property cap — though lender aggregate exposure, reserve, credit, and max-loan limits can still apply. (Source: Fannie Mae Selling Guide B2-2-03. Verified May 2026.) Second, projected ADU rent may matter more for your exit (a stabilized refinance after lease-up) than for the construction loan itself.

If you own an existing 5+ unit apartment building

Once your building has five or more units, lenders treat it as commercial real estate, and the residential playbook is gone. You're choosing between a commercial mortgage from a bank, credit union, or specialty lender, and a multifamily DSCR loan (some investor/multifamily DSCR products cover small 5–8-unit properties, but limits are lender-specific). (Source: theLender, "Commercial Mortgage vs. DSCR Loan for 5+ Unit Properties," 2026. Verified May 2026.)

Multifamily DSCR programs commonly require a minimum DSCR of 1.15 or higher and cap LTV around 75%. Commercial mortgages may also carry shorter amortization (often 20–25 years), balloon payments at 5, 7, or 10 years, higher closing costs, and recourse or carve-out guarantees, depending on the lender. (Sources: Ridge Street Capital; Lendmire, "DSCR Loan vs Commercial Mortgage," 2026. Verified May 2026.) None of that makes the project bad — it makes it a different underwriting conversation, centered on NOI, reserves, sponsor experience, and stabilized value.

Multifamily ADU Financing Path Matrix (2026)

| Your situation | Lending class | First lane | Backup lane | Key metric | Red flag |

|---|---|---|---|---|---|

| 1-unit primary residence + 1 ADU | Residential | Cash-out refi, renovation loan, construction-to-permanent, HELOC/home equity | FHA 203(k), HomeStyle, CHOICERenovation, local portfolio lender | DTI + program limits; ADU income capped at 30% of qualifying income | Appraiser treats ADU as a separate unit, changing classification |

| 1-unit residence + multiple ADUs | Residential | Fannie Mae path (up to 3 ADUs) where lender uses UAD 3.6 policy | Portfolio lender, construction loan | Effective Mar 31, 2026; lender must be on UAD 3.6 | Many lenders won't have adopted the new policy yet |

| Owner-occupied duplex + 1 ADU | Residential (if total ≤ 4 units) | 2–4-unit residential (conventional/FHA/Freddie) | HELOC if available; local portfolio lender | Total units stay ≤ 4; uses Form 1025 (2–4 unit) appraisal | Lender hasn't adopted Fannie's 2–3 unit ADU expansion |

| Triplex + 1 ADU | Residential (if total ≤ 4 units) | 2–4-unit residential path | Portfolio or investor construction loan | Primary units + ADUs ≤ 4 | Misclassification pushes you to a 5th unit |

| Fourplex + ADU | Often commercial | Portfolio, investor, or commercial review | Commercial multifamily lender | Adding the ADU likely creates a 5th unit → leaves agency lane | Assuming conventional residential still applies |

| Non-owner-occupied 2–4 unit + ADU | Residential (investment) | DSCR (long-term rental), investor construction, private/bridge | Cash-out refi if equity exists | DSCR ~1.0+ on 1–4 unit; up to ~80% LTV; subject 2–4 unit rent uses Form 1025 | Personally-obligated borrowers face a 10-financed-property cap on agency loans |

| Existing 5+ unit apartment | Commercial | Commercial mortgage; multifamily DSCR (some investor products cover 5–8 units, lender-specific) | Bridge-to-permanent | Multifamily DSCR ~1.15+ min; LTV often ~75% | Shorter amortization, balloon at 5/7/10 yrs, possible recourse |

| California multifamily lot + multiple ADUs | Depends on after-build count | If units exceed 4 → portfolio/commercial; if ≤ 4 → residential | Feasibility review + commercial lender | After-build unit count vs. financeable count | State law allows more units than a consumer loan can finance |

Sources: residential/commercial threshold and DSCR mechanics — theLender and Lendmire DSCR guides (2026); LTV and DSCR-ratio norms — Ridge Street Capital multifamily DSCR guide (2025); Form 1007/1025 — Lendmire DSCR glossary and Fannie Mae Selling Guide B3-3.8-01; Fannie 2–3 unit ADU expansion and UAD 3.6 timing — Fannie Mae Selling Guide Announcement SEL-2025-10 (Dec 2025), effective Mar 31, 2026; 30% ADU income cap — Fannie Mae SEL-2025-08 / DU 12.1; 10-financed-property cap — Fannie Mae B2-2-03; Freddie Mac ADU and 30%/75% caps — Freddie Mac ADU Fact Sheet (Feb 2026); CA multifamily ADU law — Gov. Code § 66323, SB 1211, CA HCD 2026 ADU Handbook. All verified May 2026.

