ADU Appraisal Requirements: How Your Accessory Dwelling Unit Is Valued (2026)

By The Dwelling Index Editorial Team — an independent research resource covering ADU financing, costs, and regulations. Last updated: May 22, 2026 · Last verified: May 22, 2026

Bottom line, up front

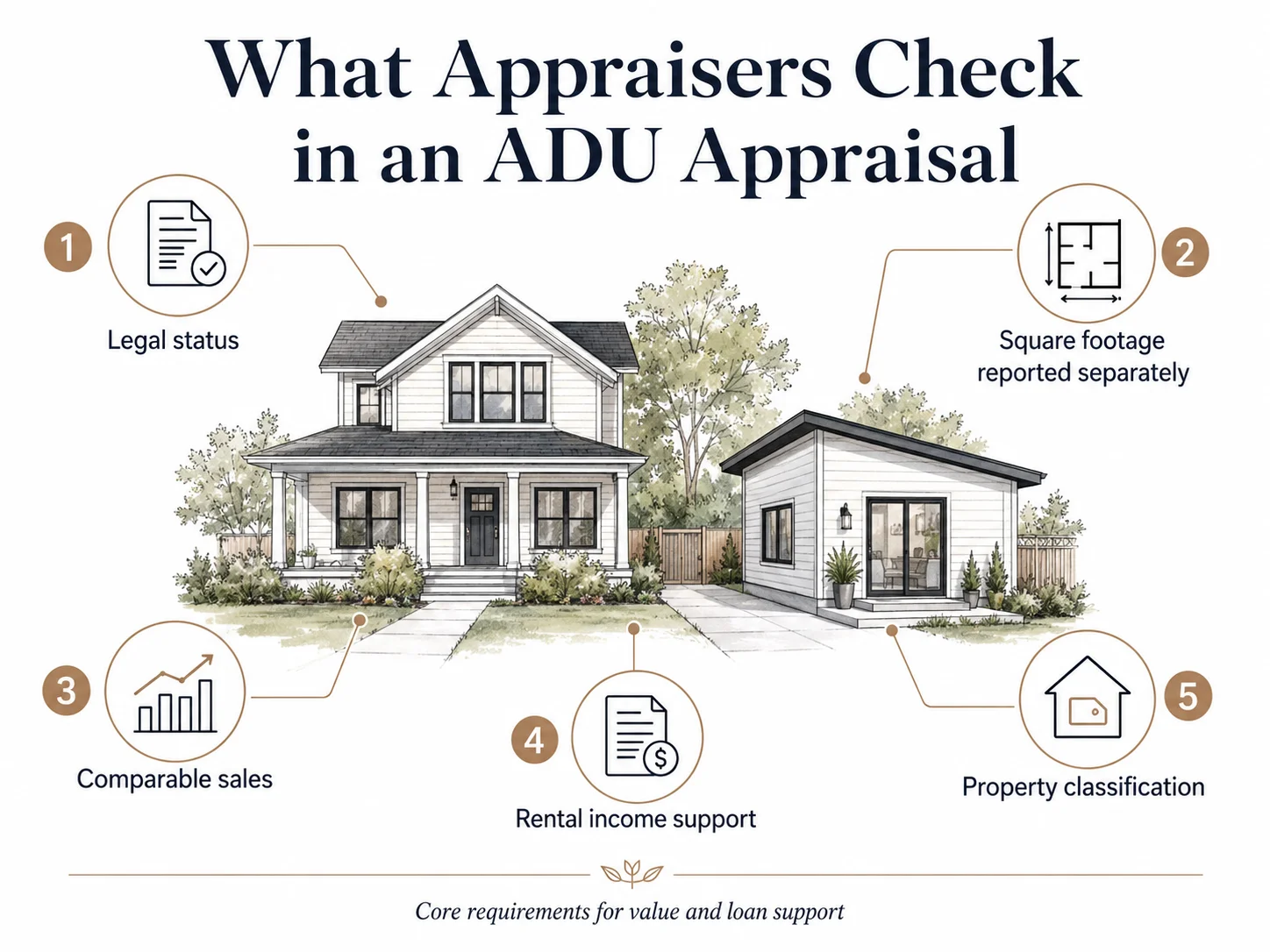

ADU appraisal requirements come down to four things the appraiser and your lender must be able to confirm: that the unit is a true accessory dwelling unit — a self-contained second home on the same lot with its own kitchen, bath, and sleeping area; that the property is classified correctly (one home with an ADU, not a duplex); that the ADU’s square footage is reported the right way (usually separately from the main house, not added to it); and that the value or rent is backed by market evidence.

An ADU does not get valued by multiplying its square footage by your home’s price per square foot. The single biggest factor in whether your unit helps or hurts is its legal/permit status — a permitted, zoning-compliant ADU is in the strongest position to be analyzed for value, and on some major loan paths its rent can help you qualify, but only when the program, transaction type, legal status, and appraisal support all line up.

Who this is for: homeowners building or refinancing, buyers purchasing a home with an ADU, and anyone whose deal hinges on the unit “counting.” One number to anchor on: an ADU-property appraisal typically runs about $400–$800, modestly more than a standard single-family appraisal. Next step: confirm permit status and gather your documents before you order the appraisal — the checklist is below.

At a glance: will your ADU count?

| If your ADU is… | Likely on the appraisal | Can its rent help you qualify? |

|---|---|---|

| Permitted & zoning-compliant | Strongest position; analyzed for contributory value with market support | Often yes — on Fannie/Freddie purchase or limited/no-cash-out refi, FHA (not cash-out), some VA |

| Legal nonconforming (legal when built; zoning later changed) | Generally financeable; appraiser notes any value effect | Usually yes, with documentation |

| Unpermitted | High-risk; value support is weak and often minimal | Usually no |

| Zoning-prohibited / illegal use | Special pathway; needs same-use comps and lender sign-off | No (illegal-use rent can’t be used) |

See what your property can support → Get your free ADU report in about 60 seconds.

Why we built this guide

Search “ADU appraisal requirements” and page one splits into two unhelpful halves. On one side, builder and real-estate blogs promise an ADU “adds 30%” and tell you to multiply square footage by a neighborhood price-per-square-foot — math appraisers do not use, and that sets homeowners up to be blindsided. On the other side, the genuinely accurate sources — the Fannie Mae Selling Guide, HUD’s Handbook 4000.1, Freddie Mac’s ADU fact sheet — are written for appraisers and underwriters, fragmented across dozens of pages, and effectively unreadable for the person whose loan is on the line.

We are Dwelling Index, an independent research resource covering ADU financing, costs, and regulations. We read the primary rulebooks for every major loan program, reconciled them against each other, and translated them into one homeowner-readable page. Every agency or lending rule below is sourced to a primary federal or government-sponsored-enterprise (GSE) document, with the verification date visible; practical, real-world examples are labeled separately as practitioner color. Where a rule is changing in 2026 — and two big ones are — we say exactly what is current law and what is merely proposed.

This page owns one job: appraisal mechanics and lender appraisal requirements for ADUs. It is not a “how much does an ADU cost” page or a “best ADU loan” page; we link to those where relevant.

One distinction to hold onto before you read the matrix, because it trips up almost everyone: appraised contributory value and qualifying rental income are two separate decisions. Your ADU can add value to the appraisal and still have its rent excluded from your income — or vice versa. We keep them separate throughout.

What are ADU appraisal requirements by loan type?

Answer capsule:

ADU appraisal requirements differ by loan program. Conventional loans (Fannie Mae and Freddie Mac), FHA, VA, and USDA each set their own rules for how the unit is classified, whether it must be permitted and zoning-compliant, how its value is captured, and whether — and on which transaction types — its rent can count toward qualifying income. The matrix below consolidates all five programs in one place, decoded from primary sources.

