Point Home Equity Investment Review (2026): The Real ADU Funding Verdict

By the Dwelling Index Editorial Team · Published: May 21, 2026 · Last updated: May 21, 2026 · Last verified: May 21, 2026 · ~40 min read

Independent analysis by The Dwelling Index, an independent research resource covering ADU financing, costs, and regulations. We do not currently receive compensation from Point Digital Finance, Inc. If that ever changes, this page will say so plainly at the top.

The bottom line

This Point home equity investment review answers one question most reviews skip: when you repay Point, the home value used to calculate Point’s share includes the appreciation your ADU created. Point’s own help center article 25 confirms this. So Point can be the right tool if you cannot service another monthly payment, have a real exit plan within 10–15 years, and accept that the value your ADU creates will be partly shared with your investor. It is the wrong tool if you can qualify for a HELOC, plan to refinance immediately after construction, or count on keeping every dollar of the ADU’s added value.

| Question | Short answer |

|---|---|

| Is Point legitimate? | Yes. BBB A+ since 2015, NMLS #1610752, 4.7/5 Trustpilot (5,198 reviews), $2B+ funded, $2.5B Blue Owl commitment Dec 2025. |

| Monthly payments during term? | None. |

| Term length | Up to 30 years, repaid in one lump sum. |

| Available where? | 27 states + Washington, D.C. (as of May 12, 2026). |

| Funding amount | $30,000 to $600,000 (max offer generally ≤20% of home value). |

| Minimum credit score | 500 per Point's published eligibility page. |

| Income requirement | None. No DTI threshold. |

| Will Point share my ADU's added value? | Yes — confirmed by Point Help Center article 25 (last updated May 6, 2025). This is the central tradeoff for ADU builders. |

| Best fit for ADU | Equity-rich, cash-flow-constrained owners with a 5–15 year exit who cannot qualify for a HELOC or renovation loan at today's underwriting. |

| Worst fit for ADU | Anyone who can qualify for a HELOC, plans to refinance right after construction, or expects to keep all ADU-added value. |

Sources verified May 21, 2026: Point.com/hei/how-hei-works; Point Help Center article 32; BBB profile; Trustpilot.

Before you weigh any financing option, confirm what your property can legally support.

See What You Can Build → Get Your Free ADU ReportFree 60-second property check. We pull your zoning, setback rules, and the size of ADU your lot can fit.

Who this review is for, and who it isn’t

We wrote this for one specific reader: the homeowner who has built up real equity, wants to build an ADU, and cannot or does not want to take on another monthly payment. We read every relevant Point help-center article in May 2026, the CFPB’s January 2025 Issue Spotlight on home equity contracts, current BBB and Trustpilot data, and seven independent reviews published between November 2025 and May 2026. We modeled the ADU math three different ways. We are not a Point affiliate at the time of writing, and we received nothing from Point to write this.

If you are an ADU builder, the analysis below is built for your decision. If you are looking at Point for debt consolidation or retirement income, you will still get value from the cost mechanics, eligibility, and trust signals, but the ADU-specific framing is tuned for the construction use case.

What we verified on May 21, 2026

| Verified item | Source |

|---|---|

| Point HEI: $30K–$600K, no monthly payments, 500+ credit, no income requirement, 30-year term | Point.com/hei/how-hei-works |

| Max offer generally 20% of home value | Point Help Center article 129 (last updated Apr 7, 2026) |

| Available in 27 states + D.C. | Point Help Center article 32 (last updated May 12, 2026) |

| Remodel policy: improvement appreciation is part of overall appreciation shared | Point Help Center article 25 (last updated May 6, 2025) |

| Rental policy: rental term cannot exceed Option Purchase Agreement term | Point Help Center article 24 (last updated May 6, 2025) |

| End-of-term policy: governed by Option Purchase Agreement | Point Help Center article 54 (last updated Dec 20, 2024) |

| Eligibility exclusions: commercial, manufactured, mobile, A-frame, geodesic dome, barndominium, log cabin, 5+ units, LLC, co-op | Point Help Center article 42 (last updated Apr 7, 2026) |

| 7+ acre exclusion | Point Help Center article 15 (last updated Apr 7, 2026) |

| Full fee schedule: up to 3.9% ($2,000 min), appraisal up to $1,000, title/gov $1,000–$1,600, credit report $40–$50, flood cert $12, counseling $130, title cleaning up to $597 | Point Help Center article 38 (last updated May 6, 2025) |

| Homeowner Protection Cap: annualized; most likely to apply in first five years | Point Help Center article 135 (last updated Dec 10, 2025) |

| BBB: A+ since Oct 13, 2015; 4.28/5 (118 reviews); 25 complaints in 3 years, 15 closed in last 12 months | BBB.org Point Digital Finance profile |

| Trustpilot: 4.7/5 across 5,198 reviews | Trustpilot.com/review/point.com |

| 20,000+ homeowners funded; $2B+ in HEIs; $2.5B Blue Owl commitment | Point press release, Dec 9, 2025 |

| CFPB findings: $94,074–$215,892 repayment on $50K HEI at year 10; 22% effective annual cost in early years | CFPB Issue Spotlight: Home Equity Contracts, Jan 15, 2025 |

| Risk-adjustment of up to 29% from independent reviewers | CNBC Select (verified May 2026) |

| HELOC national average 7.41% | Bankrate (May 20, 2026) |

| NMLS license #1610752 | NMLS Consumer Access |

What we did not verify directly: Point’s exact risk-adjustment formula (Point does not publish it; we cite the 15–29% range from independent reviews), the exact Homeowner Protection Cap rate (disclosed per-offer), Point’s specific subordination policy for new construction loans, and any individual borrower’s executed Option Purchase Agreement. Get these in writing during your specific offer review.

