Manufactured Home ADU — Complete Guide

Manufactured Home ADU: Can You Use One, What It Really Costs, and What to Check First

The bottom line, up front

Yes — a manufactured home ADU can be legal, but only when four things line up: your local zoning allows a HUD-code manufactured home as an accessory dwelling unit, the unit is a true HUD-code manufactured home (not an RV, park model, or tiny home on wheels), the foundation and utilities meet your local permit path and any financing requirements, and the project clears final approval — including a certificate of occupancy where your jurisdiction requires one. California gives the clearest “yes” — state law (Government Code §66313) expressly defines an ADU to include a manufactured home. Many other cities allow it too; some quietly block true manufactured homes and steer you toward a modular unit instead. The one number to anchor on: a new manufactured home itself averaged $88,200 (single-section) or $161,200 (double-section) as of December 2025 (U.S. Census / FRED) — but that’s a national sales-price anchor, not your installed ADU budget, which climbs once you add foundation, utilities, delivery, set, permits, and site work.

Applies to: U.S. homeowners evaluating a manufactured home ADU on a residential lot, especially single-family lots.

Do this first: Confirm what’s allowed on your lot before you pay a dealer deposit or order plans. See What You Can Build → Get Your Free ADU Report

Manufactured home ADU: the answer in 30 seconds

| Your question | Fast answer |

|---|---|

| Can a manufactured home be an ADU? | Yes in many places. California state law expressly includes manufactured homes in the ADU definition (Gov. Code §66313); other jurisdictions decide locally. |

| Is it the same as a “mobile home”? | No. Post-June-15-1976 homes are HUD-code manufactured homes. Older “mobile homes” are commonly prohibited as ADUs. |

| Is it cheaper than site-built? | The unit usually is. The installed project may not be once foundation, utilities, permits, and site work are added. |

| Does it need a permanent foundation? | Almost always, in practice — and it’s required for nearly all financing and for legal “real property” status. |

| What’s the first step? | Verify zoning, foundation, and utility path in writing before you put money down. |

Sources: U.S. Census Manufactured Housing Survey via FRED (Dec 2025); CA Gov. Code §66313; 24 CFR Part 3280. Verified .

Not sure what’s allowed on your lot?

See What You Can Build → Get Your Free ADU ReportIn this guide

Why we wrote this (and why most pages get it wrong)

Here’s the thing almost no other page tells you plainly: “manufactured home ADU” is one of the most misunderstood searches in all of ADU research. The confusion is built into the words.

A homeowner sees a factory home advertised at $60,000–$90,000, compares it to a $250,000 site-built ADU quote, and reasonably thinks, why isn’t everyone doing this? Then they start reading and run into a wall of contradictory terms — manufactured, modular, mobile, prefab, park model, tiny home — used interchangeably by people who should know better, including some city websites.

We think the most useful thing we can give you is this: the factory unit is rarely the hard part. The lot is the hard part. Setbacks, sewer capacity, crane access, the foundation, title conversion, HOA rules, and lender documentation are where manufactured-home ADU projects actually succeed or die. A low sticker price doesn’t touch any of those.

So this page does what dealer brochures and generic cost calculators won’t: it decodes the federal definition, shows you exactly which cities allow what (with the controlling code sections), builds the real cost stack, and walks the financing reality — then hands you the exact questions to ask your building department before you spend a dollar.

What can still kill the project (read this before you fall in love with a floor plan)

We’d rather you hear the dealbreakers now than after a deposit. A manufactured home ADU can stall or die when:

- Your city says no to HUD-code manufactured homes as ADUs (some allow only modular).

- There’s no delivery or crane access to the backyard.

- Sewer or septic capacity fails, or the connection run is long and expensive.

- The permanent-foundation or title-conversion path doesn’t pencil out.

- An HOA or private covenant blocks the exterior or the use.

- A lender can’t get the documentation (HUD labels, real-property classification) it needs.

Can a manufactured home be used as an ADU?

Sometimes — and the deciding factor is local, not federal. The U.S. government defines and regulates manufactured homes through HUD construction standards (24 CFR Part 3280), but your city or county decides whether that HUD-code home can be permitted as an ADU on your specific parcel. California is the clearest state-level “yes”: Government Code §66313 states that an accessory dwelling unit “also includes… a manufactured home, as defined in Section 18007 of the Health and Safety Code.” Outside California, the answer ranges from explicit yes, to allowed-with-conditions, to a hard no — and you cannot assume.

Let’s decode that California citation, because it’s the strongest legal proof in this whole topic. In March 2024, California renumbered its ADU statutes (under SB 477, effective March 25, 2024), moving the long-cited §65852.2 into a new chapter beginning at §66313. The definition was then refreshed again by SB 543, effective January 1, 2026. So if you find an older guide quoting “65852.2,” it isn’t wrong about the substance — it’s using the pre-2024 number. The current section, §66313(a)(2), puts manufactured homes inside the ADU definition itself. In plain English: in California, a city cannot say “we allow ADUs but not manufactured homes” — the state has already declared a manufactured home to be a permissible form of ADU.