A property check reads your property type and local rules and returns what you may be able to build.

See what's possible at your address → Get Your Free ADU ReportWhat loan types can actually pay for a multifamily ADU?

Answer: The realistic options are home equity loans and HELOCs, cash-out refinances, renovation loans (FHA 203(k), Fannie HomeStyle, Freddie CHOICERenovation), construction-to-permanent loans, investor or bridge construction debt, DSCR loans for stabilized rentals, and commercial multifamily financing for 5+ unit properties. The best option is the one that matches your property classification and preserves a safe exit — not the one with the most attractive headline rate.

We present these as lanes, not a ranked list, because the right answer is dictated by your property, not by any lender's marketing. (For the deeper mechanics of each, our ADU financing options guide goes product-by-product.)

Home equity loan or HELOC. A HELOC lets you borrow against equity with a flexible draw schedule that can match construction milestones; a home equity loan gives you a lump sum. Fits an equity-rich owner who wants to keep a low-rate first mortgage untouched. Downside: equity products are harder to get on non-owner-occupied property, and HELOC rates are typically variable.

Cash-out refinance. You replace your existing first mortgage with a larger one and take the difference as cash for the build. Fits an owner for whom replacing the first mortgage still makes sense. Downside: if you hold a low-rate first mortgage, refinancing into today's rate can cost far more over time than the cash is worth. Run the blended cost of debt before you commit.

Renovation loan. FHA 203(k), Fannie Mae HomeStyle Renovation, and Freddie Mac CHOICERenovation roll purchase or refinance and renovation costs into one mortgage. HUD's guidance explicitly lists converting a one-family structure to one-with-an-ADU, adding an attached ADU, and renovating an existing ADU among eligible 203(k) improvements. Downside: the FHA 203(k) Limited program caps rehabilitation costs at $75,000; the Standard 203(k) handles larger projects but adds a required consultant. (Sources: HUD Mortgagee Letter 2023-17; HUD Mortgagee Letter 2024-13. Verified May 2026.)

Construction-to-permanent loan. A single loan funds the build, then converts to a permanent mortgage on completion. Fits larger, fully permitted projects. Downside: underwriting leans on plans, budget, contractor, draw schedule, permits, and an as-completed appraisal; if your after-build unit count doesn't fit the lender's box, it stalls.

Private, bridge, or investor construction loan. Short-term, faster-closing debt for investors. Fits non-owner-occupied or speed-sensitive projects. Downside: requires more equity, a clear exit strategy, and higher risk tolerance.

DSCR loan or stabilized rental refinance. Qualifies on property cash flow, not personal income; LLC-friendly. Fits the exit — after the ADU is built, permitted, leased, and producing income, you refinance into a long-term DSCR loan. Downside: it's an exit or refinance strategy, not a guaranteed construction source for a pre-permit concept.

Commercial multifamily financing. For 5+ unit properties or projects that create a fifth unit. Fits income-producing apartment property. Downside: the balloon, recourse, and shorter-amortization structure described above; underwritten on NOI and sponsor strength.

Loan type by property and project stage

| Loan type | Best fit | Poor fit | First thing lender verifies |

|---|---|---|---|

| HELOC / home equity | Equity-rich, owner-occupied | Low-equity or non-owner-occupied | LTV, occupancy, property type |

| Cash-out refinance | Replacing first mortgage makes sense | Owner with a low-rate first mortgage | Blended cost of debt, loan-limit fit |

| Renovation loan | Eligible 1–4 unit project | 5+ unit commercial project | Program/property eligibility, after-improved value |

| Construction-to-permanent | Larger permitted build | Unclear zoning or scope | Plans, budget, as-completed appraisal |

| Private / bridge | Investor with a clear exit | Owner needing low-risk debt | Exit strategy and reserves |

| DSCR (exit) | Stabilized rental income | Pre-permit concept | Lease and NOI, DSCR ratio |

| Commercial multifamily | 5+ unit property | Simple homeowner ADU | NOI, sponsor financials, collateral |

