ADU Financing for Investment Property: Every Path That Works When You Don’t Live There

The bottom line: Yes, you can get ADU financing for an investment property — but the playbook is different from the homeowner advice you’ve probably been reading, and copying it will cost you time and possibly a denial. The headline 2026 rule that lets ADU rental income help you qualify (Fannie Mae’s Desktop Underwriter 12.1 update, effective for new casefiles submitted on or after the weekend of March 21, 2026) is owner-occupied, one-unit principal residences only — it does not apply to a true rental. The investor track has its own tools: a cash-out refinance, an investment-property HELOC or home equity loan, Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, DSCR and non-QM loans, portfolio construction, and bridge financing. Each comes with stricter LTV caps, higher reserves, and narrower lender availability than the owner-occupied equivalents — and FHA 203(k) is off the table entirely. The hierarchy that works: (1) confirm your lot can legally support the ADU, (2) sort your occupancy bucket, (3) match the lane to your equity and income docs, (4) stress-test the cash flow before you commit.

Start here — match your situation to a lane:

| Your situation | Start with | Skip |

|---|---|---|

| Own a rental with equity + a cheap first mortgage | Investment-property HELOC / home equity loan | A full cash-out that wipes out your low rate |

| Buying a rental and building the ADU | HomeStyle, CHOICERenovation, or portfolio construction | FHA 203(k) (unless you'll occupy) |

| Hold title in an LLC, or income is hard to document | DSCR / portfolio / private | Consumer owner-occupied renovation products |

| ADU is unpermitted | Legalization / permitting first | Assuming the rent or value will count |

| You need the future rent to qualify | Program-specific rent rules + the right appraisal | Generic "the ADU pays for itself" math |

Verified agency figures from the Fannie Mae Eligibility Matrix (eff. April 1, 2026), Freddie Mac maximum-LTV requirements, and the Freddie Mac ADU fact sheet (Feb. 2026). Full sources in the “What we verified” box.

→ Skip to the Investor ADU Financing Path Finder — match your equity, income docs, and timeline to the right loan lane.

Disclosure: Dwelling Index is an independent research resource — not a lender, broker, or builder. This page is reader-supported: when you use our links to explore financing options or request a feasibility report, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation, and we never rank lenders by payout. Read our full affiliate disclosure & methodology.

Can you get ADU financing for an investment property?

Here’s the honest reality most ADU financing guides won’t tell you: they quietly assume you live in the home. Nearly every “6 ways to finance an ADU” article frames the answer around a primary residence — the friendly, high-leverage, low-rate products built for owner-occupants. The moment your property is a true rental, several of those popular options become unavailable, stricter, or lender-specific.

That’s not a dead end. It just means you need the investor track, not the homeowner one. Once you sort your property into the right occupancy bucket, the path usually becomes obvious.

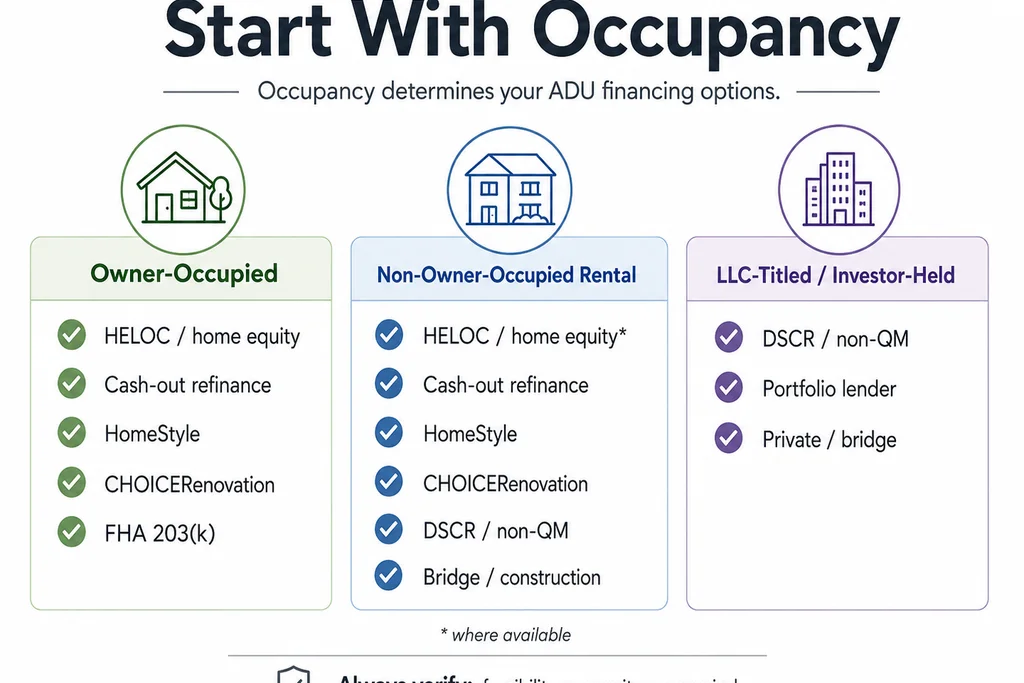

The first fork: owner-occupied, non-owner-occupied, or LLC-titled?