This is the asset we could not find anywhere else: a single homeowner-facing matrix across every major loan program. We assembled it from the Fannie Mae Selling Guide (B2-3-04, B4-1.3-05, B3-3.8-01) and Announcement SEL-2025-08, Freddie Mac’s Single-Family ADU resource, HUD’s FHA Mortgagee Letter 2023-17, the VA Lender’s Handbook, and USDA Rural Development guidance and current rulemaking.

The 2026 ADU Appraisal & Rental-Income Matrix

| Question | Conventional — Fannie Mae | Conventional — Freddie Mac | FHA | VA | USDA (Rural Dev.) |

|---|---|---|---|---|---|

| Must the ADU be legal / zoning-compliant? | Legal, or legal nonconforming, is fine. An ADU prohibited under zoning has a separate “illegal use” pathway (see below). | Generally must be legal, legal nonconforming, or in an area with no zoning; illegal-ADU rent may not be used. | Must comply with zoning, including legal nonconforming use; must meet FHA Minimum Property Requirements (MPRs). | Must meet VA MPRs; legality and local building-authority acceptance matter. | Must comply with zoning; effect of any nonconforming use on value must be reported. |

| Is the ADU counted in the main house’s GLA? | No — reported separately. Narrow exception: an interior, above-grade ADU that is part of the primary dwelling with interior access. | Reported separately; appraisal describes condition, finished area, room/bed/bath count when ADU rent is used. | GLA reported separately from the primary dwelling. | Reported separately. | Reported separately. |

| Can ADU rent help you qualify? | Yes — on a one-unit principal residence, one ADU only, 30% cap. (SEL-2025-08, eff. Oct. 8, 2025.) | Yes — on a one-unit primary residence, with specific appraisal evidence required; 30% cap. | Yes — 75% of the lesser of market or lease rent (existing ADU); 50% of projected rent via a 203(k) rehab loan. | Some lenders count rental income (commonly 75% of fair-market rent) for a legally permitted ADU — lender-overlay territory; confirm with your VA lender. | Not currently — a rented / income-producing ADU is presently ineligible; only household-support ADUs qualify. A proposed rule could change this (see below). |

| Which transactions allow ADU rent for qualifying? | Purchase or limited cash-out refinance only | Purchase or no-cash-out refinance only. | All eligible FHA forward transactions except cash-out refinances. | Per VA / lender overlay. | N/A under current rule. |

| Cap on ADU rental income | 30% of total qualifying income. | Lease-based income capped at 75%; qualifying ADU rent capped at 30% of total qualifying income. | 30% of total monthly effective income. | Per VA / lender overlay. | N/A. |

| Comp / evidence rule when sales are scarce | An aged settled sale qualifies as a comparable; an active listing or pending sale can serve as a supplemental marketability exhibit. | When ADU rent is used: ≥1 ADU sale comp and ≥3 comparable rentals (including ≥1 rented ADU); an automated appraisal waiver (ACE) is not acceptable. | ≥1 comparable rental that is a single-family dwelling with a rented ADU; if none is available, the appraiser supplements with the most appropriate rental and explains the selection. Transient rentals (under 30 days) not acceptable. | Appraiser provides a fair-market-rent estimate when no lease exists. | “Best available” comps permitted when truly comparable sales are scarce. |

Sources: Fannie Mae Selling Guide B2-3-04 (10/08/2025), B4-1.3-05, B3-3.8-01 (10/08/2025) & Announcement SEL-2025-08; Freddie Mac Single-Family ADU resource (2026); HUD FHA Mortgagee Letter 2023-17 (Oct. 16, 2023) & Handbook 4000.1; VA Lender’s Handbook Ch. 4; USDA HB-1-3555 Ch. 12 and Federal Register docket RHS-26-SFH-0100. Verified May 22, 2026.

Decoder notes

- “Legal nonconforming” means the ADU was legal when built but no longer matches current zoning (the rules tightened later). Fannie Mae instructs appraisers to report it as legal nonconforming and reflect any adverse value effect — it is generally financeable.

- “Limited cash-out refinance” (Fannie’s term; also called a rate-and-term refinance) is a refinance where you take essentially no cash out — just rolling the existing balance and costs into a new loan. It is not the same as a cash-out refinance, where you pull equity out as cash. This distinction is the difference between your ADU rent counting or not on a Fannie loan.

- “Reported separately” is the rule homeowners trip on most. Your 1,500-square-foot house with a 600-square-foot detached ADU is not a “2,100-square-foot home” on the appraisal. We dedicate a full section to this below.

- The 30% cap (Fannie, Freddie, FHA) means ADU rent can only do so much lifting. If you need the ADU’s income to account for more than 30% of the income you qualify on, it won’t stretch that far on those programs.

🔎 Two 2026 rule changes worth knowing — both verified, both consequential.

(1) Multiple ADUs, under the new appraisal format. Under Fannie’s existing UAD 2.6 Selling Guide text, only one ADU is permitted on a one-unit dwelling and ADUs aren’t permitted on 2–4 unit dwellings. Under the new UAD 3.6 Policy supplement, for loans sold on or after March 31, 2026 and only for lenders using UAD 3.6, Fannie expands eligibility to one-unit properties with up to three ADUs and 2–3 unit properties with ADUs, capped at four total dwelling units (Fannie Mae UAD 3.6 Policy, May 2026). Important: even with multiple ADUs allowed for eligibility, only one ADU’s rent can be used for qualifying.

(2) A new appraisal format becomes mandatory. For new appraisal reports submitted to the Uniform Collateral Data Portal (UCDP) on or after November 2, 2026, lenders must use UAD 3.6; the familiar form-based experience (Form 1004/70) changes to a redesigned dynamic report (Fannie Mae UAD webpage). If your appraisal is ordered near or after that date, it will look different.

➡️ See what your property can support.

Rules are one thing; your specific lot, zoning, and ADU type are another. Get your free ADU report → and see what’s possible at your address before you spend a dollar on plans or an appraisal.

🔎 What we verified (this table)

Conventional rules from the Fannie Mae Selling Guide (B2-3-04, B4-1.3-05, B3-3.8-01) and Announcement SEL-2025-08; Freddie Mac’s ADU resource; FHA from HUD ML 2023-17 and Handbook 4000.1; USDA from HB-1-3555 Ch. 12 and Federal Register docket RHS-26-SFH-0100; VA from the VA Lender’s Handbook. Two items we flag plainly: (1) VA does not publish a single clean ADU-specific rental-income rule — the 75% figure reflects VA’s general rental framework applied through lender overlays, so confirm with your VA lender; (2) Fannie’s ADU-income rule reached Desktop Underwriter® in Q1 2026 (manual underwriting was eligible from October 8, 2025) — your lender’s path may affect timing. Verified May 22, 2026.