How Point’s home equity investment works, in plain English

That structure matters because it changes how the product behaves. A HELOC is debt — you owe a balance, you pay interest, the balance is predictable. A Point HEI is equity participation — you owe a share of a future number that doesn’t exist yet. The CFPB’s January 2025 Issue Spotlight classifies these as “home equity contracts” and notes the repayment amount “can be difficult to predict and can run in the hundreds of thousands of dollars.” Point says it has never foreclosed on a homeowner, but retains the contractual right to do so on default.

The five-step funding process

- Prequalification (~60 seconds). You enter your address. Point pulls public valuation data and runs a soft credit check that does not affect your credit score. You see an estimated offer range.

- Application and underwriting. You complete documentation. Point does not underwrite to your income, but verifies you and the property.

- Independent appraisal. Point arranges and pays for the appraisal upfront, then recovers this cost from your proceeds at closing.

- Appreciation Starting Value is set. This is the number that matters most. It is not your appraised value. Point applies a risk adjustment that lowers the baseline below your actual appraised value; independent reviews document this adjustment at up to 29% in some cases. This produces an “Appreciation Starting Value” used to measure home gains.

- Closing. Point’s lien is recorded in at least third lien position. The processing fee and third-party costs are deducted from your investment. You receive the net. Five to eight weeks total is typical; Point says motivated homeowners can sometimes close in three weeks.

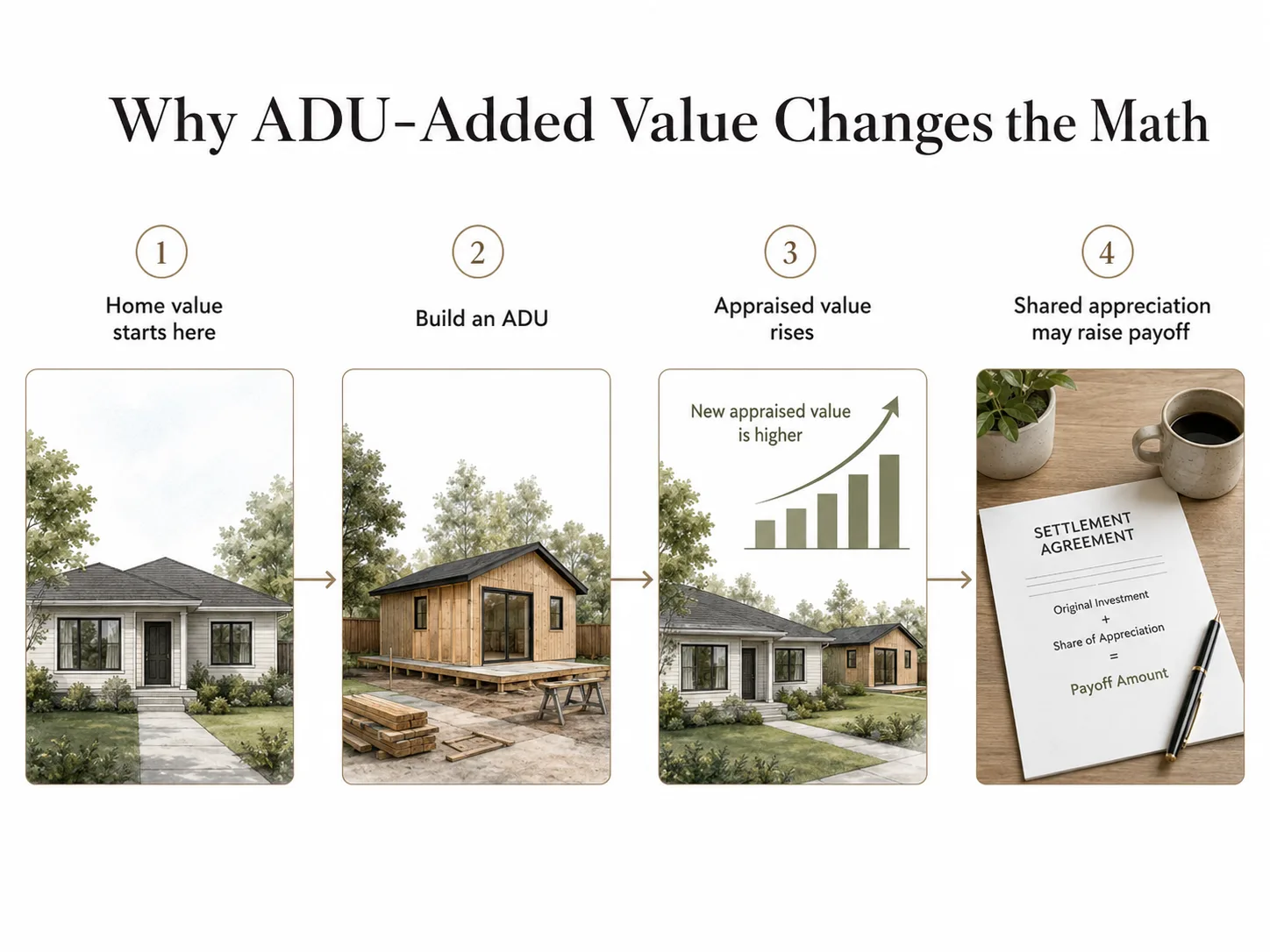

What “appreciation share” really means

When you settle with Point, the formula looks like this:

