ADU Appraisal Value: How Much an ADU Can Add and What Appraisers Actually Count

Bottom line, up front

ADU appraisal value can be real and lasting — but only when the unit is legal, documented, and supported by local market evidence. There is no verified national rule that an ADU adds 15%, 25%, or 35% to every home, and your ADU will rarely appraise for exactly what it cost to build. Appraisers don’t price your ADU off your invoice or a percentage formula. They price it off what buyers in your market have actually paid for similar properties.

The biggest lever most homeowners control isn’t square footage or finishes. It’s permit status and documentation. A well-documented, legal ADU gets described and analyzed as a separate living area, and its rental income can support a loan file when the unit is legal to rent and the loan product allows it. An undocumented or noncompliant unit usually gets conservative treatment — no matter what it cost to build.

Who this is for: homeowners building or refinancing, buyers purchasing a home with an ADU, and anyone whose deal hinges on the unit “counting.” One number to anchor on: an ADU-property appraisal typically runs about $400–$800, modestly more than a standard single-family appraisal. Next step: confirm permit status and gather your documents before you order the appraisal — the checklist is below.

Will your ADU value be easy or hard to support? At a glance:

| Signal | Stronger appraisal support | Weaker appraisal support |

|---|---|---|

| Legal status | Permitted and finaled, or legal nonconforming | Unpermitted, unclear, or not allowed under zoning |

| Market evidence | Recent local sales of homes with ADUs | No ADU comps and no market data |

| Use | Legal long-term rental, or clear family/flex use | Rental use prohibited or legally murky |

| Documentation | Plans, permits, final inspection, photos, rent comps | “Trust me, it cost $250,000” |

| Design | Independent, functional, marketable layout | Awkward access, poor privacy, over-improvement |

| Lender review | ADU described and analyzed in the appraisal | ADU buried or treated as storage |

The right column is fixable. Most of this guide is about moving every row from right to left.

Screen your lot and your next steps in about 60 seconds — before you spend on plans, financing, or an appraisal.

By the Dwelling Index Editorial Team · Last updated: · Last verified: · ~40 min read

An independent guide from Dwelling Index — an independent research resource covering ADU financing, costs, and regulations.

How much appraisal value does an ADU add?

Appraised value is an opinion of market value: what a typical buyer would pay today. It is not a reimbursement of what you spent, and it is not your home’s price multiplied by some magic percentage. So when a builder’s blog tells you an ADU “adds 35%,” they’re quoting a correlation, not an appraisal method. The number that lands in your report comes from comparable sales in your specific market — and those vary enormously between, say, a San Diego neighborhood where buyers expect ADU rental income and a rural area where ADUs are still unusual.

What the FHFA California data proves — and what it doesn’t

The most-cited statistic in this entire topic comes from the Federal Housing Finance Agency (FHFA), the federal regulator of Fannie Mae and Freddie Mac. In January 2025, FHFA published the first long-run federal look at ADU appraisal data, drawn from the Uniform Appraisal Dataset (UAD) — the standardized record lenders submit on every appraisal backing a Fannie Mae or Freddie Mac loan.

| FHFA California metric (single-family purchase appraisals) | With ADU | Without ADU | What it actually means |

|---|---|---|---|

| 2013 median appraised value | $550,000 | $405,000 | ADU-equipped homes already started higher |

| 2023 median appraised value | $1,064,000 | $715,000 | A large gap — but between whole properties, not a measure of ADU contribution |

| Annualized median-value growth, 2013–2023 (CA) | 9.34% | 7.65% | ADU properties grew faster in this dataset |

| Annualized growth, 2013–2023 (national) | 7.20% | 6.25% | The same pattern nationally, but a smaller gap |

Source: FHFA, “Trends in Median Appraised Value for Properties With Accessory Dwelling Units in California,” published Jan 2, 2025 (national figures from footnote 17); FHFA page last updated Apr 7, 2026. Verified May 22, 2026.

Now the part most pages leave out: that $1,064,000-vs-$715,000 gap is not “an ADU adds $349,000.” It compares the median value of all properties that happen to have an ADU against all properties that don’t. Homes with ADUs skew toward larger lots, pricier neighborhoods, and higher-end construction — they were already worth more before the ADU existed (note they started $145,000 apart back in 2013). FHFA’s own authors say the faster growth “requires further analysis” before drawing causal conclusions, and they limit the finding to California.

If you want a defensible way to think about your own number, ignore the percentage and ask three questions instead: Is my unit legal? Are there ADU sales near me? Can it be legally rented? Those three answers move your value far more than any formula. You can run a fuller version of this with our ADU Equity Calculator to estimate net value and rent impact — this page is about how that value holds up under an actual appraisal and lender review.

Why “ADUs add 35%” is too simple to trust

Popular pages repeat ranges from 15% to 54% depending on region. Those figures describe how priced homes with ADUs correlate with homes without — they don’t isolate the appraiser’s contributory-value adjustment, and they don’t survive the “no comps nearby” problem. Treat any single percentage as a marketing shorthand, not an appraisal you can rely on.

How do appraisers value an ADU?

An appraiser has three tools. Understanding which one drives your number tells you which evidence to gather.

