RenoFi vs Figure HELOC for ADUs: Which One Fits Your Build?

The 30-second answer

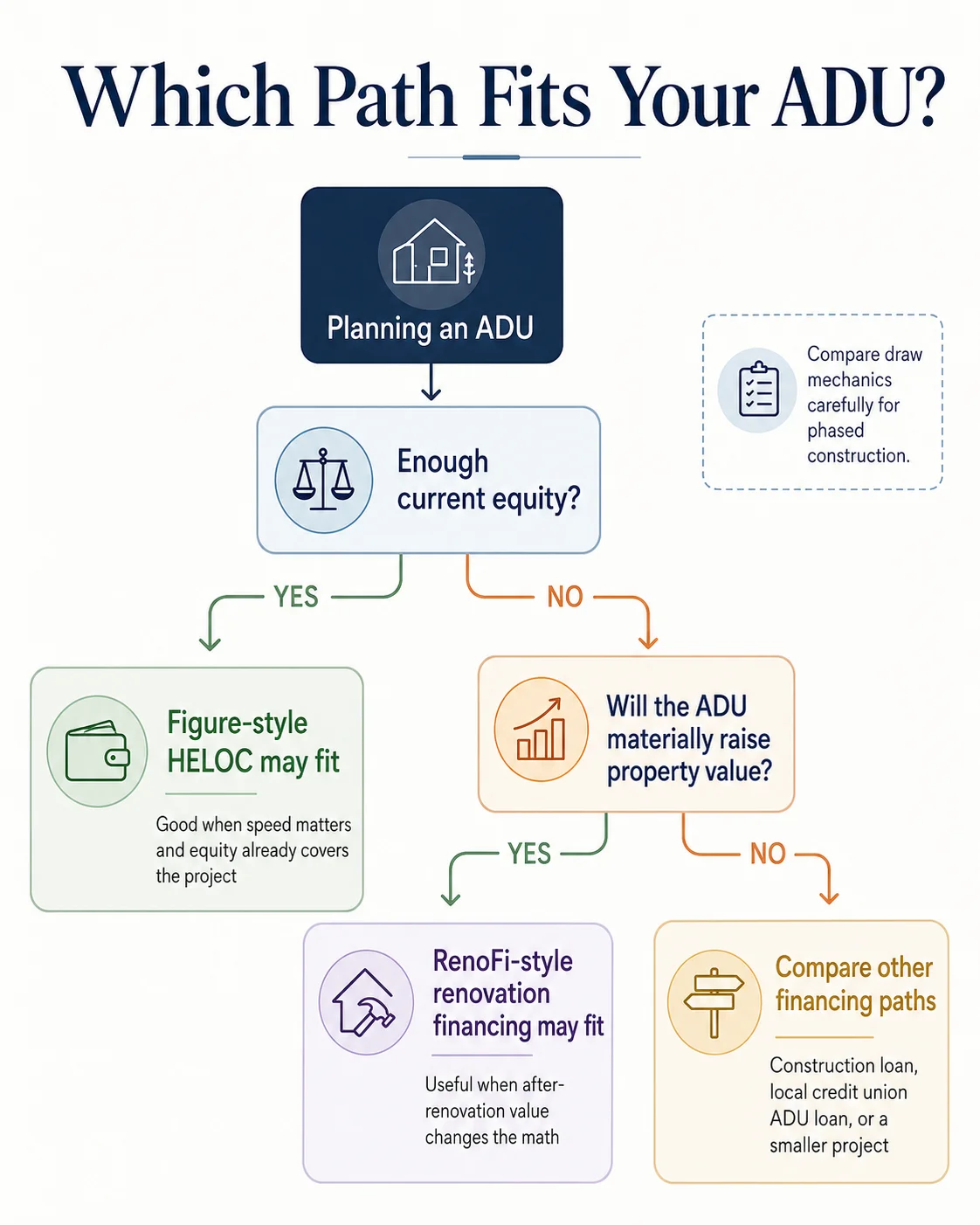

For a RenoFi vs Figure HELOC decision on an ADU build, the answer comes down to where your bottleneck is. Pick a RenoFi-style renovation HELOC if your current home equity won’t cover the project but the ADU will materially raise your property’s value. Pick a Figure HELOC if you already have substantial current equity, want a fast online process, and can put most of the funds to work within a few months. Pick neither — and look at a construction loan, cash-out refinance, or local credit union ADU product — if your state excludes one or both lenders (Hawaii excludes both; New York and Massachusetts exclude RenoFi; New York blocks Figure’s HELOC application through its site; Texas requires careful verification with either).

