Figure HELOC Review 2026: Is It Actually a Good Way to Finance an ADU?

Last updated: May 21, 2026 · Last verified: May 21, 2026 · By the Dwelling Index Editorial Team

The bottom line on Figure HELOC for ADU financing

Figure can be a workable way to pay for an ADU — but only if your project will actually spend most of the loan within a few months of closing. Figure describes itself as the #1 non-bank HELOC lender in America, and NerdWallet ranks it the fourth-largest HELOC lender in the country by 2024 origination volume. Funding can be initiated in as few as five days, and lines run up to $750,000 at up to 85% combined loan-to-value. The catch most reviews bury: Figure requires you to draw 100% of the approved line at closing, minus the origination fee. From day one, you pay interest on the full amount — whether your contractor has broken ground or not.

Who this answer applies to: U.S. homeowners considering Figure to pay for an accessory dwelling unit, in states where Figure’s own application channel is authorized. One key number: Figure’s origination fee can reach 4.99% of your full initial draw — that’s up to $14,970 on a $300,000 line, paid whether you spend the money in week one or in year two. Next step: Confirm your ADU is actually buildable before you borrow against your home.

At-a-glance verdict table

| Question | Bottom line | Verified |

|---|---|---|

| Is Figure legit? | Yes. Figure Lending LLC (NMLS #1717824) is a direct lender founded in 2018, BBB A+ accredited since April 25, 2025, and 4.8/5 on Trustpilot across 4,301 reviews as of May 21, 2026. | NerdWallet, BBB, Trustpilot |

| Is it a normal HELOC? | No. Figure funds 100% of the approved line at closing, minus origination fee — more like a home-equity loan with redraw access during a shortened 2–5 year draw period. | Figure HELOC guide; NerdWallet; CNBC Select |

| Best ADU fit | Garage conversion or ready-to-build attached/detached ADU with permits in hand and a firm contractor contract. | Dwelling Index analysis |

| Weak ADU fit | Early feasibility, long permit queues, soft-cost-only spending, or homeowners who want true draw-as-needed control. | Dwelling Index analysis |

| State availability | 49 states + D.C. per Figure’s marketing; not in Hawaii. New York has a partner-channel caveat — figure.com is not authorized by NY DFS for direct applications; verify current channel. | Figure disclosure; Figure Oct. 2024 announcement |

| State minimums | $15,000 standard; $25,001 in Alaska; $35,000 in Texas. | Figure disclosure footnote #5 |

| Loan amount range | $15,000 to $750,000, subject to home value, lien position, credit profile, verified income, and equity. Loans above $400,000 require full appraisal. | Figure disclosure #5; CNBC Select |

| Origination fee | Up to 4.99% of the initial draw, varying by state and credit profile. Figure offers a fee-for-rate trade-off where a higher origination fee buys a lower APR. | Figure disclosure #6; CNBC Select |

| Funding speed | As few as 5 business days assuming remote online notary, loan under $400,000, and no county/state restriction on e-signatures. | Figure disclosure #2 |

| Active lawsuit | Ward v. Figure Lending, LLC (Case No. 3:24-cv-00533, W.D.N.C., filed June 5, 2024) — allegations only; case ongoing. An earlier similar complaint was dismissed with leave to amend in Arizona in August 2023. | Law360; National Mortgage News; Justia |

| Biggest caution | Your home is collateral. CFPB warns that falling behind on a HELOC can result in losing your home. | Consumer Financial Protection Bureau |

See what you can build → Get your free ADU report.

Before you borrow against your house, confirm your lot can actually support the ADU you want. Our Feasibility Engine pulls local zoning and lot data so you don’t borrow $300,000 for a project a 20-foot side setback would have killed. Free, no credit pull.

Get Your Free ADU Report →

What we verified for this Figure HELOC review

We are an independent research resource covering ADU financing, costs, and regulations. For this review we verified product terms, complaint patterns, legal status, and ADU cost context between May 17–21, 2026:

| Claim category | Primary source |

|---|---|

| Full initial draw, $750K cap, 10/15/20/30-yr terms, 5-day funding, redraw mechanics | Figure HELOC guide and calculator (figure.com); Figure disclosure footnotes #1, #2, #5, #8 |

| Origination fee up to 4.99%, $15K minimum draw, $25,001 minimum in Alaska, $35,000 minimum in Texas, AVM/appraisal/notarization/recording fee ranges, $400,000 appraisal threshold | Figure HELOC disclosures #5 and #6 |

| State availability and NY caveat | Figure HELOC disclosure (state list); Figure October 22, 2024 newsroom announcement |

| No account-opening, maintenance, prepayment, inactivity, early-closure, or minimum-withdrawal fees | Figure blog: “Understanding HELOC Closing Costs” |

| BBB A+ accreditation since April 25, 2025; Trustpilot 4.8/5 across 4,301 reviews | BBB Business Profile; Trustpilot, figure.com profile (verified May 21, 2026) |

| Customer-experience score 2.49/5 vs. editorial score 4.5/5 | Bankrate Figure home equity review (Dec 23, 2025) |

| Ward v. Figure Lending, LLC (3:24-cv-00533, W.D.N.C., filed June 5, 2024); prior 2023 Arizona filing dismissed with leave to amend | Law360, National Mortgage News, HELN News, ClassAction.org; Justia and PacerMonitor |

| 4th-largest HELOC lender 2024; $19B+ originated since 2018 | NerdWallet Figure HELOC review (Jan 2026); Bankrate (Dec 2025) |

| ADU as a Figure-cited customer use case | Figure Technology Solutions press release, October 22, 2024 |

| HELOC consumer-risk and collateral guidance | Consumer Financial Protection Bureau HELOC consumer brochure |

| ADU cost ranges: garage conversion, attached, detached, prefab | Angi 2026 (total cost only); SelfStorage.com 2026; Silver Hammer Builders LA 2026; GatherADU 2026 California guide |

Editorial note: Rates, fees, state availability, and lawsuit status change. Verify current Figure terms directly before applying. Editorial conclusions are not loan offers, financial advice, or approval guarantees.

Is Figure HELOC legit?

Yes. Figure Lending, LLC (NMLS #1717824) is a direct lender founded in 2018, headquartered in Charlotte, North Carolina. It is BBB-accredited with an A+ rating since April 25, 2025. Figure positions itself as the #1 non-bank HELOC lender in America; NerdWallet’s January 2026 review describes Figure as the fourth-largest HELOC lender in the country by 2024 origination volume, with Bankrate reporting more than $19 billion in cumulative home-equity originations since 2018. Trustpilot shows 4.8 out of 5 stars across 4,301 reviews as of May 21, 2026.