Lenders price risk by occupancy. A property you live in is statistically less likely to default than one you rent out, so investment-property loans come with lower loan-to-value (LTV) ceilings, higher rates, larger cash-reserve requirements, and more documentation. If the property is titled in a limited liability company (LLC), most consumer mortgage products don’t fit at all — you’re typically looking at a portfolio, private, or DSCR lender.

Here’s how the two worlds split:

| If you LIVE in the property (owner-occupied) | If you DON’T live there (true investment) |

|---|---|

| Fannie Mae now lets one ADU’s projected rent help you qualify (purchase or limited cash-out refi), capped at 30% of total qualifying income — primary residence only, via DU 12.1. | That Fannie rule doesn’t apply. But Freddie Mac can count ADU rental income on a subject one-unit investment property when its requirements are met, and DSCR/renovation loans underwrite the property’s cash flow or after-built value. |

| FHA 203(k) and FHA ADU rental-income provisions are available (owner-occupancy required). | No FHA 203(k) path — that program is owner-occupants only. |

| HELOC / home-equity loan at primary-residence pricing, often up to ~80–85% combined LTV. | Non-owner HELOC exists but with fewer lenders, lower combined LTV, and a rate premium. |

| Conventional cash-out refi up to ~80% LTV. | Conventional cash-out refi capped at 75% LTV (one-unit) / 70% (2–4-unit) with larger reserves. |

Sources: Fannie Mae Selling Guide SEL-2025-08 and B3-3.8-01 (owner-occupied ADU income, 30% cap, DU 12.1); Freddie Mac ADU fact sheet, Feb. 2026 (ADU rental income on a subject 1-unit investment property, Guide Ch. 5306); Fannie Mae Eligibility Matrix and Freddie Mac maximum-LTV page (investment cash-out 75%/70%); FDIC 203(k) guide (owner-occupants only). Verified May 24, 2026.

Why zoning and permits come before lender shopping

Setbacks (the minimum distance a structure must sit from property lines), lot-coverage limits, and local owner-occupancy ordinances can quietly disqualify a project before a lender ever sees it. Here’s a tripwire that catches investors specifically:

| Tripwire | What it means for an investor | Example |

|---|---|---|

| Owner-occupancy requirement | The owner must live on-site to permit/keep the ADU — a direct conflict with a pure rental | Salt Lake City requires the owner of a single-family property with an ADU to reside on the property (Salt Lake City Code, ADU ordinance) |

| Short-term-rental ban | Your projected nightly-rental income may be illegal, undercutting your underwriting | Many cities restrict or ban STRs in ADUs; underwrite the long-term-rent case first |

| Parking / setback minimums | Can shrink or block the buildable footprint | Varies by municipality; check before design |

Source: Salt Lake City Code (ADU owner-occupancy requirement), verified May 24, 2026. Always confirm current local rules with your city or county.

→ See what’s possible at your address

Before you compare loans, confirm your lot can legally fit an income-producing ADU. Our Feasibility Engine checks your address against local zoning, ADU type, and the build-fit questions lenders will eventually ask — and returns a free build-potential report in about 60 seconds. No obligation, no sales call required.

See What You Can Build → Get Your Free ADU ReportFree · No commitment

Which ADU financing paths actually allow rental property?

We built the table below by cross-referencing the Fannie Mae Eligibility Matrix, Freddie Mac’s maximum-LTV requirements and ADU fact sheet, HUD/FHA program rules, the FDIC’s lending guide, and current investor-lending sources into one decision tool.

| Financing path | Works for true non-owner-occupied rental? | ADU construction fit | Best fit | The dealbreaker to check first |

|---|---|---|---|---|

| Cash | Yes | Any legal, permitted ADU | Investors avoiding debt complexity | Liquidity risk and opportunity cost |

| Investment-property HELOC | Sometimes | Flexible draws for construction invoices | High-equity owners protecting a low-rate first mortgage | Few lenders offer it; lower LTV than a primary line; variable rate |

| Investment-property home equity loan | Sometimes | Lump-sum ADU budget | Fixed-scope projects with a defined budget | Lender-specific terms; lower LTV and higher reserves than a primary home |

| Cash-out refinance | Yes, if qualified | Proceeds fund the build | Owners whose existing first mortgage isn't worth preserving | Replaces your first mortgage; 75% LTV (1-unit) / 70% (2–4-unit) agency cap |

| Fannie Mae HomeStyle Renovation | Yes — matrix lists 1-unit investment purchase (85%) and limited cash-out refi (75%) | Strong: purchase or refi plus ADU construction in one loan | Buying or refinancing a 1-unit rental and funding a permitted ADU | Renovation escrow, plans, bids, as-completed appraisal, lender approval |