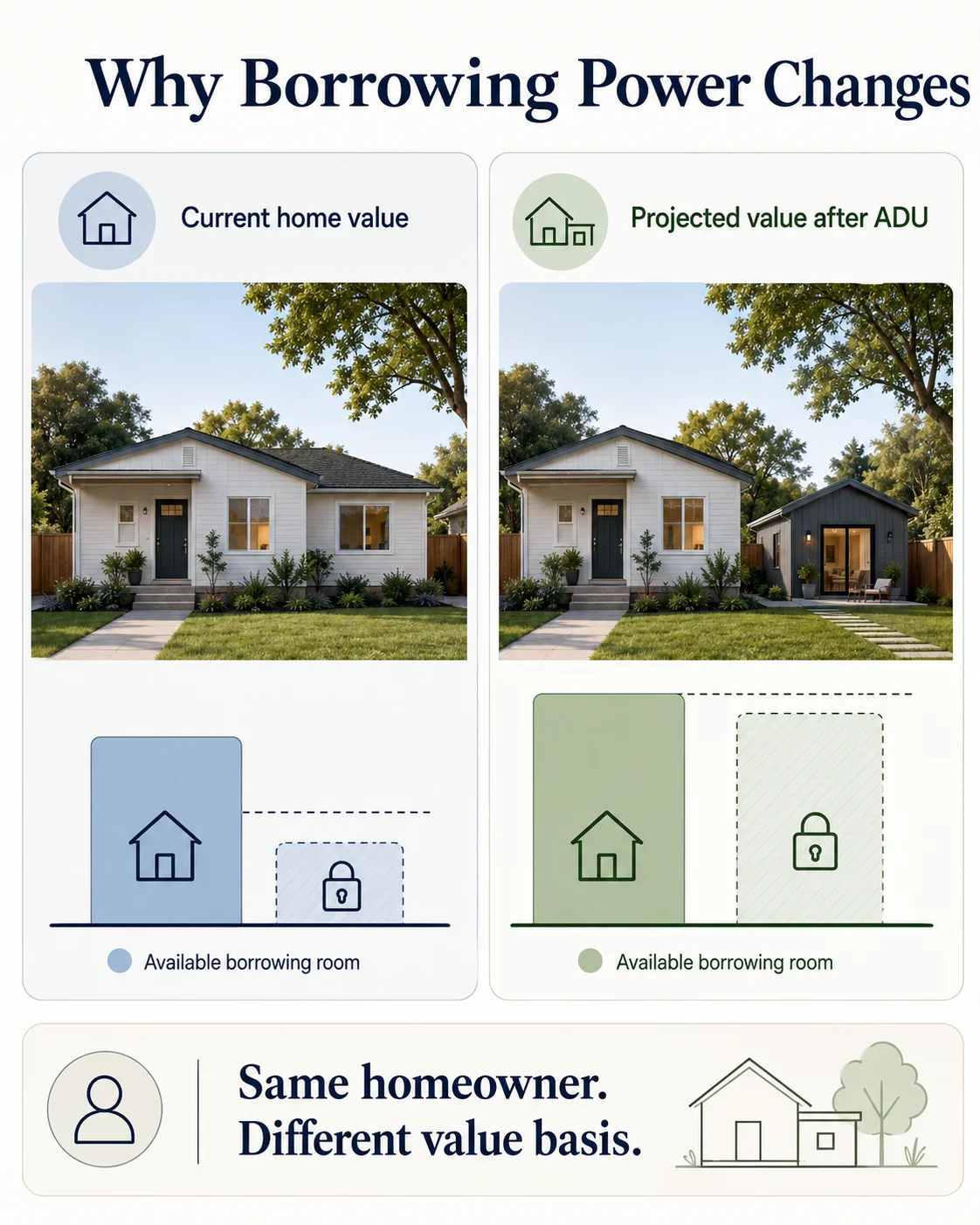

The single number that decides most of this comparison: a recent homebuyer with $130,000 of current equity in a $650,000 home, planning a $250,000 ADU, typically shows roughly $0 in usable borrowing room under a current-equity HELOC formula. The same homeowner can show $235,000–$280,000 of borrowing room under an after-renovation-value (ARV) formula — assuming the appraisal supports the projected post-build value. That gap is what RenoFi exists to fill and what Figure cannot reach by design.

See What You Can Build → Get Your Free ADU ReportEnter your zip code and ADU plan. Our Feasibility Engine returns your local zoning posture, an early borrowing-power read, and which financing paths actually fit your property and state. Free, no credit pull, under 60 seconds.

By the Dwelling Index Editorial Team · Published: May 21, 2026 · Last updated: May 21, 2026 · Last verified: May 21, 2026 · ~32 min read

Independent editorial comparison. We have no affiliate relationship with RenoFi or with Figure as of this publish date.

What we verified for this comparison

Primary sources: RenoFi official pages (homepage, how-it-works, FAQ, wholesale docs); Figure official HELOC FAQ (figure.com); Bankrate Best HELOC Lenders (May 2026) and RenoFi Review (Feb 27, 2026); NerdWallet Figure HELOC Review (updated May 6, 2026); CNBC Select Figure HELOC Review (April 2026); LendEdu Figure and RenoFi reviews (May 2026); Credit Karma Figure HELOC Review; Figure/Lowe's HELOC partner disclosure; CFPB HELOC consumer guidance; IRS Publication 936; California State Board of Equalization; Curinos national rate benchmark (May 20, 2026); Bankrate national HELOC survey (May 6, 2026). Terms vary by state, partner, and credit profile; verify specifics directly with the lender before applying.

RenoFi vs Figure HELOC at a glance

The fastest way to use this comparison: find the row that describes your situation and start with the right product. Everything below the table is the verification you need before you actually apply.

| If this describes you | Start with | Why |

|---|---|---|

| You bought your home in the last ~5 years and have limited current equity, but your ADU will materially raise the property’s value | RenoFi-style ARV path | Current-equity HELOC math typically can’t reach project size; ARV-based underwriting can. |

| You’ve owned for 10+ years, have substantial equity, and your builder needs you funded in days | Figure HELOC | Existing equity already covers it; Figure can fund in as few as 5 days. |

| Your ADU budget is $250K–$500K+ and you’re in a high-cost metro | RenoFi-style ARV path | Higher-cost ADUs routinely exceed pure current-equity capacity. |

| You need money in 3–4 phases as your builder invoices each construction milestone | Compare carefully — Figure may be a structural mismatch | Figure requires drawing 100% of the line at closing; interest accrues on the full balance from day one. |

| You only need $60K–$120K for a garage conversion in a non-coastal market | Figure HELOC may be enough | Current equity often covers smaller conversions; speed and simplicity matter more. |

| You’re in Hawaii | Neither | Figure does not lend in Hawaii. Bankrate’s 2026 RenoFi review states RenoFi is not available in Hawaii. Look at local Hawaii credit union products instead. |

| You’re in New York | Verify Figure directly; not RenoFi | RenoFi is excluded in New York. Figure’s own FAQ states its Home Equity Line application is not for use for New York mortgage applications through its site. |

| You’re in Massachusetts | Not RenoFi | RenoFi is excluded in Massachusetts. Figure or a Massachusetts-licensed alternative. |

| You’re in Texas | Verify both directly | RenoFi’s wholesale documentation excludes Texas; confirm retail status with a RenoFi advisor. Figure operates in Texas with a $35,000 minimum and Texas Constitution §50(a)(6) home-equity rules. |

| You’re not sure your lot can support an ADU at all | Feasibility first, then financing | A financed-but-unbuildable project is the most expensive mistake in this category. |

Sources: RenoFi published how-it-works disclosures and FAQ; Figure published HELOC FAQ; Bankrate RenoFi Review (Feb 27, 2026) and Best HELOC Lenders (May 2026); NerdWallet Figure HELOC review (May 6, 2026); CNBC Select Figure HELOC review (April 2026). Last verified May 21, 2026.