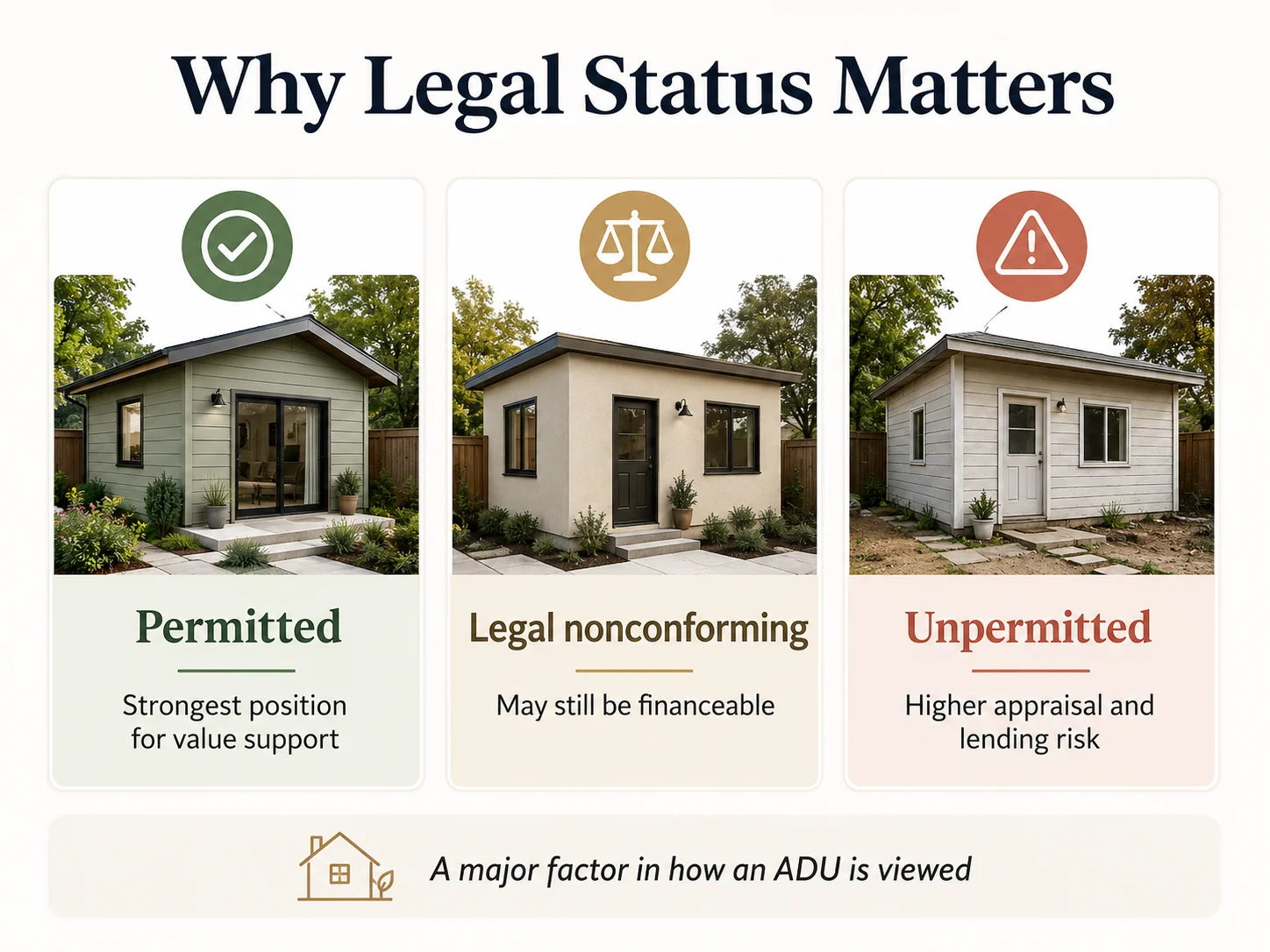

What happens if your ADU is permitted, legal nonconforming, or unpermitted?

Answer capsule:

Legal status is the highest-stakes variable in an ADU appraisal. A permitted, zoning-compliant ADU is in the strongest position to be analyzed for contributory value, and its rent can count where the loan program and transaction type allow. An unpermitted ADU is high-risk: agency guidance doesn’t impose a blanket “zero value” rule, but appraisers and lenders frequently assign little or no contributory value when legal status or market support is weak, and rent generally can’t be used.

We built a decision tree because this one variable changes everything downstream. Find your status, read across — then see the consequence table beneath it.

The permit-status decision tree

| Your ADU’s status | What it means | Likely appraisal treatment | Your move |

|---|---|---|---|

| Legal & permitted (final inspection / certificate of occupancy) | Built with permits, complies with current zoning | Strongest position; analyzed for contributory value with market support; rent eligible where program/transaction allow | Hand the appraiser your permits, plans, and certificate of occupancy. |

| Legal nonconforming | Was legal when built; zoning later changed | Generally financeable; appraiser reports it as legal nonconforming and notes any adverse value effect | Document that it predates the ordinance change; confirm your lender accepts legal nonconforming. |

| Unpermitted (work done without permits) | No permits pulled, but zoning may allow ADUs | Higher risk; appraiser must comment on quality, appearance, and any value impact — value support is often weak and conservative | Strongly consider retroactive permitting before the appraisal. |

| Zoning-prohibited / illegal use | Zoning bans ADUs here entirely | Special “illegal use” pathway; appraisal must state the improvements are an illegal zoning use and support marketability with same-use comps | Talk to your lender before ordering the appraisal — this is delicate. |

Legal status vs. lender consequence

| Issue | What the rulebook actually says | Practical consequence |

|---|---|---|

| Unpermitted work | Fannie requires the appraiser to comment on the quality and appearance of the work and on any impact on value — not an automatic $0 (Fannie Mae B4-1.3-05) | In practice, when supporting comps don’t exist, the contributory value assigned is often minimal — sometimes treated as “storage” by lenders (practitioner color: GatherADU, JVM Lending) |

| Illegal zoning use | If the property contains an ADU not allowed under zoning, Fannie requires the report to state the improvements represent an illegal zoning use and to support marketability with comparable sales of the same non-compliant use (Fannie Mae B4-1.3-05) | Financeable only in narrow cases with same-use comps; rent cannot be used |

| Legal nonconforming | Reported as legal nonconforming; adverse value effect must be reflected (Fannie Mae B2-3-04 / B4-1.3-05) | Generally financeable |

| Permitted but weak comps | The unit is legitimate, but few or no ADU comps exist nearby | Value support becomes conservative — see the “no comps” section |

Why unpermitted units so often get little value

Here’s the honest version: for lending, an unpermitted ADU is a problem, and the value frequently lands far below build cost. The rule itself doesn’t say “zero” — Fannie’s guidance directs the appraiser to comment on the work and its market-value impact. But the practical reality, reported consistently by lenders, is that when comparable sales of similar unpermitted units don’t exist (and they usually don’t), the safe and defensible treatment is minimal contributory value (GatherADU; JVM Lending). The fix is legitimacy, not relabeling — you can’t make the problem disappear by calling the kitchen a “wet bar.” If the unit functions as an ADU, it’s reported as one.

The retroactive-permitting fix

If your loan or sale depends on the ADU counting and the unit is unpermitted, the highest-leverage move is usually to resolve the permit record before the appraisal, then make sure the appraiser sees the signed-off, finaled permit. Retroactive permitting isn’t free or instant, and in some cases code issues can make it expensive — but it’s frequently the difference between minimal value and full analysis. We’d rather you know that now than discover it after a low appraisal.

➡️ Download the free ADU Starter Kit.

It includes our pre-appraisal document checklist — every record to gather and the exact questions to ask your city’s building department before you order the appraisal. Get the free Starter Kit →

🔎 What we verified (this section)

Unpermitted-additions comment requirement and the illegal-zoning-use pathway (Fannie Mae B4-1.3-05; B2-3-04). The “minimal value / storage” outcome is labeled as practitioner color (GatherADU, Mar. 2026; JVM Lending, June 2024), not an agency rule. Verified May 22, 2026.

How do appraisers actually value an ADU?

Answer capsule:

Appraisers value ADU properties using up to three methods: the sales comparison approach (the primary method for homes), the income approach (when the ADU is a rental), and the cost approach (a conservative reasonableness check). They report the ADU’s living area separately from the main home’s gross living area and do not value an ADU by multiplying its square footage by the main home’s price per square foot.