| Freddie Mac CHOICERenovation | Yes — 1-unit investment property is an eligible property type | Strong: ADU addition/renovation; can also pay off short-term ADU financing | Investors using a Freddie renovation mortgage | Lender/LPA requirements; one ADU per Freddie's ADU collateral rule; zoning compliance |

| FHA 203(k) | No — not for true investors | Owner-occupied ADU rehab only | House hackers / owner-occupants | Owner-occupancy required (FDIC: "only owner-occupants, not investors") |

| DSCR / non-QM investor loan | Sometimes | Often best as the refinance/exit once rent is stabilized | Investors whose property cash flow covers the debt | Appraisal comps + permit status; some programs carry prepayment penalties |

| Private construction / bridge / hard money | Sometimes | Short-term build funding or bridge-to-refi | Investors needing speed, collateral-based underwriting, or an agency-ineligible scenario | Higher cost, draw controls, balloon/refinance risk — you need an exit plan |

Sources: Fannie Mae Eligibility Matrix (eff. April 1, 2026) for HomeStyle and investment LTVs; Freddie Mac CHOICERenovation product page (1-unit investment property eligible; ADU additions allowed; no-cash-out refi can pay off short-term ADU financing) and Freddie ADU fact sheet (one ADU on 1–3-unit properties); FDIC 203(k) guide (owner-occupants only); DSCR ADU comp rule from OfferMarket DSCR requirements (Mar. 2026). Verified May 24, 2026.

How to read the matrix

“Eligible” is the floor, not the finish line. A product appearing here means the program permits an investment-property ADU — not that you, your property, or your project will be approved. Your credit, reserves, debt-to-income or DSCR, the appraisal, your title structure, local zoning, and the individual lender’s overlays (extra rules a lender adds on top of agency guidelines) all still apply.

Our editorial read — a judgment based on the verified facts above, not a rule: most investors land in one of three lanes. If you already own the property with real equity, a cash-out refinance or a non-owner HELOC/home-equity loan is usually simplest. If you’re buying-to-build or you’re equity-light, a HomeStyle or CHOICERenovation loan underwrites the finished value instead of what you have today. If your personal income is hard to document or you hold title in an LLC, a DSCR loan lets the property qualify itself. Your lender’s underwriting is the final word.

→ Compare your financing options

See what a cash-out refinance, construction loan, or investment-property mortgage could look like for your scenario through the Mortgage Research Center — free to explore, no rate or approval guaranteed.

Disclosure: Dwelling Index may earn a commission if you use this partner link, at no extra cost to you.

Compare Investment-Property Loan Options →Find your financing lane (and your first dealbreaker)

Answer four quick questions and the Investor ADU Financing Path Finder points you to the lane that fits your equity, your income docs, and your timeline — plus the one dealbreaker to check before you call a lender. The inputs are: (1) occupancy — owner-occupied / non-owner / LLC / buying-to-build; (2) equity — free-and-clear / 30%+ / under 30% / buying; (3) income docs — W-2 / self-employed or LLC / prefer not to document; (4) timeline — lump sum now / phased build / fastest.

→ Run the tool

Run the Investor ADU Financing Path Finder → See which loan lanes are still open

These results are educational illustrations, not loan offers, approvals, or guarantees. Actual eligibility, rates, and terms depend on lender underwriting, local market conditions, and the final appraisal.

See What You Can Build → Get Your Free ADU ReportFree · No commitment

Should you keep your current mortgage, or refinance to build the ADU?

This is the objection we hear most from real investors, and it rarely shows up in generic ADU guides. On the forums, the pattern is consistent: someone has serious equity and a first mortgage at 2–3% locked in years ago, and they’re terrified that financing an ADU means surrendering that rate. That instinct is correct. People aren’t just shopping for money — they’re trying not to destroy a favorable first mortgage. So the real first question isn’t “which loan is cheapest today,” it’s “is my existing mortgage worth protecting?”

Second lien vs. full refinance

| Decision factor | Second lien / HELOC | Cash-out refinance | Renovation mortgage |

|---|---|---|---|

| Preserves your first mortgage | Yes | No | Usually no |

| Uses after-completion value | Usually no | Usually current as-appraised value | Yes (program-dependent) |

| Supports construction draws | Limited | No | Yes |

| Best for | High equity + low first-mortgage rate | High existing rate or small balance | Purchase/refi plus a major ADU build |

| Main risk | Variable rate; fewer lenders | Repricing your entire debt stack | Paperwork, timelines, lender overlays |

If your first mortgage is at a rate you’ll never see again, lean toward a second lien or a short-term investor loan that leaves it untouched. If your first mortgage is small or already at market rate, a cash-out or renovation refinance can be the cleaner structure. Compare the blended cost of the whole debt stack, not just the monthly payment on the new money.

Can you use a HELOC or home equity loan on an investment property to build an ADU?