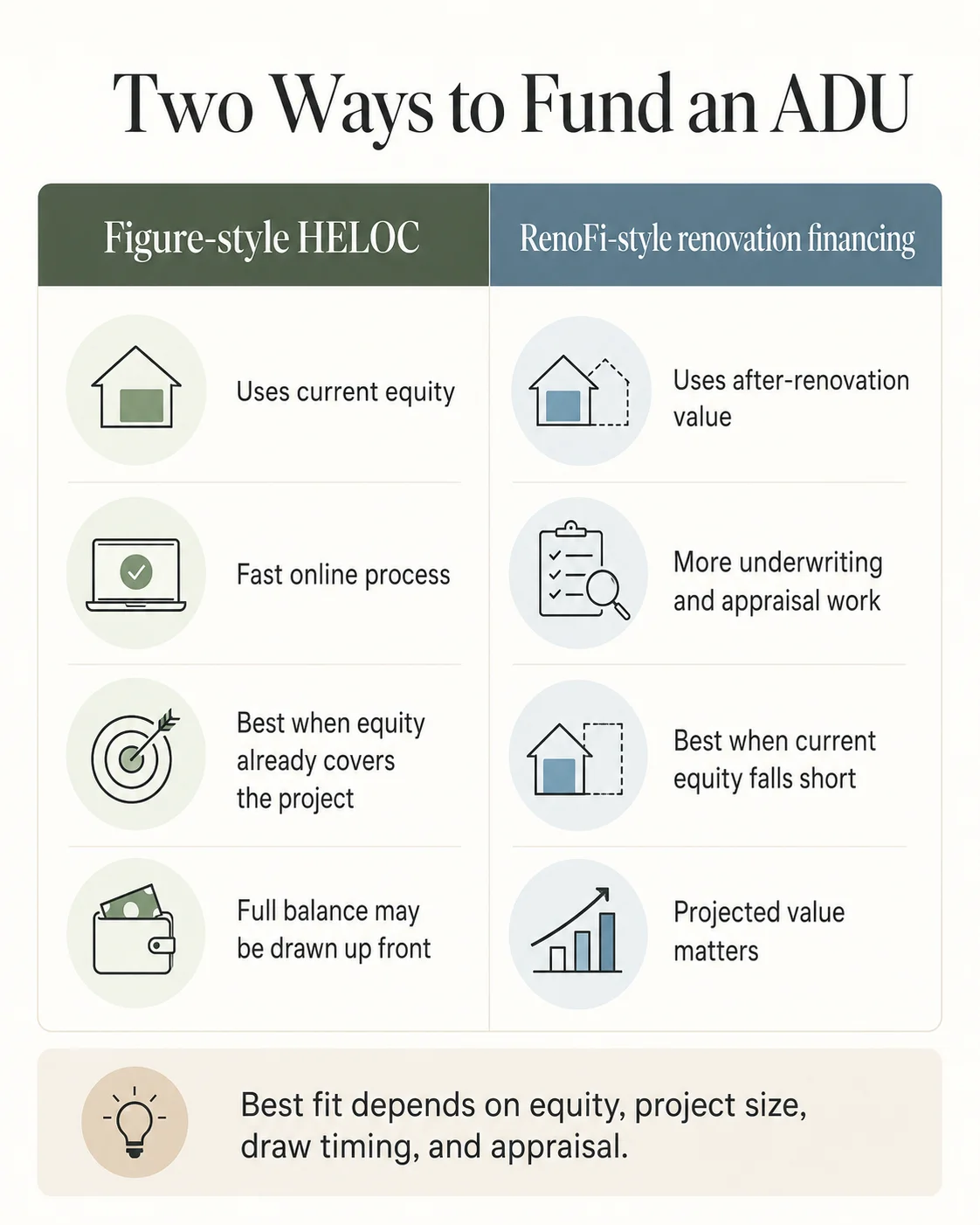

Is RenoFi or Figure better for an ADU?

Answer capsule: Neither is universally better. RenoFi-style renovation HELOCs win when current equity is the bottleneck and the ADU is expected to materially raise the home’s appraised value, because the underwriter can use after-renovation value (ARV). Figure wins when current equity already covers the project, speed matters, and the borrower can put most of the funds to work right away. The structural difference — current value vs ARV, and how draws are released — is what decides the comparison.

This is the heart of the page. The next sections break each side down in detail; the borrowing-power matrix further down shows the math for seven realistic homeowner profiles.

What RenoFi actually is (and what it isn’t)

Answer capsule: RenoFi is not a lender. It is a renovation finance broker (Renovation Finance LLC, NMLS #1802847) that pairs homeowners with credit union lending partners, and those partners underwrite a HELOC or fixed home equity loan based in part on the home’s projected after-renovation value rather than its current value. The ARV mechanic is the entire reason RenoFi exists as a category.

The “broker, not lender” distinction matters

RenoFi states plainly on its own FAQ and how-it-works pages that it is not the lender — loans are made through its third-party lending partners, almost always credit unions. RenoFi’s role is to package the project, source the appraisal, and route the file to a partner credit union licensed in your state. The credit union holds the note. The credit union services the loan. If something goes sideways during repayment in year four, you’re talking to the credit union.

This isn’t a criticism — it’s a structural fact that affects three practical things:

- Your timeline. RenoFi’s own FAQ states the process generally takes 30 to 60 days after documents are collected, and the company explicitly does not guarantee approval or timing. The file passes through both RenoFi’s renovation-specific review and the partner credit union’s standard underwriting.

- Your exact terms. RenoFi advertises product frameworks — fixed and variable structures depending on partner, loan terms up to 20 years, and specific borrowing caps that vary by partner program. The specific number you get depends on which credit union accepts your file.

- Your state availability. RenoFi’s footprint is the union of its partner credit unions’ state licenses, which is why the company is unavailable in some states even when standard HELOCs are widely available there.

What “after-renovation value” actually buys you

The single most important concept in this comparison is after-renovation value (ARV) — the appraiser’s estimate of what your home will be worth once the renovation is complete. Bankrate’s May 2026 Best HELOC Lenders review describes RenoFi as letting borrowers draw on up to 95% of after-renovation value rather than current market value, while RenoFi’s own homepage and product pages cite frameworks up to 90% of ARV and up to 125% of current home value depending on partner program. We use the more conservative 90% in our worked examples below. Source-conflict note: confirm the specific cap with your matched partner before counting on it.

A standard HELOC underwriter looks at this:

Maximum HELOC = (current appraised value × 0.80–0.85 max CLTV) − current mortgage balance

A RenoFi-style renovation HELOC underwriter looks at this:

Maximum RenoFi-style line = (projected after-renovation value × up to 0.90–0.95) − current mortgage balance, capped at up to 125% of current home value depending on the partner program

For a recent homebuyer, the difference is enormous. A buyer who closed in 2022 with $130K of current equity in a $650K home, planning a $250K ADU that the appraiser projects will lift the home to $850K, sees roughly:

- Current-equity HELOC capacity: ($650K × 0.85) − $520K mortgage ≈ $32,500. Not enough to fund a single milestone draw on a real ADU build.

- ARV-based capacity (at 90% ARV): ($850K × 0.90) − $520K ≈ $245,000. Functionally covers the project, with realistic contingency planning.

The borrower hasn’t changed. The home hasn’t changed. Only the value basis has.

Where RenoFi gets weaker

The damaging admission: RenoFi is not unlimited borrowing power. Real limits apply:

- The appraisal can come in low. ARV is an estimate. When comparable ADU sales are thin in your neighborhood, the appraiser may not project the value lift your builder assumed. Underwriting then caps at the lower projected ARV.

- DTI, credit, lien position, and partner overlays still apply. Even with strong ARV, a marginal credit profile or stretched debt-to-income ratio will be declined.

- State and partner availability. Per Bankrate’s February 2026 RenoFi review, RenoFi does not operate in Hawaii, New York, or Massachusetts. RenoFi’s wholesale documentation excludes Texas from the after-renovation-value program. Verify your state directly with a RenoFi advisor before assuming eligibility.

- Servicing complexity. Because RenoFi sits between you and the credit union, escalation paths are longer than with a direct lender.

Bankrate’s review also notes that some RenoFi partner credit unions assess a renovation servicing charge of up to $150 per month for the duration of the construction phase. On an eight-month ADU build, that’s up to $1,200 in additional cost that doesn’t show up in the headline rate. Confirm whether your matched partner charges this before you sign.

Real homeowner experiences

RenoFi’s Trustpilot profile shows a mix of customer experiences. Positive reviews emphasize advisor responsiveness and the ability to unlock ARV-based capacity that other lenders wouldn’t underwrite. Negative reviews most commonly cite timeline overruns and broker-fee surprises — one reviewer noted a 2% broker fee that surfaced late in the application. Read the full range before applying, and ask your advisor in writing what all fees will be before you commit. These are voice-of-customer signal, not proof of loan terms. Verify any specific number with the advisor and the lending partner before you sign.