Legitimacy isn’t the right question for most ADU borrowers. Figure is a real lender with real volume and real customer reviews. The better question is suitability: whether the product mechanics fit your specific project. Three things determine whether Figure is a fit at all:

- Your state. Figure’s HELOC isn’t available in Hawaii. New York has a partner-channel caveat covered below.

- Your equity. Figure caps combined loan-to-value at 85%. If your home is highly leveraged, the math may not work.

- Your draw schedule. This is the big one. Figure’s “HELOC” funds 100% of the line at closing. If your project doesn’t spend most of that money quickly, you’re paying interest on idle cash.

How Figure’s HELOC actually works (and why it matters for ADUs)

Figure’s product is technically a home-equity line of credit, but its initial funding behaves more like a lump-sum home-equity loan than what most consumers picture when they hear “HELOC.” Figure funds the entire approved line at closing, minus the origination fee. As you repay principal, you can request additional draws during a draw period that lasts only two to five years — about half the ten years most traditional HELOC lenders offer. Each additional draw is priced at Figure’s then-current rate.

This is the single most important paragraph in any Figure review, and most pages bury it under marketing copy.

The “full draw at closing” rule, in plain English

A traditional HELOC works like a credit card secured by your house. You get approved for, say, $250,000. You take $20,000 to pay your architect, $40,000 when permits clear, $80,000 for foundation and framing, and so on. You pay interest only on what you’ve drawn, when you’ve drawn it.

Figure does not work that way. If Figure approves you for $250,000, the entire $250,000 is funded into your account at closing, minus the origination fee. From day one, you are paying interest on the whole amount — even if your ADU project is months away from breaking ground.

Figure’s own disclosure language confirms this: the Figure Fixed Rate Home Equity Line is described as “an open-end product where the full loan amount (minus the origination fee) will be 100% drawn at the time of origination.” This isn’t a hidden term — it’s stated outright in the disclosure — but it’s easy to miss when “HELOC” is the headline and “100% drawn at origination” is in the footnotes.

Initial draw vs. additional draws

Once you’ve repaid some principal, you can request additional draws during the draw period. Two things to understand:

- Additional draws may carry a different rate than your initial draw. The fixed rate you locked in on day one applies to the initial draw only; future draws are priced at Figure’s then-current rate, indexed to the Wall Street Journal Prime Rate plus margin.

- The draw period is short. Figure’s draw window is two to five years. For comparison, most traditional HELOCs offer a ten-year draw period. For ADU projects with long permit timelines, this compressed window can become a real constraint.

Speed, appraisal, and the $400,000 inflection point

Figure can fund in as few as five business days — but that timeline assumes:

- The loan closes via Figure’s remote online notary process.

- The loan amount is under $400,000 (above that, a full appraisal is required, adding days or weeks).

- The property is in a county and state that permits e-signature recording and remote closings.

- Loans above $400,000 require a full appraisal ($500–$2,000 depending on property type, value, and state).

- Manual notarization: If your county doesn’t permit eNotary, you’ll pay around $350. Recording fees ($0–$315) and recording taxes ($0–$1,400 per $100,000 borrowed) vary widely by state and county.