How much should you borrow? Multifamily ADU cost ranges for 2026

Answer: Garage and space conversions typically run about $60,000–$150,000; attached ADUs about $150,000–$300,000; and detached new construction about $200,000–$400,000 or more, with high-cost metros like Los Angeles reaching detached costs of roughly $219,000–$459,000. National per-square-foot costs run about $150–$300. Multifamily projects can carry premiums single-family builds don't — fire separation, additional utility laterals, site work — so size your loan above a single-family estimate.

| ADU type | Typical 2026 range | Notes |

|---|---|---|

| Garage / space conversion | ~$60,000–$150,000 | Cheapest path; reuses existing foundation, walls, roof |

| Attached ADU | ~$150,000–$300,000 | Shares a wall and some utilities; needs foundation extension and new framing |

| Detached new construction | ~$200,000–$400,000+ | Most expensive; full foundation, separate utility runs, site work |

| Per square foot (national) | ~$150–$300/sq ft | Cost per sq ft drops as size rises (fixed costs spread out) |

| Los Angeles detached (example metro) | ~$219,000–$459,000 | High-cost metro; garage conversions ~$140,000–$245,000+ |

Sources: Angi 2026 ADU cost guide (national $150–$300/sq ft and $40k–$360k total range); SelfStorage 2026 ADU construction-cost guide; CALI ADU 2026 Los Angeles ADU cost guide. Verified May 2026. National ranges are planning estimates, not quotes — local pricing is what turns a range into a budget.

A utility lateral — the pipe or line connecting your unit to the municipal water, sewer, gas, or electric main — quietly inflates detached and multifamily ADU budgets, because a new detached unit on a multifamily lot often can't simply piggyback on the main building's connections. On multifamily lots specifically, fire-separation requirements between dwellings can push you toward more robust assemblies that a single-family backyard ADU never needs. Confirm it with a local builder and your building department. For the full cost breakdown, see our ADU cost guide.

Will the future ADU's rent help you qualify?

Answer: Sometimes, but never automatically. Existing, documented rent is far easier to use than projected rent. Fannie Mae allows ADU rental income toward qualifying income on a one-unit principal residence (purchase or limited cash-out refinance only), capped at 30% of the borrower's total qualifying income. Freddie Mac applies a similar 30% cap and limits lease-documented rent to 75% of the lease amount. FHA allows rental-income treatment but bars using ADU rent as effective income on a one-unit cash-out refinance.

Fannie Mae. Income from an ADU may be considered toward qualifying income on one-unit, principal-residence purchase and limited cash-out refinance transactions, from only one ADU, limited to 30% of the borrower's total qualifying income. Income from a 2–4 unit subject property follows the separate subject-property rental-income documentation rules. (Sources: Fannie Mae SEL-2025-08; DU 12.1 release notes; Selling Guide B3-3.8-01. Verified May 2026.)

Freddie Mac. When ADU rental income from a subject 1-unit primary residence is used, qualifying rental income cannot exceed 30% of total qualifying income, and lease-documented rent cannot exceed 75% of the lease amount. Freddie also extends ADU rental-income use to a subject 1-unit investment property under Guide Chapter 5306. (Source: Freddie Mac ADU Fact Sheet, Feb 2026. Verified May 2026.)

FHA. FHA guidance allows rental income from either a one-unit property with an ADU or a two-to-four-unit property to be considered as effective income when documentation requirements are met. One material limit: for FHA cash-out refinances, rental income from an ADU on a one-unit subject property cannot be used as effective income. (Source: HUD Mortgagee Letter 2023-17. Verified May 2026.)