A HELOC is a revolving credit line secured by your equity — you draw what you need, when you need it, which fits the staged invoices of a construction project. A home equity loan is the lump-sum, fixed-rate cousin, better for a defined budget. For investors trying to protect a cheap first mortgage, either can be smarter than a cash-out refinance, because they sit behind your existing loan instead of replacing it.

The catch is availability. NerdWallet notes that investment-property HELOCs are possible but can take legwork, because fewer lenders write them. Expect a stronger credit profile (often 700+), more reserves, and a rate premium over a comparable primary-residence line. If your equity math works after the lower LTV cap, this is frequently the path of least disruption.

→ Compare equity and refinance paths

See how a HELOC, home equity loan, or cash-out could fit your numbers through the Mortgage Research Center — educational comparison only, terms depend on lender underwriting.

Disclosure: Dwelling Index may earn a commission if you use this partner link, at no extra cost to you.

Compare HELOC & Equity Paths →When does a cash-out refinance make sense for an investor ADU?

A cash-out refinance isn’t really “ADU financing” — it’s equity extraction. You replace your existing mortgage with a larger one and take the difference in cash to fund the build. The loan itself is underwritten as a refinance against the property’s current value, not its post-ADU value.

Here’s where the investment-property caps bite, with a worked example:

Say your rental is worth $500,000 and you owe $300,000.

| Step | Figure | Note |

|---|---|---|

| Property value | $500,000 | Current appraised |

| 75% LTV cap (1-unit investment) | $375,000 | Agency maximum |

| Minus existing mortgage payoff | −$300,000 | |

| Accessible cash-out | ~$75,000 | Before closing costs of ~2–5% |

Illustrative example only — not a quote, not an offer. Actual accessible equity depends on appraised value, payoff amount, and lender-specific terms.

This gap — between the equity you have and the equity you can borrow against — is the single most common reason investor ADU projects stall on a cash-out path. It’s also exactly why renovation and construction loans (which lend against the finished, higher value) exist.

Cash-out dealbreakers to check: a low-rate first mortgage you’d lose, insufficient equity after the 75%/70% cap, six-plus months of required reserves, a property listed for sale in the last six months (which can cap LTV at 70%), and “declining market” or rural/large-acreage appraisal flags that cut LTV further.

Can Fannie Mae HomeStyle Renovation finance an ADU on an investment property?

HomeStyle is one of the most powerful investor ADU tools precisely because it underwrites against the property’s after-completion value, not what it’s worth today. That solves the equity gap from the cash-out example above: instead of borrowing against the $500,000 the property is worth now, you can borrow against what it will be worth with the income ADU built.

What HomeStyle can fund — and what it requires

It can cover plans and specifications, permit fees, contractor labor and materials, a renovation escrow account, and permanent improvements including a new accessory unit. Fannie Mae’s October 2025 update (SEL-2025-10) also expanded upfront flexibility: the initial renovation disbursement may be up to 50% of total renovation costs for eligible categories such as materials, permit fees, architectural and design services, and borrower deposits.

To approve it, lenders typically require plans and specifications, a renovation contract, an as-completed appraisal, the renovation loan agreement, a completion certificate, and clear title documentation. Lenders need special approval to deliver HomeStyle loans before the work is complete, so expect renovation oversight and draw inspections.

Can Freddie Mac CHOICERenovation finance an ADU on an investment property?

CHOICERenovation is Freddie Mac’s answer to Fannie’s HomeStyle: a conventional renovation mortgage where the loan proceeds pay directly for the work, so there’s no separate construction loan to pay off afterward. For an investor buying a one-unit rental and adding an ADU — or refinancing one without taking cash out while funding the build — it’s a strong fit.

HomeStyle vs. CHOICERenovation for investors

| Feature | Fannie Mae HomeStyle | Freddie Mac CHOICERenovation |

|---|---|---|

| 1-unit investment property | Yes — purchase (85%) and limited cash-out refi (75%) per matrix | Yes — listed eligible property type |

| ADU addition / renovation | Accessory units allowed when zoning + code permit | ADU addition or renovation allowed; one ADU per Freddie's ADU collateral rule |

| Transaction emphasis | Purchase or refi with renovation funds | Purchase, no-cash-out refi (incl. paying off short-term ADU financing) |

| Underwriting engine | Desktop Underwriter (DU) | Loan Product Advisor (LPA) |

| Biggest caution | Lender renovation approval, escrow, documentation | LPA/lender requirements; one-ADU collateral rule; zoning compliance |

| Best use | Investor purchase/refi with a full renovation packet | Investor purchase or no-cash-out refi with a defined ADU scope |

Sources: Fannie Mae Eligibility Matrix and HomeStyle Selling Guide (B5-3.2-01); Freddie Mac CHOICERenovation product page (1-unit investment property eligible; ADU additions allowed) and Freddie ADU fact sheet, Feb. 2026 (one ADU on eligible 1–3-unit properties; must be legally permissible, legal non-conforming, or in an area without zoning). Verified May 24, 2026.