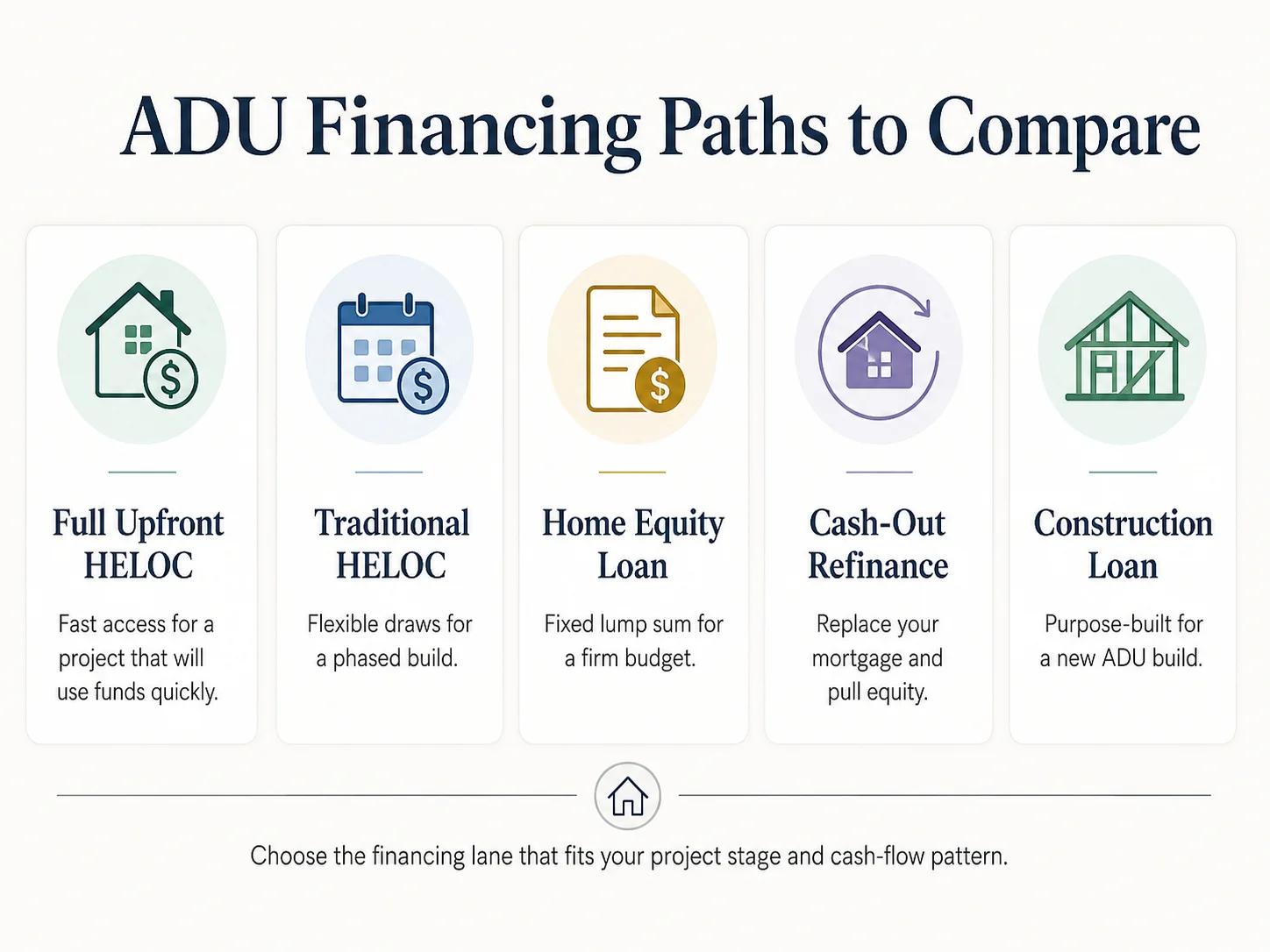

Figure HELOC vs. traditional HELOC vs. home-equity loan, side by side

| Feature | Figure HELOC | Traditional HELOC | Home-equity loan |

|---|---|---|---|

| Initial funding | Full approved line at closing, minus origination fee | Draw as needed during draw period | Lump sum at closing |

| Draw period | 2–5 years | Typically 10 years | N/A (one-time disbursement) |

| Rate type on initial funds | Fixed (or variable on Figure Variable Rate product) | Usually variable; some lenders offer fixed-rate locks on portions | Fixed |

| Rate type on additional draws | Fixed at Figure’s then-current rate (indexed to WSJ Prime + margin) | Variable, indexed to prime | N/A |

| Origination fee | Up to 4.99% of initial draw | Varies; often $0 at major banks | Varies by lender |

| Best ADU fit | Permits-in-hand, ready-to-build project with firm contract | Phased ADU construction across multiple invoices | Firm fixed ADU budget, lump-sum need |

| Main ADU risk | Paying interest on borrowed money your ADU isn’t spending yet | Variable rate could rise during construction | Over- or under-borrowing if scope changes |

The Figure approach can be the right answer when your contractor is signed, your permits are issued, and your first major draw request is sitting on the desk. It’s the wrong answer when you’re months away from a plan-check decision and the money is sitting in your account accruing interest.

Figure HELOC fees, rates, limits, and state rules

Figure HELOC fees center on a single big number: an origination fee of up to 4.99% of your initial draw, deducted from your funds at closing. Beyond that, expect potential AVM or appraisal costs, manual-notarization costs where eNotary isn’t allowed, recording fees, and recording taxes. Figure does not charge account-opening fees, maintenance fees, prepayment penalties, inactivity fees, early-closure fees, or minimum-withdrawal fees. Loan amounts range from $15,000 to $750,000 with up to 85% combined loan-to-value. State minimums: $25,001 in Alaska and $35,000 in Texas.

The origination fee, decoded

- Maximum origination fee: 4.99% of your initial draw amount.

- The fee varies by state and credit profile.

- You can trade a higher origination fee for a lower APR — Figure explicitly offers this fee-for-rate option.

What this means on a real ADU budget:

| Initial draw | 4.99% origination fee | 3.00% origination fee | 1.00% (for comparison) |

|---|---|---|---|

| $100,000 | $4,990 | $3,000 | $1,000 |

| $200,000 | $9,980 | $6,000 | $2,000 |

| $300,000 | $14,970 | $9,000 | $3,000 |

| $400,000 | $19,960 | $12,000 | $4,000 |

On a $300,000 ADU build, the difference between a 4.99% and a 1.00% origination fee is nearly $12,000. That fee is paid out of your funding, so a $300,000 approved line at 4.99% means you walk away with $285,030 to actually spend on the ADU.

Other potential costs

- AVM valuation fee: $180 if Figure’s automated valuation model can’t be used.

- Full appraisal: $500–$2,000 for loans exceeding $400,000 or where AVM isn’t available.

- Manual notarization: $350 if your county doesn’t permit eNotary.

- Recording fees: $0–$315, varying by jurisdiction.

- Recording taxes: $0–$1,400 per $100,000 borrowed. New York borrowers should price this carefully — recording taxes there are among the highest in the country.

- Property insurance: Required; flood insurance may be required if your property is in a flood zone.

What Figure does not charge

- Account-opening fees

- Maintenance fees

- Prepayment penalties

- Inactivity fees

- Early-closure fees

- Minimum-withdrawal fees on additional draws

There is a minimum draw amount of $500 on additional draws ($4,000 in Texas). If you pay off the line early to refinance into a construction loan later, you’re not penalized for it — a real advantage over some bank HELOCs that impose early-closure fees.

Loan amount, equity math, and CLTV

Figure’s published maximum is $750,000. The actual amount you can borrow is the smaller of Figure’s program maximum for your state and profile, and the amount your equity supports at up to 85% CLTV.

A worked example: Home value $800,000 · Current mortgage $400,000 · 85% CLTV = $680,000 ceiling · Available equity: $680,000 − $400,000 = $280,000. That’s the ceiling — not an approval. Actual approval depends on credit score (minimum 600 per SuperMoney’s Figure disclosure), DTI up to 50%, income documentation, property type, and Figure’s then-current underwriting.

State-by-state availability and the New York caveat

| State | Available? | Minimum draw | Notes |

|---|---|---|---|

| 47 states + D.C. | Yes via figure.com | $15,000 | Standard terms apply |

| Alaska | Yes | $25,001 | State-specific minimum per Figure disclosure footnote #5 |

| Texas | Yes | $35,000 | $4,000 minimum on additional draws (vs. $500 elsewhere); unique constitutional limits on home-equity lending |

| New York | Partner channels only | Verify | Figure.com not authorized by NY DFS for direct applications; available through licensed lender partners announced October 2024. Verify current channel. |

| Hawaii | No | — | Figure does not lend in Hawaii |

Run the Figure HELOC ADU Fit Check.

Plug in your state, home value, current mortgage, and ADU budget, and we’ll estimate your equity ceiling at 80% and 85% CLTV, flag whether the full-draw structure matches your project timeline, and tell you which financing paths to compare before applying. Educational tool, not a loan offer.

