Unlock Home Equity Agreement Review (2026): Is It a Smart Way to Fund an ADU?

By the Dwelling Index Editorial Team · Published: May 21, 2026 · Last updated: May 21, 2026 · Last verified: May 21, 2026 · ~35 min read

We are not a lender, broker, or builder. We are not a lender, broker, or builder. We do not currently have a referral or affiliate relationship with Unlock Technologies and earn nothing if you apply with them.

Unlock home equity agreement review: the bottom line in 60 seconds

Our verdict for ADU homeowners: an Unlock Home Equity Agreement (HEA) is a legitimate, NMLS-registered product from a Tempe, AZ fintech that lets you trade a share of your home’s future value for cash today, with no monthly payments and a 10-year term (Unlock Product Guide). It can fit an equity-rich homeowner with a clear exit plan — usually one whose ADU is already built and generating rent, or whose credit blocks them from a traditional HELOC. It is almost never the right tool for funding new ADU construction and is rarely the cheapest option mathematically for homeowners who can qualify for a HELOC.

This review walks through real settlement math, the 25-state availability map, credit and property requirements, the Improvement Adjustment documentation that protects ADU owners, the regulatory status as of May 2026, and the financing alternatives we’d compare first.

| Question | Bottom line |

|---|---|

| Is Unlock legitimate? | Yes — NMLS #2657081, A+ BBB rating, 20,000+ funded HEAs, but the product category is complex. |

| Monthly payments during the term? | None. |

| Term length | Maximum 10 years. |

| Available where? | 25 states. Not available in Washington, DC. |

| Funding amount | $15,000 to $500,000. |

| Best fit for ADU | Post-build refinance or buyout cases, equity-rich with weak credit, fixed-income exit plans. |

| Biggest ADU-specific risk | The Improvement Adjustment requires comprehensive documentation; without permits, invoices, and a defensible post-build appraisal, your ADU’s value gets shared with Unlock. |

The five numbers that define an Unlock contract (verified May 21, 2026):

- $15,000 to $500,000 lump sum (called the Investment Payment)

- 4.9% origination fee of the Investment Payment, plus third-party transaction expenses (appraisal, title, escrow, recording, credit)

- 10-year term, no monthly payments during the term

- Exchange rate typically 2.0, with Unlock’s Product Guide showing examples at 2.00, 2.10, and 2.20 — higher-risk transactions may price above 2.25

- 19.9% Annualized Cost Limit (ACL) — the cap on Unlock’s annual return on its Investment Payment

Available in 25 states: AZ, CA, FL, HI, ID, IN, KY, MI, MO, MT, NV, NH, NJ, NM, NC, OH, OR, PA, SC, TN, UT, VT, VA, WI, WY. Source: Unlock.com homepage, verified May 21, 2026.

Before you decide on any financing path, confirm your lot can actually hold the ADU you want.

See What You Can Build → Get Your Free ADU ReportFree 60-second property check. We pull your address, run it against local zoning, and return your likely ADU size, setbacks, and feasibility.

What we verified on May 21, 2026

We built this review by pulling claims directly from primary sources and cross-checking conflicting third-party reports.

- Product terms (Investment Payment range, fees, term, exchange rate, ACL): Unlock /what-it-costs/, Unlock Product Guide

- Eligibility (500 credit minimum, 30% equity, $175,000 minimum): Unlock /how-it-works/

- State availability (25 states): Unlock.com homepage

- Property restrictions (no prefab, manufactured, mobile, raw land, co-op, TIC): Unlock FAQs

- BBB rating (A+, accredited September 22, 2025): BBB profile

- Trustpilot rating (~4.7–4.8, ~2,000 reviews): Trustpilot.com/review/unlock.com

- Regulatory status: CFPB amicus brief in Roberts v. Unlock Partnership Solutions AOI, Inc. (No. 1:24-cv-1374, D.N.J., January 15, 2025) — later withdrawn under the new administration; lawsuit remains active

- State-level mortgage treatment (CT, MD, IL, WA): Mayer Brown reporting; Illinois Residential Mortgage License Act amendment effective January 1, 2025

Conflicts we resolved:

- State count: LendEDU says 13; SuperMoney says 26; Bankrate says 25. Unlock’s own homepage lists 25, and DC is not among them. We treat Unlock as authoritative.

- Renovation credits: Some third-party guides claim Unlock doesn’t credit renovations. Unlock’s own FAQ and Product Guide describe the Improvement Adjustment provision. We follow the primary source.

- Founding year: CFPB market overview says 2019; Unlock’s About page references 2020. We use 2019 as the corporate founding year per regulatory disclosure.

What we did not verify: the exact final Exchange Rate Unlock would offer any specific homeowner; any individual’s appraisal outcome; whether Unlock treats a prefab ADU as irrelevant when the primary residence is site-built (confirm directly with Unlock).

Is Unlock a good idea for an ADU?

We are an independent research resource covering ADU financing, costs, and regulations — which means we’d rather lose a click than route you to a product that’s wrong for your situation.

When an Unlock HEA can make sense for an ADU

Fit 1 — You already built the ADU and it’s generating rent, but you used hard money or a high-rate personal loan.

Your ADU is finished, you’ve got documented permits and appraisal evidence of the value added, you can show rental income, and you want to retire expensive short-term debt without taking on a new monthly payment. Unlock’s lump sum can pay off the original financing, and your rental income can build a refinance or buyout reserve for year 10.

Fit 2 — Your credit score is between 500 and 620 with no recent income to verify, but you have real equity.

Banks won’t write you a HELOC. A cash-out refinance would replace the low-rate first mortgage you’d rather keep. You have at least 30% equity, and you have a plan to sell or refinance within 10 years. Unlock’s 500-credit minimum and no-income-verification policy serves this exact gap.

Fit 3 — You’re retired or on fixed income, the ADU will house family or generate predictable rent, and you can’t carry a new monthly payment.

Cash flow matters more than total cost, and a 10-year buyout from estate proceeds, downsizing, or rental income is realistic. The damaging admission: at year 10 you must settle. If your plan is to die in the home, your heirs will be the ones writing the check.

When Unlock is the wrong tool for an ADU

Anti-fit 1 — You’re funding new construction from scratch.

Unlock records a lien on your property (a performance deed of trust or performance mortgage depending on your state). Most construction lenders will not subordinate to a senior shared-equity lien. This is the single most important point in this review, and the one most other Unlock reviews skip.

Anti-fit 2 — You’re in a high-appreciation market.

Coastal California, much of Florida, Austin, Boise, Phoenix — anywhere annual appreciation runs 8% or higher — pushes your effective annualized cost into the high-teens at year 10. A HELOC at 8%–10% APR is mathematically cheaper, even with monthly payments.