Does FHA 203(k) work for an ADU investment property?

We’re flagging this loudly because 203(k) appears on nearly every generic “how to finance an ADU” list, and investors waste real time chasing it. If you will occupy one unit of the property — the classic “house hack” — then 203(k), along with HomeReady, HomeStyle, and CHOICERenovation, may be on the table, and you should read our owner-occupied ADU financing guide instead.

If you won’t live there, skip it.

FHA’s ADU rental-income rules still matter (for owner-occupants)

For house-hackers, HUD Mortgagee Letter 2023-17 is worth knowing — and it has a nuance that trips people up. In general, for a one-unit-with-ADU property with limited or no rental history, FHA uses 75% of the lesser of the appraiser’s fair-market rent or the lease amount. But under the Standard 203(k) program specifically, for a proposed ADU with no rental history, FHA uses 50% of the lesser of those two figures — a more conservative haircut. Either way, ADU rental income is capped at 30% of total monthly effective income, and a one-unit-with-ADU property using that income requires two months of PITI reserves. ADU rental income cannot be used to qualify for an FHA cash-out refinance at all. These are owner-occupant rules — they don’t open a path for pure investors, but they shape how an owner-occupied ADU deal pencils.

Source: HUD Mortgagee Letter 2023-17 (Oct. 16, 2023), Sections II.A.4.c.xii(I), II.A.8.a.ii(A), and II.A.8.d.v(A). Verified May 24, 2026.

Can projected ADU rent help you qualify?

This is the second-biggest source of investor confusion, right after occupancy. Existing rent (a unit already leased) has the strongest documentation — leases, a rent roll, Schedule E on your tax return. Projected rent (a unit not yet built or leased) requires an appraiser’s rent estimate or program-specific treatment, and lenders haircut it for vacancy and expenses (commonly around 25%).

How investors actually get ADU income to count

- Freddie Mac (conventional). Per Freddie’s February 2026 ADU fact sheet, ADU rental income may help qualify on a subject one-unit investment property (or a non-subject investment property), with rental-income requirements in Guide Chapter 5306. That’s a genuine investor lane the Fannie DU 12.1 update doesn’t offer.

- DSCR loans qualify on the ratio of the property’s rent to its total payment — principal, interest, taxes, insurance, and any HOA, abbreviated PITIA. A DSCR (debt service coverage ratio) of 1.0 means rent exactly covers the payment; most programs want 1.25 for the best terms, and some go as low as a 0.75 floor.

But here’s a catch almost no competing page mentions: some DSCR programs apply a hard ADU-comp rule. OfferMarket’s 2026 DSCR requirements state that to include ADU rental income, the appraisal must show at least one comparable sale with an ADU and at least one comparable rent with an ADU — and if no such comps exist, the ADU income is excluded entirely. In neighborhoods where ADUs are still rare, a perfectly good, permitted, rented ADU can be invisible to that lender’s math. - HomeStyle and CHOICERenovation lean on the property’s after-completion value, which can fold in the value an income ADU creates — a different (and often friendlier) mechanism than rent comps.

Forms lenders may ask for

Schedule E, the current lease, a rent roll, Form 1007 (Single-Family Comparable Rent Schedule) or Freddie Mac Form 1000, Form 1025 / Freddie Mac Form 72 for small income properties, the appraisal with explicit ADU treatment, and evidence of your property-management history.

The unpermitted-ADU problem

If your ADU is unpermitted, do not assume a lender or appraiser will count its rent or value. Lenders are blunt on this: the unpermitted nature would likely be flagged and excluded from the value and rent calculations. Treat unpermitted-ADU income as an unsafe underwriting assumption until the unit is legalized through your city’s permitting or amnesty path.

Related: Can ADU Rental Income Help Me Qualify? and ADU appraisal and rent-schedule requirements.

What if the property is in an LLC, already rented, or being subdivided?

- LLC-titled property. Holding in an LLC is common for liability protection, but it generally takes you out of conventional consumer-mortgage territory. Portfolio, private, and DSCR lenders routinely lend to LLCs; Fannie/Freddie products typically don’t. If you’re planning to retitle into an LLC, talk to your lender first — doing it mid-process can derail an approval.

- Unit-lot split or condo map. Subdividing the parcel or recording a condo map can change the collateral and your future financing and exit options. Get lender and, ideally, legal input before you file anything.

- Existing tenants. If the property is already leased, your lender will want the lease terms, notice rules, parking and access arrangements, utility separation, and an insurance review reflecting rental use.

Lender- and title-specific outcomes vary by state and entity. Confirm with a licensed lender, and where ownership structure or subdivision is involved, an attorney, before acting.

How do DSCR, bridge, private, and portfolio loans fit an investor ADU?

For many investors, the cleanest sequence is a bridge-to-DSCR strategy:

- Verify the ADU is legal and permittable on your lot.

- Build with a private, bridge, or portfolio construction loan that funds in staged draws.