Check ADU Feasibility First →Why Figure’s full upfront draw matters for ADU construction

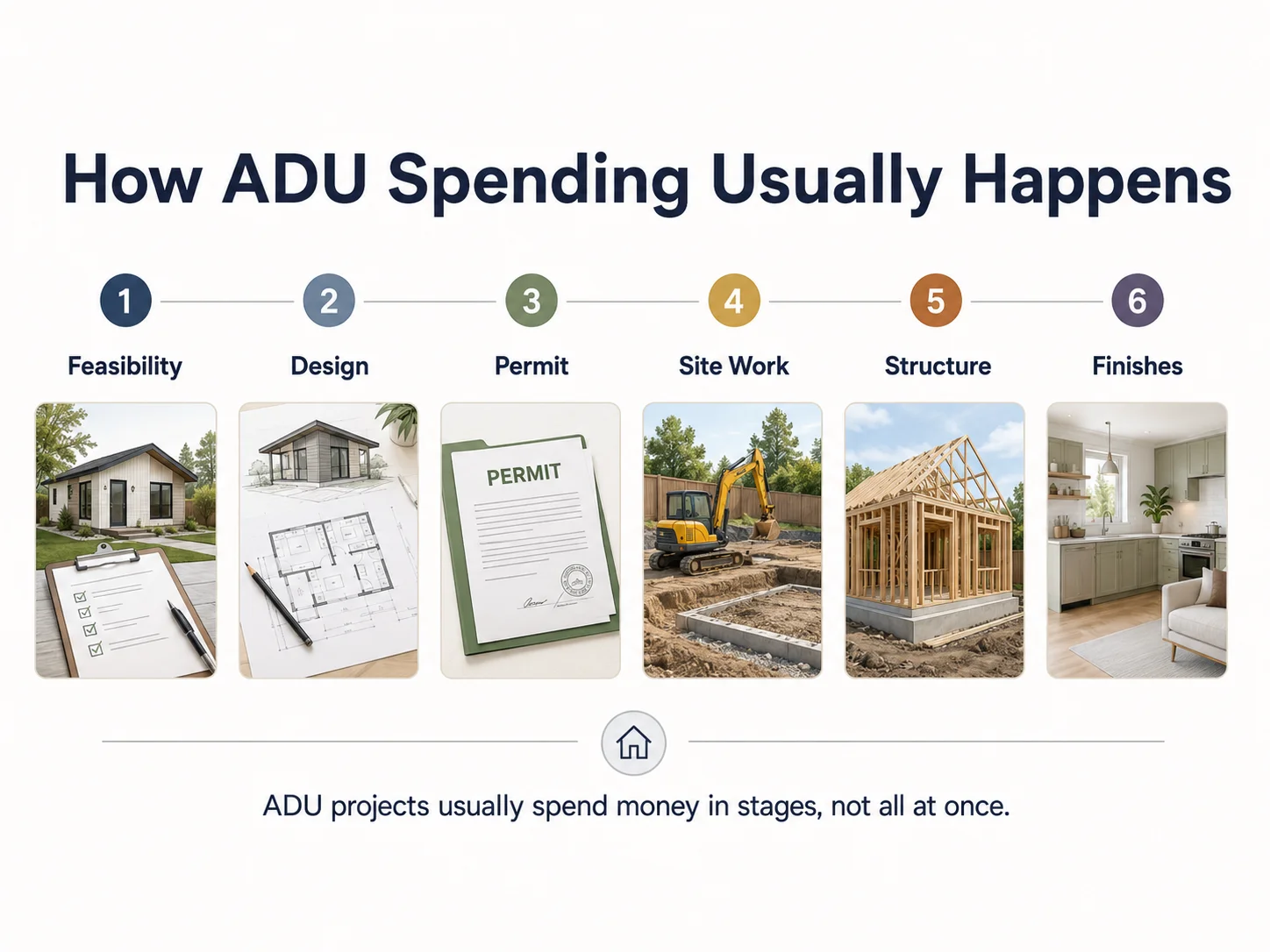

ADU construction spends money in distinct stages over 12–36 months. Figure funds you in one lump sum on day one. That mismatch creates a real, calculable cost — interest paid on borrowed money your ADU isn’t using yet — and it’s the central reason a Figure HELOC fits some ADU projects beautifully and others poorly.

A typical ADU spending timeline (Dwelling Index modeled)

| Month | Stage | % of budget spent (cumulative) |

|---|---|---|

| 1–2 | Feasibility, survey, site analysis | 1–3% |

| 2–5 | Design, engineering, structural | 5–10% |

| 4–8 | Permit application, plan check, revisions | 8–12% |

| 6–10 | Permit issuance, utility planning, contractor mobilization | 12–18% |

| 8–14 | Site work, foundation | 25–40% |

| 12–18 | Framing, rough mechanical/electrical/plumbing | 50–65% |

| 16–22 | Drywall, finishes, fixtures | 75–90% |

| 20–24 | Final inspections, certificate of occupancy | 100% |

Dwelling Index modeled estimates assembled from contractor draw schedules, typical permit-process steps, and standard construction-finance milestone payment patterns. Your actual timeline will vary by jurisdiction, project complexity, and contractor billing structure.

The idle-cash problem, with numbers

Assume you take a $300,000 Figure HELOC at 9% APR for a 15-year detached ADU build, full draw at closing, project takes 18 months from closing to substantial completion. Your monthly interest accrual on the full $300,000 is roughly $2,250.

In month 3 you’ve used maybe $20,000 of it. The remaining $280,000 is sitting in your account, accruing interest at $2,100 per month — interest you could have avoided with a draw-as-needed HELOC or a construction loan that funds against contractor invoices. Over the first six months of an 18-month build, this idle-cash interest can easily run $8,000–$12,000.

When the full upfront draw is actually a feature, not a bug

A homeowner in San Diego signs a fixed-price contract for a 600 SF garage conversion. Plans are already approved, permits are issued, and the contractor needs: 10% deposit at signing, 25% at mobilization, 30% at rough framing/MEP, 25% at substantial completion, 10% at final inspection. The whole project runs five months. By month four, roughly 90% of the budget is deployed.

In that scenario, Figure’s structure becomes a feature. You’ve locked in certainty that the full project budget is funded, front-loaded the underwriting and closing work, and don’t have to manage draw requests with a bank during a fast-moving build.