What a Figure HELOC actually is

Answer capsule: Figure is a direct online lender (Figure Lending LLC, NMLS #1717824) that offers a HELOC with fixed and variable rate options and an unusual structural requirement: borrowers must draw 100% of the approved line at closing. Interest accrues on the full balance from day one, and additional draws are permitted during a 3-to-5-year draw window as the initial balance is repaid. The result is a product that behaves like a hybrid between a HELOC and a home equity loan, optimized for speed.

The 100%-draw-at-closing requirement

Most HELOCs work like a credit card: you have an approved line, you draw on it as needed, you pay interest only on what you’ve drawn. Figure does not work that way. At closing, Figure funds the entire approved line into your bank account. Interest accrues on the full balance immediately.

You can take additional draws during the 3-to-5-year draw window — the exact length depends on the repayment term you select at origination — but those redraws happen only as you pay down the initial balance. Each additional draw locks in the lender’s rate at the time of that draw, not your original rate.

Credit Karma’s review confirms the requirement plainly: borrowers must initially withdraw 100% of the approved amount at closing, similar to a home equity loan or cash-out refinance rather than a traditional revolving HELOC. NerdWallet’s May 2026 Figure review describes the draw window as three to five years.

Why this matters specifically for an ADU build

An ADU build typically pays out in milestones: a deposit, permits, foundation, framing, finishes, final. Your builder doesn’t ask you for the full $250K on day one. They invoice you in 3 to 5 stages over 6 to 12 months. We work through the dead-interest math on that exact scenario in the cost section below.

Speed as the real feature

Figure advertises funding initiated in as few as five days from a complete online application. That is genuinely fast for the category — most credit unions, banks, and broker-mediated products run 30 to 60 days. For homeowners under permit-clock pressure or builder-slot pressure, that speed has real value.

The origination fee

Figure charges an origination fee of up to 4.99% of the loan amount. The structure is intentional: paying a higher origination fee buys you a lower locked rate. For a borrower who plans to pay the loan off in 5–10 years, the trade can be worth it; for a 30-year payoff, the math depends on the rate spread. On a $250,000 HELOC, a 4.99% origination fee is up to $12,475, added to the loan balance at closing. NerdWallet, CNBC Select, and LendEdu all flag this as Figure’s primary affordability drawback in their 2026 reviews.

State availability, product mechanics, and minimums (verified)

- Available in 49 states: Per multiple 2026 reviewer sources, Figure does not lend in Hawaii.

- New York: Figure’s own published FAQ states that its Home Equity Line application is not for New York mortgage applications or products through its site. Verify directly with Figure before assuming product availability in NY.

- Minimum loan amounts: $10,000 in most states; $25,001 in Alaska; $35,000 in Texas. Minimums vary by channel and disclosure date, so verify against Figure directly.

- Maximum line size: Up to $750,000 for the most qualified borrowers. Loans above $400,000 may require a full appraisal in addition to Figure’s standard automated valuation.

- Minimum credit score: Source-specific. NerdWallet currently lists 600; Credit Karma describes minimum qualification requirements as generally 600 (with a 660 minimum on investment properties); LendEdu lists 640. Verify the current minimum directly with Figure.

- Rate type: Fixed and variable options depending on product, channel, and state. The fixed-rate-per-draw mechanic is the more commonly described structure in published reviews.

- Repayment terms: 10, 15, 20, or 30 years, chosen at origination.

- Property eligibility: Figure HELOCs may be available for primary residences, secondary residences, and investment properties, with different minimum-score requirements for each. Verify investment-property eligibility directly with Figure for the current product.

Sources: Figure published HELOC FAQ; NerdWallet Figure HELOC Review (updated May 6, 2026); CNBC Select Figure HELOC Review (April 2026); LendEdu Figure HELOC Review (May 2026); Credit Karma Figure HELOC Review; Figure/Lowe's HELOC partner disclosure. Last verified May 21, 2026.

Real cost comparison: fees, draws, and dead interest

Answer capsule: The headline cost of either product is the interest rate plus origination fees. The hidden cost — the one no other comparison page surfaces — is the interest paid on money that hasn’t been spent yet. For a phased ADU build, that dead interest can outweigh the rate difference between the two products.

Origination, closing costs, and renovation servicing fees side by side

For a $250,000 HELOC, the fee picture looks roughly like this:

| Cost category | RenoFi (via partner credit union) | Figure HELOC |

|---|---|---|

| Origination fee | Varies by partner; commonly 0–1% | Up to 4.99% (on $250K, up to $12,475) |

| Closing costs (title, recording, valuation, notary) | Typically 1–3% (on $250K, $2,500–$7,500) | Standard recording fees plus AVM/appraisal costs; loans over $400K may require a full appraisal |

| Renovation servicing charge | Up to $150/month with some RenoFi partners during construction (Bankrate) | None |

| Inactivity / early closure fees | Varies by partner | None per Figure’s published terms |

Figure’s higher origination fee is real money — $12K+ on a $250K loan — but it’s bundled into the balance and amortized. RenoFi’s closing costs are typically lower, but the renovation servicing charge from some partners can add over a thousand dollars during a long build.

The phased-draw dead-interest calculation

This is the cost almost nobody surfaces in lender reviews. We worked through it because it is the single most consequential mechanical difference between these two products for an ADU buyer.

Scenario assumptions (illustrative — not a rate quote, not APR, not a loan offer):

- ADU project: $250,000 total, built over 8 months

- Builder invoices in 4 milestones: 25% at month 1 (deposit + permits), 25% at month 3 (foundation + framing), 25% at month 5 (mechanical, electrical, plumbing, drywall), 25% at month 7 (finishes + final inspection)

Path A — True phased-draw HELOC. You draw only as your builder invoices. Average outstanding balance across the 8-month construction window ≈ $125,000 (half of the full line, because you ramp to it over time).

Path B — Figure 100%-draw-at-closing. You draw the full $250,000 at closing. Even if you park the unused portion in a high-yield savings account, your loan balance is $250,000 from day one. Average outstanding balance across the 8 months ≈ $250,000.

Dead-interest cost difference at a 7% rate, over the 8-month construction phase:

($250,000 − $125,000) × 7% × (8 ÷ 12) ≈ $5,830 in extra interest paid on the Figure structure

Even if you offset by parking the undrawn balance in a 4% high-yield savings account, net cost is roughly:

$5,830 − ($125,000 × 4% × 8/12) ≈ $2,500–$3,000 of net dead interest you wouldn’t pay on a true phased-draw HELOC

What rates look like as of May 2026

Per Bankrate’s national HELOC survey, the average rate for a $30,000 HELOC was 7.26% as of May 6, 2026. Curinos data via Yahoo Finance shows national-average HELOC rates around 7.21% as of May 20, 2026, for applicants with 780+ credit and CLTV under 70%. The Federal Reserve has held its benchmark rate at its March, April, and May 2026 meetings.

- Figure’s fixed-rate mechanic (when used) protects you against rate increases but doesn’t capture rate decreases if they happen.

- A variable-rate HELOC (the typical structure with RenoFi’s credit union partners, or any traditional HELOC) tracks the prime rate — currently 6.75% — and floats with it.

Neither is universally better. It depends on how quickly you’ll pay down the balance and your view of the rate path.