Repayment = original investment + (Point’s share % × (final appraised value − Appreciation Starting Value))

Then compared against the Homeowner Protection Cap. Whichever is smaller is what you pay.

| Term | What it means |

|---|---|

| Appreciation Starting Value | Risk-adjusted starting baseline, lower than your appraised value. Sets the point from which Point measures appreciation. |

| Share percentage | Point's agreed cut of appreciation above the Appreciation Starting Value. Third-party reviewers consistently put this in the 15–35% range. |

| Homeowner Protection Cap | An annualized maximum that limits what you can owe regardless of how much your home appreciates. Disclosed in your offer. Most likely to apply in the first five years. |

| Processing fee | Up to 3.9% of your HEI (minimum $2,000). Deducted from proceeds at closing. |

| Exit fees | Reconveyance $40–$70, recording $50–$250, exit appraisal up to $1,000 — paid at repayment. |

The ADU question every Point review fails to answer

This is the most important paragraph in this review.

If you take $100,000 from Point to build an ADU, build the ADU, and the ADU adds $180,000 of value to your home, Point’s share at exit is calculated on a number that includes that $180,000. Point does not carve the ADU’s value out. The help-center language is unambiguous: improvement appreciation is part of overall appreciation shared.

Some third-party reviews state that Point recognizes a “home improvement credit” that adjusts the ending value. We could not verify that this language reflects current Point policy. Point’s own help-center article 25 (last updated May 6, 2025) says the opposite. Until Point publishes a separate, current improvement-credit policy on its own help center, we treat the help-center article as authoritative. If you believe Point has changed this policy, ask for the current written policy before signing.

The CFPB found that improvement treatment varies by provider across the home equity contract category — some companies credit homeowner improvements and others do not. Point’s current help-center language places it in the “does not credit” group.

A worked ADU scenario with Point

Assumptions (illustrative only):

- Current home value: $850,000

- Existing first mortgage: $400,000 (equity of $450,000, ~53%)

- Point HEI taken: $100,000 (~12% of home value)

- Processing fee 3.9% ($3,900) + ~$2,500 third-party costs → net to homeowner: ~$93,600

- Appreciation Starting Value (after ~20% risk adjustment): $680,000

- Point’s share: 25% of appreciation above starting value (mid-range industry assumption)

- ADU adds $180,000 of appraised value upon completion

- Market appreciation: 3.5% per year on underlying property

| Exit year | Underlying value (3.5%) | Plus ADU value | Final appraised | Appreciation above starting | Point’s share at 25% | Total repayment | Effective annualized cost |

|---|---|---|---|---|---|---|---|

| Year 5 | ~$1,009,000 | +$180,000 | ~$1,189,000 | ~$509,000 | ~$127,250 | ~$227,250 | ~17.8% |

| Year 10 | ~$1,199,000 | +$180,000 | ~$1,379,000 | ~$699,000 | ~$174,750 | ~$274,750 | ~10.6% |

| Year 20 | ~$1,691,000 | +$180,000 | ~$1,871,000 | ~$1,191,000 | ~$297,750 | ~$397,750 | ~7.2% (likely hits cap) |

- The ADU’s $180,000 of added value is inside Point’s share calculation every year. Without the ADU, the Year 5 share would be ~$82,250 instead of ~$127,250. The ADU adds roughly $45,000 to Point’s repayment at Year 5.

- Effective cost looks ugliest in the early years. The CFPB’s example found settlement amounts often growing by as much as 22% per year in early years — consistent with Year 5 shown above.

- The Homeowner Protection Cap can bind in any year. In our Year 20 scenario, the formula amount would likely be reduced by the cap; the exact reduction depends on the specific cap rate in your offer.

HELOC comparison

A $250,000 HELOC at Bankrate’s national average of 7.41% (May 20, 2026), interest-only during a 10-year draw and amortized over 20 years, would carry payments of roughly $1,544/month during draw and ~$1,999/month during repayment, with total interest of ~$414,000 over 30 years. The homeowner keeps 100% of the ADU’s added value.

The honest framing:

- The HEI saves cash flow. No monthly payment for up to 30 years.

- The HEI is more expensive in the early-to-mid years. For ADU builders especially, because the ADU’s added value increases the share owed.

- The HEI can be cheaper than a HELOC over very long holds with modest appreciation. Especially if the cap binds.

- The HEI is dramatically cheaper if the home depreciates. Point shares in losses; HELOC interest does not.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Before you weigh financing, confirm your ADU math. What can your lot legally support?