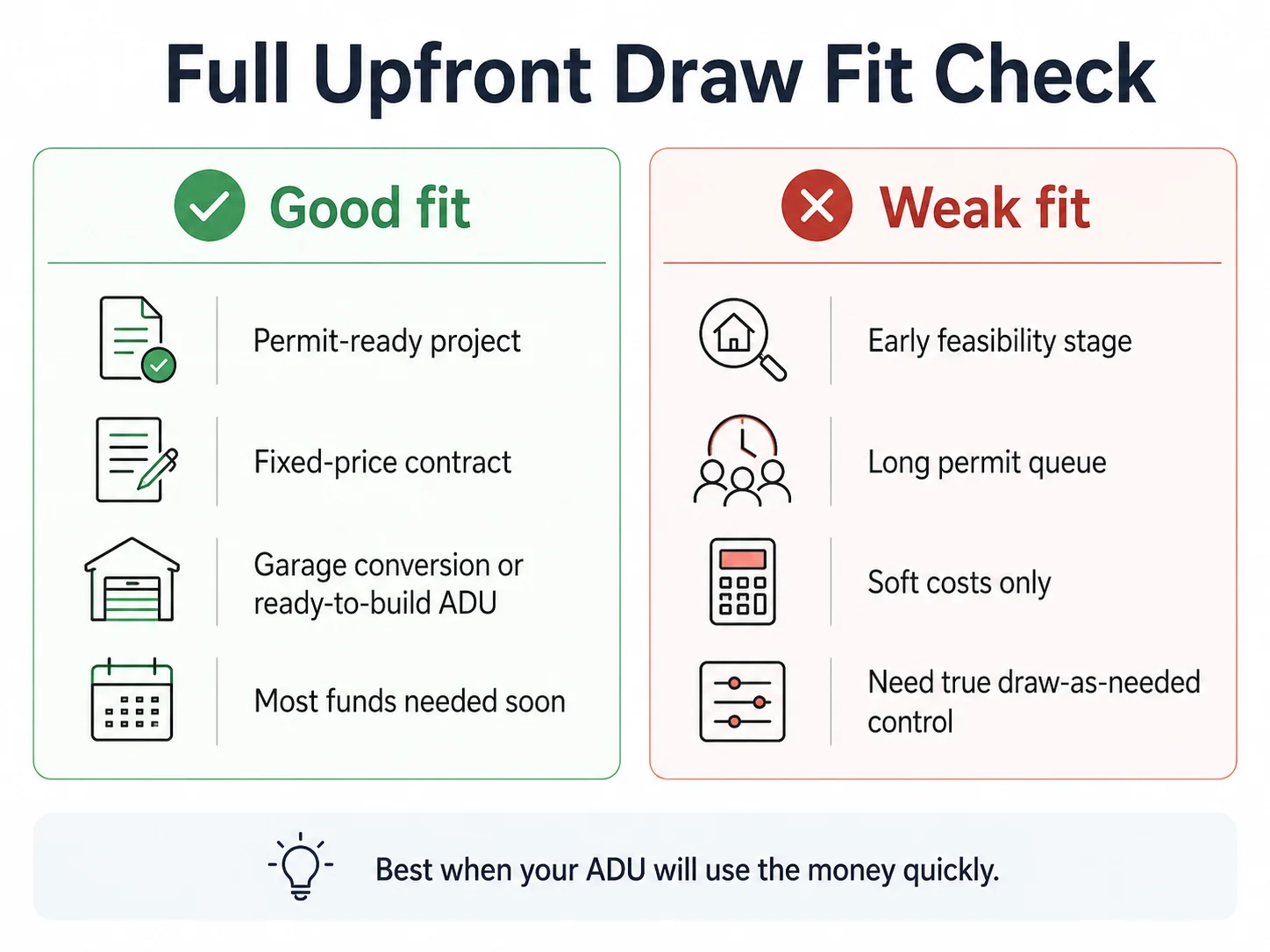

The Figure HELOC × ADU Draw-Fit Matrix

Not every ADU project is a good Figure candidate. We assembled this matrix from current ADU cost data, Figure’s product mechanics per published disclosures, and the draw-schedule analysis above. Use it as a starting point.

Methodology note: Fit labels are assigned based on four factors: (1) project stage at loan application; (2) how quickly funds will likely be deployed; (3) carrying-cost exposure from Figure’s full-draw structure; and (4) whether the project budget is within Figure’s 85% CLTV equity ceiling. “Good” fits clear all four. “Weak” fits fail one or more critical factor.

| ADU project type | Typical national cost range | Figure fit | Why |

|---|---|---|---|

| Early feasibility only | $3,000–$15,000 | Weak | Too small for a $15K minimum draw. Use savings or a personal loan. |

| Plans + permits only (no construction yet) | $10,000–$30,000 | Weak to poor | If construction is more than 6 months out, you’re paying interest on borrowed money the ADU isn’t spending. |

| Garage conversion ADU | $60K–$150K national; $80K–$200K+ San Diego; $100K–$175K CA two-car | Mixed to good | Defined scope, often permits-ready, 4–8 month build, contractor draws cluster early. |

| Attached ADU | $150,000–$300,000 | Good if budget is firm | Shared utilities accelerate the schedule. Full draw works if construction starts within 30–60 days of closing. |

| Detached ADU (new construction) | $200K–$400K national; $375–$600/SF West Coast | Mixed | Good fit if permitted and shovel-ready; weak if permitting may take months. A construction loan often beats Figure here. |

| Prefab / modular ADU | $80,000–$250,000+ depending on model and site work | Mixed to good | Factory build compresses timeline once permits clear. Pay factory deposit and milestone draws quickly. |

| High-cost detached ADU above $400K | $400,000+ in coastal CA, NYC metro, parts of Northeast | Mixed to weak | Figure requires full appraisal above $400K and longer timeline; consider a construction loan instead. |

| ADU primarily for rental income | Varies by ADU type | Depends on payment math | Don’t assume rent will cover the payment. Underwrite as if the unit sits empty for 3–6 months. |

| ADU for aging-in-place / multigenerational housing | Varies by ADU type | Depends on cash flow | No rental offset means the household carries the full payment. Confirm DTI works without that income. |

Illustrative cost ranges from cited public sources — actual ADU costs vary by location, lot conditions, finishes, contractor pricing, utility hookups, and permit fees. Verify a real budget with at least two local builders before borrowing.

See what you can build → Get your free ADU report.

Confirm your lot supports the ADU type you’re pricing before you sign for a HELOC. Our Feasibility Engine reads local zoning rules and gives you a buildable envelope and rough cost range in about 60 seconds. Free, no credit pull.

Get Your Free ADU Report →Compare mortgage and refinance-based ADU funding options.