Anti-fit 3 — You plan to sell or refinance within five years.

The 19.9% Annualized Cost Limit is a ceiling, not a floor — many short-horizon exits hit it. Per Unlock’s Product Guide example using a 2.0 Exchange Rate and 19.9% ACL at 3% appreciation, the cap applies in years 1–4; by year 5 the annualized cost lands at 18.32%.

Anti-fit 4 — Your home itself is manufactured, mobile, prefab, raw land, a co-op, or a tenancy-in-common.

Per Unlock’s stated investment criteria in their FAQ, these property types are not accepted.

Anti-fit 5 — Your home value is below $175,000 or above $3,000,000.

$175,000 is the published minimum, $3,000,000 the published maximum. Below roughly $300,000, the fixed origination fee and third-party costs eat enough of the lump sum that an HEA is rarely the economic choice.

Unlock-for-ADU fit by use case

| ADU use case | Unlock fit | Why |

|---|---|---|

| Pay off completed rental ADU’s hard money or HELOC | Strong fit | Exit plan exists, ADU income supports refinance, lien isn’t blocking new construction |

| Retiree with finished family ADU, fixed income | Possible fit | Cash flow matters more than total cost; estate or sale provides exit |

| Detached ADU build, $250K–$450K budget | Wrong tool | Subordination risk blocks construction loan; use HELOC, HomeStyle, or construction loan instead |

| Garage conversion, $100K–$180K budget | Wrong tool | HELOC or personal loan almost always cheaper for this size project |

| ADU for aging parents, plan to hold forever | High caution | Year-10 settlement requires refi or sale; not compatible with permanent hold |

| Rental ADU with refinance planned after stabilization | Possible fit | Only if rental projections and appraisal will actually support refi |

| Prefab/manufactured primary residence | Not eligible | Unlock does not invest against manufactured housing |

| Speculative ADU plan, no permits in hand | Wrong tool | Improvement Adjustment requires documented permits |

Unlock fit by ADU project phase

| Project phase | Unlock fit | What to do instead |

|---|---|---|

| Pre-permit (exploring) | Not yet | Run a free feasibility check first |

| Permit approved, not started | Wrong tool | Construction loan, HELOC, 203(k), or HomeStyle |

| Under construction | Wrong tool | Construction loan or renovation loan |

| Built, not rented (seasoning) | Possible fit | Consider if you need to retire short-term financing |

| Built and rented, stable income | Strong fit | Best window — documented value-add, rent supports exit |

| Refinance / buyout stage | Possible fit | Compare cash-out refi rates against Unlock buyout math |

An ADU is not a kitchen remodel. It’s an income-generating addition to your property that materially changes the home’s appraisal complexity, rental potential, and financing options. That changes the calculus on any equity-sharing product. Read the Improvement Adjustment section below before you sign anything.

The next question worth answering before financing: can your lot hold the ADU you want, at the size you want, under your city’s current rules?

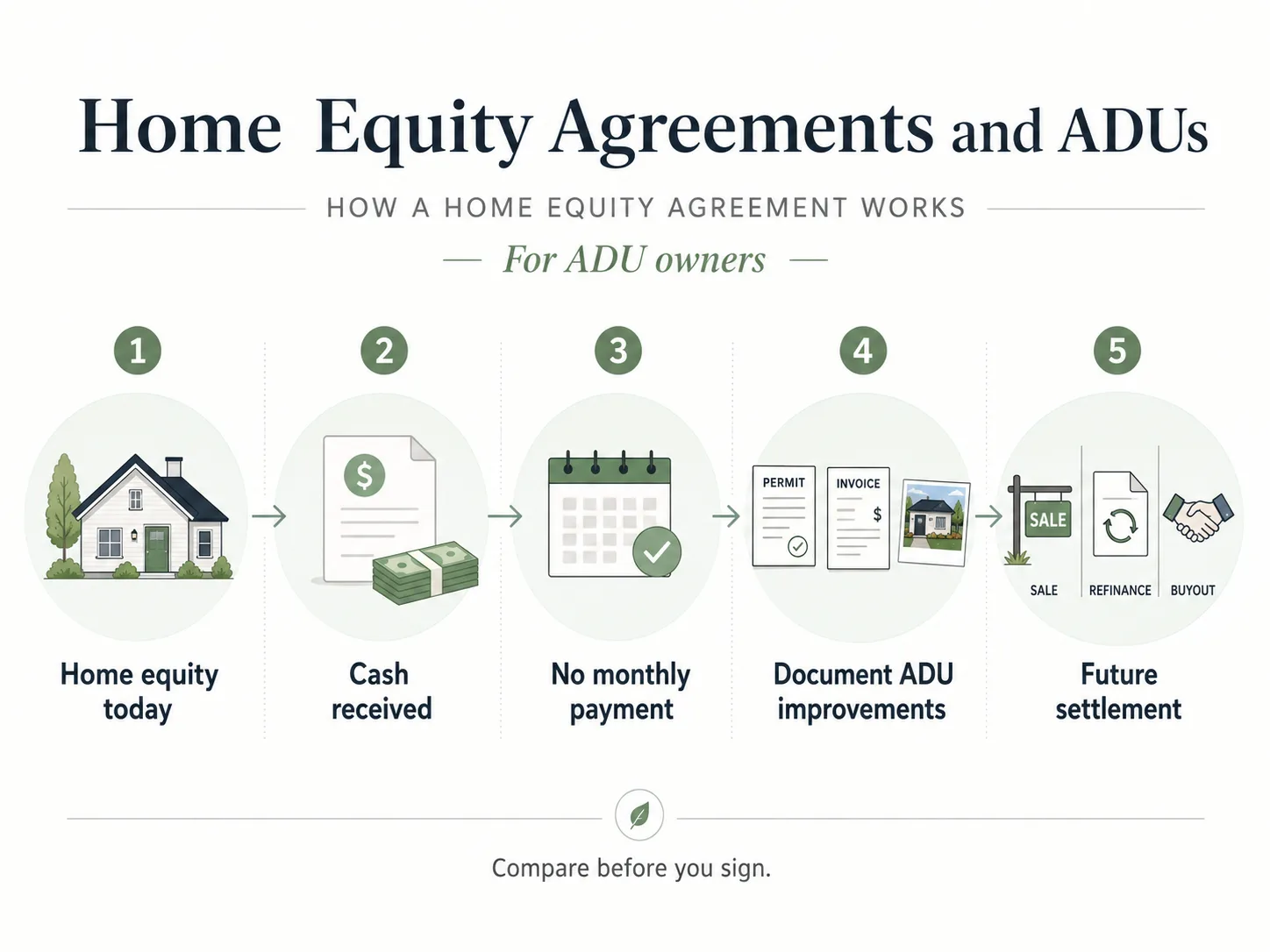

See What You Can Build → Get Your Free ADU ReportHow an Unlock HEA actually works

The six-step process

- Online estimator — A two-minute soft-credit check returns an initial offer range. No impact to your credit score.

