Hometap Review 2026: Is It a Good Way to Fund an ADU?

By the Dwelling Index Editorial Team · Published: May 21, 2026 · Last updated: May 21, 2026 · Last verified: May 21, 2026 · ~30 min read

This is an independent editorial review. We have no affiliate relationship with Hometap as of this publish date.

What we verified for this review

Primary sources consulted: Hometap official pages (homepage, How It Works, pricing blog, bad-credit guide updated October 17, 2025, application guide, renovation adjustment materials, customer stories); Massachusetts AG press release Feb 19, 2025 (mass.gov); CFPB Issue Spotlight on home equity contracts Jan 15, 2025 (consumerfinance.gov); HousingWire Aug & Dec 2025; BusinessWire Dec 9, 2025 funding announcement; ClassAction.org Feb 2026 NJ filing; BBB Hometap profile; Trustpilot.com (sampled May 2026); Curinos national rate benchmark May 17, 2026. Terms vary by contract and state; verify specifics in your offer documents.

The bottom line on Hometap for an ADU

Hometap can be a reasonable way to fund an accessory dwelling unit (ADU) when three things are true at once: you have at least 25% equity in a primary residence located in one of Hometap’s 16 currently available states — AZ, CA, FL, IN, MI, MN, MO, NV, NJ, NY, OH, OR, PA, SC, UT, or VA — you cannot or do not want to take on a new monthly payment, and you have a credible plan to settle the investment within 10 years by selling, refinancing, or paying cash. For ADU builders specifically, the most important provision in the Hometap agreement is the renovation adjustment, which Hometap says may exclude appreciation from qualifying renovations of $25,000 or more from the final settlement value, subject to documentation, appraisal, and Hometap approval.

Hometap is a poor fit if you can comfortably qualify for and afford a home equity line of credit (HELOC) or home equity loan, you live in a market expected to appreciate strongly and plan to hold past year seven, you have not yet confirmed your lot can legally support an ADU, or your state is not on Hometap’s list.

- Origination fee: 4.5% of the investment, deducted at closing.

- Term: 10 years, with no required monthly payments.

- Maximum investment: $600,000.

- Maximum equity accessed: up to 24.99% of current home value.

- Maximum Hometap return: capped at 20% annualized under the “Hometap Cap.”

Open regulatory question: Hometap is the defendant in an active Massachusetts Attorney General enforcement action filed February 19, 2025, alleging the product is an illegal reverse mortgage. Hometap disputes the claims and exited Massachusetts while the case proceeds. A separate proposed class action filed in New Jersey federal court in February 2026 is also reportedly pending. Neither case has produced a final ruling, but both signal that the regulatory treatment of home equity investments is still being written. Before you sign anything, confirm what you can legally build on your lot.

Quick-facts table

| Feature | Hometap (verified May 21, 2026) |

|---|---|

| Product type | Home Equity Investment (HEI), not a traditional loan; legal classification currently disputed in active litigation |

| Investment range | $15,000 – $600,000 |

| Max % of home value | Up to 24.99% |

| Term | 10 years |

| Origination fee | 4.5% of investment, deducted at closing |

| Required monthly payments | None during the term |

| Stated interest rate | None (Hometap takes a share of future home value instead) |

| Minimum FICO | 575 per Hometap’s October 2025 published guidance; homeowners with poor-to-fair credit (585+) may still qualify based on other underwriting factors |

| Minimum home equity | 25% |

| States served | 16 states — AZ, CA, FL, IN, MI, MN, MO, NV, NJ, NY, OH, OR, PA, SC, UT, VA |

| Maximum Hometap return | 20% annualized (the “Hometap Cap”) |

| ADU-relevant feature | Renovation adjustment — qualifying renovations ≥$25,000 may be excluded from settlement value, subject to documentation, appraisal, and Hometap approval |

| Settlement methods | Sale, refinance, buyout with savings or other funds, or replacement financing |

| Trustpilot | 4.8 / 5 from 6,800+ reviews (sampled May 2026) |

| BBB | Accredited (since 5/22/2019); B+ rating; 16 BBB complaints listed; profile flags pending Massachusetts AG action |

| Notable open litigation | Massachusetts AG enforcement action filed Feb 19, 2025 (motion to dismiss denied Aug 2025; key defenses limited Dec 2025; discovery proceeding). Separate proposed class action Greenidge et al. v. Hometap Equity Partners, LLC et al. reportedly filed in NJ federal court Feb 2026 |

| Funded volume | $2.3B+ deployed to 22,000+ homeowners as of Dec 9, 2025 announcement; current homepage lists 25,000+ funded homeowners |

| Founded / HQ | 2017, Boston, MA · CEO Jeffrey Glass |

Sources: hometap.com, bbb.org, businesswire.com (Dec 9, 2025), mass.gov AG press release Feb 19, 2025, HousingWire Aug & Dec 2025, classaction.org (Feb 2026 NJ filing), Trustpilot.com (sampled May 2026). Terms vary by contract and state; verify specifics in your offer documents.

Run your own Hometap numbers — the ADU Fit Calculator

Get your project-specific fit score in under 30 seconds. Enter your home value, existing mortgage balance, the cash you’d need from Hometap, expected hold period, local appreciation expectation, and ADU budget. We return: your projected Hometap settlement at year 3, 5, 7, and 10; the renovation-adjusted settlement assuming your ADU qualifies; the equivalent annualized cost; the comparison to a HELOC at the current Curinos benchmark; and a green/yellow/red verdict.

Output is illustrative, based on Hometap’s published X-for-Y pricing concept and the 20% Hometap Cap. Not a loan offer or guarantee of Hometap terms. Actual outcomes depend on Hometap’s underwriting, your specific contract, your home’s appraised value, and local market conditions.

Run the Hometap ADU Fit Calculator →See What You Can Build → Get Your Free ADU Report

Before any HEI, HELOC, or construction loan, get a clear picture of whether your property can support the ADU you want. We screen the local rules likely to affect your lot and flag what to verify with your planning department. Free, 60 seconds, no obligation.

Get Your Free ADU Report →Hometap review: is it worth it for building an ADU?

Hometap is worth considering for an ADU when avoiding a monthly payment matters more to you than preserving every dollar of future appreciation, and when you have a clear, written exit plan for year 10. It is rarely the first option to compare if you qualify for and can afford a HELOC or home equity loan at current rates, because debt-based financing typically preserves more of the value your ADU creates. We arrived at that framing by running the math across five reader profiles against Hometap’s published X-for-Y pricing concept and the 20% Hometap Cap.

Most general Hometap reviews on page one answer “is Hometap worth it” in the abstract. We answer it for the homeowner who’s about to spend $150,000 to $400,000 building an ADU and wants to know which financing product preserves the most of that new equity. Those are different questions, and the answers diverge sharply at the renovation adjustment.