Reader-supported disclosure: This partner link may compensate us at no extra cost to you.

Want to model cash-out refinance against both of these? → Explore current mortgage and construction-loan rates with Mortgage Research CenterMortgage rates and HELOC rates respond to different forces. If your existing first-mortgage rate is at or above today’s market rate, cash-out refinance can be a cleaner single-payment path than either RenoFi or Figure. Our partner Mortgage Research Center can help you model the all-in cost.

How much could RenoFi and Figure actually let you borrow? The ADU Borrowing-Power Matrix

Answer capsule: Borrowing power depends on three numbers: your current home value, your current mortgage balance, and your home’s projected value after the ADU is built. Under a current-equity HELOC formula, you’re capped by the first two numbers. Under an ARV-based formula, the third number changes everything.

The formulas we used

- Figure-style current-equity HELOC capacity: (current home value × 80%) − current mortgage balance

- RenoFi-style ARV capacity: the lower of [(projected after-ADU value × 90%) − current mortgage balance] or [(current home value × 125%) − current mortgage balance]

- Project funding gap: (estimated ADU budget × 1.15 for contingency) − estimated borrowing capacity

We deliberately used 80% LTV on the Figure side (conservative; Figure can reach 85% for top-tier borrowers per its disclosures) and the 90% ARV cap on the RenoFi side (Bankrate’s May 2026 review cites up to 95%; we use 90% because not every borrower will hit the published ceiling). Real numbers will land inside this range.

| # | Profile | Current value / mortgage / equity | Projected after-ADU value | ADU budget (+15% contingency) | Figure-style capacity | RenoFi-style capacity | Practical read |

|---|---|---|---|---|---|---|---|

| 1 | Recent buyer, detached ADU | $650K / $520K / $130K | $850K | $300K ($345K) | ~$0 | ~$245K | Figure fails the equity test. RenoFi covers most of the build with a ~$100K gap to plan around. |

| 2 | Moderate equity, garage conversion | $600K / $360K / $240K | $680K | $140K ($161K) | ~$120K | ~$252K | Figure may come up short of contingency. RenoFi clears the project comfortably. |

| 3 | High equity, detached ADU | $900K / $450K / $450K | $1.05M | $250K ($288K) | ~$270K | ~$495K | Both viable. Figure is simpler if funds are needed soon. |

| 4 | New purchase, very low equity | $500K / $475K / $25K | $625K | $150K ($173K) | ~$0 | ~$87.5K | Neither covers the full build. Look at construction loans or a scaled-back ADU type. |

| 5 | Phased build, mid-equity | $850K / $500K / $350K | $1.0M | $220K ($253K) | ~$180K | ~$400K | RenoFi solves capacity. Figure’s full initial draw is awkward for staged construction. |

| 6 | Lower-cost garage conversion | $400K / $200K / $200K | $480K | $80K ($92K) | ~$120K | ~$232K | Figure is fully sufficient and faster. Simplest path. |

| 7 | High-cost metro, detached ADU | $1.2M / $700K / $500K | $1.5M | $450K ($518K) | ~$260K | ~$650K | RenoFi math fits. Expect tighter underwriting at this loan size. |

The pattern across all seven rows: Figure wins when current equity already solves the problem. RenoFi wins when the project itself creates the equity that funds it. Scenarios 1, 4, and 5 — the recent-buyer and phased-build cases — are where the structural difference matters most.

Our Feasibility Engine takes your zip code, current home value, mortgage balance, and ADU plan and returns your estimated borrowing power under each path, plus a state-availability check and a flag for known funding gaps. Free, no credit pull, under 60 seconds.

When does RenoFi make more sense than Figure?

Answer capsule: RenoFi typically makes more sense when current equity is the bottleneck, the project is large enough that current-equity math falls short, and the ADU is expected to materially increase the property’s appraised value. The mechanism is the ARV-based loan structure; the limit is the appraisal.

The four situations RenoFi is built for

- Recent buyers (under 5 years in the home) with limited current equity but a meaningful ADU plan. This is RenoFi’s flagship use case — the borrower who would otherwise be told “come back when you have more equity.”

- Detached ADU builds in the $200K–$500K+ range. Larger projects exceed pure current-equity capacity for most homeowners; the ARV-based structure stretches what’s available.

- Owners who want to preserve a low first-mortgage rate. If you locked a 3% mortgage in 2020 or 2021, you don’t want to cash-out refinance into a 7% rate. RenoFi’s product sits as a second lien behind your existing mortgage.

- High-cost metros where ADU costs structurally exceed current equity for most owners. Bay Area, Los Angeles, Seattle, Boston-area, Denver — ADU builds in these markets commonly run $300K–$500K+, which routinely exceeds what a current-equity HELOC can support.

Where RenoFi gets weaker

- If the appraisal comes in low. ARV is an estimate. Underwriting is capped at the lower projected ARV.

- If you’re in Hawaii, New York, Massachusetts, or Texas. Bankrate’s RenoFi review (Feb 2026) confirms RenoFi does not currently operate in HI, NY, or MA. RenoFi’s wholesale documentation excludes Texas. Verify directly before assuming eligibility.

- If you need money in 5–10 days. The broker-to-credit-union handoff produces a 30–60 day timeline per RenoFi’s own FAQ.

- If your matched partner credit union charges a monthly renovation servicing fee. Bankrate notes this can run up to $150/month during construction.

When does Figure make more sense than RenoFi?

Answer capsule: Figure typically makes more sense when current equity is already sufficient to cover the ADU, when speed is non-negotiable, and when the borrower is comfortable drawing the full approved line at closing. The mechanism is direct online underwriting; the limit is the structural mismatch with phased construction draws.

The four situations Figure is built for

- Long-tenured owners with substantial existing equity. If you’ve owned for 10+ years in any reasonable appreciation market, you likely have plenty of current equity to fund an ADU without needing ARV math.

- Garage conversions and smaller ADUs in the $80K–$150K range in non-coastal markets. These projects typically fit inside current-equity capacity, and Figure’s speed advantage matters more than the ARV stretch.

- Builder-slot-driven timelines. When your builder has a slot opening in three weeks and your alternative is to lose the slot for six months, a 5-day funding timeline has real value.

- Borrowers who want a fixed-rate product. Figure’s hybrid structure can lock your rate at each draw. In a sideways or rising-rate environment, that protection has value.

Where Figure gets weaker

- The 100%-draw-at-closing requirement. You pay interest on the full balance from day one even if your builder won’t invoice for it for months. The dead-interest math above shows this commonly runs $2,500–$6,000 net on a typical phased ADU build.

- The origination fee. Up to 4.99% of the loan amount, added to the balance. On $250K, up to $12,475.

- Hawaii is excluded. New York mortgage applications are blocked through Figure’s site per its own FAQ.

- Texas has a $35,000 minimum loan amount and operates under Texas Constitution Section 50(a)(6) home-equity rules.

- Apples-to-apples rate shopping is harder than it should be. Figure’s rate structure (origination-fee-for-rate-buydown) means a published APR isn’t directly comparable to a standard credit-union HELOC.