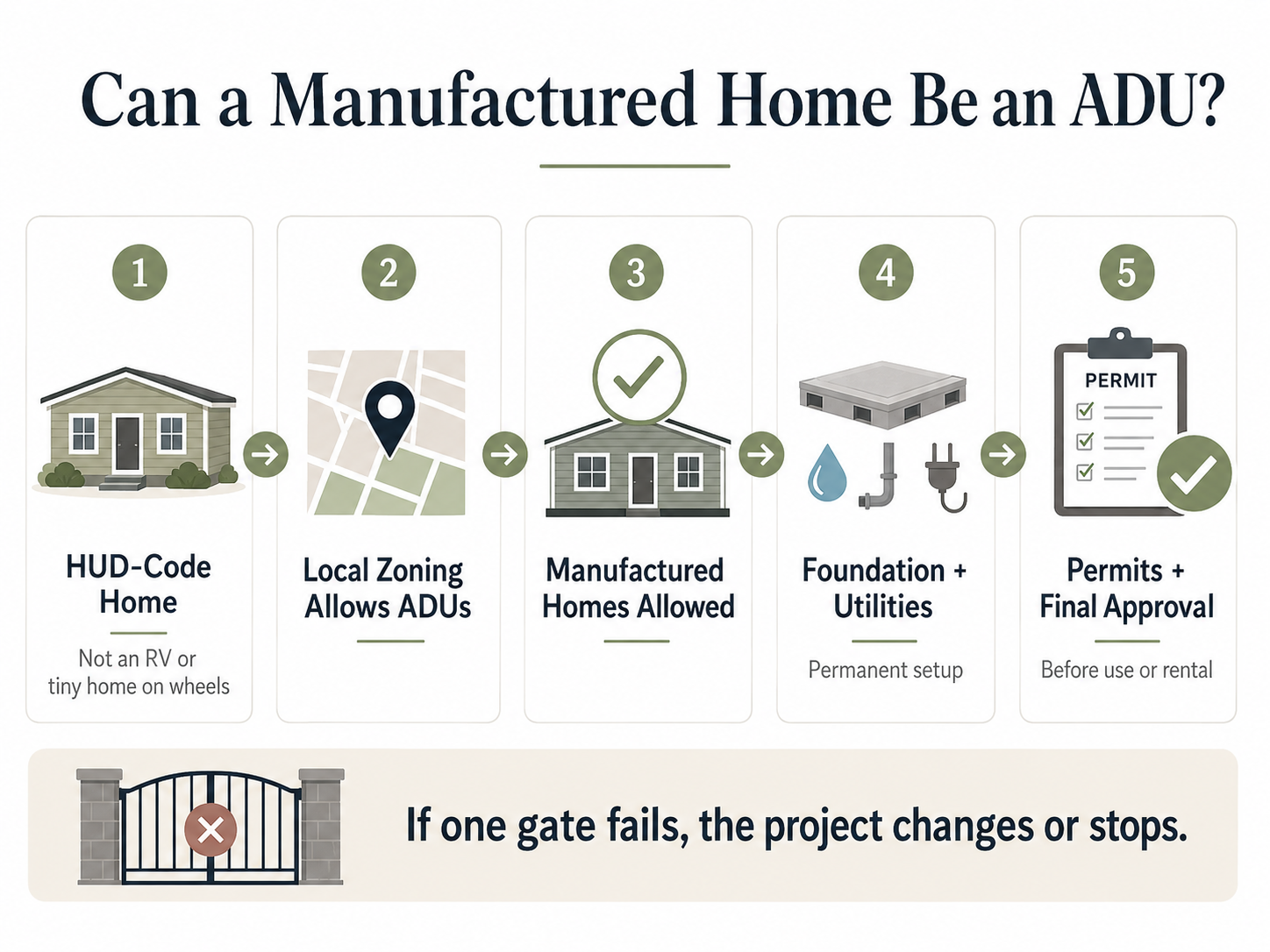

The 5-part legal test (run this before anything else)

Whether you’re in California or Connecticut, a manufactured home ADU has to clear five gates:

- 1Is the unit a HUD-code manufactured home — not an RV, park model, travel trailer, or uncertified tiny home?

- 2Does local zoning allow a detached ADU on your lot at all? (Lot size, zone, existing dwelling.)

- 3Does that code allow the ADU to be a manufactured home — or only a site-built/modular structure?

- 4Can the unit meet objective standards — setbacks, max size, height, design/roof-pitch/siding rules, foundation, access, and utility capacity?

- 5Can you obtain permits, pass inspections, and receive final approval — including a certificate of occupancy where required — before anyone lives in it or rents it?

If any gate is a “no,” that’s not a small problem — it’s the whole project.

Verified examples — where manufactured homes are explicitly addressed

We pulled these directly from the controlling sources (not summaries) so you can see how differently jurisdictions handle the same question:

- California (statewide): ADU definition includes a manufactured home per Gov. Code §66313(a)(2). Verified May 27, 2026.

- Moreno Valley, CA: An ADU may be a manufactured home on a permanent foundation only; travel trailers and tiny homes on wheels without permanent foundations and fixed utilities are excluded. moval.gov/adu. Verified May 27, 2026.

- Citrus Heights, CA: A manufactured home may be used as an ADU if it meets Health & Safety Code §18007; movable tiny homes may not be used as ADUs, and short-term rentals under 31 days are prohibited. citrusheights.net. Verified May 27, 2026.

- Portland, OR: City zoning allows an ADU to be proposed as a manufactured home, and allows ADUs on sites with a house, attached house, or manufactured home. portland.gov. Verified May 27, 2026.

- Clark County, WA: A manufactured or modular home may be considered an ADU if it meets county code; mobile homes built before June 15, 1976 are not allowed. Building permits and inspections are required, and the ADU cannot be occupied until a certificate of occupancy is issued. clark.wa.gov. Verified May 27, 2026.

- Raleigh, NC: UDO §3.6.2 permits a manufactured-home ADU only with specific design standards and no more than 600 sq. ft. A city FAQ conflicts with the ordinance — the ordinance controls. Ask the city to confirm the controlling section. Raleigh UDO §3.6.2. Verified May 27, 2026.

The Raleigh example is exactly why we tell readers never to rely on a city FAQ page. Ask for the code section.

Not sure what your city allows? You shouldn’t have to read three ordinances and a zoning map to find out.

See What You Can Build → Get Your Free ADU ReportWe’ll flag whether a manufactured home ADU is likely viable at your address and give you the exact questions to bring to your building department.