Sales comparison approach — the one that usually decides your number

This is the approach that typically carries the most weight, and for ADU-equipped homes it’s also the trickiest. The appraiser finds at least three recently sold “comps” — Fannie Mae requires a minimum of three closed comparable sales — and adjusts their prices up or down to match your property (Fannie Mae Selling Guide B4-1.3-08). The catch: legal ADU sales are still relatively rare. As of FHFA’s data, only about 2.9% of California purchase appraisals in 2023 involved properties with ADUs, and California is the nation’s most ADU-dense state. Outside California, usable comps can be even harder to find — which is exactly why the evidence packet in this guide matters.

This is also the answer to the question we hear constantly — “Why didn’t the appraiser just add my ADU’s square footage to the house?” Generally, they can’t and shouldn’t. A detached ADU is independent living area on the same parcel; it gets analyzed as its own contributory feature, not folded into the main home’s gross living area. The appraiser isn’t undervaluing you by keeping it separate — they’re following the rules.

Fannie Mae also lets appraisers support an ADU’s marketability using an aged settled sale plus an active or under-contract listing when current closed ADU comps are scarce (Fannie Mae Selling Guide B4-1.3-05). That flexibility exists because comps are hard to find — which means the evidence you hand the appraiser genuinely matters.

Income approach — matters most for rentals

When a one-unit neighborhood has a substantial rental market, the appraiser may use the income approach, estimating market rent and converting it to value (typically via a gross rent multiplier supported by comparable rentals and sales). Fannie Mae is explicit: the income approach can’t be the sole indicator of value for a one-unit property, and it must include the supporting comparable rental and sales data plus the calculations used (Fannie Mae Selling Guide B4-1.3-10).

Here’s a simple investor-math illustration of why rent evidence can matter — this is not how every one-unit GSE appraisal will capitalize an ADU:

An 800-square-foot detached ADU renting at $2,500/month produces $30,000 a year in gross rent. Subtract roughly $6,000 in expenses — property tax on the new value, insurance, maintenance, vacancy — and net operating income (NOI) is about $24,000. To an investor applying a 6% capitalization rate, that income implies a value near $400,000; at a more conservative 8%, closer to $300,000. The spread shows why the sales-comparison approach (anchored to actual comps) matters more: the number depends heavily on which cap rate and expense assumptions you choose.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Cost approach — the reasonableness check, not the whole argument

The cost approach estimates site value plus the replacement or reproduction cost of the improvements, less depreciation (Fannie Mae Selling Guide B4-1.3-10). It’s useful when comps are thin. But an appraisal that relies solely on the cost approach is not acceptable to the GSEs — and here’s the damaging admission, stated plainly: your ADU can appraise for less than it cost to build — and still be a good decision. Cost is evidence; the market is the verdict. If you’re building to house a parent, generate rent, or age in place, an “appraisal lag” in year one doesn’t erase the value the unit delivers every month.

| Approach | How the number is built | When it dominates | Typical ADU outcome | Key limitation |

|---|---|---|---|---|

| Sales comparison | Adjusts at least 3 closed comps to match your property | Usually carries the most weight for one-unit loans | Whatever local ADU comps support | Few ADU comps = conservative or stretched adjustments |

| Income | Market rent → NOI / GRM → value | One-unit areas with a substantial rental market | Can support value where rents are strong | Can’t be the sole indicator for a one-unit loan |

| Cost | Site value + replacement cost − depreciation | New builds, no comps available | A floor / reasonableness check | Cost ≠ market value; sole-cost appraisals not acceptable |

Sources: Fannie Mae Selling Guide B4-1.3-08, B4-1.3-10, B4-1.3-05; Freddie Mac Single-Family Seller/Servicer Guide §5601.2; Sacramento Appraisal Blog (working-appraiser commentary). Verified May 22, 2026.

Is your property a one-unit home with an ADU, or a 2–4 unit property?

The line between “house with an ADU” and “two-unit property” isn’t cosmetic — it changes the appraisal form, the comp set, and how rental income is treated. Fannie Mae’s test looks at the whole picture: Does the second unit have its own meter? Its own address? Can it be legally rented? Is it truly independent, or open to the main home with no expectation of privacy? An independent second kitchen by itself does not make a unit an ADU.

Why you should care before you order anything: if your unit gets classified as a second dwelling unit rather than an ADU, you’re now in two- to four-unit territory, where the income approach and multi-unit comps carry more weight and the loan rules differ. If it’s a one-unit-with-ADU, the sales-comparison approach on one-unit comps drives the number. Knowing which bucket you’re in tells you which comps and which rules to prepare for.

Source: Fannie Mae UAD 3.6 Policy / Selling Guide B2-3-04, Special Property Eligibility Considerations. Verified May 22, 2026.

Does an ADU count as gross living area or square footage?

Gross living area (GLA) is the above-grade, finished, heated square footage an appraiser measures for the main dwelling. Whether your ADU counts toward it changes which comps apply — and that changes your number. The rule is precise: ADU living area stays separate from the main dwelling’s above-grade square footage unless the ADU is contained within or part of the primary dwelling, has interior access, and is above grade (Fannie Mae Selling Guide B4-1.3-05).

- Detached ADU (sometimes “DADU”): A standalone backyard unit. Almost always kept separate from the main home’s GLA and analyzed as its own feature. This is the most common source of the “why didn’t they add my square footage?” surprise.

- Attached ADU: Shares a wall but has a separate entrance and facilities. Treatment is more nuanced; access, privacy, and classification all matter.

- Garage conversion or basement ADU: Permits, legal habitability, ceiling height, light, and egress (a code-compliant emergency exit) determine whether the space counts as livable area at all.