When Hometap may be the right fit for your ADU

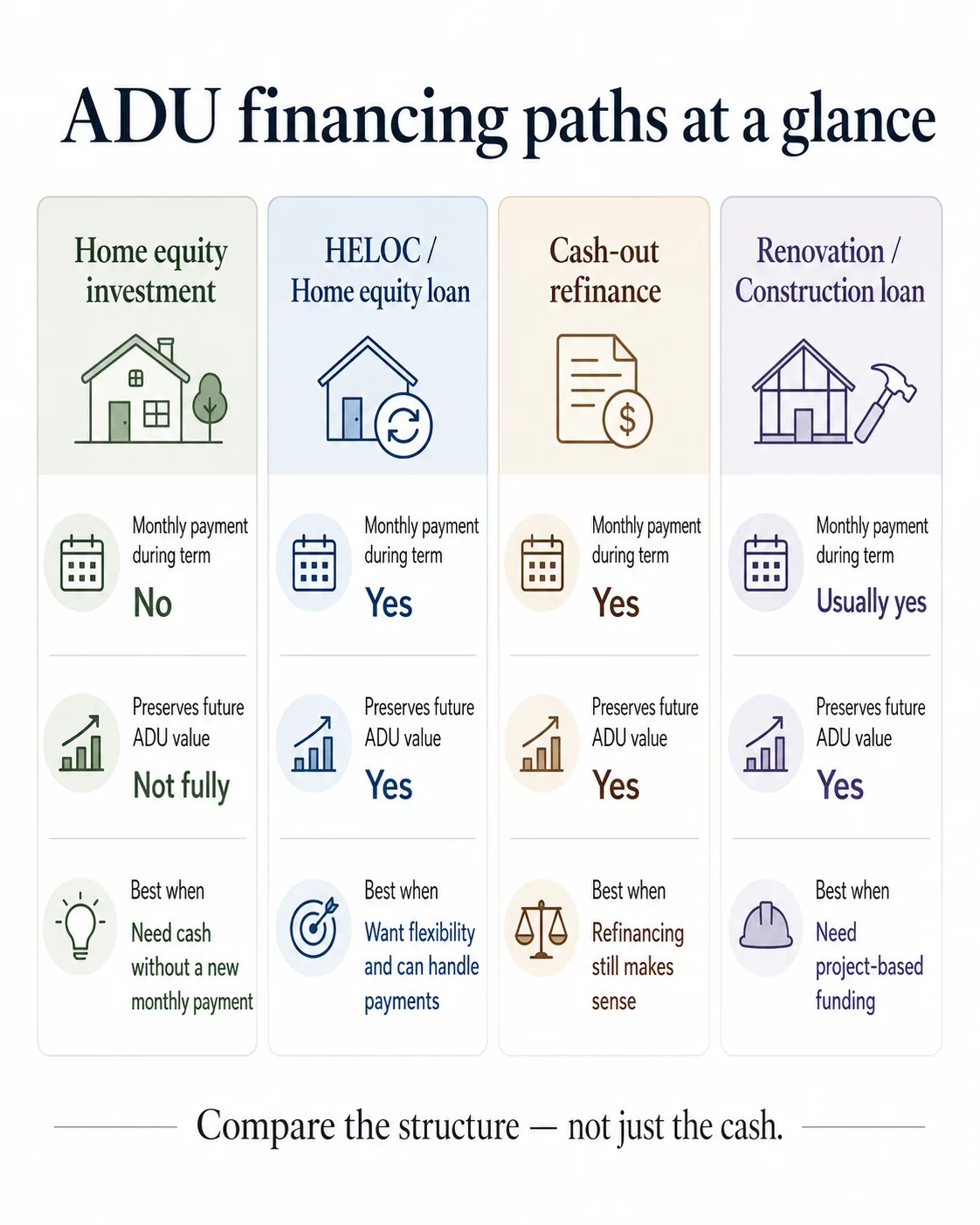

The pattern we see most often in ADU financing is the pandemic-rate protector. This homeowner refinanced or bought in 2020 or 2021 and is now sitting on a 2.75% to 3.5% first mortgage. The Curinos national average HELOC rate as of May 17, 2026 sits at 7.21%, and the national home equity loan average at 7.36%. A cash-out refinance to fund an ADU would mean replacing that sub-4% first mortgage with a new first mortgage in the mid-6% range, which on a typical $400,000 balance can cost more in additional lifetime interest than the ADU itself. For this homeowner, a HELOC or home equity loan that sits in second position is usually the right answer, because it preserves the favorable first mortgage. But if their debt-to-income (DTI) ratio is tight, if their income is self-employed and hard to document, or if they simply do not want a new payment, Hometap’s no-monthly-payment structure becomes a defensible alternative.

The second pattern is the DTI-disqualified homeowner. They have plenty of equity. They have a good credit score. They cannot qualify for a HELOC because their bank wants 43% maximum DTI and their other obligations push them over. Hometap has no stated income or DTI requirement — it underwrites the property and equity position, not the household budget. That makes Hometap a real option for self-employed homeowners, retirees living on portfolio income, and homeowners between jobs.

The third pattern is the near-term seller. This homeowner plans to sell within 3 to 5 years and wants to use the proceeds of an ADU build to maximize the sale price. Hometap can be structurally useful here because settling early — through the sale — caps the dollar amount of future appreciation exposed to the Hometap share. Long holds in strongly appreciating markets create the largest dollar settlement risk; early settlements limit that exposure, even though the effective annualized cost can still be high.

When to compare other ADU financing paths first

Hometap is the wrong starting point if you check any of these boxes: you qualify cleanly for a HELOC or home equity loan and your payment-capacity math works at the current Curinos benchmark; you live in a market with strong expected appreciation and plan to hold for ten years or more; you have not yet confirmed your lot can legally support an ADU; your state is not on Hometap’s 16-state list; or you want to keep every dollar of the appreciation your ADU build creates.

There is one more category worth naming: anyone who cannot articulate, in writing, the exit plan for year 10. Hometap describes the available settlement paths — sale, refinance, savings or other funds, or replacement financing — but it is the homeowner’s responsibility to make one of them realistic. If none of those work, the recorded lien gives Hometap the contractual right to recover its investment, which can include working with the homeowner to sell the property per Hometap’s published footer language. That is not unique to Hometap; it is part of how home equity contracts work as a category, and the Consumer Financial Protection Bureau (CFPB) called it out specifically in its January 15, 2025 Issue Spotlight on home equity contracts.

See What You Can Build → Get Your Free ADU Report

Before you choose Hometap, a HELOC, or any other financing path, find out what’s likely buildable on your lot. Setbacks, lot coverage, owner-occupancy rules, utility laterals, and fire-zone overlays end more ADU projects than financing does. We screen the local rules and flag what to verify with your planning department.

Get Your Free ADU Report →How does Hometap actually work?

Hometap is a Boston-based fintech company founded in 2017 that offers a home equity investment (HEI). The homeowner receives a lump sum of cash today in exchange for a percentage of the home’s value at the end of a 10-year term, with no monthly payments and no stated interest rate. Hometap records a lien against the property — a mortgage or deed of trust — to secure its interest, and the homeowner settles by selling the home, refinancing, paying from savings or other funds, or rolling into replacement financing within ten years. As of Hometap’s December 9, 2025 announcement of $50 million in new funding from Gallatin Point Capital, Hometap has deployed more than $2.3 billion to over 22,000 homeowners since 2017. Hometap’s current homepage lists 25,000+ funded homeowners.

A home equity investment, often shortened to HEI, is also called a home equity agreement (HEA), shared appreciation agreement, or home equity contract. The CFPB uses “home equity contract” in its regulatory writing. All these names point to the same product structure: cash now in exchange for a percentage of future home value, secured by a recorded lien, with no required monthly payment during the term. The legal classification of these products is currently disputed. The Massachusetts AG action against Hometap and the CFPB’s January 2025 actions on the category both raise the question of whether HEIs should be treated as mortgage loans for regulatory purposes.

The five-step Hometap process

The process Hometap publishes runs five steps, cross-referenced against the timelines homeowners reported on the Better Business Bureau and Sitejabber over the last 18 months.

- Online estimate. You enter property and basic financial information through Hometap’s site. Hometap performs a soft credit pull and an automated valuation model (AVM) check. The estimate quotes an investment range and an indicative Hometap share. This step takes a few minutes and does not affect your credit score.

- Application. If you accept the estimate, you submit a formal application. Documents Hometap typically requests include a government ID, your most recent mortgage statement, a homeowner’s insurance declaration page, and an HOA statement if applicable. A hard credit pull occurs at this stage.

- Appraisal and valuation. Hometap orders a third-party appraisal of the property. Reports from recent applicants put appraisal fees in the $300 to $600 range; some homeowners report Hometap covered the appraisal. The appraisal determines the contract’s starting home value, used to calculate the Hometap share at settlement.

- Final offer. After underwriting and appraisal, Hometap issues a binding offer with the exact investment amount and the exact percentage of the future value Hometap will receive at settlement under each scenario.

- Closing, rescission, and funding. You sign the agreement and the lien-recording documents. A rescission period applies in most states. Funds are wired after rescission expires. Hometap publishes a target of about three weeks from application to funded; homeowner-reported timelines in BBB complaint narratives range from three weeks to three months. We recommend budgeting 6–10 weeks rather than relying on the 3-week target.