- Call with a home equity officer — They walk through your situation, your intended use, and the contract structure.

- Third-party appraisal and title review — Independent appraiser determines starting home value; title check confirms ownership and existing liens.

- Offer letter — Unlock provides your exact Investment Payment, Exchange Rate, Unlock Percentage, and origination fee. These numbers are fixed at signing.

- Closing — You sign the agreement and a security instrument (performance deed of trust or performance mortgage). Unlock records the lien.

- Funding — Total time from application to funding is generally 30 to 60 days per Unlock’s published timeline. Actual timing varies.

The three numbers that define your contract

| Term | What it means | Verified figure (May 2026) | Source |

|---|---|---|---|

| Investment Payment (lump sum) | Cash you receive before fees | $15,000 to $500,000 | Unlock /what-it-costs/ |

| Exchange Rate | Multiplier converting investment percentage into future value share | Typically 2.0; examples at 2.00, 2.10, 2.20; higher-risk above 2.25 | Unlock Product Guide |

| Unlock Percentage | Investment Payment ÷ Starting Home Value × Exchange Rate | Maximum 70% per Product Guide | Unlock Product Guide |

| Annualized Cost Limit (ACL) | Cap on Unlock's annual return | 19.9% (or lower if state imposes stricter cap) | Unlock /what-it-costs/ |

| Term | Maximum duration before settlement required | 10 years | Unlock /what-it-costs/ |

| Origination Fee | Deducted from lump sum at closing | 4.9% of Investment Payment | Unlock /what-it-costs/ |

| Third-party expenses | Appraisal, title, escrow, recording, credit | Vary by property; not published as fixed range | Unlock /what-it-costs/ |

| Minimum credit score | 500 | — | Unlock qualification page |

| Minimum equity | At least 30% | — | Unlock blog (Jan 2026) |

| Minimum Starting Home Value | $175,000 | — | Unlock Product Guide |

| Maximum Starting Home Value | $3,000,000 | — | Unlock Product Guide |

The math, in plain English

Unlock’s Product Guide formula: Investment Payment ÷ Starting Home Value × Exchange Rate = Unlock Percentage. The Product Guide example shows $100,000 ÷ $1,000,000 = 10% Investment Percentage, multiplied by a 2.0 Exchange Rate, equals a 20% Unlock Percentage. The maximum Unlock Percentage is 70%.

A worked example: Maria’s San Diego home

Maria owns a $600,000 home in San Diego with $200,000 left on her mortgage. She takes a $60,000 Investment Payment (10% of home value).

- Origination fee: 4.9% × $60,000 = $2,940 deducted at closing

- Third-party transaction expenses: roughly $3,500 in this example

- Net cash to Maria: approximately $53,560

- If Unlock’s Exchange Rate is 2.0x, the Unlock Percentage is 20% of the home’s future value

If Maria sells in 10 years for $900,000, Unlock receives roughly $180,000 before the ACL is applied.

All figures are illustrative. Your actual Exchange Rate, Unlock Percentage, and fees will depend on your home’s value, equity position, location, credit profile, and use case.

ADU-specific questions to ask before signing

- Will Unlock subordinate to a future construction loan, HELOC, or home equity loan during the term? On what terms and at what fee?

- What is the documentation standard for the Improvement Adjustment, and does the post-build appraisal cost come out of my pocket?

- If my ADU is prefab or modular, does it affect the eligibility of my site-built primary residence or the appraisal at settlement?

- What is my exact Exchange Rate, and what made the underwriter price it where they did?

- Show me a worked example settlement statement at year 5 and year 10 under 3%, 5%, and 8% annual appreciation, with and without the ACL applied.

- If I add the ADU but my Improvement Adjustment is later disputed, what is the dispute-resolution process?