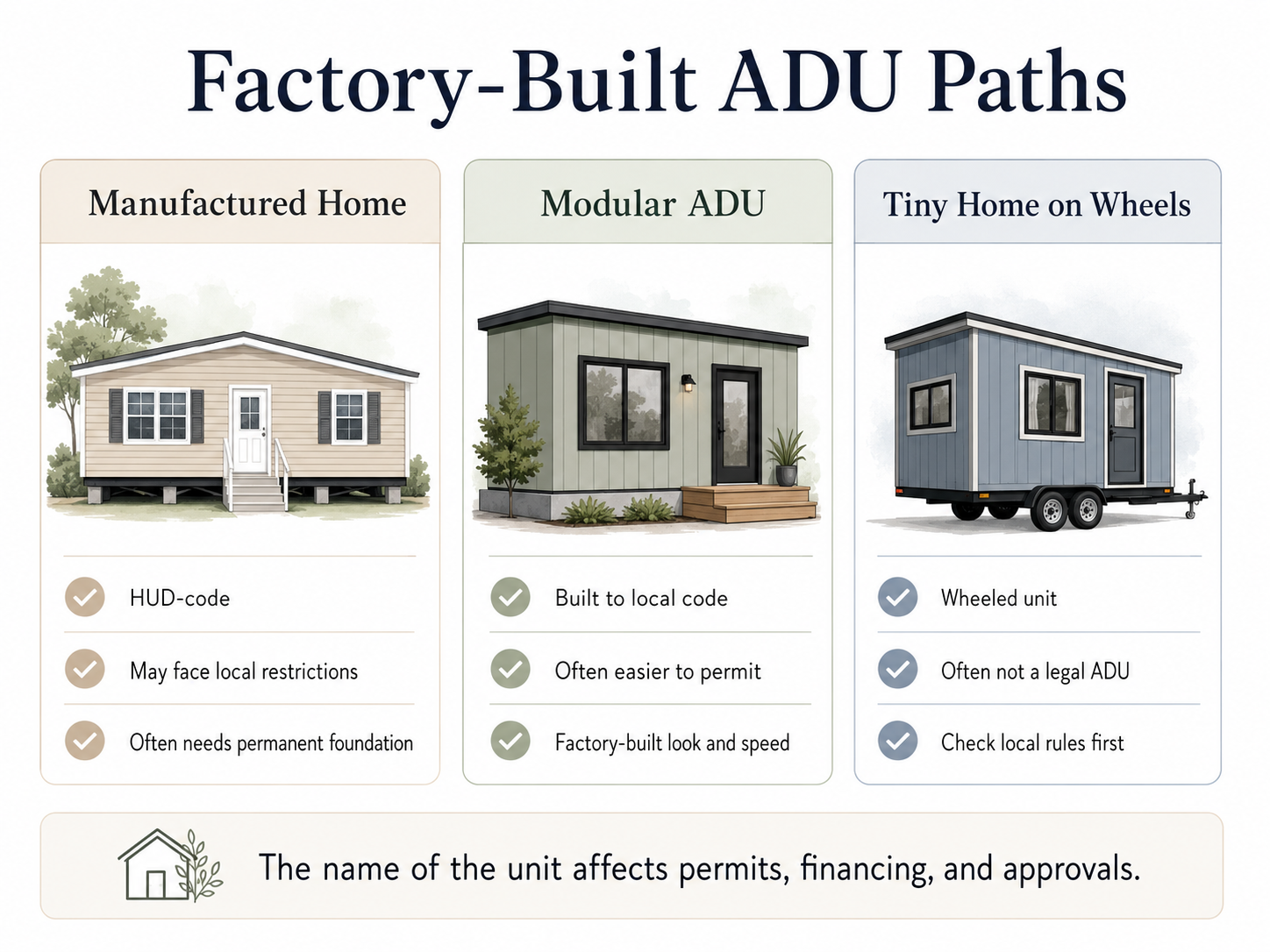

Manufactured vs. modular vs. prefab vs. mobile home: the difference that decides everything

These five terms are not interchangeable, and confusing them is the number-one reason a manufactured-home ADU gets denied. The deciding factor is which building code the home is built to. A “manufactured home” is built to the federal HUD Code (24 CFR Part 3280) on a permanent steel chassis. A “modular home” is built in a factory to your state and local building code (the same IRC code as a site-built house). A “mobile home” technically means a pre-June-15-1976 unit and is frequently prohibited. “Prefab” is just an umbrella marketing word. And a “tiny home on wheels” is usually an RV in the eyes of code — not a legal ADU unless your city specifically says so.

That single fact — which code — cascades into everything: whether you can permit it, how it’s financed, how it appraises, and what foundation it needs.

Build-type comparison

| Type | Built to | How it arrives | The common ADU issue | Best fit |

|---|---|---|---|---|

| Manufactured home | Federal HUD Code (24 CFR 3280) | One or more sections on a permanent chassis | Some cities restrict or exclude it; real-property/foundation/titling must be handled | Lots in jurisdictions that explicitly allow manufactured ADUs |

| Modular home | State/local building code (IRC) | Factory modules set on a foundation | Costs more than manufactured, but treated like site-built and accepted in far more places | Homeowners who want factory speed with site-built code treatment |

| Prefab (umbrella term) | Varies — could be any of these | Varies | The word hides whether it's manufactured, modular, panelized, or park model | Early-stage comparison only |

| Mobile home | Pre-1976 / colloquial | Varies | Older units commonly prohibited; the word alone can alarm planners and lenders | Avoid this term unless your code uses it |

| Tiny home on wheels / park model | RV/ANSI or other standard | On wheels | Many cities don't treat it as a legal ADU | Only where code expressly allows it |

The practical takeaway: when you talk to your city or a lender, use the words “HUD-code manufactured home.” Saying “mobile home” can get you a reflexive no; saying “tiny home” can get you bounced to the RV rules. Precision here is free, and it protects you.

You’ve just seen how one wrong word can sink a project.

The free ADU Starter Kit includes a one-page terminology cheat-sheet (plus a quote checklist and a city-call script) so you walk into every conversation using the language that keeps your options open.