Can ADU rent help you qualify?

| Situation | Easier or harder? | Why |

|---|---|---|

| Existing legal ADU with a signed lease | Easier | Documented income and legal status already exist |

| Proposed ADU not yet built | Harder | Projected income may be limited or excluded |

| Owner-occupied 2–4 unit | Program-specific | Existing unit rents may be documented separately |

| Non-owner-occupied rental | Depends on product | Underwriting may focus on leases, DSCR, or the exit |

| 5+ unit property | Commercial logic | Income is treated as property NOI, not household income |

Documents a lender may request to count rent:

A lease agreement, a rent schedule, Form 1007 (single-unit market rent), Form 1025 (2–4 unit operating income), an appraisal showing the ADU's characteristics, a permit or certificate of occupancy, tax returns or Schedule E, an operating statement for investment property, an insurance quote, and reserve documentation.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

What loan limits cap a 2–4 unit ADU project in 2026?

Answer: For residential 1–4 unit conventional financing, the 2026 conforming loan limits are a hard ceiling: $832,750 for one unit, $1,066,250 for two units, $1,288,800 for three units, and $1,601,750 for four units in most of the U.S. High-cost counties go up to 150% of those figures. FHA sets its own 2026 limits by county and unit count. If your after-build loan amount exceeds the relevant county limit, you move toward jumbo, portfolio, investor, or commercial financing.

2026 loan limits — conventional and FHA

| Unit count | Conv. baseline | Conv. high-cost ceiling | FHA floor | FHA high-cost ceiling |

|---|---|---|---|---|

| 1 unit | $832,750 | $1,249,125 | $541,287 | $1,249,125 |

| 2 units | $1,066,250 | $1,599,375 | $693,050 | $1,599,375 |

| 3 units | $1,288,800 | $1,933,200 | $837,700 | $1,933,200 |

| 4 units | $1,601,750 | $2,402,625 | $1,041,125 | $2,402,625 |

Sources: Fannie Mae Lender Letter LL-2025-04; FHFA 2026 Conforming Loan Limit announcement (Nov 2025); HUD 2026 FHA loan limits (HUD No. 25-145). Conventional baseline rose 3.26% over 2025. Alaska, Hawaii, Guam, and the U.S. Virgin Islands have higher statutory limits. High-cost counties exist in CA, CO, CT, DC, FL, HI, ID, MD, MA, NH, NJ, NY, PA, TN, UT, VA, WA, WV, WY and other applicable areas. Verified May 2026.

A duplex, triplex, or fourplex qualifies against the multi-unit limits above, which are far higher than the one-unit figure — good news for budget headroom. But two things can still bite. First, your county's specific limit may differ from the baseline. Second, if the ADU pushes your property past four units, this entire table stops applying and you're in commercial territory.

What if the ADU creates a fifth unit?

Answer: If the ADU causes the property to exceed four legal units, assume you've left the standard residential 1–4 unit mortgage world. The project isn't impossible — but it likely needs portfolio, investor, bridge, or commercial multifamily financing instead of a conventional or FHA ADU loan.

We keep returning to this because it's the most common and most expensive surprise in multifamily ADU projects. A fifth legal unit changes the collateral conversation entirely: appraisal method, insurance, lender appetite, and the loan's saleability to Fannie or Freddie all shift.

A fourplex-plus-ADU example (no guarantees attached):

A fourplex owner wants to add one detached ADU. The city may allow it under local code. But the after-build property may now function as five rental units — which can make ordinary residential ADU financing unavailable and require portfolio or commercial review. The build can still happen. The loan is the part that changes.

What to ask the lender before you spend on plans:

- Will you underwrite this as 1–4 unit residential or as commercial?

- How will the appraiser classify the after-build property?

- Will the ADU be counted as a separate legal unit?

- Is the loan still saleable to Fannie Mae, Freddie Mac, or FHA?

- If not, what portfolio or commercial product applies, and what exit do you require?

How do California's multifamily ADU rules affect financing?

Answer: California law may permit far more ADUs on a multifamily parcel than a residential lender will finance through a standard 1–4 unit mortgage. Government Code § 66323 allows interior-conversion ADUs equal to at least one unit or up to 25% of existing units, plus up to eight detached ADUs on a lot with an existing multifamily dwelling (capped at the number of existing units). But legal eligibility and financeability are separate tests — building more than four units can push the borrower straight into commercial underwriting.

Under § 66323, as amended by SB 1211 (effective January 1, 2025), the detached-ADU allowance on lots with an existing multifamily dwelling jumped from two to up to eight. State law preempts more restrictive local ordinances on the issues it covers — though local adoption lags, so confirm. (Sources: Gov. Code § 66323 via FindLaw; California HCD 2026 ADU Handbook; SB 1211. Verified May 2026.)