Improvement Adjustment and Maintenance Adjustment

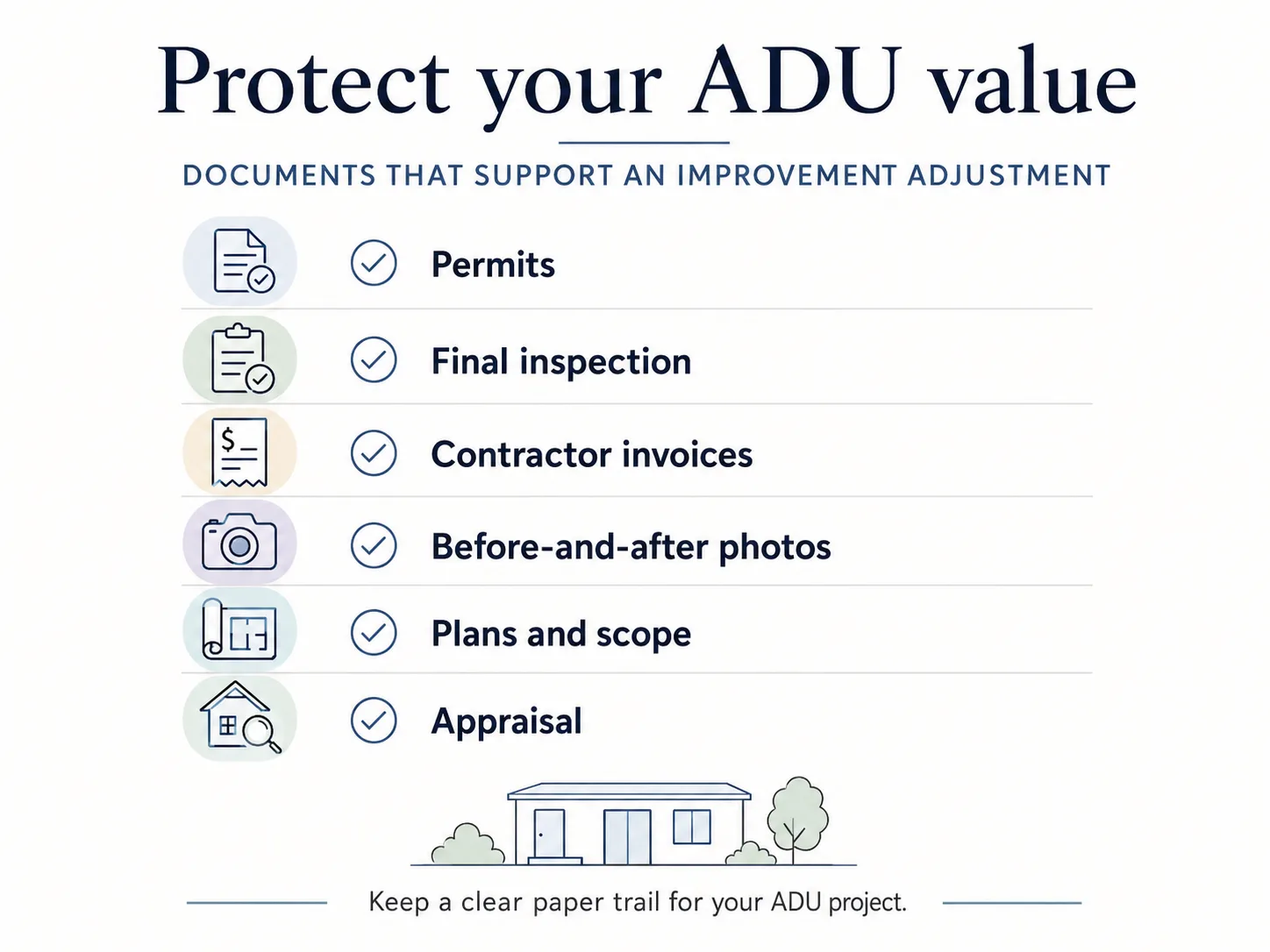

This is the part of the contract that matters most to ADU owners. When the agreement ends, an independent appraisal sets the Ending Home Value. Unlock then applies:

- An Improvement Adjustment — qualifying homeowner-funded improvements documented by permits, contractor invoices, plans, photos, and a post-build appraisal are subtracted from the Ending Home Value before Unlock’s percentage is calculated. So if your ADU adds $150,000 in appraisal-supported value, that amount is removed from the base on which Unlock’s share is computed.

- A Maintenance Adjustment — if the home is in poor condition due to deferred maintenance, the appraiser estimates what the home would be worth had it been properly maintained. That higher value is used for Unlock’s calculation, so neglect doesn’t reduce Unlock’s payout.

Ending Home Value − Improvement Adjustment + Maintenance Adjustment = Adjusted Ending Value

Adjusted Ending Value × Unlock Percentage = Calculated Unlock Share

Final Unlock Share = lesser of Calculated Share or ACL-capped Share

Two things to flag immediately. First, the Improvement Adjustment requires documentation — without permits, invoices, scope of work, photos, and a post-build appraisal, the appraiser cannot quantify the value-add. Second, Unlock indicates that projects adding less than $10,000 in value may not qualify.

Want to model the math for your own home?

Our free ADU equity calculator lets you input your home value, mortgage balance, and ADU plan, then shows your equity position, expected ADU value-add, and financing gap.

Use the Free ADU Equity Calculator →What an Unlock HEA really costs

Two ways to measure cost — both shown below

Unlock’s Product Guide method: Annualized cost is calculated against the gross Investment Payment and excludes upfront fees. This is what Unlock’s published examples report.

Consumer net-cash method: Annualized cost is calculated against the net cash you actually receive after the 4.9% origination fee and third-party transaction expenses. This will always be higher, because fees reduce your cash. We show both.

How the ACL works

The 19.9% Annualized Cost Limit caps Unlock’s annualized return on the Investment Payment. Per Unlock’s Product Guide example at 2.0 Exchange Rate and 3% appreciation, the cap binds in years 1 through 4. By year 5, the annualized cost is 18.32% — high, but not ACL-capped. By year 10 at 3% appreciation, the annualized cost is 10.39%.

Proprietary 10-year settlement matrix

Assumptions: 10% lump sum (Investment Payment = 10% of starting home value), 2.0x Exchange Rate, 20% Unlock Percentage, 4.9% origination fee, representative $3,500 in third-party transaction expenses. Your actual third-party costs will vary.

Home A — Knoxville, TN — $400,000, 10% lump sum

Investment Payment $40,000; origination fee $1,960; net cash after $3,500 third-party costs ≈ $34,540

| Annual appreciation | Home value yr 5 | Calculated share yr 5 (20%) | ACL-capped share yr 5 | Home value yr 10 | Final share yr 10 |

|---|---|---|---|---|---|

| 3% | $463,710 | $92,742 | ~$99,119 (ACL binds) | $537,567 | $107,513 (no cap) |

| 5% | $510,512 | $102,102 | ~$99,119 (ACL binds) | $651,558 | $130,312 (no cap) |

| 8% | $587,731 | $117,546 | ~$99,119 (ACL binds) | $863,571 | $172,714 (no cap) |

Home B — Sacramento, CA — $550,000, 10% lump sum

Investment Payment $55,000; origination fee $2,695; net cash after $3,500 third-party costs ≈ $48,805

| Annual appreciation | Home value yr 5 | Calculated share yr 5 (20%) | ACL-capped share yr 5 | Home value yr 10 | Final share yr 10 |

|---|---|---|---|---|---|

| 3% | $637,602 | $127,520 | ~$136,288 (ACL binds) | $739,154 | $147,831 (no cap) |

| 5% | $701,954 | $140,391 | ~$136,288 (ACL binds) | $895,892 | $179,178 (no cap) |

| 8% | $808,131 | $161,626 | ~$136,288 (ACL binds) | $1,187,419 | $237,484 (no cap) |

Home C — Tampa, FL — $700,000, 10% lump sum

Investment Payment $70,000; origination fee $3,430; net cash after $3,500 third-party costs ≈ $63,070

| Annual appreciation | Home value yr 5 | Calculated share yr 5 (20%) | ACL-capped share yr 5 | Home value yr 10 | Final share yr 10 |

|---|---|---|---|---|---|

| 3% | $811,402 | $162,280 | ~$173,458 (ACL binds) | $940,741 | $188,148 (no cap) |

| 5% | $893,303 | $178,661 | ~$173,458 (ACL binds) | $1,140,228 | $228,046 (no cap) |

| 8% | $1,028,529 | $205,706 | ~$173,458 (ACL binds) | $1,511,168 | $302,234 (no cap) |

Year-10 annualized cost ranges (consumer net-cash method) under these assumptions:

- Low appreciation (3%): roughly 11%–13% per year on net cash received

- Moderate appreciation (5%): roughly 13%–16% per year

- High appreciation (8%): roughly 16%–19% per year

Under Unlock’s own Product Guide method (gross Investment Payment, excluding upfront fees), published examples show 7.18% at 0% appreciation over 10 years and 10.39% at 3% appreciation over 10 years.

