RenoFi vs Construction Loan: Which Actually Funds Your ADU in 2026?

The answer up front

RenoFi isn’t a construction loan. RenoFi is a licensed mortgage broker (Renovation Finance LLC DBA RenoFi, NMLS #1802847) that arranges renovation-specific HELOCs, fixed-rate home equity loans, and cash-out refinances from partner credit unions. These loans are underwritten against after-renovation value (ARV) — what your home will be worth after the ADU is built — rather than current appraised value. A construction loan is short-term, milestone-draw financing released in stages as the build progresses. They are different instruments with different eligibility rules, draw mechanics, and cost structures. The wrong choice can cost tens of thousands of dollars.

Test RenoFi first if you own and occupy the home, your current first-mortgage rate is one you can’t afford to lose, your contractor doesn’t want to deal with lender draws, and public sources confirm RenoFi is available in your state (most U.S. states — public sources list Hawaii, New York, and Massachusetts as exceptions, and Texas is a separate verify-direct case because of state home-equity rules). Test a construction loan first if you’re building a new primary home with an ADU together, doing a teardown-and-rebuild, financing an investment property or LLC-held property, working with a contractor who prefers draw-based payment, or building more than roughly $500K worth.

See What You Can Build → Get Your Free ADU ReportEnter your address and ADU plan. Our Feasibility Engine returns your local zoning posture, a borrowing-power read, and which financing lanes fit your property and state. Free, no credit pull, under 60 seconds.

By the Dwelling Index Editorial Team · Published: May 21, 2026 · Last updated: May 21, 2026 · Last verified: May 21, 2026 · ~35 min read

Independent editorial comparison. We are not a lender, broker, builder, or municipal permitting authority. See our affiliate disclosure below.

What we verified for this comparison

Primary sources: RenoFi product pages, FAQ, qualification documents, and license/entity pages (renofi.com); Bankrate RenoFi review, updated February 27, 2026; Fannie Mae Selling Guide B5-3.1-02 (single-close CTP), Fannie Mae ADU originating page, SEL-2025-08/09/10; Freddie Mac ADU and CHOICERenovation pages; HUD Mortgagee Letter 2023-17; AmeriSave May 2026 construction loan guide with Q3 2025 FHFA rate data; California HCD ADU Handbook (March 2026); Trustpilot, BBB, and BiggerPockets public customer reviews. Rates and illustrative figures are editorial stress-tests based on stated assumptions, not offers or guarantees. Verify all terms directly with any lender before applying.

Quick decision strip — what to start with based on your biggest constraint

| If this is your real problem… | Start by testing… |

|---|---|

| Keep a low first mortgage rate | RenoFi-style ARV financing |

| Building a new primary home plus an ADU together | Construction-to-permanent loan |

| Current equity won’t cover the ADU but ARV will | RenoFi or Fannie HomeStyle / Freddie CHOICERenovation |

| Teardown-and-rebuild | Construction loan |

| Investment property or property held in an LLC | Construction or investor (DSCR) loan |

| Contractor wants lender-controlled draws | Construction loan |

| You’re not sure your lot even qualifies for an ADU | Property feasibility check before any loan |

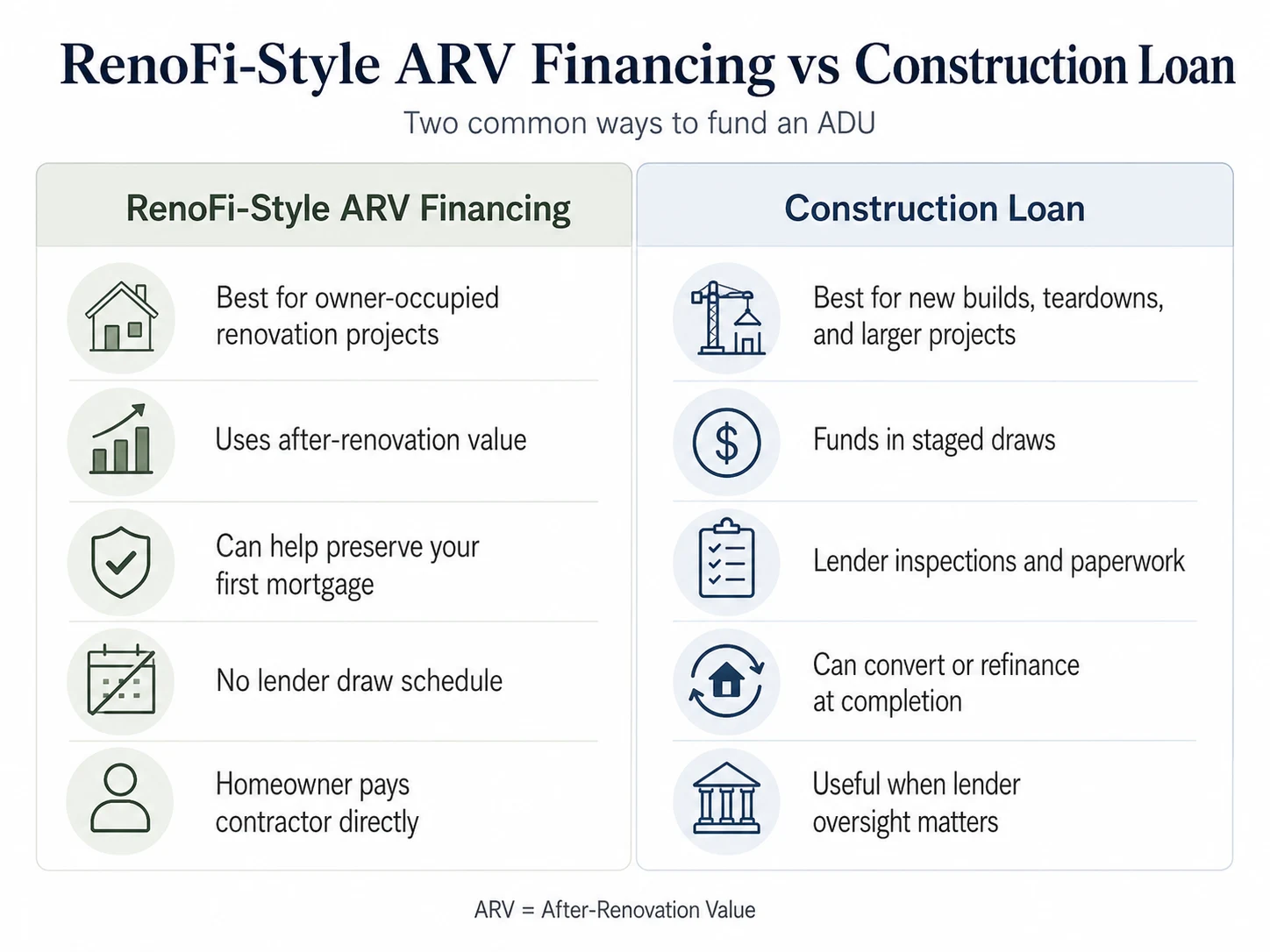

1. Is RenoFi actually a construction loan?

Answer capsule: No. RenoFi is a licensed mortgage broker — Renovation Finance LLC DBA RenoFi (NMLS #1802847), with additional state entities including Renovation Technologies LLC in Nebraska, RenoFi LLC in New Mexico, and Renovation Technologies Holdings Inc. in California (NMLS #2412747) — that connects homeowners with partner credit unions offering renovation-focused HELOCs, fixed-rate home equity loans, and cash-out refinances. These products are underwritten against after-renovation value. A construction loan is short-term first-position debt released in milestone-triggered draws.