See What You Can Build → Get Your Free ADU ReportWhat Point actually costs — the full fee stack

Upfront costs (deducted from your investment, not paid out of pocket)

Source: Point Help Center article 38 (last updated May 6, 2025), verified May 21, 2026.

| Fee | Amount | Notes |

|---|---|---|

| Processing fee | Up to 3.9%; $2,000 minimum | Covers processing, approving, and funding the HEI |

| Appraisal fee (or AVM) | Up to $1,000 | Third-party home valuation |

| Title and government fees | $1,000–$1,600 | Notary, attorney, escrow, doc prep, taxes, recording |

| Credit report fee | $40–$50 | Standard credit bureau fee |

| Flood certification fee | $12 | Confirms flood-zone status |

| Financial counseling fee | $130 | Only if HUD-certified counseling required |

| Title cleaning fee | $199/payoff, capped at $597 | Only if existing liens must be cleared |

| Reconveyance fee (exit) | $40–$70 | Paid at repayment |

| Recording fee (exit) | $50–$250 | Paid at repayment |

| Exit appraisal (exit) | Up to $1,000 | Paid at repayment |

Why the cost at exit is harder to predict than at closing

Your eventual repayment depends on three numbers you don’t fully control:

- Your home’s appraised value at exit. A new appraisal is done. ADU builders should know that the appraiser’s allocation of value between the underlying property and the ADU is not something the homeowner negotiates.

- Your Appreciation Starting Value (set at closing). Risk-adjusted below your appraised value. Third-party reviewers document Point’s risk adjustment in the roughly 15–29% range. Point does not publish the exact formula on its public site.

- Your share percentage (set at closing). Generally falls in the 15–35% range. Better credit and lower combined loan-to-value usually produce lower share percentages.

CFPB finding on home equity contract costs:

The CFPB’s January 2025 report modeled a $50,000 upfront example and found the homeowner would repay between $94,074 and $215,892 at year 10 across the appreciation scenarios studied. Settlement amounts often grew by as much as 22% per year in the early years under nearly all home price scenarios. The home equity contract was more expensive overall than a comparable HELOC if the home appreciated, and less expensive only if the home value fell at least 5%.

The Homeowner Protection Cap (the part that helps you)

Point’s cap article (last updated December 10, 2025) describes the cap as a maximum that limits what you owe regardless of how much your home appreciates. It is calculated annually as a fixed rate compounded monthly applied to the original investment.

The cap matters most in the first five years, because the risk-adjusted Appreciation Starting Value creates a built-in early “jump” in appreciation that would otherwise be punitive without the cap. In your specific offer document, the cap rate is disclosed. Ask for it in writing before signing. A reasonable benchmark question: “What is my Capped Amount at year 5, year 10, year 20, and year 30?”

Is Point legitimate or a scam?

Point Digital Finance was founded in 2015 by Eddie Lim, Eoin Matthews, and Alex Rampell. Backed by Andreessen Horowitz, Ribbit Capital, Greylock Partners, Bloomberg Beta, Westcap, Redwood Trust, and Prudential. The December 2025 Blue Owl commitment was the company’s largest to date.

Trust signals that hold up to scrutiny

| Signal | Status | Source |

|---|---|---|

| BBB rating | A+, accredited since Oct 13, 2015; 4.28/5 (118 reviews) | BBB.org Point Digital Finance profile |

| BBB complaints (last 3 years) | 25 total; 15 closed in last 12 months | BBB Complaints tab |

| NMLS registration | #1610752 | NMLS Consumer Access |

| Trustpilot score | 4.7/5 across 5,198 reviews | Trustpilot.com/review/point.com |

| Funded homeowners | 20,000+ | Point press release, Dec 9, 2025 |

| Total funded volume | Over $2 billion | Point press release, Dec 9, 2025 |

| Recent capital commitment | $2.5 billion from Blue Owl Capital | Dec 9, 2025 announcement |

| State mortgage licensing | CO, CT, GA, IL, MD, NC, OR, WA, WI | Point.com/hei/how-hei-works disclosure |

| Foreclosures executed | Per Point: zero | Point.com/hei/how-hei-works |

What the CFPB found about the HEI category

- Consumers primarily use home equity contracts for debt consolidation and home improvements.

- The repayment amount can be difficult to predict and can run in the hundreds of thousands of dollars.

- Settlement amounts often grow by as much as 22% per year in the early years under nearly all home price scenarios.

- Home equity contracts tend to be more expensive than other forms of home-secured financing unless the home depreciates.

- The CFPB observed structural features that echo some risky loan structures common before the 2008 housing crisis, particularly the difficulty of predicting the settlement amount.

These are not anti-Point findings — they are the CFPB’s analysis of the entire HEI category. Read the full report before deciding.

What Point complaints and reviews should ADU homeowners take seriously?

4.7 / 5 ★

Trustpilot

5,198 reviews · verified May 2026

A+

BBB rating

Accredited since Oct 13, 2015 · 4.28/5 (118 reviews)

Recurring complaint themes to flag before signing

- Final offer can differ from prequalification estimate after appraisal and underwriting. The Appreciation Starting Value is set after the appraisal, so what you see at prequalification is not what you will receive. Can feel like a bait-and-switch if expectations weren’t set clearly.

- Closing takes longer than the marketed three weeks. Five to eight weeks is more typical for most homeowners.

- Buyback math at exit surprises people who didn’t model it carefully at signing. Model three appreciation scenarios before you commit.

- Ineligible-property declines after weeks of application work. Recent BBB reviews include cases of homeowners spending four weeks in the application before being declined for property type. Confirm your property type early.