These examples are illustrative, not guarantees. Actual results depend on contract terms, Exchange Rate priced for your property, appraisal outcomes, home-value changes, fees, taxes, insurance, financing availability, construction costs, and regulatory approvals.

Compared to a HELOC

Current HELOC rates in 2026 generally range from approximately 7% to 13% APR depending on credit and combined LTV:

- Low appreciation (3%), 10-year hold: Unlock consumer net-cash effective cost roughly 11%–13%. Often comparable to a higher-rate HELOC, sometimes more expensive than a prime HELOC.

- Moderate appreciation (5%), 10-year hold: Unlock roughly 13%–16%. Almost always more expensive than a comparable HELOC.

- High appreciation (8%), 10-year hold: Unlock roughly 16%–19%. Substantially more expensive than any HELOC.

The honest framing: Unlock is rarely the lowest-cost option mathematically. It’s the lowest-cash-flow option. You pay a premium for the no-monthly-payment structure and the no-income-verification access. That’s the trade.

Where Unlock’s origination fee sits in the HEA market

| Provider | Origination fee | Min credit | Term |

|---|---|---|---|

| HELOC (typical 2026) | 0%–2% (often waived) | ~680+ | 10-yr draw + 20-yr repay |

| Cash-out refinance | 2%–3% closing costs | ~620+ | 15–30 yr |

| Hometap | Published terms vary; verify with provider | ~600+ | 10 yr |

| Point | Published terms vary; verify with provider | 500+ | up to 30 yr |

| Unison | Published terms vary; verify with provider | 620+ | up to 30 yr |

| Unlock | 4.9% origination | 500 | 10 yr |

Affiliate disclosure: we may earn a commission from lender partners at no cost to you. Rate ranges verified at time of publication; verify current rates with each lender before applying.

Considering an ADU and trying to figure out how to pay for it without locking in a no-monthly-payment product first? Compare HELOC, FHA 203(k), HomeStyle, CHOICERenovation, cash-out refinance, and construction loan paths side-by-side, with real May 2026 rate ranges and qualification rules.

Compare ADU Financing Options →Does Unlock share in the value your ADU creates?

Why this matters more for ADUs than any other improvement

A kitchen remodel adds value to the existing structure. An ADU is a separate income-generating unit that materially changes the property’s appraisal complexity, comparable-sales pool, and rental potential.

Without Improvement Adjustment (20% Unlock Percentage)

Ending value $900,000 × 20% = $180,000 to Unlock

With Improvement Adjustment of $150,000

Adjusted value ($900,000 − $150,000) = $750,000 × 20% = $150,000 to Unlock

You save $30,000 through proper documentation.

Value protected by documentation: quick reference

| ADU appraisal-supported value-add | Settlement difference at 20% Unlock Percentage |

|---|---|

| $75,000 | $15,000 |

| $150,000 | $30,000 |

| $200,000 | $40,000 |

| $250,000 | $50,000 |

| $350,000 | $70,000 |

Most ADU builders see appraisal-supported value-add somewhere in the $100,000 to $250,000 range, translating to $20,000 to $50,000 in settlement difference on a typical Unlock contract.

Improvement Adjustment documentation checklist

| Document | Why it matters |

|---|---|

| Issued building permit (approved permit, not just an application receipt) | Unlock's Product Guide requires qualifying improvements to comply with local building codes and required permits |

| Final inspection / certificate of occupancy or completion | Proves the ADU is legally complete and habitable |

| Signed contracts with each contractor | Supports the homeowner-funded improvement cost |

| Itemized invoices and proof of payment | Establishes the dollar amount you spent |

| Plans and full scope of work | Helps the appraiser isolate value added by the ADU vs. general home upkeep |

| Before-and-after photos with timestamps | Documents project scope and condition |

| Inspections at each phase (foundation, framing, MEP, final) | Establishes the build was done to code |

| Property tax reassessment notice (if applicable) | Independent confirmation of the value added |

| Post-build independent appraisal | Unlock's settlement appraisal is the official measure — your private appraisal gives you something to negotiate against |

| Rental documentation if leased | Supports income approach to value |

What can go wrong

- Unpermitted construction. If the ADU was built without permits or with an expired permit, the Improvement Adjustment may not apply. Resolve permit status before applying for any equity-based product.

- Documentation gaps. Lost invoices, missing inspection records, no before photos. These add up.

- Appraiser disagreement. Two appraisers can value the same ADU $40,000 apart, especially in markets where ADU comparables are thin.

- Maintenance Adjustment offset. If you let the rest of the home deteriorate while building the ADU, the Maintenance Adjustment increases the Ending Home Value, partially canceling your Improvement Adjustment.

- Threshold gap. Projects adding less than $10,000 in value may not qualify for adjustment at all.

When you should not assume the Improvement Adjustment will save you

If you cannot maintain comprehensive documentation, do not factor a generous Improvement Adjustment into your modeling. Run your settlement math assuming Unlock shares in the full ending value, including your ADU’s contribution. If that math still works, the HEA may still be a fit. If it doesn’t, look elsewhere.

Before you sign anything, see whether your lot can hold the ADU you’re modeling.

Get Your Free ADU Report →Is Unlock available in my state?

State availability matrix (verified May 21, 2026)

Pulled directly from Unlock.com’s homepage on May 21, 2026. Verify against the current Unlock homepage before applying.

| State | Unlock available? | Notes |

|---|---|---|

| Arizona | Yes | Unlock's home state |

| California | Yes | Largest single market |

| Florida | Yes | High HEI demand |

| Hawaii | Yes | High property values support eligibility |

| Idaho | Yes | |

| Indiana | Yes | |

| Kentucky | Yes | |

| Michigan | Yes | |

| Missouri | Yes | |

| Montana | Yes | |

| Nevada | Yes | |

| New Hampshire | Yes | |

| New Jersey | Yes | |

| New Mexico | Yes | |

| North Carolina | Yes | |

| Ohio | Yes | |

| Oregon | Yes | |

| Pennsylvania | Yes | |

| South Carolina | Yes | |

| Tennessee | Yes | |

| Utah | Yes | |

| Vermont | Yes | |

| Virginia | Yes | |

| Wisconsin | Yes | |

| Wyoming | Yes | |

| Texas | No | HEI providers broadly unavailable; state home equity rules are unusually restrictive |

| New York | No | Not listed on Unlock homepage as of May 2026 |

| Massachusetts | No | Not listed; active regulatory scrutiny of HEI category |

| Washington, DC | No | Specifically excluded from Unlock's 25-state list |

| All other states | No | Check Unlock.com homepage directly |

State-level regulatory treatment

Several states have applied mortgage-lending treatment to HEIs, affecting how products are licensed and disclosed:

- Connecticut and Maryland — Pre-existing licensing and statutory treatment for shared-appreciation / home-equity-option products

- Illinois — Amended its Residential Mortgage License Act effective January 1, 2025 to include shared-appreciation agreements

- Washington (state) — Case law via Olson v. Unison treats a specific HEI agreement as a reverse mortgage under Washington law

Industry counsel has predicted that more states will follow this path regardless of how the CFPB ultimately treats these products.