Where each lender actually works (state availability)

Answer capsule: State availability disqualifies at least one of these two products in four states: Hawaii (both excluded), New York (RenoFi excluded; Figure’s HELOC application is blocked through its site), Massachusetts (RenoFi excluded), and Texas (RenoFi excluded per wholesale documentation; Figure operates with a higher minimum and additional state-specific rules). Verify availability directly with the lender before applying — provider service areas change.

The state-availability matrix

| State context | RenoFi available? | Figure available? | What this means for you | Source / last checked |

|---|---|---|---|---|

| 45 standard states | Yes | Yes | Both available; choose on the criteria above. | Lender first-party + Bankrate (May 2026), NerdWallet (May 2026) — May 21, 2026 |

| Hawaii | No | No | Look at Hawaii-licensed credit unions (Hawaii State FCU, HFS FCU). | Bankrate RenoFi review (Feb 27, 2026); CNBC Select Figure review (April 2026); NerdWallet Figure review (May 6, 2026) — May 21, 2026 |

| New York | No | Verify directly | Figure’s FAQ excludes New York mortgage applications through its site. Figure HELOC alternative or NY-licensed second-lien lender. | RenoFi how-it-works disclosure; Figure HELOC FAQ — May 21, 2026 |

| Massachusetts | No | Yes | Figure or a Massachusetts-licensed alternative. | Bankrate RenoFi review (Feb 27, 2026); Figure HELOC FAQ — May 21, 2026 |

| Texas | Excluded per wholesale doc; verify retail | Yes, $35K minimum; TX §50(a)(6) rules | Figure (with Texas-specific verification) or a Texas-licensed alternative. | RenoFi wholesale doc (2025); Figure/Lowe's partner disclosure — May 21, 2026 |

| Alaska | Yes | Yes, $25,001 minimum | Either, with confirmation of Figure’s Alaska minimum. | Figure/Lowe's partner disclosure — May 21, 2026 |

If a lender on this page doesn’t serve your state, our Feasibility Engine returns the products that do — verified against current state licensing.

The Texas wrinkle

Texas has unique home-equity rules under Section 50(a)(6) of the Texas Constitution that affect both maximum CLTV and the timing of when you can take a second lien. This isn’t a RenoFi or Figure problem specifically — it’s a Texas-borrower-using-any-HELOC-product problem. If you’re in Texas, work with a lender who has explicit Texas home-equity experience and confirm in writing how 50(a)(6) applies to your specific loan structure before you sign anything.

What can go wrong with either HELOC during an ADU build

Answer capsule: The biggest risks are not brand-specific. Both products are secured by your home; both can have payments rise sharply when the draw period ends; both can be reduced or frozen by the lender if your home value drops or your financial situation changes; and construction costs commonly run over budget. These are HELOC-category risks the Consumer Financial Protection Bureau warns about for any home equity line.

Your home is the collateral

Per the Consumer Financial Protection Bureau (CFPB) HELOC consumer guidance, a HELOC is a secured loan, and the security is your home. If you can’t repay, you can lose your home. That risk doesn’t change between RenoFi and Figure. It changes between “HELOC of any kind” and “personal loan or unsecured financing.” Treat the decision accordingly.

Payment shock after the draw period ends

The CFPB also warns that HELOC payments can rise sharply when the draw period ends and the repayment period begins. During the draw period on a traditional HELOC structure, you may be paying interest only. Once draw ends — typically year 10 on a traditional HELOC, or sooner on Figure’s 3-to-5-year draw window — you begin paying principal plus interest on the outstanding balance over a shorter remaining term.

Practical step: Before you sign either product, ask the lender to show you the post-draw monthly payment, not just the draw-period payment. The two can differ by several hundred dollars on a six-figure balance.

The lender can freeze or reduce the line

Per the CFPB, lenders may reduce or freeze a HELOC if the property value declines significantly or if your financial circumstances change materially. This matters specifically during construction — if your ADU build runs over budget and you’ve already drawn most of the line, you may not be able to draw the additional cushion you assumed would be available. This is one reason we recommend planning your ADU budget with a 15% contingency baked in before financing, not as an afterthought.

Construction costs commonly run over

Three categories drive most ADU budget overruns, none of them predictable from a builder’s headline per-square-foot price:

- Utility hookups — electrical service upgrades, sewer laterals, water meters, gas extensions

- Site work — grading, drainage, demolition, retaining walls, tree removal

- Permits and impact fees — vary widely by jurisdiction and can run $5K–$20K+ before construction begins

A $250K detached ADU bid can easily become $290K once site work is fully scoped. Build the contingency. Don’t borrow against optimism.

Includes the budget contingency worksheet, the questions to ask your builder before signing, and the hidden-cost checklist by ADU type. Free, no obligation.

What if neither RenoFi nor Figure covers the full ADU budget?

Answer capsule: If neither product reaches your project budget, forcing a bad fit is the most expensive option. The honest answer is to compare paths — a construction loan, renovation loan, cash-out refinance, local credit union ADU product, or a scaled-back ADU type — rather than force-fit a product that wasn’t designed for your situation.

The full alternatives table

| Alternative | When it fits | Caution |

|---|---|---|

| Standard bank or credit union HELOC | You have current equity but want revolving access; you don’t need Figure’s speed or origination-fee structure | Variable rates can rise; line can be frozen; subject to current-equity cap |

| Home equity loan (fixed lump sum) | Your ADU budget is a known fixed number and you want predictable payments | Less flexible than a HELOC if scope or cost shifts mid-build |

| One-time-close construction loan | Large build that needs phased draws with inspections; ADU budget exceeds combined current equity and projected ARV | More documentation; lender controls draws; appraisal and contractor approval required |

| Renovation loan (Fannie HomeStyle, FHA 203(k)) | Project relies on after-improved value, similar logic to RenoFi but with conventional/agency-backed structures | Stricter contractor and timeline requirements; not all lenders offer for ADU specifically |

| Cash-out refinance | Your current mortgage rate is at or above today’s market rate, OR you want a single consolidated payment | Replaces a low-rate first mortgage with a higher-rate larger loan — frequently a net-negative move if your existing rate is below ~5% |

| Local credit union ADU-specific product | You’re in a state with strong credit union ADU lending; examples include Patelco (CA, up to 125% CLTV ADU HELOC), E-Central (CA), Monterra CU (formerly San Mateo CU, CA), and OlyFed (WA, HELP construction loan) | Member-specific terms; verify rate, fees, membership, state eligibility, and draw mechanics directly |

| Scaled-back ADU type | Budget gap is significant and your lot supports a smaller footprint | Garage conversion or JADU commonly runs 40–60% of detached ADU costs |

| Phased build | Gap is small and the scope can be split (e.g., shell-only first, finishes later) | Increases total project cost and timeline; not all jurisdictions issue partial certificates of occupancy |

| HEI (home equity investment, e.g., Hometap, Unlock, Point) | You have equity but don’t want monthly payments; willing to trade future appreciation for current cash | Not available in all states; you give up a percentage of home appreciation rather than paying interest |

If you’re considering cash-out refinance

If your existing first mortgage rate is at or above today’s market rate, a cash-out refinance can be the cleanest single-payment path to fund an ADU. If it’s below today’s market rate, the math almost always works against you. Run the numbers before assuming.

Reader-supported disclosure: This partner link may compensate us at no extra cost to you.