Understanding the method matters because it explains why your appraisal can land far from what you spent. First, here’s which approach tends to drive value on each loan path — an original cross-reference we assembled:

Which appraisal approach matters by loan path

| Loan path | Primary value method | Rent schedule used? | Required evidence highlight |

|---|---|---|---|

| Fannie Mae | Sales comparison | Form 1007/1000 when ADU rent qualifies | Aged sale OK as comp; active listing as supplemental |

| Freddie Mac | Sales comparison | Yes, when ADU rent qualifies | ≥1 ADU sale comp + ≥3 rent comps (1 a rented ADU); no ACE waiver |

| FHA | Sales comparison + market rent analysis | Form 1007/1000 | ≥1 SFR-with-rented-ADU rent comp (or explained substitute); 2 months’ PITI reserves if rent used |

| VA | Sales comparison | Appraiser fair-market-rent estimate | Lender-overlay driven for ADUs |

| USDA | Sales comparison | N/A (rental ADU ineligible now) | Appraiser confirms not currently income-producing |

| HELOC / cash-out refi / renovation | Lender/investor overlay; often as-completed value | Varies by investor | Conservative where comps are scarce |

Sales comparison approach (the one that usually decides it)

The appraiser finds 3–6 recently sold comparable properties (“comps”) and adjusts their prices for differences with yours. With ADUs, the appraiser ideally wants comps that also have ADUs, then adjusts for size, quality, and rental potential. As one lender, GatherADU, illustrates: if a comparable home with a similar but slightly smaller ADU sold for $800,000, the appraiser might add a size adjustment of $20,000–$50,000 for your larger unit.

The catch — and it’s the central tension of ADU appraisal — is comp scarcity. ADUs are still a small share of sales in most markets. FHFA’s appraisal data shows that in California Enterprise-backed single-family purchase appraisals, the share with ADUs was just 2.9% in 2023 (and nationally, the share rose only from 0.9% in 2013 to 1.2% in 2023). When ADU comps are thin, the appraiser makes larger, more subjective adjustments, and underwriters scrutinize the result harder.

Income approach (for rentals)

When the ADU produces rent, the appraiser can estimate value from income. Conceptually: take the ADU’s annual rent, subtract expenses to reach net operating income (NOI), and divide by a market capitalization rate. An 800-square-foot ADU renting for $2,500/month is $30,000/year; net out, say, $6,000 in expenses for $24,000 NOI; at a 10% cap rate that implies roughly $240,000 of contributory value (illustrative math drawn from APEX Homes’ worked example). This is why income-producing ADUs in strong rental markets sometimes appraise into six figures — but only when the rent is documented and the market supports it.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Cost approach (the conservative check)

The appraiser estimates what it would cost to rebuild the main house and ADU, then subtracts depreciation. This usually produces the most conservative number because it ignores the income premium and market demand. It functions as a sanity check: if sales comparison suggests the ADU added $250,000 but it cost $150,000 to build two years ago, the cost approach flags that gap (GatherADU).

Why the “+30% / $500-a-square-foot” math is misleading

Here’s a damaging admission, because you deserve the unvarnished version: an ADU frequently appraises for less than it cost to build, at least in the near term. The lender JVM Lending reports that when ADU comps are scarce, appraisers often value a unit conservatively in the $25,000–$50,000 range, because if they’re more aggressive, underwriters “kick back” the appraisal and demand additional comparable sales that usually don’t exist (JVM Lending, June 2024).

That is not a reason to abandon your ADU plans — it’s a reason to set the right expectation. An ADU is a long-term improvement to a property you already own, not a same-day equity machine. The value compounds over time (more on the federal data below), and much of the real return is utility: housing family, generating rent, or aging in place. But if you’re banking on the appraisal alone to reimburse your build cost the moment the unit is finished, that’s the expectation that gets people hurt — and now you won’t be one of them.

| Bad shortcut | The question the appraiser actually asks |

|---|---|

| Main-house $/sq ft × ADU sq ft = value added | What do buyers actually pay for similar homes with ADUs nearby? |

| Build cost = appraised value | What portion of that cost does market evidence support? |

| Monthly rent = guaranteed loan income | Does the program and transaction type allow it, and did the appraiser support market rent with comps? |

🔎 What we verified (this section)

FHFA’s California 2.9% (2023) and national 0.9%→1.2% ADU-appraisal shares (FHFA UAD blog, Jan. 2025); JVM Lending’s $25,000–$50,000 conservative range and underwriter “kick-back” dynamic (JVM, June 2024); the three-approach framework and worked income example (GatherADU, Mar. 2026; APEX Homes, Feb. 2026). Verified May 22, 2026.

Does ADU square footage count in my home’s total square footage?

Answer capsule:

Usually no. An ADU’s living area is normally reported separately from the primary home’s gross living area (GLA), not added to it — so a 1,500-square-foot house with a 600-square-foot ADU is not appraised as a 2,100-square-foot home. A narrow exception exists for an interior, above-grade ADU that is part of the primary dwelling with interior access, which may be included in the main GLA.

This is the question homeowners ask more than any other, so it gets its own section. The instinct is natural: “If my house is 1,500 square feet and I add a 600-square-foot ADU, my home is now 2,100 square feet, right?” For appraisal reporting, almost always no. Fannie Mae’s guidance treats the ADU’s area separately from the primary dwelling’s above-grade GLA, with the narrow exception noted above for an interior ADU that is genuinely part of the main dwelling (Fannie Mae B4-1.3-05).

Why does this matter so much to your outcome? Because GLA drives a huge share of a home’s appraised value, and how the ADU is reported changes which comps and which math apply. If the ADU were lumped into GLA, the appraiser would compare your “2,100-square-foot home” to other 2,100-square-foot homes — most of which are larger single dwellings, not a house-plus-cottage. Reporting the ADU separately lets the appraiser value it as what it is: a distinct income-and-utility feature with its own contributory value.

There’s a strategic wrinkle worth knowing. One lender (JVM Lending) notes that when an ADU is accessible from the main dwelling, the square footage can sometimes be combined — which can help, because it lets the appraiser use larger, higher-end comps. Whether that helps or hurts depends entirely on your local comps, so it’s a conversation to have with your lender and appraiser, not a default move.

🔎 What we verified (this section)

Separate-GLA reporting and the interior-ADU exception (Fannie Mae B4-1.3-05); the “accessible ADU may allow combined square footage / larger comps” point is labeled practitioner color (JVM Lending, June 2024). Verified May 22, 2026.

Can you use ADU rental income to qualify for a mortgage?

Answer capsule:

On most loan programs you can use part of an ADU’s rent to qualify, but the rules are program- and transaction-specific and capped. Fannie Mae allows it on a one-unit principal residence for purchase or limited cash-out refinance only, one ADU, capped at 30% of qualifying income. FHA allows 75% of the lesser of market or lease rent for an existing ADU (50% projected via a 203(k) loan), capped at 30%, and not on cash-out refinances. USDA currently does not allow rental-ADU income at all.

This is the rule set that genuinely changes who gets approved. Decoded program by program.

FHA — the rules FHA Mortgagee Letter 2023-17 created

Before late 2023, FHA borrowers generally couldn’t use ADU rent to qualify. FHA Mortgagee Letter 2023-17 (effective October 16, 2023, part of the federal Housing Supply Action Plan) changed that. Decoded directly from the source:

- For an existing ADU, count 75% of the lesser of (a) the appraiser’s market-rent estimate or (b) the actual lease rent. So a $1,000/month ADU adds $750/month to qualifying income.