The opportunity is real: a 4-unit building can add up to four detached ADUs; a 12-unit building can add up to eight. Plus interior conversions of non-livable space up to 25% of the existing unit count, approved ministerially.

The financing catch is just as real. Adding four detached ADUs to a fourplex creates an eight-unit property — squarely commercial. State ADU rights do not equal automatic financing approval, and any guide implying otherwise is setting you up for a hard conversation with an underwriter. If your project stays at or under four total units, you remain in the residential lanes above; if it exceeds four, plan for commercial or portfolio financing from the start.

What does a lender need before an ADU construction loan is real?

Answer: A lender needs far more than an idea and a rent estimate. Expect plans, contractor bids, permits or permit status, a construction budget with contingency, a draw schedule, appraisal support, insurance, title information, your current legal unit count and proposed after-build count, and rental documentation if income is part of the loan story.

| Document | Why it matters for a multifamily ADU |

|---|---|

| Current legal unit count | Sets your starting lane; avoids the fifth-unit surprise |

| Proposed after-build unit count | Determines residential vs. commercial before you apply |

| Plans / contractor bid / budget + contingency | Construction and renovation loans underwrite to scope, not concept |

| Permit status / zoning confirmation | Affects construction-loan draw risk and timing |

| Form 1025 (2–4 unit) or rent schedule | Drives how 2–4 unit rent is treated in qualifying |

| Rent roll / operating statement / NOI | The core of commercial (5+ unit) underwriting |

| Leases for existing units | Documents current income; easier than projected rent |

| Reserves, insurance, entity/personal financials | Standard underwriting; reserves matter more for investors |

One sequencing tip that saves money: more complete plans reduce lender uncertainty, but you shouldn't pay for a full architectural set before you've confirmed feasibility and your likely financing lane. Spending $15,000 on plans for a project that turns out to need commercial financing you can't obtain is the exact mistake this page exists to prevent.

Download the Free ADU Starter Kit

The exact questions to ask your city, lender, contractor, and insurer before you commit — plus the document checklist above in a printable format.

→ Get the Free Starter KitCan the ADU actually cash-flow after debt, taxes, utilities, and management?

Answer: Judge a multifamily ADU as a rental unit, not by gross rent. The real question is whether rent still works after debt service, taxes, insurance, utilities, vacancy, repairs, management, and reserves — and after a slower-than-expected lease-up. A unit that only pencils out at full rent with zero vacancy and no maintenance is not a financeable plan; it's a hope.

Gross rent is the most misleading number in any ADU pitch. Here's the stress test to run before committing.

Monthly rent − vacancy allowance − added insurance/taxes − owner-paid utilities − maintenance reserve − property-management cost − debt service = estimated monthly cash flow

For an investor loan: gross rent − vacancy = effective income; effective income − operating expenses = NOI; NOI ÷ debt service = DSCR. If that DSCR lands below the program minimum (~1.0 on many 1–4 unit DSCR loans, ~1.15+ on multifamily), the loan tightens or the deal doesn't pencil.

ADU rental stress-test inputs

| Input | Why it matters | Use conservative estimate? |

|---|---|---|

| Rent | Top-line income | Yes |

| Vacancy | Lease-up and turnover risk | Yes |

| Repairs | New units still need reserves | Yes |

| Utilities | ADUs may add water, sewer, power costs | Yes |

| Taxes | Improvements can raise the assessment | Yes |

| Insurance | An added unit can change coverage | Yes |

| Management | More doors mean more work | Yes |

| Debt service | Financing cost can erase the spread | Yes |

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Financing is only one piece of making a new rental unit work. If your ADU becomes a rental, you'll be handling leasing, rent collection, maintenance requests, accounting, and tenant communication — across more doors than before. Planning that workflow before lease-up is the difference between a unit that adds income and one that adds headaches.

Affiliate link: Dwelling Index may earn a commission if you use this link, at no extra cost to you.

Adding another rental unit? Plan your workflow before lease-up.

Explore property-management tools with Buildium →When should you NOT finance a multifamily ADU yet?