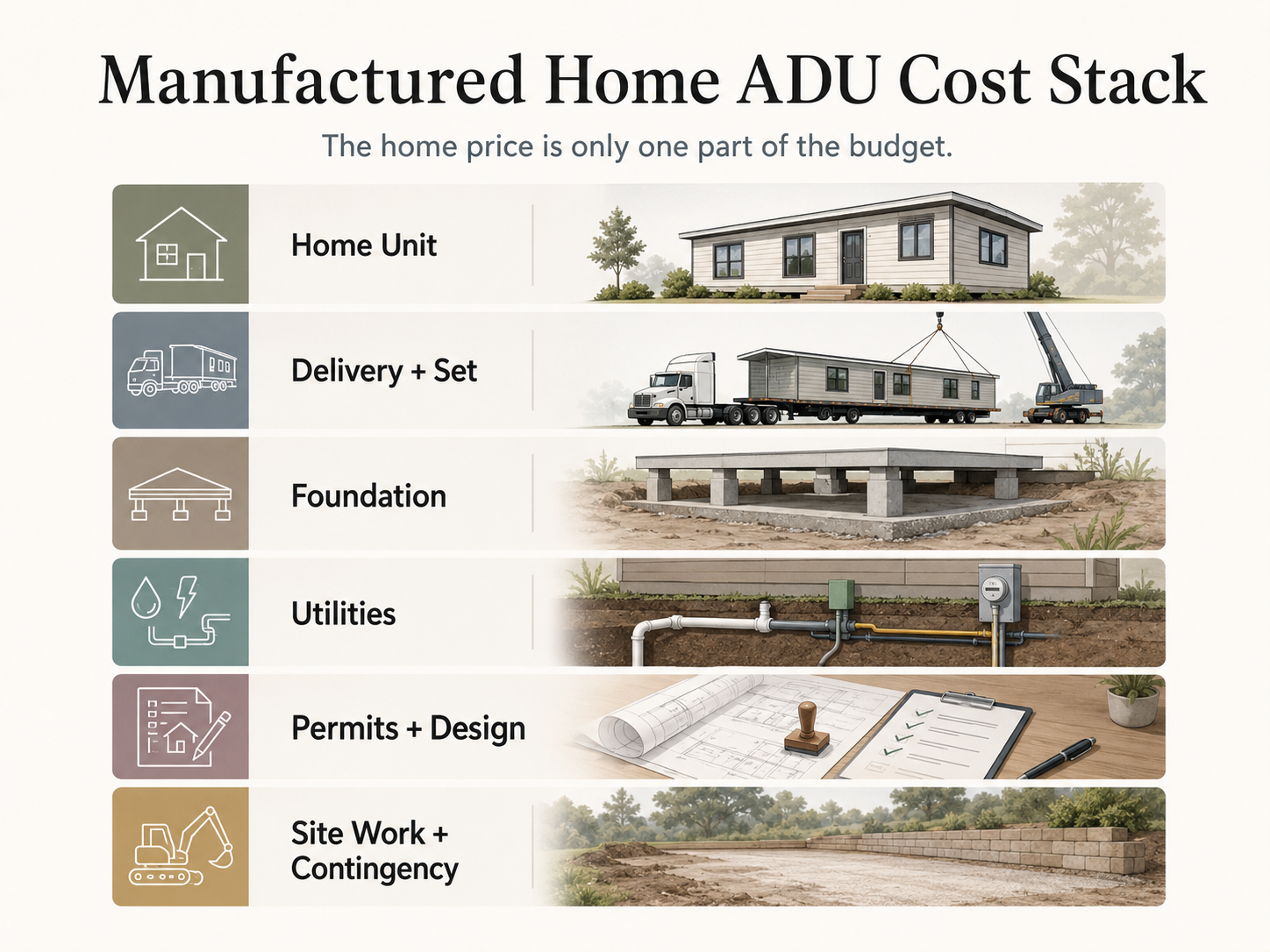

Download the Free ADU Starter KitHow much does a manufactured home ADU really cost (all-in, not the sticker)?

Don’t budget from the dealer’s unit price. U.S. Census / FRED data put the December 2025 average sales price of a new manufactured home at $88,200 for a single-section unit and $161,200 for a double-section unit — but those are national sales-price anchors, not an installed ADU budget. A complete project also requires delivery and set, a permanent foundation, utility connections, permits and design, inspections, site work, and contingency. The honest move is to treat the unit price as your starting number and get itemized local quotes for everything else.

The line we keep coming back to: the advertised home price answers “what does the box cost?” It does not answer “what does a legal dwelling in my backyard cost?”

The manufactured home ADU cost stack

| Cost line | What to verify | Notes & sources |

|---|---|---|

| Manufactured home unit | Size, HUD labels, finishes, appliances, warranty | National anchor: ~$88,200 single-section / ~$161,200 double-section (Census/FRED, Dec 2025). Your quote will differ. |

| Freight / delivery / set | Distance, escorts, crane, road width, overhead wires, staging area | Highly site-dependent — get a local bid. |

| Permanent foundation / anchoring | Engineered foundation, soil, slope, manufacturer specs, local code | Fannie Mae requires a permanent foundation appropriate for soil conditions and meeting local/state codes for a financeable manufactured ADU. |

| Utilities | Water, sewer/septic, electric, gas/propane, meter upgrades | Some cities don't require separate meters, but capacity upgrades may still be needed. Septic is a major hidden-cost risk. |

| Permits / plan review | Zoning clearance, manufactured-home installation permit, trade permits, impact fees | Portland and most jurisdictions require building and trade permits for ADU projects. |

| Site work | Grading, drainage, retaining walls, tree removal, fire access | Sloped lots and narrow access drive this up fast. Get itemized bids. |

| Design / engineering | Foundation plans, site plan, structural details, energy/fire | Can become a detailed plan set — foundation and 433A documentation become part of the permit package in CA. |

| Contingency | Utility surprises, permit revisions, soils issues | We suggest a 10–20% planning contingency (editorial guidance, not a quote). |

Where the savings can disappear

For broader context: across all ADU build types, 2026 cost guides put detached units around $150–$300 per square foot (Angi, 2026). In premium coastal-California markets the numbers run far higher — San Diego turnkey detached ADUs commonly land at $375–$600+ per square foot, or roughly $300,000–$450,000+ all-in (SnapADU, 2026). Those are San Diego examples, not national figures — but they make the key point: the site costs are similar regardless of build type.

The biggest budget-killers we see flagged repeatedly:

- Sloped lots — retaining walls and stepped foundations.

- Long utility runs — trenching far from existing connections is often billed separately.

- Narrow or no truck/crane access — if the unit must be hand-carried or specially craned in, labor climbs across every phase.

- Main-panel or sewer-capacity upgrades to the primary house.

- Material-price volatility — recheck current material and freight pricing before locking any bid.

Reality check before you sign anything: a manufactured home ADU can absolutely be the most affordable path — when your lot cooperates. Flat, accessible ground with utilities nearby and a city that allows it makes the savings real. A hillside, a long sewer run, and a strict design ordinance can shrink the gap between manufactured and modular to almost nothing. The only way to know your number is 2–3 itemized local quotes — get them before you rely on any all-in total.

You’ve now got the cost stack. The next question is how to pay for it — and that’s where manufactured homes get their own rules.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Compare the financing lanes before you assume cash or dealer financing is your only route.