- For a new ADU added through FHA’s Standard 203(k) rehabilitation loan, count 50% of the estimated rent — the unit doesn’t even have to exist yet.

- ADU rental income cannot exceed 30% of total monthly effective income.

- It cannot be used on a cash-out refinance (ML 2023-17, II.A.8.d.v(A)).

- Reserves: if ADU rental income is used to qualify on a one-unit-with-ADU property, the lender must verify two months’ PITI (principal, interest, taxes, insurance) in reserves after closing (ML 2023-17, II.A.4.d.i(C)). Budget for this — it’s a real, often-overlooked requirement.

- The appraiser documents ADU market rent on Form 1007/1000 (Single-Family Comparable Rent Schedule) using the URAR (Form 1004/70).

- A renter of an ADU is not a “boarder.” FHA treats ADU rent and boarder income under separate rules — don’t let a loan officer conflate them (ML 2023-17).

ML 2023-17 also expanded what FHA can finance: Standard 203(k) eligible improvements now include converting a one-family structure to one-family-with-ADU, adding an ADU attached to an existing structure, or renovating an existing attached or detached ADU; and FHA new construction now recognizes one-unit-with-ADU property types — though not every ground-up detached build is automatically a 203(k) deal, so confirm your scenario.

Conventional — Fannie Mae

This changed materially in late 2025. Per Fannie Mae Announcement SEL-2025-08 (effective October 8, 2025), ADU rental income can be used for qualifying only when all of these hold: the subject is a one-unit principal residence; the transaction is a purchase or limited cash-out refinance (not a cash-out refinance); the income comes from only one ADU even if multiple exist; and the ADU rent used cannot exceed 30% of total qualifying income. The rule reached Desktop Underwriter® (DU® v12.1) in Q1 2026; lenders could apply it to manually underwritten loans immediately from October 8, 2025.

Conventional — Freddie Mac

Freddie Mac’s ADU resource is the clearest evidence checklist in the industry. When ADU rental income is used to qualify on a one-unit primary residence, the appraisal must include at least one ADU sale comp and at least three comparable rentals, one of which is a rented ADU, and an automated appraisal waiver (ACE) is not acceptable. Lease-based income is capped at 75%, with the same 30% overall cap, and the qualifying path is limited to purchase and no-cash-out refinance transactions.

VA

VA loans permit rental income generally, and VA’s framework commonly applies a 75% factor to gross rent (the 25% haircut covers vacancy and maintenance). For an ADU specifically, VA does not publish a single clean ADU rental-income rule — counting that rent leans heavily on individual VA-lender overlays and typically expects a legally permitted unit with an appraiser-supported fair-market rent. Treat VA as overlay territory and confirm with your VA lender before relying on it.

USDA — the one that says no (for now)

This one surprises people. Under current USDA Single-Family Housing Guaranteed Loan Program guidance, an ADU does not automatically make a property ineligible — but if the ADU is noted as currently rented or income-producing, the property is ineligible regardless of the applicant’s future intent. Only ADUs that support the household (a mother-in-law suite for a family member) qualify (USDA HB-1-3555 Ch. 12). That may change: USDA published a proposed rule (Federal Register docket RHS-26-SFH-0100) on March 31, 2026 that would allow financing a single-family home with one or more income-producing ADUs, with public comments due June 1, 2026. Until that rule is finalized, treat income-producing USDA ADUs as not allowed.

Forms by program (the ones you’ll hear named)

| Form | What it is | Where it shows up |

|---|---|---|

| Form 1004 / Form 70 (URAR) | Standard residential appraisal report | Conventional & FHA one-unit (incl. with ADU). Being retired Nov. 2, 2026 for UAD 3.6 |

| Form 1007 / 1000 | Single-Family Comparable Rent Schedule | Documenting ADU market rent (Fannie, FHA) |

| Form 1025 / 72 | Small Residential Income Property Appraisal Report | 2–4 unit properties (not one-unit-with-ADU) |

| Form 1004D / 442 | Appraisal Update / Completion Report | Confirming completion of construction or repairs |

➡️ Explore your ADU financing paths.

If rental income is central to your plan, it’s worth understanding the lanes — purchase, limited cash-out refinance, renovation loans, and construction-to-permanent — before you order an appraisal that locks in assumptions. We present financing as education, not lender rankings, and we never sort by anything but neutral criteria. Compare ADU financing & refinance options →

🔎 What we verified (this section)

FHA 75%/50%/30%/cash-out/reserves/forms and the ADU-is-not-a-boarder rule (HUD ML 2023-17, full text); Fannie purchase/limited-cash-out limit, one-ADU rule, and 30% cap (Fannie Mae Announcement SEL-2025-08, eff. Oct. 8, 2025; Selling Guide B3-3.8-01); Freddie evidence checklist, 75% lease cap, and no-cash-out limit (Freddie Mac ADU resource); VA general 75% framework (VA Lender’s Handbook Ch. 4); USDA current prohibition and proposed rule (USDA HB-1-3555 Ch. 12; Federal Register RHS-26-SFH-0100). Verified May 22, 2026.

What if there are no ADU comps near you?

Answer capsule:

When few or no comparable sales with ADUs exist nearby, an appraiser can still develop a credible value, but the result often becomes more conservative because larger, more subjective adjustments are required. Appraisers expand search parameters and may use an aged settled sale as a comparable or an active listing as supplemental marketability evidence, per Fannie Mae guidance.

“No comps” does not mean “no value,” but it does mean more friction. Here’s how each program handles scarcity — another original cross-reference, since this is where deals quietly stall.

Comp-scarcity fallbacks by program

| Program | What’s allowed when ADU comps are scarce |

|---|---|

| Fannie Mae | An aged settled sale qualifies as a comparable; an active listing or pending sale serves as a supplemental marketability exhibit (B4-1.3-05) |

| Freddie Mac | When ADU rent is used, the ≥1 ADU sale comp + ≥3 rent comps requirement still applies — scarcity doesn’t waive it, and no ACE waiver |

| FHA | If no SFR-with-rented-ADU rent comp exists, the appraiser supplements with the most appropriate rental available and explains the selection and ADU marketability (ML 2023-17) |

| USDA / VA | Best-available comps / lender-overlay judgment |

Experienced appraisers also expand their parameters — a wider radius, a longer time window, or comps that share the subject’s main draw (the ADU itself) even if other features differ — then adjust accordingly (McKissock, Jan. 2026). Fannie’s own FAQ acknowledges that where truly comparable sales are short, the appraiser may use the best available sales even if they aren’t perfectly comparable.

The evidence packet that helps

You can’t pick the comps, but you can make the appraiser’s job easier and the file more defensible:

| Evidence | Why it helps |

|---|---|

| Final permit / certificate of occupancy | Proves legal completion — the single most important document |

| Floor plan + measured ADU area | Prevents GLA confusion and “is this storage?” questions |

| Photos of kitchen, bath, sleeping area, separate entrance | Establishes it functions as a true ADU |

| Lease + rental history | Supports rent analysis where the program allows it |

| Local long-term rental comps | Supports the appraiser’s market-rent estimate |

| Any nearby sales you know of with ADUs | Gives the appraiser candidate comps to verify |

| Zoning/code citation for your parcel | Reduces legal-status ambiguity |

| Separate utility/address documentation | Informs the one-unit-vs-2-to-4-unit classification |

🔎 What we verified (this section)

Aged-sale and active-listing flexibilities and “best available” comp principle (Fannie Mae B4-1.3-05 and Appraisal FAQ); FHA rent-comp fallback (HUD ML 2023-17); parameter-expansion practice (McKissock, Jan. 2026). Verified May 22, 2026.