Who qualifies for Unlock

Eligibility requirements

- Minimum 500 FICO score

- At least 30% equity in the property

- Home value $175,000 to $3,000,000

- Located in one of 25 eligible states

- Site-built, single-family, or eligible multi-family structure

Not eligible

- Manufactured, mobile, or prefab homes

- Raw land

- Co-ops or tenancy-in-common

- Properties outside the 25 eligible states

- Investment properties without verifiable rental income

Documents you’ll need to apply

- Recent mortgage statement

- Property tax records

- Homeowners insurance declaration page

- Government-issued ID

- Proof of property occupancy if primary residence (utility bill, voter registration)

- Trust documents if the property is held in a trust

- Verifiable rental income documentation if property is an investment property

Not sure where to start? Before you apply anywhere, run a free feasibility check on your property.

See What You Can Build → Get Your Free ADU ReportFree 60-second property check. No account required.

What do Unlock reviews and complaints actually say?

~4.7–4.8 ★

Trustpilot rating

~2,000 reviews · verified May 2026

Positive themes: transparent process, helpful officers, fast funding, no payment relief.

A+

BBB rating

Accredited September 22, 2025

20,000+ HEAs funded per Unlock About page.

What positive reviewers consistently mention

- Fast, transparent process from application to funding

- Helpful home equity officers who explain the math without pressure

- Relief from monthly payments on existing high-rate debt

- Straightforward closing experience for homeowners with clean title

What negative reviewers consistently mention

- Valuation disputes at buyout. One Consumer Affairs reviewer in September 2025 alleged that Unlock’s valuations during the buyout process came in well above their estimate of fair market value. Unlock responds that valuations are determined by third-party appraisers.

- Settlement-size surprise. Customers who didn’t fully model the appreciation scenario report shock at the final number — not bad faith from Unlock, but underscoring how important the modeling exercise is before signing.

- Closing and title friction. Like any real estate transaction involving liens, the process can stall when title issues, existing junior liens, or HOA fees complicate things.

- Difficulty refinancing. Because Unlock will not subordinate to certain new debt, some customers have reported difficulty refinancing or taking on construction loans during the term.

A representative cautionary review from Consumer Affairs (September 2025): one homeowner advised others to “read the fine print very carefully” before signing. Trustpilot and Consumer Affairs reviews represent the experience of people who chose to leave a review, not a random sample of all Unlock customers. Use them as signals, not statistics.

Is Unlock legitimate or a scam?

Legitimacy signals we verified

| Signal | Verified detail |

|---|---|

| Legal entity | Unlock Technologies Inc. (parent); Unlock Home Equity Solutions Inc. (operating entity) |

| NMLS | #2657081 — verifiable through NMLS Consumer Access database |

| Headquarters | 1230 W. Washington Street, Suite 310, Tempe, AZ 85288 |

| Phone | 800-560-3450 |

| CEO | Jim Riccitelli |

| Founded | 2019 (per CFPB market overview) |

| Funding raised | $280M total (Series B led by D2 Asset Management, September 2024) |

| HEAs funded | 20,000+ (per Unlock's current About page) |

| BBB | A+ rating, accredited since September 22, 2025 |

| Trustpilot | ~4.7–4.8 stars on ~2,000 reviews |

| Regulator | Arizona Department of Insurance and Financial Institutions (DIFI) |

Why the regulators still issue cautions

The product category — home equity contracts, HEIs, HEAs, shared appreciation agreements — sits in a gray area between investment and credit. The CFPB took three coordinated actions on January 15, 2025:

- Filed an amicus brief in Roberts v. Unlock Partnership Solutions AOI, Inc. (No. 1:24-cv-1374, D.N.J.) arguing that the specific Unlock product qualifies as a “residential mortgage loan” under TILA.

- Issued a consumer advisory warning of the complexity and risk of home equity contracts.

- Published an Issue Spotlight flagging non-standardized disclosures, difficulty comparing products, and the risk of large lump-sum repayment obligations.

The CFPB’s amicus brief was later withdrawn under the new administration in 2025. The lawsuit itself remains active. The National Consumer Law Center (May 2025) takes the strongest position in the consumer-advocacy community on this product category.

Our position: legal and operational legitimacy is necessary but not sufficient. The product is real. Whether it’s right for your specific situation is a separate question, answered by the cost and fit analysis above.

What happens when you sell, refinance, die, or reach the 10-year term?

Selling the home

This is the cleanest exit. At closing, the escrow officer pays Unlock its share from sale proceeds and Unlock releases the lien. Your share is whatever's left after paying off your first mortgage, Unlock, and selling costs.

Owner buyout (cash on hand)

You can buy back Unlock's share at any time during the 10-year term. Unlock orders a fresh appraisal, calculates the payoff, and issues a settlement statement. No prepayment penalty.

Refinance to buy out

Many homeowners settle Unlock by refinancing (cash-out refinance) or taking out a HELOC or home equity loan and using proceeds to buy Unlock out. This only works if you qualify for the new financing — the same credit or income issues that made Unlock attractive may still block traditional financing 10 years later.

Partial buyouts during the term

Unlock allows partial buyouts — a real differentiator versus Hometap or Point. Each partial buyout requires an appraisal and fees. Unlock can decline if the remaining Unlock Percentage would drop below 25% of the original (e.g., if your starting Unlock Percentage was 20%, the smallest remaining share is 5%).

Death of the homeowner

The HEA does not terminate at the homeowner's death. The estate or heirs must settle the agreement, typically by selling the home or refinancing. This matters for ADU homeowners building family housing or aging-in-place units — your heirs inherit the buyout obligation along with the property.

Term expiration (year 10)

If you reach year 10 without selling, refinancing, or buying out, settlement is required. The "Year 10 trap" is the most cited risk in customer reviews and consumer-advocacy critiques.

The damaging admission

Unlock can solve a monthly cash-flow problem today and create a settlement problem 10 years from now. The customers who chose Unlock often did so because they couldn’t qualify for traditional financing. If their credit or income hasn’t improved and their home hasn’t appreciated enough to sell into the buyout, they may be forced to sell.

This isn’t a dealbreaker. It’s a plan-this-now requirement. You need a credible exit plan documented at signing — not vague optimism.