- JADU (junior accessory dwelling unit): A small unit (often capped around 500 sq ft) carved out of the existing home, typically sharing some facilities. State and local definitions vary widely.

There’s a strategic nuance: when an ADU is internal, above grade, and accessible from the main dwelling, the appraiser may be able to include the square footage and reach for larger, higher-value comps — which can lift the appraisal. When it’s truly independent, keeping it separate is correct and protects the integrity of the report. Don’t ask an appraiser to combine areas that shouldn’t be combined — that’s an unacceptable practice and underwriting will catch it.

| ADU type | How it usually appears in the appraisal | What strengthens its value |

|---|---|---|

| Detached ADU | Separate contributory feature; not main-home GLA | ADU comps, rent evidence, privacy, independent utilities |

| Attached ADU | Separate feature; combined only if interior-accessible & above grade | Clear separation, separate entrance, classification clarity |

| Garage conversion | Habitable area only if permitted and code-compliant | Final inspection, egress, retained/replacement parking |

| Basement ADU | Often below-grade; reported separately from GLA | Egress, ceiling height, moisture mitigation, permits |

| JADU | Small interior unit per local definition | Local compliance, documented kitchenette/bath |

Source: Fannie Mae Selling Guide B4-1.3-05 (Improvements Section) and B2-3-04. Verified May 22, 2026. This is one of the most important and most misunderstood facts on this page — verify it directly in B4-1.3-05.

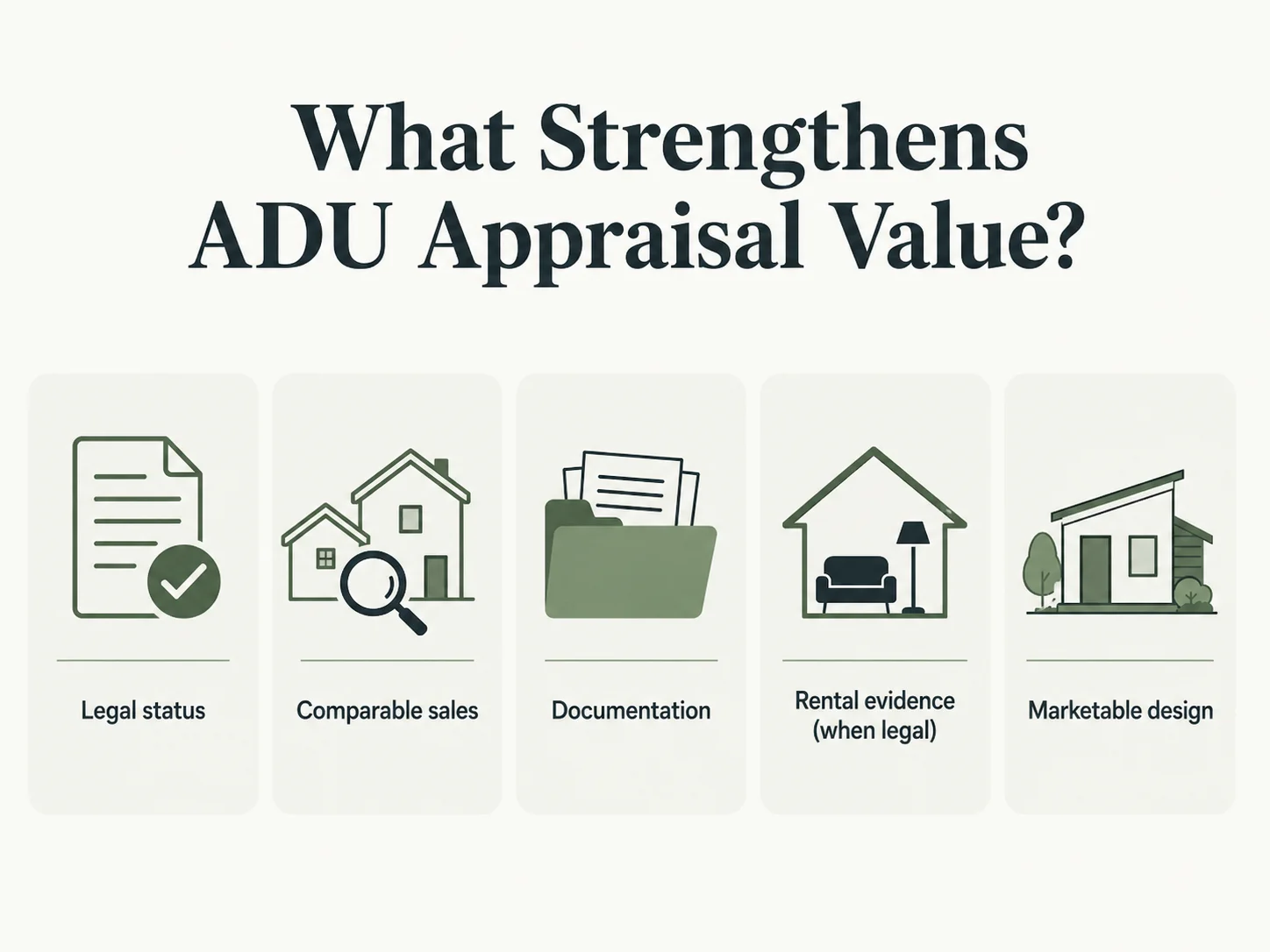

What makes an ADU appraisal strong or weak?