No rates or approvals are guaranteed.

Explore ADU Financing Paths → See Mortgage and Refinance OptionsCan you finance or appraise a manufactured home ADU?

Financing is possible, but it’s more documentation-sensitive than most homeowners expect — and the rules are specific to manufactured housing. Lenders and appraisers generally need HUD label/data-plate documentation, real-property classification (the hitch, wheels, and axles removed and the unit affixed to a permanent foundation), and permanent utility connections before a manufactured home counts toward a financeable property. The structural nuance that trips people up: under standard conventional rules, a manufactured home can be the ADU — but the primary dwelling on the lot must be site-built or modular. Newer policy is starting to loosen that.

Why documentation matters more here than anywhere else

Fannie Mae’s ADU rules (B2-3-04) state that an ADU can include single- or multi-width HUD-code manufactured homes that are legally classified as real property — and that if an ADU is present, the primary dwelling must be site-built or a modular home. Fannie’s delivery guidance adds the operative appraisal rule in one sentence: to be valued in the appraisal, the manufactured ADU must be real property; if it’s still personal property, the appraiser excludes its value. Translation: an appraiser isn’t asking “does it look permanent?” — they’re asking “is it documented as permanent real property?” If your installer skips the foundation certification or you can’t produce the HUD Data Plate or Certification Label, the loan can be ineligible — even on a beautiful unit.

In California, that real-property conversion typically runs through HCD Form 433A (the document that records a manufactured home as affixed to a permanent foundation). Verified May 27, 2026.

Conventional ADU rules at a glance (Fannie & Freddie)

We present this as path education, not a lender ranking — and these are agency purchase rules, not an offer or approval. See our full Fannie Mae and Freddie Mac ADU rules comparison.

| Rule | Fannie Mae | Freddie Mac |

|---|---|---|

| Can the ADU be a manufactured home? | Yes — single- or multi-width HUD-code MH, if legally classified as real property (B2-3-04) | Yes — MH ADUs must meet Freddie's ADU and manufactured-home guide rules |

| Primary dwelling requirement (standard rules) | Must be site-built or modular when an ADU is present | ADU allowed on 1-, 2-, or 3-unit properties; one ADU only (Bulletin 2022-11) |

| Size minimum for the MH | Real-property classification + HUD labels required | The 12-ft-width / 400-sq-ft minimum is waived when the manufactured home is an ADU |

| Appraisal treatment | ADU must be real property to be given value | Specific ADU appraisal/comparable rules apply (Guide §5601) |

| Newer expansion | UAD 3.6 / SEL-2025-10 expands eligibility — including, for the first time, one ADU on a single-unit manufactured-home primary | Confirm current Freddie bulletins for MH-primary changes |

The financing lanes (not a lender ranking)

We present financing as paths, sorted by how they work — never ranked by anything else. None is a guarantee, and we quote no rates.

| Path | What it funds | Manufactured-ADU fit | Best for |

|---|---|---|---|

| Cash-out refinance | Pulls existing home equity into cash for the build | Strong when you have equity and the ADU will be real property | Owners with substantial equity willing to replace their primary mortgage |

| Renovation loan | Finances the project based on completed/after-improvement value | Workable; lender must accept the manufactured ADU in the appraisal | Owners with less current equity who want one loan for the build |

| Construction loan | Funds the build in draws, then converts | Possible; requires lender comfort with manufactured installation | Larger or phased projects |

| HELOC / home equity loan | Borrows against existing equity as a line or lump sum | Common for smaller all-in budgets | Owners financing site work or covering a gap |

| Manufactured-home chattel loan | Finances the home as personal property | Generally a poor fit for an ADU on land you own — you want it as real property, not chattel | Rarely appropriate for the ADU-on-owned-land case |

Policy is actively changing — verify at the loan

Financing rules for ADUs and manufactured housing are moving in homeowners’ favor. Fannie Mae’s announcement SEL-2025-10 expands ADU and manufactured-housing eligibility tied to the UAD 3.6 appraisal policy — including extending eligibility to a single-unit manufactured home as the primary dwelling with one ADU, and up to three ADUs on certain one-unit properties. Lender execution and overlays vary, so confirm specifics for your exact loan. Verified May 27, 2026; re-check monthly to quarterly.

Best used after you have a rough all-in budget and before you commit to a deposit.

Compare ADU Financing Paths → Explore Mortgage and Refinance OptionsWill it hurt your property value? The appraisal reality

Used as a primary residence, manufactured homes have historically appraised lower than site-built homes — but as an ADU on a conventional lot, the dynamic changes. A properly foundationed, permitted manufactured ADU that’s classified as real property is valued as an improvement to your existing property, and it can generate rental or family-housing income that supports the investment. The honest caveat: appraisal comparables for manufactured ADUs can still be thin in some markets, which is one more reason the real-property documentation matters.

Why the flip? When a manufactured home is your only home, the appraiser values the manufactured home itself, against other manufactured homes, in a market that has historically discounted them. When it’s an ADU behind a stick-built house, the appraiser is valuing your whole property — land plus primary home plus a permitted, income-capable accessory unit. The manufactured unit becomes an improvement, not the headline asset. See also: how ADUs are appraised.

Appraisal-friction checklist (what an appraiser actually looks for)

- HUD Data Plate and HUD Certification Label(s) present and photographed — without them, the loan can be ineligible.

- Real-property classification recorded (in CA, via Form 433A) — a personal-property unit gets excluded from value.

- Permanent foundation appropriate for soil and meeting local/state code.

- Primary-dwelling type confirmed (site-built or modular under standard conventional rules).

- Legal rental status — appraisers may weigh whether the unit can be legally rented, plus separate meters and a unique address.

- Comparable sales — ask your appraiser early whether nearby manufactured-ADU comps exist; scarcity can affect contributory value.

What permits, foundation, and utility hookups does a manufactured home ADU need?

Assume you need the full permitting stack: zoning approval, a building or manufactured-home installation permit, foundation/anchoring approval, trade permits, inspections, utility approval, and final approval — including a certificate of occupancy where your jurisdiction requires one — before anyone lives in or rents the unit. A signed dealer quote is not a city-approved ADU permit, and the order of operations matters: you confirm the path first, then buy the home.