Answer: Hold off if your current or after-build legal unit count is unclear, if your city hasn't confirmed basic eligibility, if no lender has confirmed how they'll classify the property, if the project only cash-flows under perfect assumptions, or if a builder is pressuring you to put down a deposit before financing is verified.

- You don't know the property's current legal unit count.

- The ADU may create a fifth unit, and no lender has confirmed a path.

- You need projected rent to qualify, but no lender has confirmed it can count.

- A builder's financing pitch requires a fast deposit.

- The project only cash-flows with zero vacancy, no repairs, and maximum rent.

- The permit path is unclear or unconfirmed.

- The property has title, insurance, HOA, or non-conforming-use issues.

- You're relying on a future refinance with no fallback if rates or rents move.

The honest catch worth repeating: local zoning can say "yes" while your financing path says "not yet." Permitting isn't instant, site work can change the budget after you've started, and a unit that's legal to build isn't automatically a unit a lender will finance on the terms you assumed. None of that stops a well-planned multifamily ADU — it just means feasibility comes before deposits.

Not ready to apply? Start with the property, not the loan application. A property check confirms what your specific parcel may support before you spend on plans or permits — and tells you which side of the four-unit line you're on.

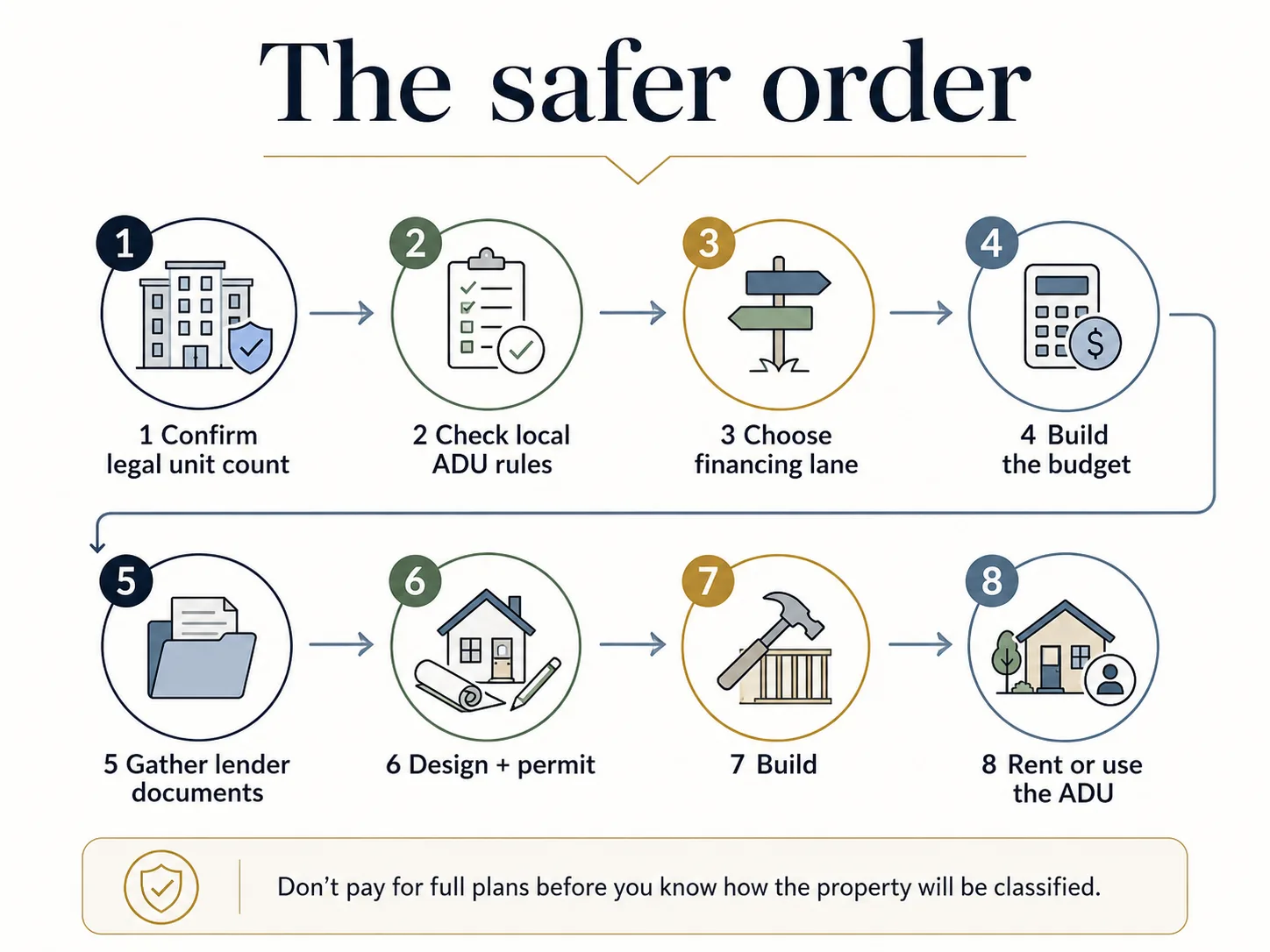

See what's possible at your address → Get Your Free ADU ReportThe safe order to finance a multifamily ADU

Answer: The safe sequence is feasibility first, financing second, design third, permits fourth, construction last. Many owners reverse this — paying for plans and deposits before confirming whether their property classification even supports the loan they want — and that's where projects stall or die.

| The wrong order (where projects die) | The safe order (where projects close) |

|---|---|

| Pay for plans → pull permits → discover the lender won't classify it the way you assumed | Confirm feasibility → confirm after-build unit count → lock your financing lane → then design and permit |

The full safe sequence:

- Confirm the current legal unit count.

- Confirm local ADU eligibility.

- Confirm the after-build unit count.

- Decide whether the property stays 1–4 unit residential or becomes commercial.

- Estimate total project cost (use the ranges above as a floor, not a target).

- Estimate rent conservatively.

- Check your county loan limits.