Strong signals (move every row left):

Permitted and finaled; legal long-term rental rights; recent nearby ADU sales; a functional, private layout; a separate entrance; documented, professionally measured square footage; market rent comps; separate or sub-metered utilities.

Weak signals (the report fights you):

Unpermitted construction; illegal or prohibited rental use; no final inspection; awkward access through the main home or backyard; low neighborhood demand for ADUs; luxury over-improvement the market won’t pay for; zero ADU comps; visibly poor workmanship.

A strong appraisal starts with a legal, buildable unit. See what’s possible at your address before you commit a dollar.

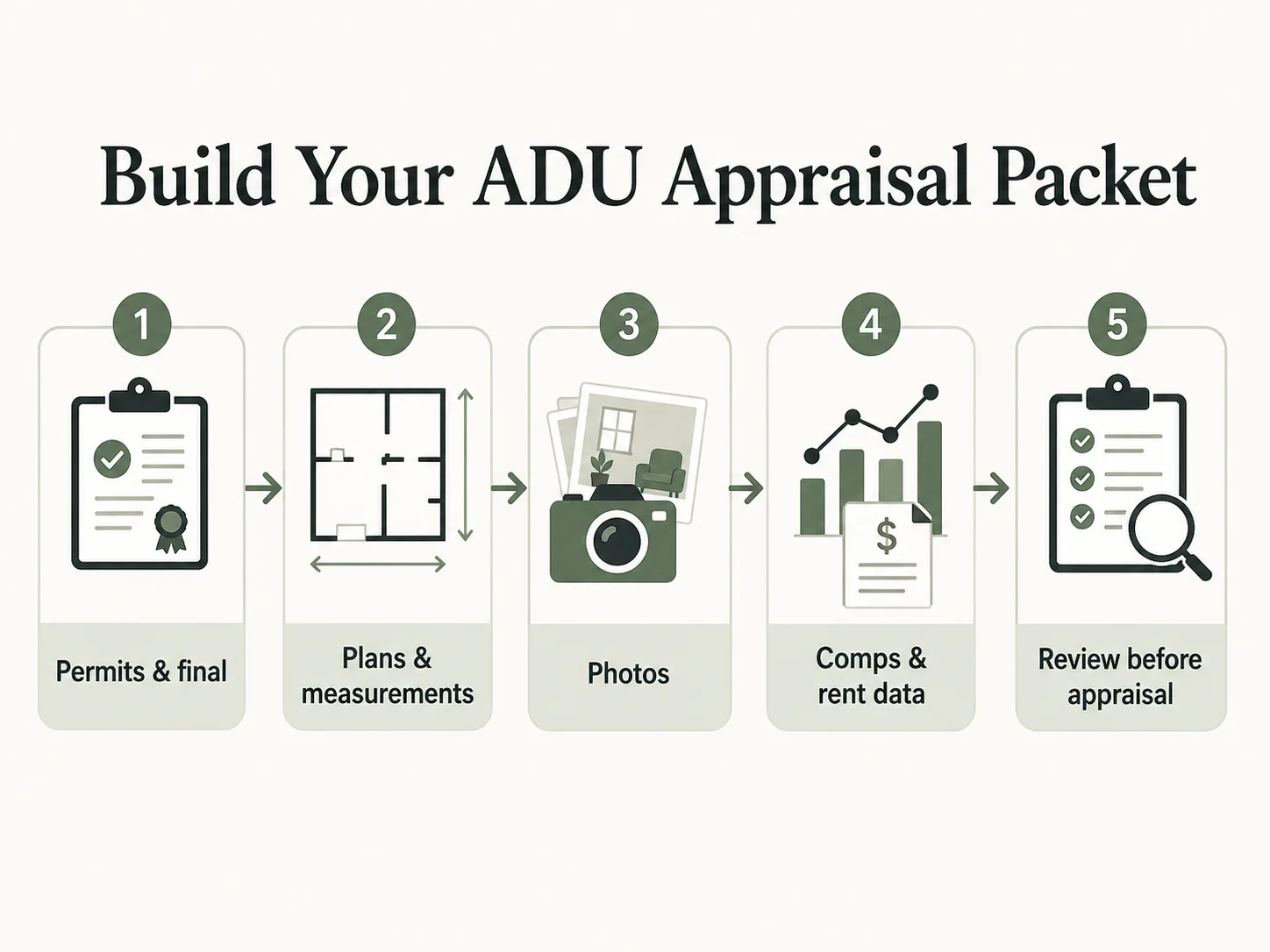

What should you give the appraiser or lender?

Appraisers are independent and form their own opinions — you cannot coach the value. But you can make sure the unit is fully visible and properly documented. This is our 2026 ADU Appraisal Evidence Matrix, built from the actual Fannie Mae, Freddie Mac, and assessor sources, decoded into what you hand over and why it matters.