What “no monthly payment” really means

This is the line that sells Hometap, and it is true at face value: there are no required monthly payments during the term. There is no interest accrual on a balance, no draw period, no amortization schedule. What that phrase does not mean is “no cost.” The cost is the share of future home value that Hometap collects at settlement. That number is uncertain at signing and depends on how much your home appreciates and when you settle. In a flat market with an early settlement, Hometap’s total dollar cost can be moderate. In a 6%+ annual appreciation market held to year 10, Hometap is usually meaningfully more expensive than the equivalent HELOC — until the Hometap Cap engages.

The CFPB’s January 15, 2025 Issue Spotlight on home equity contracts singled out exactly this issue: HEI products use nonstandard disclosures, calculate the final amount owed differently across providers, and operate outside the Truth in Lending Act framework that governs HELOCs and cash-out refinances. These are not Hometap-specific findings — they apply to the HEI category — but they are the regulatory reason this product warrants careful reading of the actual contract, not just the marketing language.

The four settlement paths Hometap describes

At or before the end of the 10-year term, you settle the investment. Hometap describes four available paths:

- Sale of the home. Hometap is paid from sale proceeds at closing. This is the cleanest exit and the one Hometap’s own materials describe most prominently.

- Refinance and pay off. You take a cash-out refinance or a new HELOC and use the proceeds to buy out Hometap’s share. This requires you to qualify for the new loan at then-current rates and equity levels.

- Buyout with savings or other funds. Less common in practice, because the settlement amount is often well into six figures.

- Replacement financing. Some homeowners settle a maturing Hometap investment by taking a new HEI from Hometap or a competitor. The CFPB Issue Spotlight flagged this as a particular consumer-risk pattern because it can compound effective cost.

Important: If none of these paths is feasible, Hometap’s published footer says it may “exercise its right to acquire a percent ownership interest and work with the homeowner to sell the property.” The contract is enforceable through the recorded lien.

How much does Hometap really cost? The X-for-Y pricing decoded

Hometap uses a tiered “X-for-Y” pricing structure published on its own pricing-blog page. In exchange for cash equal to X% of your home’s current value, Hometap is entitled to Y% of your home’s value at settlement, where Y is consistently larger than X. As an illustrative example Hometap publishes, taking 10% of current home value as cash today is paired with Hometap receiving roughly 15% of home value at settlement during years 0–3, with the share scaling higher as the term runs longer. There is also a 4.5% origination fee deducted from your investment proceeds at closing. Whether the effective cost is competitive with a HELOC depends almost entirely on how much your home appreciates and when you settle.

No general Hometap review on page one currently shows this math in actual dollars across multiple scenarios. That is the gap we are closing.

The 4.5% origination fee and what else comes out at closing

The headline cost is the 4.5% origination fee deducted from your investment proceeds at closing. On a $50,000 Hometap investment, that is $2,250 out of your gross. On a $150,000 investment, it is $6,750. You do not pay this out of pocket; Hometap takes it from the disbursement. In addition to the origination fee, expect standard third-party closing costs: an appraisal in the $300 to $600 range (sometimes covered by Hometap), title-related charges, government recording fees for the lien, and any required attorney or notary fees in attorney states.

The X-for-Y model: worked dollar examples

Assume a primary residence currently appraised at $700,000, with a $300,000 first mortgage and the homeowner taking a $70,000 Hometap investment (10% of current value). After the 4.5% origination fee ($3,150), net cash to the homeowner is approximately $66,850 before any other closing costs.

| Hold period | 0% annual appreciation | 4% annual appreciation | 8% annual appreciation |

|---|---|---|---|

| Year 3 settlement | Home $700K · ~15% = $105,000 settlement · Cost: ~$38,150 | Home $787K · ~15% = $118,100 · Cost: ~$51,250 | Home $882K · ~15% = $132,300 · Cost: ~$65,450 |

| Year 5 settlement | Home $700K · ~17% = $119,000 · Cost: ~$52,150 | Home $852K · ~17% = $144,800 · Cost: ~$77,950 | Home $1,028K · ~17% = $174,800 · Cost: ~$107,950 |

| Year 7 settlement | Home $700K · ~19% = $133,000 · Cost: ~$66,150 | Home $921K · ~19% = $175,000 · Cost: ~$108,150 | Home $1,200K · ~19% = $228,100 · Cost: ~$161,250 |

| Year 10 settlement | Home $700K · ~20% = $140,000 · Cost: ~$73,150 | Home $1,036K · ~20% = $207,200 · Cost: ~$140,350 | Home $1,511K · ~20% = $302,300 · Cost: ~$235,450 |

Illustrative only. “Cost above net proceeds” subtracts the $66,850 net cash received from the settlement amount. Numbers are rounded. The later-year share percentages (17%, 19%, 20%) are assumptions consistent with Hometap’s published tiered-pricing concept; verify your actual contract share percentages in your Hometap offer documents. Not a loan offer or guarantee of Hometap terms. Source: hometap.com/blog/how-hometap-pricing-works, verified May 21, 2026.

Effective annualized cost — what is the Hometap “interest rate”?

Hometap does not charge a stated interest rate, but you can back-calculate one. Using the year-7 / 4% scenario above: $175,000 settlement on a $70,000 gross Hometap investment over 7 years produces roughly a 14% annualized internal rate of return (IRR) for Hometap.

- Year 3 / 4% appreciation: $118,100 on $70,000 in 3 years ≈ 19% annualized IRR

- Year 5 / 4% appreciation: $144,800 on $70,000 in 5 years ≈ 16% annualized IRR

- Year 7 / 4% appreciation: $175,000 on $70,000 in 7 years ≈ 14% annualized IRR

- Year 10 / 4% appreciation: $207,200 on $70,000 in 10 years ≈ 11% annualized IRR

- Year 10 / 0% appreciation: $140,000 on $70,000 in 10 years ≈ 7% annualized IRR

Compare to the Curinos national average HELOC rate of 7.21% and home equity loan rate of 7.36% as of May 17, 2026. Hometap is typically more expensive than a HELOC on an effective-annualized-cost basis, especially in early-settlement or high-appreciation scenarios. The Hometap value proposition is not lower cost — it is structural: no monthly payment, no income or DTI requirement, no rate-rise risk on a variable-rate product, and the option to preserve a favorable first mortgage.

The Hometap Cap is the consumer-protection feature that limits Hometap’s annualized return to 20%. In most scenarios with moderate appreciation and a mid-term settlement, the cap does not engage. Confirm exactly how the cap is calculated in your specific contract.

Can you use Hometap to build an ADU?

Yes. Hometap publicly lists home improvements and renovations among the use cases its investment can fund, and Hometap publishes a customer story featuring a Los Angeles homeowner who used a Hometap investment to fund a detached ADU and a junior accessory dwelling unit on his property. The structural fit is strong — ADUs are exactly the kind of large-ticket, lump-sum-funded project that Hometap’s product is sized for, and the absence of a monthly payment during construction can ease cash flow pressure when contractor draws are landing every few weeks. What matters more than whether Hometap is technically available for an ADU is whether the renovation adjustment in your specific contract will protect the value your ADU creates from being included in the final settlement math.

For context, detached ADUs in California metros frequently run $300–$500 per square foot all-in, with a typical 600-square-foot one-bedroom detached unit landing in the $180,000–$300,000 range before sitework surprises. Garage conversions can land at $100,000–$200,000. See our ADU Cost Per Square Foot guide for full 2026 methodology.

Why ADUs are not ordinary renovations

For financing purposes, ADUs differ from kitchen remodels and bathroom updates in five ways that matter:

- Zoning and permit risk. An ADU needs zoning approval, setback compliance, lot coverage compliance, parking analysis, possibly owner-occupancy compliance, utility-lateral capacity confirmation, and in some jurisdictions, design review or historic-district review. Any one of these can block the build after you have already borrowed the money. Financing first is the wrong sequence.

- Utility upgrade risk. Many ADU builds trigger water, sewer, electrical, or gas-service upgrades the homeowner did not budget for. Unexpected utility-upgrade costs between $15,000 and $40,000 appear in a meaningful share of detached ADU projects in California metros.

- Variable cost-per-square-foot. ADU cost-per-square-foot has enormous range — from $200/sf for a prefab on a flat, served lot to $600/sf for a custom detached unit on a sloped, fire-zone parcel needing fire sprinklers and defensible-space landscaping.