- Disagreement about cap rates between offer and approval. A recent BBB complaint references a 12.5% homeowner cap the homeowner felt changed during underwriting. Verify your cap rate in writing.

The CFPB received 13 mortgage-related complaints in 2024 about Point Digital Finance LLC; the most common involved applying or refinancing an existing mortgage and trouble during the payment process. The lender offered a timely response to all and closed each with an explanation. (Source: US News.)

Will you qualify? Point’s eligibility decoded

You must meet all of these:

- Located in one of 27 Point-served states or D.C.

- Home value above $155,000

- Credit score 500 or higher

- Retain “significant percentage” of equity (typically 20–40% before Point’s investment)

- No disqualifying bankruptcy or foreclosure

- Accepted property type

- Roof, foundation, and mold issues resolved before Point invests

- Point’s lien in at least third lien position

Excluded property types (absolute — no waiver):

- Commercial properties

- Manufactured homes

- Mobile homes

- A-frames

- Geodesic domes

- Barndominiums

- Log cabins

- Properties with 5+ units

- LLC-held properties

- Co-ops

- Properties on 7+ acres

ADU-specific eligibility flags

- Property condition before funding. Point requires roof, foundation, and mold issues resolved before investing. If your ADU project is part of a broader rehab, you may need to pay for structural fixes first.

- Property type at funding. Point looks at the existing structure, not the planned ADU. A single-family lot remains eligible even if you plan to add a detached ADU.

- Acreage limit. Point does not invest in properties on 7 or more acres. Rural ADU builders should check parcel size carefully.

Where Point is available, and where your state lets you build an ADU

Point’s 27 served states with ADU policy snapshot (verified May 21, 2026)

| State | Point? | Statewide ADU policy | Notes |

|---|---|---|---|

| Arizona | Yes | Local control; some statewide preemption pending | Phoenix and Tucson among the more permissive |

| California | Yes | Strongest in the nation (AB 68, AB 671, AB 2221, AB 1033, AB 1332) | Up to 1,200 sq ft detached on most single-family lots |

| Colorado | Yes | HB24-1152 for 'subject jurisdictions' starting June 30, 2025 | Verify your jurisdiction is subject |

| Connecticut | Yes | Local control | Mostly local |

| Florida | Yes | Local control | Local |

| Georgia | Yes | Local control | Local |

| Hawaii | Yes | County-specific ADU and ohana rules | Heavy variance across counties |

| Illinois | Yes | Local control | Chicago has its own ordinance |

| Indiana | Yes | Local control | Local |

| Kentucky | Yes | Local control | Local |

| Maryland | Yes | State ADU framework; local adoption due Oct 1, 2026 | Strongest demand in Montgomery County |

| Michigan | Yes | Local control | Local |

| Minnesota | Yes | Local control | Minneapolis and St. Paul permissive |

| Missouri | Yes | Local control | Local |

| Nevada | Yes | Local control | Local |

| New Jersey | Yes | Local control | Local |

| New York | Yes | Local control | NYC complex; some upstate permissive |

| North Carolina | Yes | Local control | Local |

| Ohio | Yes | Local control | Local |

| Oregon | Yes | HB 2001 and HB 3214 preempt statewide | Clear statewide pathway; owner-occupancy not required |

| Pennsylvania | Yes | Local control | Local |

| South Carolina | Yes | Local control | Local |

| Tennessee | Yes | Local control | Nashville reform-friendly |

| Utah | Yes | HB 82 (2021) covers internal ADUs only; detached under local control | Statewide preemption narrower than commonly assumed |

| Virginia | Yes | Local control | Local |

| Washington | Yes | HB 1337 requires ≥2 ADUs on qualifying lots in GMA areas | Owner-occupancy prohibited in covered jurisdictions |

| Washington, D.C. | Yes | Comprehensive Plan permissive | Citywide; not required |

| Wisconsin | Yes | Local control | Madison and Milwaukee permissive |

States where Point is not available (as of May 12, 2026)

Alabama, Alaska, Arkansas, Delaware, Idaho, Iowa, Kansas, Louisiana, Maine, Massachusetts, Mississippi, Montana, Nebraska, New Hampshire, New Mexico, North Dakota, Oklahoma, Rhode Island, South Dakota, Texas, Vermont, West Virginia, Wyoming. If you live in one of these, Point’s HEI is not on the table; compare other financing paths instead.

What “select regions” means

Point says it is “available to homeowners in select regions” of the listed states. Being in a Point-served state is necessary, not sufficient. Specific zip codes, valuation areas, or property types can still trigger an underwriting decline. The only way to confirm is to enter your address into Point’s prequalification flow.

Before you decide on financing, verify the ADU your property can legally support.

Get Your Free ADU Report in 60 Seconds →Who should use Point for an ADU?