The confusion makes sense. RenoFi markets directly against construction loans, ranks for “construction loan” queries, and uses future-value underwriting that sounds similar to a construction loan’s as-completed appraisal logic. They are different instruments. Here is every mechanical difference in one place:

| Mechanic | RenoFi Loan | Construction loan |

|---|---|---|

| Loan instrument | Second mortgage (home equity loan / HELOC) or cash-out refi | Short-term first-position construction note |

| Lender | A partner credit union; RenoFi is the broker | A bank, credit union, or mortgage lender directly |

| Underwriting value basis | After-Renovation Value (ARV) | As-completed appraised value |

| How funds reach the borrower | Full amount made available upfront; HELOC variants drawn as needed at borrower’s discretion | Disbursed in 4–6 lender-controlled draws tied to construction milestones |

| Inspection per draw | None | Yes; per AmeriSave’s May 2026 guide, $300–$600 per inspection, 4 to 6 inspections during the build |

| Refinances your first mortgage? | No, except the RenoFi cash-out refi option | Stand-alone: no. Construction-to-permanent: yes |

| Conversion to permanent mortgage | Not applicable (the loan is already permanent) | Single-close CTP converts automatically; stand-alone requires a separate refinance |

| Loan term | 10/15/20 years typical for home equity loan; HELOC has draw + repayment periods | 12–18 months build phase, then permanent mortgage |

| Borrower interest payment during build | Standard amortization or HELOC interest on drawn balance | Interest-only on funds drawn so far |

| Contractor controls | None imposed by lender | Builder approval, lien waivers, retainage, draw paperwork |

Sources: RenoFi product structure and entity disclosures (renofi.com/notices/licenses/, renofi.com/faq/). Construction loan mechanics, inspection counts, and fees — AmeriSave 2026 construction loan guide. Construction-to-permanent rules — Fannie Mae Selling Guide B5-3.1-02.

2. What a construction loan actually is (and how draws work in 2026)

Answer capsule: A construction loan is short-term financing — typically 12 to 18 months — that funds an ADU build through staged disbursements called draws, released as your contractor completes verified milestones. You pay interest only on funds drawn during the build. At completion the loan either converts to a permanent mortgage (construction-to-permanent) or is paid off by a separately arranged mortgage.

Two flavors, same starting point

There are two production paths, and the difference matters more than most homeowners realize.

Single-close construction-to-permanent (CTP). One closing covers both the build phase and the permanent mortgage that takes over when the ADU is done. Fannie Mae’s Selling Guide explicitly allows this for borrowers building a new 1-unit property with an ADU — the same loan can finance both the home and the ADU. The construction period under Fannie’s rules cannot exceed 18 months total, and no single period can exceed 12 months — Fannie also states that “exceptions to the 12-month and 18-month periods will not be granted.” If your build slips, you’re forced into a two-close structure.

Stand-alone (two-close) construction loan. The build is financed by a temporary loan, and the permanent mortgage closes separately at completion. You pay closing costs twice. The advantage is flexibility — you can shop the takeout mortgage when construction ends. The disadvantage is timing risk: if rates rise during construction or you no longer qualify at takeout, you can be stranded with a completed ADU and no refinance lined up.

How draws actually work, step by step

The construction loan draw schedule isn’t optional paperwork — it’s the operating system of the loan. Here’s a typical 2026 sequence on an ADU build, drawn from AmeriSave’s current guide:

- Draw 1 — Land purchase and site preparation (10–15% of loan). Clearing, leveling, utility lateral work to the property line.

- Draw 2 — Foundation (15–20%). Released after foundation pour and inspection.

- Draw 3 — Framing and roof (20–25%). Released after rough-framing inspection.

- Draw 4 — Mechanicals (15–20%). Plumbing, electrical, HVAC rough-in.

- Draw 5 — Interior finishes (15–20%). Drywall, flooring, cabinets, countertops, trim.

- Draw 6 — Final completion (10–15%). Appliances, paint, landscaping, punch list.

Per AmeriSave’s May 2026 guide, inspection fees are $300 to $600 per inspection, with 4 to 6 inspections during the build — roughly $1,800 to $3,600 in inspection costs alone. Lenders also typically hold back retainage — a percentage of each disbursement, commonly 5% to 10%, kept until project completion or certificate of occupancy. On a $70,000 framing draw with 10% retainage, the contractor receives $63,000; the remaining $7,000 is held back. That retainage is real cash the contractor doesn’t see until the end.

What gets confused

The phrase “construction loan” gets applied loosely in ADU marketing. Three different products often get lumped together:

- A true construction loan — short-term, draw-based, designed for ground-up building.

- A renovation mortgage like Fannie Mae HomeStyle Renovation or Freddie Mac CHOICERenovation — a first-lien mortgage that bundles purchase or refinance with renovation funds, underwritten against future appraised value. Freddie Mac’s CHOICERenovation page states the product can finance “the renovation of an old barn, garage or shed into an ADU” and can also add a factory-built ADU. Fannie Mae says HomeStyle Renovation can finance the construction or installation of a new ADU on a 1-unit property.

- An FHA 203(k) rehab loan — government-insured renovation mortgage, useful for older homes needing structural work alongside an ADU conversion.

Sources: Fannie Mae Selling Guide B5-3.1-02; Fannie Mae ADU originating page; Freddie Mac ADU page; AmeriSave 2026 construction loan guide.

3. The verdict — RenoFi vs construction loan decision matrix across 9 attributes

Answer capsule: Scored across nine attributes that actually drive the ADU financing decision, neither product wins outright. Each wins clearly within a specific buyer profile.