What if your appraisal comes in low? The Reconsideration of Value (ROV) playbook

Answer capsule:

If an appraisal undervalues your ADU, you generally cannot choose the appraiser — the lender orders it through an Appraisal Management Company (AMC) — but you can file a Reconsideration of Value (ROV) through your lender. A successful ROV is evidence-based: additional comparable sales, documented rental data, proof of permits, or factual corrections to the report.

The number came in low. Before you panic, understand the mechanics and your actual leverage.

For a lender transaction, the appraisal is ordered through an AMC, and you usually can’t select the specific appraiser — though you can ask your lender for one with ADU experience, and some accommodate it (GatherADU, Mar. 2026). Once the report is in, the lever is the ROV. Here’s exactly what to submit, by problem:

ROV evidence triage

| If the problem is… | What to submit |

|---|---|

| Wrong square footage | Your measured floor plan and any prior appraisal or builder plans |

| Missing permit proof | The finaled permit / certificate of occupancy — especially if value was docked on a mistaken “unpermitted” assumption |

| A missed ADU comp | The address and details of a comparable sale with an ADU the appraiser didn’t use (within standard guidelines) |

| Missed rent data | A signed lease, rental history, and credible local rent comps (where the program counts ADU income) |

| Wrong classification | Evidence supporting one-unit-with-ADU vs. duplex (utility, address, legal-rentability facts) |

Avoid sending comps that violate standard appraisal guidelines — wildly different size, across a major barrier like a freeway, or in a different city — because the appraiser can’t use them anyway (JVM Lending). Quality over quantity.

Sometimes the honest answer is that no ROV will rescue a unit that simply isn’t legal yet. If the low value traces to permit status, the durable fix is to permit the unit and re-appraise — not to argue the existing report. We’d rather tell you that now than have you spend two weeks fighting an unwinnable ROV.

➡️ Check your lot before you rely on ADU value or rent.

If you’re early enough to plan, our free report shows what your address can support — and flags the permit and zoning questions to resolve before an appraiser is ever involved. Get your free ADU report →

🔎 What we verified (this section)

AMC ordering, ROV process, and request-an-experienced-appraiser option (GatherADU, Mar. 2026); comp-eligibility guardrails (JVM Lending, Aug. 2023). Verified May 22, 2026.

Does an ADU actually add value at resale? What the federal data shows

Answer capsule:

FHFA California appraisal data shows that properties with ADUs had higher median appraised values and stronger median-value growth than properties without ADUs — about $1,064,000 versus $715,000 in 2023 — but the data does not prove that an individual ADU adds the full difference in value. It is California-specific aggregate data, not a promise for any single property.

This is where we part ways with the “+30%” blog claims and show you the real source. The Federal Housing Finance Agency (FHFA) — the regulator over Fannie Mae and Freddie Mac — added ADU data to its Uniform Appraisal Dataset (UAD) Aggregate Statistics and published Trends in Median Appraised Value for Properties With Accessory Dwelling Units in California in January 2025.

The headline figures: in 2023, the median appraised value was about $1,064,000 for California properties with ADUs versus about $715,000 without (FHFA, Jan. 2025). Properties with ADUs also showed faster median-value growth across 2013–2023.

Two honest caveats, because the gap above is not a clean “an ADU adds $349,000” claim:

- It’s California, and it’s aggregate. Homes with ADUs may differ systematically from homes without them (bigger lots, pricier neighborhoods). FHFA itself notes the data is emerging and further analysis is needed.

- Appraisal rarely captures the full benefit immediately. As SnapADU candidly observes from the same data, for many homeowners the return isn’t the appraisal bump — it’s the ability to house family, age in place, or earn rent where buying a second property is out of reach. If you need fast equity extraction, an ADU is probably the wrong vehicle.

For the full ROI and resale deep-dive, see our companion guide on whether an ADU increases property value.

🔎 What we verified (this section)

FHFA median appraised values (~$1,064,000 with ADU vs. ~$715,000 without, 2023) and faster decade growth (FHFA UAD blog, Trends in Median Appraised Value for Properties With ADUs in California, Jan. 2025); “appraisal rarely captures full benefit” framing (SnapADU, Mar. 2026, labeled practitioner color). Verified May 22, 2026.

What counts as an ADU in an appraisal (and what doesn’t)?

Answer capsule:

For appraisal and lending, an ADU is an independent living area on the same parcel as the primary one-unit home, with its own facilities for living, sleeping, cooking, and bathing. A second kitchen alone does not make a property an ADU, and removing a stove does not necessarily avoid ADU classification — the appraiser evaluates independent access, full living facilities, legal status, and how the property would be marketed.

Definitions decide outcomes here. Fannie Mae’s definition requires the unit to provide living, sleeping, cooking, and bathroom facilities on the same parcel as the primary dwelling. Fannie even specifies kitchen detail — cabinets, a countertop, a sink, and a stove or stove hookup — and clarifies that a hotplate, microwave, or toaster oven is not a substitute for a stove (Fannie Mae B2-3-04). Translation: you can’t dodge ADU classification by unplugging the range, and you can’t claim ADU value with just a wet bar. Here’s how the categories sort out:

ADU vs. wet bar vs. guest house vs. duplex

| Feature | Independent kitchen? | Sleeping + bath? | Separate entrance? | Likely classification |

|---|---|---|---|---|

| Wet bar / second kitchenette only | Partial (no stove) | No | No | Not an ADU |

| Guest room / “in-law” with shared facilities | No | Maybe | Maybe | Usually part of main dwelling |

| True ADU | Yes (incl. stove/hookup) | Yes | Yes | One-unit with ADU |

| Full second unit (own meter, own address, freely rentable) | Yes | Yes | Yes | May be classified as a duplex / 2-unit |

One-unit-with-ADU vs. 2-to-4-unit — the classification that changes your loan

This is subtle but pivotal. Whether your home is treated as “one unit with an ADU” or as a “2-to-4-unit property” changes which loan rules apply. Fannie Mae says the classification turns on characteristics like separate utility meters, a unique postal address, and whether the unit can be legally rented — and the appraiser determines it in the highest-and-best-use analysis (Fannie Mae B2-3-04). If your “ADU” looks and functions like a full second unit, an appraiser may classify the property as a duplex, a different lending box entirely.

Subordinate in size, and the unit types

Across programs, an ADU must be subordinate to the primary dwelling — smaller and clearly secondary. A backyard structure that rivals the main house invites the reclassification above. On unit types: appraisers care less about the marketing label than about real-property status, permanent installation, legality, and market evidence.

A JADU (junior ADU) is a smaller unit carved out within the home’s existing footprint; in California, a junior ADU is no more than 500 square feet of interior livable space and is contained within the residence (California HCD ADU Handbook). Manufactured-home ADUs are eligible under Fannie Mae when titled as real property, and Fannie’s March 2026 UAD 3.6 update expanded eligibility further.

🔎 What we verified (this section)

ADU facility definition and stove-vs-hotplate clarification, plus one-unit-vs-2-4-unit classification factors (Fannie Mae B2-3-04); JADU 500-sq-ft definition as California-specific (California HCD ADU Handbook, 2026); manufactured-home ADU eligibility and UAD 3.6 expansion (Fannie Mae UAD 3.6 Policy, May 2026). Verified May 22, 2026.

What can my lender reject even if the appraiser gives value?

Answer capsule:

A favorable appraised value does not guarantee your loan. A lender can still reject ADU value or rent if the transaction type doesn’t allow ADU income, if illegal-use rent is involved, if required reserves are missing, if an appraisal waiver isn’t permitted for the scenario, or if the required rent schedule or ADU comps aren’t in the file.