For cash-out refinance or construction loan alternatives to Figure, compare current rate offers from multiple lenders.

Educational only — not a loan offer; eligibility and terms depend on your situation, state, and lender underwriting.

What the Ward v. Figure Lending lawsuit actually alleges

On June 5, 2024, plaintiff Lee Ward filed a proposed class-action complaint against Figure Lending, LLC in the U.S. District Court for the Western District of North Carolina (Ward v. Figure Lending, LLC, Case No. 3:24-cv-00533). The complaint alleges that Figure markets home-equity loans as HELOCs in what the plaintiff calls an “automated bait-and-switch scheme,” and challenges the requirement that borrowers draw the full approved line at closing. These are allegations, not findings. The case remains active. A nearly identical earlier complaint was dismissed with leave to amend in the U.S. District Court for the District of Arizona in August 2023 before being refiled in North Carolina in 2024.

The core allegations

According to court filings and reporting in Law360, National Mortgage News, ClassAction.org, and HELN News:

- The complaint contends that Figure’s marketing describes a HELOC, but the product functions as a home-equity loan because the entire approved amount is funded at closing.

- It alleges this results in higher origination fees and interest costs than a borrower expecting a true draw-as-needed HELOC would face.

- It cites consumer complaints filed with the BBB and CFPB describing applicants who say they were initially quoted favorable terms and then closed at higher rates or with different structures than expected.

- The complaint quotes the plaintiff’s own experience, alleging that when Ward applied in fall 2019, he was told his rate would be far below the 9.75% rate he was ultimately charged.

- Three proposed nationwide classes include borrowers who allegedly paid inflated payoff amounts based on inaccurate lender figures and borrowers assessed improper post-closing fees.

Procedural history

A nearly identical Ward complaint was originally filed in late 2022 in Georgia state court, removed to federal court, and then transferred to the U.S. District Court for the District of Arizona. In August 2023, Judge Steven P. Logan granted Figure’s motion to dismiss that complaint, with leave to amend. The case was refiled in the Western District of North Carolina in June 2024. According to Law360, Figure has urged the North Carolina court to dismiss the new complaint, arguing the plaintiff “is forum shopping with insufficient claims that have been dismissed in other courts.” The case is active; check the current docket for the latest status.

How to weight this if you’re considering Figure

What it signals

- The gap between consumer expectation of a “HELOC” and Figure’s full-draw structure is real enough to attract litigation.

- A meaningful number of consumers feel they were quoted one rate and closed at another — a pattern worth taking seriously.

- Read your closing documents carefully. Compare your initial quote to your actual closing terms line by line. If the rate has moved, ask why before you sign.

What it doesn’t signal

- A pending lawsuit is not a finding of wrongdoing. The earlier substantively similar filing was dismissed.

- Figure has originated more than $19 billion in HELOCs since 2018. Litigation involving one plaintiff does not establish a systemic pattern across that volume.

- BBB still maintains Figure as A+ accredited. Trustpilot’s 4.8/5 across 4,301 reviews sits above industry norms.

What customer reviews, BBB complaints, and Trustpilot signal

The customer-feedback picture for Figure splits sharply between platforms. Trustpilot shows 4.8/5 across 4,301 reviews as of May 21, 2026, with recurring themes of “fast, easy, painless.” BBB shows A+ accreditation since April 25, 2025 but a customer-review average closer to the low single digits out of 5, with complaints clustered around servicing and post-closing issues. Bankrate’s December 2025 review pegs the customer satisfaction score at 2.49/5 against an editorial score of 4.5/5. The pattern: smooth applications produce happy reviews; servicing and post-closing issues produce angry ones.

Trustpilot read

4.8/5 across 4,301 reviews as of May 21, 2026. Recurring positive themes: speed (funded in under two weeks), simplicity (fully digital, remote online notary), and loan officer responsiveness. We’re not quoting individual reviews — the aggregate rating is a directional signal that the application experience is genuinely good for most borrowers. Trustpilot does not fact-check the substance of individual reviews.

BBB read

BBB maintains Figure as A+ accredited since April 25, 2025. Important context: customer reviews are not used in calculating the BBB letter grade. Complaint and review patterns visible on BBB cluster around:

- Forced-placed insurance disputes: Borrowers describing repeated proof-of-insurance submissions while being billed for lender-placed insurance.

- Payoff discrepancies: Complaints about payoff amounts that don’t match borrower calculations — the same pattern alleged in the Ward lawsuit.

- Post-closing servicing: Borrowers describing difficulty reaching servicing teams after origination handoff.

- Rate surprise: Applicants who say the rate at closing differed from early quotes — the core pattern of the Ward lawsuit’s allegations.

These are complaint patterns, not a statistical frequency claim. Bankrate’s editorial review notes Figure’s customer satisfaction at 2.49/5 — considerably below the Trustpilot headline. The difference likely reflects selection bias (Trustpilot prompts satisfied customers; BBB attracts complaints). Read both.

Two ADU borrower scenarios, worked through

These are illustrative scenarios assembled from publicly available cost ranges and Figure’s published terms — not real, named clients. Your actual quote and project will vary.

Scenario A: The Figure-good case

- Homeowner profile (modeled): Couple in a San Diego County coastal city. Home worth $950,000, mortgage balance $410,000. Strong credit. Combined income comfortably above $200,000.

- ADU project: 720 SF garage conversion with a small detached addition, fixed-price contract estimated at $185,000. Plans approved, permits issued, contractor mobilizing in 30 days.

- Equity math: $950,000 × 0.85 = $807,500 CLTV ceiling. Minus $410,000 mortgage = $397,500 available. Project needs $185,000 — comfortably under the ceiling.

Why Figure fits: Permits already in hand. Contractor mobilizing in 30 days. The 5-month build will deploy most of the $185,000 within four months. Origination fee at say 3% is roughly $5,550 — annoying, but the speed and certainty buy peace of mind.

Honest tradeoff: They could get a lower origination fee at their local credit union but would likely wait 4–6 weeks for closing. Their contractor’s schedule won’t wait. Figure earns the premium.

Scenario B: The Figure-bad case

- Homeowner profile (modeled): Single homeowner in Austin, TX. Home worth $620,000, mortgage balance $280,000. Strong credit. Income $135,000.

- ADU project: 950 SF detached ADU, custom design, still in schematic phase. Architect bid $14,000. Estimated construction budget $310,000. Austin permitting timelines vary — verify current timing with Austin Development Services before choosing a full-draw loan.