| Appraisal question | What the source says | What you should provide | Why it matters |

|---|---|---|---|

| Is it legally an ADU? | Fannie Mae defines an ADU as additional living area independent of the primary dwelling, on the same parcel, with living, sleeping, cooking, and bathroom facilities (B4-1.3-05 / B2-3-04) | Permit, final inspection, floor plan, kitchen/bath photos, certificate of occupancy if issued | If it isn’t legally and functionally an ADU, value support weakens fast |

| Must the appraisal address the ADU? | Yes — the report “must include a description of the ADU and analysis of any effect it has on the value or marketability of the subject property” (Fannie Mae Appraisal FAQs) | A one-page ADU summary for the appraiser | The ADU should never be invisible in the report |

| What if it’s legal nonconforming? | Fannie Mae will purchase loans on legal nonconforming use if the appraisal reflects any adverse effect on value/marketability (B4-1.3-04) | Zoning confirmation, permit history, a planning-department note | Legal status matters as much as physical construction |

| What if there are no perfect ADU comps? | Appraisers may broaden the search and use supplemental exhibits (aged sales, active/pending listings) to show marketability (Fannie Mae B4-1.3-05) | Broadened comp search, older ADU sales, paired sales, active listings | No perfect comp ≠ zero value, but it raises the support burden |

| Can rental income matter? | Freddie Mac requires a full appraisal with at least one comparable sale that has an ADU, plus a rental analysis with a minimum of three comparable rentals (Freddie Mac §5601.2 / ADU fact sheet) | Lease, rent roll, market-rent comps, proof of legal rental use | Appraisal value and qualifying income are related but not identical |

| Should value equal cost or $/sq ft? | Working appraisers warn against arbitrary price-per-square-foot logic — the real question is what buyers will pay (Sacramento Appraisal Blog) | Cost breakdown as support only, never the sole argument | Cost is not value; market evidence wins |

| Will taxes change? | San Mateo County (CA): new construction such as an ADU is assessed at market value upon completion; existing land/structures not involved are not reassassed | Local assessor lookup, a tax estimate | Tax treatment is state- and county-specific — don’t generalize |

Sources: Fannie Mae Selling Guide B2-3-04, B4-1.3-04, B4-1.3-05, and Appraisal & Property FAQs; Freddie Mac Single-Family Seller/Servicer Guide §5601.2 and ADU fact sheet; San Mateo County Assessor; Sacramento Appraisal Blog. Verified May 22, 2026.

ADU Appraisal Evidence Packet Builder — coming soon

Tell us your state, ADU type, permit status, intended use, and whether you’re refinancing, selling, or buying — and we’ll generate a personalized document checklist and appraiser handoff memo. Available soon.

Download the free ADU Starter Kit

Includes the appraisal document checklist, a permit-document tracker, a cost worksheet, and a financing-path reference — yours to keep.

Download the Free ADU Starter Kit →Why did my ADU appraise lower than construction cost?

If your appraisal came back under what you spent, you’re not alone and you didn’t necessarily make a mistake. Here’s what actually drives the gap.

Cost does not equal value. This is the core principle every appraiser repeats. When comps are thin, appraisers often value an ADU conservatively — sometimes only in the $25,000 to $50,000 range — not because the unit is worthless, but because underwriters will reject an appraisal that claims a higher figure without comparable sales to support it. In strong-demand markets with real ADU comps, the same units can be credited in the six figures. The unit didn’t change. The comps did.

Thin comps suppress support. When there are few legal ADU sales nearby, the appraiser has little to anchor to, and adjustments drift conservative — sometimes well below your per-square-foot build cost.

Lender overlays can matter. Even when the appraiser believes value exists, the lender or investor reviewing the file can require additional support. UAD 3.6 is designed to reduce this friction over time by capturing ADU details in standardized data fields.

What to do after a low ADU appraisal

- Read the report. Confirm the ADU was actually described and analyzed. If it’s missing or buried, that’s a documentable issue.

- Verify permits and square footage were recorded correctly.

- Gather omitted comps. If you know of a nearby ADU sale the appraiser didn’t use, document it with address, date, and sale price.

- Request a Reconsideration of Value (ROV) through your lender. An ROV is a formal process to submit specific, factual evidence — comparable sales the appraiser missed or data errors — for the appraiser to review. Under Fannie Mae’s framework, a borrower may initiate one ROV per appraisal, and any borrower-supplied additional comparable sales are limited to five, each with its data source and an explanation of why it supports a different value (Fannie Mae Selling Guide B4-1.3-12). An ROV is not pressuring the appraiser to “hit a number” — that’s prohibited.

- Don’t over-rely on the appraisal for your decision if your real goals are rental income, family housing, or aging in place — those returns show up monthly, not in year-one equity.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

See which financing paths use current value vs. as-completed value

If you’re planning to pull equity to cover the build, it helps to understand how cash-out refinances and renovation loans treat your ADU’s value before you assume the appraisal will cover the project.

Compare ADU Financing Options →Independent education — not lender rankings.

Can ADU rental income increase appraisal value or borrowing power?

Appraisal value versus qualifying income

Appraisal value is what the property is worth. Qualifying income is how much of the ADU’s rent a lender will let you count toward your debt-to-income ratio when approving a loan. They’re related — both lean on rent evidence — but they’re not the same number, and a strong rent doesn’t guarantee a high appraisal.