Foundation and anchoring

The permanent foundation is the single most important physical decision, and in practice it does triple duty:

Many jurisdictions require a permanent foundation for a manufactured home used as a dwelling (Moreno Valley, for example, allows manufactured-home ADUs “on a permanent foundation only”). Note the federal definition technically contemplates a manufactured home “with or without a permanent foundation,” but as an ADU you’ll almost always need one to satisfy local approval, real-property status, and financing.

Affixing the home to a permanent foundation (with the hitch, axles, and wheels removed) converts it from “personal property” to taxable real property — in California, recorded via HCD Form 433A.

Conventional manufactured-housing rules require a permanent foundation, completed site prep, and permanent utility connections.

A unit left on its wheels is, to most planners and lenders, a trailer — and it will be rejected or treated as temporary.

Utilities

Plan to confirm, item by item:

- Water capacity and connection

- Sewer lateral or septic approval (septic is the most common hidden dealbreaker)

- Electrical service — possibly a panel upgrade on the main house

- Gas/propane if applicable

- Fire sprinklers where local code requires them

- Metering/billing — separate service may or may not be required

Certificate of occupancy

Where your jurisdiction issues one, this is the finish line, not a formality. Clark County, WA, for instance, requires ADUs to comply with building/fire/health/safety codes and prohibits occupancy until a certificate of occupancy is issued. No CO, no legal occupancy, no legal rental in those jurisdictions. Verified May 27, 2026. Some areas use different terminology for final residential sign-off — ask your building department which applies.

The permit reality box — ask the city this before buying the unit

Print this. Bring it to your building department or paste it into an email:

- 1"Does your code allow a HUD-code manufactured home as a detached ADU on this property?"

- 2"Which code section controls that answer?"

- 3"Is a permanent foundation required?"

- 4"Will this be reviewed as a manufactured-home installation, a modular building, or a standard detached ADU?"

- 5"Are pre-approved ADU plans available, and do they apply to manufactured homes?"

- 6"What utility-capacity documents do you require?"

- 7"Is a certificate of occupancy (or other final approval) required before family or rental use?"

- 8"Are there design, roof-pitch, siding, skirting, or minimum-width standards?"

- 9"Do HOA or private covenants affect city approval here?"

- 10"Can I submit the dealer's model/spec sheet for a preliminary review before I place a deposit?"

The most expensive mistake in this entire topic is buying a perfectly legal manufactured home that turns out to be illegal as an ADU on your lot. Questions 1 and 2 prevent it.

What documents should you get from the dealer before you pay a deposit?

Before any money changes hands, get written confirmation that the unit is a true HUD-code manufactured home and that the quote’s scope is clear. The single most useful pre-deposit step is matching the dealer’s paperwork to what your city and a future lender will demand — because a missing HUD label or a vague “installation included” line is where budgets and approvals break.

Ask the dealer for, in writing:

- Confirmation the unit is HUD-code manufactured — not modular, park model, RV, or tiny home on wheels (the word changes your entire permit and financing path).

- HUD Certification Label and HUD Data Plate details — these prove federal-standard construction and are required for most financing.

- Model and spec sheet — so your building department can do a preliminary review.

- Manufacturer's installation manual and foundation requirements — what foundation the home is engineered for.

- Wind and thermal zone rating — must match your region's requirements.

- Delivery and set scope — what's included (transport, escorts, crane, leveling, marriage-line close-up) and what isn't.

- Warranty terms and what voids them.

- An itemized included/excluded list for site work — foundation, utilities, skirting, stairs, permits. If it's not on paper, assume it's excluded.

Keep all of it. This packet is what turns a “box price” into a real, lender-ready project — and it’s the difference between a smooth approval and a stalled one.

Where are manufactured home ADUs clearly allowed — or at least addressed?

The safe approach is never “ADUs are allowed here, so I’m fine.” You want a source that specifically addresses manufactured homes, modular homes, mobile homes, or tiny homes on wheels by name. Because the terms are regulated so differently, a generic “ADUs allowed” statement tells you almost nothing about whether your HUD-code unit qualifies.

Below is our Manufactured Home ADU Reality Matrix. It combines federal regulations, state code, city ordinances, lender selling-guide rules, and government price data in one place — so you don’t have to open a dozen tabs to compare them. Treat it as a research starting point and verify your own jurisdiction in writing.

| Source / jurisdiction | What it establishes | Plain-English takeaway | Source · Verified |

|---|---|---|---|

| Federal — HUD Code, 24 CFR Part 3280 | Manufactured homes are a federally regulated dwelling type (design, construction, transport, fire, plumbing, heating, electrical). | A manufactured home is a specific HUD-code dwelling category — not "any movable small house." | eCFR · May 27, 2026 |

| California — Gov. Code §66313(a)(2) | The ADU definition expressly includes a manufactured home (per H&S Code §18007). | California is a statewide "yes," subject to local objective standards. | leginfo · May 27, 2026 |

| Moreno Valley, CA | ADU may be a manufactured home on a permanent foundation only; excludes wheels-based tiny homes. | Even in friendly CA, permanent foundation and fixed utilities are central. | moval.gov · May 27, 2026 |

| Citrus Heights, CA | Manufactured home OK as ADU if it meets H&S §18007; movable tiny homes not allowed; no STR under 31 days. | "Manufactured" can pass where "tiny home on wheels" fails. | citrusheights.net · May 27, 2026 |

| Portland, OR | An ADU may be proposed as a manufactured home; ADUs allowed on sites with a house or manufactured home. | Strong manufactured-ADU language — but size, lot, and zoning standards still apply. | portland.gov · May 27, 2026 |

| Clark County, WA | Manufactured or modular home may be an ADU if it meets county code; pre-6/15/1976 mobile homes not allowed; permits + CO required. | Some places explicitly allow manufactured ADUs while excluding older mobile homes. | clark.wa.gov · May 27, 2026 |

| Raleigh, NC | UDO §3.6.2 allows a manufactured-home ADU only with specific design standards and ≤600 sq. ft.; a city FAQ conflicts — code controls. | The ordinance beats the FAQ; make the city cite the controlling section. | Raleigh UDO §3.6.2 · May 27, 2026 |