- Equity math: $620,000 × 0.85 = $527,000. Minus $280,000 = $247,000 available — already short of the $310,000 project cost.

Why Figure fits badly:

- The $35,000 Texas minimum draw means she can’t take a small line for the architect fee alone.

- The current equity ceiling can’t fund the construction budget — she’d need future-value financing.

- A long permit runway means a full upfront draw would accrue interest for months before the contractor sees a major invoice.

- If construction runs 16–22 months, she’s pushing toward the end of Figure’s 5-year draw period before the ADU is complete.

Better path: Pay the architect fee in cash, run the permit process in parallel, and apply for a construction loan or renovation HELOC that underwrites against after-renovation value once she has approved plans and a real contractor bid.

Idle-cash interest comparison (illustrative, $310,000 at 9% APR, 16-month build):

| Period | Avg. unspent balance | Approx. idle interest |

|---|---|---|

| Months 1–4 | ~$280,000 | ~$8,400 |

| Months 5–8 | ~$200,000 | ~$6,000 |

| Months 9–12 | ~$110,000 | ~$3,300 |

| Months 13–16 | ~$30,000 | ~$900 |

| Total | ~$18,600 |

Illustrative calculations using a hypothetical 9% APR for math demonstration; actual savings depend on the rate gap between products, actual draw timing, and specific loan terms in each offer. Compare real offers from at least two lenders before deciding.

How to actually decide: a 7-step checklist

Not sure what to do next? Walk this in order. Each step removes a specific source of decision risk.

- Confirm your ADU is buildable on your lot. Pull your zoning, setbacks, FAR, and any HOA covenants. Run our Feasibility Engine for a 60-second buildable envelope.

- Pick an ADU type with a realistic budget range. Garage conversion ($60K–$150K national, higher in coastal CA), attached ($150K–$300K), detached ($200K–$400K+), or prefab/modular (varies).

- Get at least two preliminary bids from local builders. Don’t price an ADU off a national average. Local labor, materials, and permit costs vary materially between markets.

- Calculate your equity ceiling at 85% CLTV. (Home value × 0.85) − current mortgage balance. If that ceiling is less than your project budget plus contingency, you need future-value financing, not a current-equity HELOC.

- Match your financing path to your draw schedule. Full deployment within 6 months → Figure or home-equity loan can work. Staged build over 12+ months → traditional HELOC or construction loan.

- Apply to two lenders, not one. Even if Figure is your top pick, get a competing quote from your bank or credit union. The 4.99% origination fee gap is real money — leverage it.

- Read your closing documents line by line. Compare your final APR and origination fee against your initial quote. If anything moved, ask why. Do this before you sign anything.

Not sure where to start? Check ADU feasibility first → Get your free ADU report in 60 seconds.

Don’t borrow against your house for a project a 5-foot side setback or a $40,000 utility lateral can kill. Free, no credit pull.

Get Your Free ADU Report →What’s next

This Figure HELOC review covers Figure as one path among many. For deeper dives on the alternatives:

- HELOC vs construction loan for ADU — the full traditional HELOC playbook, draw schedules, lender comparison criteria

- Home-equity loan for ADU — when a fixed lump sum beats a line of credit

- ADU construction loan — future-value underwriting for larger detached builds

- Best ADU financing options — financing-lane overview if you’re still deciding

- Hometap vs HELOC for ADU — home-equity investment as a no-monthly-payment alternative

- How to finance an ADU with no equity — paths for new homeowners and low-equity scenarios

- Home-equity investment for ADU — HEI deep-dive with state availability matrices

- ADU financing without monthly payments — HEI products compared by state availability

- ADU loan vs HELOC — decode what “ADU loan” actually means

Get the Dwelling Index ADU Starter Kit

Before you sign for a HELOC against your home, get the decision frameworks we built for every stage of an ADU project — feasibility checklists, financing-path decision matrices, permit-process questions to ask your city, contractor-bid comparison templates, and the same cost benchmarks we used to verify the ranges in this review.

Download the Free ADU Starter Kit →Decision frameworks, cost calculators, and permit checklists from every state we’ve covered. Free, no credit card, no upsell.

Figure HELOC review FAQ

- Is Figure HELOC legit?

- Yes. Figure Lending, LLC (NMLS #1717824) is a real lender, BBB A+ accredited since April 25, 2025, and 4.8/5 on Trustpilot across 4,301 reviews as of May 21, 2026. NerdWallet describes Figure as the fourth-largest HELOC lender in the U.S. by 2024 origination volume, with Bankrate reporting more than $19 billion originated since 2018. Legitimacy is separate from suitability — verify state availability, current fees, and whether the full upfront draw fits your project.

- Is Figure really a HELOC if the full amount is drawn upfront?

- Figure markets and documents the product as a home-equity line of credit, but the initial funding mechanic differs from what most consumers picture when they hear 'HELOC.' Per Figure's own disclosure, 'the full loan amount (minus the origination fee) will be 100% drawn at the time of origination.' The 'line of credit' character comes from the ability to request additional draws during the 2–5 year draw period after repaying principal. A proposed class-action complaint (Ward v. Figure Lending, LLC) alleges this distinction makes the product effectively a home-equity loan; those are allegations, not findings.

- Can I use a Figure HELOC to build an ADU?

- Yes — Figure's October 2024 expansion announcement explicitly cites ADU builds as a customer use case. The more important question is whether Figure's full-draw structure fits your specific ADU's spending timeline. It fits permits-in-hand projects with firm contractor contracts; it fits poorly when permitting may take many months.

- How much can I borrow from Figure?

- Figure's published maximum is $750,000. Your actual amount depends on home value, current mortgage balance, credit, income, DTI, property type, and state. The arithmetic ceiling is (home value × 0.85) minus your current mortgage balance. Loans above $400,000 are subject to full appraisal per Figure's disclosure.

- Does Figure charge an origination fee?

- Yes. Up to 4.99% of your initial draw, depending on state, credit profile, and whether you're trading a higher fee for a lower APR. On a $300,000 line at 4.99%, that's $14,970 deducted from your funds at closing. Other potential costs include AVM fees ($180), full appraisal for loans above $400,000 ($500–$2,000), manual notarization where eNotary isn't permitted ($350), and state/county recording fees and taxes.

- Is Figure available in New York?