Here’s how the two big agencies handle ADU rental income in 2026:

| Rule | Fannie Mae | Freddie Mac |

|---|---|---|

| Property type | One-unit principal residence | One-unit primary residence |

| Eligible transactions | Purchase and limited cash-out refinance | Purchase and no-cash-out refinance |

| Income cap | ≤ 30% of total qualifying income | ≤ 30% of total qualifying income |

| Lease documentation | Standard rental-income documentation applies | Documented lease counted up to 75% of the lease amount |

| Multiple ADUs | Rental income from only one ADU, even if several exist | Rules apply to the subject one-unit primary residence |

| Appraisal | Required; ADU described and rent analyzed | Full appraisal required; appraisal waiver (ACE) not acceptable |

| Comparable requirements | Comparable sale/rent support for the ADU | ≥ 1 comparable sale with an ADU; rental analysis of ≥ 3 comparable rentals, ≥ 1 with an ADU |

| Landlord education | — | May be required for a purchase if you lack ≥ 1 year landlord experience |

Sources: Fannie Mae Selling Guide B3-3.1-08 (Rental Income) and Appraiser Update; Freddie Mac Single-Family Seller/Servicer Guide §5601.2 and ADU fact sheet. Verified May 22, 2026.

Long-term versus short-term rental

A long-term lease is the cleanest evidence. Short-term rental (STR) income is far weaker support: many cities restrict or ban STRs, lenders generally won’t credit projected STR income for qualifying, and an appraiser can’t lean on rent the unit isn’t legally allowed to earn. If your value thesis depends on Airbnb, confirm local STR legality first.

What rental evidence to collect

A signed lease, three local rent comps (at least one with an ADU), proof the rental use is legal, and a realistic expense estimate (taxes on the new value, insurance, maintenance, vacancy). Hand that to the appraiser and the lender as part of your packet.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Explore ADU mortgage and refinance options

Compare financing paths before you assume your ADU value will cover the project. Independent education — not lender rankings.

Explore ADU Mortgage and Refinance Options →Legal, legal nonconforming, zoning-illegal, or unpermitted: what changes?

The reason status matters so much is mechanical, not punitive: appraisers value against comparable legal sales, and underwriters reject appraisals that assign value without that support.

| Status | How it’s typically treated | Financing/eligibility note |

|---|---|---|

| Permitted / legal conforming | Full description and analysis as a separate living area; income support possible if legally rentable | Can be eligible for standard GSE financing if borrower, property, appraisal, and loan product meet all other requirements |

| Legal nonconforming (was legal when built; predates current zoning) | Supported, with any adverse effect on value/marketability analyzed | Can be acceptable when the appraisal reflects any adverse effect on value and marketability |

| Not allowed under zoning / illegal zoning use | Appraised based on current use; the appraisal must state the illegal use | May be eligible only if insurance isn’t jeopardized, the use conforms to the market, and the appraisal includes at least two comparable sales with the same non-compliant zoning use plus at least three settled sales total |

| Addition or conversion without required permits | Appraiser must comment on quality, appearance, and the effect on market value | Often conservative treatment; financeability is lender- and market-dependent |

Source: Fannie Mae Selling Guide B2-3-04 (Special Property Eligibility Considerations), B4-1.3-04 (Site Section), and B4-1.3-05 (Improvements Section). Verified May 22, 2026.

Can you fix an unpermitted unit?

Often, yes. Many states and cities have created amnesty or legalization pathways. In California, AB 2533 (signed September 28, 2024; effective January 1, 2025) amended Government Code §66332 to create a legalization pathway for unpermitted ADUs and JADUs built before January 1, 2020: local agencies generally can’t deny a permit for those units based solely on code violations, unless correcting a violation is necessary to address a “substandard condition” under Health & Safety Code §17920.3. Cities including Santa Cruz, Hayward, San Diego, and others run AB 2533 amnesty programs. Check your local ADU rules before assuming the unit is a lost cause — many states have their own programs.

Buying a home with an existing ADU?

Verify before you rely on the unit’s value or rent: pull the permit history and final inspection, confirm the unit is legal or legal nonconforming, check whether rental use is allowed, and confirm utilities and address status. An unpermitted unit you assumed was income can become a financing problem at the closing table.

What if there are no ADU comps nearby?

This is the most common real obstacle, especially outside California. Here’s the action tree:

- Expand the search intelligently. A nearby city with similar price points, the same school district, a comparable rental market, or similar lot sizes can all yield usable comps.

- Use active and pending listings as support, not primary proof. Fannie Mae permits active or under-contract sales as supplemental exhibits to demonstrate marketability when an ADU is present (B4-1.3-05). They show demand even when closed comps are scarce.

- Bring paired sales. If you can find two otherwise-similar homes that sold close in time, one with an ADU and one without, the price difference helps the appraiser quantify the contribution.

- Ask better questions before you order. “Has the appraiser valued ADUs in this market before?” “Will the lender accept ADU rental-income support?” “What comparable evidence do you need from me up front?” The answers tell you whether to gather more before spending on the appraisal.

No comps is a support burden, not a verdict. The homeowners who do best are the ones who hand the appraiser a head start.

How does ADU appraisal value affect refinancing, selling, and property taxes?

Refinance

Two products treat your ADU differently. A standard refinance uses current appraised value — what the unit is worth today, which may lag your cost if comps are thin. A renovation loan (such as a Fannie Mae HomeStyle Renovation or Freddie Mac CHOICERenovation) can use as-completed value — what the property will be worth after the ADU is built — which can unlock financing the current value wouldn’t support. Know which one your lender is using, because it changes the number that matters.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

Compare ADU financing paths that use current value vs. as-completed value

See how each lane treats your ADU’s appraised value. Independent education — not lender rankings.

Compare ADU Financing Paths →Sale

For buyers using financing, the home generally has to appraise at the purchase price for the loan to close — so a well-documented, permitted ADU that appraises cleanly protects your sale, while an unpermitted one can blow up a deal at the appraisal stage. Prepare a buyer-facing packet: permits, final inspection, rent comps, and a clear note that the unit is legal.