Per-cell sources are noted below the table. Rate ranges are illustrative industry context from secondary sources, not offers or guarantees.

| Attribute | RenoFi Loan | Stand-alone construction loan | Construction-to-permanent (single close) |

|---|---|---|---|

| 1. Available in your state | Most U.S. states; public sources list HI, NY, MA as exceptions; TX is a check-direct case | Nationwide via banks and credit unions | Nationwide via banks and credit unions |

| 2. Preserves your first mortgage rate | ✅ Yes (unless you choose the RenoFi cash-out refi) | ✅ Yes — separate first lien from your existing mortgage | ❌ No — replaces or refinances your first mortgage |

| 3. How funds reach the borrower | ✅ Full amount made available upfront; HELOC variants drawn as needed | ❌ Lender-controlled milestone draws (4–6) with per-draw inspections | ❌ Lender-controlled draws during build, then converts |

| 4. Maximum loan size, typical | RenoFi’s FAQ says most lenders allow up to $500K; broader product copy describes $25K–$750K. Use $500K as the practical planning breakpoint. | Typically 70–80% of future appraised value, no fixed dollar cap | Same as stand-alone |

| 5. Rate environment, May 2026 | Variable HELOC tied to prime + lender margin; fixed home equity rates set by partner CU | ~7.5–9%+ during build (AmeriSave 2026: ~1–2 pts over conventional) | Rate typically locked at closing near conventional 30-year; construction-phase note converts to that permanent rate |

| 6. Closing costs | One set; ~1–3% of loan plus appraisal covering current and after-renovation value | Build-phase closing costs; second closing for the permanent refi | Single set of closing costs |

| 7. Contractor friendliness | ✅ High — no lender-controlled draws or inspections during build | ❌ Low — many GCs decline; draws, retainage, lien waivers required | ❌ Low — same as stand-alone during build phase |

| 8. Qualification difficulty | Moderate; minimum credit ~620–640 with partner CU; over $250K is stricter | Stricter; typically 680+ credit, 20%+ down | Same as stand-alone; Fannie Mae removed the minimum credit score for DU-underwritten loans in November 2025 (SEL-2025-09) |

| 9. Customer-service risk | Broker model means timing depends on partner CU; mixed independent reviews (see Section 12) | Direct lender relationship; risk concentrated in builder coordination and draw timing | Direct lender relationship |

- RenoFi wins on funding flexibility, first-mortgage preservation, and contractor friction. If those three things matter most, RenoFi-style ARV financing is usually the first path to test.

- The construction loan wins on maximum loan size, nationwide availability, and lender-controlled disbursement. If your build is over $500K, you live in a state where public sources don’t confirm RenoFi availability, or your project genuinely needs lender oversight, construction is your lane.

- Construction-to-permanent wins when you’re building a new home with an ADU together — Fannie Mae says so explicitly.

Free 60-second feasibility report.

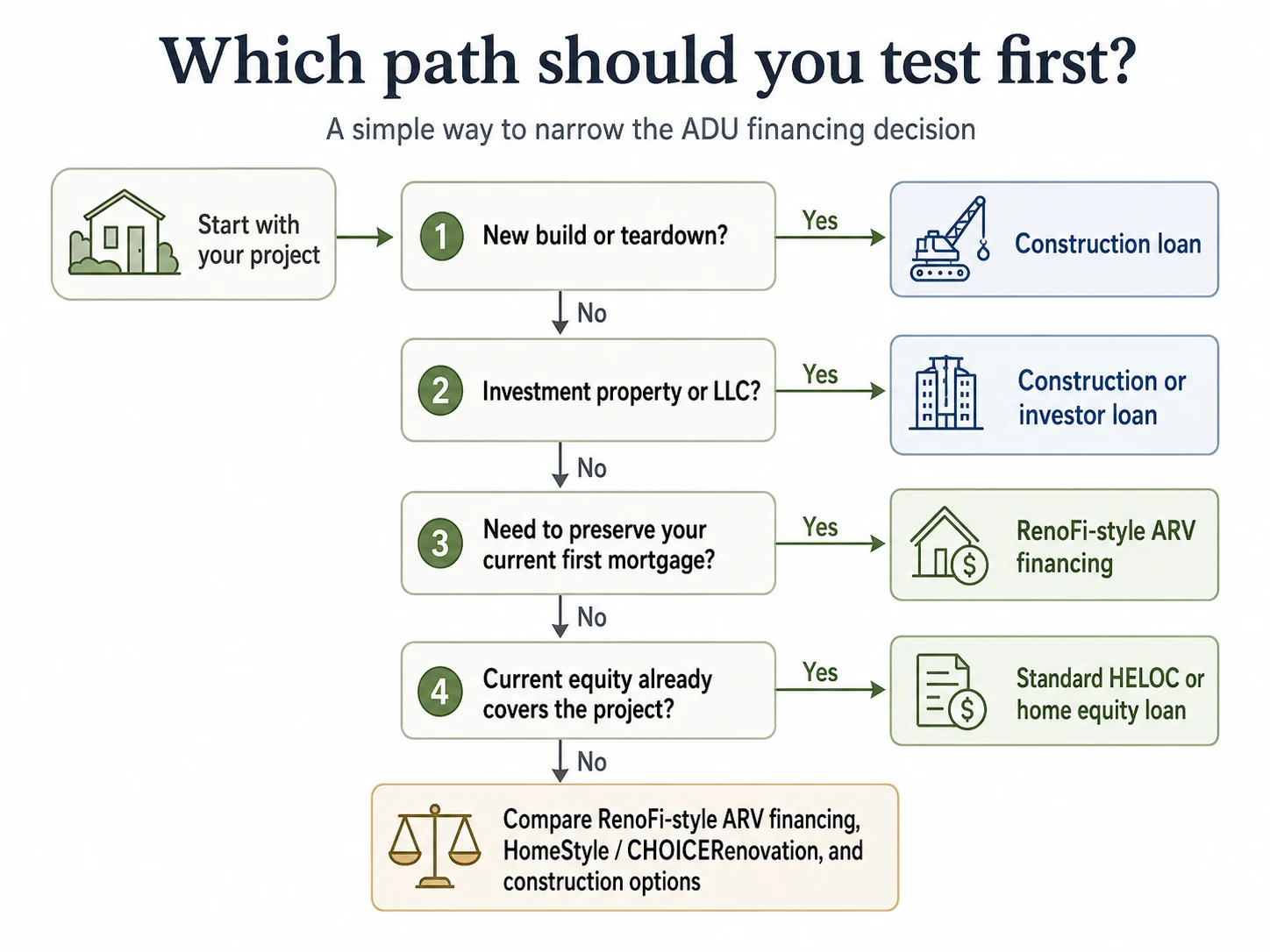

4. Which one fits your ADU? The 7-question routing

Answer capsule: Most homeowners can resolve the RenoFi vs construction loan decision in under three minutes by walking through seven yes/no questions about state, project type, ownership, equity, mortgage rate, contractor preference, and project size.

Question 1: Do you live in Hawaii, New York, or Massachusetts?

If yes, public sources list these states as RenoFi exceptions, and RenoFi’s own website footer cites a New York DFS restriction on mortgage solicitation. Your test order: construction-to-permanent, then HomeStyle Renovation, then a standard HELOC if equity allows.

Question 2: Are you doing a ground-up build of a new primary home with an ADU together?

If yes, construction-to-permanent is your first test. Fannie Mae’s ADU originating/underwriting page states plainly: borrowers building a new 1-unit property with an ADU can use a Construction-to-Permanent loan to finance both the home and the ADU. RenoFi explicitly excludes ground-up scratch builds from its product. Don’t waste a RenoFi application on this scenario.

Question 3: Are you tearing down and rebuilding?

If yes, construction or CTP is your only path. RenoFi’s qualification page lists scratch builds and knockdown rebuilds among projects that don’t fit. The ARV/renovation logic breaks when there’s nothing left to renovate.

Question 4: Is the property held in an LLC, or is it titled as an investment property?