- Stabilize the rent — get the unit leased and documented.

- Refinance into a DSCR or conventional investor loan once the numbers support it, converting short-term construction debt into a permanent mortgage at better terms.

Private and portfolio lenders care most about the collateral, the after-completion (ARV) value, your experience, your liquidity, the draw schedule, the permit status, and — above all — your exit strategy. A bridge loan without a credible refinance or sale exit is how investors end up facing a balloon payment they can’t cover.

Related: ADU bridge-loan exit strategy.

Will the ADU still cash flow after debt service?

Here’s a transparent, source-backed walkthrough you can copy for your own lot. Every figure is illustrative — substitute your real local numbers.

Step 1 — Construction cost range

| Cost basis | Range | Source |

|---|---|---|

| Detached ADU — construction, per sq ft | $150–$250/sq ft | HomeGuide (2026) |

| Detached ADU — broader national average | $150–$300/sq ft; $40,000–$360,000 total | Angi (2026) |

| 600 sq ft detached — construction only (illustrative) | ~$90,000–$150,000 | HomeGuide (2026) |

| High-cost metro — turnkey all-in (e.g., San Diego) | $375–$600+/sq ft; commonly $300,000–$450,000+ | Snap ADU (Mar. 2026) |

Step 2 — Illustrative scenario. Take a 600 sq ft detached ADU at a mid-cost ~$250/sq ft construction assumption (~$150,000), plus soft costs — design, permits ($1,350–$9,000+), utility hookups, contingency — at roughly 15–25%, for an all-in of about $185,000.

Step 3 — Illustrative debt service (not a quote or offer)

| Illustrative rate | Approx. monthly P&I on $185,000 / 30 yr |

|---|---|

| 7% | ~$1,231 |

| 8% | ~$1,358 |

| 9% | ~$1,489 |

Add taxes, insurance, and any HOA to get your full PITIA.

Step 4 — Stress-test the rent. A roughly 600 sq ft unit in a major metro is commonly cited around $1,600–$2,500/month (Maxable, via Yahoo Finance). Apply a lender-style ~25% vacancy-and-expense haircut and you net roughly $1,200–$1,875/month.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Investor ADU cash-flow stress-test inputs

| Input | Why it matters |

|---|---|

| ADU construction budget | Determines funding need and contingency risk |

| Loan amount + draw timing | Drives debt service and interest carry during the build |

| Long-term market rent | Your core revenue assumption — use conservative comps |

| Vacancy | Reduces effective income; budget for turnover |

| Property management | A real expense, especially for out-of-area landlords |

| Repairs / maintenance | An ADU is a second dwelling, not a bonus room |

| Insurance | Coverage and cost may change with rental use |

| Property-tax reassessment | Can reduce expected net operating income |

| Utilities | Separate meters vs. shared billing changes operations |

| Reserves / capital expenditures | Protect against vacancy and big-ticket repairs |

→ Run your own numbers in the Investor ADU Financing Path Finder above.

Managing the ADU once it’s rented (protecting the ROI)

Once the ADU is leased, you’re operating two income streams on one parcel. Here’s the operations checklist that keeps an ADU profitable — and audit-ready at tax time:

- Rent roll — track rent due, paid, and late across both units

- Lease file — signed lease, addenda, and renewal dates

- Deposit tracking — security deposits held per your state’s rules

- Maintenance log — requests, vendors, costs, and dates (supports deductions)

- Utility billing method — separate meters, sub-metering, or a flat allocation

- Schedule E support — income and expense records mapped to tax categories

- Insurance review — confirm coverage reflects rental use on both units

Property-management software handles the repetitive parts — screening, rent collection, maintenance requests, and accounting — so the unit’s net income survives contact with reality.

→ Set up your rental operations

Planning to rent the ADU? Explore management tools through Buildium, our property-management partner — handle leases, maintenance, and accounting before the unit is occupied.

Disclosure: Dwelling Index may earn a commission if you use this partner link, at no extra cost to you.

Explore Property Management Tools →What documents should you gather before calling lenders?

| Document | Most relevant for |

|---|---|

| Property address + ownership structure (individual vs. LLC) | All lanes |

| Current mortgage statement (balance, rate, term) | HELOC, cash-out, keep-vs-refi decision |

| Title vesting / LLC operating documents | DSCR, portfolio, private |

| Insurance declarations page | All lanes |

| Current leases + rent roll (if rented) | DSCR, Freddie investment ADU income, cash-out |

| Schedule E or property P&L | DSCR, cash-out, conventional |

| ADU plans + scope of work | HomeStyle, CHOICERenovation, construction |

| Licensed contractor's bid, license, and insurance | HomeStyle, CHOICERenovation, construction |

| Permit status / written zoning confirmation | All lanes (dealbreaker if missing) |

| Utility plan (separate vs. shared meters) | HomeStyle, CHOICERenovation, construction |

| Appraisal / rent-comp assumptions + ADU rent comps | DSCR, Freddie investment ADU income |

| Contingency budget | HomeStyle, CHOICERenovation, construction, private |

| Proof of reserves (expect 6+ months for investment) | All lanes |

| Written exit strategy (refinance, hold, or sale) | Bridge, private, construction |

→ Get the checklist + the playbook

Download the free ADU Investor Starter Kit → Includes this lender-packet checklist, the dealbreaker list, the equity math, and the exact questions to ask a lender before you apply. Free, sent straight to your inbox.