Property taxes

Building or converting to an ADU will generally increase your property-tax bill — but in many jurisdictions only the new construction is assessed at market value upon completion, while your existing land and structures are not reassessed. San Mateo County, California is a documented example of this treatment: the ADU is assessed on completion; the rest of the property isn’t triggered. Tax treatment varies significantly by state and county, so confirm with your local assessor before assuming any particular outcome applies to you.

What’s changing in 2026? UAD 3.6 and expanded ADU eligibility

The part that trips up homeowners and even some loan officers right now: the expanded ADU eligibility rules only apply under UAD 3.6. Before the November 2026 mandate, your loan may still be running under the current (UAD 2.6) framework, where the older limits apply. Know which set you’re under before you count on the new flexibility.

| Topic | Current Selling Guide / UAD 2.6 | UAD 3.6 supplement (effective for loans sold on/after Mar 31, 2026) |

|---|---|---|

| ADUs on a one-unit property | One ADU permitted on the parcel | Up to three ADUs on a one-unit property |

| ADUs on 2–4 unit properties | ADUs not permitted with a two- to four-unit dwelling | Two- to three-unit properties may include ADUs, if dwelling units + ADUs ≤ 4 |

| ADU rental income (qualifying) | From only one ADU; one-unit principal residence; purchase or limited cash-out refi; ≤ 30% of qualifying income | Same income framework, with broader property eligibility under the supplement |

| Manufactured housing ADUs | Limited | Expanded eligibility under the supplement |

Sources: Fannie Mae UAD 3.6 Policy Supplement and Selling Guide Announcement SEL-2025-10 (Dec 10, 2025); Fannie Mae Appraiser Update; Freddie Mac / Fannie Mae UAD redesign timeline. Verified May 22, 2026. Re-verify quarterly through the November 2026 mandate.

Our read of these rules: Based on the verified facts above, we expect the changes to modestly help homeowners who can document a legal, rentable ADU — clearer data fields and broader eligibility reduce the friction that has historically suppressed ADU appraisals. That’s our editorial conclusion from the policy, not a promise about your specific loan.

For the full side-by-side, see our Fannie Mae ADU rules vs. Freddie Mac ADU rules guide.

ADU appraisal value by type: detached, attached, garage, basement, prefab, JADU

| ADU type | How appraisal support usually shows up | Evidence to gather | Main underwriting / GLA issue |

|---|---|---|---|

| Detached ADU | Separate contributory feature; privacy and rental appeal | ADU comps, rent comps, independent utilities | Highest build cost; may not recapture cost in newer markets |

| Attached ADU | Separate feature; sometimes combined GLA if interior-accessible & above grade | Plans showing separation, separate entrance | Classification can complicate the comp set |

| Garage conversion | Habitable area only if permitted/code-compliant | Final inspection, egress proof, parking plan | Lost parking and habitability questions |

| Basement ADU | Reported separately; often below-grade | Egress, ceiling height, moisture mitigation, permits | Below-grade treatment limits GLA credit |

| Prefab / modular ADU | Valued like any installed ADU against local comps | Site work, foundation, install permits, comps | Local acceptance; the delivery method doesn’t change the valuation method |

| JADU | Small interior unit per local definition | Local compliance, documented kitchenette/bath | Size/use limits; smaller value add |

A note on prefab and modular: factory construction can shorten timelines and stabilize cost, but it does not eliminate local permitting, site work, foundation, or utility-connection requirements — and an appraiser values the finished, installed unit the same way they’d value any other ADU: against local comps. The delivery method doesn’t change the valuation method. Our ADU cost per square foot breakdown shows why cost doesn’t equal appraised value.

Which path fits your situation?

- I’m planning an ADU. Confirm a legal, buildable unit before you spend on plans or financing. → See what you can build → Get your free ADU report.

- I’m building and want future appraisal support. Preserve every permit, plan, final inspection, invoice, and progress photo from day one. → Build my ADU appraisal packet (tool coming soon).

- I’m refinancing after completion. Gather permits, final inspection, and rent comps; confirm whether your lender uses current or as-completed value. → Compare ADU financing options.

- I’m selling a home with an ADU. Prepare a listing packet: permits, final inspection, rent comps, and an appraiser handoff memo so the deal survives the appraisal.

- I’m buying a home with an existing ADU. Verify permit, final inspection, and legal rental status before relying on the ADU’s value or income.

See what’s possible at your address, with your local rules, in about 60 seconds.

✅ What we verified for this guide

All sources checked May 22, 2026. We used primary and high-authority sources for every appraisal, lending, tax, and regulatory claim. Forum posts were used only to understand homeowner language and decision friction — never as proof of law, finance terms, or appraisal rules.

- FHFA — California ADU appraised-value trend data and national figures (“Trends in Median Appraised Value for Properties With Accessory Dwelling Units in California,” published Jan 2, 2025; FHFA page last updated Apr 7, 2026). FHFA notes the data may contain appraiser entry errors and excludes manufactured homes and small multifamily rentals. Verified May 22, 2026.