Unlock vs HELOC, home equity loan, Hometap, Point, and Unison

Comparison table — verified May 21, 2026

| Feature | Unlock | Hometap | Point | Unison | HELOC | Home equity loan |

|---|---|---|---|---|---|---|

| Min credit score | 500 | ~600 | 500 | 620 | typically 680+ | typically 620+ |

| Income verification | None generally; rental income required for investment properties | Light | Light | Required | Full | Full |

| Term | 10 years | 10 years | up to 30 years | up to 30 years | 10-yr draw + 20-yr repay | 5–30 years |

| Max investment | $500K | Published terms vary | $600K | $500K (typical) | Varies by lender | Varies by lender |

| Origination fee | 4.9% | Published terms vary; verify | Published terms vary; verify | Published terms vary; verify | 0%–2% | 0%–5% |

| Renovation credit | Improvement Adjustment (requires documentation) | Yes | Varies by contract | Varies | N/A | N/A |

| Partial buyouts | Yes | Generally lump only | Generally lump only | Generally lump only | N/A | N/A |

| Rental property | Yes (rental income required) | Limited | Yes | Limited | Some lenders | Some lenders |

| Annualized cost cap | 19.9% ACL | Provider-specific cap | Provider-specific cap | Varies | None | None |

| State footprint | 25 states | 16 states | 27 states + DC | 24 states + DC | All 50 | All 50 |

| Monthly payments | None | None | None | None | Yes (variable) | Yes (fixed) |

| BBB rating | A+ | A+ | A+ | Varies | N/A | N/A |

| Subordinates to construction loan? | Approval required; fees may apply | Approval required | Approval required | Approval required | Varies | Varies |

Provider terms shift quarterly. Verify current terms with each provider before applying. Sources: Unlock.com; Hometap.com; Point.com; Unison FAQs. Last checked May 21, 2026.

Quick fit guide

- Choose Unlock if: Your credit is 500–620, you want partial-buyout flexibility, you own a rental property and can verify rental income, you can’t qualify for a HELOC, and you have a clear 10-year exit plan.

- Choose Hometap if: You’re planning major renovations and want explicit renovation credit, your credit is at least 600, and you’re in one of their 16 states.

- Choose Point if: You need a term longer than 10 years, your funding need is up to $600,000, or you’re in a state Point lists where Unlock isn’t available.

- Choose Unison if: Your credit is 620+, you prefer the longest possible term, and you’re in their 24-state + DC footprint.

- Choose a HELOC if: Your credit is 700+, you can handle a monthly payment, and you want the lowest mathematical cost on a flexible draw schedule.

- Choose a home equity loan if: You want a fixed lump sum with a predictable monthly payment over a defined term.

- Choose a cash-out refinance if: Your current first mortgage rate is high enough that replacing it with a new loan still makes sense.

One critical thing every comparison table misses

No HEI provider’s lien plays nicely with new construction financing. All HEAs and HEIs create the same subordination concern when you later try to take out a construction loan. Each provider’s FAQs note that subordination requires their approval and may carry fees. If your ADU isn’t built yet, the entire equity-sharing category is the wrong starting point. Use a purpose-built construction loan, HELOC drawn during construction, FHA 203(k), Fannie Mae HomeStyle Renovation, or Freddie Mac CHOICERenovation.

Affiliate disclosure: we may earn a commission from lender partners at no cost to you. Rate ranges verified at time of publication; verify your specific rate with each lender before applying.

For new ADU builds, compare construction-loan and renovation-loan paths. Real May 2026 rate ranges, qualification thresholds, and Fannie Mae’s 2024 rule update on ADU rental income.

Compare ADU Financing Paths →Should you use Unlock for a rental ADU specifically?

The single most common mistake: treating future rental income as a sure thing. ADU rents in your zip code today are a useful starting point — they are not the income an underwriter will allow you to count toward a refinance qualification 10 years from now. Lenders typically discount projected rent by 25% to account for vacancy and management costs.

Rental exit stress test — what to model

| Input | What to enter | Why it matters |

|---|---|---|

| ADU build cost | Real local cost from comparable builds | Sets your basis |

| Realistic monthly rent | Actual ADU comparables in your zip code, not the highest listing | Underwriters use comps, not aspirations |

| Vacancy assumption | 5%–8% even in tight markets | Real-world annual gap |

| Property management | 8%–12% of gross rent if not self-managing | A real recurring cost |

| Property taxes, insurance, utilities, maintenance | Annualized | Erodes net income |

| Net operating income | Gross rent − all of the above | What an underwriter counts |

| Refinance feasibility at year 10 | Project your credit, DTI, and rates at that point | The real exit question |

| Buyout amount under 0%, 3%, 5% appreciation | Use the cost matrix above | Stress test the exit |

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, regulatory approvals, and rental demand.

Documents you must review before signing an Unlock HEA

| Document or section | Question to answer before you sign |

|---|---|

| Product Guide | Do I understand the Investment Payment, Exchange Rate, and Unlock Percentage formula on a worked example for my home? |

| Forward Sale and Exchange Agreement | What exactly am I agreeing to sell or transfer? What are my obligations during the term? |

| Security Instrument | What lien type is being recorded (performance deed of trust vs. performance mortgage)? What does that mean for my future financing? |

| Investment Closing Statement | What cash do I net after the 4.9% origination fee and third-party transaction expenses? |

| Improvement Adjustment section | Exactly what documentation is required for an ADU to qualify, and who pays for the post-build appraisal? |

| Maintenance Adjustment section | What conditions or deferred maintenance could increase the Ending Home Value calculation? |

| Default and Triggering Events | What events force early settlement? (Failure to pay property taxes? Insurance? Bankruptcy? Property abandonment?) |

| Buyout procedure | What are the partial buyout rules and minimum thresholds? What fees apply to each partial buyout? |

| Subordination policy | If I later want a construction loan or HELOC, will Unlock subordinate? On what terms and at what fee? |

| State-specific addendum | Are there state-specific provisions (annualized cost caps, additional disclosures) that apply to my contract? |

| Death and inheritance | What happens to my heirs if I die during the term? |

Always get an independent attorney to review the contract before signing.

The Massachusetts Division of Banks consumer advisory has recommended this since 2018. A few hundred dollars in legal fees is the cheapest insurance policy you can buy against a 10-year contract you don’t fully understand.

Building an ADU is complicated enough without a financing structure you can’t fully model. Our free ADU Starter Kit walks you through the financing path decision, the document checklist, the questions to ask any builder, and the permit-prep timeline.