Point is a real fit when:

- You have 30%+ equity and a meaningful HEI available (typically $400K+ home value)

- You cannot service another monthly payment — irregular income, maxed DTI, recently retired

- You have a concrete exit plan within 10–15 years (sale, refi, or other liquidity)

- The ADU is for non-financial reasons (aging parents, multigenerational housing) where sharing some appreciation is acceptable

- Your home value, property type, equity, and credit all clear Point’s underwriting

- You have read your offer, asked the questions in writing, and modeled repayment scenarios

Point is the wrong fit when:

- You qualify for a HELOC at today’s rates — the HELOC almost always wins on total cost and you keep the ADU’s upside

- You plan to refinance immediately after the ADU is built (cash-out triggers settlement including ADU appreciation)

- The ADU is your primary financial play (rental income + appreciation)

- Your hold horizon is 20+ years with no expected liquidity event

- Your property is on the exclusion list (manufactured, mobile, A-frame, barndominium, log cabin, LLC, co-op, 7+ acres, 5+ units, commercial)

Point HEI vs. HELOC vs. home equity loan vs. cash-out vs. renovation loan for your ADU

ADU financing path comparison

| Path | Monthly payment? | Keeps ADU-added value? | Income required? | Best fit | Main risk |

|---|---|---|---|---|---|

| Point HEI | None | No — Point shares ADU appreciation | No | Equity-rich, cash-flow-constrained, 5–15 yr exit | Uncertain lump-sum payoff; ADU value increases share |

| HELOC | Yes, variable | Yes | Yes | Staged ADU draws, qualifying borrowers | Rate/payment fluctuation; balloon at draw end |

| Home equity loan | Yes, fixed | Yes | Yes | Fixed ADU budget, predictable payment | Immediate full debt service |

| Cash-out refinance | Yes, new first mortgage | Yes | Yes | Only when current rate is at or above market | Losing a sub-market existing rate |

| Renovation loan (203(k) / HomeStyle / CHOICERenovation) | Yes, fixed or ARM | Yes | Yes | Ground-up ADU; underwrites to after-renovation value | Stricter contractor and plan requirements |

| Construction loan (short-term) | Yes, often interest-only | Yes | Yes | Specialized ADU/construction lenders | Two-close structure or tight conversion window |

| Other HEI providers (Hometap, Unlock, Splitero, Unison) | None | Treatment varies; many do not credit improvements | No | Same equity-rich, cash-flow-constrained profile | Same as Point; terms and state coverage vary |

HEI availability changes by state, zip code, lien position, property type, and underwriting. Check provider availability before relying on any HEI path.

Other HEI providers compared on ADU-relevant criteria

| Criterion | Point | Hometap | Unlock | Splitero |

|---|---|---|---|---|

| States served | 27 + D.C. | 16 + D.C. | 24 | 13 |

| Maximum funding | $600,000 | $600,000 | $500,000 | $500,000 |

| Minimum credit | 500 | 600 (some cite 585) | 500 | 500 |

| Term length | 30 years | 10 years | 10 years | 10–30 years |

| Processing fee | Up to 3.9% ($2,000 min) | 4.5% (capped at $20,000) | 4.9% (approx.) | 4.99% (approx.) |

| Partial buyback | No | No | Yes | Yes (limited) |

| Best-fit ADU profile | Long hold, no immediate exit | Planned sale/refi within 10 yrs | Want partial buyback flexibility | Speed of funding |

Verified May 21, 2026 from each provider’s public pages and independent reviews (FinanceBuzz, LendEDU, US News, SuperMoney, CNBC Select). Provider terms change; verify before deciding.

Important caveat for all HEI providers:

The CFPB’s analysis — uncertain settlement, repayment growing at up to 22% per year in early years, more expensive than HELOCs unless homes depreciate — applies broadly to the entire home equity contract category. The choice between Point and another HEI provider is meaningful, but the choice between any HEI and traditional debt financing is more meaningful.

Mortgage Research Center is an affiliate partner. We may earn a commission if you complete a quote. No rate, payment, approval, or savings is guaranteed. Rate ranges verified at time of publication; verify with each lender before applying.

Compare mortgage-based ADU financing paths before sharing future appreciation. Get personalized rate quotes for HELOC, home equity loan, cash-out refinance, and construction loan options.

Compare ADU Financing Paths → Get Personalized Rate QuotesRenting the ADU, refinancing, and the end of the term

Renting the ADU

Yes, you can rent your ADU. Two things to know: lease term cannot exceed the HEI term (so year-to-year is fine; 40-year ground leases are not). Rental income does not offset the appreciation share — your rent receipts are yours and Point's share is calculated on home value, not income.

Refinancing while the HEI is in place

A cash-out refinance is a repayment trigger — pulling cash out via your first mortgage usually requires settling Point's share. A rate-and-term refinance may be allowed without triggering full settlement, but Point's coordination is typically required. For ADU builders: if your plan was 'build the ADU, wait for the appraisal bump, then cash-out refinance to pay Point back,' that plan works — but the cash-out triggers repayment that includes the ADU's added value. There is no way to use ADU appreciation to pay Point without Point taking its share first.

Selling the home

Point's share is calculated on the final sales price. You are solely responsible for selling costs — agent commissions, transfer taxes, repairs. Point does not contribute to these costs but does share in the appreciation that produced your gain.

End of the 30-year term

Per Point's help-center article 54 (last updated December 20, 2024), Point works with homeowners to ensure they are on track to repay through sale, HELOC, cash-out refinance, or use of own funds. Specific end-of-term events are outlined in the Option Purchase Agreement. Read your agreement carefully.

If you cannot repay

Point says it has never foreclosed and that foreclosure is not in its financial interest. But the contractual right exists, and the lien is real. If you reach end of term unable to repay: sell the home, do a cash-out refinance, use a HELOC or home equity loan, or negotiate an extension with Point. You cannot wait Point out.