- Decide whether to preserve or replace the first mortgage.

- Choose a first financing lane and a backup lane.

- Gather lender documents.

- Confirm appraisal and rent documentation.

- Get financing terms in writing.

- Finalize plans and pull permits.

- Build.

- Lease, stabilize, manage — and refinance only if the numbers still work.

Owner-occupants in a 1–4 unit residential lane who want to explore the mortgage and refinance side can start comparing options here.

Affiliate link: Dwelling Index may earn a commission if you use this link, at no extra cost to you.

Explore ADU-friendly mortgage and refinance options.

See current options with Mortgage Research Center →Best fit for owner-occupied or residential 1–4 unit financing questions. If your project creates a fifth unit or starts on a 5+ unit apartment property, talk with a commercial multifamily lender instead.

What we verified for this guide

Last verified: May 25, 2026. We are Dwelling Index — an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder. This guide was assembled from primary and authoritative sources:

- Fannie Mae ADU eligibility expansion (2–3 unit properties may include ADUs where total units ≤ 4; up to 3 ADUs on one-unit properties) — Fannie Mae Selling Guide Announcement SEL-2025-10, effective March 31, 2026.

- ADU rental income, 30% cap, purchase/limited-cash-out only — Fannie Mae SEL-2025-08 and Selling Guide B3-3.8-01.

- Fannie Mae 10-financed-property cap — Selling Guide B2-2-03.

- Freddie Mac one ADU on 1–3 unit properties; 30%/75% caps — Freddie Mac ADU Fact Sheet (Feb 2026).

- FHA ADU/rental-income treatment, 203(k) ADU scope, one-unit cash-out restriction — HUD Mortgagee Letter 2023-17; 203(k) Limited $75,000 cap — HUD Mortgagee Letter 2024-13.

- 2026 conforming loan limits — Fannie Mae Lender Letter LL-2025-04; FHFA 2026 announcement. 2026 FHA limits — HUD No. 25-145.

- Residential/commercial 5-unit threshold and DSCR mechanics — theLender, Lendmire, Ridge Street Capital, American Heritage Lending DSCR program guides (2025–2026).

- California multifamily ADU rules — California Government Code § 66323; SB 1211; California HCD 2026 ADU Handbook.

- 2026 construction cost ranges — Angi, SelfStorage, CALI ADU (2026).

Loan-program rules, DSCR norms, and costs change. We re-verify agency guidance and loan limits quarterly (and after any FHFA, Fannie, Freddie, FHA, HUD, or California HCD update), and cost data quarterly. DSCR ratios and LTV figures are typical lender norms, not universal guarantees — confirm current terms directly with a lender.