If yes, RenoFi is out and you’re on an investor track. RenoFi states that ARV-based RenoFi Loans do not currently allow renovations on investment property or property titled in an LLC. Your test order: stand-alone construction loan from a community bank, DSCR investor loan, or a private/portfolio construction lender. Our hard money loan for ADU guide breaks down the alternatives.

Question 5: Is your current first mortgage rate something you actually want to keep?

If your existing rate is 5% or lower — and many U.S. homeowners locked 3%–4% between 2020 and 2022 — replacing it would cost real money over the next 25 to 30 years. RenoFi or a stand-alone construction loan preserves your first lien. A single-close CTP replaces it. Quick gut-check: on a $400,000 first-mortgage balance, the difference between a 3.5% locked rate and a 7% replacement rate is roughly $810 a month in payment difference, or about $290,000 over the life of a 30-year loan.

Question 6: Will your contractor work with a construction loan?

This is the question almost nobody asks before applying. Ask your contractor directly: “Have you worked with construction loans before? Are you willing to handle the draw inspections, lien waivers, and retainage?” If the answer is “I prefer not to,” that’s not a red flag against the contractor — it’s a routing signal toward RenoFi. RenoFi’s whole structural advantage is that the homeowner gets the funds and pays the contractor on a private schedule the two of them agree to.

Question 7: How big is your build?

- Under $150K all-in (small garage conversion, basement ADU, JADU): A standard HELOC, home equity loan, or cash-out refinance often funds this without ARV gymnastics. Don’t reach for RenoFi or a construction loan if you don’t have to.

- $150K to $500K (most detached and attached ADUs): RenoFi’s sweet spot and also workable on a construction loan. Use Questions 1–6 to break the tie.

- Above $500K (premium builds, full lot redevelopment, ADU as part of a primary-home rebuild): RenoFi’s typical $500K cap starts to bite. A construction loan or CTP has no equivalent ceiling. Construction wins this bracket on size alone.

- Answered “yes” to Q2 or Q3 → CTP / construction loan.

- Answered “yes” to Q4 → investor construction or DSCR loan, not RenoFi.

- Live in HI/NY/MA → construction or HomeStyle Renovation, not RenoFi.

- Build is over $500K → construction or CTP.

- First mortgage rate is precious and contractor doesn’t want draws → RenoFi-style ARV financing.

- Somewhere in the middle → run the worked scenarios below.

Financing decision tree, the 14-question lender vetting script, and the permit checklist. Free.

5. How much each will actually fund — four worked ADU scenarios

Answer capsule: The borrowing math is where the abstract becomes concrete. Below are four realistic ADU scenarios at $150K, $250K, $350K, and $450K total build cost, showing what each financing path would actually deliver under typical 2026 lender rules. Numbers are illustrative based on stated assumptions, not loan offers.

Scenario 1: $150K garage conversion

Build cost: $150,000 • Estimated ARV: $600,000 + ($150,000 × 0.70) = $705,000

| Product | Borrowing room calculation | Estimated max loan |

|---|---|---|

| Standard HELOC | 85% × $600K = $510K; minus $400K existing = | ~$110,000 |

| RenoFi-style ARV loan | lesser of: (a) 125% × $600K − $400K = $350K; (b) 90% × $705K − $400K = $234.5K | ~$234,000 |

| Construction loan | 75% × $705K = $529K possible; project cost is binding constraint | ~$150,000 (project-capped) |

Read: For a $150K garage conversion, both ARV-based products easily cover. A standard HELOC falls short by about $40K. RenoFi is comfortable. A construction loan works but brings draw friction you don’t need for a build this size. Winner: RenoFi for the cleanest funding, or a standard HELOC if you can stretch the gap with cash. A construction loan is overkill.

Scenario 2: $250K modest detached ADU

Build cost: $250,000 • Estimated ARV: $600,000 + ($250,000 × 0.70) = $775,000

| Product | Borrowing room calculation | Estimated max loan |

|---|---|---|

| Standard HELOC | $510K cap minus $400K existing | ~$110,000 — won’t cover the project |

| RenoFi-style ARV loan | lesser of: (a) $350K from 125% current-value; (b) 90% × $775K − $400K = $297.5K | ~$297,000 |

| Construction loan | 75% × $775K = $581K possible; project-capped | ~$250,000 |

Read: The standard HELOC has broken — current equity simply can’t fund this build. RenoFi handles it cleanly. A construction loan handles it but introduces draws. Winner: RenoFi for owner-occupied builds with a low first mortgage. Construction loan if the contractor demands draws or you live somewhere RenoFi doesn’t serve.

Scenario 3: $350K larger detached ADU

Build cost: $350,000 • Estimated ARV: $600,000 + ($350,000 × 0.70) = $845,000

| Product | Borrowing room calculation | Estimated max loan |

|---|---|---|

| Standard HELOC | Won’t cover | ~$110,000 |

| RenoFi-style ARV loan | lesser of: (a) $350K from current-value cap; (b) 90% × $845K − $400K = $360.5K | ~$350,000 (current-value cap is binding) |

| Construction loan | 75% × $845K = $634K possible; project-capped | ~$350,000 |

Read: At $350K, RenoFi’s 125% current-value cap starts to bite. The ARV math still works on its own, but the lower of the two limits is the controlling number. The borrower is right at the edge of comfortable RenoFi capacity. Winner: Either works. Decide on contractor preference, state availability, and total cost of money.

Scenario 4: $450K premium build

Build cost: $450,000 • Estimated ARV: $600,000 + ($450,000 × 0.70) = $915,000

| Product | Borrowing room calculation | Estimated max loan |

|---|---|---|

| Standard HELOC | Won’t cover | ~$110,000 |

| RenoFi-style ARV loan | lesser of: (a) $350K from current-value cap; (b) 90% × $915K − $400K = $423.5K | ~$350,000 (current-value cap binds; also subject to typical $500K policy ceiling) — $100K short |

| Construction loan | 75% × $915K = $686K possible; project-capped | ~$450,000 |

Read: This is where the construction loan pulls clearly ahead. RenoFi’s current-value cap of 125% leaves the borrower $100K short of the build. The construction loan handles the full $450K without breaking a sweat. Winner: Construction loan, almost regardless of contractor preference.

Total cost of money — illustrative

| Product | Illustrative rate range (May 2026) | Approx. monthly P&I on $250K | Approx. total interest over loan life |

|---|---|---|---|

| RenoFi-style fixed home equity loan, 20-year | 8.0–9.5% | $2,090–$2,330 | $251K–$309K |

| Stand-alone construction loan during build (interest-only) | 7.5–9.0% | ~$1,560–$1,875 IO on full $250K drawn | Build-phase interest of $10K–$20K typical; then permanent loan |

| Construction-to-permanent, 30-year at conversion | 6.5–7.5% conventional + ~0.5 pts construction | $1,580–$1,750 | $319K–$380K total over 30 years |

These are illustrative examples, not guarantees of returns or available rates. Actual loan terms depend on lender, state, credit profile, property, and project specifics.