Appraisal and underwriting are two gates, and people forget the second one. Even with a strong appraisal, your file can stall on:

- Wrong transaction type — e.g., trying to use ADU rent on a Fannie cash-out refinance, or an FHA cash-out (not allowed).

- Illegal-use rent — Freddie won’t let you qualify on illegal-ADU rent even if the appraiser noted market acceptance.

- Missing reserves — FHA’s two-months’-PITI reserve requirement when ADU rent is used.

- No appraisal waiver allowed — Freddie’s ACE waiver isn’t acceptable when ADU rent is used; the full appraisal is required.

- Missing rent schedule or ADU comps — no Form 1007/1000, or the required ADU sale/rent comps absent from the file.

The fix for all of these is the same: confirm your program’s rules with your lender before you order the appraisal, so the file is built right the first time.

🔎 What we verified (this section)

Transaction-type limits (Fannie SEL-2025-08; Freddie ADU resource; FHA ML 2023-17 cash-out exclusion); FHA reserves (ML 2023-17); Freddie no-ACE rule (Freddie Mac ADU resource). Verified May 22, 2026.

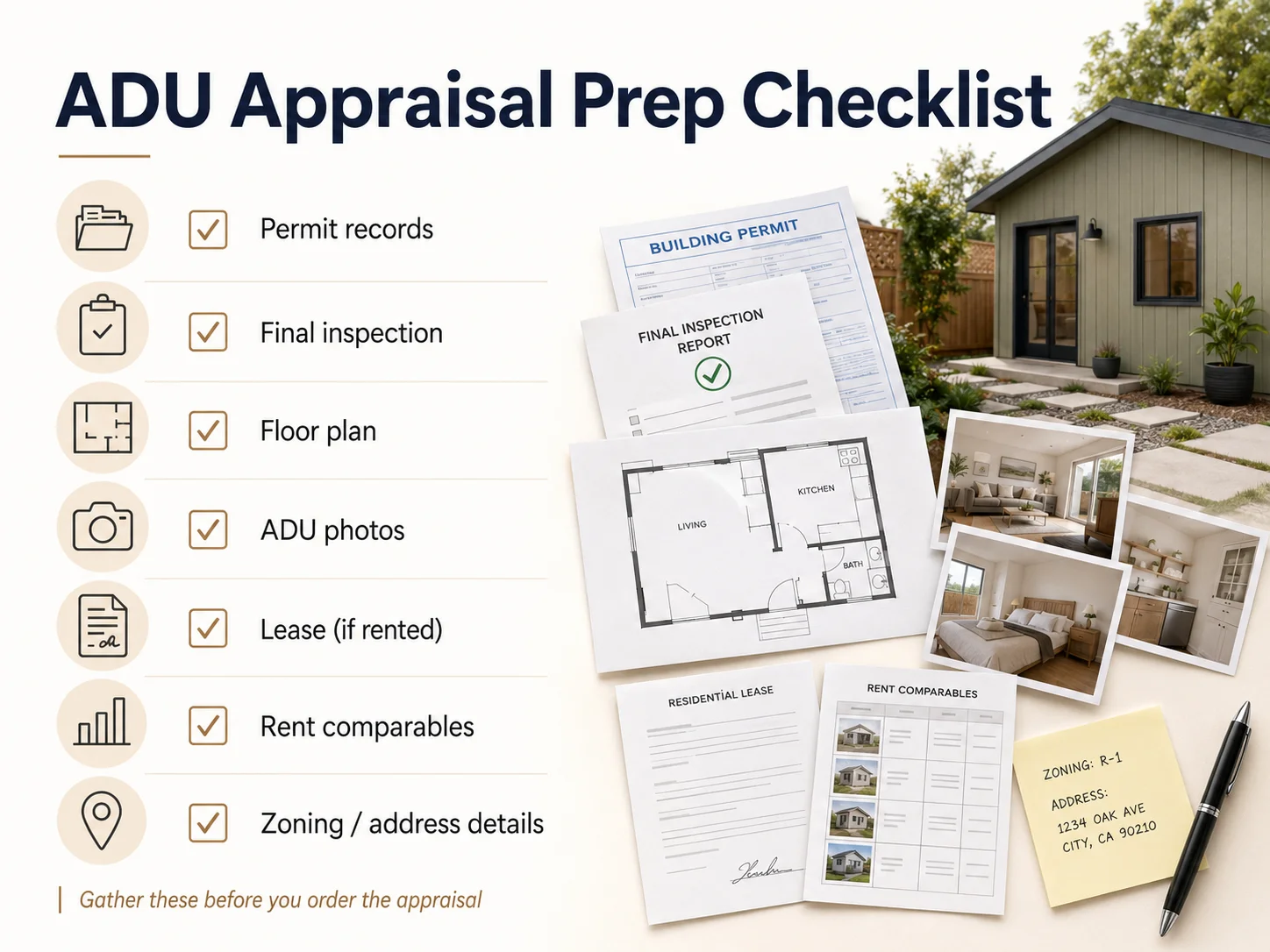

How to prepare for an ADU appraisal: a step-by-step checklist

Answer capsule:

To prepare for an ADU appraisal, assemble a documentation packet before the inspection and confirm the loan rules with your lender first. The goal is not to influence the appraiser but to make the ADU easy to identify, measure, classify, and support with verifiable records — permits, floor plans, photos, leases, and zoning proof.

Step 1 — Before you order the appraisal (ask your lender these exact questions)

- Which loan program and investor rules apply to my file?

- Will ADU rent be used to qualify — and is my transaction type eligible (purchase, limited/no-cash-out refi, not cash-out)?

- Which rent form is required — Form 1007/1000, or the UAD 3.6 rental fields?

- Will my appraisal be UAD 2.6 or UAD 3.6, given the November 2, 2026 transition?

- Is an appraisal waiver (value acceptance / ACE) allowed or disallowed for my scenario?

- If ADU rent is used, what reserves will I need (FHA requires two months’ PITI)?

- How will an unpermitted or legal-nonconforming ADU be handled?

Step 2 — Before the appraiser visits (assemble the packet)

- Permit records and the final inspection / certificate of occupancy

- A floor plan and the measured ADU square footage

- Photos of the kitchen, bath, sleeping area, and separate entrance

- Utility and address documentation (informs classification)

- Your parcel’s zoning/ADU ordinance citation

Step 3 — If rent is involved

- Current lease and rental history

- Long-term rent comps (avoid relying on short-term/Airbnb projections — FHA won’t accept transient rentals under 30 days)

- Any local rental-registration or short-term-rental rules that apply

Step 4 — After the appraisal (review before you accept)

- Was the ADU correctly identified as an ADU?

- Was its square footage reported separately (usually correct) and accurately?

- Was rent included or excluded — and does that match your program’s rules?

- If something’s wrong, use the ROV evidence triage above and ask your lender about a Reconsideration of Value.

🔎 What we verified (this section)

Form 1007/1000 and UAD documentation (Fannie Mae B3-3.8-01; HUD ML 2023-17; Fannie Mae UAD webpage); Freddie no-ACE-with-ADU-rent rule (Freddie Mac ADU resource); FHA transient-rental exclusion and reserves (HUD ML 2023-17). Verified May 22, 2026.

What ADU appraisal edge cases change the rules?

Answer capsule:

Several less-common situations materially alter an ADU appraisal: multiple ADUs on one lot (now allowed by Fannie Mae under UAD 3.6 as of March 2026), HOA restrictions, selling before comparable sales exist to support the unit, manufactured-home ADUs, and the appraisal-cost premium for ADU properties.