| U.S. Census / FRED price anchors | Dec 2025 avg new sales price: $88,200 single-section / $161,200 double-section. | The unit price is a starting anchor, not the installed ADU budget. | FRED · May 27, 2026 |

| Fannie Mae Selling Guide (B2-3-04 + B2-3-02 / B5-2) | HUD-code MH allowed as an ADU if real property; primary dwelling must be site-built or modular (standard rules); HUD labels required. | Financing depends on documentation and real-property treatment, not appearance. | Fannie B2-3-04 · May 27, 2026 |

| Fannie Mae SEL-2025-10 / UAD 3.6 | Expands ADU/MH eligibility — including one ADU on a single-unit manufactured-home primary — for lenders using UAD 3.6. | Financing policy is loosening — but confirm execution per loan. | SEL-2025-10 · May 27, 2026 |

| Freddie Mac (ADU + MH guide rules) | One ADU allowed on 1-, 2-, or 3-unit properties; MH ADU must meet HUD-code/foundation rules; 12-ft/400-sq-ft minimum waived for ADUs. | A second agency path exists — with its own documentation rules. | Freddie ADU · May 27, 2026 |

Want this checked for your exact city instead of reading ordinances yourself?

See What You Can Build → Get Your Free ADU ReportWhen is a manufactured home ADU a good idea — and when is it the wrong path?

A manufactured home ADU is strongest when your city clearly allows it, your lot has easy access, utilities are straightforward, the foundation path is clear, and you value speed and cost control over deep customization. It’s the wrong path when your lot is tight or sloped, design standards are strict, sewer/septic is uncertain, an HOA demands custom exterior matching, or conventional financing and appraisal treatment are central to the deal. The decision usually comes down to your lot and your code, not the home itself.

Use this to place yourself — the right-hand column points to the path that removes the specific friction:

| Your situation | Manufactured home ADU fit | Why / better path if it's a poor fit |

|---|---|---|

| City explicitly allows manufactured homes as ADUs | Strong | Code risk is low — proceed to a feasibility check |

| City allows ADUs but is silent on manufactured homes | Uncertain | Code silence is the risk — get a written interpretation first |

| Tight urban lot, narrow access | Weak | Delivery/crane access fails — site-built or panelized ADU |

| HOA requires custom exterior matching | Weak | Design-match rules block it — modular/site-built with approved finishes |

| Septic capacity uncertain | Uncertain | Utility risk dominates — feasibility study before any build type |

| You need maximum resale/appraisal confidence | Uncertain | Comp scarcity is the risk — modular or site-built may be safer |

| You need family housing fast and code is clear | Potentially strong | Speed favors factory — compare manufactured vs. modular head-to-head |

| You want a tiny home on wheels | Usually weak | Usually not a legal ADU — only proceed where code expressly allows it |

Find your best-fit path before you commit to a build type.

Find your best ADU path before you commit.

Find Your Best ADU Path → Get Your Free ADU ReportIf a manufactured home is blocked on your lot, here’s your best alternative

If your jurisdiction allows only modular (not HUD-code manufactured) ADUs, you have not hit a dead end. A modular ADU is built in the same kind of factory, looks identical when finished, is constructed to your local building code, and faces far fewer manufactured-housing restrictions — so it qualifies in places a HUD-code unit won’t, while still delivering factory speed. It’s the single most reliable fallback when “manufactured” is a no.

The tradeoff is honest: modular generally costs more per unit than a comparable manufactured home, because it’s engineered to local code rather than the federal standard. But it sidesteps the exact zoning and lender friction that blocks manufactured homes in stricter cities — and because it’s treated like site-built housing for financing and appraisal (Fannie Mae B2-3-02), it often carries fewer surprises in total.

If manufactured is blocked, compare these four fallback paths

| Path | Built to | Local-approval friction | Financing/appraisal | Best-fit lot |

|---|---|---|---|---|

| Modular | State/local IRC | Low — treated like site-built | Same treatment as site-built | Most lots where manufactured is blocked |

| Panelized | Local code, assembled on site | Low–moderate | Site-built treatment | Tight access where modules can't crane in |

| Site-built | Local code | Standard ADU process | Strongest comps | Custom needs, strict design areas |

| Garage conversion | Local code (within footprint) | Often the lowest | Site-built treatment | Existing structure, smallest budget |

For homeowners exploring factory-built options nationally, Modular Home Direct is one broad national resource for comparing modular and prefab units. (Foldable, compact units like BOXABL’s Casita are a narrower niche worth knowing about if your priority is the smallest, fastest-to-deliver footprint.) Service areas and availability vary by provider and region, so confirm a provider serves your state before you rely on them. See also: compare prefab ADU companies.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Compare modular and prefab units that qualify in more jurisdictions. Check availability in your area.

How to compare manufactured home ADU quotes without getting trapped

A useful quote separates the home from the site. If a quote doesn’t clearly show what’s included and what’s excluded, you don’t have a project budget yet — you have a box price. The most common trap is a low headline number that quietly excludes foundation, utility trenching, septic upgrades, permits, and skirting, then climbs by tens of thousands once the real scope appears.

Take any quote and force it onto this grid before you compare two providers:

| Quote item | Dealer included? | GC included? | You’re responsible? | Watch for |

|---|---|---|---|---|

| Manufactured home unit | ☐ | ☐ | ☐ | Model, size, HUD labels, finishes |

| Delivery | ☐ | ☐ | ☐ | Distance, escorts, crane |

| Set / installation | ☐ | ☐ | ☐ | Blocking, leveling, marriage line |

| Permanent foundation | ☐ | ☐ | ☐ | Engineered plan, soil report |

| Skirting / stairs / porches | ☐ | ☐ | ☐ | Often excluded or quoted separately |

| Utility trenching | ☐ | ☐ | ☐ | Water, sewer, electric, gas |

| Septic / sewer upgrades | ☐ | ☐ | ☐ | Major hidden-cost risk |

| Permits & impact fees | ☐ | ☐ | ☐ | Building, trade, impact fees |

| Design / engineering | ☐ | ☐ | ☐ | Site plan, foundation, energy |

| Inspections / final approval | ☐ | ☐ | ☐ | Required before use |

| Contingency | ☐ | ☐ | ☐ | Budget protection (10–20%) |

If two quotes don’t fill the same boxes, they aren’t comparable — full stop.