6. Which one preserves your low first mortgage?

Answer capsule: RenoFi-style ARV financing is structured as a second-lien home equity loan or HELOC (or, optionally, as a cash-out refinance that would replace the first mortgage). The two non-refi RenoFi options keep your existing first-mortgage rate untouched. Stand-alone construction loans also leave the first mortgage in place. Single-close construction-to-permanent loans replace your first mortgage with new permanent financing at the rate available at closing.

Between roughly 2020 and 2022, the median 30-year fixed mortgage rate dipped below 3.0% several times. Borrowers who locked then hold rates so far below current market that giving them up isn’t financially rational, even if a refinance would simplify their finances.

If you locked a 3.0% to 4.0% first mortgage, refinancing into a 7.0% construction-to-permanent loan to fund an ADU is often equivalent to paying $1,500 to $3,000 a month forever for the privilege of one clean loan. That math rarely pencils.

| Path | Preserves first mortgage? |

|---|---|

| RenoFi home equity loan or HELOC | ✅ Yes — second lien behind your existing first |

| RenoFi cash-out refinance option | ❌ No — replaces your first mortgage |

| Stand-alone construction loan | ✅ Yes — temporary lien on new construction, paid off by permanent loan at completion |

| Single-close construction-to-permanent | ❌ No — by design, becomes the new permanent first mortgage |

7. Does RenoFi work for detached ADUs, garage conversions, and additions?

Answer capsule: RenoFi-style ARV financing fits most owner-occupied ADU additions and conversions — detached ADUs, attached ADUs, garage conversions, basement ADUs, and similar internal conversions — but does not fit ground-up scratch builds, teardown-and-rebuild projects, or properties titled to an LLC or held as investment property.

| ADU type | Define | RenoFi-style ARV fit | Construction loan fit | First path to test |

|---|---|---|---|---|

| Detached ADU (DADU) | Detached cottage, 400–1,200 sq ft | Strong if owner-occupied | Strong for builds >$300K or LLC ownership | RenoFi or HomeStyle if owner-occupied |

| Attached ADU | Addition sharing a wall | Strong | Workable | RenoFi or HomeStyle |

| Garage conversion | Existing garage to dwelling | Often the cleanest fit | Workable but draws are overkill | RenoFi or CHOICERenovation |

| Basement ADU | Finished basement with kitchen + bath + separate entry | Strong | Often overkill | RenoFi or standard HELOC |

| JADU (Junior ADU) | Per CA HCD: ≤500 sq ft of interior livable space within a single-family residence | Strong | Overkill | RenoFi or HELOC |

| Prefab or modular ADU | Factory-built unit, installed on site | Workable but timing requires lender coordination | Often required by builder | Check builder-preferred financing first; CHOICERenovation supports factory-built ADUs |

| New home + ADU together | Ground-up primary + ADU | ❌ Not eligible | Strong | Construction-to-permanent (Fannie Mae explicit) |

| Teardown + rebuild | Existing home demolished | ❌ Not eligible | Strong | Construction or CTP |

Sources: RenoFi qualification page; Freddie Mac ADU page; Fannie Mae ADU originating page; California HCD ADU Handbook, March 2026.

8. What can disqualify you from RenoFi?

Answer capsule: The top blockers are: FICO score under approximately 640 with most partner lenders, DTI well above 45%, investment-property or LLC ownership, ground-up scratch builds and teardowns, projects under $20K–$25K (practical minimum range from RenoFi’s own materials), after-renovation value too low to support the loan, and state availability (public sources list HI, NY, and MA as exceptions; TX should be verified directly).

| Blocker | What it means | Backup path to test |

|---|---|---|

| FICO under ~640 | Most RenoFi partner lenders require at least 640; some accept lower on smaller loans | FHA 203(k), construction loan from a local CU, work to raise FICO |

| DTI well above 45% | New loan payment would push debt-to-income too high | Reduce other debt, add income documentation, consider programs that allow ADU rental income to qualify |

| Investment property | Not held as primary residence | DSCR investor loan, portfolio construction loan, hard money |

| LLC ownership | Property titled to a limited liability company | Investor construction lender; consider moving title only if your CPA approves |

| Ground-up scratch build | No existing structure to renovate | Construction-to-permanent |

| Teardown-and-rebuild | Demolition followed by new construction | CTP or two-close construction loan |

| Project too small | Under $20K won’t qualify per RenoFi’s disqualifier page; ARV loans start at $25K | Standard HELOC, personal loan, or pay cash |

| ARV too low to support the loan | After-renovation appraisal doesn’t justify the borrowing | Smaller ADU scope, find better comps, wait for market improvement |

| State unavailable (HI, NY, MA — public sources) | RenoFi can’t underwrite in your state | HomeStyle Renovation, CHOICERenovation, local construction loan |

| High existing CLTV | Your current loans already encumber most of the home’s value | Pay down existing debt before reapplying |

The most painful disqualifier is the one borrowers learn about after paying for the appraisal. Per RenoFi’s product disclosures, the appraisal covers both current value and after-renovation value, and that cost can be paid even if the loan is not ultimately approved. Verify your eligibility profile before you order the appraisal.

Disqualifiers that exist for construction loans too

- Credit under 680 — most construction lenders draw a harder line here.

- Down payment under 20% — typical floor; some programs go lower with PMI, but not many for ADUs.

- Builder not approved by the lender — many construction lenders require their own builder vetting, which can disqualify a contractor you’ve already signed with.

- DTI above lender’s cutoff — usually 43–45%.

- Build timeline beyond 18 months — Fannie Mae’s single-close CTP rule cannot extend the construction period beyond 18 months total. No exceptions.

- As-completed appraisal that doesn’t support the project cost — same risk as RenoFi’s ARV-low scenario.

Affiliate disclosure: Mortgage Research Center is an active research partner. We may earn a commission if you request information through this link, at no cost to you.

If RenoFi isn’t your fit, explore construction loan and cash-out refinance options → Compare Construction Loan & Refinance Options with Mortgage Research Center9. When is a construction loan better than RenoFi?

Answer capsule: A construction loan is the better first test when you’re building a new primary home together with an ADU, doing a teardown-and-rebuild, using investment-property or LLC ownership, need lender-controlled disbursement, want one financing package that covers build and permanent mortgage, or have a build above approximately $500,000.

The five clear-cut “construction loan first” cases

- New construction of a primary home with an ADU together. Fannie Mae Selling Guide and the agency’s ADU originating/underwriting page explicitly support CTP for this scenario. RenoFi explicitly doesn’t.

- Teardown-and-rebuild. ARV/renovation logic breaks when the existing structure is being demolished. Construction or CTP is the only path.

- Investment property or LLC-held title. RenoFi’s ARV product line does not allow these. A construction loan from a portfolio lender, a DSCR investor loan, or a private/hard money construction lender is the path.

- Builds above $500K. RenoFi’s typical product breakpoint means very large ADUs (or ADUs in high-cost markets like coastal California) can run into the cap. Construction loans have no equivalent fixed cap.

- Contractor or builder requires construction-loan structure. Some larger ADU builders — especially those building prefab or modular units on a known schedule — only accept payment via a construction lender’s draw process. Ask early; this is binary information.