- Fannie Mae Selling Guide — ADU definition and eligibility (B2-3-04), Improvements/GLA treatment (B4-1.3-05), legal-nonconforming use and site section (B4-1.3-04), comparable sales minimums (B4-1.3-08), cost and income approaches (B4-1.3-10), rental income (B3-3.1-08), reconsideration-of-value rules (B4-1.3-12), and the requirement that the appraisal describe and analyze the ADU’s effect on value/marketability (Appraisal & Property FAQs). Verified May 22, 2026.

- Fannie Mae UAD 3.6 Policy Supplement & Announcement SEL-2025-10 (Dec 10, 2025); Appraiser Update — expanded ADU eligibility effective for loans sold on/after Mar 31, 2026 (UAD 3.6 lenders only); ADU rental-income rules. Verified May 22, 2026.

- Freddie Mac — Single-Family Seller/Servicer Guide §5601.2 and ADU fact sheet: rental-income qualifying rules, comparable-sale and comparable-rental requirements, 30%/75% caps, no-appraisal-waiver rule. Verified May 22, 2026.

- UAD 3.6 / URAR transition — mandatory for new appraisal reports submitted to UCDP on/after Nov 2, 2026 for loans sold to Fannie Mae or Freddie Mac; ANSI Z765-2021 applies to square-footage measurement. Verified May 22, 2026; re-verify quarterly through the mandate.

- California AB 2533 — amends Government Code §66332; legalization pathway for pre-Jan 1, 2020 unpermitted ADUs/JADUs (signed Sep 28, 2024; effective Jan 1, 2025); references Health & Safety Code §17920.3. Verified May 22, 2026.

- San Mateo County Assessor — ADU new-construction assessment example (illustrative; tax treatment varies by jurisdiction). Verified May 22, 2026.

- Practitioner commentary — JVM Lending; Sacramento Appraisal Blog; appraiser industry forums. Used as supporting professional perspective; specific dollar figures carry inline sourcing on this page.

Note on the most-cited statistic: the FHFA “$1,064,000 vs $715,000” figures compare whole properties with and without ADUs — they are not a measure of the dollar value a single ADU adds, and we don’t present them that way.

Methodology and limitations

This guide does not estimate your home’s actual appraised value, and it is not legal, tax, mortgage, or appraisal advice. It explains how ADU value is generally supported, what evidence matters, and what to verify before relying on ADU value for a financing, buying, or selling decision.

We researched it using FHFA appraisal data, the Fannie Mae and Freddie Mac selling guides and UAD 3.6 policy materials, official county assessor guidance, current California legislation, and appraiser-side professional commentary. Primary and official sources were used for all appraisal, lending, tax, and regulatory claims; homeowner forum posts were used only to understand real questions and language. We deliberately do not publish a national “ADUs add X%” guarantee, because no verified national figure exists and the outcome is controlled by local appraiser and lender review. Last verified: May 22, 2026.

Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. For ADU loan documentation requirements and a related view on the numbers, our ADU Equity Calculator helps you estimate net value and rent impact. For financing math, the ADU Financing Calculator lets you run your ADU financing numbers. To estimate rental income assumptions, see the ADU Rental Income Calculator.

Frequently asked questions

- Do ADUs increase appraisal value?

- Often, yes — a permitted ADU in a market with comparable sales can add meaningful value. But there's no guaranteed national percentage, and the increase depends on legal status, comps, marketability, and local demand.

- How much value does an ADU add to a home?

- It depends on your market's comps, not a fixed formula. In thin-comp markets, conservative appraiser adjustments can land in the $25,000–$50,000 range; in strong ADU markets with real comps, contributions can reach six figures. The widely repeated '20–35%' is a correlation, not an appraisal method.

- Does an ADU count as square footage?

- Usually not directly. Fannie Mae keeps ADU living area separate from the main home's above-grade square footage unless the ADU is contained within or part of the primary dwelling, has interior access, and is above grade.

- Does an unpermitted ADU add value?

- Often little or none. Appraisers frequently treat unpermitted units conservatively because there are rarely comparable legal sales to support a higher value, and many lenders won't finance them as ADUs. Some states, including California under AB 2533, offer legalization pathways for older units.

- Can rental income from an ADU help me qualify for a loan?

- Sometimes. Both Fannie Mae and Freddie Mac allow ADU rental income on a one-unit principal residence, capped at 30% of qualifying income, with a full appraisal and specific comparable-sale and comparable-rental requirements. Illegal ADUs don't qualify.

- What if there are no ADU comps nearby?

- The appraiser broadens the search — older sales, a wider area, active and pending listings, paired sales, and rent comps. No perfect comp doesn't mean zero value, but it raises the support burden, so bring evidence.

- Should I order an appraisal before building an ADU?

- Usually start with feasibility, cost, and financing review first. A pre-build appraisal can help in certain lending scenarios (like an as-completed renovation loan) but it isn't a guarantee of the final value.

- Will an ADU increase my property taxes?

- Generally yes, but the method varies by state and county. In many places only the new ADU construction is assessed at completion, not your whole property. Confirm with your local assessor.

- Does a garage conversion appraise like a detached ADU?

- Not necessarily. Design, permits, retained parking, egress, and local demand all affect the value, and conversions can face habitability questions a purpose-built detached unit doesn't.

- Can I challenge a low ADU appraisal?

- Often, yes — through a Reconsideration of Value (ROV) request with your lender, supported by specific omitted comps or documented errors. Under Fannie Mae's framework, a borrower may initiate one ROV per appraisal and submit up to five additional comparable sales. You cannot simply pressure the appraiser to reach a number.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

Get My Free ADU Report →