Get the full checklist, the city-call script, and a cost-line worksheet in one place.

Built for manufactured-home ADU shoppers, before you talk to a dealer.

Download the Free ADU Starter KitWhat to send your city before you buy the home

Get written zoning and permit-path confirmation before you place a deposit. A manufactured home can be a perfectly legal dwelling and still fail as an ADU on a specific lot because of zoning, setbacks, foundation, utility, access, design, HOA, or lender requirements. A two-paragraph email now can save five figures later.

Copy, fill the brackets, and send:

Subject: Manufactured home as detached ADU — code confirmation request

Hello,

I own (or am evaluating) the property at [address / APN]. I’m considering a HUD-code manufactured home as a detached ADU. Before purchasing plans or placing a deposit, could you confirm:

- Whether a manufactured home is allowed as an ADU at this property.

- The code section or policy that controls that answer.

- Whether a permanent foundation is required.

- Any maximum size, height, setback, design, roof-pitch, siding, skirting, or utility requirements.

- Whether the project would be reviewed as a manufactured-home installation, a modular building, or a standard detached ADU.

- Which permits, inspections, and final-approval (certificate of occupancy) steps apply.

Thank you.

Keep the written reply. If you later get conflicting information, the email is your record.

What we verified for this guide

Last verified: . We built this page from primary and authoritative sources, not aggregators. Source categories:

- Federal manufactured-home standards — 24 CFR Part 3280 (HUD Code); HUD Office of Manufactured Housing Programs role in standards, installation, inspections, and certification labels.

- California state ADU law — Government Code §66313 (renumbered from §65852.2 via SB 477, effective March 25, 2024; amended by SB 543, effective January 1, 2026) and Health & Safety Code §18007.

- City/county code examples — Moreno Valley, Citrus Heights, Portland (OR), Clark County (WA), Raleigh (NC) UDO §3.6.2, Monterey County (CA).

- Price anchors — U.S. Census Manufactured Housing Survey via FRED (December 2025 averages).

- Financing/appraisal rules — Fannie Mae Selling Guide B2-3-04 and B2-3-02; announcement SEL-2025-10 / UAD 3.6; Freddie Mac ADU and manufactured-home guide rules.

- Cost context — 2026 ADU cost ranges from Angi ($150–$300/sf, all build types) and SnapADU (San Diego turnkey detached examples).

- Voice-of-customer research — homeowner forum and social posts were used only to understand searcher language and objections, never as proof for legal, cost, financing, or code claims.

Because installed totals depend on your lot (delivery, foundation, site work), we publish national anchors and city examples rather than a one-size national total — and we recommend 2–3 itemized local quotes before you rely on any all-in number.

Methodology

This guide was researched and written by the Dwelling Index Editorial Team. The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We prioritized primary sources (federal regulations, state statutes, municipal codes, lender selling guides, and government price data) over secondary summaries, and we cite a verification date for every factual claim about zoning, permits, costs, regulations, financing availability, or code sections.

We re-verify state statutes quarterly (monthly during legislative season), city rules quarterly, federal standards semiannually, financing rules monthly to quarterly, and price anchors monthly to quarterly. The “Last verified” date above reflects the most recent full review.

Manufactured home ADU FAQ

Can a manufactured home be an ADU in California?

Yes. California Government Code §66313 defines an accessory dwelling unit to include a manufactured home as defined in Health & Safety Code §18007. Local objective standards — permits, foundation, utilities, setbacks, and size limits — still apply, but the category cannot be banned outright. (Verified May 27, 2026.)

Does a manufactured home ADU need a permanent foundation?

In practice, almost always. A permanent foundation is commonly required by local code, is necessary for real-property (and tax) treatment, and is a financing prerequisite. Moreno Valley, for example, allows manufactured-home ADUs on a permanent foundation only, and conventional manufactured-housing rules require a permanent foundation and permanent utility connections. (Verified May 27, 2026.)

Is a manufactured home ADU cheaper than a site-built ADU?

The home itself usually is — a new manufactured home averaged about $88,200 (single-section) to $161,200 (double-section) in December 2025 per Census/FRED data. But the installed project may not be dramatically cheaper once foundation, delivery, utilities, permits, design, inspections, and site work are added, because those site costs are similar regardless of build type. Use unit prices as a starting anchor, not a total. (Verified May 27, 2026.)

Can I put a mobile home in my backyard and call it an ADU?

Usually not safely. Many jurisdictions allow HUD-code manufactured homes as ADUs but prohibit older mobile homes, RVs, park models, or tiny homes on wheels. Clark County, WA, for example, does not allow mobile homes built before June 15, 1976 as ADUs. Use the term "HUD-code manufactured home," and confirm your unit's classification. (Verified May 27, 2026.)

Can a tiny home on wheels be an ADU?

Usually not, unless local code expressly allows it. Moreno Valley excludes tiny homes on wheels that lack a permanent foundation and fixed utilities, and Citrus Heights states that movable tiny homes may not be used as ADUs. (Verified May 27, 2026.)

Can I rent out a manufactured home ADU?

Often yes for long-term rental, but rental rules are local and short-term rentals are frequently restricted. Citrus Heights, for instance, allows ADUs as rental property but prohibits short-term rentals under 31 days. Confirm both long-term and short-term rules with your city. (Verified May 27, 2026.)

Can Fannie Mae or Freddie Mac finance a property with a manufactured home ADU?

Possibly, with documentation. Fannie Mae allows a HUD-code manufactured home as an ADU when it's legally classified as real property, and under standard rules the primary dwelling must be site-built or modular; its UAD 3.6 / SEL-2025-10 update expands eligibility further. Freddie Mac allows one ADU on 1-, 2-, or 3-unit properties and waives the 12-ft-width/400-sq-ft minimum when the manufactured home is the ADU, subject to its guide rules. Lender execution and overlays vary. (Verified May 27, 2026.)

Should I buy the manufactured home before getting permit feedback?

No. Get written zoning and permit-path confirmation first. A manufactured home can be a fully legal dwelling and still fail as an ADU on a specific lot due to zoning, setbacks, foundation, utility, access, design, HOA, or lender requirements. The order is: confirm the path, then buy the home.

Not sure where to start?

See what’s possible at your address — get your free ADU report in about a minute.

See What You Can Build → Get Your Free ADU Report