- Time-to-completion. A typical detached ADU project runs roughly 9–14 months from permit issuance to certificate of occupancy in California-metro datasets. That timing matters for the Hometap renovation adjustment, which requires a completed renovation that can be separately appraised.

- Rental income variability. If your ADU underwriting depends on rental income, your settlement math depends on whether the rental income materializes as projected. These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

When Hometap funding may not be enough

For a $250,000 detached ADU build in a high-cost metro, Hometap may fund only a portion of total project cost depending on the homeowner’s equity. Hometap caps investments at the lesser of $600,000 or roughly 24.99% of current home value. A homeowner with a $700,000 home can access up to roughly $175,000 from Hometap — meaningful, but not enough for a full-cost detached ADU in some markets. In those cases, layered financing (Hometap plus owner cash plus a small construction loan) becomes the practical structure. That layering complicates underwriting, because Hometap typically requires consent before you take on additional liens during the term. Confirm the consent process in writing before signing.

Check Your ADU Feasibility First → Get Your Free ADU Report

The renovation adjustment only matters if the ADU can actually be permitted and built. Setbacks, fire-zone overlays, owner-occupancy rules, parking minimums, and utility-lateral capacity end more ADU projects than any financing product ever will. Our free 60-second screen flags what to verify locally.

Get Your Free ADU Report →Will Hometap share in the value your ADU creates? The renovation adjustment, decoded

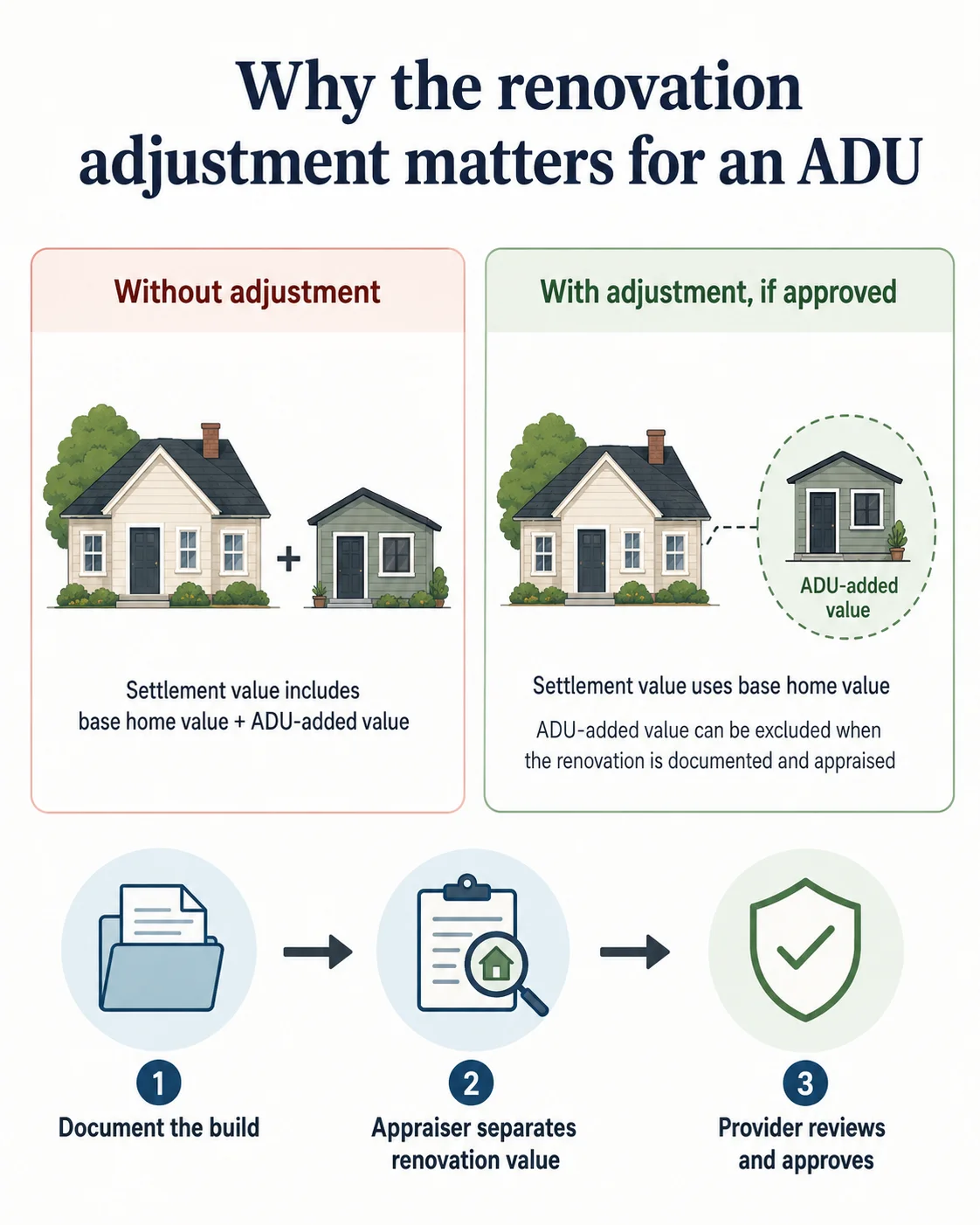

This is the most important section of any Hometap review written for an ADU builder, and it is the section every general Hometap review buries in a single paragraph. Hometap’s renovation adjustment is a contractual provision that may exclude the value increase from a qualifying renovation of $25,000 or more from the home value used to calculate Hometap’s settlement share, provided the homeowner documents the work and the appraiser at settlement can separate market appreciation from renovation-driven appreciation. For an ADU build that typically adds $100,000 to $300,000 in appraised value, this provision can be the difference between Hometap being competitive with a HELOC and Hometap being meaningfully more expensive over a 10-year hold.

The renovation adjustment is described in Hometap’s published materials and discussed in Hometap-published customer stories. It is real. It is also not automatic. Approval requires documentation, an appraiser’s specific methodology for isolating renovation value, and Hometap’s review and acceptance at settlement.

How the renovation adjustment works in dollars

Walking the same $700,000 home and $70,000 Hometap investment through a year-7 settlement: assume a $200,000 detached ADU that adds $160,000 in appraised value at settlement, in a market where underlying home value (without the ADU) appreciated at 4% annually.

Without the renovation adjustment

- Home value at year 7 (with ADU): $1,081,200

- Hometap’s ~19% share: $205,400

- Cost above net proceeds: ~$138,550

With the renovation adjustment applied

- Settlement value (ADU excluded): $921,200

- Hometap’s ~19% share: $175,000

- Cost above net proceeds: ~$108,150

- Homeowner savings: ~$30,400

| Hold period | Without adjustment | With adjustment | Homeowner savings |

|---|---|---|---|

| Year 3 | ~$142,100 | ~$118,100 | ~$24,000 |

| Year 5 | ~$172,000 | ~$144,800 | ~$27,200 |

| Year 7 | ~$205,400 | ~$175,000 | ~$30,400 |

| Year 10 | ~$239,400 | ~$207,200 | ~$32,200 |

Illustrative only. Assumes 4% annual baseline appreciation, $160,000 appraised value increase from a qualifying $200,000 ADU build, and renovation-adjustment approval by Hometap. Not a loan offer or guarantee of Hometap terms. Source: Hometap published materials, verified May 21, 2026.

The ADU documentation checklist for the renovation adjustment

| Document | Why it matters |

|---|---|

| ADU building permit application and issued permit | Establishes the renovation as a legal, permitted improvement |

| Stamped architectural and structural plans | Documents scope, square footage, and project specifications |

| Signed contractor agreement and change orders | Shows what was built and at what cost |

| All paid invoices and receipts (materials, labor, fixtures) | Substantiates the $25,000+ qualifying-renovation threshold and total spend |

| Date-stamped before, during, and after photos | Helps the appraiser distinguish ADU value from baseline home value |

| Final inspection sign-offs and certificate of occupancy | Confirms completion and code compliance |

| As-built appraisal or appraiser memo isolating ADU-driven value | The core evidence Hometap needs for the renovation-adjustment calculation |

| Written confirmation from Hometap that your specific ADU qualifies | Critical — request this in writing before signing, not at settlement |

Is Hometap legit? The BBB rating, Trustpilot reviews, and the lawsuit explained

Hometap is a legitimate, BBB-accredited fintech company with verifiable NMLS-listed entities, $2.3 billion in deployed capital across 22,000+ homeowners as of its December 2025 announcement, a B+ BBB rating with 16 complaints listed, and a Trustpilot rating of 4.8 out of 5 from 6,800+ reviews sampled in May 2026. It is also the defendant in an active enforcement action filed by the Massachusetts Attorney General on February 19, 2025, and the defendant in a separate proposed class action reportedly filed in New Jersey federal court in February 2026. Neither case has produced a final ruling. Hometap denies the allegations.