Frequently asked questions

Can I get an ADU loan for a duplex?

Yes. A duplex may be financeable through residential 2–4 unit lending, depending on occupancy, ADU legality, the after-build unit count, and program eligibility. As of March 31, 2026, Fannie Mae allows ADUs on 2–3 unit properties where total units stay at or below four — but only through lenders using UAD 3.6 policy. (Source: Fannie Mae SEL-2025-10.)

Can I finance an ADU on a triplex?

Possibly. The key issue is whether the triplex plus ADU stays within a financeable 1–4 unit residential framework and whether your lender has adopted the current agency ADU rules. If the ADU would create a fifth unit, expect to move toward portfolio or commercial financing.

Can I add an ADU to a fourplex?

Maybe legally, but the financing is the hard part. A fourplex is already at the top of the residential band, so adding an ADU likely creates a fifth legal unit — which can require portfolio, investor, or commercial multifamily financing rather than a conventional or FHA ADU loan.

Does Fannie Mae allow ADUs on multifamily properties?

As of March 31, 2026, Fannie Mae allows two- to three-unit properties to include ADUs if the primary dwelling units plus ADUs do not exceed four — a configuration previously ineligible. The expanded criteria are only available to lenders utilizing UAD 3.6 policy. (Source: Fannie Mae Selling Guide Announcement SEL-2025-10.)

Does Freddie Mac allow ADUs on 2–3 unit properties?

Freddie Mac allows one ADU on eligible one-, two-, and three-unit properties when the unit complies with zoning and land-use requirements (legal, legal non-conforming, or no zoning). (Source: Freddie Mac ADU Fact Sheet, Feb 2026.)

Can FHA count ADU or 2–4-unit rental income?

FHA guidance allows rental income from a one-unit property with an ADU or a two-to-four-unit property to be considered as effective income when documentation requirements are met — though ADU rent on a one-unit cash-out refinance cannot be used. FHA 203(k) project eligibility for adding or renovating an ADU depends on the property, scope, occupancy, and appraisal classification. (Source: HUD Mortgagee Letter 2023-17.)

Can future ADU rent help me qualify?

Sometimes, but never assume it. Existing legal rent with a lease is far easier to document than projected rent. Fannie and Freddie both cap ADU rental income at 30% of qualifying income on a one-unit principal residence, and Freddie limits lease-documented rent to 75% of the lease amount.

Can I use a HELOC to build an ADU on a rental property?

Possibly, but HELOCs are generally easier to obtain on owner-occupied property. On a rental, availability, LTV, pricing, and underwriting are typically stricter.

What if my ADU makes the property five units?

Assume standard 1–4 unit residential financing may no longer fit. Ask your lender about portfolio, investor, bridge, DSCR-exit, or commercial multifamily financing, and confirm how the after-build property will be classified.

Should I refinance my low-rate mortgage to build an ADU?

Not automatically. Compare the total cost of replacing your first mortgage against home equity, construction, or staged financing. The lowest advertised rate is not always the lowest total-cost path, especially if you're giving up a low first-mortgage rate.

How many ADUs can a California multifamily property add?

Government Code § 66323 requires local agencies to allow at least one ADU (or up to 25% of existing units) through qualifying interior conversions of non-livable space, plus up to eight detached ADUs on a lot with an existing multifamily dwelling — capped at the number of existing units. For a proposed multifamily dwelling, the detached allowance is two. Local site constraints still apply. (Source: Gov. Code § 66323; SB 1211; CA HCD 2026 ADU Handbook.)

How we researched this page

We reviewed official Fannie Mae, Freddie Mac, FHA/HUD, FHFA, and California code sources; compared current lender and competitor pages; and assembled the financing matrix around the one practical decision a multifamily owner must make before applying — whether the project fits residential 1–4 unit financing, investor financing, or commercial multifamily financing. We do not guarantee loan approval, rent, returns, or permit approval. Always verify your property's local zoning, legal unit count, county loan limits, and lender requirements before committing to financing or construction.

Related guides

Not sure where to start? See what's possible at your address — get your free ADU report in 60 seconds.

→ Get Your Free ADU Report