- It's nuanced. Figure announced expansion into New York and Delaware in October 2024 through its licensed lender partner network. At the same time, Figure's current direct-channel disclosure states that figure.com is not authorized by the New York State Department of Financial Services and that no mortgage applications for NY properties can be facilitated through figure.com itself. New York borrowers should verify the current application channel and state-specific terms before assuming national reviews describe their experience.

- Is Figure available in Texas? In Hawaii?

- Texas: yes, with a $35,000 minimum initial draw (vs. $15,000 in most states) and $4,000 minimum on additional draws. Texas has unique state-constitutional limits on home-equity lending; verify before applying. Hawaii: no. Figure does not lend in Hawaii.

- What's the state minimum in Alaska?

- $25,001 per Figure's HELOC disclosure footnote #5. If you've seen older reviews list Arkansas as having a higher minimum, that's incorrect — Figure's own disclosure specifies Alaska, not Arkansas.

- Is Figure better than a home-equity loan for ADU construction?

- It depends on whether you value the redraw option after initial repayment. If you want a true lump sum, no redraw, fully fixed payment, and a lower origination fee, a home-equity loan from a major bank is often simpler and cheaper. If you want a fast digital process and the option to draw additional funds during a 2–5 year window, Figure is worth comparing. If you need staged draws across a long construction timeline, a traditional HELOC or a construction loan is usually the better fit.

- What credit score do I need for Figure?

- Figure's published minimum is 600 per SuperMoney's Figure disclosure, with rates and approved amounts varying by credit profile. The lowest published APRs go to borrowers with credit scores around 780+ at low CLTV who also opt for a higher origination fee in exchange for a lower rate. Don't assume the lowest advertised rate applies to your file.

- What is the draw period on a Figure HELOC?

- Two to five years, depending on your loan term. This is roughly half the 10-year draw period most traditional HELOCs offer. For ADU projects with long permit timelines or staged construction over more than 24 months, this shortened window can become a meaningful constraint.

- What happens if I sell my home with an outstanding Figure HELOC balance?

- The balance is typically due in full at sale, paid from your sale proceeds at closing alongside your first mortgage. CFPB consumer materials cover this in detail. Confirm with Figure if your situation involves any complications such as transfer of ownership to a trust or sale at below-market value.

- Is there a pending lawsuit against Figure?

- Yes. Ward v. Figure Lending, LLC (Case No. 3:24-cv-00533, U.S. District Court, Western District of North Carolina, filed June 5, 2024) is a proposed class-action complaint alleging Figure markets home-equity loans as HELOCs in a 'bait-and-switch scheme.' Figure has urged dismissal, arguing forum shopping after an earlier substantively similar complaint by the same plaintiff was dismissed with leave to amend in Arizona federal court in August 2023. The case remains active. These are allegations, not findings of wrongdoing.

- What is the biggest risk of using any HELOC for an ADU?

- Your home is collateral. CFPB consumer guidance is explicit: if you can't repay a HELOC, you can lose your home. ADU rental-income projections are illustrative, not guaranteed — actual returns depend on local rental markets, vacancy, maintenance costs, financing terms, and regulatory approvals. Don't underwrite the loan on the assumption that the unit will be rented at full ask, on day one, for the entire term.

Methodology: how we reviewed Figure for ADU financing

We reviewed Figure Lending, LLC as an ADU financing path — not as a generic HELOC lender — because the structural mechanics of Figure’s HELOC interact with ADU construction draw schedules in ways generic reviews don’t address.

Sources verified May 17–21, 2026:

- Figure’s official HELOC guide, calculator, closing-cost blog, licensing pages, and October 2024 corporate announcements (NY/DE expansion).

- Figure’s published HELOC disclosure footnotes #1 through #8 — full-draw mechanics, funding speed, credit pull, collateral, loan amount range and state minimums, APR range, fee structures, variable-rate product mechanics.

- Third-party Figure reviews (past six months): NerdWallet (Jan 2026), CNBC Select (Apr 2026), Credit Karma, The Mortgage Reports (Feb 2026), Bankrate (Dec 2025), Benzinga (Feb 2025), LendEDU (2026), SuperMoney.

- Federal court filings and reporting: Law360, National Mortgage News, HELN News, ClassAction.org, PacerMonitor, Justia — on Ward v. Figure Lending, LLC.

- BBB Business Profile and Trustpilot for Figure Lending (both verified May 21, 2026).

- CFPB HELOC consumer brochure and collateral risk guidance.

- ADU cost data: Angi 2026, SelfStorage.com 2026, Silver Hammer Builders LA 2026, GatherADU 2026 California guide.

Methodology for the Draw-Fit Matrix:

Fit labels assigned on four factors: (1) project stage at loan application; (2) likely fund deployment speed based on typical construction timelines; (3) carrying-cost exposure from Figure’s full-draw structure; and (4) whether the project budget is within Figure’s 85% CLTV equity ceiling. “Good” fits clear all four. “Mixed” fits clear most but raise meaningful concerns. “Weak” or “Poor” fits fail one or more critical factor.

Methodology for the ADU spending timeline:

Month-by-month percentages are Dwelling Index modeled estimates assembled from contractor draw schedules visible in published ADU project case studies, typical permit-process steps documented in city ADU guides, and standard construction-finance milestone payment patterns. They are illustrative starting points for understanding Figure’s full-draw exposure; your actual timeline will vary.

Editorial conclusions in this review are not loan offers, financial advice, or approval guarantees. Dwelling Index is an independent research resource. We are paid by neither Figure nor any lender for the editorial conclusions on this page.

Editorial disclosures

About this review. This Figure HELOC review was researched and written by the Dwelling Index Editorial Team. Dwelling Index does not currently have an active affiliate or referral relationship with Figure Lending, LLC. No CTA on this page sends you to Figure through a paid link. All product mechanics, fee structures, and lawsuit references were verified against the primary sources listed above.

Affiliate disclosure. The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. On this page, links to comparison alternatives may route through Mortgage Research Center, an active Dwelling Index mortgage research partner.

Compliance notes. This page is educational. Nothing here is a loan offer, an offer to extend credit, financial advice, or a guarantee of approval, rate, or terms. HELOC products are secured by your home; if you can’t repay, you can lose your home (CFPB). Rental-income examples are illustrative — actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals. Verify current Figure terms, state availability, fees, and APRs directly with Figure or a licensed partner before applying. Lawsuit references describe allegations as alleged; nothing here should be read as a finding of wrongdoing.

Last verified: May 21, 2026.