Get the Free ADU Investor Starter Kit →Free · No spam

Which ADU financing path should you choose, by scenario?

| Your scenario | Start here | Backup path | Why |

|---|---|---|---|

| Rental, high equity, low first-mortgage rate | Investment-property HELOC / home equity loan | Private second lien or bridge | Preserves the cheap first mortgage |

| Buying a rental and building the ADU | HomeStyle or CHOICERenovation | Portfolio construction loan | Underwrites the finished value; one closing |

| Rental that needs cash extracted | Cash-out refinance | Bridge, then refinance | Uses equity, but reprices the first mortgage |

| LLC-titled property | Portfolio / private / DSCR | Retitle only after legal + lender review | Consumer agency products usually don't fit |

| Unpermitted existing ADU | Permit / legalization first | Cash or private, only if the lender accepts the risk | Rent and value likely won't count otherwise |

| Owner-occupied 'house hack' | FHA 203(k), HomeReady, HomeStyle, CHOICERenovation | HELOC / home equity | A more favorable owner-occupied rule set applies |

| Completed, already-rented ADU | DSCR or investor refinance | Conventional investor cash-out | Documented rent strengthens the file |

→ Confirm your build before you pick a loan

See What You Can Build → Get Your Free ADU Report. Confirm your lot, ADU type, and the financing-fit questions a lender will ask — free, at your address, in about 60 seconds.

See What You Can Build → Get Your Free ADU ReportFree · No commitment

What are the biggest risks and dealbreakers?

| Risk | Why it matters | How to reduce it |

|---|---|---|

| Local zoning blocks the ADU | Financing can't fix an illegal scope | Verify city/county rules first (Feasibility Engine) |

| Permit not issued | Lender/appraiser may not credit value or rent | Get the permit path in writing |

| Budget underestimates utilities/site work | Loan proceeds run short mid-build | Add a contingency; line-item utility laterals (the pipes/wires connecting the ADU to the main lines) |

| Lender won't count future rent | Qualification fails | Confirm the program's rent rules before applying; gather ADU rent comps |

| First mortgage is too valuable to replace | Cash-out becomes expensive | Compare second-lien / HELOC paths |

| LLC / title mismatch | Consumer loan path fails | Confirm title treatment with lender (and attorney) |

| Bridge loan lacks an exit | Balloon-payment risk | Identify the refinance/sale/DSCR exit first |

| Short-term-rental restrictions | Your rent assumptions may be wrong | Underwrite the long-term-rent case first |

| No comparable ADU rentals nearby | A comp-dependent DSCR program may exclude ADU income | Lean toward renovation/construction loans in emerging ADU markets |

What we verified for this guide

What we verified — Last verified:

- Owner-occupied ADU rental-income rule — one-unit principal residence only, 30% cap, purchase or limited cash-out refi only — Fannie Mae Selling Guide SEL-2025-08 and B3-3.8-01; DU 12.1 effective for new casefiles on or after the weekend of March 21, 2026.

- Investor ADU rental income can count on a subject one-unit investment property under Freddie Mac rules (Guide Ch. 5306) — Freddie Mac ADU fact sheet, February 2026.

- Investment-property LTV caps — cash-out 75% (1-unit) / 70% (2–4-unit); HomeStyle 1-unit investment purchase 85% / limited cash-out 75% — Fannie Mae Eligibility Matrix (eff. April 1, 2026) and Freddie Mac maximum LTV/TLTV/HTLTV requirements.

- Freddie Mac CHOICERenovation lists 1-unit investment property as eligible and permits ADU additions/renovation — Freddie CHOICERenovation product page and ADU fact sheet (one ADU on 1–3-unit properties).

- HomeStyle upfront disbursement up to 50% of renovation costs for eligible categories — Fannie Mae SEL-2025-10; UAD 3.6 multiple-ADU expansion is limited to properties classified as principal residences (same source).

- FHA 203(k) is owner-occupants only — FDIC affordable-mortgage-lending guide; HUD 203(k) program page. FHA ADU rental-income rules (general 75% of lesser; Standard 203(k) proposed-ADU 50% of lesser; 30% cap; two months’ reserves; no ADU income on FHA cash-out) — HUD Mortgagee Letter 2023-17.

- DSCR ADU comp rule (at least one comparable ADU sale and one comparable ADU rent, or income excluded) — OfferMarket DSCR requirements, March 2026.