The “either could work” cases

For owner-occupied detached ADU builds in the $200K to $400K range where the contractor is comfortable with either funding model and you live in a RenoFi-eligible state, the choice often comes down to:

- Total cost of money over the loan’s life. RenoFi fixed home equity products amortize faster (10–20 years) with higher monthly payments and lower total interest. CTP amortizes over 30 years with lower monthly payments and higher total interest.

- First-mortgage rate sensitivity. If your current first mortgage is below 5%, RenoFi (or stand-alone construction) preserves it. CTP replaces it.

- Patience for draws. RenoFi funds upfront; construction loans require milestone draws and inspections. Some homeowners choose RenoFi specifically because they don’t want a lender inspector showing up at the site mid-build. Others choose construction loans specifically because they want that level of oversight on their builder. Neither preference is wrong.

10. The honest downsides nobody else publishes

Answer capsule: Both products carry verified downsides that the marketing pages omit. RenoFi’s documented downsides include broker-model timing variability, mixed customer-service reviews on Bankrate (4.6/5 product, 3.7/5 customer) and Trustpilot, variable-rate HELOC exposure to prime, the practical ~$500K typical loan breakpoint, and three-state public-source unavailability (HI, NY, MA). Construction loan downsides include $300–$600 per-inspection draw fees across 4–6 inspections, retainage of 5–10% held back from each disbursement, contractor coordination requirements, build-phase rates running 1–2 points over conventional, and the 18-month Fannie Mae single-close CTP construction-period limit with no exceptions.

RenoFi: what the product page won’t tell you

- Not available in Hawaii, New York, or Massachusetts per Bankrate’s RenoFi review (last updated February 27, 2026). RenoFi’s own website footer additionally confirms that no mortgage solicitation activity can occur in New York via their site, citing NY Department of Financial Services restrictions.

- Broker model, not direct lender. RenoFi states clearly: “RenoFi is not the actual lender” — they connect homeowners with partner credit unions. This means your timeline, communication, and underwriting standards depend on the specific credit union you’re matched with.

- Sample-payment disclosures show variable rates. RenoFi’s own footnote sample (as published) used 8.5% on a variable-rate HELOC with a 10-year draw and 15-year repayment period, requiring at least a 740 credit score. Your actual rate may be higher or lower; the variable rate moves with prime.

- Public reviews are mixed. Bankrate’s review gives RenoFi a 4.6/5 product score with a 3.7/5 customer score. Trustpilot reviews include both strong positives and clear negatives (see Section 12).

- $500K is the practical breakpoint, not a universal cap. RenoFi’s FAQ states most lenders allow RenoFi Loans up to $500K with stricter qualification criteria above $250K; broader product copy describes ARV loan amounts ranging from $25K to $750K. Use $500K as your planning ceiling unless your matched lender confirms more.

- You can pay for the appraisal and still not get approved. RenoFi’s disclosures note that lenders may charge for appraisal even when the loan isn’t approved.

Construction loans: what the lender’s pamphlet downplays

- Draw friction is real. Per AmeriSave’s May 2026 construction loan guide, inspection fees are $300 to $600 per inspection, with 4 to 6 inspections during the build — roughly $1,800 to $3,600 in inspection costs alone, plus the contractor’s time documenting each draw.

- Retainage tightens contractor cash flow. Lenders typically hold back 5–10% of each draw until certificate of occupancy. A 10% retainage on a $70K draw means the contractor receives $63K and waits for the remaining $7K until completion. Some contractors price this risk into their bid.

- Construction-to-permanent has a hard 18-month limit. Fannie Mae’s Selling Guide B5-3.1-02 states that single-close CTP construction periods may not exceed 18 months total, with no single period exceeding 12 months. “Exceptions to the 12-month and 18-month periods will not be granted.” If your build slips, you’re forced into a two-close structure.

- Builds run 1–2 points over conventional. Industry rate context from AmeriSave’s 2026 guide cites a Q3 2025 spread of 6.89% (30-year fixed) versus 8.34% (construction loan) — a 1.45 percentage point difference during the build phase.

- Single-close CTP replaces your first mortgage. If you have a sub-5% locked rate, that’s a real cost. The math has to support giving it up.

11. Is RenoFi available in my state?

Answer capsule: Per Bankrate’s RenoFi review updated February 27, 2026, public sources list RenoFi as available in most U.S. states and Washington, D.C., with exceptions in Hawaii, New York, and Massachusetts. RenoFi’s own website footer additionally notes a New York DFS restriction on mortgage solicitation activity. State availability can change as RenoFi adds or loses credit union partners; verify directly with RenoFi before applying, especially in Texas.

| If you live in… | RenoFi available? (as of May 21, 2026) | Best alternative path for an ADU |

|---|---|---|

| Hawaii | ❌ Not per public sources | Local credit union construction loan; HomeStyle Renovation; standard HELOC |

| New York | ❌ Not per public sources (NY DFS restriction on RenoFi’s site) | NY credit union HELOC; CTP from local lender; HomeStyle Renovation |

| Massachusetts | ❌ Not per public sources | Construction loan from a Massachusetts bank or credit union; CHOICERenovation; Mass Save HEAT Loan (0% up to $25,000 for qualifying energy-efficiency upgrades — not a construction loan, but useful for qualifying efficiency components) |

| Texas | ⚠️ Public sources suggest availability; Dwelling Index treats TX as check-direct because of TX Const. art. XVI §50(a)(6) (80% CLTV cap + other restrictions) | If verified ineligible: Texas-specific home equity loan with TX 80% CLTV cap; construction-to-permanent |

| All other U.S. states + D.C. | ✅ Per public sources (subject to specific credit union partner availability) | Return to the decision matrix above |

What to do if RenoFi isn’t available where you live

- Fannie Mae HomeStyle Renovation. A first-lien renovation mortgage that bundles purchase or refinance with renovation funds underwritten against future appraised value. Available nationwide. Better than RenoFi for borrowers who’d be refinancing anyway. Worse than RenoFi if you’d lose a low first mortgage rate.

- Freddie Mac CHOICERenovation. Similar concept to HomeStyle. Freddie Mac’s ADU page explicitly states CHOICERenovation can finance the renovation of an old barn, garage or shed into an ADU and adds factory-built ADUs. Available nationwide.

- Local credit union or community bank construction loan. Often the best route in NY, MA, and HI where RenoFi can’t operate. Smaller institutions tend to be more flexible on specific state rules.

12. Real customer experiences — both sides

Answer capsule: Independent reviews of RenoFi are mixed. Bankrate’s overall score is 4.6/5 with a customer-rating sub-score of 3.7/5 as of February 2026. Publicly available reviews on Trustpilot include strongly positive experiences and documented complaints about communication, documentation requests, and timeline. We will not invent testimonials.

Positive themes from public reviews

- Borrowers who couldn’t qualify through their personal bank report that RenoFi’s partner network found them a workable loan.

- Multiple reviewers cite specific RenoFi loan officers by first name and describe patient explanation of the HELOC process.

- One BiggerPockets thread participant (January 2025) framed RenoFi accurately and positively: a broker, not a lender — which can be a good thing if a partner program fits.