Compare cash-out refinance and construction-loan paths → Current rates with Mortgage Research CenterIs HELOC interest deductible if I use it to build an ADU?

Answer capsule: Possibly, but only under specific conditions. IRS Publication 936 establishes that home equity debt interest is generally deductible only when the proceeds are used to buy, build, or substantially improve the home that secures the loan, subject to mortgage-interest limits and itemized-deduction rules. Building an ADU on the property securing the HELOC typically qualifies — but specifics matter, and this is general information, not tax advice.

What IRS Publication 936 actually says

In plain English: home equity loan and HELOC interest is potentially deductible only if (1) the loan is secured by the home, (2) the proceeds are used to buy, build, or substantially improve that same home, and (3) the borrower itemizes deductions and stays within the overall mortgage-interest cap ($750,000 for loans originated after December 15, 2017, in most cases). For an ADU built on the property securing the HELOC, condition (2) is typically met because constructing a new dwelling unit qualifies as a substantial improvement to the property.

Where it gets complicated

- Mixed-use draws. If you draw $300K and use $250K for the ADU and $50K for a vacation, only the $250K portion’s interest is potentially deductible.

- The standard deduction. If you take the standard deduction, the HELOC interest deduction provides no benefit.

- The $750K cap. Total mortgage debt (first mortgage + HELOC combined) above $750K may not be fully deductible.

- State tax treatment varies. Some states diverge from federal rules.

Does building an ADU affect my property taxes?

Yes. In most jurisdictions, new ADU construction is added to the property tax roll at its current assessed value. In California, per the California State Board of Equalization, new construction is generally assessable and the assessor determines fair market value of new construction when completed; under Proposition 13, your original primary residence retains its protected base-year value and only the ADU addition is assessed at current value. Check with your county assessor for your specific jurisdiction.

How to decide in 10 minutes: a checklist

Answer capsule: Start with the constraint, not the product. If your bottleneck is borrowing capacity, test the ARV path first. If your bottleneck is speed and you already have equity, test the current-equity HELOC. If your bottleneck is project feasibility or zoning, the financing decision is premature.

| Question | If yes | If no |

|---|---|---|

| Do you have enough current equity (after the 20–25% LTV haircut) to cover your ADU plus 15% contingency? | Figure HELOC is viable; start there. | Test RenoFi-style ARV path. |

| Will you actually use most of the funds within 3 months? | Figure’s 100%-draw structure is acceptable. | Be cautious with Figure; phased-draw HELOC or RenoFi partner product is likely a better fit. |

| Is your total ADU budget over $250K? | Test ARV path and one-time-close construction loans; pure current-equity HELOC likely won’t reach it. | Current-equity HELOC may be sufficient. |

| Do you have a sub-5% first mortgage you want to preserve? | Avoid cash-out refinance reflexively; prefer second-lien products. | Cash-out refi may be worth modeling. |

| Has your lot, ADU type, and zoning been confirmed feasible? | Compare financing now. | Pause financing; run feasibility first. |

| Are you in HI, NY, MA, or TX? | Check the state-availability table above before applying to either lender. | Continue product comparison. |

| Do you want a predictable fixed rate? | Figure’s fixed-per-draw mechanic or some RenoFi partners’ fixed home equity loan products may fit. | A variable-rate HELOC may be cheaper if rates fall. |

| Are you comfortable with the lender being a credit union (RenoFi) versus a direct fintech (Figure)? | Both options remain viable. | Lean toward the model you trust. |

If you answered five or more of these confidently, you have enough inputs to start lender-specific verification and compare quotes. If three or more are still unclear, run the Feasibility Engine first.

Pull together your zip code, equity position, and ADU plan in under 60 seconds. Free, no credit pull.

Frequently asked questions

Is RenoFi a lender?

No. RenoFi is a renovation finance broker (Renovation Finance LLC, NMLS #1802847) that originates HELOCs and home equity loans through partner credit unions. The credit union holds the note, services the loan, and handles all post-closing questions. RenoFi's role is sourcing, packaging, and matching borrowers to partner lenders.

Is the Figure HELOC legitimate?

Yes. Figure Lending LLC (NMLS #1717824) is a licensed direct lender headquartered in Reno, Nevada, founded in 2018. The parent company, Figure Technology Solutions, is publicly traded on Nasdaq. Whether the product is right for your specific situation is the actual decision to evaluate.

Does RenoFi let you borrow against future home value?

Yes. RenoFi's partner credit unions underwrite loans based in part on the projected after-renovation value (ARV) of the home. Bankrate's May 2026 review describes the cap as up to 95% of ARV; RenoFi's own homepage cites up to 90% of ARV and up to 125% of current home value depending on partner program. The credit union — not RenoFi — holds the underwriting decision.

Does Figure require you to draw 100% of the line at closing?

Yes. Figure funds the entire approved line into the borrower's bank account at closing, and interest accrues on the full balance from day one. Additional draws are permitted during the 3-to-5-year draw window as the initial balance is repaid, with each draw locking in the lender's rate at the time of that draw.

Which is faster, RenoFi or Figure?

Figure is faster. Figure advertises funding initiated in as few as 5 days from a complete application. Per RenoFi's own FAQ, RenoFi's process generally takes 30–60 days after documents are collected, and the company does not guarantee approval or timing.

What is the minimum credit score for each?

For Figure, third-party sources currently differ: NerdWallet lists 600; Credit Karma describes minimum qualification requirements as generally 600 (with 660 on investment properties); LendEdu lists 640. Verify the current minimum directly with Figure. RenoFi's minimum varies by partner credit union, typically in the 640+ range, with the best terms at 720+.

What is the maximum loan amount?

Both products advertise maximums up to $750,000 for the most qualified borrowers. Loans above $400,000 with Figure may require a full appraisal in addition to the standard automated valuation.

Are these products available for investment properties?

RenoFi's ARV product is structured primarily for primary residences and second homes; partner lenders may offer current-value products for investment property. Figure HELOCs may be available for primary residences, secondary residences, and investment properties per Credit Karma's review, with different minimum-credit-score requirements for each. Verify investment-property eligibility directly with Figure for the current product.

What happens if my ADU appraisal comes in lower than expected?

Your borrowing capacity is recalculated against the lower ARV, and you may not be able to borrow as much as your initial plan assumed. Never commit to a contractor deposit or non-refundable plans-and-permits costs based on borrowing capacity you haven't verified through an actual appraisal.

Will building an ADU affect my property taxes?

Yes, in most jurisdictions the new ADU construction is added to the property tax roll at its current assessed value. Per the California State Board of Equalization, new construction is generally assessable in California; under Proposition 13, the original primary residence retains its protected base-year value and only the ADU addition is assessed at current value. Check with your county assessor for your jurisdiction.