The honest tradeoffs nobody else lays out

One: The risk-adjusted Appreciation Starting Value is a real cost.

Reducing your appraised value by 15–29% before measuring appreciation means Point starts capturing appreciation from a point well below your actual value. The Homeowner Protection Cap helps mitigate this in the early years, but it's the structural reason early-year payoffs look unusually high.

Two: The processing fee comes out of your investment.

You pay appreciation share on the full $100,000, but you receive about $94,000. That is an effective cost embedded before the appreciation math even starts.

Three: Appreciation share compounds with hold time, even with the cap.

Year 5 looks expensive because of the risk adjustment. Year 20 looks expensive because total appreciation has accumulated. There is no point in the term where the math becomes 'free.'

Four: For ADU builders, the improvement-appreciation issue is binding.

Point's help center is clear: the value your ADU creates is part of the shared appreciation. Some third-party reviewers describe a 'home improvement credit,' but we could not verify that this language reflects current Point policy. Treat the help-center article as authoritative until Point publishes something more favorable.

Five: You can't easily layer senior debt.

Point must be in at least third lien position. Adding a senior construction loan typically requires Point's consent or subordination, which Point handles case by case but does not guarantee.

Six: Property-type exclusions are absolute.

If your property is on 7+ acres, held in an LLC, manufactured, mobile, a barndominium, an A-frame, a log cabin, a geodesic dome, in a co-op, or in a 5+ unit building, Point will not invest. There is no waiver process.

Seven: Final offers can differ from prequalification estimates.

The Appreciation Starting Value is set after the appraisal, not at prequalification. If your home appraises lower than Point's automated estimate, your offer shrinks accordingly. Set expectations correctly.

None of these are inventions — they are all in Point’s own documents or in regulatory commentary, and they are all things a prospective customer should weigh before signing.

What to ask Point in writing before you sign

Print this checklist. Bring it to your phone call. Get answers in writing — email, dashboard message, or PDF — not verbally.

About your specific offer:

- What is my Appreciation Starting Value, and what is the risk-adjustment percentage applied to my appraised value?

- What is my share percentage of appreciation?

- What is my Capped Amount at year 5, year 10, year 20, and year 30?

- What is the exact processing fee dollar amount, and what are the projected third-party costs?

- What will I receive in net proceeds after all closing deductions?

About using funds for an ADU:

- If I build a permitted ADU after closing, will Point share in the appreciation attributable to that ADU? (Per Point Help Center article 25, the answer is yes. Get the company’s specific written acknowledgment.)

- Is there any documentation I can provide — permit records, contractor invoices, before/after appraisals — that would adjust the calculation? If so, what format do you require?

- How does the appraiser at settlement allocate value between the underlying property and the ADU?

About future financing while the HEI is in place:

- Can I take out a HELOC or home equity loan after closing without triggering full HEI repayment?

- Can I refinance my first mortgage (rate-and-term, no cash-out) without triggering HEI settlement?

- Will a cash-out refinance trigger HEI settlement, and what is the exact mechanism?

- Will Point consent to subordinate to a construction loan for the ADU?

About renting the ADU:

- Are standard 12-month leases acceptable? What lease term would create a problem?

- Does short-term rental (Airbnb, Vrbo) trigger any contractual issues?

About exit:

- Can you provide payoff scenarios for years 3, 5, 10, 15, 20, and 30 across low (1%), medium (3.5%), and high (5.5%) appreciation assumptions?

- What happens at the end of the 30-year term if I cannot repay?

- What appraisal dispute rights do I have at settlement?

Download the Free ADU Starter Kit. Get the complete homeowner financing checklist to bring to your Point call, your HELOC underwriter, or your builder consultation.

Download the Free ADU Starter Kit → (no obligation)Point home equity investment review: frequently asked questions

Is Point Home Equity Investment a loan?

No. Point's HEI is a real estate option agreement. There is no interest rate and no monthly payment. Point places a lien on your property to secure performance of the agreement, and you repay through a single lump sum at sale, refinance, buyback, or end of the 30-year term.

Is Point legitimate?

Yes. Point Digital Finance, Inc. has been BBB-accredited since October 2015 with an A+ rating, is NMLS-registered (#1610752), holds a 4.7/5 Trustpilot rating across 5,198 reviews, has funded more than 20,000 homeowners and over $2 billion in HEIs, and secured a $2.5 billion capital commitment from Blue Owl Capital in December 2025. Legitimate, however, does not mean right for every situation.

How much does Point cost?

The upfront cost is a processing fee of up to 3.9% with a $2,000 minimum, plus third-party closing costs (appraisal up to $1,000, title and government fees $1,000–$1,600, credit report $40–$50, flood cert $12, optional title cleaning up to $597, optional counseling $130). The total cost at exit depends on your Appreciation Starting Value, your share percentage, the final appraised value, and the Homeowner Protection Cap. The CFPB's January 2025 analysis found home equity contract settlements often grow by as much as 22% per year in the early years.

How does Point make money?

Point makes money two ways: the processing fee at closing, and Point's share of your home's appreciation at exit. Point also reduces its risk through the Appreciation Starting Value adjustment — measuring appreciation from a baseline below your appraised value — which means Point captures appreciation faster than a simple 'share of the increase from today's value' structure would suggest.