Sources: Trustpilot (trustpilot.com/review/renofi.com); BiggerPockets RenoFi thread; RenoFi’s own published testimonials (renofi.com/reviews/).

Negative themes from public reviews

- Documentation requests that repeated themselves and slowed the process.

- Fees applied to the loan after paperwork was signed.

- Communication gaps during the underwriting phase, especially around timeline updates.

- RenoFi’s own responses on BBB complaints acknowledge “areas where we can improve” and apologize for delays in specific cases.

Sources: Trustpilot (trustpilot.com/review/renofi.com); BBB RenoFi profile.

- Ask which partner credit union you’ll be working with. Get the specific lender name, not just “a RenoFi partner.”

- Set communication expectations in writing. Ask for a target loan estimate date, conditional approval date, and closing date — and get them in an email, not a verbal promise.

13. What to ask any lender before you sign anything

Answer capsule: Before applying to either a RenoFi partner credit union or a construction lender, ask 11 questions about lender role, lien position, value basis, funding mechanics, state availability, ADU eligibility, contractor requirements, draw rules, and what costs are due before final approval. These questions surface deal-breakers before you’ve paid for an appraisal.

The 11-question lender script

- “Are you the actual lender, a broker, a platform, or a lead marketplace?” — Confirms who underwrites and closes, and who you call when something goes wrong.

- “Does this loan replace my first mortgage, or sit behind it as a second lien?” — Protects a low first-mortgage rate.

- “Is this loan underwritten against current value, after-renovation value, or as-completed value?” — Determines borrowing power.

- “What is the hard maximum loan amount for my profile and project?” — Prevents discovering the cap too late.

- “Is this exact product available in my state today?” — Availability changes; double-check.

- “Can this finance a [detached ADU / garage conversion / JADU / attached addition / new home + ADU]?” — ADU type can be an automatic decline.

- “Do you allow this loan on an investment property or LLC-titled property?” — RenoFi’s ARV loans don’t; some construction lenders do.

- “What happens if construction has already started?” — Some products won’t accept work-in-progress.

- “How are funds released — upfront, draw on demand, or staged lender-controlled draws?” — Determines contractor coordination and your role.

- “Does my builder need to be approved by your lender before closing?” — Construction loans often require builder vetting; can disqualify a contractor you already signed with.

- “What costs are due before final approval, and are any of them non-refundable?” — The appraisal is often the biggest one. Know whether you eat it if the loan is denied.

Three red flags that should make you walk away from any lender

- They won’t give you the Loan Estimate within three business days of a full application. Required by federal law (TILA-RESPA Integrated Disclosure rule).

- They guarantee approval before reviewing your documents. No legitimate lender does this.

- They tell you to start construction before closing. A loan officer who suggests this is exposing you to denial risk on partially-completed work.

14. What if neither path fits?

Answer capsule: If neither RenoFi nor a construction loan fits, the alternatives depend on the specific blocker. Standard HELOC works if current equity is sufficient. Fannie Mae HomeStyle Renovation and Freddie Mac CHOICERenovation are first-lien renovation mortgages with nationwide availability. FHA 203(k) supports rehab work on eligible properties. Cash-out refinance can fund a smaller ADU if replacing the first mortgage is acceptable. State and local ADU grant programs exist in some markets.

| Situation | Best alternative | Internal resource |

|---|---|---|

| Current equity already covers the build | Standard HELOC | HELOC for ADU |

| First-lien renovation mortgage works | Fannie Mae HomeStyle Renovation | Best ADU financing options |

| Garage-to-ADU or shed-to-ADU conversion | Freddie Mac CHOICERenovation (explicitly supports this) | Best ADU financing options |

| Older home needs rehab + ADU | FHA 203(k) | ADU loan requirements |

| Replacing first mortgage is fine | Cash-out refinance | How to qualify for ADU financing |

| Need bridge financing during build | Bridge loan | Bridge loan for ADU |

| Can’t qualify conventionally | Hard money or private lender | Hard money loan for ADU |

| Comparing ADU loan generally vs HELOC | Side-by-side decision | ADU loan vs HELOC |

| Need to check whether the project even pencils | ROI/equity calculator | ADU equity calculator |

| Looking for the full overview | Broad comparison | Best ADU financing options |

Free 60-second property feasibility check. No credit pull.

15. How we researched this comparison

Answer capsule: This comparison was built from primary lender disclosures (RenoFi product pages, FAQ, qualification documents, and license/entity pages), agency rules (Fannie Mae Selling Guide B5-3.1-02 on single-close CTP, Fannie Mae’s ADU originating/underwriting page, SEL-2025-08/09/10, Freddie Mac’s ADU and CHOICERenovation pages, HUD Mortgagee Letter 2023-17), independent third-party reviews (Bankrate’s February 2026 RenoFi review), industry rate context (AmeriSave’s May 2026 construction loan guide with secondary citations to FHFA Q3 2025 data), and public customer-experience sources (Trustpilot, BBB, BiggerPockets).

We used forum and Reddit content only to understand borrower confusion and decision friction, not as proof of financial terms, costs, eligibility, or legal claims.

We are an independent research resource. We are not a lender, broker, builder, or municipal permitting authority. We do not rank lenders by compensation. We do not quote rates or monthly payments as guarantees.

When sources conflict — for example, when public availability sources list only HI/NY/MA as RenoFi exclusions while Texas home-equity rules require special verification — we flag the conflict and recommend direct verification with the lender.

For 2026 rate ranges in this article, we used industry context from AmeriSave’s May 2026 construction loan guide (which cites Q3 2025 rate averages of 6.89% on a 30-year fixed and 8.34% on a construction loan). We treat all rates as illustrative and clearly date-stamped, not as offers.

The “ADU value-add” assumption used in the worked scenarios — 70% of build cost added to home value — is a Dwelling Index conservative editorial stress-test, not a market claim. We chose a conservative ratio rather than a marketing-friendly one so the scenarios pressure-test the products honestly. Actual ARV varies by market, comp availability, ADU quality, rental potential, and appraiser methodology, and only a live appraisal answers it precisely.

16. Frequently asked questions

Is RenoFi a construction loan?

No. RenoFi is a licensed mortgage broker — Renovation Finance LLC DBA RenoFi (NMLS #1802847), with additional state entities — that arranges renovation-focused HELOCs, fixed-rate home equity loans, and cash-out refinances from partner credit unions. These products are underwritten against after-renovation value. A construction loan is short-term, draw-based financing that releases funds in stages as the build progresses.

Does RenoFi require a draw schedule for an ADU build?

No lender-controlled construction draw schedule. RenoFi states that the full loan amount is made available upfront by the lender, with no inspections during the build. The HELOC variants among RenoFi's product lineup allow the borrower to draw funds as needed at their own discretion, which is different from a construction loan's lender-controlled milestone draws.

What credit score do I need for RenoFi?

Per Bankrate's February 2026 RenoFi review, some partner lenders go as low as 620, while most loans over $250,000 require higher scores. RenoFi's own qualification page indicates that most partner lenders require at least 640.