What the Trustpilot 4.8/5 actually tells you

Hometap’s Trustpilot profile shows 4.8 out of 5 stars across 6,800+ reviews sampled in May 2026. The pattern is consistent: customers overwhelmingly praise the Investment Manager relationship, the clarity of the up-front pricing presentation, and the speed of the initial estimate. What Trustpilot does not yet tell you is how Hometap customers experience the settlement end of the contract. Because Hometap was founded in 2017, the first cohorts of customers are only now reaching the natural 10-year settlement point. The customer-service experience at origination is well-documented; the customer-service experience at settlement in a high-appreciation market is mostly speculative. Trustpilot is useful for origination-stage customer sentiment, not as proof Hometap is the right product for an ADU.

Hometap’s BBB rating: B+ with 16 listed complaints

Hometap’s BBB profile, sampled May 2026, shows the company is BBB-accredited since May 22, 2019, holds a B+ rating, and has 16 complaints listed. The BBB profile also displays a “Pending Government Action” notice referencing the Massachusetts AG enforcement action. Verify both the BBB rating and the pending-action notice directly at the BBB profile before any decision.

What Hometap complaints say

From publicly available BBB complaint narratives and Sitejabber 1- and 2-star reviews from the last 18 months, three consistent patterns emerge:

- Timeline drift. Multiple complaint narratives describe applications that took 8–14 weeks against an expected ~3-week target.

- Late-stage disqualification. A smaller cluster describes homeowners who completed full applications, paid for appraisals, and were declined at the end of underwriting — often for reasons related to title structure (LLC ownership), recent late mortgage payments, or property-condition issues.

- Investment Manager turnover. Some reviewers report being reassigned to multiple Investment Managers during a single application, complicating communication.

None of these are universal experiences, and they should be weighed against the 6,800+ positive reviews. They are real, however, and worth budgeting time for. Treat Hometap’s published 3-week timeline as a best-case scenario and plan for 6–10 weeks.

The Hometap Massachusetts AG lawsuit, explained

On February 19, 2025, Massachusetts Attorney General Andrea Joy Campbell filed a 45-page enforcement action against Hometap Equity Partners LLC in Suffolk County Superior Court, alleging Hometap “pervasively and systematically violated the state’s consumer protection laws, including mortgage and foreclosure prevention laws.”

| AG allegation | Plain English | Hometap response |

|---|---|---|

| “Unlawfully high interest” | The AG argues the effective return Hometap collects equates to an interest rate exceeding Massachusetts usury limits | Hometap denies it charges interest; asserts the product is an investment in future value, not a loan |

| “Inadequate underwriting” | Hometap markets to “house rich, cash poor” homeowners without assessing whether they can realistically settle in 10 years | Hometap argues its underwriting uses property and market data rather than income/DTI, which is the structural feature of the HEI product class |

| “Illegal reverse mortgages” | The AG contends Hometap’s product meets the legal definition of a reverse mortgage under Massachusetts law | Hometap rejects the reverse-mortgage characterization and argues the Massachusetts Division of Banks did not raise this concern between 2018 and 2024 |

| “Deceptive concealment of cost” | The AG argues Hometap’s marketing emphasizes “no monthly payment” while obscuring the magnitude of the future settlement obligation | Hometap argues its disclosures show worst-case and best-case scenarios in plain language |

Procedural status of the Massachusetts AG case

| Date | Event | Source |

|---|---|---|

| Feb 19, 2025 | AG files complaint in Suffolk Superior Court | mass.gov AG press release |

| Mid-2025 | Hometap exits Massachusetts market during pendency | HousingWire |

| Aug 26, 2025 | Suffolk County judge denies Hometap’s motion to dismiss | National Mortgage News; HousingWire |

| Dec 2025 | Court limits Hometap’s use of prior regulator interactions as a defense; allows limited discovery on what Hometap was told by regulators | HousingWire, December 2025 |

| Feb 2026 | Proposed class action Greenidge et al. v. Hometap Equity Partners, LLC et al. reportedly filed in NJ federal court | ClassAction.org reporting |

| May 21, 2026 | No verdict; no settlement; no public trial date | n/a |

Note: The Massachusetts AG action is a Massachusetts enforcement action and has not produced a final ruling invalidating Hometap contracts in other states. Hometap continues to originate in its other 16 served states. Read the contract carefully; if you have doubts, consult a real estate attorney before signing. This is YMYL-adjacent financial content; we are not your lawyer.

Hometap eligibility requirements and state availability in 2026

Hometap requires a minimum of 25% home equity, a minimum credit score of 575 (per Hometap’s October 2025 published guidance), and a property located in one of 16 currently served states. There are no stated income, employment, or DTI requirements, which is the structural feature that makes Hometap accessible to self-employed homeowners, retirees, and homeowners between jobs who would not qualify for traditional debt-based equity products.

Hometap state availability as of May 21, 2026

| State | ADU context (verify local rules) |

|---|---|

| Arizona (AZ) | No statewide ADU mandate; permissibility varies by city. Phoenix, Tucson, Mesa, and Scottsdale have ADU ordinances of varying restrictiveness. |

| California (CA) | Statewide ADU framework under AB 68 (2019), AB 2221 (2022), and subsequent legislation. ADUs are broadly by-right on most single-family lots. Highest-volume Hometap-for-ADU state. |

| Florida (FL) | No statewide ADU right; permissibility varies by city. Miami-Dade, Orange County, Hillsborough County, and individual municipalities differ sharply. |

| Indiana (IN) | No statewide ADU mandate; local zoning controls. |

| Michigan (MI) | No statewide ADU mandate; local zoning controls. |

| Minnesota (MN) | No statewide mandate; Minneapolis and St. Paul have enabling ordinances. |

| Missouri (MO) | No statewide mandate; local zoning controls. |

| Nevada (NV) | No statewide mandate; Las Vegas, Reno, and Henderson have differing ADU rules. |

| New Jersey (NJ) | No statewide mandate; municipality-by-municipality. |

| New York (NY) | No statewide mandate; NYC, Long Island, and upstate differ sharply. |

| Ohio (OH) | No statewide mandate; Columbus and Cincinnati have varying frameworks. |

| Oregon (OR) | Strong statewide ADU framework under HB 2001 (2019); ADUs broadly permitted in cities of 2,500+. |

| Pennsylvania (PA) | No statewide mandate; Philadelphia and Pittsburgh differ from rural townships. |

| South Carolina (SC) | No statewide mandate; local zoning controls. |

| Utah (UT) | Some statewide enabling legislation; Salt Lake City, Provo, and other municipalities have detailed local frameworks. |

| Virginia (VA) | No statewide mandate; Northern Virginia counties differ from Richmond and Tidewater. |

State availability sourced from cross-referenced Hometap official disclosures and HousingWire coverage of Hometap’s 16-state operating footprint (November 2025). ADU context is summary-level only — see our state ADU regulation library for underlying statute and city-ordinance citations.

If your state isn’t on the list (including Texas, Georgia, Colorado, Illinois, Tennessee, Maryland, Washington, North Carolina, and most of the Northeast outside NY/NJ/PA), Hometap is not an option for you today. Your alternatives include other HEI providers (Point, Unlock, Unison), traditional debt-based ADU financing (HELOCs, home equity loans, cash-out refinances, construction loans), and renovation-aware financing that underwrites against post-renovation home value.