What we verified

Verified on May 21, 2026. If you’re reading this more than 90 days after this date, treat lender-specific terms as starting points and reconfirm with the lender directly.

| Verified fact | Source | Last checked |

|---|---|---|

| RenoFi is a broker, not a lender; loans made through partner credit unions | RenoFi how-it-works page and FAQ (renofi.com) | May 21, 2026 |

| RenoFi ARV cap up to 95% per Bankrate; up to 90% per RenoFi homepage; up to 125% of current home value | Bankrate Best HELOC Lenders (May 2026); RenoFi homepage and product pages | May 21, 2026 |

| RenoFi state exclusions: Hawaii, New York, Massachusetts | Bankrate RenoFi Review (Feb 27, 2026); RenoFi how-it-works disclosures | May 21, 2026 |

| RenoFi Texas exclusion per wholesale documentation | RenoFi wholesale doc (2025) — retail status flagged for direct re-verification | May 21, 2026 |

| RenoFi timeline 30–60 days; no committed approval or timing | RenoFi FAQ (renofi.com/faq/) | May 21, 2026 |

| Figure 100% draw at closing; 3-to-5-year draw window | NerdWallet Figure HELOC Review (updated May 6, 2026); Credit Karma Figure HELOC Review | May 21, 2026 |

| Figure offers fixed and variable rate options | Credit Karma Figure HELOC Review; NerdWallet Figure HELOC Review | May 21, 2026 |

| Figure repayment terms: 10, 15, 20, 30 years | Credit Karma Figure HELOC Review | May 21, 2026 |

| Figure origination fee up to 4.99% | NerdWallet (May 2026); CNBC Select (April 2026); LendEdu (May 2026) | May 21, 2026 |

| Figure not available in Hawaii | CNBC Select Figure Review (April 2026); NerdWallet Figure HELOC Review (May 2026) | May 21, 2026 |

| Figure New York exclusion via FAQ for Home Equity Line application | Figure HELOC FAQ (figure.com/faqs/home-equity-line/) | May 21, 2026 |

| Figure minimum loan amounts: $10,000 most states; $25,001 Alaska; $35,000 Texas | Figure/Lowe's HELOC partner disclosure | May 21, 2026 |

| Figure max line up to $750,000; loans over $400K may require appraisal | NerdWallet Figure HELOC Review (May 2026) | May 21, 2026 |

| National HELOC rate environment: 7.26% Bankrate (May 6, 2026); 7.21% Curinos (May 20, 2026); Fed held in March, April, and May 2026 | Bankrate national HELOC survey; Curinos via Yahoo Finance; Bankrate Fed coverage | May 21, 2026 |

| HELOC general risks (collateral, payment shock, line freeze/reduction) | CFPB HELOC consumer guidance (consumerfinance.gov/ask-cfpb/) | May 21, 2026 |

| HELOC interest tax deductibility framework | IRS Publication 936 (irs.gov/publications/p936) | May 21, 2026 |

| California new construction assessment / Prop 13 framework | California State Board of Equalization (boe.ca.gov) | May 21, 2026 |

| ADU cost ranges and hidden-cost categories | The Dwelling Index ADU cost dataset; cross-checked against builder bid data | May 21, 2026 |

Methodology

We built this comparison by combining each lender’s first-party product disclosures, third-party review data from publications that update their numbers regularly (Bankrate, NerdWallet, CNBC Select, LendEdu, Credit Karma), primary-source consumer-protection and tax guidance (CFPB, IRS, California BOE), and our own ADU cost dataset.

For the borrowing-power matrix, we used conservative formulas: 80% LTV on the current-equity (Figure) side, and the 90% ARV cap with the 125%-of-current-value secondary cap on the RenoFi side. Every scenario is illustrative and disclosed as such — none represents a loan quote, approval, or guarantee. Actual borrowing capacity will fall within or below these ranges based on your credit, income, DTI, lien position, property type, appraisal results, and lender overlays.

For the dead-interest calculation, we modeled the standard 4-milestone ADU draw schedule against Figure’s 100%-draw-at-closing requirement, then sensitivity-tested with the offset of parking unused funds in a 4% high-yield savings account. The resulting net cost of $2,500–$6,000 on a $250K HELOC over an 8-month build is the calculation we surface in the body.

Where sources disagreed on a specific data point, we cited the range and flagged the source — most prominently on RenoFi’s 90% vs 95% ARV cap and Figure’s minimum credit score. The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. Editorial conclusions on this page are formed from the verified facts cited above; they are never influenced by compensation.

Final word

The honest comparison is not “which is better” — it’s “which is structurally designed for your situation.” Recent buyer with a big plan and limited equity? Start with RenoFi’s ARV path and pressure-test the appraisal early. Long-tenured owner with substantial equity and a builder slot opening next month? Figure’s speed advantage is real. Project that exceeds both products’ realistic reach, or in a state that excludes one or both? Pivot to construction loans, conventional renovation products, or your local credit union — and don’t force a fit that wasn’t designed for you.

The most expensive mistake we see in ADU financing is the homeowner who picks a product based on marketing language, signs application paperwork, gets a quote that doesn’t match the marketing language, and finds out three months in that the project is underfunded with deposits already paid. That’s avoidable. Run the math first.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU ReportFull affiliate disclosure

The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. We are not currently in an affiliate or referral relationship with RenoFi or with Figure, and earn no commission if you apply with either. We maintain affiliate relationships with Mortgage Research Center for broader mortgage, refinance, cash-out refinance, and construction-loan content, and with other partners listed elsewhere on this site. Our editorial conclusions are formed from the verified facts cited above and are never influenced by compensation. Nothing on this page is financial, legal, or tax advice. Loan products, rates, fees, and state availability change frequently. Verify current terms directly with any lender before applying.

Sources

- Bankrate — Current HELOC Rates In May 2026 (bankrate.com/home-equity/heloc-rates/)

- Bankrate — Best HELOC Lenders In May 2026 (bankrate.com/home-equity/heloc-lenders/)

- Bankrate — RenoFi: 2026 Home Equity Review (Feb 27, 2026) (bankrate.com/home-equity/reviews/renofi/)

- NerdWallet — Figure HELOC Review (updated May 6, 2026) (nerdwallet.com/mortgages/reviews/figure-heloc-review)

- CNBC Select — Figure HELOC Review (April 2026) (cnbc.com/select/figure-heloc-review/)

- LendEdu — Figure HELOC Review (May 2026) (lendedu.com/blog/figure-home-equity-loan-review/)

- LendEdu — RenoFi Review 2026 (lendedu.com/blog/renofi-review/)

- Credit Karma — Figure HELOC Review (creditkarma.com/home-loans/i/figure-heloc-review)

- Figure — Home Equity Line FAQ (figure.com/faqs/home-equity-line/)

- Figure / Lowe's — HELOC partner disclosure (lowes.com/l/Credit/Figure)

- RenoFi — Homepage and how-it-works (renofi.com)

- RenoFi — FAQ (renofi.com/faq/)

- RenoFi — Wholesale documentation (renofi.com/wholesale/)

- Consumer Financial Protection Bureau — HELOC consumer guidance (consumerfinance.gov/ask-cfpb/)

- IRS — Publication 936, Home Mortgage Interest Deduction (irs.gov/publications/p936)

- California State Board of Equalization — New construction property tax guidance (boe.ca.gov/proptaxes/newconstructionproperty.htm)

- Patelco Credit Union — ADU HELOC product (patelco.org/credit-cards-and-loans/home-equity/adu-line-of-credit)

- Yahoo Finance / Curinos — HELOC and home equity loan rates (May 2026)