Download the Free ADU Starter Kit → (free, no obligation)How to apply and what to expect

Timeline

- Two minutes — online estimator (soft credit pull, no impact to your score)

- Same week — call with an Unlock home equity officer to discuss your situation

- 2–4 weeks — third-party appraisal and title review

- 30–60 days from application — final offer, signing, and funding

Six questions to ask before signing

- What is my exact Exchange Rate, and how was it calculated for my property?

- What is the maximum I would owe Unlock at year 5? Year 10? Under 3%, 5%, and 8% annual appreciation? Show me both the calculated share and the ACL-capped share.

- Can I see a fully-worked example settlement statement using my actual offer terms?

- What is the Improvement Adjustment documentation requirement if I add an ADU or major renovation during the term?

- What happens if I cannot pay at year 10 and my home value hasn’t increased enough to sell into the buyout?

- Will Unlock subordinate to a future HELOC or construction loan, and on what terms and fee?

Bottom line: who should consider Unlock and who should walk away

Consider Unlock if you are:

- Equity-rich with 30%+ equity in a home valued $175,000 to $3,000,000

- Credit-challenged (500–620) or unable to verify income

- Located in one of Unlock’s 25 states

- Past the construction phase, with an ADU already built and documented

- Capable of articulating a real 10-year exit plan

- Comfortable trading higher long-term cost for zero monthly payments today

Walk away from Unlock if you are:

- Funding new ADU construction (use a construction loan, HELOC, 203(k), or HomeStyle instead)

- Likely to sell or refinance within 5 years

- In a state Unlock doesn’t serve, or in a property type Unlock won’t accept

- Planning to hold the home indefinitely without a buyout plan

- Able to qualify for a HELOC or home equity loan with a manageable monthly payment

- Unable or unwilling to maintain rigorous Improvement Adjustment documentation

- Counting on speculative rental income or appreciation to fund the year-10 buyout

The Dwelling Index editorial conclusion:

An Unlock HEA is a legitimate product priced within the normal HEA cost structure, though its 4.9% origination fee is at the high end of the provider comparison in this article. Compared to the broader home equity universe, it is rarely the cheapest option mathematically, and it is almost never the right tool for funding new ADU construction. If you’re researching it because you’ve been denied a HELOC, that’s a meaningful use case. If you’re researching it because the “no monthly payment” pitch caught your attention before you compared the math, run the comparison before you commit.

Unlock home equity agreement FAQ

Is Unlock a real company?

Yes. Unlock Technologies Inc. is a Tempe, AZ-based fintech founded in 2019, NMLS-registered (#2657081), BBB-accredited with an A+ rating since September 2025, and backed by $280M from institutional investors. It has funded 20,000+ HEAs per its current About page.

Is Unlock a loan?

Unlock structures its Home Equity Agreement as a non-loan investment product — no monthly payments, no interest, no APR. However, the CFPB argued in a January 2025 amicus brief in Roberts v. Unlock that the product functions as a 'credit' transaction under the Truth in Lending Act, and several states apply mortgage-lending treatment to these contracts. The category is in regulatory gray space.

Does Unlock have monthly payments?

No monthly payments during the 10-year term. A lump-sum settlement is due at term end or when a triggering event (sale, refinance, owner buyout, default) occurs.

How much does Unlock charge upfront?

4.9% origination fee on the Investment Payment, plus third-party transaction expenses (appraisal, title, escrow, recording, credit) that vary by property. Both are deducted from your lump sum at closing.

What credit score do you need for Unlock?

500 minimum FICO. This is one of the lowest minimums in the home equity category.

Does Unlock require income verification?

No income requirement for the HEA generally. Investment-property applicants must be able to verify rental income per Unlock's FAQ.

What states is Unlock available in?

25 states as of May 21, 2026: AZ, CA, FL, HI, ID, IN, KY, MI, MO, MT, NV, NH, NJ, NM, NC, OH, OR, PA, SC, TN, UT, VT, VA, WI, WY. Unlock is not available in Washington, DC.

Can I use Unlock money to build an ADU?

You can use the cash for whatever you want, but Unlock is generally not the right tool for funding new ADU construction. The Unlock lien complicates construction financing, and unless you keep airtight Improvement Adjustment documentation, you'll share the appreciation your ADU creates with Unlock. Use a construction loan, HELOC, FHA 203(k), Fannie Mae HomeStyle, or Freddie Mac CHOICERenovation for new builds instead.

Will Unlock take part of my ADU's value?

Only if you don't document the Improvement Adjustment properly. Unlock's contract subtracts qualifying homeowner-funded improvements from the Ending Home Value before calculating Unlock's share — but only with permits, contractor invoices, plans, photos, and a defensible post-build appraisal.

Does Unlock fund prefab or modular ADUs?

Unlock does not invest in homes that are manufactured housing, mobile homes, or prefabricated homes per its FAQ. If your existing primary residence is a manufactured home, you cannot use Unlock. If your planned ADU is prefab or modular, confirm directly with Unlock whether the ADU type affects eligibility or settlement appraisal before relying on assumptions.

What happens after 10 years?

You must settle by selling the home, buying out Unlock with cash or new financing, or completing partial buyouts that satisfy the contract. If you can't, you may need to sell.

Can I pay Unlock back early?

Yes. There is no prepayment penalty. You can do a full owner buyout at any time, or partial buyouts during the term (subject to the 25% minimum remaining Unlock Percentage threshold).

What's the difference between Unlock and Hometap?

Unlock has a lower credit minimum (500 vs ~600), allows partial buyouts, and serves 25 states. Hometap offers explicit renovation credit and serves 16 states. Both have similar 10-year terms and lump-sum structures otherwise. Verify each provider's current published fee terms before applying.

Is Unlock available in Texas?

No. Unlock, Hometap, Point, and Unison do not list Texas in their current availability pages. Texas home equity rules are unusually restrictive — verify any HEI provider directly before assuming availability.

What happens if my home loses value?

Unlock shares in the loss to the extent of its percentage share, so your buyout cost is lower. But the Maintenance Adjustment provision can increase the Ending Home Value if your home is in poor condition from deferred maintenance.

Does applying hurt my credit?

No. The initial application uses a soft credit pull, which does not impact your score.

Does Unlock report to credit bureaus?

The HEA itself is not reported as a tradeline to credit bureaus, though the lien is recorded against your property in public records.

Sources and methodology

This review is built on primary-source verification with cross-checking against third-party reviewers. Where sources conflicted, we followed Unlock’s own current published materials and noted the conflict.

Primary sources (Unlock):

Refresh schedule: State availability and fee structure checked monthly. Trustpilot/BBB ratings checked quarterly. Regulatory status checked quarterly. HELOC comparison rates checked monthly during periods of rate volatility.

Not sure where to start? See what’s possible at your address.

Get Your Free ADU Report in 60 Seconds →