- Investment HELOC LTV ~75–80% and limited availability — Bankrate and NerdWallet, 2026.

- ADU construction-cost ranges — HomeGuide, Angi (2026), and Snap ADU (March 2026); treat as ranges, not quotes. ADU rent range (~$1,600–$2,500/mo for ~600 sq ft major-metro units) — Maxable, via Yahoo Finance.

- Owner-occupancy zoning example — Salt Lake City Code (ADU owner-occupancy requirement).

Re-check before relying on: the current FHFA conforming loan limit, any rate range, agency LTVs, UAD 3.6 lender implementation, and current FHA provisions — these change frequently. We re-verify quarterly and on any GSE/FHA bulletin. We are not a lender; confirm your numbers with a licensed professional. Forum sources (Reddit, BiggerPockets) were used only for borrower language and objections, never as proof of laws or loan rules.

Methodology and editorial standards

Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We built this guide’s eligibility matrix by cross-referencing primary agency sources — Fannie Mae’s Selling Guide and Eligibility Matrix, Freddie Mac’s CHOICERenovation documentation, maximum-LTV requirements, and ADU fact sheet, HUD/FHA program rules and Mortgagee Letter 2023-17, and the FDIC’s lending guide — against current investor-lending guidelines and 2026 ADU construction-cost data. Regulatory facts are sourced to primary or authoritative documents and dated. Commercial terms (rates, LTV bands, availability) are verified at publication and re-checked quarterly. Any “which option fits whom” guidance is labeled as our editorial judgment based on those verified facts.

We reviewed competitor lender and builder pages for format and gaps, and we used investor forums (Reddit, BiggerPockets) solely for voice-of-customer language and objections — never as evidence for laws or loan terms. We are not a lender, broker, or builder, and we do not rank options by compensation. This guide is educational and is not financial, legal, tax, or lending advice. Loan approval, available products, rates, fees, loan-to-value limits, rental-income treatment, and ADU eligibility all depend on the lender, the borrower, the property, local regulations, the appraisal, and current program rules.

Frequently asked questions

Can you finance an ADU on a rental property?

Yes, but use investor-eligible paths: an investment-property HELOC or home equity loan, a cash-out refinance, Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, a DSCR loan, or portfolio/bridge financing. Owner-occupied ADU loan advice often won't apply to a true rental.

Can I use an FHA 203(k) loan for an ADU investment property?

No, not for a true non-owner-occupied investor — the FDIC guide states the 203(k) program is for owner-occupants, not investors. It can matter for a house-hack or owner-occupied ADU, but not for a pure rental.

Can Fannie Mae HomeStyle finance an ADU on an investment property?

Yes, under specific conditions. Fannie's current matrix lists HomeStyle Renovation for a one-unit investment-property purchase (85% LTV) and limited cash-out refinance (75%), and allows accessory units where local zoning and building codes permit.

Can Freddie Mac CHOICERenovation finance an ADU on an investment property?

Yes, for a one-unit investment property within CHOICERenovation's limits. Freddie lists 1-unit investment property as an eligible property type and allows adding or renovating an ADU, including via a no-cash-out refinance that pays off short-term ADU financing.

Can projected ADU rent help me qualify on an investment property?

Sometimes. Freddie Mac can count ADU rental income on a subject one-unit investment property when its Guide requirements are met, and DSCR loans qualify on the property's overall cash flow. The Fannie Mae DU 12.1 ADU-income update, by contrast, is owner-occupied only.

Can I use a HELOC on an investment property to build an ADU?

Sometimes. Investment-property HELOCs exist, but fewer lenders offer them, LTV caps are lower (Bankrate lists ~75–80% combined LTV), and qualification is stricter than for a primary-residence line.

Should I refinance or keep my low mortgage?

Compare the full debt stack. A second lien or HELOC can preserve a low-rate first mortgage, while a cash-out refinance replaces it. The right answer depends on your equity, the rate spread, the loan amount, the construction timeline, and your exit strategy.

Can a DSCR loan include ADU rent?

Possibly — but the ADU usually needs to be legal and appraisable, and some programs require comparable ADU sales and rents in the area or the ADU income is excluded. Don't assume unpermitted-ADU rent will count.

What if my ADU isn't permitted?

Permitting or legalization comes before financing. Unpermitted ADUs can create appraisal, insurance, rental-income, and lender-acceptance problems, and their rent and value are often excluded.

Can I finance two ADUs on one investment property?

Maybe — it depends on the program, the lender's appraisal/UAD implementation, unit count, local law, and property classification. Fannie's UAD 3.6 multiple-ADU expansion is tied to properties classified as principal residences, so don't assume it applies to a pure investment property; verify with your lender.

Does local zoning matter if the lender says yes?

Yes. Financing never overrides local zoning, building code, utility, fire, parking, owner-occupancy, or rental rules. Some cities — Salt Lake City, for example — require owner occupancy for an ADU, which can conflict with a pure investor strategy. Confirm legality first.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU ReportFree · No commitment