What's the catch with Point Home Equity Investment?

Four real catches: First, Point's share at exit includes appreciation from improvements you made — including an ADU — per Point's own help center. Second, the Appreciation Starting Value is risk-adjusted below your appraised value (independent sources report up to 29% reduction in some cases). Third, the processing fee is deducted from your investment — on a $100,000 HEI you receive roughly $94,000 but pay appreciation share on the full $100,000. Fourth, the CFPB found home equity contract settlements often grow by as much as 22% per year in the early years.

What credit score do I need for Point?

500 minimum, per Point's product page. Point does not require income verification or set a DTI threshold.

How much equity do I need for Point?

You need to retain a significant percentage of equity after Point's investment. Independent reviewers commonly cite a 20–40% equity requirement before Point's investment. Maximum offers are generally 20% of home value, capped at $600,000.

Will Point share in the value my ADU adds?

Yes. Per Point's help center article 25 (last updated May 6, 2025): when it's time to repay, the value of your home will include any appreciation from improvements made during your agreement with Point, and that increase in value is part of the overall appreciation you share. This is the single most important fact for ADU builders to model before signing.

Can I rent my ADU if I have a Point HEI?

Yes. Per Point's help center article 24, you can rent out your property, but the rental term cannot exceed the term of the Option Purchase Agreement. Standard year-to-year leases are unaffected.

Can I pay off Point early?

Yes, with no prepayment penalty, any time during the 30-year term.

What if my home loses value?

Point shares in the loss. If your final value is below the Appreciation Starting Value, you may repay less than the original investment.

What if my home's value explodes?

Point's Homeowner Protection Cap limits what you can owe regardless of how high your home value goes. The cap is an annualized maximum applied to the original investment, compounded monthly. Your specific cap rate is disclosed in your offer.

What states is Point available in?

27 states plus Washington, D.C., as of May 12, 2026: AZ, CA, CO, CT, FL, GA, HI, IL, IN, KY, MD, MI, MN, MO, NV, NJ, NY, NC, OH, OR, PA, SC, TN, UT, VA, WA, WI, and D.C.

How long does Point take to close?

Point says motivated homeowners can close in as little as three weeks. Actual timelines can be longer depending on document responsiveness, mortgage payment status, appraiser timing, and property-debt obligations. Five to eight weeks is more typical in independent reviews.

Can I get a HELOC or refinance while I have a Point HEI?

Adding a senior lien typically requires Point's coordination. A cash-out refinance is a repayment trigger. Rate-and-term refinances may be allowed without triggering full settlement, but require Point's involvement. Ask Point's homeowner services team for your specific situation in writing.

What if I can't repay Point at year 30?

Per Point's help center article 54 (last updated December 20, 2024), during the 30-year term Point works with homeowners to plan repayment through sale, HELOC, cash-out refinance, or own funds. Specific end-of-term events are governed by the Option Purchase Agreement. Read your agreement.

Should I apply to Point before I confirm my property can support an ADU?

No. Confirm what you can legally build first, then choose the financing path. Run a free 60-second feasibility check before signing anything.

Methodology

We built this review from primary sources first, regulatory analysis second, and independent third-party reviews third:

- Read every relevant Point help-center article in May 2026 (articles 15, 24, 25, 32, 38, 42, 54, 129, 135) and noted last-updated dates.

- Read Point’s product page at point.com/hei/how-hei-works and its full legal footnotes.

- Read the CFPB’s January 15, 2025 Issue Spotlight: Home Equity Contracts: Market Overview in full.

- Reviewed Point’s NMLS registration and state license disclosures.

- Cross-checked against eight independent reviews from LendEDU (Apr 2026), US News (Feb 2026), FinanceBuzz (Mar 2026), SuperMoney (Apr 2026), Money.com (May 2026), CNBC Select (Apr 2026), MoneyAtlas (2026), and The Ways to Wealth (Nov 2025).

- Modeled cost-of-capital scenarios using Point’s disclosed formula structure, published share-percentage ranges from third-party reviews, and three appreciation assumptions (1.5%, 3.5%, 5.5% annual).

- Recomputed HELOC scenario math against Bankrate’s national average HELOC rate as of May 20, 2026 (7.41%).

- Reviewed BBB profile, Trustpilot rating history, and CFPB Consumer Complaint Database entries.

What we did not do: We did not interview Point executives, did not receive internal documents, did not review an active borrower’s executed Option Purchase Agreement, did not call individual homeowners for testimonials, and did not receive any draft review or input from Point or any HEI competitor. We received zero compensation for this article from Point or any HEI provider.

Editorial standards. The Dwelling Index is an independent research resource. We do not rank lenders by commission or present financing as “best lender” rankings. Examples involving rental income, ADU cost recovery, or appreciation are illustrative, not guarantees. Actual results depend on local market conditions, construction costs, financing terms, regulatory approvals, and individual contract terms. This article is not financial, legal, tax, or lending advice.

Sources

Primary sources (Point):

The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. We do not currently receive compensation from Point Digital Finance, Inc. or any other HEI provider mentioned in this review. This article is informational and does not constitute financial, legal, tax, or lending advice. Consult qualified professionals before signing any home equity agreement.

Confirm what you can legally build before committing to any financing.

See What You Can Build → Get Your Free ADU ReportFree 60-second check. No account required.