- Multiple ADUs. As of March 31, 2026, Fannie Mae (for UAD 3.6 appraisals) allows up to three ADUs on a one-unit property, and ADUs on 2–3 unit properties, capped at four total dwelling units (Fannie Mae UAD 3.6 Policy, May 2026). Note: even so, only one ADU’s rent can be used to qualify.

- HOA restrictions. Even where state and local law permit an ADU, a homeowners association can impose restrictions. These don’t change the appraisal mechanics, but they can affect marketability — which the appraiser considers.

- Selling before comps exist. If you’re the first ADU on your block, expect a conservative appraisal. The market premium materializes as more ADU sales accumulate nearby.

- Appraisal cost. One 2026 private-source estimate puts a single-family-with-ADU appraisal at about $400–$800 (vs. roughly $350–$500 for a standard single-family) and $600–$1,200 if the income approach is used on an investment property; local lender, property, FHA/VA, and market factors can differ (GatherADU, Mar. 2026).

- The November 2, 2026 form change. Appraisals submitted to UCDP on or after that date use the new dynamic UAD 3.6 report instead of Form 1004/70.

🔎 What we verified (this section)

Multiple-ADU eligibility and one-ADU rent limit (Fannie Mae UAD 3.6 Policy, May 2026; SEL-2025-08); appraisal cost ranges labeled as a private-source estimate (GatherADU, Mar. 2026); UAD 3.6 mandate date (Fannie Mae UAD webpage). Verified May 22, 2026.

ADU appraisal requirements FAQ

How do appraisers value a property with an ADU?

Appraisers use the sales comparison approach (the primary method — finding comparable sold homes, ideally with ADUs, and adjusting), the income approach (capitalizing the ADU's net rental income), and the cost approach (a conservative rebuild-cost-minus-depreciation check). They report the ADU's square footage separately from the main home's gross living area and do not value it by a simple price-per-square-foot multiplication (Fannie Mae B4-1.3-05; GatherADU).

Does an unpermitted ADU add value to an appraisal?

Usually very little, for lending. Agency guidance doesn't impose a blanket "zero value" rule — Fannie requires the appraiser to comment on the work and its value impact — but when supporting comps don't exist, appraisers and lenders frequently assign minimal contributory value, sometimes treating the space as "storage." The durable fix is usually retroactive permitting before the appraisal (Fannie Mae B4-1.3-05; GatherADU; JVM Lending).

Can I use ADU rental income to qualify for a mortgage?

Often, with caps and conditions. Fannie Mae allows it on a one-unit principal residence for purchase or limited cash-out refinance, one ADU, 30% cap (SEL-2025-08). FHA allows 75% of the lesser of market or lease rent (50% projected via 203(k)), 30% cap, not on cash-out, with two months' PITI reserves. USDA currently does not allow rental-ADU income (Fannie Mae SEL-2025-08; HUD ML 2023-17; USDA HB-1-3555).

Does ADU square footage count in my home's total square footage?

Usually no. The ADU is reported separately from the main house's gross living area, with a narrow exception for an interior, above-grade ADU that is part of the primary dwelling with interior access (Fannie Mae B4-1.3-05).

Why did my ADU appraise for so little?

Most often because comparable sales with ADUs were scarce, forcing a conservative value; or because the unit was unpermitted; or because the build cost exceeded what the local market currently pays for ADU homes. Appraisers value market reaction, not your construction invoice (JVM Lending).

How much does an ADU appraisal cost?

A 2026 private-source estimate puts it at roughly $400–$800 for a single-family home with an ADU, and $600–$1,200 if an income approach is required; local factors vary (GatherADU, Mar. 2026).

What's the difference between an ADU and a 2-to-4-unit property?

Classification turns on features like separate utility meters, a unique postal address, and whether the unit can be legally rented. The appraiser decides in the highest-and-best-use analysis. A unit that functions like a full second residence may push the property into duplex/multi-unit lending territory (Fannie Mae B2-3-04).

What is a Reconsideration of Value (ROV)?

A formal request, filed through your lender, asking the appraiser to revisit value based on new evidence — additional comps, rental data, permit proof, or factual corrections. You generally can't pick the appraiser, but a well-documented ROV can change the number (GatherADU).

Are prefab or manufactured ADUs treated differently?

They can be. Treatment depends on whether the unit is legally installed, considered real property, permitted, and permanently affixed where required. Fannie Mae has specific manufactured-home ADU guidance and, as of March 2026, expanded eligibility under UAD 3.6 (Fannie Mae B2-3-04; UAD 3.6 Policy).

How we researched this guide (methodology)

Answer capsule:

This guide was researched by reviewing primary federal and GSE sources first — the Fannie Mae and Freddie Mac selling guides, HUD’s FHA Mortgagee Letter and Handbook 4000.1, VA and USDA guidance, and FHFA data — then translating those lender-and-appraiser-facing rules into homeowner decisions. Community sources were used only to understand how homeowners phrase their questions, never as proof for legal, financing, or appraisal claims.

We are Dwelling Index, an independent research resource covering ADU financing, costs, and regulations. We built this page because page-one results were either accurate-but-unreadable (agency rulebooks) or readable-but-misleading (builder blogs). Our source priority: (1) primary agency guidance and rulebooks; (2) official mortgagee letters, guides, and fact sheets; (3) federal data sources; (4) lender and appraiser education pages for practical color, always labeled as such; (5) community forums for homeowner language only.

What this page is not: it is not a loan approval, a rate quote, legal or tax advice, a local zoning determination, or an appraiser’s instruction manual. ADU rules vary by lender, investor, property, and jurisdiction, and 2026 is an unusually active year for rule changes. Always verify current requirements with your lender, your appraiser, and your local building department before you commit.

Recency plan (what we re-check, and when)

| Element | Refresh cadence | How we verify |

|---|---|---|

| Fannie Mae / Freddie Mac ADU rules | Monthly through Nov. 2026, then quarterly | selling-guide.fanniemae.com; sf.freddiemac.com |

| UAD 3.6 transition (Nov. 2, 2026 mandate) | Monthly until mandate | Fannie Mae & Freddie Mac UAD webpages |

| FHA ADU rules | Quarterly, or immediately on a new Mortgagee Letter | hud.gov / Handbook 4000.1 |

| USDA income-producing ADU rule | Monthly until the proposed rule is finalized or withdrawn | Federal Register docket RHS-26-SFH-0100 |

| VA appraisal/MPR treatment | Quarterly | VA Lender’s Handbook |

| FHFA value data | Semi-annually | fhfa.gov/data/uad |

| Appraisal cost ranges & rental percentages | Quarterly | Primary sources above |

🔎 What we verified (page summary)

Source categories used: Conventional appraisal & ADU rules — Fannie Mae Selling Guide (B2-3-04, B4-1.3-05, B3-3.8-01), Announcement SEL-2025-08, and UAD 3.6 Policy; Freddie Mac Single-Family ADU resource. FHA — HUD Mortgagee Letter 2023-17 (full text) and Handbook 4000.1. VA — VA Lender’s Handbook (Ch. 4). USDA — HB-1-3555 Ch. 12 and Federal Register docket RHS-26-SFH-0100. Market/value context — FHFA UAD Aggregate Statistics. State code — California HCD ADU Handbook (JADU). Practitioner color (labeled, not used for agency rules) — JVM Lending, GatherADU, McKissock, APEX Homes.

Items we flagged for you to confirm with your lender: (1) VA’s ADU rental treatment is overlay-driven, not a single clean published rule; (2) Fannie’s ADU-income rule reached Desktop Underwriter in Q1 2026 (manual underwriting eligible since Oct. 8, 2025), so timing can depend on your lender’s path.

Last updated: May 22, 2026 · Last verified: May 22, 2026.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

Get your free ADU report →