Hometap eligibility checklist

- At least 25% home equity at appraisal-determined value

- Minimum FICO of 575 per Hometap’s October 2025 guidance; 585+ may still qualify based on broader underwriting

- Property type — single-family home, condo, or townhome as primary residence; investment property under separate rules

- No active mortgage delinquency — typically no 30-day-or-more late payments in the recent past

- Title held in homeowner’s individual name or revocable living trust — properties titled in LLCs or corporate entities are typically disqualified, which surprises some applicants late in the process

- Property in good condition — significant deferred maintenance can disqualify

- Manufactured homes — eligible in some cases, not eligible in flood zones

- Flood-zone properties — eligible if you maintain flood insurance throughout the term

Compare ADU financing options side-by-side

Through Mortgage Research Center, you can compare HELOC, cash-out refinance, construction-loan, and renovation-loan options from multiple lenders.

Affiliate link — see disclosure. Not a guarantee of approval, savings, or specific rates.

Compare ADU Mortgage Options →The honest downsides of Hometap

The five real risks of a Hometap investment, stated plainly: the balloon settlement obligation at year 10; the uncertainty of the final settlement amount in appreciating markets; the recorded lien and consent-to-encumber clause that constrains additional financing during the term; the inconsistent customer-service experience reported by a meaningful minority of applicants; and the open regulatory question signaled by the Massachusetts AG action, the February 2026 NJ proposed class action, and the CFPB’s January 2025 Issue Spotlight on home equity contracts.

Risk 1 — The balloon settlement at year 10

Hometap is a 10-year contract with a single balloon settlement at the end, calculated as a percentage of your home’s value at settlement. If your plan to sell or refinance does not materialize at year 10, you have three remaining options: pay from savings (rarely realistic at the settlement amounts most contracts produce), take a new HEI to replace the maturing one (compounding effective cost), or face a forced sale under the recorded lien. The CFPB Issue Spotlight on home equity contracts highlighted exactly this risk profile as the central concern with HEI products as a category.

The honest trade-off: Hometap’s biggest benefit — no monthly payment — is also the source of its biggest risk. By deferring all cost to a single future balloon, you avoid budget pressure now in exchange for a much larger uncertain obligation later. For a homeowner with a clear sale or refinance plan, that is a reasonable trade. For a homeowner planning to age in place with no exit, it is dangerous.

Risk 2 — The cost is back-loaded and uncertain

Unlike a HELOC where you know the variable rate and can model the payment, the Hometap cost is determined by a future home value you cannot predict at signing. The Hometap Cap at 20% annualized provides a ceiling, but the ceiling itself can be expensive in dollar terms on a long hold in a strong market.

Risk 3 — The recorded lien and consent-to-encumber restrictions

Hometap records a mortgage or deed of trust against the property at closing. During the 10-year term, taking on most additional liens (a HELOC, a second mortgage, a renovation loan beyond a small amount) typically requires Hometap’s written consent. This can constrain refinancing options, complicate emergency-cash-out scenarios, and require coordination during an ADU build if the project budget exceeds the original Hometap investment and additional financing is needed.

Risk 4 — Customer-service inconsistency at edge cases

The macro Trustpilot rating is overwhelmingly positive. The micro picture from BBB complaint narratives and Sitejabber 1- and 2-star reviews shows three real patterns: applications that stretched 8 to 14 weeks against the published 3-week target; late-stage disqualifications after appraisals had been paid for; and multiple Investment Manager handoffs that complicated communication. These are not universal experiences but they happen often enough to budget for. Treat Hometap’s 3-week target as a best-case and plan for 6–10 weeks.

Risk 5 — Open regulatory and legal questions

The Massachusetts AG action and the February 2026 NJ proposed class action together signal that the legal classification of HEI products — investment versus loan — is not settled. The CFPB’s January 15, 2025 Issue Spotlight, consumer advisory, and amicus brief (later withdrawn) all reflected the agency’s interest in the consumer-protection issues raised by the category. Whatever you sign today may be the subject of state-by-state rulemaking over the next 24–36 months. Read the contract carefully and consider consulting a real estate attorney before signing.

Hometap customer reviews — what people actually say

Across 6,800+ Trustpilot reviews, the publicly available BBB complaint records (16 listed on the current BBB profile), and other review platforms, the Hometap customer experience clusters into three distinct patterns: highly positive application-stage experiences (the modal review), application-process frustration among a meaningful minority, and very few reviews so far from customers who have actually reached settlement in the 10-year term.

What consistently positive reviews emphasize

- The Investment Manager relationship as the single most-praised element of the experience. Reviews repeatedly name specific employees and describe a personal, patient approach to a complex product.

- The clarity of the up-front pricing presentation. Multiple reviewers note that Hometap walked them through worst-case and best-case scenarios with real numbers before asking them to commit.

- The speed and simplicity of the initial online estimate.

- The absence of monthly payments and the relief that produced for cash-flow-constrained households.

- The product’s accessibility for self-employed homeowners and those declined by traditional HELOCs.

What consistently negative reviews emphasize

- Timeline drift. Multiple BBB complaint narratives describe applications that took 8–14 weeks against an expected 3-week target.

- Late-stage disqualification. A smaller cluster of complaints describes homeowners who completed full applications, paid for appraisals, and were declined at the end of underwriting.

- Difficulty reaching humans during slow periods. A subset of reviewers report long callback times and difficulty escalating issues.

The Hometap-published ADU customer story

Hometap publishes a customer story on its own site featuring Matthew C., a Los Angeles homeowner who used a Hometap investment to fund a detached ADU and a junior accessory dwelling unit on his property. Matthew describes the renovation adjustment as the deciding factor in choosing Hometap over a competing HEI provider. We treat this as a Hometap-published customer testimonial — useful as anecdotal voice on what the renovation-adjustment provision is intended to do, but not as proof that results are typical. Hometap selected and published the story, and the customer received the renovation adjustment in the specific facts of that case.

What no Hometap review can tell you yet

Because Hometap was founded in 2017, the first cohorts of customers are only now reaching the natural 10-year settlement point. There is not yet a large public corpus of reviews from customers who completed a full 10-year cycle, settled in a strong-appreciation market, and reported on the experience. The Trustpilot picture is overwhelmingly an origination-experience picture, not a full-lifecycle picture. We expect the review landscape to shift meaningfully over the next 24 months as more 10-year settlements occur.

Who should not use Hometap for an ADU?

Do not use Hometap for an ADU if any of these apply: you haven’t confirmed the ADU is legal on your lot; you can qualify for and comfortably afford a HELOC or home equity loan at current rates; you plan to hold the home for ten or more years in a market expected to appreciate strongly; you do not have a clear, written exit plan for year 10; you’re relying on uncertain future rental income to justify the cost; you live in a state Hometap doesn’t serve; or you can’t articulate the X-for-Y settlement math in your own words.

| You should pause Hometap consideration if… | Better next step |

|---|---|

| You haven’t run a feasibility check on the ADU | Run the free 60-second ADU Eligibility Check before any financing decision |

| You qualify for a HELOC and can afford the payment | Compare debt-based options first — see our ADU Financing Options guide |

| You plan to hold the home for 10+ years | The cumulative cost of Hometap in a long hold typically exceeds debt alternatives |

| You can’t explain the settlement formula in your own words | Ask Hometap for three written example settlements before committing |

| You’re relying on uncertain future rent to justify the cost | Build a conservative pro forma assuming no rental income for years 1–2 |

| You can’t document a $25,000+ qualifying renovation | The renovation adjustment becomes unavailable; the math gets worse |

| Your state isn’t on Hometap’s 16-state list | Explore HELOC or another HEI provider after checking state availability |

| Title to the property is held in an LLC | Hometap typically disqualifies LLC-titled properties; consider personal-name retitling or a different financing path |

What should you ask Hometap in writing before signing?

Before signing any Hometap agreement — especially one intended to fund an ADU — get written answers from your Investment Manager to a specific set of questions covering settlement math, the renovation adjustment, the lien structure, default and forced-sale terms, the refinance-during-term consent process, and the appraisal dispute process. Phone answers are not enough. Email answers are evidence.

Settlement math (4 questions)

- What exact percentage of my home’s future value will Hometap receive at settlement? Please confirm this figure in writing and tell me whether it changes by year of settlement.