How much can I borrow with RenoFi vs a construction loan?

RenoFi's FAQ states most lenders allow RenoFi Loans up to $500K, with stricter qualification criteria above $250K; broader product copy describes ARV-based loan amounts ranging from $25K to $750K. The loan amount is the lower of two limits: 125% of current value (with some lenders going to 150%) or 90% of after-renovation value. Construction loans are typically capped at 70–80% of the future appraised value with no equivalent fixed dollar cap.

Why do some contractors refuse construction loans?

Three reasons: draw paperwork (each milestone requires documentation and lender inspection), retainage (5–10% of each draw held back until completion, tightening contractor cash flow), and lien-waiver collection (subs and suppliers must sign waivers releasing claims). Most large GCs handle this routinely. Smaller solo-operator ADU builders sometimes won't.

Can I use my ADU's projected rental income to qualify?

Rules are program-specific. Fannie Mae's October 2025 selling guide update (SEL-2025-08) allows up to 30% of qualifying income to come from one ADU's rental income on purchase money mortgages and limited cash-out refinances on one-unit primary residences. Freddie Mac allows ADU rental income as qualifying income under specific guidelines. For FHA loans, HUD Mortgagee Letter 2023-17 allows 75% of the lesser of fair-market rent or lease for properties with an existing ADU, 50% of projected rent for a Standard 203(k) transaction adding a new ADU with no rental history, and no ADU rental income permitted on FHA cash-out refinances — with ADU income capped at 30% of total monthly effective income. RenoFi-style ARV second-lien loans may or may not accept rental income depending on the partner lender. Confirm with your specific lender.

Is RenoFi available in Texas?

Public sources including Bankrate's February 2026 review do not list Texas among the explicit RenoFi exclusions (only HI, NY, and MA are explicitly excluded). However, Texas home-equity rules under Tex. Const. art. XVI §50(a)(6) impose unique restrictions on second-lien home equity products — including an 80% combined loan-to-value cap — so Dwelling Index treats Texas as a check-direct case. Confirm Texas availability and structure directly with RenoFi before applying.

How long does each take to close?

Construction loans typically close in 30–60 days from application. RenoFi's marketing materials target 30–45 days, though public reviews indicate some borrowers have experienced longer timelines depending on the partner credit union and documentation back-and-forth. Single-close construction-to-permanent loans take similar timelines to stand-alone construction loans because the underwriting is more involved — it has to qualify the permanent mortgage at the same time as the construction note.

What if I need more than $500,000?

RenoFi's practical product breakpoint is around $500,000 per their FAQ; some lenders accommodate higher ARV-based amounts per RenoFi's product disclosures, but stricter qualification kicks in well below that ceiling. For builds reliably above $500K, a construction loan or jumbo cash-out refinance is the path. Construction loans constrain based on as-completed appraised value (typically 70–80%), so a higher-value property supports a larger loan.

Can I use RenoFi on an investment property or LLC-titled property?

No. RenoFi's qualification page states that ARV-based RenoFi Loans do not currently allow renovations on investment property or property titled in an LLC. Your path is a DSCR investor loan, a private/portfolio construction lender, or a hard money loan from a non-bank construction lender.

Will a construction loan replace my mortgage?

It depends on the structure. A single-close construction-to-permanent loan does replace your first mortgage — that's the design. A stand-alone (two-close) construction loan does not; it sits as a temporary first lien on the new construction and is paid off by a separate permanent loan you choose at completion.

What if I already started construction?

Already-started construction does not automatically disqualify a RenoFi Loan, but per RenoFi's qualification page, lenders are less likely to approve if the project is far into construction or the home is demolished. Many construction lenders impose similar restrictions and may require inspection and documentation of work-to-date before financing the remaining work. Ask both lender types directly before applying.

Should I talk to RenoFi or a construction lender first?

If your goal is preserving a low first-mortgage rate and the project is an owner-occupied addition or conversion, start by checking RenoFi-style ARV financing and one construction-lender quote for comparison. If your project is a teardown, new build, investment-titled property, or LLC-held property, start with construction or investor lending — RenoFi is not eligible for those scenarios.

Did Fannie Mae change anything important about ADU financing recently?

Yes. In late 2025, Fannie Mae issued three relevant updates: (a) SEL-2025-08 in October allowed up to 30% of qualifying income to come from a single ADU's rental income on one-unit primary residences; (b) SEL-2025-09 in November extended credit-document validity to 18 months for single-close CTP loans and removed the minimum representative credit-score requirement for DU-underwritten loans; (c) SEL-2025-10 in December expanded ADU eligibility, including up to three ADUs on one-unit properties and ADUs on two- and three-unit properties effective March 31, 2026, for lenders using UAD 3.6. Lender adoption may vary. Confirm with your specific lender.

17. What we verified

Verification stamp: May 21, 2026. This page is built on the following primary source categories.

- RenoFi product structure, entity, and license disclosures — renofi.com/notices/licenses/, renofi.com/faq/, RenoFi qualification page, renofi.com homepage footer NY DFS disclosure

- Independent RenoFi review — Bankrate, “RenoFi: 2026 Home Equity Review,” last updated February 27, 2026

- Fannie Mae construction-to-permanent rules — Selling Guide B5-3.1-02; ADU originating/underwriting page; SEL-2025-08 (October 2025); SEL-2025-09 (November 2025); SEL-2025-10 (December 2025, effective March 31, 2026 for lenders using UAD 3.6)

- Freddie Mac ADU rules — sf.freddiemac.com/working-with-us/accessory-dwelling-units; CHOICERenovation product page

- FHA ADU rental income rules — HUD Mortgagee Letter 2023-17 (effective October 16, 2023)

- Industry rate context — AmeriSave 2026 construction loan guide, citing Q3 2025 rate averages from FHFA

- California JADU definition — California HCD ADU Handbook, March 2026

- Massachusetts efficiency financing — Mass Save HEAT Loan (0% financing up to $25,000 for qualifying energy-efficiency upgrades)

- Customer experience — Trustpilot RenoFi reviews; BBB RenoFi profile; BiggerPockets RenoFi discussion thread (January 2025)

- Texas state availability for RenoFi — confirm directly with RenoFi before applying.

- Specific partner credit union assignment — ask for the specific CU name during your application call.

- SEL-2025-10 expanded ADU eligibility — effective March 31, 2026 only for lenders using Fannie Mae’s UAD 3.6. Lender adoption varies.

- Current rate ranges — get a current Loan Estimate from any lender you’re considering. Rates are not promised.

If you find anything stale or incorrect, email us — we update on confirmed reports. See our editorial standards, methodology, and corrections policy.

Affiliate disclosure

The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. RenoFi is mentioned in this article as the named subject of a comparison; we are not currently in an active affiliate relationship with RenoFi and do not earn commission on links to renofi.com. Our active research partner for broad mortgage, refinance, cash-out refi, and construction loan content is Mortgage Research Center. See the full affiliate disclosure and our partner vetting policy. This article is for informational purposes only and does not constitute financial, legal, tax, lending, or construction advice. Verify all information with qualified local professionals before making decisions.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU Report