- Show me three example settlement calculations: settlement at year 3, year 5, and year 10, using my actual home value and appreciation rates of 0%, 4%, and 8% annually.

- At what specific home value does the Hometap Cap engage in my contract? Please show me the breakpoint math.

- What is the absolute maximum I could owe Hometap at settlement under my contract terms? What is the absolute minimum (assuming home declines in value)?

Renovation adjustment for the ADU (4 questions)

- Will a detached ADU on this property qualify for a renovation adjustment at settlement, assuming I document the build per your stated requirements?

- If I build a garage conversion ADU instead of a detached ADU, does the treatment differ?

- If the ADU is permitted and started during the term but not finished by my settlement date, what happens?

- Who selects the appraiser at settlement, and can you commit in writing to a specific methodology for separating ADU-driven appreciation from market-driven appreciation?

Lien and additional borrowing (3 questions)

- Will the lien Hometap records be a first-position or second-position lien against my property?

- During the term, if I need to take a HELOC, second mortgage, or construction loan to complete the ADU build, what is your consent process and what is your typical response time?

- Does the consent process change if the additional financing is specifically for the ADU build that we discussed at origination?

Default and forced sale (2 questions)

- Under what specific circumstances does Hometap have the right to require a sale of my home?

- If I cannot settle at year 10 — what is the cure process before any forced-sale action begins?

Refinance and exit (2 questions)

- If I want to refinance my first mortgage during the term, will Hometap subordinate its lien so I can refinance, and what is the process?

- If I want to settle early (before year 10), can I do so, and what is the calculation Hometap uses for an early settlement?

Download the Free ADU Starter Kit

Get our printable Hometap question checklist plus our 14-point ADU contractor bid template, state ADU regulation summary, and budget worksheet — emailed instantly.

Get the ADU Starter Kit →What is the safest next step if you’re considering Hometap for an ADU?

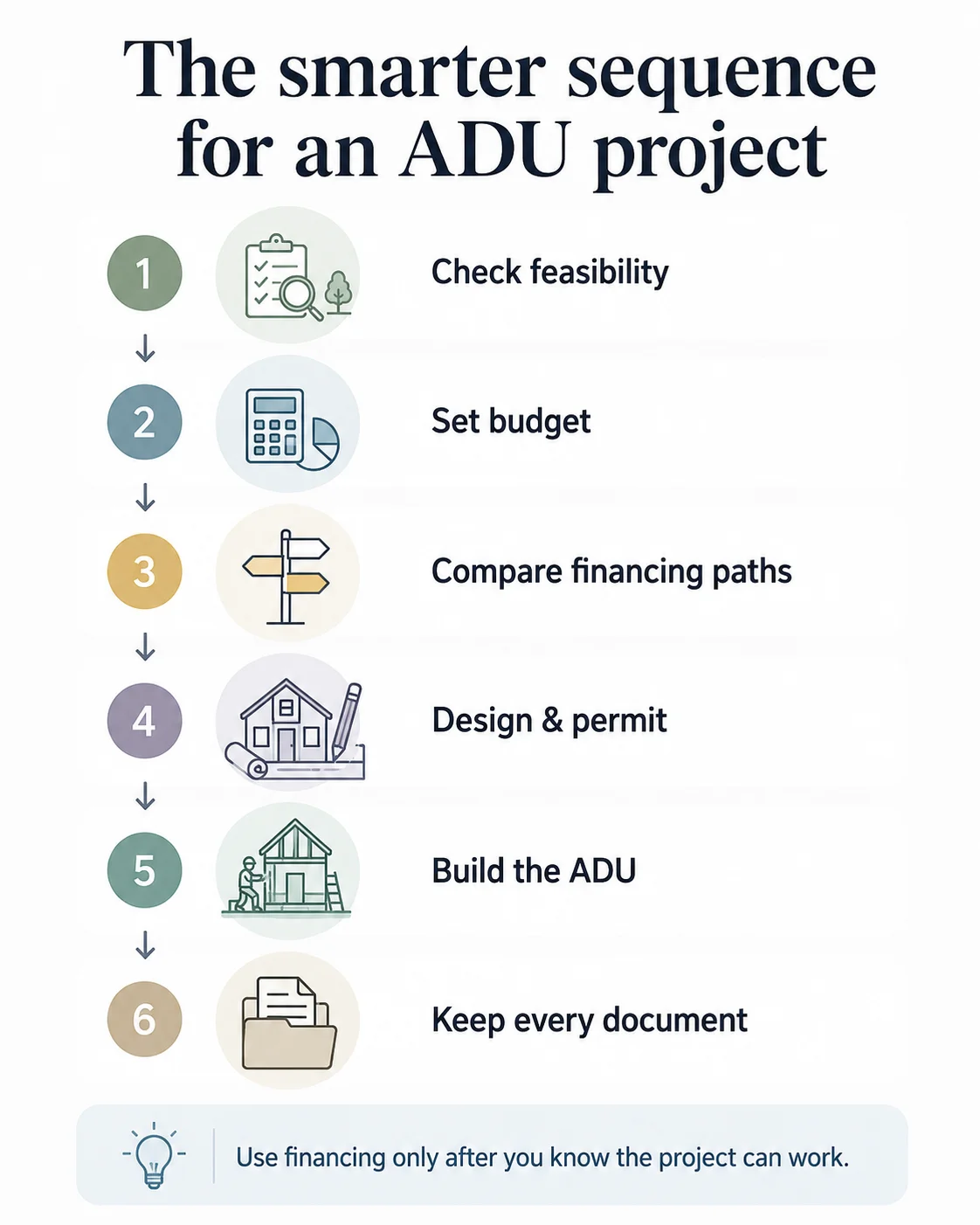

The safest sequence is: confirm what you can legally build, estimate the full ADU budget honestly, compare financing paths systematically, get Hometap’s written answers to the question list above, and only then make the commitment. Skipping any of these steps creates more risk than Hometap itself does. Most homeowners who regret a Hometap decision regretted not running steps one through four first.

The three-step decision framework

- Screen buildability. Before any financing conversation, screen whether your lot can support the ADU you want to build. Setbacks, lot coverage, owner-occupancy rules (where they still exist), utility-lateral capacity, fire-zone overlays, HOA restrictions, parking minimums, and historic-district overlays all affect what is actually buildable. A free 60-second feasibility screen costs you nothing and protects you from borrowing for an impossible project. Always verify the final answer with your local planning department.

- Estimate the full ADU budget. Per Dwelling Index’s 2026 cost research, detached ADUs in California metros run $300–$500 per square foot all-in. A 600-square-foot one-bedroom detached ADU typically lands between $180,000 and $300,000 before sitework surprises and utility upgrades. Garage conversions can be 30–50% cheaper. Use our ADU Cost Per Square Foot guide and our How Much Does an ADU Cost calculator to build a realistic number.

- Compare financing paths systematically. Use our ADU Financing Options guide to walk through the paths (HELOC, home equity loan, cash-out refinance, construction loan, renovation loan, HEI like Hometap, local grant programs, and wait-and-save). Compare on five dimensions: monthly payment, qualification requirements, treatment of ADU-driven value, total 10-year cost, and exit flexibility. See also: Hometap vs. HELOC for ADU and Home Equity Investment for ADU guide.

See What You Can Build → Get Your Free ADU Report

Start with step one. Our Feasibility Engine screens your lot against the local rules most likely to affect your ADU and tells you what to verify with your planning department. Free, 60 seconds, no obligation.

Get Your Free ADU Report →

Frequently asked questions about Hometap

Is Hometap a scam?

No. Hometap is a legitimate, BBB-accredited fintech company with verifiable NMLS-listed entities. As of Hometap's December 9, 2025 press release, it had deployed more than $2.3 billion to over 22,000 homeowners since 2017, and its current homepage lists 25,000+ funded homeowners. Hometap is the defendant in an active Massachusetts Attorney General enforcement action filed February 19, 2025, alleging the product is an illegal reverse mortgage, and reportedly a defendant in a February 2026 proposed New Jersey class action. Hometap disputes the allegations and the cases are unresolved. Calling Hometap a 'scam' overstates the situation. The product is real, the company is real, and the regulatory framework around HEI products is still being written.

Can Hometap foreclose on my house?

Hometap records a mortgage or deed of trust as a lien against your property, which gives it the contractual right to recover its investment if you cannot settle at year 10 through any of the four published settlement paths. Hometap's published footer language says it may 'exercise its right to acquire a percent ownership interest and work with the homeowner to sell the property' if the investment is not settled by term expiration. This is structurally similar to how a HELOC or home equity loan can result in foreclosure if you default. Read the default and forced-sale provisions in your specific contract carefully.

What is the catch with Hometap?

The catch is the back-loaded balloon settlement at year 10, the uncertainty of the final settlement amount, and the share of your home's future value that Hometap receives. Hometap is upfront about the structure — there is no hidden interest rate or hidden fee — but the cost is contingent on future home value, which most homeowners under-weight at signing. The Hometap Cap at 20% annualized provides a ceiling, but the ceiling itself can be large in dollar terms on a long hold.

What is Hometap's interest rate?

Hometap does not charge a stated interest rate. It charges a 4.5% origination fee at closing and takes a percentage of your home's future value at settlement. The effective annualized cost on the gross investment, back-calculated, typically lands in the 7–19% range depending on hold period and appreciation — moderate appreciation with longer holds produces lower annualized IRRs; strong appreciation or short holds produce higher ones. The 20% Hometap Cap engages only in scenarios where the share calculation would otherwise produce a higher implied annualized return.

How much does Hometap take?

Hometap's share is set at contract origination based on the X-for-Y tiered model. As a published example, taking 10% of your home's current value as cash today pairs with Hometap receiving roughly 15% of home value at settlement during years 0–3, scaling higher with hold period. The maximum Hometap can collect is capped at 20% annualized return under the Hometap Cap. The exact percentage in your contract depends on how much you take and is documented in your offer.

What credit score do you need for Hometap?

Per Hometap's October 2025 published guidance, the minimum FICO score for a Hometap home equity investment is 575. Hometap also states that homeowners with poor-to-fair credit (585+) may still qualify, with applicants evaluated on multiple underwriting factors beyond credit score alone.

Is Hometap better than a HELOC for an ADU?

Not automatically. A HELOC at the current Curinos national average of 7.21% (as of May 17, 2026) typically costs less in absolute dollars over a 10-year ADU build than a Hometap investment. Hometap wins when you cannot qualify for a HELOC (DTI, self-employment, retirement income), when you cannot afford a new monthly payment, or when you want to keep your favorable existing first mortgage intact and the renovation adjustment protects your ADU's added value. This is an editorial conclusion based on the cost math in our worked examples above.

What happens at the end of 10 years with Hometap?

At or before year 10, you settle the investment through one of Hometap's described settlement paths: sale of the home, refinance, buyout from savings or other funds, or replacement financing. If none of these is feasible, Hometap's published footer says it may exercise its lien rights to recover its investment, which can include working with the homeowner to sell the property.

Can I sell my house with a Hometap investment in place?

Yes. Selling is the most prominently documented Hometap settlement path, and the sale typically funds the settlement at closing. The Hometap lien is paid off from sale proceeds in the same way a mortgage or HELOC is paid off — through a payoff statement at closing.

Does Hometap show up on my credit report?

Hometap performs a hard credit pull at the application stage, which appears on your credit report. The Hometap investment itself is structured as an investment, not a debt, and is not typically reported as a debt obligation on your monthly credit report. Confirm specifics with Hometap in your individual case.

Can I use Hometap to build an ADU?

Yes. Hometap publicly lists home improvements and renovations among the use cases its product can fund, and Hometap publishes a customer story featuring a homeowner who used Hometap to fund a detached ADU and a junior ADU in Los Angeles. Whether it is the right way to fund your specific ADU depends on the math, your state, and whether the renovation adjustment will apply to your build. See the detailed sections above.

What states does Hometap operate in?

As of May 21, 2026, Hometap operates in 16 states: Arizona, California, Florida, Indiana, Michigan, Minnesota, Missouri, Nevada, New Jersey, New York, Ohio, Oregon, Pennsylvania, South Carolina, Utah, and Virginia. Hometap exited Massachusetts in 2025 during the AG enforcement action. Verify against hometap.com's current state list before any application.

Is Hometap available in Texas?

No. Hometap does not currently operate in Texas. Texas homeowners considering an HEI should check current state availability for Point, Unlock, Unison, or other HEI providers before comparing terms, and consider HELOCs and home equity loans from in-state lenders as alternatives.

What is the Massachusetts lawsuit against Hometap about?

On February 19, 2025, Massachusetts Attorney General Andrea Joy Campbell filed an enforcement action alleging Hometap's HEI product is an illegal reverse mortgage that fails to comply with Massachusetts consumer protection laws, charges unlawfully high interest, lacks adequate underwriting, and deceptively conceals the product's true cost. Hometap denies the allegations. A Suffolk County Superior Court judge denied Hometap's motion to dismiss in August 2025; in December 2025 the court limited Hometap's ability to use prior regulator interactions as a defense and allowed limited discovery on what Hometap was told by regulators. As of May 21, 2026, the case is proceeding through discovery with no verdict and no public trial date.

What is the February 2026 Hometap class action about?

A proposed class action, Greenidge et al. v. Hometap Equity Partners, LLC et al., was reportedly filed in New Jersey federal court in February 2026, alleging Hometap misbrands its HEI contracts as option purchase agreements and that the products are predatory in nature. This is a separate matter from the Massachusetts AG action. As of May 21, 2026, the allegations have not been proven, and Hometap has not yet publicly responded in detail. Verify the docket directly before any decision.

What happens if my city denies my ADU permit after I've taken Hometap money?

Hometap funding does not guarantee ADU approval, and your Hometap obligations follow the agreement regardless of permit outcome. If your permit is denied, you still owe Hometap's settlement at the end of the term. This is exactly why we recommend screening ADU feasibility before signing any financing agreement. Ask Hometap in writing what happens to your obligations if your planned renovation use changes.

How does Hometap's renovation adjustment work?

Hometap's renovation adjustment is a contractual provision that may exclude the value increase from a qualifying renovation of $25,000 or more from the home value used to calculate Hometap's settlement share, subject to homeowner documentation, an appraiser's methodology for isolating renovation-driven value, and Hometap's approval at settlement. For an ADU build that typically adds $100,000 to $300,000 in appraised value, the adjustment can save the homeowner $24,000 to $32,000+ in settlement cost across the scenarios we modeled above. It is not automatic and requires careful documentation throughout the build.

How we researched this Hometap review

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. For this review, we worked from primary sources where available and verified secondary sources against each other before reporting any figure.

Primary sources consulted

- Hometap official pages — homepage (hometap.com), How It Works, pricing blog (how-hometap-pricing-works), bad-credit guide updated October 17, 2025, application guide, renovation adjustment materials, customer stories, and current footer

- Massachusetts Attorney General official press release dated February 19, 2025 (mass.gov)

- Consumer Financial Protection Bureau Issue Spotlight on home equity contracts dated January 15, 2025 (consumerfinance.gov)

- CFPB consumer advisory on home equity contracts (January 15, 2025)

- BBB Hometap Equity Partners LLC company profile (bbb.org, sampled May 2026)

- Trustpilot Hometap profile (sampled May 2026, 6,800+ reviews)

- BusinessWire press release dated December 9, 2025 (Hometap $50M Gallatin Point Capital announcement)

- HousingWire coverage of the Massachusetts AG action and its procedural developments (August 2025; December 2025) and coverage of Hometap’s 16-state operating footprint (November 2025)

- National Mortgage News coverage of August 2025 motion-to-dismiss ruling

- ClassAction.org coverage of the February 2026 Greenidge et al. New Jersey proposed class action

- Curinos national HELOC rate benchmark as of May 17, 2026 (7.21% HELOC; 7.36% home equity loan)

Disclaimer: This is an independent editorial review. The Dwelling Index has no affiliate relationship with Hometap as of the publish date. Some links on this page (to traditional mortgage and renovation-loan comparison tools) are affiliate links; our editorial analysis is never influenced by compensation. This content is for informational purposes only and is not financial, legal, or tax advice. Verify all product terms, state availability, and eligibility requirements directly with Hometap before making any financial decision.